19 September 2024

By Maynard Paton

FY 2024 results summary for S & U (SUS):

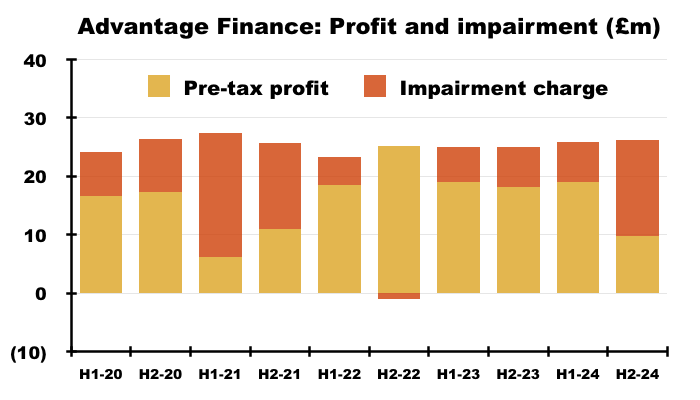

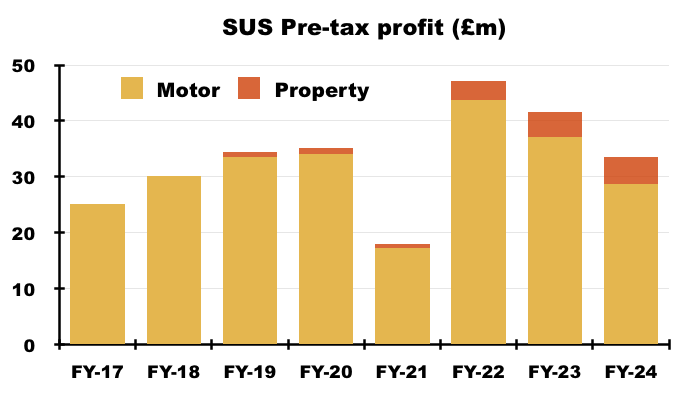

- A very disappointing FY, with H2 profit slumping 41% and the final dividend cut by 17% as enhanced FCA “forbearance” regulations prompted the “temporary” modification of motor-finance collections and led to impairments surging 74%.

- Various motor-finance ratios unsurprisingly deteriorated, including the first-payment proportion plunging to an alarming 94%, collections of due falling to a below-budget 90%, anticipated repayments hitting a fresh 127% low and up-to-date accounts sliding to 74%.

- At least the property-loan subsidiary continues to perform well, as minimal bad loans led to a new £5m profit high, an impressive 58% divisional return on equity and a company-blog ambition to double cumulative lending to £1 billion “in the next couple of years“.

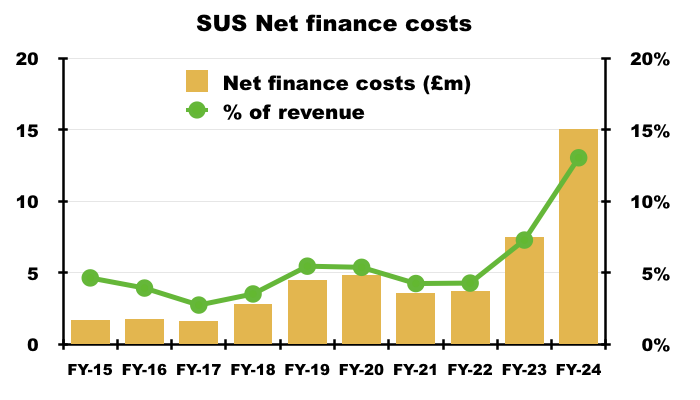

- Debt advancing to £224m and borrowing rates climbing to 8% caused net finance costs to absorb a significant 13% of revenue; extra post-FY debt could meanwhile take net finance costs from £15m to £19m and exacerbate the profit “headwinds“.

- Post-FY references to “vigorous” FCA discussions, political intervention and up-to-date accounts running at a pandemic-like 69% now leave the £18 shares firmly below NAV, a valuation witnessed only very occasionally during the last 30 years. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own SUS

- Results summary

- Revenue, profit, net asset value and dividend

- Advantage Finance: loan sizes and rates

- Advantage Finance: loan volumes and first payments

- Advantage Finance: collections and estimated repayments

- Advantage Finance: up-to-date and overdue accounts

- Advantage Finance: impairments

- Aspen Bridging

- Boardroom

- Financials: cash flow and debt

- Financials: returns on assets and equity

- Financials: employees

- Regulation: Borrowers in Financial Difficulty

- Regulation: Consumer Duty

- Regulation: SUS response

- June and August trading updates

- Valuation

News links, share data and disclosure

- Annual results, presentation and webinar for the twelve months to 31 January 2024 published/hosted 09 April 2024;

- Trading update published 06 June 2024, and;

- Trading update published 12 August 2024.

- Share price: 1,800p

- Share count: 12,150,760

- Market capitalisation: £219m

- Disclosure: Maynard owns shares in S & U. This blog post contains SharePad affiliate links.

Why I own SUS

- Provides ‘non-prime’ credit to used-car buyers and property developers, where disciplined lending, conservative financing and reliable service have supported an illustrious NAV and dividend record.

- Boasts veteran family management with a 40-year-plus tenure, 44%-plus/£97m-plus shareholding and a “steady, sustainable” and organic approach to long-term expansion.

- Enhanced regulation, economic “headwinds“ plus higher debt costs have left the shares trading below NAV, which history suggests can be an attractive buying opportunity.

Further reading: My SUS Buy report | All my SUS posts | SUS website

Results summary

Revenue, profit, net asset value and dividend

- An adverse statement during February that confessed to various “headwinds“…

[RNS 2024] “Since S&U’s last trading statement two months ago, the headwinds I reported then of poor consumer confidence, continuing high interest rates, cost of living pressures and regulation have, unsurprisingly, impacted the Group’s progress and profitability.”

- …and warned pre-tax profit would be 10-15% below the then-£38m consensus expectation…

[RNS 2024] “In particular, the reduction in the rate of collections has necessitated increased provisioning under the IFRS9 accounting standard. Thus, our group profit before tax for the year ended 31 January 2024 is likely to finish between 10% and 15% below consensus expectations of c£38m. Nonetheless, we expect a solid rebound; hence our continued funding investment in both businesses of £15m during the period.”

- ...and announced the second interim dividend would be cut by 8%…

[RNS 2024] “It is therefore right that at a time when the cost of living, funding and regulatory challenges have had an impact on profits, we partially protect returns to shareholders as we also did during the pandemic. Hence this year we propose that S&U’s second interim dividend should be 35p (2023: 38p), payable on 8th March to shareholders on the register on 16th February.“

- …had already heralded this very disappointing FY 2024.

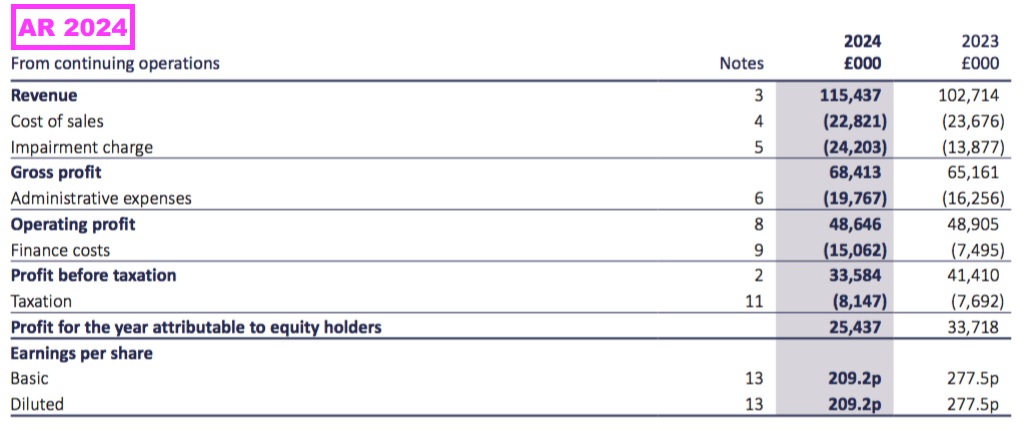

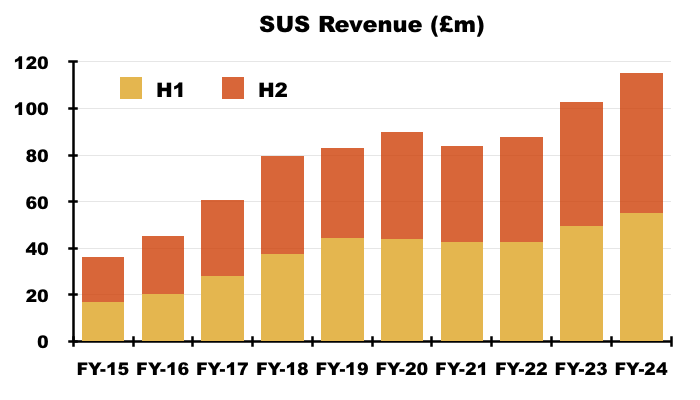

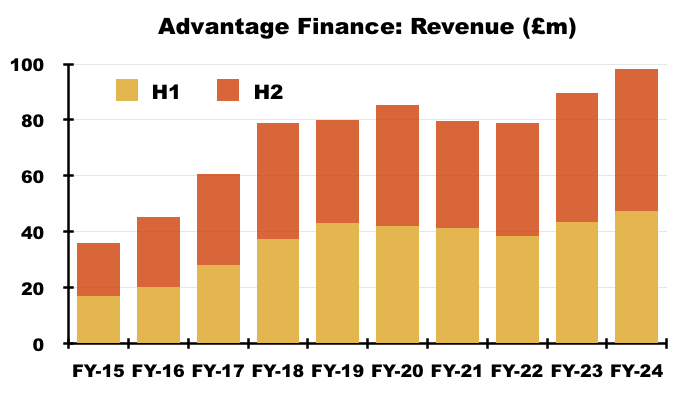

- The lower profit and dividend were declared despite revenue gaining 12% to £115m, which in fact set a new annual peak:

- H2 revenue in fact gained 13% to £60m to set a new record for any H1 or H2.

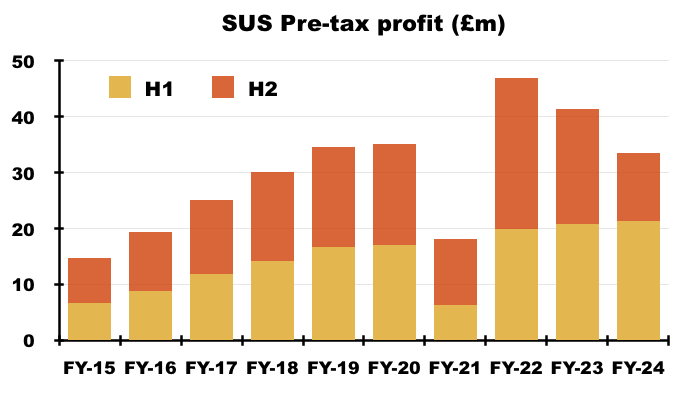

- Pre-tax profit did indeed reduce by 10-15% below the then-£38m consensus, falling 19% to £34m:

- H2 pre-tax profit slumped 41% to £12m after February’s statement claimed the “headwinds” had been “largely confined” to Q4.

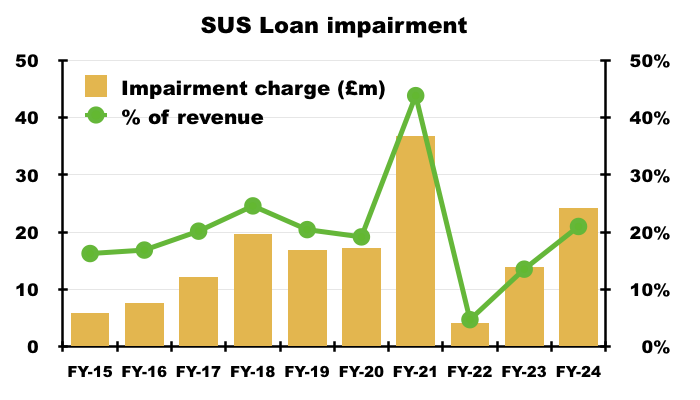

- The FY profit reduction followed loan impairments surging 74% to absorb 21% of FY revenue (see Advantage Finance: impairments)…

- …and FY net finance costs more than doubling to £15m to absorb 13% of FY revenue (see Financials: cash flow and debt):

- Greater impairments and finance costs were experienced during H2 versus H1.

- H2 impairments absorbed 28% of H2 revenue (versus 13% during H1)…

- …while H2 net finance costs absorbed 14% of H2 revenue (versus 12% during H1):

- The pre-tax profit reduction was in part amplified by the comparable FY enjoying “lower than normal” loan impairments:

[FY 2023] “Impairment charge of £12.9m (2022: £3.8m; 2021: £36.0m) still lower than normal as increase in stage 1 and macroeconomic overlays for forecast future inflation and car prices, more than offset by excellent collections and lower than anticipated realised bad debts“

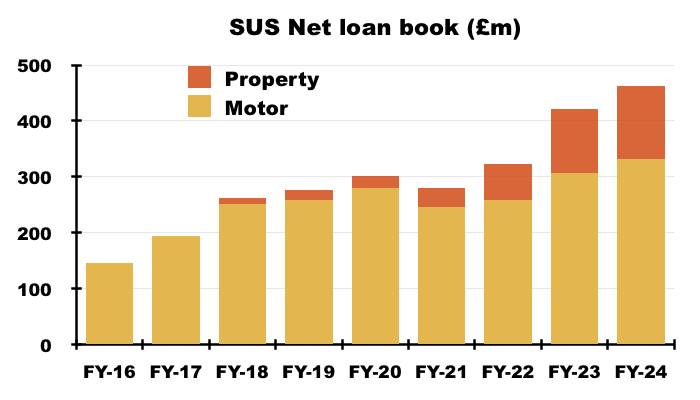

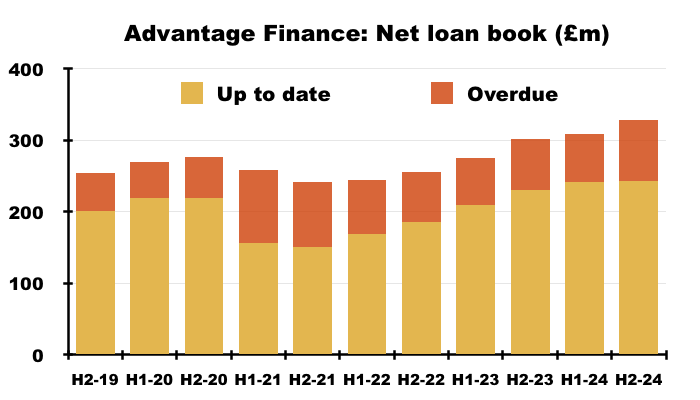

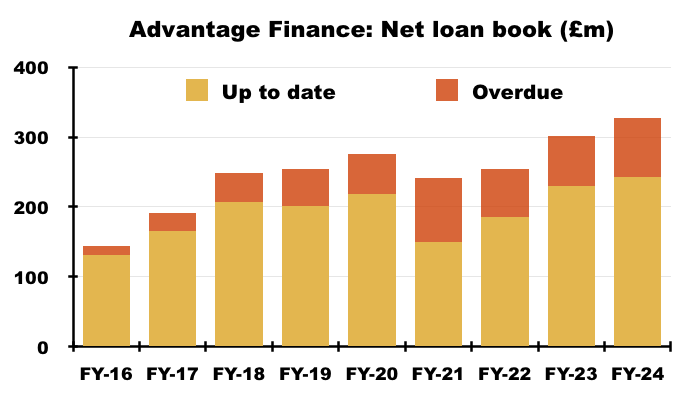

- The accounts continue to be dominated by SUS’s motor-finance division, Advantage Finance, although SUS’s property-loan division, Aspen Bridging, is becoming a greater part of the group:

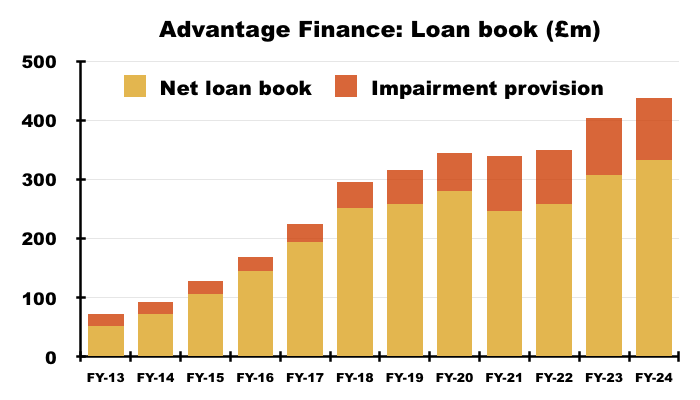

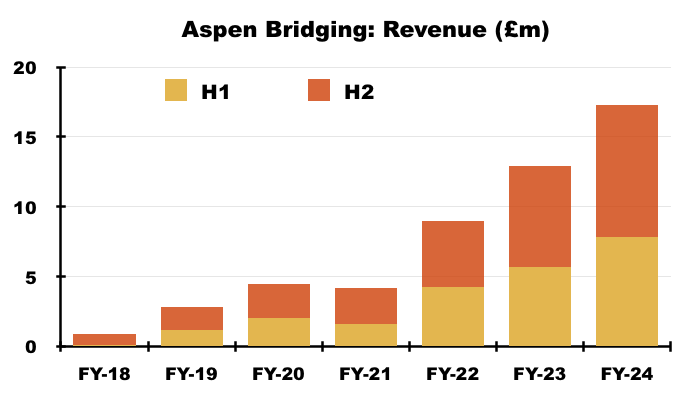

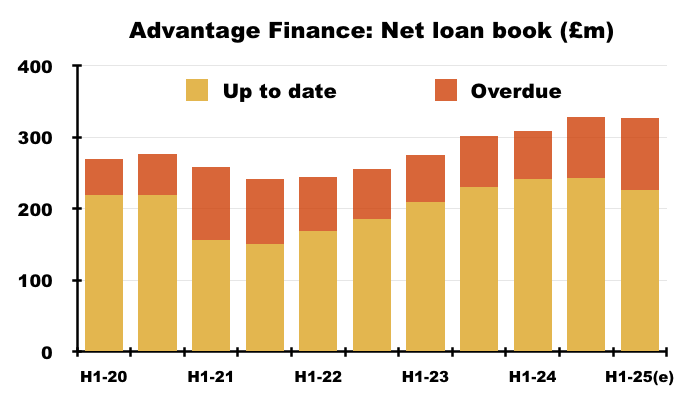

- The group’s net loan book advanced 10%, or £43m, to £463m during this FY, spread between an 8% advance to the motor-finance book (see Advantage Finance: loan sizes and rates) and a 15% advance to the property-finance book (see Aspen Bridging).

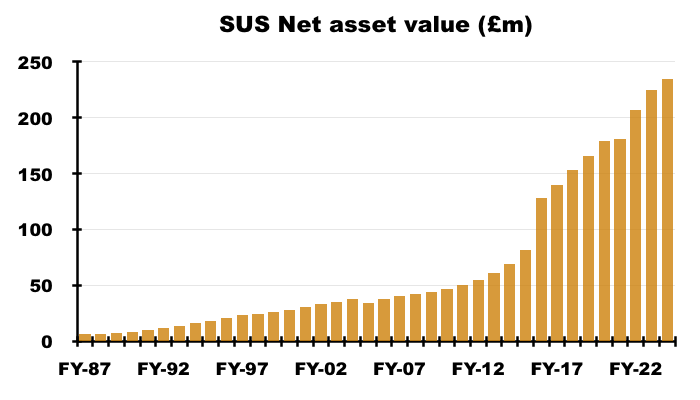

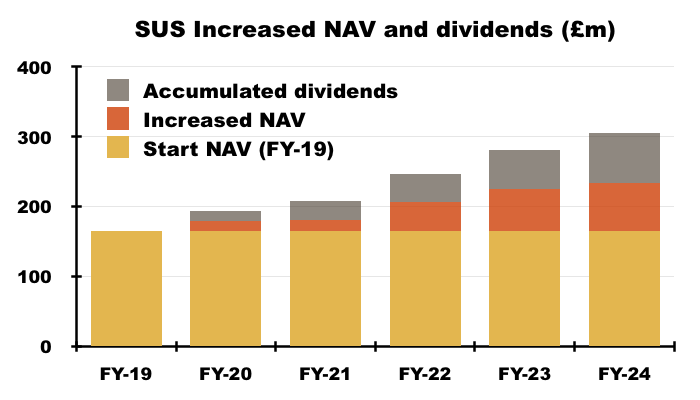

- The larger loan books were funded by greater debt, which during this FY expanded 15% to £224m (see Financials: cash flow and debt) to leave the group’s net asset value (NAV) £9m/4% higher at £234m — equivalent to £19.27 per share and a fresh NAV record:

- The £234m NAV exceeds the £219m market cap (see Valuation).

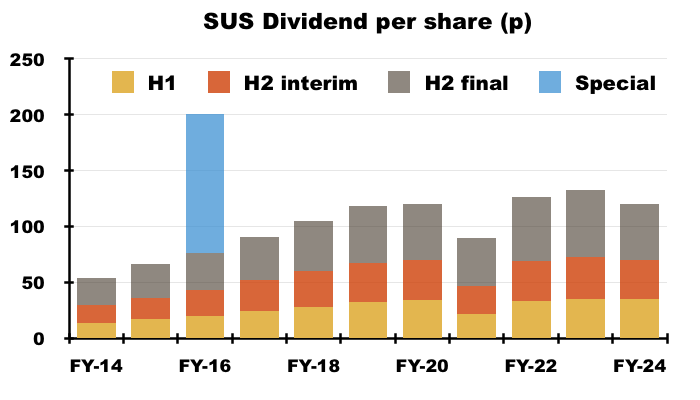

- February’s cut to the second interim dividend may have already hinted the final payout would not be maintained.

- This FY revealed a 17% final-divided reduction as SUS bemoaned higher wage inflation, higher debt costs and higher taxes:

“Whilst recognising its primary responsibilities to its shareholders,S&U has always sought to balance the interests of all its stakeholders. This year’s fall in profit together with our wish to protect our loyal staff from recent increases in the cost of living has made this a particularly delicate one this year.

Thus, except for senior directors, average salaries this year have matched the rate of inflation, with more for living wage earners. Higher base interest rates have cost the Group an additional £8m this year, and our incoherent Government have raised the rate of corporation tax by nearly a third.

Taking all this into account, subject to the approval of shareholders at our AGM on 6 June, the board proposes a final dividend of 50p per ordinary share (2023: 60p).”

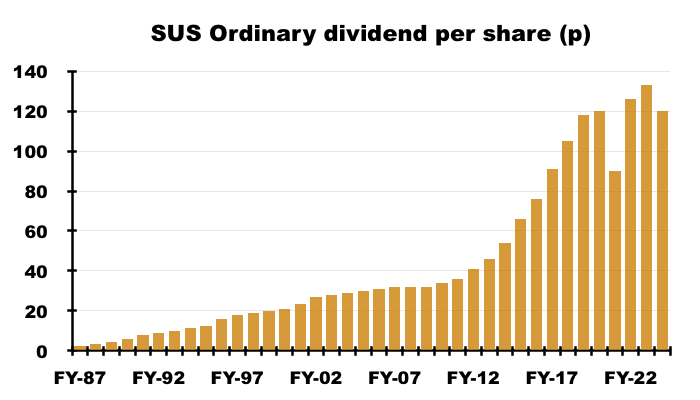

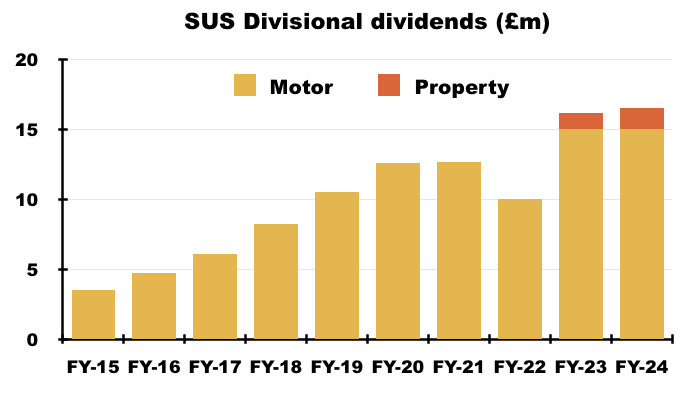

- The 17% final-dividend reduction left the FY dividend down 10% at 120p per share:

- Prior to the pandemic, SUS had not cut its annual dividend since 1987:

- Such an illustrious payout record suggests the aforementioned “headwinds” that have cut this FY’s dividend are unprecedented.

- This FY’s disappointing performance has extended into FY 2025. June’s trading update admitted Q1 2025 profit had dropped 34% while August’s trading update warned of motor-finance repayments sliding to 87% of due (see June and August trading updates).

Advantage Finance: loan sizes and rates

- SUS describes the customers of Advantage Finance as ‘non-prime’ and this FY outlined their typical circumstances:

“This long experience has enabled Advantage to gain a significant understanding of the kind of simple hire purchase motor finance suitable for customers in lower and middle-income groups. Although decent, hardworking and well intentioned, some of these customers may have impaired credit records, which have seen them in the past unable to access rigid and inflexible “mainstream” finance products.”

- Advantage has operated since 1999 and attracts customers for used-car loans via competitive rates and excellent customer service. Customers are acquired mostly through car dealers and finance brokers, and often receive their loans on the day of their application.

- However, Advantage’s “experienced, sensitive and sophisticated under-writing” does limit the number of successful applications. Advantage now receives more than 2 million applications a year, from which only 21,565 loans were awarded during this FY (see Advantage Finance: loan volumes and first payments).

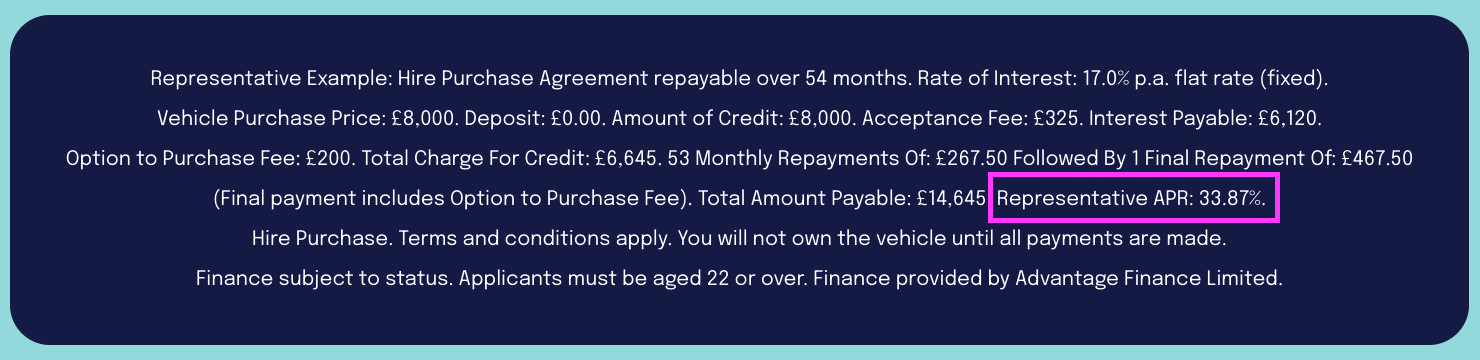

- Advantage’s website cites a representative APR of 33.87%:

- The representative example indicates borrowing £8.0k at a flat 17% a year over 54 months leads to interest of £6.1k and a total repayable of £14.6k including a £325 acceptance fee and a £200 vehicle-purchase fee.

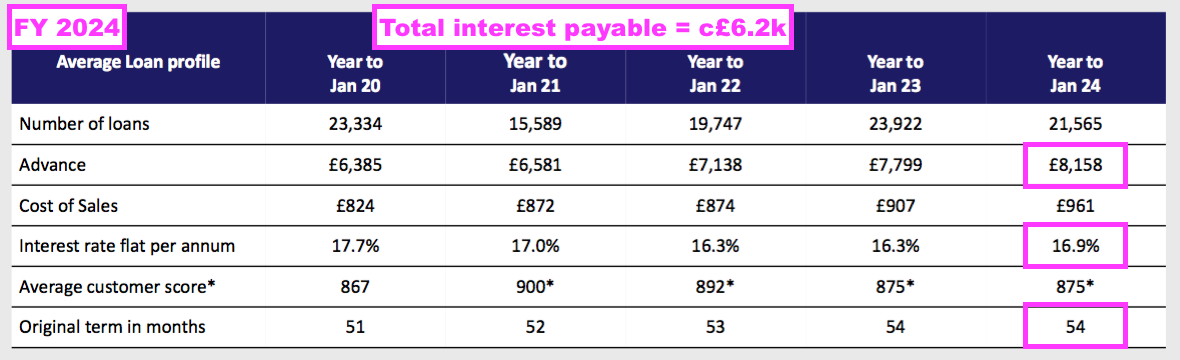

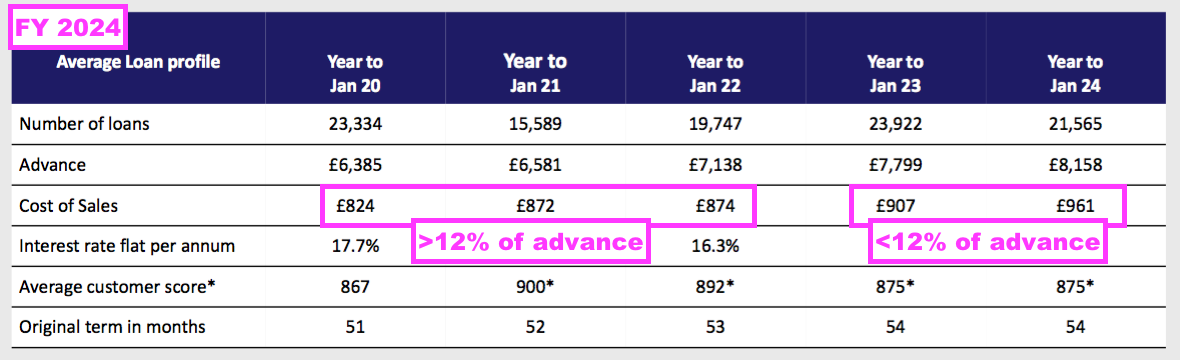

- Loan sizes have increased over time. The average amount borrowed by Advantage’s customers to buy a used car surpassed £5k during FY 2012, £6k during FY 2015, £7k during FY 2022 and £8k during this FY:

- The greater loan size reflects the greater price of a used car. The comparable FY claimed the wider used-car market had seen average prices almost double to £17.6k between 2011 and 2022…

- …although this FY quietly noted a “used-car price correction” without giving specific details.

- Rising car prices should be positive for Advantage; customers ought to borrow more money, pay more interest and (in theory) provide SUS (and shareholders) with more profit.

- Customers are ranked into different tiers based on their likelihood to repay, and management said during the preceding H1 webinar that SUS had concentrated on tier B/C/D customers who “give us a higher margin“:

[H1 2024] “The tier mix is very stable. The average… credit score is very stable as well. And we have been spending this year making small increases and improvements in terms of the mid-quality customers, the B to D categories that give us a higher margin, which has helped us to manage our overall interest rate margin moving forward. “

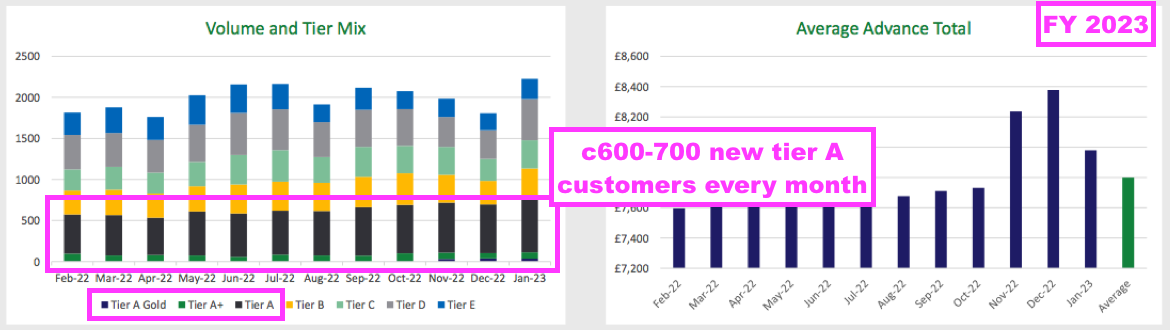

- This FY confirmed a slight shift away the top-tier A+/A customers.

- The preceding FY indicated between 600 and 700 A+/A customers were recruited every month:

- But this FY showed Advantage recruiting approximately 550 monthly A+/A customers:

- The two charts suggest the monthly numbers of B/C/D customers did not change dramatically during this FY, although perhaps the number of bottom-tier-E customers did increase a fraction.

- The shift away from A+/A towards B/C/D/E increased the average (flat per annum) rate the borrowers paid during this FY from 16.3% to 16.9%.

- For perspective, the average rate paid between FYs 2016 and FY 2021 was at least 17%, while the 16.3% charged during FYs 2022 and 2023 was the lowest since at least FY 2012:

- The duration of the typical loan remains longer than historical norms. The 54 months for this FY compares to 50 for FY 2017 and 44 for FY 2012.

- I speculate the lengthier repayment duration reflects the aforementioned higher cost of used cars as customer budgets generally reach a c£275 per month repayment ceiling.

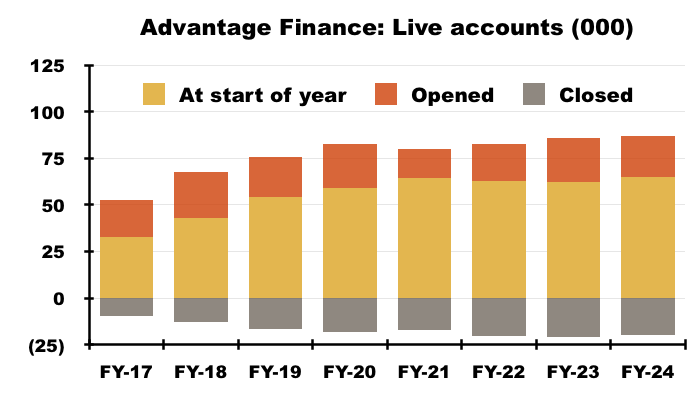

Advantage Finance: loan volumes and first payments

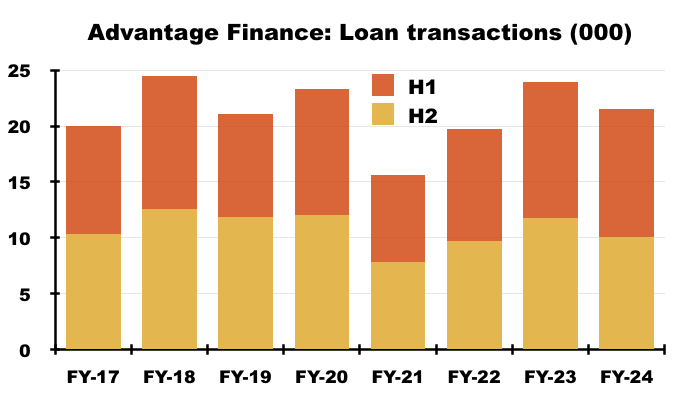

- The 21,565 new motor loans issued during this FY were 10% down versus the comparable FY, but were nonetheless “on budget” given the “the need for a cautious approach in a difficult macro economy“:

- This FY witnessed 53% of loans issued during H2 (11,493), the strongest H2 bias since at least FY 2017.

- The 21,565 new loans issued during this FY were offset by 20,086 accounts closed due to completed repayments, voluntary terminations or the commencement of legal proceedings:

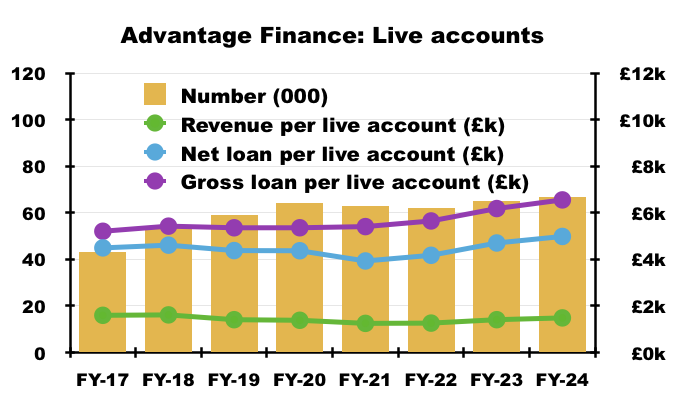

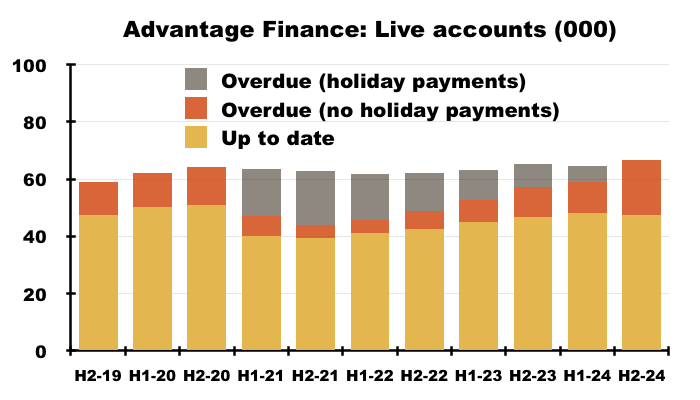

- The account openings and closures left total ‘live’ accounts 1,479 higher at a record 66,702:

- The higher 16.9% average (flat per annum) rate with account numbers surpassing 66,000 helped push Advantage’s FY revenue to a record £98m:

- Emphasising how rapid Advantage has grown, H2 revenue of £51m exceeded the division’s FY 2016 revenue of £45m.

- The aforementioned higher loan sizes translated into revenue per account increasing to nearly £1.5k (the highest since FY 2018), with the average loan outstanding before impairments now at a new £6.6k high and the average loan outstanding after impairments at a new £5.0k high.

- The aforementioned 2 million-plus unique applications during this FY was lower than the 2.5 million cited during the comparable FY, but was double the 1 million cited for FY 2019.

- The preceding H1 webinar revealed a “fairly consistent” 30-35% acceptance application rate that helped “demonstrate the rigour of Advantage’s underwriting and affordability checks”.

- But then converting only 3% or so of accepted applications into actual loans — say, 2 million applications reduced to 650,000 successful applications converted then into 20,000 actual loans — is influenced by what management has claimed to be “digital tyre kickers”.

- 90% of Advantage’s loans continue to be sourced through brokers.

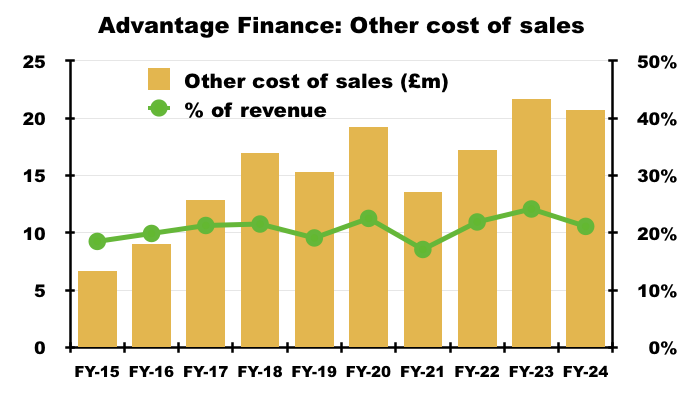

- Cost of sales per loan increased 6% to £961:

- Management’s FY webinar revealed the bulk of the £961 was paid as commissions:

“Cost of sales were £961 in the latest year. For information, about £700 of that is introduced commission, which is a variable cost that goes straight to the broker. Other costs of sales are consumer credit referencing and our data costs.”

- Cost of sales per loan at £961 equated to 11.8% of the £8.2k average loan and remains below the proportion witnessed during FYs 2020, 2021 and 2022.

- Perhaps reflecting the aforementioned shift to higher margin B/C/D-tier customers, cost of sales absorbed 21% of motor-finance revenue during this FY — a welcome reduction following the 24% registered during the comparable FY:

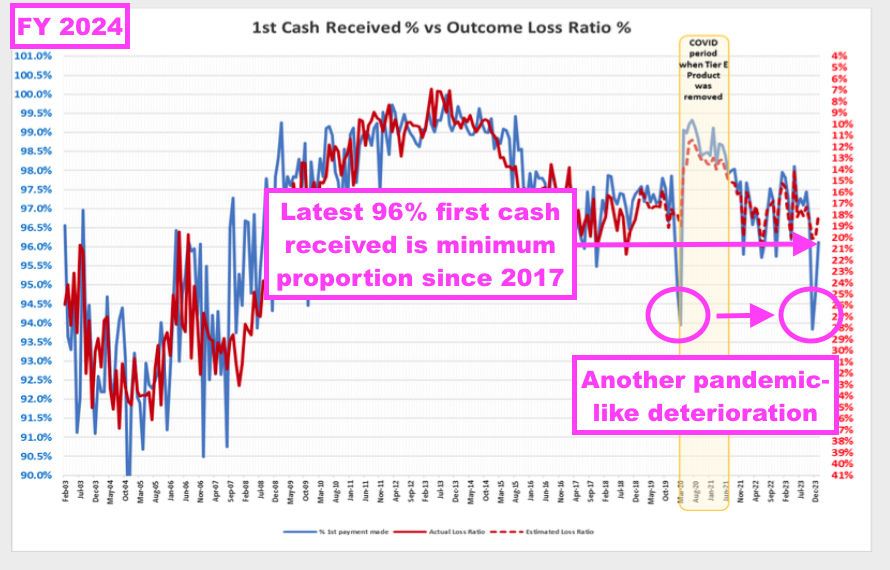

- SUS’s first-payment chart showed an alarming pandemic-like deterioration during Q4 (blue line, left axis):

- The first-payment proportion plunging to 94% during Q4 was referred to as only a “blip” during management’s FY webinar:

“Towards the right of the chart we have got a couple of blips. So the first blip was just at the start of the pandemic when people panicked a bit and didn’t pay their first payment on time. We have also had a blip at Christmas this year, which happily for us has recovered a bit in January but we continue to monitor that as we go.“

- I can only presume the “blip” was due to the aforementioned Q4 “headwinds” of “poor consumer confidence, continuing high interest rates, cost of living pressures and regulation“.

- The proportion rebounding to 96% by January is reassuring, but 96% has typically been the minimum first-payment level (pandemic aside) since late 2017.

- The proportion of borrowers making their first payments on time has shown to correlate inversely to the proportion of loans that ultimately suffer losses (red line, right axis).

- I await the forthcoming H1 2025 to supply a revised version of this first-payment chart. The adverse updates during June and August suggest the blue line may have deteriorated (see June and August trading updates).

Advantage Finance: collections and estimated repayments

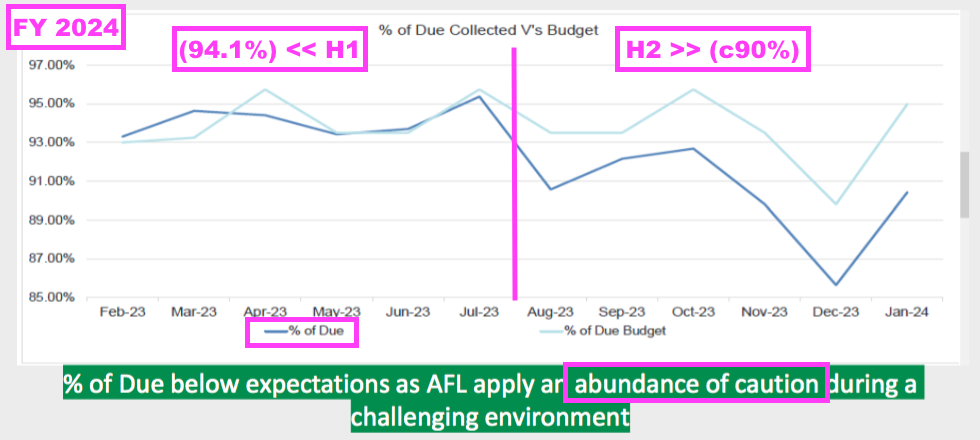

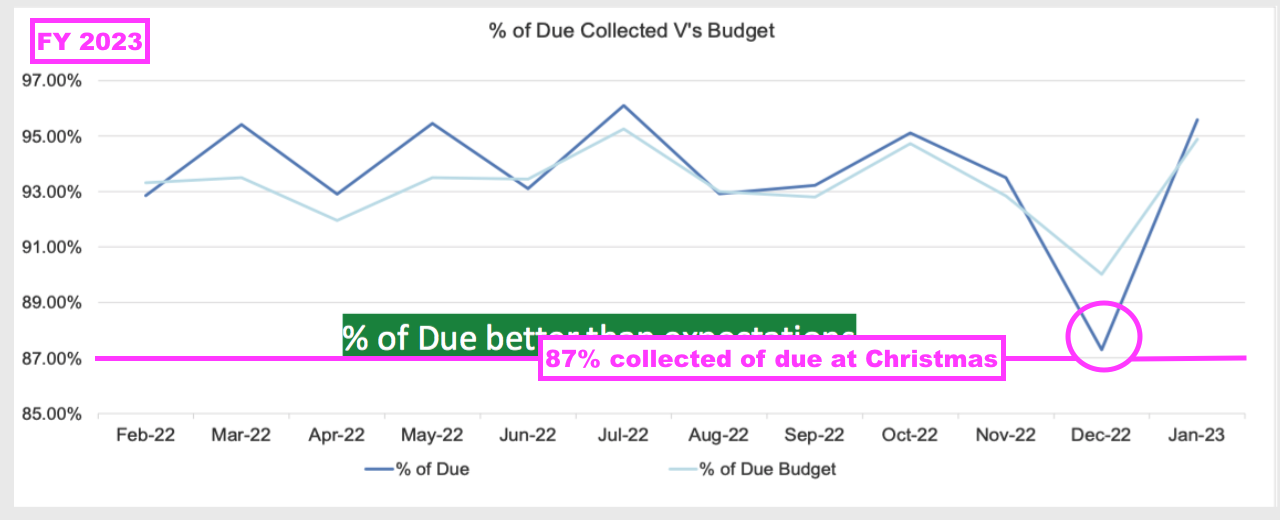

- SUS reported collections during this FY at 92.1% despite a “temporary hiatus” during Q4:

“Our repayments are one indicator of our historically good relations with our valued customers. Thus, despite what we anticipate to be a temporary hiatus in the last quarter, Advantage live monthly repayments as percent of due finished at 92.1% for the year (2023: 93.6%).

- Collections at 92.1% of due compares reasonably well to the 93.6% for FY 2023, 93.2% for FY 2022, 83.3% for (pandemic-blighted) FY 2021 and 93.5% for FY 2020.

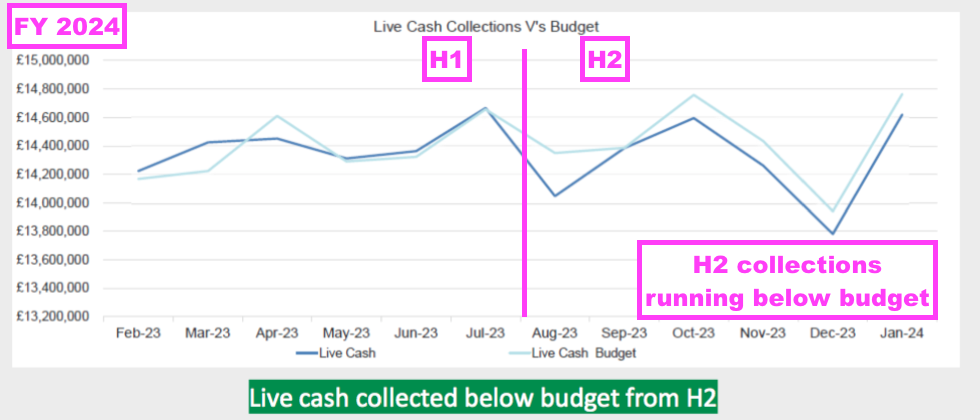

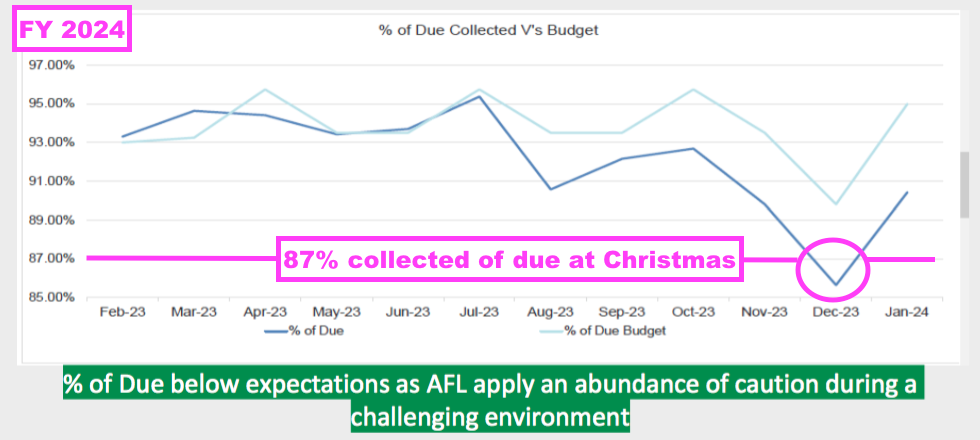

- Mind you, collections were 94.1% of due during H1 and SUS’s chart shows collections were consistently below budget at an approximate 90% average during H2:

- The “temporary hiatus” of collections reflected regulatory intervention and SUS applying an “abundance of caution” with its repayment processes (see Regulation: SUS response):

“In response to ongoing concerns regarding the cost of living and its declared objective to “deliver quantifiable consumer benefits,” the FCA has launched comprehensive inquiries across the industry, affecting approximately two-thirds of non-prime motor finance companies. In anticipation of the findings, Advantage has consented to specific limitations on its repayment processes. These modifications have temporarily influenced monthly repayments and recovery efforts.”

- Trading updates issued during June and August admitted Advantage’s collections had since deteriorated to 87% of due (see June and August trading updates).

- Given the faltering percentage of due-collections, total cash collections ran behind budget throughout H2:

- At least the number of bad debts incurred and the number of voluntary terminations handled for this FY were better than budget:

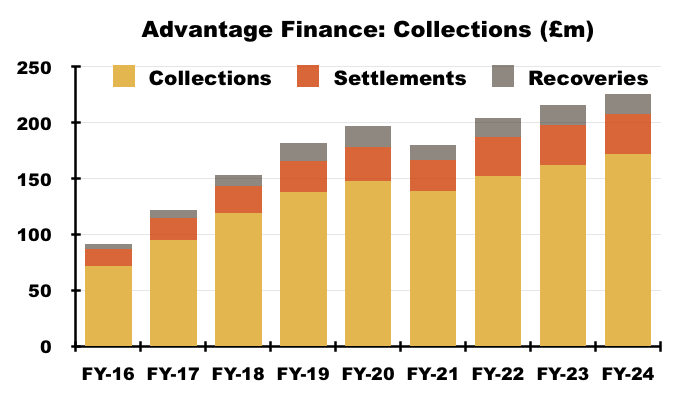

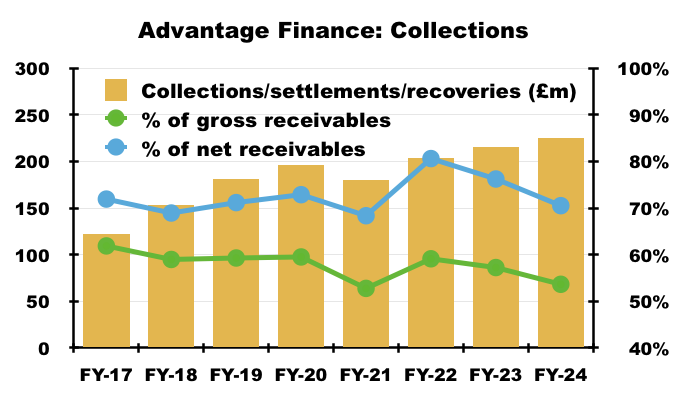

- Advantage’s collections, settlements and recoveries for this FY amounted to £225m, up 4% on the comparable FY:

- However, that 4% advance was less than the 8% increase to Advantage’s loan book.

- As such, collections, settlements and recoveries as a proportion of the gross loan book (i.e. before impairments) and the net loan book (i.e. after impairments) were 57% and 75% respectively, and on a par with the pandemic lows of FY 2021:

- Collections, settlements and recoveries becoming a smaller proportion of the loan book may suggest Advantage’s borrowers are becoming more reluctant to repay.

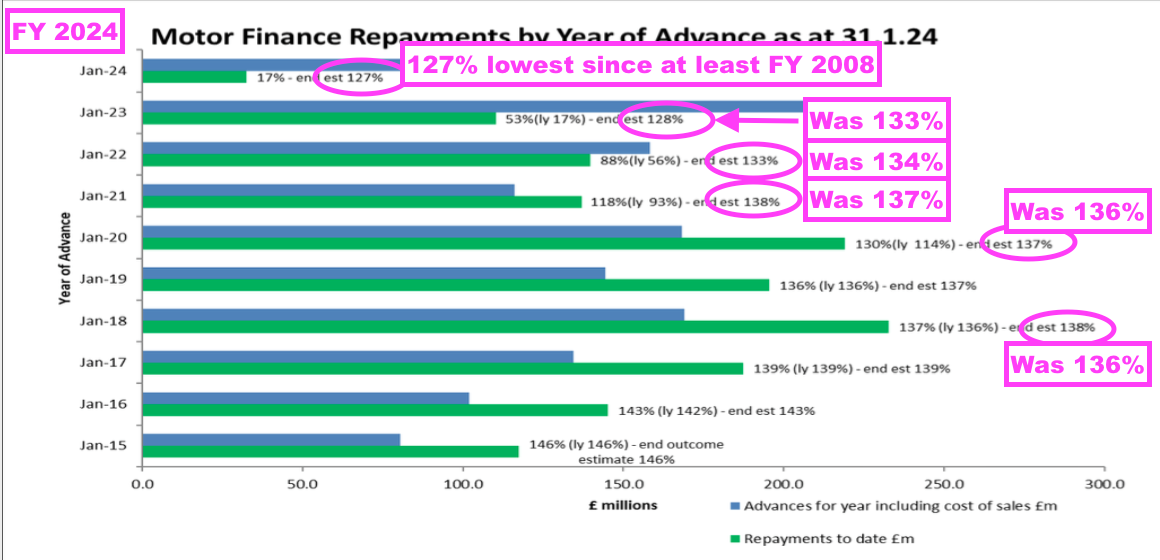

- Advantage’s estimates of future repayments have declined to a worrying new low:

- SUS expects customers will eventually repay 127% of the loans advanced during this FY, which will be the lowest payback percentage since at least FY 2008 if the estimate proves accurate.

- For the loans advanced during the comparable FY, the expected repayment has been reduced from 133% to 128%.

- Collecting 127% of the original loan is some way off the 150%-plus collected for money lent between FYs 2010 and 2014:

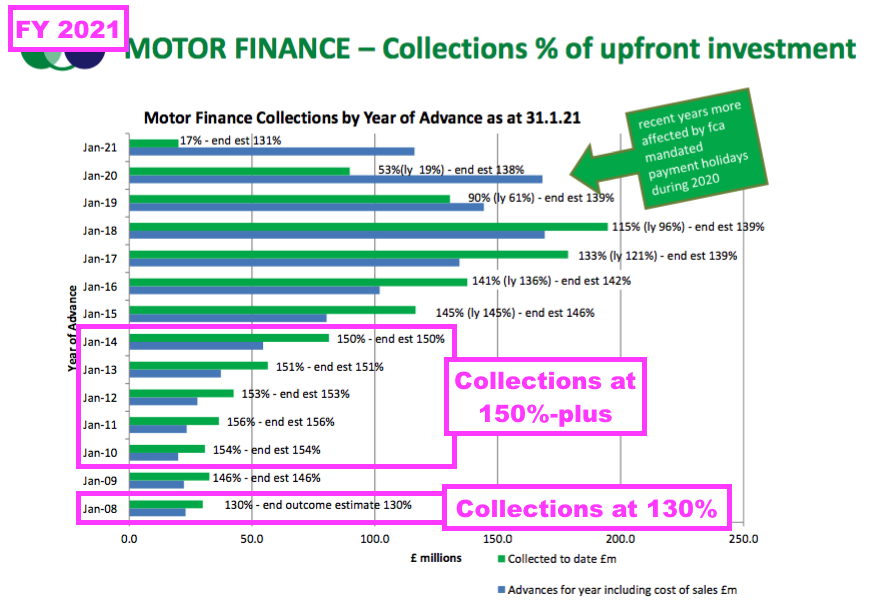

- Note that for (pandemic-blighted) FY 2021, SUS initially estimated a 131% payback for that year’s loans… which has since been uplifted to 138%.

- I am hopeful SUS is once again ‘under-promising’ with a 127% payback estimate for an ‘over-delivery’ during the next few years.

- That said, the introduction of a 127% payback estimate — below the 131% estimate made during the depths of the pandemic — provides further evidence the aforementioned “headwinds” are unprecedented.

Advantage Finance: up-to-date and overdue accounts

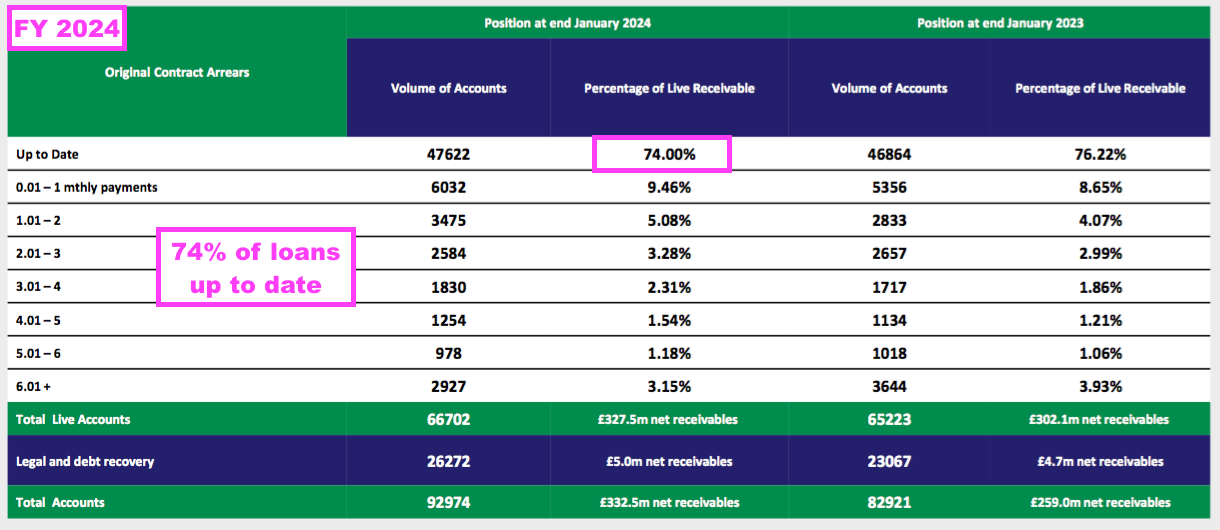

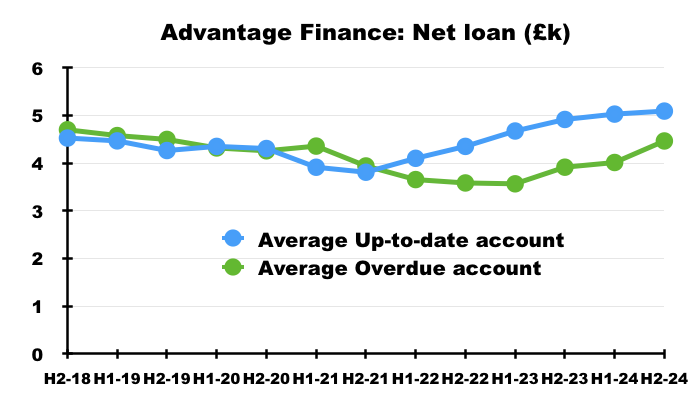

- The slower rate of repayments during H2 left only 74% of Advantage’s loans up-to-date at the end of this FY:

- The 74% compares to 79% for the preceding H1 and 76% for the comparable FY:

- However, the up-to-date 74% exceeds the 61% (H1 2021), 62% (FY 2021), 69% (H1 2022) and 73% (FY 2022) recorded during the pandemic.

- During the pandemic, approximately 20,000 Advantage customers enjoyed FCA-authorised payment holidays that lasted up to six months and a cut-off date of 31 July 2021.

- SUS deemed the payment-holiday customers as ‘overdue’ even if normal repayments were resumed.

- The FCA may arguably be authorising payment holidays once again — although this time the cessation of payments may last longer than six months and no cut-off date has been set (see Regulation: Borrowers in Financial Difficulty).

- Note that August’s trading update revealed just 69% of Advantage’s loans were up to date (see June and August trading updates).

- For perspective, the up-to-date proportion topped 80% during FYs 2017 and 2018, and reached a super 91% during FY 2016:

- This FY did not disclose any pandemic payment-holiday statistics.

- But 2,285 payment-holiday customers did close their accounts (one way or another) during the preceding H1, which suggested payment-holiday customers may have all vanished from the loan book by the end of FY 2025:

- The average net loan outstanding (i.e. after impairments) at overdue accounts continues to creep higher to match the average at up-to-date accounts:

Advantage Finance: impairments

- SUS’s loan impairments are classified as:

- Stage 1, which reflects expected write-offs from up-to-date customers;

- Stage 2, which reflects expected write-offs from customers not in arrears but who are deemed “vulnerable” by factors such as “health, life events, resilience or capability” that create a greater credit risk, and;

- Stage 3, which reflects expected write-offs from customers one month or more in arrears.

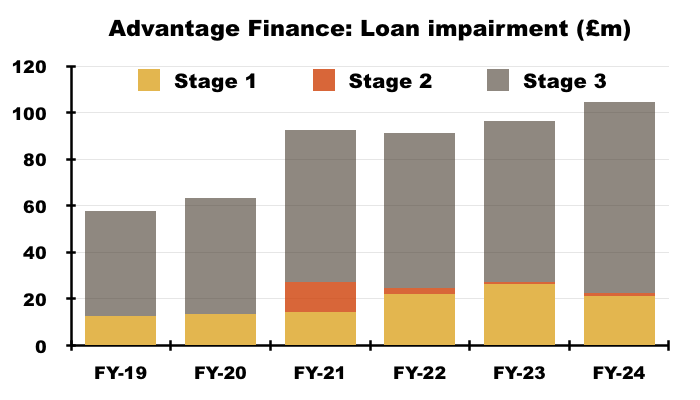

- Advantage’s total impairment provision increased by £9m to £105m during this FY:

- Encouragingly perhaps, this FY’s split between Stage 1 (20%) and Stage 3 (78%) impairments were similar to the Stage 1 (21-22%) and Stage 3 (78-79%) splits witnessed for pre-pandemic FYs 2019 and 2020.

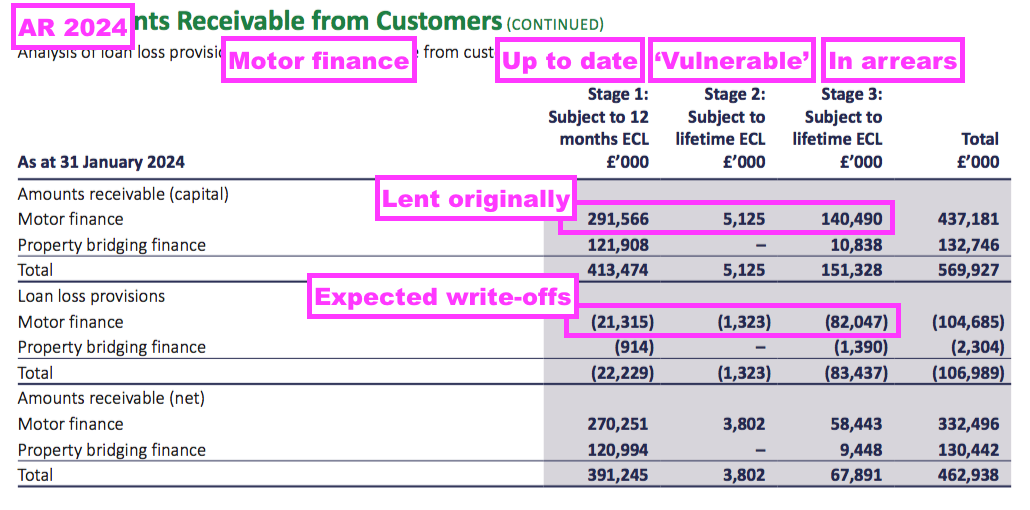

- Of the £292m lent to up-to-date Stage 1 borrowers, SUS reckoned £21m or 7% will not be repaid:

- Of the £140m lent to in-arrears Stage 3 borrowers, SUS reckoned £82m or 58% will not be repaid.

- The 7% and 58% broadly match the 9% and 60% proportions reported at the preceding FY.

- Lending a total £437m and impairing £105m means Advantage expects to receive 76p of capital for every £1 currently loaned.

- Charging the aforementioned 33.87% APR is therefore required to recoup the 24p of capital not repaid as well as earn an adequate return on the overall £1 lent.

- The total £105m impairment provision was equivalent to 24% of the overall £437m lent originally and still outstanding:

- The proportion for the preceding FY was also 24%, and for FYs 2021 and 2022 were 27% and 26% respectively.

- For pre-pandemic FYs 2019 and 2020, though, Advantage’s impairments ran at 18% of total money lent. But Advantage’s impairments did surpass 25% during FYs 2011, 2012 and 2013.

- I fear Advantage’s adverse collection trend (see Advantage Finance: collections and estimated repayments) is likely to inflate that 24% proportion.

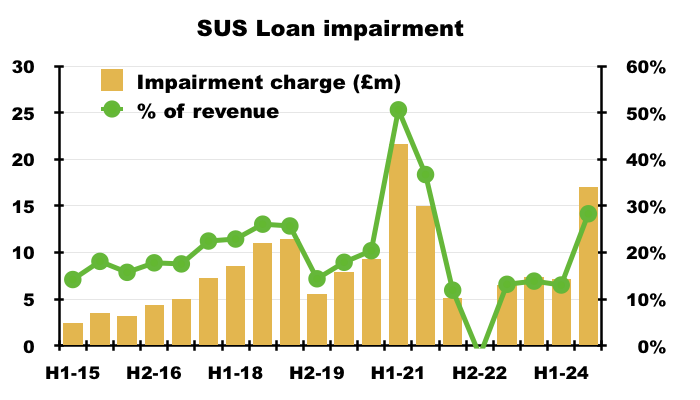

- Indeed, Advantage’s impairment charge during this H2 was £16m versus only £7m for the preceding H1:

- Advantage’s gross loan book (i.e. before impairments) meanwhile increased by £28m during H2.

- If continued, impairing an extra £16m after lending an additional £28m will certainly lead to a gross loan book with much greater expected write-offs.

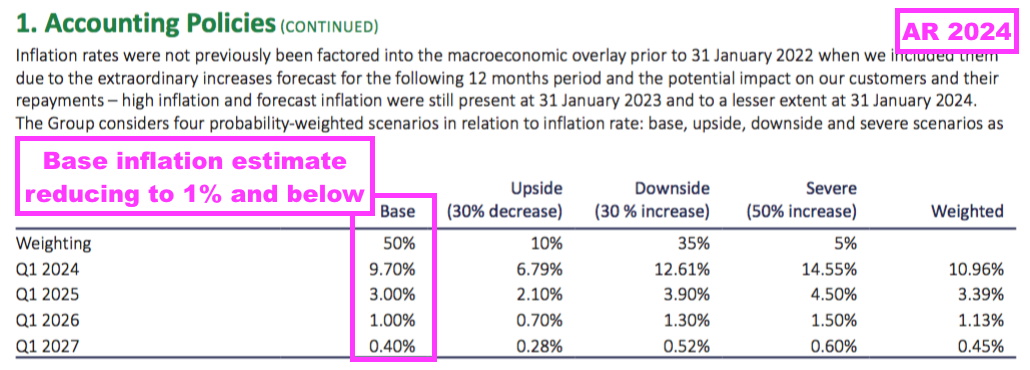

- This FY repeated the “macroeconomic overlays” that are employed within the impairment calculations:

“The macroeconomic overlay assessments for 31 January 2024 reflect that further to considering such external macroeconomic forecast data, management have judged that there is currently a more heightened risk of an adverse economic environment for our customers. To factor in such uncertainties, management has included an overlay for certain groups of assets to reflect this macroeconomic outlook, based on estimated unemployment and inflation levels in future periods.”

- Once again SUS said there was “currently a more heightened risk of an adverse economic environment”.

- Part of SUS’s impairment estimates are based on assuming inflation falls to 1% during early 2026:

- SUS is not expecting used-car prices to decline during FY 2025:

“An overlay for used vehicle prices was also included at 31 January 2023 as we assumed at that point that these prices would fall by 13.5% after a large increase in the previous 12 months. As at 31 January 2024, we have not included an overlay for used vehicle prices as we assume that used vehicle prices will now remain stable after the anticipated large decrease in the previous 12 months.”

- Note that SUS will register an extra £3m impairment charge if used-car prices decline by 5%:

“If used car prices were assumed to fall by 5% instead, then this would result in an increase in loan loss provisions of £2,967,534.”

- The overlay assessments also include a £69m “trade value” estimate of vehicles in Stage 3 arrears:

“As stated in note 1.13 above, valuing these used vehicles secured under our hire purchase agreements is uncertain as the condition and mileage of the used vehicle are unknown. We estimate the trade value of collateral held at 31.1.24 for motor finance loans currently in stage 3 was £68.8m (2023: £64.5m) – these estimated values are stated before taking into account recovery and disposal costs.

- The £58m Stage 3 net loan book was less than that £69m “trade value”, suggesting SUS could (if need be) repossess the Stage 3 vehicles (for £69m) and perhaps recoup the their Stage 3 loan-book value (of £58m) after costs.

Aspen Bridging

- Established at the start of FY 2018, Aspen offers property-bridging loans for small/individual property developers.

- This FY outlined the division’s attractions to borrowers:

“Mainstream” banks, including the newer “challengers”, continue to lack the speed, flexibility and appetite to furnish the smaller, short-term loans in which Aspen specialises. Recent consolidation and instability in the challenger banking sector is evidence of this and again shows that, technology, speed and a quality bespoke service – as well as price – are what give smaller entrants like Aspen their competitive edge.”

- The subsidiary’s profitability is supported by conservative lending to low-risk “experienced” customers:

“Aspen values its security properties very conservatively and keeps gross LTVs to an average 70% and the business now only considers experienced borrowers from the top three quality bands.“

- The conservative lending is underlined by Aspen visiting every property…

“Every property upon which Aspen lends for security is personally visited by a member of the team.”

- …which this FY claimed was unique within the industry:

“Increased margins, steady LTV’s and sensible valuations approach with our USP of visiting all projects.”

- This FY revealed “most” of Aspen’s loans were secured on properties within south east England, and these case studies give a flavour of the transactions involved:

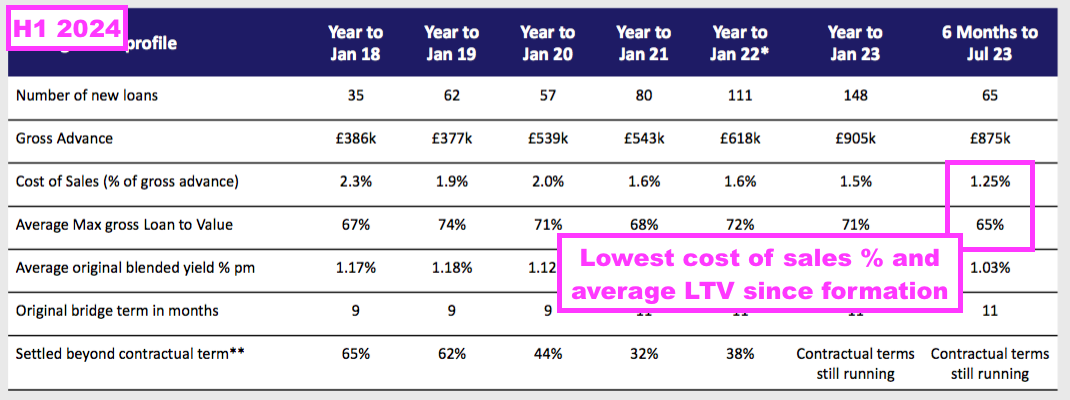

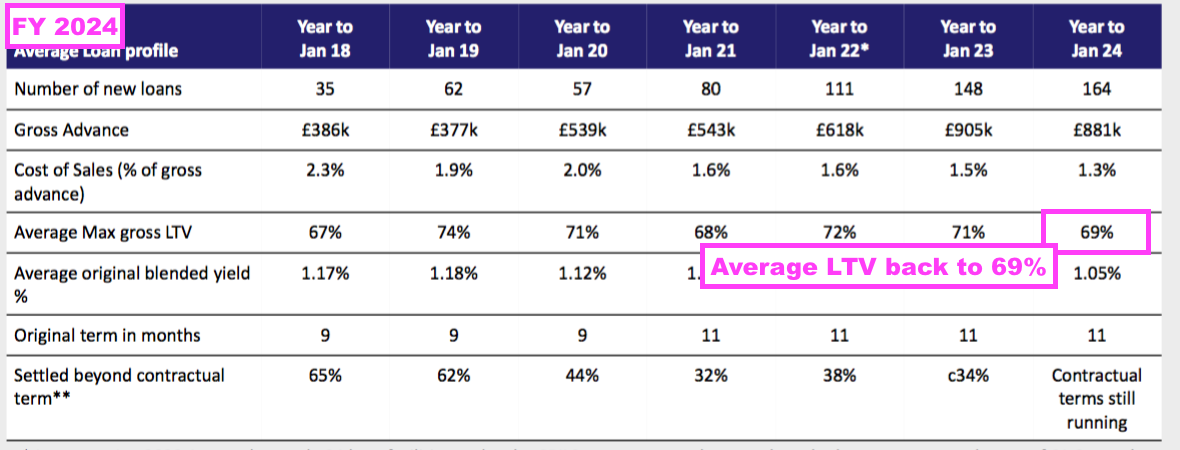

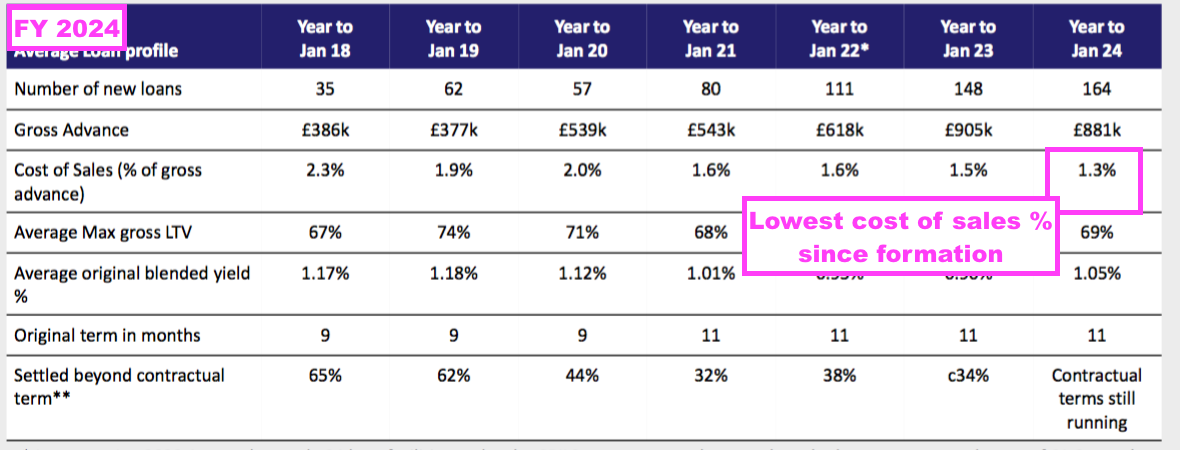

- Lending appears to have loosened during H2. The preceding H1 showed an average 65% gross loan-to-value, the lowest since Aspen’s formation…

- …but this FY showed the average gross loan-to-value rising to a more normal 69%:

- Aspen’s rate card says developers borrowing against residential properties pay a flat monthly interest rate of 0.94% on a 75% loan-to-value arrangement.

- For perspective, my FY 2022 review had highlighted 0.69% monthly interest on a 70% loan-to-value arrangement.

- This FY talked of “excellent” progress that may continue into FY 2025 despite a “subdued” housing market:

“Aspen’s has continued to make excellent but careful progress in a fluctuating and still subdued housing market, affected by continued high interest rates and persistently high mortgage costs as a proportion of average incomes. Both are expected to improve in 2024.

…

[D]emand from good borrowers remains high and hence Aspen plans a slightly accelerated rate of growth this year“

- June and August’s trading updates confirmed positive progress was achieved during H1 2025 (see June and August trading updates).

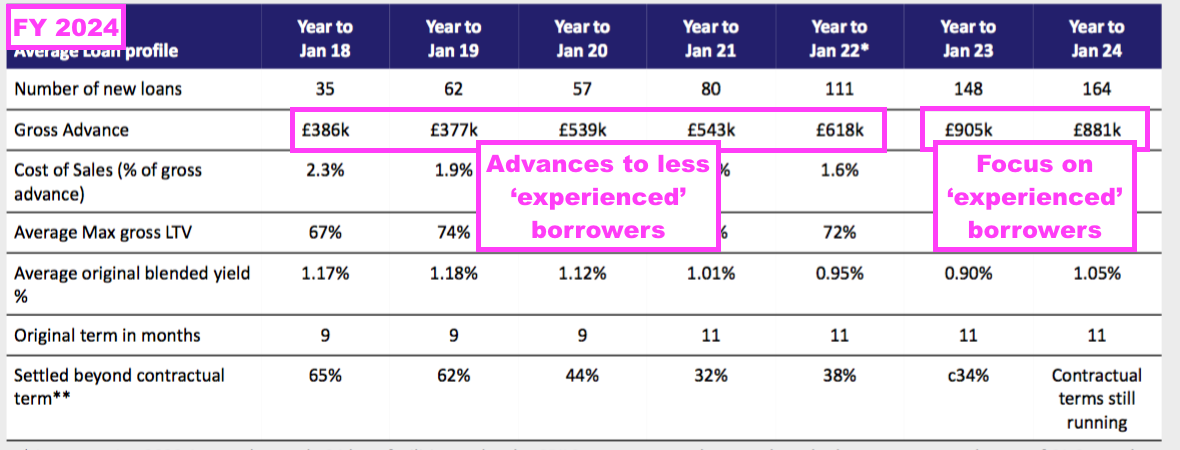

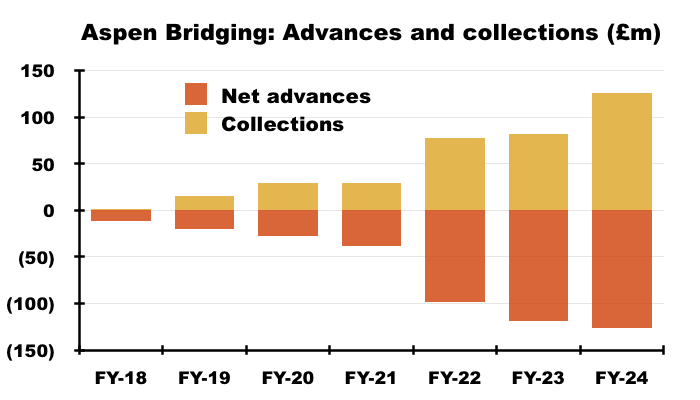

- 165 customers were advanced an average £881k for 11 months during this FY.

- The £881k average reflected the “experienced” borrowers and remains much higher than the average £618k or less (excluding CBILS) advanced to perhaps less experienced borrowers up to FY 2022:

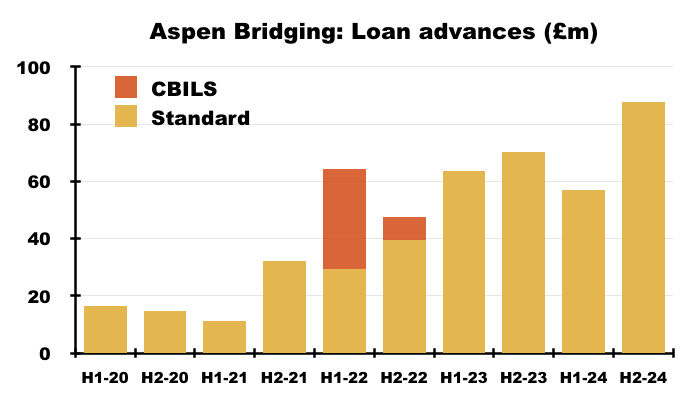

- 165 clients receiving an average £881k gave a total £145m gross advance:

- Lending was biased towards H2, with 99 borrowers taking on £88m versus H1’s 65 borrowers taking on £57m.

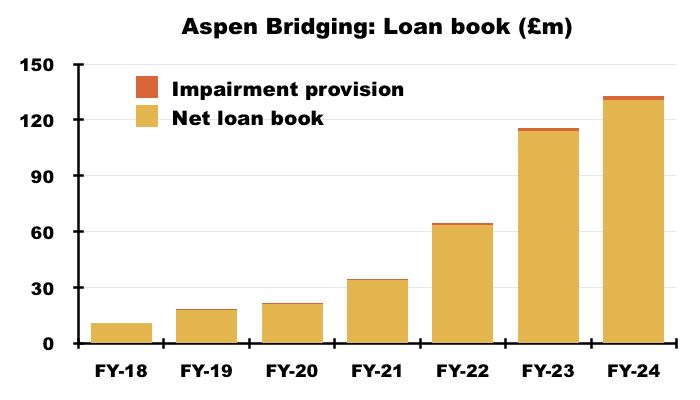

- The total FY £145m advance allowed Aspen’s net loan book to expand by 15% to £130m:

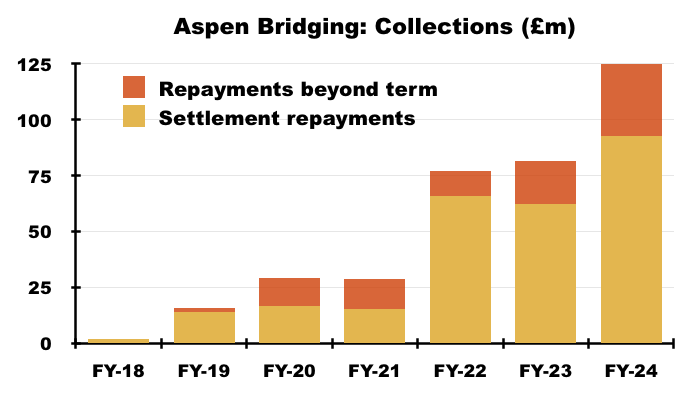

- Aspen’s FY net advances (i.e. after retentions) of £126m equalled collections of £126m:

- Boosting this FY’s collections were ‘repayments beyond term’, which surged 77% to £34m:

- Greater ‘repayments beyond term’ suggest not every Aspen borrower completed their development on time. Such repayments have bolstered standard repayments by a total 34% since Aspen’s formation:

- Of the aggregate 681 loans advanced by Aspen since the subsidiary’s formation, 518 have been repaid and only 15 of the remaining 163 are “in default” — versus 12 of 141 for the comparable FY.

- This FY noted four properties were “in repossession” at the year end, for which “recovery is in progress and adequate provision has been made“. The comparable FY reported only one repossession.

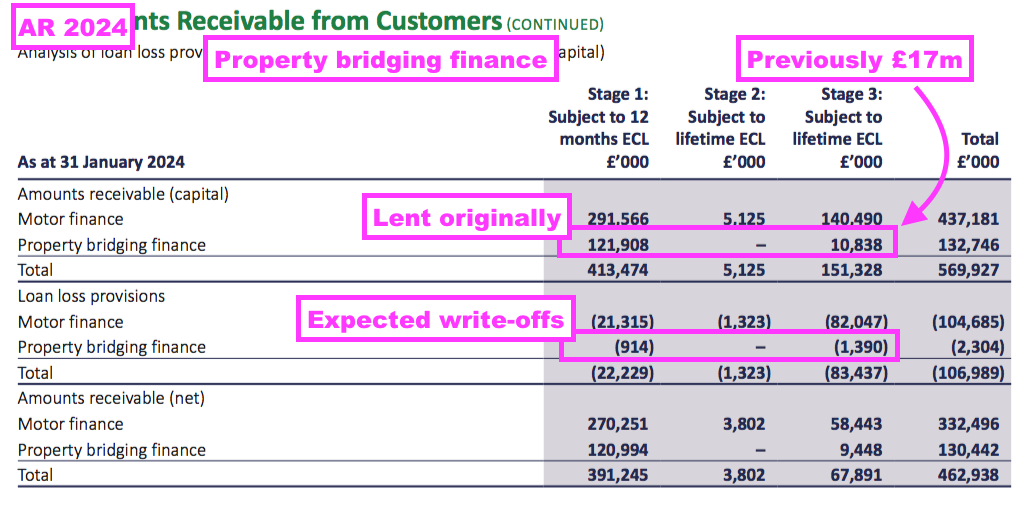

- The 15 defaulters are categorised as Stage 3 borrowers, and although the £11m Stage 3 property loans are greater than the £7m reported at the comparable FY…

- …they are encouragingly less than the £17m reported at the preceding H1.

- This FY implied the £11m lent originally on these Stage 3 properties would be recouped if the properties were sold for their estimated £15m market value:

“The estimated value of first charge secured properties held under our bridging loan facility agreements at 31.1.24 is £199.6m (2023: £184.7m). This includes £15.3m estimated value of properties secured which is held for loan agreements currently in Stage 3 (2023: £13.4m).”

- The same text revealed the market value of all Aspen’s properties was £200m, which equates to a 65% loan-to-value given Aspen’s net loan book finished this FY at £130m.

- Aspen’s enlarged loan book pushed FY revenue 34% higher to £17m:

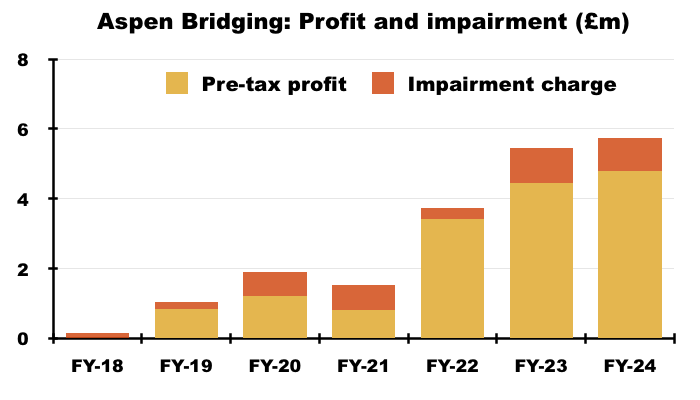

- Aspen’s impairment provision increased by 48% during this FY to £2.3m, but remains tiny versus the £133m gross loan book:

- Cost of sales (mostly broker fees) at a reported 1.3% of the average advance for this FY was the lowest since Aspen’s formation:

- Aspen’s cost of sales were a welcome 12% of revenue (£2.1m/£17m) versus 14-17% between FYs 2020 and 2023.

- The low cost of sales and low impairments allowed Aspen’s FY profit to reach £4.8m:

- Although Aspen’s loan book represented 28% of SUS’s entire lending (after impairment provisions)…

- …Aspen’s profit represented 14% of SUS’s entire profit:

- The implication therefore is Aspen currently generates much lower returns on its loans than Advantage, although the use of debt within the subsidiaries must also be considered (see Financials: returns on assets and equity).

- This FY anticipated Aspen would enjoy “further steady and sustainable growth” during FY 2025, and “great things” further out:

“Since its launch in 2017, Aspen has more than met S&U’s expectations, and great things are expected of it in the future.”

- Aspen’s blog reveals the aim of taking cumulative lending from £500m to £1 billion “in the next couple of years“:

[Aspen website] “Jack Coombs, Managing Director at Aspen Bridging, said: “The business has successfully grown these last few years which resulted in us recently surpassing the £500m lending landmark from when the business was founded in 2017.

As we look upwards to £1bn worth of lending, which we are looking to realise in the next couple of years, we have to invest in the business and our core teams. These promotions are all well-deserved and we are excited about the positive contribution they will make to the business going forwards.” “

Boardroom

- SUS is run by the Coombs family, and lead executives Anthony and Graham Coombs are grandsons of founder Clifford Coombs and have worked at the business since the mid-1970s:

- The Coombs family controls at least 44% of the shares and it’s this owner-managed boardroom that has delivered the illustrious dividend since 1987.

- Various appointments do suggest the Coombs family prefers Aspen to Advantage.

- Jack Coombs for instance is a main SUS board executive and an Aspen director. At 37 years old, Jack Coombs may well become the lead SUS/Coombs director when his 71-year-old cousins Anthony and Graham decide to retire.

- Richard Coombs — the son of Graham Coombs — joined Aspen last year.

- I note SUS’s head office and Aspen are both located in Solihull while Advantage is based in Grimsby.

- Aspen may have much greater returns on equity, too (see Financials: returns on assets and equity).

- From what I can tell, Anthony and Graham Coombs act as ‘capital allocators’ within S&U.

- Dividends are paid by Advantage and Aspen to the parent company, whereby Anthony and Graham can then decide to:

- Redeploy the money back into Advantage and/or Aspen;

- Return the money to shareholders as a dividend, or;

- Reduce debt.

- Despite the shares trading below book value (see Valuation), management’s FY webinar confirmed buybacks are not being considered:

“We have no plans to buy the preference shares back currently and also have no plans to seek authority to buy back our main ordinary shares which would be likely to reduce further the already limited free float. We have previously deployed capital to grow our businesses where there are sensible potential forecast returns and pay regular dividends and that is still our current plan.”

- Management’s FY webinar also dismissed ideas of selling Advantage to focus on Aspen:

“We have no plans to sell Advantage. We believe it is an excellent business which can emerge strongly from the current uncertainties caused mainly by regulatory activity in the sector.”

- Advantage does seem to be an ‘external’ investment for SUS.

- This Advantage blog post seemingly refers to the division’s founders approaching SUS for start-up funds:

[Advantage website] “Three founding members, with one shared goal: putting customers first while providing an opportunity to purchase and own their own motor vehicle without the aggressive sales approach. With this goal in mind, there was a clear and obvious investment choice – S&U. S&U has always offered and looked for a way to support the lesser served section of society, so when the three founding members shared the goal, the Coombs family knew they were the right people to lead them into a new area of finance for the group.”

- This FY welcomed Advantage’s new boss Karl Werner…

“[SUS has] great pleasure in welcoming Karl Werner as the new Chief Executive of Advantage. Karl has impressed enormously in the few months he has been with us, and his long experience of the finance industry and its regulation, particularly at MotoNovo and Aldermore Bank will make him a distinguished successor to Graham Wheeler.”

- …who became Advantage’s boss the day after this FY ended and therefore has yet to make a real impact on the division’s progress.

- Mr Werner’s first task at Advantage is to oversee the FCA’s new Borrowers in Financial Difficulty rules (see Regulation: Borrowers in Financial Difficulty) and the FCA’s new Consumer Duty regime (see Regulation: Consumer Duty).

- Mr Werner has encouragingly worked within a group much larger than SUS. His former employer, MotoNovo Finance, is part of Aldermore Bank, which is part of FirstRand Group. MotoNovo’s FY 2023 accounts showed customer lending of more than £4b.

- Although Mr Werner has not joined SUS’s main board, his predecessor, Graham Wheeler, only joined SUS’s main board a year after becoming Advantage’s boss.

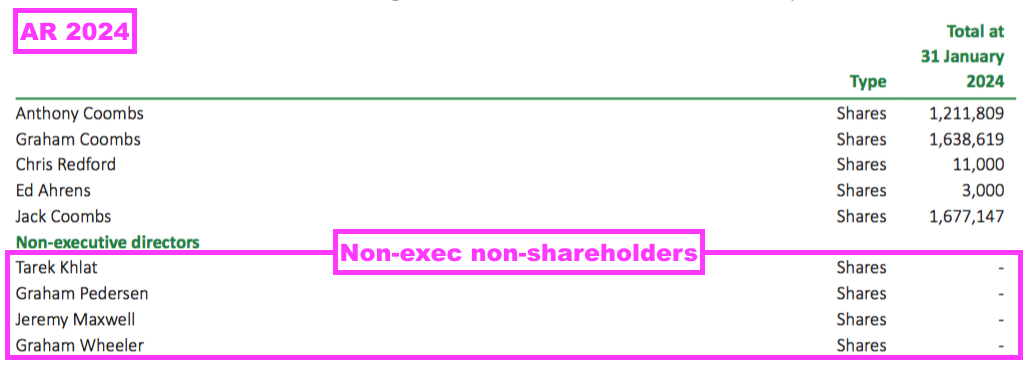

- Mr Wheeler is now a non-executive director, and matches the other non-execs with a zero shareholding:

Financials: cash flow and debt

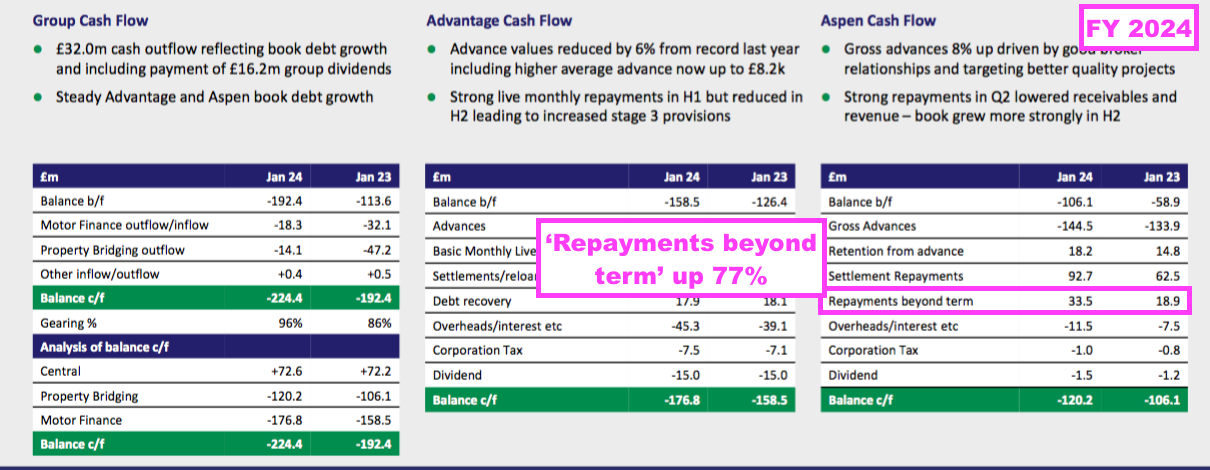

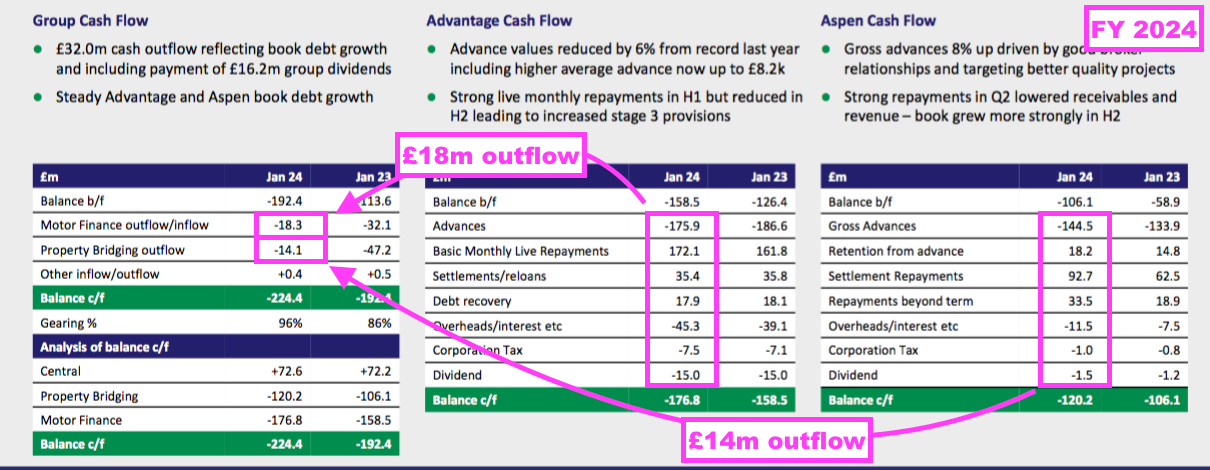

- This FY witnessed Advantage report an £18m cash outflow after lending £176m, collecting £225m, expensing £53m and paying £15m as dividends to the parent company:

- Aspen meanwhile reported an FY £14m cash outflow after lending a net £126m, collecting £126m, expensing £13m and paying £2m as dividends to the parent company.

- Advantage’s FY outflow surpassed Aspen’s FY outflow for the first time since FY 2020:

- But Aspen has absorbed the bulk of SUS’s funding over time. During the last five years for example, SUS has taken on additional debt of £116m, of which Advantage received approximately £12m while Aspen received approximately £104m (see Financials: returns on assets and equity).

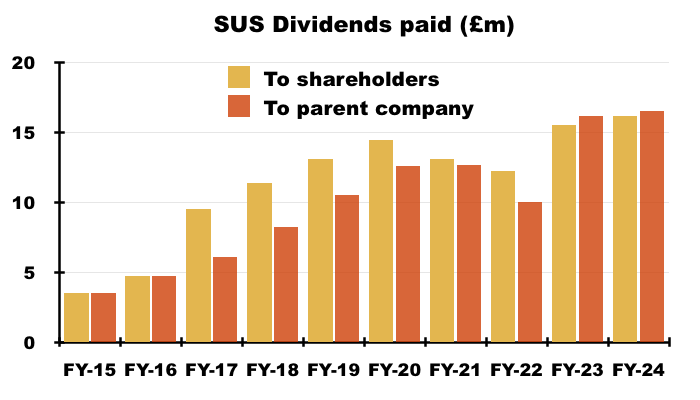

- The dividends paid by Advantage and Aspen to the parent company do not always tally exactly with the dividends paid to SUS shareholders:

- During this FY and the comparable FY, aggregate dividends paid by Advantage and Aspen were £1m greater than the aggregate paid by SUS to shareholders:

- Mind you, between FYs 2017 and 2022, SUS paid shareholders an aggregate £14m more than was paid by Advantage and Aspen to the parent company.

- The extra £32m required during this FY to fund operations/dividends at Advantage (£18m) and Aspen (£14m) was covered by additional borrowings.

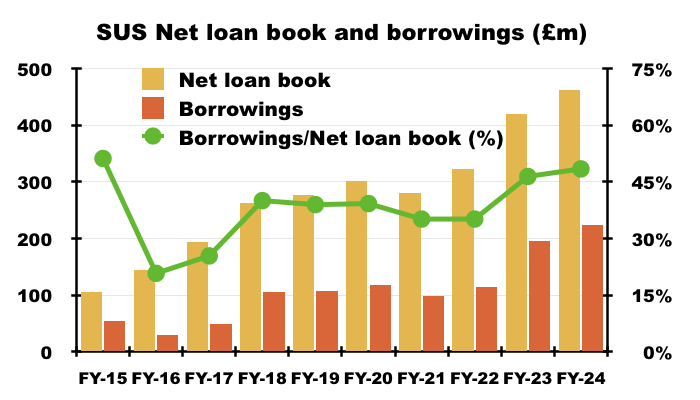

- Net debt increased by £32m to £224m and remains under control; borrowings are more than twice covered by the £463m lent to customers (after impairments):

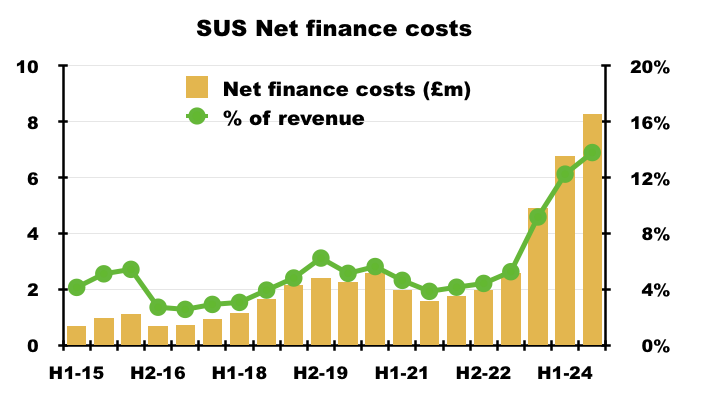

- Bank interest paid during this FY was £15m, implying SUS’s average £210m FY borrowings incurred interest at approximately 7.1%.

- H2 interest was approximately £8m, implying SUS’s average £205m H2 borrowings incurred interest at 8.0%.

- 8.0% compares to 4.8% for the comparable FY and 3.4% for FY 2022.

- This FY confirmed an 8% borrowing rate:

“The average effective interest rate on financial assets of the Group at 31 January 2024 was estimated to be 26% (2023: 25%). The average effective interest rate of financial liabilities of the Group at 31 January 2024 was estimated to be 8% (2023: 6%).“

- This FY also admitted “interest rates remained higher than anticipated”.

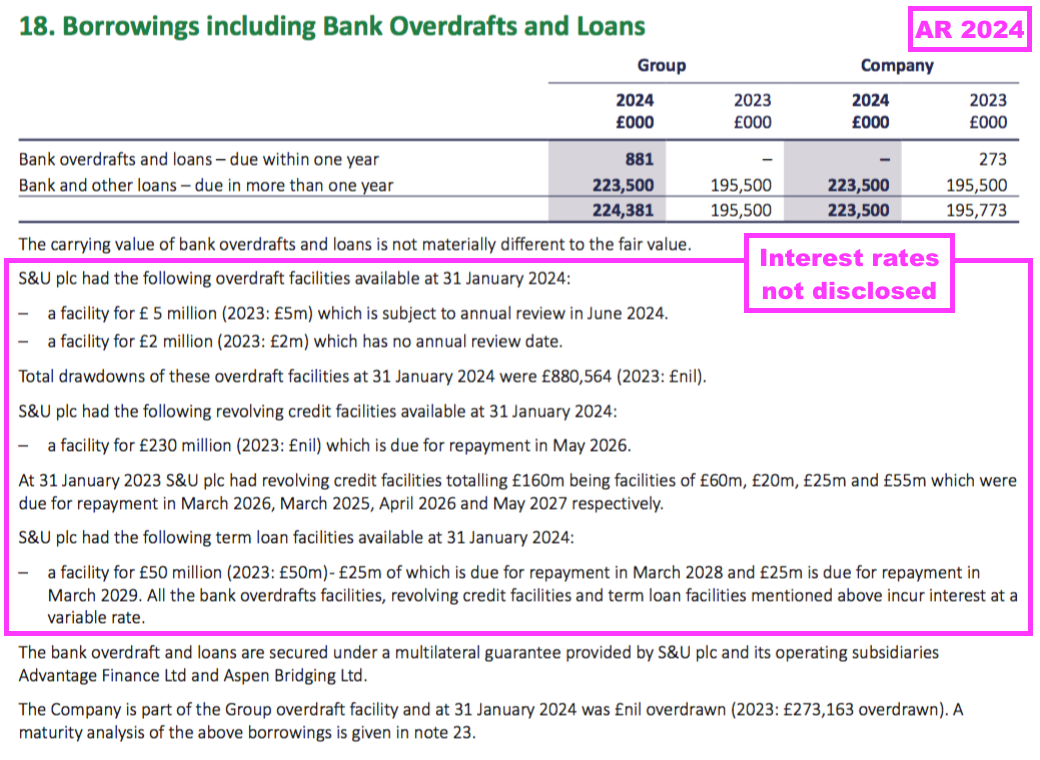

- SUS still does not disclose the exact rates payable on its debt facilities, which is very poor form for a main-market company:

- Management’s webinar for the comparable FY disclosed:

- Borrowing costs were “just less than 3%” above SONIA, and;

- All borrowings were variable.

- SONIA is currently 4.95%, which means SUS will still be paying 8% on its debt.

- 8% on debt of £224m equates to annual bank interest of £18m — £3m more than this FY’s £15m.

- SUS could increase its borrowings by another £56m, given the loan facilities supplied by the group’s “excellent, loyal and constructive funding partners” amount to £280m (excluding a further £7m overdraft facility).

- Following this FY, August’s trading update revealed debt had increased by £16m to £240m (see June and August trading updates).

- This FY said group gearing remained “conservative, especially for a lending organisation” and management’s FY webinar reiterated several times the board was “comfortable” with the level of borrowings.

- Still, higher interest rates will diminish the returns earned on the money SUS has already lent, particularly at Advantage, where loan terms last for 54 months (see Advantage Finance: loan sizes and rates).

- Interest payable by all customers (Advantage and Aspen) is fixed throughout their agreements, meaning SUS’s variable-rate debt leads to a greater margin when rates go down but a lower margin when rates go up.

Financials: returns on assets and equity

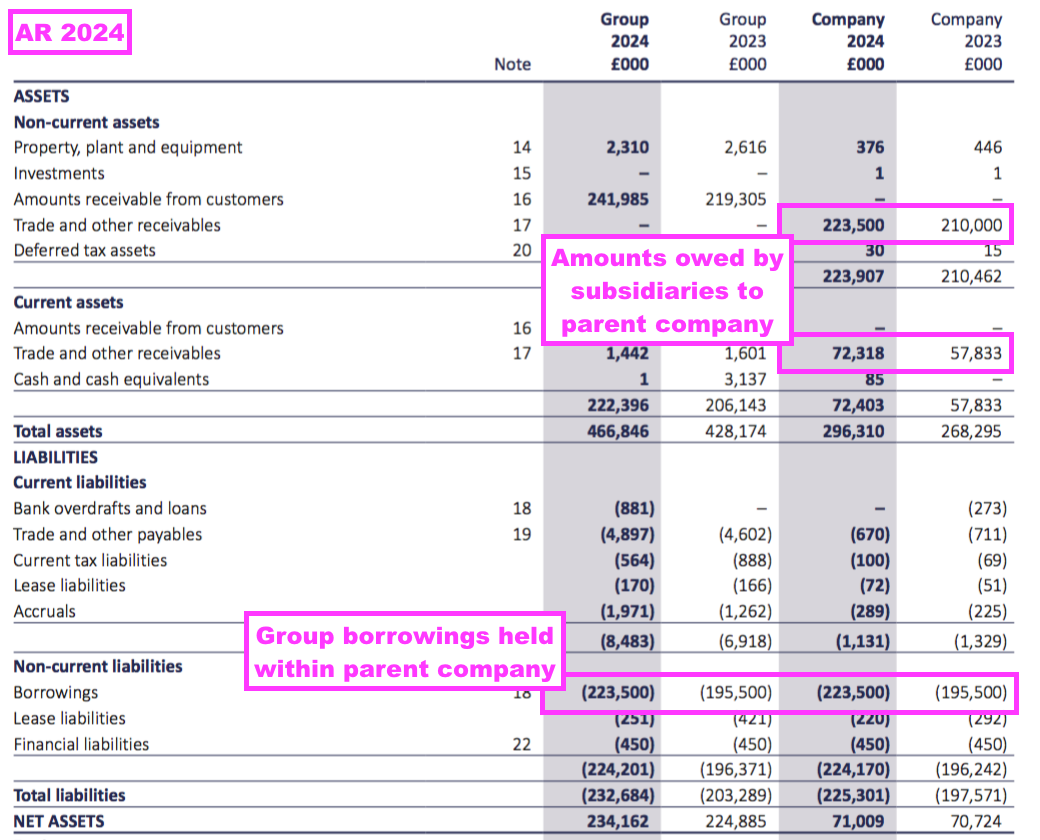

- SUS’s debt is held within the parent company and then ‘re-lent’ to Advantage and Aspen as necessary:

- This FY implied Advantage and Aspen owed the parent company a further £72m, which alongside the £224m bank debt effectively means the subsidiaries owe a combined £296m.

- The debts owed to the parent company — plus minor other subsidiary liabilities — enhances divisional returns on equity very significantly.

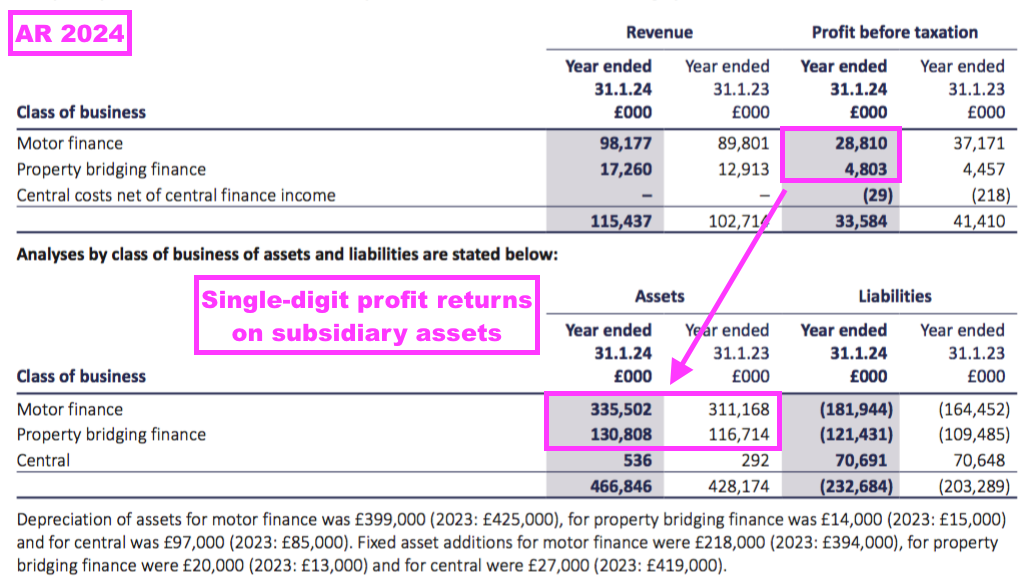

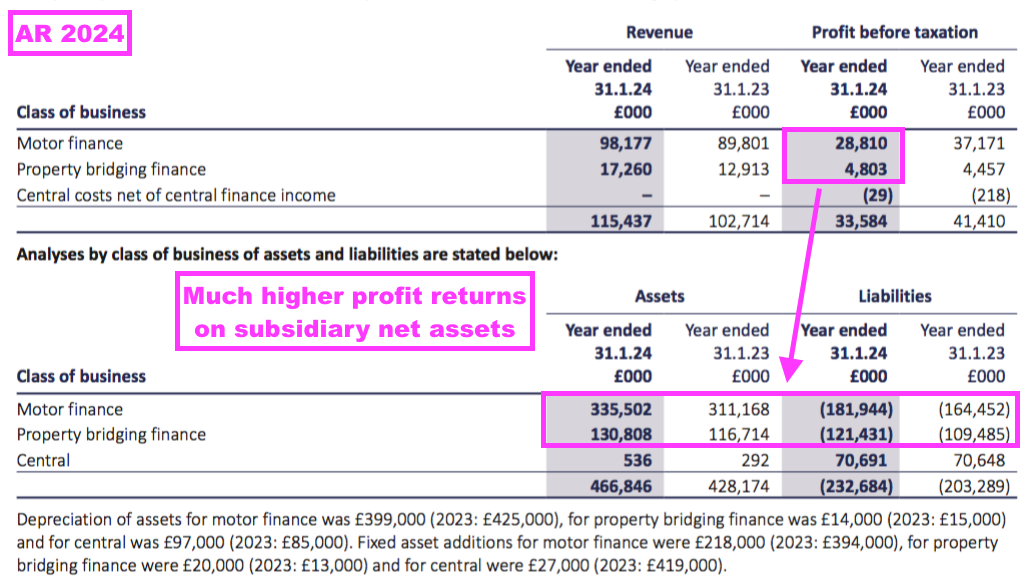

- For example, a simple pre-tax return on average assets (i.e. customer loans) for this FY gives:

- £29m/£323m = 9% for Advantage, and

- £5m/£123m = 4% for Aspen:

- But a simple pre-tax return on average equity (i.e. customer loans less liabilities) for this FY gives:

- £29m/£150m = 19% for Advantage, and

- £5m/£8m = 58%(!) for Aspen:

- For comparison, a simple pre-tax return on average equity for SUS gives £34m/£448m = 15%.

- With pre-tax returns on average equity surpassing that 15% for both divisions, Advantage and Aspen appear to operate successfully with gearing greater than the group accounts suggest.

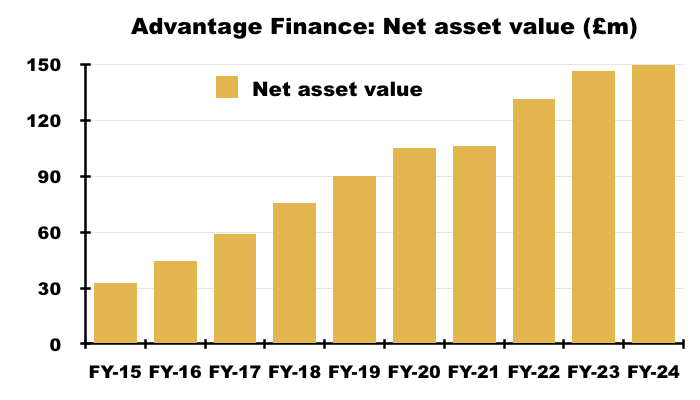

- Indeed, Companies House shows Advantage’s net asset value advancing from £90m to £154m during the last five years…

- …with cumulative dividends paid to the parent company of £65m during the same time:

- Advantage creating an additional £129m (i.e. £64m extra NAV and dividends of £65m) over five years from a starting equity base of £90m is extremely impressive, especially as the subsidiary’s expansion during those five years required extra debt funding of only £12m (see Financials: cash flow and debt).

- Companies House meanwhile shows Aspen’s net asset value increasing from £0.4m to £9.4m during the last five years, with cumulative dividends paid to the parent company of £2.7m.

- Aspen’s £12.1m of extra net asset value and dividends (£9.4m+£2.7m) was created through additional debt funding of £104m (see Financials: cash flow and debt).

- Aspen’s return on capital for that five-year period is therefore arguably £12.1m/£104m = 12%.

- But Aspen’s return on equity is off the scale — a starting £0.4m equity base generated an additional £12.1m of extra net asset value and dividends over five years without any extra equity funding.

- Advantage ought to enjoy lucrative ROCEs when customers repay their loans in full and on time.

- Charging a flat 16.9% annual interest on a £8.2k loan over 54 months less cost of sales of £961 generates approximately £5.2k.

- Earning £5.2k from an £8.2k investment over 54 months equates to a 64% return or approximately 14% a year.

- Note that Advantage customers repay a mix of loan capital and interest during the terms of their loans.

- That c14% return could therefore be approximately 28% assuming the loan capital is repaid equally throughout the term.

- The same calculations for the ten years to FY 2023 are within a consistent — and appealing — 27% to 31% range.

- Of course not every Advantage loan is repaid in full and on time.

- 24% of the £437m Advantage lent originally (and still outstanding) has been impaired as a bad debt (see Advantage Finance: impairments).

- Reducing that 27% return by 24% gives a 22% return, which remains very healthy and still leaves good room for a greater proportion of non- or part-paying borrowers.

- Aspen does not seem to enjoy as lucrative ROCEs as Advantage when customers repay their loans in full and on time.

- Charging a flat 1.05% monthly interest on a £881k loan over 11 months (£102k) less cost of sales of 1.3% (£11k) generates approximately £91k.

- Earning £91k from an £881k investment over 11 months equates to only a 10% return or approximately 11% annualised.

- However, the aforementioned minimal impairments for Aspen’s loans (see Aspen Bridging) indicate the division’s borrowers are much more likely to repay their loans in full and on time.

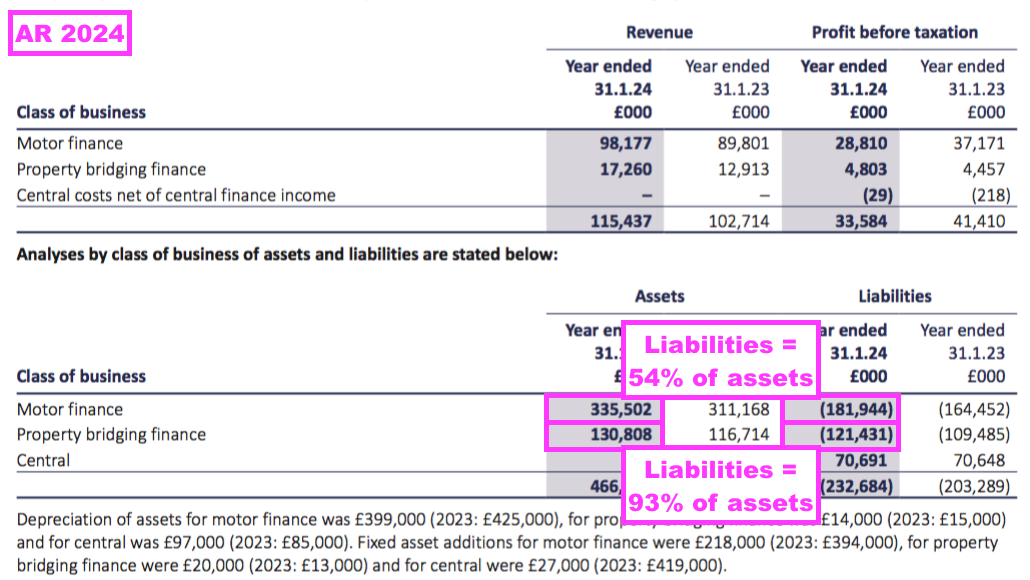

- The minimal impairments allows Aspen to operate with much higher levels of gearing.

- Indeed, Aspen’s liabilities represent 93% of its assets versus only 54% at Advantage:

- As noted above, Aspen’s net asset value of only £8m allowed the division to earn a pre-tax return on average equity of 58% (£5m/£8m) during this FY.

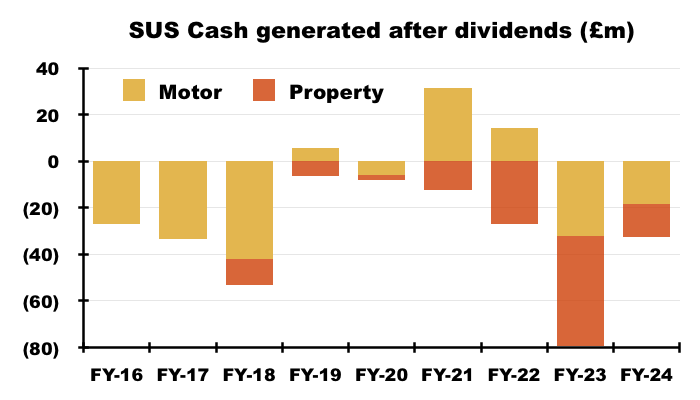

- From a group perspective, between FY 2019 and this FY, SUS has created additional net asset value of £69m and paid cumulative dividends of £72m. Creating an additional £141m for shareholders from a starting equity base of £165m is respectable, and equivalent to a compound 13% total NAV/dividend return:

Financials: employees

- This FY’s dividend was reduced in part due to greater staff salaries (see Revenue, profit, net asset value and dividend):

“Whilst recognising its primary responsibilities to its shareholders,S&U has always sought to balance the interests of all its stakeholders. This year’s fall in profit together with our wish to protect our loyal staff from recent increases in the cost of living has made this a particularly delicate one this year.

Thus, except for senior directors, average salaries this year have matched the rate of inflation, with more for living wage earners. Higher base interest rates have cost the Group an additional £8m this year, and our incoherent Government have raised the rate of corporation tax by nearly a third.

Taking all this into account, subject to the approval of shareholders at our AGM on 6 June, the board proposes a final dividend of 50p per ordinary share (2023: 60p).”

- This FY disclosed the wider workforce enjoyed a 9% pay rise, with a 5.5% pay rise agreed for FY 2025:

“For the year ended 31 January 2024 salary increases were in the range 1.3% to 3.3% except where exceptional circumstances merited a higher increase. This was below the average increases given to the wider workforce which averaged 9.0% in a difficult inflationary cost of living environment for our employees. The Remuneration Committee has now agreed salary increases for the year ended 31 January 2025 in the range 1.7% to 3.6% except where exceptional circumstances merited a higher increase, as noted below. This is below the average increases given to the wider workforce which averaged 5.5% in light of the continued difficult inflationary cost of living environment for our employees.”

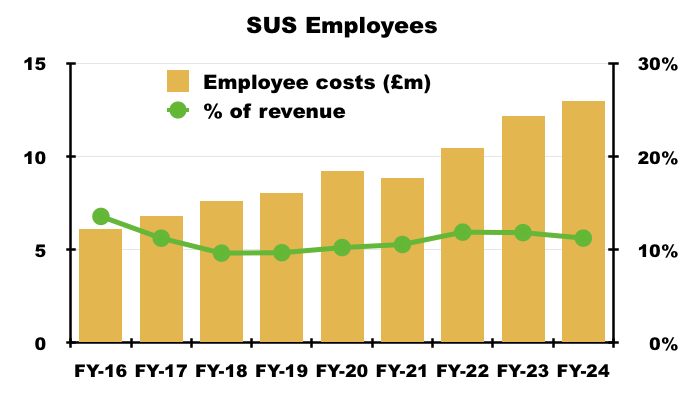

- Total employee costs increased by 7% to £13m and, despite the 9% workforce pay rise, continues to absorb 11% of revenue:

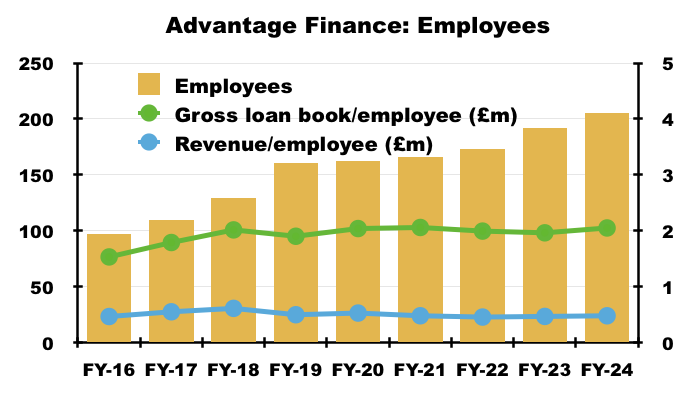

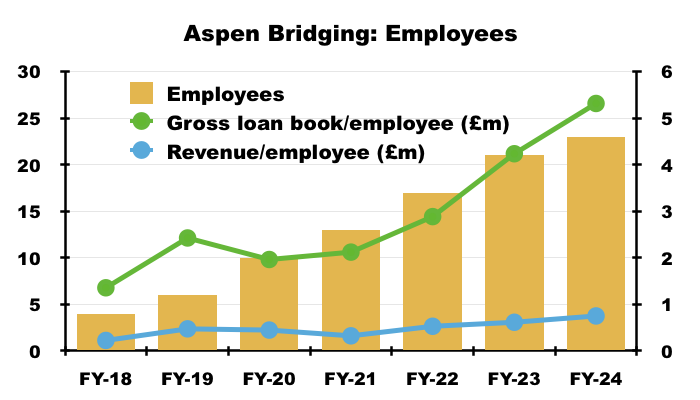

- Advantage and Aspen exhibit differing employee productivity profiles.

- Advantage’s employee productivity has not shown obvious improvements during recent FYs:

- Each Advantage employee continues to handle motor loans (before impairments) of approximately £2m and generate revenue of approximately £480k.

- Aspen employees meanwhile each handle property loans (before impairments) of approximately £5m and generate revenue of £750k:

- Karl Werner, Advantage’s new boss, suggested during management’s FY webinar the efficiency of the group could be improved:

“While the the cost of operating in this modern market never seems to reduce too much there is I think an awful lot of opportunities to improve efficiencies across the firm going forward“

- This FY’s auditor’s report even noted the presence of (now automated) manual calculations for dealer commissions:

“The calculation of dealer commissions, which was previously a manual process, was automated during that year and the transition to automatic calculation simplified the audit procedures required to gain sufficient appropriate evidence on this matter so that it is no longer considered a key audit matter in the current year’s audit.”

Regulation: Borrowers in Financial Difficulty

- This FY devoted extensive text to the enhanced regulation of used-car finance (see Regulation: SUS response).

- The enhanced regulation was prompted initially by the FCA’s Tailored Support Guidance (TSG), which addressed how lenders should handle borrowers suffering payment difficulties caused by the pandemic.

- The FCA’s Borrowers in Financial Difficulty (BiFD) project then assessed how lenders had met the TSG.

- An FCA follow-up to the BiFD project then proposed various “forbearance” changes as “consumers…faced increased financial challenges due to the rising cost of living“.

- The FCA’s proposals (Annex D) were finalised during April and will come into force within the Consumer Credit sourcebook on 04 November 2024.

- From what I can tell, the general implications for Advantage (and other motor-loan lenders) are:

- More information must now be obtained from customers before lending;

- More customers may now be deemed to suffer from payment difficulties;

- Customers suffering payment difficulties may now be given more leeway to repay their loans, and;

- Vehicle repossessions may now become more difficult to undertake.

- The FCA’s policy statement widened the scope of customers who could now seek “forbearance” options.

- In particular, FCA rules concerning “particularly vulnerable” customers now apply to just “vulnerable” customers, while rules concerning customers “in arrears” now apply to customers “in or approaching arrears“.

- The new FCA text below suggests a customer “approaching arrears” may become known to Advantage sooner than before:

[FCA PS24/2] “A firm should regard a customer as approaching arrears when the customer indicates to the firm that they are at risk of not meeting one or more repayments when they fall due.”

- Forbearance measures now include accepting “no payments“…

[FCA PS24/2] “Examples of treating a customer with forbearance and due consideration would include the firm…

…accepting no payments, reduced payments or token payments”

- …and re-arranging payments over an (unspecified) “reasonable” period of time:

[FCA PS24/2] “…agreeing a repayment arrangement with the customer that allows the customer a reasonable period of time to repay the debt“.

- The new FCA text below mentions “individual circumstances of the customer“…

[FCA PS24/2] “When determining appropriate forbearance and treating the customer with due consideration, a firm must take into account the individual circumstances of the customer of which the firm is or should be aware.”

- …which must now be “sufficiently detailed“:

[FCA PS24/2] “the assessment should be informed by sufficiently detailed information;“

- Customer details include essential living expenses that may now go beyond “mortgage, rent, council tax, food and utility bills”:

[FCA PS24/2] “Priority debts and essential living expenses include, but are not limited to, payments for mortgage, rent, council tax, food and utility bills.”

- And significantly, vehicles can now only be repossessed as a “last resort“:

[FCA PS24/2] “A firm must not take steps to repossess a customer’s home, goods or vehicles other than as a last resort, having explored all other possible options.”

- Recent results from specialist lender Secure Bank Trust (STB) acknowledged the profit impact of repossessing fewer vehicles:

[STB H1 2024] “We engaged in formal discussions with the FCA about our collections processes, procedures and policies following its Borrowers in Financial Difficulty (‘BiFD’) review. As a consequence of this review, the Group temporarily paused Vehicle Finance collection activities. This has caused higher volumes of loans reaching default status and delays in repossession and recovery activities, resulting in a higher provision coverage in Vehicle Finance of 10.7% (FY 2023: 8.9%) and a cost of risk of 8.8% (HY 2023: 2.4%) for this business.”

Regulation: Consumer Duty

- Overlaying all the new BiFD rules is the FCA’s new Consumer Duty principle:

[FCA PS24/2] “Principle 12 (a firm must act to deliver good outcomes for retail customers), including PRIN 2A “

- This FY described Consumer Duty as a “paradigm shift” that replaced “a raft of secondary legislation and regulatory controls over the past 20 years”.

- The FCA’s new regime now requires lenders to deliver “good outcomes” for retail customers — although “good outcomes” are not precisely defined.

- However, the FCA has published a round-up of Consumer Duty best practices, which includes the topic of “fair value“:

“Retail customers experience harm where they don’t get value for their money. A lack of fair value is unlikely to be consistent with customers realising their financial objectives and firms cannot act in good faith if they are knowingly manufacturing or distributing poor value products or services.

Good practice:

We have seen firms:

Examine whether the total cost to consumers of their products and services – including fees, charges and other costs – provides fair value relative to their benefits. Firms have made changes to improve their value proposition by reducing costs for consumers by:

Updating pricing models for products and services. For example, reducing the rate of interest paid on certain credit products and/or for certain types of customers;

Reducing or removing charges for certain products or ongoing services where these were deemed too high relative to the benefits provided;

Putting controls in place for certain groups or customers, for whom charges over a certain amount do not offer fair value, to improve value and remove these charges“

- The main worry perhaps for SUS is the FCA not believing motor-finance products charging Advantage’s typical 33.87% APR are providing “fair value“.

- Management’s FY webinar responded to my question on this matter:

“Q: The FCA’s Consumer Duty requires firms to deliver ‘good outcomes’ for retail customers relating to, among other elements, ‘price and value’. How will S&U persuade the FCA that motor-loan APRs at 33% provide ‘fair value’ to a consumer that repays in full? Customers who repay their motor loan in full and on time may not see themselves as receiving ‘fair value’, because they effectively subsidise the customers that do not pay on time to ensure Advantage as a whole makes a suitable ROCE.

A: Ahead of the implementation of Consumer Duty in July 2023, Advantage conducted a full review and assessed that its hire purchase product did provide fair value to customers in its target market. On the cross subsidisation point please note the FCA has stated that ‘Our price and value outcome rules do not require firms to charge all customers the same amount, or to make the same level of profit from all customers’. We constantly review our pricing point in the market and continue to believe we offer a great product, competitively priced.”

- Another Consumer Duty concern is the regulatory desire for consistent product “fair value” may restrict the ability for lenders to satisfactorily recoup losses from non-paying customers. This FCA letter stated:

[FCA 2023] “Products need to continue to offer fair value when a customer falls behind with their payments, so in considering the fair value of their products firms must consider all interest, fees and charges a consumer may incur, including late payment/arrears charges. This is especially important if the target market includes consumers with poor credit rating.”

- Consumer Duty could therefore open the door for a greater number of borrowers to delay repayment and not suffer any financial penalty.

- Management’s FY webinar responded to my question on this matter:

Q: A ‘Dear CEO’ letter last year from the FCA to the motor-finance industry said: “Products need to continue to offer fair value when a customer falls behind with their payments, so in considering the fair value of their products firms must consider all interest, fees and charges a consumer may incur, including late payment/arrears charges. This is especially important if the target market includes consumers with poor credit ratings.”. This letter implies Advantage customers can now delay repayments and not suffer any great financial penalty, which would lead to lower Advantage’s ROCE. Does the board therefore agree the new forbearance rules have fundamentally weakened the long-term economics of Advantage and the wider sector?

A: Our income from collection charges and additional interest on arrears has historically not been significant (we actually do not charge any additional interest on arrears except if there are court recovery proceedings later). The more important point you indicate therefore is that a potential collection charge does help encourage customers to not delay repayment unnecessarily. We don’t believe the FCA plans to do away with reasonable collection charges in the motor finance sector as this would affect other financial sectors and products too. We also do not believe that new forbearance rules have fundamentally changed the economics of our sector, mainly as the current evolution of these rules is likely in time to provide collections improvement through a more transparent and certain platform for our customer collections activities. Moreover, we anticipate that our own continuous improvement of credit risk identification and pricing alongside these collections improvements may give us some competitive advantage.”

- The one certainty from Consumer Duty (and BiFD) is the greater regulatory cost. This FY revealed an extra £1.5m compliance expense:

“Administrative expenses [at Advantage] increased by 25% reflecting continued staff cost inflation and an extra £1.5m spent on regulatory costs this year”

- This FY repeated SUS’s claim that Consumer Duty would, with the help of a ‘skilled person‘, benefit the group (eventually):

“Of course, Advantage have responsibly embraced the new consumer duty and will further work with the regulator to make it effective in practice. First, because it is right to do so and second, since it will give well organised companies like Advantage a commercial advantage over those who are not. Advantage is currently working with the regulator and a company-appointed ‘skilled person’ to do so.”

- One regulatory issue thankfully not impacting SUS directly concerns the FCA’s investigation into motor-finance discretionary commission arrangements.

Regulation: SUS response

- This FY included numerous remarks about BiFD and Consumer Duty.

- SUS confirmed its support for the FCA’s wider objectives…

“S&U endorses the FCA’s objectives aimed at enhancing the consumer experience, safeguarding customers from the infrequent but possible negligence within the finance sector and assisting individuals in navigating challenges that may arise during the tenure of their loan. We have consistently maintained that lending is not a win-lose scenario, and believe that transparent, straightforward, and mutually agreed-upon regulations serve the best interests of both the customer and the lender.”

- …but also noted “unintended consequences” — such as a withdrawal of industry capital — arising from the FCA’s enhanced regulatory regime:

“In recent years, a notable trend has emerged contrary to expectations. The workforce of the FCA has expanded to 4,289 employees, an increase of 1,100 in the last year, paralleled by a substantial contraction in credit availability. A February report by Clearscore, a data provider and credit scorer, in collaboration with Ernst and Young, highlights a marked decrease in the availability of debt products for non-standard customers over the last twelve years.

…

Unintended consequences may include a dampening effect on [both] innovation and the introduction of new products. Furthermore, there has been a notable decrease in industry capital, with Ernst & Young estimating a reduction of £2 billion in recent years, as funders grow cautious due to concerns about repayment reliability.”

- SUS claimed an industry-wide withdrawal of capital might lead to some motor-finance borrowers unable to improve their credit scores…

“Imposing restrictions on customers’ ability to address their arrears, in pursuit of comprehensive and sometimes intrusive affordability assessments, may inadvertently lead to a preventable worsening of their credit scores.“

- …or even obtain car loans legitimately:

“For the markets serving these [non-prime] consumers to remain stable and competitive, ensuring access is paramount. Without this, numerous vulnerable consumers might find themselves resorting to unregulated, and potentially illicit, lending options—a scenario diametrically opposed to the expectations of a civilised society.“

- Undefined terms such as “affordability” and “vulnerability” within the FCA’s regulations appeared to be particularly frustrating for SUS:

“Central to ensuring consistent and equitable outcomes for customers is the precise definition of terms such as ‘affordability’ and ‘vulnerability’, which are inherently subjective and fluctuate over time, particularly in an inflationary environment where the lines between ‘essential’ and ‘discretionary’ spending may become indistinct.”

- SUS reassuringly confirmed Advantage was one of many non-prime lenders being assessed by the FCA:

“In response to ongoing concerns regarding the cost of living and its declared objective to “deliver quantifiable consumer benefits,” the FCA has launched comprehensive inquiries across the industry, affecting approximately two-thirds of non-prime motor finance companies.”

- SUS pre-empted the FCA’s assessment by modifying certain collection and recovery actions…

“In anticipation of the findings, Advantage has consented to specific limitations on its repayment processes. These modifications have temporarily influenced monthly repayments and recovery efforts. However, following constructive dialogues with the regulatory body, these measures are being thoughtfully adjusted to ensure flexibility and effectiveness.”

- …which caused the aforementioned increases to overdue accounts (see Advantage Finance: up-to-date and overdue accounts) and impairments (see Advantage Finance: impairments), and led to the 41% H2 profit slump.

- SUS’s modifying of certain collection and recovery actions has continued into FY 2025 (see June and August trading updates).

- SUS believed the regulatory changes would lead only to “temporary disruption“…

“As the motor finance industry transitions to new modes of regulation and evolving assurance of fair customer outcomes, it is to be expected that the mutual learning and understanding between firms and regulator will cause some temporary disruption.“

- …and the group would prosper thereafter:

“In future however, Advantage expects that its long-term experience and humane approach to every customer, irrespective of their background, as evidenced by its industry-leading customer satisfaction and Ombudsman “uphold” rates, will be vindicated and rightly bear fruit.“

- Trading updates issued during June and August suggested Advantage’s collection processes may become excused from FCA scrutiny during H2 2025 (see June and August trading updates)

- That said, this FY admitted SUS may be on the hook to pay compensation to borrowers “adversely affected” by Advantage’s collection practices:

“Our motor finance subsidiary Advantage was included in the FCA’s multi-firm Cost of Living Forbearance Outcomes review in 2023 and as a result the FCA concluded that enhancements may be required to Advantage’s approach to arrears management and the application of forbearance. Advantage and the FCA have been in correspondence throughout 2023/24 to discuss and agree the necessary steps and Advantage will carry out an assessment of whether any customers were adversely affected by its practices. Where this is found to be the case Advantage will seek to redress any detriment.

The financial effect of any customer redress cannot be reliably assessed at this early stage of the review. This ongoing assessment is expected to be in advanced stages in Summer 2024, with any redress being made after that.”

June and August trading updates

- Trading updates during June and August reported an extension of Advantage’s regulatory upheaval.

- June’s update said Advantage’s Q1 2025 repayments had declined by 4% and collections-of-due had dropped to 88%:

[RNS June 2024] “At Advantage, our cautious approach to repayments in the light of continuing discussions with the FCA and Skilled Person on interpreting and adapting to the new Consumer Duty regime and the sector wide review of Borrowers in Financial Difficulty, have had a significant impact on repayments and profitability.

…

Total repayments including settlements in the first quarter were 4% less than last year.

…

This cautious approach and temporary restrictions on repayments have seen live monthly collections reduce from 92.1% of due in the year ended 31st January 2024 to 87.7% of due in the first quarter this financial year with repossession receipts similarly affected.”

- Additional motor-loan impairments left SUS’s Q1 2025 profit down 34%:

[RNS June 2024] “Group profit before tax for the first quarter fell to £6.9m (2023: £10.5m)… Increased impairment provisioning arising from the lower repayments at Advantage accounted for £3.6m of this reduction.”

- June’s update anticipated “regulatory clarity” during H2 2025…

[RNS June 2024] “We anticipate that these discussions [with the FCA and Skilled Person] will be concluded during the second half of the year, when we will welcome the new regulatory clarity which will provide a strong platform for the continuing growth of the business.”

- …although August’s update then referred to “constructive but vigorous negotiations” with the FCA:

[RNS August 2024] “This [consolidation and retrenchment] has resulted from a period of restrictions and caution arising from a Financial Conduct Authority (“FCA”) section 166 notice and the constructive but vigorous negotiations taking place to remove the [collection capability] restrictions, which are now nearing their conclusion.“

- “Vigorous” negotiations suggest Advantage may have to modify certain collection and recovery actions for a while longer.

- Indeed, August’s update calling for political intervention does not feel promising:

[RNS August 2024] “The welcome (at least for now) election of a Labour government with a strong majority and a stated commitment to restoring Britain’s feeble rate of growth, will, we hope, gradually lead to a more pragmatic and realistic approach to regulation…

If these credit requirements [of our target market], which are an essential component in achieving economic growth, are to be met, the Labour ministers must change the restrictive and constantly changing regulatory regime in this country, and the paternalistic mindset behind it.”

- August’s update revealed repayments of due had dropped to 87% and up-to-date loans had dropped to 69%:

[RNS August 2024] “Although the value of monthly collections is marginally up on last year, the above restrictions on managing customer arrears and on repossessions have seen a year to date level of 87% repayments to due, from 94% last year. Up‐to‐date live receivables have fallen to 69% of the total, from 79% last year, although a release from current restrictions should see a bounce back in the second half of this year“

- At least SUS still expects a “bounce back” during H2 2025.

- Collecting 87% of repayments due is akin to Christmas occurring every month:

- Up-to-date loans of 69% compares to 74% for this FY, 61-73% during the pandemic and c80% pre-pandemic:

- August’s update said Advantage’s net loan book was £327m, down only £5m on the £332m reported for this FY.

- Aspen’s net loan book meanwhile had improved £19m to a record £149m since this FY. The division’s collections are up 20% on budget, too.

- August’s update confirmed year-end borrowings at £240m:

[RNS August 2024] “Group borrowings stand at around £240m (2023: £183.7m) against £224m at year end, well within current committed facilities available of £280m.

- Borrowings of £240m would incur annual interest of £19m if SUS is indeed paying interest at the aforementioned 8%.

Valuation

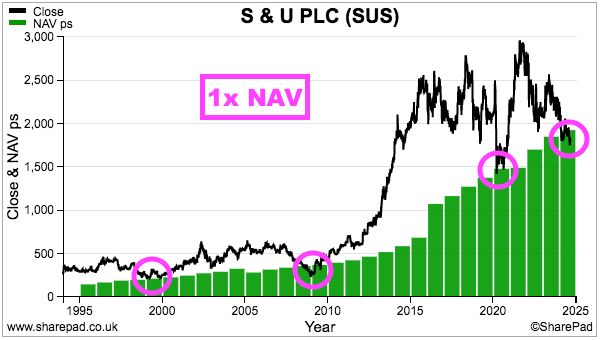

- The £18 shares suggest the profitability of used-car finance — and perhaps property-bridging finance as well — has been permanently diluted.

- This FY showed net assets at £234m or £19.27 per share, although August’s update implied net assets might be £236m or £19.42 per share.

- The stock market therefore values SUS at c0.93x NAV.

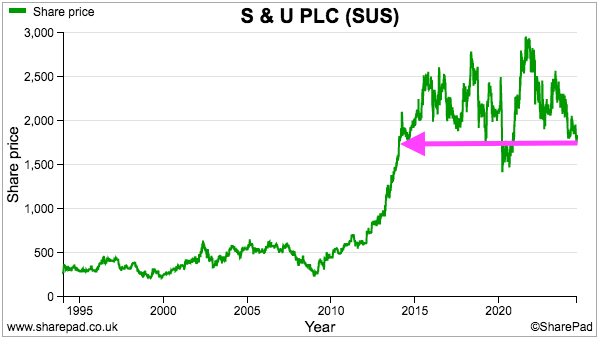

- The shares have traded below NAV only occasionally during the last 30 years:

- Buying at NAV should (in theory) deliver returns equivalent to lending direct to SUS’s customers — with NAV effectively protected by the right (regulations permitting!) to repossess the secured vehicles/properties if the loans default.

- An 0.93x NAV rating therefore implies the market is very worried that regulatory changes — and possibly economic trouble — will lead to reduced collections, greater impairments and limited lending progress.

- After all, if BiFD and Consumer Duty now restrict the ability for motor-loan lenders to repossess their cars, then maybe the sector will soon be awash with later payers.

- Assuming (regulation-free) Aspen is valued by the stock market at book value, Advantage must therefore be valued at less than 0.93x its book value.

- The shares fell to £14.75 during the August 2020 pandemic lockdowns, at which point the last declared NAV was £14.81 per share.

- SUS then navigated through FCA-authorised payment holidays and general Covid disruption and, with hindsight, over-estimated pandemic-related write-offs by £15m.

- I am hopeful SUS is once again taking a prudent view of expected impairments given August’s update, but Advantage’s collections of due declining to 87% and up-to-date loans reducing to 69% are not encouraging.

- For extra perspective on past valuations, the shares dropped to 250p at the end of 2008 when NAV at the time was £43m or 366p per share.

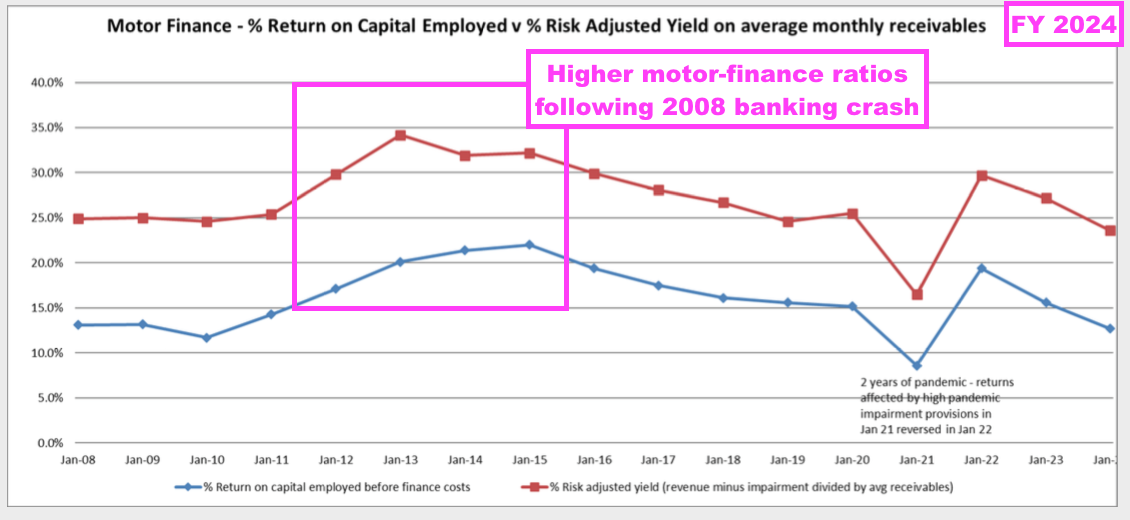

- Mind you, SUS was predominantly a home-credit business during 2008 and may have attracted much greater worries to justify a 0.7x NAV valuation during the banking crash.

- Bear in mind the banking crash did reduce lending competition, and various measures of Advantage’s profitability improved until rivals re-emerged from 2015 onwards:

- Perhaps BiFD and Consumer Duty will combine to inhibit motor-finance competition and eventually bolster Advantage’s profitability and performance.

- In the meantime, the forthcoming H1 2025 results will reveal whether reduced collections, greater impairments and higher debt costs will continue to hinder earnings, NAV and the dividend.

- Assuming no further payout reductions, this FY’s 120p per share dividend supports a handy 6.7% yield at £18.

- This share has typically offered a useful income.

- My initial purchase during Q1 2017 was in retrospect not a great bargain at £21 with a trailing 4.1% yield, but my following top-ups did capture a greater income:

- Right now, dividends are the primary source of returns given the £18 shares are back to a level first achieved during 2014:

- To conclude, the aforementioned Coombs family managers have successfully navigated many previous downturns (not least the pandemic), and this FY reminded shareholders of the long-term benefit of employing such leadership:

“Our over-arching factor in the success of our business over 80 years and through three family generations of management is our business philosophy. The identity of interest between management and shareholders has fused our ambition for growth with a conservative approach to both credit quality and funding.”

- I trust the “the identity of interest between management and shareholders” will (once again) prove its worth when the regulatory dust eventually settles.

Maynard Paton

S & U (SUS)

Trading update published 19 September 2024

Oh dear — a profit warning for H1 2025. But not a huge surprise given the adverse motor-finance commentary within the June and August updates noted in the blog post above. This update was issued during market hours, which is bad form. Here is the full text:

——————————————————————————————————————

S&U PLC, the specialist motor and property finance lender, today issues an update for its expectations for the financial year ending 31 January 2025.

Advantage Finance

As previously referenced in the Group’s announcement on 12 August the cautious approach and business retrenchment adopted by Advantage Finance, the Group’s motor finance division, since the imposition of the Financial Conduct Authority’s (“FCA”) Section 166 notice have continued to impact the performance of the division, primarily resulting from restrictions on its collections capabilities.

Whilst Advantage continues to actively pursue a conclusion of negotiations with the FCA for a removal of the restrictions soon, their cumulative impact on Advantage Finance’s profitability has caused Advantage’s first half profitability to fall below expectations. As a result, Group profits in H1 are expected to be c.£12.8m and this is likely to cause the Group’s financial year profitability to 31 January 2025 to fall below market expectations.

However, the Group still anticipates improvements in Advantage Finance’s performance in the second half brought about by a plan to be implemented upon the anticipated removal of the FCA’s restrictions and appropriate modifications as a result. The timing of these nevertheless remains uncertain.

Aspen Bridging

Aspen Bridging, S&U’s property lending division, continues to deliver strong and profitable growth driven by robust business momentum and excellent credit quality whilst the outlook for the division remains exciting owing to a healthy deal pipeline, its talented and entrepreneurial team and the backdrop of falling interest rates.

S&U will announce its half year results on 8 October 2024 at which point it anticipates providing additional detail on Group and divisional performance and an update on the outlook for the full year.

Commenting on S&U’s trading outlook, Anthony Coombs, S&U Chairman, said: ”Although operating conditions at our motor finance business remain challenging, we are confident in our plan to improve performance once it is set in motion in the second half. Aspen continues to deliver healthy results and faces a bright future.””

——————————————————————————————————————

The tone of this statement implied relations between SUS and the FCA have deteriorated.

The FY 2024 statement referred politely to the FCA’s “inquiry” that focused on affordability, forbearance and vulnerable customers.

August’s statement then referred to “a period of restrictions and caution arising from a [FCA] section 166 notice“.

But now we are told about the “imposition” of the FCA’s section 166 notice, which does read as if SUS is undertaking the s166 under duress.

August’s statement mentioning “vigorous” discussions with the FCA did suggest a conclusion to the s166 might not be imminent, and sure enough this statement confirms the regulatory discussions continue. Modifications to motor-loan collections — including fewer repossessions — therefore stay in place.

SUS says H2 2025 should see an improved motor-loan performance, but everything depends on the FCA discussions… and I would not be surprised if the “anticipated removal of the FCA’s restrictions” were actually pushed into H1 2026.

An H1 2025 profit (I assume pre-tax) of £12.8m compares to £21.4m for H1 2024 but is similar to the £12.2m for H2 2024.

However, June’s statement said Q1 2025 pre-tax profit was £6.9m, so Q2 pre-tax profit was therefore £5.9m. June’s statement indicated Q1 2025 profit was hampered by extra motor-loan impairments of £3.6m. So perhaps extra motor-loan impairments for Q2 2025 were closer to £5m?

What is slightly unnerving is August’s statement had already said motor-loan net receivables were “around £327m“.

So SUS knew the value of the H1 2025 motor-loan book in August, but only now knows the H1 profit outcome — which is confusing, as the impairments within the profit calculation also influence the loan-book value.

I therefore wonder if the greater-than-expected impairments for H1 2025 may lead to the motor-loan book value within the upcoming H1 2025 results being different to the £327m stated within August’s statement. Would not look good for SUS if that was the case. The H1 2025 results will confirm whether NAV is still approximately £19 per share.

At least Aspen continues to do well.

Maynard

Hi Maynard,

I still hold S&U and, frustratingly, it seems the FCA is still ramping up its post-GFC crusade to stop anything bad happening to any consumer for any reason ever.

For lenders, this means having to bend over backwards to support borrowers who are struggling to repay loans, by reducing repayments and stretching the repayment period out to infinity. In reality, a default and repossession often makes more sense for all parties.

I also hold Close Brothers and like other motor finance businesses, it’s currently facing a huge compensation bill for so-called “hidden” commissions that were standard across the industry for more than a decade!

In both cases, I think these issues are the fault of the regulator rather than the fault of the affected companies, as was the case when the UK’s retail energy market collapsed a few years ago.

Hopefully our new government will change the FCA’s culture to focus on growth rather than an obsession with over-protecting consumers, but in the meantime, financial stocks are a painful place to be.

John

Hi John

Yes, I agree with the sentiment here. SUS has mentioned the ‘unintended consequences’ of the greater regulation, which include a withdrawal of capital from the sector and consumers seeking loans from less legitimate sources. Ultimately the sector is not a charity and, if the FCA demands the likes of SUS have to continue with their modified collection processes and repossessions become almost impossible to implement, then the APRs will have to increase and/or loan availability will shrink to compensate for the lower returns from the loan book. I fear politicians will become involved to perhaps reassess the FCA’s regime only when too many would-be borrowers (=voters) find themselves excluded from used-car finance.

Maynard