30 June 2017

By Maynard Paton

Happy Friday! I hope you continue to find my Blog useful… and that your portfolio is still performing well during 2017.

After experiencing a buoyant start to the year, I am pleased my investments have generally held on to their value during the last few months.

All in all, the recent news from my portfolio has not been too bad, with a few minor share-price gains helping my performance improve to 9.5% for the year so far.

Warning: This could be quite a dull update

If you like your investing blogs to be full of share-trading activity, then you might as well stop reading now…

…because this quarter has been the first since I started this Blog during which I have not bought or sold any shares.

One reason for the lack of activity is that a lot of my time of late has been absorbed by matters outside of investing.

I’ve just about managed to keep on top of my existing holdings, and simply not had the chance to study other companies and publish fresh watch-list reviews.

Furthermore, current market valuations — especially those applied to higher-quality companies or those exhibiting superior growth potential — do not seem conducive to much buying at present.

Plus, I am becoming quite comfortable with how my portfolio is evolving.

You see, some of my past share-trading has involved ditching ‘deep value’ dreadfuls, and currently my holdings almost all exhibit a rich mix of high insider ownership, appealing track records, attractive financials and respectable prospects.

As such, there really has to be a striking opportunity for me to trim down an existing position in order to purchase a new holding.

This is how my portfolio has changed since the start of the year

I publish quarterly updates to round-up what has happened within my portfolio, and this Blog post outlines my April/May/June activity (or in this case, lack of activity). You can read all of my previous round-ups here.

The table below shows how my portfolio has changed since the start of the year:

| Holding | Weighting 31 Dec 2016 (%) | Weighting 31 Mar 2017 (%) | Weighting 30 Jun 2017 (%) |

| Andrews Sykes | 3.4 | 3.3 | 4.2 |

| Bioventix | 5.3 | 6.6 | 6.9 |

| Castings | 6.7 | 7.1 | 6.7 |

| City of London Inv | 6.5 | 6.7 | 7.1 |

| Daejan | 7.1 | 7.0 | 6.6 |

| Electronic Data Proc | 2.8 | - | - |

| Getech | 3.8 | 3.4 | 2.9 |

| Mincon | 3.3 | 3.8 | 4.0 |

| Mountview Estates | 8.9 | 8.3 | 8.5 |

| Record | 5.7 | 6.9 | 6.4 |

| S & U | - | 4.3 | 4.1 |

| System1 | 2.6 | 3.5 | 3.6 |

| Tasty | 7.6 | 3.7 | 2.6 |

| FW Thorpe | 9.1 | 8.8 | 10.2 |

| Tristel | 8.0 | 9.9 | 8.9 |

| M Winkworth | 5.6 | 5.4 | 5.7 |

| World Careers Network | 4.4 | 4.1 | 4.1 |

| Cash | 9.2 | 7.2 | 7.5 |

| TOTAL | 100.0 | 100.0 | 100.0 |

The left-hand column is how I reported my portfolio at the end of 2016, the middle column shows the Q1 position while the right-hand column is how my portfolio stood at today’s close.

I have studied updates from eight holdings

As usual I have kept watch on all of my existing holdings — trying to seek out bargain buys just in case.

Here is a summary of the Q2 news:

* Decent figures from Andrews Sykes, Mountview Estates and System1.

* Acceptable progress at Castings, Record and S & U.

* Unremarkable or mixed news from Getech and World Career Networks.

* Nothing from Bioventix, City of London Investment, Daejan, FW Thorpe, M Winkworth, Mincon, Tasty and Tristel.

The only other Q2 development I can add is my attendance at Tasty’s AGM.

Meanwhile, I plan to attend Tristel’s Open Day on 19th July.

A study of management loyalty and commitment

With no trading or watch-list activity during the quarter, I have decided to use this update to evaluate my holdings on a particular investing theme.

I have always found these types of evaluations to be quite helpful, as they can underline to me the most — and least! — appealing companies within my portfolio.

For this study I have chosen to look at company management. As I have stated in How I Invest (my bold):

“I want my investments to be led by loyal and capable bosses that have served in the top job for several years. I want to see improvements to profits and the dividend throughout their leadership. Better still is the founder/entrepreneur boss, who set up the firm in the first place, has led it ever since and has therefore shown even more commitment to building the business.”

For this study I will be concentrating on loyalty and commitment (through a sizeable ordinary shareholding). I will endeavour to look at management capability and track records in a future Blog post.

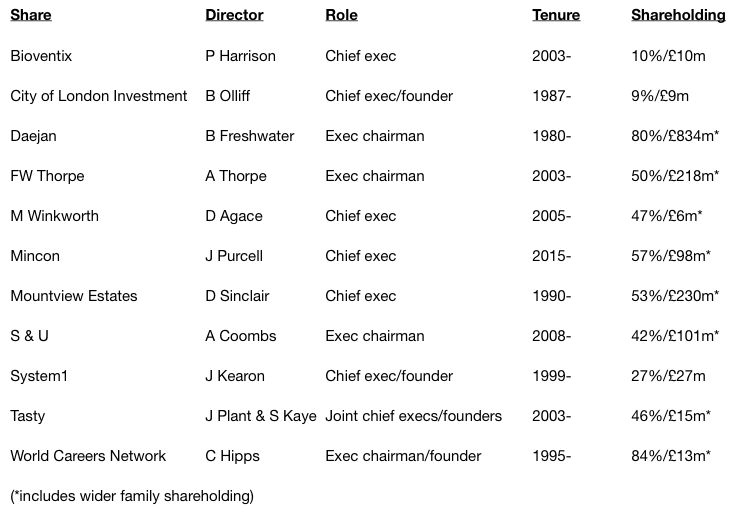

I feel these eleven shares are textbook holdings

I’ve ranked my 16 holdings into three groups. Here is group A:

These are the companies where the lead executive has generally been in charge for a long time and has a substantial amount of money riding on the share price.

You may have spotted that Mincon chief exec Joseph Purcell has the shortest tenure as a boss at just two years.

However, he did serve as chief technical officer from 1998 while his father (currently a Mincon non-exec) was in charge between 1977 and 2012. As such, Mr Purcell ought to have a good understanding of how to run the business.

Otherwise, I would say those eleven shares appear to be textbook holdings for me — at least on a management loyalty and commitment basis.

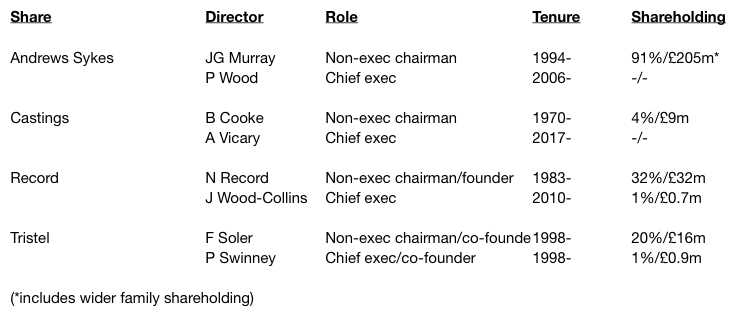

Part of my portfolio relies on these ‘salarymen’ executives

Now to group B:

These are the four holdings where the chief exec does not offer a long tenure or a significant shareholding (or both).

However, what (I hope) saves the day is the presence of a non-exec chairman that boasts either:

i) a long executive history (e.g. Castings), or;

ii) a significant shareholding (e.g. Andrews Sykes and Tristel), or;

iii) both a long executive history and significant shareholding (e.g. Record).

I would like to think these chairmen would look to protect their investments (and mine) by appointing a fresh chief exec should the need ever arise. So far at least, none of these ‘salarymen’ chief execs has let me down too badly.

Finally there is group C… consisting of just Getech:

There is no getting away from this… various board changes have left a new chief exec — who owns no shares — running the show.

There’s not even a major shareholder on the board, either. Getech’s founder still holds 10% but he left the company a few years ago.

Traditional business ‘moats’ versus motivated executive leaders

Years ago I used to believe that traditional business ‘moats’ — such as brands, patents, regulations, economies of scale, network effects, and so on — were the most critical feature of any investment .

But these days, such ‘barriers to entry’ appear increasingly at risk of being challenged by intrepid startups that can use the Internet to gain customers much more quickly than ever before. This investment paper cites a good example of Gillette and Dollar Shave Club.

Over time then, I have become far more convinced about the importance of management to an investment.

Put simply, I’d like to think a business is more likely to enjoy long-term success — and fend off intrepid startups — with a loyal and committed executive at the helm.

(Indeed, a company’s positive and adaptive working culture — instigated by a loyal and committed boss — can in itself be a difficult-to-replicate ‘moat’.)

On the other hand, I am no longer so sure about professional ‘salarymen’ executives, who may be quite happy to run things in a customary way and risk becoming complacent when it comes to fresh competition.

These bosses offered the tenure, but not the talent

Of course, investing in a business that’s led by a long-time executive with a major shareholding is no guarantee of stock-market success.

Looking through my past investments, I recall Electronic Data Processing, French Connection, Instore and London Capital all offered ‘owner-orientated’ directors…

…but that did not prevent those shares losing me money or struggling for years to deliver a gain.

What counts is backing loyal, committed — and capable — bosses. I sadly discovered the leaders at Electronic Data Processing, French Connection, and so on, were not that capable…

As I say, I will endeavour to look at management capability and track records in a future Blog post.

Until next time, I wish you happy and profitable investing!

Maynard Paton

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, Castings, City of London Investment, Daejan, Getech, Mincon, Mountview Estates, Record, S&U, System1, Tasty, FW Thorpe, Tristel, M Winkworth and World Careers Network.

Hi Maynard,

You really had great post! This serves an inspiration as we can learn from it. Your strategies and the portfolios that you have can provide us somehow an idea on what to do with our investments.

Your posts reads like all the comment spam I receive. I assume it is genuine as it mentions my name :-)

Sorry if that’s what you think. :) I sincerely appreciate this post as I’m currently having queries as a newbie for investing and at the same time reading successful investing stories for insights and I was lucky that your blog was listed as well. Thanks!

Ok, sorry about that. I am glad you find my Blog useful.

Maynard

Maynard,

Great update, an interesting view on Management / ownership

As always thanks for sharing

David

Thanks Maynard, a v interesting analysis

Maynard,

Your article prompted me to run a similar exercise on my own portfolio. I didn’t realise how on board I was with the motivated founder/owner theory. Over half of my holdings meet the criteria.

The levels of ignorance towards company management among investors is mindboggling. You wouldn’t employ someone to run a business in real life without vetting them thoroughly first. If you’re buying a chunk of a company for the long-term a similar set of standards should be applied where possible.

Hopefully you’ve helped a few people learn that today!

I also just stumbled across your Tasty AGM notes and was glad to hear the management team offered to meet with you. I’d love to get a more detailed breakdown of the problems facing the company and a phone call would probably be the best way to do that. Asking the crowd for menu choices is a little disconcerting — I hope this was very tongue in cheek!

Best,

Zach Coffell

Hello Zach,

I think management is overlooked by many investors because it is hard to evaluate in a mathematical way. But the people in charge can make all of the difference, and a lot of the ‘moats’ we see today were in fact dug out by individuals some time ago. I guess the task for us is to identify the ‘moat-diggers’ well before the moat is so wide it becomes obvious to everyone.

Maynard