08 July 2022

By Maynard Paton

Results summary for M Winkworth (WINK):

- “Extraordinary levels of activity” due to pandemic stamp-duty reductions ensured an outstanding FY 2021 with underlying profit up 167%.

- Talk of sales income again exceeding lettings income plus lifting the Q1 2022 dividend by 23% underpinned a promising FY 2022.

- Earnings at the company-owned Tooting office may have slumped during the year, although the effective return on the branch’s valuation remains impressive.

- A super 34% margin, net cash at more than 20% of the share price and trade receivables at just 7% of revenue leave the accounts in good order.

- A possible 9-12x P/E and 6% yield match WINK’s past rating as investors presumably worry about potential problems within the housing market. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- Franchisee sales and lettings income

- Winkworth versus Foxtons

- Corporate-owned offices

- Financials

- Valuation

News links, share data and disclosure

News: Annual results, presentation and webinar for the twelve months to 31 December 2021 published/hosted 12 April 2022

Share price: 175p

Share count: 12,733,238

Market capitalisation: £22.3m

Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, with progress buoyed by motivated franchisee owners capturing market share from conventional rivals.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments.

- Seasoned family management boasts £10m/47% shareholding and rewards investors through durable quarterly dividends and occasional special payouts.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Revenue, profit and dividend

- Record H1 results followed by profit upgrades during November…

“As a result of this buoyant level of activity during the current year, Winkworth’s full year revenues are expected to exceed management forecasts and our full year profits to be materially higher than expectations.”

- …and then January...

“Winkworth’s full year revenues have again exceeded management expectations and pre-tax profits are expected to be ahead of market forecasts at the time of the last trading update.“

- …had already confirmed these FY 2021 figures would be outstanding.

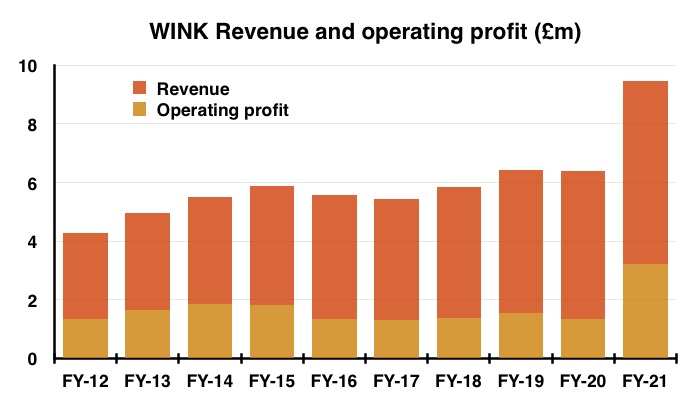

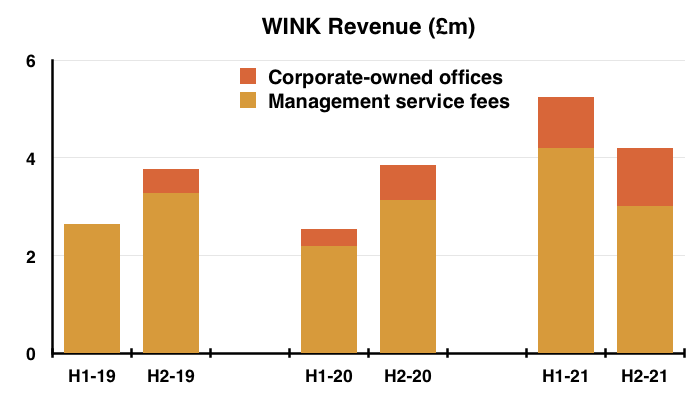

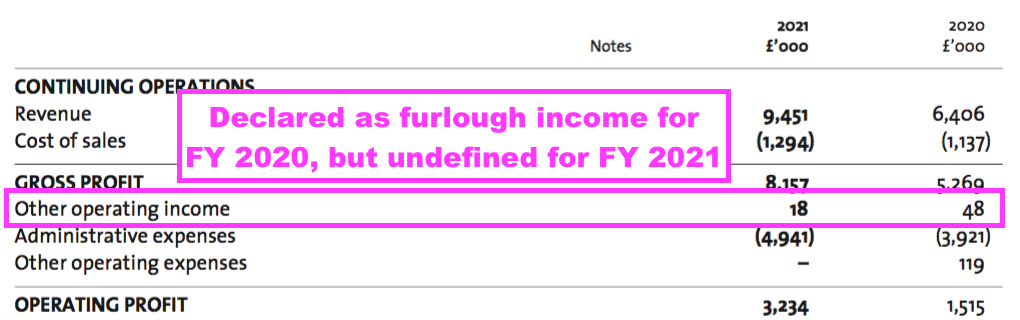

- Revenue jumped 48% while reported operating profit surged 113% to set WINK’s best-ever yearly performance:

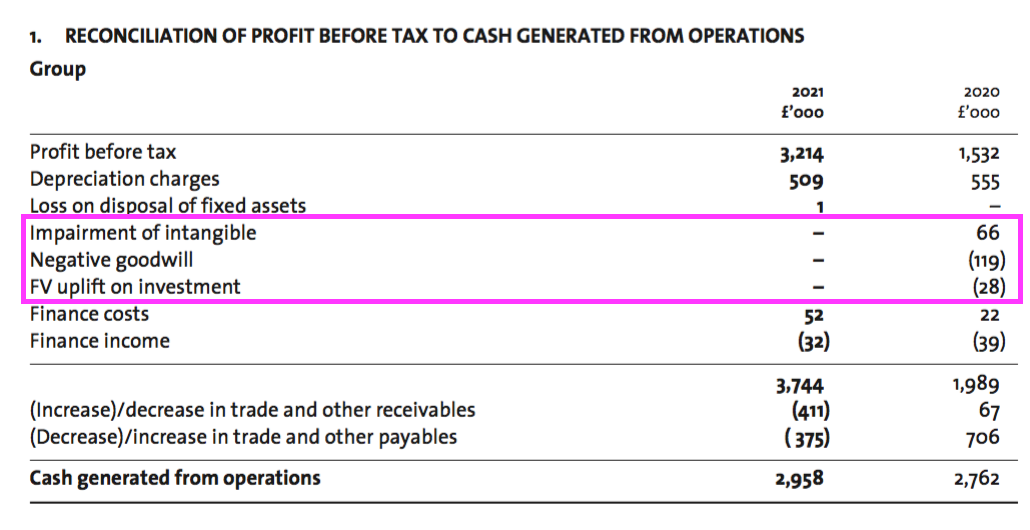

- Several minor items influenced the profit comparison (see Financials):

- Negative goodwill of £0 (2020: £119k);

- Government furlough benefits of £0 (2020: £48k);

- Undefined other operating income of £18k (2020: £0);

- Fair-value investment gains of £0 (2020: £28k);

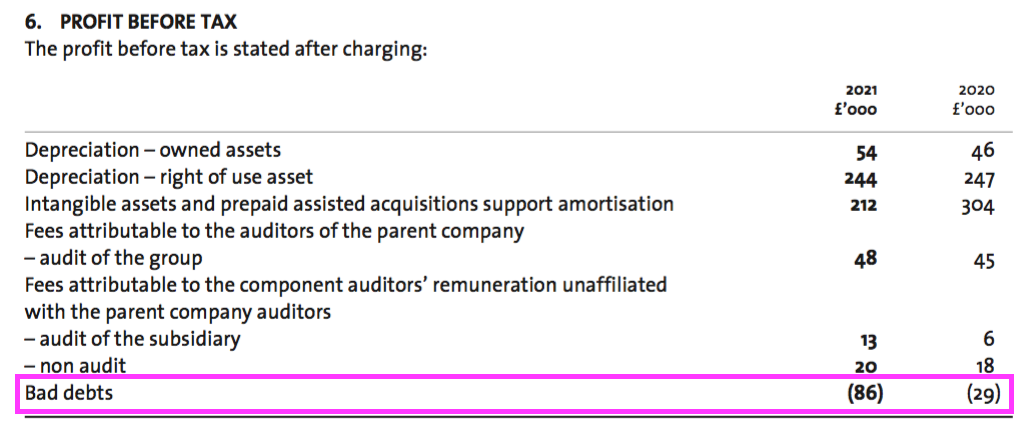

- Bad-debt reversals of £89k (2020: £29k), and;

- Impairments of £0 (2020: £66k).

- Operating profit gained 167% to £3.1m adjusted for those items.

- WINK reiterated the exceptional performance had followed “extraordinary levels of activity” due to stamp-duty reductions during the pandemic:

“The powerful post pandemic recovery drove a very buoyant property market in 2021, fuelled by extraordinary levels of activity around the time of the first proposed stamp duty deadline in June and then the extended deadline at the end of September, producing record months of sales income for the Company.“

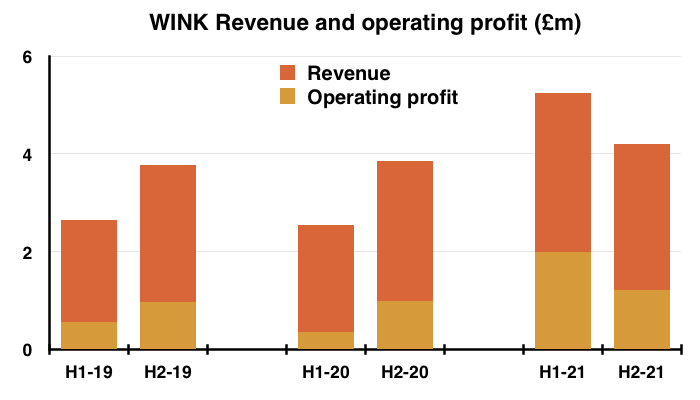

- H2 notably did not match the remarkable H1.

- H2 revenue was £4.2m and £1m less than H1, while H2 operating profit was £1.2m and £0.7m less than H1:

- H2 was nonetheless a record H2 performance for both revenue and profit.

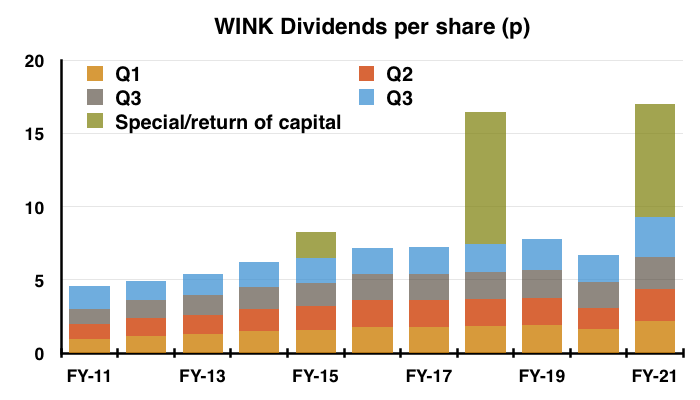

- WINK’s quarterly dividend declarations during October and January had already heralded a 4.9p per share ordinary payout for H2:

- Total ordinary dividends of 9.3p per share were 19% higher than the 7.8p per share payout for pre-pandemic FY 2019.

- January’s update announced a 3.8p per share special distribution, the third for FY 2021 after 1.3p and 2.6p per share specials were declared during H1.

- Annualising the 2.7p per share Q1 2022 dividend announced within these FY results gives a 10.8p per share payout — 16% higher than the 9.3p per share declared for this FY (see Valuation).

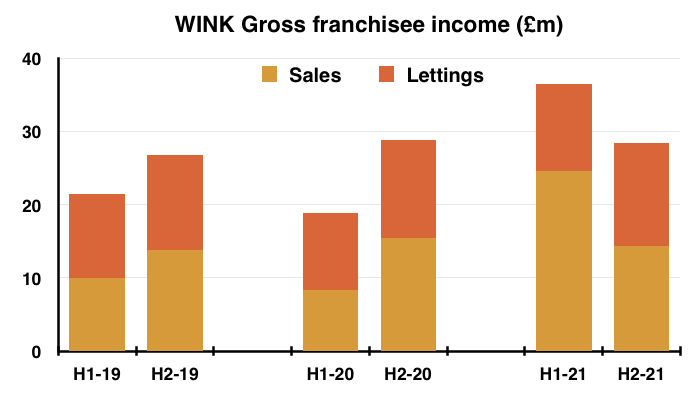

Franchisee sales and lettings income

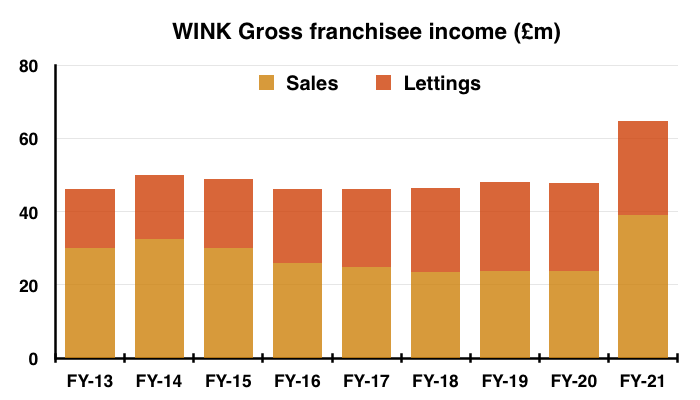

- WINK’s franchisee network consists of 102 estate-agency branches located throughout London and south-east England.

- Franchisees pay WINK a straight 8% of all their sales and letting commissions, plus variable sums towards IT, training, landlord/tenant referrals and other services.

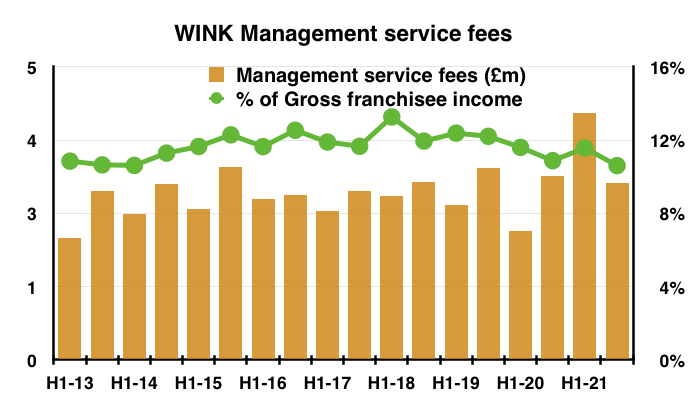

- During this FY, 11.1% of the £65m earned by the franchisees was taken by WINK as revenue:

- The 11.1% proportion was the lowest since FY 2014. Perhaps franchisees were overwhelmed with property transactions to bother with extra WINK services.

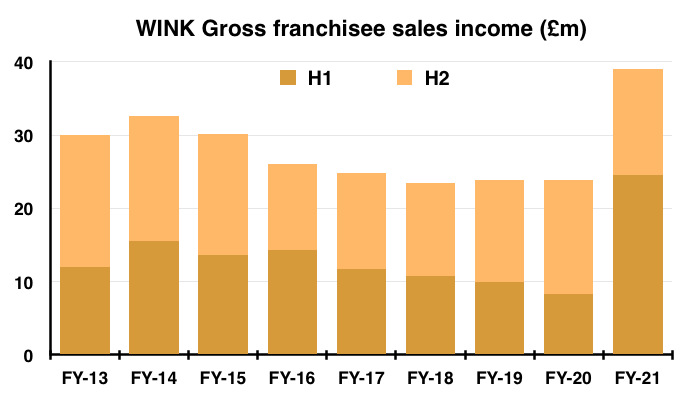

- The aforementioned “extraordinarily active” sales market was not as active during H2 as H1.

- Sales commissions earned by WINK’s franchisees reached almost £25m during H1 but then fell to less than £15m during H2:

- Franchisee sales commissions for H2 were in fact £1m less than the level achieved during the comparable H2 2020.

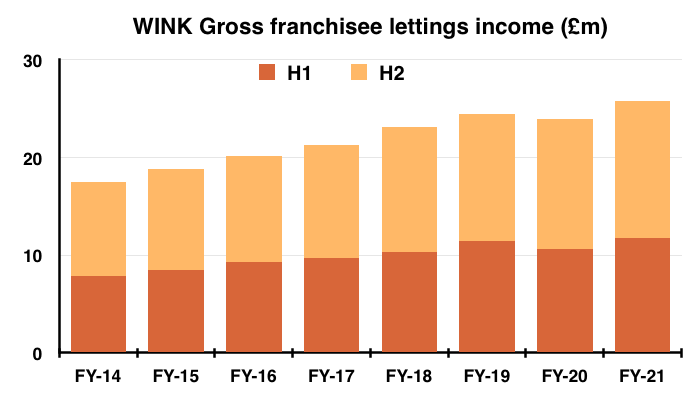

- Lettings commissions collected by franchisees set a new annual record of almost £26m:

- WINK said lettings income had improved following “an upturn in London in the second half of the year following the return of young professionals, some international travel and international students.“

- Franchisee lettings commissions as a proportion of total commissions dropped to 40% for this FY, the lowest proportion since FY 2015:

- Mind you, the lettings proportion was 49% for H2 and in keeping with the equal split between sales and lettings for FYs 2018, 2019 and 2020:

- WINK helpfully indicated sales commissions were likely to surpass lettings commissions during FY 2022:

“Winkworth benefits from a broadly even mix between sales and rentals, but for the immediate future we expect our sales commissions to account for more than half of total revenues, as was the case in 2021.”

- Assuming lettings commissions hold steady, the projection may imply sales commissions of at least £26m and total franchisee commissions of at least £52m for FY 2022.

- Prior to FY 2021, the previous time franchisee sales commissions reached £26m was FY 2016.

- Prior to FY 2021, the previous time total franchisee commissions topped £50m was FY 2014.

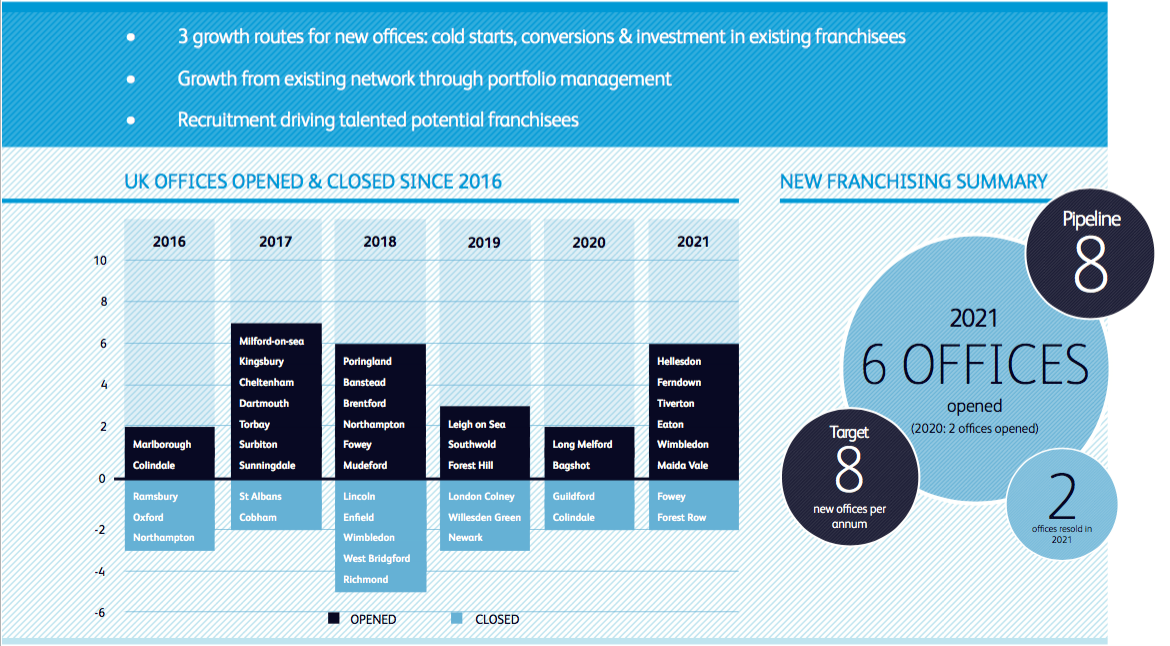

- WINK’s presentation contained a useful slide that highlighted new and closed franchisee offices:

- Some 26 offices have been opened and 17 have been closed since FY 2016.

- Some new offices have not worked out; Collindale and Fowey for example were both opened and then closed a few years later.

- But closed offices can re-open; Northampton and Wimbledon for example were both shut and then re-opened a few years later.

- Expanding the franchisee network has been slow going. The 102 franchised branches operating during FY 2021 compare to 86 quoted within the 2009 flotation document.

- My notes from the 2016 AGM explain management’s thinking on branch numbers:

“WINK’s franchise network has expanded from 86 to c100 branches in the last 6 years. I said that seems like slow progress. The chairman suggested his experience was that in some years it was good to open offices, and some times it was good to consolidate. He made the point that in the early 90s, the business made a greater profit with 35 offices than it did earlier with more than 40.

The chairman also cited the importance of having higher quality franchisees, rather than a higher quantity. A bad franchise in one area could have a knock-on effect on reputation in a neighbouring area. He was keen to ensure franchisees could produce £500k revenue/year, as those earning much less could be susceptible to ‘shrinkage’ (loss of transactions) and fall into financial trouble, damage the brand etc.

The company evaluates its franchisees every year and looks to get rid of 6-8 under-performers. Apparently, a fresh franchisee can increase a sub-standard franchise’s revenue from £150k to £400k. Ideally WINK wants its franchises to earn £500k revenue/year.“

- 102 franchised branches earning the chairman’s ideal £500k revenue gives gross franchisee income of £51m — versus £65m for FY 2021 and £48m for pre-pandemic FY 2019.

Winkworth versus Foxtons

- WINK’s FY 2020 statement had confirmed the group capturing greater market share during the pandemic:

“We further improved our strong position in the marketplace and ranked 2nd in London with a market share of 4.53%, having increased our share of SSTC properties in 2020 by 0.35% [Source: TwentyCI]”.

- Although these FY 2021 results did not refer to market share, the presentation did say WINK remained second in London:

“Maintained position as number 2 in London by SSTC market share”

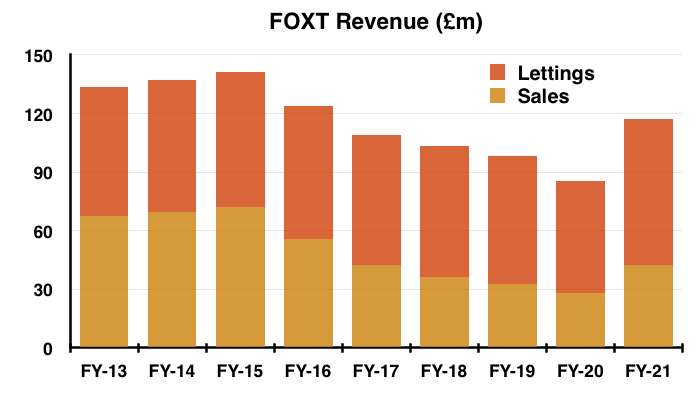

- Comparing WINK to Foxtons (FOXT) — which still claims to be “London’s leading estate agent” — provides a useful guide as to the relative progress of both operators.

- FY 2021 was FOXT’s best year for revenue since FY 2017:

- The chart below expresses the sales, lettings and total franchisee income of WINK as percentages of the comparable FOXT revenue:

- WINK has consistently outperformed FOXT during the last few years.

- During H1 2013, total income at WINK’s franchisees represented approximately 32% of FOXT’s sales and lettings revenue (middle line above):

- That 32% proportion has subsequently increased to 51%.

- Since H1 2013:

- Total sales commissions at WINK’s franchisees have advanced from 42% to represent a very impressive 102% of FOXT’s sales revenue, and;

- Total lettings commissions at WINK’s franchisees have advanced from 22% to represent 34% of FOXT’s lettings revenue.

- Note that the FOXT comparison is not strictly like-for-like. FOXT generates almost all of its revenue from branches within London while WINK has historically generated approximately 80%.

- FOXT acquiring lettings agencies and WINK now operating its own branches (see Corporate-owned offices) also distorts the comparison.

- WINK’s self-employed franchisees do nonetheless appear to have handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees.

- Mind you, FOXT has been subject to a shake-up and could one day recapture its lost market share.

- Board changes within the last twelve months include a new chairman, a new chief exec and a new finance director.

- The new chief exec will join FOXT during September after heading fellow London agents Chestertons since 2018.

- FOXT’s incoming boss apparently grew EBITDA “exponentially” at Chestertons:

“Since his 2018 appointment as Chief Executive of Chestertons, [Guy Gittins] has exponentially grown EBITDA, and transformed the business into a technology led, performance focused business, winning market share; increasing sales in each year; and significantly growing the lettings business both via acquisition and organically.”

- Companies House shows Chestertons’ EBITDA growing from £3.5m to £6.8m between FYs 2018 and 2020:

- FOXT’s shake-up looks to have been driven by activist shareholder Catalist Partners, which last year claimed FOXT could one day sport an enterprise value of £1 BILLION:

- Catalist believes FOXT should compete against the likes of Knight Frank, Chestertons and Savills to sell more £3m-plus properties.

- The appointment of the Chestertons boss suggests FOXT will follow that strategy, which may leave WINK more room within its preferred sub-£1m London market.

- FOXT has also received an activist letter encouraging the group to undertake a formal sale process.

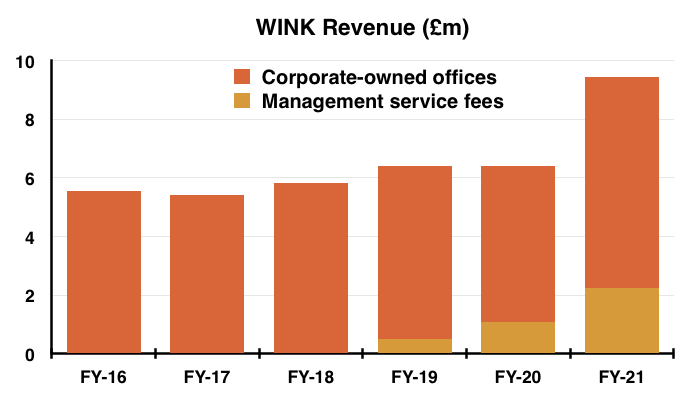

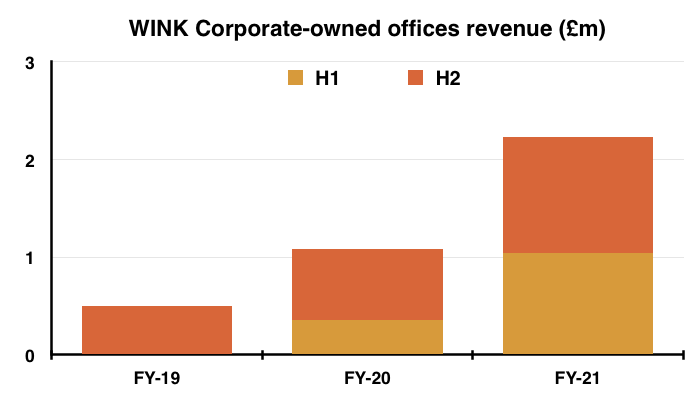

Corporate-owned offices

- WINK’s two controlled branches — Tooting and Crystal Palace in London — seem to outperform the group’s wider franchisee network during this FY.

- Revenue from these corporate-owned offices represented 24% of total revenue during this FY, with the proportion rising from 19% during H2 2020 to 28% during H2 2021:

- To recap, WINK acquired:

- The 2020 annual report (point 15) said the two offices would lead to greater “front-end” insight:

“As with the acquisition of Tooting Estates Limited as a subsidiary, Crystal Palace Estates Limited will keep Winkworth in touch with and learning from front-end experiences and industry trends, It will also provide a live platform to test and develop future digital initiative and evolve our centralised CRM systems, which be of benefit to all our franchisees.”

- Complementing the two majority-owned branches is WINK’s start-up Developments and Commercial agency, which advises on converting business premises into residential accommodation and has displayed “early signs of promise“.

- The presentation hinted further corporate-owned offices could be opened:

“Target new equity participation businesses with key talent in suitable areas”

- WINK’s commentary on Tooting and Crystal Palace was positive:

“Wholly owned offices continued to grow above market trend in 2021, providing the Company with returns over and above the 8% franchise fee.

Our Tooting office was ranked first in its areas by sales agreed in 2021 and has progressed from being Winkworth’s 13th office by gross revenue generated to its 9th.

Our Crystal Palace office completed its first full calendar year under our ownership and revenue progressed successfully in the period.”

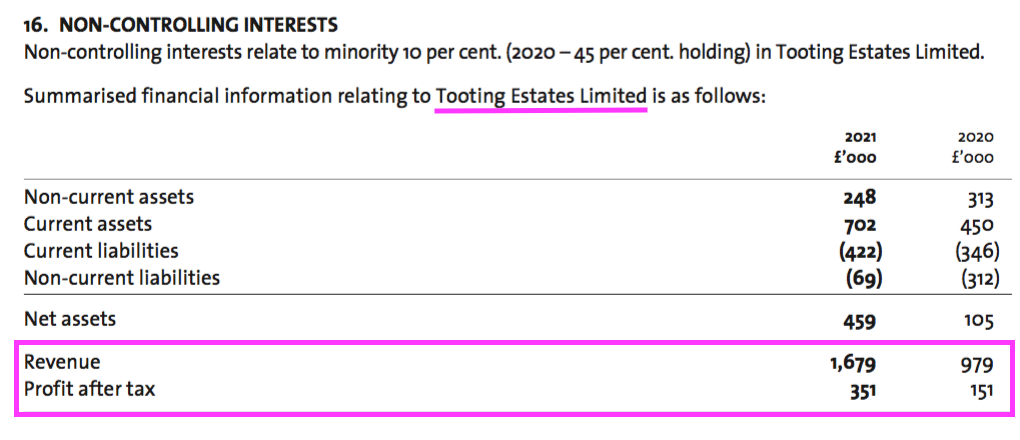

- The FY 2021 contribution from the Tooting office was very encouraging, with revenue up 72% and earnings up 132%:

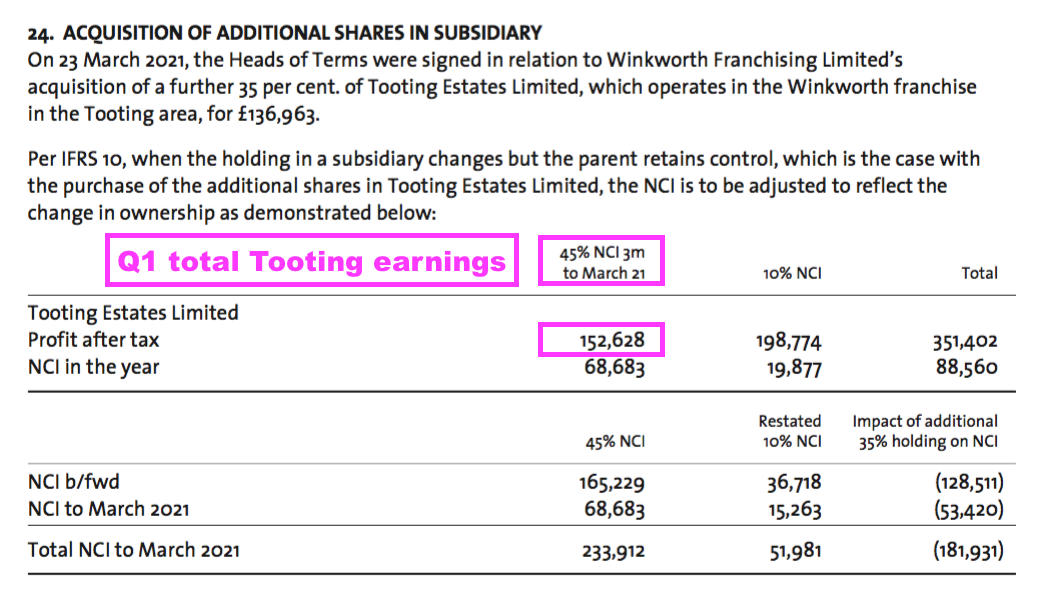

- WINK paid £137k during Q1 to increase its ownership of Tooting Estates from 55% to 90%:

24. ACQUISITION OF ADDITIONAL SHARES IN SUBSIDIARY

On 23 March 2021, the Heads of Terms were signed in relation to Winkworth Franchising Limited’s acquisition of a further 35% of Tooting Estates Limited, which operates in the Winkworth franchise in the Tooting area, for £136,963.

- Paying £137k for 35% priced the entire Tooting operation at £391k.

- Obtaining (albeit on a 90% pro-rata basis) FY 2021 earnings of £351k for £391k seems a remarkably good deal for WINK.

- But earnings from the Tooting office were biased heavily towards Q1.

- Some £153k of Tooting’s £351k full-year earnings were recorded during the first three months of the year:

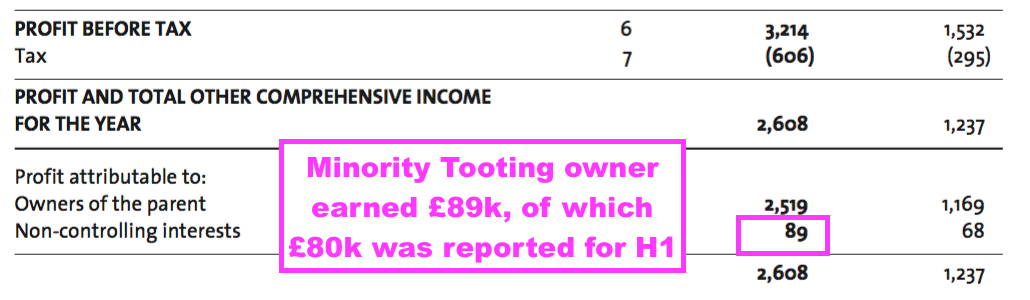

- The minority 10% owner collected Tooting earnings of £89k during the year, of which £80k were reported during H1 leaving only £9k for the 10% minority during H2:

- The 10% minority collecting H2 Tooting earnings of £9k implies the Tooting office generated H2 earnings of just £90k.

- Full-year Tooting earnings of £351k less £153k for Q1 and £90k for H2 implies Tooting earnings of £108k for Q2.

- Tooting’s earnings therefore look to have fallen dramatically as FY 2021 progressed.

- Mind you, doubling up H2 Tooting earnings of £90k gives £180k, which is still a remarkable return on the £391k valuation for the Tooting office.

- The Crystal Palace branch generated revenue of up to £504k during FY 2021, which seemed very satisfactory versus the £104k stated for H2 2020.

- Unlike the wider franchisee network, where the majority of gross income (56%) was biased towards H1, the Tooting, Crystal Palace and Developments operations generated the majority of their combined revenue (53%) during H2:

- Why Tooting’s earnings slumped during H2 despite total revenue from corporate-owned offices holding up feels rather peculiar.

- One explanation could be H1 Tooting revenue was predominantly high-profit sales commissions, while H2 Tooting revenue was mainly lower-margin lettings commissions.

- The Tooting and Crystal Palace branches generated aggregate sales of up to £2,231k during this FY. Were the branches franchised, WINK could have earned revenue of up to £250k (11% of £2,231k) — somewhat less than Tooting’s earnings of £351k.

- Tooting’s £351k earnings less the minority owner’s £89k gives £262k attributable to WINK.

- WINK’s £262k from Tooting represents 10% of the total £2,519k earnings attributable to the group during this FY. The proportion for H2 was 8% (£81k/£1,028k).

- Relying on the Tooting office for up to 10% of group earnings is not ideal, although that dependence is offset by that implied £180k annualised earnings return on the branch’s £391k valuation.

Financials

- WINK’s accounts remain in good shape.

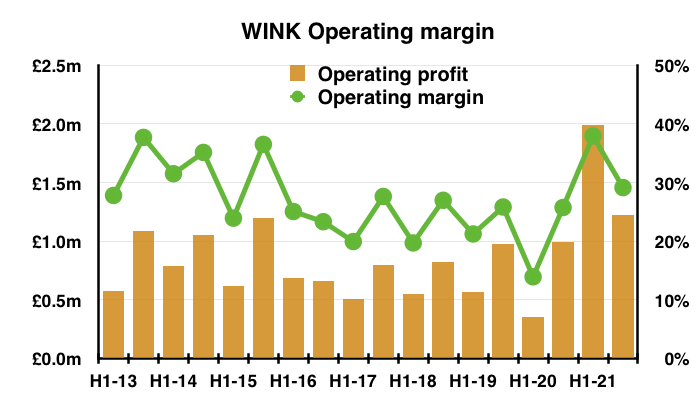

- Although not as high as the remarkable 38% witnessed during H1, the 29% operating margin during H2 was the best H2 conversion of revenue into profit since H2 2015:

- The 34% operating margin for the full year was WINK’s highest since at least FY 2009.

- The lower H2 margin versus H1 coincides with lower sales transactions, and maybe confirms sales commissions attracting much higher profit than lettings income.

- Property sales are of course less predictable than monthly lettings payments.

- Various minor items reported during FY 2020 were not repeated within these FY 2021 figures:

- But (welcome) bad-debt reversals and undefined other operating income did make an appearance:

- Cash conversion improved during H2 after H1 witnessed a notable £1.2m adverse working-capital movement.

- Cash generated from operations for the year was a useful £3.0m, with £1.9m produced during H2.

- WINK’s working-capital cash requirements fluctuate from year to year but have broadly evened out over time:

| Year to 31 December | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit (£k) | 1,302 | 1,369 | 1,535 | 1,348 | 3,216 |

| Depreciation and amortisation (£k) | 246 | 270 | 288* | 308* | 265* |

| Net capital expenditure (£k) | (247) | (189) | (277) | (241) | (276) |

| Working-capital movement (£k) | 567 | (56) | 157 | 773 | (786) |

| Net cash and investments (£k) | 3,586 | 2,988 | 3,614 | 4,732 | 5,090 |

(*excludes IFRS 16 depreciation)

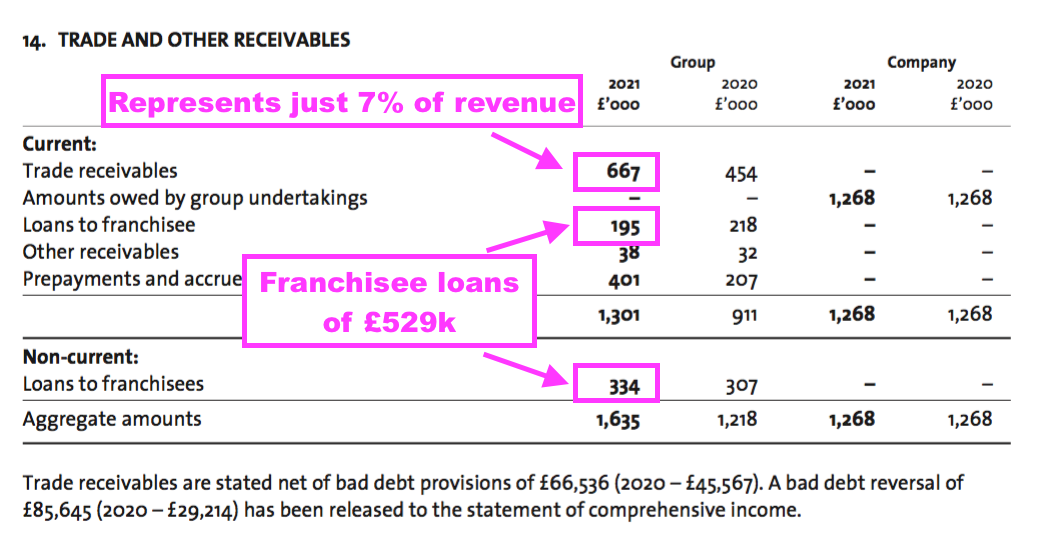

- Trade receivables equivalent to just 7% of revenue indicates franchisees are timely payers:

- Note that WINK’s receivables include loans to franchisees, which for this FY were unchanged at £0.5m but can sometimes lead to notable cash movements as franchisees receive or repay their loans.

- Loans to franchisees peaked at £1.2m during FY 2016, and the subsequent reduction to £0.5m suggests greater (and welcome) sufficiency among new franchisees.

- Capitalised website costs, franchisee “prepaid assisted support” payments and general capex came to less than £0.3m and were once again adequately covered by the depreciation and amortisation charged against reported earnings.

- The working-capital movement, capex, tax of £0.4m, lease costs of £0.3m and that £137k Tooting investment left £2.0m over to pay dividends of £1.6m and £0.4m to increase the year-end cash position to £5.0m.

- Bank debt and defined-benefit pension obligations remain at zero.

- An investment portfolio that started FY 2021 at £71k and was revalued at £56k for H1 was revalued back at £71k for the year end.

- Net cash, loans to franchisees and investments therefore finished the year at £5.6m or 44p per share.

- Finance income from that £5.6m was a very low £7k during H1 but increased to a more reasonable £25k during H2.

- Although cash of £5.0m earning next to nothing remains by far the largest item on the balance sheet, return on average equity was still an appealing 44% (£2.6m/£5.9m):

| Year to 31 December | 2017 | 2018 | 2019 | 2020 | 2021 |

| Return on average equity (%) | 19.8 | 22.6 | 26.8 | 23.8 | 44.4 |

- WINK remains an incredibly capital-light business. Net asset value excluding cash/investments (£5.1) and intangibles (£1.2m) for FY 2021 was only £38k.

- Emphasising the absence of hefty reinvestment requirements, between FYs 2017 and 2021 WINK reported aggregate earnings of 57p per share of which 46p per share (81%) were declared as ordinary or special dividends.

Valuation

- Shareholders must now guess what proportion of FY 2021’s exceptional activity will be sustained into FY 2022 and beyond.

- WINK reckoned London activity would be “brisk“:

“With a busy end to the year in London and increasing interest in central London markets, where both sales and lettings are benefiting as city life returns to a more normal footing, we expect activity to be brisk in 2022.“

- The presentation hinted that FY 2022 could be more lucrative than FY 2019:

“Market conditions to remain positive overall above 2019 levels“

- WINK did not suggest economic conditions were curtailing activity:

“We are mindful of the impact that the tragic situation in Ukraine may have on UK inflation, interest rates and consumer confidence, but have seen ongoing strong demand in the first quarter of the current year with encouraging numbers of applications for both sales and lettings.“

- Management in fact confirmed during the webinar that sales applicants were up 10% and lettings applicants were up 20% during Q1 2022 versus Q1 2021.

- WINK suggesting sales commissions could surpass lettings commissions for FY 2022 — and therefore deliver possible total franchisee commissions of at least £50m — would also indicate the current year may see improved trading versus FY 2019.

- Doubling up the reported H2 performance gives total franchisee commissions of £56m and operating profit of approximately £2.4m.

- Profit of £2.4m taxed at the upcoming 25% UK standard rate leaves earnings of £1.8m or 14.3p per share.

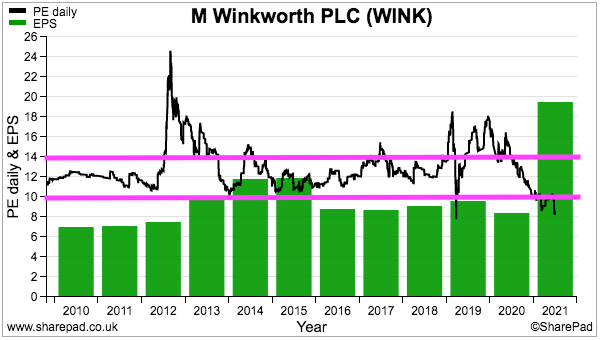

- Dividing the 175p offer price by 14.3p per share gives a P/E of 12x.

- Assume the cash and investments of 44p per share are not required for the business to operate successfully, and a cash-adjusted P/E could be (131p/14.3p) = 9x.

- A multiple of 9x or 12x or somewhere in between appears modest for a business that has been trading very well and feels optimistic about FY 2022.

- But the rating is not out of keeping with WINK’s typical trailing P/E of 10x-14x:

- WINK’s past rating has reflected the group’s largely stagnant profit between FYs 2016 and 2020.

- WINK’s current rating may reflect potential economic problems upsetting the housing market.

- WINK emphasised a “progressive dividend” ambition…

“We see opportunities to grow our business above market trend whilst both paying a progressive dividend and maintaining a healthy cash balance“

- …that was underpinned by lifting the Q1 2022 dividend by 23% to 2.7p per share.

- A 2.7p per share quarterly implies 10.8p per share for the full year to support a 6.2% income at 175p:

- An intriguing valuation snippet was provided during the webinar.

- Management revealed WINK would essentially pay a suitable independent agency up to 32% of its annual revenue to convert into a WINK franchisee.

- With WINK’s total franchisee commissions running at approximately £50m, the group’s own acquisition formula could value all the franchisee offices at £16m (32% of £50m).

- Add on WINK’s £5m cash position to that £16m and the total £21m is just £1m less than the £22m market cap at 175p.

Maynard Paton

M Winkworth (WINK)

Dividend Announcement and Trading Update published 13 July 2022

A reasonable update that may be indicating a weaker H2 to FY 2022. Here is the full text:

——————————————————————————————————————

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 2.7p per ordinary share for the second quarter of 2022 (“Q2 2022”) to shareholders.

While gross sales income across the network in H1 2022 was down some 40% on the exceptionally strong H1 2021, when buyers rushed to complete purchases to take advantage of the stamp duty holiday introduced by the Chancellor in July 2020 and extended from June 2021 to September 2021, H1 2022 was almost 50% higher than in H1 2019, the last period to be unaffected by Covid measures.

Gross lettings income showed a 6% improvement on H1 2021 and a marked increase on H1 2019.

The Directors believe that there is a backlog of unfulfilled sales transactions which are being carried over into the second half of the year and are encouraged by the good levels of both sales applications and valuations, which should provide further support to sales volumes in H2 2022. The outlook for lettings continues to be strong.

While the UK economic outlook and confidence in the housing market remain in question, the Directors are pleased with the Company’s performance in H1 2022 and expect that full year pre-tax profits will be in line with the market forecast of £2.1m, marking a substantial increase on the outcome for 2019.

The timetable for the dividend is as follows:

Ex-Dividend Date* 21/07/2022 Record Date** 22/07/2022

Expected Payment Date 17/08/2022

*Shares bought on or after the ex-dividend date will not qualify for the dividend

** Shareholders must be on the Winkworth share register on this date to receive this dividend

——————————————————————————————————————

The H1 2022 performance look set to just about match the performance of the preceding H2 2021.

Franchisee sales down 40% on last year implies franchisee sales of £24.6m*0.6 = £14.8m for H1 2022. Franchisee letting income up 6% meanwhile indicates £11.8m*1.06 = £12.5m. For H2 2021, franchisee sales were £14.4m and franchisee lettings were £14.0m. Lettings income tends to be biased slightly to H2 over H1, so there is scope for H1 2022 to match/outperform H1 2021 on both measures.

The “strong” outlook for lettings feels reassuring given sales transactions may continue to cool following the elevated levels of the prior 1-2 years.

A £2.1m pre-tax profit for FY 2022 compares with £3.2m for FY 2021 and may lead to earnings of nearly £1.6m or 12.4p per share after 25% tax. My calculations within the blog post above looking for EPS of 14.3p by doubling the H2 2021 performance were therefore a little optimistic.

The implication I think from this update is H2 2022 may be a tad weaker than H1 2022. Talk of “ While the UK economic outlook and confidence in the housing market remain in question…” reads as if WINK is starting to acknowledge a difficult economy. The word “economy” was not mentioned within the preceding FY 2021 statement.

A Q2 dividend of 2.7p per share matches the Q1 payout and, as extrapolated within the blog post above, ought to underpin a 10.8p per share payment for the full year.

Maynard

M Winkworth (WINK)

Publication of 2021 annual report

Here are the points of interest beyond those noted in the blog post above:

1) GROUP STRATEGIC REPORT

a) Revenue

Useful confirmation of pre-tax profit from the corporate-owned offices:

“Winkworth’s revenues benefited from the buoyant market, with franchising income also up by 36% in the year as the increase in network revenue fed through to the franchising business. The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited and Winkworth Development and Commercial Investment Limited, contributed £2.2 million (2020: £1.0 million) to revenue and £0.45 million (2020: £0.19 million) to profit before tax.”

Note 24 says the Tooting office reported post-tax profit of £351k, so pre-tax was approximately £430k — and therefore almost representing the entire £450k for the three corporate-owned offices.

b) Principal risks and uncertainties

Various changes here. Out go risks about ‘Brexit’ and ‘Stamp Duty Holiday’, and in come risks about ‘Geopolitical Developments’ and ‘Digital Infrastructure and IT Risk’.

“GEOPOLITICAL DEVELOPMENTS

Risk: Consumer confidence may weaken as a result of the Ukrainian crisis and its impact on inflation, particularly of energy costs. A tightening of UK interest rates in response to higher prices could have a negative impact on housing demand.

Management action: Winkworth is used to working through all points of the interest rate cycle and, through a conservative management approach to costs, is well positioned to adapt to changing market conditions.”

“DIGITAL INFRASTRUCTURE AND IT RISK

Risk: Winkworth’s IT and Digital infrastructure connects the Winkworth network and is therefore a source of competitive advantage. However, it also means that our operations are reliant on IT systems and technology and certain external suppliers. These are at risk of failure either because of technical issues or from the growing threat of cyber-attacks. Any failure of systems or technology would cause disruption, and any extended period of downtime, loss of backed up information or delay in recovering information could impact significantly on our ability to conduct business.

Mitigation: Firewalls and anti-virus software are installed to protect our networks. Information is routinely backed up and our in-house IT team works with external parties to ensure that the IT infrastructure is securely maintained in accordance with data protection regulations and appropriate disaster recovery and business continuity plans are in place. The IT needs of the business are regularly monitored, and we invest in new technology and services as necessary.”

Among the other risks, ‘Lockdowns’ has been watered down while ‘Market’, ‘Legal & Regulatory Environment’, ‘Recruitment of Franchisees and the Building of Franchises’ and ‘Reputational Risk’ remain unchanged.

c) Section 172

No changes here save for confirmation that WINK is now carbon neutral:

“Winkworth is a carbon neutral company. Our Corporate Carbon Footprint (CCF) has been independently calculated and we are continuously reducing our carbon emissions while offsetting unavoidable ones through carbon offset projects.”

The text reiterates investors are welcome to the AGM:

“Shareholders: The directors provide information for shareholders through the AGM, the annual report, the interim report, public announcements made through RNS and via its website. The Board recognises the AGM as an important opportunity to meet private shareholders and the Directors are available to listen to the views of shareholders informally immediately following the AGM. The CEO and CFO conduct roadshows for institutional investors at the time of our interim and annual reports.”

Can’t say my previous AGM visit was entirely welcome (2016), but things may have changed since. I will have to attend again one year.

2) REPORT OF THE DIRECTORS

A short report that lacks a lot of standard information provided by other small AIM-traded companies. Some information is published only on the website…

“The Directors names, together with biographical details, are shown on the group’s website http://www.winkworthplc.com. The directors’ remuneration for the year is set out in note 4 to the financial statements. There were no changes to the directors during the period. Compliance with the QCA Code

As mentioned in the Chairman’s Statement on Corporate Governance, Winkworth adheres to the QCA Code on Corporate Governance. Full details of how the ten principles have been applied are shown on our website http://www.winkworthplc.com.”

…and some information is published only the website (e.g. director shareholdings), but not even referred to in the annual report.

Committee reports remain very short:

“Remuneration Committee The Committee, chaired by Lawrence Alkin and with John Nicol in attendance met in December to discuss and approve certain bonuses in respect of 2021 and the 2022 remuneration of the Executive Directors and key senior managers in the group.

”Audit Committee

The Committee, chaired by John Nicol, and with Lawrence Alkin in attendance met three times in 2021. In March the Committee met with Crowe to discuss and approve the 2020 Accounts and to review the Audit. In September, the Committee met to discuss and approve the 2021 Interim results and Announcement. In December, the Committee met to discuss Risk and approve the Accounting Policies.”

But at least the FY 2021 report included this extra text about remuneration:

“The Remuneration Committee looks to ensure that the pay of directors and other senior Winkworth staff is set at a level that is competitive and will help retain senior talent. Remuneration is reviewed annually against internal and external measures to ensure that levels are appropriate. In addition, the Committee will sound out major shareholders before finalising their decisions.

As well as considering wage inflation and other economic considerations in the UK, the Committee review executive director fixed and variable remuneration levels against a peer group of quoted estate agency companies to ensure that the different elements are not out of line. The level of bonuses paid in 2021 reflect the group’s exceptionally strong performance in the year and the significantly increased returns that shareholders enjoyed in the period. ”

I am pleased the directors like to talk more about auditing than remuneration:

The non-execs still work 15 days a year.

And somewhat refreshingly, the acronym ESG was not mentioned in the annual report.

3) INDEPENDENT AUDIT REPORT

a) Going concern conclusions

Extra text this year that lists exactly what the auditor considered before approving the ‘going concern’ basis:

“* Reviewing management’s financial projections for the Group and Parent Company for a period of more than 12 months from the date of approval of the financial statements.

* Checking the numerical accuracy of management’s financial projections

* Challenging management on the assumptions underlying those projections and considering the impact of reductions in anticipated net cash inflows.

* Obtaining the latest management results post year end 31 December 2021 to assess how the Group and Parent Company are performing compared to the projections.

* Performing sensitivity analysis on key inputs into the projections by calculating the impact of various scenarios and considering the impact on the group and parent Company’s ability to continue as a going concern in the event that a downward scenario occurs.

* Assessing the completeness and accuracy of the matters described in the going concern disclosures within the significant accounting policies as set out in Note 2.”

b) Materiality and scope

Materiality is the standard 5% of pre-tax profit, with the auditor understandably keeping materiality at a reasonable level by using a three-year average of profit and not using just the elevated 2021 profit:

“Based on our professional judgement, we determined overall materiality for the Group financial statements as a whole to be £105,000 (2020: £76,500) based on 5% of the average profit before tax over the 3 financial years to the reporting date, a benchmark chosen to normalise the effects of the Covid-19 pandemic on the group. ”

I presume the Tooting office isn’t covered by a full-scope audit because of its smaller size:

“There are three significant components in the group, the parent company, Winkworth Franchising and Tooting Estates. The parent company and Winkworth Franchising were subject to full scope audit by ourselves, Tooting Estates was audited by a component auditor.”

c) Key audit matter

Just the one key audit matter — ‘Completeness of revenue’ — and all the text was unchanged from the previous year.

4) NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

a) Accounting policies

Confirmation the group still takes an 8% commission from franchisees:

“Revenue represents the value of commissions and subscriptions due to the group under franchise agreements, together with the value of fees earned by its subsidiary lettings business. Revenue in respect of commissions due on house sales is recognised at the point of the relevant property sale having been completed by the franchisee. Revenue in respect of commissions due on lettings, property management and administration services is recognised in the period to which the services relate. The group earns a straight 8 per cent. by value on all sales and lettings income generated by the franchisees.”

Website costs are now amortised over 3-6 years rather than just 3 years (see point 4d below):

“The website development costs are amortised over their useful life which is deemed to be 3-6 years. Customer lists are amortised over 15 years on a straight line basis.”

Customer lists are tested for impairment by somewhat harshly assuming lettings cash flows decline by 7% a year:

“Valuation and impairment of customer lists

The valuation of customer lists was based on industry multiples of 150 per cent. of the historic lettings revenue and 100 per cent. of the sales revenue, discounted by 30 per cent. for lettings and 70 per cent. for sales revenues, to reflect the future prospects and inherent goodwill relating to the staff of the business. An assumption has been made that cash flows from the lettings business will fall by 7 per cent. per annum. The group is required to test, where indicators of impairment exist, whether customer lists have suffered any impairment. At 31 December 2021 there were no indications of impairment. Should future cashflows of the business fall by 15 per cent., this would give rise to impairment of £85,769.”

And fixtures and fittings are now depreciated at a simple 25% straight-line rather than 15-33% straight-line.

b) Employees

Employees increased to 54, which may be due to a full year’s ownership of Crystal Palace as well as extra headcount to service the year’s elevated trading:

Would be helpful if WINK segmented its employee types to distinguish between the conventional franchising division and the corporate-owned offices.

Revenue per employee for FY 2021 was £175k, the highest since FY 2018 (£177k) but below the £200k-plus recorded between FYs 2009 and 2014 when WINK was a much smaller (and pure) franchising business.

Cost per employee was £65k last year, the highest since FY 2011 (£65k) and led to employee costs equating to 37% of revenue — WINK’s highest level barring the pandemic-blighted FY 2020 (40%). Let’s see if the higher wages are temporary because of the elevated revenue, or become permanent.

c) Director remuneration

The two executives look to have each enjoyed an extra £50k payment because of the bumper performance:

Total remuneration does not feel grandiose given the group’s level of profitability.

d) Intangible assets

Website costs are worth monitoring as the useful life is now 3-6 years (see point 4a above) and other annual report text suggests greater IT expenditure in the future:

The historic cost of website development averaged £657k during the year, with £59k amortised implying the useful life is 11 years — which does not seem right to me. The same calculation for customer lists (£45k/£643k) gives 14 years, which matches the 15-year useful life cited for that particular intangible.

I suppose some website development costs are capitalised and are not amortised until the website goes live sometime later, which could skew my sums. Anyway, website costs show a £385k net book value still to be expensed against earnings, which admittedly is not significant versus the aggregate profit reported since website costs started to be capitalised a decade ago.

e) Property, plant and equipment

No real issues here. WINK spent only £47k on conventional tangible assets last year and amply covered such expense with £54k depreciation:

f) Prepaid assisted acquisitions

This intangible asset reflects cash paid to franchisees to convert their established businesses into WINK offices, with the cost amortised against earnings over the term of the franchise agreement:

Depreciation has exceeded additions for the last four years, suggesting WINK has struggled to find significant new conversions of late.

g) Investments

No change to WINK’s small investment portfolio last year:

h) Trade and other receivables

The ‘quality’ of overdue trade receivables improved last year. Those payments that are 60-plus days late have a 28% loss rate rather than 44%:

i) Trade and other payables

Nothing of great concern here:

Lower payables alongside much greater revenue can look odd, but the difference appears mostly due to tax that could be down to pandemic-related payment timings.

j) Related party disclosures

The chief exec’s wife has started her own WINK franchise:

“On 17 December 2021 Faith Cook, Dominic Agace’s wife, and her business partner acquired the Fulham franchise from its previous owner. Fees of £3,204 were payable by the new venture in respect of the period to 31 December 2021, and £Nil was owed to Winkworth Franchising Limited at the year end. ”

Extrapolating the 14 days of fees gives yearly fees of £83k. This RPT will in future give an insight into the performance of another London branch.

k) Share-based payment transactions

Options represent 4.4% of the total share count:

Of the 4.4%, 3.8% are owned by the two executives. WINK has never incurred a share-based payment charge, which does feel odd but could be due to immateriality. 4% of the share count under option is not immaterial though.

l) Financial instruments

Now for some guesswork on the interest WINK receives from its loans to franchisees, which were £529k as per the blog post above.

This text implies cash of £5m does indeed generate interest of c£12k interest at 0.25%:

“Interest rate and currency of cash balances

Floating rate financial assets of £5,019,677 (2020 – £4,661,788) comprise sterling cash deposits. There are no fixed rate financial assets. If interest rates had been 0.25 per cent. higher during the year, then the group would have generated c£12,000 of additional interest income.”

Interest income was £32k during the year:

So if the £5m cash produced £12k, then the loans to franchisees produced £20k — or a c3.8% interest rate on the £529k loans.

Interest income back in FY 2018 was much higher at £83k, and bolstered operating profit by 6%. I recall the franchisees paying higher rates of interest back then, but I am generally pleased the loans have diminished from £1m-plus (between FYs 2014-2018) as presumably the self-financing quality of the franchisees has improved.

Maynard