05 November 2021

By Maynard Paton

Results summary for Bioventix (BVXP):

- Acceptable annual figures that included a record H2 profit (+14%) despite the pandemic continuing to disrupt demand for routine blood tests.

- Mixed progress from vitamin D and other established antibodies leaves near-term growth dependent mostly on the fast-selling troponin product.

- Additional research efforts suggest pyrene biomonitoring and detecting Alzheimer’s disease may be the more likely long-term pipeline winners.

- A 19% dividend lift, another special payout, 70%-plus margins and low retained-profit requirements underlined the wonderful economics of collecting antibody royalties.

- Troponin’s finite income and a resultant sum-of-the-parts valuation do not indicate an obviously tantalising £36 share price. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Vitamin D

- Troponin

- Other antibodies

- Pipeline developments

- Financials

- Valuation

Event links, share data and disclosure

Event: Preliminary results and presentation for the twelve months to 30 June 2021 published 18 October 2021

Price: £36

Shares in issue: 5,209,333

Market capitalisation: £188m

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Why I own BVXP

- Develops diagnostic blood-test antibodies, direct competition for which is limited due to the necessary scientific innovation, protracted regulatory testing, onerous switching procedures and ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£15m shareholding and has declared six special dividends.

- Employs ‘scalable’ royalty/licensing model that requires few employees and leads to terrific margins, generous cash flow and high returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit and dividend

- These FY 2021 results were never going to be sensational after March’s H1 statement confessed to pandemic disruption:

“The continuing global pandemic has, without doubt, affected the activity within diagnostic pathways in hospitals and clinics around the world to which our business is intrinsically linked. Not only have medical care resources been diverted to cope with COVID-19 patients but, even where capacity remains, there is ongoing evidence that patients are choosing not to present to healthcare professionals or not to enter diagnostic pathways.”

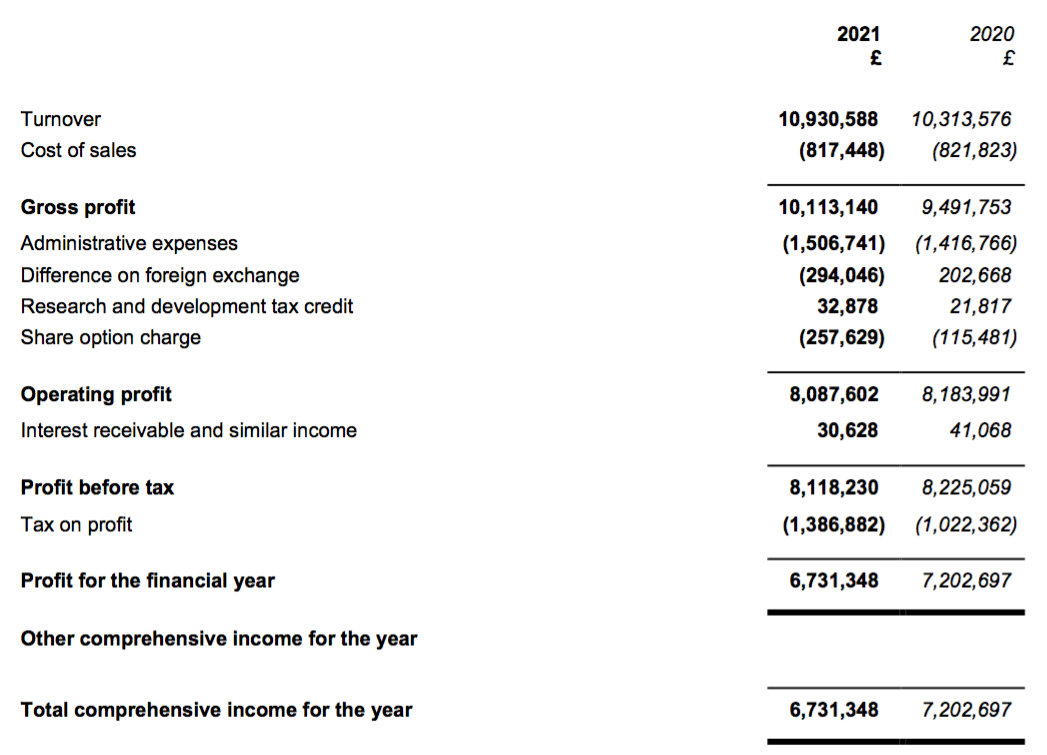

- The Covid-19 interference had restricted H1 revenue growth to just 1% and caused reported H1 profit to decline 9%.

- However, for the full year, revenue gained 6% and reported profit fell just 1% following an encouraging H2.

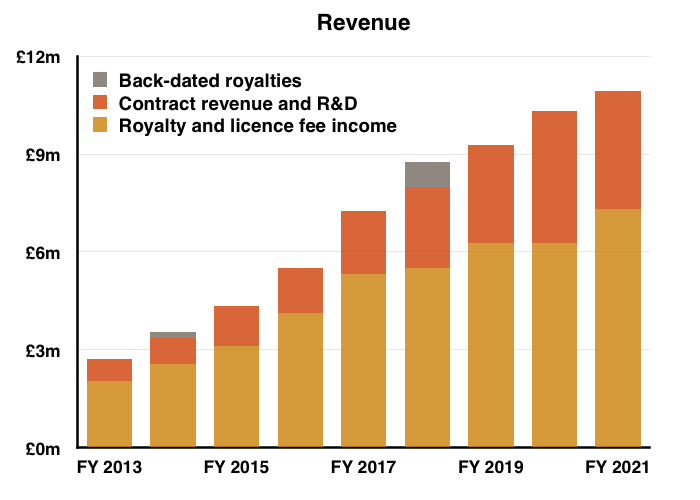

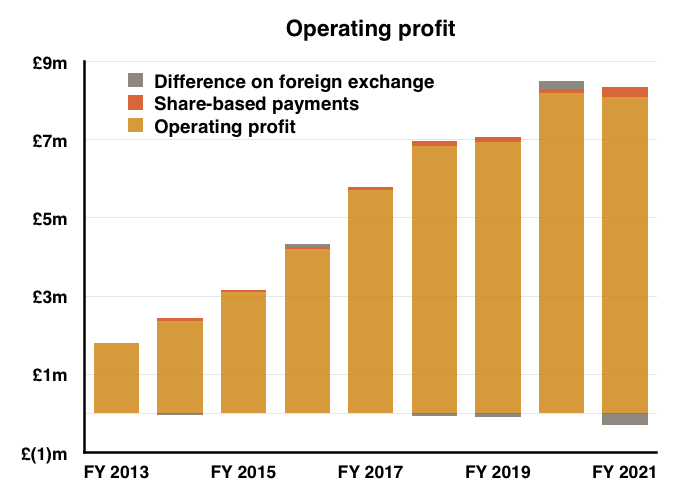

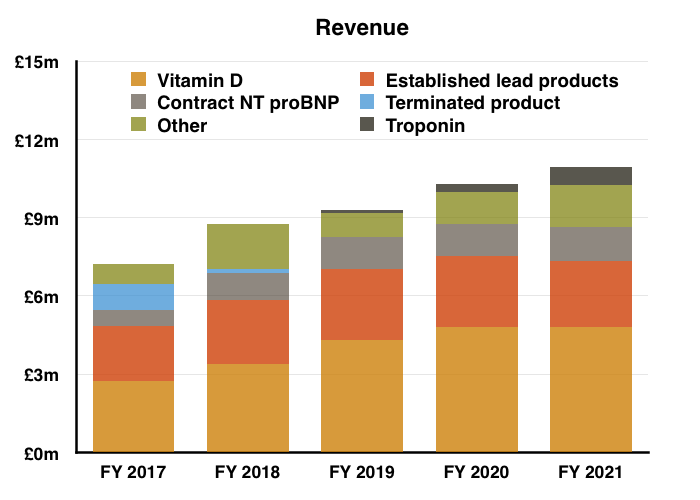

- This FY 2021 performance extended BVXP’s run of revenue increases to eleven years…

- …but could not extend a similar run of annual profit increases.

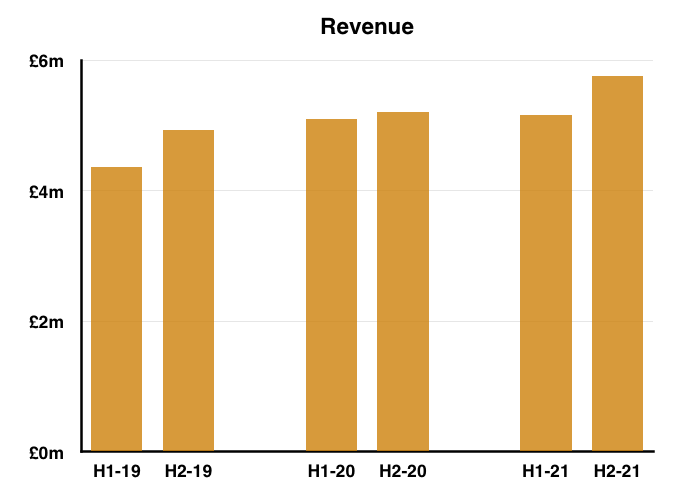

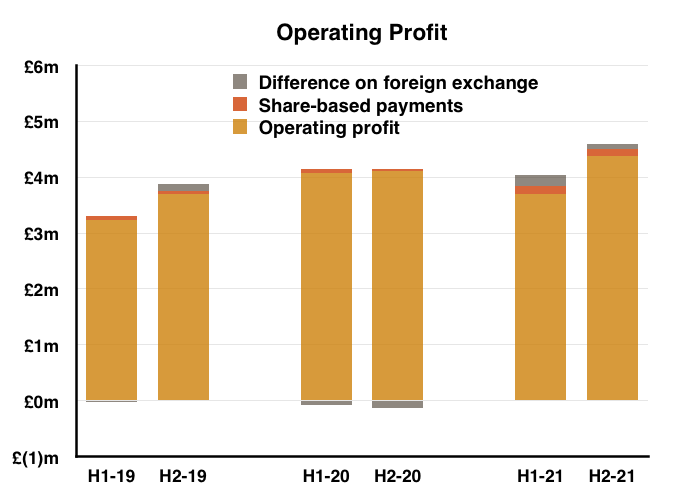

- H2 nonetheless delivered a record six-month performance for both revenue and profit:

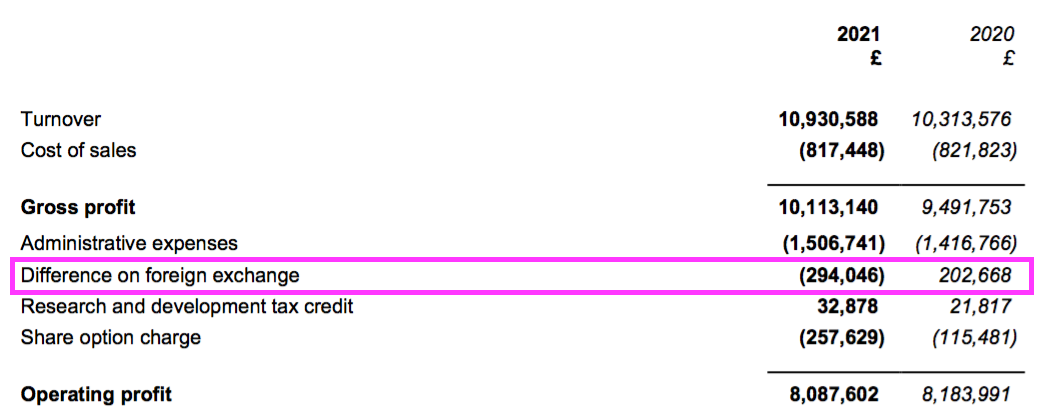

- Reported profit progress was distorted a little by foreign-exchange gains/losses and share-based payments (see Financials below).

- Before foreign-exchange gains/losses and share-based payments, full-year operating profit climbed 7%. The H2 profit advance on the same basis was +14%.

- Despite the improved H2, BVXP acknowledged the pandemic disruption to blood testing had not yet cleared:

“As we observed earlier in the pandemic, through our multinational in vitro diagnostics (IVD) customers, our main business is intrinsically linked to the diagnostic pathways that exist at hospitals and clinics around the world. The activity within these routine diagnostic pathways continues to be adversely affected by the COVID-19 pandemic as hospital resources are diverted to cope with the additional patient burden created by the pandemic.

Even where diagnostic capability exists, there is still evidence that concerned patients have chosen not to enter diagnostic pathways and have not presented to healthcare professionals as would normally be expected.“

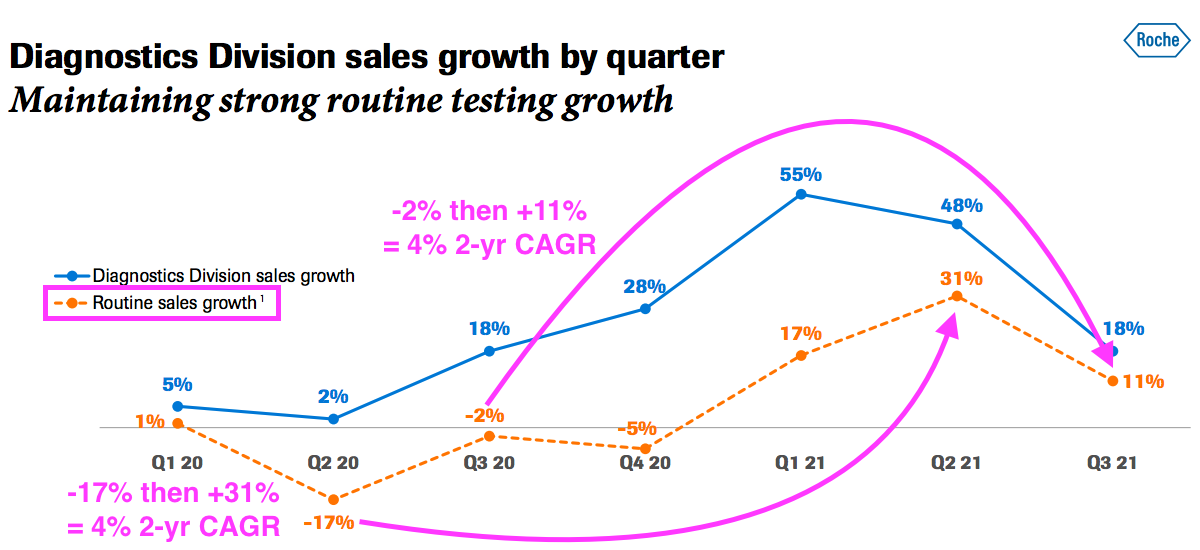

- That said, a Q3 update from Roche showed its routine diagnostic sales (i.e. excluding income from Covid-19 tests) recovering during 2021:

- Roche is the world’s largest in vitro diagnostic (IVD) company and is as good a benchmark as any to judge demand for the type of blood-test antibodies that BVXP develops.

- Roche’s slide implies its routine-diagnostic sales have compounded at an approximate 4% average between (pre-pandemic) Qs 2 and 3 2019 and Qs 2 and 3 2021.

- The 4% growth rate matches the ten-year sector growth cited by Roche within an earlier 2021 presentation:

- BVXP’s final dividend was raised 19% to 62p per share and matched the percentage increase applied to the interim payout.

- For the sixth consecutive year, the ordinary dividend was accompanied by a special payout.

- The 38p per share special dividend gave a total full-year payout of 143p per share versus a total 141p per share for FY 2020.

- The 38p per share special dividend brought the total of special dividends declared during the past six years to 233p per share — versus 378p per share declared as ordinary dividends.

- Between FYs 2016 and 2021, BVXP has paid total ordinary/special dividends representing 90% of total reported earnings (£31m of £34m).

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Vitamin D

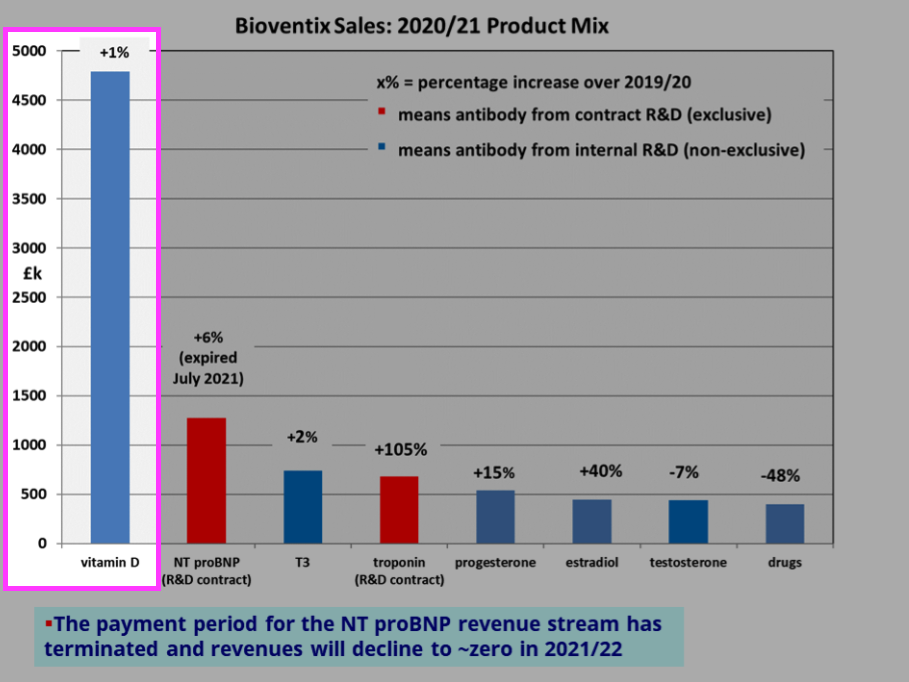

- BVXP’s vitamin D antibody remains by some distance the group’s best-seller at 44% of revenue:

- BVXP said vitamin D income had “remained relatively unchanged” at £4.8m.

- Perhaps vitamin D revenue really has “plateaued“.

- Warnings of the vitamin D market “plateauing” were issued within the FY 2017, FY 2018 and FY 2019 results when the antibody was delivering 20%-plus per annum revenue growth.

- Management has in the past claimed the ‘plateauing’ of vitamin D growth to mean the rate reducing to between 5% and 10% — to match the projected expansion of the wider antibody market.

- BVXP’s short FY 2021 comment on vitamin D did not imply an imminent return to material growth:

“The importance of vitamin D in human biology is widely acknowledged and does indicate that vitamin D testing will continue to be part of clinical diagnostics in the long term.“

Troponin

- BVXP reiterated future revenue and profit growth being dependent mostly on demand for its new-ish troponin antibody:

“Over the next few years, the commercial development of the new troponin assays will have the most significant influence on Bioventix sales. There are currently no antibodies in the future pipeline that are comparable to our troponin products in potential value and the ability to influence revenues in the next few years.”

- I had interpreted the H1 text as saying troponin sales could double for the full year, and sure enough troponin sales did double:

“Total troponin antibody sales from Siemens Healthineers and another separate technology sub-license doubled during the year to £0.68 million (2019/20: £0.33 million). This significant increase clearly demonstrates a gathering momentum of product roll-outs for the new high sensitivity troponin assays supported by SMAs and we believe that these revenues will continue to grow in the next financial years.“

- The “gathering momentum” text was used this time last year, which might imply the 100% growth rate enjoyed during this FY 2021 can be maintained for FY 2022.

- This time last year management claimed via a webinar:

- Troponin revenue reaching £1.2m during FY 2022 — to replace lost income from another product — was “entirely plausible”, and;

- House broker Finncap was predicting “revenues that are around £3m for troponin going into the future.”

- Note that twelve months ago management also confirmed the royalty licence for troponin would expire during the summer of 2032.

- Management has said new antibodies would always enjoy perpetual licence income, but development work on troponin started during 2006 when BVXP generated revenue of only £593k and was not the business it is today.

- The finite troponin income does complicate BVXP’s valuation and puts greater emphasis on the group’s pipeline developments (see Pipeline developments below).

- Troponin currently represents 6% of total revenue.

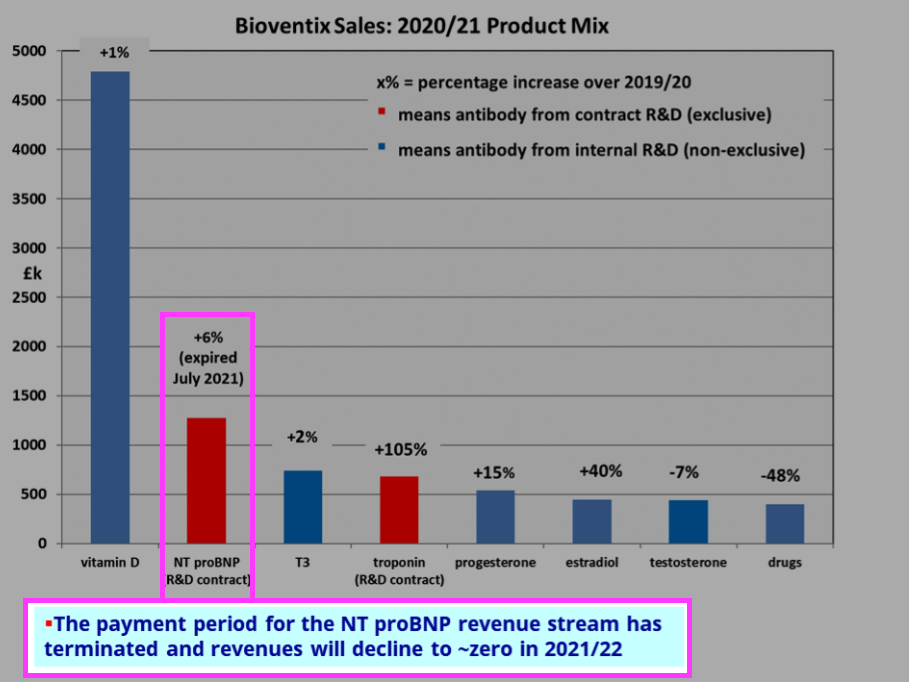

Other antibodies

- BVXP’s revenue from its five other “lead” antibodies ranged from up 40% to down 48% during this FY 2021, and combined was down 7%:

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Revenue (£k) | |||||

| Testosterone | 574 | 660 | 800 | 480 | 440 |

| T3 | 495 | 460 | 640 | 720 | 740 |

| Drug testing | 485 | 640 | 490 | 760 | 400 |

| Estradiol | 333 | 290 | 330 | 320 | 440 |

| Progesterone | 178 | 400 | 470 | 470 | 540 |

| Total | 2,064 | 2,450 | 2,730 | 2,750 | 2,560 |

- Total revenue from the five antibodies has advanced only 4% between FY 2018 and FY 2021, which feels disappointing.

- Mind you, the pandemic has influenced recent progress and the preceding H1 statement did say:

“Our antibodies for thyroid disease diagnostics (T3) and others for fertility diagnostics (estradiol, progesterone and testosterone) form part of routine diagnostics for chronic conditions which are often not life-threatening. We believe that such diagnostic tests have experienced lower volumes in pandemic affected areas and this has had a small impact on our own revenues.”

- Omitted from the table above is revenue of £1.28m from NT proBNP (an antibody used to diagnose potential heart failure), the income from which ceased a month after the FY 2021 year end:

- Troponin doubling once again to £1.36m during the current year will offset the £1.28m that will be lost from NT proBNP.

Quality UK investment discussion at Quidisq. Visit forum.

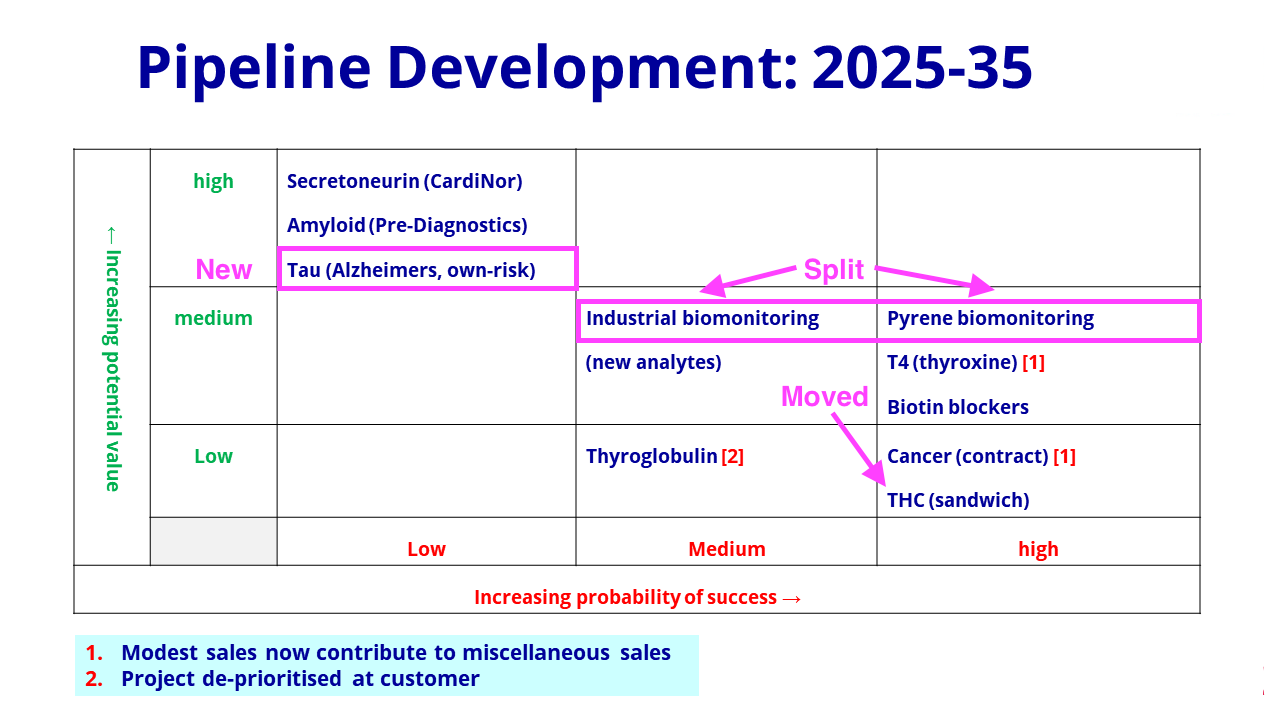

Pipeline developments

- BVXP thankfully replaced the “research news” slide used within the H1 powerpoint…

- …with the customary pipeline grid for these FY results:

- The latest grid included changes to what was presented this time last year.

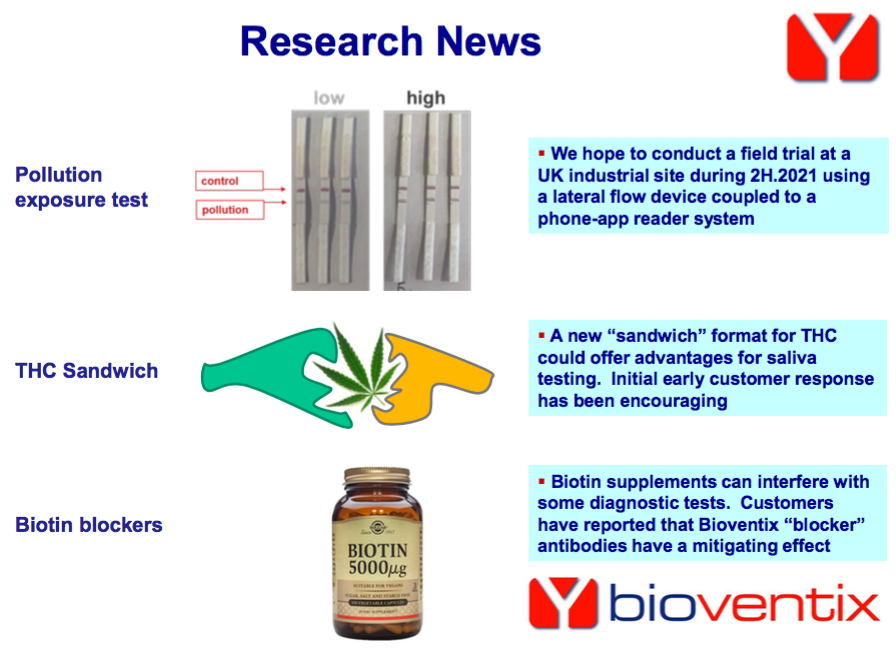

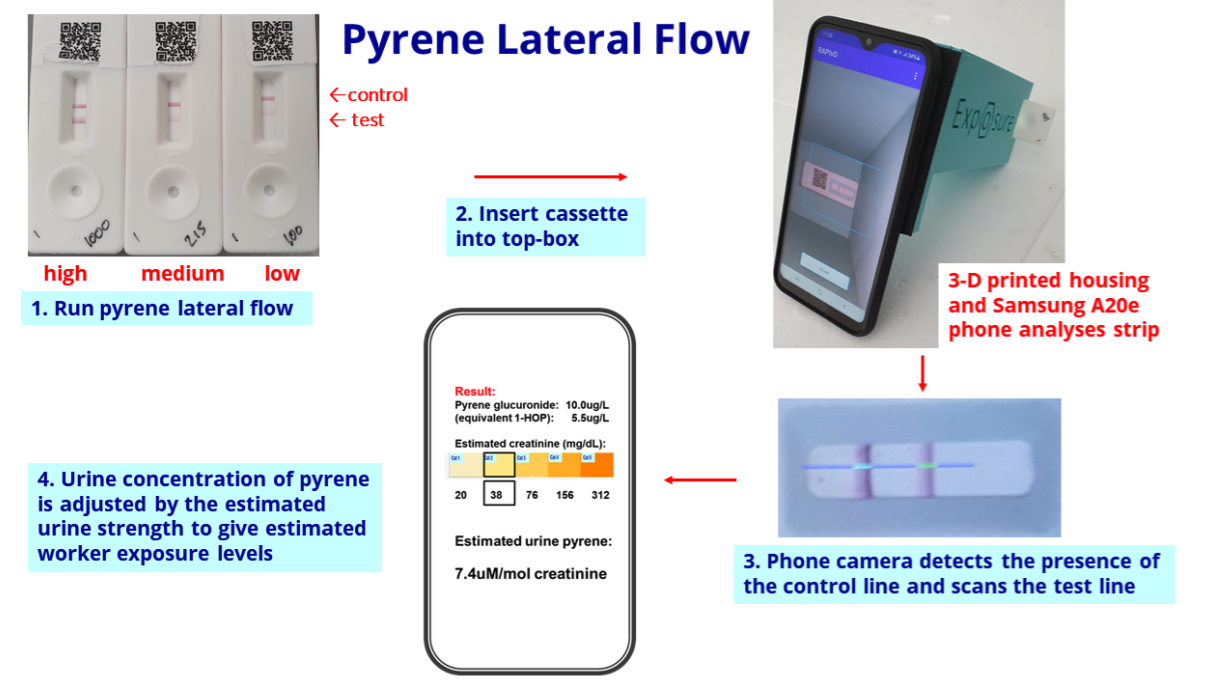

- The pollution biomonitoring project has now been split into two: “industrial biomonitoring” and “pyrene biomonitoring” (pyrene is a hydrocarbon produced by combustion engines).

- The pyrene project has maintained its “high” probability of success on the grid.

- The slide below explains how the pyrene test works through a urine sample and a mobile phone:

- BVXP said:

“We are particularly pleased with the progress of the pyrene exposure project.

Internal results (using a small bank of industrial urine samples) are encouraging and we are working with a UK industrial site to conduct a field trial of the device and app over the next few months.

We accept that the creation, manufacture and supply of final assay products is outside our normal focus of bulk antibody sales but we believe that through our own efforts we can substantiate the viability of such products and generate demand, thereby stimulating the interest of future commercial partners.“

- The split into “industrial biomonitoring” and “pyrene biomonitoring” follows the pyrene work having prompted additional research:

“The progress of the pyrene project has encouraged us to consider additional assays in the field of industrial health and safety. Work on these new analytes has only just started and is planned to continue into 2022 and 2023.“

- The additional research implies the pyrene project is one of the more likely pipeline ventures to become commercial, although the final product may not exhibit the same wonderful economics as an antibody (see Financials below).

- Other research projects are not exhibiting wonderful economics.

- In particular, FDA guidelines have created “cost/price constraints” for the biotin blockers while the antibody quantity required for each tetrahydrocannabinol (THC) test is presenting “cost/price challenges“.

- Among the ‘long shot’ projects, the introduction of development work on tau (a protein found predominantly in brain cells) to detect potential Alzheimer’s disease now complements BVXP’s investment in Alzheimer’s researcher Pre-Diagnostics.

- The extra Alzheimer’s efforts suggest this work may be further developed than BVXP’s involvement with Cardinor, which is analysing secretoneruin to detect potential heart failure.

- Exactly which pipeline products (if any) eventually make it to market remains anyone’s guess. The troponin antibody took more than ten years in development before its commercial launch.

Financials

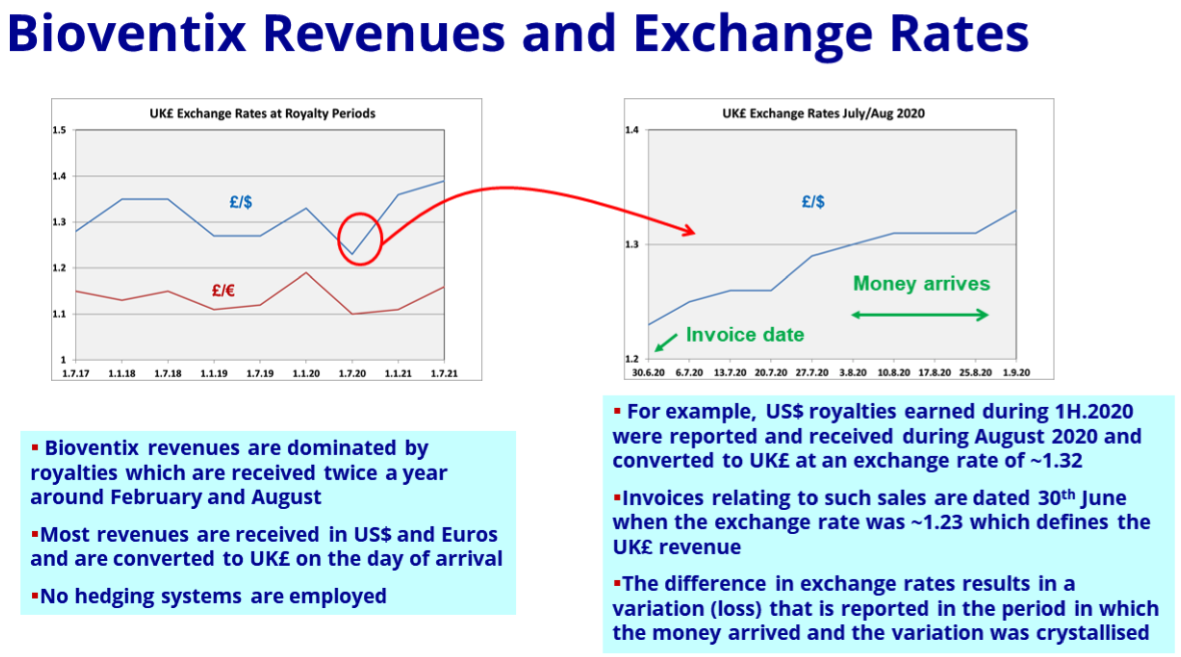

- The aforementioned foreign-exchange gains/losses warranted a slide within the presentation:

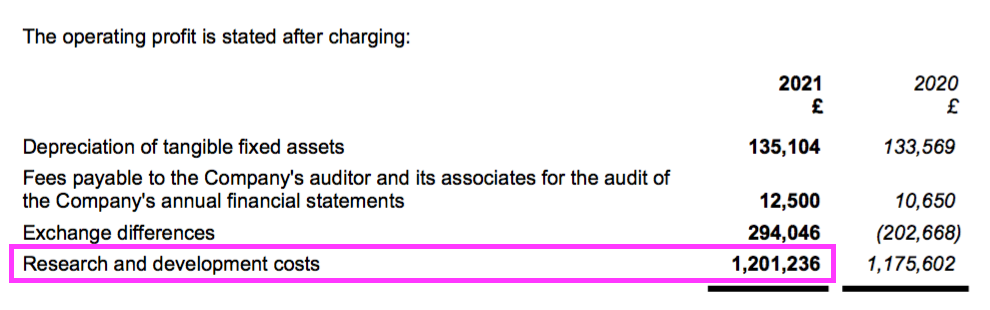

- For FY 2021, “difference on foreign exchange” knocked 4% off operating profit, but added 3% for the comparable FY 2020:

- The foreign-exchange gains/losses arise when customers pay BVXP more/less than what was initially recognised as revenue because of subsequent exchange-rate movements.

- Such foreign-exchange gains/losses can be significant for BVXP because the majority of group revenue is:

- Denominated in USD or EUR, and;

- Invoiced only every six months (which amplifies the accounting impact of currency movements).

- Confusing matters is the fact these foreign exchange gains/losses relate to the prior period.

- For example, the £294k foreign-exchange loss reported for FY 2021 really should be subtracted from FY 2020 revenue and profit to derive a ‘currency-adjusted’ FY 2020 result.

- These foreign-exchange gains/losses can make year-on-year comparisons awkward, but thankfully their longer-term effect has been minimal.

- Foreign-exchange gains/losses during the last five years total a negative £262k versus aggregate revenue of £47m and aggregate reported operating profit of £36m.

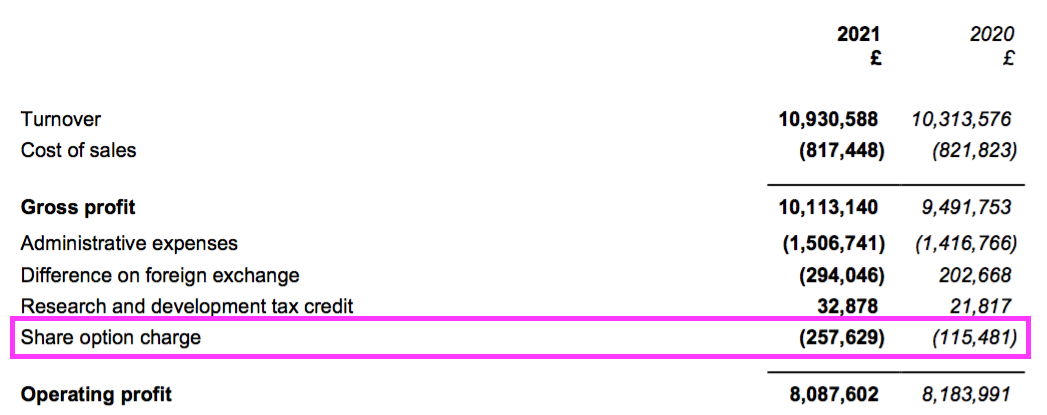

- Share-based payments created another slight distortion on reported profit.

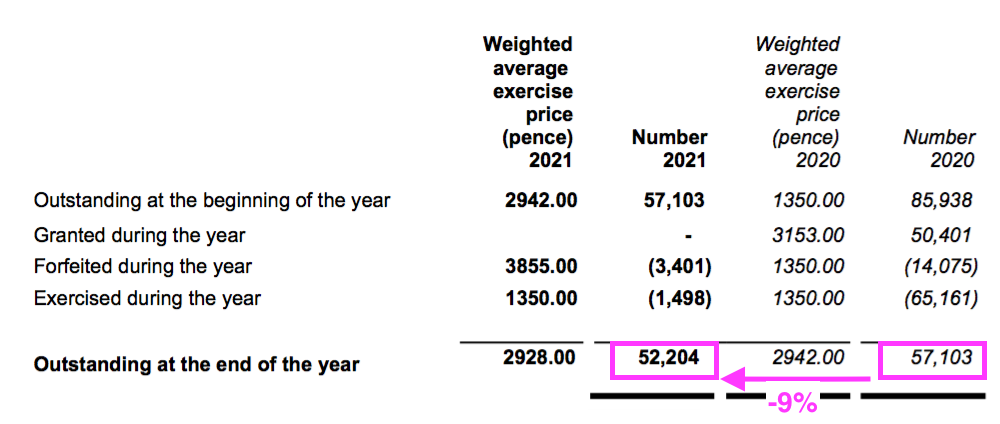

- The mysteries of IFRS 2 accounting ensured the share-based payment more than doubled to £258k…

- …while the number of outstanding options declined by 9%:

- Outstanding options represent 1% of the share count while their IFRS 2 cost reduced reported operating profit by 3%.

- Cash conversion was not as exceptional as previous years:

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit* (£k) | 5,691 | 6,060 | 6,931 | 8,184 | 8,087 |

| Depreciation (£k) | 39 | 58 | 76 | 134 | 135 |

| Cash capital expenditure (£k) | (22) | (108) | (85) | (340) | (260) |

| Working-capital movement (£k) | (570) | (539) | (47) | 412 | (1,004) |

| Net cash (£k) | 6,167 | 6,987 | 6,537 | 8,076 | 6,495 |

(*before back-dated royalties)

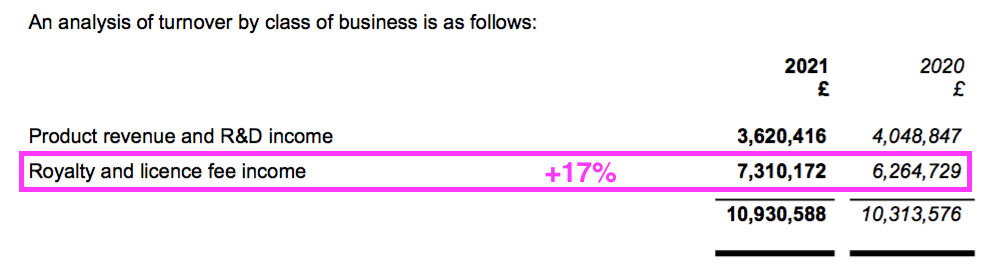

- Working-capital absorbed an extra £1m after royalty and licence-fee income gained 17% to represent a larger (68%) proportion of revenue:

- Royalty and licence-fee income is invoiced at every half-year/year-end, and the £1m working-capital movement represents the cash still to be paid as an increased debtor after the associated income was recognised as revenue:

- The £1m working-capital movement alongside £0.2m spent finishing the laboratory revamp meant free cash flow dropped by £1.3m to £6.1m for the year.

- Total cash dividends of £7.7m then left the cash position £1.6m lighter at £6.5m.

- The £6.5m cash position exceeds the £5m that BVXP reiterated was “sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future and to provide comfort against the ongoing impact of the pandemic and any economic uncertainty arising from it.”

- The £1.5m difference between the £6.5m cash position and the £5m “comfort” buffer equates to 29p per share — and compares to the 38p per share special dividend declared within these results.

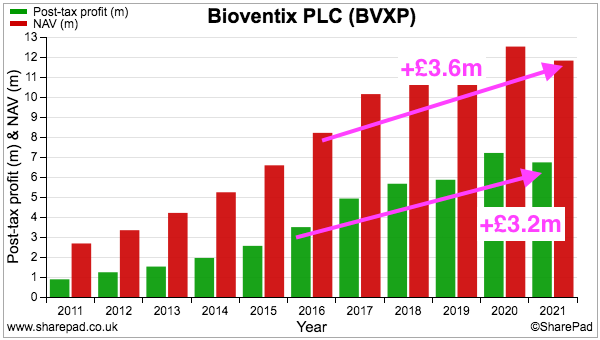

- The sixth consecutive year of declaring a special dividend re-emphasised how BVXP has expanded without significant retained profits.

- Since FY 2016, BVXP’s earnings have advanced £3.2m to £6.7m while shareholder equity (i.e. earnings less all dividends paid) has advanced £3.6m to £11.8m:

- Retaining £3.6m to earn an extra £3.2m since FY 2016 has been very impressive.

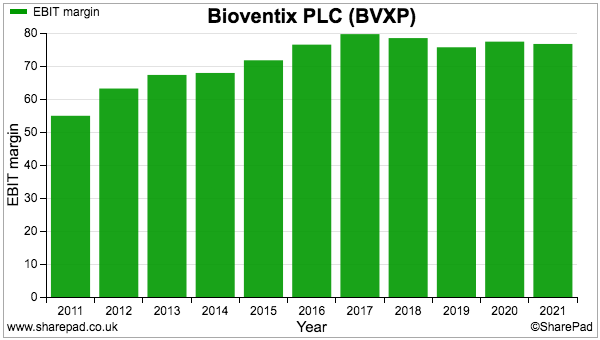

- The operating margin remains in the 70%-plus stratosphere and underlines the wonderful economics of collecting royalties and license fees from successful antibodies:

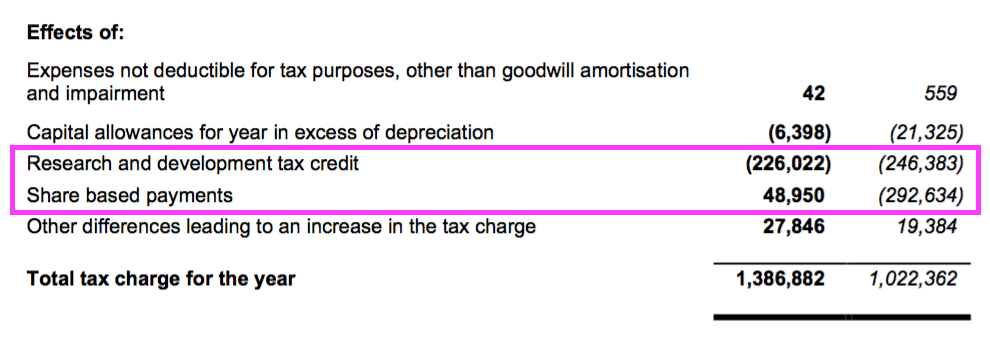

- BVXP’s tax charge increased from a rather modest 12% to 17% of pre-tax profit following a lower R&D tax credit and (complicated) movements associated with share-based payments:

- The £610k book value of BVXP’s investments in pipeline-development partners Cardinor and Pre-Diagnostics appears understated.

- Intuitive Investments (IIG) paid £125k for 1.8% of Cardinor during March, which implies Cardinor is worth almost £7m.

- This 2018 document from the Cardinor website indicates BVXP is a 21.5% Cardinor shareholder, and suggests BVXP’s investment has a £1.5m value based on IIG’s purchase.

- This document from the Pre-Diagnostics website indicates BVXP is a 7.5% Pre-Diagnostics shareholder, the investment cost of which I think is approximately £0.4m.

- The balance sheet carries no bank debt and no pension complications.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- BVXP’s outlook was identical to that of last year and again did not seem too concerning:

“The timing of a return to normality is uncertain but when it does, we expect our business will revert to an established trajectory, albeit without the income from NT-proBNP which ceased from July 2021. Regardless of the pandemic effects, we anticipate the continued roll-out of the high sensitivity troponin assays and the royalties associated with this.”

- Exactly what the “established trajectory” will be post-pandemic remains to be seen. But a return to the c20% growth rates of the past feels very unlikely.

- In contrast to last year, when BVXP singled out “remarkable” progress at the pollution-exposure project, this year’s outlook noted positive progress within more than one research project:

“Excellent technical progress has been made with our research projects including the industrial pollution exposure project and we anticipate that this project and others in our pipeline will create additional shareholder value in the years ahead.”

- The pipeline projects will take on greater importance as the 2032 expiry of troponin income becomes closer.

- BVXP’s valuation remains elevated.

- Doubling up the record H2 gives an operating profit of £9.2m before foreign-exchange gains/losses and share-based payments.

- Applying standard 19% UK tax then gives earnings of 143p per share and a possible P/E of 25 with the shares at £36.

- Remember that BVXP has lost NT proBNP revenue (and perhaps profit) of £1.28m since the year end.

- Consider, too, that troponin profit can’t really be valued on a simple multiple since its contributions will cease during 2032.

- Assuming troponin revenue:

- Averages (a probably optimistic) £4m for the next 10.5 years before expiry;

- Has no associated cost:

- Is taxed at the present 19% standard UK rate…

- …gives an after-tax value of £34m before any time-value discounting.

- The table below derives the possible earnings from BVXP’s vitamin D and other commercialised antibodies by:

- Estimating FY 2021 revenue without NT proBNP and troponin;

- Then subtracting all cost of sales and administration expenses;

- Then adding back all R&D costs, and;

- Ignoring foreign-exchange gains, share-based payments and R&D tax credits:

| Estimated FY 2021 for vitamin D and other antibodies | (£k) |

| Revenue | 10,931 |

| Less NT proBNP revenue | (1,280) |

| Less troponin revenue | (680) |

| Less cost of sales | (817) |

| Less admin expenses | (1,507) |

| Add back R&D expenses | 1,201 |

| Operating profit | 7,848 |

| Less tax at 19% | (1,491) |

| Earnings | 6,357 |

- Applying a 25x multiple to the derived £6.4m earnings values BVXP’s vitamin D and other commercialised antibodies at £159m.

- The present £188m market cap less the £34m troponin estimate less the £159m vitamin D/other estimate therefore leaves the pipeline valued at a negative £5m.

- Valuing the pipeline at a negative £5m seems about right if annual R&D costs are £1.2m and research commercialisation is not expected until 2025 at the earliest:

- True, these valuation sums could be fine-tuned further to:

- Calculate a more realistic net present value for troponin;

- Adjust for the forthcoming 25% UK tax rate;

- Allocate cost of sales to the appropriate antibody, and;

- Apply different multiples to that £6.4m vitamin D/other estimate…

- …but right now signs of a tantalising valuation are not exactly obvious.

- A premium rating is nonetheless understandable. Attractions include:

- The predictable and ongoing income from antibody sales and royalties (pandemics aside);

- A competitive ‘moat’, helped in part by protracted development/regulatory timescales and customer contractual/installation restrictions, and;

- The amazing margins and returns on equity, which underline the terrific economics of antibody commercialisation.

- The present market cap leaves longer-term upside rather dependent on the success of the pipeline, with the pyrene project and then the Alzheimer’s work perhaps looking the favourites to succeed.

- In the meantime the income yield is a useful 4% if BVXP continues to distribute ordinary and special payouts that total 143p per share.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Maynard,

Great write up and analysis.

I have Bioventix and I have been doing my own process as to whether I hold or sell.

Thanks

Colin Farrier

Thanks Colin. Glad you found it useful.

Maynard

I am in awe of your analysis. Fantastic.

Thanks Stephen. Hope everything I’ve written is accurate!

Maynard

Bioventix (BVXP)

Publication of 2021 annual report

Very late catching up with this report, which includes much more information (including photos!) than the previous (text-only) editions. The appointment of an employee finance director during 2020 (versus the ‘outsourced’ predecessor) now looks prompted by the need for enhanced corporate disclosures as the reporting requirements of quoted companies increase.

Anyway, here are the points of interest:

1) INTRODUCTION AND TECHNOLOGY

BVXP’s reports start with a useful primer about the business. No major changes to the text from last year, although the total of purified physical antibody sold annually has increased from 10-20 grams to 15-20:

“Over the past 17 years, we have created and supplied approximately 20 different SMAs that are used by IVD companies around the world. We currently sell a total of 15–20 grams of purified physical antibody per year, the vast majority of which is exported.”

The text reiterates the regulatory and R&D “barrier to entry” enjoyed by proven antibodies:

“The process of subsequent development thereafter by our customers can take many years before registration or approval from the relevant authority, for example the US Food and Drug Administration (FDA) or EU authorities, is obtained and products can be sold to the bene t of the customers and of course Bioventix through the agreed sales royalty. This does mean that there is a lead time of 4–10 years between our own research work and the receipt by Bioventix of royalty revenue from product sales.

However, because of the resource required to gain such approvals, after having achieved approval for an accurate diagnostic test using a Bioventix antibody, there is a natural incentive for continued antibody use. This results in a barrier to entry for potential replacement antibodies, which would require at least partial repetition of the approval process arising on a change from one antibody to another. ”

2) 2020-2021 FINANCIAL RESULTS

Useful text explaining the financial effect of currency movements:

“Sales invoiced in foreign currencies are recorded in Sterling at the exchange rate on the date of sale. When Dollar and Euro monies are received, they are immediately converted into Sterling at the exchange rate applying on the date of arrival. Any difference in exchange rate between the date of invoice and the date of receipt is reported in the form of an exchange rate adjustment and is recorded in the period as a loss or gain when it is crystallised.

The effect of these adjustments during the current year has been particularly large and provided a negative effect of £0.29 million which has been crystallised and recognised in our results for this year, compared to a positive effect of £0.20 million for the previous year; a total movement between the years of almost £0.5 million.

The critical period for such differences arises around the time of royalty receipts in February and August when debtors, in respect of turnover recognised in the six-month periods ended 31st December and 30th June respectively, are recorded in Sterling at exchange rates applicable at those balance sheet dates rather than at the exchange rates at the date the royalties are received.

We have no current plans to institute any hedging mechanisms to cover these short periods or indeed any longer periods and therefore any future changes in exchange rates, up or down, may impact our reported Sterling revenues accordingly.”

Royalty income represents a significant level of BVXP’s revenue and is received twice a year from various customers. Therefore BVXP is more exposed to currency fluctuations than businesses where customers pay evenly throughout the year. Essentially BVXP takes a hit if USD weakens against GBP during the c6 weeks after each balance-sheet date, but enjoys a gain if GBP weakens against USD.

3) STRATEGIC REPORT

BVXP made no changes to its principal risks and uncertainties.

a) Directors’ statement of compliance with duty to promote the success of the Company

Some new text for 2021 explaining the enhanced disclosures:

“Our 2021 Annual Report contains expanded governance disclosures and a sustainability report. The Corporate Governance report details the structure of the Board, its Committees and the meetings held during the year to 30th June 2021. Discussion topics at each meeting included the Company’s response to the COVID-19 pandemic, health and safety, staff welfare, research and development progress, customer feedback and financial performance. The Sustainability report on pages 26 to 29 contains information on our social and environmental interactions with our immediate and wider communities.

Culture, values and standards form the foundations for a company’s operating behaviours and processes by which it creates and sustains value. They also assist and guide decision-making and thereby help promote a company’s success. The Board will continue to build its model for engagement with key stakeholders and will, in future reports, provide more detail of our progress, including how we engage and the impact of such engagement on the Company’s strategy and principal decisions.“

4) SUSTAINABILITY REPORT

A brand new section for 2021. No great revelations, but a few interesting snippets.

I can’t recall another company within my portfolio that says the boss conducts a results briefing for the staff:

“In addition, to ensure that all staff are aware of the Company’s strategy and performance, all staff are notified when interim and full year Annual Reports are published and the CEO conducts a briefing to which all staff are invited where full information is provided and discussed in an open and inclusive environment.”

The pollution-detection project may enjoy an ESG tailwind:

“The provision of pollution-free, safe environments is a core responsibility for governments and many organisations. The work to adapt our technology to develop straightforward tests with accessible and timely analysis and results is a new development in the Company’s product set.”

BVXP’s enhanced reporting does not extend to a full Carbon Emissions report (presumably due to the group’s low emissions), but the staff (many of whom apparently are part time) do their bit for the environment:

“Whilst our products are used all round the world, Bioventix is a small organisation with laboratory and administration facilities in one location in the UK occupying c600 sqm. We employ 16 people, many on a part-time basis. Our environmental impact is therefore relatively small…

We encourage all staff to reduce wastage, not to print unnecessarily, to optimise the use of lighting and heating and cooling units and switch off any electrical equipment when not in use.”

5) THE BOARD OF DIRECTORS

The enhanced disclosure within this report include fresh director biographies. The two non-execs both offer useful sector experience:

“Ian was appointed as Non-Executive Chairman of Bioventix in November 2004. Ian is also a Non-Executive Director of Clinigen Group PLC, a specialty pharmaceuticals and services business and also an Operating Partner at Advent Life Sciences LLP. From 2013 to 2021 Ian was Chief Executive Officer of F2G Ltd, an antifungal drug development company, and from 2004 to 2012 Ian was Chief Executive of Chroma Therapeutics Limited, a drug discovery and development company. He previously held the position of Senior Vice President, Business Development at Celltech Group PLC, then the UK’s largest biotechnology company. He has extensive experience in licensing, mergers and acquisitions, and market development in the UK, Europe and the US. Ian is Chairman of the Audit Committee and is a member of the Remuneration Committee.”

“Nick was appointed as Non-Executive Director of Bioventix in 2014 when the Company first listed on AIM. Nick has worked in the biotech industry for over 30 years and is now an independent consultant providing operational, strategic and commercial advice and hands-on support to biotech companies. He has led several successful companies. He was the founding CEO of Solexa, the Cambridge University spin-out where he built the team that invented and developed Next Generation DNA sequencing. Subsequently he was CEO of Belgian company Pronota, which translated novel protein biomarkers into diagnostics, and where he gained much knowledge and expertise in the diagnostic development and market access process. Most recently he was CEO of DNA sequencing technology company Longas Technologies pty Ltd. He has an MBA from the London Business School. Nick is Chairman of the Remuneration Committee and Nomination Committee and is a member of the Audit Committee. ”

The two non-execs are deemed independent by BVXP, but both have been awarded options (and the chairman was appointed in 2007 and so has been in place for more than the standard nine years):

“The Independent Non-Executive Directors, Ian Nicholson and Nick McCooke, are both considered as independent by the Board and are both participants in the Company’s Unapproved Share Option Scheme. The Board recognises that since independence can be easily compromised, Non-Executive Directors should not normally participate in performance-related remuneration schemes or have a significant interest in a company share option scheme. The QCA Code acknowledges that where performance-related remuneration is under consideration, it should be proportionate, and shareholders must be consulted and their support obtained. Prior to the grant of share option awards, in 2017 and in 2020, the Board consulted with all material shareholders and there were no dissenting views. Furthermore, the Board believes that the participation, by the Non-Executive Directors, in the Company’s Unapproved Share Option Scheme has not and does not impair their ability to act as independent Non-Executive Directors.

6) CORPORATE GOVERNANCE

BVXP has revamped its compliance statement concerning the 10-point QCA Code. No great revelations, but the text says AGM questions are encouraged:

“The Company recognises the importance and the benefit of engaging with its shareholders…

The Board also engages with shareholders to understand their needs and expectations primarily through meetings with Executive Directors when presenting financial results but as required at other times (this applies in the main to institutional investors or those with significant shareholdings) including at the AGM to which, subject to any restrictions implemented in response to the COVID-19 pandemic, all shareholders are welcome and encouraged to ask questions of the Board. Formal feedback from shareholder meetings is provided by the Company’s broker and discussion of this feedback is a standard item on the Board’s agenda.”

I have owned BVXP shares for six years and have yet to attend any company presentation or meeting. I hope to attend this year’s AGM to understand more about the pipeline developments.

7) AUDIT COMMITEE REPORT

All new (boilerplate) text for 2021.

8) REMUNERATION COMMITEE REPORT

Nothing of great concern here.

The chief exec’s total pay increased by only £1k, with an £11k lower salary made up for by a £9k higher bonus and a £1k greater pension contribution:

The new FD was appointed at the start of the 2021 financial year, so his £62k salary is either very good value for an AIM finance director or he works part time.

The bonus calculation remains dependent partially on EPS:

“The Chief Executive bonus above was determined by the Remuneration Committee. The basis was designed to be consistent with companies of a similar profile and contains performance conditions relating to Earnings per Share (EPS) and share price parameters, together with a smaller Research and Development (R&D) element.”

EPS was flat during 2021 but gained 20%-plus during 2020, so presumably the other measures were assessed to ensure a higher bonus was paid to the chief exec for 2021 than for 2020.

Pay for 2022 will commendably remain the same, but the door has been left open for greater pay for 2023:

“The Committee met in July 2021 and considered Director remuneration for the financial year 2021/22. In light of the ongoing COVID-19 pandemic and the ensuing uncertainty it was deemed that remuneration would remain unchanged for 2021/22 and that the Committee would carry out a comprehensive review for 2022/23.

BVXP has clarified its option grants:

*Following legal advice Options granted to two directors under the Company’s EMI Share Option Scheme on 6/1/2017 were surrendered and regranted with replacement non-EMI Share Options granted under the Company’s Unapproved Share Option Scheme on 17/1/2020; the key terms and conditions relating to price, vesting and option periods for the regranted options remained unchanged from those originally granted which were surrendered. However, the replacement non-EMI options will not benefit from the tax-advantaged status of EMI Options.

The original grant and subsequent regrant were not announced at the time, which is why the option table within the 2020 report was so confusing.

BVXP does not in fact announce director option grants at all via the RNS, which seems bad practice, and shareholders are left to consult the annual report for changes:

9) NOMINATION COMMITEE REPORT

All new (mostly boilerplate) text for 2021. A few lines on diversity and potential new recruits “as the business grows:

“A diversity of skills, background knowledge, international and industry experience, race and gender, amongst many other qualities, will always be taken into consideration when seeking to appoint new Directors to the Board.

The Committee met twice during the year to consider the composition of the Board and, in particular, to review the requirement to appoint further Non-Executive Directors as the business grows. Future appointments will be made based on required expertise to match the needs of the business whilst bearing in mind the need to introduce diversity into the Board composition.”

FCA rules on board diversity cover only companies traded on the main market, not AIM. BVXP’s directors are all white and all men.

10) INDEPENDENT AUDITOR’S REPORT

Nothing too alarming here.

Key audit matters remain the same as before: revenue recognition, management override and valuation of investments.

Materiality was a standard 5% of pre-tax profit and a full-scope audit was performed.

11) NOTES TO THE FINANCIAL STATEMENTS

No changes to BVXP’s accounting policies for 2021. But this new text was added about the company’s investments:

“Carrying value of Unlisted Investments

The Company holds two unlisted investments in companies carrying out research in identifying biomarkers for diagnosing health conditions. The Directors have reviewed the progress of this research over the last year and, in common with much scientific research there is uncertainty, both in relation to the science and to the commercial outcome, and no information to be able to reliably calculate a fair value for these investments. The carrying value of these investments will continue to be historic cost.”

My research in the blog post above indicated the £610k historic cost (and carrying value) may be understated after those unlisted investments raised further money. Arguably BVXP calculated a fair value at the time of purchase, so should be able to derive a fair value today.

12) OPERATING EXPENSES

Minimal audit fees once again:

R&D costs at £1.2m are equivalent to 11% of revenue and within the 10-13% range seen since 2014. I presume an overlap exists between staff costs and R&D costs, or some sort of correlation.

Missing from the disclosure is a ‘cost of stock expensed’ entry, which may be due to BVXP adhering to the old-style UK GAAP accounting (AIM rule 19 for single-entity companies).

12) EMPLOYEES

Nothing too concerning here:

Average cost per employee increased by £8k to £77k, but that advance was due to the greater share option charge. Average wage/salary per employee was in fact £1k lower at £53k. Revenue per employee was £1k lower, too, but at a still-impressive £643k. The annual report says elsewhere there are 16 employees (not 17), and some are part time, so the staff productivity ratios on a full-time equivalent basis could be even better.

13) STOCKS

BVXP continues to carry stock (the aforementioned “purified physical antibody) at a minimal sub-3% of revenue:

Average year-end stock of £289k and cost of sales at £817k imply the stock sits in BVXP’s freezers for c4 months before being sold.

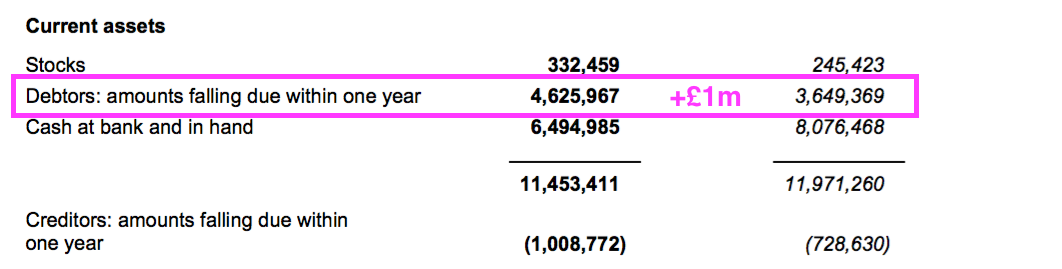

13) DEBTORS

A significant increase to prepayments and accrued income:

The bulk of prepayments and accrued income is represented by royalty income, which is accounted as revenue for the period although the customer had not been invoiced (and of course had not paid) at the balance-sheet date.

(BVXP’s customers inform (or “self declare”) BVXP of their global sales after each period end, and therefore BVXP can never be in a position to invoice the appropriate royalty sum at the balance-sheet date).

Anyway, the year-end prepayment and accrued income figure for 2021 is equivalent to 54% of royalty revenue, which compares well to between 51% and 56% for 2014-2019. The low level of prepayment and accrued income for 2020 now looks to have been a pandemic-influenced figure.

14) CREDITORS

Nothing amiss here:

BVXP owes relatively little to its suppliers and other creditors; most money owed is tax.

15) TAXATION

Useful footnote here:

Text reveals what the tax would have been had the upcoming 25% rate been applied for FY 2021. Charge would have been 22% instead of 17%, with BVXP still benefitting from R&D tax credits. I do not know why the £1,359k footnote tax figure excludes the £28k ‘other differences’ cited with the calculation table.

Maynard