13 March 2018

By Maynard Paton

Update on Tasty (TAST).

Event: Preliminary results for the 52 weeks to 31 December 2017 published 13 March 2018

Summary: Phew! I had thought TAST’s plunging share price was signalling these results would be accompanied by an emergency equity placing. As it turns out, the beleaguered restaurant chain continues to report a profit and has surprised me by raising £4m — equivalent to half of its market cap — from two property transactions. Furthermore, management now has a proper turnaround plan in place, the second half showed a few glimmers of hope while the upside could be considerable if a recovery ever occurs. I have bought more shares, both before and after these results.

Price: 13p

Shares in issue: 59,795,496

Market capitalisation: £7.8m

Click here to read all my TAST posts.

Results:

My thoughts:

* Directors issue “clear plan to return to growth” and suggest 2018 outlook is not terminal

These results were not quite the disaster TAST’s plunging share price had been suggesting.

Grim half-year figures back in September had already heralded a substantial profit drop.

Furthermore, persistent bad news within the wider casual-dining sector — notably from Prezzo and Carluccio’s — had prompted me to speculate whether TAST was losing money and could require extra funding.

Thankfully these results confirmed the business had remained profitable, and that various property deals had shored up the balance sheet.

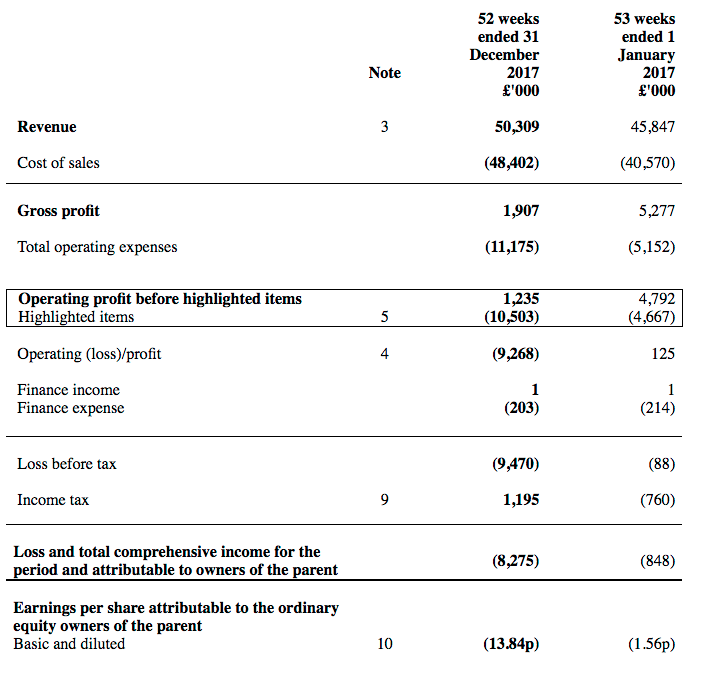

Total revenue gained 10% to £50m — a group record — after TAST’s estate was increased from 61 to 64 restaurants. However, operating profit before various write offs collapsed 77% to £1.1m:

| Year to c31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 23,192 | 29,734 | 35,794 | 45,847 | 50,309 |

| Operating profit before pre-opening costs (£k) | 2,106 | 2,986 | 3,818 | 4,692 | 1,101 |

| Pre-opening costs (£k) | (244) | (360) | (644) | (642) | (413) |

| Operating profit (£k) | 1,847 | 2,626 | 3,174 | 4,050 | 688 |

| Net finance cost (£k) | (120) | (74) | (107) | (213) | (202) |

| Other items (£k) | 15 | - | - | (3,925) | (9,956) |

| Pre-tax profit (£k) | 1,742 | 2,552 | 3,067 | (88) | (9.470) |

| Earnings per share (p) | 2.95 | 3.88 | 4.64 | (1.56) | (13.84) |

| Dividend per share (p) | - | - | - | - | - |

TAST’s statement did not dwell on the “difficult market conditions” that had blighted the group’s performance.

Instead, the management narrative — which I note was much more informative and lengthier than those of previous years — outlined the board’s “clear plan to return to growth”.

Action items included:

“Rationalise the estate

For each of these [underperforming] sites, turnaround strategies have been introduced and where these have not been successful the Group has sought to dispose of the property.Re-connect with customers

The Group identified that customer engagement was too low in a number of areas including feedback on service, feedback on food and customer communication via social media. The marketing department has been strengthened in 2017 to facilitate changes in these areas.Invest in our staff

The Group has begun to completely overhaul the training framework that exists in the business with a view to increasing staff retention and improving overall customer experience. The framework is being drastically improved at all levels of the organisation supported by apprenticeships.Invest in our structure

During 2018 the Group plans to restructure the operations team, flattening the structure and reducing headcount. This will reduce the operational costs and provide clear reporting lines to the senior management team, improving the speed and quality of business decision.”

Certainly TAST’s directors now appear much more focused on revitalising the business than they were a year ago. During the last AGM, the executives admitted they had been “a bit slow” to react to the various trading problems.

The outlook for 2018 is not great, but is not terminal either:

“The Board does not expect market conditions to improve in 2018 and believes that a further deterioration is likely. Underlying input costs will continue to rise and consumer spending will face increased pressures. The Group’s next round of operational improvements are targeting improvements in the areas of sales, food and labour margins, however it will be some time before the full benefit of these changes is felt and financial performance in 2018 is very unlikely to see any improvement on 2017.”

I dare say the most shareholders can expect for 2018 is a similar £1m profit to that recorded for 2017. TAST admitted a “number of restructuring costs” would be incurred this year.

* H2 shows glimmer of hope through greater revenue per site

There were some (relatively) encouraging signs within the first-half/second-half split:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 21,794 | 24,053 | 45,847 | 24,375 | 25,934 | 50,309 | |

| Average number of units | 50 | 56.5 | 54.5 | 63 | 64.5 | 62.5 | |

| Average revenue per unit (£k) | 839 | 851 | 841 | 774 | 804 | 805 |

Average revenue per restaurant during H2 was £804k — a decent 4% improvement on the terrible £774k for H1 and down ‘only’ 6% on the £851k for H2 2016 (average revenue per unit during H1 was down 8% on H1 2016).

For some context, the average TAST restaurant generated revenue of £929k during 2014:

| Year to c31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 23,192 | 29,734 | 35,794 | 45,847 | 50,309 |

| Year-end restaurants | 28 | 36 | 48 | 61 | 64 |

| Average restaurants | 25.5 | 32 | 42 | 54.5 | 62.5 |

| Average revenue per restaurant (£k) | 909 | 929 | 852 | 841 | 805 |

The second half enjoyed minor margin improvements, too, although the effect of various trading initiatives — notably discount vouchers — can be clearly seen by the thin levels of profitability:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 21,794 | 24,053 | 45,847 | 24,375 | 25,934 | 50,309 | |

| Gross profit (£k) | 2,252 | 3,025 | 5,277 | 893 | 1,014 | 1,907 | |

| Operating profit*(£k) | 1,875 | 2,817 | 4,692 | 494 | 607 | 1,101 | |

| Gross margin (%) | 10.3 | 12.6 | 11.5 | 3.7 | 3.9 | 3.8 | |

| Operating margin* (%) | 8.6 | 11.7 | 10.2 | 2.0 | 2.3 | 2.2 |

(*before pre-opening costs and various write-offs)

I was pleased the second half did not present shareholders with further substantial restaurant write-offs:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Profit on disposal (£k) | - | - | - | - | 1,237 | 1,237 | |

| Onerous leases (£k) | - | - | - | - | (1,635) | (1,635) | |

| Lease impairment (£k) | (294) | - | (294) | (172) | 76 | (96) | |

| Asset impairment (£k) | (3,576) | - | (3,576) | (9,320) | (142) | (9,462) | |

TAST has written off assets of some £13m during the past two years.

The £1.6m onerous lease provision covers four sites where “projected future trading income is insufficient to cover the unavoidable costs under the lease“.

Essentially TAST is taking an upfront charge for seeking to abandon these properties, and an exit timescale was suggested:

“It is expected the majority of the provision will be utilised over the next 24 months.“

* Post-year-end property deals raise £4m with further sites still to be sold

A trading statement during January revealed TAST had received £2m following four restaurant closures and a sale-and-leaseback transaction.

These results confirmed six units had closed and, notably, proceeds from two transactions completed after the year end had raised £4.15m.

Here are the details:

“Canary Wharf Wildwood

The lease for this property was assigned on 5 January 2018 for a premium receivable by the Group of £1.45m.Ilkley Wildwood Kitchen

The lease of this property was assigned on 22 September 2017 for a premium receivable by the Group of £120,000.Abingdon Wildwood Kitchen

A surrender of the lease was agreed on 14 January 2018 at no cost to the Group.Bristol Wildwood Kitchen

The lease on this site was surrendered on 31 December 2017 at a cost of £195,000 to the Group.Barnes Wildwood Kitchen

Contracts have exchanged on this property with the lease due to be assigned imminently at a net cost of £nil to the Group.Gloucester Road Wildwood

On 8 March 2018 this unit was sold as a going concern for a consideration of £2.7m”

I have to admit, I am pleasantly surprised only one site incurred an exit cost.

Here is a very important note (my bold):

“Funds for Canary Wharf and Gloucester Road totalling £4.15m have been received in 2018 and are not included in the cash and cash equivalents in these financial statements.”

TAST also said:

“In addition to the above, the Company undertook a sale and leaseback transaction during the period, purchasing and later selling the freehold of our Kettering site.”

I am glad this sale-and-leaseback transaction has been explained (I had been confused), and has led to a profit. The accounting small-print stated:

“During the period the Company purchased and disposed of a freehold property in a sale and leaseback transaction. Net proceeds of this transaction was an inflow of £620,000…”

Given the disposal proceeds raised to date — and how they compare to the current market cap — I welcome this next remark:

“There are a number of sites that the Group is still planning to dispose of…”

* Current borrowings do not appear alarming

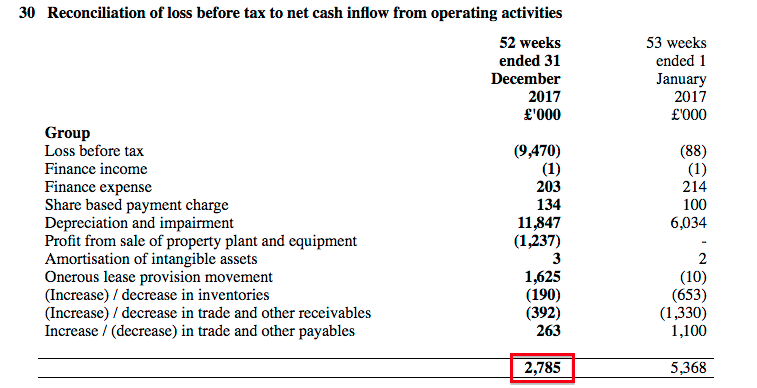

TAST’s cash generation did not look too bad to me.

Net cash from operations was £2.8m, of which £1.7m was produced during the second half:

Net capital expenditure for 2017 came to £5.8m, while the working-capital movement was minor:

| Year to c31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit* (£k) | 1,847 | 2,626 | 3,174 | 4,050 | 1,101 |

| Depreciation and amortisation (£k) | 1,124 | 1,312 | 1,712 | 2,045 | 2,149 |

| Net capital expenditure (£k) | (4,783) | (6,378) | (9,844) | (11,652) | (5,777) |

| Change in working capital (£k) | (1) | 1,215 | 67 | (883) | (319) |

| Net cash/(debt) (£k) | 2,407 | 1,294 | (3,529) | (1,996) | (5,157) |

(*before pre-opening costs and various write-offs)

It all left cash in the bank at £1.8m, which ought now to stand close to £6m following the aforementioned Canary Wharf and Gloucester Road disposals.

Borrowings of £7m mean net debt could now be approximately £1m — which, despite what TAST’s share price may be suggesting — does not appear too alarming.

These results also confirmed:

“At present the Group is not committed to any new openings in 2018.”

As such, capital expenditure should be reduced significantly this year. I am hopeful the cost of maintaining the restaurant chain can be broadly similar to the £2m depreciation charge.

* Overcapacity, rising costs, fading high streets and bargain-seeking diners

Twelve months ago I felt TAST’s problems were more to do with stale menus and complacent management than wider sector problems.

However, the aforementioned bad news from the likes of Prezzo and Carluccio’s — plus various warnings from sector star Fulham Shore — do underline the industry difficulties TAST currently faces.

Problems include:

i) overcapacity leading to discounting, not helped by struggling chains desperate for revenue;

ii) rising costs — staff, ingredients, business rates, and so on;

iii) fading high streets leading to lower footfall, and;

iv) bargain-seeking diners — now accustomed to vouchers (see point i)

At least TAST’s directors are taking action. Units have been closed, menus have been trimmed and even a fresh dining format has been launched. Whether the recovery plan is enough, though, is hard to judge.

As before, I am resting everything on management’s past history.

TAST’s boardroom is staffed by two members of the Kaye family, which in total owns approximately 40% of the business and has already built and sold multi-bagger chains ASK Central for £223m (in 2004) and Prezzo for £304m (in 2015).

I have written this before, but I don’t think you can lose decades of such expertise overnight.

Valuation

This time last year I remarked:

“My past experience with ‘roll-out’ companies has told me valuations can become very depressed if investors worry about the chain format failing entirely…

…and I dare say a very depressed rating could soon befall TAST.”

The share price then was 80p and I do recall thinking, if the worst ever came to the worst, we could see 40p.

Well, the price today is 13p, which supports an £8m market cap.

It is worth noting that an £8m market cap compares very favourably to the £4m TAST has just raised from the Canary Wharf and Gloucester Road transactions.

Even if TAST’s future property proceeds come to nothing, the present valuation can hardly be described as expensive… assuming that is:

i) the business can sustain an underlying £1m operating profit for 2018, and;

ii) net debt can be kept at £1m.

Here is one recovery scenario. Closed units cut revenue by 20% to £40m, while other actions help improve the group’s operating margin to 5%. TAST would then report a £2m operating profit.

Such a performance could clear the outstanding net debt… and leave the present £8m market cap looking remarkably cheap.

Also consider the Kaye family management, and its track record of building and then selling quoted restaurant chains for £200m-plus.

Revitalising TAST and then selling it for ‘only’ £40m would still give a five-bagger from here.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in Tasty.

Tasty (TAST)

Effective publication of 2017 annual report

This results RNS effectively included the 2017 annual report. Credit to TAST for publishing the full audited numbers in a reasonable timescale.

Here are the points of interest:

1) Going concern and covenant tests

This report is the first I have ever looked at where I had to double-check the ‘going concern’ and ‘covenant test’ notes:

Everything seems in order, given the circumstances.

I have to say, I do not like having to check such notes when reading a set of results.

2) Risks and uncertainties

Not surprisingly, the report’s Risk section was expanded.

‘Supplier failure’, ‘consumer habits and competition’, and ‘regulatory risk’ were all added:

The ‘strategic risks’ section was changed, and claims the chain will one day look to acquire sites.

3) Sale and leaseback

So here is the note referred to in the Blog post above that mentioned the £620k cash inflow from the sale-and-leaseback transaction:

The accounts indicate the freehold was purchased for £417k:

The cash flow statement indicates the freehold was sold for up to £975k:

£975k less £417k = £558k. I am not sure why there is a difference to the £620k in the other note. To be honest, I am pleased TAST could make a decent turn on this freehold in such a short time.

4) Profit on disposal of property, plant and equipment

The “highlighted items” shows a £1,237k gain following the disposal of property, plant and equipment:

This £1,237k must be a combination of the gains following the sale-and-leaseback and the Canary Wharf disposal, the latter transaction bringing in £1.45m after the year end but the accounting gain being recognised in these accounts.

5) Onerous lease provision

This ‘key audit matter’ note is informative. It suggests there are restaurants that lose money on an EBITDA basis:

The left-hand column shows the provision relates to four leases.

Here is the relevant accounting policy:

And here is confirmation the provision will cover the next three years:

By making a three-year provision now — and taking a single ‘exceptional’ charge to the 2017 income statement — TAST’s future income statements will be flattered because the costs were not spread out over the three years.

However, the actual cash costs can’t be rejigged and will be shown in future cash flow statements under ‘onerous lease provision movement’.

6) Impairment of property, plant and equipment

Another informative ‘key audit matter’:

It seems some of the restaurants incurring write-offs were “new“. That does not sound great.

This next note seems to indicate assets of £17,520k were written down to £8,058k — or by 54%. The difference — £9,462k — is indeed the impairment entry against property, plant and equipment:

7) IFRS16 lease accounting

Brace yourself for IFRS16’s ‘material impact’ on the accounts:

IFRS16 introduces a new regime for lease bookkeeping. Essentially TAST’s lease obligations, which are currently tucked away in this accounting note…

…will be brought onto the balance sheet and various movements will be passed through the income statement. There will be no effect on actual cash flow, but the accounting will become more complex. I look forward to reading the associated “extensive disclosures“.

8) Lease costs

Still on leases, I see lease costs increased by 30% during 2017:

I am not sure whether that figure includes pay offs for abandoning certain restaurants. Still, it is not a great sign that lease costs are up 30% when revenue is up only 10%. Lease costs represented 12% of revenue for 2017, versus between 10.0% to 10.5% for 2014/15/16. The 12% proportion is the highest seen since 2010.

10) Related party transactions

And still on leases… TAST paid less to the Kaye family’s property empire last year:

I don’t know whether these related-party notes are prepared on an accounting/accrued basis, or a simple cash-flow basis. Either way, TAST owes the Kayes £137k.

11) Employees

TAST managed to trim the average employee cost during 2017:

A total £20,617k employee bill for 1,184 employees gives £17,413 each — versus £17,878 for 2016.

That said, the employee bill as a proportion of revenue increased from 39.7% to 41.0% during 2017, while revenue per employee dropped from £44,992k to £42,491k. Employees per restaurants remained at the 18-19 level.

12) Director pay

No pay rises for the board, and I would not expect otherwise:

Maynard

Hi Maynard,

Once again thank you for your analysis. You mentioned that you bought more shares, if you don’t mind me asking, what percentage did you increase your holding by?

Hello Eric

Since the start of the year I have increased my TAST holding by 85% at an average of 15p.

Maynard

Thanks for the analysis Maynard, really detailed and useful. It looks like it could potentially be very cheap, if they can achieve a decent level of sustainable profitability. It’s a very tough sector, I think the restaurant idea / experience is very key to whether they manage to stick around or not.

Do you actually rate the Wildwood restaurants? Appreciate you view the management as strong, given past performance, but do you have a view as to whether this idea is a good or bad one. I’ve not eaten at one, (perhaps partly because) they don’t look very interesting.

I like the dim-t restaurant near the Tower of London, and they seem like a good concept, but unfortunately are a small portion of their total restaurants.

Hello Alan,

The Wildwood concept is not thrilling. It is not Wagamama or Nando’s. But if you wish to grow a chain beyond London and major City centres, the best bet is go somewhat mainstream. The advantage of having a grill/pizza/pasta/burger mix is that dishes can be changed if tastes change or some particular dish from another chain becomes fashionable. Focus on say, burgers, and you can be in trouble if burgers lose their appeal.

That said…

Wildwood’s broad menu is not that dissimilar to that of Prezzo, ASK, and so on, which is why perhaps all of these chains have hit problems.

Also… I do like TAST’s Centuno venture — a pizza-focused restaurant with a low-ish cost menu and similar-ish to Fulham Shore’s Franco Manca concept.

Low-cost menus are the way forward I think, given the structural cost increase of running restaurants these days, and the growing custom of using discount vouchers. I have to admit I would not eat in a Wildwood, Prezzo, ASK etc without a decent discount voucher.

Dim-t was the firm’s initial chain, but expansion was redirected to Wildwood in about 2010 when (I presume) the board felt the dim-sum concept would not travel that well outside London.

Maynard

Thanks for the reply. Interesting point about the pro of being flexible / mainstream but at risk of being too generic / boring.

The numbers look intriguing to me, but do think the concept is key too in a situation like this, I may look into this one further.

Thanks.

Tasty (TAST)

Restaurant numbers

The closures reported within TAST’s results have now been reflected on the Wildwood website: https://wildwoodrestaurants.co.uk/restaurants/all

Abingdon, Ilkley, Canary Wharf, Bristol and now Barnes, have been removed. Gloucester Road continues to be listed — I presume it remains a Wildwood restaurant but under different ownership.

From these links:

https://wildwoodrestaurants.co.uk/restaurants/all

https://dimt.co.uk/restaurants/

https://www.centuno.co.uk/

I see 55 Wildwoods, 6 dim-ts and 1 centuno = 62 sites.

Maynard

I never imagined the numbers would go backwards. A sign of the times as they say but good to see the management is taking action and has a plan

Thanks Maynard

David

Tasty (TAST)

Prezzo CVA Document

https://www.prezzorestaurants.co.uk/special-pages/cva/

The proposal allows Prezzo to rationalise its estate and to reduce the cost of its leased restaurants. This will allow the company to focus its resources on the core, more profitable restaurants whilst continuing to meet its obligations to suppliers and creditors.

Prezzo will be better placed to implement the changes required to refresh the Prezzo brand and to counter the economic challenges currently affecting the casual dining sector.

This proposed restructuring, under the terms of a company voluntary arrangement (“CVA”), will allow Prezzo to continue operating while it implements plans to improve its food and service and to invest in new restaurant layouts and designs.

Under the CVA process, Prezzo has submitted a restructuring plan to its creditors and will seek their approval of the CVA at a meeting on 23 March 2018. If approved by the creditors, the CVA proposal will substantially reduce Prezzo’s rental obligations and will move the business towards a more robust business model. Where restaurants are closed, we will do everything possible to redeploy staff to other sites.

Everything was formally approved today.

From a quick check of the CVA document…

PRZ divided its restaurant estate into seven categories.

Category 1 covered the sites that remained profitable at the current rent or had some “strategic value“, and would not require a rent cut. The other six categories covered units that would require a rent cut or be closed down.

I have compared TAST’s 55 Wildwood restaurants to those in the CVA document.

I ignored the 3 Wildwood’s based in central London:

Gloucester Road (now operated by a third party), Covent Garden, Shaftesbury Avenue

I found 14 Wildwoods that were not located near any PRZ-owned sites:

Birmingham, Gerrards Cross, Liverpool, Llandudno, Loughton, Ludlow, Market Harborough, Northwich, Oakham, Rushden Lakes, Skipton, Wantage, Worcester, Worcester Park

I found 26 Wildwoods that were located near a Category 1 PRZ-owned site:

Bicester, Billericay, Braintree, Brentwood, Cambridge, Canterbury, Cheam, Chelmsford, Chichester, Crawley, Didcot, Edinburgh, Ely, Hinckley, Hornchurch, Kettering, Letchworth, Maidstone, Newmarket, Nottingham, Peterborough, Plymouth, Salisbury, South Woodford, Whiteley, York.

I found 12 Wildwoods that were located in an area with only Category 2-7 PRZ-owned sites:

Bournemouth, Brentwood, Camberley, Cobham, Epping, Hereford, Kingston, Lincoln, Port Solent, Stratford-upon-Avon, Taunton, Telford.

(Of those 12, 5 of the nearby PRZ units needed a rent cut while 7 of the nearby PRZ units were due to be closed. Of those 7, 2 are a Chimichanga rather than the main Prezzo format.)

So what we have out of 55 Wildwood sites are 26 near a profitable Prezzo unit, with 12 in locations with a PRZ unit that needs a rent cut or closure. Then we have a further 17 Wildwood sites where the PRZ CVA impact is unclear.

Of course, a profitable PRZ unit does not mean the Wildwood down the road makes any money — rents, footfall and so on may differ significantly. But it is a reasonable indicator the Wildwood ought to be relatively successful.

So with 26 Wildwood outlets perhaps offering a Category 1 status, and 12 probably in Categories 2-7, the profitable-to-troubled unit ratio is about 2-to-1. Could two-thirds of TAST’s Wildwood sites actually make money?

I will read through the finer details in due course.

Maynard

(PS I note various Kaye family property companies are listed in the CVA document as landlords.)

Tasty (TAST)

Prezzo CVA Document

https://www.prezzorestaurants.co.uk/special-pages/cva/

I thought I would check to see what effect the Prezzo CVA would have on the Kaye family’s property interests.

Here are the Kaye family companies (that I know of) and the Prezzo locations listed in the CVA document. Category 1 sites are those that had remained profitable at the current rent or had some “strategic value“, and would not require a rent cut. The other categories covered units that would require a rent cut or be closed down.

Kropifko: Category 1: Bury St Edmonds, Salisbury.

ECH Properties: Category 1: Canterbury, Glasgow. Category 4: Canterbury.

Regis 2000: Category 1: Hornchurch, Maldon, Thame, Tring, Windsor.

Proper Proper T: (none)

Benja Properties: Category 1: Chichester.

Abear Properties: Category 1: Wimborne. Category 3: Maidenhead.

Noodle Properties: Category 1: Rugby, Torquay.

Superheroes Properties: (none)

Evie Milly Properties: Category 1: Peterborough.

Rosphill Properties: Category 3: Pinner

GK Property Associates: Category 1: Kings Lynn

E & J Property Associates: Category 4: Peterborough

Amberstar: Category 1: Aldeburgh, Buckingham, Horsham, New Oxford Street, Oswestry, Romsey, Uxbridge. Category 2: Radlett. Category 4: Alton, Sheffield. Category 5: Haverstock Hill.

By my calculations, these Kaye family companies owned 30 sites of which 22 are Category 1 units and therefore should not be affected directly by Prezzo’s CVA. Of the other 8 sites, 7 will face rent cuts of between 25% and 75%, while the other site will see Prezzo exit completely.

So overall, I guess this is not too bad an outcome for the Kayes.

Maynard

Excellent piece of analysis Maynard. Thanks for sharing

David

Tasty (TAST)

Director/PDMR Shareholding

This is promising. True, the transaction involved the non-exec chairman and amounted to only £20k. But what is important is that a director can’t (or should not be able to) buy or sell shares if he is privvy to precise insider information that, if released to the market, would likely cause a significant share-price movement.

That being the case, perhaps we can assume TAST is not planning a rights issue to shore up the balance sheet (at least for the moment).

Of course, this purchase could be just a token gesture by an ‘out-of-the-loop’ chairman that did not realise he owned an extra 20,000 shares last year.

Here is the full text:

——————————————————————————————————————————-

The Company today announces that on 29 March 2018, Keith Lassman, Non-Executive Chairman, purchased 165,000 ordinary shares of 10p each in the capital of the company (“Ordinary Shares”), at a purchase price of 11.9p per Ordinary Share.

Following this purchase, Mr Lassman holds 333,185 Ordinary Shares representing approximately 0.56% per cent of the Company’s issued share capital.

——————————————————————————————————————————-

Maynard

Maynard, why didn’t he realise he had 20k shares? Nice bump in the share price for once in a while

David

David, I don’t know why he had missed owning some shares. The statement also revealed another director had overstated his holding. I am not sure if any new rules about what counts as a director shareholding prompted the recalculations.

Maynard

Tasty (TAST)

Centuno menu price increases

It appears TAST’s single Centuno restaurant (centuno.co.uk) has increased some of its menu prices. The previous increase occurred only a month ago.

Maynard

Hi Maynard,

I don’t own Tasty, but watched in horror as the sp crashed.

I read with interest your analysis on the company, but was still uncomfortable in investing in a restaurant chain.

sp was 11p at the time and given that it’s now doubled in such a short space of time, do you think it’s still got further to go?

Hindsight is of course a wonderful thing, but I’ve bought into other fallers expecting them to rise, only to see them slump further; Capita, Luceco and Monetise the worst offenders.

Regards

NJC

Hello NJC

Thanks for the comment. I must admit I was not 100% comfortable buying more TAST all the way done, because there is always the doubt that the market knows something you don’t.

I did not expect the shares to rebound as quickly as they have. All the worries about the sector remain. The only thing that has changed has been the director buying, which to me at least indicates there is no rescue rights issue planned right now. The realisation the company may not be going bust, and the market cap, may have prompted the buying. Rising share prices can of course attract more buyers simply because of the rising share price.

I think the price at 24p has further to go longer term — assuming the estate is rationalised, earnings can recover, and maybe one day the expansion plans are resurrected.

I started buying TAST last year at 55p expecting them to rise. So you are not alone in watching fallers fall further. The trick is to buy into companies where you are confident the problems are solvable while the share price is expecting the very worst… and be able to hold your nerve while averaging down. Easier said than done of course, and not something I really enjoy.

Maynard

Question is why such volume buying over the last week?

Appreciate your thoughts Maynard

Regards

David

Hello David

I don’t know. I can only repeat the answer to the previous post, and the director buying etc. But I may have missed some positive sector news.

Maynard

Tasty (TAST)

Publication of 2017 annual report

Not much to see here, as everything important was published within the results RNS.

What the RNS did not cover, however, was the AGM arrangements. Here are the main details:

A 9am start is not great. Last year’s gig started at 9:30am. The year before was 10:30am.

More importantly, TAST wishes to lift the aggregate nominal value of the extra shares the group can issue. Last year the aggregate amount was £590k, this year it is £1,196k.

The nominal price of TAST shares is 10p, so £1,196k is equivalent of issuing 11,960k shares — or 20% of the current share count. I suppose this facility could come in handy — issuing 11,960k shares at, say, 25p would raise a useful £3m.

This ‘aggregate nominal value’ number has bobbed around a bit:

2006: £2,399k

2007: £1,883k

2008: £1,216k

2009: £2,599k

2010: £1,000k

2011: £1,000k

2012: £478k

2013: £525k

2014: £530k

2015: £530k

2016: £590k

2017: £1,196k

I suppose during TAST’s heyday of 2012-2015, the rising share price meant fewer shares were needed to be issued to raise decent sums for expansion.

Also, the variable nature of the ‘aggregate nominal value’ suggests the board actively considers this resolution, and does reduce it when necessary to perhaps appease the worry of further dilution.

The obvious question now is whether the board will at some point issue extra shares. The increase to £1,196k does nothing to dampen that suspicion.

Maynard

Tasty (TAST)

New set menu

Just been alerted to a new set menu:

“We’ve been busy over the past few months working on some brand new creations that we think you’ll love just as much as us.

Will it be our Pizza Fiorentina served with black olives, spinach, a free-range egg & Gran Moravia or satisfy that sweet tooth with one of our brand new ice cream cones – perfect for the warmer months.

You can get 2 courses for just £11.95 or 3 for just £14.95.*

Head over to the website for more information!”

I have headed over to the website and there are no details :-( The link takes me to here.

The same alert refers to the ‘Big Wood’:

£13 a pop. At least this burger is listed on the website’s Specials menu.