17 June 2025

By Maynard Paton

H1 2025 results summary for System1 (SYS1):

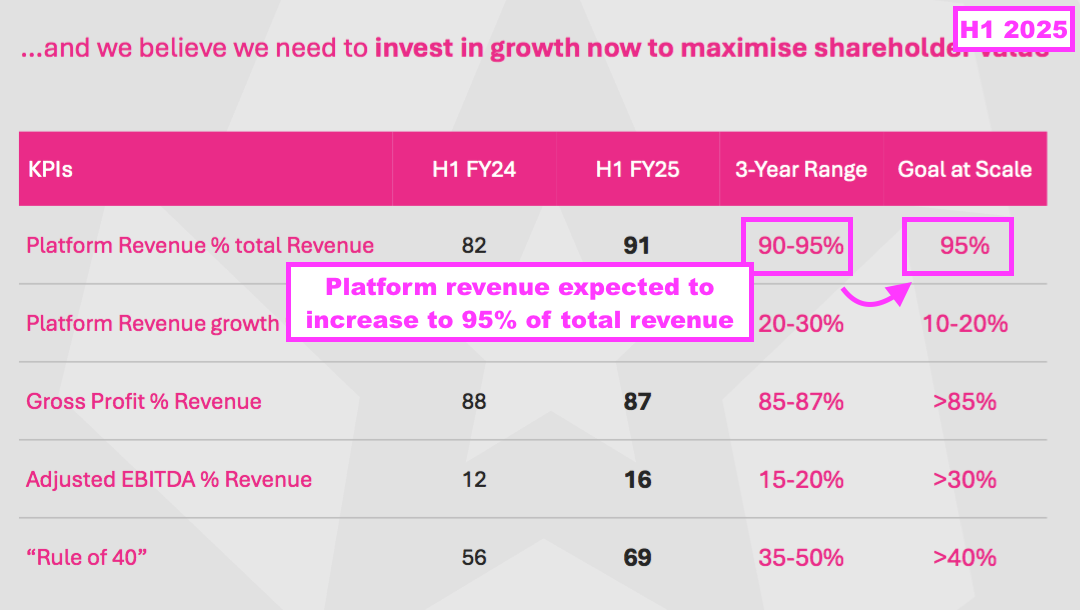

- A record H1 for both revenue and profit, after Test Your Ad income gained 53%, the gross margin once again exceeded its 85% target and employee productivity reached a £229k high.

- News of a £2m “additional discretionary investment” led to an upgraded “illustrative growth scenario“, whereby a tantalising 20-30% platform-revenue CAGR ambition could now apparently lead to a “longer term” £36m Ebitda.

- But the £2m “discretionary” investment actually appears mandatory, given the lack of obvious ‘fame building’ options for Test Your Innovation and a startling admission of needing to further “professionalise” the workforce.

- Although January’s Q3 update raised FY 2025 profit guidance, April’s Q4 update revealed a sudden sensitivity to the global economy alongside ominous revenue performances from Test Your Ad, the United States and ‘data-led’ consultancy.

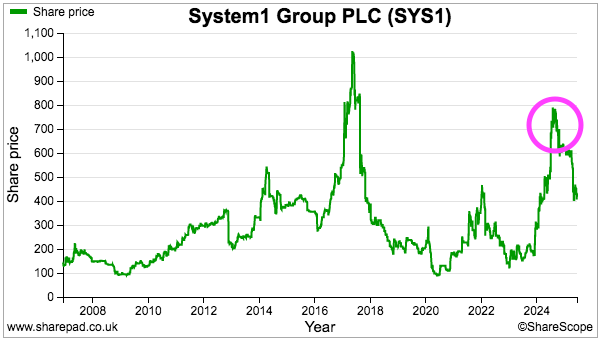

- The shares trade on an estimated 15x P/E, which seems to adequately reflect SYS1’s anticipated “strong revenue growth” for FY 2026 mixed with a greater “downside risk” to client budgets. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue, profit and dividend

- Strategic review and ‘predictiveness’

- Platform versus non-platform

- Ad testing, innovation testing and brand tracking

- ‘Fame building’ and partnerships

- 3 Reasons to Believe: Innovation

- 3 Reasons to Believe: United States

- 3 Reasons to Believe: world’s largest advertisers

- Employee productivity and remuneration

- Financials: margins

- Financials: cash flow and balance sheet

- Additional discretionary investment and illustrative growth scenarios

- Q3 and Q4 2025 trading statements

- LTIP

- Valuation

News links, share data and disclosure

- Interim results, presentation and webinar for the six months to 30 September 2024 published/hosted 03 December 2024;

- Management investor-group Q&A hosted 06 December 2024;

- Q3 2025 trading update published 21 January 2025;

- Q4 2025 trading update published 23 April 2025, and;

- Establishment of New Long-Term Incentive Plan published 14 May 2025.

- Share price: 425p

- Share count: 12,689,073

- Market capitalisation: £54m

- Disclosure: Maynard owns shares in System1. This blog post contains ShareScope affiliate links.

Why I own SYS1

- Research specialist that forecasts the success of television and digital adverts, with progress resting upon a “unique selling proposition of predictiveness” backed by 25 years of behavioural-science research delivered through a “world-class” product suite.

- Transition from bespoke consultancy to automated ‘platform’ services has created a more attractive business underpinned by superior revenue growth, greater employee productivity, improving margins and healthy net cash.

- Ambitious LTIP targets plus a tantalising “illustrative growth scenario” might signal multi-bagger possibilities should revenue progress be maximised through ‘innovation testing’, the United States and multinational customers.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Revenue, profit and dividend

- Upbeat commentary within July’s Q1 statement…

[Q1 2025] “Total Q1 FY25 Revenue of £9.5m was 53% higher than the equivalent quarter last year, with Platform Revenue growing by 74% to £8.6m and non-platform consultancy falling by 30%, in line with our expectations, to £0.9m. Growth in Revenue was driven mainly by the US where US Total Revenue rose by 94% to £3.3m and US Platform Revenue by 164% to £2.9m.”

- …followed by favourable commentary within October’s Q2 statement…

[Q2 2025] “Platform Revenue in H1 FY25 increased by 53% versus H1 FY24 to £16.7m with data sales 48% and data-led consultancy 76% higher.

Total H1 FY25 Revenue of £18.3m was 38% above the same period last year, including the impact of a £0.7m reduction in non-platform business. Growth in Revenue was driven mainly by the US where Platform Revenue was more than double H1 FY24

- …had already confirmed this H1 would be positive.

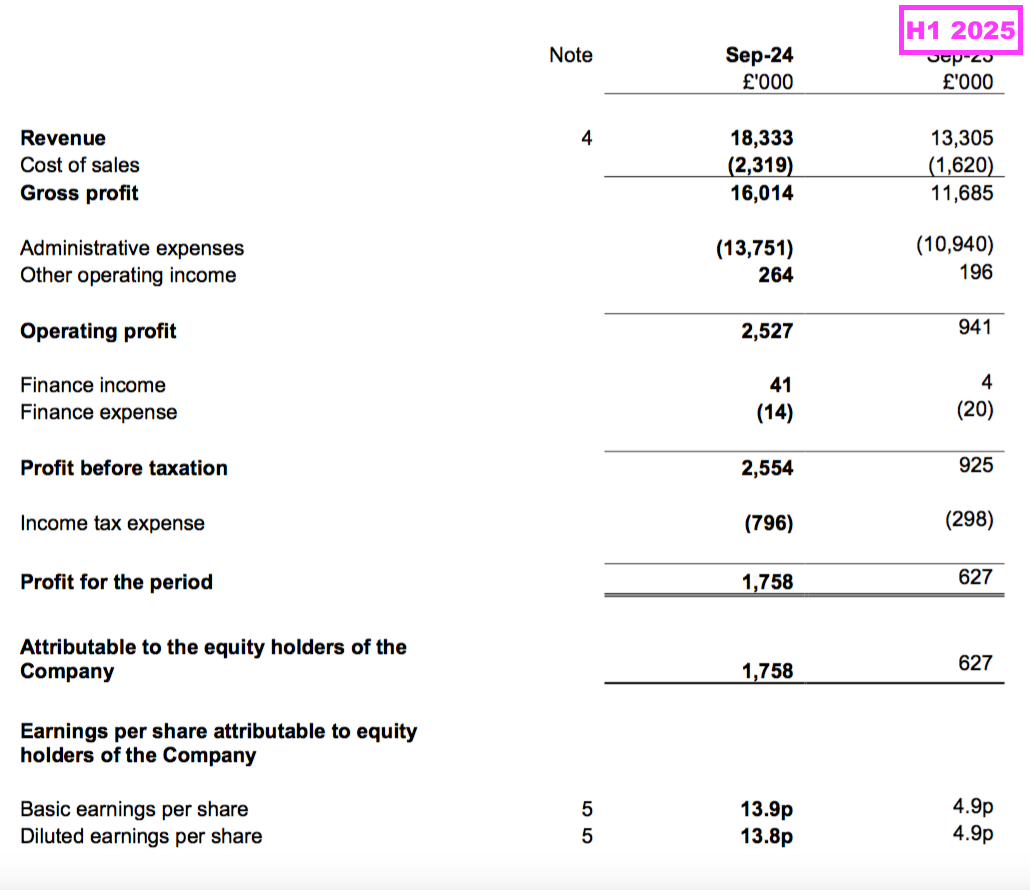

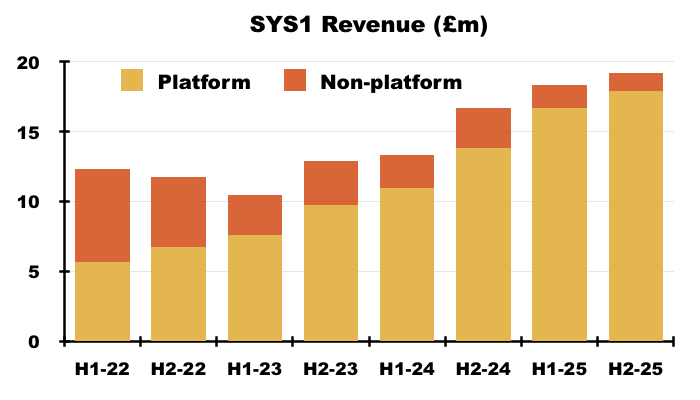

- As per October’s Q2 statement, H1 platform revenue did increase 53% to £16.7m and total H1 revenue did increase 38% to £18.3m.

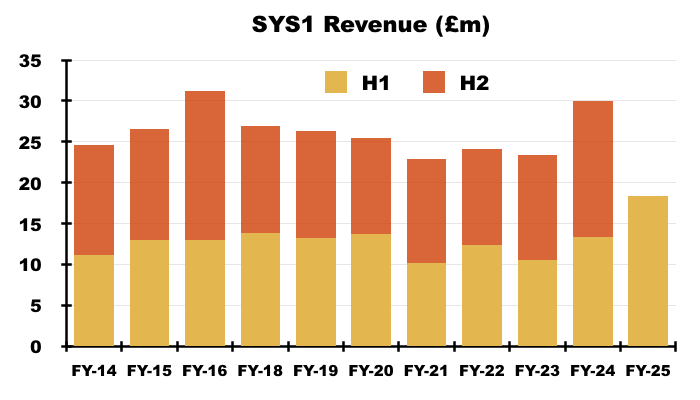

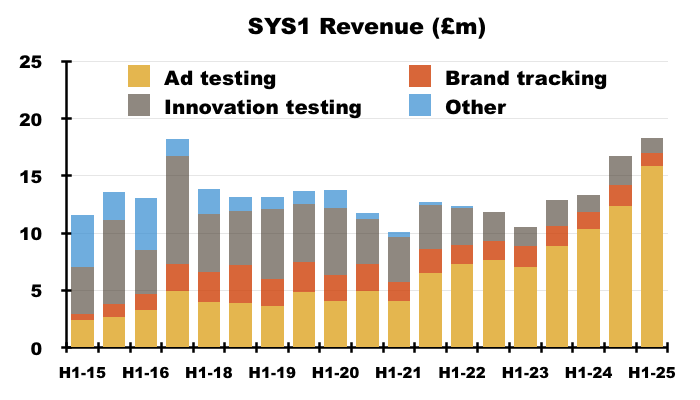

- H1 revenue at £18.3m in fact set a new record for any H1 or H2:

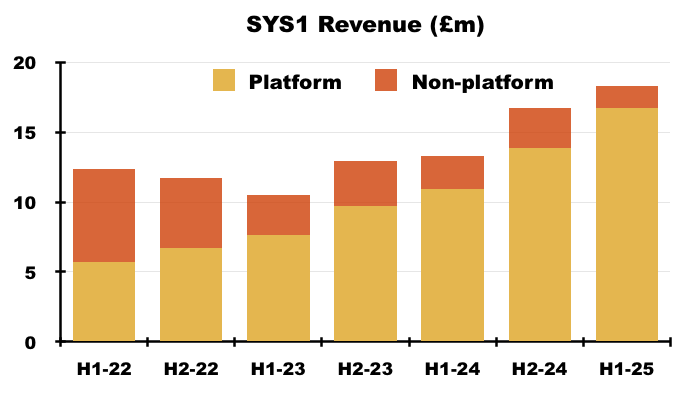

- Progress was underpinned entirely by the 53% H1 improvement to platform revenue, which now supports 91% of total revenue. This H1’s non-platform bespoke-consultancy income meanwhile fell 31% (see Platform versus non-platform):

- This H1 also delivered all the H1 profit and cash projections contained within October’s Q2 statement:

[Q2 2025] “Gross Profit in H1 FY25 reached £16.0m at a margin of 87.3% (H1 FY24: £11.7m at 87.8% margin). Operating expenditure increased by £2.6m (+23% on H1 FY24), due to increased investment in people, product and marketing to fuel the next phase of growth.

Based on the unaudited management accounts, the Group expects to report a Statutory Pre-Tax Profit of ca £2.5 million for the half-year including a £0.1m credit to share-based payments (H1 FY24: £0.9m).

Free cashflow in H1 was in line with our plan, with an outflow of £0.3m, due mainly to the payment of £2.6m of FY24 performance bonuses. The reduction in the value of the US dollar and other currencies against Sterling, notably in September, reduced the converted value of non-Sterling bank balances by £0.4m compared to 31 March 2024 and, combined with the free cash outflow, resulted in a 30 September 2024 cash balance of £8.9m (31 March 2024: £9.6m; 30 September 2023: £6.3m).”

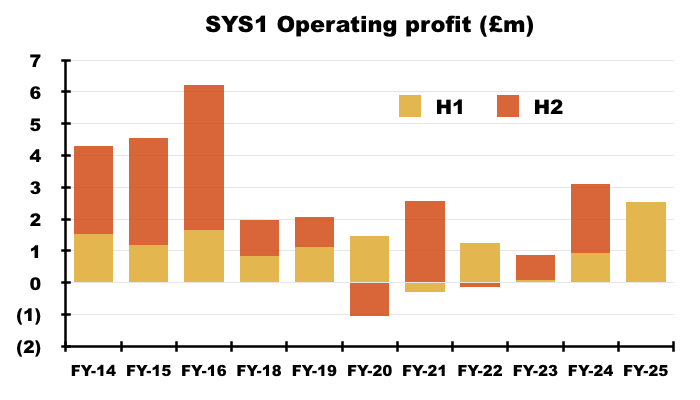

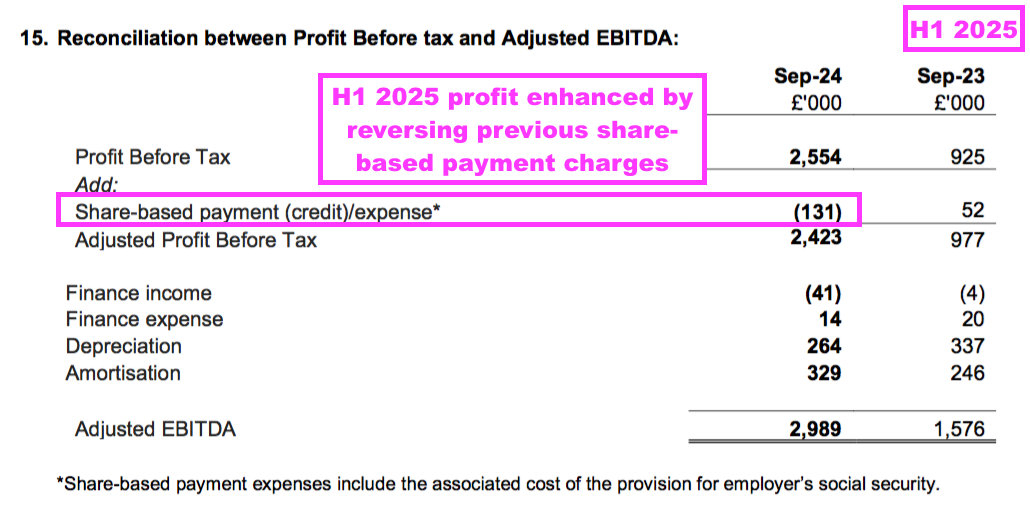

- This H1’s reported £2.5m operating profit set a new H1 record and was almost £1.6m greater than the level reported for the comparable H1:

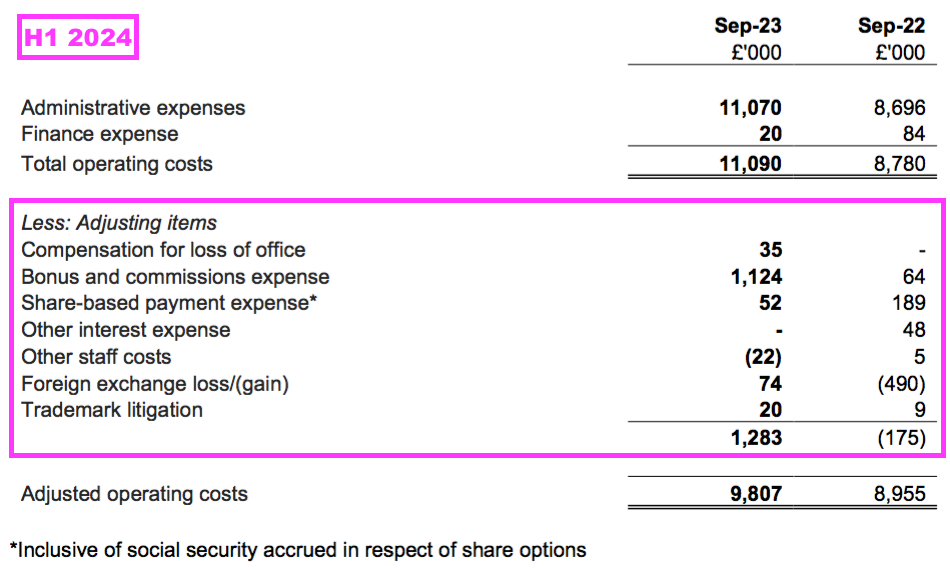

- Note that the comparable H1 (and the H1 before that) had originally featured an array of adjusting items:

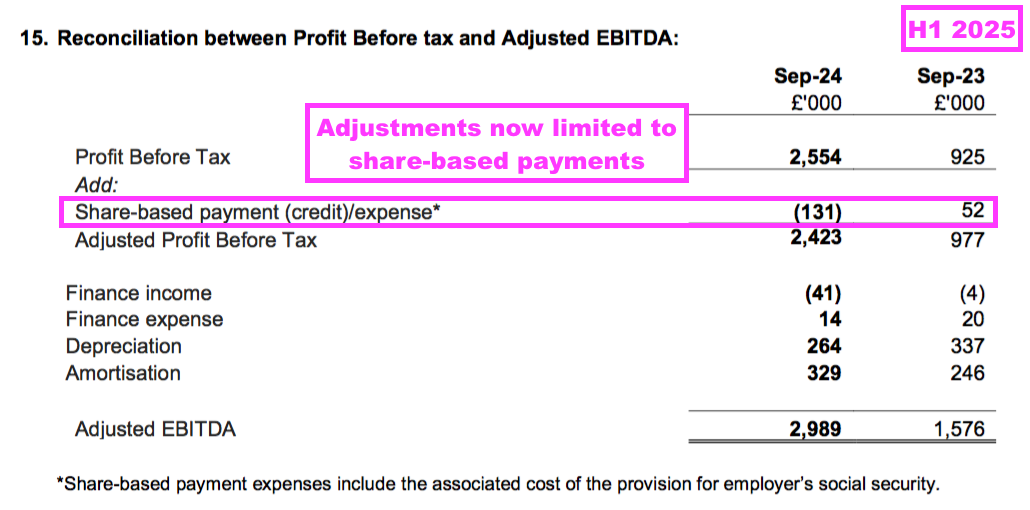

- But the preceding FY had thankfully limited adjusting items to only share-based payments, and that limitation continued for this H1:

- This H1’s reported operating profit was enhanced by:

- A £131k share-based payment credit, and;

- Other income of £264k, which I believe relates entirely to a trademark-infringement settlement (see Financials: margins).

- Unlike the preceding FY and the FY before that, this H1’s profit was not influenced by significant development costs bypassing the income statement (see Financials: cash flow and balance sheet).

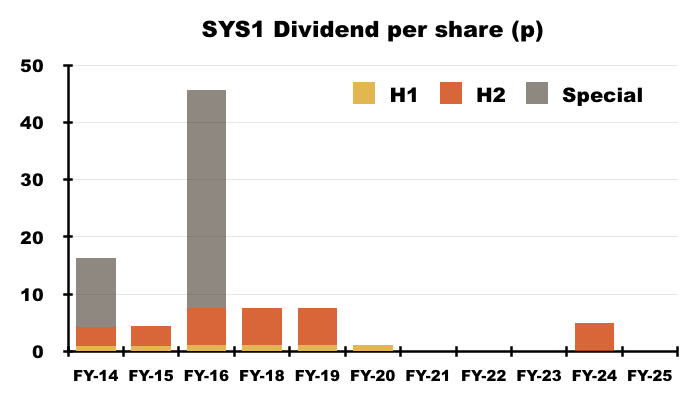

- The preceding FY announced a resumption to dividends, albeit through single annual payments…

[FY 2024] “No dividend was paid during FY24. In April 2024 the Board announced its intention to resume paying dividends, in line with the existing policy to distribute 30-40% of after-tax earnings through the cycle. At this stage the Board expect this to be through the declaration of a single ordinary dividend each year alongside the Company’s full-year results. The Board is proposing a dividend of 5.0 pence per share for FY24…“

- …and this H1 as expected did not propose a payout:

Strategic review and ‘predictiveness’

- This H1 repeated the ‘3 Reasons to Believe’ first disclosed during the 2024 Capital Markets Day:

- These ‘3 Reasons to Believe’ reflect a trio of major revenue opportunities:

- Test Your Innovation (see 3 Reasons to Believe: Innovation);

- The United States (see 3 Reasons to Believe: United States), and;

- The world’s largest advertisers (see 3 Reasons to Believe: world’s largest advertisers).

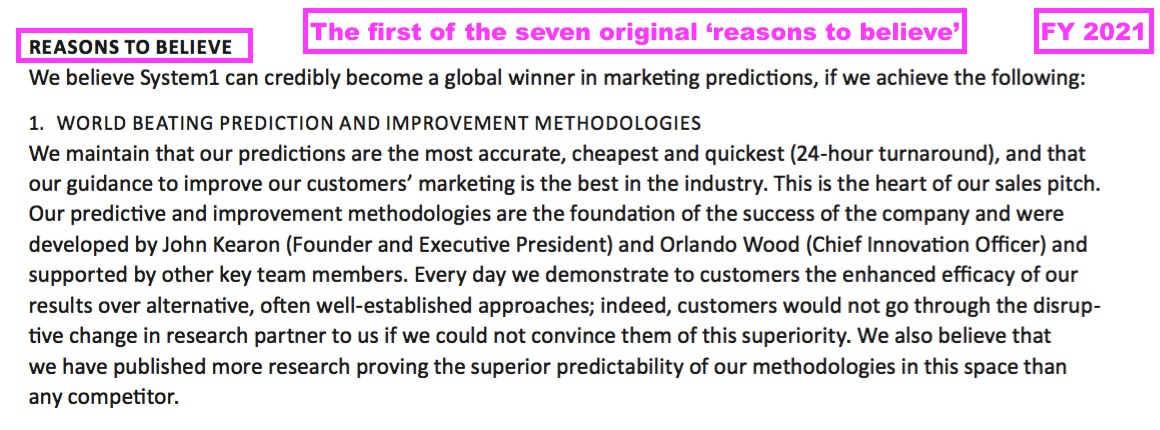

- The ‘3 Reasons to Believe’ follow the seven ‘Reasons to Believe’ declared within FY 2021…

- That strategic review concluded SYS1 should focus on:

- The group’s “unique selling proposition [of] ‘predictiveness’“;

- Digital ads;

- The world’s largest advertisers;

- Partnerships with media groups, such as the existing tie-ups with ITV and LinkedIn;

- Partnerships with industry agencies, such as Omnicom/BBDO, and;

- The United States.

- SYS1’s “unique selling proposition [of] ‘predictiveness’“ underpins the entire investment case…

- …whereby the group’s 25 years of behavioural-science research has led to a collection of services that are said to deliver the most accurate ‘predictions’ within the marketing ‘insights’ industry.

- Past presentations have often referred to the group’s “world class” products…

- …and claimed the group understands, predicts and improves the effectiveness of corporate advertising and marketing “better than anyone“:

- This H1 implied the group retained its “unique selling proposition [of] ‘predictiveness’“:

“Despite a difficult economic environment in some key markets, and challenging conditions for media owners and advertisers, we believe System1 can continue to grow profitably by gaining market share from large incumbents that we believe have less predictive products.“

- The H1 webinar meanwhile reiterated SYS1’s “25 years of behavioural-science IP” as a competitive advantage:

“We know that 51% of advertising has no long-term impact on market share growth. We know that 95% of new product launches fail. There are customers out there who are crying for help and we’re the only ones who can help here.”

…

“When you look across the market-research space, there are quite a few people who are in the market who can do an advert test, who can do an idea test and who can track brand. I guess what none of them can do is look at how emotion drives real-world results, be that brand growth, be that short-term sales, be that long-term profit.

There are some big brands out there who people will know, the likes of Kantar and Ipsos… and then there are smaller players out there as well. There are people who have a platform service, who might be able to say they can compete with us on offering a similar level of speed or price.

But they don’t have 25 years of behavioural science underpinning their IP that we do. So we do believe we are truly uniquely positioned in the market-research space, offering a platform and products based on true behavioural-science IP that uses emotion to underpin it.”

- The H1 webinar also reflected on the group’s AdRatings service — a “jewel in the crown” database containing SYS1’s verdict on c150k adverts — as a source of industry differentiation:

“If you look at the people who buy this [AdRatings database subscription] product, they are in our top 20 of our strategic customers because they’re the ones who truly buy into our methodology and our service offering. [The AdRatings database] also underpins everything we do from both the marketing and the thought leadership perspective. We are the only people out there in the industry who have an open database of ads, of which every one is tested

If you look at our competition, while they might test a bunch of ads they don’t provide all of their data to customers — including what the customer’s competition is doing.

Because we test every advert for every brand… when we’re going and pitching for new business we can talk not just about the business we’re pitching to but also the competition and how they compete in comparison.

What matters isn’t just the advertising you do, it’s whether it’s better than the competition because that’s what allows you to grow market share. [The AdRatings database] is always the jewel in the crown and if it can bring in money that will allow it to be self-funding, even better.”

- Management remarks during this H1’s investor-group Q&A provided further competition insight:

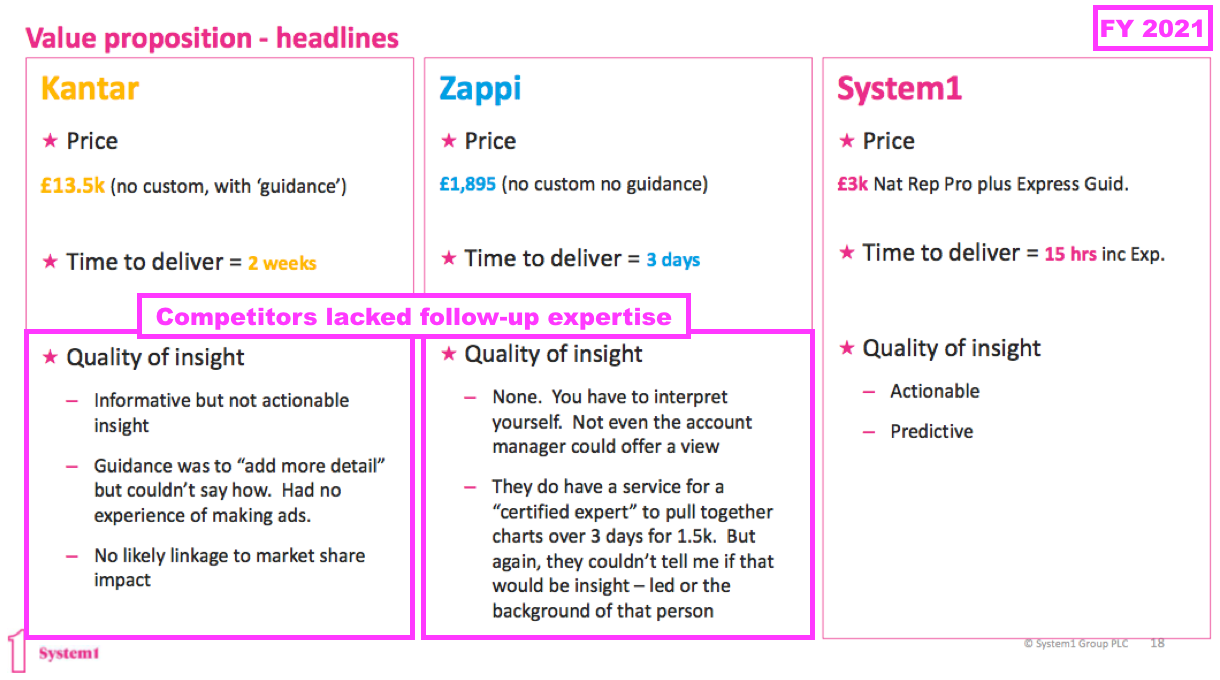

- Rivals Kantar and Ipsos “kind of offer an emotional [SYS1-like] measure“, but their services “do not fit in with what they do“. They provide “just a data point” and “there’s no link to [the anticipated] ROI, brand building and sales”.

- Lots of start-up competitors have built platforms, but “they don’t have the expertise in terms of what’s predictive yet… they will just provide the data.” SYS1 in contrast has “millions of data points” from 25 years of research to underpin the group’s superior ‘predictiveness’.

- SYS1 employs expert consultants who understand how adverts can be improved. But larger start-up rivals, including Zappi, don’t employ such consultants: “They can give you a score saying your ad isn’t very good. What do you do then? You don’t know. You need expertise as well. The big customers who stay are those who buy the tests and the consulting.”

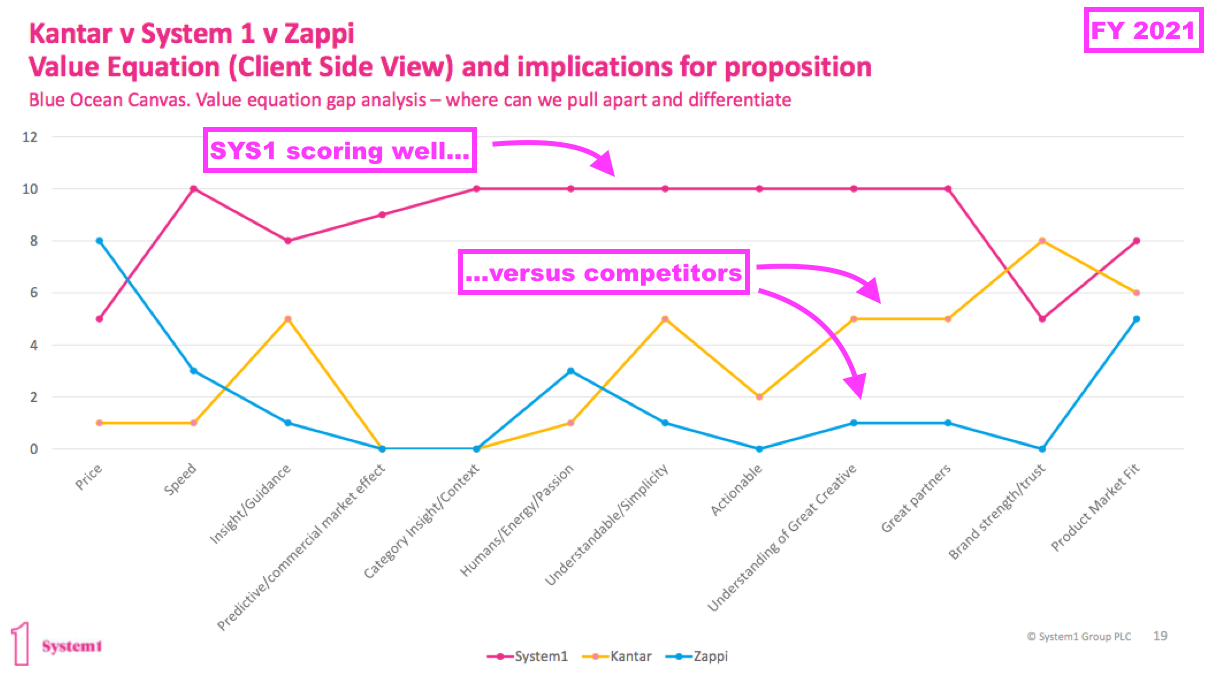

- Management remarks about Kantar and Zappi during this H1’s investor-group Q&A reflected the same conclusions about the two competitors presented during FY 2021:

- Perhaps SYS1’s best independent testimonial of late emerged from the Financial Times, which published an article last Christmas about festive adverts:

[Financial Times December 2024] “System1 asks the same question and many others, too. Over the past five years, it has come to dominate the industry. Every retail brand I spoke to for this story tests its advertising with System1.

…

Most brands use System1 while they’re still making their ads to check they’re hitting the right emotional beats. The success of Aldi’s Kevin the Carrot campaigns, which feature Kevin getting into superhero-style scrapes across the dinner table, can largely be put down to System1.”

- Among the other strategic-review initiatives, the arrangements with media groups and advertising agencies have seemingly morphed into SYS1’s general sales/marketing activities (see ‘Fame building’ and partnerships).

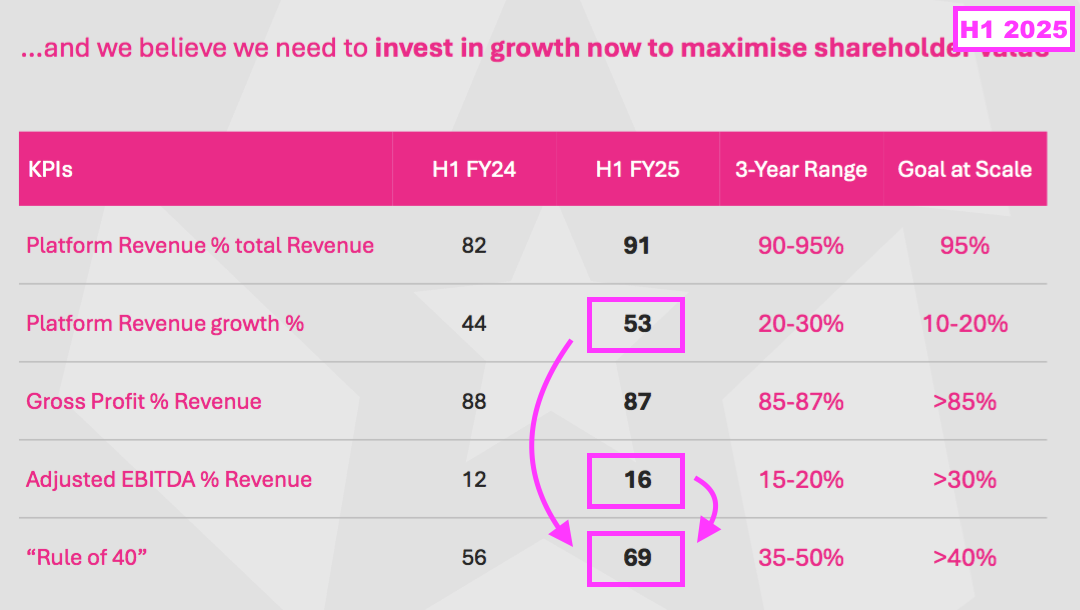

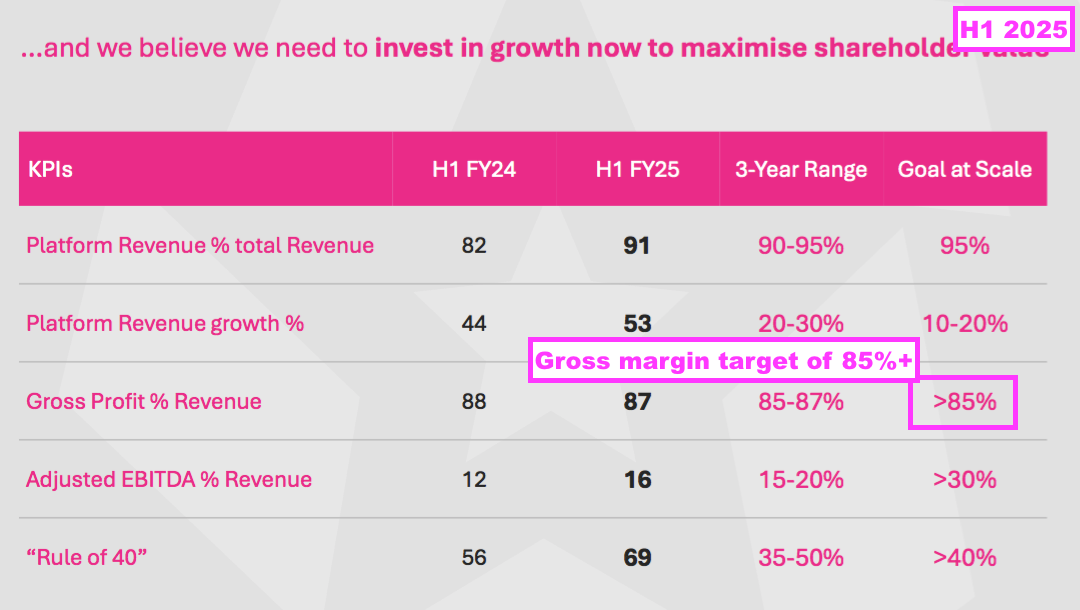

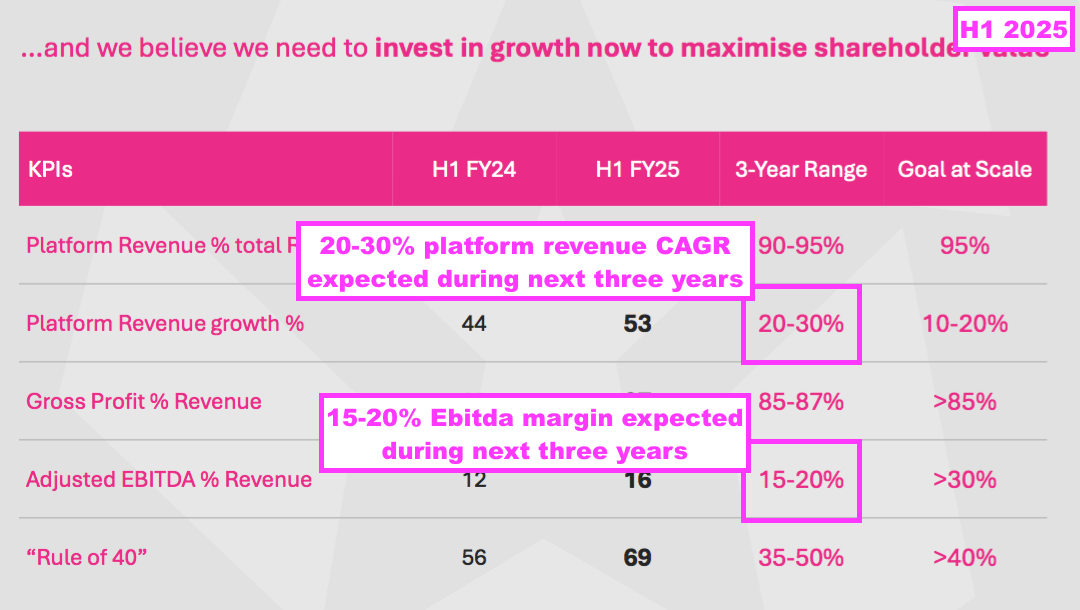

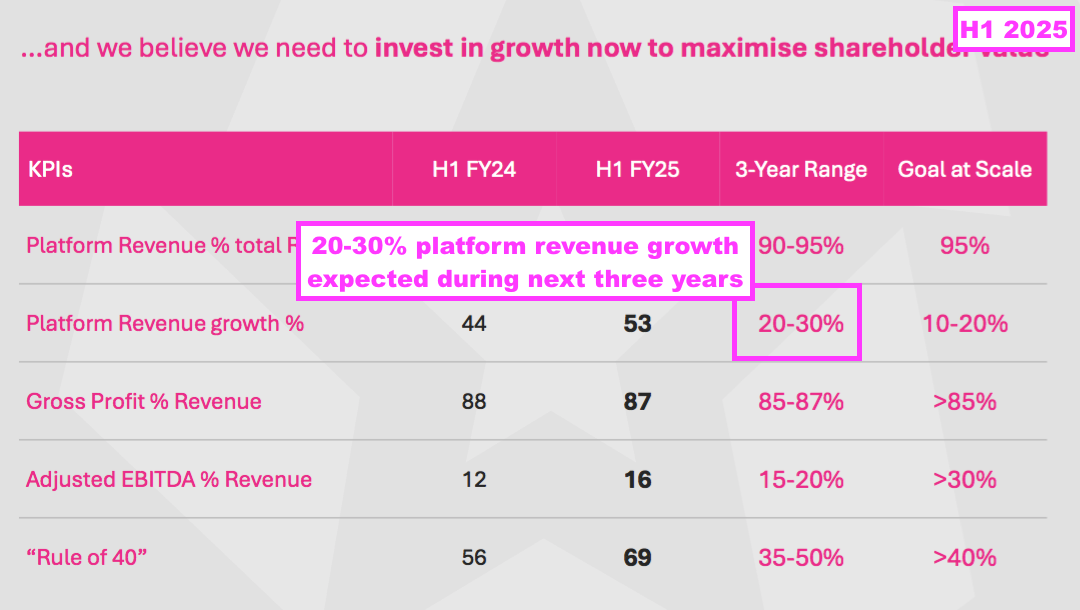

- The ‘Rule of 40’ target introduced by the strategic review was reassuringly maintained for this H1:

- The Rule of 40 measure is derived by adding platform revenue growth (H1 2025: 53%) to the total adjusted Ebitda margin (H1 2025: 16%) and aims to reach at least 40%.

- This H1’s Rule of 40 measure came to 69%, and would still have been met if SYS1 instead added total revenue growth (H1 2025: 38%) to the total adjusted Ebitda margin.

Platform versus non-platform

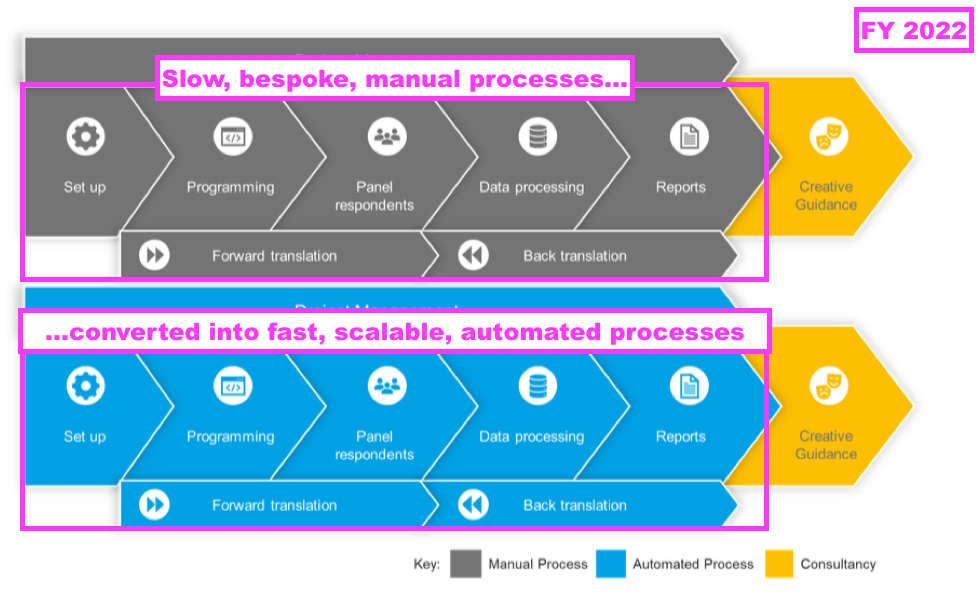

- The aforementioned AdRatings database was developed during FY 2018 and was SYS1’s first step towards selling marketing-prediction data. A difficult few years then followed as the group converted its entire bespoke-consultancy set-up into automated prediction-data services:

- H1 2022 introduced SYS1’s mission to become “the world’s marketing decision-making platform” and the strategic review subsequently validated the platform-data transition.

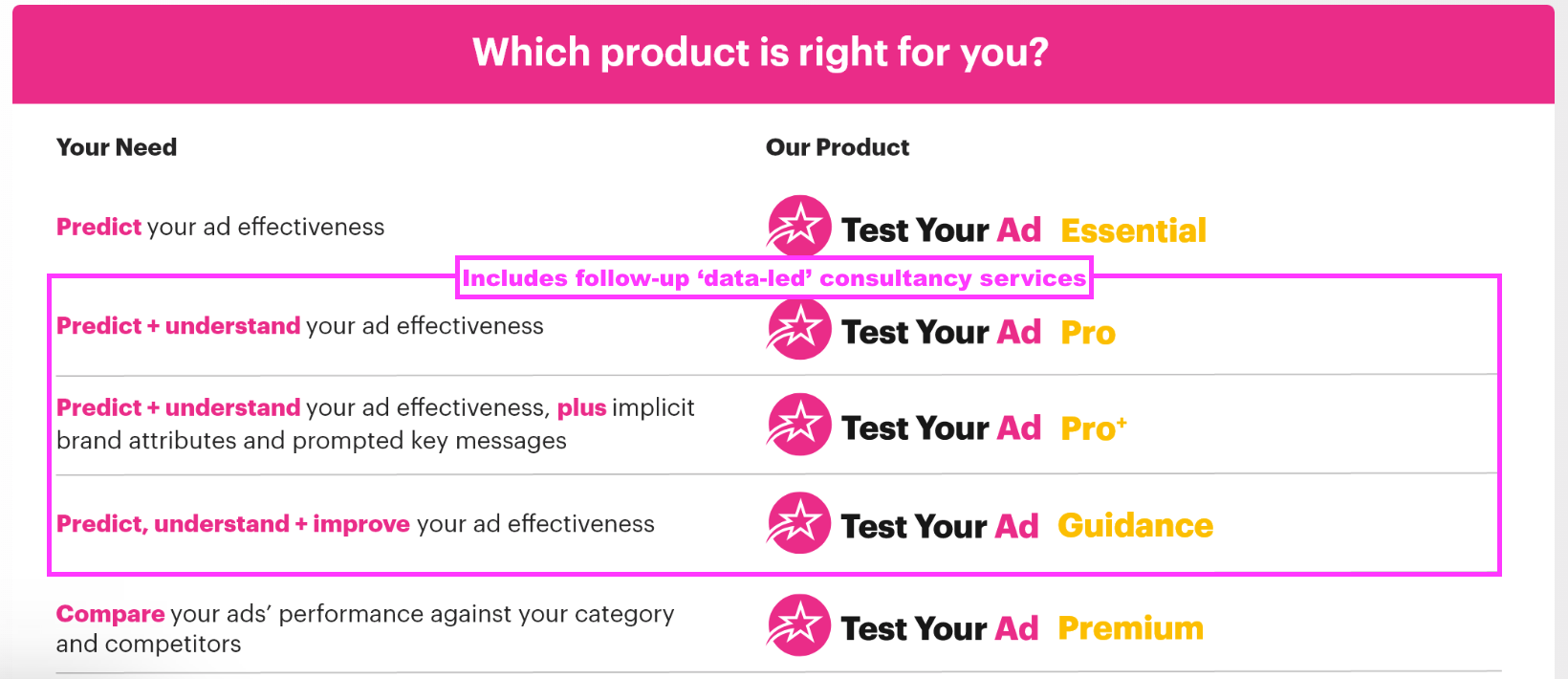

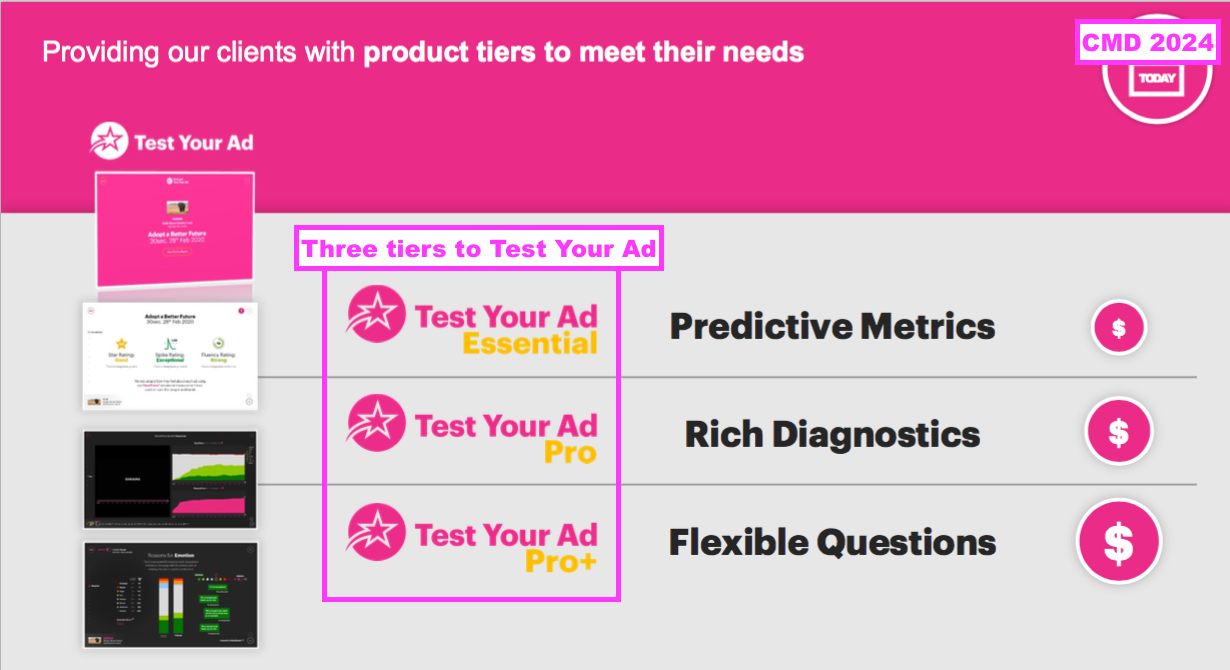

- Platform products are today led by Test Your Ad (TYA)…

- …which was launched during April 2020 and allows customers to upload proposed adverts to SYS1 and receive a report within 24 hours based upon the verdict of an online panel:

- Platform revenue is supported by Test Your Innovation (TYI) and Test Your Brand (TYB), which perform the same online-panel function for product ideas and company brands:

- TYB and TYI were launched during November 2021 and May 2022 respectively.

- Platform ‘data’ revenue is bolstered by ‘data-led’ consultancy revenue, which consists of follow-up improvements and guidance from SYS1’s marketing experts:

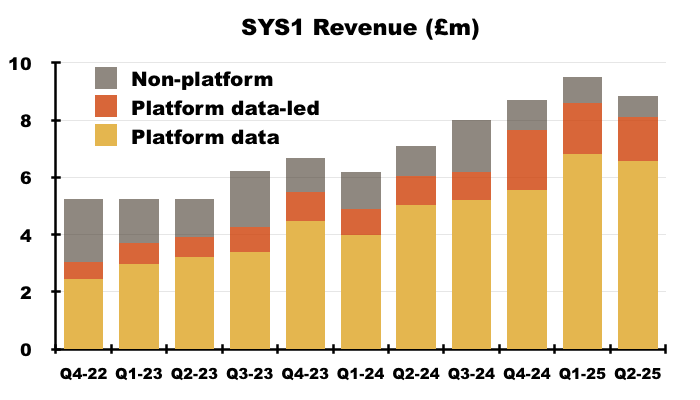

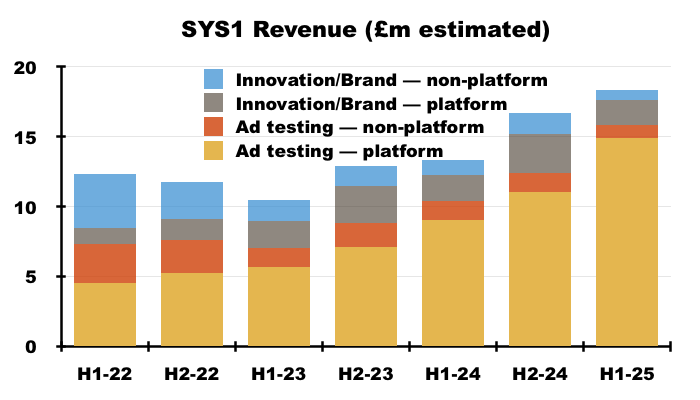

- This H1 confirmed:

- H1 platform ‘data’ revenue gained 48% to £13.4m, and;

- H1 platform ‘data-led’ revenue gained 75% to £3.3m.

- While this H1 and prior results have shown platform revenue consistently increasing since H1 2022…

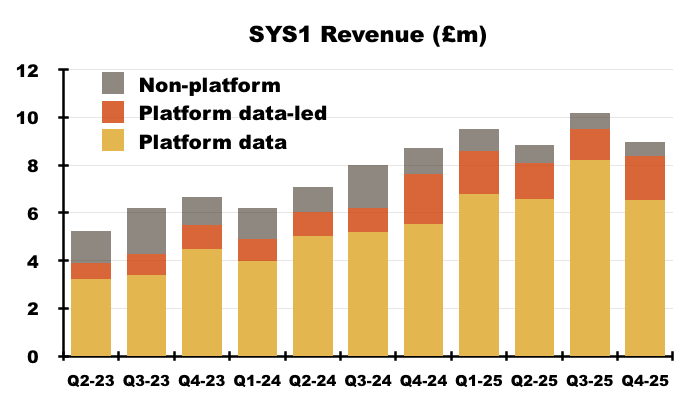

- …the group’s quarterly statements do not always show platform revenue enjoying such a smooth trajectory.

- For example, this H1’s Q2 2025 ‘data’ revenue was approximately £6.6m — £0.2m lower than the £6.8m for the preceding Q1 2025:

- In fact, ‘data’ revenue also:

- Declined during Q4 2022 versus the preceding Q3 2022, and;

- Declined during Q1 2024 versus the preceding Q4 2023…

- …before immediately rebounding to new quarterly highs on both occasions (see Q3 and Q4 2025 trading statements).

- Furthermore, Q4 2024 witnessed platform ‘data-led’ revenue of £2.1m versus the lower £1.8m and £1.5m for this H1’s Q1 and Q2.

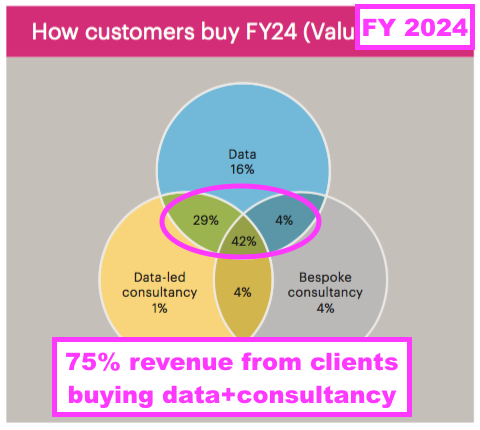

- The preceding FY included a chart that showed how revenue was split between clients who purchased ‘data’ and/or ‘data-led’ consultancy and/or non-platform consultancy:

- The chart showed that, during the preceding FY at least, most customers (75% of revenue) bought ‘data’ plus some form of consultancy.

- ‘Data-led’ revenue should therefore track ‘data’ revenue higher over time as SYS1’s customers typically accompany their ‘data’ purchases with SYS1’s follow-up guidance (see Q3 and Q4 2025 trading statements).

- This H1’s non-platform revenue fell 31% to £1.6m and represented only 9% of H1 revenue.

- The preceding FY explained how TYA Pro+ — the top-tier TYA service that supplies extra data insights — had accelerated the group’s transition from bespoke work to automated testing:

[FY 2024] “Test Your Ad Pro+ has been a game-changer as we’ve built the ability to deliver customer and project-specific customisation in a scalable manner, through the automated platform.

…

TYA Pro+…allowed us to effectively automate some features that could previously only be delivered with a complex bespoke workaround.“

- Management remarks during this H1’s investor-group Q&A included the following snippets about bespoke revenue:

- TYA Pro+ continues to convert bespoke work onto the platform;

- Winning a £1m platform contract might require an initial £50k-£100k of bespoke work;

- Bespoke revenue might in time reduce to c3% of total revenue, but will unlikely be zero within three to five years, and;

- Some long-time customers may always want to utilise bespoke consultancy.

- This H1 reconfirmed platform revenue could reach 95% of total revenue “at scale“:

Ad testing, innovation testing and brand tracking

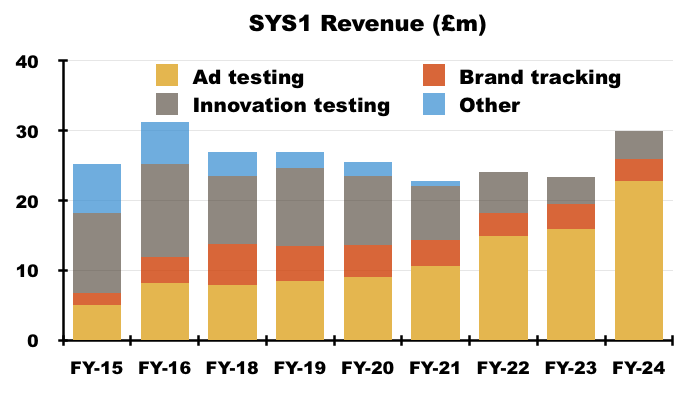

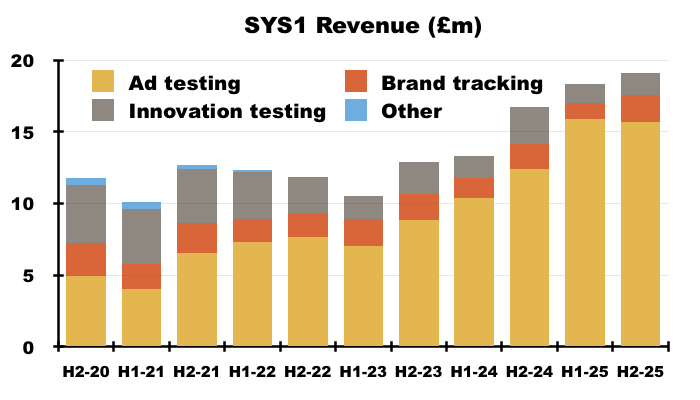

- Ad testing — via the TYA platform service and certain non-platform consultancy work — continues to dominate SYS1’s revenue:

- Ad-testing revenue supported 87% of H1 revenue versus 78% for the comparable H1 and just 20% for H1 2015.

- While H1 ad-testing revenue gained 53% to £15.9m…

- …H1 innovation-testing revenue declined 13% to £1.3m and H1 brand-tracking revenue fell 19% to £1.1m.

- Note that October’s Q2 2025 statement had described this H1’s innovation-testing and brand-tracking revenue to have been “broadly in line” with the comparable H1:

[Q2 2025] “Revenue growth in H1 derived from Ad testing (Comms), with Brand and Innovation product groups broadly in line with H1 FY24.”

- This H1 emphasised how efforts to develop and promote TYA appear to have been at the expense of enhancing TYI and TYB.

- In fact, this H1’s innovation-testing revenue was the lowest for any H1 or H2 since SYS1 began disclosing ad-testing, innovation-testing and brand-tracking revenue during H1 2015.

- This H1’s brand-tracking revenue was meanwhile the lowest for any H1 or H2 since H1 2015 (£0.6m).

- This H1 admitted a brand-tracking contract had finished while revealing TYI was “now the subject of significant and accelerated investment” (see 3 Reasons to Believe: Innovation):

“Brand was 20% down on H1 FY24 to £1.1m due to the runoff of a bespoke brand-tracking contract in the UK. The Innovation product group fell by 13% over the same period to £1.3m and is now the subject of significant and accelerated investment as we set about revitalising it.”

- This H1’s loss of a bespoke brand-tracking contract highlights how brand-tracking (and innovation-testing) could be at greater risk of further income shortfalls as the group focuses on its platform services.

- The H1 webinar helpfully disclosed 94% of H1 ad-testing revenue was conducted through the platform, which implied 72% of H1 innovation-testing and brand-tracking revenue was also conducted through the platform…

- …and which then leaves 28% of H1 innovation-testing and brand-tracking revenue exposed to bespoke consultancy.

- This H1’s lowly innovation-testing revenue was especially disappointing given the preceding FY had spotlighted the relaunch of TYI:

[FY 2024] “With our customer-centric focus, in April 2024 we have launched a new Test Your Innovation product suite to replace Test Your Idea. This repositions the previous version in a way that better suits our clients, ensuring our products neatly follow a standard product development cycle. This exciting development will help accelerate our growth in the Innovation space in the upcoming year.”

- Whereas the initial TYI platform service had involved bespoke consultancy work and assessed a limited range of product characteristics, the relaunched TYI offers five distinct automated steps…

- …and can assess a variety of different product characteristics:

- The challenge for SYS1 is to persuade prospective customers to use TYI, a task that will now take longer — and cost more! — than previously expected (see 3 Reasons to Believe: Innovation and Additional discretionary investment and illustrative growth scenarios).

- Brand-tracking still features as a sub-step of TYI and presumably is not a major component of SYS1’s growth plan.

‘Fame building’ and partnerships

- This H1 listed the following “fame building” initiatives:

“• The Extraordinary Cost of Dull research in collaboration with Peter Field and Adam Morgan was showcased on the main stage at the Cannes Festival and became the second-most downloaded report in System1 history;

• Uncensored CMO interviews with US-based leading voices, including Scott Galloway;

• The Greenprint USA and The Greenprint Brazil, a guide on how to effectively incorporate sustainability messaging in advertising

• System1 Chief Innovation Officer Orlando Wood, Sir John Hegarty and The Garage launched Advertising Principles Explained (a.p.e.), an advertising effectiveness course that will engage with System1 clients and prospects”

- The initiatives were notable for engaging particular industry individuals rather than engaging prominent media groups.

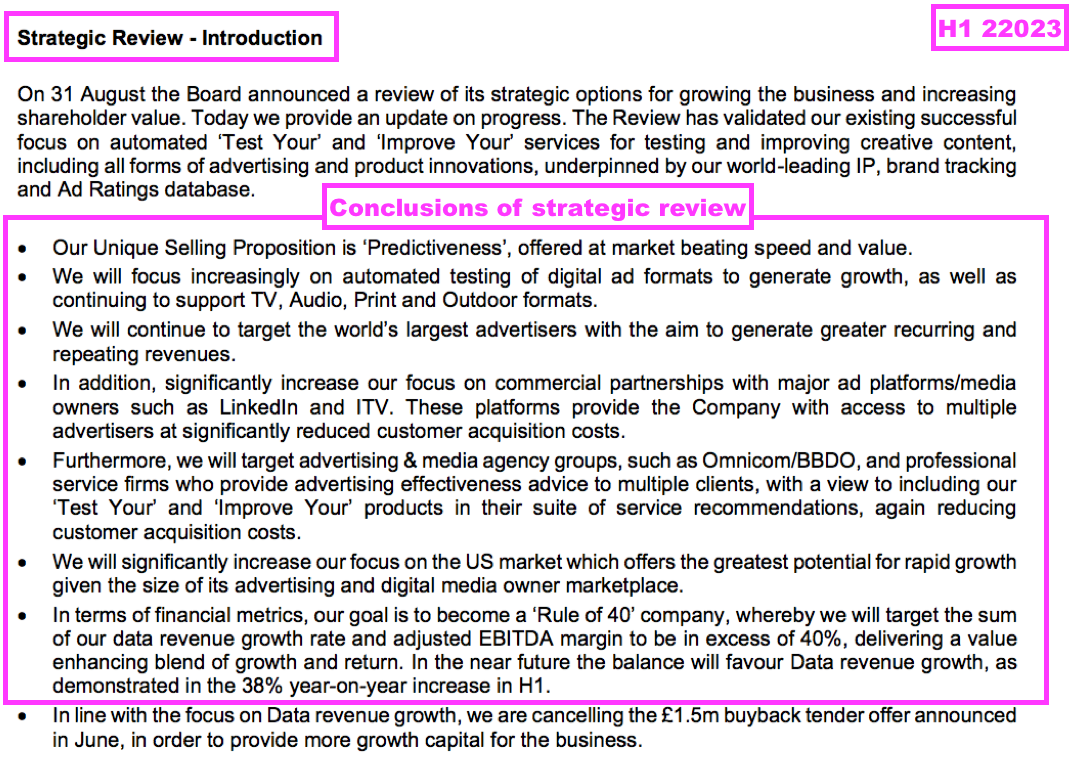

- At the time of the strategic review, SYS1 emphasised the importance of developing corporate partnerships with the likes of ITV and LinkedIn…

[H1 2023] “In addition, significantly increase our focus on commercial partnerships with major ad platforms/media owners such as LinkedIn and ITV. These platforms provide the Company with access to multiple advertisers at significantly reduced customer acquisition costs.”

- …and the group even revealed the revenue generated through such partnerships:

- Although the comparable H1 dedicated a slide to new corporate partnerships…

- …this H1 did not mention corporate partnerships at all.

- I am therefore not quite sure how corporate partnerships rank within SYS1’s promotional work, which the preceding FY listed as:

- PR;

- Events;

- Partnerships;

- “Uncensored CMO” podcasts;

- Ad of the Week articles, and;

- “Thought Leadership“.

- Corporate partnerships with ITV, LinkedIn and so on do provide industry validation of SYS1’s services and I imagine are more likely to broaden SYS1’s sector recognition — and perhaps more likely to capture new customers — than collaborations with particular individuals.

- The preceding FY mentioned impending new partnerships with with video-sharing website TikTok and marketing-effectiveness organisation Effie:

[FY 2024] “New partnerships with TikTok and Effie will be highlighted with research coming in FY25.“

- I am pleased SYS1’s presence at Cannes Lions this month spotlighted the TikTok and Effie collaborations.

- H1 platform revenue advancing 53% does suggest the ‘fame building’ — whether through corporate partnerships, prominent individuals or some other method — has proven effective at capturing industry attention.

- Mind you, I must confess I remain unsure if all of SYS1’s promotional work is truly effective.

- For example, Lemon and Look Out were written by SYS1’s chief innovation officer, Orlando Wood, to promote SYS1’s behavioural-science research:

- FY 2022 described one book as a “seminal work” and claimed the other received “widespread critical acclaim“:

[FY 2022] “We continue to be recognised for thought leadership in the industry. Following on from his earlier seminal work, Lemon, published jointly with the Institute of Practitioners in Advertising (IPA), our Chief Innovation Officer, Orlando Wood, published Look Out, to widespread critical acclaim.“

- Both books help the reader understand advertising effectiveness, albeit using very ‘System2’ lessons drawn from very highbrow sources:

- I will let you decide whether Mr Wood’s latest film — a 27m15s recap of SYS1’s behavioural-science research set within an art museum — is likely to spur greater platform revenue:

- A strategic-review ambition that has faded over time is working with advertising agencies:

[H1 2023] “Furthermore, we will target advertising & media agency groups, such as Omnicom/BBDO, and professional service firms who provide advertising effectiveness advice to multiple clients, with a view to including our ‘Test Your’ and ‘Improve Your’ products in their suite of service recommendations, again reducing customer acquisition costs.“

- Shareholders have never since been updated with this advertising-agency ambition, although management remarks during this H1’s investor-group Q&A revealed:

- Advertising-agency groups such as WPP support approximately 10% of group revenue;

- “They bring us in when it’s helpful [to their client], but they don’t always bring us in“, and;

- Sometimes the end client will use SYS1 to “check the homework” of an agency, which can lead to a “frosty reception“.

3 Reasons to Believe: Innovation

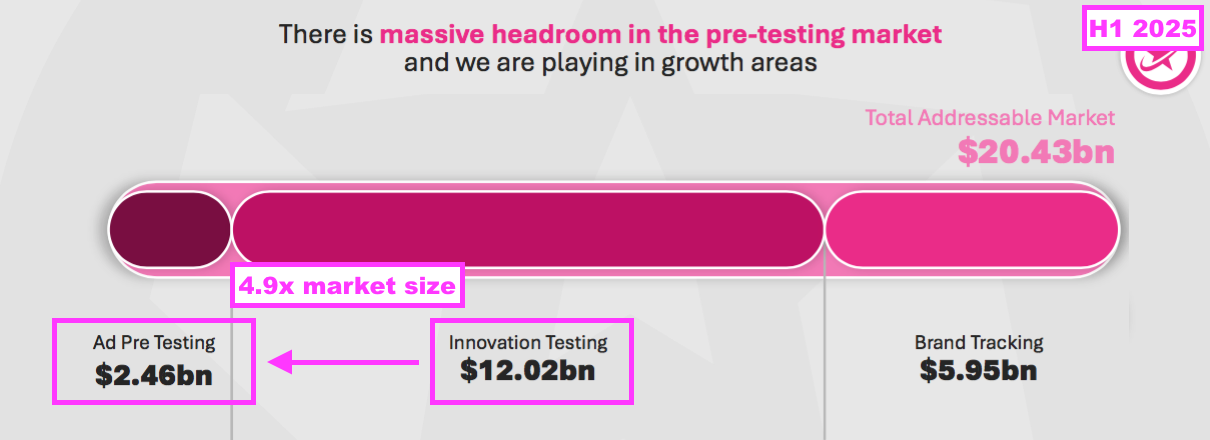

- This H1 re-emphasised the $12b size of the innovation-testing market:

- The size of the innovation-testing market is almost 5x the size of the ad-testing market, and the preceding FY encouragingly hinted a relaunched TYI could therefore become a much greater money-spinner than TYA:

[FY 2024] “The relaunch of our Test Your Innovation product suite will allow us to create a revenue stream for Innovation that could eventually become bigger than our Comms [advert-testing] revenue stream. We say this because according to ESOMAR research, the target addressable market for innovation is 4.8X that of communications at $12.02bn.“

- Innovation testing was once SYS1’s main earner, generating revenue of £13m revenue during FY 2016 versus £4m during the preceding FY:

- This H1 outlined three steps to “revitalise” TYI:

- Creating a new role of managing director for the Innovation products;

- The recruitment of extra sales, marketing and product employees to develop and support TYI, and;

- The adoption of the same ‘fame-building’ tactics used for TYA for TYI.

- Following this H1, January’s Q3 2025 statement confirmed the appointment of the new Innovation MD:

[Q3 2025] “System1 has appointed Tristan Findlay as Managing Director of Innovation. In this role on the Executive Team, Tristan will lead System1’s innovation function, driving the development and growth of solutions that help brands confidently optimise their ideas. He was previously group commercial officer and European commercial lead for AI at Toluna. Prior to Toluna, Tristan was chief growth officer at MMR Research, head of innovation practice at Zappi and began his career at Nielsen Bases.”

- The new Innovation MD appears a useful recruit, having worked previously at SYS1 panel-suppler Toluna and SYS1 competitor Zappi.

- The Innovation MD’s bio discloses an unusual insight into SYS1’s “performance culture” (see Employee productivity and remuneration):

[SYS1 website June 2025] “Not sure if fun is the right word, but being at an exec offsite on day 7 of my tenure and doing guided meditation in the middle of a wood with the rest of the executive team was certainly unexpected.”

- Management remarks during this H1’s investor-group Q&A disclosed the following snippets about Innovation:

- The new Innovation MD will have “true accountability” over the innovation-testing P&L;

- The Innovation team will comprise sales, marketing and product staff working on only TYI, and;

- In order to avoid a “separate cost base“, Innovation team members will report both to the new Innovation MD and their respective sales, marketing and product bosses.

- Management remarks during this H1’s investor-group Q&A also confirmed TYI was not subject to any further planned development work, but could in time be enhanced following client feedback.

- The H1 webinar claimed TYI was “world class” and would mimic TYA’s promotional tactics:

“We’ve created a world-class proposition and product and platform. We grow our fame through partnerships and our own channels and then we can convert new business. We need to apply that same [ad-testing] method and tactics into the innovation space, which is what we’re planning on doing.“

- The H1 webinar highlighted SYS1’s podcast as a TYI ‘fame-building’ option:

“We do have a world-class [innovation] product. What we now need to be able to do is focus on building out the thought leadership, the validations and the fame alongside it to be able to help it grow.

We can use our comms team to help. Jon Evans for example interviewed the head of innovation at Pepsi, so that’s a great opportunity where there is true overlap where we can reach the advertising audience who are also often at times the innovation audience as well through the same channels“.

- The Innovation MD has work to do to get innovation testing some podcast airtime. Since the Pepsi “innovation masterclass” published during September, I count only two episodes (177 and 181) have since mentioned innovation testing to any great degree.

- The Innovation MD will also know SYS1’s website currently lacks meaningful TYI promotion.

- SYS1’s research for example — including Break Through, Compound Creativity and The Extraordinary Cost of Dull — still focuses entirely on improving the effectiveness of adverts.

- And among the website’s 14 case studies, 12 relate to advertising and only two cover product innovation.

- At least the Innovation MD’s social-media feed refers to some early Innovation promotion.

- I am not convinced TYI will receive attention through a new SYS1 book.

- Management remarks during this H1’s investor-group Q&A were quite vague about publishing a TYI equivalent to the aforementioned Lemon or Look Out. Mr Wood could apparently “share what’s worked with advertising” for an Innovation publication, but might only “help promote it rather than be the author“.

- Probably the greatest challenge to promoting TYI is the lack of an equivalent “jewel in the crown” AdRatings database.

- AdRatings is built upon adverts that have been publicly broadcast and helps establish the aforementioned ‘fame building’ research such as Break Through, Compound Creativity and The Extraordinary Cost of Dull.

- In contrast, SYS1’s collection of innovation tests are built upon product ideas that are inherently private to clients…

- …that would prohibit becoming part of any public analysis for a SYS1 promotion.

- Innovation testing also lacks the equivalent of Christmas and the Super Bowl — two significant “cultural moments” that are renowned for adverts and help spotlight TYA every year.

- And Innovation lacks an obvious equivalent of an ITV or LinkedIn partner that may wish to promote the TYI service.

- Maybe TYI will be promoted by particular TYI clients. Management remarks during this H1’s investor-group Q&A suggested SYS1 may promote TYI by “finding the right customers” who “might want to shout about the products they’ve created“.

- Management remarks during this H1’s investor-group Q&A also claimed clients could return to TYI because the service’s “wisdom of the crowds” approach remains “quite unique” to SYS1.

- All told, I do worry TYI will be fundamentally more difficult to promote than TYA…

- … and SYS1 witnessing innovation-testing revenue slide from £13m to £4m since FY 2016 clearly signals clients have found alternatives to the group’s behavioural-science approach for evaluating new ideas.

- In fact, maybe clients are happy to test their innovations through services without 25 years of unique IP. Perhaps just a plausible methodology or convincing algorithm will suffice instead.

- The fact SYS1 has allocated about half of a £2m additional investment into TYI does suggest promoting TYI is not as straightforward as the group may have anticipated (see Additional discretionary investment and illustrative growth scenarios).

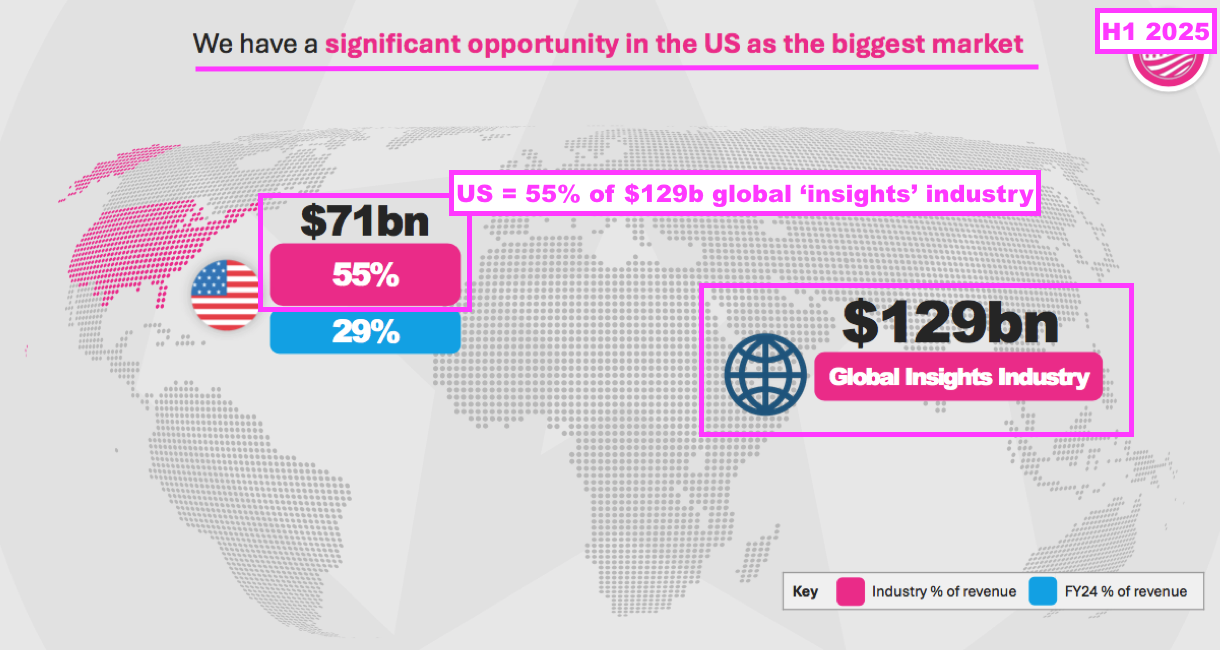

3 Reasons to Believe: United States

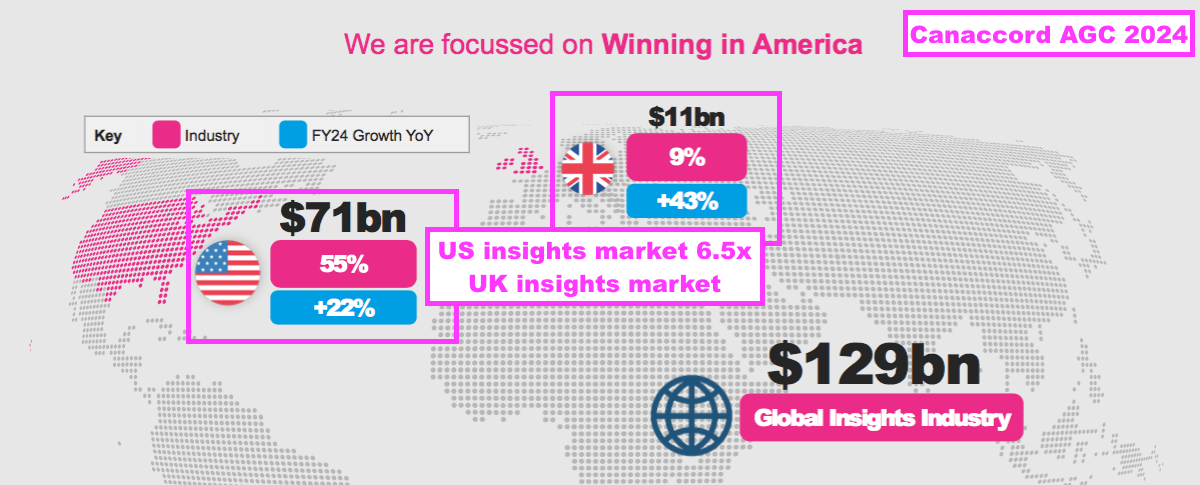

- This H1 re-emphasised the $71b size of the United States market:

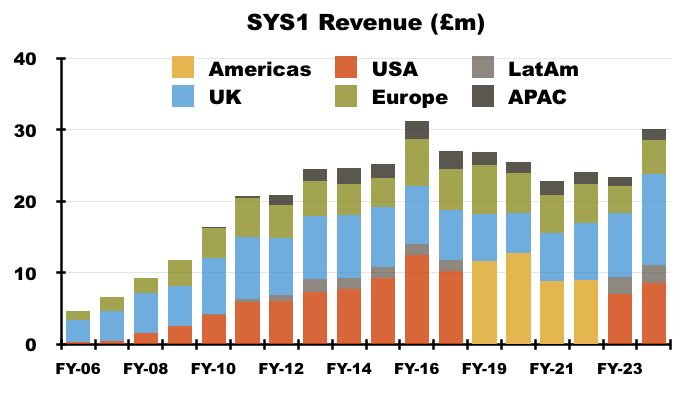

- The US had once been SYS1’s largest market. Between FYs 2006 and 2016, US revenue surged from £0.4m to £12.5m to support 40% of total revenue:

- Note also that innovation testing supported 42% of revenue during SYS1’s FY 2016 US heyday:

- SYS1 therefore has a strong US-TYI heritage, which I trust bodes well for a US-TYI revival.

- US revenue has yet to exceed its FY 2016 peak, although this H1 did show the US as the group’s second-largest market and supporting 35% of total H1 revenue:

- The preceding FY confirmed recent recruits Michael Perlman and Alex Banks were tasked with capturing greater US revenue:

[FY 2024] “We are making headway into the US market. Our go-to-market investment in FY24 has grown our fame, and we plan to increase this investment for the year ahead. We have strengthened the commercial teams across sales and marketing, with Michael Perlman joining as global Chief Commercial Officer, and Alex Banks as SVP Commercial Americas, leading the US and LatAm sales teams – both executives are based in the US and have significant commercial leadership experience in our industry sector. “

- Mr Perlman and Mr Banks are SYS1’s latest pair of senior US salesmen following a US sales mishap three years ago.

- To recap, a Q4 2022 profit warning citing weak US revenue effectively led to the aforementioned strategic review, which decided SYS1 founder John Kearon should be given “the priority task of securing new business and partnership opportunities in the US”.

- The 2023 Capital Markets Day then revealed the appointments of Jason Chebib and Steve Olenski as senior US executives…

- …while FY 2023 confirmed the appointments of Jon Bond and Noah Brier as US “advisors“:

- Mr Kearon now works on SYS1’s AI back in the UK, Mr Chebib and Mr Olenski no longer work for SYS1 while SYS1 has never since mentioned Mr Bond and Mr Brier.

- So far at least, Mr Perlman and Mr Banks appear to be working well.

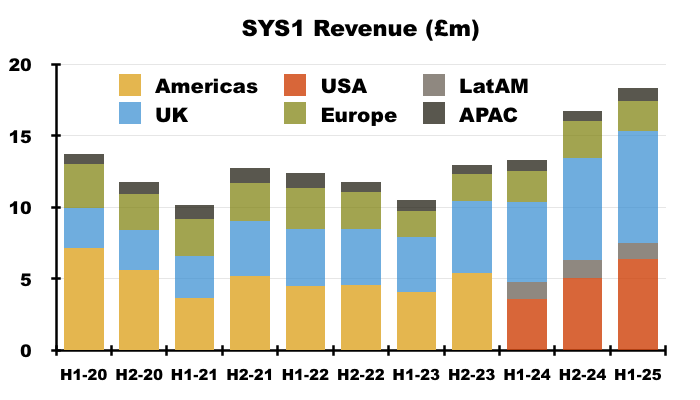

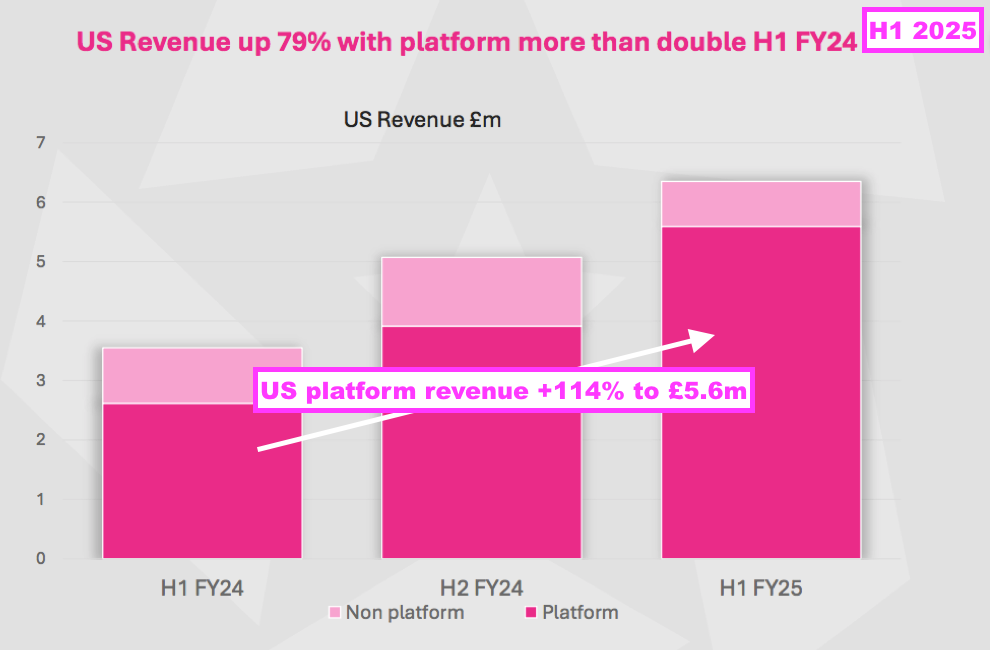

- This H1 witnessed total US revenue advance 79% to £6.4m, with H1 US platform revenue up 114% to £5.6m and H1 US non-platform revenue down 24% to £0.7m:

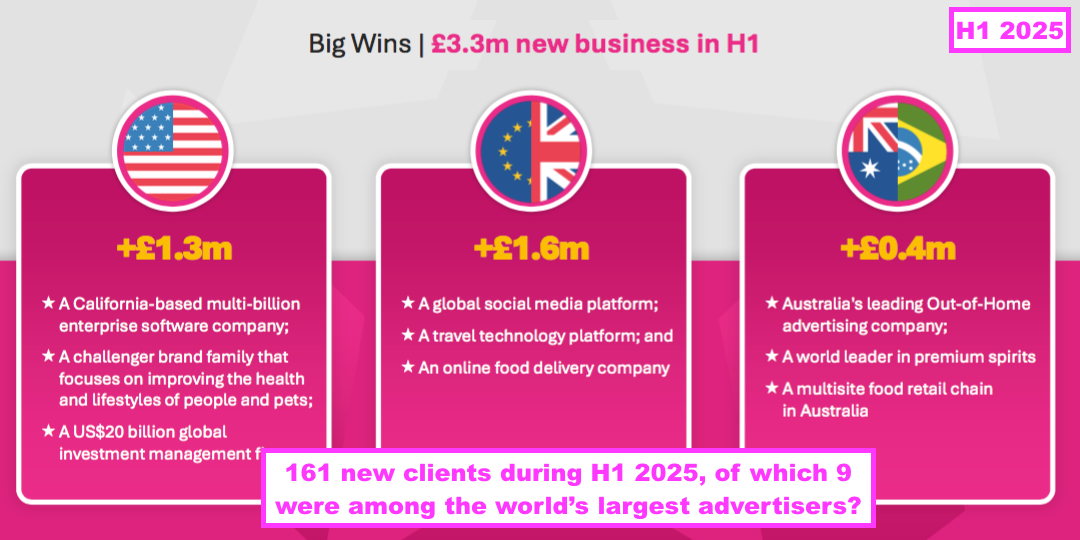

- This H1 reported new US clients supplying revenue of £1.3m:

“New business wins in the US delivered £1.3m of revenue in H1 and included:

• A large, California-based multi-billion revenue enterprise software company;

• A challenger brand family that focuses on improving the health and lifestyles of both people and their pets;

• A large, global investment-management firm with US$20 billion in annual revenue”

- New US client revenue at £1.3m for this H1 implies revenue from existing US clients for this H1 was £5.1m.

- Versus the comparable H1’s total US revenue of £3.4m, this H1’s revenue of £5.1m from existing US clients therefore showed an impressive £1.7m/50% improvement.

- However, SYS1’s presentation of new H1 client revenue is not straightforward! (see 3 Reasons to Believe: world’s largest advertisers).

- A previous SYS1 presentation suggested the US market was at least six times larger than the equivalent UK market…

- …which may imply US revenue could in time reach six times annual UK revenue, i.e. 6 * £14.9m = £89m.

- The larger US market comes with larger US costs.

- In particular, management remarks during my Q&A for the preceding FY disclosed that salaries of US salespeople are “double” what they are in the UK, but “you do get a lot of impact“.

- In addition, management remarks during this H1’s investor-group Q&A revealed “standing on a stage” at US industry events costs £50k-£100k, while SYS1 is “invited for free” to the equivalent UK events.

- Perhaps unsurprisingly, SYS1 has increased its US expense budget to exploit the US market further (see Additional discretionary investment and illustrative growth scenarios).

- SYS1’s focus on the US could mean other overseas regions become less relevant to the group.

- Indeed, combined H1 revenue from Latin America, Europe and Asia advanced only 2% to £4.2m to support 23% of total H1 revenue.

- This H1’s webinar clarified growth will be focused on the US and UK, while other regions will be employed to support US- and UK-based multinational clients:

“We have said over recent years that our biggest area of focus for growth would be in the US and then the UK. We serve globally, but if you look at where our new business, our marketing and our partnerships are based, they’re across the US and the UK.

We have always expected the US and the UK to grow at a faster rate than we would see in Europe, Latin America or Asia. That’s a conscious decision. But we need to operate in those other overseas areas because when we serve the world’s largest advertisers, they are global businesses and they want to be able to test in those regions and have local sales and consultancy teams who can support them. But when you look at the areas of growth, it will be across the US and the UK.“

3 Reasons to Believe: world’s largest advertisers

- This H1 re-emphasised SYS1’s desire to attract the world’s largest advertisers:

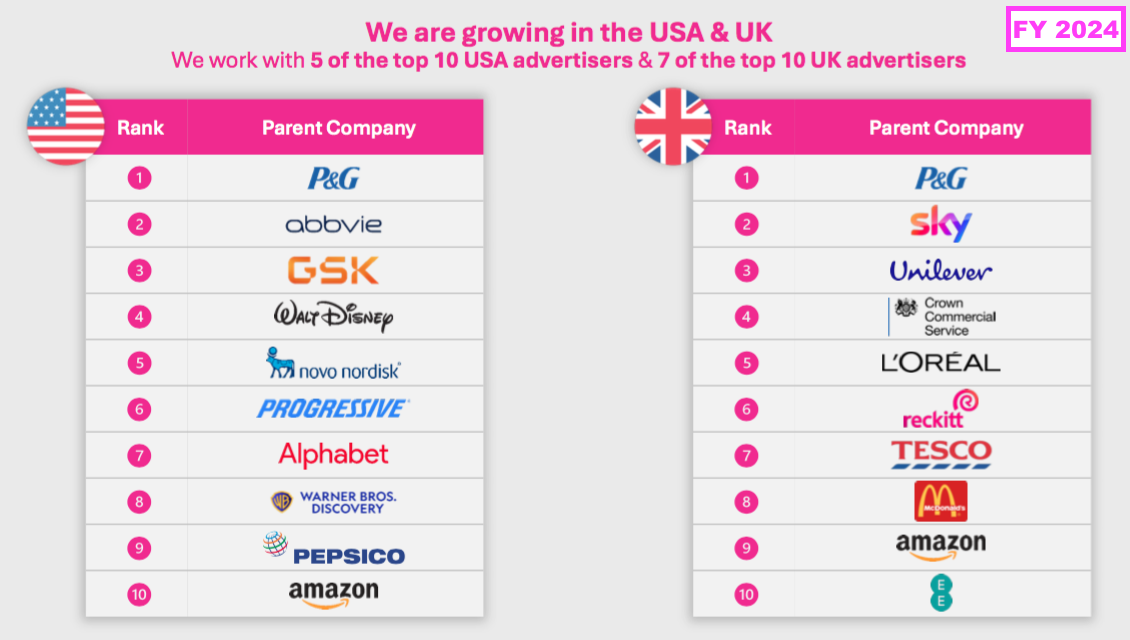

- The preceding FY listed the 10 largest US and UK advertisers, of which 12 were SYS1 customers:

- This H1 did not name any clients — SYS1 has in the past claimed it is “not permitted” to disclose the advertisers it works with — but the group’s podcast during this H1 did feature senior executives from AB InBev, Cadbury, Guinness and Pepsi.

- The H1 webinar provided this interesting line about appealing to the world’s largest advertisers:

“The world’s largest advertisers, we know that they are our target audience. We know that they are the people who have the capacity to be able to spend with us in the way we need, but also they have capability to be able to use the data and the insights we provide them to make their innovation and advertising truly world class.“

- I get the impression SYS1 needs the world’s largest advertisers — with the world’s largest advertising budgets! — as the costs of the platform would not be covered without them.

- SYS1’s clients possess an extremely wide range of ad-testing budgets, with a handful of clients paying significant sums but most paying relatively little.

- The preceding FY outlined how the top 10 and 20 clients of the then 428 total dominated SYS1’s revenue:

[FY 2024] “Concentration in our top 10 and top 20 clients was consistent year on year. Our top 10 clients made up 30% of revenue and our top 20 clients 45% of revenue. All of our top 20 clients in FY24 bought platform products with 78% of spend from the top 20 clients being on data and data-led consultancy. No one client in FY24 was larger than 5% of total company revenue.“

- That text from the preceding FY indicated the following:

- Average revenue per clients 1-10 was £900k;

- Average revenue per clients 1-20 was £675k;

- Average revenue per clients 11-20 was £450k;

- Average revenue per clients 21-428 was £40k, and;

- Client 1 spent no more than £1.5m.

- This H1 did not divulge the revenue concentration from the top 10 or 20 clients, nor the total number of clients.

- But this H1 did disclose 161 new platform clients provided £3.3m additional revenue… or £20k each.

- For the comparable H1, 136 new platform clients generated extra platform revenue of approximately £2.2m — equivalent to £16k each.

- True, this H1’s £20k per new platform client could be extrapolated to beyond £50k were the new clients all to employ SYS1 for a full year…

- …but £50k a year still has a long way to go to reach the £900k a year spent by a top-10 customer.

- No doubt this H1’s new clients were spread between a handful of big spenders and numerous smaller spenders.

- Note that SYS1 does not use revenue per client to judge its progress. The preceding FY’s webinar explained the measure was distorted by the few hundred clients who employ SYS1 very occasionally:

“£79k… that’s basically the revenue in FY 2023 divided by the number of clients and the equivalent figure for FY 2024 is £70k.

So on that basis [revenue per client] did decline. Would we read anything into that? Not particularly. It’s not a metric we particularly look at in the business, because the more successful we are, [the more we] recruit low-cost-to-service clients — people who might just test one ad a year or one every two years. They’re cheap to serve and they are profitable”.

- Bear in mind that SYS1’s occasional clients are (presumably) developing adverts for television, which suggests they are actually reasonably sized companies… but just somewhat tight with their ad-test expenditure.

- The preceding FY introduced net revenue retention (NRR) as a measure for shareholders to track client/revenue progress:

- In theory at least, NRR shows how ‘like for like’ client spending has changed from one period to the next… and if existing clients keep spending more on SYS1’s platform, then shareholders should become more convinced about the group’s progress and potential.

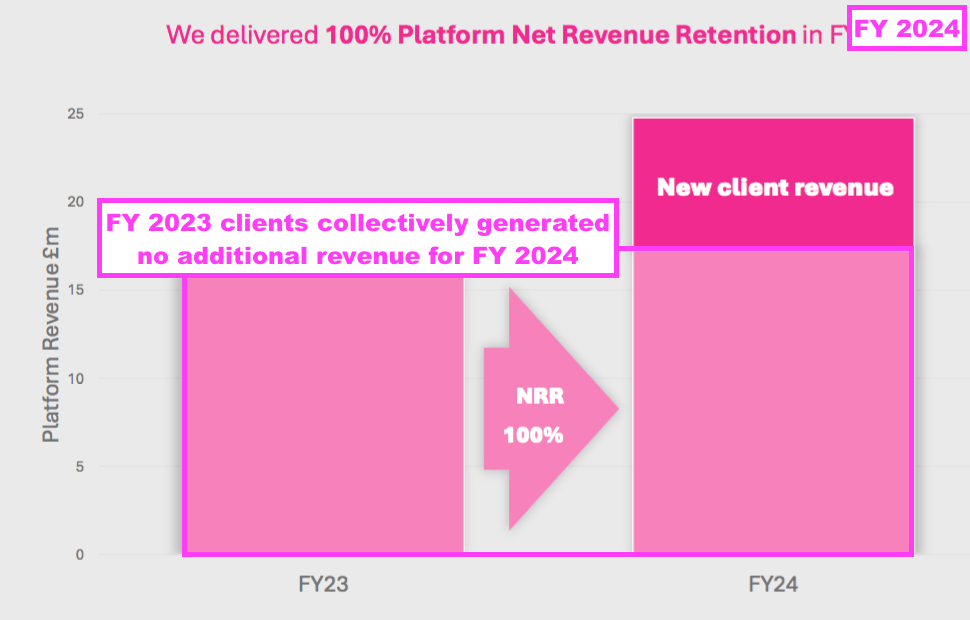

- The preceding FY’s platform NRR was 100%, which meant the preceding FY’s extra platform revenue was generated entirely from new clients. Or put another way, clients employing SYS1 during FY 2023 collectively paid the same amount during FY 2024.

- I had expected the preceding FY’s platform NRR to surpass 100%, given SYS1’s platform services are still relatively new and clients should be spending more as the platform services prove their worth.

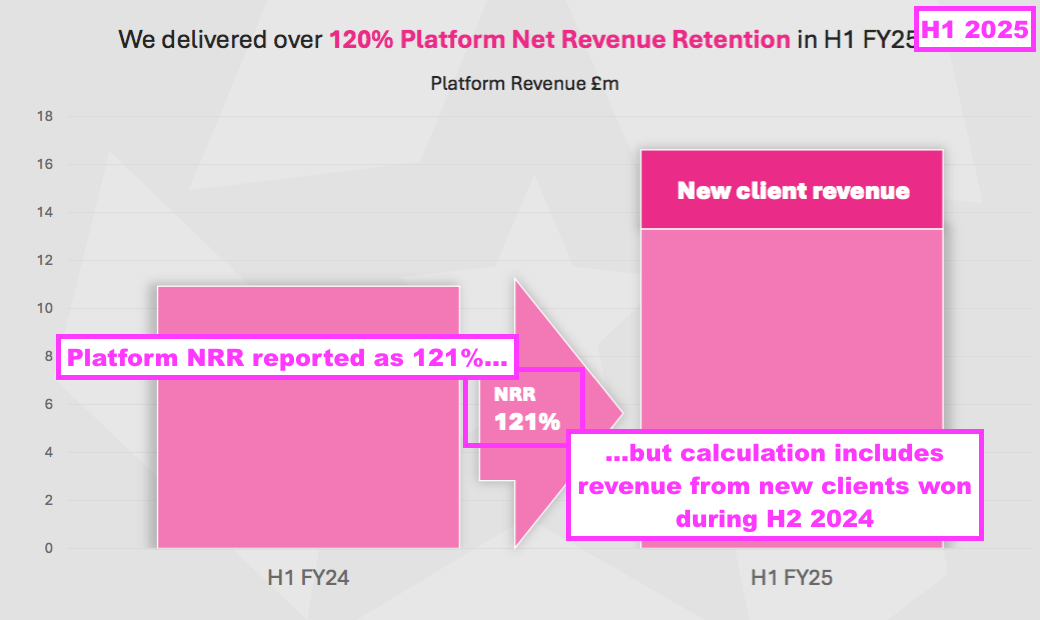

- This H1 disclosed platform NRR at a seemingly impressive 121%:

- This H1 explained how the NRR was calculated:

“Net Revenue Retention (NRR) improved in H1 to over 120% for platform revenue and over 110% overall, due to strong growth in the US and UK. (NRR is calculated as H1 FY25 Revenue excluding new clients divided by H1 FY24 Revenue).”

- Management remarks during this H1’s investor-group Q&A confirmed this H1’s 121% platform NRR “included new customer wins in the second half of last year that weren’t in the first half”.

- As such, the 121% platform NRR did not mean clients employing SYS1 during the comparable H1 had lifted their collective expenditure by 21% for this H1.

- Instead, the 121% platform NRR reflected clients employing SYS1 during the comparable H1 — plus clients employing SYS1 during the preceding H2! — had lifted their collective expenditure by 21% for this H1 versus the comparable H1.

- There is scope therefore that new clients from the preceding H2 flattered the 121% NRR result.

- If all that sounds complicated, it is. I recall management remarks during my Q&A for the preceding FY saying a platform NRR should be published for every FY, but not for H1s because the calculation may then become “incredibly confusing”.

- The 121% NRR calculation comparing this H1 to the comparable H1 is indeed “incredibly confusing”, as accounting for the intervening H2 clients is not straightforward.

- I would venture SYS1’s NRR calculations ought to be consistent, and for H1s should compare contiguous twelve-month periods as per the FY NRR calculation.

- At present, shareholders cannot really compare the preceding FY’s 100% platform NRR to this H1’s 121% platform NRR.

- Management remarks during this H1’s investor-group Q&A indicated many shareholders had questioned this H1’s 121% platform NRR… and the questions may have increased after the subsequent Q4 2025 update showed a lower, 106% platform NRR (see Q3 and Q4 2025 trading statements).

- If NRR calculations are now disclosed for H1s, then revenue contributions from the top 10 and 20 clients should be disclosed for H1s as well.

- After all, SYS1 is targeting the world’s largest advertisers, and monitoring the collective expenditure of the very largest clients could validate whether the group’s platform really is attracting the world’s largest advertisers.

- Note that the 2024 Capital Markets Day suggested the very largest clients could in time spend £3m a year versus the preceding FY’s top-10 average of £900k:

[CMD 2024] “Fairly consistently, our top ten customers represent about a third of the company’s revenue… It is very plausible we can have multiple customers over £1m and have some customers over £2m and maybe some over £3m. That is not at all out of the question.“

- A single client spending £3m during one year could occur sooner than expected.

- Management remarks during this H1’s investor-group Q&A disclosed SYS1 now has a customer that is “significantly larger” than the preceding FY’s largest customer, and which could generate “close to 10%” of revenue for FY 2025.

- Following this H1, SYS1 has indicated revenue for FY 2025 to be £37.4m, and one client being “close to 10%” could therefore have contributed revenue beyond £3m (see Q3 and Q4 2025 trading statements).

- The forthcoming FY 2025 should reveal just how dependent SYS1’s progress has been on this particularly large client. I estimate at least 20% of the extra revenue for FY 2025 could have been supported by the largest client’s additional spending.

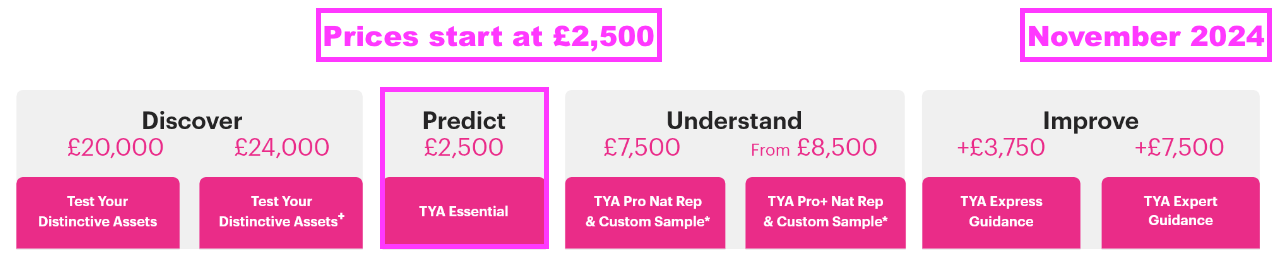

- SYS1 did increase its headline product pricing the other year, which may have helped those reported NRRs. But SYS1’s website sadly no longer discloses service pricing, and TYA prices were last seen starting at £2,500:

Employee productivity and remuneration

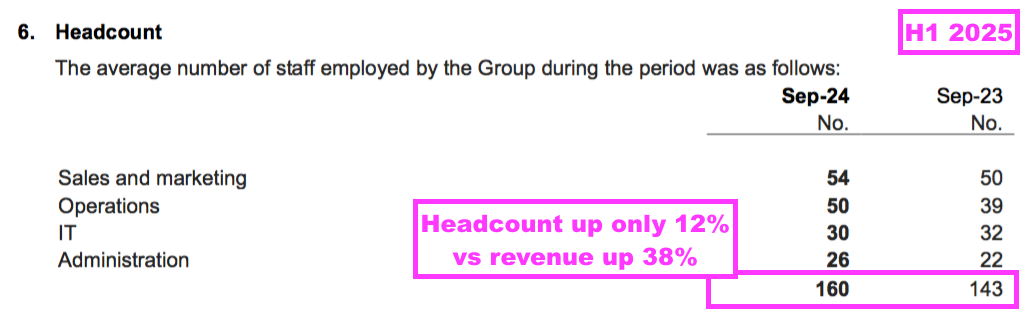

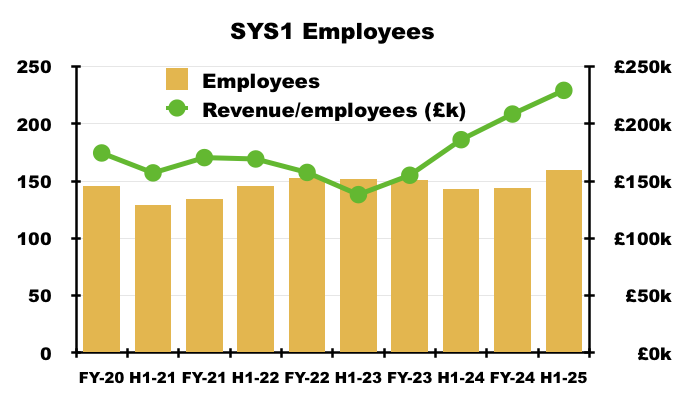

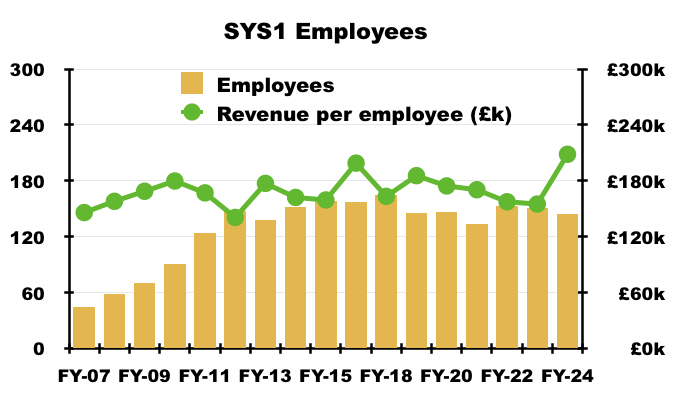

- Probably the most encouraging development during this H1 was the improvement to employee productivity.

- H1 revenue up 38% to £18.3m compared to the H1 headcount up 12% to 160…

- …and equated to a new record revenue per employee of £229k:

- 160 employees is SYS1’s largest workforce since FY 2018 (165), when revenue per employee was only £163k:

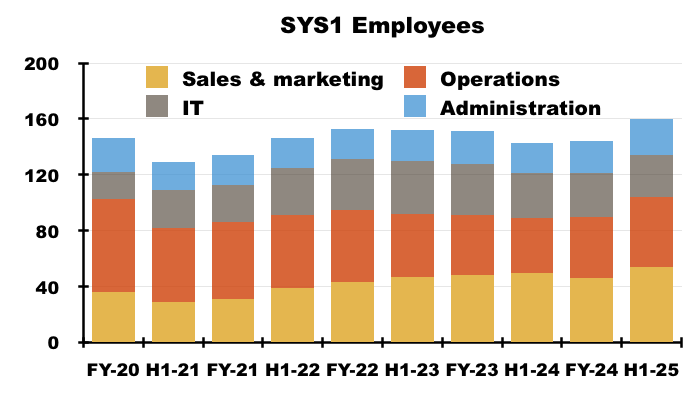

- Between FY 2020 and this H1, the split of workforce roles has altered as follows:

- Sales and marketing: from 25% to 34%;

- Operations: from 46% to 31%;

- IT: from 13% to 19%, and;

- Administration: maintained at 16%.

- The shift away from consultancy ‘operations’ staff towards sales and IT employees clearly reflects the group’s platform strategy and — encouragingly — SYS1”s “scalable business model” continuing to improve on a revenue-per-employee basis.

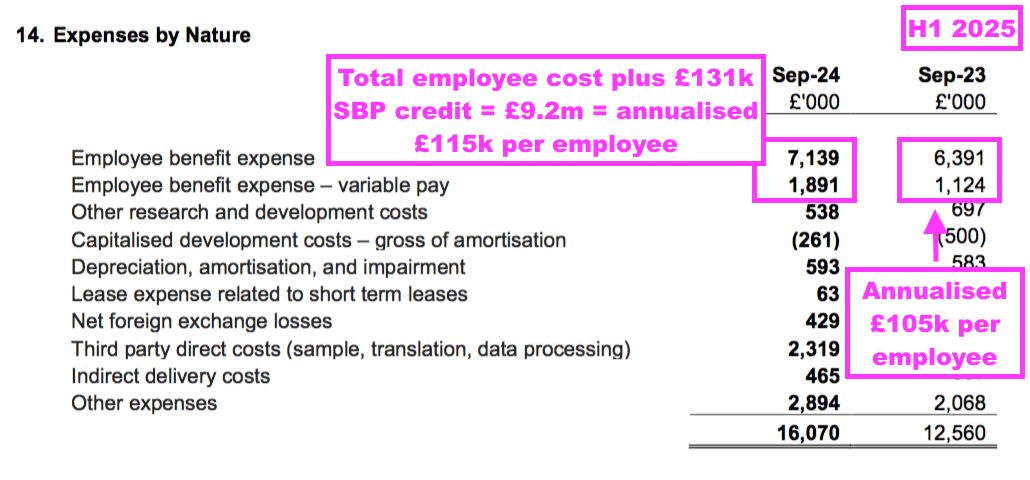

- Adjusting for the aforementioned £131k share-based payment credit…

- …SYS1 spent £9.2m on its 160 employees during this H1…

- …equating to an annualised cost of £115k per person (+10%)

- The preceding FY claimed the group’s “performance culture” had underpinned the group’s recent progress:

[FY 2024] “FY24 has been a strong year in building out our performance culture and we have highly motivated teams with strong retention and employee engagement. We create an environment where all colleagues can do their jobs with ease to ensure they are focussed on adding value to our clients.”

- The preceding FY’s “performance culture” appeared driven by a revamped remuneration policy, which placed a “greater emphasis on variable pay linked to growth”:

[FY 2024] “In the second half of FY23 we changed the way that most people in the business are rewarded by placing greater emphasis on variable pay linked to growth in the Group’s gross profit.

FY24 was therefore the first full year of this approach which we believe is working well. Whereas only a few colleagues received a cost-of-living increase to their salary, variable pay across the Group rose by £2.8m year-on-year as a result of significantly higher sales volumes and improved profit margins.”

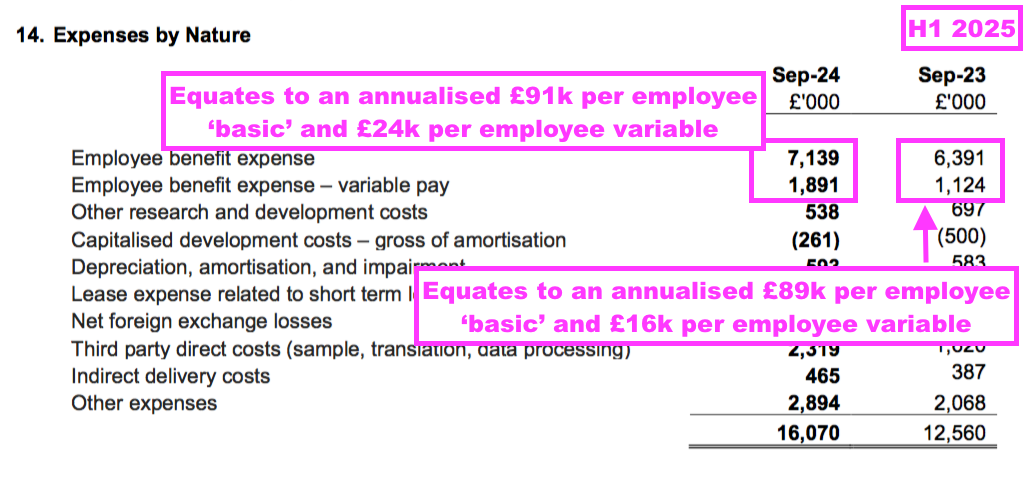

- This H1 appeared to extend the “greater emphasis on variable pay linked to growth”.

- Adjusted for the £131k share-based payment credit, ‘basic’ pay per head for this H1 increased by £2k (2%) to £91k versus the comparable H1.

- But variable pay per head for this H1 increased by £8k (50%) to £24k versus the comparable H1:

- Employee bonuses are linked to gross profit, which during this H1 advanced by £4.3m, or 37%, to £16.0m.

- This H1 therefore witnessed a greater proportion of gross profit absorbed by variable pay — 12% (£1.9m/£16.0m) versus 10% for the comparable H1.

- However, the limited increase to basic pay ensured total employee pay absorbed a lower proportion of this H1’s gross profit — 57% (£9.2m/£16.0m) versus 64% for the comparable H1.

- SYS1’s bonuses are weighted towards H2 and while the forthcoming FY 2025 will divulge the full variable-pay details, for now I am hopeful employee remuneration will not disrupt the group eventually reaching its illustrative 30% Ebitda-margin target (see Additional discretionary investment and illustrative growth scenarios).

Financials: margins

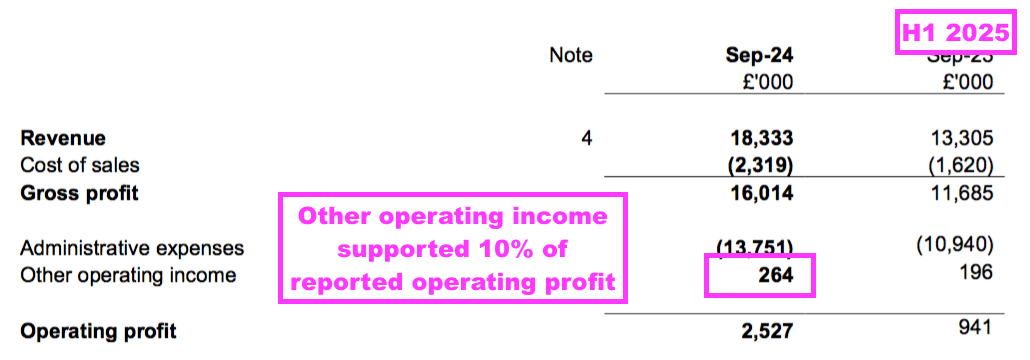

- Total employee pay absorbing a lower proportion of this H1’s gross profit helped this H1’s adjusted Ebitda margin to improve to 16.3% versus 11.8% for the comparable H1.

- Note that SYS1’s adjusted Ebitda margin does not adjust for the group’s ‘other operating income’, which I believe relates entirely to a trademark-settlement agreement:

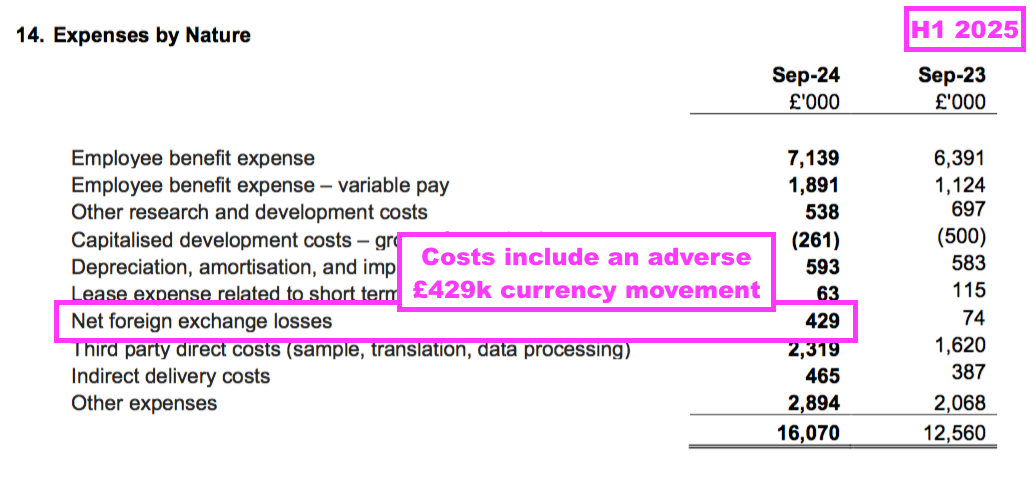

- Excluding the share-based payment credit and the other operating income, this H1’s statutory operating profit of £2.5m converts into to £2.1m.

- A profit adjustment could arguably be made also for ‘net foreign-exchange losses’ of £429k:

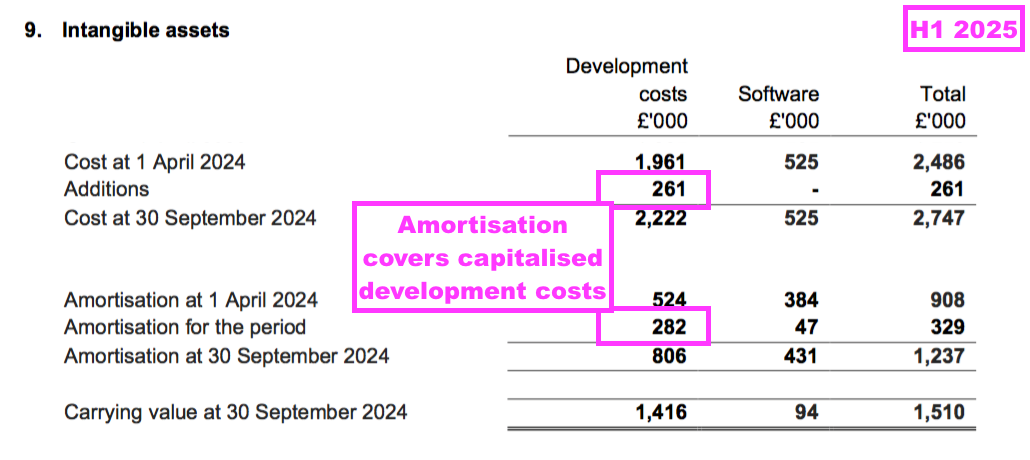

- At least this H1’s profit was not flattered by significant costs being capitalised directly onto the balance sheet.

- This H1 witnessed capitalised development costs of only £261k that were covered entirely by the associated £282k amortisation charge:

- This H1 indicated capitalised development costs should now cease following the completion of the associated IT project:

“Development costs relate to costs capitalised for the development of the “Test Your” platform (carrying value £358k; March 2024: £509k), which completed during the year ended 31 March 2023, and the Supply Chain Automation platform (carrying value £1,030k; March 2024: £930k), which enables System1 to interface (via API) with multiple suppliers of panel respondents, was completed during the period ended 30 September 2024″

- Capitalised development costs of £1.4m remain to be expensed against future profits.

- A promising financial measure from this H1 that required no adjustments was the 87% gross margin:

- An 87% gross margin implies SYS1 can buy online-panel responses for £13 and repackage and interpret those responses for £100.

- This H1’s 87% gross margin means SYS1 has now exceeded its minimum “at scale” 85% gross margin since H2 2023:

- The gross margin impressively increased during the subsequent H2 2025 (see Q3 and Q4 2025 trading statements).

Financials: cash flow and balance sheet

- Employee bonuses have a significant influence on SYS1’s H1 and H2 cash flows.

- The bulk of bonuses are determined during an H2 and are paid to employees during the following H1. As such, an H1’s cash flow and cash position (after bonuses are paid) can look very different to the preceding H2’s cash flow and cash position (before bonuses are paid).

- This H1’s cash flow was suppressed by bonuses of £2.6m relating to the preceding FY:

“Free cash flow after property lease costs and interest income amounted to an outflow of £0.3m in the first half, reflecting the payment of £2.6m in bonuses and commissions relating to FY24. (H1 FY24: free cash inflow of £0.6m).”

- Excluding the preceding FY’s bonuses, this H1’s free cash flow was £2.3m — some £0.5m greater than reported H1 earnings of £1.8m.

- Tax was the primary reason for the £0.5m difference; this H1 paid £0.4m cash tax while the income statement showed £0.8m tax. SYS1 has over time reported a greater tax charge than the sum actually paid (point 26).

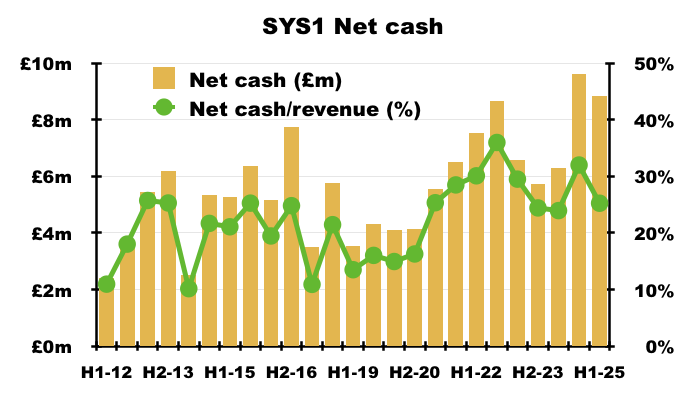

- This H1’s free cash outflow of £0.3m plus an £0.4m adverse currency translation meant cash ended this H1 £0.7m lower at £8.9m.

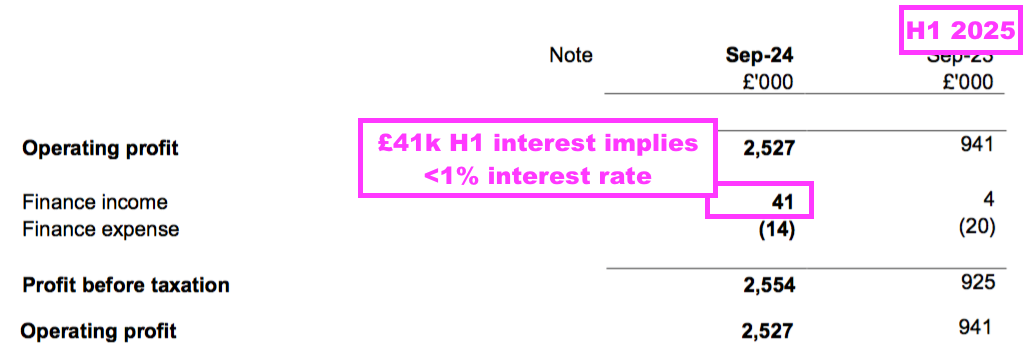

- SYS1 continues to carry no bank debt.

- Despite the significant cash position, this H1 disclosed interest of only £41k — equivalent to an annualised interest rate of less than 1%:

- The H1 webinar revealed most of the cash does not earn interest because it is held for day-to-day purposes:

“We are spread around the world and our banking relationships are spread around the world. Our biggest cash centres are Brazil, where we have quite a big operation and we employ a lot of people, the United States, the UK and Switzerland.

Of the £8m cash in the first half, at any one time typically between a quarter and a third of that was on an interest-bearing account and the rest was on site accounts so that we could use it to meet our day-to-day obligations.

We tend to be very selective how we deposit. We’re trying to repatriate as much foreign exchange as we can back into sterling and then we deposit it from there to deal with the kind of volatility we’ve seen particularly in [GBP:USD] over the last few months.“

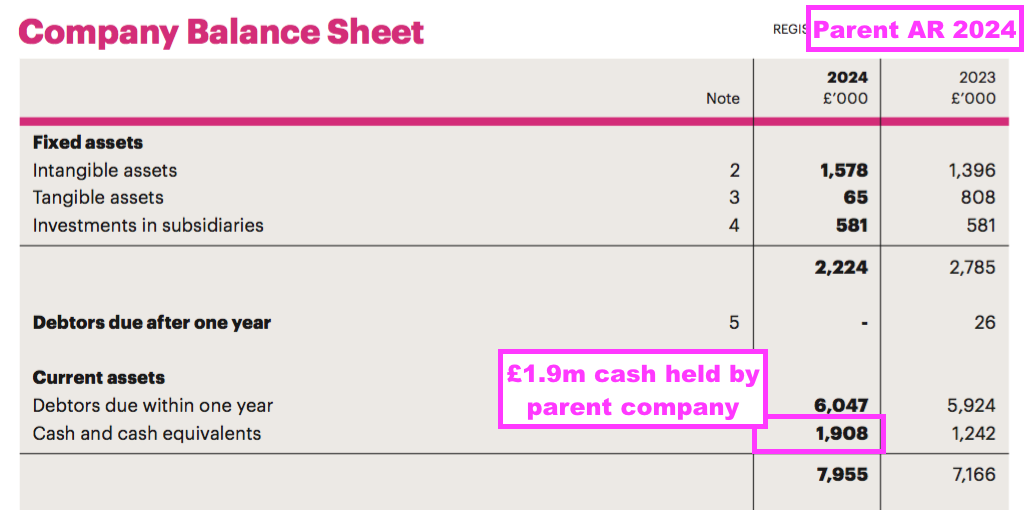

- Note the preceding FY revealed SYS1’s parent-company accounts held cash of £1.9m:

- £1.9m held by the parent company implied the remaining £7.7m of the then cash position was spread around various subsidiaries and seemingly required for day-to-day purposes, and perhaps therefore accrued no interest.

- The preceding FY’s £1.9m parent-company cash earning 4% would get close to generating this H1’s £41k interest.

- I would venture only the parent-company cash reflects SYS1’s ‘surplus’ money, while the balance seems inherent to running the business and ought not to be considered for ‘enterprise valuation’ purposes.

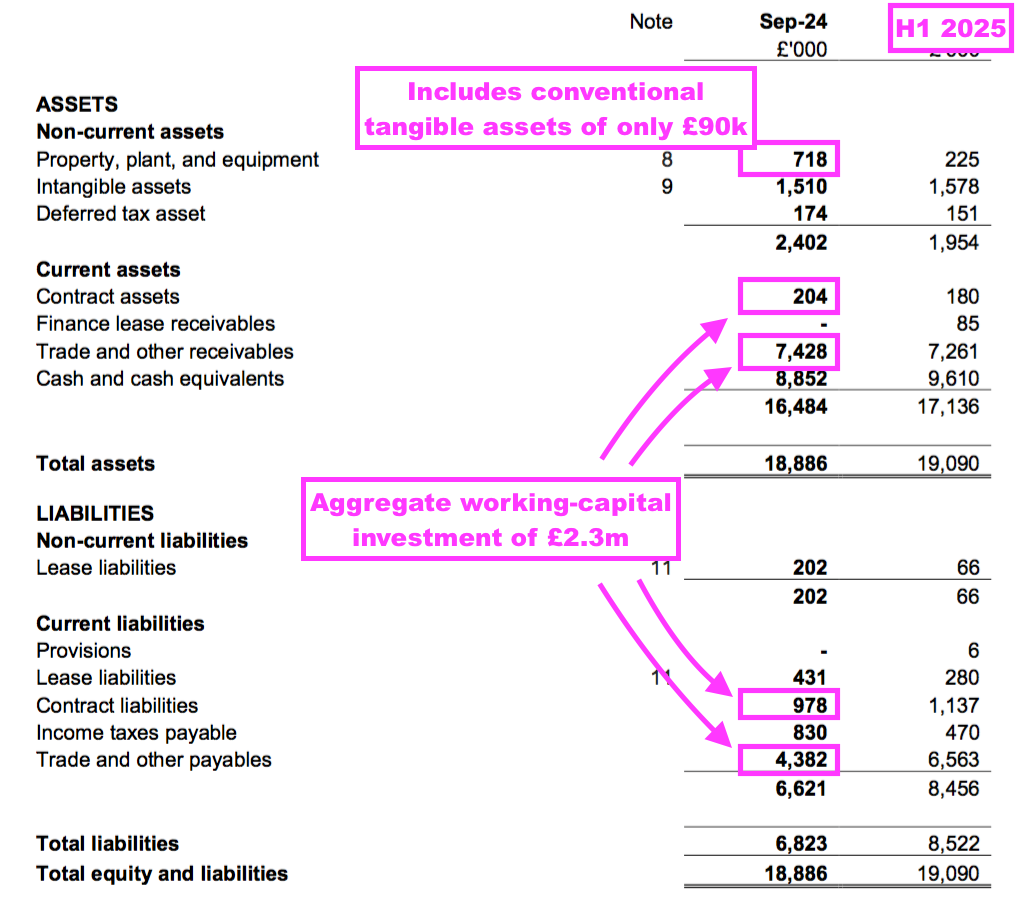

- Alongside the cash, this H1 showed aggregate working capital of £2.3m alongside conventional tangible assets of only £90k…

- …which does not seem a huge balance-sheet commitment versus a trailing twelve-month pre-tax profit in excess of £4m.

- SYS1’s software platform ought to be a fundamentally capital-light operation, although how much cash will be required to remain in the business is difficult to judge.

- This H1’s £8.9m net cash position was equivalent to a sizeable 25% of revenue:

- If revenue does advance substantially during the next few years, I would hope net cash as a proportion of that revenue can become lower than 25%.

Additional discretionary investment and illustrative growth scenarios

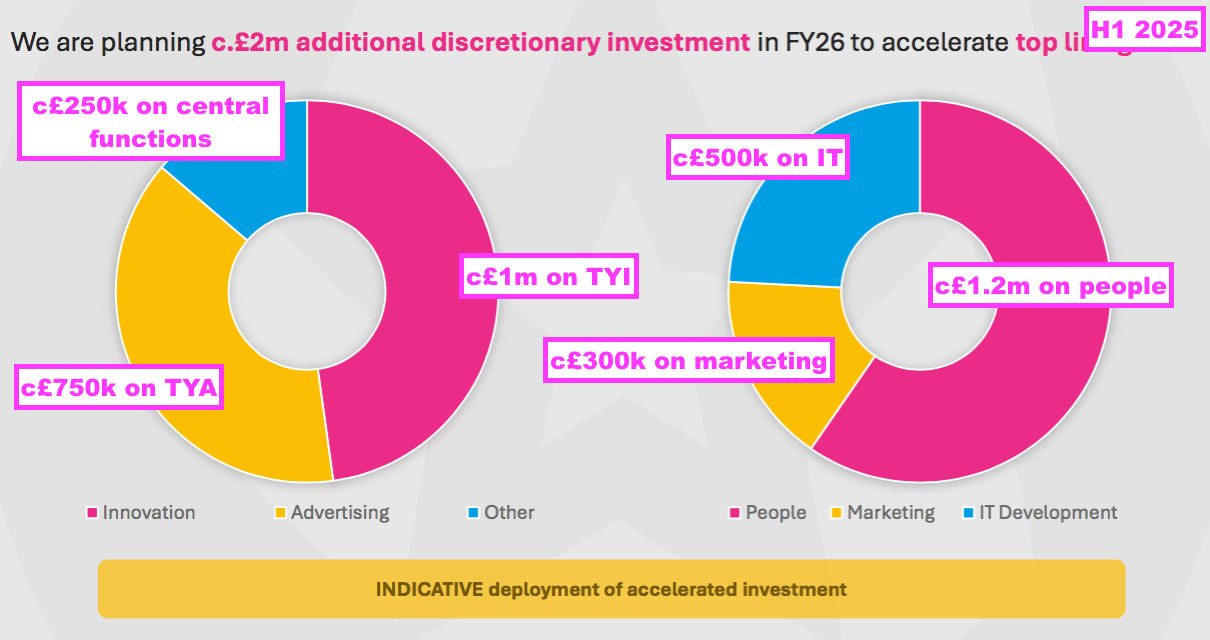

- This H1’s most significant news was a £2m “additional discretionary investment“:

“We are investing £2m in additional discretionary investment in the next 18 months aimed at building our position in America and revitalising System1’s Innovation proposition, covering recruitment of additional personnel, marketing and further IT development costs, and we believe we need to continue to invest in growth to grow shareholder value.”

- Approximately £1m of the £2m will be spent “revitalising” TYI, with approximately £750k spent on TYA (mostly in the US) and approximately £250k spent on central functions:

- In terms of resources, approximately £1.2m of the £2m will be spent on people, with approximately £500k spent on IT and approximately £300k on marketing.

- The extra £1.2m to be spent on people seems partly to ensure this H1’s record employee productivity does not deteriorate.

- In fact, the H1 webinar included a somewhat startling admission of needing to further “professionalise” the workforce and to “step-change the calibre” of employees:

“We need to continue to professionalise and really step-up and step-change the calibre and quantity of the people we have in the business.”

- “Professionalise” was also mentioned during this H1’s investor-group Q&A, which again suggested the workforce has not been entirely up to the group’s “performance culture” standard.

- At least management remarks during this H1’s investor-group Q&A said:

- Recruiting is “a heck of lot easier” than two years ago;

- “Very good people” are interested in SYS1, who can see the group is “going places“, and;

- “We are getting great CVs“.

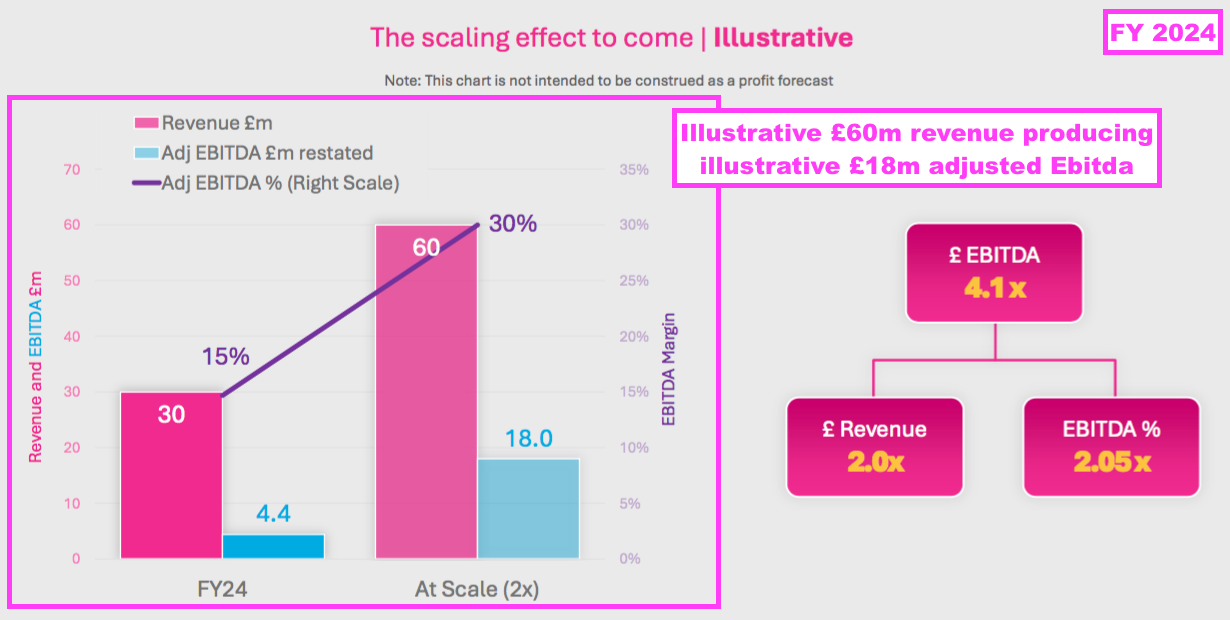

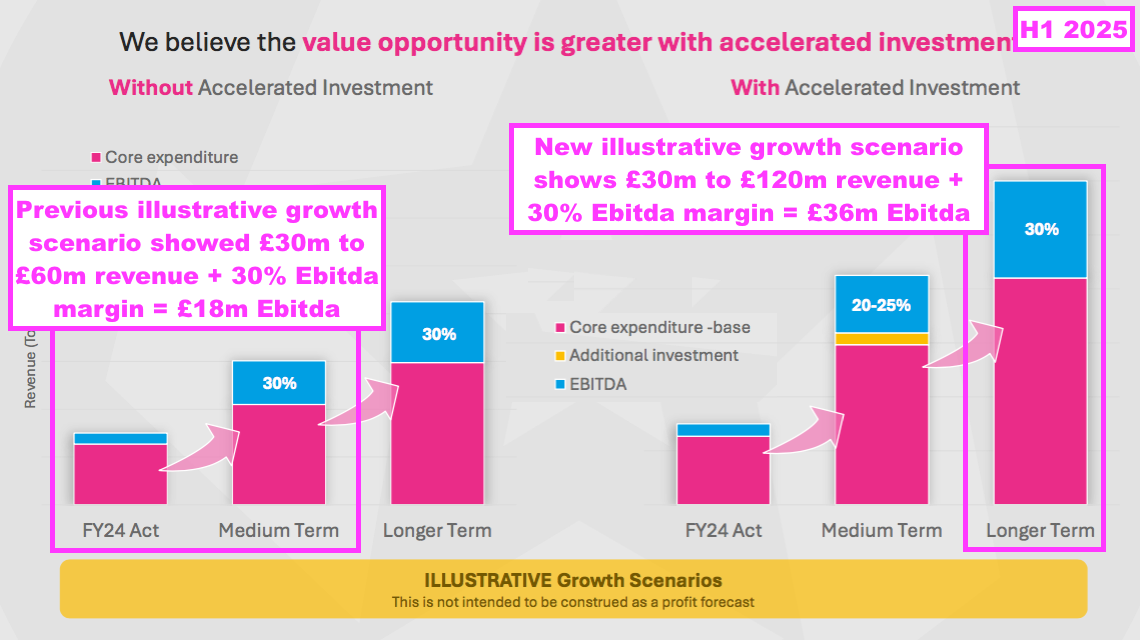

- To demonstrate how SYS1 could ‘scale’ its platform services for the benefit of shareholders, the preceding FY provided an illustrative projection of revenue doubling to £60m and an illustrative adjusted Ebitda margin of 30% leading to an illustrative adjusted Ebitda of £18m:

- This H1 implied the £2m “additional discretionary investment” could double SYS1’s illustrative revenue potential from £60m to £120m, that could in turn double the illustrative adjusted Ebitda from £18m to £36m through an illustrative adjusted Ebitda margin of 30%:

- Management remarks during this H1’s investor-group Q&A included the following snippets:

- TYI could “easily be half” of the upgraded £120m illustrative revenue;

- But TYI may not work out, in which case SYS1 will then focus on TYA;

- If TYI is not revitalised now, “we will never know the outcome“, and;

- The illustrative charts are not profit forecasts, but the “opportunity we believe we can go after“.

- I am not truly convinced the £2m “additional discretionary investment” is entirely “discretionary“.

- In particular, the additional £1m earmarked to revive TYI appears mandatory.

- For example, the preceding FY’s webinar suggested TYI could start recovering from FY 2026:

[FY 2024] “Going forwards we think there’ll be marginal [TYI] growth this year [FY 2025] but really we’ll start to see high percentage growth from next year [FY 2026] onwards and the challenge then will be for us in terms of how fast we can make it grow… We think that it can definitely have legs to be growing fast from next year [FY 2026] onwards.”

- But management remarks during this H1’s investor-group Q&A implied a TYI recovery may now commence during FY 2027. Snippets included:

- “People do buy TYI, use TYI and love TYI”;

- But “we need to make more people aware of TYI“, and;

- Innovation revenue may be “similar” for FY 2025 and FY 2026, and could “really crack on” during FY 2027.

- I don’t understand how spending £1m more to revitalise TYI could lead to its recovery being delayed by a year.

- I speculate early attempts to cross-sell TYI through TYA have not worked, and SYS1 now has no option but to spend £1m to develop the TYI promotional equivalents of TYA’s AdRatings, Lemon, Christmas and ITV.

- Assuming the £2m additional investment bears fruit, the expenditure would seem likely to become part of SYS1’s regular cost base.

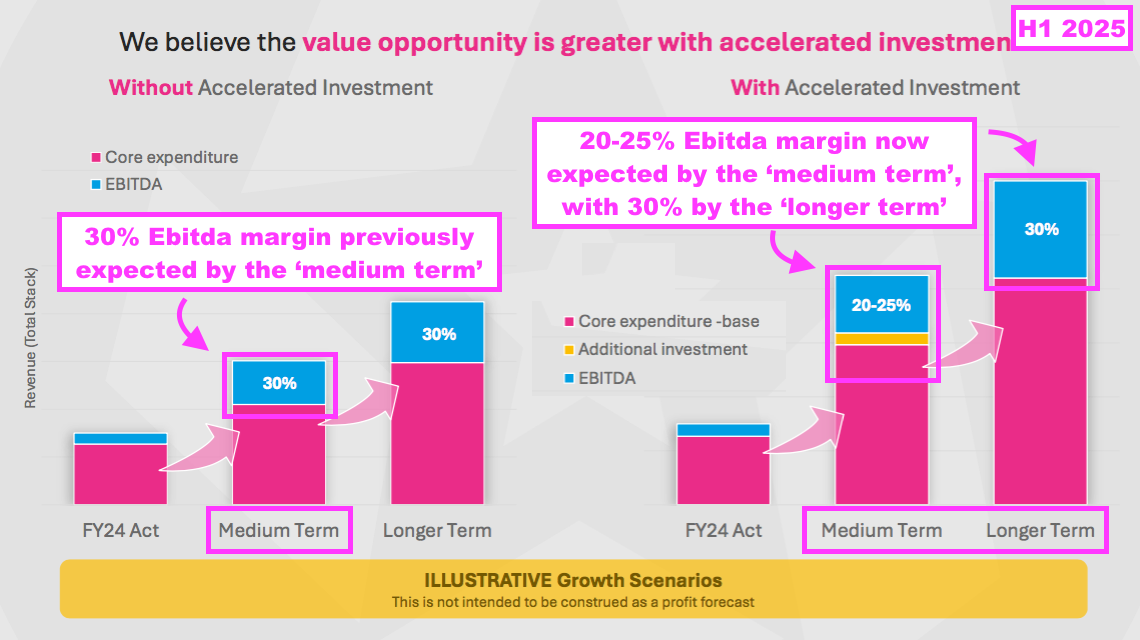

- As such, achieving the illustrative 30% adjusted Ebitda margin will now take longer than before:

- SYS1 is hopeful of an adjusted Ebitda margin between 20-25% by the “medium term“, which seems at least four years away as this H1 also indicated an adjusted Ebitda margin of between 15-20% during the next three years:

- SYS1 also indicated platform revenue ought to grow between 20-30% per annum during the next three years.

- Growing platform revenue at the low-point 20% per annum would mean SYS1 achieves its illustrative £120m “longer term” revenue potential within the next seven years.

Q3 and Q4 2025 trading statements

- This H1’s outlook brushed off economic concerns and suggested H2 2025 revenue could be better than expected:

“Despite a difficult economic environment in some key markets, and challenging conditions for media owners and advertisers, we believe System1 can continue to grow profitably by gaining market share from large incumbents that we believe have less predictive products.

The Company is trading in line with market expectations, including the impact of the cost of additional [£2m] investment to be incurred in the second half of the fiscal year.

The third quarter has begun well, and at this stage we recognise that there may potentially be some revenue upside compared to current market expectations.“

- January’s Q3 2025 statement then revealed a record-revenue quarter. Details included:

- Q3 platform revenue up 53% to £9.5m, which comprised:

- Q3 ‘data’ revenue up 57% to £8.2m, and;

- Q3 ‘data-led’ revenue up 33% to £1.3m;

- Q3 non-platform revenue down 62% to £0.7m, and;

- Q3 total revenue up 26% to £10.2m.

- Q3 platform revenue up 53% to £9.5m, which comprised:

- The Q3 performance was unsurprisingly supported by the US and UK and less so by Europe and Innovation:

[Q3 2025] “…with strong platform revenue growth in the US, UK and APAC more than offsetting reductions in Europe, Innovation and non-platform sales.“

- The Q3 statement suggested revenue may have been enhanced by a particularly “large project“:

[Q3 2025] “The increase in platform revenue reflected consistent growth in ad testing together with completion of a large project for a US-based client in December 2024.”

- The Q3 statement contained confusing client numbers:

[Q3 2025] “System1 won over 120 new clients in Q3 FY25, and over 230 in the first nine months of FY25.“

- This H1 reported 161 new platform clients, which if added to the “over 120” clients subsequently won during Q3 equals over 281…

- …which is indeed “over 230” as per the Q3 statement, but does not give the impression the new-client tally is consistently reported.

- The Q3 statement added:

[Q3 2025] “Net platform revenue retention remained broadly in line with H1 FY25, above 110%.”

- Following the aforementioned complications of understanding this H1’s 121% platform NRR, I dare not try to interpret the Q3 110%-plus NRR.

- Despite “economic headwinds“, the Q3 statement upgraded the FY 2025 profit outcome:

[Q3 2025] “System1 enters the final three months of this financial year on the back of a record third quarter achieved while facing some economic headwinds in Europe and the UK.

The Board now believes that the Group is well placed to achieve full-year revenue at least in line with current market expectations [£36.5m] and deliver a full-year adjusted profit before taxation of approximately £5m, comfortably above current market expectations [of £4.4m] (FY24: £3.1m).”

- April’s Q4 2025 statement was unfortunately not as positive as January’s Q3 statement. Details included:

- Q4 platform revenue up 9% to £8.4m, which comprised:

- Q4 ‘data’ revenue up 19% to £6.6m, and;

- Q4 ‘data-led’ revenue down 15% to £1.8m;

- Q4 non-platform revenue down 48% to £0.5m, and;

- Q4 total revenue up 2% to £8.9m.

- Although Q4 platform revenue of £8.4m was somewhat lower than Q3 platform revenue of £9.5m…

- …H2 2025 platform revenue of £17.9m was:

- 7% higher than this H1’s platform revenue of £16.7m, and;

- 29% higher than the preceding H2 2024 platform revenue of £13.8m:

- H2 2025 platform revenue was supported entirely by greater ‘data’ income, which gained 10% on this H1 and 37% on the preceding H2 2024.

- H2 2025 ‘data-led’ revenue meanwhile was a disappointing £3.1m, some 7% lower than the £3.3m reported for this H1 and equal to the £3.1m reported for the preceding H2 2024.

- I had assumed ‘data-led’ revenue would generally track ‘data’ revenue higher, and I do hope demand has not stalled for SYS1’s follow-up expertise.

- The Q3 and Q4 statements meant for FY 2025 as a whole:

- Platform revenue gained 39% to £34.6m;

- ‘Data’ revenue gained 42% to £28.1m, and;

- ‘Data-led’ revenue gained 29% to £6.5m.

- An ominous development within the Q4 statement was SYS1 becoming sensitive to the global economy…

[Q4 2025] “The relatively modest overall revenue growth in Q4 reflected recent global disruption, volatility and uncertainty in global markets. In spite of this, March was the highest revenue month of the financial year.“

- …and referring to “clients’ budgets” and “downside risk“:

[Q4 2025] “While it is too early for us to gauge the effect that the current volatility in global markets will have on our clients’ budgets, inevitably at this stage there is more downside than upside risk and we will provide a further update in our full-year results.”

- Further ominous developments from the Q4 statement could be deduced from the following FY 2025 details:

- Ad-testing revenue up 39% (to an estimated £31.6m);

- Innovation-testing revenue down 30% (to an estimated £2.8m);

- Brand-tracking revenue down 4% (to an estimated £3.0m);

- US revenue up 49% (to an estimated £12.9m), and;

- UK revenue up 28% (to an estimated £16.2m).

- Those FY 2025 details imply the following H2 2025 revenue estimates:

- Ad-testing at £15.7m, versus £15.9m for this H1;

- Innovation-testing at £1.5m, versus £1.3m for this H1;

- Brand-tracking at £1.9m, versus £1.1m for this H1;

- US revenue at £6.5m, versus £6.4m for this H1, and;

- UK revenue at £8.5m, versus £7.8m for this H1.

- While H2 2025 platform revenue of £17.9m was 7% higher than this H1’s platform revenue of £16.7m…

- …most of that growth appeared supported by brand-tracking and the UK.

- In contrast, both ad-testing revenue and US revenue during this H1 seemed to remain the same during the subsequent H2 2025.

- The obvious worry is that SYS1’s efforts to expand in the US and capture more of the world’s largest advertisers have plateaued…

- …which is certainly not what shareholders were expecting given this H1 trumpeted that £2m additional investment and targeted a 20-30% platform-revenue CAGR for the next three years.

- April’s Q4 statement indicated a (straightforward!) platform NRR of 106% for FY 2025 — i.e. like-for-like FY client revenue gained 6%, which again is perhaps not the level shareholders were expecting following this H1’s talk of a 20-30% platform-revenue CAGR.

- True, Q4 2025 could have been another quarterly aberration and April’s Q4 statement did say March (the final month of FY 2025) was the “highest revenue month of the financial year” (although that implies January and February were relatively weak).

- At least April’s Q4 statement reported “over 300” new platform clients producing FY 2025 revenue of £8.1m (versus £7.5m for the preceding FY), which if repeated for FY 2026 would lift platform revenue by a further 23%.

- Maybe the prospect of another large batch of new clients is why the Q4 statement suggested “strong revenue growth” should be achieved for FY 2026:

[Q4 2025] “While we remain focused on continuing the profitable growth momentum in the business, replicating 40%+ platform revenue growth may be challenging in the current global economic and political climate, however we do anticipate continuing to deliver strong revenue growth.“

- The Q3 and Q4 statements did not suggest anything untoward occurring with profitability or cash flow. Indicated figures for FY 2025 included:

- A gross margin of 88%;

- Adjusted Ebitda of £6.5m (up c49%);

- Adjusted profit before tax of £5.2m (up c68%), and;

- Free cash flow of £4.2m that improved the cash position to £12.9m.

- Those indicated figures for FY 2025 imply the following improved margins for H2 2025:

- A gross margin close to a 89%, above the 85% “at scale” target, and;

- An 18% adjusted Ebitda margin, above this H1’s 16% and well within the 15-20% three-year target.

- While the mix and level of revenue during H2 2025 raises questions, the promising margin progress does suggest the platform’s ‘scalable’ economics are strengthening.

- Announced after the Q3 and Q4 trading statements, SYS1’s revised LTIP provides shareholders with the board’s best guess as to how the group may perform during the next few years…

LTIP

- The preceding FY mentioned the group’s LTIP was unlikely to vest:

[FY 2024] “During the year we reintroduced a short-term incentive plan (STIP) for members of the executive committee and our three executive directors. We did this because in spite of the impressive turnaround in financial performance, the Long-Term Incentive Plan (LTIP) will likely not meet its lowest threshold even if revenue growth in the new financial year matches an exceptional FY24.”

- To recap, SYS1 introduced a new LTIP during FY 2017, extended it during FY 2019 and then modified it during FY 2021 with some vesting conditions reduced and the plan limit increased to 10% of the share count.

- No LTIP shares have vested since FY 2017 due to SYS1 failing to meet the scheme’s various targets — which since FY 2021 have included a £45m minimum-revenue goal.

- I am not truly convinced SYS1 needs an LTIP.

- LTIP participants historically forwent their annual bonuses, but the preceding FY introduced annual bonuses for the LTIP participants…

- …and the preceding FY’s new “performance culture” suddenly delivered SYS1’s highest profit for seven years that led to a reinstated dividend.

- Indeed, board remarks at the 2024 AGM said the bonuses “worked brilliantly“:

[AGM 2024] “One of the things we felt was really missing in the company was short-term incentives to drive the sales process. And it also gives us flexibility on our cost base if we don’t hit targets because obviously it’s very much variable and was based on huge stretch targets. And we’re delighted to say it worked brilliantly. There is no other word for it“

- Board remarks during the 2024 AGM also claimed an LTIP was needed to help staff retention and engender employee-shareholder alignment should the company grow “three, four, five times“:

[AGM 2024] “In principle, we think we do [need an LTIP]. A lot of it’s to do with the nature of the senior employees in the company, who are quite entrepreneurial and very ambitious. Some of them could, in different circumstances, go off and then start their own businesses.

A long-term scheme has much more capability to retain people for the long term rather than saying ‘we had a great year this year, can’t say we’re having a great year next year, so I’m out of here’.

We want the employees to be aligned with shareholders’ long-term vision for the business, and not focus very much on the short term.

The LTIP [allows employees to] benefit alongside shareholders. If we grow the company three, four, five times, where is the employee’s longer-term reward for being a big part of that? And the answer is the LTIP.“

- SYS1 announced its revised LTIP last month.

- As before, 10% of the share count could be awarded to participants, although the initial award covers 8%:

[RNS May 2025] “A maximum of 10% of the total share capital is capable of being awarded under the 2025 LTIP. 3.5% is initially awarded to Executive Directors and 4.5% to the wider executive team, with the balance currently reserved for new participants, if required.”

- Note that SYS1 founder/executive/22% shareholder John Kearon had participated in the previous LTIP, but does not participate in this new LTIP.

- The new LTIP covers FYs 2027, 2028 and 2029 and contains some striking maximum targets:

[RNS May 2025] “Full vesting of Options on the achievement of performance targets as follows:

o Revenue of £60m, £71.0m and £85.0m for the year ending 31 March 2027, 31 March 2028 and 31 March 2029 respectively, and;

o Adjusted Profit Before Tax of £10.5m, £15.3m and £20.0m for the year ending 31 March 2027, 31 March 2028 and 31 March 2029 respectively.

- I would happily issue SYS1’s managers 10% of the share count were revenue to reach £85m and adjusted pre-tax profit to reach £20m by FY 2029 (versus £37.4m and £5.2m indicated for FY 2025) (see Valuation).

- I am pleased the LTIP’s threshold targets were not reduced:

[RNS May 2025] “The Options vest over three vesting dates starting at the end of July 2027, subject to the achievement of threshold performance levels related to Revenue and Adjusted Profit Before Tax for the year ending 31 March 2027 of £46m and £5.9m respectively (“Threshold”)”

- The new LTIP’s threshold £46m revenue target is £1m greater than the minimum set by the previous LTIP…

- …while the new LTIP’s threshold £5.9m adjusted pre-tax profit target is much better than the old LTIP’s minimum £0 adjusted post-tax profit target.

- To achieve the new LTIP’s threshold targets by FY 2027, FY 2025 revenue must advance by 23% (11% CAGR) and FY 2025 pre-tax profit must advance by 13% (6.5% CAGR).

- Those threshold targets therefore appear extremely achievable, especially given this H1’s 20-30% platform-revenue CAGR ambition…

- …alongside the upgraded illustrative growth scenario:

- The new LTIP lifted the scheme’s share-price ‘underpin’ from 400p to 635p:

[RNS May 2025] “Share price underpin of £6.35 – equivalent to ca £80m market capitalisation – applies to the three vesting dates, being 31 July 2027, 31 July 2028 and 31 July 2029.”

- Although 635p is almost 50% greater than the recent 425p share price, the shares did trade for more than 635p for three months during 2024:

- Will the new LTIP encourage the workforce to grow the company “three, four, five times“ in size?

- The incentive is certainly there. Should the current market cap grow, say, 4x by FY 2029, a 10% maximum LTIP payout would equate to a collective £20m-plus windfall (see Valuation).

- But will the new LTIP reward employees for just a modest performance?

- Equalling the threshold targets pays out 12.5% of the LTIP’s options (equivalent to up to 1.25% of the share count)…

[RNS May 2025] “12.5% of the Options vest on achievement of Threshold, with proportional vesting from the Threshold through to 100% on achievement of Target performance. Revenue weighting is 60%, Adjusted Profit Before Tax weighting is 40%.”

- …which may be acceptable for FY 2027, but not very acceptable for FY 2028 and FY 2029 if SYS1’s performance shows further no improvement.

- Still, the shares have to reach 635p before any claims of unjust LTIP dilution can be made… and in the meantime SYS1 must first circumvent the “downside risk” to “clients’ budgets” due to the global economy.

Valuation

- April’s Q4 statement indicated an FY 2025 adjusted pre-tax profit of £5.2m, which after this H1’s 31% tax charge would create earnings of £3.6m or approximately 28p per share.

- The 425p shares are valued at 15x my 28p per share estimate, a rating that does not appear outrageous for a business that has signalled a 20-30% platform-revenue CAGR for the next three years.

- My valuation sums could be fine-tuned by:

- Excluding trademark-settlement income (£264k for this H1);

- Treating some of the FY 2025 £12.9m cash position as ‘surplus’, and;

- Investigating SYS1’s tax profile (point 26).

- The new LTIP suggests SYS1 has ambitions to create significant share-price upside.

- Assume the LTIP’s the maximum profit target is met and pre-tax profit does indeed quadruple from £5m to £20m by FY 2029, then I believe the market cap could easily quadruple beyond £200m and the share price then reach £16.

- Even greater share-price upside would be enjoyed were SYS1 to achieve this H1’s upgraded illustrative growth scenario:

- Assume revenue of £120m is achieved and does lead to an adjusted Ebitda of £36m, earnings may then approach £25m. I suspect the market cap could then easily surpass £300m and the share price could then reach £25.

- Is SYS1’s upgraded illustrative scenario actually achievable?

- Well, very few quoted small-caps are confident enough to provide tantalising illustrative projections of revenue and Ebitda… and I trust no sensible board would publish — and then upgrade! — such illustrative projections unless they were reasonably plausible.

- Grounds for long-term shareholder optimism include:

- The platform services still retain a ‘unique selling proposition of predictiveness’;

- Scores of new clients continue to be captured, while existing clients appear to be spending more;

- The group’s market share of its $10b-plus industry remains negligible;

- This H1 underpinned the “scalable business model” through record employee productivity and improved margins, and;

- The new LTIP will motivate the workforce to deliver an exceptional profit-growth performance.

- Grounds for long-term shareholder disappointment include:

- Despite the additional investment, TYI never takes off due to ineffective ‘fame building’ and/or having lost too much ground to rivals;

- TYA and/or US revenue growth falters as efforts to enhance the calibre of the workforce flounder;

- An adverse global economy exposes a greater-than-anticipated “downside risk” to client budgets;

- Platform growth slows because ‘data-led’ revenue does not keep pace with ‘data’ revenue, and;

- Ebitda margins do not improve as greater staff remuneration compensates for another LTIP failure.

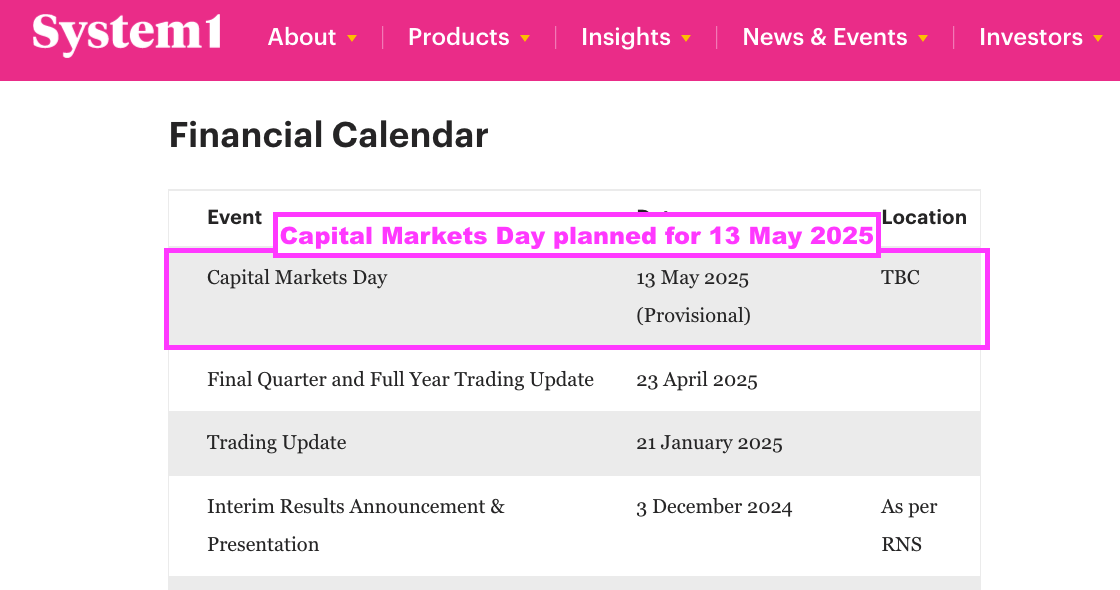

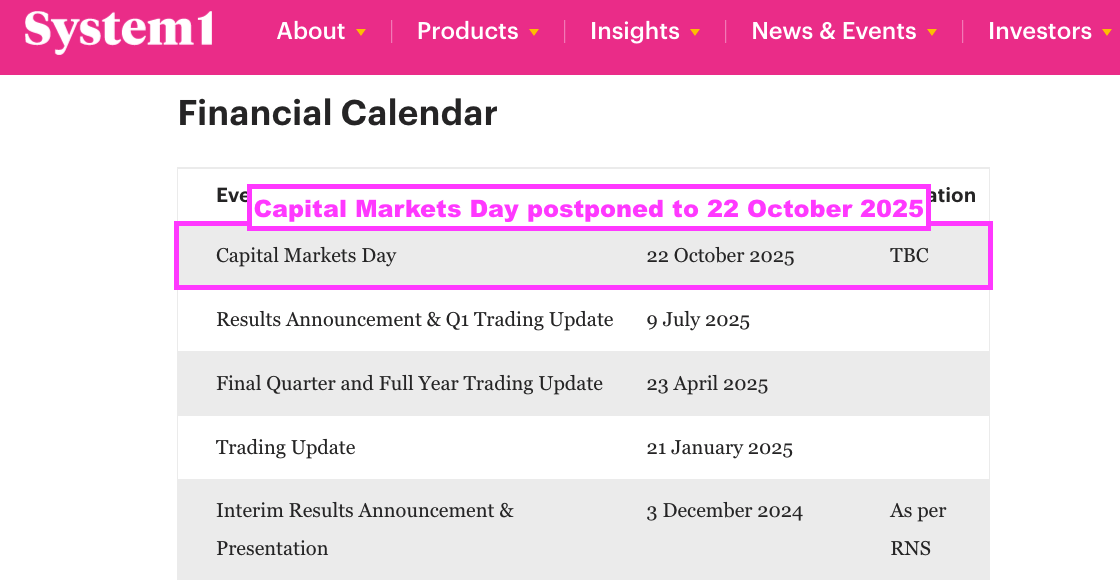

- SYS1 had planned a Capital Markets Day (CMD) for last month…

- …but subsequently postponed the event until October:

- Alongside the ominous developments within April’s Q4 statement, deferring the CMD for five months implies SYS1’s ‘3 Reasons to Believe’ may not be progressing quite as expected.

- Next month’s FY 2025 results and the accompanying Q1 2026 statement in particular have therefore taken on much greater significance.

- Another quarterly update that raises questions about TYA, US and/or ‘data-led’ revenue growth could easily lead shareholders to conclude the platform opportunity has stalled after only two years of significant progress.

- The preceding FY cited a 30-40% dividend payout policy, which applied to my 28p per share FY 2025 earnings guess gives a possible 10p per share dividend that supports a potential 2.5% income at 425p.

Maynard Paton

Hi Maynard

Regarding SYS1 latest results (y/e Mar25) – I know that you will look at them in detail at some point.