23 June 2017

By Maynard Paton

Quick update on Record (REC).

Event: Final results and shareholder presentation for the twelve months to 31 March 2017 published 16 June 2017, and proposed tender offer.

Summary: There was a certain irony about these figures. REC makes its money by managing currency movements for clients… yet the group itself has prospered of late largely because the weaker GBP has translated into greater management fees. Whether REC’s clients have actually prospered is harder to say, as there still seems little evidence of a growing customer base. Still, I welcome REC’s decision to hand excess cash back via larger dividends, but the accompanying £10m tender offer does appear as if it was devised primarily to help REC’s founder plan for his retirement. With operating costs expected to rise, too, I reckon the tender price equates to an underlying P/E of 14-15. I continue to hold.

Price: 45p

Shares in issue: 221,380,800

Market capitalisation: £99m

Click here for all my previous REC posts

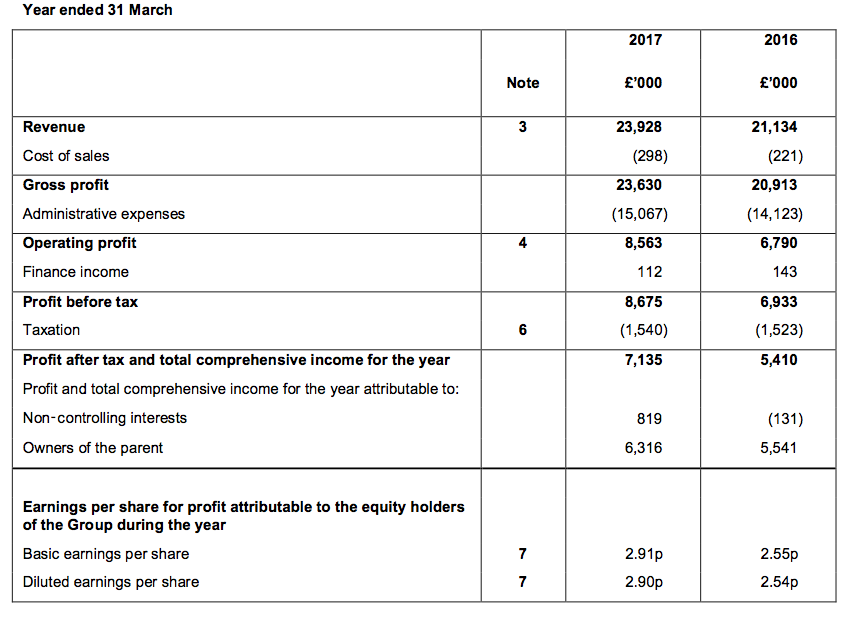

Results:

My thoughts:

* The best full-year effort since 2011, with growth due mostly to the weaker GBP

REC’s half-year statement and the firm’s subsequent quarterly updates (Q3 and Q4) had already indicated these results would not be too surprising.

My guess at the interim stage was that earnings for the second half could run at 1.56p per share (3.11p per share annualised), and in the event H2 earnings came in at 1.58p to give full-year earnings of 2.91p per share.

For the year as a whole, total revenue improved 13% while operating profit gained 26%. Excluding third-party investment gains, the underlying picture showed revenue up 7% to £22.7m and operating profit up 12% to £7.7m.

The 2017 numbers were the best since 2011, when revenue was £28m and operating profit was £12m:

| Year to 31 March | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 18,552 | 19,922 | 21,057 | 21,134 | 23,928 |

| Operating profit (£k) | 5,920 | 6,424 | 7,536 | 6,790 | 8,563 |

| Finance income (£k) | 158 | 113 | 146 | 143 | 112 |

| Other items (£k) | - | - | - | - | - |

| Pre-tax profit (£k) | 6,078 | 6,537 | 7,682 | 6,933 | 8,675 |

| Earnings per share (p) | 1.98 | 2.48 | 2.66 | 2.55 | 2.91 |

| Dividend per share (p) | 1.50 | 1.50 | 1.65 | 1.65 | 2.00 |

| Special dividend per share (p) | - | - | - | - | 0.91 |

REC was keen to imply that extra client money — assets under management equivalent (AUMe) gained 8% to $58.2bn — had supported the progress:

| Year to 31 March | 2013 | 2014 | 2015 | 2016 | 2017 |

| Year-start AUMe ($bn) | 30.9 | 34.8 | 51.9 | 55.4 | 53.7 |

| Net client inflow ($bn) | 1.9 | 14.1 | 2.9 | (2.3) | 3.2 |

| Market movement ($bn) | 3.2 | 0.4 | 5.6 | 0.4 | 5.4 |

| Currency translation ($bn) | (1.2) | 2.6 | (5.0) | 0.2 | (3.3) |

| Reclassification adjustment ($bn) | - | - | - | - | (0.8) |

| Year-end AUMe ($bn) | 34.8 | 51.9 | 55.4 | 53.7 | 58.2 |

However, the results small-print did admit that the revenue and profit advances were… (my bold):

“…principally due to the impact of sterling weakness on the conversion of the 82% of management fees that are denominated in currencies other than sterling.”

Indeed, it was difficult to pinpoint within the results RNS exactly why REC had attracted greater AUMe during the year. This is the best explanation I could find:

“Constant innovation is key to meeting the needs of our clients in a challenging environment. One of the Group’s key strengths is its flexibility which is demonstrated in its capability to adapt products, processes or distribution methods, and to tailor its approach to suit individual client requirements.

This innovation can be seen in each of our established products, where our strategy has been continually to enhance the value proposition offered to clients in order to resist competitive pressures on revenue margins. This is particularly true in the case of Passive Hedging, which can be mis-characterised by others as a commodity service, but which instead offers growing opportunities to save costs and add value for clients.

Both Dynamic Hedging and Multi-Strategy have also benefited from enhancements to their investment process, and combinations of these products are increasingly tailored to specific clients’ needs.”

Labouring through REC’s long-winded narrative about uncertain political and economic events, I was disappointed to discover such matters apparently provide only “opportunities to engage with clients”.

The sad reality is that REC has for some years now talked of “opportunities to engage with clients”… but such opportunities have yet to push the group decisively forward with much greater revenue and profit.

The fact that overall customer numbers improved by just one to 59 during the year suggests new clients remain as elusive as ever.

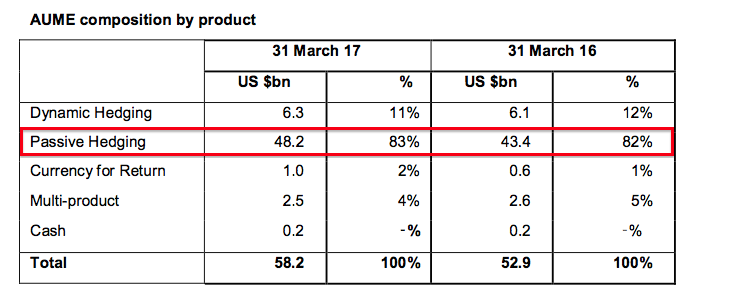

* Passive Hedging remains REC’s largest source of income

REC’s AUMe progress was due mainly to attracting additional — but low-margin — Passive Hedging money:

The Passive Hedging product therefore extended its position as the group’s largest source of fees:

| Year to 31 March | 2013 | 2014 | 2015 | 2016* | 2017 |

| Dynamic Hedging fees (£k) | 11,834 | 11,872 | 9,376 | 5,514 | 5,542 |

| Passive Hedging fees (£k) | 4,093 | 5,728 | 8,105 | 9,438 | 12,130 |

| Currency for Return fees (£k) | 2,134 | 2,671 | 2,774 | 790 | 1,025 |

| Multi-product (£k) | - | - | - | 5,199 | 4,021 |

| Total management fees (£k) | 18,061 | 20,271 | 20,255 | 20,941 | 22,718 |

| Performance fees (£k) | - | - | 480 | 315 | - |

| Other (£k) | 491 | (349) | 322 | (122) | 1,210 |

| Revenue (£k) | 18,552 | 19,922 | 21,057 | 21,134 | 23,928 |

(*certain fees for Dynamic Hedging and Currency for Return were re-categorised as Multi-product)

REC described Passive Hedging income as “stable”, which is no doubt because large Swiss pension funds are required by regulation to use such hedging.

For 2016, some 32% of revenue was derived from such Swiss clients and I dare say a similar proportion was received during 2017.

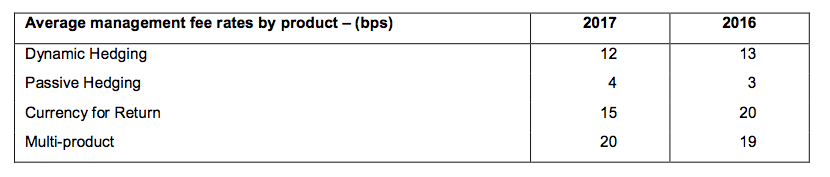

REC published the following full-year fee rates for each service:

When I studied November’s interims, my own fee-rate sums differed to those REC presented and I have therefore produced my own calculations again.

I have focused on REC’s second half, and taken the average AUMe for each product category plus the average £1:$1.24 exchange rate seen during the six months:

| 6 months to 31 March 2017 | Average AUMe ($m) | Management fee (£k) | Fee Rate (bps) |

| Currency for Return | 950 | 556 | 14.5 |

| Dynamic Hedging | 6,000 | 2,946 | 12.2 |

| Passive Hedging | 46,900 | 6,517 | 3.4 |

| Multi-product | 2,550 | 2,114 | 20.6 |

| Cash and other | 200 | 0 | 0.0 |

| TOTAL | 56,600 | 12,133 | - |

The differences may look small compared to REC’s own figures, but they can carry a sizeable impact on REC’s possible earnings.

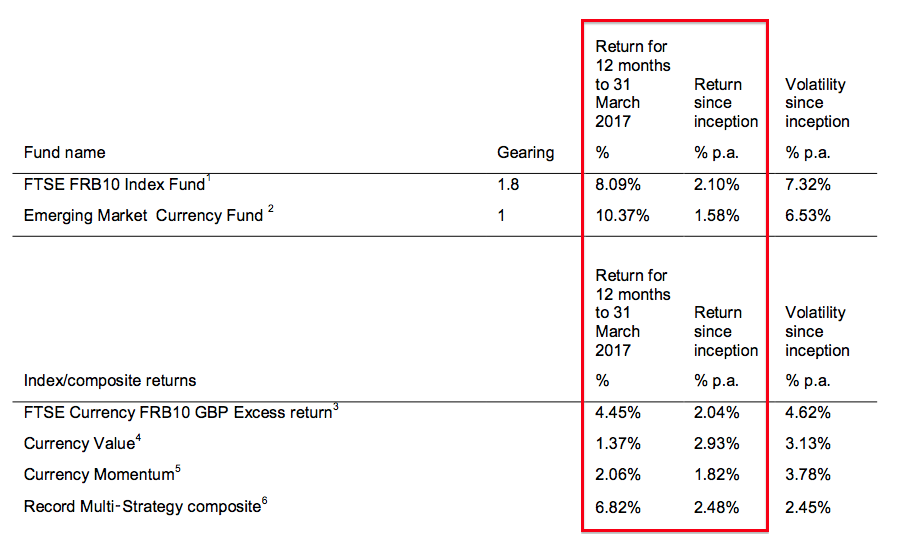

* All strategies still showing positive returns

I was pleased REC’s main profit-seeking strategies could all report positive performances for the full year — something last seen during 2013:

What’s more, all the strategies are showing positive returns since inception. So clearly something has been going well — which makes the standstill client numbers all the more disappointing.

Perhaps this line from management provides an explanation:

“Since the rationale for combining these four [profit-seeking strategies] is that we expect diversification between them, positive performances from all four should be seen as the exception rather than the norm”

Oh dear. It appears as if 2017 was a freakishly good year for currency returns.

I am now left wondering what exactly needs to happen for REC to attract new clients — at least on a ‘past performance’ returns perspective.

* Regulation threat appears to have diminished

One positive from the management narrative concerned new regulation.

You may recall November’s half-year statement had declared the following:

“Regulatory change continues to be a major theme in the foreign exchange markets. This half year saw the first implementation of mandatory variation margin rules amongst bank counterparties, with the effects on our clients expected to be felt from the first calendar quarter in 2017.”

However, last week’s results provided a more reassuring update (my bold):

“Some of our clients were affected from 1 March 2017; many more clients will be affected from January 2018.

As of the date of this report, the market-wide impact of such changes has been muted, with no evident differences in pricing between those market participants that have to exchange margin and those that do not.”

At least that is something less to worry about (for now).

* No complaints about the accounts

While I do like to whinge about REC’s lack of progress with its client base, you won’t find me complaining too much about the group’s financials.

In particular, cash conversion is generally superb.

Fitting out a new office caused tangible asset expenditure to spike last year, but for most years such expenditure is minimal. Meanwhile, relatively modest sums of cash are absorbed into working capital:

| Year to 31 March | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit (£k) | 5,920 | 6,424 | 7,536 | 6,790 | 8,563 |

| Depreciation and amortisation (£k) | 283 | 308 | 315 | 321 | 342 |

| Cash capital expenditure (£k) | (83) | (25) | (128) | (68) | (1,088) |

| Working-capital movement (£k) | (312) | (39) | (429) | (10) | (627) |

| Net cash and investments* (£k) | 25,379 | 26,078 | 28,801 | 30,721 | 32,443 |

(*excludes third-party investments)

The cash generation has allowed a substantial £17m to be distributed as dividends since 2013, while also adding a further £12m to the cash pile.

Total year-end cash was reported at £37.2m, and that sum included regulatory capital of £8.9m and third-party money of £4.8m. The £23.5m balance is equivalent to almost 11p per share.

(REC’s tender offer (see below) has shed further light on what the business deems to be ‘surplus’ cash.)

Other positive ratios include the operating margin and return on average equity. Excluding investment gains, I calculate REC converts a hefty 30%-plus of revenue into profit. The firm also produces appealing levels of earnings from its small equity base.

| Year to 31 March | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating margin (%) | 30.4 | 33.4 | 33.2 | 31.5 | 32.4 |

| Return on average equity* (%) | 35.1 | 45.4 | 48.6 | 47.4 | 51.0 |

(*adjusted for cash, regulatory capital and third-party investments)

I should add that REC operates without any debt and does not have any defined-benefit pension obligations.

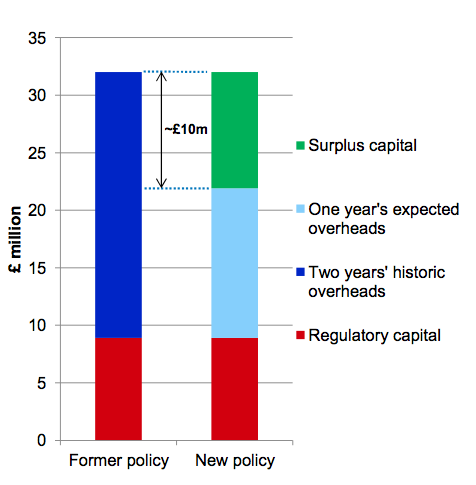

* Ordinary dividend up 21%, a special dividend and a £10m tender offer

The major development from last week’s RNS was REC’s decision to become a little more relaxed with its cash hoard.

The executives now reckon the business can cope with having just one year’s worth of overheads in reserve instead of two:

Squinting at the chart above, it appears one year’s expected overheads now come to £13m. Given REC said overheads for 2017 were £11.7m, I am disappointed additional costs still seem to be creeping into the business.

Anyway, I was pleased the group said it would pay out all of its 2017 earnings as dividends — by lifting the full-year payout by 21% to 2p per share and distributing the 0.91p per share balance as a special payment.

What’s more, REC also admitted it was contemplating a potential £10m return of capital back to shareholders.

The £10m capital return was confirmed this week through a separate announcement of a formal tender offer. REC will acquire about 10% of its share count at around 45p per share.

REC started hinting at a special dividend this time last year, so I am glad such a payment is finally on its way.

However, I am not so sure about the tender offer. Potential drawbacks to these types of ‘shareholder returns’ include:

i) The price at which the shares are purchased may not deliver great value;

ii) Directors can use them as an easy way to cash in their own shares, and;

iii) Earnings per share can be enhanced and help trigger associated board bonuses.

True, some shareholders may prefer the taxation consequences of a tender offer. However, at least with a special dividend every shareholder has the choice with what to do with the handout.

Looking at those drawbacks with respect to this tender offer:

i) The effective 45p purchase price does not seem outrageously extravagant, although it does not reflect an obvious bargain either (see my Valuation notes below).

ii) REC’s founder and non-exec chairman, Neil Record, has committed to sell between 7 million and 15 million of his own shares.

With REC able to purchase a maximum of 22 million shares through this tender offer, Mr Record appears very keen for shareholders’ money to be spent acquiring part of his shareholding.

Mr Record turns 64 on Sunday and I dare say this tender offer is part of his retirement planning. I just wonder if he could have raised even more money by selling the whole business instead.

Mr Record’s holding will reduce from 32% to 27% of the company if he is able to sell the full 15 million shares. He will retain at least 56 million shares after the offer.

iii) The tender-offer documentation confirmed there should be no option shenanigans:

“The Tender Offer will not affect the satisfaction or otherwise of the earnings per share related performance conditions to which all share options awarded to the Company’s executive Directors under the Record plc Share Scheme are subject, since the terms of such options provide for earnings per share to be adjusted to take account of any capital reorganisation.”

One final thought on the larger dividends and tender offer — I do wonder if releasing so much cash signals REC has given up on any significant expansion hopes.

Valuation

Using my own fee-rate calculations and the AUMe numbers from the Q4 update, I reckon potential management fees could now be running at £23.7m with £1 buying $1.27:

| Year to 31 March 2018 (est) | AUMe ($m) | Fee Rate (bps) | Management fee (£k) |

| Currency for Return | 1,000 | 14.5 | 1,143 |

| Dynamic Hedging | 6,000 | 12.2 | 5,755 |

| Passive Hedging | 47,000 | 3.4 | 12,758 |

| Multi-product | 2,500 | 20.6 | 4,049 |

| Cash and other | 200 | 0.0 | 0 |

| TOTAL | 23,706 |

Applying the £13m expected overhead and then the group’s 30% profit share gives a £7.5m pre-tax profit:

| Year to 31 March 2018 (est) | |

| Management fees (£k) | 23,706 |

| Less expected overhead (£k) | (13,000) |

| Less 30% profit share (£k) | (3,212) |

| Operating and pre-tax profit (£k) | 7,494 |

After standard 19% tax, my new sums suggest earnings could be £6.1m or 2.74p per share.

(Had I used REC’s own fee-rate figures, my sums would have shown management fees of £25.5m and earnings at 3.20p per share.)

REC’s market cap at the 45p tender-offer price is £99m, which adjusting for the £10m earmarked for the offer gives an enterprise value (EV) of £89m or 40p per share.

Dividing that 40p per share by my 2.74p per share earnings guess gives an underlying P/E of 14-15.

While that rating is not outrageously extravagant for the tender offer, it does not strike me as an obvious bargain either.

If you assume REC could have used £23.5m for the tender offer — to leave only the £8.9m regulatory-capital cash and the £4.8m third-party investments on the balance sheet — then the P/E drops to 12-13.

Meanwhile, REC’s lifted 2p per share ordinary dividend supports a 4.4% income.

Maynard Paton

Disclosure: Maynard owns shares in Record.

Record (REC)

Annual results notes:

Credit to REC for publishing a full set of accounting notes within its results RNS. The forthcoming full annual report should include further information on director pay etc.

Here are a few points of interest from the account notes:

1) Expenses

My Blog post above noted that REC expects its overheads to increase from £11.7m to about £13m. The following note reveals some of the costs (and gains) for 2017:

Looking at the last four entries, which all seem to be non-trading items, they total a gain of £976k for 2017 versus a loss of £195k for 2016. So it appears the reported 2017 profit and overhead were flattered somewhat.

A new office move increased lease costs by about £300k:

All told, I am not sure what has prompted the extra overheads for 2018 and beyond. I guess they may come from activities such as this:

Nice shorts!

2) Employee ratios

I see REC employed four more people for 2017:

Nice to see two of the newcomers were employed in Client Relationships, which I assume involves looking for new clients.

The average cost of each employee was £143k and each employee produced an average £311k management fee. Those ratios are the highest since 2011. Staff costs as a proportion of management fees was 45.9% for 2017, which was a touch below the 46.3% for 2016, but above the 44.0% for 2015 and 2014. I would like to think this ratio will not advance much further.

3) Large clients

REC remains dependent on a few major clients:

Some 52% of 2017 revenue was received from the group’s five largest customers. At least this ratio is less than the 60.1% seen for 2016 and 57.9% seen for 2015.

4) Share options

REC is not afraid of granting options to staff:

The option count now stands at 13.7 million, of which 3.6 million could be satisfied by shares held in an employee benefit trust. The other 10.1 million represent 4.5% of the current 221.4 million share count.

Something to consider with these options is their potential effect following the tender offer.

The tender offer could purchase up to 22.3 million shares, which would leave 199.1 million shares in issue. So the dilution effect post-tender would increase to 5.1%. I guess that percentage remains acceptable.

5) Trade receivables

Nothing too much to worry about here:

Certainly REC’s clients pay on time given the small (£147k) sum past due. Total trade receivables equate to 26.1% of management fees, which seems right to me given the business invoices on a quarterly cycle. Past years have seen this ratio as low as 19%, but I suspect the fluctuations could be due to currency conversions on the balance sheet date. REC’s working-capital cash generation is very sound anyway.

6) Regulatory capital

I have seen other bloggers write about REC and suggest all the group’s cash is surplus to requirements. They ignore the group’s regulatory capital, without which the business could not operate.

So here is the relevant note:

7) Product reclassification

This is a bit weird. REC reclassified its product range back in November and I commented then that $0.8bn of client AUMe had effectively vanished last year.

These annual results now suggest $1.5bn of AUMe has vanished due to the reclassification:

I don’t understand how total client money can differ depending on the product classification. Maybe there has been some double counting here, or as I speculated in November, perhaps some of the ‘old’ AUMe was not incurring any fees from REC.

Whatever, it is all a bit odd and does not do REC any favours when it talks about AUMe ‘growth’.

Maynard

Record (REC)

Reader question

Someone has contacted me with the following request:

“I wonder if you could do a small note of whether the buyback is a good use of shareholder funds (compared to a dividend). I don’t really grasp the intricacies of this. A special dividend would help the founder to retire comfortably too. I don’t see why taking up the tender is really good for a small-holder. Am I missing something? (as is usual).”

It is not obvious to me that the tender offer is a very good use of shareholder money. My sums in the Blog post above suggest REC is buying back the shares at a P/E multiple of between 14 and 15.

Looking back, there was an opportunity for REC to buy back shares this time last year when the company first mooted returning cash to shareholders. Back then the price was about 25p, the post-Brexit effect on GBP had started and the firm could have projected the associated EPS benefit. The purchase multiple could have been 10 or less at the time and a buy back then could have done real wonders for EPS and the share price..

Essentially dithering for a year and waiting for the price to climb to 45p suggests to me this offer is more about Mr Record’s retirement planning than anything else. True, REC could declare a special dividend — but a tender offer gives Mr Record the additional flexibility of raising more cash by selling more than his basic entitlement. He could sell 20% of his holding through this offer if enough other shareholders don’t tender their shares.

As far as I can tell, the only reason for ordinary shareholders to take up the offer is because they feel the price is generous and they want out. For what it is worth, I have voted against the tender-offer resolution.

If the tender offer purchases the maximum number of shares, I reckon my £7.5m operating profit guess from the Blog post above would translate into EPS of 3.05p. Assuming the £13m remaining cash is not surplus to requirements, then the 45p share price would be valued at 14.8x. If the £13m remaining cash is viewed as surplus to requirements, then the multiple drops to 12.5x.

Maynard

Record (REC)

Publication of 2017 annual report

Not too much to go through here as the main points were all revealed within the final results RNS.

1) Business risks

REC has admitted it faces increased risks in three areas:

a) Regulatory intervention:

At least the results text did say the new ‘variation margin’ rules had not seen any early effect just yet.

b) Market liquidity:

Liquidity in ‘stressed market environments’ has apparently become ‘less reliable’.

c) Economic:

Brexit may cause issues with REC and clients being subject to EU rules.

2) Swiss clients

34% of revenue is derived from Swiss funds that are forced to use a hedging service:

That revenue would appear quite reliable, until the associated rules are ever relaxed of course.

3) Director pay

The directors were awarded 3% pay rises during the year and REC’s profit-share arrangements continue to provide significant annual bonuses:

These are chunky payments for a business that has just delivered an £8m operating profit.

For some perspective, the board at TFW receives about half of what REC’s board collects, despite TFW producing twice the annual profit.

4) Staff pay, profit share and nil-cost options

I see that staff continue to extract more from this business. I moan about this issue because the staff do not appear that capable pushing earnings higher by garnering new clients and keeping existing ones. Progress during 2017 was almost all due to the weaker GBP.

I had an ironic snigger at this:

Let’s not forget that REC’s staff all enjoyed a 10% pay rise from May 2015, and that was due to staff pay apparently being below market levels. So pay remaining static after that was to be expected.

Again, I don’t mind staff receiving pay rises, but REC’s lack of client wins is hardly justification for more catch-up payments. It seems to me REC’s staff are below-industry-average performers anyway, so probably deserve below-industry-average pay as well.

These next snippets suggest the staff wish to extract more value from the ordinary shareholder.

Essentially REC’s main staff-option scheme will now be able to grant options at nil cost, rather than at market price. So a can’t-lose gift to the employee at the expense of us ordinary shareholders.

Note the reference to ‘shorter term’ — not a great example of remuneration-committee thinking.

Also, the profit-share scheme has been revised. The staff pool remains at 30% of pre-bonus profit, but all 30% is now paid in cash:

You see, it seems the staff prefer cash to shares:

Oh dear. That is not a great advert for the shares, from the very people who know most about the business.

Maynard

Record (REC)

Q1 Trading Update:

This update was the latest in a long line of quarterly statements that did not reveal any significant progress.

Total effective client assets under management (AUMe) advanced by $1.7bn to $59.9bn during the 3 months to 30 June 2017, and in sterling terms lost £0.5bn to £46.1bn.

The preceding Q4 update had said:

“During the quarter, six associated Passive Hedging clients representing $0.6 billion AUME terminated, and one client reduced its Multi-Product mandate by $0.9 billion. The impact of these AUME reductions was offset by a new Passive Hedging client (+$0.2 billion) and inflows of +$0.8 billion to existing hedging mandates. Record has been notified of the termination of a Passive Hedging mandate of $1.2 billion expected during the current quarter.”

This Q1 update stated:

“It’s pleasing to report continued growth in aggregate AUME in the quarter and to note the diversity of inflows from existing clients across both hedging and return-seeking products, sufficient to offset the previously announced termination of a $1.2 billion Passive Hedging mandate. During the quarter, a Dynamic Hedging client on a management plus performance fee basis notified its intention to switch to Passive Hedging, at fees consistent with Record’s standard management fee scales.”

So yet another mixed quarter, with client money both coming in and going out.

Among REC’s higher-margin strategies, Dynamic Hedging saw clients withdraw $1.1bn, although this movement was almost offset by Currency for Return and Multi-Product clients adding $0.9bn. Alongside other movements, the higher-margin strategies lost an overall $0.4bn to $9.4bn.

I also see a Dynamic Hedging client has “notified its intention to switch” to Passive Hedging, the effect of which no doubt will be seen during Q2. So that is further higher-margin business lost to lower-margin Passive Hedging. At least it is business that is not lost entirely.

This Q1 update gave the now familiar outlook of ‘engaging with clients’:

“We continue to engage with both existing and prospective clients as to their preferences in managing currency risk and opportunity, and in achieving their investment objectives. With our diversified product suite and our ability to tailor solutions to fit individual client objectives, we are confident that further progress can be made in the current financial year“.

Just when ‘engaging with clients’ will actually translate into decisively adding new client mandates remains anyone’s guess at present.

Anyway, I have adjusted my valuation sums for the revised AUMe and, assuming fee rates remain the same as those noted in the Blog post above, and using £1:$1.30, then:

* Currency for Return AUMe of $1.6bn gives fees of £1,787k;

* Dynamic Hedging AUMe of $5.0bn gives fees of £4,685k;

* Passive Hedging AUMe of $50.3bn gives fees of £13,339k;

* Multi-product AUMe of $2.8bn gives fees of £4,430k;

* Total fees = £24,242k

Less my guesses of £7,400k for staff costs and £5,600k for other costs as noted in the Blog post above, then less the 30% profit share (of £3,372k), I arrive at an operating profit of £7,869k. Taxed at 19% gives earnings of £6,374k or 3.20p per share (based on 199m shares in issue following the tender offer).

With the share price at 43p, my P/E comes to 13.4.

REC’s ‘surplus’ net cash position — i.e. cash excluding regulatory capital and third-party investments — is close to £14m or 7p per share following the tender offer. My P/E adjusted for this ‘surplus’ cash is 11.3.

At least my 3.20p per share guess covers last year’s 2p per share ordinary divined and should perhaps fund another special payout. A 2p per share payout offers a 4.65% income at 43p.

Maynard

Record (REC)

Q2 Trading Update:

This update extended the run of quarterly statements that did not reveal any significant progress.

Total effective client assets under management (AUMe) advanced by $1.3bn to $61.2bn during the 3 months to 30 September 2017, and in sterling terms lost £0.5bn to £45.6bn.

This Q2 update stated:

“For UK-based clients, Dynamic Hedging achieved cost-effective protection of currency gains from sterling’s depreciation in the six months following the EU referendum. However, persistent weakness in sterling meant negative returns and cash flows were unavoidable. As a result Record’s remaining UK-based Dynamic Hedging clients converted their mandates to Passive Hedging or terminated during the period.”

So another quarter where certain clients became fed up with one of REC’s higher-margin products.

All told, Dynamic Hedging saw clients withdraw $0.6bn and Passive Hedging saw clients withdraw $0.5bn. However, those movements were offset by stock-market and exchange-rate gains adding $2.2bn to AUMe.

This Q2 update gave the all-too-familiar outlook of ‘engaging with clients’:

“The theme of volatility in currency markets linked to political and economic uncertainty continues, and the consequent uncertainty provides opportunities for engagement with both existing and potential clients. We remain confident of making further progress in the second half of the financial year“.

Just when ‘engaging with clients’ will actually translate into decisively adding new client mandates remains anyone’s guess at present.

The Q2 statement introduced a particular niggle. Despite the standstill AUMe, costs are growing:

“We have continued to innovate and enhance our products to meet clients’ developing needs. This focus on service enhancement has contributed to growth in employee numbers and hence costs over the first half of the financial year.”

I can’t say I am surprised. This business is not shy when it comes to paying staff well for mediocre performances.

Anyway, I have adjusted my valuation sums for the revised AUMe and, assuming fee rates remain the same as those noted in the Blog post above, and using £1:$1.31, then:

* Currency for Return AUMe of $1.7bn gives fees of £1,994k;

* Dynamic Hedging AUMe of $4.5bn gives fees of £4,185k;

* Passive Hedging AUMe of $51.7bn gives fees of £13,606k;

* Multi-product AUMe of $3.0bn gives fees of £4,710k;

* Total fees = £24,385k

Less my guesses of £7,400k for staff costs and £5,600k for other costs as noted in the Blog post above, then less the 30% profit share (of £3,415k), I arrive at an operating profit of £7,969k. Taxed at 19% gives earnings of £6,455k or 3.24p per share (based on 199m shares in issue following the tender offer).

With the share price at 43p, my P/E comes to 13.3.

REC’s ‘surplus’ net cash position — i.e. cash excluding regulatory capital and third-party investments — is close to £14m or 7p per share following the tender offer. My P/E adjusted for this ‘surplus’ cash is 11.3.

At least my 3.24p per share guess covers last year’s 2p per share ordinary divined and should perhaps fund another special payout. A 2p per share payout offers a 4.65% income at 43p.

Maynard