22 May 2015

By Maynard Paton

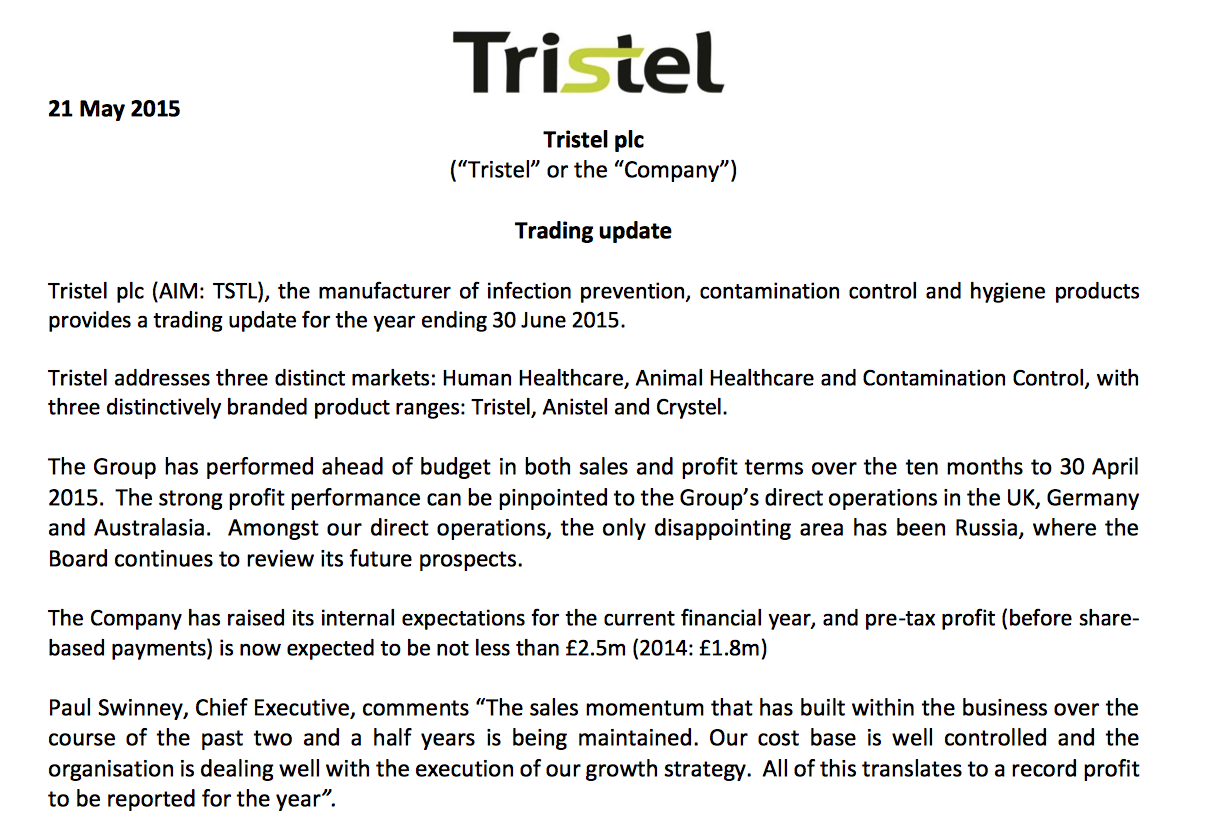

Quick update on Tristel (TSTL).

Event: Trading update published 21 May.

Summary: At last — one of my shares has issued an ‘ahead of expectations’ trading statement! TSTL’s medical wipes appear to be selling very well and second-half profits now seem set to grow by 35%. There could be further upside, too, if TSTL’s past ‘sandbagging’ form is anything to go by. My valuation sums still suggest annual returns of 15%-plus could be earned. I continue to hold.

Price: 85p

Shares in issue: 40,949,701

Market capitalisation: £34.8m

Click here for all my previous TSTL posts.

Statement:

My thoughts:

* Second-half profits up at least 35%

Full-year pre-tax profits of not less than £2.5m indicate pre-tax profits of at least £1.5m for the second half — equivalent to a 35% increase on H2 from the year before.

TSTL’s first-half results from February had already showed pre-tax profits up 43%, so I am very pleased the group’s significant trading momentum has continued.

* Could there be further ‘sandbagging’?

I have noted in the past how TSTL has ‘sandbagged’ its statements, with subsequent results coming in well above the earlier ‘no less than’ forecast.

In particular, back in April 2014, TSTL issued this ‘ahead of expectations’ update:

In the event, full-year 2014 pre-tax profits came in at £1.8m — some 20% above the ‘no less than’ £1.5m figure.

I’m hopeful the latest ‘not less than’ £2.5m figure will be beaten by a similar margin!

* On track to easily meet the 2017 revenue target

TSTL’s interim results confirmed the group was aiming to grow its revenue by at least 50% to £20.2m during the three years to June 2017.

That top-line target looks very achievable now. The interim results webinar revealed the business was aiming for 15% margins for the current year, so a pre-tax result of £2.5m suggests turnover for this year could be about £16.7m.

As such, I now feel it is not out of the question to see revenues top £19m for 2016 and approach £22m for 2017.

* Earnings of 4.6p per share?

Using the 26% tax charge applied in the interim results, a pre-tax profit of £2.5m would produce full-year earnings of 4.5p per share.

I just wonder if we could see 4.6p or even 4.7p per share, as that would mean the indicated 2.34p per share full-year dividend would be twice covered.

Within February’s interims, TSTL did say it would target a twice-covered dividend:

I recall thinking it was odd that commissioned-broker Equity Development was looking for earnings of 4.01p per share — and therefore dividend cover of only 1.7x — prior to this latest statement.

For what it is worth, Equity Development is now forecasting earnings of 4.36p per share for 2015 (and therefore dividend cover of 1.85x).

Valuation

* My estimate of surplus year-end 2015 net cash is now £3.7m or 9p per share. TSTL’s near-term enterprise value (EV) could therefore be £31m or 76p per share. Using the aforementioned 4.5p per share earnings guess, the forecast P/E on my EV is 17.

* I was previously projecting 2017 revenue of £20.2m but I think that is now more likely to be closer to £22m.

* Applying margins of 15% and tax at 26% on that 2017 revenue gives me possible 2017 earnings of 5.9p per share (versus the 5.5p per share I was previously expecting)

* Applying a P/E of 17.5 on that 5.9p EPS estimate to reflect the growth expected during the next few years (and TSTL’s longer-term opportunities in the States), I arrive at a potential 2017 value of about 104p per share for the underlying business.

* Between now and 2017, I think TSTL could pay out a further 5p per share through dividends and retain a further 6p per share of extra cash in the business (to give a net cash position of 15p per share).

* So… 104p plus 5p collected via dividends plus net cash of 15p gives a potential total value of 124p per share during 2017.

* Assuming my sums are accurate, I’m looking for 45% upside from 85p during the next couple of years — equivalent to compound returns in excess of 15%. That projection matches the calculations I made back in February.

* Next update — probably a pre-close statement in late July.

Maynard Paton

Disclosure: Maynard owns shares in Tristel.

TSTL has published two pieces of positive news this month:

First, details of a study of detergent wipes used by hospitals:

http://www.tristel.com/wp-content/uploads/2015/06/090615TSTL-Wipes-study.pdf

Tristel plc (AIM: TSTL), the manufacturer of infection prevention, contamination control and hygiene products, welcomes the recent study by Cardiff University published in American Journal of Infection Control which concludes that commercially available detergent wipes are inconsistent in their ability to remove spores of bacteria from hospital surfaces following a 10 second wipe.

Tristel’s range of infection prevention products for hospitals have been developed specifically to disinfect medical instruments, using a proprietary chlorine dioxide chemistry clinically proven to be effective against the most common bacteria, micro-bacteria, viruses and fungi as well as being effective at a sporicidal level. This chemistry has been applied to Tristel’s range of surfaces products so that the same effectiveness can be achieved on hospital surfaces, the area that this study shows to be ineffectively cleaned when only detergent wipes are used.

Commenting Paul Swinney, Chief Executive Officer of Tristel, said:

That final paragraph is most welcome — I do like the sound of “the wider understanding of this issue provides Tristel with a huge opportunity“.

Perhaps the “wider understanding” of TSTL’s medical wipes has helped prompt this second piece of news today…

…concerning details of a special dividend:

http://www.tristel.com/wp-content/uploads/2015/06/180615-TSTL-Special-Dividend.pdf

Tristel plc (AIM: TSTL), the manufacturer of infection prevention, contamination control and hygiene products declares a special dividend of three pence per share payable on 6 August 2015 to shareholders on the register on 26 June 2015. The corresponding ex-dividend date is 25 June 2015. The Company expects to declare a final dividend for the year at the time of the preliminary results which are expected to be announced on 12 October 2015.

Francisco Soler, Chairman, comments:

Here are my thoughts:

* TSTL has a 30 June year-end — just 12 days away — so this 3p per share special dividend could well be a sign that the board is very confident of bumper annual results. Indeed, I’m hoping TSTL will soon upgrade its statement from May that said profits would be “not less than £2.5m“. Maybe not less than £2.7m?

* I see TSTL has reiterated its dividend policy: “The prevailing policy is two times cover with one quarter of our expectation for the full year pay-out paid as an interim dividend.”.

TSTL’s interim results indicated a 2.36p per share payout for the year to June 2015. So, with TSTL looking for 2x cover, I still believe EPS could be 4.6p or even 4.7p per share as I noted in the Blog post above. (The chaps at broker Equity Development continue to stick with 4.3p)

* The 3p per share special dividend is equivalent to £1.2m. For context, net cash at 31 December 2014 was already £2.9m, so this special handout is hardly going to stretch the company — particularly when TSTL confirmed: “We continue to generate significant levels of cash“.

* I am pleased TSTL’s chairman/founder remains upbeat: “We have a more exciting pipeline of new product developments than I have seen at any time in our corporate history.”

* I wonder if the plan to sell products in the States is moving a bit faster than expected: “At the same time we are moving forward with regulatory approvals in new, game-changing markets.”

TSTL has implied in the past that there would be no US sales until 2018 at the earliest.

* Is there scope for better-than-expected margins during the next few years? “Also, during the past six months we have devoted a great deal of management time to assessing the challenges of the Biocidal Products Regulation and are now confident that the future costs associated with it will be met comfortably from ongoing cash flow.”

TSTL had previously suggested margins may be kept at 15% as some investment would be needed to adapt to the new regulations. But I like the sound of such expenses being “met comfortably” and I wonder if future margins may now top 15%.

* I am not minded to update my valuation sums from the Blog post above just yet. Nonetheless, it is pleasing to see part of the surplus cash I had expected to build up within the company is now to be distributed via a special payout. And I would not be surprised if future years see similar one-off payments. TSTL has said that it is focusing on organic growth, so hopefully no surplus cash will be wasted on acquisitions.

I continue to hold.

Maynard

Hi Maynard, Wise to still hold but the shares look a little toppy here. Even at 4.7 EPS we are looking at 20 P/E ratio. Understandable that you continue to hold because “huge opportunity” probably means just that. But a buyer at these levels? Unless I’m missing something the growth is already priced in and therefore it could possible disappoint if there was any kind blip further down the road?

Hi Stuart,

Yes, the near-term P/E does not look great value. But the firm has predicted its sales for the 3 years to June 2017 should grow by 50%-plus and margins should be 15% (or perhaps more), so there is some justification for the current rating. The main wipes product also is a repeat-purchase item, demand for which is not correlated to the financial markets or economy, and where the largest buyer (the NHS buying agency) has agreed a multi-year purchase arrangement with TSTL. So as quoted companies go, there is a bit more predictability here than usual. But of course all this could be derailed by something unexpected. I am not a buyer at these levels though, and if the upside becomes very limited I will consider top-slicing.

Maynard