03 November 2015

By Maynard Paton

Quick update on Getech (GTC).

Event: Final results published 03 November

Summary: Oh dear — a profit warning for 2016. So much for management’s optimism from just a few months ago! The oil-sector downturn has also created extra guesswork with GTC’s valuation, while I remain concerned about the firm’s hefty development expenditure. Nevertheless, I believe GTC’s range of specialist data and services, alongside an asset-rich balance sheet, should see the firm through the difficulties. I continue to hold.

Price: 40p

Shares in issue: 32,895,748

Market capitalisation: £13.1m

Click here for all my previous GTC posts

Results:

My thoughts:

* The results were no surprise…

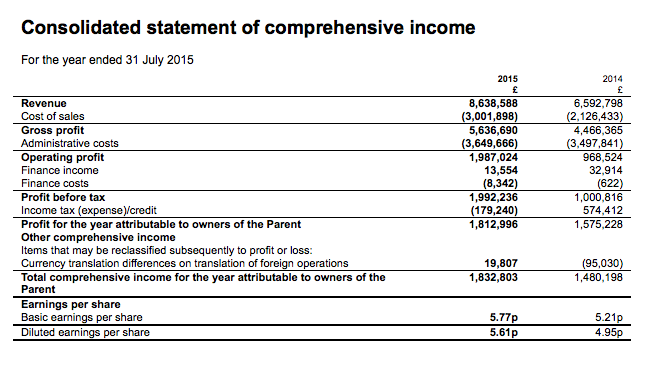

An update during August had already indicated that revenue would be £8.5m and pre-tax profit would be £2.0m.

The figures confirmed GTC’s second-half was much better than its first:

| H1 2014 | H2 2014 | FY 2014 | H1 2015 | H2 2015 | FY 2015 | ||

| Revenue (£k) | 3,110 | 3,483 | 6,593 | 3,619 | 5,020 | 8,639 | |

| Operating profit (£k) | 218 | 751 | 969 | 703 | 1,284 | 1,987 |

The only number that did not improve in the second half was the dividend. After the first-half payout was raised by 0.02p to 0.46p per share, the final payout for the year was trimmed by the same 0.02p to 1.74p per share.

* …but the board has suddenly become much less optimistic :-(

Back in August — and despite the firm serving clients operating in the battered oil sector — GTC’s managers appeared quite upbeat. At the time they said:

“We are increasingly confident about the prospects for 2016 as a number of significant discussions have already, at the request of our clients, been aimed at inclusion of Getech products in their 2016 budgets.”

However, today’s statement owned up to the effect of the oil-price downturn (my bold):

“At the same time, the deep cuts to staffing in many companies, including the international oil companies (IOCs) and large US independents, mean that their capability to undertake exploration is severely curtailed… In the short-term there remains considerable uncertainty about the state of the market and its impact on our trading and accordingly we believe the year ahead will be trading substantially below current market expectations.”

At least the board continued to be positive about the longer term:

“While there remains significant uncertainty about the short term and we cannot predict how the market will develop during 2016, we remain convinced that our products and staff are well regarded and satisfy a clear industry need. As such, whilst we anticipate a slow start to 2016, we remain confident about the long-term prospects for the extended Getech Group.”

* Few hard facts about the performance of ERCL

GTC bought fellow geosciences consultancy ERCL during April. The £4.3m price-tag exceeded GTC’s annual profits and so prompted me to raise an ‘amber acquisition alert’.

I must admit I was disappointed by GTC’s description of the financial performance of ERCL post-acquisition. The commentary was limited to just this:

“The acquisition of ERCL in April 2015 contributed to our growth in the year.”

Anyway, a look at the accounts reveals some interesting numbers relating to ERCL.

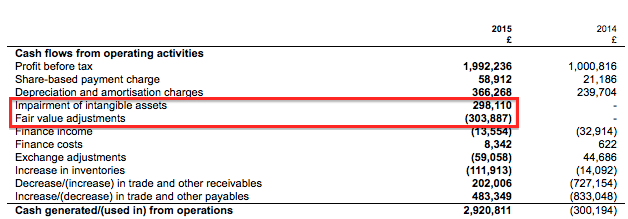

First up is the initial cash payment to buy the business. The original acquisition announcement referred to £1.75m, but the cash flow statement reveals a net £1.13m. So it appears as if ERCL came with a useful cash hoard of £0.62m:

Second, the deferred earn-out. The original acquisition announcement stated £1.55m, but the balance sheet shows a non-current trade payable of £980k. I get the impression that this £980k represents the earn-out, which suggests profits at ERCL may not be as high as originally expected:

Third, the cash flow statement records a £298k intangible write-off and a somewhat mysterious £304k fair value adjustment. To me, these look to be post-acquisition adjustments — the net effect of which is insignificant. But closer inspection of these two entries is required, just in case something else is afoot:

Due to be published next week, the 2015 annual report ought to confirm how much ERCL contributed after purchase and what exactly the numbers above represent.

* Hefty expenditure on intangible assets

GTC’s interims from March revealed the business capitalising a substantial £482k of development costs onto its balance sheet.

The full-year figures showed a further £495k of development costs side-stepping the income statement, alongside a further £128k spent on intangibles:

Despite this £1m-plus of development and intangible expenditure representing half of the £2m accounting profit, GTC did not make clear what all the expenditure related to.

Quotes from the results statement suggest the expenditure concerns enhancements to the firm’s Globe database (my bold):

“We have continued the Globe development programme during the year… Globe continues to be our global exploration database and is actively used to add value to new sub-global products and proprietary contracts. It is essential that Globe is built with a balance between primary data (i.e. data measurements) and interpreted data. Our staff continue to build the interpretations but we have also added two significant third party data-sets – a well data-set comprising more than a million North American wells, and a seismic data-set which covers a number of areas of interest across the world.”

“We have continued to enhance Globe as an exploration data-set and to increasingly realise the value from it in a number ways. We anticipate that the work in the current three-year development period will continue to add to its intrinsic value as well as increasingly enabling us to realise value directly through its use at a variety of scales and in a range of product types.”

The reference to a “three-year development period” indicates there could be further hefty development expenses to come — most of which could also travel directly to the balance sheet.

Without more detail, it looks to me as if reported profits are being inflated — and I need to investigate this point further.

Valuation

With current-year profits set to come in “substantially below current market expectations”, judging GTC’s valuation on an earnings basis is tricky.

Profit estimates are made trickier by GTC serving relatively few customers and collecting somewhat lumpy income. For instance, these results recognised the majority of a single $5m contract — which probably represented at least 30% of the year’s revenue.

My best guess is to assume the current depressed year will achieve a negligible operating profit and that a return to the good old days will see operating profit reach £2m again (seen in 2013 and 2015).

(True, a negligible profit may prove to be too pessimistic this year, but that is counterbalanced by GTC spending significant amounts on intangibles. I can foresee GTC reporting a break-even year on a cash flow basis).

As such, a middling year could therefore see a £1m operating profit, which after 9% tax (aided by R&D tax credits) would equate to earnings of 2.8p per share. That’s just enough to cover the 2.2p per share dividend.

What is more certain is GTC’s balance sheet, which carries a freehold with a £2.6m (8p per share) book value as well as net cash of £3.7m. Taking into account the aforementioned £980k earn-out, and making a few minor adjustments for other working-capital items, I make net cash to be £2.3m or 7p per share.

With the shares at 40p and market cap at £13.1m, I reckon GTC’s enterprise value (EV) to be 33p per share or £10.8m. The P/E on my EV and middling EPS guess is therefore 12.

That valuation does not tempt me to top up just yet, especially as I need to learn more about that development expenditure and study the finer details within the forthcoming annual report.

Nonetheless, GTC does have net cash, should survive the current downturn and demand for its range of specialist data and services ought to rebound as and when the oil sector recovers. When that recovery occurs, of course, is anyone’s guess.

* Next events: Ex-div on 19 November, AGM on 8 December, 1.74p final dividend paid on 17 December.

Maynard Paton

Disclosure: Maynard owns shares in Getech.

Dear Maynard,

I would be interested to hear your thoughts on Billington Holdings. High stock ranks, but doesn’t seem to have much coverage. Just wondered if you had considered it and rejected it, not yet considered it, or were getting round to publishing your findings.

Thanks,

Dan

Hello Dan

Thanks for the comment. I vaguely recall looking at Billington (I think it is the steel scaffolding business) a few years ago when the shares were in the doldrums at <40p. I think the management changes then put me off, though I never got round to digging any deeper sadly. It is not high on my to-do list at present.

Maynard

Getech (GTC)

I have been doing some digging into past GTC reports and found this from the 2009 edition. Essentially it explains what could be going on with the ‘mysterious’ £304k fair-value adjustment I mentioned in the Blog post above.

I believe the £304k adjustment and the £298k impairment are indeed linked to the ERCL purchase.

You see, GTC has form in making acquisitions and then quickly lowering its guess for the deferred consideration and writing off some of the purchased goodwill.

Back in late 2008, GTC purchased Lisle Gravity for a total of £1.9m including estimated deferred payments:

Then in the 2009 accounts, we see profits were hit by a £463k goodwill impairment and bolstered by a £465k fair-value adjustment on a financial liability.

Anyway, it transpires both of these entries related to that Lisle purchase:

I think the accounting story goes like this:

i) on purchase, GTC spent about £1m cash and booked about £900k as a liability on the balance sheet (the deferred consideration)

ii) when the accounts were drawn up, GTC lowered its deferred consideration estimate by £465k

iii) lowering the deferred consideration meant GTC had to write-off a similar amount of goodwill

I am not sure why the impairment and fair-value adjustment did not match exactly in 2009 (or indeed 2015), but the differences are insignificant.

One more thing…

I am sure the £980k figure I mentioned in the Blog post above does relate to the deferred ERCL consideration. But it won’t include any deferred consideration that is set to be paid within the current year. That liability (if it exists) will be in current liabilities, and should be disclosed in the upcoming annual report. Looking at the figures, I wonder if the latest deferred consideration is the £1,550k original figure less the £304k fair-value adjustment = £1,246k, of which £980k is a non-current liability and £266k is a current liability.

I will publish another comment when the annual report is available and I have finally resolved all these figures!

Maynard

Getech (GTC)

I might (or might not) be on to something with the capitalised development costs. They could be related to GTC’s multi-satellite gravity project:

From July 2014 (my bold):

http://www.getech.com/stock-exchange-announcements-2014/#160714

“Getech (AIM: GTC), the oil services business specialising in the provision of exploration data and petroleum systems studies and evaluations, is pleased to announce that it has now signed further clients to fund its new global multi-satellite gravity project.

In July 2013, the Company announced that it had funding in excess of £500k to commence a global roll-out of the CryoSat pilot study. This pilot project aimed to develop and demonstrate methodologies to improve the exploration value of satellite gravity data by combining new data from CryoSat-2 with existing data. The Company is now pleased to announce that additional sponsors of the global project have brought the total funding to more than £1m. This project is due to run over a three year period to June 2016, with the majority of this income to be recognised over the next two financial years.”

Capitalised development costs were £83k in H2 2014 and £977k in FY 2015, giving a total of £1,060k. So equal to “more than £1m“. The timing seems to fit as well, supported by this page…

http://www.getech.com/gravity-magnetic/multi-satellite-altimeter/

…which states:

“The first complete global coverage of new gravity data was released to members in June 2015. This included one full year of data from the CryoSat-2. The final release will include four years of CryoSat-2 data and is scheduled for release in July 2016.”

So my theory is the sponsors have given GTC £1m-plus, of which £1,060k was spent during FY14 and FY15 on the first full-year data-set from CryoSat-2. As such, it is probably right that GTC capitalises this expenditure as it ought to be a long-lasting asset for the business. I think for the accounting, this sponsor cash payment would be declared initially as deferred income in the liability ledger (similar to an upfront payment for a year’s magazine subscription) and the associated revenue may not have been recognised at present. As such, I am beginning to become happier with the development spend, as it appears GTC is not capitalising its own operating costs.

I will look into this further.

Maynard

Hi Maynard,

Excellent work as always. I was also a little concerned that there may have been a change in accounting policy which had the effect of superficially boasting EPS in the short term but looking through the Annual Report the company expensed as incurred £1.341m of R&D in 2015 compared to 0.953m in 2014 which certainly doesn’t suggest they have transferred any R&D spend from the P & L to intangibles.

Hello Patrick

Thanks for the comment. Yes, I have been studying the Annual Report today and, as you say, R&D of £1.3m was expensed, so I’m convinced the development spend must be this satellite project. Also, the deferred income entry shows a c£1m increase, which ties in with my theory. True, deferred income can increase because other customers may have paid upfront for different contracts, but I think the latest trading guidance suggests this is unlikely to be the case. My theory about the mysterious £304k fair-value adjustment also looks correct. Anyway, I will post my thoughts on the AR possibly tomorrow or Monday.

Maynard

Getech (GTC)

Publication of 2015 Annual Report:

http://www.getech.com/wp-content/uploads/2015/11/Getech-Group-plc-Annual-Report-and-Accounts-2015.pdf

Lots to go through here.

1) Capitalised development costs

My original Blog post highlighted GTC’s £977k capitalised development expenditure:

I wrote in an earlier comment above that I believe this capitalised expenditure relates to GTC’s multi-satellite gravity project, and that remains the case. The operating cost note shows the company continues to expense a sizeable amount of R&D through the income statement (£1.3m):

I reckon the sponsor money for the multi-satellite gravity project has been accounted for as accrued and deferred income:

That figure increased by £951k during the year and, although this entry will be affected by any upfront payment for other contracts, the tone of GTC’s current guidance suggests the likelihood of receiving such other pre-payments at present is small.

For the current year (FY16), I expect GTC to capitalise further development costs paid for by sponsors as this multi-satellite project leads up to GTC receiving the final part of the data during mid-2016. I suspect any material revenue from this multi-satellite project will be first produced in the financial year to July 2017.

All told, I am happy there is nothing untoward going on here with capitalised development costs.

2) Acquisition of ERCL

a) Impairment and fair-value adjustment

My original Blog post highlighted GTC’s £298k impairment of intangible assets and a mysterious £304k fair-value adjustment:

These are indeed post-acqusition adjustments.

We can see the £298k impairment relates to ‘customer relationships’ of £877k purchased during the year:

And we can see those ‘customer relationships’ of £877k was indeed part of ERCL:

As well as writing down part of the asset acquired, GTC has ‘written up’ (i.e. reduced) the value of an associated liability. The liability in this case is the deferred consideration for ERCL.

This becomes a little complicated, but the deferred consideration is described in the accounts as an ‘other payable’ or ‘financial liability’ that is ‘held at fair value through profit and loss’. There’s a clue in one of the accounting notes:

And you can see below that, all of a sudden, GTC’s ‘trade and other payables — held at fair value through profit and loss’ has soared from £14k to £2m. This increase is due purely to ERCL:

The accounts don’t show it, but I believe the original deferred consideration would have been £2,035k plus £304k fair-value adjustment = £2,339k.

So as I suspected originally, these adjustments suggest profits at ERCL may not be as high as originally expected.

(Footnote: the post-acquisition impairment of ERCL’s ‘customer relationships’ may not be too surprising when you read how the initial value was calculated.

Apparently ERCL has enjoyed a 90% customer retention rate:

…and the life-time amortisation period is a very long 15 years:

Those look aggressive assumptions to me.

b) Deferred and contingent consideration

More complications now.

The original statement announcing the ERCL deal referred to a potential £1.55m deferred consideration for ERCL. But the annual report now reveals the purchase involved a deferred consideration of £1,386k plus a net asset payment of £1,185k:

What has occurred? I believe ERCL bagged a sizeable contract during the two weeks between the deal announcement and the completion. Within the original deal announcement, GTC claimed ERCL had net assets of £40k. Now we see, excluding ‘customer relationships’, ERCL had £2,336k less £877k = £1,459k net assets. That looks suspiciously similar to the £1,504k trade debtor number below:

All this leads me to believe GTC re-jigged the initial deal in order to pay ERCL (via a new net asset payment arrangement) what money this trade debtor eventually pays (less tax and the other liabilities ERCL carried).

Because of this extra net asset payment, it is not clear from the accounts what exactly the deferred consideration based on profits for ERCL currently is. All I can say for sure is that the £977k ‘other payable — held at fair value through profit and loss’, which is set to be paid after one year, is part of this particular consideration.

c) ERCL revenue and profit

I wondered in my Blog post above just how much ERCL contributed to GTC during its 4 months of ownership. The answer is revenue of £936k and a pre-tax profit of £230k. More than I expected, actually.

Without ERCL, I calculate GTC would have reported revenue of £7,703k and a pre-tax profit of £1,762k.

I calculate ERCL during the full-year reported revenue of £4,235k and a pre-tax profit of £1,600k.

The £230k contribution extrapolated over a year gives £690k. I suppose that does not make the underlying £4.3m price-tag super-expensive.

d) ERCL discounted cash-flow value

I see GTC has prepared a note to head off any dissent about the valuation of ERCL. The firm has calculated the net present value of ERCL plus its other similar project division to be £7m.

3) Central costs

On to something else now. I was slightly alarmed when I saw central costs rise by £1m:

But it seems GTC has re-jigged its allocation of costs. For FY15, the divisional profits add up (almost) to the group gross profit, so the divisional profit figures are gross profit figures. For FY14, the divisional profits are £1m below the group gross profit figure, and I can only assume those prior numbers included other divisional expenses (probably R&D). All told, nothing to worry about but a presentational note would have helped I think.

4) Large customer

Confirmation of GTC’s largest contract representing 29% of total revenue:

5) Useful tax number

GTC has received another £280k rebate for R&D tax credits. That could make calculating the firm’s tax charge easier.

6) Thin-cat director pay

I can’t complain about the level of board pay:

Phew. That is it. I hope all this makes some sense. I must admit GTC could have helped matters by explaining some of adjustments in the accounts. But I believe there is nothing untoward going on and actually I am more reassured by the business now that I seen the annual report and thought more about the numbers.

Maynard

Excellent analysis Maynard, one thing I would add is that presumably Hugh Edwards salary is just for 3 months which would make him the highest paid director with an annual salary north of £200,000. The going rate for Henley on Thames rather than Leeds I imagine :-)

Thanks Patrick — good spot!

Getech (GTC)

Valuation Ramble:

I see GTC shares have sunk to 24p. Following the warning about 2016 trading in the recent results, how low could the price go?

GTC’s all-time low occurred in 2010. Non-exec Peter Stephens was able to pick up the shares for 11p during April and July. In hindsight they were smart purchases — assuming you took profits on the way to 100p a few years later!

The (interim) results immediately prior to those purchases of Mr Stephens showed revenue down 51%, a loss of £392k and the dividend passed. Net cash was a measly £7k, too.

With no earnings and no dividend, net asset value (NAV) was the only valuation crutch back then. At the time, GTC’s NAV was £4,021k, or 14p per share. Less intangibles, tangible NAV (TNAV) came to £2,986k or 10p per share.

So there is a precedent for GTC’s shares to trade just above TNAV.

Back to 2015 and GTC’s latest results showed a TNAV of £5,029k or 15.3p per share. So perhaps the current price could sink to something like 16p to 17p.

Bear in mind that GTC back in 2010 was in a less secure financial position. As mentioned, net cash was just £7k. But the group then seemed relatively optimistic of a recovery: “The oil price appears to be less volatile and has remained generally above $70 per barrel for several months, and we believe we are now seeing a return towards normality of client buying patterns.”

Right now GTC enjoys a more secure financial position — net cash at the last count was £3.7m. But the outlook is not great: “there remains significant uncertainty about the short term and we cannot predict how the market will develop during 2016…” Oil is presently sub-$40 a barrel.

The sole broker forecast I can find at present is for pre-tax profit of £700k and earnings of 1.7p per share for 2016. Those projections compare to £2m and 5.8p per share respectively for 2015.

I do wonder if GTC’s next results (interims for the six months to January 2016, due in March), could show a break-even performance or loss. Given the grim environment for oil services outfits at present, I get the feeling the company has guided the broker to a H2-weighted performance to meet that aforementioned 1.7p EPS guess.

We’ll just have to wait and see.

Still, to put GTC’s current share price into perspective, here are a few more sums.

The group’s latest TNAV was £5,029k. Less the recent 1.74p per share dividend payment, TNAV then comes to £4,457k or 13.5p per share. The bulk of that TNAV is represented by cash and freehold property.

Meanwhile, the current market cap at 24p is £7,895k.

You could argue the difference between the market cap and the TNAV — £3,438k or 10.5p per share — is the inherent ‘intangible’ value of the group’s magnetic and gravity databases.

(In GTC’s latest results, the firm received £1m from certain clients to buy new satellite-gravity information. So clearly some of the firm’s data has a value to someone.)

In comparison to the implied £3,438k ’database’ value, GTC has since its flotation ten years ago earned a total post-tax profit of £7.7m.

So… the theory is that a bidder can buy GTC for 24p a share, effectively own cash and property with a net value of 10.5p per share and obtain a database for 13.5p per share that has produced aggregate earnings of 23p per share during the last decade.

You could also argue GTC’s TNAV may be understated a bit, given the books show it could pay at least £980k (3p per share) for the earn-out of ERCL. If ERCL’s profit does not meet expectations, GTC’s TNAV could improve by a not insignificant amount.

That said, the net cash position could go the wrong way if the next results do show a loss.

Maynard

Getech (GTC)

Board changes:

http://www.investegate.co.uk/getech-group-plc–gtc-/rns/board-changes/201602091403295499O/

“The Board announces that Raymond Wolfson is stepping down as Chief Executive Officer and director of the Company with effect from no later than 31 July 2016. In the interim until a new CEO is appointed Mr Wolfson will continue in the role of CEO and the Chairman, Stuart Paton, will increase his level of day to day involvement.

Mr Wolfson was appointed CEO of Getech in 2007 having been a non-executive director since it started trading as a separate company in the year 2000. Following his resignation as CEO, Mr Wolfson will take on the role of Commercial Director which will be a non-board position and will provide continuity for the new CEO, as well as advice and support on a range of matters including commercial, financial, regulatory and contractual.

Stuart Paton, Chairman said “The Board is extremely grateful to Raymond for his outstanding contribution and commitment over many years. He has been a key part of the growth of the company following its spin out from the University of Leeds in 2000. The Board will now actively seek a replacement and considers that, for the next stage in the Company’s development, a person with direct industry experience and knowledge is required. A specialist recruitment agency has been exclusively retained for this search.

I have very much valued working with Raymond during my time at Getech and have the highest regard for him. I am very pleased that he will continue to provide invaluable support to the Company after stepping down as CEO.”

A further announcement will be made when a new CEO is appointed.”

———————————–

This could be ominous. The chief exec suddenly steps down at a time when the group’s oil and gas clients are experiencing very difficult trading conditions.

The worry is that the board has just got wind of the first-half results (six months to 31 Jan 2016), the figures and outlook are not great… and have decided fresh leadership is required. Mr Wolfson, who I don’t think has really done much wrong in his time at the top of GTC, is demoted to Commercial Director. I note that the statement did not contain any comments from Mr Wolfson himself.

I wonder if the “specialist recruitment agency” that has been “exclusively retained for this search” is Zinc Consultants, which is the recruitment business of newly appointed non-exec Chris Flavell:

http://www.investegate.co.uk/getech-group-plc–gtc-/rns/board-changes/201511100700051041F/

It would make sense if Zinc was retained.

I also wonder if this move opens the door for Huw Edwards to become GTC’s chief exec. He is one of the co-founders of ERCL, the geoscience consultancy bought by GTC during April last year, and was appointed as a GTC executive board member after the purchase.

Mr Edwards appears to have a more entrepreneurial background than Mr Wolfson, and he also owns 2.68% of GTC. I would welcome his appointment as GTC chief exec.

Anyway, let’s see what happens. My earlier comment about GTC’s valuation recalled how these shares have in the past traded at book value when times became very hard — but then rallied spectacularly when the good times returned. I wonder if any forthcoming bad news could provided a similar buying opportunity.

Maynard