08 September 2015

By Maynard Paton

Quick update on Tasty (TAST).

Event: Interim results published 8 September

Summary: A very satisfactory set of results, with highlights including higher margins and a further acceleration of new restaurant openings. It certainly appears as if TAST will expand using debt rather than equity, though further borrowings will be needed for the business to become self-funding. I remain convinced the family management here can replicate its earlier success at Prezzo (PRZ) and can perhaps quadruple TAST’s market cap. I continue to hold.

Price: 135p

Shares in issue: 53,215,324

Market capitalisation: £71.8m

Click here for my previous TAST posts

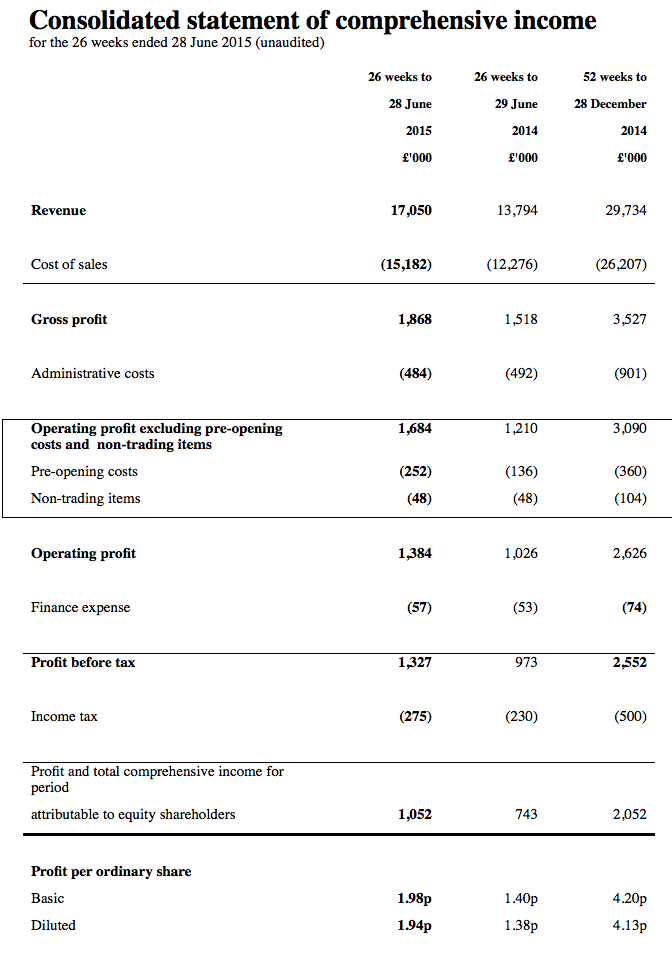

Results:

My thoughts:

* These results appeared very satisfactory

I felt TAST’s progress was very satisfactory, and further extended the positive momentum reported within March’s full-year results.

During the six months, the chain operated with an average of 39 outlets — up from 30 during the comparable period of 2014. As such, it was no surprise to see a substantial performance improvement. First-half revenue advanced 24% while operating profits climbed 35%.

* Operating margins continue to improve

TAST’s expansion continues to showcase higher operating margins — they improved from 7.4% to 8.1% during this first half. The group said today that “actions are regularly taken to improve profitability at all sites, increasing sales through updated menus and improving food and labour margins.”

Something important to consider with future margins is the National Living Wage. Its introduction next April will see workers aged 25 or more receive a minimum of £7.20 an hour, which will increase to £9 an hour by 2020. (The current minimum wage rises to £6.70 an hour from October.)

Last year the average TAST restaurant employee was paid about £16k and I am sure the company will face higher staff costs once the new legislation comes into force.

* Restaurant openings continue to accelerate

Today’s statement confirmed six new restaurants had opened, with a further five to start trading before the end of the year. However, one outlet was closed during the six months.

So… 2015 will witness an extra 10 net new sites — up from an extra 8 during 2014, an extra 5 during 2013 and 2012, and an extra 4 during 2011. I am very pleased TAST’s expansion continues to accelerate and the group is now adding meaningful numbers of new outlets.

* Further debt funding looks likely

TAST’s expansion is presently funded by debt. The six months witnessed TAST’s net cash position of £1.3m turn into net debt of £2.7m as the business spent £4.5m on new restaurants.

Earlier this month, TAST confirmed it had lifted its debt facilities from £4m to £8m. That gives the firm an extra £4m to spend on new sites, but my rough sums indicate the business needs to produce operating profits of £6m-plus to self-fund 10 new outlets a year from its existing estate. Right now profits are running at around £3m.

Looking back at how PRZ expanded, it raised £16m by issuing new shares between 2004 and 2006 to take its estate from 35 to 98 sites — at which point that business became self-funding.

All told, I get the impression TAST will need to take on further debt — probably another £8m — to stand any chance of repeating the roll-out achievement of PRZ.

At least the cost of TAST’s debt does not appear onerous at present. The interest charge paid during these latest six months came to just £57k. I am also pleased the amount of capex per new site matches that spent during recent years.

Valuation

* I continue to believe TAST can replicate the success of ASK and PRZ

TAST’s family management has already built and sold two multi-bagger restaurant chains (ASK Central for £223m in 2004 and PRZ for £304m in 2015) and I see no reason why TAST cannot complete the hat-tick.

PRZ was acquired earlier this year for £304m when it operated with 245 restaurants. Back in December 2004, PRZ had 48 outlets — comparable to TAST’s 42 at the end of June 2015.

So if TAST simply follows the success of PRZ, then the next 10 years could see TAST’s £72m market cap become £304m — or advance 4-fold or 15% a year.

(Subtract PRZ’s £33m freehold assets from its final £304m market cap, and TAST’s market cap could grow 3.8-fold or 14% a year. TAST does not own any freeholds).

* In the meantime, the shares remain highly rated

TAST’s trailing P/E is 28— so the downside will be considerable if a setback occurred and/or the expansion history of PRZ can’t be replicated.

Next events: Preliminary results, probably March 2016

Maynard Paton

Disclosure: Maynard owns shares in Tasty.

Coincidentally I own shares in TAST listed in the US…some similar characteristics

Thanks for the update Mayn. Market is certainly pushing up the share price at the moment.

Regards

David

Mayn,

What’s going on with the Tasty share price, up nearly 50% in the last 2 months. Very nice but feels too good!

Cheers

David

David,

Yes, very nice, and yes, feels too good! Not sure why the rise — it feels as if it has been tipped somewhere. The last results looked good and presumably more investors are latching onto the long-term potential.

Maynard

(Update: ADVFN sources are saying: Tipped 06-11-15 by The Penny Share Letter [ThePennyShareLetter@agora.co.uk] “A family of restaurant geniuses could make you 343%”)

Hi there,

At the current share price of 198p, would you say this company is good value, taking into account some conservative growth projections for the next, say, 10 years? By my estimations, it is, provided as a shareholder you are okay with having all FCF (and more) being invested for expansion. But I’m having a hard time getting myself to buy, purely because of the recent surge in share price. Would love a second opinion!

Thanks,

William

Hello William

Well, it is not as good value as it once was. If you look at my Blog post above, I refer to market cap of £304m for Prezzo. Current market cap of Tasty is £106m. So does that near 3x return over, say, 10 years give sufficient upside potential given the risks of the expansion plan going wrong? That is what you have to consider. It was easier to make that decision when the shares were lower earlier this year.

Maynard

Thank you Maynard. That is a very interesting way of looking at this investment. I guess one way to estimate the risk of the expansion failing is to look at what the customers think of the restaurants. Wildwood generally gets good reviews though Dim T might be lagging behind a bit.

Willem

Hello Willem

Yes, dim t was the original restaurant concept at Tasty but its dim-sum menu did not have the roll-out potential. So the business kick-started the Wildwood format a few years ago, but kept the handful of dim t outlets.

Maynard

Hi Mayn,

Bit concerned that Tasty seems to have suffered in price drop off more than the fall in the FTSE for no apparent reason. Maybe I should be looking at the AIM index which springs to mind as I’m writing this!

Results should be out for Tasty in the next few weeks

Cheers

David

Hello David

All I can say is that no share goes up in a straight line. Good evidence comes from this article:

http://www.fool.com/investing/general/2016/02/09/the-agony-of-high-returns.aspx

I am not saying TAST will definitely produce high returns in the future. But I guess the lesson is that to enjoy high returns, you have to endure substantial drops on the way.

Maynard

Thanks for sharing Mayn. I’m in to Tasty for the long term and I get the ups and downs. This current down is pretty significant at circa 25% and unusual for them looking at the last 6 years since I have been following them. The volume of trades is nothing special and many are small trades so it looks like ‘noise’ (maybe on the back of the recent market slide) and once the slide starts others will be ploughing in. This is my hope as I don’t see anything fundamental that would change the outlook. Trying to make sense of it is probably not worth the effort and trying to predict what to do is definitely not worth it.

David

Hello David

The drop has been significant, but the share did jump significantly late last year due to it being tipped somewhere (I forget where). I suspect any ‘hot money’ buying on that advice may now have sold, which may have caused the slide. In terms of the fundamentals, the only TAST-specific worry perhaps is the advent on the National Living Wage on TAST’s staff costs. There is of course the usual economic worries as well. Ultimately our returns from here will be mostly dependent on whether TAST’s expansion can eventually match that of previous Kaye family ventures.

Maynard

Mayn,

The growth of restaurant’s is not easy to follow and even the Wildwood web site has less restaurant’s listed (only 31) than that declared last September in the update. They keep their opening plans very close to their chest

Also interesting to me is the Board and major share holders have 76% of shares. The recent trades are miniscule so its fascinating to me that the price can drop 25% on the basis of thin trading in the negative direction.

Mayn,

just done so more research and found a wildwood recruitment site and if you add all the sites they are recruiting for today in totals 50. I think their count last September was 44 so its about 1 per month. The site also says they are opening another 30 in the next 18 months so looks like the acceleration is one!

David

Tasty (TAST)

Restaurant count re-cap:

Further to David’s excellent tip-off about TAST’s recruiting and potential expansion plan, I thought it best to double-check where the group stood currently with its estate:

There are three brands: Wildwood, Wildwood Kitchen and dim-t.

http://www.wildwoodrestaurants.co.uk/restaurants/

http://www.wildwoodkitchen.co.uk/contact.html

http://www.dimt.co.uk/locations/

As at 19 February, these websites listed 31 Wildwood, 10 Wildwood Kitchen and 7 dim-t outlets = 48 total sites.

September’s half-year results said the group would have 46 sites by the end of 2015 — 40 Wildwood and Wildwood Kitchens, and 6 dim-t. So an extra two sites have been added, one of which looks to me to be the dim-t site at Whitely.

Now to the recruiting:

A quick search has unearthed these links:

http://www.simplyhired.co.uk/job/assistant-manager-wildwood-are-growing-job/wildwood-restaurants/o7mqlxfyku?cid=flvwsavcjnqrctejgqnzgltymafefuyl

https://www.linkedin.com/pulse/tasty-set-exciting-2016-you-joshua-field?trk=mp-reader-card

The job advert confirms David’s 30 new openings within the next 18 months, while the Linkedin post claims 15-20 openings in 2016.

Either way we are looking at a significantly accelerated pace of new sites — a net 10 new locations were opened in 2015, up from 8 in 2014 and 4-5 in 2011, 2012 and 2013.

Just so I know for next time, I think this could be the most comprehensive jobs site for Wildwood: http://www.leisurejobs.com/minisites/wildwood/jobs/

Maynard

Tasty (TAST)

Restaurant number update:

Just to update the latest restaurant count.

There are three brands: Wildwood, Wildwood Kitchen and dim-t.

http://www.wildwoodrestaurants.co.uk/restaurants/

http://www.wildwoodkitchen.co.uk/contact.html

http://www.dimt.co.uk/locations/

As at 24 March, these websites listed 32 Wildwood, 10 Wildwood Kitchen and 7 dim-t outlets = 49 total sites. An extra Wildwood outlet has opened at Braintree, Essex.

Maynard

Mayn

It looks the actual new restaurants opened hasn’t changed unless the web sites are out of date which I suspect they are

David

Prelim results released today for 2015 year end, revenues up 28% and profit up 20%. 13 new outlets opened in 2015 and 2 more recently. A total of 15 planned to open for 2016 as part of the accelerated growth program

David