25 March 2022

By Maynard Paton

Results summary for Mountview Estates (MTVW):

- An acceptable H1 performance, albeit profit was suppressed by fewer property sales that in aggregate achieved a relatively low gross margin.

- Certain property disposals realising a record 65% premium to their 2014 valuation alongside an £11m special dividend do not suggest inherent trading difficulties.

- Management remarks of “difficult times that may lie ahead” may explain why expenditure on new properties remains low and net debt has been kept at just 4% of the property estate.

- The special dividend, low expenditure and modest debt all perhaps signal a new ‘run off’ chapter, whereby the group consistently sells more properties than it buys.

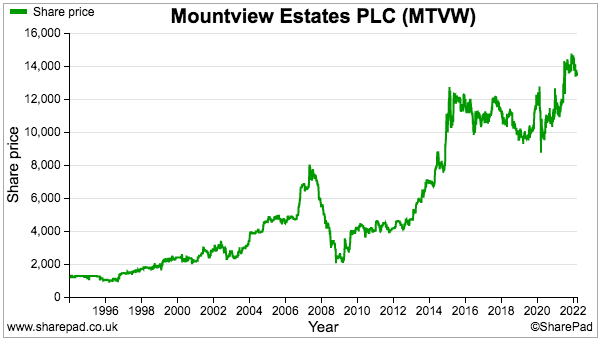

- Book value inched to a record £102 per share, although run-off guesstimates suggest total dividends following a complete estate disposal could total £264 per share. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own MTVW

- Results summary

- Revenue, profit, dividend and net asset value

- Gross margin

- Allsop valuation

- Financials

- Protest votes and shareholder engagement

- Valuation

News link, share data and disclosure

News: Interim results for the six months to 30 September 2021 published 25 November 2021

Share price: £135

Share count: 3,899,014

Market capitalisation: £526m

Disclosure: Maynard owns shares in Mountview Estates. This blog post contains SharePad affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy (and similar) properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to boast an aggregate 50%/£263m shareholding.

- Properties are carried at cost, and when eventually sold at their ‘reversionary’ values may generate dividends significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Revenue, profit, dividend and net asset value

- This acceptable H1 2022 performance was not a total surprise.

- The preceding FY 2021 results had already revealed a remarkable comeback during H2 2021 following the pandemic-disrupted H1 2021, as well as giving a favourable outlook for the current year:

“Taken together with our strong financial position and conservative gearing, then as we look ahead to 2021/22 and beyond, we believe that the business is well positioned to respond, however the markets evolve in the coming months and as the various [pandemic] support mechanisms unwind.

The results from early auctions in the current year are promising and, thus, we are hopeful that we will be able to continue to acquire new stock to sustain the business going forward.“

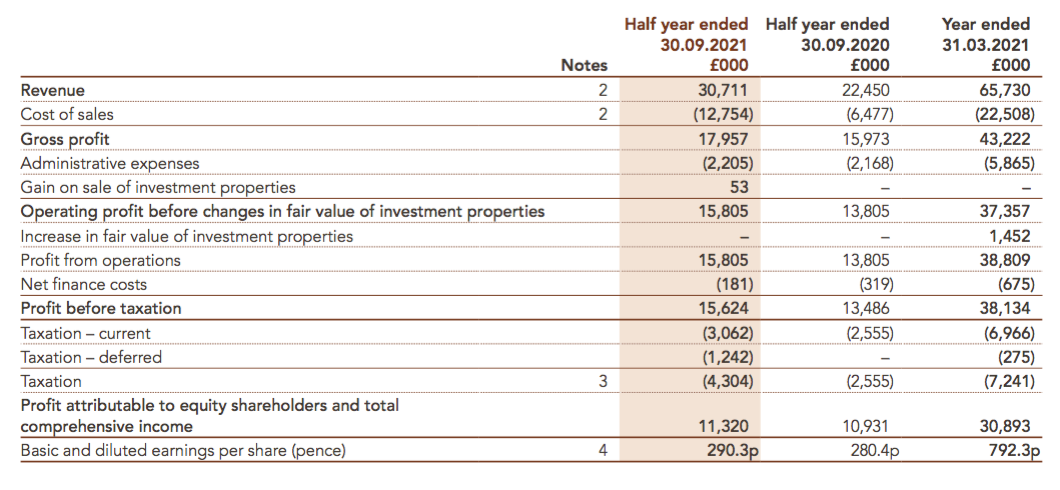

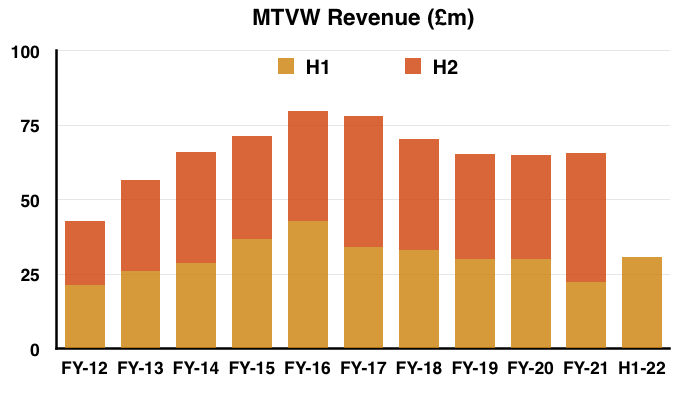

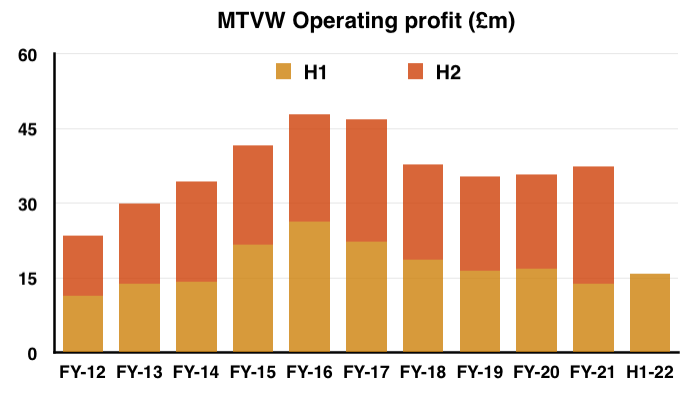

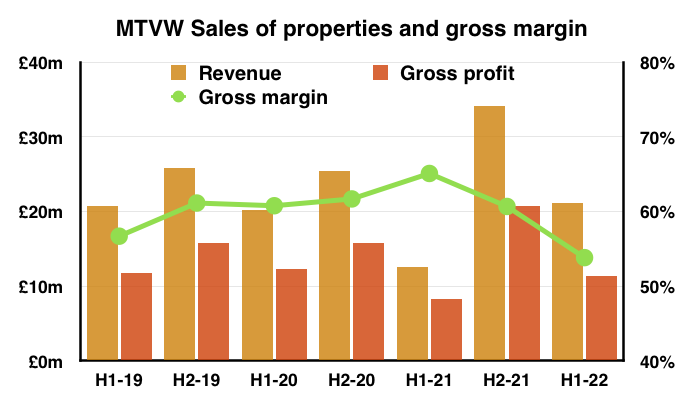

- For this H1, revenue gained 37% although operating profit gained only 14%:

- A much lower margin on property sales caused profit growth to lag revenue growth (see Gross margin).

- Aside from the pandemic-disrupted H1 2021, this H1’s £16m operating profit was in fact the lowest for any six-month period since H1 2014.

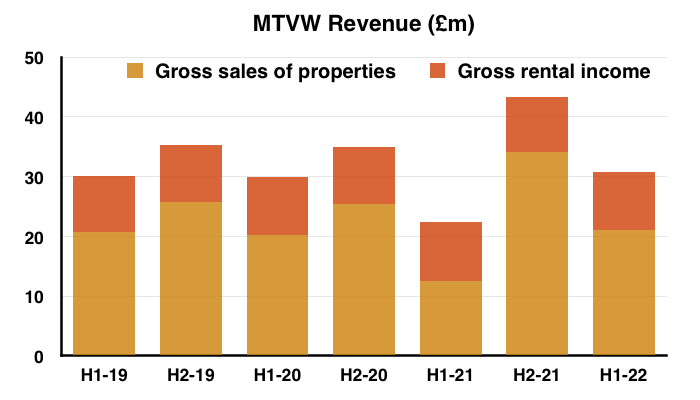

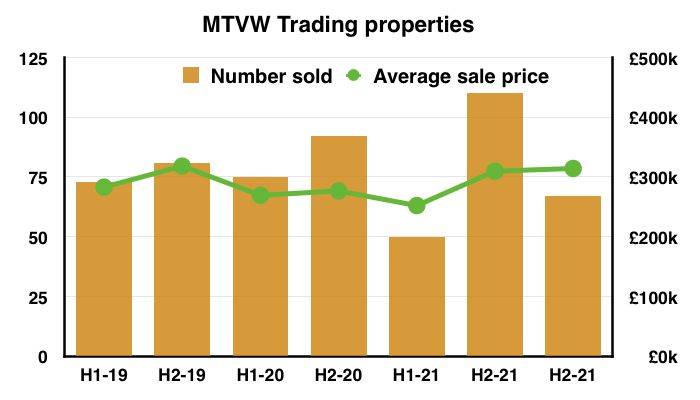

- Revenue was split approximately 70%/30% between property sales and rental income — and closely matched the pre-pandemic splits of H1s 2019 and 2020:

- Note that MTVW sells its regulated-tenancy (and similar) properties only when the tenancy ends — which typically occurs when the tenant has died.

- The mix of properties becoming available for sale — and the total proceeds MTVW earns — can therefore vary from one set of results to the next.

- The 67 properties sold during this H1 compares to 110 during the preceding H2 and approximately 75 for H1s 2019 and 2020:

- Perhaps reflecting the aforementioned “promising” auction results, the £314k average sale price for this H1 improved slightly on the preceding H2.

- I trust sales prices can be sustained above £300k. FYs 2017, 2018 and 2019 witnessed average prices in excess of £300k, only for the figure to drop to £273k for FY 2020.

- Approximately 90% of MTVW’s properties are sold for less than £500k, while the rest are generally sold below £1m with the occasional property sold for more than £1m.

- Earnings of £11m less paid dividends of almost £9m meant net asset value (NAV) improved by less than £3m during the six months to £397m.

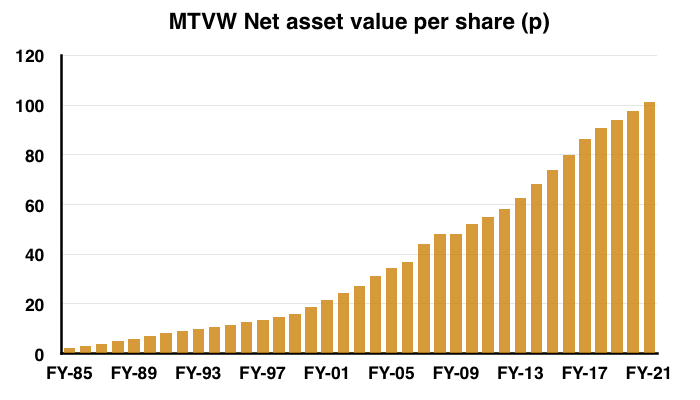

- £397m is equivalent to £101.93 per share and sets a fresh NAV record:

- As noted within my FY 2021 review, MTVW’s NAV per share growth has slowed over time.

- NAV per share has compounded at:

- 5% during the five years to FY 2021;

- 6% during the ten years to FY 2021;

- 7% during the 15 years to FY 2021, and;

- 10% during the 20 years to FY 2021.

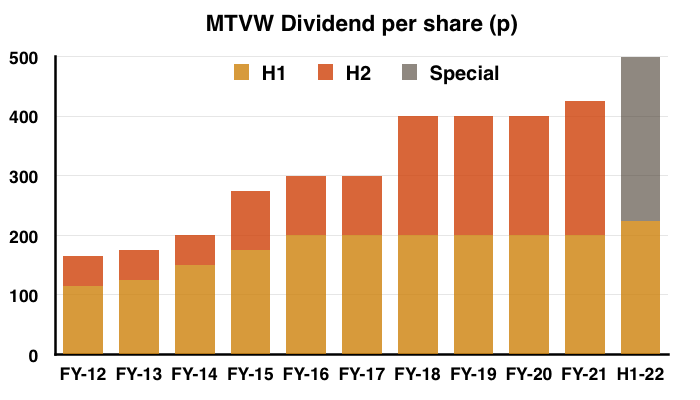

- MTVW expressed confidence about the dividend within the preceding annual results:

“We only increase the dividend when we are confident of maintaining that increase and, indeed, we look forward to being able to increase the dividend further.“

- Sure enough the interim payout was lifted 12.5% to 225p per share to replicate the increase and level of the preceding final dividend.

- The highlight of this H1 was the 275p per share special dividend:

- The archives are not 100% clear, but Companies House suggests the previous special payout (one of “two interim dividends“) occurred during FY 1999 and amounted to 12p per share:

- The latest 275p per share special dividend could be confirmation that MTVW faces fewer buying opportunities for additional properties.

- Management’s outlook text also hinted of fewer buying opportunities (at least at present):

“Good purchases are vital to the future prosperity of the Company and our financial strength will enable us to compete when good opportunities occur.“

- I had speculated on future special dividends within my 2021 AGM notes:

“(MP note: MTVW repaid debt of £10m last year. Borrowings at c£20m are very modest versus the near-£400m property portfolio, while interest rates remain low. Perhaps MTVW should consider special dividends instead of repaying further debt. Another £10m debt repayment would be equivalent to a c£2.50 per share payout).“

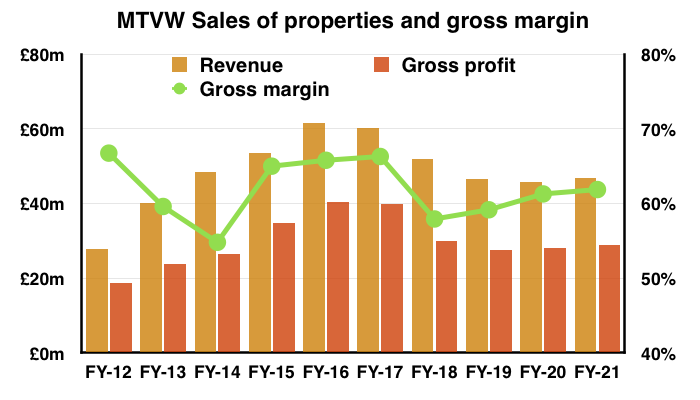

Gross margin

- An important measure of MTVW’s progress is the margin generated through property sales.

- Between FYs 2012 and 2021, the gross margin achieved through selling properties has been as low as 49% (H1 2014) and as high as 71% (H1 2017):

- The gross margin achieved from selling properties during this H1 was a lowly 54%:

- A 54% gross margin is equivalent to buying a property for £100k and selling it for £217k.

- The gross margin achieved from a property sale is correlated to the duration of MTVW’s ownership of that property, which can range from a few years to a few decades.

- The gross margin reported from property sales within any set of results can therefore fluctuate depending on the mix of properties sold during that period.

- The mix of properties sold tends to even out over time. MTVW’s average gross margin over five-year periods has been remarkably consistent:

- FYs 2017 to 2021: 61.3%

- FYs 2012 to 2016: 62.4%

- FYs 2007 to 2011: 60.0%

- FYs 2002 to 2006: 62.6%

- I trust the 54% property-sales gross margin for this H1 was caused by an unusual collection of properties becoming available for disposal during the six months…

- …and that MTVW’s longer-term gross margin will continue to average approximately 61%.

- A 61% gross margin is equivalent to buying a property for £100k and selling it for £256k.

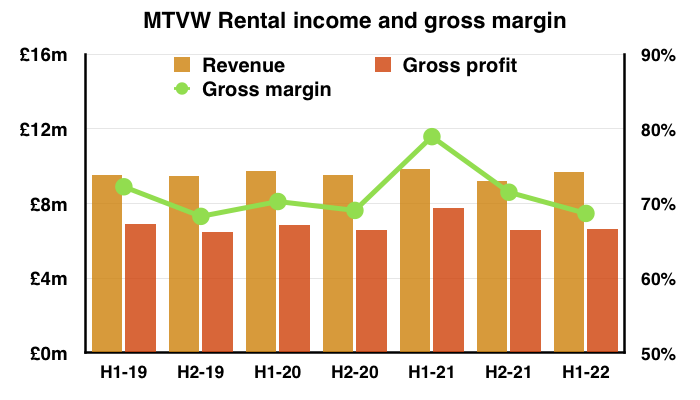

- MTVW’s rental-income gross margin at 69% has reverted to normal levels after certain work was deferred during the pandemic:

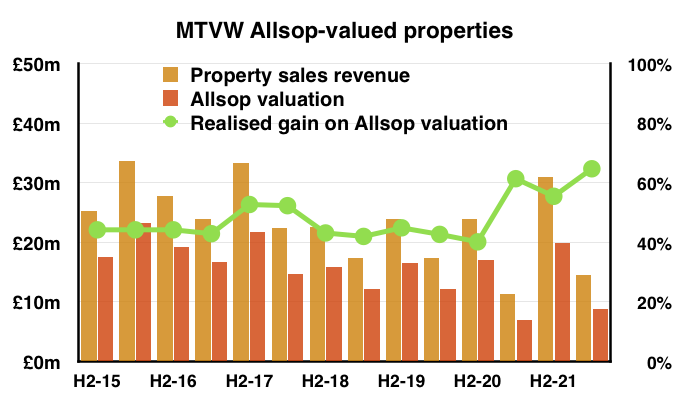

Allsop valuation

- A promising development from this H1 concerned the proceeds from sold properties compared to a past valuation.

- To recap, MTVW commissioned property agent Allsop during September 2014 to assess the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties owned at the time.

- The Allsop assessment was based on MTVW’s properties remaining in their regulated-tenancy state and therefore excluded any ‘reversion’ premium (i.e. the value uplift that occurs when a regulated tenancy finishes, the rent reverts to a proper market level and the property can then be sold at a fair market value).

- The Allsop assessment was not applied to the audited accounts. MTVW’s properties instead remain on the balance sheet at their cost price.

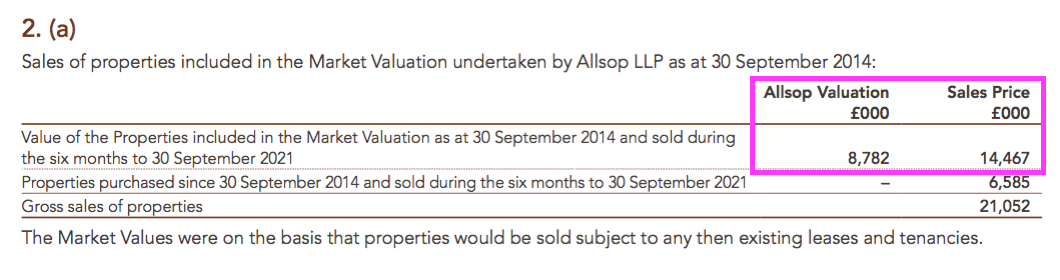

- Following the Allsop assessment, MTVW reveals the proceeds from sold properties versus their Allsop valuation:

- Sale proceeds following the Allsop assessment have realised an average 48% gain on the property agent’s valuation, with a high of 61% witnessed during H1 2021.

- However, this H1 showed the realised gains on the Allsop valuation to be even higher at 65%.

- MTVW has never referred to the Allsop valuation within its results commentary since the assessment was conducted.

- As such, shareholders are left to guess whether the record 65% gain during this H1 was due to a random mix of properties being sold…

- …or generally higher sale prices being achieved at auction.

- A greater realised gain versus the Allsop valuation has favourable implications for assessing MTVW’s property estate and possible share price (see Valuation).

- During the seven years following the Allsop assessment, MTVW has raised £329m from selling properties that the agent had valued at £223m.

- Selling properties that Allsop had valued at £223m implies the book value (i.e. the original cost) of the properties sold was £106m (£223m divided by that earlier 2.1x multiple).

- Selling Allsop-valued properties with a £106m book value indicates Allsop-valued properties with a £211m book value remain within MTVW’s ownership today (i.e. the £318m book value at the September 2014 assessment less the £106m since sold).

- MTVW has during recent years sold Allsop-valued properties with an estimated book value of approximately £14m per annum, suggesting the remaining Allsop-valued properties of £211m could take a further 15 years to sell.

- These H1 results showed total trading properties with a £395m book value, implying properties purchased after the Allsop review have a £184m book value (i.e. £395m less the remaining Allsop-valued properties of £211m).

- Bear in mind the figures above are guesstimates and could be rather inaccurate.

- As more Allsop-valued properties are sold and other properties are purchased, the less relevant the Allsop valuation becomes to the share price.

- MTVW refuses to undertake another Allsop-type valuation. The 2020 AGM Q&A statement declared:

“The cost of carrying out a valuation is such that your Board are reluctant to inflict such an expense on the shareholders when the information so acquired is not a useful management tool.”

- During the 2021 AGM, the board:

- Repeated it was “reluctant to inflict shareholders the cost” of another assessment;

- Disclosed Allsop was paid £600k for the 2014 assessment, and;

- Described the expense as a “substantial amount for something of very little use“.

- I maintain MTVW ought to implement regular valuations to provide greater clarity as to the inherent value of the group’s property estate.

- Further valuations could also judge the astuteness of MTVW’s more recent purchases.

Financials

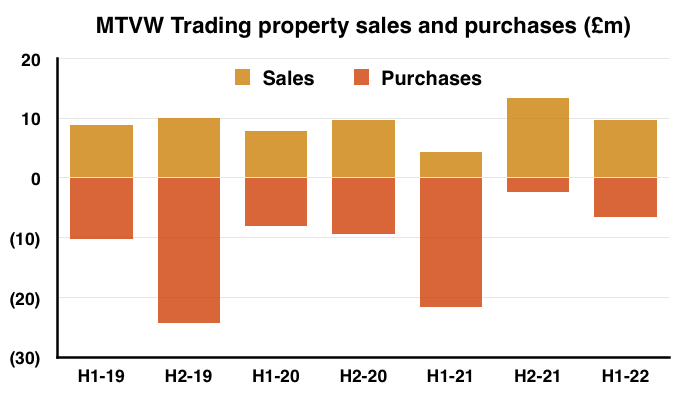

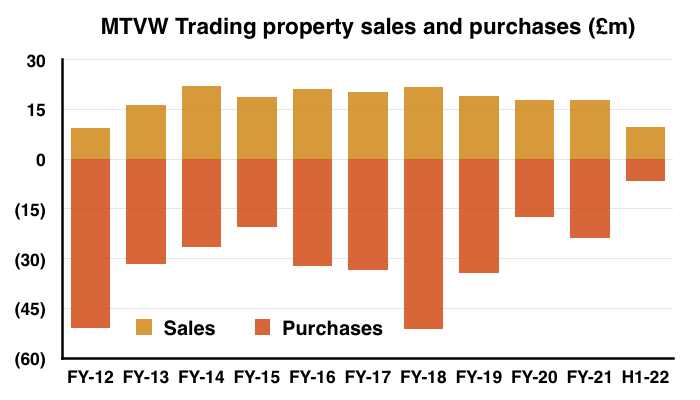

- Only £6m was spent acquiring new properties during this H1, which followed just £2m spent during the preceding H2 2021:

- The trailing £8m twelve-month expense compares to at least £17m spent on new properties annually since FY 2012:

- The following remark could explain why less money was spent buying new properties:

“The Company has generated strong cash flow and we are thus in a good position to shield ourselves from the difficult times that may lie ahead.

- The low level of expenditure on new properties alongside the declaration of that 275p per share special dividend (cost: c£11m) may in fact signal the beginning of a new company chapter, in which MTVW effectively goes into ‘run off’ as the group sells more properties than it buys (see Valuation).

- The market for MTVW’s regulated tenancies will continue to shrink. Such tenancies have not been created since 1989 and Allsop estimates fewer than 75,000 currently exist.

- The number of regulated tenancies owned by MTVW topped 3,000 20 years ago, topped 2,500 ten years ago but today is less than 2,000.

- This H1 revealed a conventional investment property was sold for £620k to realise a £53k (or 9%) gain. These conventional investment properties are presently in the books at £25m or £6 a share.

- The lower rate of new property expenditure helped fund cash dividends of almost £9m and debt repayments of close to £5m.

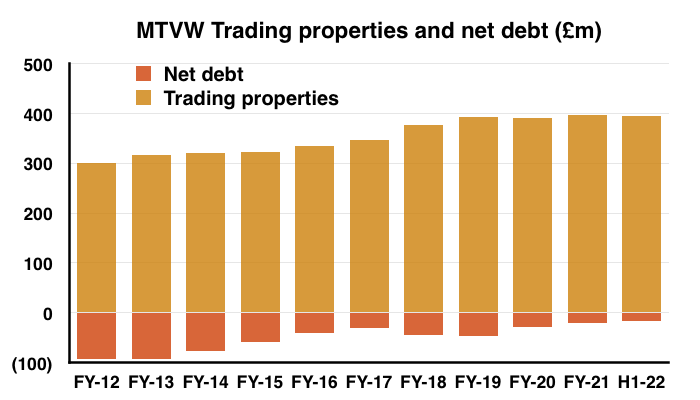

- Borrowings finished H1 at £17m with net borrowings at £16m — the lowest level since FY 1999.

- Net debt of £16m is equivalent to 4% of the group’s £395m property estate — the lowest percentage since at least FY 1997:

- MTVW’s gearing has been much higher. During FYs 2012 and 2013 for example, net debt was equivalent to 30% of the property portfolio.

- The annual report (point 13) disclosed banking facilities of up to £90m — equivalent to 23% of the property estate.

- The modest level of gearing alongside the debt headroom suggests the group would have no problem buying future property bargains should any “difficult times” emerge.

- Interest of just £181k for this H1 implies a very manageable 1.9% interest rate on the period’s £19m average debt.

- MTVW’s accounts are free of defined-benefit pension obligations.

Protest votes and shareholder engagement

- Despite MTVW’s illustrious history of NAV and dividend advances, not every shareholder is content with the way the company is managed.

- The last five AGMs have witnessed c30% protest votes against re-electing independent non-execs, approving the board’s pay and re-appointing the auditors.

- MTVW’s shareholders fall into three camps:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and represents just over 50% of the share count;

- The Murphy family and connected parties, who claim to own 24% of the share count and whose leading shareholder is the chief executive’s sister, and;

- Everybody else, who own 25% of the share count.

- The protest votes come from the Murphy family and connected parties.

- From what I can tell, the Murphy family is broadly satisfied with how MTVW’s day-to-day operations are run, but:

- Is aggrieved about the board’s pay;

- Has lost the trust of the non-execs to act on the views of shareholders, and;

- Is frustrated about a general lack of influence at board level.

- The Murphy family stated during the 2021 AGM that it was no longer in direct communication with the company and would only engage with the directors through a “public forum“.

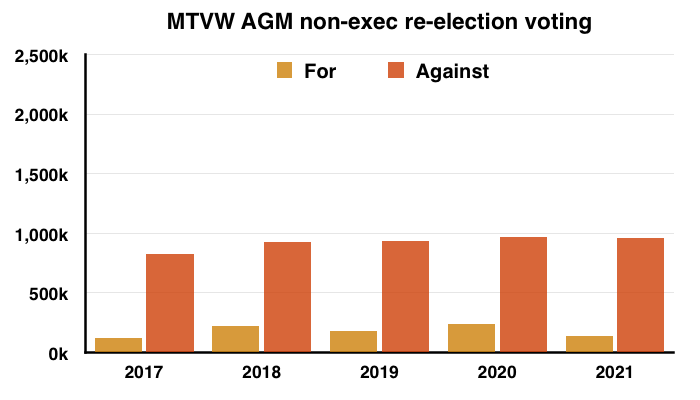

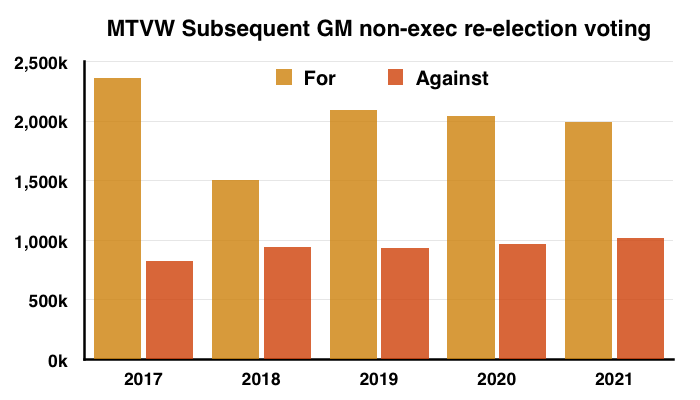

- The Murphy family and other dissident shareholders have prevented the re-election of certain non-execs at the 2017, 2018, 2019, 2020 and 2021 AGMs:

- Following those AGMs, MTVW held general meetings to reinstate the ousted non-execs.

- The non-execs were all re-appointed at the general meetings because the Sinclair concert party could then vote on the non-exec re-elections (unlike at the AGMs, where the concert party is prohibited from voting on particular resolutions):

- The voting charts above show the average votes for and against the certain non-execs up for re-election. At the 2021 AGM, the non-exec chairman gained only 93,785 ‘for’ votes versus 990,479 ‘against’.

- Stock market rules dictate any company incurring a sizeable protest vote has to contact the dissenting shareholders and publish an update within six months.

- Six months after the 2020 AGM, MTVW stated:

“Following the 2020 AGM, and as it has done previously, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage. The Company remains committed to shareholder engagement and we will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.“

- The response text was altered slightly for 2021. Six months after the 2021 AGM, MTVW stated:

“Following the 2021 AGM, and as it has done previously, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. Those shareholders did not wish to engage. The Company remains committed to shareholder engagement and we will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.“

- The changed wording implies some shareholders who engaged after the 2020 AGM did not engage after the 2021 AGM.

- This changed wording and the aforementioned AGM comments from the Murphy family indicate discussions have broken down completely between the unhappy shareholders and MTVW’s board.

Valuation

- The declaration of a special dividend, the modest borrowings and low level of property buying prompts a closer look at MTVW’s valuation on a ‘run-off’ basis.

- This run-off scenario assumes MTVW:

- Keeps selling its properties;

- No longer buys any replacements;

- Hands back all the cash generated each year through dividends, and;

- Eventually owns no properties and the market cap falls to zero.

- The run-off calculations are performed in two parts:

- The Allsop-valued properties owned by MTVW at September 2014, and;

- Properties acquired by MTVW since September 2014.

- Bear in mind the figures below are guesstimates and could be rather inaccurate.

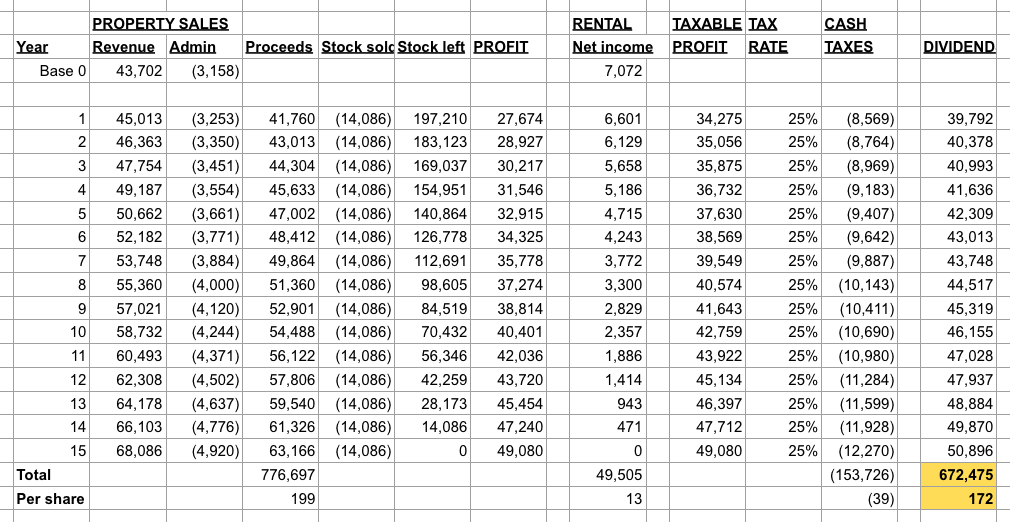

- My earlier sums indicated Allsop-valued properties still owned by MTVW had a £211m book value that, based on the rate of recent disposals, would take another 15 years to sell (i.e at £14m per annum).

- The spreadsheet image below shows the possible dividends achieved from selling the remaining Allsop-valued properties over 15 years:

- The dividends total £672m or £172 per share.

- The base ‘year 0’ assumptions for this first spreadsheet include:

- Sales proceeds of £43.7m derived from the aforementioned:

- 2.1x Allsop valuation multiple versus book value and;

- Average 48% gain on the Allsop valuation at disposal.

- Trailing twelve-month admin costs of £5.9m pro-rated to £3.2m to reflect the Allsop-valued properties’ 53% share of total book value (i.e. £211m / £395m), and;

- Trailing twelve-month net rental income of £13.2m pro-rated to £7.0m to reflect the Allsop-valued properties’ 53% share of total book value (i.e. £211m / £395m).

- Sales proceeds of £43.7m derived from the aforementioned:

- Assumptions for the subsequent 15 years for this first spreadsheet include:

- Property prices and admin costs increasing by 3% a year;

- Net rental income declining in line with the disposal of Allsop-valued properties, and;

- Tax at a constant 25%.

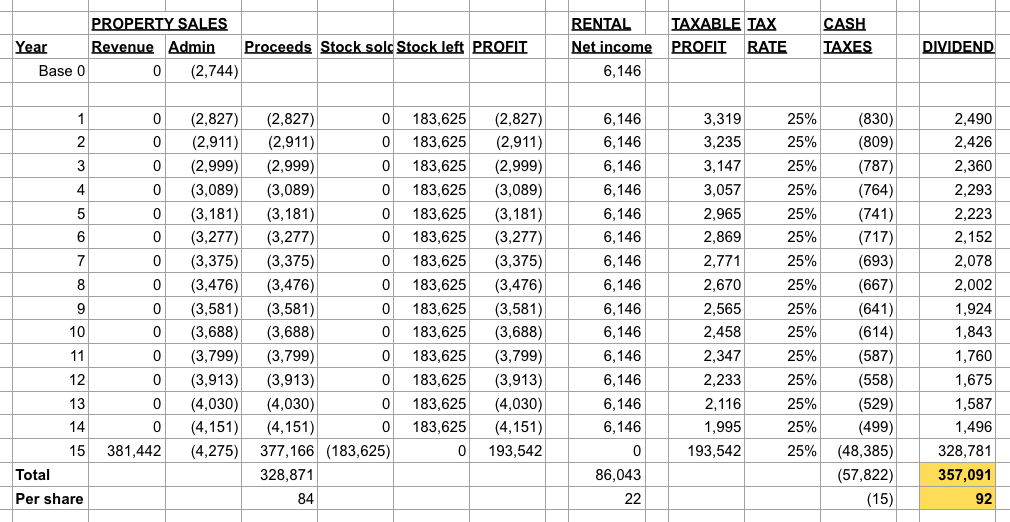

- This next spreadsheet image shows the possible dividends resulting from selling the properties bought following the Allsop assessment:

- The dividends total £357m or £92 per share.

- Property-disposal assumptions for this second spreadsheet include:

- The remaining properties were purchased at a 75% discount to their fair market value (as per management comments during the 2019 AGM) and revert to 100% of their fair market value on disposal, and;

- Proceeds of zero until year 15, at which point all the remaining properties are sold.

- (Note: Although the remaining properties can in reality be sold at any time, a bulk sale after 15 years perhaps provides a realistic average outcome given the purchases all occurred relatively recently (i.e. after September 2014))

- The base ‘year 0’ assumptions for this second spreadsheet include:

- Trailing twelve-month admin costs of £5.9m pro-rated to £2.7m to reflect the remaining properties’ 47% share of total book value (£184m / £395m), and;

- Trailing twelve-month net rental income of £13.2m pro-rated to £6.1m to reflect the remaining properties’ 44% share of total book value (£184m / £395m).

- Assumptions for the subsequent 15 years for this second spreadsheet include:

- Property prices and admin costs increasing by 3% a year;

- Net rental income remaining constant until all the remaining properties are sold during year 15, and;

- Tax at a constant 25%.

- Add the spreadsheet totals together and MTVW’s eventual run-off value could be £1,029m or £264 per share paid through dividends.

- Adjusting that overall total for MTVW’s conventional investment properties (£25m), net borrowings (£16m) and other liabilities (£6m) would not make a significant difference to the sums.

- Buying at the recent £135 share price to collect a potential £264 per share through dividends after 15 years implies average annual returns of less than 5%.

- Assuming the spreadsheets prove accurate, enjoying annual returns beyond 5% will require MTVW to buy additional properties and earn greater profits.

- The run-off sums can of course be fine tuned. For example, replacing the 48% realised gain on the Allsop valuation with the record 65% achieved during this H1 could lead to a potential £283 per share through dividends.

- The ordinary and special dividend in the meantime supply a trailing 725p per share income and support a 5.4% yield at a £135 share price.

- My spreadsheets suggest run-off dividends could start at £42m or £11 per share a year.

- Trailing twelve-month free cash flow before any property purchases, debt repayment and dividends is in fact £53m or £13 per share.

- Collecting £11 or £13 per share from dividends at a £135 share price would support an 8%-plus income — offset of course by MTVW paying out all of its free cash to shareholders…

- …and its property estate (and share price) then slowly dwindling to nothing.

Maynard Paton

Cannot find any estimate/allowance on how much it will cost Mountview to upgrade ALL their rentals to EPC C rating by 2025. As the fine could be up to £30,000 a property, surely this issue should be mentioned somewhere in the accounts??? Or have I got it wrong?

Hi Richard,

Thanks for the comment. Unlikely MTVW will freely divulge this information, as management has for years dodged questions at the AGM on the finer points of costs, tenants and valuations. I suspect this EPC upgrade cost will be bundled in with the usual property expenses and only if the cost is notable will MTVW explain the reason for the increase. Quoted companies are not obliged to disclose additional future costs unless the information is deemed ‘price sensitive’ — i.e. the information is likely to lead to a significant share-price movement. The extra expense could be spread over the next few years, so may not be material in any particular year. Do you know how much upgrading a property to EPC C costs?

Maynard

Quoting the Independent newspaper, Feb 22

“Aldermore Bank polled landlords asking how much they expected to spend on the renovations needed to get their properties up to scratch.

On average, they put the cost at around £10,400 per property to fund improvements such as cavity wall insulation, roof insulation and double glazing.

Just 7 per cent said they expect to spend less than £1,000, while more than a quarter think it will cost a minimum of £10,000 or more.”

Now remember, most if not all of Mountview’s properties are older, and so I think it will be £10,000 or more

Thanks Richard. 2021 annual report revealed 3,540 units, comprising: 1,898 regulated properties, 253 assured tenancies, 227 life tenancies and 1,162 freehold/leasehold ground units. 3,540*10k = £35m = £9/share cost perhaps spread over the next few years.

Maynard

I think the proposed up grades on EPC are going to be quite a game changer. There is a great deal of disquiet as you can presently rent out at EPC E, but to go up 2 grades to C can be very expensive, like insulating the internal walls or even external walls. It could be mission impossible for a lot of landlords. With house prices high, it certainly could be the time to cash out and begin the run off as you suggest

As MP states, MTVW usually sell their properties when the current tenancy ends rather than re-letting. In these circumstances the changes to EPC ratings will not affect Mountview until 2028 as the 2025 requirements will only apply when a new tenant enters the property.

Thanks Andrew. Good point about 2028. MTVW’s 2022 annual report says this about the EPC requirements:

“For example, on the horizon is the expected tightening of the energy performance certificate (EPC) requirements where the detailed requirements remain subject to further consultation before becoming law. Thus the CWG [Climate Working Group] has a current task to monitor the development of these requirements and prepare for the necessary operational and financial planning that will follow once the provisions are finalised.”

The report also notes:

“Our EPC ratings 91.4% passed or with valid exemptions; 6.6% currently having remedial works carried out and 2% not yet assessed due to access issues (including Covid-19 related matters)”

I am not sure what the EPC pass mark was.

Maynard