27 July 2025

By Maynard Paton

FY 2024 results summary for M Winkworth (WINK):

- Sales transactions rebounding 17% involving property worth £3.4b helped ensure a positive FY, with franchise-network income up 12%, revenue up 17%, underlying profit up 24% and the dividend up 5%.

- Assisted by branch resales to “best-in-class” agents, the “vast majority” of London branches now boast WINK’s necessary top-three local position. The average commission income from all branches meanwhile reached a new £628k high.

- A potential “shrinkage in rentals” due to new legislation could create a greater dependency on sales transactions and differentiate WINK from resurgent rival Foxtons, which plans to strengthen its leading market share by spending £15m a year acquiring further lettings agencies.

- Despite minimal profits from company-owned offices, the FY margin was a respectable 21% following commendable control of employee — and director! — pay. Greater loans to franchisees meanwhile reduced net cash to £4m, equivalent to a sizeable 38% of FY revenue.

- Post-FY statements signalling FY 2025 profit advancing 10% and dividends up at least 7% support a 6%-plus yield and possible dividend cover of only 1.14x, all of which re-emphasises the board’s preference for income. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own WINK

- Results summary

- Franchise-network income, revenue, profit and dividend

- Franchisees: network competitive position

- Franchisees: branch openings, closures and resales

- Franchisees: network productivity

- Franchisees: sales and lettings income

- Winkworth versus Foxtons

- Company-owned offices

- Boardroom

- Financials: margin and employees

- Financials: cash flow and balance sheet

- Valuation

News links, share data and disclosure

- Annual results, presentation and webinar for the twelve months to 31 December 2024 published/hosted 16/23 April 2025;

- AGM attendance on 22 May 2025 (notes coming soon!);

- Q2 2025 dividend declaration and trading update published 16 July 2025, and;

- Conditional grant of share options published 17 July 2025.

- Share price: 208p

- Share count: 12,908,792

- Market capitalisation: £26.9m

- Disclosure: Maynard owns shares in M Winkworth. This blog post contains ShareScope affiliate links.

Why I own WINK

- Supports a London estate-agency franchising network, with progress buoyed by motivated franchisees winning business through tip-top service to underpin a highly reputable brand.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments and company-owned offices.

- Conservative family management boasts a £13m/47% shareholding, rewards investors through durable quarterly dividends and seems likely one day to consider an M&A exit.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Franchise-network income, revenue, profit and dividend

- This FY was always going to be positive after January’s Q4 2024 update signalled completed FY property sales had rallied 19% and franchise-network lettings income had gained 5-6%:

[Q4 2024] “Completed sales in FY 2024 rose by 19%, compared with the prior period, and the Board is pleased with the momentum going into FY 2025.

…

The renewed focus on sales was reflected in slower lettings activity. Lettings applicants in 2024 were 5% down on 2023 figures, but full year revenues are expected to have risen by 5-6% due to rental price increases.”

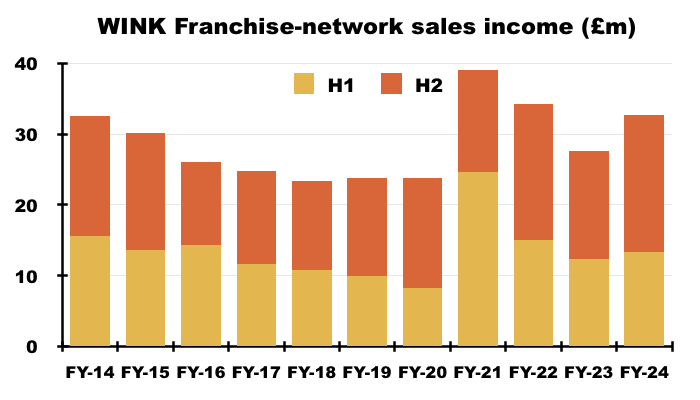

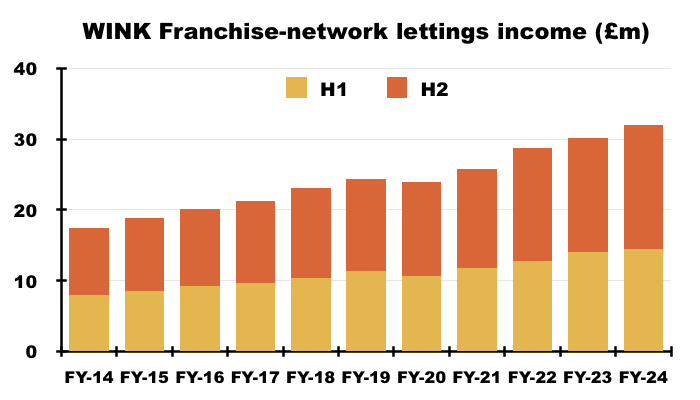

- In the event, FY franchise-network sales income gained 18% to £32.7m while franchise-network lettings income gained 6% to £32.0m:

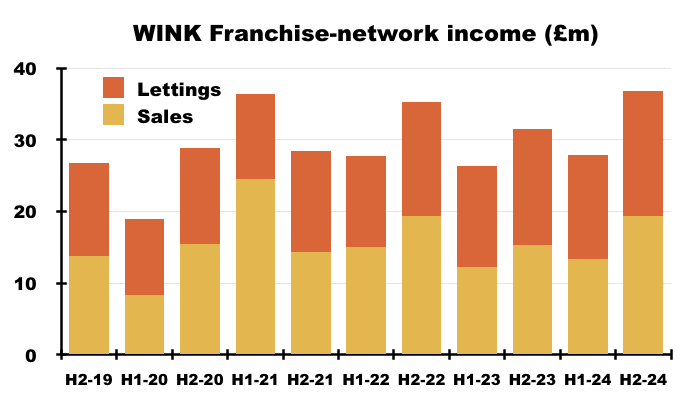

- Progress was much stronger during H2 than H1.

- After the preceding H1 reported network sales income up 9% and network lettings income up 4%, this FY delivered H2 network sales income up 26% to £19.3m and H2 network lettings income up 8% to £17.5m:

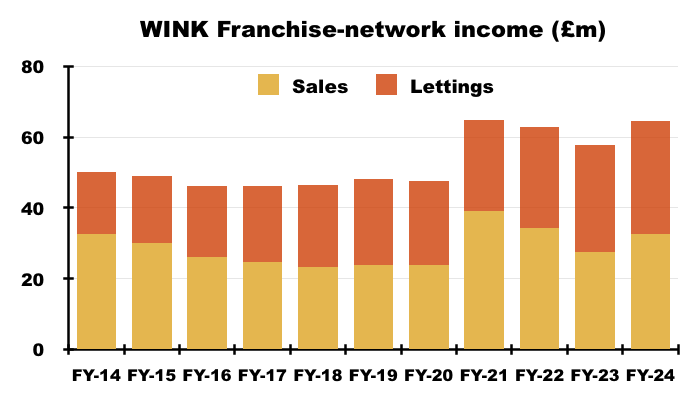

- Total FY network income gained 12% to £64.7m, and was only £0.1m less than the record FY network income set during FY 2021.

- Total H2 network income of £36.8m set a new record for any H1 or H2.

- Note that this FY’s network sales income of £32.7m was only £0.1m more than the level set during FY 2014:

- WINK’s franchisees continue to battle a standstill housing market, whereby UK residential property transactions have stabilised at c100k a month since 2014 (see Franchisees: sales and lettings income):

- At least this FY’s network lettings income set a new FY record, and was 82% greater than the level witnessed during FY 2014:

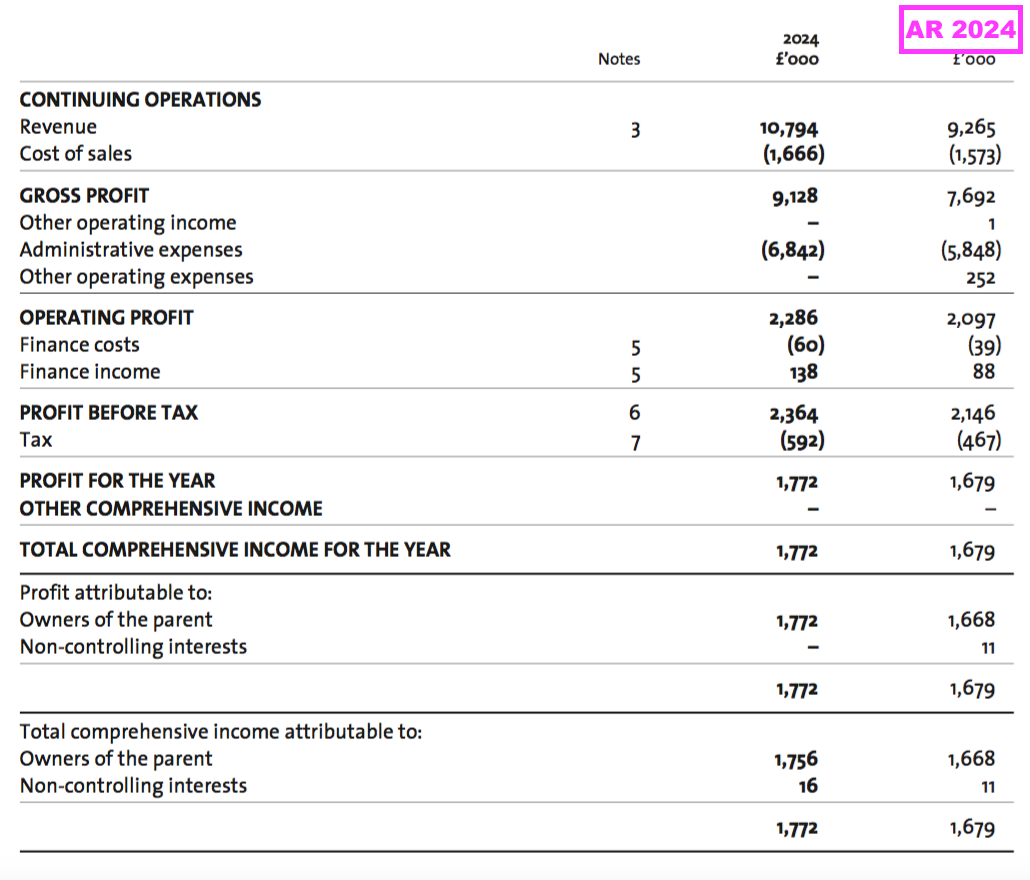

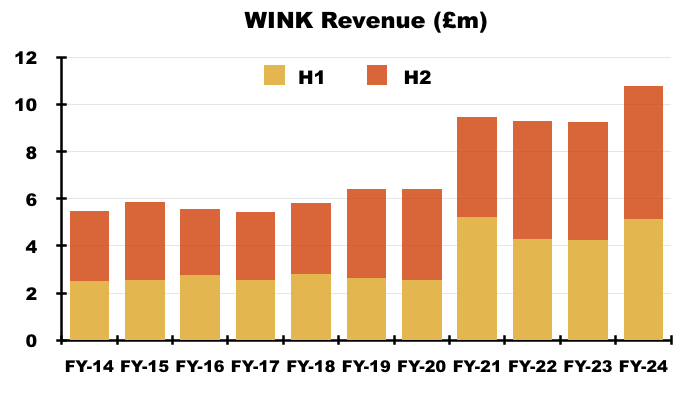

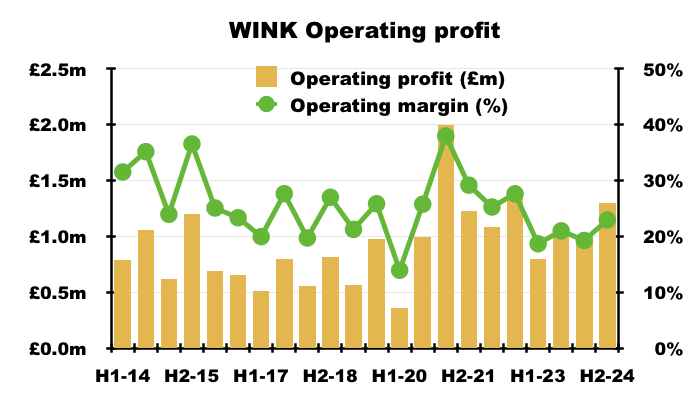

- The greater network income helped push FY revenue up 17% to a record £10.8m:

- H2 revenue climbed 13% to £5.7m and was the highest for any H1 or H2.

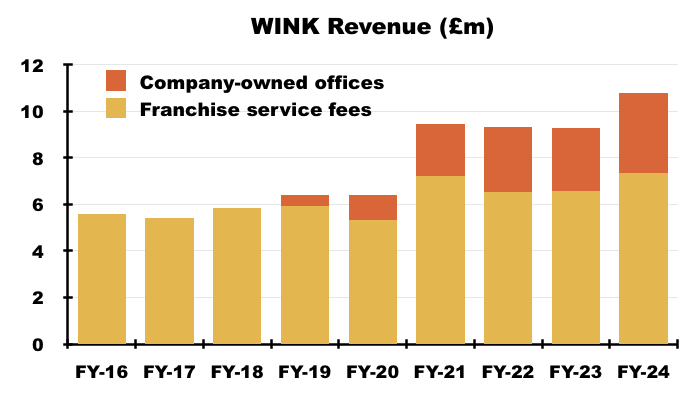

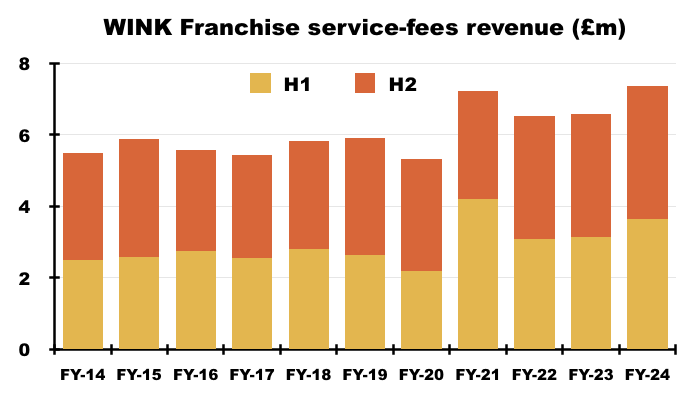

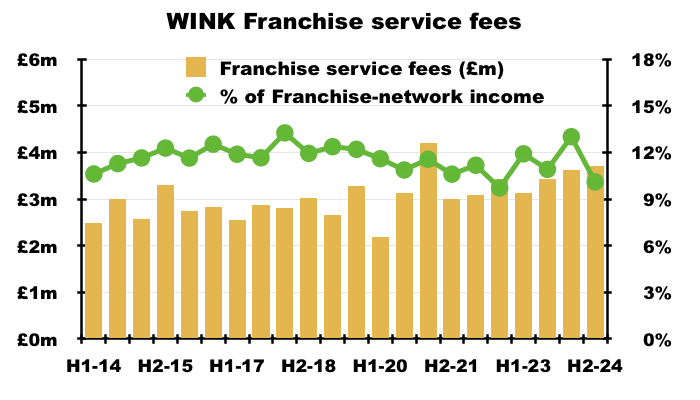

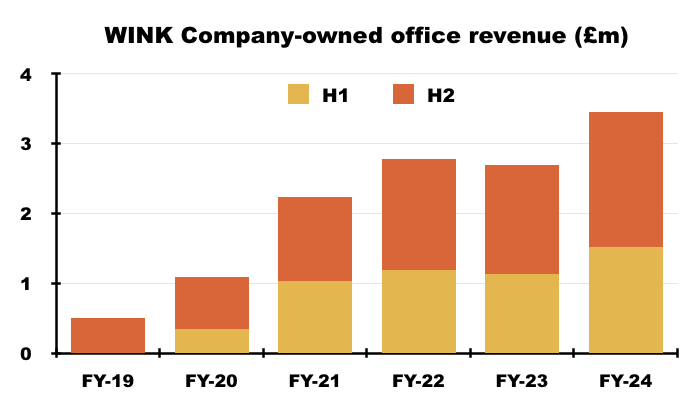

- FY revenue from franchise service fees gained 12% to a record £7.3m while FY revenue from company-owned offices advanced 28% to a record £3.4m:

- The 12% FY revenue increase from franchise fees matched the 12% advance to franchise-network income, indicating no change to the proportion of franchise-network income WINK keeps for itself (see Franchisees: network competitive position):

- The 28% advance to FY revenue from company-owned offices was supported in part by the first twelve-month contribution from the group’s Pimlico office (see Company-owned offices).

- January’s Q4 2024 update stated FY pre-tax profit would improve 9% and FY net cash would decline by as much as £0.65m:

[Q4 2024] “Winkworth’s full year pre-tax profits, subject to audit, are expected to be in line with current market expectations of £2.35m (31 December 2023: £2.15m) with net cash at year end to be at least £3.90m (31 December 2023: £4.55m).“

- This FY’s pre-tax profit was £10k better than projected at £2.36m, while FY net cash was indeed “at least £3.90m” at £4.09m.

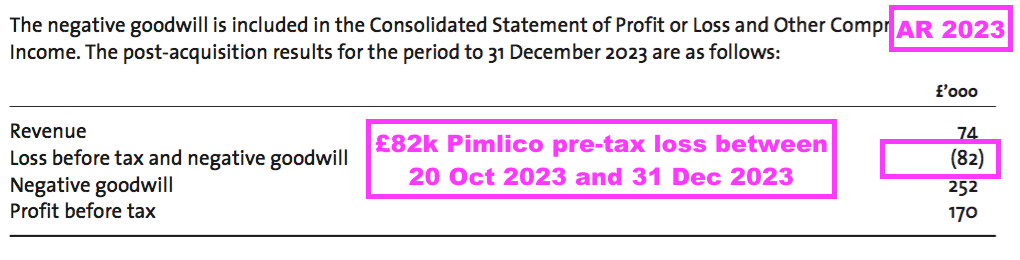

- Note that the comparable FY’s reported profit was bolstered by a £252k negative goodwill entry created by the Pimlico purchase (see Company-owned offices).

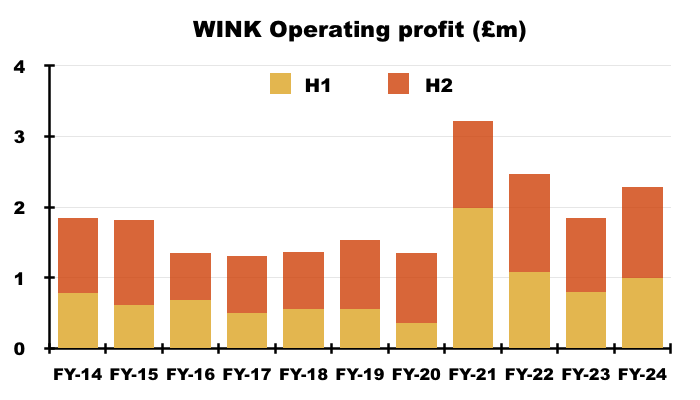

- Excluding this negative goodwill, FY operating profit increased 24% to £2.4m:

- H2 operating profit gained 24% to £1.3m, the group’s best-ever H2 profit save for H2 2022 (£1.4m).

- This FY’s reported profit was suppressed by minimal contributions from company-owned offices (see Company-owned offices).

- This FY’s profit was not complicated by any adjustments.

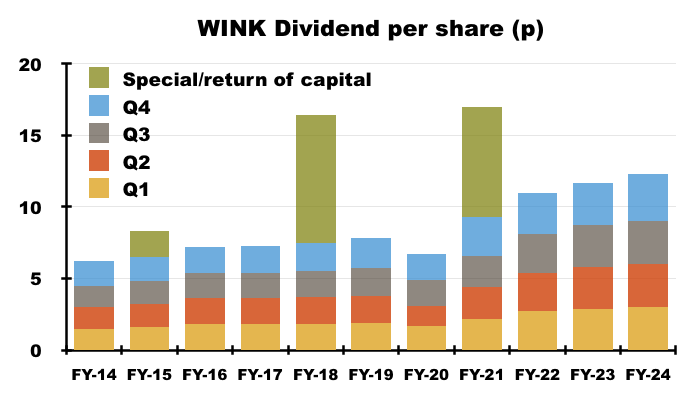

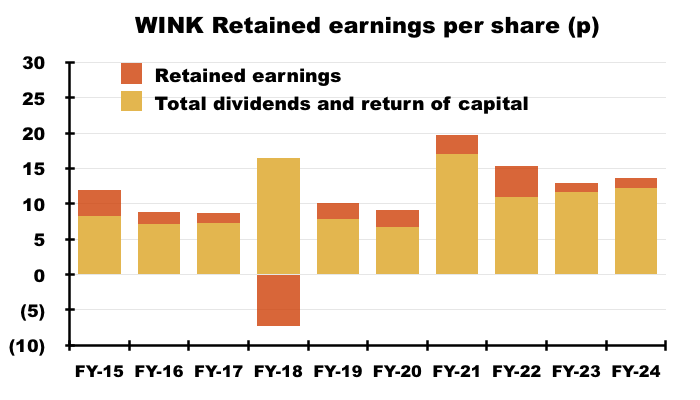

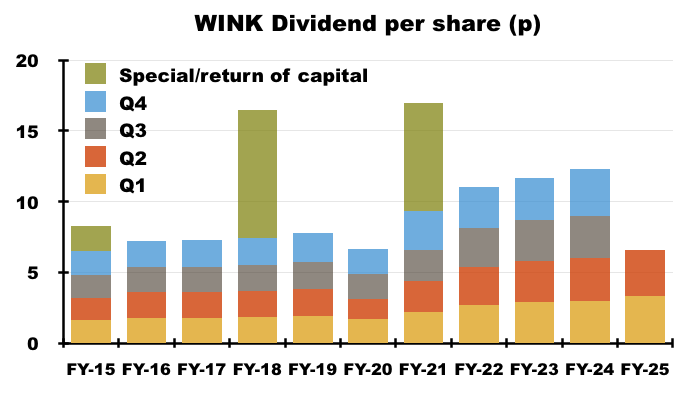

- October’s Q3 2024 update and January’s Q4 2024 update had already revealed quarterly dividends of 3.0p and 3.3p per share respectively, which helped improve the total FY payout by 5% to 12.3p per share:

- Reported FY earning were 13.73p per share, which limited dividend cover to a tight 1.12x.

- Board comments at the 2025 AGM signalled the low dividend cover was a deliberate decision supported by the group’s cash position:

[AGM 2025] “We are sitting on a lot of cash and have no debt. When we want to expand, we have the cash to expand. Why should we then take money from the dividend pool and put it to one side?

It’s embarrassing to have too much money.“

- Following this FY, WINK announced the following dividends to raise the H1 2025 payout by 10% to 6.6p per share:

- These post-FY dividends imply the FY 2025 payout could increase by at least 7% to at least 13.2p per share (see Valuation).

Franchisees: network competitive position

- WINK’s franchise network consists of 100 estate-agency branches located throughout London and affluent areas of southern England.

- Franchisees pay WINK a straight 8% of all of their sales and lettings income, plus variable sums towards IT, training, marketing, legal, compliance, landlord/tenant referrals and other services.

- While WINK’s basic 8% is fixed, the associated agent commissions from sales and lettings to which the 8% is applied can vary… meaning WINK is not entirely in control of the level of franchise service fees received.

- This FY disclosed property sold through the network amounted to £3.4b:

“These principles are evident in our achievements: £3.4 billion worth of property sold last year; 175,000 registered applicants; a database of over four million contacts; and more than four million visits to our website. Our 100 offices meet these varying needs, with Central London having fewer instructions per office than outer London or the country, and some areas in the UK have a low turnover as residents in those areas tend to stay for life.”

- I cannot recall WINK disclosing the aggregate annual value of property sold through its network before.

- Network sales income of £32.7m versus sold property worth £3.4b suggests the collective franchise network charged a sales commission of less than 1%.

- The FY webinar claimed the average commission was “well above 1%“:

“It’s quite a broad-brush calculation and the average is well above 1%. Winkworth will always be competitive in its local market but will never seek to be the cheapest in the marketplace as we believe we add value to our clients.“

- The FY webinar sadly did not explain how the commission rate was “well above 1%“.

- But perhaps the £3.4b includes properties sold through the group’s in-house Development and Commercial Investment (DCI) agency, which handles sales of new builds and commercial properties and which does not contribute to franchise-network income (see Company-owned offices).

- During this FY, £7.3m, or 11.4%, of the £64.7m earned by the franchisees was taken by WINK as service fees:

- The 11.4% proportion matched the level reported by the comparable FY and was assisted by a £350k “one-off large franchise-sale fee” disclosed during the preceding H1’s webinar:

[H1 2024] “The franchising business increased revenue by £500k. The increase in sales and lettings generated £125k of additional income for us and we had a one-off large franchise sale fee, which meant that revenue line was up by £350k on the previous half year“.

- Without the £350k one-off fee, the 11.4% proportion would have been 10.8% — towards the bottom of the 10.3% to 12.5% FY range witnessed since FY 2014.

- I presume WINK’s share of the network’s total income will always fluctuate from year to year, as different franchisees pay different amounts for different levels of extra services.

- This FY reiterated how WINK’s competitive edge is based upon ensuring the franchisees provide a tip-top service to support a highly reputable brand:

“Winkworth’s franchise proposition is rooted in its brand and reputation.

…

Winkworth places significant value on the integrity of its brand, upholding it through exemplary standards of ethics and business conduct in all interactions

…

Winkworth strives to maintain a reputation for the highest standards of business conduct. The directors always endeavour to operate to the highest ethical standards in order to maintain and promote the reputation of the Company.

…

We have strong local market knowledge and expertise, both in London and in the country markets, and we commit to maintaining competitive fees while delivering unparalleled service to meet our customers’ needs.

…

We aim to expand our portfolio of rental properties by providing landlords with top-tier service and striving to equitably meet the needs of both landlords and tenants.

…

With our people-based ethos and as a premium, customer-focussed business dependent on its reputation, we understand that our success depends on everyone working under the Winkworth brand doing so with respect, loyalty and pride. All our offices need to ensure we exceed our customers’ expectations by delivering the highest quality service at all times so that our customers not only return, but also share their experience with other potential customers.“

- As such, not every franchisee applicant is successful. This FY said:

“Winkworth has a rigorous vetting procedure for new franchisees and only a small number of applicants are successful in joining the group. Once accepted, franchisees are closely monitored to make sure that they achieve the best practice service levels expected of them and remain compliant with the law. Winkworth provides regular training through its centralised in-house training academy, alongside which it runs regular compliance audits of franchisee offices, both remote and in-person.“

- Appointing higher-quality franchisees who can consistently operate as a “top three agency” helps ensure branches generate sufficient commissions during both strong and weak property markets. This FY stated:

“We are forging ahead with our plan to invest in our platform and bring on new talent to position us as a top three agency in each local area we operate in within London. We believe that this focus will ensure our franchisees are profitable through the various cycles of the property market and well positioned to continue to invest in their businesses.”

- This FY described the proportion of branches boasting a top-three local market share:

“Almost half of our franchises and the vast majority of our London offices are now in the top three slot by market share in their local area and our performance figures continue to improve.“

- I cannot recall WINK disclosing its proportion of ‘top three’ agents before.

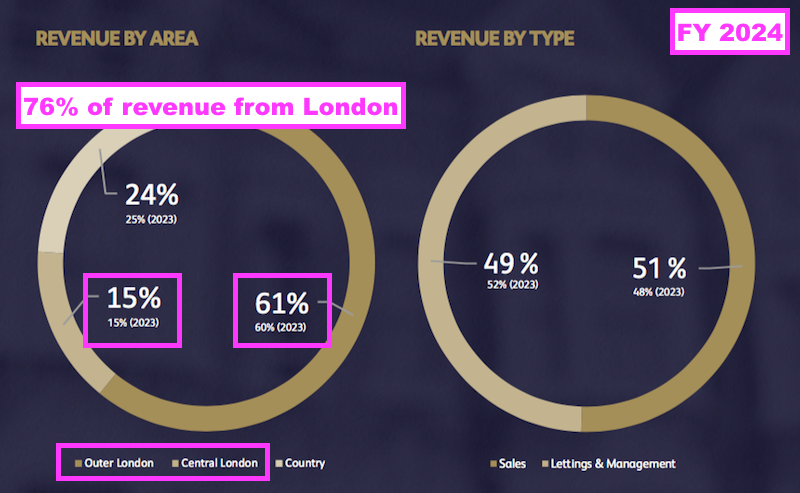

- The “vast majority of our London offices” enjoying a “top-three slot” feels encouraging, given London branches contributed 76% to this FY’s revenue:

- Not only is WINK selective with its franchisees, the franchisees are selective with their vendors. This FY revealed:

“We aim not to take on more properties than we believe we can service and, to a certain extent, that has meant that every time an office reached its natural optimum turnover, the franchisee has been encouraged to open a new office to service an adjacent popular area.”

…

“We plan to keep a balance between not going after every single instruction in each area with offering the best selection. This benefits vendors and also attracts the most buyers.”

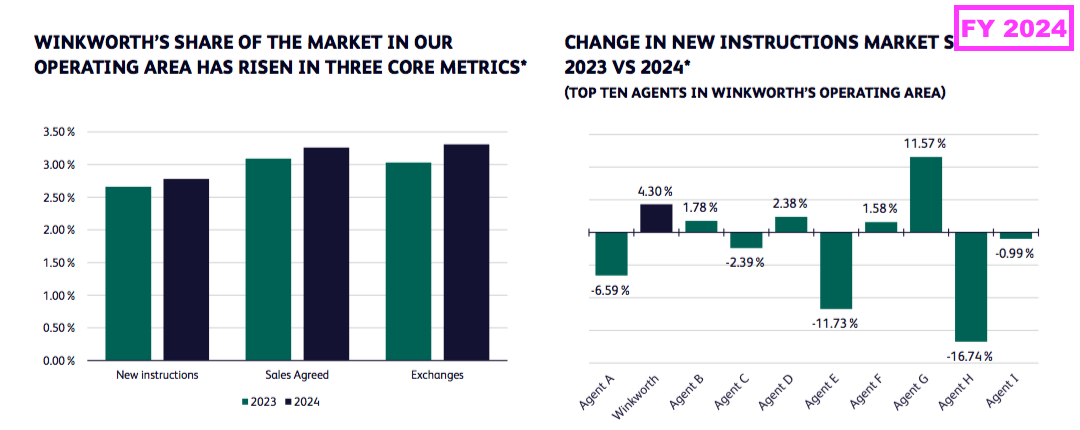

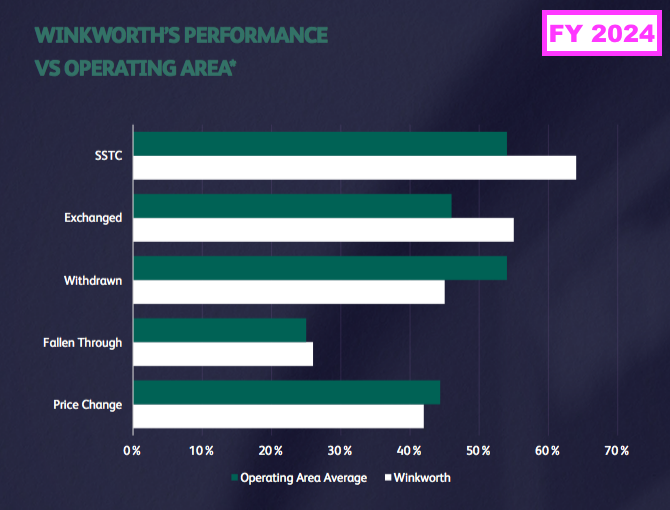

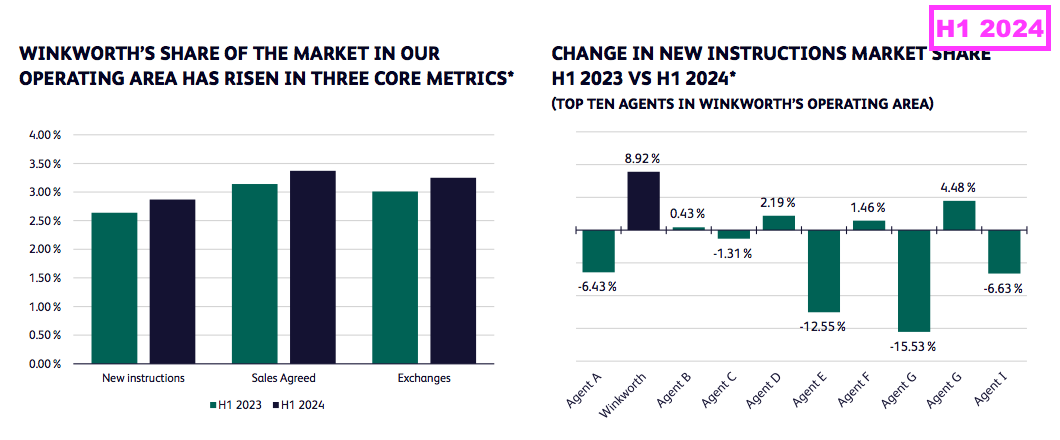

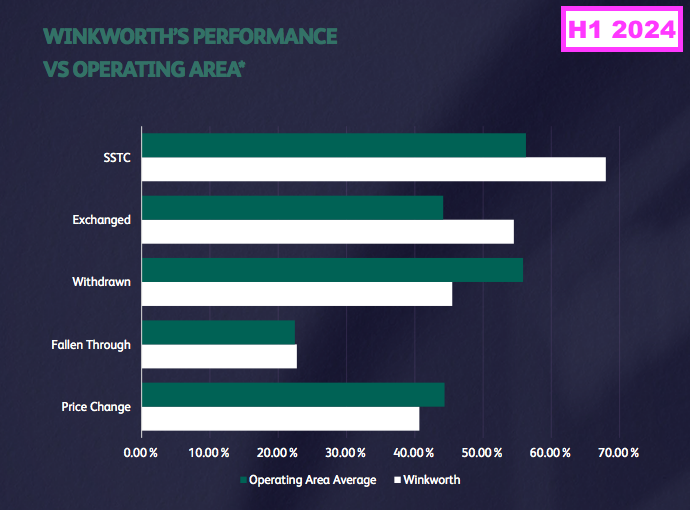

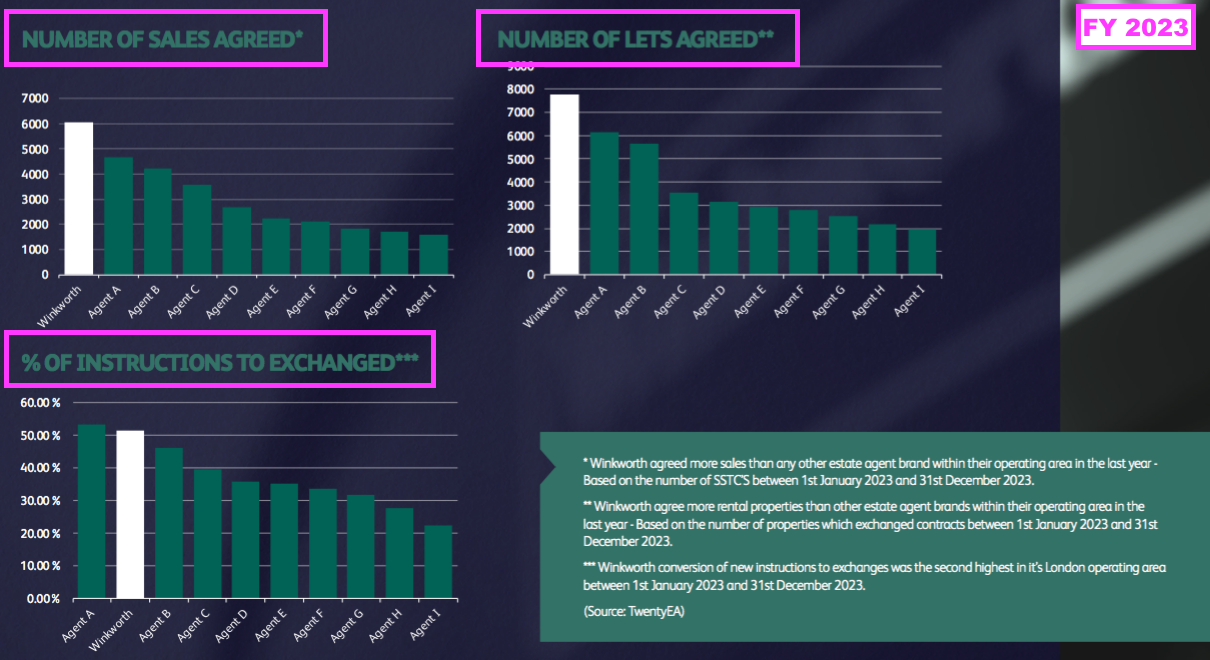

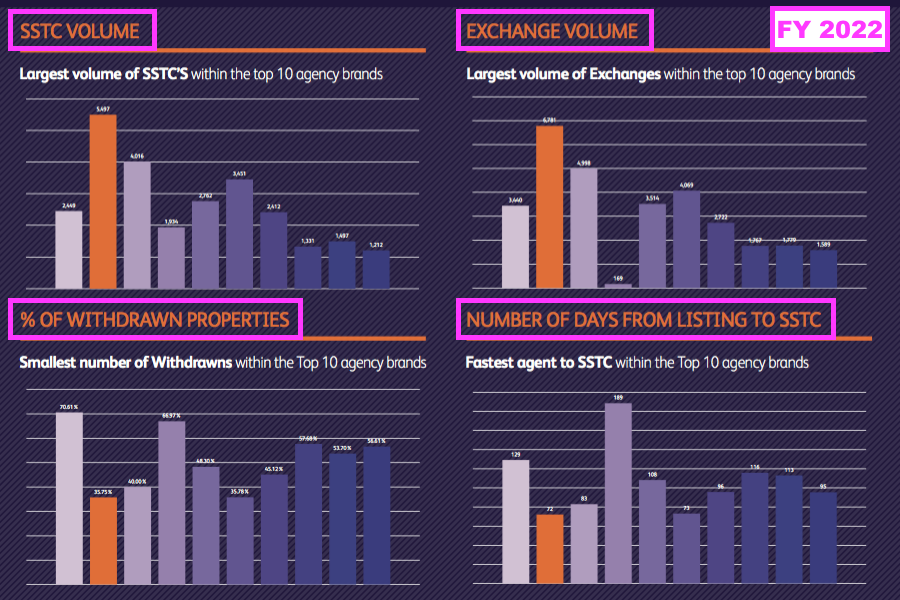

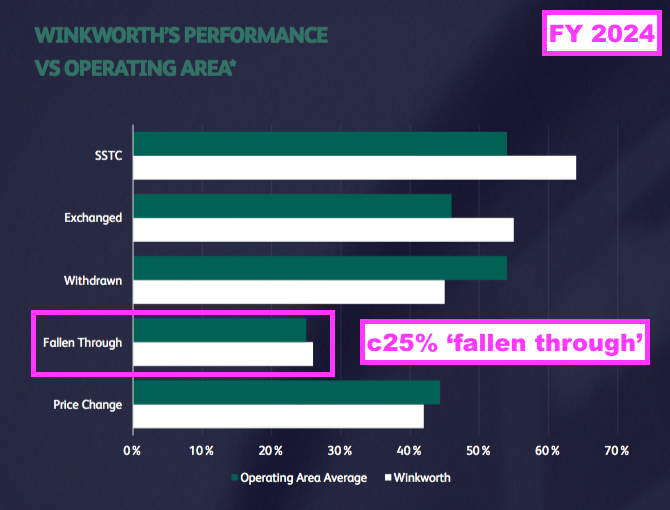

- Being discerning with franchisees (and vendors) resulted in this FY showcasing the greater effectiveness of WINK’s franchisee network versus nine other (anonymous) London estate agents:

- Note the industry measures published for this FY matched those measures published for the preceding H1…

- …but differed to those published for the comparable FY…

- …and differed to those published for the FY before that:

- I trust WINK will continue to report consistent industry measures; the previous changes had implied WINK was cherry-picking the most favourable stats.

- Indeed, this FY referred to WINK’s superior market share of new listings and agreed sales:

“I am delighted that the hard work and professionalism of our franchisees led to Winkworth’s market share of new listings growing at the fastest rate of the top five agencies in London, while our market share of sales agreed (“SSTC”) grew by more than any of the other top ten agents in London“

- But for the comparable FY, WINK referred to its superior volume of agreed sales and lettings, and its superior number of exchanges:

[FY 2023] “The quality of our platform and of our franchisees meant that we agreed more sales and lettings than any other agent within our operating area. In sales, we ranked second against our peers for converting listings to exchange, a measure of which we are proud as we believe it is the one that best reflects goodwill for the Winkworth brand and the achievements of our franchisees.”

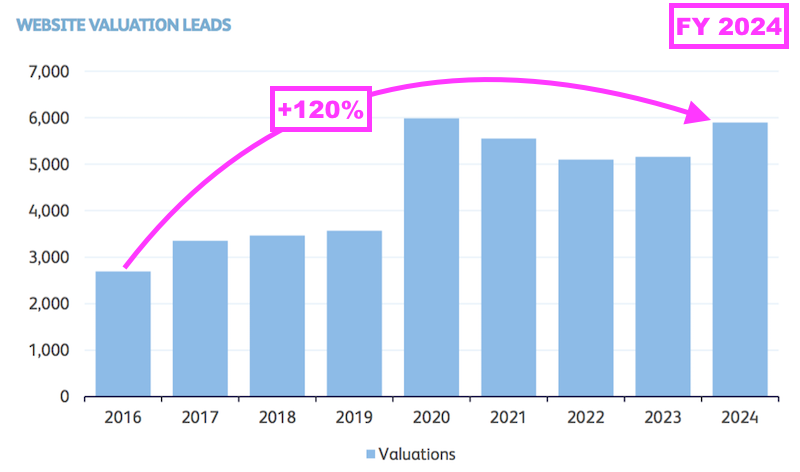

- Despite the relatively impressive industry data, WINK’s conversion of website valuation leads has not obviously improved since FY 2016:

- Such leads have increased by approximately 120% while network sales income since FY 2016 has advanced by only 26%:

- Almost 6,000 website valuation leads were generated during this FY — equivalent to approximately 60 per branch.

- 60 valuation leads a year per branch does not seem a huge amount, given a proportion of those leads will then not employ WINK to sell the property and, of those that do employ WINK, a proportion will then not exchange and deliver a commission.

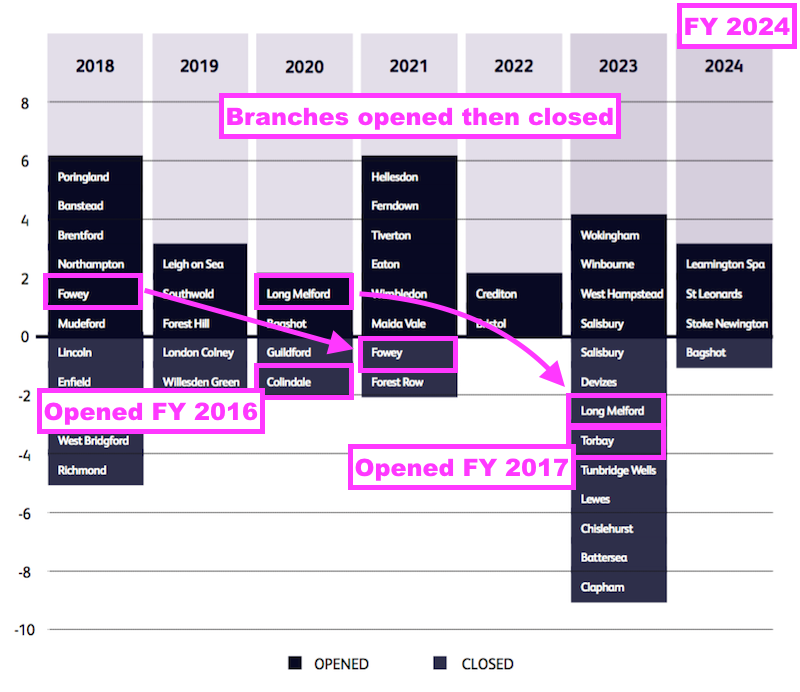

Franchisees: branch openings, closures and resales

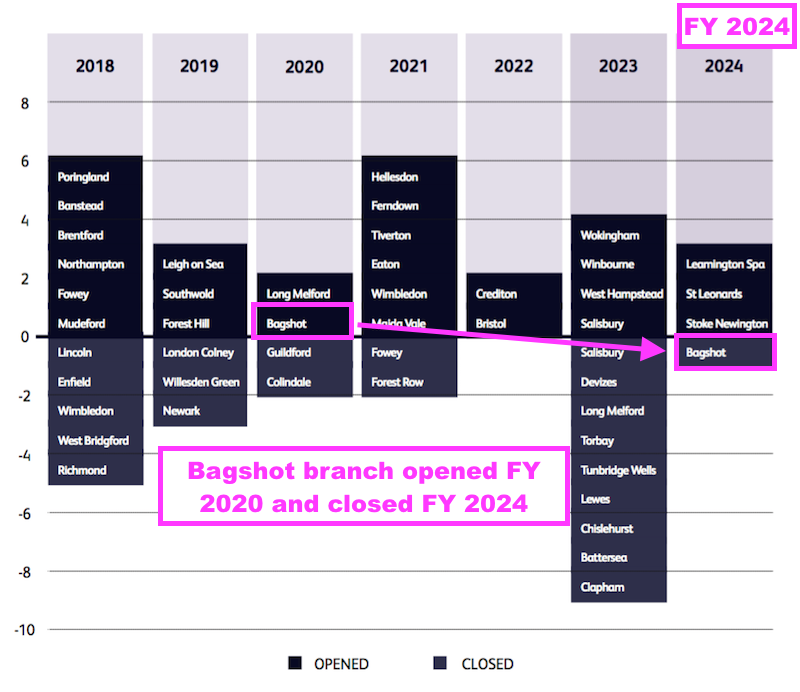

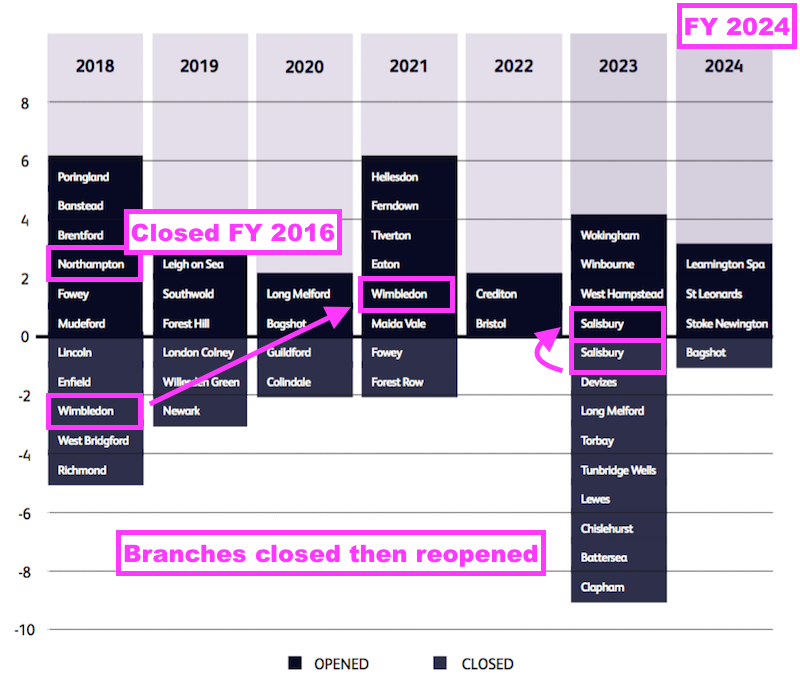

- Following the closure of nine branches during the comparable FY, this FY reported only the Bagshot branch had been shut:

- Bagshot joins Colindale, Fowey, Long Melford and Torbay as branches that have opened but then closed since FY 2016:

- The FY webinar made the point that, despite the nine closures during the comparable FY, the network’s market share improved during this FY:

“To validate the strategy, you look at the fact that, despite these closures in 2023, our market share grew by more than any other top 10 agent in London in 2024.“

- The FY webinar reiterated branches are closed when the franchisee appears unable to meet the aforementioned “top-three agency” status:

“The overarching vision is to bring in the best talent into the business… [Our approach] incorporates [branch] resales and areas where we have walked away from because we felt that they were not good for the franchisee and not good for the Winkworth brand, [albeit] with the confidence that we could return to those areas with new operators if need be.“

- Board comments at the 2025 AGM emphasised the same point. Attendees were told:

- “We are not going to hang on to people where it’s not the right thing for them or for us“;

- Unprofitable franchisees “cost” WINK, and;

- If a franchisee is not earning suitable returns, then something has to change “or they lose the franchise“.

- Board comments at the 2025 AGM also noted some locations may not be suitable for WINK because of their low level of transactions. Attendees were for example told “people go to Sheen and they never move” whereas “Putney is a big moving area“.

- This FY confirmed five branches had been resold and said a further nine resales could be undertaken:

“During the course of 2024, we opened three new offices and resold five franchises to new operators. At the end of the period under review, the Group consisted of 100 offices. We ended the year with a strong pipeline of nine potential resales and six new openings. In 2025, we have already opened two new offices.”

- Branch resales — rather than new branches — have attracted greater management attention over time. Attendees at the 2025 AGM were told:

[AGM 2025] “We have learnt the opportunity to increase revenue through resales is bigger than the opportunity through ‘cold starts’. There is a database already there and so we can work it harder. That is a bit of a change in direction.“

- In fact, H1 2023 claimed “new blood” could improve revenue from resold branches in London by “three- or four-fold“:

[H1 2023] “In London, we have identified further opportunities to both introduce new blood to existing businesses and to significantly improve the sales performance of offices with strong underlying lettings businesses. We believe that in certain situations we may be able to increase the available franchise revenue three- or four-fold, the equivalent of opening multiple cold start offices.“

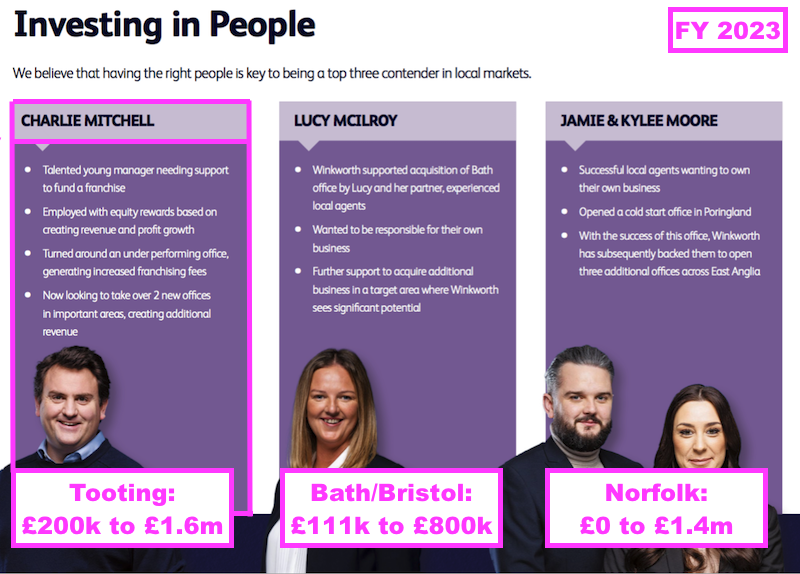

- Among the five branches resold during this FY were Herne Hill and Streatham.

- Herne Hill and Streatham were taken on by Charlie Mitchell, the “new blood” who turned around WINK’s Tooting branch to improve revenue eight-fold (see Company-owned offices):

- I said at the 2025 AGM that Mr Mitchell did really well at Tooting, and I was told he was “doing even better at Streatham“.

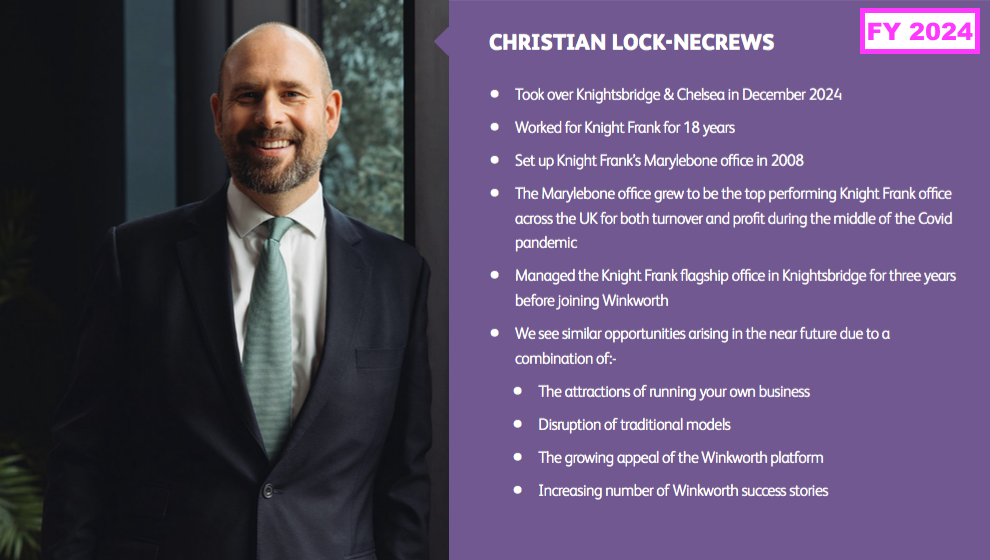

- This FY highlighted the resale of the Knightsbridge & Chelsea branch to Christian Lock-Necrews:

- Mr Lock-Necrews joined WINK with an impressive CV:

- “Set up Knight Frank’s Marylebone office in 2008“;

- “The Marylebone office grew to be the top performing Knight Frank office across the UK for both turnover and profit during the middle of the Covid pandemic“, and;

- “Managed the Knight Frank flagship office in Knightsbridge for three years before joining Winkworth”

- The FY webinar described Mr Lock-Necrews as a “best-in-class” agent:

“We headhunted Christian Lock-Necrews to take over our Knightsbridge & Chelsea office, which was sadly not in the top three. He has 18 years at Knight Frank and obviously was running the market leader in that area. It shows we can go and secure the best-in-class operator and bring them into Winkworth, so hopefully Winkworth can appeal to anyone“.

- The FY webinar also noted the appointment of Mr Lock-Necrews might persuade other “best-in-class” agents to join WINK:

“The impact of this recruit in terms of others approaching us has been fantastic. We’re very pleased that Mr Lock-Necrews obviously believes that we can compete at the top and we will continue to look to recruit others where possible“

- Mr Lock-Necrews participated in this WINK podcast earlier this year.

- The FY webinar also confirmed “best-in-class” agents joining WINK agree to the same franchise terms — notably the 8% commission rate paid to WINK — as everybody else.

- H2 appeared much quieter for branch resales and new openings than H1.

- The preceding H1 reported four resales and three new openings, with H2 witnessing only the aforementioned Knightsbridge & Chelsea resale.

- The preceding H1 highlighted WINK’s target of opening eight new offices a year, which in turn implied a further five new offices should have been opened during H2:

[H1 2024] “We are on track to deliver on our annual target of eight new offices, having in H1 2024 already opened three and with a further five in the pipeline.”

- This FY did not mention the new-openings target and just said six new openings were now in the pipeline:

“We ended the year with a strong pipeline of nine potential resales and six new openings. In 2025, we have already opened two new offices.”

- WINK may have dropped its public target for new openings, which seems sensible given:

- Resales appear to have much greater opportunity for revenue growth than new branches, and;

- Suitable franchisees for new branches are unlikely to be recruited at regular intervals.

- Since this FY, new openings include West Putney and Belsize Park and resales include Hammersmith and Beckenham.

- Note that new branches can include WINK locations that had previously been closed. Since FY 2016, Northampton, Salisbury and Wimbledon have been re-opened under fresh management:

Franchisees: network productivity

- Although 35 branches have been opened since FY 2016, some 27 have meanwhile been closed.

- Opening only a net eight new branches during nine years underlines how WINK’s expansion is dependent on capturing “talented agents“. As this FY’s webinar said:

“Our focus as a business is really about getting the best people into the network. We have developed over the years different routes to allow us to capture as many talented estate agents as possible because once they’re in our network, good things follow. So we’re very focused on that.”

- Presumably the 27 branch closures since FY 2016 emphasise an agent’s ‘talent’ may deteriorate over time.

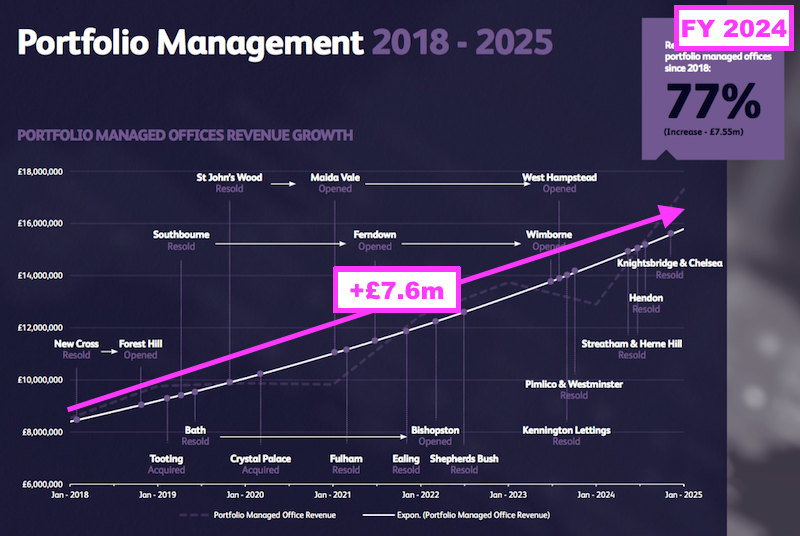

- The comparable FY summarised the extra revenue earned since FY 2018 from seven resold franchise branches, six new franchise branches and two WINK-acquired offices:

- This FY updated that summary:

- The updated summary now shows extra revenue of £7.6m (previously £3.3m) generated by 20 (previously 15) resold/opened/acquired locations between FY 2018 and this FY.

- The extra £7.6m from those 20 branches compares to the extra £18.2m of total franchise network income generated during the same time, which suggests the other 80 or so branches raised their collective income by £10.6m.

- Clearly the 20 resold/opened/acquired locations have on average grown somewhat faster than the typical branch since FY 2018.

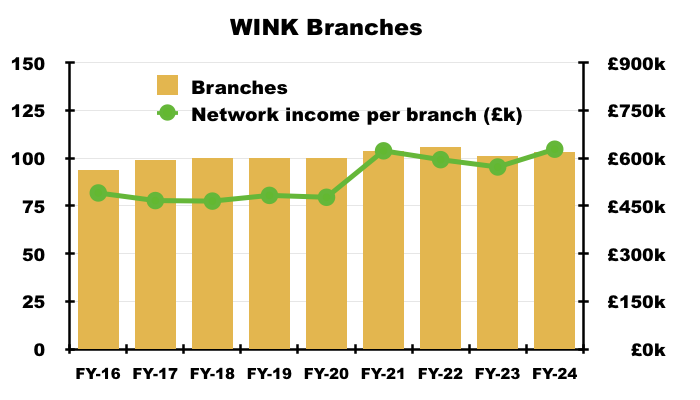

- Network income per branch during this FY was approximately £628k, which was:

- Up 10% versus the comparable FY;

- Up 35% versus FY 2018, and;

- £5k more than the previous high set during FY 2021:

- WINK has never disclosed revenue per branch, and the comparable FY’s webinar explained how a branch’s market share was more important to the group than comparing its income to the network average:

[FY 2023] “[Franchisee income] varies hugely as to what is acceptable and what is not. A franchise in, say, Dartmouth has low costs but commensurately lower revenues. In central London costs are higher but revenue potential is high. To average it out is always difficult as it does not reflect either. But we can see what we can do with the transparency on that.

One size unfortunately doesn’t fit all, there isn’t one metric we could apply to all offices fairly. That’s why we look at market share per area because it’s fairer. If you’re within the top three in your area, with some exceptions, that is a sustainable place to be, but revenues will be very different for, say, Dartmouth compared to Chelsea.”

- Board remarks at the 2025 AGM explained why WINK limits the information it discloses. Attendees were told:

[AGM 2025] “Our competitors open offices where we are simply because we are there. They know we are good and we get neighbours we don’t want. We have to be careful with our information.“

- Network income per branch is an obvious — but perhaps simplistic — measure to assess whether network productivity has improved or not.

- Network income per branch could be flattered just through rising house prices, which could mask the lack of relative progress from the network’s weaker agents.

- Mind you, board remarks at the 2025 AGM claimed WINK’s progress in London since 2016 had in fact been “all market-share growth” because the capital had experienced “no price rises“.

- To reassure shareholders that network productivity remains healthy and is not underpinned only by rising prices, WINK should regularly disclose the proportion of network revenue derived from branches with top-three local positions.

- After all, WINK did use this FY to outline the number of branches with a top-three status:

“Almost half of our franchises and the vast majority of our London offices are now in the top three slot by market share in their local area and our performance figures continue to improve.“

Franchisees: sales and lettings income

- The preceding H1 claimed “extended conveyancing times” had deferred many agreed sales from H1 into H2:

[H1 2024] “Network sales revenue in H1 2024 was up by 9% on H1 2023, but sales agreed is a much stronger 21%, reflecting extended conveyancing times which will push much of this activity into H2 2024 completions.”

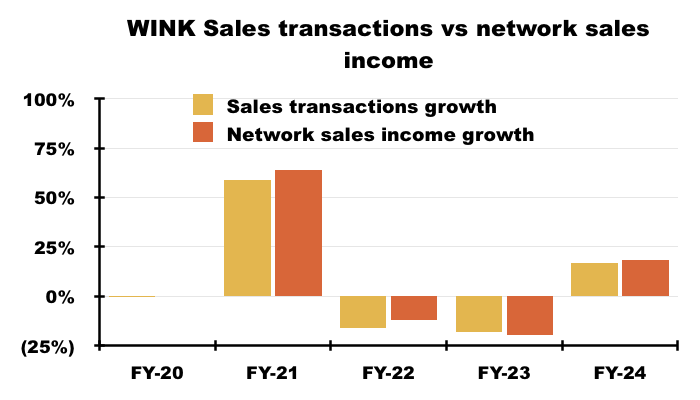

- Sure enough, this FY reported H2 network sales income up 26% versus 9% for H1:

- Given H2 network sales income gained 26% due in part to deferred H1 completions, the 27% improvement to agreed H2 sales…

[Q4 2024] “Having risen by 19% year-on-year in H1 2024, the number of sales agreed rose by 27% in H2 2024 and by 23% for the year as a whole. Completed sales in FY 2024 rose by 19%, compared with the prior period, and the Board is pleased with the momentum going into FY 2025.”

- …presumably implies many of those agreed H2 sales will spill over into H1 2025.

- Mind you, an agreed sale is not a completed sale… and those earlier industry statistics did include a ‘fallen through’ rate of approximately 25%:

- This FY showed sales transactions up 17%, with exchanges within London supporting the majority of the 18% advance to FY network sales income:

- FY sales transactions gaining 17% is a welcome improvement on the two prior FYs, during which transaction volumes declined following the post-pandemic boom of FY 2021:

- I had to double check, but WINK actually recorded flat network sales income (at £23.8m) and flat transaction volumes during pandemic-blighted FY 2020:

- My sums indicate between FY 2019 and this FY, annual sales transactions have improved 28% while annual network sales income has gained 37%. Possible reasons for the difference include:

- Higher value properties being sold;

- Rising property prices, and/or;

- Improved commission rates from vendors.

- My sums suggest WINK’s franchisees have not lowered their fees to win transactions. But this FY did repeat the risks to sustaining commissions:

“Risk: Winkworth faces ongoing competition from three types of agencies – corporate networks, independent businesses and franchise networks. Further consolidation among corporate networks or the emergence of innovative or discounted service models may exert pressure on commissions, potentially leading to reduced revenues for the company.

…

Risk: In a market with reduced trading activity, pressure on commissions may escalate, potentially resulting in lower earnings from fewer transactions. Specifically, Winkworth is vulnerable to shifts in the London market, as the majority of its revenue stems from franchisees concentrated in this region.”

- Note that this FY also reiterated a commitment to “maintaining competitive fees”:

“We have strong local market knowledge and expertise, both in London and in the country markets, and we commit to maintaining competitive fees while delivering unparalleled service to meet our customers’ needs. We strive to cultivate trust and confidence, fostering enduring relationships and earning recurring business.”

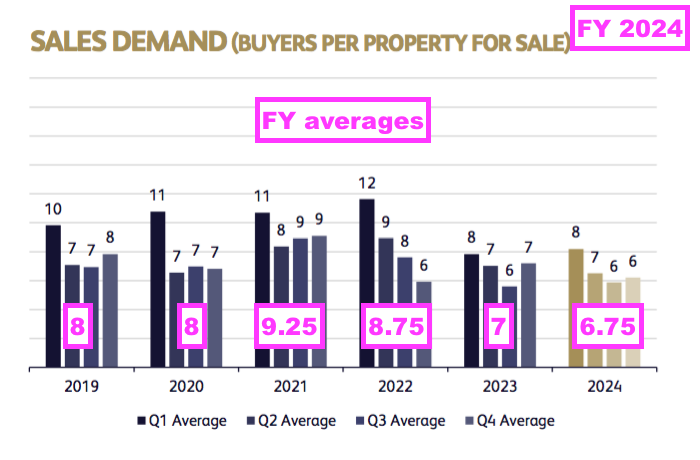

- This FY confirmed the number of potential buyers per property for sale had slipped from an average 7 to an average 6.75:

- Slightly lower buyer demand therefore suggests greater supply — rather than higher prices — supported the 18% advance to this FY’s network sales income.

- This FY said both buyers and sellers had simply decided to get on with moving home:

“As buyers sensed an end to the interest rate tightening cycle and the cost of mortgages fell, in 2024 we saw buyers (21% ahead of 2023) and sellers (20% ahead of 2023) brush aside previous electoral concerns both in the UK and internationally and expedite home moves that had been delayed by the cost of living crisis.

…

Increased costs of finance, high rental prices, changes to the taxation of pensions and school fees, and the higher cost of living are all factors that add to the motivation of both buyers and sellers to transact.”

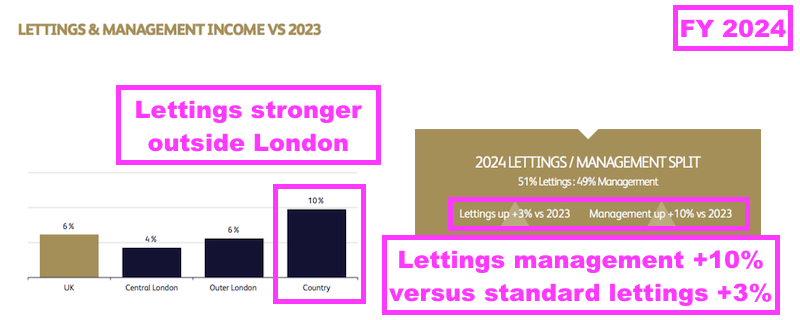

- In contrast to network sales income, this FY’s network lettings income performed better outside London:

- This FY noted the lettings growth outside London was supported by rental-portfolio acquisitions:

“Despite this reduction in registrations and a flattening of rental prices, we achieved lettings and management network revenue growth of 6% in 2024 to £32.0m (2023: £30.2m). This was led by the country markets where we saw an increase in revenues of 10%, driven by newer Winkworth businesses growing rapidly and supported acquisitions bolstering existing franchisee portfolios.“

- Note that board remarks at the 2025 AGM were not entirely supportive of lettings acquisitions (see below).

- WINK’s full property-management service continues to remain popular with landlords, with such FY income gaining 10%.

- In contrast, FY network income generated through the standard lettings service for ‘hands-on’ landlords improved only 3%.

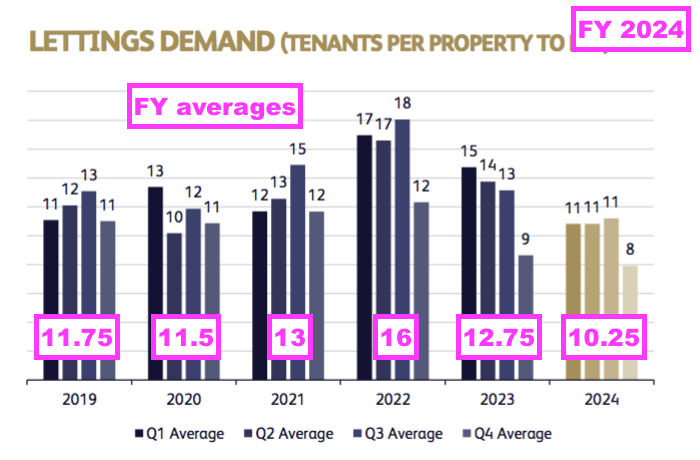

- The number of potential tenants per property to let was 10.25 during this FY — the lowest for an FY since at least FY 2019:

- Similar to the comparable FY and the preceding H1, this FY cited “affordability” reasons for the slower lettings progress:

“In the lettings and management business, increasing costs for landlords continued to see them exiting the sector, leading to a reduction in supply of properties to let. With rents at record levels, we have seen affordability ceilings reached and increasing trends in room sharing, young professionals choosing cheaper areas to rent or staying at home longer, and the bank of mum and dad lending to make buying more affordable. These developments have led to a reduction in tenant demand, and in 2024 we saw a 5% decline in tenants registered compared to 2023.”

- The tone of this FY’s lettings commentary contrasted with that of FY 2022, during which properties to let attracted up to 18 potential tenants that led to price increases of 10% or more:

[FY 2023] “The rental market remained incredibly strong across all regions, with price increases of over 10% in many areas due to a shortage of supply following the sell-off of many buy-to-let properties by landlords facing the higher tax and regulatory changes that have reduced the viability of this activity in recent years.”

- This FY’s sales-lettings network split was 51%-49% and reversed the 48%-52% split recorded by the comparable FY:

- This FY gave strong hints that future revenue would become biased towards sales rather than lettings:

“A couple of years ago I was asked why we were not diving into the rental market. My response was that while the lettings and management business will always be important to Winkworth, rental portfolios remain fairly static and do not rush to change. We would only look to buy [rental portfolios] in order to secure a growth point into sales.

In our opinion, sales agency has always offered greater profitability and better reflects selling skills, and the public is attracted to the best operators. Our rentals and management business has in the past grown to up to 50% of Group turnover, but sales are now dominating, and I am sure that over the long-term there will be some shrinkage in rentals as the trend of landlords exiting the business continues.

How would that affect Winkworth? There may be some impact on our business, but we would expect it to be compensated by increased sales and growth of market share as some competitors may have focused too much on rentals and diluted their sales teams.“

- Board remarks at the 2025 AGM covered the subject of (adverse) “government changes” to the lettings market. Attendees were told:

- The “shrinkage in rentals” is a “prediction“, but WINK “has to warn shareholders” about what may happen;

- 10% of a particular branch’s lettings portfolio was sold as a “direct result of government changes“;

- WINK’s chairman “would not be buying rental portfolios“, and;

- Lettings are “not disappearing” and they “support costs“, but growth has slowed and landlords are selling.

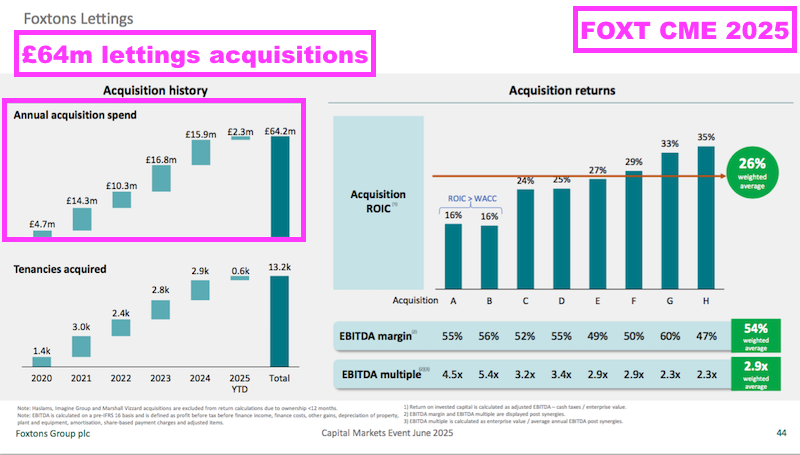

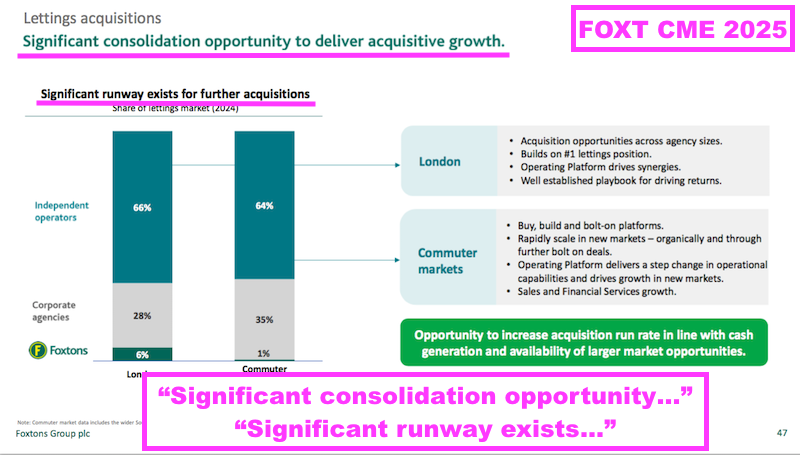

- WINK’s caution towards lettings contrasts to the optimism cited by London rival Foxtons (FOXT), which during a recent Capital Markets Event (CME) reported spending £64m on lettings agencies since FY 2020…

- …and has plans to purchase more:

Winkworth versus Foxtons

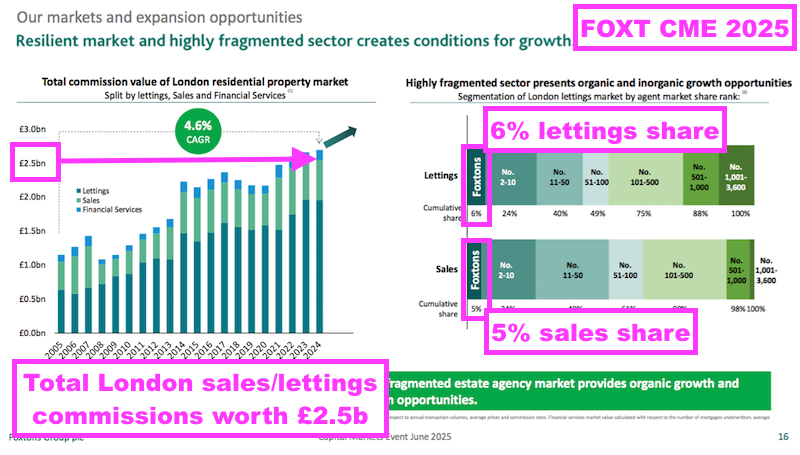

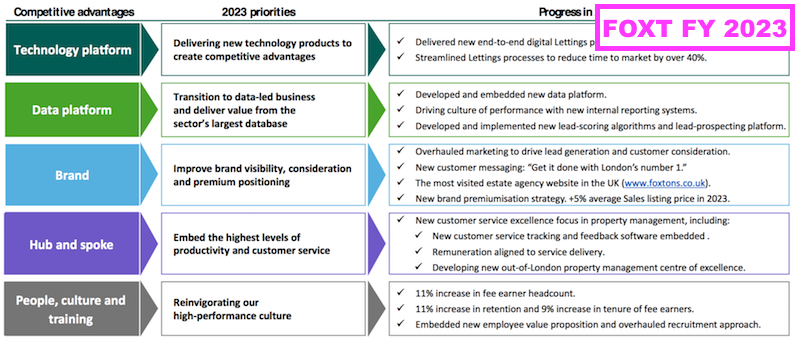

- FOXT claims to be “London’s leading estate agency” and remains as good a benchmark as any to assess WINK’s relative progress.

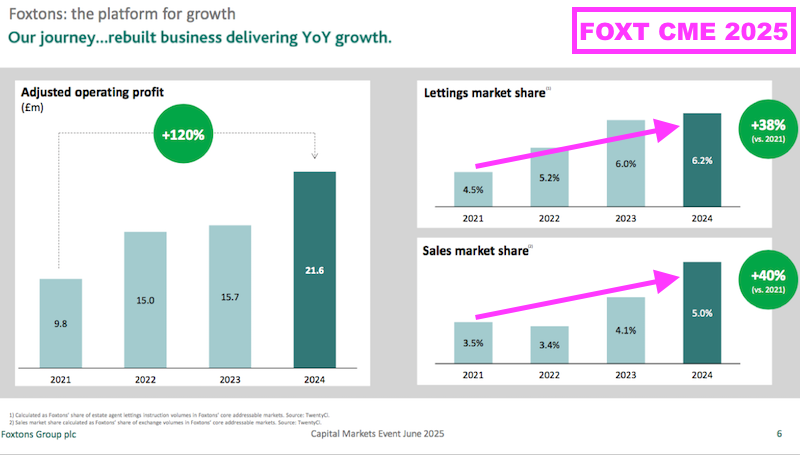

- FOXT’s recent CME showcased a 6% leading share of London’s lettings market and a 5% leading share of London’s sales market:

- FOXT’s CME also revealed the London property market to be worth approximately £2.5b a year from sales and lettings commissions.

- London branches earned 76% of WINK’s network income during this FY, equivalent to £49m or a 2% share of the capital’s estate-agency market (according to FOXT’s £2.5b estimate).

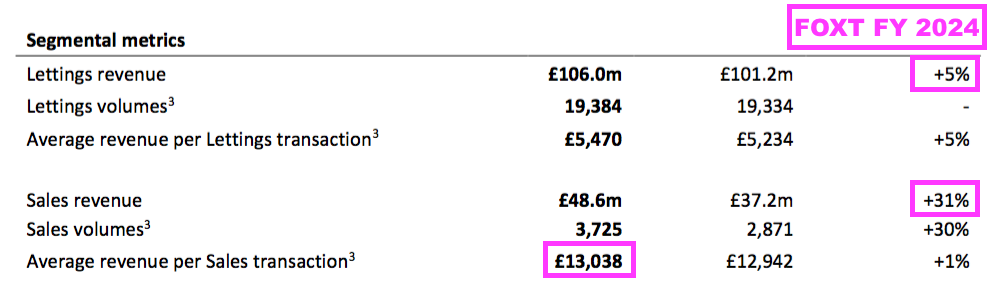

- FOXT experienced a much better FY 2024 for sales than WINK. FOXT’s FY sales revenue advanced an impressive 31%:

- Note FOXT’s £13k average revenue per sales transaction, which was achieved through a very commendable 2.25% rate of commission:

[FOXT FY 2024] “Average revenue per transaction was 1% higher than 2023 reflecting a 1% increase in the average price of properties sold (2024: £592,000; 2023: £586,000), whilst commission rates remained flat at 2.25% (2023: 2.25%).“

- FOXT’s FY sales income at £48.6m and a 2.25% commission rate implies FOXT sold properties for an aggregate £1.9b during FY 2024. WINK in comparison sold properties for an aggregate £3.4b and generated network sales income of £32.7m.

- FOXT’s FY lettings revenue meanwhile gained a modest 5%, slightly behind WINK’s 6%.

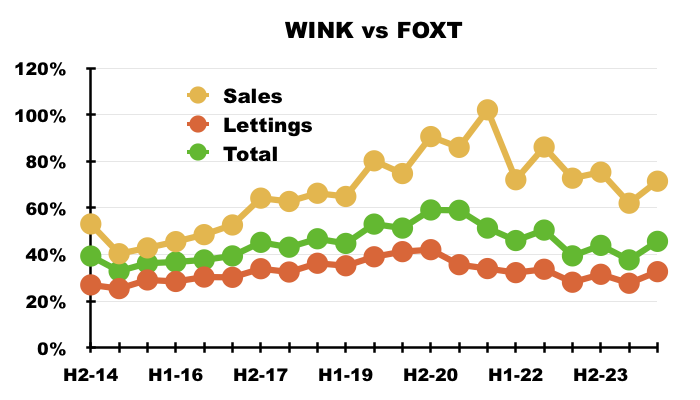

- The chart below expresses WINK’s network sales, network lettings and total network income as percentages of the comparable FOXT revenue:

- Note that comparing WINK against FOXT is not strictly like-for-like, given FOXT at present generates almost all of its revenue from locations within London while WINK’s franchisees generated 76% during this FY.

- Further distortion will be caused by FOXT and WINK acquiring and/or selling businesses. FOXT’s lettings revenue also includes interest on tenant deposits (£6.6m during FY 2024).

- Nevertheless, the rising trends until FY 2021 do suggest WINK’s self-employed franchisees handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees…

- …although FOXT has improved its performance markedly versus WINK since FY 2022.

- FOXT’s resurgence is linked to the 2022 appointment of a new chief executive, who instigated a number of initiatives to revitalise the group:

- The CME showed FOXT’s share of lettings and sales improving of late…

- …and might explain why WINK previously altered the industry measures reported to shareholders!

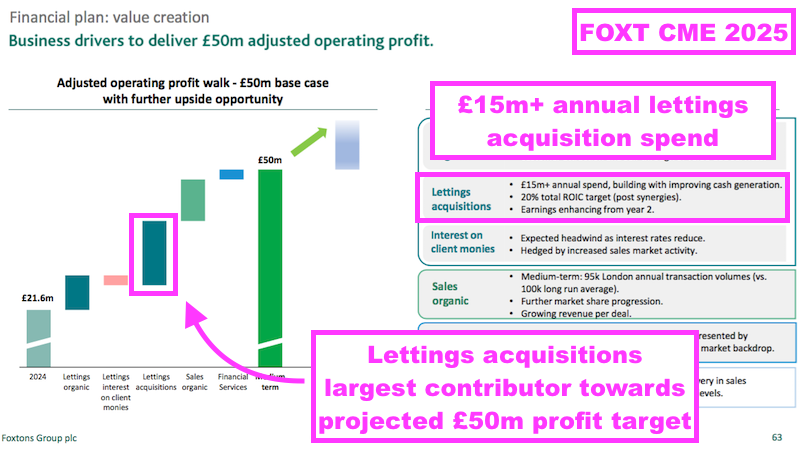

- FOXT declared a £21.6m FY 2024 profit and its CME revealed a fresh £50m “medium term” ambition:

- The largest component of FOXT’s projected profit growth is lettings acquisitions, with FOXT assuming an annual £15m-plus spend on lettings businesses.

- FOXT’s FY 2024 claimed extra lettings regulation ought to prove beneficial to large letting agents:

[FOXT FY 2024] “On the regulatory front, the Government is advancing the Renters’ Rights Bill, largely continuing the legislative framework proposed by the prior administration. While we support several elements of the Bill, we recognise that ongoing regulatory changes may introduce short-term uncertainty for landlords. Our focus remains on ensuring our customers—both landlords and tenants—are well-informed and positioned to navigate any potential market impacts. As the industry becomes increasingly complex, landlords are likely to place greater reliance on large, professional lettings agents, reinforcing Foxtons’ competitive advantage.”

- FOXT’s lettings optimism contrasts to the aforementioned lettings caution expressed by WINK.

- The differing viewpoints on lettings from WINK and FOXT should create a fascinating comparison during the next few years.

- FOXT’s CME also implied London sales transactions might recover to approximately 100k a year:

- FOXT’s assumptions for profit to reach £50m include London sales transactions limited to 95k a year.

- Board remarks at the 2025 AGM suggested London sales volumes could improve. Reasons included:

- Landlords realising they have another few years of a “slightly antagonistic government” that may prompt further supply, and;

- Following years of flat transactions, a greater “reality with pricing” emerging, whereby:

- Buyers finally decide whether they want to “buy in London or go somewhere else“, and

- Vendors finally decide to “drop their prices and get moving“.

- FOXT’s revitalised leadership could nonetheless leave WINK continuing to face stiffer London competition, and may even have prompted WINK to resell some of those five branches during this FY.

Company-owned offices

- WINK presently operates three company-owned offices:

- Tooting, acquired in stages between FY 2019 and the comparable FY for almost £300k;

- Crystal Palace, acquired during FY 2020 for zero, and;

- Pimlico, acquired during FY 2023 for zero.

- WINK has often said how the company-owned offices supply the group with greater “front-end” insight:

[FY 2023] “As with the acquisitions of Tooting Estates Limited and Crystal Palace Estates Limited, Lumley 1 Limited [Pimlico] will keep Winkworth in touch with and learning from front-end experiences and industry trends. It will also provide a live platform to test and develop future digital initiatives and evolve our centralised CRM systems, which will be of benefit to all our franchisees.”

- But WINK’s webinars have regularly explained the purchases are driven by improving lacklustre branches through talented agents who do not have the finances to become a franchisee:

[FY 2023] “The agenda we started with these offices was to bring people in who are really good at what they do, but don’t have the money [to launch their own franchise]. We are a franchise business and the better the people we have, the better our 8%, and we want to maintain our model as a franchise business.”

- Tooting was WINK’s first company-owned office and was turned around in spectacular fashion by the aforementioned Charlie Mitchell:

[H1 2024] “Tooting is an area where we identified a huge amount of transactions and we had a poor underperforming office, I should say with a franchisee keen to exit. By… acquiring it with Charlie Mitchell, our partner in the venture, he grew that revenue to £1.6m during the boom of 2021.”

- Mr Mitchell left Tooting to operate WINK’s Herne Hill and Streatham franchises, and his departure impacted Tooting’s profit during this FY:

“With our help, the manager in Tooting moved to acquire neighbouring franchises for his own account and our Tooting office was temporarily impacted by the transition to a new team, affecting its profitability. This team is now fully integrated and, with stable management across the own-equity offices, we expect to see strength in 2025 as Tooting returns to form and the more recent offices mature into profitability.“

- Mr Mitchell’s Tooting exit underlines the downside with WINK’s company-owned office approach: up-and-coming agents take charge, become successful and then move onto their own franchised branches…

- …leaving the financial performances of the company-owned offices somewhat unpredictable as replacement up-and-coming agents are recruited every few years.

- Indeed, the preceding H1 notably described the company-owned offices as “training grounds” for would-be franchisees…

[H1 2024] “Our equity-owned offices have expanded, and we are targeting good profitability from all four businesses in 2025. I have confidence that these offices are increasingly providing not only an important financial contribution to the Group, but also training grounds for future franchisees.“

- …which suggests Tooting and the other company-owned offices are likely to cycle through lots of different agents over time.

- Mind you, board remarks at the 2025 AGM indicated Tooting may not be a permanent ‘training ground’ should the right offer be received:

[AGM 2025] “If somebody offered good money [for Tooting], it would be off our portfolio“.

- Attendees at the 2025 AGM were also told WINK:

- Was “not looking to make huge money” through company-owned offices;

- Did not want to “risk the business” by having “too many” company-owned offices, and;

- Wanted to see the present company-owned offices “on trajectory before going further“.

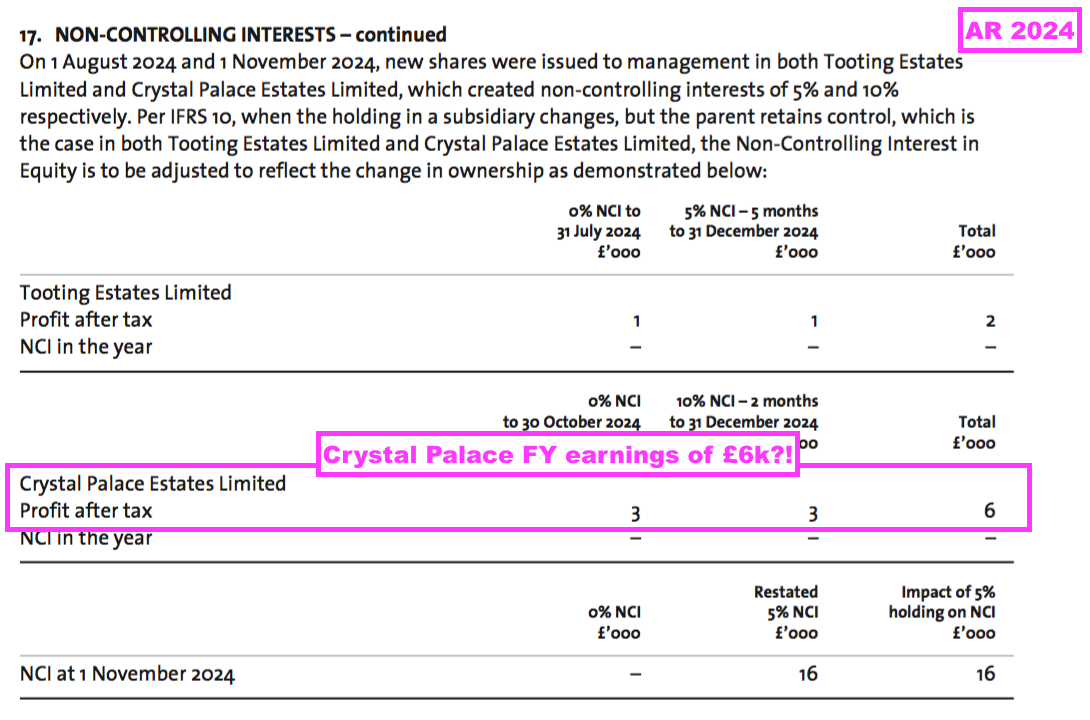

- This FY offered hope that Tooting’s fresh leadership could one day restore Tooting’s profit. WINK has given 5% of the office to the new management:

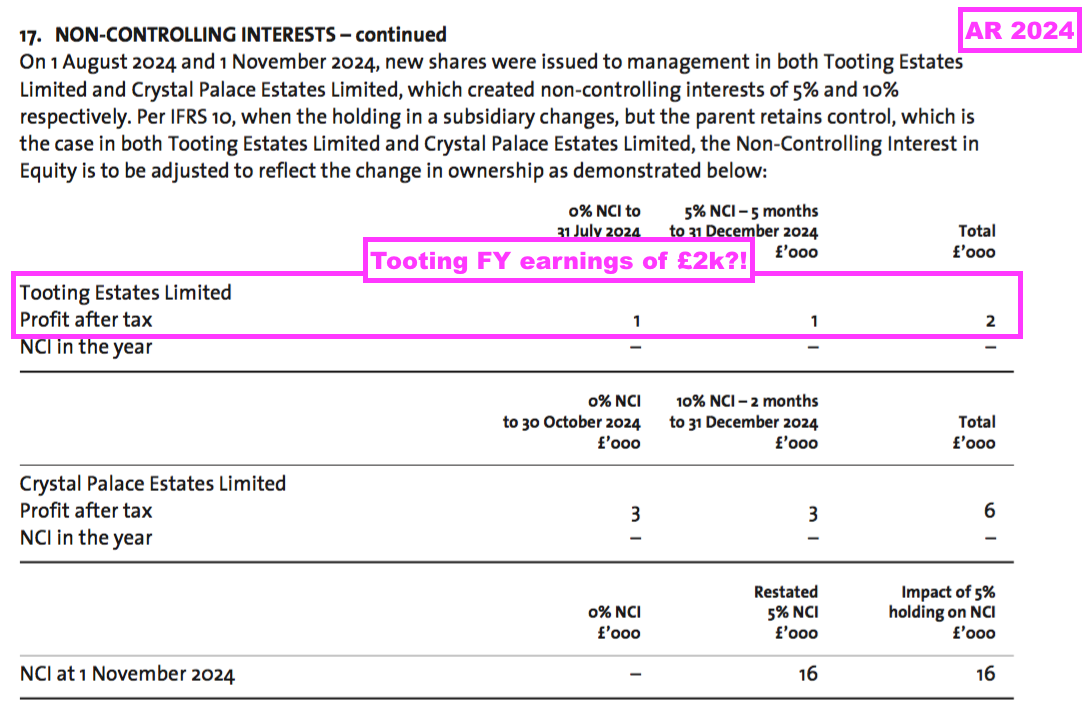

“On 1 August 2024 and 1 November 2024, new shares were issued to management in both Tooting Estates Limited and Crystal Palace Estates Limited, which created non-controlling interests of 5% and 10% respectively”

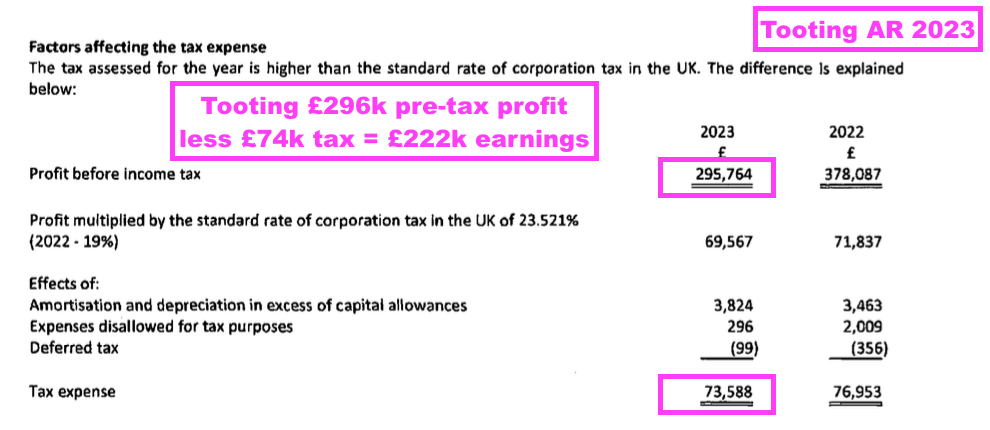

- This FY indicated Tooting’s FY profit was minimal:

- WINK has yet to publish Tooting’s accounts for this FY via Companies House, but the comparable FY showed a £296k pre-tax profit and £222k earnings:

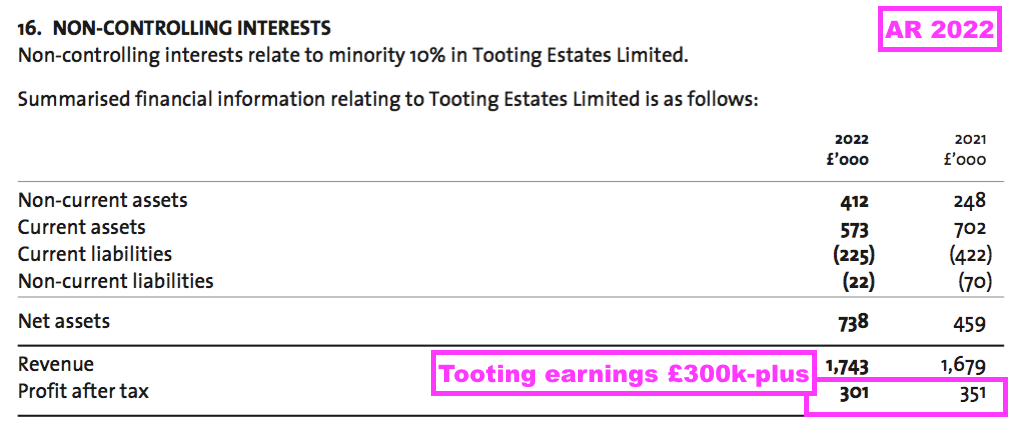

- Tooting’s earnings during FYs 2021 and 2022 in fact exceeded £300k:

- Tooting’s profits have generally been exceptional given only £300k or so was spent acquiring 100% of the office between FY 2019 and the comparable FY.

- Although this FY revealed Crystal Palace was profitable…

“With the exception of Tooting, our Owned Offices made good progress. Crystal Palace was profitable in the year and Winkworth Development and Commercial Investment Limited returned to profit.”

- ...Crystal Palace’s profit was also minimal:

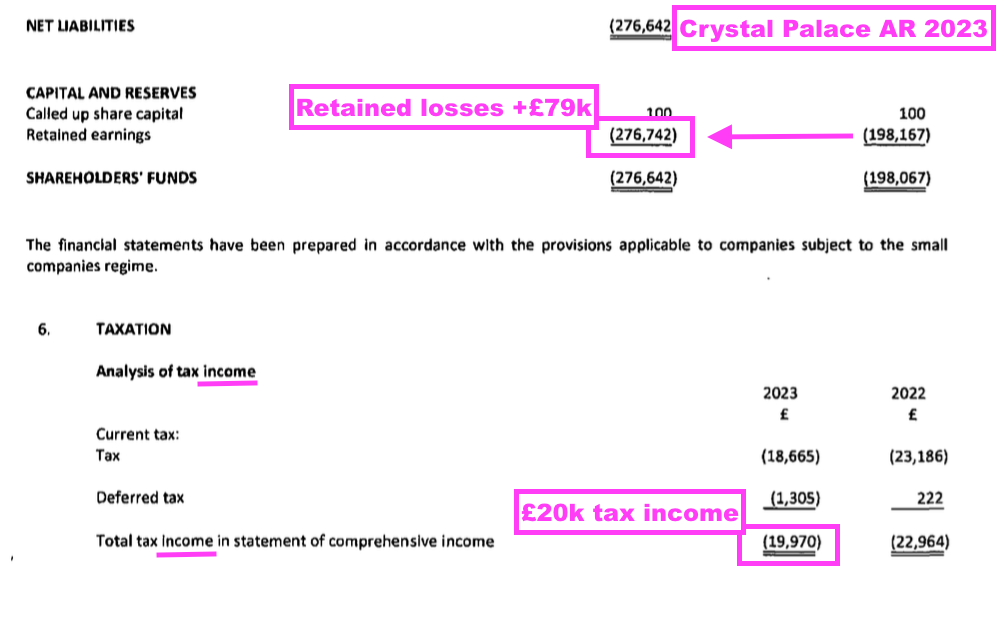

- Companies House indicates Crystal Palace suffered an approximate £99k operating loss during the comparable FY given the accounts showed retained losses up £79k and a £20k tax credit:

- Crystal Palace becoming (just about) profitable during this FY feels encouraging, given social media indicates Crystal Palace’s current manager has been in place since early 2022 and his loss-to-profit turnaround has therefore taken less than three years.

- Note also that Crystal Palace looks to have been a very poor performer prior to WINK’s ownership. The value of the intangible ‘customer lists’ acquired at Crystal Palace (£147k) indicates the office operated at half the revenue of Pimlico (£336k customer lists) and a third of the revenue of Tooting (£496k customer lists) at the time of their respective WINK purchases (customer lists are valued based on the respective office’s historic revenue (point 20)).

- This FY revealed WINK had rewarded Crystal Palace’s leadership with a 10% share of the office:

“On 1 August 2024 and 1 November 2024, new shares were issued to management in both Tooting Estates Limited and Crystal Palace Estates Limited, which created non-controlling interests of 5% and 10% respectively“

- This FY revealed Pimlico performed “ahead of expectations“:

“Lumley 1 Limited, our Pimlico office acquired at the end of 2023, performed ahead of expectations in its first full year under our ownership.”

- Board remarks at the 2025 AGM confirmed Pimlico “lost money” during this FY, but “lost less than expected“.

- The comparable FY (and Companies House) confirmed Pimlico incurred an £82k pre-tax loss during its first ten weeks of WINK ownership:

- Pimlico’s management has yet to receive any shares in its office.

- Reading between the lines, this FY suggested Crystal Palace and Pimlico would boast a top-three local position during FY 2025:

“After intensive repositioning we would expect to see most of our own-equity offices ranking as top three operators in 2025.”

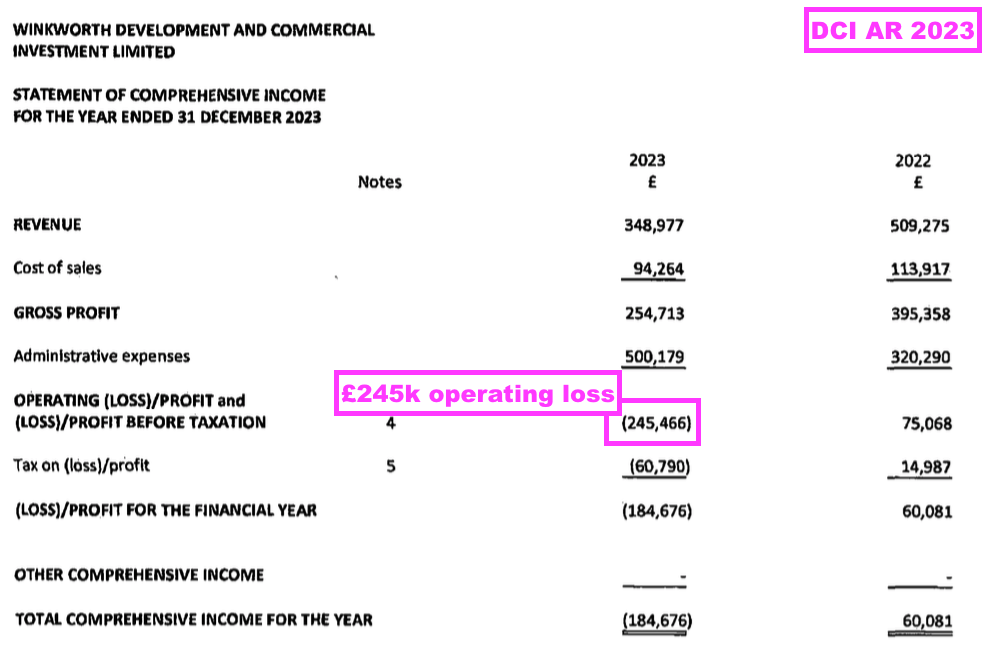

- The trio of WINK-owned offices is complemented by the aforementioned DCI agency. This FY said DCI returned to profit:

“With the exception of Tooting, our Owned Offices made good progress. Crystal Palace was profitable in the year and Winkworth Development and Commercial Investment Limited returned to profit.“

- Companies House reveals DCI suffered a £245k loss during the comparable FY:

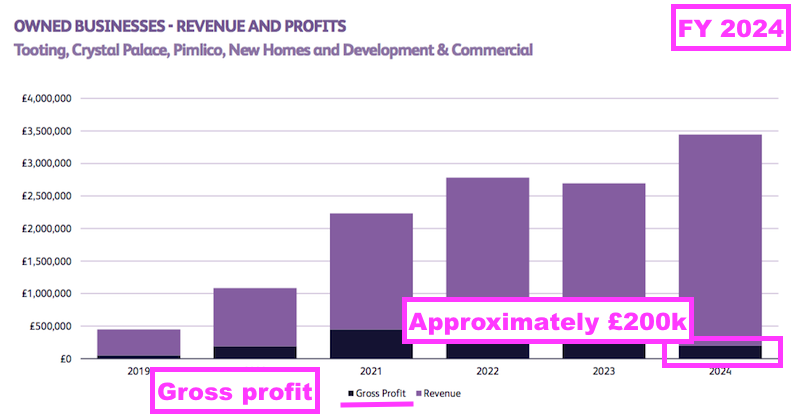

- This FY claimed the collective pre-tax profit of the group’s four company-owned offices was £200k:

“The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited, Lumley 1 Limited and Winkworth Development and Commercial Investment Limited, contributed revenue of £3.44 million (2023: £2.69 million). The New Homes element of Winkworth Development and Commercial Investment Limited generated c£0.25m of revenue and Lumley 1 Limited generated £0.61 million of revenue in the year. Overall, the owned offices contributed £0.20 million (2023: £0.48 million) of profit before tax in the year after deducting a year-one loss for Lumley 1 Limited, in line with expectations.”

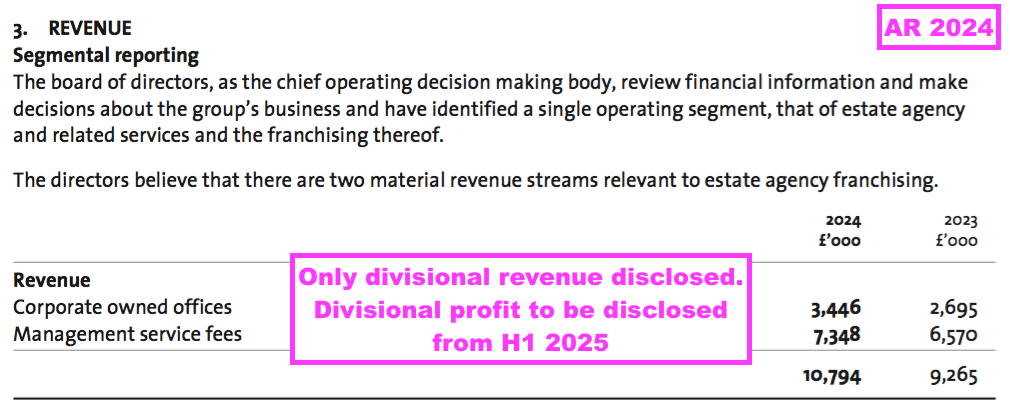

- However, the accompanying slides indicated the £200k pre-tax profit was in fact gross profit:

- This confusion surrounding the profitability of the company-owned offices should soon be resolved; board remarks at the 2025 AGM indicated WINK will formally disclose divisional profitability within the accounting notes from H1 2025:

- A significant remark from the preceding H1 was the targeting of “good profitability” from all of the company-owned businesses for FY 2025:

[H1 2024] “Our equity-owned offices have expanded, and we are targeting good profitability from all four businesses in 2025.“

- This FY did not repeat that target, and board remarks at the 2025 AGM described profits at company-owned offices as a “work in progress“.

- For FY 2025, I am hopeful Crystal Palace and DCI can remain profitable while Tooting can perhaps avoid losing money. I also hope Pimlico — judging by the loss-to-profit timescale at Crystal Palace — can become profitable during FY 2026.

- The full twelve-month contribution from Pimlico helped total FY company-owned office revenue gain 28% to £3.4m:

- Revenue from company-owned offices represented 32% of total revenue during this FY, and reached 34% during H2 — the highest proportion ever for the division.

- Should Crystal Palace, Pimlico and DCI ever sustain notable earnings, WINK’s return on these investments should be superb given the first two were acquired for zero and the latter was established internally.

- Indeed, although WINK’s long-term profitability has been dependent on the group’s main franchising division (see Financials: margin and employees)…

- …the company-owned offices do offer the group greater opportunity to influence earnings directly rather than rely on franchisees…

- …and could prove particularly valuable, especially if Crystal Palace, Pimlico and/or DCI can repeat the initial success of Tooting.

Boardroom

- WINK is run by the Agace family, with Simon Agace acting as non-executive chairman and his son Dominic Agace performing the role of chief executive.

- Simon Agace bought WINK during 1974 and began converting the then chain of eight company-owned offices into franchises during 1981. Dominic Agace joined WINK during 2001 and became chief executive during 2006:

- Simon Agace still retains a 41%/£11.1m shareholding, while Dominic Agace holds a 6%/£1.5m stake.

- As demonstrated by the franchise network increasing by just a net eight branches since FY 2016, the Agaces have adopted a cautious approach to expansion:

[FY 2023] “Winkworth looks to grow its franchise network and add like-minded entrepreneurial franchisees and offices to the network. Not, however, through growth at any cost, as new franchisees need to adhere to the Winkworth brand values. We also have a conservative approach to financing expansion.”

- The Agaces have clearly prioritised income over growth, with the ten years to this FY witnessing approximately 88% of reported earnings distributed through dividends or a return of capital:

- The “conservative approach to financing expansion” is meanwhile reflected by the group carrying net cash since FY 2008 (see Financials: cash flow and balance sheet).

- WINK’s board has witnessed several changes of late.

- A third executive — the group’s long-term legal counsel — was appointed to the board as chief operating officer last year in order to “offer better protection to Winkworth and its franchisees in a competitive industry facing increasing regulation” (point 1).

- More intriguing were last year’s appointment of two new non-executives, both of whom work as business consultants with M&A knowledge:

[RNS June 2024] “Tom Fyson is a Managing Director of Blackdown Partners, an independent advisory firm providing public and private businesses with advice on corporate finance, M&A, capital markets, investor relations and strategy. He brings over 20 years of financial experience, having begun his career at KPMG, where he qualified as a chartered accountant, before moving into corporate finance in 2006.”

Jonathan Adams spent 14 years in M&A and as an equity analyst at JPMorgan before working as a global fund manager, initially at Citigroup and, subsequently, for 16 years at Investec. In 2022, he founded Butterwalk Advisory LLP, providing advice to, and investing directly in, small cap companies. He is a Senior Advisory Board Member to King’s College Cambridge’s Entrepreneurship Lab, a privately funded body with the goal of increasing awareness of entrepreneurship amongst its student membership.“

- I must confess to be in two minds about a possible buyout at this share.

- An approach could of course deliver a useful short-term capital gain. But shareholders would then have to reinvest in a business that is also:

- Run by owners;

- Focused on dividends, and;

- Valued with a decent yield…

- ….to sustain a similar quality and level of income.

- Not surprisingly, board remarks at the 2025 AGM did not hint at any M&A action. Attendees were instead told:

- The appointment of the new non-execs was a move to “rejuvenate the board” (their predecessors were in their 80s);

- The new non-execs have public-market expertise beyond M&A to assist the board, and;

- The board remains focused on dividends and “growth under a certain amount of control”.

- Furthermore, WINK’s payment of quarterly dividends is possibly unique on AIM at present.

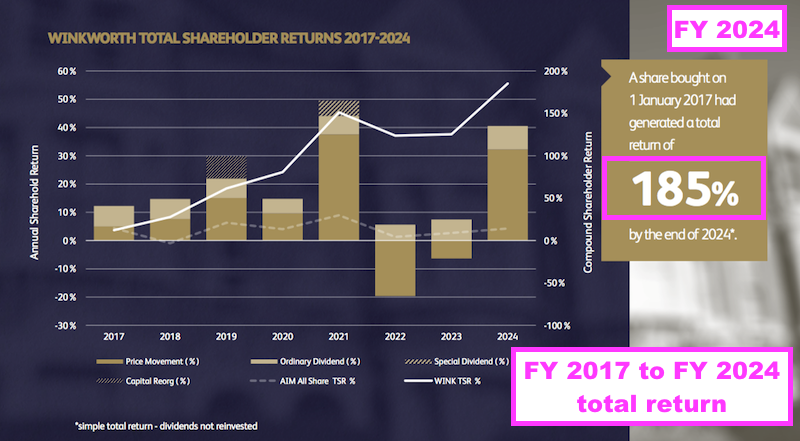

- The influence of the new non-execs might have been reflected by this new FY slide showing WINK’s total return since the start of FY 2017:

- That slide was mentioned by one of the new non-execs at the 2025 AGM. Note the FY 2017 start price used by the slide was a low point:

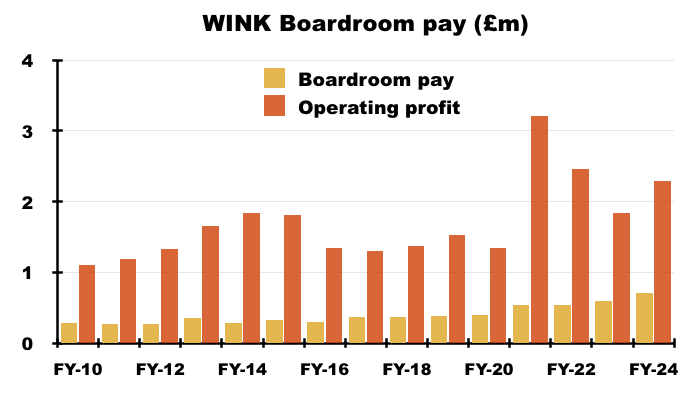

- I am pleased underlying board pay reduced during this FY.

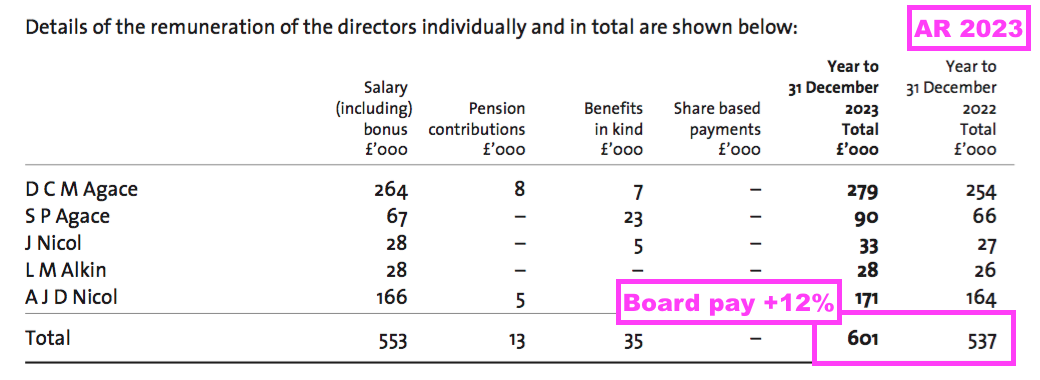

- During the comparable FY, total director remuneration had climbed 12% to £601k despite underlying operating profit sliding 25% to £1.8m:

- Note that total board pay was £330k during FY 2015 when operating profit was also £1.8m:

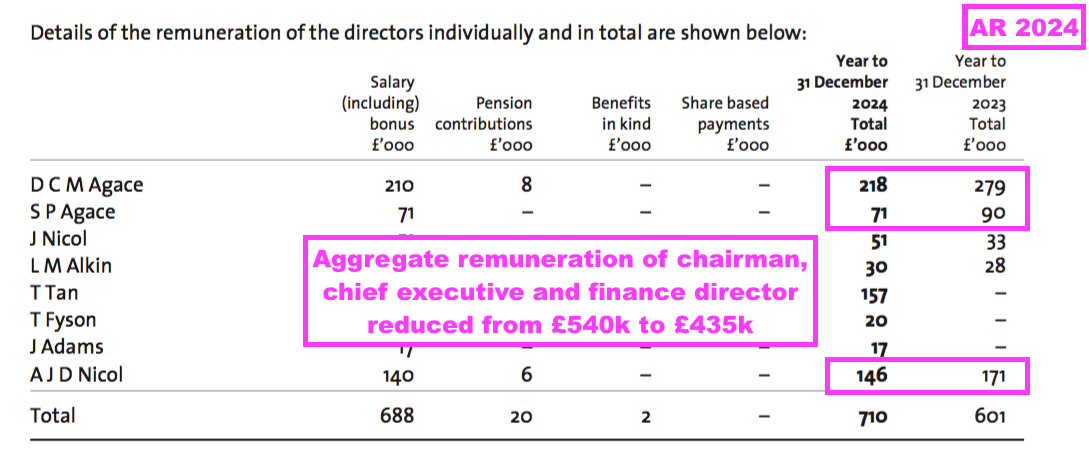

- This FY commendably witnessed the aggregate remuneration of the chairman, chief executive and finance director decline £105k despite underlying operating profit gaining 24% to £2.4m:

- For perspective, between FY 2014 and this FY, the chief executive’s annual pay and bonus has advanced 50% (£140k to £210k) while shareholders have seen their annual dividend increase 98% (6.2p to 12.3p per share).

- The board’s attitude towards possible share-price upside can be gleaned from the options granted to the chief operating officer earlier this month.

- The 75k options vest during July 2027 and simply require the shares to reach 250p before July 2035 versus the recent 208p.

- WINK does not have a history of extravagant option targets. The group’s previous options were granted during May 2017 when the share price was 112p and the option target price was 150p (the shares reached 150p less than three years later).

- Options now represent 3.6% of the share count and the option plan has a welcome 5% limit on dilution (the standard is 10%).

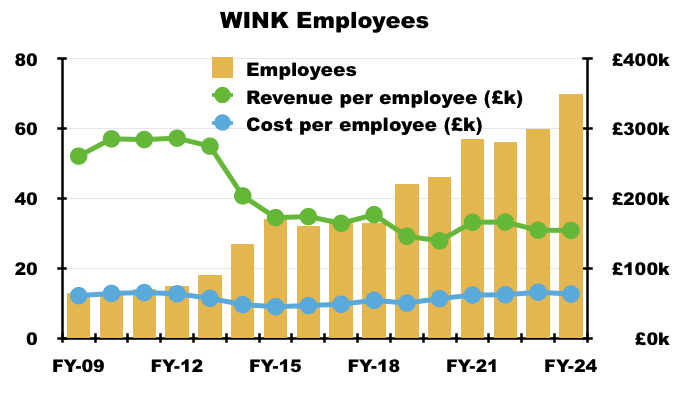

Financials: margin and employees

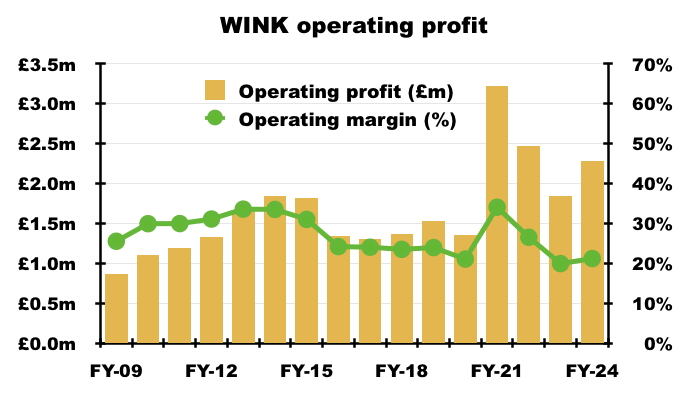

- Despite the minimal contributions from the company-owned offices, this FY still converted a respectable 21% of revenue into profit:

- For perspective, the average FY margin between FYs 2009 and 2018 — during which WINK operated as a pure franchisor — was a very appealing 29%.

- WINK typically enjoys a stronger H2 margin, and this FY’s 21% margin was split 19% during H1 and 23% during H2:

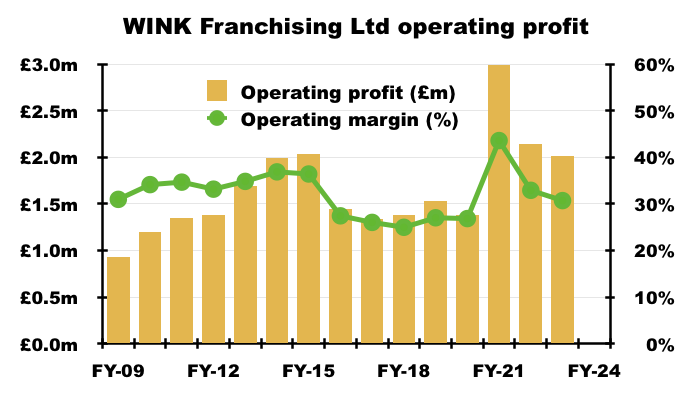

- WINK has yet to file this FY’s accounts for its main Winkworth Franchising subsidiary at Companies House, but the comparable FY witnessed the subsidiary earn a 31% operating margin:

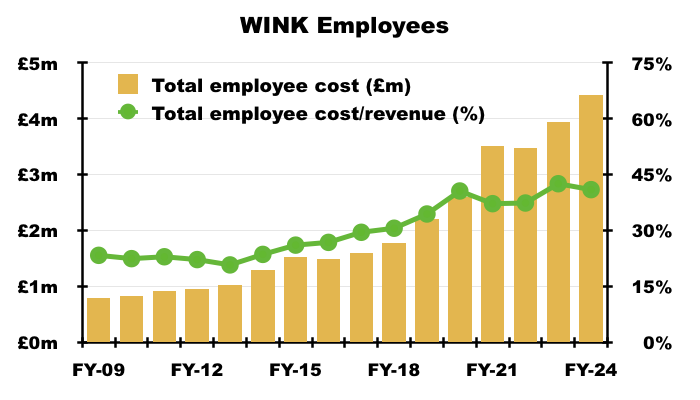

- Employees continue to be WINK’s largest expense:

- This FY witnessed 41% of revenue absorbed by the workforce.

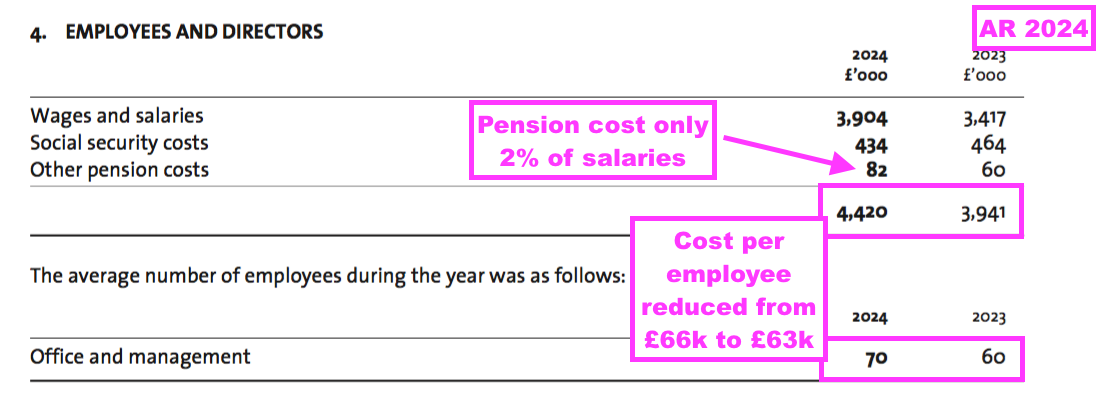

- I am pleased salaries have been kept under control, with this FY showing a £63k average employee cost versus a £66k average during the comparable FY:

- Keeping a lid on employee costs are pension contributions equivalent to just 2% of total salaries. I note share-based payments — despite the aforementioned 3%-plus dilution potential — were deemed to be “immaterial” for the ninth consecutive FY:

“The fair value of share-based payment awards granted is recognised as an employee expense with a corresponding increase in equity, over the period that the employees become unconditionally entitled to the awards. The fair value of the options granted is measured using the Black-Scholes pricing model, taking into account the terms and conditions upon which the options were granted…The share based payment vested in the year and the charge was immaterial.”

- Headcount increased by ten during this FY to 70:

- Revenue per employee was more than £280k for FYs 2010, 2011 and 2012, but was £173k for FY 2015 and £154k during both this FY and the comparable FY.

- Two key years for employee productivity were:

- FY 2015, during which WINK recruited extra personnel to handle i) client referrals within the network, and; ii) businesses looking to relocate executives, and;

- FY 2019, during which WINK commenced its company-owned office strategy through the purchase of Tooting.

- The company-owned offices in particular have diluted WINK’s revenue per employee. When Tooting’s revenue surpassed £1.6m during the buoyant FYs of 2021 and 2022 for example, Tooting’s revenue per employee reached only £160k.

Financials: cash flow and balance sheet

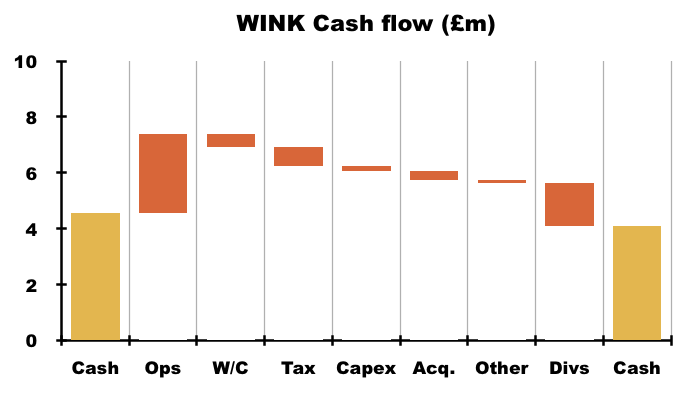

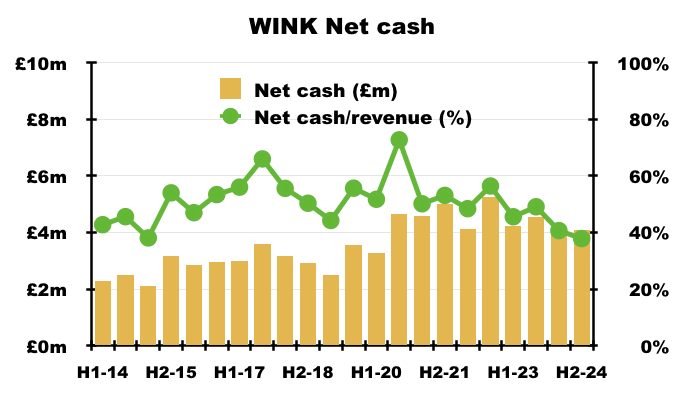

- Cash generation seemed slightly better than January’s Q4 2024 update had projected. The Q4 update said this FY would show net cash of “at least £3.9m“, and net cash was in fact £4.09m.

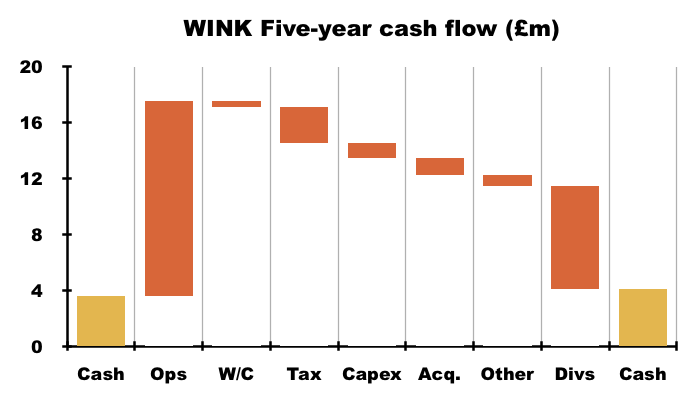

- Reported FY earnings of £1.76m translated into FY free cash flow of only £1.36m.

- The modest FY cash conversion was due primarily to:

- An adverse £469k working-capital movement, and

- Cash tax payments exceeding the associated accounting charge by £108k:

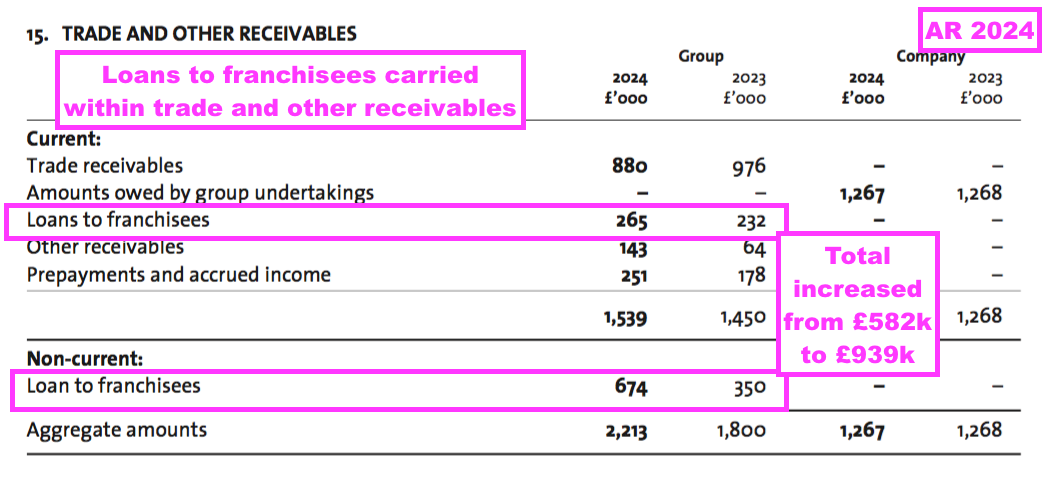

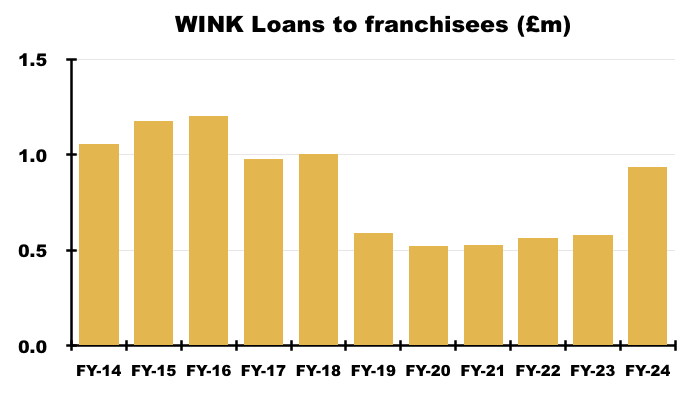

- WINK’s working capital includes loans to franchisees, which during this FY increased by £357k to £939k:

- This FY’s adverse working-capital movement was therefore due mostly to WINK issuing more loans to franchisees, rather than franchisees becoming slower to pay WINK their 8% service fees.

- I am still not sure whether greater loans to franchisees are good or bad. They may signal greater expansion potential ahead…or they could mean franchisees are now more likely to be tight for cash through a lack of prior success:

- FY free cash flow at £1.36m less £1.55m paid as dividends less £330k paid for ‘assisted acquisitions support’ plus £56k from the sale of some investments then left FY cash £463k lighter at £4.09m (31p per share).

- Over five years, WINK’s cash generation has been very satisfactory. A total £14.0m operating cash flow has funded additional working-capital, tax, capex and lease costs of £4.8m to allow bumper dividend payments of £7.4m, ‘acquisitions support’ payments of £1.2m and net cash to advance by £0.6m:

- Cash has consistently topped £4m since FY 2020 and remains reassuringly significant at 38% of trailing twelve-month revenue:

- WINK’s balance sheet remains free of bank debt and defined-benefit pension obligations.

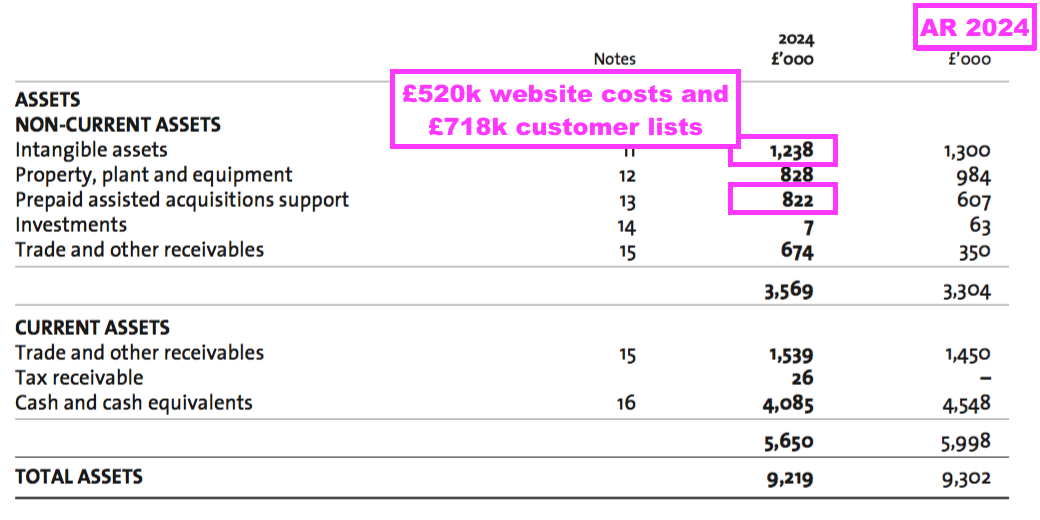

- Intangible balance-sheet items consist of capitalised website costs (£520k), the aforementioned ‘customer lists’ acquired with Tooting, Crystal Palace and Pimlico (£718k) and ‘assisted acquisitions support’ (£822k), all of which has still to be amortised through the income statement:

- ‘Assisted acquisitions support’ are ‘goodwill’-like sums paid by WINK to assist franchisees:

- Convert their existing agencies into WINK franchises;

- (The FY 2021 webinar talked of WINK paying four years’ worth of 8% commission to a suitable independent agent to convert into a WINK franchisee).

- Launch new WINK franchises in neighbouring locations, and/or;

- Acquire additional businesses (typically lettings portfolios).

- (The FY 2022 webinar talked of WINK paying three times 8% of the revenue from a target lettings portfolio on behalf of a franchisee).

- Convert their existing agencies into WINK franchises;

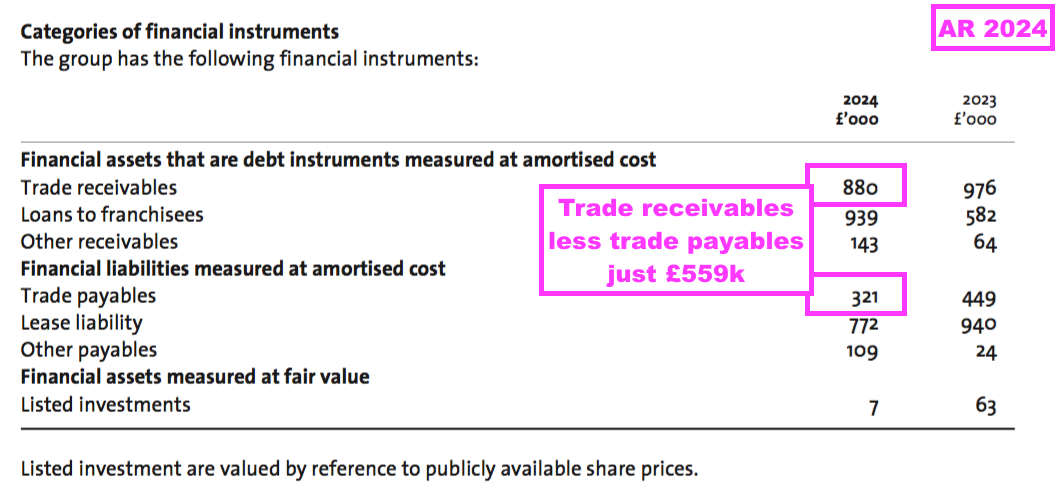

- WINK’s intangibles add up to £2.1m, and compare to the modest £559k net trade working-capital position…

- …as well as office and computer equipment that sport an £104k book value.

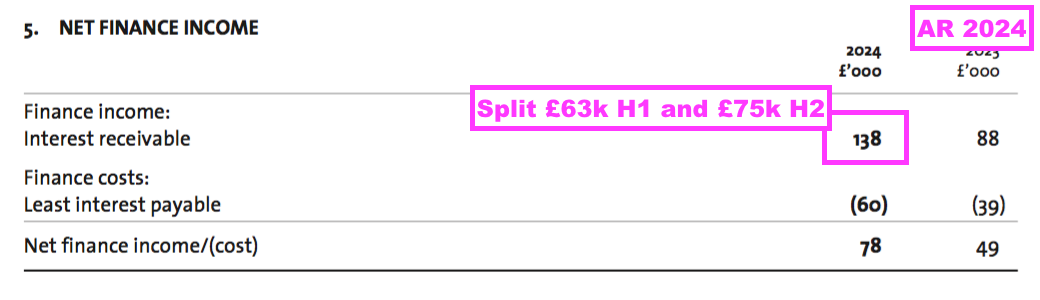

- FY finance income of £138k implied a 2.7% annualised return from the £4.3m average FY cash position and the £761k average FY loans to franchisees:

- WINK’s finance income improved from H1 to H2 — £63k versus £75k — which could mean interest on the cash and loans is running at approximately 3%.

- But 3% does not seem high, especially given the preceding H1 webinar confirmed loans to franchisees were paying interest to WINK “above base” and £1m was on “long-term deposit“:

[H1 2024] “The franchisee loans are above base rate with a minor exception, and we have £1m on long-term deposit at the moment. It’s an area that we’re looking at to improve returns constantly.“

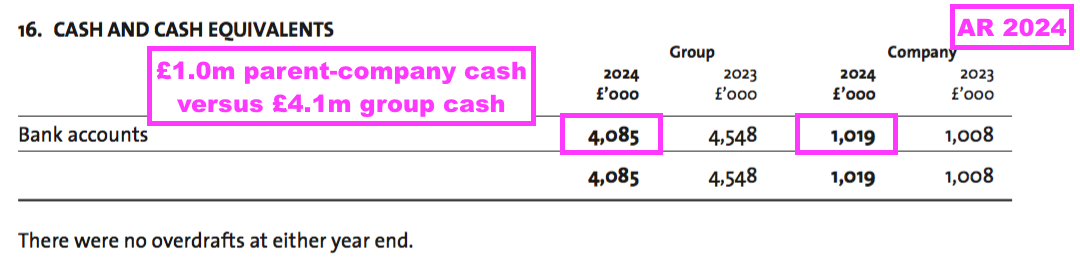

- Note that this FY’s parent-company accounts showed cash at £1m, which may reflect the £1m on “long-term deposit” and the portion of cash that is truly surplus to daily operational requirements:

- This FY claimed extra interest of £10k could have been collected had interest rates been 0.25% higher:

“Floating rate financial assets of £4,085,248 (2023 – £4,547,138) comprise sterling cash deposits. There are no fixed rate financial assets. If interest rates had been 0.25% higher during the year, then the group would have generated c£10,000 of additional interest income.”

- An extra 10k from an extra 0.25% interest implies WINK’s interest rate was 3.45% to generate the actual FY £138k interest.

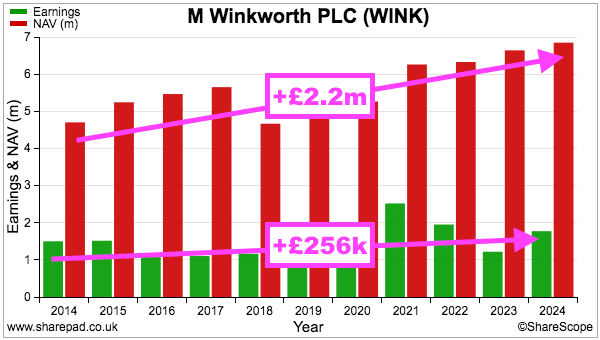

- Despite WINK’s low returns on its hefty cash position, retained earnings over time have delivered a useful incremental profit.

- During the last ten years for instance, net asset value has advanced by £2.2m to deliver additional earnings of £256k — an incremental return of 12%:

Valuation

- This FY said FY 2025 had started well for sales:

“We see the rejuvenated sales market remaining firm in 2025 and into 2026, with a needs-driven property market leading to greater activity and more properties becoming available as households re-align their sights and adjust to higher taxation and inflationary costs. We see a broadly balanced picture between buyers and sellers in 2025 and so anticipate that price increases of around 3% will be in line with the general rate of inflation. We expect activity to be heightened in London as a return to the office motivates buyers to seek properties there.“

- The FY outlook for lettings was less straightforward:

“With the renters rights bill coming into statute we envisage that some landlords, already burdened with losing part of the mortgage interest tax relief and higher costs of finance, will not wish to continue to hold their investments. However, with affordability ceilings having in many cases been reached, we do not expect further rapid rises in rents but rather a reversion to these tracking wage inflation, as prospective tenants avoid entering the market or change location to reduce their costs.”

- Perhaps contradicting the aforementioned board remarks at the 2025 AGM, the FY lettings commentary suggested franchisees could acquire further rental portfolios:

“With these changes we see an opportunity to continue to grow our lettings portfolios as landlords look for greater guidance in the face of tighter regulation. With weaker repossession rights, the need for higher quality tenants will mean that more private landlords will look to use agents. Additionally, increased regulation will push more independent letting agencies to exit the business, generating opportunities for our supported acquisition programme which provides funding to franchisees that wish to acquire portfolios to bolster their business.”

- This month’s Q2 2025 update reiterated the positive H1 for sales…

[Q2 2025] “As anticipated, an uptick in the sales market in H1 2025 helped Winkworth deliver a strong performance, with preliminary results showing an increase in network sales revenue of approximately 25% on H1 2024, with a particularly strong month of March. While Q1 2025 sales benefited from an acceleration of activity prior to the reduction in the stamp duty exemption threshold for first time buyers as of April 2025, interest remained buoyant in Q2 2025.

- …and described slower progress for lettings:

[Q2 2025] “As a counterbalance to this, lettings activity was more subdued, with network management and letting revenue up by approximately 3% over the period.”

- The Q2 update also confirmed further changes to the branch network…

[Q2 2025] “In the first half of the year the Company opened three new offices and resold two franchises.“

- ..and indicated FY 2025 pre-tax profit should advance £236k or 10% to £2.6m:

[Q2 2025] “The Directors expect pre-tax profits for the year to 31 December 2025 to be in line with market expectations of £2.6 million“.

- FY 2025 pre-tax profit of £2.6m compares to £2.5m for (pandemic-boosted) FY 2022, £3.2m for (pandemic-boosted) FY 2021, £1.5m for (pandemic-blighted) FY 2020 and £1.6m for (pre-pandemic) FY 2019.

- £2.6m after standard 25% UK tax gives earnings of almost £2.0m or 15.1p per share.

- Earnings of 15.1p per share ought to support further quarterly dividends of 3.3p per share and supply an FY 2025 payout of at least 13.2p per share:

- Earnings at 15.1p per share and a total annual payout of 13.2p per share lead to dividend cover of 1.14x.

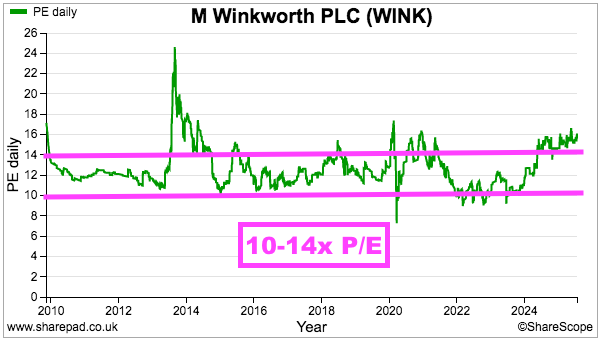

- Dividing the 208p share price by my 15.1p per share earnings guess gives a P/E of 13-14x.

- A possible multiple of 13-14x is not outrageous, but is at the top end of WINK’s typical trailing P/E range of 10x-14x:

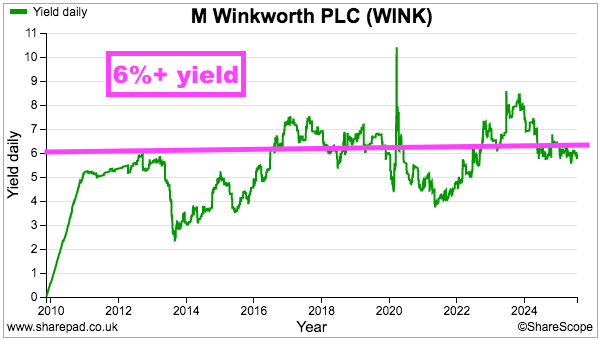

- The 12.9p per share trailing twelve-month dividend meanwhile supports a useful — but not entirely unusual — 6.2% income:

- While new openings and revitalised branches could underpin near-term progress, longer-term earnings growth may well require a fundamental improvement to transaction activity within the London property market.

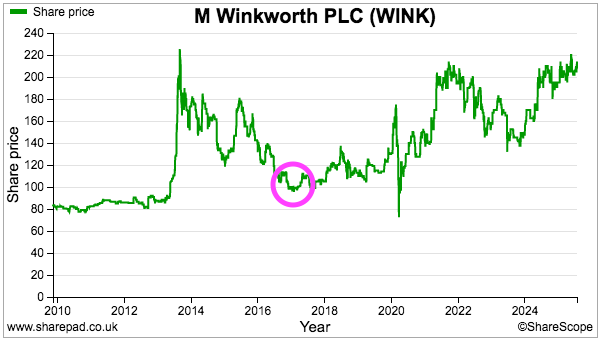

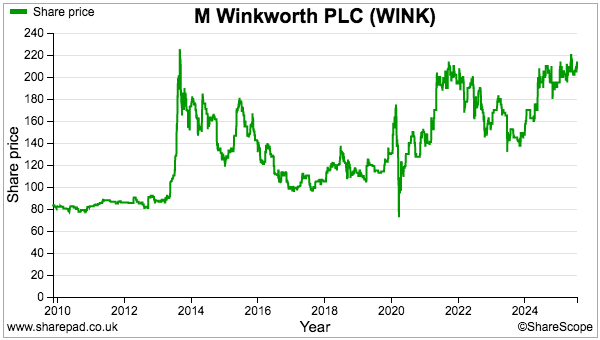

- I first bought WINK during 2011 at 90p and the shares have since delivered a very generous income. Total dividends (ordinary and special) plus a return of capital throughout the last 14 years have totalled 129p per share to recoup my entire initial investment.

- Add on the 118p per share capital gain during the same 14 years to my income, and that initial 90p purchase has returned an approximate 10% CAGR:

- A 10% CAGR is acceptable but not incredible, and the risks for long-term shareholders hoping for more include:

- Transaction volumes within London (and nationally) continuing to stagnate;

- Industry ‘growth’ faltering as an increasingly fragile economy diminishes property valuations and rental affordability;

- Further branch closures, as less talented franchisees fail to sustain the necessary top-three local position;

- Heightened competition forcing competent franchisees to cut their own commissions to remain competitive, which in turn reduces WINK’s 8% service-fee income, and;

- The board’s desire for dividends and notable net cash, leading to only modest investments in potentially lucrative new opportunities.

Maynard Paton