24 April 2015

By Maynard Paton

Quick update on French Connection (FCCN).

Event: Trading update published 24 April

Summary: Profit warning — poor H1 Retail sales will mean greater-than-expected group losses this year. However, the profitable Wholesale and Licensing divisions continue to perform as expected. Turnaround possibilities remain, but the protracted wait has become just that bit longer once again. What’s needed now is some radical management action. I continue to hold.

Price: 42p

Shares in issue: 96,178,134

Market capitalisation: £41m

Click here for my previous FCCN posts.

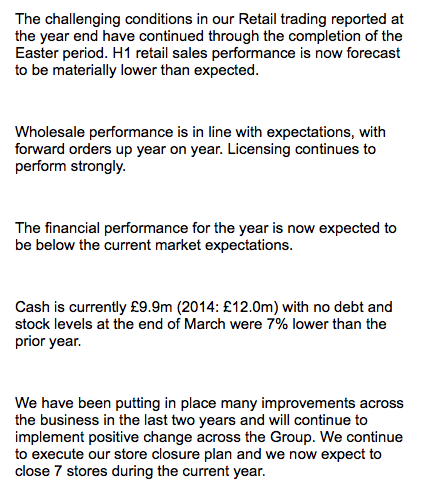

Statement:

My thoughts:

* Who was it that said ‘turnarounds seldom turn’?

Well, I did say in my last FCCN post that the fashion retailer’s turnaround is “unlikely to be entirely smooth”.

The chain suffered a poor Easter and — despite being less than three months into the current financial year — has essentially warned of higher losses for the full twelve months.

No doubt about it, this is disappointing news — especially when the business had almost returned to break-even in the previous year. I suppose the weaker H2 performance revealed within the last results was a signal that trading wasn’t going too well.

* But all is not lost

At least FCCN’s profitable Wholesale and Licensing divisions continue to perform as expected — and such progress tells me FCCN’s product range is not a complete write-off just yet. Remember, these two divisions produced a sizeable £21m profit before central costs last year.

Furthermore, cash burn for the last twelve months appears to be £2.1m. While it’s not great to see FCCN continue to lose money, the burn-rate does not seem too worrying at present with net cash at a seasonal low of £10m. (Net cash at the seasonal high has recently been £20m-plus).

* More stores to close

FCCN has upped its store-closure plan for the current year from 3-4 to 7. At the last count the chain had 88 stores.

Given the latest trading setback, the additional closures are welcome — and I’d like to think FCCN is now becoming even more decisive with its loss-making outlets. The Retail division lost £11m before central costs last year, with onerous lease payments not helping.

During the previous two financial years, FCCN closed 18 under-performing stores and its annual lease charge dropped by £4.5m to £23.9m. I calculate another 7 store closures might therefore save a further £1.75m a year.

As a reminder, FCCN’s last results presentation revealed the average store lease had 4.4 years to run, with “poorer performing stores lower than this average”.

* I still believe this share can one day top 100p — but the wait has just become longer :-(

My previous FCCN post contained various recovery forecasts and valuation sums, and today’s news has made them somewhat redundant.

So think about FCCN this way. Last year’s Wholesale and Licensing profits were £21m, which after all central costs would still leave £10m. In contrast, the market cap is just £41m at 42p — and there is net cash of £10m on the balance sheet, too.

As I see things, all the board needs to do is to take a thumping great axe to the Retail estate, which in turn would substantially reduce lease payments, stock levels and (I trust) central costs. I reckon cutting Retail losses from last year’s £11m to £5-6m would take group earnings to 8-9p per share and the share price beyond 100p.

In fact, the ideal outcome here is FCCN evolving into a pure Wholesale and Licensing operation — with perhaps a token own-store Retail presence. I’m sure the company would then enjoy a greater quality of income with much less in the way of liabilities and expenditure.

This could be pipe-dream stuff — but I do hope this latest setback has the board contemplating such a radical change to its business. I mean, if such a transformation were ever to happen, the share-price re-rating from 42p could be dramatic.

* Next update — probably an AGM update on 12 May.

Maynard Paton

Disclosure: Maynard owns shares in French Connection.

I wrote in my Dewhurst post yesterday that:

“A purchase today would be heavily biased towards ‘value’ rather than ‘quality’ and I’m keen to limit such investments — as they often go wrong for me.”

Well, FCCN is definitely more ‘value’ than ‘quality’, and this is what can happen!

Just to add to the worries, I see FCCN’s HQ is up for sale:

http://www.michaelelliott.co.uk/uploads/201501301042202104607Centro%201and2,%20Camden,%20London%20NW1%20-%202015.pdf

Seems as if FCCN has been paying a cheap HQ rent and the agent now reckons the property could command higher payments from tenants:

It looks as if FCCN’s HQ rent could rise by £1m :-(

FCCN AGM voting results now available:

http://www.frenchconnection.com/stormsites/fcuk/media/pdf/IR/AGM%20Voting%20Results%20May%202015.pdf

I was disappointed to see the voting for resolution 3 — the re-election of chairman and chief executive Stephen Marks:

I had hoped for more votes against.

Three years ago, when Mr Marks was last up for re-election, the votes against were much higher:

I must admit I have written to Mr Marks to urge him to consider radical management action.

The gist of the letter was as follows:

* FY2016 is now likely to be the 7th year of the last 8 that FCCN has reported losses

* FY2016 is now likely to see no dividend paid for the 4th year running

* Shareholders have already been fobbed off with two different business reviews (in 2010 and 2012) to help stage a turnaround

* Competitors such as Ted Baker continue to shine, suggesting “a tough high street” etc is no excuse for FCCN’s lamentable performance

* A much more business-like approach is required with the Retail division, not least by forcing new rental deals upon landlords.

* The roles of chairman and chief executive should be separated

* Mr Marks should step down to become non-exec chairman

* The current Operations Director should be dismissed

* A new, energetic and ruthless chief executive should be appointed, with the goal of transforming the business into a pure Wholesale and Licensing operation (in which FCCN is already very profitable)

* The FCCN board should look at Crawshaw, a small AIM-quoted butchers chain based in Rotherham that has just 21 outlets. It has a market cap of about £40m — the same as FCCN — but has managed to hire the Operations Director of Lidl UK as its new boss. Part of his package included a 7- or 8-figure incentive scheme. I am convinced a similar package for a new boss at FCCN would lead to greater talent at the helm and a much quicker turnaround.

I also suggested to the FCCN board that it is not out of the question that a new, energetic and ruthless chief executive could propel operating profits to between £15m-£20m within five to ten years, which could in turn take the share price beyond 200p.

Anyway, I was told “Mr Marks thanks you for your correspondence, and has made note of your views.”

Maynard

Some extra thoughts on FCCN in this article: http://maynardpaton.com/2015/06/30/q2-2015-how-my-portfolio-looks-now/

I am a tad nervous.

Maynard

Just thought I’d repost some comments I have made about FCCN over on ADVFN:

——————-

FCCN being taken private by Marks is a risk, but there have been better times for him to shaft shareholders with a low-ball bid. The shares dropped to 20p a few years ago and, in the early 90s recession, Marks had to loan FCCN a few million quid to keep the business going. Those would have been cheaper times for going private.

There are interviews on the web I have read that suggest Marks is not keen on lettinggo. He had to relinquish the role of chief exec in the late 80s due to losses — and then watched the business suffer even further. That is also why the business has since carried a large cash pile, just in case.

FCCN instigated restructures in 2010 and 2012 and a third, far-more-radical, restructure is now urgently required. All the shops really ought to be shut and the group should become a pure licensing and wholesale business, activities from which it actually makes money.

The FCUK brand (such that it is) is almost 20 years old now. No sign yet of Marks contacting Trevor Beattie again for his marketing advice — Beattie hit upon FCUK after seeing the FCUK acronym (vs FCHK for FC Hong Kong) on FCCN faxes. It’s as if the brand was developed purely by luck — and that looks to be the case now it has run its course (at least in the UK).

Anyway, save for another Beattie-esque brand revival, we can only hope Marks launches a radical restructure to cull losses. The HQ issue might add to the urgency. He has hired new executives before, including the current Ops Director, and maybe the ‘don’t-take-fools-gladly’ attitude that seems to prevail in old newspaper interviews on the web ought to come to the fore right now.

Marks should fire his Ops Director, hire a new, dynamic and entrepreneurial chief exec (with a suitable incentive) and step down to become non-exec chairman. Old annual reports indicate Marks was prepared to give away up to 15% of the company (through his own shareholding) to a former chief exec and I would suggest him doing the same thing today to attract some top executive talent.

Mayn

More thoughts originally posted on ADVFN:

————————————————————

Well, FCCN is a bit contradictory in itself. Its Retail division consistently loses money and yet its Wholesaling and Licensing activities remain profitable.

Seems to me the brand has gone stale in the UK, and as such can no longer command the gross margins in the shops needed to cover the lease costs, staff wages etc.

But the economics of wholesaling, overseas franchising and licensing still allow FCCN to turn a profit from the those activities. Maybe that is because the brand has not gone stale outside of the UK, or the wholesalers, franchisees etc have a much lower cost base to sell FCCN products and still make money.

I cited ASOS as an example of a retailer that has not needed bricks to prosper. I did not mean to suggest its low-aspirational brand is what FCCN should aim for. I agree, FCCN should remain as a mid-luxury brand. But when the associated bricks have cost FCCN £50m of losses over the last ten years or so, you have to seriously question why you need these bricks.

‘Turning the stores around’ ultimately requires fresh product that can produce the gross margins necessary to cover the store costs etc. History suggests that is unlikely to happen anytime soon, given FCCN refreshes its range once/twice a year anyway?

To me at least, it seems obvious for FCCN to go all out and become a pure wholesale and licensing business. The firm simply makes money that way, and it would operate with fewer liabilities and less expenditure than it does now, and would generally be seen as a much better business by investors.

And yet Marks seems happy to plod on with a few stores shutting here and there, and he really is responsible for the lacklustre product and consistently woeful Retail results. Sure, the average duff store has just 4 years on its lease left to run, but roll on 2019 and we may find the better outlets have since deteriorated and today’s manageable leases have suddenly become tomorrow’s onerous millstones. We then could easily find ourselves in the same situation as now.

It’s best if Marks bit the bullet now with Retail. Either that, or he should step back and hire a new CEO that can do the job for him.

Mayn