31 October 2017

By Maynard Paton

Update on Getech (GTC).

Event: Interim results for the twelve months to 31 July 2017 published 31 October 2017

Summary: These results were never going to show a major turnaround, but glimmers of hope continue to emerge at the geoscience software specialist. In particular, a new chief exec has cut costs, reorganised the firm and spotlighted some of the company’s product attractions. True, minimal earnings are likely during the short term. But with the upbeat stock market making obvious buying opportunities hard to find, I am beginning to warm to GTC’s recovery potential. I continue to hold.

Price: 24p

Shares in issue: 37,562,415

Market capitalisation: £9.0m

Click here to read all my GTC posts

Results:

My thoughts:

* I was pleasantly surprised to read about a “more buoyant market“

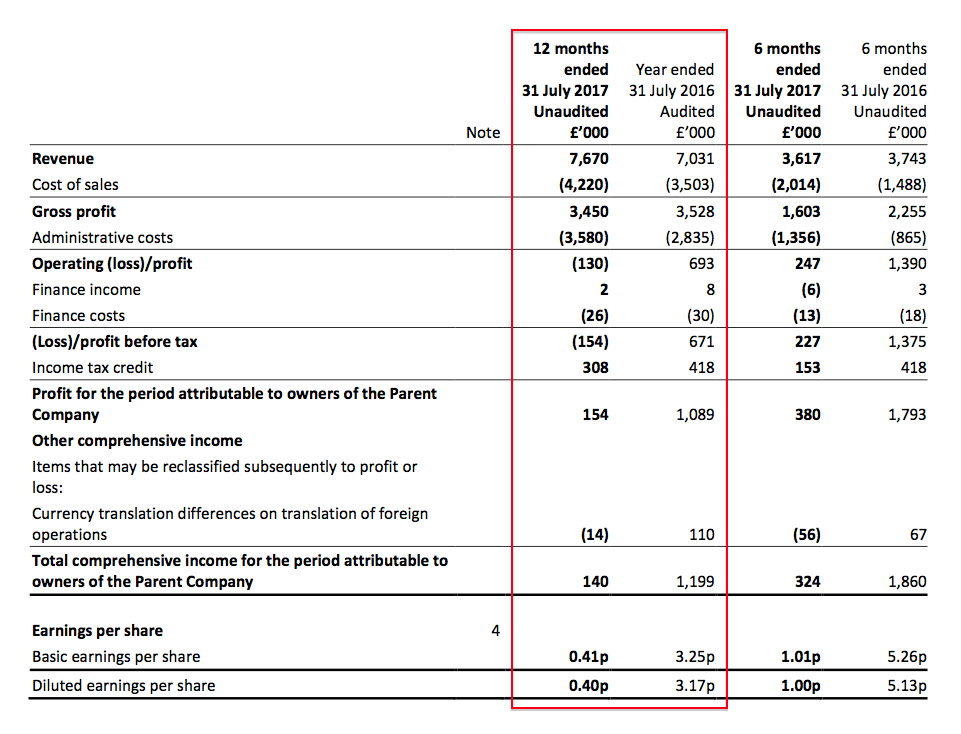

A rather unremarkable set of interims followed by a mixed trading statement had already confirmed a major turnaround at GTC had not occurred during 2017.

Annual revenue gained 9% and last year’s underlying operating loss was transformed into a £0.3m profit (excluding a £451k restructuring charge). My earlier sums had predicted a £0.2m profit.

The fortunes of the business remain some way off its 2013 heyday:

| Year to 31 July | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 8,011 | 6,593 | 8,638 | 7,031 | 7,670 |

| Operating profit (£k) | 2,221 | 969 | 1,987 | (126) | 321 |

| Finance costs (£k) | 25 | 32 | 5 | (22) | (24) |

| Other items (£k) | - | - | - | 819 | (451) |

| Pre-tax profit (£k) | 2,246 | 1,001 | 1,992 | 671 | (154) |

| Earnings per share (p) | 5.57 | 5.21 | 5.77 | 3.25 | 0.41 |

| Dividend per share (p) | 2.00 | 2.20 | 2.20 | - | - |

I should add that GTC’s progress during 2017 was inflated by the full-year contribution of a 2016 acquisition. Had GTC owned the acquisition throughout both years, these 2017 results would have shown revenue dropping from £9.1m, or 15%, to £7.7m.

The management narrative described various ups and downs within the group.

I was pleasantly surprised to read that the Products division, which develops and sells geoscience data and software, had apparently enjoyed “a more buoyant market”.

However, the Services division, which offers geoscience consultancy work, continues to suffer “challenging” trading conditions following “intensified” competition.

Similar to previous years, GTC enjoyed a more profitable second-half:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 3,288 | 3,743 | 7,031 | 4,053 | 3,617 | 7,670 | |

| Operating profit* (£k) | (697) | 571 | (126) | 74 | 247 | 321 |

(*adjusted for exceptional £845k acquisition write-back and £26k restructure cost during H2 2016 and £451k restructure cost during H1 2017)

Following the awful H1 of 2016, I am somewhat relieved the business has managed to scrape a profit for the subsequent 18 months.

* Staff sacked let go during H1 have saved shareholders £0.4m during H2

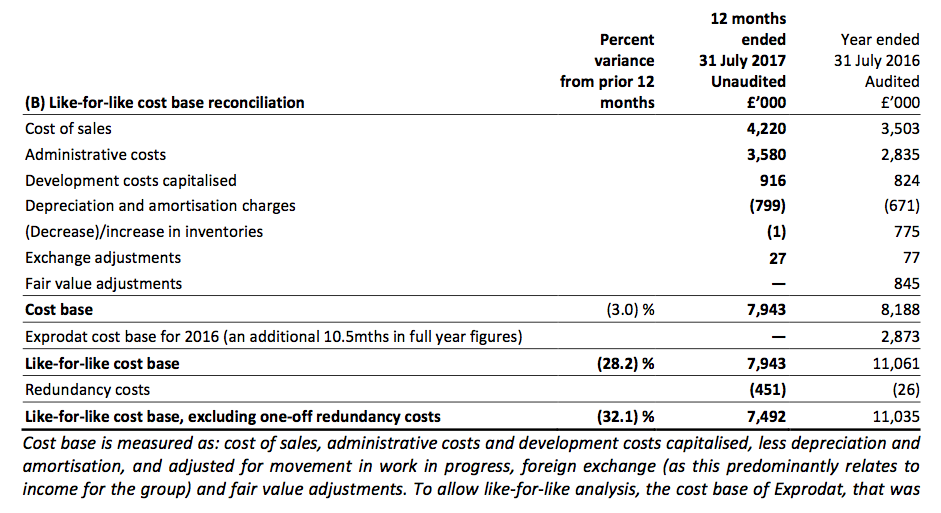

GTC’s profitability has been sustained by its new chief exec reducing the group’s costs (mostly by sacking staff making redundancies).

My half-year write-up noted the introduction of a welcome new cost-base table and this annual statement provided an updated version:

I derived the following table using GTC’s definition of its like-for-like cost base, excluding redundancy costs:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Underlying cost base (£k) | 5,908 | 5,127 | 11,035 | 3,934 | 3,558 | 7,492 |

The savings from H1 2017 to H2 2017 were £0.4m, without which I dare say the business would have remained a loss-maker.

* These remarks suggest the business may not be broken

Although GTC has suffered badly during the last few years, I’m trusting the group’s software and data still enjoy relatively strong competitive positions.

Past GTC reports have never really outlined the importance of the firm’s products to its customers, and so I applaud the new chief exec spotlighting such attributes.

Here are some choice quotes from the RNS (my bold):

“At the heart of our product offerings lie our market-leading inventory of Gravity & Magnetic data. Sales of these data were strong – it being an essential and cost-effective component of the integrated campaigns of our oil & gas customers, and a core operational tool for the mining industry.”

“Customer feedback on Globe Phase Two’s new content and delivery enhancements has been strong and through a new programme of training and practical support we are seeing our userbase expand as the product becomes more central to our customers’ daily workflow.”

“The re-subscription rate across all the software products maintained 2016 levels at above 95%, and our install-base grew further – driven by new sales (14% overall customer increase) and by customers with Global licenses deploying the software more widely within their organisations.”

True, these quotes relate only to one division. But the remarks do suggest GTC’s business is not completely broken.

* Tardy payments would have added almost £1m to the cash position

There’s not a lot to say about GTC’s finances.

The trading downturn has meant various ratios have slumped to mediocre levels:

| Year to 31 July | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating margin (%) | 27.7 | 14.7 | 23.0 | (1.8) | 4.2 |

| Return on average equity* (%) | 59.1 | 44.7 | 33.3 | 13.0 | 1.4 |

(*adjusted for net cash)

Cash generation during 2017 was not great, although the £700k working-capital outflow was due to tardy customer payments of £985k that have since been received:

| Year to 31 July | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit (£k) | 2,221 | 969 | 1,987 | (126) | 321 |

| Depreciation and amortisation (£k) | 214 | 240 | 366 | 671 | 799 |

| Net capital expenditure (£k) | (190) | (190) | (1,364) | (856) | (939) |

| Working-capital movement (£k) | 942 | (1,574) | 573 | (448) | (700) |

| Net cash (£k) | 4,249 | 3,423 | 3,694 | 1,888 | 941 |

I continue to be niggled by GTC’s capitalisation of certain development expenditure on the balance sheet (£916k during 2017, and £2.8m between 2014 and 2017).

Such expenditure now occurs every year at this business, and what with the amounts also included within the aforementioned cost-base table, I do wonder why they are not written off as expensed through the income statement.

It goes without saying that the capitalised expenditure is invariably larger than the associated amortisation charge that is used to calculate reported earnings.

At least year-end cash was £1.7m, which after debt of £0.8m and plus those tardy payments would have given an adjusted net cash position of £1.9m or 5.1p per share.

Furthermore, the balance sheet carries the group’s freehold headquarters at a £2.4m (6.6p per share) book value and is also free of pension obligations.

Valuation

I wrote in April that I felt the worst had been and gone at GTC.

I think these results underline that view, and confirm the business has stabilised somewhat following some decisive cost cutting.

Certainly the Products division appears to be where any future excitement is most likely to lie. The immediate outlook here seems relatively promising (my bold):

“From this starting point, we are better positioned to capture opportunities as green shoots emerge around oil and gas exploration spending, and we take cautious encouragement from recent trading.

Following the period under review, we have seen a continuation of 2017’s buoyant market for data, and we have a strong pipeline of pre-funded work. At the core of this are subscriptions to Globe 2018.”

Right now, I think it is fair to project a near-term annual operating profit of no more than £500k. Combine that with the net £1.9m cash position and the current £9m market cap is probably about right.

That said, the share price could be a bargain longer term if the leaner cost base plus greater client activity can one day combine to regain the high margins of yesteryear.

I have to confess, I have previously described GTC as a “debatable” portfolio holding due to its haphazard track record and absence of stable leadership.

But with obvious buying opportunities hard to find in the current market, I am now beginning to warm to GTC’s potential recovery upside.

A lowly share price, that decisive cost-cutting, the cash position and some “market-leading” products is enough for me to conduct some further research.

Maynard Paton

Disclosure: Maynard owns shares in Getech.

Getech (GTC)

ShareSoc presentation, Leeds, 14 November 2017

————————————-

EDIT: 01 February 2018

PDF presentation now available.

————————————-

I attended this event to hear what GTC’s new chief exec, Dr Jonathan Copus, had to say about the business.

(Credit should go to Sharesoc for organising this and similar presentations.)

My Blog post above noted a few choice quotes from the recent RNS — “market-leading inventory” etc — and I hoped to gain some insight into GTC’s more attractive Products division.

Here is my best recollection of the points made by Dr Copus (some bits may be paraphrased).

Products vs Services:

* Dr Copus said group revenue was split two-thirds Products versus one-third Services.

The split suggests that, during 2017, Products produced revenue of £5,113k and Services produced revenue of £2,557k.

I assume Products and Services are essentially the same segments as “Multiclient products and services” and “Consultancy projects” as stated in the 2016 annual report:

If so, then Products improved its revenue by 18% and Services decreased its revenue by 3%.

The mixed progress seems about right given the management results commentary. I am sure Dr Copus mentioned the Products division had enjoyed a 14% increase to its customer base last year.

(Quick note: The acquisition last year of Exprodat brought mostly additional Services revenue into the business. Had Exprodat been owned throughout the whole of 2016 and 2017, I calculate the underlying decrease of Services revenue would have been 47% (£4,762k to £2,557k).)

* Dr Copus did not disclose the profit from either Products and Services, but he did say Services as a whole was profitable. Within Services, he said the geoscience consultancy operation had run at break-even.

* Dr Copus claimed GTC’s cash margin — rather than the headline operating margin — reflected the high-margin features of its products.

I was not too convinced by that statement. Cash margin can fluctuate year-to-year and, within GTC in particular, can be influenced by upfront customer payments.

I trust the headline operating margin can one day reflect the claimed higher-margin power (see below) of GTC’s products. The 2017 results showed a 4% group margin — not great, but perhaps the group margin was depressed by the low profitability at the Services division.

* On the subject of cash flow, Dr Copus said the late £1m payment was only made known to GTC by the client on 30 July — the day before the firm’s year-end. Apparently the client “screwed up” its invoice procedure.

Products:

A few quotes from Dr Copus:

* GTC is the “world’s largest broker of gravity and magnetic data”.

* “Pretty much all the oil super-majors subscribe to Globe”

* “[We have] great products — they [the customers] won’t switch it off”

* Selling off-the-shelf datasets were a “100% profit activity”.

* Three-quarters of the two-thirds Product revenue (i.e. 50% of group revenue) is “repeat revenue” — i.e. subscription software revenue or Globe revenue.

* Globe revenue — paid by ‘sponsors’. Difference between a Globe ‘sponsor’ and an ordinary Products customer is that the sponsors pay upfront for the Globe development work and then get to keep the finished product.

If customers don’t pay, GTC can “switch their product off”.

* Shelf-life of data — “data does not go stale”

Datasets that are 10-15 years old still sell, due in part to no competition and “improved resolution” of product.

Services:

More points from Dr Copus:

* “Much more difficult market”

* Lots of oil industry consultants have emerged of late after losing their jobs during the oil-price downturn.

The knock-on effect to GTC was that it could not compete with such ‘back bedroom’ consultants on cost.

So Services strategy is now focused on “complex consulting that builds on the underlying data we provide”

* Dr Copus was upbeat about GTC’s government-advisory department within the Services division.

The recent Sierra Leone deal — where GTC was selected to manage and run a licensing round and provide all the associated data — in particular was exciting.

Other:

Dr Copus on new opportunities:

* GTC is currently serving mainly on oil/gas exploration-related activities -— but possibilities could also lie within oil/gas well development, production and abandonment.

* Nuclear — just won third contract, although this activity currently contributes small revenue to the group. But the sector has similarities with oil and gas — complex engineering, government regulation and large capital expenditure.

The nuclear contract apparently involves “monitoring movement of nuclear material”.

* The challenge to entering new areas is a “lack of expertise… need to find a product to put in Nuclear for instance”.

* An oil rig located in a Kazakhstani lake was highlighted. Apparently GTC supplies data (or can supply data) to help monitor the movement of ice on the lake during the winter.

Competition:

Dr Copus on competition:

* Competition has reduced during the downturn. Many rivals have gone bust.

* GTC “not under competitive pressure”.

* “Customers say that Globe is the last global data product they still subscribe to”.

* Rivals have been acquired by larger seismic data groups, however the downturn has seen them being “starved of capital” within the larger parent.

Rivals named as:

CGG — French seismic data firm

Player — Australian

AustinBridgeporth

* “Our software is the best” and is “easy to use, intuitive to use”

* GTC software is “data agnostic”

GTC is (I think) not restricted in what data it can use, but rival products apparently have to use certain data, which limits the scope of the geological evaluation by the customer.

“Exploration is all about innovative thinking”

* “We know who owns what data and what it’s used for”.

* Dr Copus suggested some customers purchased data so competing explorers didn’t have an information advantage.

* GTC never discounts data — not afraid of saying no to low purchase offers. “We know what the data is worth”.

Other points:

* 55% of shares owned by IP Group, former staff and current employees.

* Cost base — main cost cutting now done.

* Freehold HQ (£2m-plus book value) could be looked at. Money tied up there could be reinvested in the business.

* Group currently operating at three locations (Leeds and 2x London). Looking at suitability of having three sites — implication: could be cut down to two sites.

* 85 staff — 45 at Leeds, 15 with Dr Copus in one London office, 25 presumably at the other London office or elsewhere (one member of staff has a full-time desk at the UK’s Oil & Gas Authority office in Aberdeen).

* 32% reduction to cost base versus 18% reduction to workforce. Implication: expensive geoscience consultants had been given the heave-ho.

* Cash development costs should not diverge too much from the associated amortisation charge in the future.

Dr Copus made lots of remarks about customers:

* “Cannot have too much customer interaction”

* He said that GTC in the past would, if given the chance, add new geology or technical features to a product — most probably a throwback to the group’s academic roots.

Now the business speaks more to customers, and improvements are more likely to include making the product easier to use and the provision of training courses.

* Focus more on the customers that need the product. Prospects that say “We’ll look at the product later in the year if we have a budget left” are now non-starters.

* I think Dr Copus has brought a more commercial and customer focus to GTC. I get the impression GTC’s academic heritage (the firm was spun-out from the University of Leeds) may have been great for product development but perhaps not so great for ultimate product profitability.

* Dr Copus said he had been a geologist at Shell, an Oil & Gas equity analyst at Deutsche Bank and the finance director at Salamander Energy. He joined GTC because he was looking for a “business to build”, with GTC having decent core products but requiring a refocus on customers.

Maynard

Hey, thanks for the great work. Is there anyway I could see the presentation for myself online. I can’t get the link to work

Hello Sam

————————————-

EDIT: 01 February 2018

PDF presentation now available.

————————————-

The link went to the ShareSoc site and showed brief details advertising the event. The page has now been removed, so I have removed the link.

GTC does not publish presentations on its website, and the slides shown last week are not there either: https://getech.com/annual-reports-and-accounts/

To be honest the slides were nothing special and did not contain anything that a reasonably informed shareholder would already know.

You could contact GTC direct for a copy of the presentation slides I guess.

Maynard

The presentation is available at the sharesoc site in the members area under Seminars and Presentations (page 17). Along with the CLIG slides from the same evening.

Good to meet up Maynard……….however briefly :-)

Thanks Patrick. It was good to meet you, too.

Maynard

Getech is really trading down now. Seems like a great buy in the low 20’s. I estimate over a 100% upside and little downside given their cash position, land/building, and data sets. Furthermore, business should improve in this somewhat stabilizing energy environment. Just thought I would throw this comment out there

Hello Sam,

Thanks for throwing out the Comment. Yes, I think upside potential is greater than downside risks at the moment, although it is hard to know a timescale for any sort of recovery. I think the new-ish boss has steadied the ship.

Maynard

Hi Sam,

I’m not sure I would say the energy environment is stabilising. Yes Oil is up and that is helping Refiners and investment to high value chemical and fine Chemicals but from what I see upstream or offshore exploration is still pretty dead

David

Hi David,

Sorry for the late reply – i somehow missed your comment. I do agree with that assessment, however I believe that if oil stays higher than say 50$ – offshore will be able to cut costs and comply with the new lower priced environment. Furthermore, I don’t think offshore has to make a full comeback for an investment in getech to work as their products revenue has a large recurring revenue basis. Furthermore, the service segment has been in the dumps and should see a slight turnaround given the slightly better conditions without taking into consideration the sierra leonne licensing project.

Sam

Getech (GTC)

Launch of the Fourth Sierra Leone Offshore Petroleum Licensing Round

This announcement provides some interesting insights into GTC’s business. Here is the full text:

—————————————————————————————————————————-

The Petroleum Directorate of Sierra Leone today launches the country’s Fourth Offshore Petroleum Licensing Round. This Round is being exclusively supported by the Getech Group (AIM; GTC), through its wholly owned subsidiary ERCL. Applications to the Round close at 12-noon on 28th June 2018.

At a meeting to be held at the Geological Society, London, the Director General of the Petroleum Directorate, Raymond S Kargbo and team, and ERCL Director Huw Edwards, will present detail of:

· The Contract Areas on offer

· The technical data available to support bids

· The application procedure for interested companies

With over thirty oil companies registered to attend, the high number of attendees demonstrates the strength of interest in Sierra Leone’s hydrocarbon potential.

Huw Edwards commented:

“Having worked in partnership with the Petroleum Directorate of Sierra Leone since 2016, we are delighted to be hosting Raymond and his team as they launch this exciting new phase for the country’s petroleum sector. Together, we have assembled an extremely high quality technical database, and put in place a robust licencing framework. These will assist investors in their evaluation of the significant potential of the Sierra Leone margin – much of the well and seismic data are being made available for the first time. Investors also have the opportunity to license a number of value-add products, built using the Government’s released seismic and well database.”

For further information:

https://getech.com/sierra-leone-oil-gas-exploration/ http://www.pd-sl.com

—————————————————————————————————————————-

Those two websites shown at the end provide useful links

https://getech.com/sierra-leone-oil-gas-exploration/ links to https://getech.maps.arcgis.com/apps/webappviewer/index.html?id=199b131d577248f1ba69152d627f2ab3

…from which you can ‘drill down’ (haha) into GTC’s map data:

The http://www.pd-sl.com site includes a Data Room Rules PDF:

It costs $2k a day to inspect the data at GTC’s Henley office:

Travel to Sierra Leone, though, and your first day in the Data Room there is free!

Maynard

Getech (GTC)

Trading Update: 17 months to 31 December 2017

This statement revealed nothing of major significance. My sums indicate pre-tax profit could be running at close to c£300k/year. Year-end net cash was £1,800k or about 4.8p/share.

Here is the full text:

—————————————————————————————————————

The Getech Group (AIM; GTC) provides geoscience and geospatial products and services to a wide variety of companies and governments, which they use to de-risk their exploration programmes and improve their management of natural resources.

On 20 September 2017 Getech announced steps to align its reporting cycle with its customers’ budget cycle. To do this the Group’s Accounting Reference Date was moved to 31 December and Getech has already reported interim financial results (12 months to 31 July 2017).

This Trading Update concerns the 17-month accounting period to 31 December 2017 (referred to as AP 2017), the previously reported accounting period being the 12 months to 31 July 2016 (referred to as FY 2016). Audited final results for AP 2017 will be published on or before 28 February 2018. All figures stated in this Trading Update are unaudited.

In AP 2017, under the leadership of a new management team, Getech undertook a wide-ranging programme of organisational and cultural change. Through cost control, customer engagement and a repositioning of how we invest our operating cash flow, we have significantly enhanced both the Group’s cash profitability and the commercial positioning of our Products and Services.

Revenue

Revenue in AP 2017 totalled £10.9 million (12 months FY 2016: £7.0 million). Products remained a key engine of growth, accounting for 69% of Group revenue in AP 2017. Pro-rata, this is an increase of 24% on FY 2016. Within our Services division, the geoscience services market remained challenging, but work completed in AP 2017 has laid the foundation for a number of important 2018 sales opportunities – principal amongst which is the recently launched Fourth Sierra Leone Licensing Round.

Cost base

Actions taken in the first 12 months of AP 2017 reduced Getech’s underlying like-for-like cost base by 32%, when compared to 12 months to 31 July 2016. Across the next five months we continued our programme of product investment and enhanced our sales and project management capabilities. The cost base, excluding one-off restructuring costs, remained on a flat trajectory, totalling £10.6 million across the 17 months. Within this figure product investment was £1.2 million.

Before product investment and restructuring costs, Getech delivered a 17-month net operating cash inflow of £2.1 million, which compares to a £0.3 million net cash out-flow for the 12-months of 2016.

Restructuring costs, final M&A payments, and debt repayments

Restructuring costs in AP 2017 totalled £0.5 million, all outstanding M&A cash payments were settled (£0.5 million), and a further £0.3 million of debt was repaid.

Cash balances

Net of these cash movements, cash balances at 31 December 2017 totalled £2.4 million. This was flat on the figure reported in September 2017 and compares to an opening cash balance of £2.8 million.

Balance sheet adjustments

To keep our balance sheet in step with the Group’s new investment and sales strategies, management has decided at year-end to write-down inventories totalling £0.5 million that had built up on the Group balance sheet through the sector downturn.

Jonathan Copus, Getech CEO, commented:

“In 2017 we undertook a programme of commercial, operational and cultural change that has significantly strengthened the Getech Group. These steps align our products and services more firmly with the practical commercial needs of our customers, and we have entered 2018 with a full and diverse pipeline of opportunities – to which our cash profitability is strongly leveraged.”

—————————————————————————————————————

Revenue of £10,900k for Aug-16 to Dec-17 (‘AP17’) suggests revenue for Aug-17 to Dec-17 was £10,900k – £7,670k (FY17) = £3,230k. So £646k/mo, which is about the same as £639k/mo for FY17.

Given revenue continues to flatline, the reference to Product revenue advancing 24% indicates the Services division continued to suffer badly.

An underlying cost base of £10,600k for AP17 suggests an underlying cost base for Aug-17 to Dec-17 of £10,600k – £7,492k (FY17) = £3,108k. So £621k/mo, which is about the same as £624k/mo for FY17.

For the extra five months of AP17 (Aug-17 to Dec-17), it appears GTC was recording a c£25k/mo profit, or a run-rate of £300k/year.

GTC said restructuring costs in AP17 were £500k, outstanding M&A cash payments were £500k and debt repayments were £300k. For the extra five months of AP17 (Aug-17 to Dec-17), it appears GTC incurred restructure costs of £49k, no further M&A payments and debt repayments of £155k.

Cash at Dec-17 was £2,400k, versus £2,788k at Jul-16. So an outflow of £388k for AP17.

Adjustments are: restructuring cost £500k, M&A £500k, debt repayment £300k and tax refund £521k = £779k. So underlying cash inflow was (£388k) + £779k = £391k over 17 months. Over 12 months that is £276k, which is close enough to the aforementioned profit run-rate of £300k/year.

Debt at Dec-17 should be £900k debt at Jul-17 less £300k debt repayment = £600k.

Net cash at Dec-17 should be £2,400k cash less £600k debt = £1,800k (c4.8p/share).

Maynard

EBIT margin for the 5 months looked to be $417k or 12.7% excluding exceptional costs. That’s a solid bump considering where they were and the low production of the service division.

Getech (GTC)

I have reviewed GTC’s latest 17-month results here:

https://maynardpaton.com/2018/03/02/getech-17-month-results-provide-further-hope-of-a-profit-rebound-and-decent-share-price-upside/

Maynard