20 March 2019

By Maynard Paton

Results verdict on Mincon (MCON):

- Acceptable double-digit growth supported by encouraging organic sales and the purchase of Driconeq.

- New ‘Greenhammer’ product appears to offer attractive possibilities through “disruptive technology”.

- Year ahead to focus on consolidating operations after bumper orders created production constraints during 2017 and 2018. Recent trading not buoyant.

- Accounts offer scope for improvement as hefty stock build-up unwinds, capital expenditure falls and cost savings are found.

- The underlying P/E of 19 is not an obvious bargain. I continue to hold.

Contents

- Event link and share data

- Why I own MCON

- Results summary

- Revenue and profit

- Drill strings

- Greenhammer project

- Working capital

- Capital expenditure, cash and debt

- Margins and ROE

- Outlook

- Valuation

Event link and share data

Event: Final results for the twelve months to 31 December 2018 published 19 March 2019

Price: 105p

Shares in issue: 210,541,102

Market capitalisation: £221m

Why I own MCON

- Designs and manufactures industrial drill bits, with sales supported by established reputation, quality engineering, product patents and technical services.

- Boasts veteran family management with 42-year tenure, 57%/£126m shareholding and long-term perspective.

- Offers financials that include respectable margins, a cash-positive balance sheet and opportunities for greater efficiencies.

Further reading: My MCON Buy report | All my MCON posts

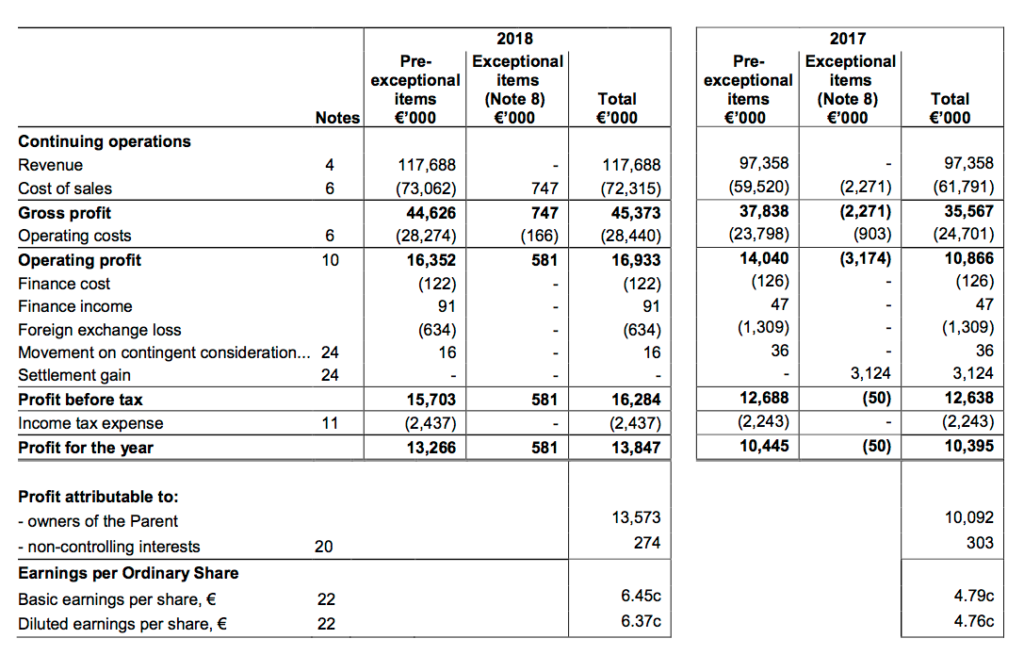

Results summary

Revenue and profit

- August’s interim figures and October’s Q3 update had already suggested MCON would report significant financial progress.

- In the event, total revenue gained 21% while operating profit before exceptional items advanced 16%.

- The purchase of Driconeq — a Swedish drill-pipe specialist — this time last year made MCON’s underlying growth harder to determine.

- The table below includes my best interpretation of Driconeq’s revenue contribution:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (own brand) (€k)* | 35,211 | 39,754 | 74,965 | 39,307 | 43,020 | 82,327 | |

| Revenue (third party) (€k) | 11,745 | 10,648 | 22,393 | 8,315 | 9,054 | 17,369 | |

| Revenue (Driconeq) (€k)* | - | - | - | 8,099 | 9,893 | 17,992 | |

| Revenue (total) (€k) | 46,956 | 50,402 | 97,358 | 55,721 | 61,967 | 117,688 | |

| Operating profit (€k) | 6,789 | 7,251 | 14,040 | 8,087 | 8,265 | 16,352 | |

| Exceptional costs (€k) | (3,047) | (127) | (3,174) | (298) | 879 | 581 |

(*estimated)

- I am not sure my Driconeq sums are correct. First-half sales of €8m reflect only the first three months post-acquisition, while second-half sales of €10m represent a full six-month contribution.

- MCON had initially claimed Driconeq would create extra sales of €21m during 2018.

- Nevertheless, my table does show (estimated) 2018 revenue from own-brand products gaining 10% — which matches the comments given by the chief executive.

- Reading between the lines, I am not sure Driconeq has performed as well as expected (my bold).

“Driconeq represents good value for the Group, but it has taken some work, which will continue into 2019. Overall, we are happy with the businesses, their teams, the trading and the additions to the product line-up.”

- At least the overall results set new revenue, profit and dividend highs:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (€k) | 54,544 | 70,266 | 76,181 | 97,358 | 117,688 |

| Operating profit (€k) | 10,350 | 9,990 | 10,178 | 14,040 | 16,352 |

| Exceptional charges (€k) | - | - | - | (3,174) | (166) |

| Exceptional gains (€k) | - | - | - | 3,124 | 747 |

| Discontinued operations (€k) | - | - | - | - | - |

| Other items (€k) | 364 | (481) | 1,125 | (1,273) | (618) |

| Finance income (€k) | 535 | 114 | 30 | (79) | (31) |

| Pre-tax profit (€k) | 11,249 | 9,623 | 11,333 | 12,638 | 16,284 |

| Earnings per share (c) | 4.34 | 3.79 | 4.39 | 4.79 | 6.45 |

| Dividend per share (c) | 2.00 | 2.00 | 2.00 | 2.05 | 2.10 |

- The final dividend was maintained at €0.0105 per share, which left the full-year payout 2.4% higher. The dividend announcement was hidden within notes 21 and 30 of the accompanying accounts.

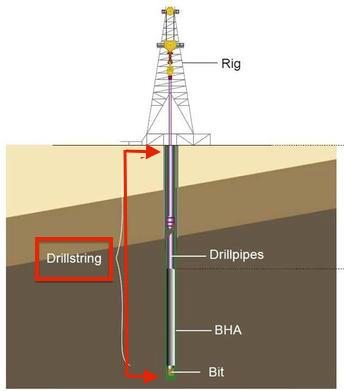

Drill strings

- These results were the first in which I noticed the term “drill string”.

- A drill string combines a drill pipe, a bottom hole assembly and any other tools used to make the drill bit turn correctly.

- MCON has traditionally developed and made industrial drill bits.

- Driconeq and some previous acquisitions manufacture drill pipes. These results explained the strategy to develop other drill parts (my bold):

“In recent years we have set out to assemble the full range of the drill string for different types of mining and construction piling. This provides us with the opportunity to deliver a full-service offering to end customers, as we now design and manufacture the key elements in the drill string.

We are differentiating ourselves from the less developed businesses in low margin activities in the sector, and we are positioning ourselves to deal directly with end customers and to win large contracts.”

“Going forward we plan to… seek long-term partnerships and multi-year contracts with end customers incorporating direct delivery to their sites.”

- MCON appears to sell its drill bits to intermediaries, who in turn seemingly supply the end customer with the full drill string. I had always assumed MCON sold direct to the end customer.

- Driconeq’s drill pipes are not as profitable as drill bits. These results claimed Driconeq’s gross margin was 23% versus 40% for the ‘core’ group.

- Driconeq was acquired for €7.8m, incurred further transaction costs of €166k and contributed earnings of €396k during the nine months of ownership.

- Driconeq’s contribution ought to improve during 2019:

“We do not expect acquisitions to add much to profitability in their first year due to acquisition and transition costs, but we expect to improve the gross and net margins in the full year coming”

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Greenhammer project

- Comments about MCON’s ‘Greenhammer’ project appeared encouraging (my bold):

“We believe we are moving towards the commercialisation phase of the hydraulic hammer systems (or “Greenhammer” systems) in 2019.

The system on the rig, prior to the drill string being added, weighs about eight tonnes, and eleven tonnes when the full drill string is added. This is not a small system or easily replicable, and we have placed patents around the system to protect it.

The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.

It is a disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base, and there is growing interest from other potential customers with the problems that this technology can address, such as hard rock, and high-altitude drilling.

It is the current embodiment of our challenger brand strategy.”

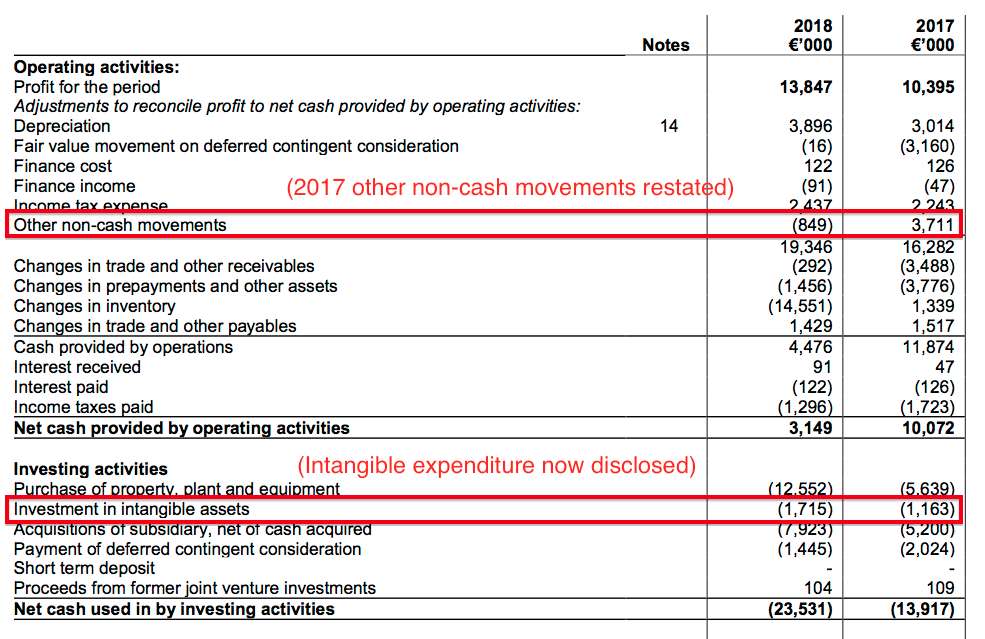

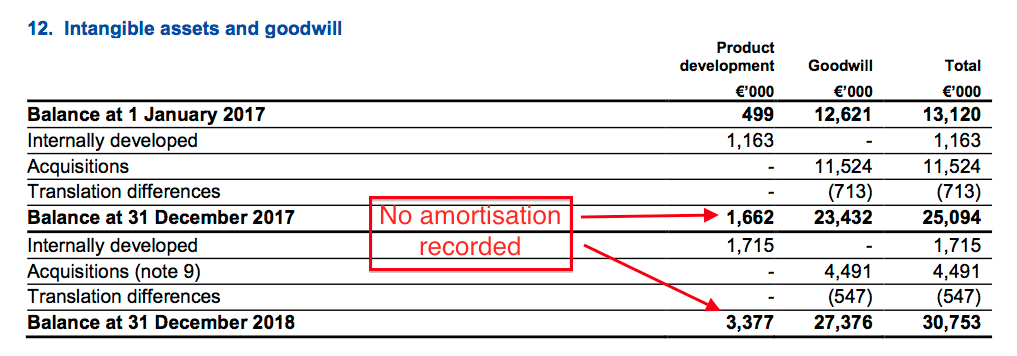

- Greenhammer has been seven years in the making and to date has involved capitalised development costs of €3.4m, of which €0.7m was capitalised during H1 and €1.0m capitalised during H2.

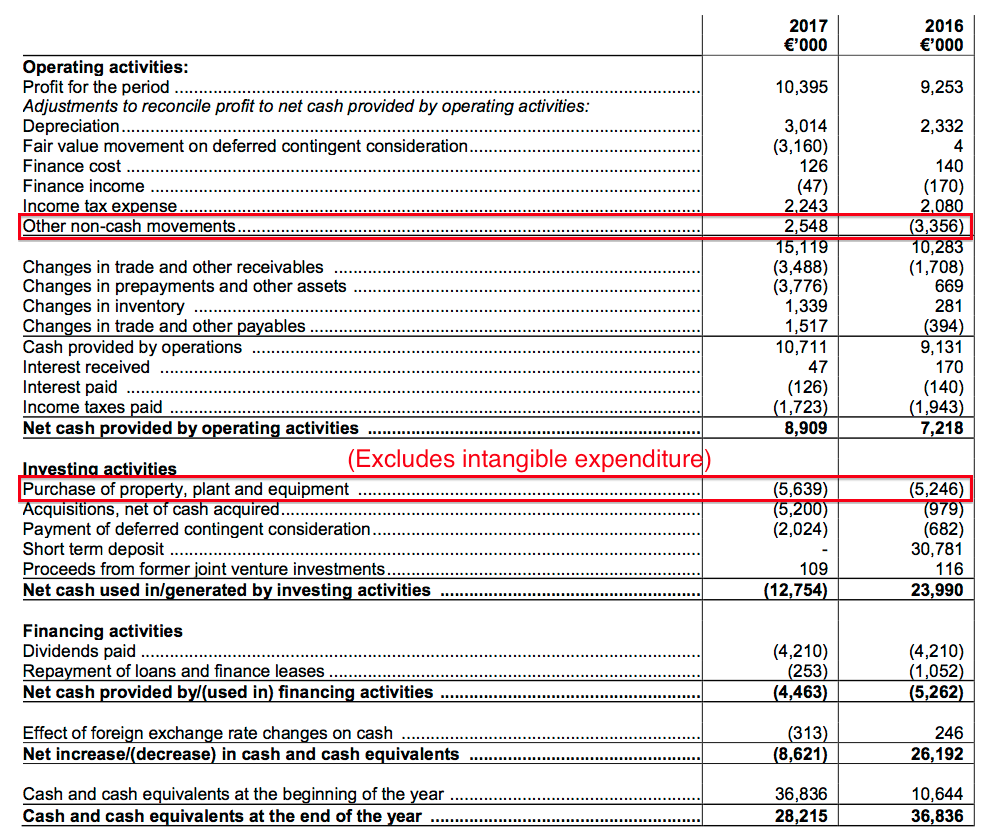

- These results revealed exactly where the Greenhammer development costs reside within the cash flow statement.

- Previous statements had not declared any intangible expenditure, and I assumed such costs were lumped in with ‘other non-cash movements’:

- My assumption was correct. ‘Investments in intangible assets’ have been introduced for 2018 and the prior year’s ‘other non-cash movements’ have been restated accordingly:

- Amortisation has yet to commence against the capitalised expenditure:

Working capital

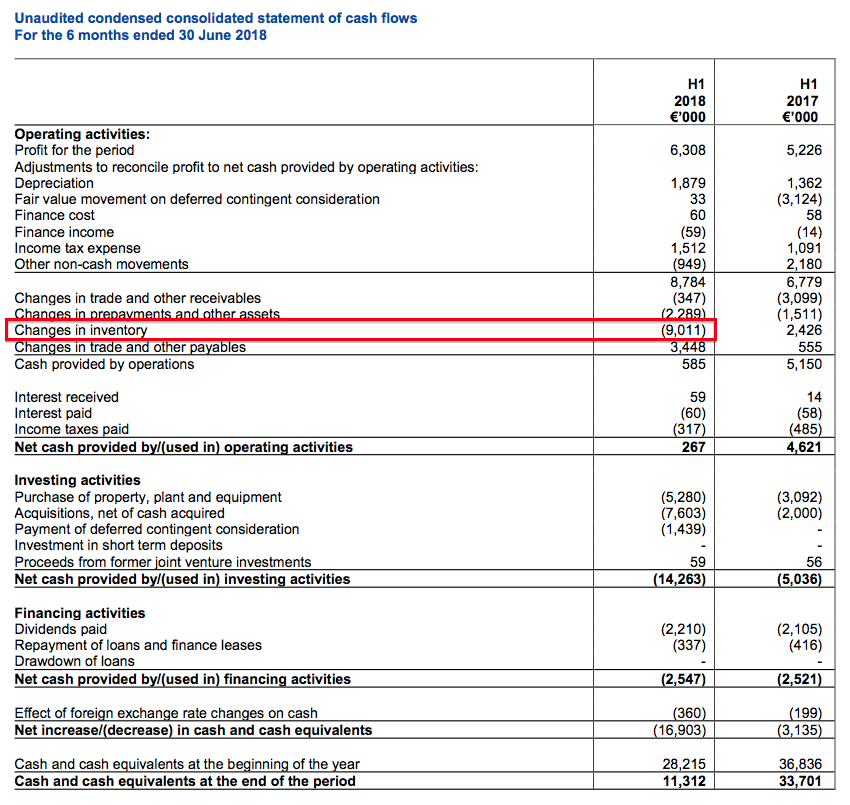

- MCON’s first-half cash flow had already showed a €9m “inventory swell”:

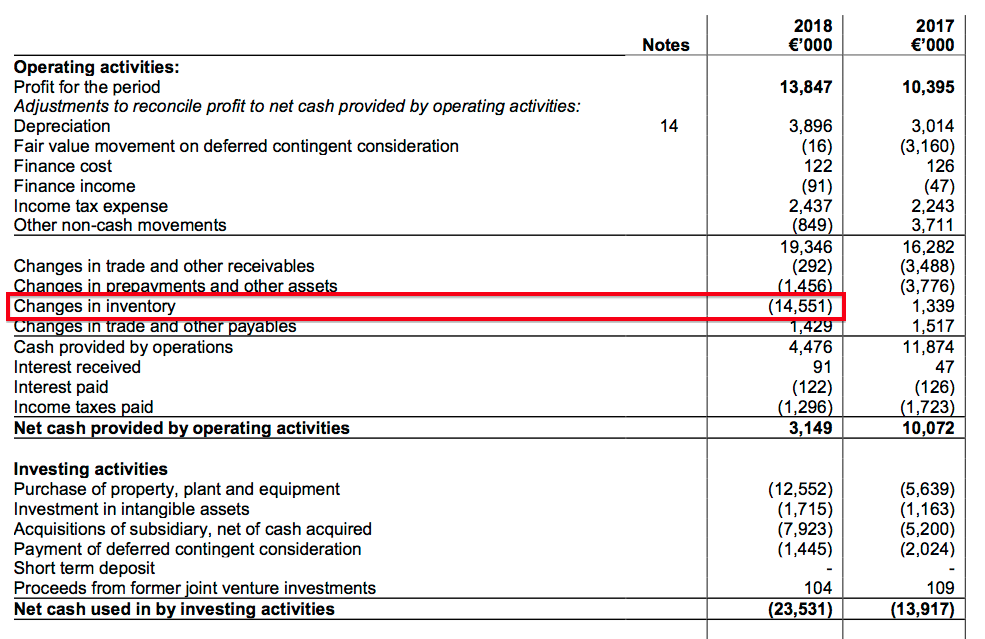

- This full-year statement revealed stock levels had increased by a further €5.5m:

- MCON gave three reasons for the substantial stock build-up:

- The placing of Driconeq products throughout the group’s distribution network;

- Advance orders of raw materials to ensure reliable supplies and to avoid price increases, and;

- Delivery backlogs due to customer demand exceeding manufacturing capacity during 2017 and 2018.

- At €49m, year-end stock levels represented a huge 42% of revenue.

- MCON’s stock-turn history is shown below:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Stock turn (days) | 276 | 263 | 269 | 206 | 203 |

Note: Stock turn = (average stock held / cost of sales) * 365 days

- Stock in the factory and warehouses is now held on average for six months rather than the nine months seen during 2014.

- MCON reckons approximately €10m could be released from working capital during 2019:

“In the coming year we intend to realise all of the €2.3 million tied up in rigs, to reduce raw material inventory by approximately €4 million, and depending on the sales level, reduce the work in progress and finished goods inventory by, perhaps €4 million. We will review this plan through the year as we unwind the working capital.”

- MCON may always carry relatively high stock levels because such levels could support a competitive advantage.

- The group’s flotation document cited “customers now demand effective service, spare parts and consumables” and “stock availability in remote locations enhance[s] Mincon’s reputation in the marketplace.”

Capital expenditure, cash and debt

- Capital expenditure was €7m during H2 to total almost €13m during the year.

- MCON explained:

“We substantially completed the build out of the factories during the year, and capital equipment has been installed and commissioned in our factories through the period. The heat treatment plants, exceeding some €5 million in total investment were commissioned over the year end period and they should facilitate the delivery of consistent quality in our products across our key factories…”

- At least capex is set to reduce to the c€4m depreciation charge for 2019:

“We are planning that our capital expenditure in the coming years will be in the region of our depreciation charge for the maintenance of our current production and product ranges.”

- The total cost of the hefty capex, the substantial stock investment, the Driconeq acquisition, the notable Greenhammer expenditure and the dividend came to €40m.

- Of that €40m, €14m was funded by earnings, €5m funded by extra debt, €1m funded by other cash movements and the remaining €20m funded by cash in the bank.

- Cash in the bank therefore dropped from €28m to €8m, while debt advanced from €2m to €7m. Net cash ended the year at just €1m — excluding €5m earmarked for possible acquisition earn-outs.

- The following table puts the working-capital movements and capex into perspective:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (€k) | 10,350 | 9,990 | 10,178 | 14,040 | 16,352 |

| Depreciation and amortisation (€k) | 2,053 | 2,346 | 2,332 | 3,014 | 3,896 |

| Net capital expenditure (€k) | (1,750) | (1,768) | (5,246) | (5,639) | (12,552) |

| Working-capital movements (€k) | (6,503) | (2,837) | (1,152) | (4,408) | (14,870) |

| Net cash (€k) | 41,754 | 38,610 | 34,960 | 26,142 | 846 |

- Of MCON’s €61m aggregate operating profit from 2014 to 2018, an enormous €30m was absorbed into working capital.

- During the same five years, total capital expenditure has been double the total depreciation charged against earnings.

- Five years ago MCON raised €47m through its flotation. Those proceeds have now all been spent.

Margins and ROE

- MCON’s operating margin and return on equity (ROE) remain reasonable but not spectacular:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating margin (%) | 19.0 | 14.2 | 13.4 | 14.4 | 13.9 |

| Return on average equity* (%) | 18.6 | 12.7 | 13.0 | 12.6 | 12.6 |

(*adjusted for net cash and deferred considerations)

- MCON said the operating margin excluding Driconeq was 15.2%.

- Margins may have scope to increase. MCON claimed:

“We plan to review the overheads that we have built up with a view to improving efficiency across the Group.”

- ROE could improve if/when the aforementioned stock levels reduce and/or when the aforementioned recent capex generates a suitable return. Stock and property, plant and equipment represented a significant 72% of the year-end balance sheet.

- MCON admitted:

“We have yet to see the expected returns on some of these investments. We understand that we have to increase revenue and improve the returns on these investments. We have made the investments, and, in the coming year, we expect to build out the income streams.”

- MCON carries no pension obligations.

Outlook

- MCON anticipates growth will pause during 2019 (my bold):

“We have ramped up overheads over the last two years, much of it necessary as part of the Group build-out and through our acquisitions, and we will spend much of 2019 consolidating our operations, reducing our overheads and moving strongly back into cash generation.”

- Current trading does not appear buoyant:

“Trading in the new year to date has been fitful and flat.”

- This time last year, MCON claimed 2017 had looked “very much like the first [year] of the current upturn”.

- MCON did not say whether its customers continue to enjoy an upturn while the group consolidates its acquisitions.

Valuation

- MCON’s €16.4m operating profit for 2018 translates into £14.0m at £1:€1.17.

- Taxed at the 15.5% rate applied in these results gives earnings of £11.8m or 5.6p per share.

- Adjust the £221m market cap for the net cash and potential acquisition earn-outs, and the P/E is approximately 19.

- No adjustment has been made for the capitalised Greenhammer expenditure.

- The 19x multiple may be justified if:

- Organic sales growth can continue at 10%;

- Margins improve as overheads are reduced, and/or;

- Capital is released from stock and leads to a greater ROE.

- The trailing €0.021 per share dividend equates to 1.79p per share and supplies a 1.7% yield (before Irish withholding taxes for UK-resident investors).

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Mincon.

Mincon (MCON)

Publication of 2018 annual report

MCON’s annual reports provide a very different management narrative to that published within the preliminary results RNSs.

Although parts of the chief exec’s RNS commentary are contained in the annual report, many parts are completely re-written and some parts are dropped entirely. For instance, the outlook section given in the 2018 results RNS was not reproduced within this annual report.

Nonetheless, the management text within this annual report read very well. Management appears to be concentrating on developing better products, creating a wider competitive advantage and running the business with a long-term mindset.

Here are the snippets of interest:

1) Chairman’s and chief exec’s statements

The key points:

* Improving the group’s financial returns (my bold):

“It is good that we have continued to build profitability, now we will focus on increasing the return on capital employed, on the cash growth and on the efficiency of our manufacturing and distribution base. These are among the objectives the Board has set for the Executive in 2019.”

…

“The Executive has installed the additional factory capacity as planned, and the factories are meeting the order books without undue delays. We are now seeking increases in efficiency, savings in overhead spend, increased return on our investment, in our sales expenditure, and in cash allocation to prioritise the reward for all our stakeholders.”

…

“Over the last few years we have doubled our size and more, but there is no gain in this if the earnings don’t follow. While we now have a stronger market position and offer a wider range of excellent products, this market position must translate into better profitability and a better return on this investment.”

…

“We are embracing a regime of continuous development, of continuous improvement in the service delivery, and new ways to enable our customers to achieve the same objectives as we seek ourselves; capital efficiency, better safety, improved environmental protection, higher return on capital employed and better cash flow for investment and for stakeholders.”

* developing a competitive advantage — product design and customer service (my bold):

“The Group’s overall strategic objective is to develop long term sustainable competitive advantage with our products and services for customers, for the benefit of our shareholders and all stakeholders.”

…

“We are committed to:

*better engineering

*the creation of intellectual property at the core of our products, supporter inter alia by patents

*better service delivery,

*and improving the skill sets of our teams”

…

“We put engineering at the core of what we do, and high quality products and customer service at the centre of our offering. It is our belief that the building up of our intellectual property, the increased quality of our manufacturing, and the investment in our service is a combination that protects and develops our products, our people and our margins.”

…

“Our out-sourcing, and third party manufacturing is minimal. This gives us substantial control over the quality of what we manufacture but more importantly it means that the compound intellectual property of our products resides in-house. This has been key in the development of the next generation of products outlined below.”

…

“If we do not work to make our current range of products redundant by developing new, better products, we can rely on our competitors to do this. If we don’t renew our channels to market, and play our part in accepting the way our customers wish to develop their requirements then we will be superseded. If we copy what the market structure already is, we will fail, as we will have embraced the existing structures without the market advantages of the leaders. Not only do we have to continue to develop our own range of current products, but we have to plot their replacement by newer technologies and newer delivery systems.”

…

“We have found that the intellectual property of our business is as much in the service of our customer at the mine or construction site, as it is in the performance of our product designs, or the quality of our manufacturing processes.”

…

“We are working to find a balance, and we are prepared to take a longer view of our business rather than chase growth for the sake of growth.”

…

“As owners we believe that long-term sustainability will remain a key priority for Mincon’s business, and consequently our engineering efforts and global growth. Mincon is building a business for the future by recruiting and nurturing new engineering talent; developing its existing service and manufacturing centres; diversifying its product range; and expanding market presence.”

…

“Mincon has had a clear vision and determined focus giving priority towards:

* Highest design specifications

* Best manufacturing methods and processes

* Delivery of superior products to our customers”

…

(I like the quote “If we do not work to make our current range of products redundant by developing new, better products, we can rely on our competitors to do this”. Seems as if management has the required paranoia to avoid complacency).

* Products, product range and becoming a challenger brand (my bold):

“Mincon’s primary engineering objective is to design and manufacture class-leading and highly efficient drilling consumable tools that use less energy per metre of drilling. Rock drilling is an energy-intensive undertaking, with efficiency being measured in the speed of drilling; the life of consumables; and the reliability of equipment.”

…

“In building up the Group in recent years, and in assembling the drill string offering, the team in the Mincon Group has concluded that there is a world of difference between offering the products in a catalogue, even an on-line catalogue, and engaging directly with the end customers on their specific requirements to achieve their objectives.”

…

“We have assembled and now present the entire drill string as a sales offering, with a range of sizes and product types that address a wider range of markets, directed at the surface drilling customer. With a full range of drilling consumables we can meet the requirements of our larger customers, and through joint partnerships with these end users, savings will accrue on both sides. This positions us as a challenger brand in the mid-market, and away from the more commoditised low end business.”

…

“Our business has to play its part in being environmentally aware, in minimising the energy that the products use, in reducing ground disturbance in sensitive and high population density sites, and in matching our customers ambition for efficiency. We see this as a challenge to be met, not a burden to be endured, and it is this opportunity to rethink and renew the industries that we serve that characterises the challenger mentality we are adopting.”

2) Competition

Mincon helpfully named its main competitors (my bold):

“The markets for the Group’s products are highly competitive in terms of pricing, product design, service and quality, the timing and development and introduction of new products, customer services and terms of financing. The Group faces intense competition from significant competitors and to a lesser extent small regional companies.”

“The Group’s principle competitors are Epiroc which is headquartered in Stockholm, Sweden with a global reach spanning more than 170 countries and Sandvik which is also headquartered in Stockholm, Sweden with business activities in more than 130 countries.”

3) Customer concentration

The report suggested Mincon is not dependent on a handful of clients:

“During 2018, the Group’s top ten customers have accounted for approximately 21% of its revenues.”

The 2017 report said the group’s top ten customers had accounted for approximately 24% of group revenue over the past three years.

4) Risks

The report included a new Brexit risk:

“Implications in relation to Brexit

The Group has a carbide manufacturing facility in the UK, along with a sales and distribution centre selling all our major manufacturing components and some third party product. The Group envisages minimal impact from Brexit in the coming year. The Group’s revenue that was generated in the UK during 2018 was €3.3 million.”

5) Driconeq

Confirmation that the integration of Driconeq was indeed not straightforward (my bold):

“Driconeq was a difficult acquisition, geographically spread, marginally profitable, with a subsidiary in administration, and it consequently required very significant senior management time, but it has bedded in well and we believe that it meet all our expectations for it.”

6) Mincon Nordic

Parts of the group are not profitable and have scope to improve the group’s total margin (my bold):

“Our Mincon Nordic business grew very significantly in 2018, and while still marginally loss making, it is becoming a formidable competitor in that market. The competitive response in the region has been robust, if uncommercial, but it is breaking their business and will prove to be short term. We will continue to build our sales in the region as we are in this market for the long term, and may continue to make investments in the territory.”

The 2017 annual report (point 2) indicated Mincon Nordic had the objective of breaking even during 2018.

7) Cash flow

Confirmation that the significant 2018 cash investment in working capital and capital expenditure is not expected to be repeated for 2019 (my bold):

“The capital investment and inventory investment took a heavy toll of our cash flow in 2018, with the improved cash inflow being met by a significant inventory increase and capital expenditure build out. However we have passed peak investment and expenditure related to these categories and through 2019 should see the outflows reverse.”

In fact, capex could reduce to below the depreciation charge during the next three years (my bold):

“Capital expenditure is expected to run at or below depreciation in the coming three year cycle unless we see the type of growth that we achieved in the last three years or unless we decide building a new factory makes sense. We will flag that some months in advance if we do, otherwise the plan for 2019 is to return to cash generation as we stabilise our growth.”

8) Review phase

The results RNS mentioned the business pausing for breath following a few years of rapid growth. The following text suggests the acquisitions made since the flotation may have brought with them products that are not as lucrative as others within the group:

“At the same time we will review our product portfolio and decide on the basis of margins and scale, which products, customers and markets are worth the investment and risk, and which are not. We are fully in favour of growth, but we feel it should be deliberate, commercial and valuable to the Group.”

9) Corporate governance

New AIM rules introduced last year have prompted MCON to include a new corporate governance section.

Most of the text is very ‘boilerplate’ but two items stood out (my bold):

“The Mincon Group plc has decided to deliver considerable detail on the operations and trading on a quarterly basis to the shareholders and market, beyond what is required just for compliance, and at a level of detail committed to providing insight on the thinking, the strategy, and the allocation of the assets and people. In addition to this, shareholders are actively encouraged to visit key sites, meet key people and discuss the business of the Group.”

MCON’s quarterly updates are commendable, but could lead to short-term decision making (by investors and management).

Having the chief exec know all about the products is encouraging (my bold):

“The current CEO is the chief engineer and is the principal designer of the current range of products.”

That said, being chief exec and “principal designer” could be too much for one person.

Within the chief exec’s statement, the chief exec wrote: (my bold):

“Our primary engineering objective will be driven by our engineering leadership, the Technology Steering Group. This group of five is led by myself (chief executive Joseph Purcell) and is made up of senior engineers who each have many decades of experience in the rock drilling industry. The experience in the group is very broad and includes the areas of mechanical design and simulation; metallurgy and heat treatment; market and application knowledge; and hands-on drilling. The function of the group is to develop the next generation of engineering leaders and to liaise with all levels of the Mincon Group, including the customer service centres, so that it can analyse customer feedback, and prioritise areas for technology development.”

The ‘principal designer’ of future products may well be one of the “next generation engineering leaders”.

10) Director pay

The chief exec’s basic pay gained 12% — perhaps not surprising given underlying operating profit advanced 16%. €300k is equivalent to £261k and does not seem outlandish given the profitability of the business:

The sales director’s pay is denominated in USD and I suspect his 22% EUR pay rise is due mostly to currency fluctuations. His basic pay fell from €207k for 2016 to €201k for 2017.

The executives have commendably not collected any bonuses since the 2013 flotation. I do get the impression the executives — with a 56% combined family shareholding — are aligned to ordinary shareholders.

11) New accounting standards

No major impact from the new IFRSs:

The effect from IFRS 16 Leases is small:

12) Employees

I am sure the Driconeq acquisition has dampened my employee ratios:

Revenue per employee dropped from €300k to €229k, which is still reasonable but is the lowest since my records start at 2010 (prior lowest was €256k during 2016).

The average employee cost €64k, down from €73k during 2017 and in line with the €64k seen during 2015 and 2016.

Employee costs as a proportion of revenue advanced from 24.2% to 28.1% during 2018 — the proportion is now the highest since 2010 (previous high was 25.2% during 2016).

No wonder revenue per head was not mentioned in this annual report (the ratio was mentioned in the 2017 edition (point 2)).

13) Inventory

As mentioned in the Blog post above, year-end stock levels represented a huge 42% of revenue:

MCON aims to reduce the level for 2019.

14) Trade receivables

Year-end trade receivables encouragingly represented 18% of revenue — matching the level for 2017 and the lowest since 2013 (16%).

70% of trade receivables were less than 60 days old — in line with 65%-76% range seen during the last five years.

I suppose within its forthcoming efficiency drive, MCON could do with asking customers to pay a little quicker.

15) Land and buildings

Part of the sizeable capex spend was on land and buildings:

Of the €27m capex spent between 2014 and 2018, €8m has been on land and buildings. Total depreciation during the same time was €14m — so not entirely covering the €19m capex spent on plant, equipment etc.

16) Share options

Options represent a modest 1.1% of the share count:

Maynard

Mincon (MCON)

Q1 Trading Update published 25 April 2019

Nothing too surprising was revealed within this rather long-winded update following the 2018 results RNS and the extra management narrative within annual report. My comments are interspersed within the full text:

———————————————————————————————————

Key elements (comparison of Q1, 2019 to Q1, 2018):

Continued improvement in our product sales mix:

· Mincon manufactured product sales up 30%

· Being organic growth of c. 4% and

· Acquisition growth of 26%

· Third party product sales down 5%

Resulting in:

· Revenue up 24% overall

· Profitability slightly behind last year in Q1

We continue our strategy of improving our product mix by manufacturing what we sell, where this provides commercial advantage. This has resulted in Mincon product representing 86% of sales in the quarter compared to 81% last year and in the period under review our manufacturing capability has now built to a level where we are able to meet customer orders in a normal commercial timeframe. This allows us to focus on the efficiency of delivery and margins, and to reduce the extra overhead that had come into place to meet the last phase of growth, before we meet the service requirements of the new direct sales coming on stream through the rest of the year.

———————————————————————————————————

This follows MCON’s plan for a ‘year of consolidation’ — organic sales up 4% does not sound great but is positive at least.

Profitability “slightly behind” may be due to the upfront costs of becoming a ‘challenger’ brand (see below).

———————————————————————————————————

Revenue

In the quarter the Group caught up with the order book, is current with its orders, and has additional capacity available in the production facilities of certainly 10% to 20% even at the new levels of throughput.

The heat treatment facilities are now coming on stream in Benton, Illinois this month after a successful series of commissioning throughput, and are expected to come on-line in Perth, Australia in June/July this year. The additional vacuum furnace capacity has been commissioned in the Marshalls Carbide plant, and the final furnace arrives in Shannon in July. These capital commitments extend back several years in some cases, and in the last year new plant and equipment capital commitments are running well below the depreciation run rate of c. €4m a year.

Factories are, in the main, well specified now for the product range and sales level. In the first quarter we continued to reduce our inventory of rigs, with the later ones getting sold at cost less commission and a degree of refurbishment, certainly above the written down value they were held in prior to the year end. We had eleven rigs, and we have sold six in the last few months. This was an important objective, and to some degree it suggests we are reasonably well into the mining recovery flagged two years ago.

———————————————————————————————————

Good to hear:

* capacity can handle another 10%-plus production increase

* capex commitments running below depreciation after some years of at higher levels, and

* those difficult-to-shift rigs are being sold above book.

———————————————————————————————————

The Challenger brand

We found, as we completed our drill string build out, and extended our ranges of hammers and bits, that we began to be able to compete in supplying complete drill consumable solutions directly to mines. As we build out our revenue in construction piling, we find that the natural shape of the business is higher value contracts extending over a number of years. The investment in our engineers and engineering, together with the experience of drilling held by key service team members, means we can advise on the consumables solutions for the end customers.

This is a relatively new business structure for us, but it both fits with the ambition to build out relationships with the end-customers, and with the engineering philosophy in the Group. We have to offer better value, whether it is the service commitment, the engineering, the pricing or, as we find, a combination of all three. Dealing directly with the end customers allows us to create the breadth in relationship that positions the Group as a reliable element of the construction or mining process.

We have to be reliable. So much of what we do is at the start of the processes, whether it is delivering the ore tonnage, or the piling that supports buildings and harbours, that the fault tolerance of the end customers is low, and the potential liabilities higher than simply replacing a hammer or a bit. We are getting much deeper into the service element. This dependence by customers on our service and engineering means that we also have to keep the requisite inventory near the contract site, and service individuals proximate to the service delivery. This is an emerging model for us, and each contract requires people, investment, service-guarantees and time.

We have recently won multi-million dollar business in Chesapeake Virginia, in Indonesia, in Chile, and in Finland which are not reflected in this growth as yet to any degree. These will require some restructuring and build out in the Group to support the end customers, incur some initiation and front-end costs, and this is causing a rethink of our management structure to lean towards a regional footprint, mapping the thinking behind the investment in the key factories in the Americas, Australasia/Asia Pacific (APAC) and EMEA (Europe Middle East Africa)

———————————————————————————————————

The ‘challenger brand’ approach — which seems a very credible long-term plan — would appear to require upfront costs, which might help explain the lower Q1 profitability.

———————————————————————————————————

Gross margin

Gross margin was at about the budgeted level considering the expected product mix changes, at 35%, as this includes a full quarter of the lower margin Driconeq Group in Q1, 2019, and nothing from this acquisition in the previous year. The drill pipe business (excluding their profitable heat treatment activity) has a gross margin of c. 20%, and the turnover is about a sixth of our revenue. It’s a good acquisition and a good team, and there is additional margin to play for in the supply costs side of the business in phase 2 of the on-boarding. Overall in the Group we can comfortably produce what we couldn’t deliver a year ago, and our eyes are inward now on overhead reduction, factory efficiency, and the realisation of assets and disposal of businesses that don’t sit with the current three year plan.

———————————————————————————————————

“Phase 2 of the on-boarding” reads as if the Driconeq integration has not yet been entirely completed.

A 20% gross margin from 1/6th of revenue is useful to know for future results comparisons.

———————————————————————————————————

Group review and streamlining

We have developed a complex business model over the last few years as we added factories, customer service centres and products, organically and through acquisition.

We have decided to overhaul the Group, reduce the overhead by a targeted €3 million a year, and reorganize on a regional basis into three zones; Americas, EMEA, and Australasia/Asia Pacific. This will cost some money, take some time, but we have already reduced overhead by a run rate of €1 million a year since the recent budgeting and review planning. It is our expectation that the reduction in expenses will become self-financing in the current year and provide the service level and response needed to support the positioning of the Group and the brand as a challenger to the incumbent market structure.

Initially this will not substantially disrupt the Group, but develop the reporting structure, and increasingly as the other Group reviews take place from the operational side, we will be making decisions through 2019 on what we make and where we make it. We have flagged this before. Since we expect low margin, less engineered products to come increasingly under pressure in an interconnected world, Mincon Group is repositioning with the full consumables offering and a higher service element, directly to the larger end customers. We aim to combine this with product systems that are more fuel efficient, offer better value in use overall and are more environmentally friendly.

———————————————————————————————————

Savings of €3m per annum are significant when 2018 operating profit was €16m. The text confirmed the annual report narrative that certain less-profitable products may be sidelined.

———————————————————————————————————

The Greenhammer hydraulic systems

We expected the system to go back into the beta testing on site in Australia in March, but the mine was evacuated for the first time in nine years as cyclone Veronica blew through Western Australia. In consequence the mine suffered flooding and the production schedules were severely disrupted. The rigs had to go back into full production to catch up on the ore shortfall , and we now expect to be back on site in May. We have spent the time improving the system in accordance with our own testing and constant development, and we are ready to re-engage the system when the rig comes off-line.

The smaller size system is also available, and we continue to develop the thinking and engineering around different applications and hammer types to continue to increase the addressable market for the system suites.

———————————————————————————————————

No further developments.

———————————————————————————————————

Market comment

We have seen the quarter deliver increased revenue with only moderate profit movement, and the growth is mostly from the addition of a distributor, and the additional quarter of the Driconeq Group, both lower margin activities. We have seen the full quarter impact of the overhead build out while the business growth in the direct model will be realised through the coming months and years.

Our manufacturing and delivery, which has been an issue for the last two years, has caught up with our sales growth, and now that we can deliver in accordance with the customer requirements, we can focus on the efficiency of our factories and the value from our customer centres. Other than that, we have to take each new direct customer opportunity as a separate project, and make sure that we engage cross-functionally to meet the service requirements while earning a return commensurate with the investment and risks.

———————————————————————————————————

Nothing was said about the wider demand for MCON’s products.

As MCON has noted, the year ahead is one of consolidation and re-jigging the business structure to accommodate dealing direct with end-customers.

The prospects for the rest of 2019 would therefore seem subdued.

Maynard