29 March 2025

By Maynard Paton

H1 2025 results summary for S & U (SUS):

- Yet more figures blighted by ongoing regulatory matters, with H1 profit slumping 40% and the dividend cut once again after “voluntary” motor-finance restrictions led to loan impairments surging 162%.

- The H1 performance was overshadowed by the Court of Appeal deeming the FCA’s disclosure rules on car-loan commissions to be unlawful. The Supreme Court will hear the cases next week and the “definitive pronouncement” declared thereafter.

- Given the £14 shares trade at 0.73x NAV — a rating last seen at the banking-crash lows — investors have seemingly decided SUS could be liable to repay ‘secret’ commissions of up to £63m… although the “appropriate compensation” could arguably be minimal.

- Debt headroom of £88m, a shift towards “lower-risk” motor-finance customers alongside “sparkling” progress at the (unregulated) property-loan division (H1 profit up 42%!) may help SUS muddle through any “industry-wide redress scheme“.

- Then again, post-H1 updates did not bode well following another dividend cut and the motor-finance division curtailing lending by 33% and suffering a further 50% profit reduction. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own SUS

- Results summary

- Revenue, profit, net asset value and dividend

- Advantage Finance: Borrowers in Financial Difficulty

- Advantage Finance: Consumer Duty and Skilled Person

- Advantage Finance: loan volumes and rates

- Advantage Finance: revenue and cost of sales

- Advantage Finance: first payments

- Advantage Finance: collections

- Advantage Finance: up-to-date and overdue accounts

- Advantage Finance: impairments

- Advantage Finance: Court of Appeal judgements

- Advantage Finance: Supreme Court hearing and FCA intervention

- Advantage Finance: potential ‘secret’-commission compensation

- Aspen Bridging

- Boardroom

- Financials

- H2 2025 trading updates

- Valuation

News links, share data and disclosure

- Interim results, presentation and webinar for the six months to 31 July 2024 published/hosted 08 October 2024;

- Update on Advantage Finance Limited published 14 October 2024;

- Update on Advantage Finance Limited published 29 October 2024;

- Trading statement published 11 December 2024, and;

- Trading statement published 11 February 2025.

- Share price: 1,400p

- Share count: 12,150,760

- Market capitalisation: £170m

- Disclosure: Maynard owns shares in S & U. This blog post contains ShareScope affiliate links.

Why I own SUS

- Provides ‘non-prime’ credit to used-car buyers and property developers, where disciplined lending and reliable service have supported an illustrious NAV and dividend record.

- Boasts veteran family management with a 40-year-plus tenure, 52%/£89m shareholding and a “steady, sustainable” and organic approach to long-term expansion.

- Adverse regulatory and legal developments within the motor-finance sector have depressed the market cap to well below net asset value, which should offer upside if the industry-wide problems recede and greater market share is captured.

Further reading: My SUS Buy report | All my SUS posts | SUS website

Results summary

Revenue, profit, net asset value and dividend

- This H1 was never going to impress after adverse trading statements during June…

[RNS June 2024] “The overall result for the Group is that whilst customer numbers and net receivables continue to grow, albeit more slowly at £478m, Group profit before tax for the first quarter fell to £6.9m (2023: £10.5m) on net assets of £235m (2023: £228m). Increased impairment provisioning arising from the lower repayments at Advantage accounted for £3.6m of this reduction.“

- …and September…

[RNS September 2024] “Whilst Advantage continues to actively pursue a conclusion of negotiations with the FCA for a removal of the restrictions soon, their cumulative impact on Advantage Finance’s profitability has caused Advantage’s first half profitability to fall below expectations. As a result, Group profits in H1 are expected to be c.£12.8m and this is likely to cause the Group’s financial year profitability to 31 January 2025 to fall below market expectations.“

- …had warned of ongoing regulatory matters leading to additional loan impairments within SUS’s motor-finance division (see Advantage Finance: Borrowers in Financial Difficulty and Advantage Finance: impairments).

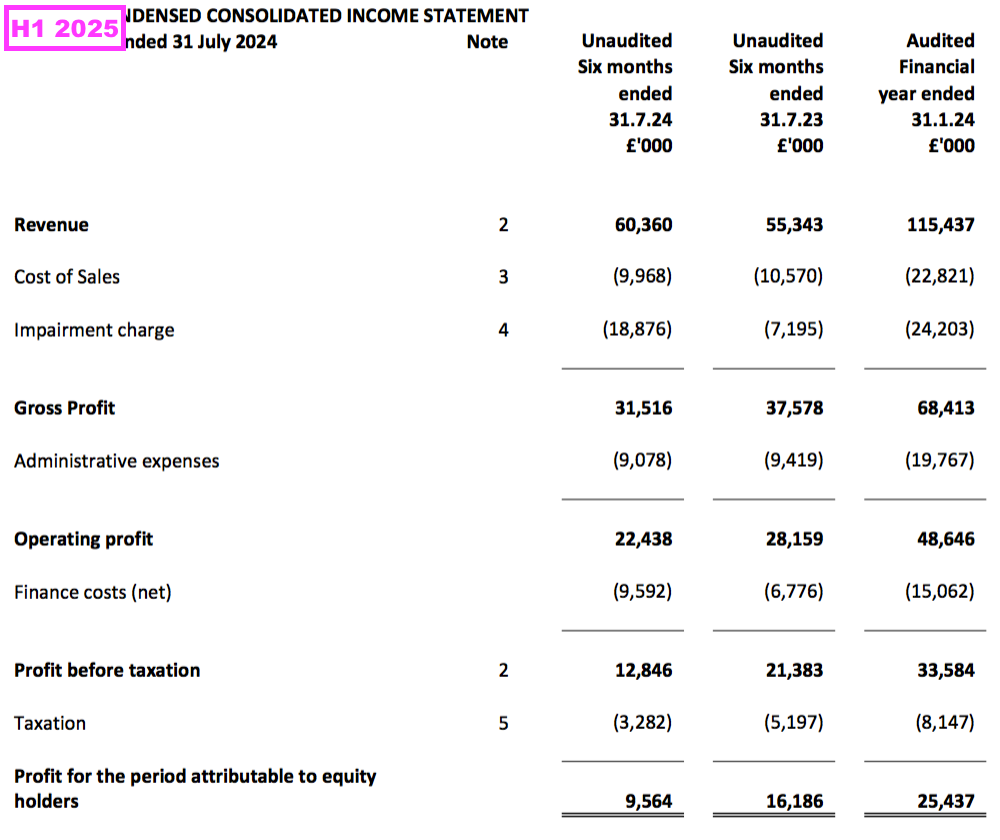

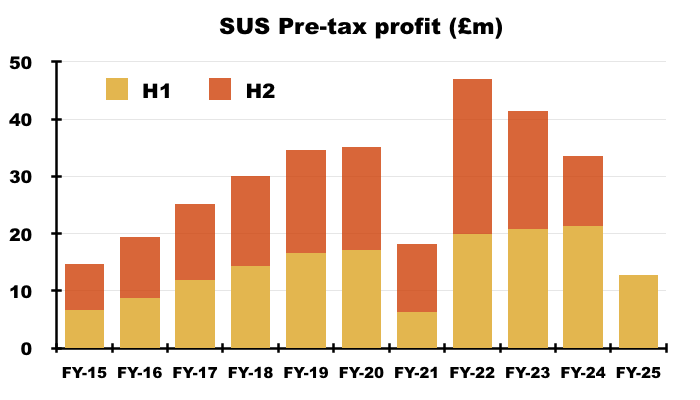

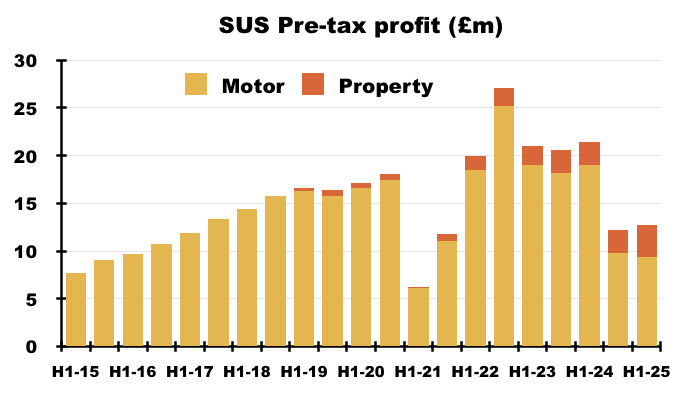

- H1 pre-tax profit was indeed £12.8m, down 40%, as SUS had predicted during September:

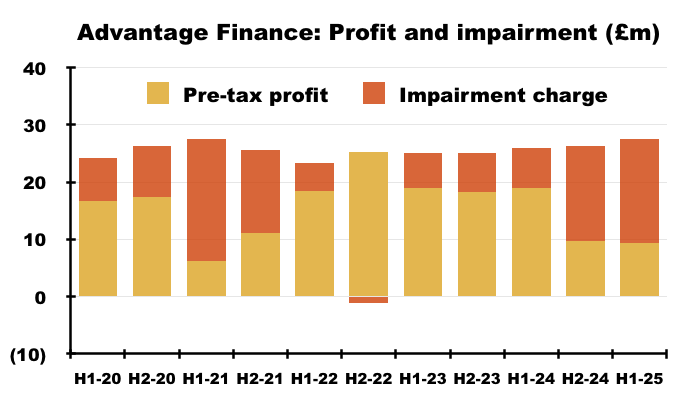

- The H1 profit slump matched that of the preceding H2, during which pre-tax profit fell 41% to £12.2m following similar motor-loan impairments.

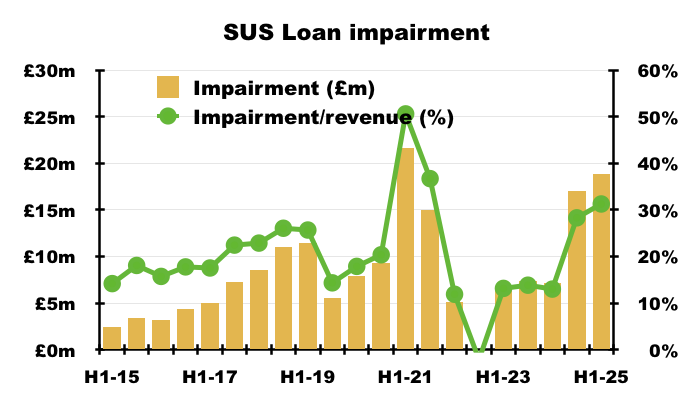

- Total H1 loan impairments surged 162% to £18.9m and absorbed a substantial 31% of H1 revenue:

- The 162% surge was amplified by “lower than normal” impairments recorded during the preceding H1:

[H1 2024] “Impairment charge of £6.8m (H1 2022: £6.1m) still lower than normal as an increase in receivables mitigated by good collections and lower than anticipated realised bad debts and voluntary terminations.“

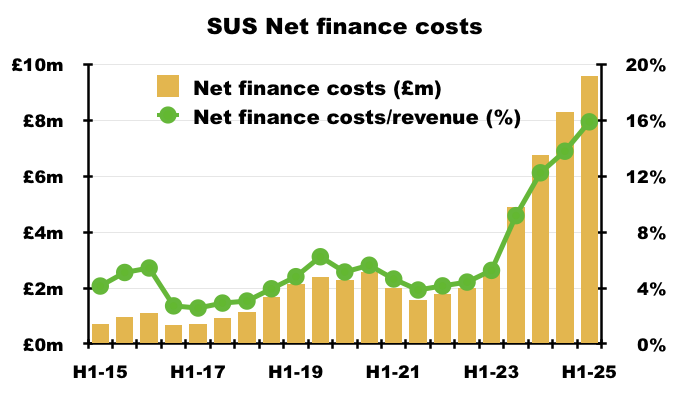

- Alongside the greater loan impairments, H1 net finance costs increased 42% to £9.6m to absorb 16% of H1 revenue (see Financials):

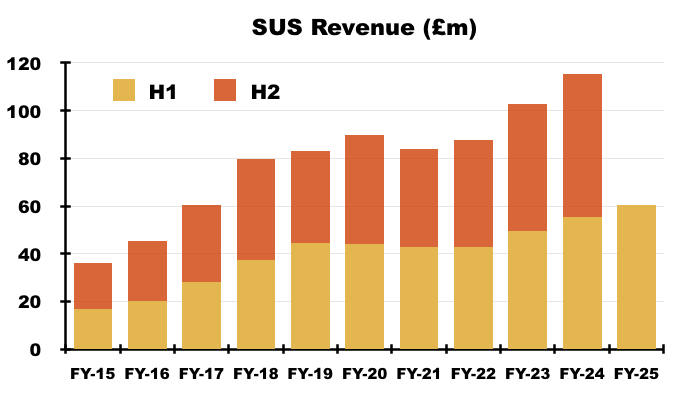

- The lower profit was declared despite H1 revenue gaining 9% to £60.4m, which in fact set a new record for any H1 or H2:

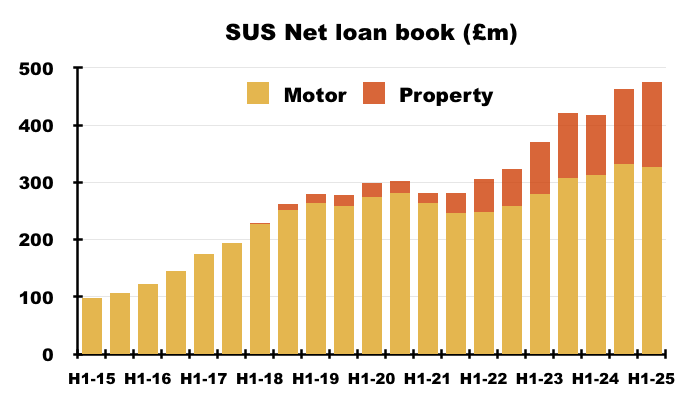

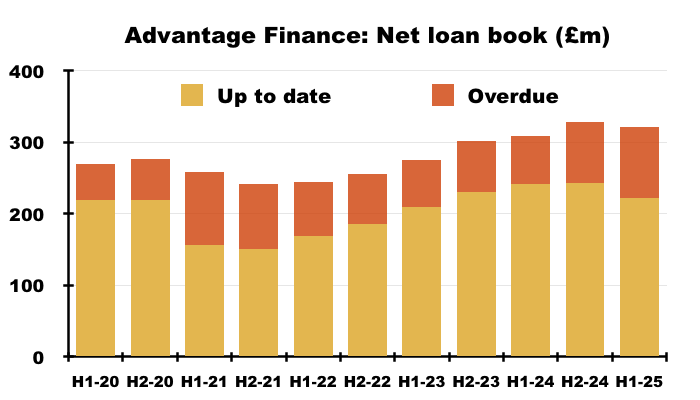

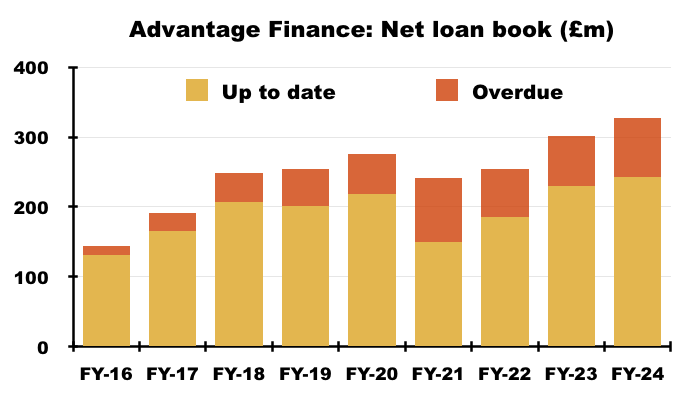

- The accounts continue to be dictated by SUS’s motor-loan division, Advantage Finance, although SUS’s property-loan division, Aspen Bridging, is (thankfully) becoming a greater part of the group:

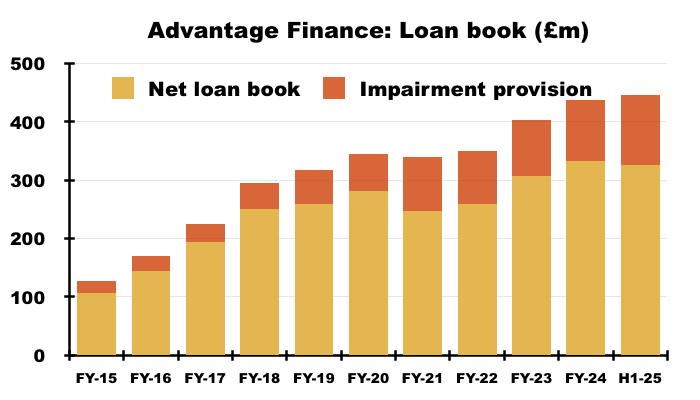

- This H1 witnessed the group’s net loan book advance approximately £12m, or 3%, to £475m. The £12m advance was split between a £6m decrease to the motor-finance book (see Advantage Finance: loan volumes and rates) and a near-£19m advance to the property-finance book (see Aspen Bridging).

- Aspen’s larger loan book was funded by greater group debt, which during this H1 expanded by £15m to £240m (see Financials).

- This H1’s reduced £12.8m pre-tax profit converted into earnings of £9.6m, which did not cover the £10.3m (35p and 50p per share) paid as dividends during the half.

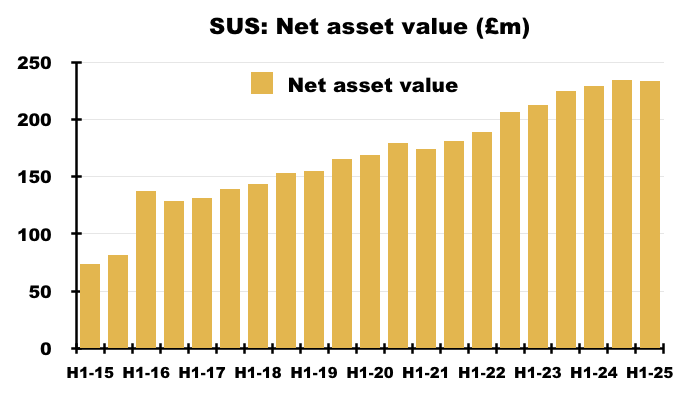

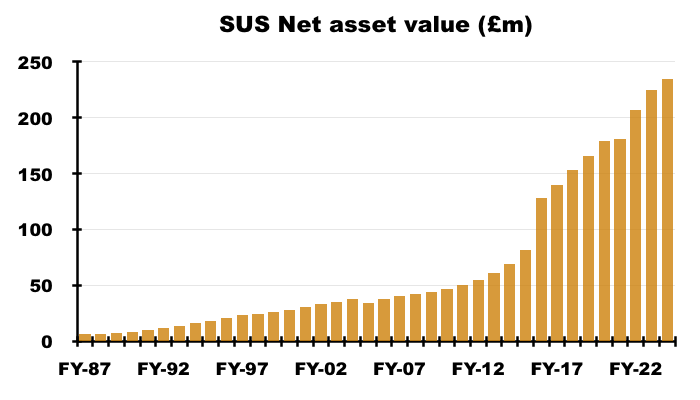

- The £0.7m shortfall between H1 earnings and paid dividends therefore left SUS’s net asset value (NAV) £0.7m lower at £233m — equivalent to £19.21 per share:

- The £233m NAV significantly exceeds the £170m market cap (see Advantage Finance: Court of Appeal judgements and Valuation).

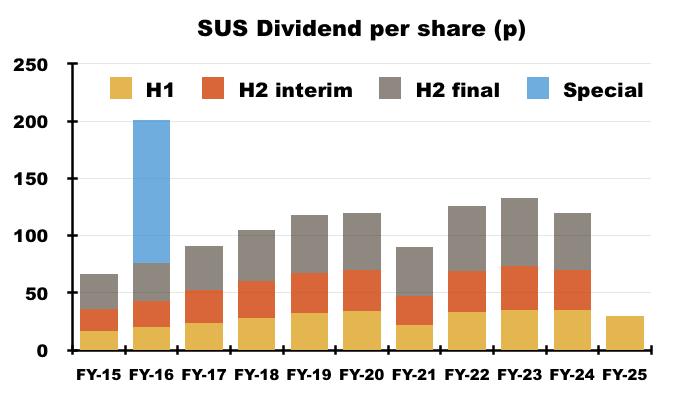

- This H1 continued SUS’s run of unfortunate dividend news.

- An RNS during February 2024 had blamed “the cost of living, funding and regulatory challenges” for reducing the second interim dividend of FY 2024 by 3p to 35p per share.

- The preceding FY then cut the final FY 2024 dividend by 10p to 50p per share following higher salaries, higher interest and higher taxes.

- This H1 then cut the H1 dividend by 5p to 30p per share following the aforementioned 40% lower profit:

“Given S&U’s shareholding structure and its relatively limited free float, it has been our consistent aim to ensure shareholder returns through dividends, provided these are sustainable. Lower than normal projected group profits this year, though temporary, will not alter this aim. The board therefore conclude that the first of three dividend payments this year will be 30p per share (2023: 35p). The first dividend will be paid on 22 November 2024 to shareholders on the register on 1 November 2024.”

- The run of dividend cuts has extended beyond this H1, with an RNS last month reducing the H2 2025 second interim dividend by 5p per share (see H2 2025 trading updates).

- SUS’s twelve-month trailing dividend is presently 110p per share versus 133p per share declared for FY 2023.

- The forthcoming FY 2025 statement could extend the run of dividend cuts further. An update during December implied Advantage’s H2 profit might be “around half” that of H2 2024 (see H2 2025 trading updates).

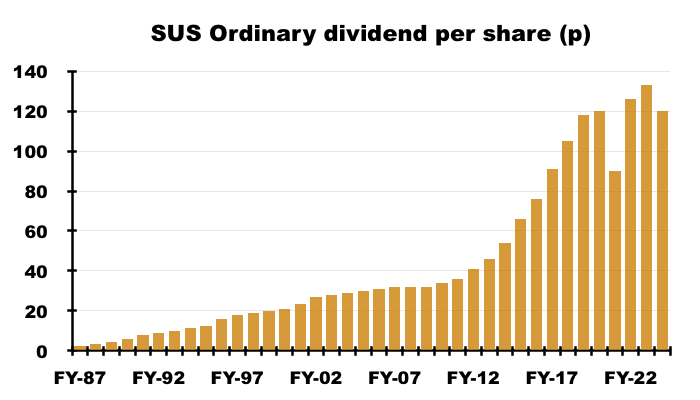

- Prior to the pandemic, SUS had not reduced its annual dividend since 1987:

Advantage Finance: Borrowers in Financial Difficulty

- Advantage Finance was established during 1999 and provides buyers of used cars with hire-purchase loans of between £2k and £20k.

- The preceding FY outlined how Advantage’s customers typically possess low credit scores:

[FY 2024] “This long experience has enabled Advantage to gain a significant understanding of the kind of simple hire-purchase motor finance suitable for customers in lower and middle-income groups. Although decent, hardworking and well intentioned, some of these customers may have impaired credit records, which have seen them in the past unable to access rigid and inflexible “mainstream” finance products.”

- Customers are acquired through finance brokers and car dealers (see Advantage Finance: Court of Appeal judgements), and often receive their loans on the day of their application and do not need to provide a deposit.

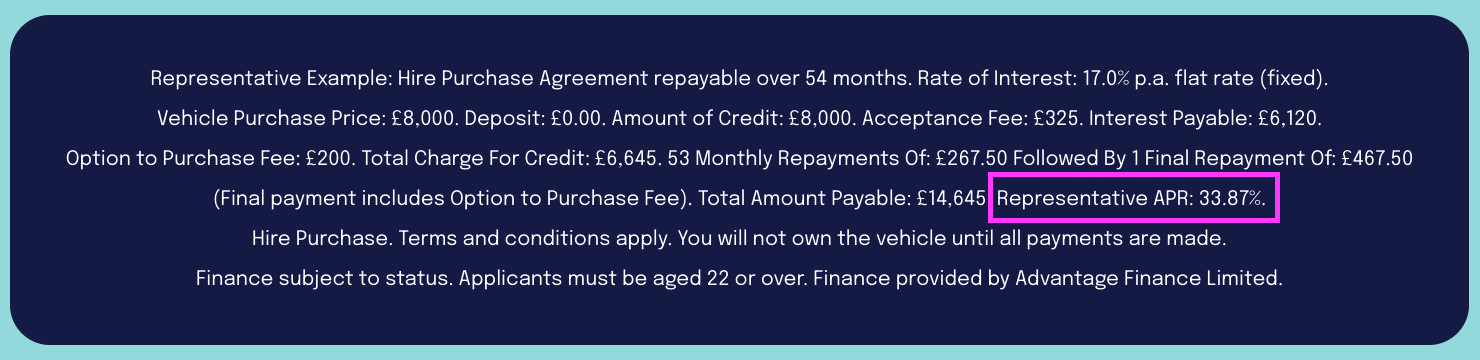

- Advantage cites a representative APR of 33.87%:

- The representative example indicates borrowing £8.0k at a flat 17% a year over 54 months leads to interest of £6.1k and a total repayable of £14.6k including a £325 acceptance fee and a £200 vehicle-purchase fee.

- Recent years have witnessed Advantage and the wider motor-finance sector attract greater regulatory attention.

- This H1 noted the “increasingly interventionist stance from the Financial Conduct Authority” at Advantage:

“During the [six] months to 31 July 2024, the trading environment for S&U and especially Advantage operating in the regulated sector was challenging. Increases in taxation, interest rates and the cost of living brought forth an increasingly interventionist stance from the Financial Conduct Authority (FCA).“

- This H1 also listed the FCA’s “recent wave of initiatives“:

“Although it is in Advantage’s very DNA to nurture their valuable customers, the recent experience has led them to address the challenges posed by an evolving regulatory landscape. It is to be hoped that the recent wave of initiatives including the FCA’s forbearance review, the bedding down of Consumer Duty, the borrowers in financial difficulty (BIFD) initiative, the interaction with CONC rules and the impending updating of the 50-year-old Consumer Credit Act will lead to a period of relative stability.”

- To recap, the FCA’s “wave of initiatives” commenced with its Tailored Support Guidance (TSG), which addressed how lenders should handle borrowers suffering payment difficulties caused by the pandemic.

- The FCA’s Borrowers in Financial Difficulty (BiFD) project then assessed how lenders had met the TSG.

- An FCA follow-up to the BiFD project then proposed various “forbearance” changes as “consumers…faced increased financial challenges due to the rising cost of living“.

- The FCA’s proposals (Annex D) were written into the Consumer Credit sourcebook (CONC) during November 2024.

- The general implications for Advantage (and other motor-finance lenders) are:

- More information must now be obtained from customers before lending;

- More customers may now be deemed to suffer from payment difficulties;

- Customers suffering payment difficulties may now be given more leeway to repay their loans, and;

- Vehicle repossessions may now become more difficult to undertake.

- The FCA’s policy statement widened the scope of customers who could now seek “forbearance” options.

- In particular, FCA rules previously concerning “particularly vulnerable” customers now apply to just “vulnerable” customers, while rules previously concerning customers “in arrears” now apply to customers “in or approaching arrears“.

- The revised FCA rules suggest a customer “approaching arrears” may become known to Advantage sooner than before:

[FCA PS24/2] “A firm should regard a customer as approaching arrears when the customer indicates to the firm that they are at risk of not meeting one or more repayments when they fall due.”

- Forbearance measures now include accepting “no payments“…

[FCA PS24/2] “Examples of treating a customer with forbearance and due consideration would include the firm…

…accepting no payments, reduced payments or token payments”

- …and re-arranging payments over an (unspecified) “reasonable” period of time:

[FCA PS24/2] “…agreeing a repayment arrangement with the customer that allows the customer a reasonable period of time to repay the debt“.

- The revised FCA rules also mention the “individual circumstances of the customer“…

[FCA PS24/2] “When determining appropriate forbearance and treating the customer with due consideration, a firm must take into account the individual circumstances of the customer of which the firm is or should be aware.”

- …which must now be “sufficiently detailed“:

[FCA PS24/2] “the assessment should be informed by sufficiently detailed information;“

- Customer details include essential living expenses that may now go beyond “mortgage, rent, council tax, food and utility bills”:

[FCA PS24/2] “Priority debts and essential living expenses include, but are not limited to, payments for mortgage, rent, council tax, food and utility bills.”

- And significantly, vehicles can now only be repossessed as a “last resort“:

[FCA PS24/2] “A firm must not take steps to repossess a customer’s home, goods or vehicles other than as a last resort, having explored all other possible options.”

Advantage Finance: Consumer Duty and Skilled Person

- Overlaying the new BiFD rules is the FCA’s additional Consumer Duty principle of ensuring “good outcomes for retail customers“:

[FCA PS24/2] “Principle 12 (a firm must act to deliver good outcomes for retail customers), including PRIN 2A “

- The FCA states Consumer Duty “sets higher and clearer standards of consumer protection across financial services and requires firms to put their customers’ needs first.”

- Under Consumer Duty, lenders such as Advantage must:

[FCA March 2025]

“Monitor and regularly review the outcomes their customers are experiencing.

Identify where customers or groups of customers are not getting good outcomes and understand why.

Have processes in place to adapt and change products and services, or policies and practices, to address any risks or issues identified and stop them occurring in the future.”

- In addition, to ensure customers in “vulnerable circumstances” receive “outcomes as good as those for other customers“, lenders such as Advantage should:

[FCA March 2025]

“Implement appropriate processes to evaluate where they have not met the needs of customers in vulnerable circumstances, so that they can make improvements.

Produce and regularly review relevant management information on the outcomes they are delivering for customers in vulnerable circumstances.

Ensure that firms they work with treat customers in vulnerable circumstances fairly, particularly where they rely on third party providers and outsourcers, through ongoing due diligence.”

- This H1 referred to a section 166 notice and “voluntary” operational restrictions:

“For S&U itself, this has resulted over the past year in the focus of the FCA’s attention on Advantage Finance. On the initial basis of only 10 customer files, a s166 notice (swiftly followed by adoption of “voluntary” restrictions) has significantly constrained Advantage’s ability to interact with and manage its traditional customers, with whom it has happily worked for the past 25 years.”

- A section 166 notice is issued by the FCA and instructs a regulated firm to appoint a ‘Skilled Person’ to investigate the firm’s activities. The Skilled Person then reports back to the regulator.

- SUS confirmed during December 2023 that Advantage had appointed a Skilled Person to help implement BiFD and Consumer Duty:

[RNS December 2023] “Following the FCA’s special focus on Borrowers in Financial Difficulty (BiFD) in non-prime motor finance, the “review of Advantage’s, collecting processes, procedures and policies” we noted at half year, has developed into a more formal interaction with the FCA.

Along with many other lenders in our market segment, Advantage has appointed a Skilled Person. They are tasked, where necessary, to advise and guide Advantage in delivering, these regulatory requirements.

- SUS at the time warned the Skilled Person’s work would not be quick nor cheap:

[RNS December 2023] “This may be a lengthy and costly process, but it should prove valuable in providing assurance on our longstanding methods of serving our customers, and ensuring, that our products continue to meet their differing needs.“

- By February 2024, Advantage was making “precautionary changes to its collection and repossession processes” because of the Skilled Person’s review:

[RNS February 2024] “During this period, the interaction with the FCA, through our Skilled Advisor appointed as part of their industry wide investigation into customer forbearance and affordability, has deepened.

In response to this, Advantage has made precautionary changes to its collection and repossession processes with a particular focus on those customers in payment arrears, or who are identified as vulnerable. Given the evolving demands of the regulatory landscape, operating within them will require a proportionate and constructive dialogue between Advantage and the regulator.”

- By June 2024, implementing BiFD and Consumer Duty through the Skilled Person had caused Advantage to suffer a “significant impact on repayments and profitability“:

[RNS June 2024] “At Advantage, our cautious approach to repayments in the light of continuing discussions with the FCA and Skilled Person on interpreting and adapting to the new Consumer Duty regime and the sector wide review of Borrowers in Financial Difficulty, have had a significant impact on repayments and profitability. We anticipate that these discussions will be concluded during the second half of the year, when we will welcome the new regulatory clarity which will provide a strong platform for the continuing growth of the business.”

- A statement during August 2024 then emphasised the aforementioned “voluntary” restrictions imposed on Advantage by the FCA via the Skilled Person’s review, and the knock-on impact those restrictions had on customer collections:

[RNS August 2024] “In the motor finance sector, however, Advantage Finance, which has just celebrated an excellent 25 years in business, continues its period of consolidation and retrenchment. This has resulted from a period of restrictions and caution arising from a Financial Conduct Authority (“FCA”) section 166 notice and the constructive but vigorous negotiations taking place to remove the restrictions, which are now nearing their conclusion. These negotiations will determine a second contrast between a significant impact on Advantage’s profitability in the first half (primarily resulting from restrictions on its collections capabilities)”.

- And by September 2024, SUS acknowledged the FCA’s restrictions had led to Advantage’s profit for this H1 to “fall below expectations”:

[RNS September 2024] “As previously referenced in the Group’s announcement on 12 August the cautious approach and business retrenchment adopted by Advantage Finance, the Group’s motor finance division, since the imposition of the Financial Conduct Authority’s (“FCA”) Section 166 notice have continued to impact the performance of the division, primarily resulting from restrictions on its collections capabilities.

Whilst Advantage continues to actively pursue a conclusion of negotiations with the FCA for a removal of the restrictions soon, their cumulative impact on Advantage Finance’s profitability has caused Advantage’s first half profitability to fall below expectations.”

- With BiFD and Consumer Duty combining to reduce Advantage’s ability to collect payments from “vulnerable” borrowers and therefore leading to greater bad loans (see Advantage Finance: impairments), this H1 unsurprisingly announced Advantage was seeking “lower-risk” customers:

“Meanwhile, Advantage’s risk appetite statement has been revised and new quarterly reports produced on productivity and customer contact. The former is leading to a movement towards lower-risk customers with greater affordability where potential vulnerabilities are less.”

- The search for “lower-risk” customers also reduced the number of new H1 loans issued by Advantage (see Advantage Finance: loan volumes and rates).

- Following this H1, a statement during October announced the “voluntary” FCA restrictions had been lifted:

[RNS October 2024] “S&U, the specialist motor and property financier, today announces that the collection process restrictions for Advantage Finance Limited, S&U’s motor finance subsidiary, have now been successfully lifted with the agreement of the Financial Conduct Authority (FCA).”

- The H1 webinar claimed Advantage had enjoyed a relatively early exit from the restrictions:

“We do believe that we are first out of the gates so far as responding to a Section 166 is concerned.”

- But that October RNS did reveal the FCA discussions were continuing:

[RNS October 2024] “Regulatory discussions are still ongoing and we anticipate they will also move towards a successful conclusion.“

- I speculate such FCA discussions concern potential redress following the Skilled Person’s BiFD/Consumer Duty review.

- In particular, the preceding FY admitted “enhancements may be required” to Advantage’s BiFD processes…

[FY 2024] “Our motor finance subsidiary Advantage was included in the FCA’s multi-firm Cost of Living Forbearance Outcomes review in 2023 and as a result the FCA concluded that enhancements may be required to Advantage’s approach to arrears management and the application of forbearance.”

- …and potential redress perhaps being finalised during last summer:

[FY 2024] “Advantage and the FCA have been in correspondence throughout 2023/24 to discuss and agree the necessary steps and Advantage will carry out an assessment of whether any customers were adversely affected by its practices. Where this is found to be the case Advantage will seek to redress any detriment.

The financial effect of any customer redress cannot be reliably assessed at this early stage of the review. This ongoing assessment is expected to be in advanced stages in Summer 2024, with any redress being made after that.”

- But this H1 instead confirmed “enhancements were required” to Advantage’s BiFD processes…

“Our motor finance subsidiary Advantage was included in the FCA’s multi-firm Cost of Living Forbearance Outcomes review in 2023 and as a result the FCA concluded that enhancements were required to Advantage’s approach to arrears management and the application of forbearance.”

- …and potential redress perhaps being finalised during last autumn:

“Advantage and the FCA have been in correspondence throughout 2023/2024 to discuss and agree the necessary steps and Advantage will carry out an assessment of whether any customers were adversely affected by its practices. Where this is found to be the case Advantage will seek to redress any detriment.

The financial effect of any customer redress cannot be reliably assessed at this stage of the review. This ongoing assessment is now expected to be in advanced stages in Autumn 2024, with any redress being made after that.”

- The prolonged finalisation of any BiFD redress is not encouraging. But the H1 webinar claimed the Skilled Person and the FCA dictated the pace at which potential BiFD redress is calculated:

“I would not necessarily agree that bad numbers always need to take longer to add up… The pace of the [redress] work is entirely at the behest of the Skilled Person and the regulator as to the expectation of it. What I would say on our side, because it’s a joint responsibility, crunching the numbers does take a fair amount of time, and the pace of that is really due to three parties being involved at the same time”

- While the possible BiFD redress remains unquantified, the preceding FY did reveal an extra £1.5m compliance expense:

[FY 2024] “Administrative expenses [at Advantage] increased by 25% reflecting continued staff cost inflation and an extra £1.5m spent on regulatory costs this year.“

- The H1 webinar suggested ongoing compliance costs would not be “excessively higher”.

- The potential BiFD redress is in addition to SUS paying potential compensation following the Court of Appeal’s judgements concerning ‘secret’ commissions paid by motor-finance lenders to car dealers (see Advantage Finance: Court of Appeal judgements).

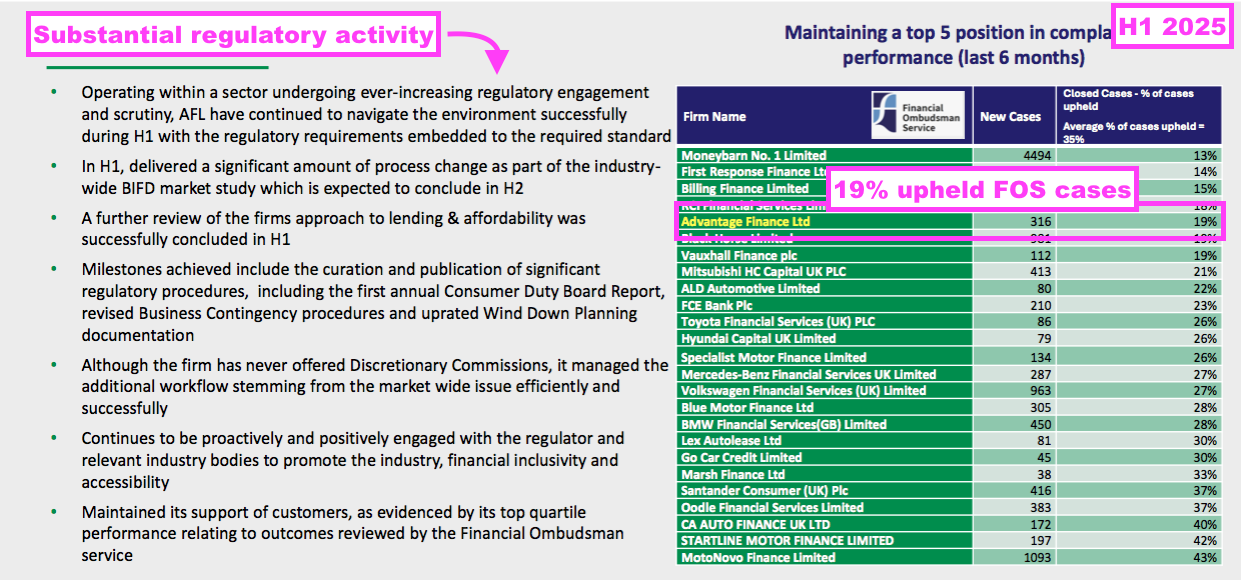

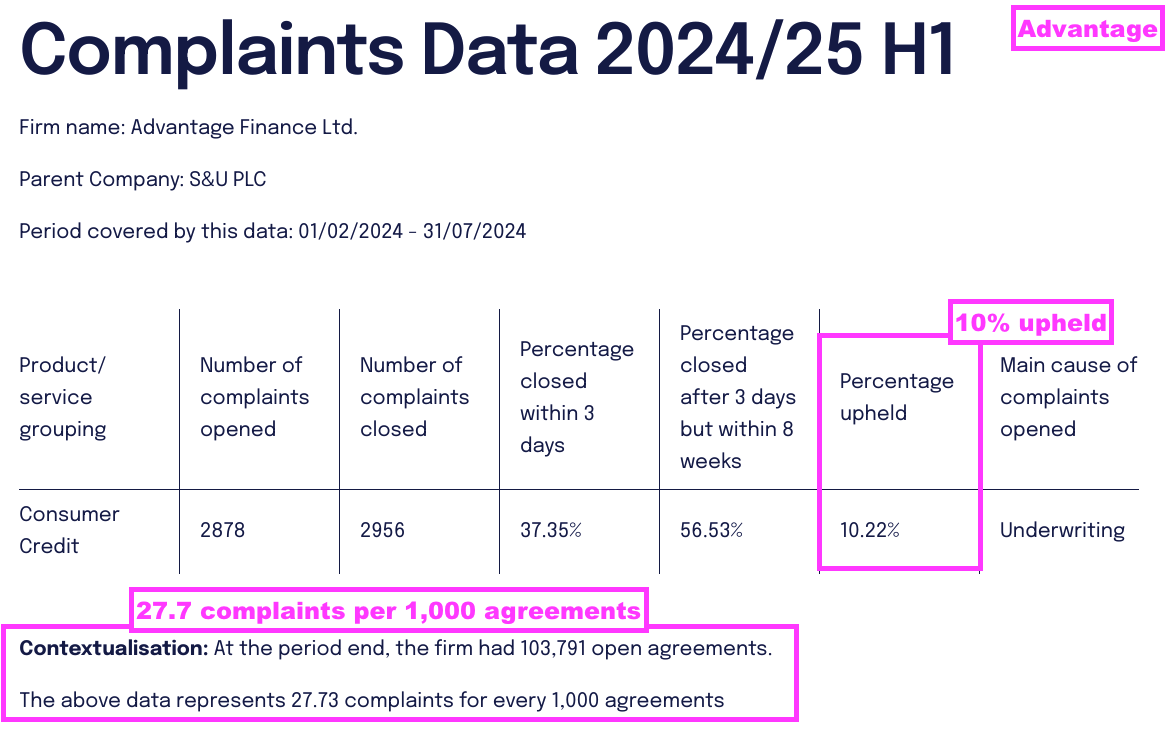

- BiFD-like redress continues to be sought by borrowers through the Financial Ombudsman Service (FOS), which lists all the complaints against Advantage.

- During this H1, only two cases of “irresponsible” lending against Advantage were upheld by the FOS (here and here).

- This H1 said the FOS upheld a relatively low 19% of cases against Advantage:

- Advantage indicates an upheld rate of 10% for all complaints:

- Highlighting the greater desire for customers to complain, the number of complaints per 1,000 agreements was 27.7 during this H1 versus 18.9 for the preceding H2 and 14.5 for the comparable H1.

- One regulatory issue thankfully not impacting SUS directly concerns the FCA’s investigation into motor-finance discretionary commission arrangements (DCAs), which is a matter separate to the ‘secret’ commissions ruled by the Court of Appeal.

Advantage Finance: loan volumes and rates

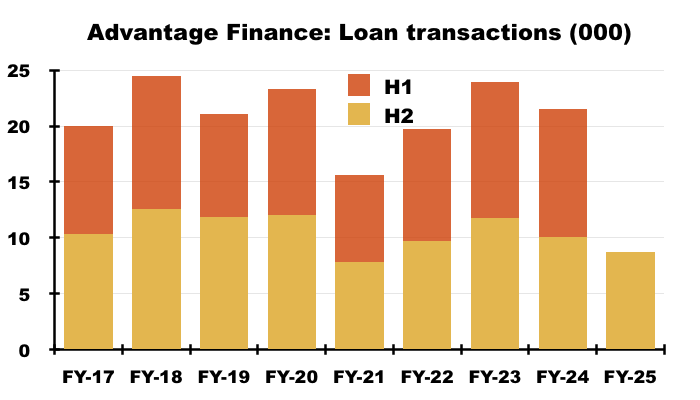

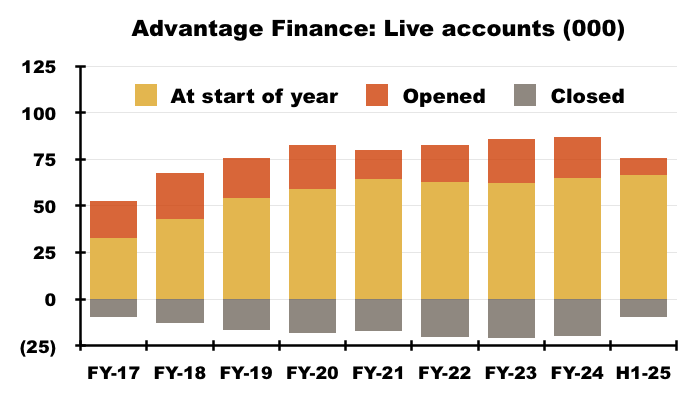

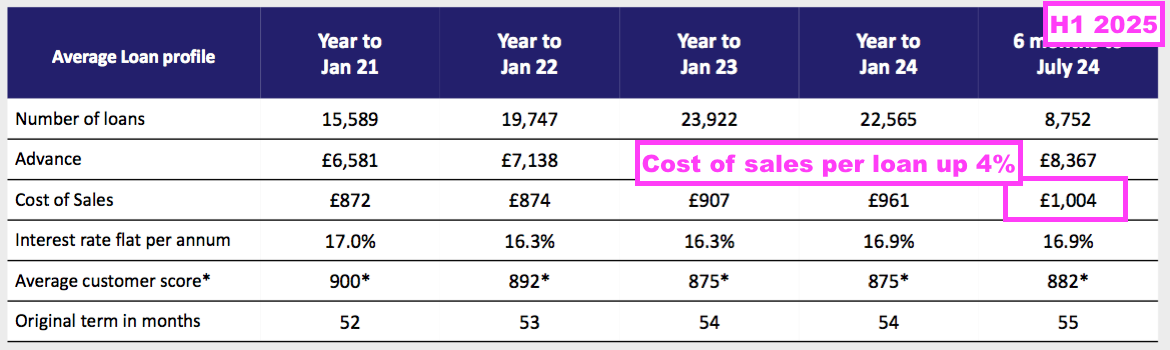

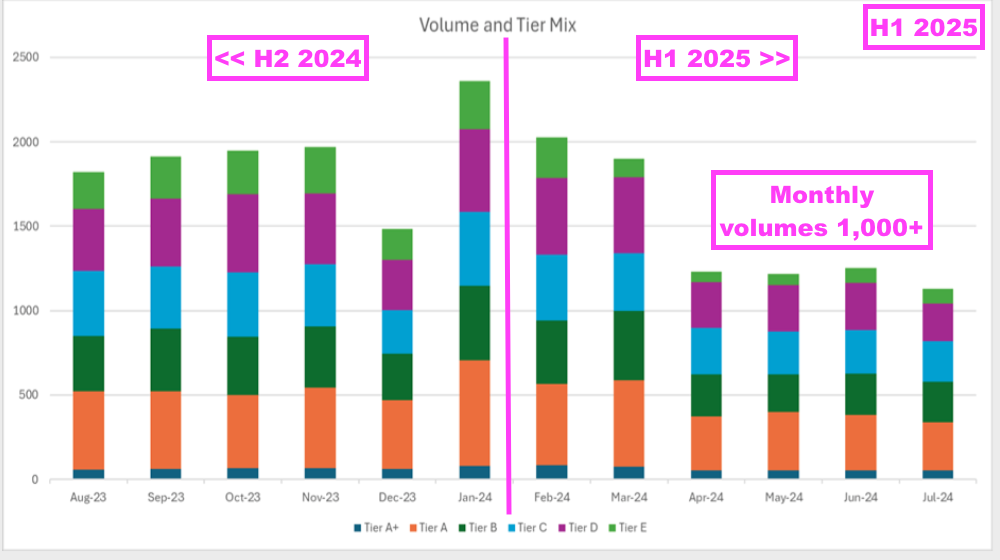

- The aforementioned Skilled Person’s review and “voluntary” operational restrictions led to this H1 witnessing Advantage issue 8,752 loans — down 13% on the comparable H1:

- Doubling up this H1’s 8,572 new loans gives 17,504 — a figure less than the 20,042 new loans issued during FY 2017 and which emphasises Advantage’s aforementioned shift towards “lower-risk” borrowers.

- The 13% lower volume of loans was not due to a lack of wider customer demand. In fact, this H1 confirmed a “healthy market” with applications up 22%:

“…since loan applications were 22% higher, this points to a healthy market but an increasingly cautious underwriting appetite.”

- The preceding FY reported two million-plus unique motor-finance applications while FY 2023 disclosed a “fairly consistent” 30-35% approval rate.

- Therefore for this H1, perhaps 1.2 million H1 applications were reduced to, say, 400,000 successful applications, of which only 8,752 — or 2% — then converted into actual loans.

- SUS has in the past claimed “digital tyre kickers” have limited Advantage’s conversion rate to low single digits, but the low conversion may also reflect Advantage losing out to the dubious commission practices of rival lenders (see Advantage Finance: Court of Appeal judgements).

- This H1’s reduction to new loans clearly started during April 2024:

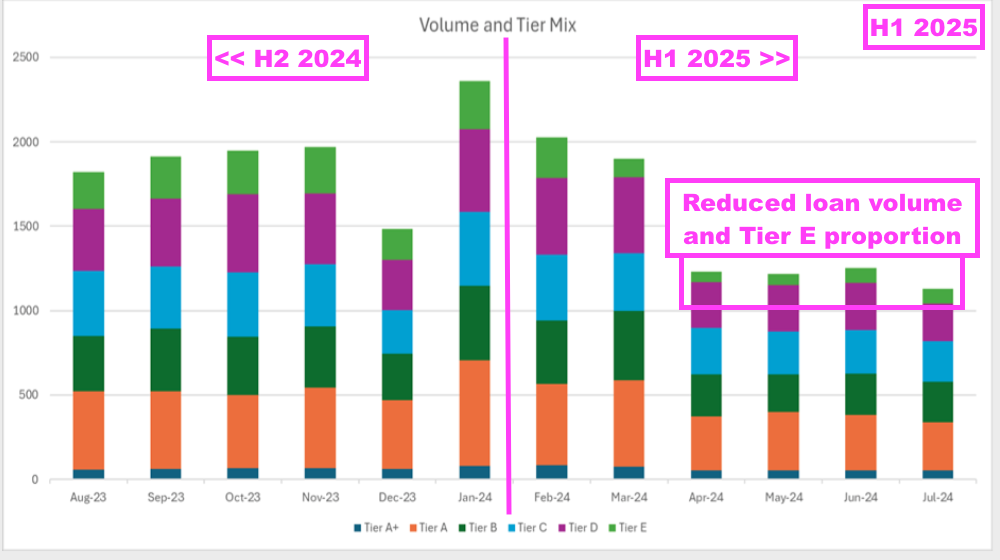

- Mind you, the aforementioned shift to less “vulnerable” customers…

“Meanwhile, Advantage’s risk appetite statement has been revised and new quarterly reports produced on productivity and customer contact. The former is leading to a movement towards lower-risk customers with greater affordability where potential vulnerabilities are less.”

- …seemed in reality to reduce only the proportion of the riskiest tier E borrowers.

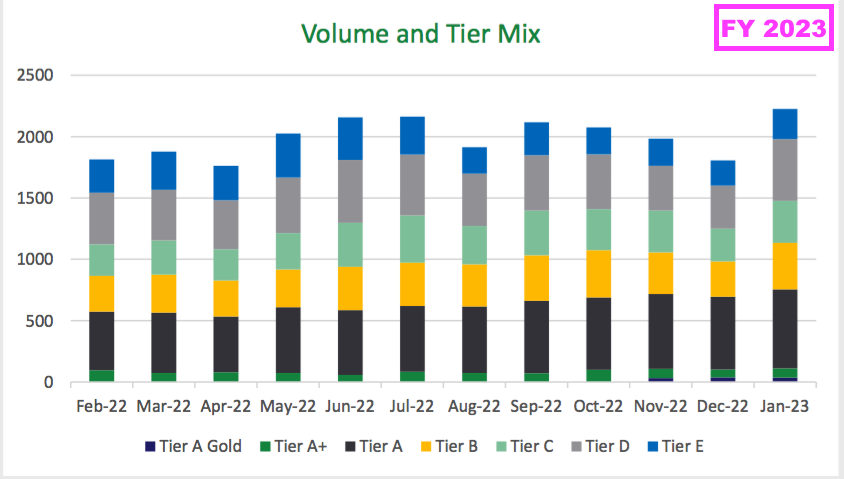

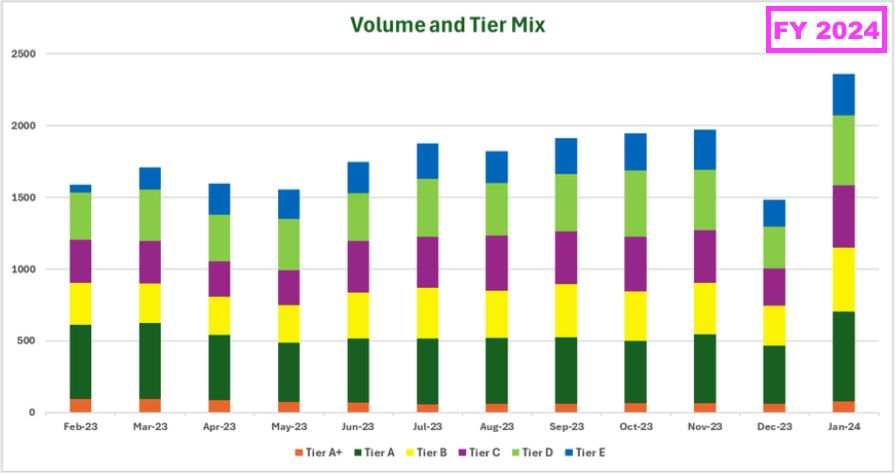

- From what I can tell, the higher quality tier A+/A borrowers continue to represent approximately 28% of the total mix.

- Indeed, looking back at the tier mixes for FYs 2023 and 2024…

- …this H1’s tier mix does not appear obviously different.

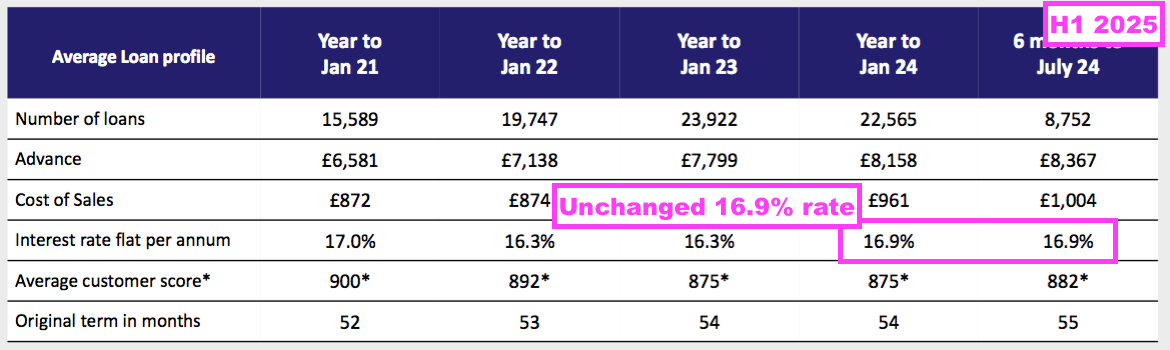

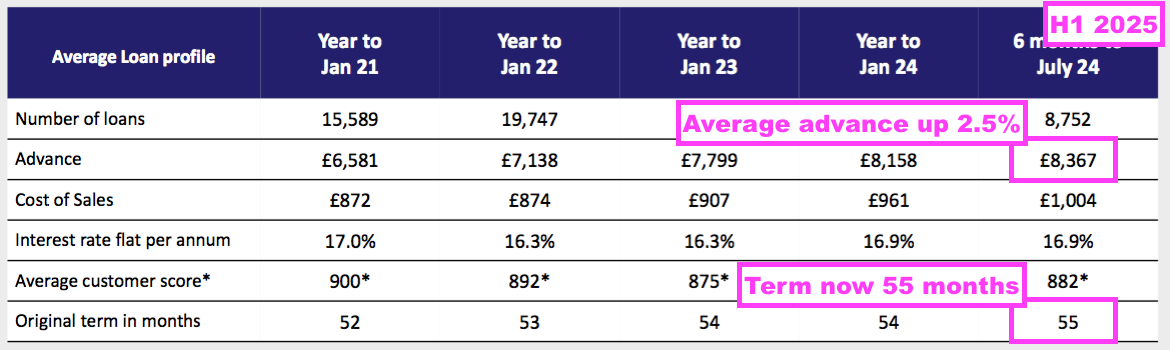

- Emphasising perhaps the lack of any significant tier-mix shift, this H1’s new borrowers were charged the same 16.9% (flat per annum) average interest rate as the preceding FY’s new borrowers:

- For perspective, the average rate paid between FYs 2016 and FY 2021 was at least 17%, while the 16.3% charged during FYs 2022 and 2023 was the lowest since at least FY 2012:

- The duration of the typical loan continues to extend. The 55 months for this H1 compares to 54 for the preceding FY, 50 for FY 2017 and 44 for FY 2012.

- I speculate the lengthier repayment duration reflects the higher cost of used cars as customer budgets generally reach a c£275 per month repayment ceiling.

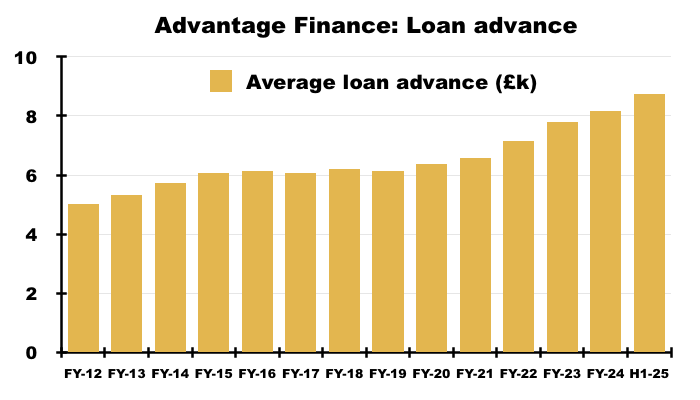

- This H1’s average loan advance increased £209 from the preceding FY to £8,367:

- Loan sizes have increased over time. The average amount borrowed by Advantage customers surpassed £5k during FY 2012, £6k during FY 2015, £7k during FY 2022 and £8k during the preceding FY:

- The greater average loan size reflects the greater price of a used car. FY 2023 claimed the used-car market had seen average prices almost double to £17.6k between 2011 and 2022.

- Rising car prices should be positive for Advantage; customers ought to borrow more money, pay more interest and (in theory, regulations and law courts permitting!) provide SUS with more profit.

- The 8,572 new loans issued during this H1 were offset by 9,498 accounts closed due to completed repayments, voluntary terminations or the commencement of legal proceedings:

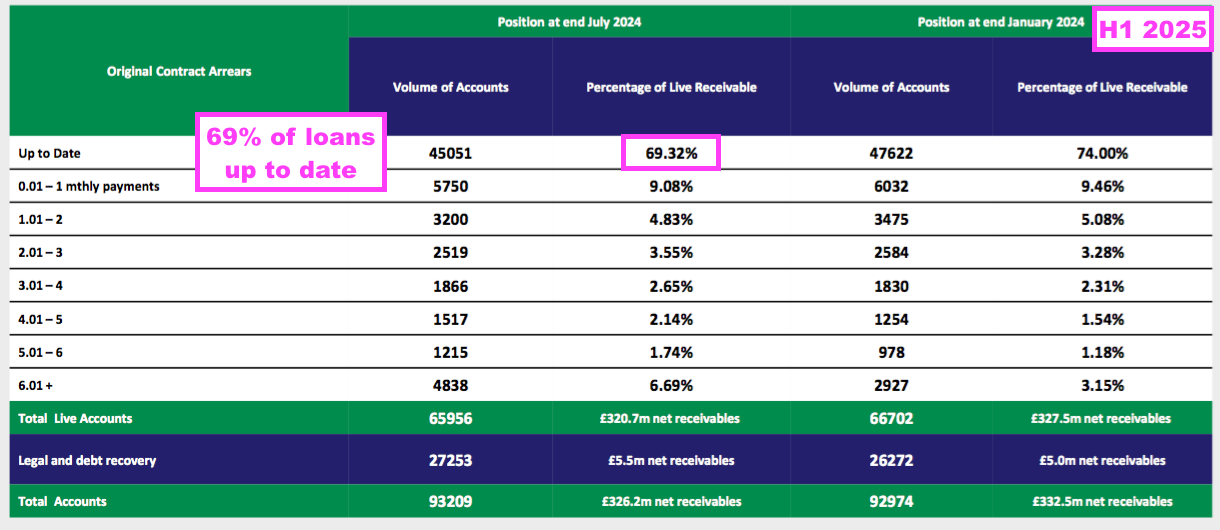

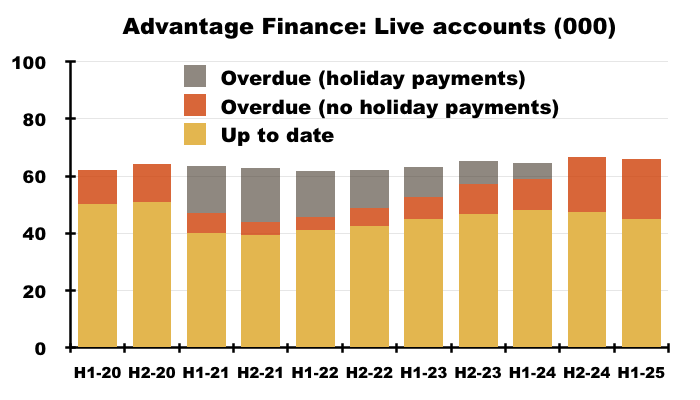

- The account openings and closures left total ‘live’ accounts 746 lower at 65,956.

Advantage Finance: revenue and cost of sales

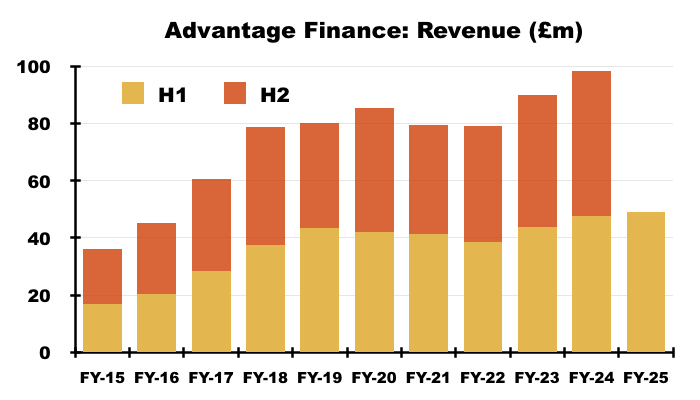

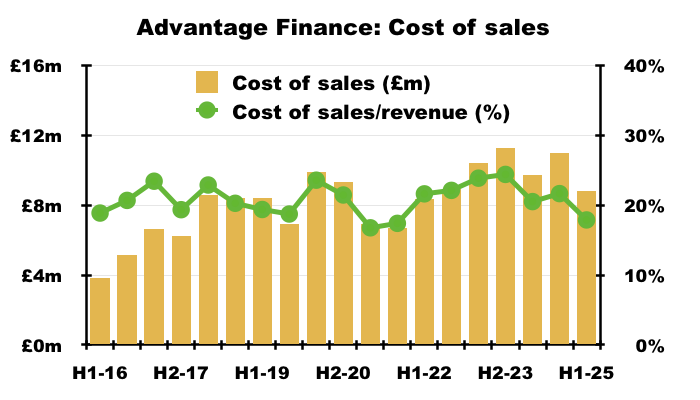

- The greater average loan size, the (flat per annum) loan rate remaining at 16.9% and account numbers remaining close to 66,000 combined to improve Advantage’s H1 revenue by 3% to £49m — a new H1 record:

- Emphasising how rapid Advantage has grown, H1 revenue of £49m exceeded the division’s FY 2016 revenue of £45m.

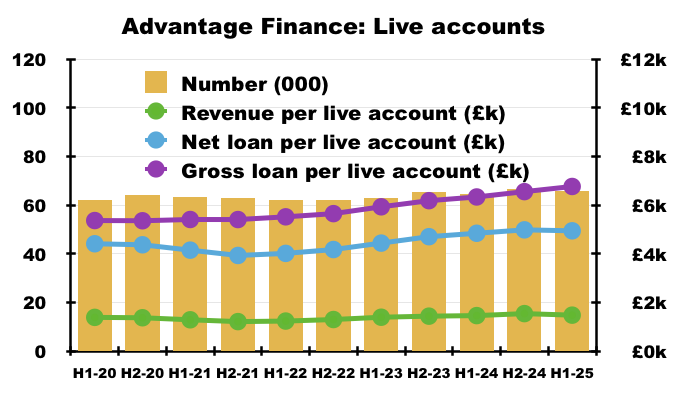

- The aforementioned higher loan sizes translated into revenue per account remaining at nearly £1.5k (the highest since H1 2018), with the average loan outstanding before impairments now at a new £6.8k high and the average loan outstanding after impairments at a new £5.0k high:

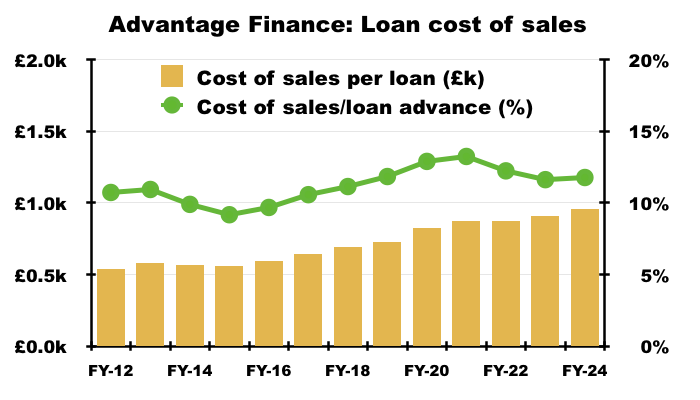

- Cost of sales per loan increased 4% to a record £1,004:

- Cost of sales per loan at £1,004 equates to 12.0% of the £8.4k average loan and is slightly below the 12.4% average recorded during the preceding five FYs:

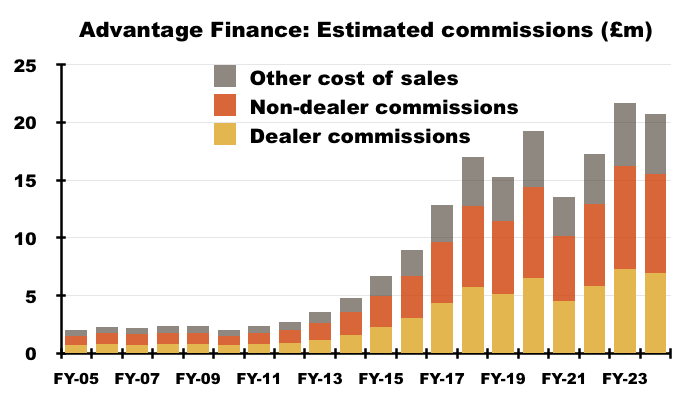

- The proportion of Advantage’s cost of sales paid as commission to car dealers has become critical to understanding SUS’s valuation following October’s Court of Appeal judgements (see Advantage Finance: Court of Appeal judgements).

- The preceding FY revealed “about £700” of the then £961 cost of sales was paid as commission:

[FY 2024] “Cost of sales were £961 in the latest year, for information about £700 of that is introduced commission, which is a variable cost that goes straight to the broker. Other costs of sales are consumer credit referencing and our data costs“

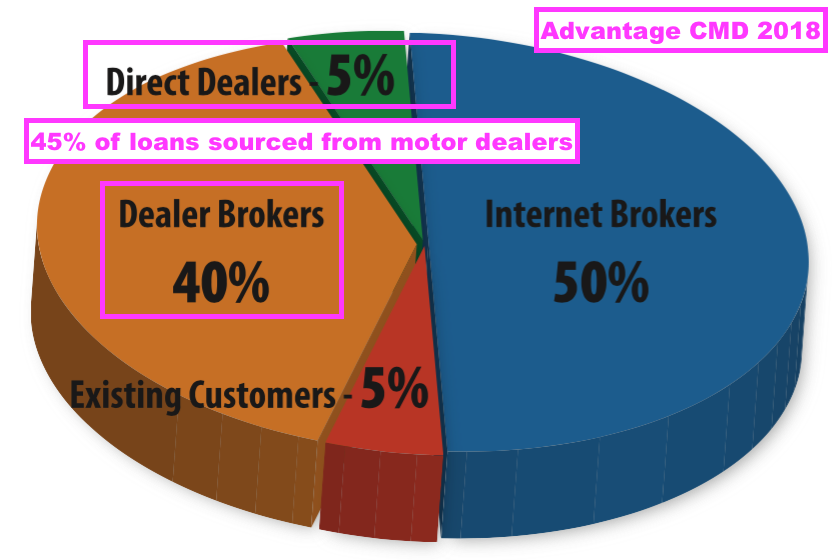

- This H1 reiterated 90% of Advantage’s loans were sourced through “brokers“:

“Used car finance on hire purchase – 90% sourced through brokers – 5% refinances for previous customers – 5% direct from dealers.”

- Within that 90%, perhaps 50% of loans are derived from internet brokers and 40% are derived from car dealers (see Advantage Finance: potential ‘secret’-commission compensation).

- Reflecting the lower number of loan advances, Advantage’s total H1 cost of sales dropped 10% to £8.8m:

- Advantage’s total cost of sales absorbed 17.9% of motor-finance revenue during this H1 — the lowest since at least FY 2016 barring the pandemic-blighted FY 2021.

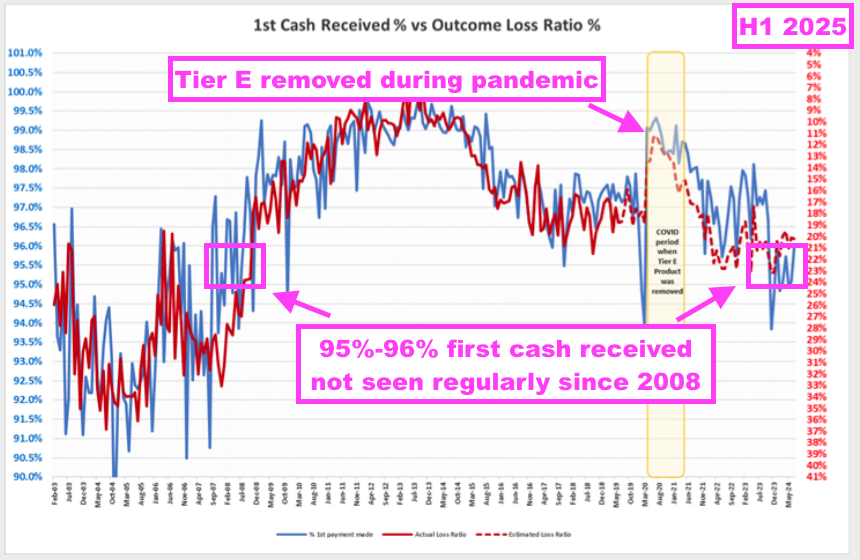

Advantage Finance: first payments

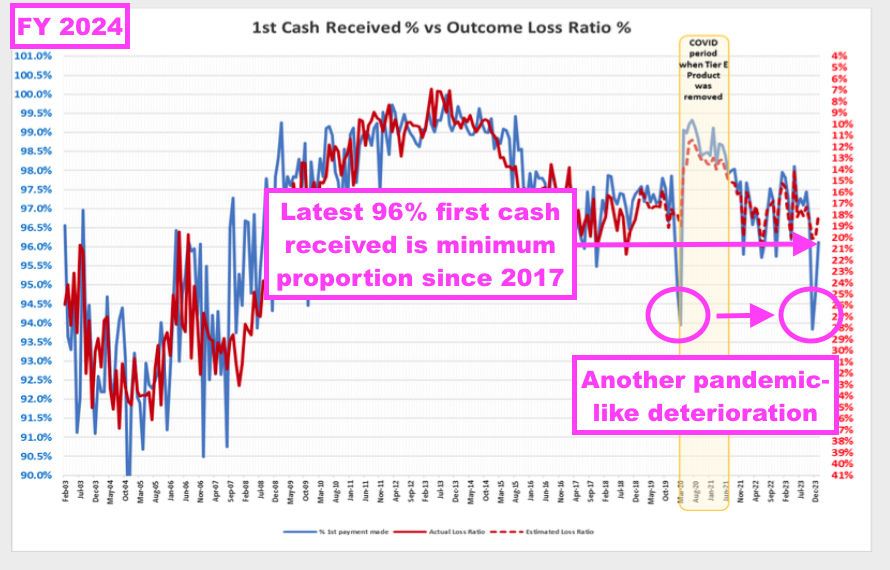

- The preceding FY’s first-payment chart showed an alarming pandemic-like deterioration (blue line, left axis):

- The first-payment proportion plunging to 94% was described as only a “blip” during the preceding FY webinar:

[FY 2024] “Towards the right of the chart we have got a couple of blips. So the first blip was just at the start of the pandemic when people panicked a bit and didn’t pay their first payment on time. We have also had a blip at Christmas this year, which happily for us has recovered a bit in January but we continue to monitor that as we go.“

- The proportion rebounding to 96% by the end of the preceding FY was reassuring, but 96% has typically been the minimum first-payment level (pandemic aside) since late 2017.

- This H1 showed the first-payment proportion fluctuating between 95% and 96%:

- A first-payment proportion between 95% and 96% does not seem encouraging versus the 97% and 98% experienced before and after the pandemic.

- The proportion of borrowers making their first payments on time has shown to correlate inversely to the proportion of loans that ultimately suffer losses (red line, right axis).

- The first-payment chart highlights the removal of tier E products during the pandemic and the sudden improvement of first payments.

- I speculate whether Advantage should again remove tier E products to reduce the likelihood of suffering further impairments following the aforementioned regulatory developments.

Advantage Finance: collections

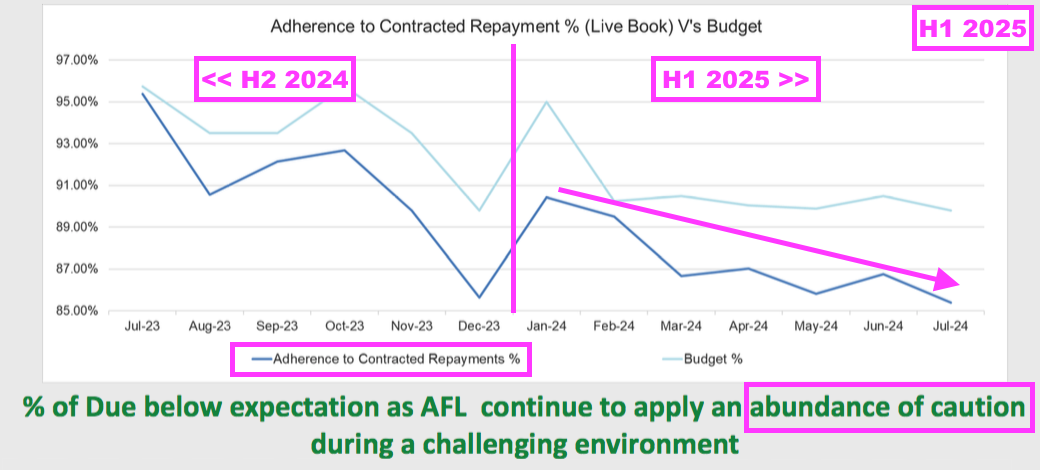

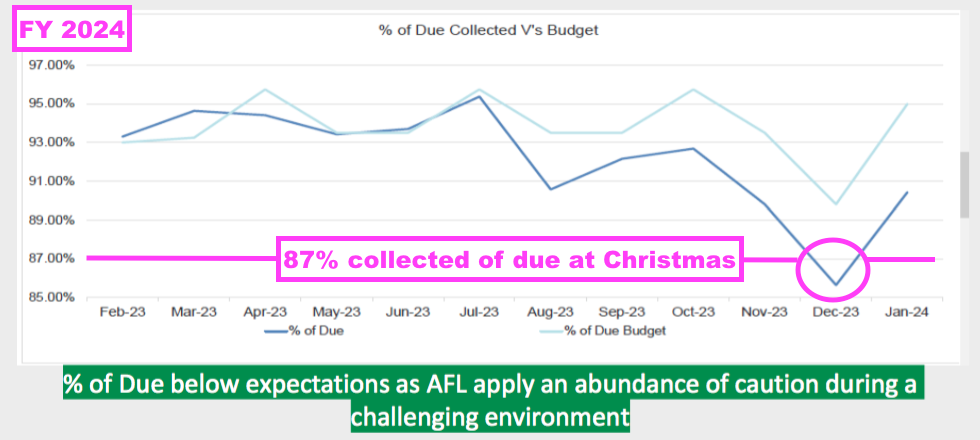

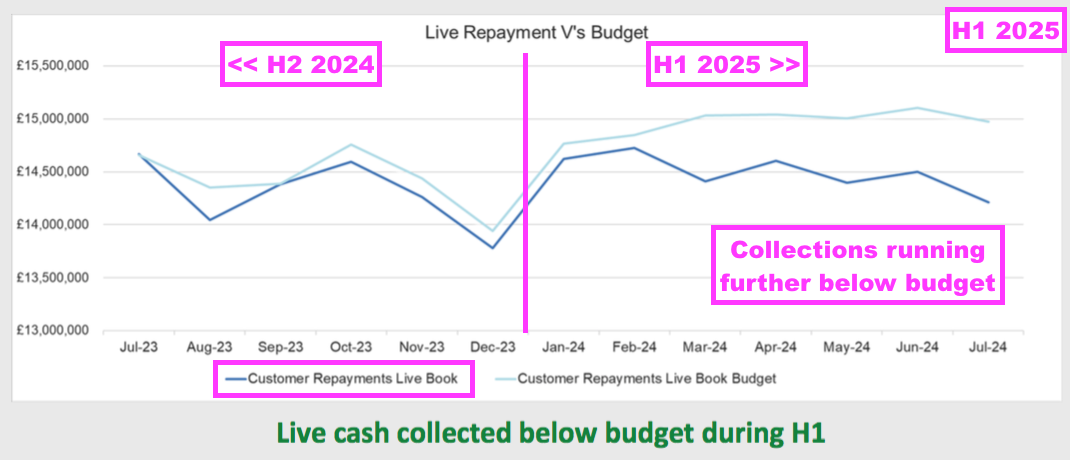

- The aforementioned “voluntary” FCA restrictions and SUS applying an “abundance of caution” caused H1 collections of due payments to average 87%:

“The result was an increase in revenue of 3% for the half year despite capital receivables at £446m, 9% higher than 2023. This resulted from a decline in collection rates caused in part by the restrictions on Advantage’s ability to manage its customers. Thus, live repayments as a percentage of repayments due fell in the half year from 94% a year ago to an average of 87% for the first half this year. Advantage now has in place specific measurements for customer satisfaction avoidance of stress, and encouragingly adherence to repayment arrangements is on the rise.”

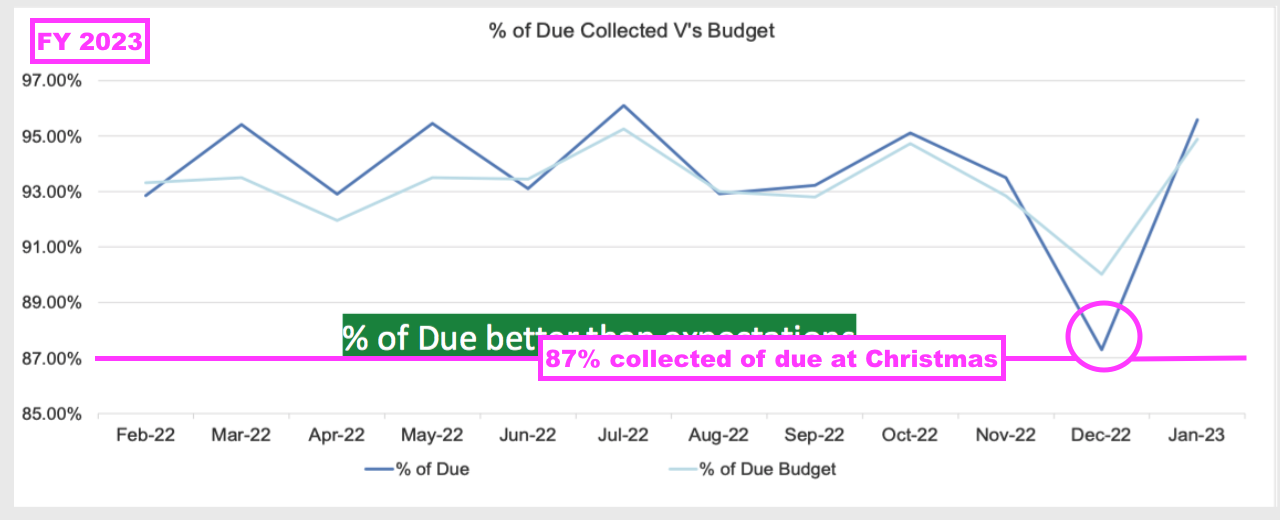

- For perspective, collections of due were 92.1% for the preceding FY, 93.6% for FY 2023, 93.2% for FY 2022, 83.3% for (pandemic-blighted) FY 2021 and 93.5% for FY 2020.

- Note that collections of due deteriorated throughout this H1, starting at 90% and finishing at 85%:

- Collections of due at 85% is less than the 87% typically collected at Christmas:

- Note that SUS’s charts show collections consistently below budget since the start of FY 2024.

- Despite the aforementioned lifting of the “voluntary” FCA restrictions during October, trading updates issued after this H1 confirmed only small improvements of collections due to 86% and then 87% (see H2 2025 trading updates).

- Following the faltering percentage of collections due, total H1 cash collections unsurprisingly ran further below budget:

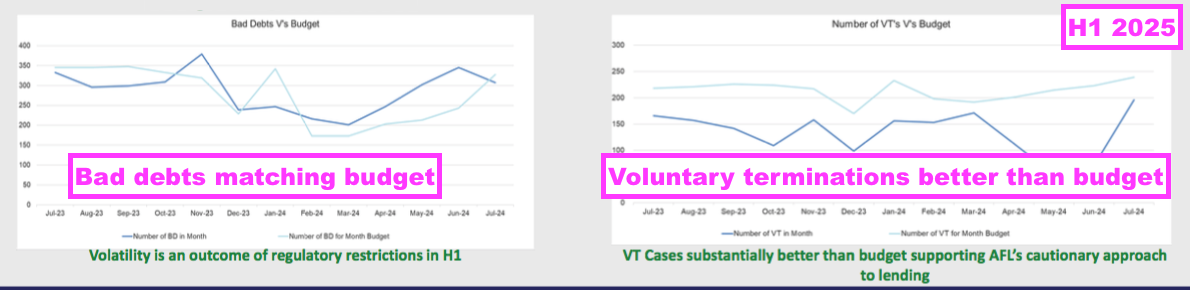

- At least the number of bad debts incurred and the number of voluntary terminations handled during this H1 matched or exceeded budget:

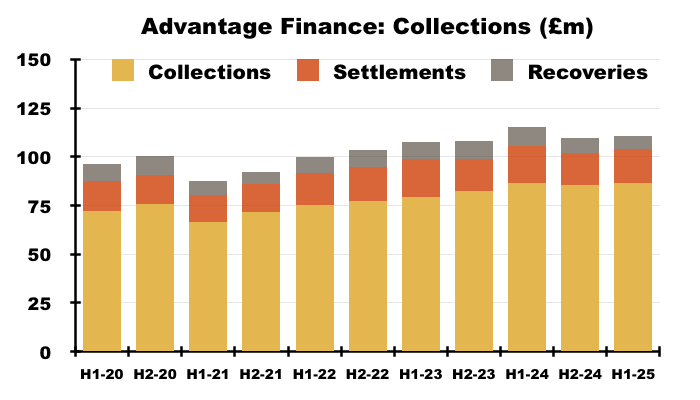

- Advantage’s collections, settlements and recoveries for this H1 amounted to £111m, down 4% on the comparable H1:

- That 4% decrease compares to an 8% increase to Advantage’s loan book.

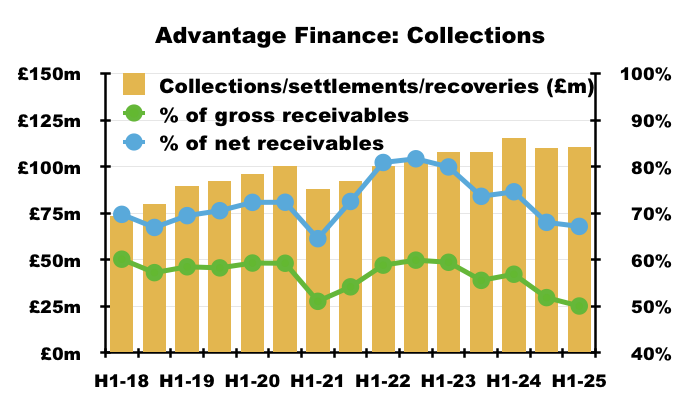

- As such, collections, settlements and recoveries as a proportion of the gross loan book (i.e. before impairments) and the net loan book (i.e. after impairments) were 50% and 67% respectively, and on a par with the pandemic lows of H1 2021:

- Collections, settlements and recoveries becoming a smaller proportion of the loan book confirms Advantage’s borrowers are becoming more reluctant to repay what they owe.

Advantage Finance: up-to-date and overdue accounts

- The slower rate of repayments during this H1 left only 69% of Advantage’s loans up to date:

- The up-to-date 69% compares to 74% for the preceding FY and 79% for the comparable H1:

- However, the up-to-date 69% exceeds the 61% (H1 2021) and 62% (FY 2021) recorded during the early stages of the pandemic.

- During the pandemic, approximately 20,000 Advantage customers enjoyed FCA-authorised payment holidays that lasted up to six months.

- SUS deemed the payment-holiday customers as ‘overdue’ even if normal repayments were resumed.

- The FCA has arguably authorised payment holidays once again through its aforementioned “voluntary” restrictions — although this time the cessation of some payments appears to be lasting far longer than six months.

- For perspective, the up-to-date customer proportion topped 80% during FYs 2017 and 2018, and reached a super 91% during FY 2016:

- The comparable H1 last disclosed the number of pandemic payment-holiday accounts (5,558), which should have all vanished from the loan book by the end of FY 2025:

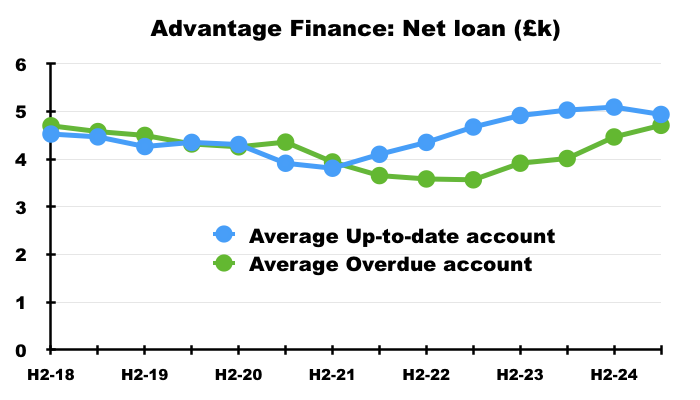

- The average net loan outstanding (i.e. after impairments) at overdue accounts continues to creep higher to match the average at up-to-date accounts:

- I presume the FY 2021 divergence between the amounts owed by up-to-date accounts and the amounts owed by overdue accounts was caused by the loan impairments for pandemic-related payment holidays. Of the £20m Covid impairments, only £5m were deemed necessary with hindsight and the remaining £15m were effectively reversed during FY 2022.

Advantage Finance: impairments

- SUS’s loan impairments are classified as:

- Stage 1, which reflects expected write-offs from up-to-date customers;

- Stage 2, which reflects expected write-offs from customers with a “good payment record” but have been identified as “vulnerable” by factors such as “health, life events, resilience or capability” that create a greater credit risk, and;

- Stage 3, which reflects expected write-offs from customers one month or more in arrears.

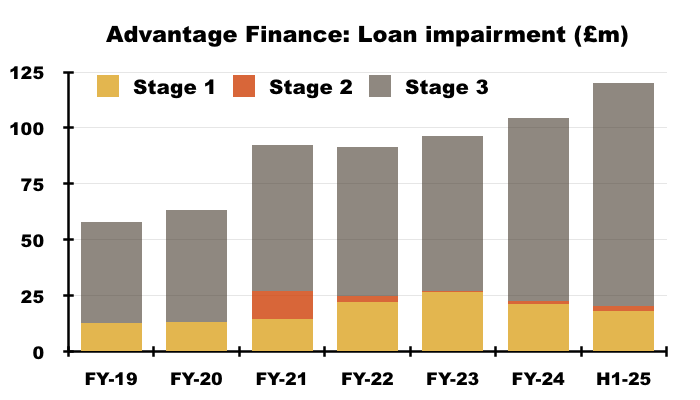

- This H1’s total impairment provision for Advantage increased by £15m to £120m:

- The aforementioned lower rate of collections unsurprisingly swelled the level of expected Stage 3 impairments.

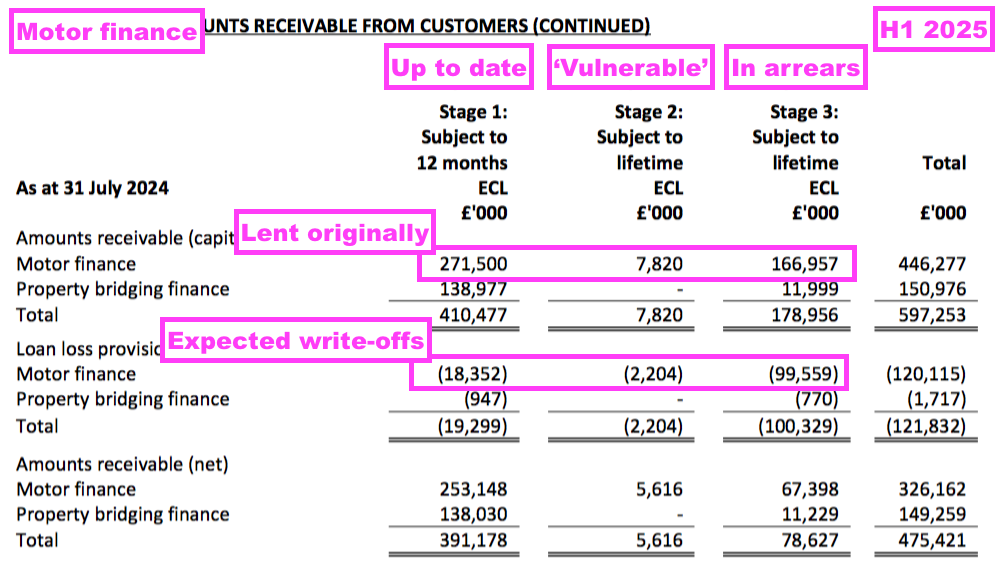

- Of the £167m lent to in-arrears Stage 3 Advantage borrowers, SUS reckoned £100m or 60% would not be repaid:

- The 60% broadly matches the Stage 3 proportions reported for the preceding FY (58%) and FY 2023 (60%).

- Of the £272m lent to up-to-date Stage 1 Advantage borrowers, SUS reckoned £18m or 7% would not be repaid.

- The 7% broadly matches the Stage 1 proportions reported for the preceding FY (7%) and FY 2023 (9%).

- The total £120m Advantage impairment provision was equivalent to 27% of the overall £446m lent originally and still outstanding:

- The 27% proportion compares to 24% for the preceding FY and FY 2023, and 26%-27% for the pandemic-blighted FYs 2021 and 2022.

- For pre-pandemic FYs 2019 and 2020, Advantage’s impairments ran at 18% of total money lent. But Advantage’s impairments did surpass 25% during FYs 2011, 2012 and 2013.

- Lending a total £446m and impairing £120m means Advantage expects to receive 73p of capital back for every £1 loaned.

- Charging the aforementioned 33.87% APR is therefore required to recoup the 27p of capital not repaid as well as earn an adequate return on the overall £1 lent.

- I fear Advantage’s ongoing unfavourable rate of collections (see H2 2025 trading updates) is unlikely to reduce that 27% proportion.

- Indeed, Advantage’s impairment charge during this H1 was £18m versus £16m for the preceding H2 and only £7m for the comparable H1:

- Advantage’s gross loan book (i.e. before impairments) meanwhile increased by £9m during this H1.

- The outlook for Advantage’s loan book will not be favourable if every additional £9m lent keeps incurring an extra £18m impairment.

Advantage Finance: Court of Appeal judgements

- Advantage’s H1 progress was overshadowed by the Court of Appeal’s judgements on three cases involving the disclosure of motor-finance commissions.

- The judgements — if not overturned by the Supreme Court — could have significant adverse consequences for Advantage and the wider motor-finance industry.

- Following this H1, SUS acknowledged the Court of Appeal’s judgements:

[RNS October 2024] “S&U, the specialist motor and property financier, today notes the recent Court of Appeal decisions on Johnson and Wrench v Firstrand Bank Limited [MotoNovo] and Hopcraft v Close Brothers Limited, the implications of which it is considering. These decisions provide guidance for lower courts on the subject of commissions disclosure in the financial services industry. They unexpectedly overturned hitherto received judicial positions on the duties of motor dealers, credit brokers and lenders to disclose and obtain consent for the payment of commission. The Group also notes the intention of those companies to appeal those decisions to the UK Supreme Court.

The Court of Appeal decisions set a higher bar for the disclosure of, and consent to, the existence, nature, and quantum of any commission paid than that required by current FCA rules, as adhered to by regulated motor finance firms including the Group’s motor finance subsidiary Advantage Finance Limited (“Advantage Finance”).

However, the Court of Appeal recognised the ‘tensions’ between previous lower court judgements on the extent of commission disclosure in the cases of ‘Hurstanger’ and ‘Wood’. It therefore called for ‘a definitive announcement to be made by the Supreme Court about the circumstances in which the payment of a commission …. will give rise to a liability …. on the part of the payer.’ It is therefore unsurprising that it is the intention of the companies involved to appeal the judgement to the UK Supreme Court.

In the meantime, S&U notes that these decisions do not specifically relate to ‘difference in charges’ models of commission (currently the subject of an FCA review) in which Advantage Finance has never been engaged.”

- The three cases were heard during July and the judgements were handed down during October. Appeals for the three cases will be heard by the Supreme Court next week (01-03 April 2025) and definitive judgements could be handed down by the summer.

- The three cases concern three individual borrowers, who the Court of Appeal described as “financially unsophisticated consumers on relatively low incomes“:

- Miss Hopcraft, a student nurse, who purchased a car during 2014 for £8,530, of which £8,280 was through finance. The lender, Close Brothers, paid the car dealer commission of £183.

- Mr Wrench, a postman, who purchased two cars, one during 2015 and the other during 2017, for a total £18,745, of which £14,745 was though finance. The lender, MotoNovo, paid the car dealers total commission of £589.

- Mr Johnson, a factory supervisor, who purchased a car during 2017 for £6,499, of which £6,399 was through finance. The lender, MotoNovo, paid the car dealer commission of £1,650.

- All three borrowers:

- Believed car dealers profited only from selling cars and were unaware their particular car dealers received commissions from lenders;

- Argued their car dealers owed them a “duty to provide information, advice or recommendation” about motor finance on an “impartial or disinterested basis“, and;

- Sought the return of the ‘secret’ commissions paid to their car dealers by the lenders.

- The Court of Appeal determined the car dealers involved:

- “Were undoubtedly acting as credit brokers” as defined by the FCA’s CONC rules;

- Either never declared they could receive a commission from a lender, or effectively “buried in the small print” any declaration of a possible commission from a lender, and;

- Undertook “two separate commercial roles” when selling the cars in question:

- The first to agree a price for the car with the purchaser, and;

- The second to sell the car to the lender through a finance agreement.

- The Court of Appeal’s judgements referred extensively to the following case law:

- Wood v Commercial First Business Ltd [2021] (“Wood“), which found that a ‘secret’ commission is considered to be a bribe, and;

- Hurstanger v Wilson [2007] (“Hurstanger“), which found that accepting commissions creates a conflict of interest for brokers, unless customers give their “informed consent” for the associated arrangements to proceed.

- The Court of Appeal’s summary deemed the two lenders liable as “primary wrongdoers” or “accessories for procuring the brokers’ breach of fiduciary duty”:

[Court of Appeal October 2024]

“For the reasons set out in this judgment, we allow all three appeals.

The dealers were the sellers of the cars, but they were also acting as credit brokers on behalf of the claimants. In the latter role, their task was to search for and offer the customer a finance deal from their panel of lenders which was suitable for their needs and competitive. In some cases they undertook to find the best deal or the one which was most suitable for the customer. They therefore owed the claimants the “disinterested duty” described in Wood. The relationship was also a fiduciary one. In all three cases there was a conflict of interest and no informed consent by the consumer to the receipt of the commission. However, that would be insufficient in itself to make the lender a primary wrongdoer. In order to give rise to a primary liability on the part of the lender, the commission must be secret. If there is partial disclosure which suffices to negate secrecy, there is binding authority (Hurstanger) that the lender can only be held liable in equity as an accessory to the broker’s breach of fiduciary duty.

On the facts, there was no disclosure in Hopcraft and, we find, insufficient disclosure in Wrench to negate secrecy. The payment of the commission in those cases was secret, and the lenders were therefore liable as primary wrongdoers. In the light of the concession which was made below, we must treat the situation in Johnson as similar to that in Hurstanger, where there was sufficient disclosure to negate secrecy, but insufficient disclosure to procure the consumer’s fully informed consent to the payment. We find that the lenders in Johnson are liable as accessories for procuring the brokers’ breach of fiduciary duty by making the commission payment to them in the circumstances in which they did.”

- The Court of Appeal made clear the basic remedy to the three cases:

[Court of Appeal October 2024]

“Is the lender liable for the repayment of the commission? Answer: yes.“

- But in the case of Mr Johnson, whose finance agreement was particularly inflated by a substantial £1,650 commission, the Court of Appeal decided the interest he paid on that commission ought to be returned as well:

[Court of Appeal October 2024] “We did not hear submissions on remedy, but are of the view that the solution on that question also is clear. The commission of £1,650 should be repaid to Mr Johnson by the lender, together with the interest he paid on it under the hire purchase and personal loan agreements, and interest on the total of those two elements at an appropriate commercial rate from the date of the agreement, 29 July 2017. If the rate cannot be agreed we will consider written submissions about it.”

- The BBC reported MotoNovo has since repaid Mr Johnson £3,200, which implies his interest payments on his £1,650 commission came to £1,550.

Advantage Finance: Supreme Court hearing and FCA intervention

- The Court of Appeal notably admitted its “analysis” amounted only to “sufficient guidance” for County Court judges and was not the “definitive pronouncement” on the matters concerned:

[Court of Appeal October 2024] “We hope that our analysis will provide sufficient guidance for the County Court judges who have to deal with these types of claim on a virtually daily basis, but it may be that on some future occasion it will be felt desirable for the Hurstanger and Wood lines of authority to be considered in greater depth, and for a definitive pronouncement to be made by the Supreme Court about the circumstances in which the payment of a commission by a third party to another person’s agent or fiduciary will give rise to a liability (whether as principal wrongdoer or an accessory) on the part of the payer.“

- The “definitive pronouncement” should be made by the Supreme Court after the ‘definitive’ hearing is held next week (01-03 April 2025).

- Likely arguments for the lenders during the Supreme Court hearing are included within this assessment of the Court of Appeal judgements by Gough Square Chambers.

- Gough Square Chambers employs barrister Simon Popplewell, who helped represent MotoNovo during the Court of Appeal hearing.

- The Supreme Court has accepted two ‘interventions’ — one from the National Franchised Dealers Association and one from the FCA — for the hearing.

- The Supreme Court rejected interventions from group-claims affiliate Consumer Voice, trade body the Finance and Leasing Association and, notably, HM Treasury.

- The Supreme Court hearing places the FCA in an extremely awkward position.

- After all, the FCA is supposed to protect consumers through a raft of rules and regulations…

- …and yet the FCA’s disclosure requirements for motor-finance commissions were essentially found unlawful by the Court of Appeal.

- The FCA’s proposed intervention does not give 100% backing to the two lenders involved.

- In particular, the FCA seems set to argue the regulatory position is “more nuanced” than that claimed by the lenders:

[FCA January 2025] “The Appellants argue that the motor dealers’ function as credit brokers was not advisory and that therefore they did not owe either any ‘disinterested’ duty or any fiduciary duties to their customers. As an aspect of this ground, the Appellants argue that the Judgment errs in imposing a substantially and unjustifiably higher standard (e.g. for disclosure) than the regulatory framework in place at the relevant time.

The FCA does not agree with such a stark submission, and will submit that the position is more nuanced.”

- Furthermore, the FCA talks of the “proper role” of a lender and refers to various CONC rules hinting the two lenders should not have acted in the way they did:

[FCA January 2025] “The FCA proposes to develop submissions as to its understanding of the proper role of the lender vis-à-vis the customer based on the regulatory framework (which, as noted above under Ground 1, ought to be taken into account).

For example, Principle 8 requires the lender to ensure that conflicts of interest are managed. In addition, CONC 1.2.2R imposes an obligation on lenders to ensure its agents comply with CONC and to take reasonable steps to ensure others acting on its behalf comply with CONC.

Furthermore, CONC 4.5.2G provides that the lender ought not to enter into differential commission models unless additional payments are justified by extra work undertaken by the broker. “

- Mind you, if scores of other lenders and car dealers also failed to adhere to these CONC rules (which appears to be the case), why then was this entire ‘secret’-commission matter left to be exposed by a student nurse, a postman and a factory supervisor at the Court of Appeal…

- …and not proactively investigated by the FCA…

- …especially when the FCA investigated discretionary motor-finance commissions during 2019?!

- UPDATE 05 April 2025: The FCA has published its intervention document for the Supreme Court hearing.

[Advantage March 2025] “The existence of a commission arrangement was made clear in the pre-contractual information that we sent directly to you, prior to you taking out the agreement. You agreed to the payment of the commission when you entered into the agreement. We were not required by the FCA to explicitly state the amount of the commission.

…

“For many years, and as with many other areas of the financial services industry, motor finance lenders have paid a commission to motor dealers/brokers for the acquisition of new motor finance business. In doing so, lenders have followed rules set out by the FCA in relation to the disclosure of the existence of these commissions.”

…

“These rules did not require any disclosure of the amount of commission paid and the FCA has been satisfied that, where a commission is on a flat-fee basis, no consumer harm occurs.”

- If the Supreme Court agrees with the Court of Appeal, then Advantage would presumably be liable to repay all its (now unlawful) ‘secret’ commissions to its customers.

Advantage Finance: potential ‘secret’-commission compensation

- The FCA suggested the other week that, should the Supreme Court agree with the Court of Appeal’s judgements, an “industry-wide redress scheme” could be established:

[FCA March 2025] “So, we are confirming that if, taking into account the Supreme Court’s decision, we conclude motor-finance customers have lost out from widespread failings by firms, then it’s likely we will consult on an industry-wide redress scheme.

Under a redress scheme, firms would be responsible for determining whether customers have lost out due to the firm’s failings. If they have, firms would need to offer appropriate compensation. We would set rules firms must follow and put checks in place to make sure they do.”

- But lenders becoming “responsible for determining whether customers have lost out due to the firm’s failings” and then determining the level of “appropriate compensation” does offer some hope that customer repayments can be kept under control.

- The aforementioned Hopcraft case judged by the Court of Appeal provides a useful case study for determining whether a customer has truly “lost out“.

- Miss Hopcraft borrowed £8,280 through a hire-purchase agreement that resulted in the lender paying the car dealer a commission of £183 — equivalent to just 2.2% of the sum borrowed.

- Miss Hopcraft claimed she would have “shopped around” had she known about the £183 commission:

[Court of Appeal October 2024] “Miss Hopcraft was unaware that Jordans were being paid a commission. She told the judge that if she had known about the commission she would have shopped around, but he found that she was focused on buying the car and as long as the monthly payments were “about right”, she was happy with the situation”.

- Whether Miss Hopcraft would have located an alternative dealer with:

- A similar car at a similar price with a similar finance offer to those supplied by the original dealer, and

- A fully disclosed commission much less than £183…

- …is hard to determine some eleven years following her actual purchase.

- Note that the Court of Appeal did not claim Miss Hopcraft’s finance agreement employed an excessive rate, nor did the Court of Appeal question whether her car dealer had a commercial bias towards Close Brothers.

- I would therefore argue Miss Hopcraft has not truly “lost out” and her “appropriate compensation” ought therefore to be minimal.

- In contrast, the Court of Appeal made clear that Messrs Wrench and Johnson were unaware of their car dealers possessing a commercial bias towards MotoNovo…

- …and as such their “appropriate compensation” ought to be more significant.

- Assuming Advantage’s loans were all:

- Chosen without bias by car dealers from a panel of different lenders, and;

- Inherently suitable for each customer’s circumstances…

- …then Advantage could argue to the FCA that — despite paying ‘secret’ commissions — the practical financial harm suffered by the division’s customers was generally small and few “lost out” in any significant way.

- Note that the FCA says “firms would be responsible for determining whether customers have lost out due to the firm’s failings“.

- I suppose Advantage could also argue it found no “failings“, as the FCA rules were presumably adhered to at all times.

- For some perspective on Advantage’s ‘secret’ commissions, the preceding FY indicated approximately 75% of cost of sales were paid to brokers:

[FY 2024] “Cost of sales were £961 in the latest year, for information about £700 of that is introduced commission, which is a variable cost that goes straight to the broker. Other costs of sales are consumer credit referencing and our data costs“

- This Advantage presentation from 2018 revealed 45% of new loans were sourced from car dealers:

- Assume 75% of Advantage’s cost of sales were always paid to brokers, of which 45% was always paid to car dealers, then Advantage may have paid total ‘secret’ commissions of £61m between FY 2005 and the preceding FY:

- Perhaps by coincidence, SUS’s present market cap is £63m below this H1’s NAV (see Valuation)…

- …implying Advantage may become liable to repay all that estimated £61m back to customers.

- Note that the Court of Appeal’s judgements covered only car dealers and not ‘pure’ intermediaries:

[Court of Appeal October 2025] “In situations in which a broker is acting purely as an intermediary, and has no other means of remuneration, one of the parties to whom he provides his services might reasonably assume (or be expected to assume) that if they do not remunerate him, the other party will.

But in the present context, the purchaser/borrower would view the procuring of the finance as an adjunct to the sale transaction, and would not expect the dealer to receive a commission from the lender for the introduction of the business, unless he tells them. Indeed, the claimants in these three cases believed that the dealers would make their money from the profit on the sales.”

- This point was emphasised recently by fellow quoted lenders Secure Trust Bank (STB) and Vanquis Bank (VANQ):

[STB FY 2024] “A key feature of the fact pattern in these [Court of Appeal] cases was the linked sale by a dealer of the vehicle and the direct introduction of the finance by that same dealer. Commission payments to dealers make up only 20% of our historical motor commission payments, with the remainder involving brokers and various other introducers, independent of the vehicle dealer, and with different sales distribution arrangements and customer journeys.”

[VANQ FY 2024] “Our Vehicle Finance division, Moneybarn, offers motor finance through intermediaries. The majority of these intermediaries are independent credit brokers. From the period January 2013 to October 2024, it wrote £3.0bn of loans of which 10% were written via dealers acting as credit brokers, upon which £23m was paid out as commission.”

- I expect SUS to disclose its level of past ‘secret’ commissions within the group’s forthcoming FY 2025 statement.

Aspen Bridging

- Established at the start of FY 2018, Aspen Bridging offers property-bridging loans for small/individual property developers and investors.

- The preceding FY outlined the division’s attractions to borrowers:

[FY 2024] “Mainstream” banks, including the newer “challengers”, continue to lack the speed, flexibility and appetite to furnish the smaller, short-term loans in which Aspen specialises. Recent consolidation and instability in the challenger banking sector is evidence of this and again shows that, technology, speed and a quality bespoke service – as well as price – are what give smaller entrants like Aspen their competitive edge.”

- The subsidiary’s profitability is supported by conservative lending to low-risk “experienced” customers:

[FY 2024] “Aspen values its security properties very conservatively and keeps gross LTVs to an average 70% and the business now only considers experienced borrowers from the top three quality bands.“

- The conservative lending is underlined by Aspen visiting every property…

[FY 2024] “Every property upon which Aspen lends for security is personally visited by a member of the team”

- …which SUS has implied is unique within the industry:

[FY 2024] “Increased margins, steady LTV’s and sensible valuations approach with our USP of visiting all projects”

- Loans range from £200k to £15m, can be issued within ten working days and are deployed to fund a wide variety of property development and investment transactions:

- Aspen offers only commercial loans, which are unregulated and therefore not subject to any FCA interference.

- This H1 encouragingly disclosed:

- 26% of customers had employed Aspen before, and;

- 15% of new loans were sourced direct from the borrower instead of through a broker.

- This H1 described Aspen’s performance within the “market-orientated residential sector” as “sparkling“.

- Greater activity within the housing market underpinned Aspen’s progress:

“Average house prices are reported by Halifax to be 4.3% up on 2023 and the strongest monthly figures for 2 years. As relevant for Aspen is housing activity and therefore potential market transactions which rose 10% year-on-year in August. Indeed, the number of home sales was then reported at a 7-year high. This is accompanied by a burgeoning rental market into which many of Aspen’s customers invest. The massive increase in affordable and rented housing proposed by the new Government will continue to drive significant demand in this sector.“

…

“The residential property market is improving both in value and activity. The Labour government’s house building plans and reforms to the UK’s dysfunctional planning system should benefit SME developers and investors who are increasingly Aspen’s most active customers.”

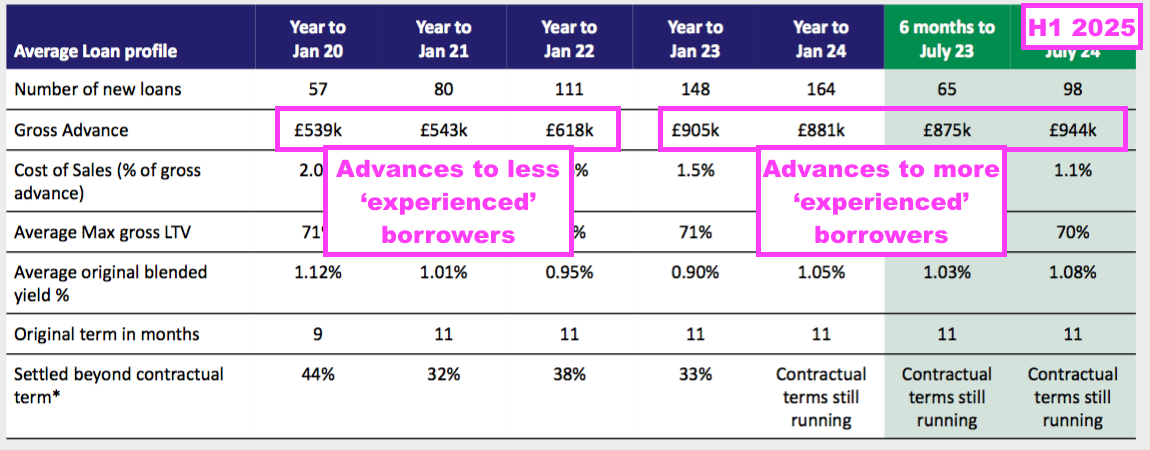

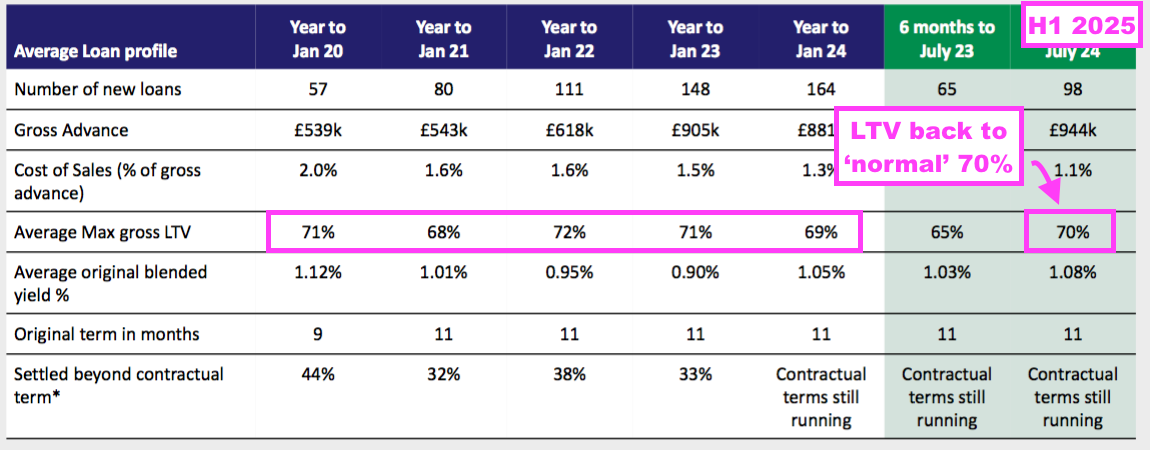

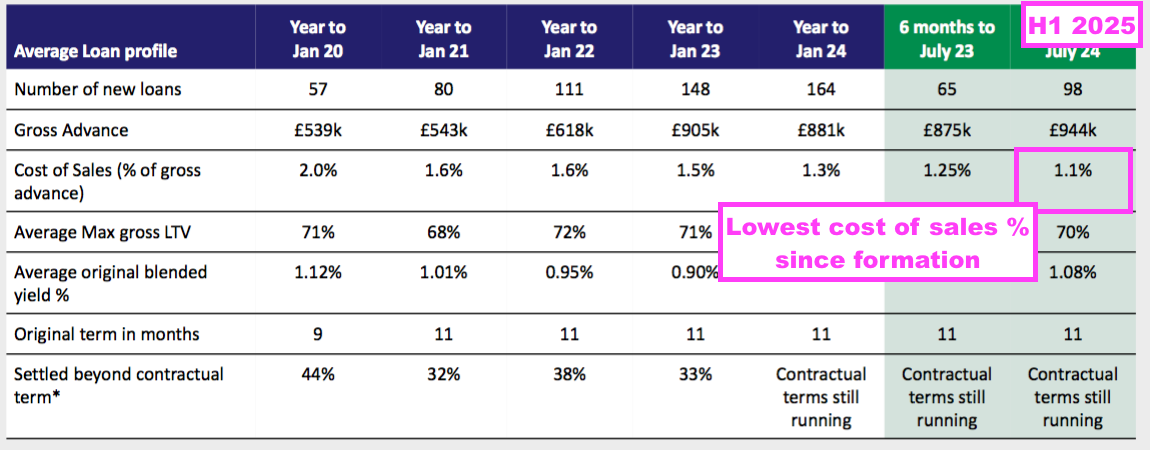

- 98 customers were advanced an average £944k for 11 months during this H1:

- The £944k average reflected the “experienced” borrowers and remains much higher than the average £618k or less (excluding CBILS) advanced to perhaps less experienced borrowers up to FY 2022.

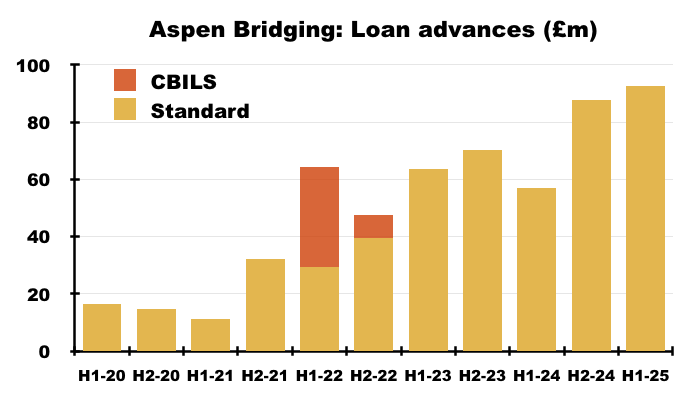

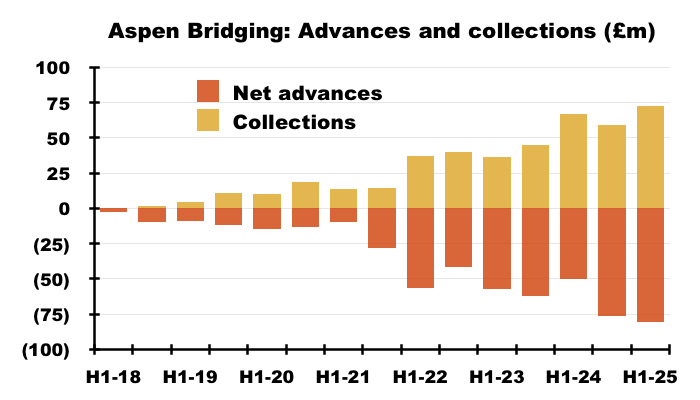

- 98 clients receiving an average £944k equates to a total £93m gross advance, Aspen’s highest for any H1 or H2:

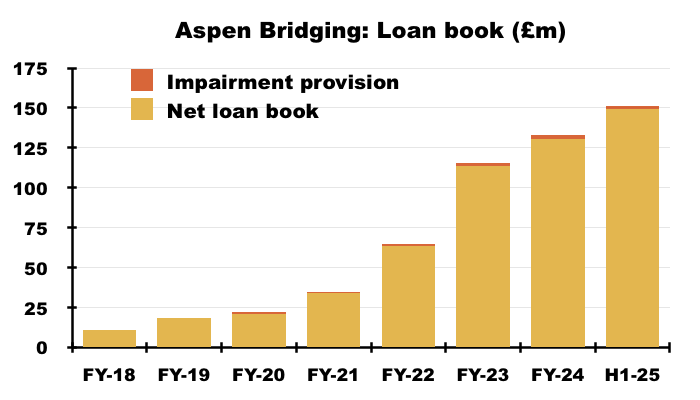

- The £93m gross advance led to Aspen’s net loan book expanding by £19m, or 14%, to £149m:

- After the comparable H1 showed an average 65% gross loan-to-value (LTV) — the lowest since Aspen’s formation — this H1 showed the LTV at a more normal 70%:

- Aspen’s latest product guide says developers borrowing against residential properties pay a flat monthly interest rate of 0.84% on a 75% LTV arrangement.

- Aspen’s rates do not seem to have tightened of late. My H1 2023 review for example also cited a flat monthly interest rate of 0.84% on a 75% LTV arrangement.

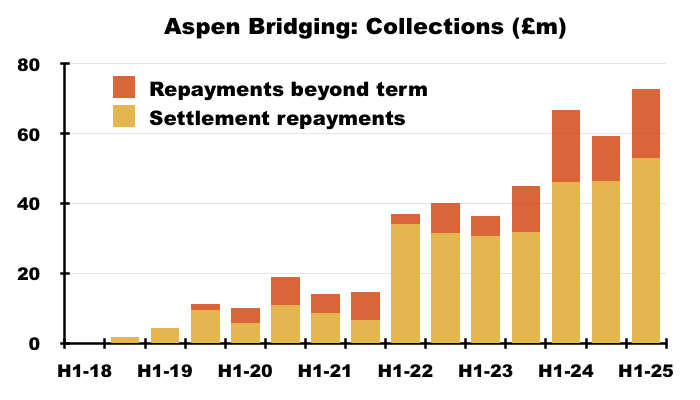

- Aspen’s H1 net advances (i.e. after retentions) of £81m surpassed collections of £73m by £8m:

- Boosting H1 collections were ‘repayments beyond term’, which at £20m were not insignificant versus the standard settlement repayments of £53m:

- Regular ‘repayments beyond term’ emphasise not all Aspen borrowers clear their loans on time. Such repayments have bolstered standard repayments by a total 34% since Aspen’s formation:

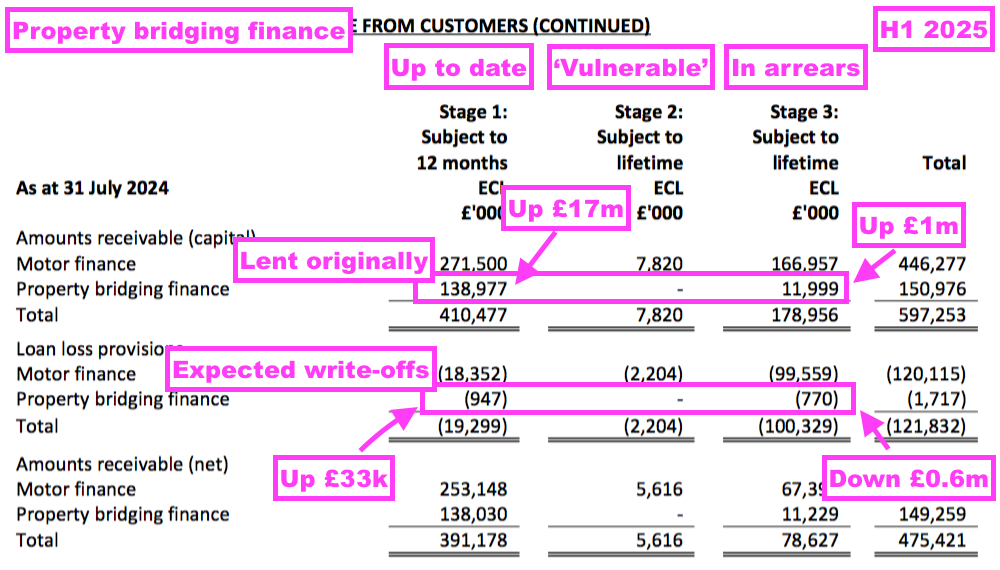

- Of the aggregate 779 loans advanced by Aspen since the subsidiary’s formation, 602 have been repaid and only 13 of the remaining 177 are “in default” — versus 15 of 163 for the preceding FY.

- The 13 defaulters are categorised as Stage 3 borrowers, and their £12m Stage 3 property loans were only £1m greater than the level reported at the preceding FY:

- Of the £12m lent to the in-arrears Stage 3 borrowers, SUS reckoned just £770k or 6% would not be repaid.

- The projected Stage 3 impairments have encouragingly reduced since the preceding FY; back then, SUS calculated Stage 3 borrowers would not repay £1.4m or 13% of their outstanding loans.

- Aspen’s Stage 1 borrowers appear to carry less risk of problems than before.

- The preceding FY showed £122m Stage 1 loans with a £914k impairment, while this H1 showed Stage 1 loans up a further £17m but with impairments up only a further £33k.

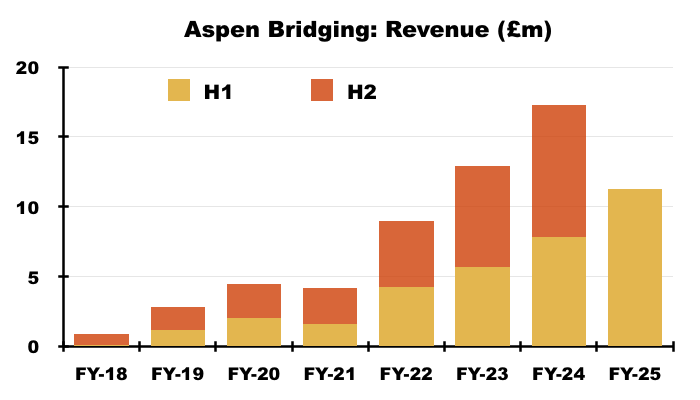

- Aspen’s enlarged loan book pushed H1 revenue 43% higher to £11m, which set a new record for any H1 or H2:

- Cost of sales (mostly broker fees) at a reported 1.1% of the average advance for this H1 was the lowest since Aspen’s formation:

- Aspen’s cost of sales were a welcome 10% of revenue (£1.18m/£11.2m) versus 12-17% between FYs 2020 and 2024.

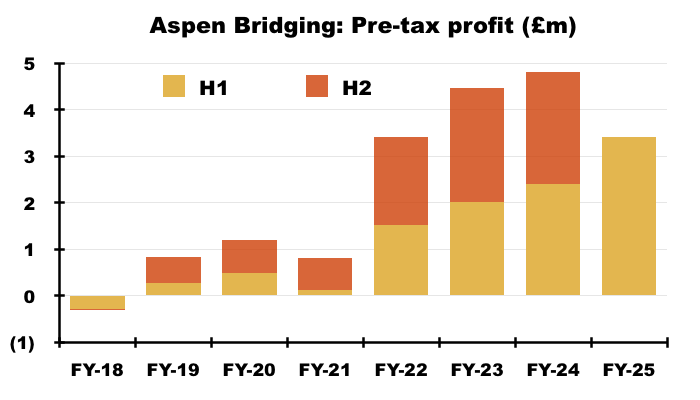

- The low cost of sales and tiny impairments allowed Aspen’s H1 profit to gain 42% to £3.4m:

- This H1’s profit setback for Advantage means Aspen’s profit represented a record 27% of SUS’s total profit:

- This H1 predicted a record FY for Aspen:

“With its current drive and focus, Aspen can look forward to a record year.”

- Sure enough, trading updates during December and February confirmed FY 2025 was a record year for Aspen (see H2 2025 trading updates).

- Aspen’s blog reveals the aim of taking cumulative lending from £500m to £1b “in the next few years“:

[Aspen March 2024] “Aspen Bridging has revamped its sales force – including two new appointments – as the company targets £1bn in total lending in the next few years.

…

“Jack Coombs, Managing Director at Aspen Bridging, said: “Recently we have made several key personnel decisions as we structure the business for £1bn in total lending, having recently hit the £500m mark.”

- This H1 took cumulative Aspen lending to £594m, and lending this H1’s £93m every six months would get Aspen to £1b during H2 2027.

Boardroom

- SUS is run by the Coombs family, and lead executives Anthony and Graham Coombs are grandsons of founder Clifford Coombs and have worked at the business since the mid-1970s:

- The H1 webinar revealed the Coombs family controls at least 52% of the shares (an £89m-plus combined investment) and it’s this “identity of interest between management and shareholders”...

[FY 2024] “Our over-arching factor in the success of our business over 80 years and through three family generations of management is our business philosophy. The identity of interest between management and shareholders has fused our ambition for growth with a conservative approach to both credit quality and funding.”

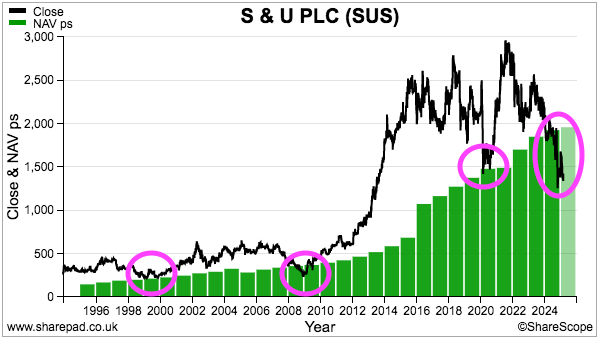

- …that has delivered illustrious dividend and NAV advances since 1987:

- Various appointments do suggest the Coombs family prefers Aspen to Advantage.

- Jack Coombs for instance is a main SUS board executive and an Aspen director. At 37 years old, Jack Coombs may well become the lead SUS/Coombs director when his 72-year-old cousins Anthony and Graham decide to retire.

- Richard Coombs — son of Graham Coombs — joined Aspen during 2023.

- I note SUS’s head office and Aspen are both located in Solihull while Advantage is based in Grimsby.

- From what I can tell, Anthony and Graham Coombs act as ‘capital allocators’ within S&U.

- Dividends are paid by Advantage and Aspen to the parent company, whereby Anthony and Graham Coombs can then decide to:

- Redeploy the money back into Advantage and/or Aspen;

- Return the money to shareholders as a dividend, or;

- Reduce debt.

- This H1 witnessed the Coombs executives allocate the bulk of the parent-company’s incoming capital towards Aspen (see Financials), which SUS disclosed had for the first time attained an 11% return on capital employed.

- Despite the then £17 shares trading below book value (see Valuation), the H1 webinar confirmed buybacks were still not being considered:

“Share buyback makes the market for the shares even narrower because there will be less shares out there and possibly less shareholders as well. So given the fact that we’re a public company and we do value shareholder value… we tend to say we’ll stay with the same structure and we’ll pay dividends instead. We have obviously thought about other forms of shareholder structure but at the moment we intend to stay with the interesting one that pays dividends.“

- While that explanation may not have been entirely satisfactory, the subsequent Court of Appeal judgements have nonetheless proved SUS was right not to undertake buybacks at that time.

- The preceding FY welcomed Advantage’s new boss Karl Werner…

[FY 2024] “[SUS has] great pleasure in welcoming Karl Werner as the new Chief Executive of Advantage. Karl has impressed enormously in the few months he has been with us, and his long experience of the finance industry and its regulation, particularly at MotoNovo and Aldermore Bank will make him a distinguished successor to Graham Wheeler.”

- …who became Advantage’s boss on the first day of this H1.

- Mr Werner’s “long experience of the finance industry and its regulation, particularly at MotoNovo and Aldermore Bank” has taken on greater relevance following the Court of Appeal’s judgements.

- The exposing of MotoNovo’s commission arrangements by the Court of Appeal does not present Mr Werner’s MotoNovo tenure in a good light.

- In particular, the Court of Appeal revealed the “materially untruthful and misleading” customer documentation that hid a car dealer’s commercial bias towards MotoNovo:

[Court of Appeal October 2024] “Although it made reference to the possible payment of a commission, and made it clear that the broker was not going to search the whole market, there were a number of materially untruthful and misleading statements in the Suitability Document. In consequence the document created the false impression that the Trade Centre Wales were exercising their judgement in selecting a finance provider which “may be most appropriate” for the customer’s needs from a panel of 22 lenders, when in fact there was an undisclosed obligation which tied the broker into giving FirstRand [MotoNovo] first refusal in every case.”

- I note Mr Werner has not yet joined SUS’s main board despite leading Advantage since 01 February 2024 — a period of 14 months.

- In contrast, Mr Werner’s predecessor joined SUS’s main board exactly a year after becoming Advantage’s boss on 01 October 2019.

Financials

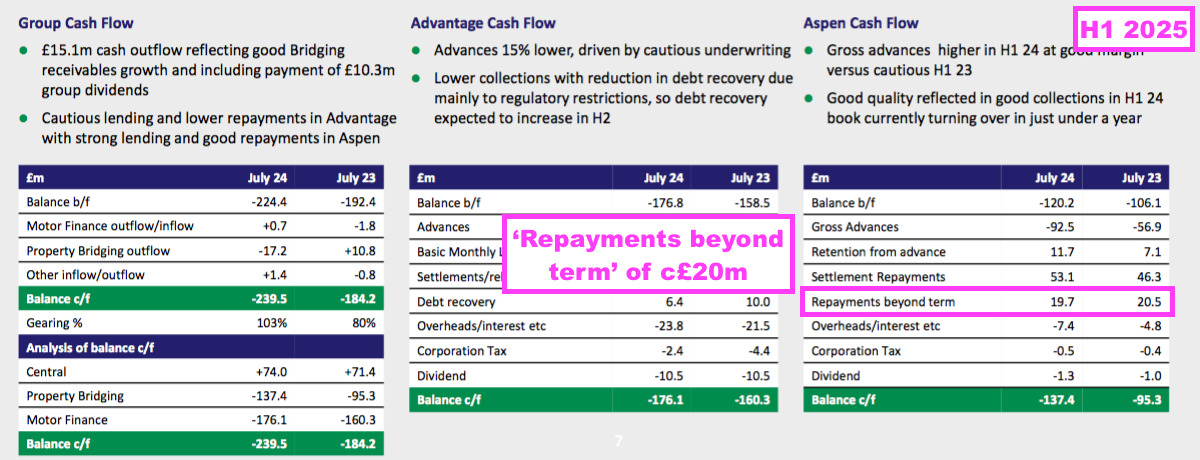

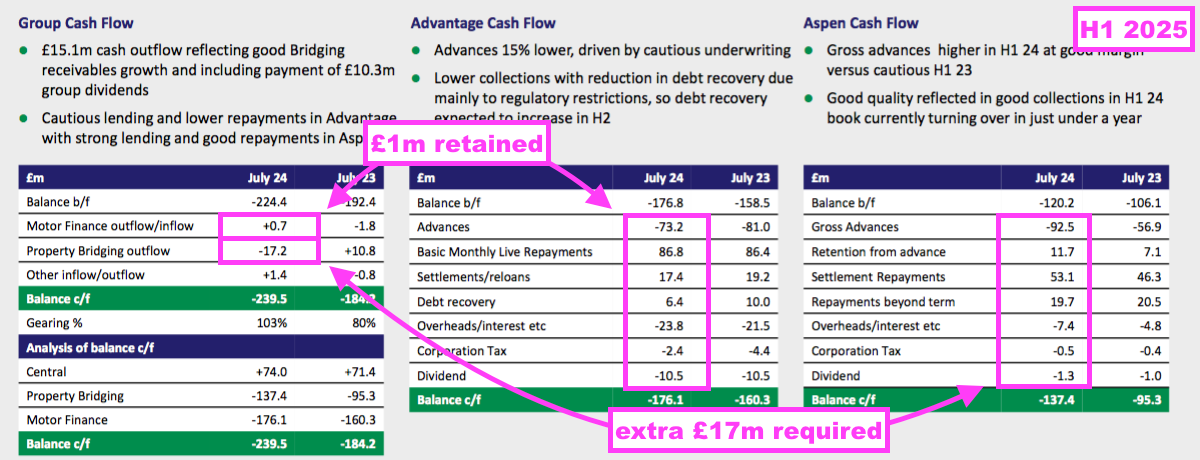

- This H1 witnessed Advantage retain £1m after lending £73m, collecting £111m, expensing £26m and paying £11m through dividends to the parent company:

- Aspen meanwhile required an extra £17m after lending a net £81m, collecting £73m, expensing £8m and paying £1m through dividends to the parent company.

- Advantage retaining £1m while Aspen requiring an extra £17m emphasises clearly which division SUS expects to earn the greater returns:

- Indeed, since the start of FY 2020, SUS has taken on additional debt of approximately £130m to fund new loans, of which Advantage received approximately £10m while Aspen received approximately £120m.

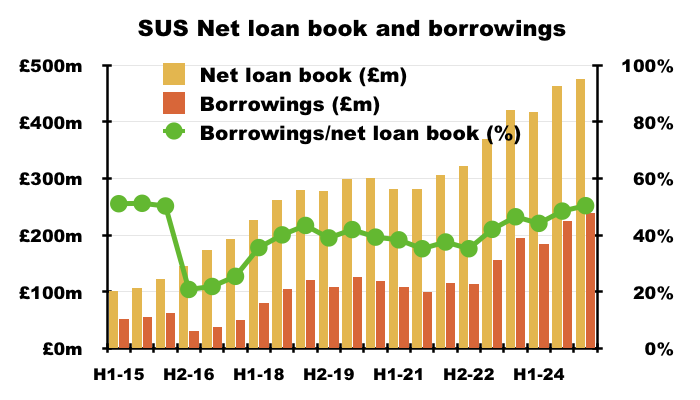

- The extra £17m required by Aspen during this H1 was covered mostly by additional borrowings of £15m that took debt to £240m.

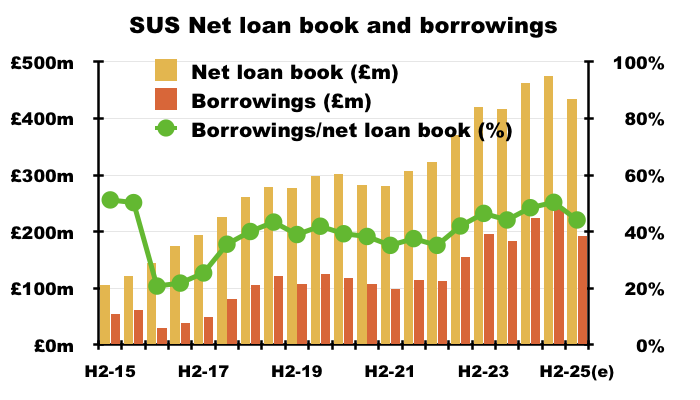

- Debt at £240m does not appear excessive relative to the £475m lent to customers (after impairments):

- Net finance costs during this H1 were £9.6m, implying SUS’s average £232m H1 borrowings incurred interest at approximately 8.3%.

- 8.3% compares to 8.0% for the preceding H2, 7.1% for the comparable H1 and 4.8% for FY 2023.

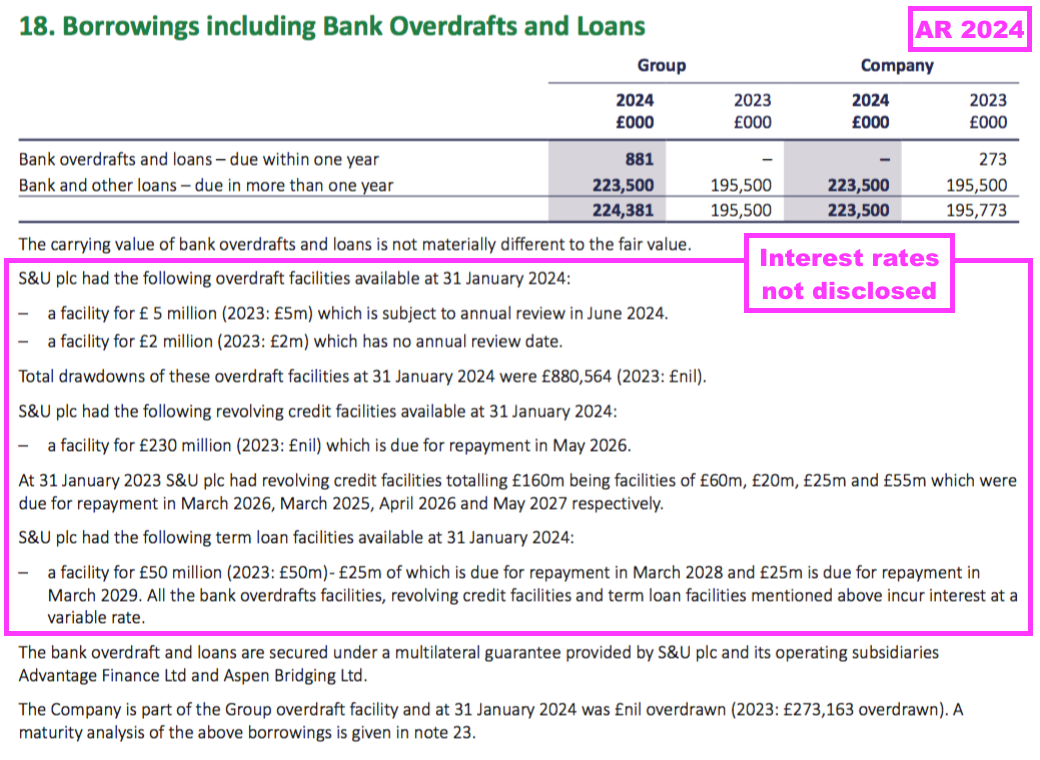

- SUS does not disclose the exact rates payable on its debt facilities, which is very poor form for a main-market company:

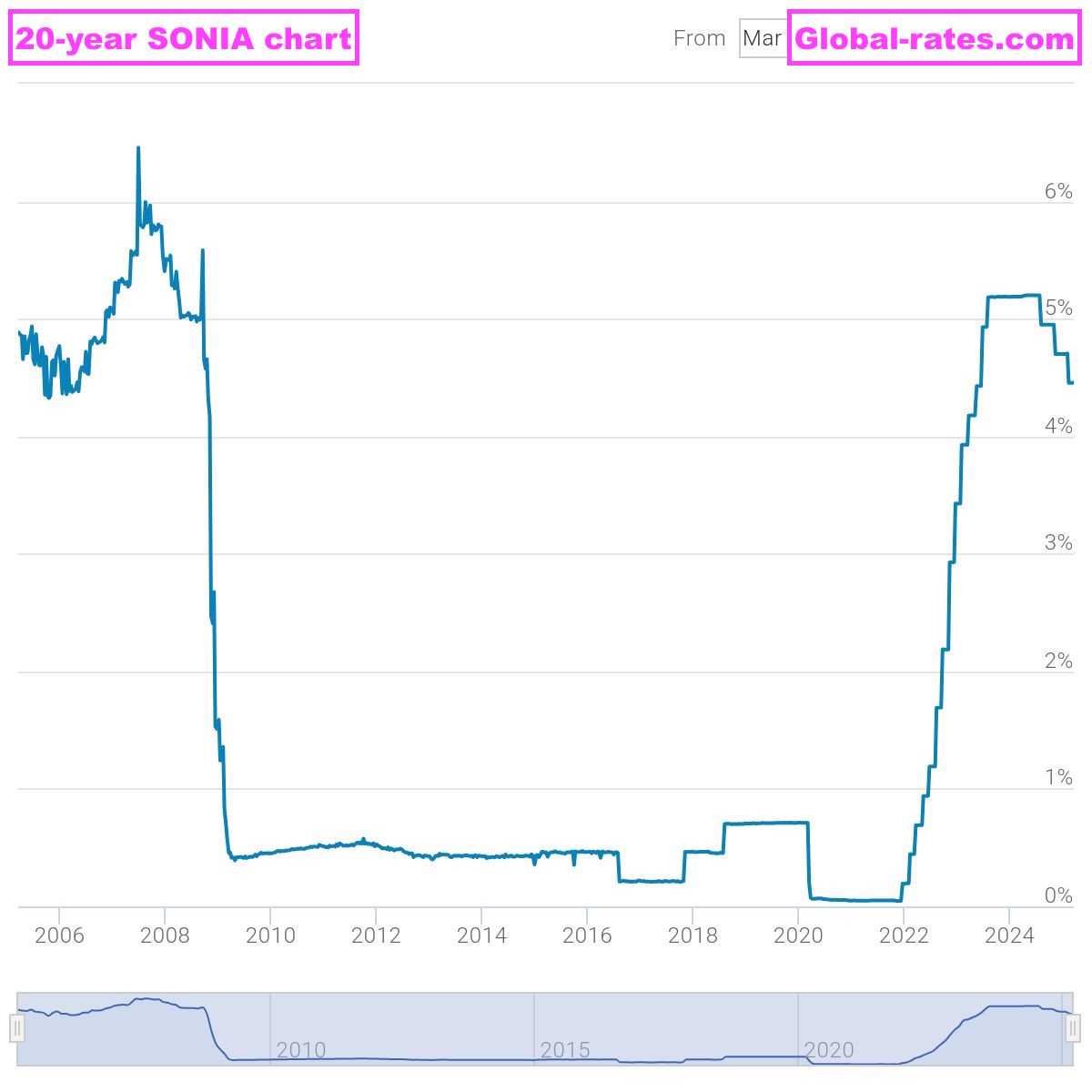

- The FY 2023 webinar disclosed borrowing costs were “just less than 3%” above SONIA.

- SONIA is currently 4.45%, which means SUS may now be paying approximately 7.45% on its debt.

- This H1 revealed borrowings had since reduced from £240m to £220m:

“Borrowings in early October are just under £220m, which gives ample headroom, and are currently projected to continue to do so for the next 18 months. As usual, facilities will be supplemented if required.”

- Trading updates during December and February then revealed borrowings reducing further to £211m and £192m (see H2 2025 trading updates).

- 7.45% on debt of £192m equates to annual bank interest of £14m versus the £18m or so paid during this H1 and the preceding H2.

- Interest payable by all customers (both Advantage and Aspen) is fixed throughout their agreements, and therefore the higher interest incurred by SUS has diminished the returns earned on the money the group has already lent…

- …particularly at Advantage, where loan terms now last for 55 months.

- SONIA surpassed 5% during 2023, and another three years or so will be required before all the Advantage loans written when SONIA was much lower are settled:

- Given the Court of Appeal judgements and the possibility of Advantage becoming liable to pay significant ‘secret’-commission compensation, this H1 (in retrospect!) wisely reiterated SUS’s borrowing facilities were supported by long-time banking partners:

“S&U has long benefitted from its banking relationships stretching back over 80 years. It is therefore appropriate that £230m of its facilities are both sustainably linked and have a 3-year profile. A further £50m of facilities stretch to 2028/2029.”

- Post-H1 borrowings of £192m and borrowing facilities of £280m give headroom of £88m, which should allow Advantage to pay significant ‘secret’-commission compensation without truly alarming shareholders.

- Paying 7.45% on borrowings at the maximum £280m would lead to interest of £21m, which is only £3m more than the £18m or so paid during this H1 and the preceding H2.

- £3m extra interest equates to 25p per share, which I presume would be funded by a further dividend reduction were compensation claims suddenly to push borrowings to their £280m limit.

H2 2025 trading updates

- The regulatory and legal upheaval suffered by Advantage throughout H2 2025 dominated the trading updates published during December and February.

- December’s RNS referred to “chaotic market conditions produced by the Court of Appeal decision“, with Advantage enduring the following adverse H2 2025 progress:

- The net loan book declining 10% since this H1 to £295m;

- Advances down 33% versus H2 2024;

- Collections of due payments reduced to 86% versus 91% for H2 2024, and;

- Pre-tax profit at “around half the level” of H2 2024.

- Advantage’s pre-tax profit “around half the level” of H2 2024 implies a divisional H2 2025 pre-tax profit of less than £5m versus £9.4m for this H1.

- Advances down 33% clearly indicates Advantage curtailed its lending following the Court of Appeal judgements.

- I am sure SUS has studied the Court of Appeal’s summary of the Hopcraft case, given December’s update also stated claims of “consumer harm” can “reasonably be evidenced not to exist”:

[RNS December 2024] “The Court of Appeal decision… introduced a shift in expectations that differed from previous regulatory guidance on the matter followed by Advantage and most of the industry. The result has been a cock‐shy of opportunistic claims by CMCs (Claims Management Companies) on social media which are disruptive and which in the case of regulatory-compliant commission disclosures seek to allege a consumer harm which can reasonably be evidenced not to exist.”

- SUS’s request for the Supreme Court to adopt a “common-sense approach” seemed reasonable in the circumstances:

[RNS December 2024] “I therefore hope and expect that a common‐sense approach to the matter will be taken by the Supreme Court and the Government thus restoring order to a very important industry.”

- February’s update reiterated the request to the Supreme Court for a “common-sense approach“:

[RNS February 2025] “The question does remain as to whether this new encouragement of responsible risk‐taking will extend to the Supreme Court, when it reviews last October’s Court of Appeal decision on commission disclosure which has so disrupted the entire motor finance market. Again, the signs are cautiously encouraging. The speed with which the Supreme Court is considering the matter and their sanctioning direct representations from the Treasury, the FLA, and the Financial Conduct Authority, speak to a common‐sense approach.“

- February’s update also described the ‘consumer harm’ from ‘secret’ commissions as “marginal” and any subsequent compensation being “minimal“:

[RNS February 2025] “My view is that even should the Supreme Court uphold the lower courts’ decision in principle, any ‘harm’ found to have been suffered by consumers will be so marginal as to make demands for redress minimal.”

- February’s update confirmed Advantage had witnessed its:

- Net loan book shrink from the £295m stated within the December update to £283m;

- Collections of due improve from the 86% stated within the December update to 87%, and;

- Transactions recover to “over 900” during January.

- Transactions recovering to “over 900” during January is further evidence of curtailed lending following the Court of Appeal judgements; loans issued during this H1 exceeded 1,000 a month:

- February’s update revealed the following positive Aspen progress for FY 2025:

- Transactions up 16% on loans averaging more than £900k;

- Total net loans up 17% to £152m;

- Collections up 25% to £157m;

- Defaults remaining “stable“, and;

- Profit before tax up approximately 50%.

- Aspen’s profit before tax up 50% implies £7.2m for FY 2025.

- December’s update revealed borrowings had reduced from this H1’s £240m to £211m, while February’s update disclosed borrowings had reduced further to £192m.

- Reducing borrowings seems the wisest capital-allocation decision ahead of a potentially adverse Supreme Court decision.

- Based on February’s update, the group’s net loan book for FY 2025 appears to be £283m (Advantage) + £152m (Aspen) = £435m, and borrowings of £192m would be equivalent to 44% of that £435m:

- Based on February’s update, SUS’s FY 2025 NAV could be £435m (net loan book) less £192m (borrowings) = £243m or approximately £20 a share.

- February’s update underlined Advantage’s ongoing difficulties by announcing the second interim dividend of FY 2025 would be reduced by 5p to 30p per share:

[RNS February 2025] “S&U’s dividend policy has always had three aims. First, the close alignment of interest between management and shareholders, reflecting sustainable growth and a conservative approach to gearing. Second, we satisfy shareholders’ appetite for yield in a narrow trading market. Third, we take a sensible but ambitious view of S&U’s prospects. Thus, despite this year’s hiatus in profit growth, we propose that the second interim dividend should be 30p per share (2024: 35p), payable on 7 March 2025 to shareholders on the register on 17 February 2025.“

Valuation

- SUS’s current valuation suggests:

- The profitability of used-car finance has been eroded permanently, and;

- A substantial compensation bill will follow the Supreme Court decision.

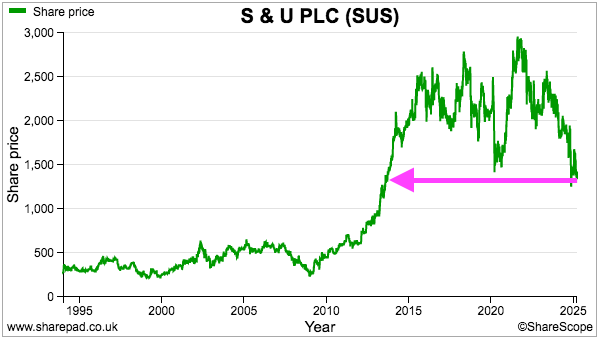

- The £14 shares trade at just 0.73x this H1’s £19.21 NAV per share.

- For perspective, the shares have traded at or below NAV only occasionally during the last 30 years: