19 May 2015

By Maynard Paton

Today I’m continuing my hunt for Watch List shares with a look at Cenkos (CNKS).

Here are the initial attractions that prompted this research:

Lowly valuation: The P/E is 6 and the yield is 9%

Appealing accounts: Recent results showed high margins and net cash

Owner management: The directors control 23% of the business

As usual, I’m applying a question-and-answer template to help me pinpoint companies that match the criteria set out in How I Invest. I’m looking for as many Yes answers as possible.

Activity: Institutional stockbroker and corporate advisor

Website: www.cenkos.com

Share price: 192p

Shares in issue: 59,369,783

Market capitalisation: £114m

Does the business boast a respectable track record?

Yes.

CNKS was established in 2004, joined AIM during 2006 and initially provided a range of stockbroking services to institutional clients and wealth-management services to rich individuals.

By 2012, however, the private-client operations had been sold and the business has since focused on supplying industry research, corporate advice and market-making services to City funds and quoted companies.

CNKS certainly wasn’t slow to become profitable — the table below shows the business reporting a £6m operating profit during its first 16 months! I’m also impressed how the business remained profitable during the banking crash of 2008:

| Year to 31 December | 2005* | 2006** | 2007 | 2008 | 2009 |

| Revenues (£k) | 15,572 | 32,670 | 53,791 | 28.275 | 46,204 |

| Operating profit (£k) | 5,915 | 12,192 | 20,127 | 3,958 | 10,588 |

| Exceptional items (£k) | - | - | - | - | (3,848) |

| Gains on investments (£k) | - | - | - | - | 254 |

| Gain on disposal of subsidiary (£k) | - | - | 1,709 | - | - |

| Finance income (£k) | 210 | 798 | 1,983 | 1,166 | 506 |

| Pre-tax profit (£k) | 6,125 | 12,990 | 23,819 | 5,124 | 7,500 |

| Earnings per share (p) | 18.4 | 16.2 | 22.8 | 4.9 | 6.2 |

| Dividend per share (p) | - | - | 22.0 | 10.0 | 20.0 |

(*16 months to November 2005 **13 months to December 2006)

Earnings were somewhat depressed during 2010, 2011 and 2012, but then recovered strongly during 2014:

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Revenues (£k) | 58,531 | 37,360 | 43,155 | 51,433 | 88,516 |

| Operating profit (£k) | 6,444 | 4,804 | 6,485 | 10,577 | 26,812 |

| Gains on investments (£k) | (294) | - | 170 | - | - |

| Finance income (£k) | 453 | 311 | 351 | 134 | 160 |

| Pre-tax profit (£k) | 6,603 | 5,115 | 7,006 | 10,711 | 26,972 |

| Earnings per share (p) | 5.2 | 5.2 | 12.1 | 14.2 | 35.2 |

| Dividend per share (p) | 8.0 | 5.0 | 7.5 | 12.0 | 17.0 |

The dividend has bobbed up and down over time due to CNKS paying out all of its surplus cash flow each year to shareholders. I have to admit, the generous dividends alongside the consistent profitability does give CNKS the upper hand on rival broker Numis.

Exceptional items from the last few years have related only to the cessation and introduction of staff incentive schemes (more on those later).

Has the business grown mostly without acquisition?

Yes.

CNKS has not acquired any business since its formation, although the firm did enter negotiations to buy Close Brothers and Arden Partners at the start of 2008.

(I suspect CNKS’ shareholders are now thankful those discussions were terminated before the banking crash erupted!)

Has the business mostly self-funded its growth?

Yes.

CNKS has consistently operated without bank debt and its balance-sheet reserves are almost entirely represented by retained profits.

Does the business possess an asset-strong balance sheet?

Yes.

At the last count, net cash over and above regulatory capital requirements was £12.4m or 21p per share.

Does the business convert profits into free cash?

Generally.

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (£k) | 6,444 | 4,804 | 6,485 | 10,577 | 26,812 |

| Depreciation and amortisation (£k) | 346 | 362 | 331 | 311 | 386 |

| Cash capital expenditure (£k) | (405) | (568) | (92) | (148) | (420) |

| Working-capital movements (£k) | 11,339 | (10,683) | 13,134 | 5,542 | (7,343) |

The last five years have seen relatively small amounts spent on capital expenditure alongside somewhat large working-capital fluctuations. Notably, the aggregate cash movements of CNKS’ working capital give a cash-positive result for the last five years.

Something to note within CNKS’ cash flow is that it sometimes receives shares and options from companies in lieu of cash fees:

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (£k) | 6,444 | 4,804 | 6,485 | 10,577 | 26,812 |

| Shares/options received in lieu of fees (£k) | (1,143) | (607) | (2,898) | (1,335) | (3,443) |

Such payments have totalled £9m during the last five years and always carry the risk of not doing as well as cash over time. (I am not 100% sure, but it seems to me the options and shares CNKS receives are accounted for within the group’s working-capital movements.)

Unlike Numis, CNKS has not spent vast amounts on share buybacks to negate the dilutive effect of staff options. Between 2010 and 2014, CNKS used just £1m to repurchase shares for an employee trust — and I’m pleased the associated charge against earnings covered that expense.

| Year to 31 December | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (£k) | 6,444 | 4,804 | 6,485 | 10,577 | 26,812 |

| Share-based payment charge (£k) | 570 | 195 | 335 | 138 | 250 |

| Share purchases for EBT (£k) | (100) | (43) | (755) | (283) | - |

Does the business enjoy a competitive advantage?

Possibly.

Similar to Numis, CNKS reckons client service and staff expertise have underpinned its success to date. However, it does seem CNKS employs a different approach to staff pay from that of Numis and other brokers.

From the 2014 CNKS annual report:

“We manage our cost base carefully. We offer our client-facing staff relatively low basic salaries but reward their performance based on factors that include their net income generation. This cost flexibility allows us to operate during economic downturns more successfully than many of our competitors who have higher levels of fixed or guaranteed pay.”

This “cost flexibility” has ensured the business has reported a profit every year since its flotation — which does provide some reassurance for when the next downturn arrives.

During 2014, operating margins were a super 30% while for the last five and ten years, the average operating margin has been a decent 18% and a robust 23% respectively.

Such levels of profitability suggest to me CNKS employs an acceptable balance between staff pay and shareholder returns — at least for a stockbroker!

Does the business produce a respectable return on equity?

Yes.

Return on average equity for 2014 was £21m/£33m = 64%. Only twice since the flotation has that annual figure dipped below 15%.

Does the business employ capable executives?

Possibly.

Chief executive Jim Durkin is a founder shareholder, was a board executive between 2006 and 2009 and took the top job in 2011. The performance of CNKS since his appointment suggests he might be a safe pair of hands for the long term.

Mr Durkin is in his mid-50s, so succession planning does not seem to be an imminent worry just yet.

Mr Durkin is accompanied by four other executives, three of whom joined CNKS before the float and can each boast 25-plus years of institutional broking experience.

Does the business employ good-value-for-money executives?

Sort of.

Reflecting the aforementioned “cost flexibility”, Mr Durkin’s basic wage was £125k last year, which seems very reasonable for running a business that made annual profits of £27m. What’s more, three of his fellow executives took home basic salaries of less than £100k.

However, the executives can enjoy sizeable bonuses. Between them they divvied up £7m last year and £4m the year before.

I am not entirely sure about the payment arrangements for the three non-execs. Last year the chairman collected £285k and the other two each claimed £98k after the trio performed “additional duties”. I understand these duties related to the flotation of the AA (see below).

A bad sign perhaps is that the board held no less than seven remuneration meetings during 2014 — versus seven ordinary board meetings and three audit meetings. I also see the well-paid chairman missed one board meeting and two remuneration meetings last year (And I now hear he also missed last week’s AGM).

Does the business employ owner-orientated executives?

Sort of.

Mr Durkin boasts an 9%/£10m stake, while his fellow executives enjoy a combined 13%/£15m holding.

I should add that Mr Durkin and three other executives sold 9% of their holdings earlier this year through a general shareholder tender offer that was priced at 188p.

Similar to Numis, the drawback to the CNKS board is its liberal granting of options and share awards to staff. The 2014 annual report indicated outstanding options represented a huge 24% of the share count!

However, the aforementioned tender offer and the recent vesting of various options means potential dilution is currently ‘only’ 16%. The remaining options should be exercised before or during 2019.

Notably, the vast majority CNKS’ options entitle the option holder to receive the ordinary dividend — which I guess is another reason why the firm likes to distribute as much surplus cash as it can.

Does the business enjoy reasonable growth prospects?

Possibly.

The 2014 results contained an upbeat assessment of current trading:

“We are pleased with our performance since the start of 2015. There continues to be strong institutional demand to fund high quality companies and ideas. Since January we have been engaged in a number of significant fundraisings and our current pipeline is encouraging.”

An AGM update last week confirmed the positive trading:

“Since the announcement of our 2014 final results, issued on 30 March 2015, the Company has continued to trade well and our revenues are in line with our expectations. Our pipeline of potential new business activity remains encouraging.”

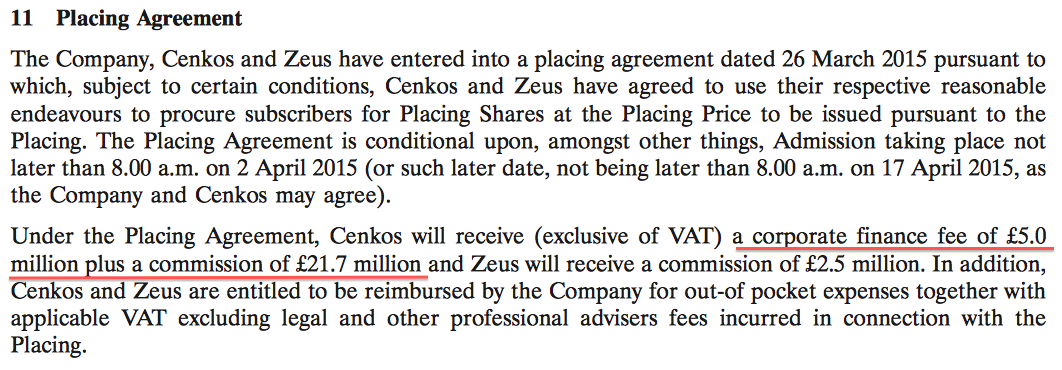

Significantly, in March CNKS was appointed lead broker to handle the acquisition of BCA by Haversham Holdings, which produced fees of £27m:

Longer term, progress at CNKS should ultimately be correlated to the health of the stock market and the general appetite for flotations and corporate deals. However, CNKS has alerted shareholders to a potential setback with certain commission rates:

“However, the pressure on secondary commissions shows no sign of relenting, including the potential impact of recent FCA initiatives in terms of the unbundling of dealing commission and payment for equity research.”

Does the share price stand a good chance of becoming a bargain?

It already looks a bargain.

Reported earnings of 35p per share for 2014 give a P/E of 6. The trailing 17p per share dividend provides an income of 9%.

However, CNKS has recently enjoyed bumper profits from substantial individual deals to support its progress.

In particular, during 2014, revenue of £33m — some 38% of the overall top-line figure — related to the flotation of the AA. This year is likely to see a similar concentration of revenue from the aforementioned Haversham/BCA deal.

The following table shows the first and second halves of CNKS for 2013 and 2014. You can clearly see the impact of the AA deal in the first half of 2014:

| H1 2013 | H2 2013 | FY 2013 | H1 2014 | H2 2014 | FY 2014 | ||

| Revenue (£k) | 19,995 | 31,438 | 51,433 | 65,225 | 23,291 | 88,516 | |

| Operating profit (£k) | 3,026 | 7,551 | 10,577 | 23,468 | 3,344 | 26,812 |

I’m guessing without the AA deal, profits for 2014 may have been around £10m to £15m or so.

For what it is worth, annual operating profits of £12.5m would equate to earnings of around £10m or 16-17p per share. Subtract the aforementioned 21p per share of cash from the 192p share price, and the underlying P/E excluding the AA deal may be about 10 or 11.

Is it worth watching Cenkos?

This is a difficult one.

On the one hand, CNKS offers cash-rich accounts, generous dividend payments and directors with 23% of the share count. There’s also that lowly valuation.

But there’s no denying that lowly valuation is dependent heavily on CNKS securing further large flotation fees. This year CNKS already has the Haversham/BCA deal in the bag, but what about next year?

Other points to consider include the potential 16% dilution from existing options and why most of the executives sold some of their shares at around the current price.

All told, CNKS appears more attractive than rival broker Numis. But the more I think about City brokers and how their revenues are dependent on one-off deals, the more I come to the conclusion that I much prefer the economics of asset managers such as City of London Investment and Ashmore.

True, asset managers too are sensitive to the swings in the financial markets. But they can also enjoy a decent level of recurring revenues when clients stick around and continue to pay annual management fees.

Plus, regular updates on assets under management can provide shareholders with a good insight into potential revenues and profits. Finally, the shares of asset managers can often trade on very modest multiples as well.

It’s a very borderline decision, but in an effort to become more selective with my shares, I will not be investing in CNKS right now. In the meantime, it will be fascinating to see whether CNKS can secure any more bumper flotation deals — and where its profits might stand without the bumper fees.

Maynard Paton

Disclosure: Maynard does not own shares in Cenkos.

Option holders get get dividends! You cannot be serious.

Divs are to reward providers of capital. If you want a dividend, divvy up.

I wouldn’t want to play these greedy buggers at Monopoly. They’d be charging me £1150 for landing on Mayfair even if they hadn’t bought the hotel yet.

On top of that exec & talent take 40% of profits for bonuses. See ShareSoc’s AGM report (member only).

http://sharesoc.ning.com/forum/topics/the-agm-forum?commentId=6389471%3AComment%3A34404

Hi MrContrarian

Option holders get get dividends! You cannot be serious.

Well that is how it reads in the annual reports. Certain option holders receive a payment every time an ordinary dividend is paid. This from the 2014 AR:

Maynard

Mayn

Great analysis, thanks for sharing and I agree with your conclusion

David

Thanks David

Hi Maynard,

Thank you for sharing this post. Appreciate it was some time ago now, however I wondered if you had kept watching Cenkos, and if so whether you had any updated thoughts you could share?

Clearly you were correct on how performance is majorly swayed by big deals, which don’t always happen. It seems the lack of a big deal in 2016, plus the FCA fine / investigation have brought these shares down substantially. I haven’t yet looked in detail, but it appears for H1 2016 costs were controlled quite impressively, such that they still reported a small profit even though revenue was down 71% from H1 2015.

Essentially I’m wondering if you have any thoughts on if the recent distress provides a good opportunity to enter the shares, or not.

Thanks,

Alan

Hello Alan

Thanks for the Comment.

I have not followed Cenkos since the write-up. If anything I have gone off City-type businesses in the meantime, as it does appear the staff do like to grab a greater part of the earnings…whether their business does well or not (well, that has happened at two of my shares).

I think if I were looking at Cenkos now, I would have to evaluate it as a shorter-term recovery gamble… but the upside may be limited as even if a large IPO deal is won and helps earnings to recover substantially, the market won’t re-rate the shares that highly as it now knows from Cenkos’ recent history that such deals don’t come along every year.

Maynard

Thanks for the response, your points make sense.

I would normally wholeheartedly agree with the comments about option awards and bonus levels. However in this case it makes sense given the feast or famine business model and the need to keep fixed costs low and protect cash during the droughts like we are experiencing now. Cenkos has delivered strong returns on capital across the years. The big question mark for 2019 is whether they can survive – with a current regulatory cash surplus of only £11m can flex their cost base enough if capital markets activity continues to stagnate.

Might also help if they could be more transparent about when a CEO and CFO will turn up.

Hello Jerry

Thanks for the comment and apologies for the tardy reply.

I have not looked at Cenkos since that review as over time I have become less enthused with City-type businesses.

I have followed a few fund managers over the years and I do get the impression their (highly paid) staff generally take precedence over outside shareholders. I know that City of London Investment (a fund manager in which I own shares) tries to balance the interests of employees with those of shareholders, but even this company is happy giving notable pay rises and introducing new retention schemes even when the dividend was flat for years.

A lot of non-City businesses have no difficulty ensuring returns are generated primarily for shareholders and not employees.

With brokers such as Cenkos, I just worry the talent will one day leave and set up shop on their own. The lumpy nature of deal income is also a factor that puts me off.

I do think brokers really ought to be private businesses/partnerships, that way the owners/employees/talent can decide their own remuneration and not have outside shareholders to think about. Trouble is, brokers these days require significant capital which may be hard to raise without outside help.

Maynard