02 March 2017

By Maynard Paton

Quick update on Tristel (TSTL).

Event: Interim results, City presentation and investor webinar for the six months to 31 December 2016 published 23 February 2017

Summary: These first-half figures were slightly better than I had expected, with the finer details confirming December’s AGM statement had downplayed the group’s underlying progress. Impressive 20%-plus revenue advances — both in the UK and abroad — were delivered by the group’s main medical disinfectant products, while adjusted profit would have soared 29% were it not for the costs of entering North America. Sadly it remains anyone’s guess as to when those costs will first see any payback. Nonetheless, TSTL remains on course to meet management’s ambitious three-year growth projections… and the shares are priced accordingly. I continue to hold.

Price: 170p

Shares in issue: 42,403,417

Market capitalisation: £72m

Click here for all my previous TSTL posts

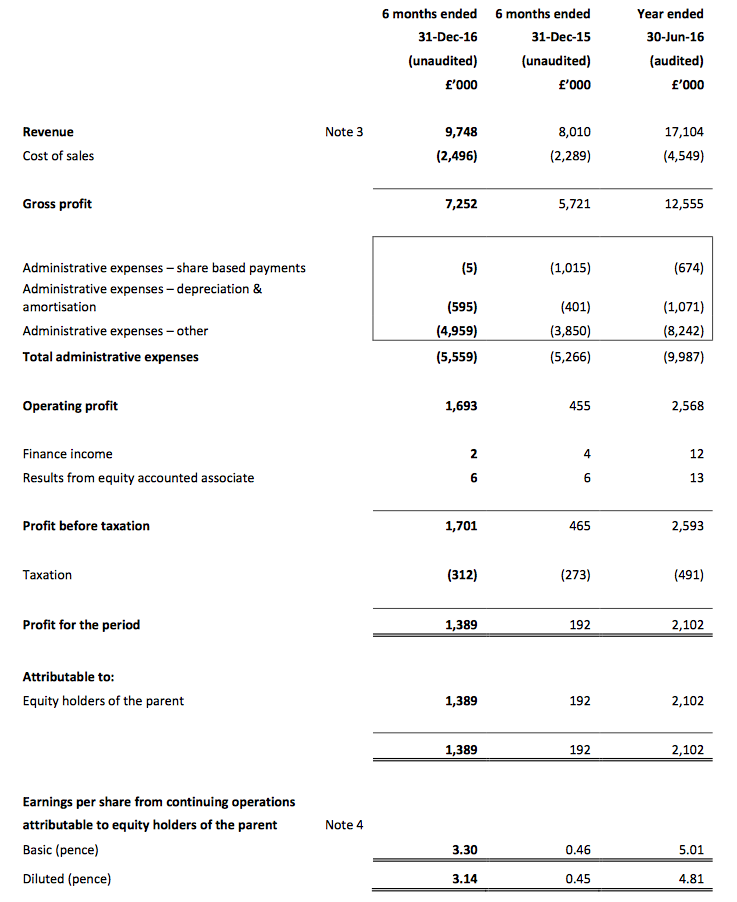

Results:

Picture:

My thoughts:

* My profit guess was just £26k short

These half-year results were slightly better than I had anticipated — and were far more enjoyable to read than the interim figures from this time last year!

December’s AGM statement had already indicated the first-half pre-tax profit (before share-based payments) would be “no less than £1.6m”, and my guess of £1,680k was not far off the actual £1,706k.

I was impressed by TSTL’s 22% total revenue advance, and reassured in particular that UK revenue — which had apparently stalled this time last year — had climbed 9%. Aided partly by the weaker GBP, sales to overseas market boomed 45%.

Alongside favourable foreign-exchange movements, TSTL’s top-line performance was boosted also by a £150k bulk purchase of discontinued products by the NHS, as well as the group’s acquisition of its Australian distributor.

TSTL’s presentation suggested underlying revenue grew by 12% adjusted for the currency movements, the bulk purchase and the Australian transaction.

Also, these H1 numbers included an extra £200k-plus of costs associated with regulatory work for various new markets (including North America). Excluding those costs — and share-based payments, too — reported operating profit would have soared 29%.

Moving higher, too, was the half-year dividend — up 23% to 1.4p per share.

However, TSTL’s 40:60 dividend-split policy suggests the full-year distribution will be only 5% ahead of last year’s 3.33p per share payout at 3.5p per share.

* Core UK product revenue climbed 20%-plus

October’s annual results showed TSTL’s UK division reviving during the second half and I was pleased that momentum extended into this H1.

The headline figures said first-half UK revenue gained 9%. However, the core instrument disinfectant products (including TSTL’s popular wipes) — alongside the fluids used to clean hospital floors and surfaces — witnessed their combined revenue surge 26%.

Even adjusting for the aforementioned NHS bulk buy, core UK product revenue advanced 21%:

| UK Revenue | H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | H1 2017 | ||

| Instrument (£k) | 2,621 | 2,469 | 5,090 | 2,695 | 3,025 | 5,720 | 3,478 | ||

| Surface (£k) | 586 | 583 | 1,169 | 620 | 633 | 1,253 | 683 | ||

| Total 'core' (£k) | 3,207 | 3,052 | 6,259 | 3,315 | 3,658 | 6,973 | 4,161 | ||

| Other (£k) | 1,799 | 1,775 | 3,574 | 1,802 | 1,591 | 3,393 | 1,394 | ||

| Total (£k) | 5,006 | 4,827 | 9,833 | 5,117 | 5,249 | 10,366 | 5,555 |

Other UK revenue declined as TSTL abandoned old products that do not use the group’s central chlorine-dioxide chemistry.

(It is notable that TSTL’s H1 statement and presentation barely mentioned the divisions that serve veterinary practices and clean rooms. These operations have surely now become ‘non-core’.)

Management remarks during the results webinar and City presentation suggested the UK could still offer “a lot of growth”.

Apparently, “infection prevention is probably the most important thing UK hospitals are dealing with” at present. Also supplied were anecdotes of hospitals placing the infection-control budget ahead of other departmental spending.

Claims were made, too, about a “diminishing number” of antibiotics that were useful for treating hospital infections.

Furthermore, the development of new medical instruments, as well as the opening of new hospital areas, were touted as reasons for potentially greater demand for TSTL’s wipes and foams in the UK.

* Germany and Australia lead overseas revenue higher

TSTL’s overseas operations continue to perform very well.

Total foreign revenue jumped 45%, or 29% without the favourable currency movements. International sales now represent 43% of the top line.

I calculate overseas revenue from the main wipes and disinfectant products jumped 64% during H1:

| Rest of World Revenue | H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | H1 2017 | ||

| Instrument (£k) | 1,823 | 2,415 | 4,238 | 2,307 | 3,070 | 5,377 | 3,801 | ||

| Surface (£k) | 86 | 108 | 194 | 65 | 97 | 162 | 96 | ||

| Total 'core' (£k) | 1,909 | 2,523 | 4,432 | 2,372 | 3,167 | 5,539 | 3,897 | ||

| Other (£k) | 497 | 572 | 1,069 | 521 | 678 | 1,199 | 296 | ||

| Total (£k) | 2,406 | 3,095 | 5,501 | 2,893 | 3,845 | 6,738 | 4,193 |

I mentioned in October that it was becoming clear that TSTL’s direct overseas operations were more productive for the group than the foreign independent distributors.

Certainly that remains the case, with German revenue being a particular highlight.

Sales from TSTL’s Berlin office, which also serves Austria, Switzerland and now Poland, soared an underlying 62% to £1.5m.

Back in October, TSTL’s executives said they could “imagine a scenario” when the German unit could one day generate as much revenue as the UK (i.e. almost £11m).

At the latest presentation, that scenario was upgraded to “no reason [why] German sales won’t [one day] dwarf UK sales”.

Australia also appeared impressive.

Purchased for £1.1m during August, the new subsidiary (it was previously an independent distributor) was said by management to have delivered a £100k profit during the first four months of ownership.

For some perspective, statements made during July’s Open Day suggested the Australian acquisition could deliver at least an extra £100k profit during its first full year of ownership.

Management reckoned underlying volumes at the Australian division improved by between 5% and 10% during the first few months of ownership.

* I did not dare ask about Monte Carlo

I’m grateful these figures did not provide any share-option headaches.

This time last year TSTL owned up to a £1m option charge following the implementation of a rather cavalier incentive scheme.

Then in October, TSTL’s annual results showed a £341k ‘refund’ after the group’s option calculation was changed from Black Scholes to Monte Carlo.

I wrote at the time that I had no idea about which method was more suitable, and that one day I would have to study exactly how the cost of share-based payments are calculated… and why companies can use different methods and arrive at different values.

I must admit that I did start to evaluate option charges, but I did not get very far before I became somewhat bamboozled by all the calculations.

At least these H1 results showed a share-option charge of just £5k. I did not dare ask management at the presentation whether that £5k charge was derived from Black Scholes or Monte Carlo.

* Still nothing definitive submitted to the FDA

There were no new developments on TSTL’s plan to enter North America.

If you recall, TSTL hopes to launch a handful of products in the United States and Canada within the next few years. Management has previously estimated the total market size in the States for just two particular disinfectants to be £18m — which compares well to current group sales of £19m.

TSTL claimed it was “progressing satisfactorily” with its North American project, although I get the impression the whole venture is taking far longer and requiring far more resources than initially expected. I recall the original timescale for receiving a regulatory approval was June this year.

Anyway, after two meetings with the US Food and Drug Administration, management comments at the City presentation confirmed TSTL had yet to submit any definitive product application to the agency.

Instead, the company is currently embarking on various in-depth product tests and management did admit there was a risk the results and data may not satisfy the FDA.

Indeed, I thought it a tad ominous that management used the adjective “tortuous” to describe the FDA’s demands for ensuring the disinfectants continued to work properly right until the end of their shelf lives.

I should add that management claimed it would be “almost inconceivable” for all of the FDA testing and applications to eventually come to nothing.

I can only hope the FDA submissions will all be worth it. One casualty perhaps of the North American project is the South American market, whereby plans to enter that continent trumpeted 18 months ago look to have been shelved.

* It could be too soon to expect another special dividend

Once again I could not find fault with TSTL’s accounts.

October’s City presentation had seen management envisage the weaker GBP leading to higher chemical costs and gross margins perhaps of 71% for the current year (versus 73% for 2016).

In the event, these H1 numbers revealed a 74% gross margin — with further manufacturing efficiencies helping to sustain profitability. In turn, the pre-tax margin was a decent 17.5% and in line with the group’s target for the next three years.

(Notably, the pre-tax margin would have been a super 20% had TSTL not spent £254k on plans to launch into North America and other overseas countries.)

Cash generation was satisfactory and money in the bank ended the half at £3.9m.

TSTL stated last year that it intended to retain cash reserves in excess of £3m, and has twice paid £1.2m special dividends when the cash position topped £4m.

However, management was keen to stress during the webinar and presentation that the £3m figure was cited last year — which appeared to hint the number could change.

The message I took (perhaps mistakenly) from these comments was that more cash could be needed on standby for North America, and so the likelihood of yet another £1m-plus special dividend may be less now than it was before.

At least TSTL confirmed its expenses for North American regulatory approval would remain at £300k for H2 and £300k for the next financial year.

Management also claimed at the presentation that the next few years would not see any major capex demands and perhaps only a 10% increase to the headcount.

The balance sheet continues to carry no debt and no pension obligations.

Valuation

Adjusting the share-based payment charge to a less cavalier £100k, I calculate TSTL’s trailing operating profit to be £3,370k. Adding back £290k of North American investment costs gives me £3,660k.

After tax at the forthcoming 19% standard UK rate, I arrive at earnings of £2.9m or about 6.9p per share.

Subtract the cash position of 9p per share from the 170p share price and the underlying trailing P/E comes to about 161p/6.9p = 23.

Assuming TSTL’s top line grows at 17% for the current year to £20m, and then compounds at the top end of the group’s 10%-15% guidance, I reckon revenue by 2019 could top £26m.

Assuming, too, that TSTL can meet its 17.5% pre-tax margin target, I estimate earnings for 2019 may be 8.9p per share. But if I assume a 20% margin for 2019 (by ignoring North American costs), then I arrive at a 10p per share earnings guess.

That 10p per share estimate would bring the possible 2019 underlying P/E down to 15 based on the cash pile perhaps having advanced to 20p a share.

I admit there may be a little optimism involved with those assumptions, but I suppose there is a chance the projections could actually prove to be accurate.

All told, I think it is fair to say TSTL’s current valuation pretty much prices in the group meeting its three-year growth targets. Superior medium-term returns from here will probably depend upon progress with the North American project, significant revenues from which appear very distant at present.

Maynard Paton

Disclosure: Maynard owns shares in Tristel.

Nice piece, Maynard

Had a look at Tristel in the past and thought the margins were too thin, that was three years ago. Having missed out on the ride, do you think the shares are priced in for this year?

Hello Walter

Thanks for the Comment.

I think the current share price is generally pricing in management’s three-year projections (of revenue growing at 10-15% a year and margins being sustained at 17.5%). As I mentioned in the blog post, superior gains from here will most likely be achieved following some positive North American developments. That said, I suppose better-than-expected trading at the existing business could deliver healthy share-price gains… although revenue from TSTL’s core products are already growing at 20% or so at present.

Maynard

Thanks for the feedback, Maynard.

Excellent report, as usual, MP.

Delay on entering the US market is pretty normal I guess.

Buying the 90p dip last July was a gift from the gods.

apad

Hello apad

Thanks for the Comment — I got there in the end after some time away from the computer.

Maynard

Hi Maynard,

I have registered for the Tristel open day now, thanks for pointing this out.

Have you looked at the competitor and regulatory environment for this company? Nanosonics (it has a UK website) has launched a product called Trophon that uses ultrasound and hydrogen peroxide to sterilise probes. This Australian company claims that the HSE has issued Scottish and Welsh guidance that states that using just wipes is the least acceptable method for sterilisation, it is also very well established in the US, 22% of the market (8700 units sold at $5k each). (https://www.nanosonics.co.uk/clinical/high-level-disinfection-hld-why-when/). This is probably the reason for the Tristel comment that acceptance in the USA will be tortuous, basically the Trophon method is internationally accepted. Further more Tristel does not make any claims about removing HPV (human papilloma virus) from probes a key selling point for trophon.

Roger

Hello Roger

Thanks for the comment. I have put my thoughts in a comment below.

See you at the Open Day.

Maynard

Tristel (TSTL)

Submission to EPA & subsidiary incorporated in USA

TSTL has issued the following statement:

———————————————————————————————————————————–

Tristel incorporates a wholly-owned subsidiary in Delaware, USA, and makes a submission to the Environmental Protection Agency for its Duo chlorine dioxide disinfection foam

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces that it has established its presence in the United States by incorporating a wholly-owned subsidiary in the State of Delaware. This initiative is part of the Company’s stated intention to enter the North American infection prevention market. This plan was unveiled in the Company’s preliminary results announcement in October 2015.

In pursuit of this plan, on 30 June 2017 Tristel made a submission for regulatory clearance by the Environmental Protection Agency (“EPA”) of its Duo chlorine dioxide disinfection foam. The Company expects to receive approval in the second half of its financial year commencing 1 July 2017. Following EPA federal approval, the Company will then need to secure state-by-state approval before it can commence selling Duo.

The EPA clearance will enable Duo to claim intermediate disinfection of all non-porous surfaces, including those of medical instruments. This is Tristel’s core activity worldwide and accounts for approximately 80% of the Company’s revenues.

In addition, the Company continues to develop two submissions to be made to the Food and Drug Administration (FDA) for 510(K) clearance in respect of Duo. The 510(K) approval will permit Duo to claim high-level disinfection of medical instruments. Tristel expects to complete and make these submissions during the first half of its financial year commencing 1 July 2018.

In all other markets worldwide, Duo is classified as a high-level disinfectant. It is important to note that there is no difference in formulation or performance of the Duo product submitted to the EPA and the Duo product that will be submitted to the FDA in due course.

The Company continues to develop a further four additional submissions to be made to the EPA during the coming 12 months for other products selected from its global portfolio. These products are also chlorine dioxide based.

Paul Swinney, CEO, comments: “We are very pleased with the progress that our team has made in reaching our first major milestone to enter the North American infection prevention market – a submission to the EPA for approval of our Duo chlorine dioxide foam. Attaining this milestone keeps us on track to achieve our objective of generating revenues in the North American market during the 2018-19 financial year.

“Duo has patent protection in both the United States and Canada.

“We are now formulating our manufacturing and distribution strategy for North America and will provide further detail at the time of our preliminary results announcement in October.“

————————————————————————————————————————————

Here is the first paragraph of interest:

“In pursuit of this plan, on 30 June 2017 Tristel made a submission for regulatory clearance by the Environmental Protection Agency (“EPA”) of its Duo chlorine dioxide disinfection foam. The Company expects to receive approval in the second half of its financial year commencing 1 July 2017. Following EPA federal approval, the Company will then need to secure state-by-state approval before it can commence selling Duo.”

This may be good news.

I could have got this wrong, but it appears TSTL is now hoping to gain regulatory approval for a medical-device foam disinfectant in the States via the EDA. Approval should be quicker than the FDA, but EDA approval will only classify the disinfectant as ‘intermediate’ rather than the FDA’s ‘high level’.

The table below has been extracted from TSTL’s interim results presentation from February:

It shows the proposed EPA submissions relating to products used for cleaning hospital surfaces (floors, consoles, etc) and washer rinse management, but not for medical devices.

However, this RNS text…

“The EPA clearance will enable Duo to claim intermediate disinfection of all non-porous surfaces, including those of medical instruments.”

…suggests the ‘intermediate’ disinfection status gained from the EDA will allow the foam to be used to clean medical devices.

So this development seems promising and could be significant, because at present the majority of TSTL’s revenue is earned from products that disinfect medical devices. And cleaning medical devices should be where the big money is in the States.

That said… I have no idea whether EDA approval will prompt US hospitals to use the foam to clean medical devices in practice. If it would, then why should TSTL bother trying to obtain FDA approval for ‘high-level’ disinfection status?

Also, this RNS is the first where TSTL management has talked about state-by-state approval. I am not sure whether gaining state-by-state approval following EDA approval will be a formality or something more onerous.

Anyway, here is the next paragraph of interest:

“In addition, the Company continues to develop two submissions to be made to the Food and Drug Administration (FDA) for 510(K) clearance in respect of Duo. The 510(K) approval will permit Duo to claim high-level disinfection of medical instruments. Tristel expects to complete and make these submissions during the first half of its financial year commencing 1 July 2018.”

So a submission to the FDA on or before 31 December 2018 — that seems a long time to wait. I think the original plan back in October 2015 was to have received FDA approval by 30 June 2017!

Following this RNS, I’ll endeavour to discover via TSTL’s forthcoming Open Day:

* what the likely take-up rate within the US market will be for an ‘intermediate’ disinfectant for cleaning medical devices

* whether state-by-state approval is a formality or onerous

* whether FDA approval then requires state-by-state approval

Maynard

Tristel (TSTL)

Strategic Investment

I must admit I was worried when I initially skimmed today’s second RNS and saw $750k being invested in an Israeli business. However, further reading provided some encouraging snippets.

Here is the full text:

———————————————————————————————————————————–

Tristel makes a strategic investment in Mobile ODT, an Israeli company that is combining smartphone technology with hand-held medical devices for point-of-care diagnostics

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces that it has made a US$750,000 investment in Mobile ODT (“MODT”) an Israeli company that is combining smartphone technology with hand-held medical devices to make diagnostics available at the point-of-care (www.mobileodt.com).

Tristel is taking a 3.27% equity stake. Francisco Soler, Chairman of Tristel, and Paul Barnes, NED, are also making personal investments in the fund raising, for which the lead investor is Orbimed Healthcare Advisors (www.orbimed.com). MODT has raised total funding of approximately US$10.7 million. Tristel will have a seat on the MODT board of directors.

MODT has developed the proprietary EVA System, a smart-phone based medical device, which enables any healthcare provider, anywhere in the world, to examine patients for indications of cervical cancer using a technique known as colposcopy. The product was approved by the USA FDA in 2016.

The EVA System is especially relevant in lesser-resourced healthcare settings as it is significantly less expensive than the traditional examination device (colposcope). Furthermore, it is portable and self-contained, and enables consultation with medical experts who may be located remotely from the examination site.

Tristel’s Duo high-level disinfectant foam is the perfect partner for EVA – as it is portable and self-contained, has no requirement for water or power supply, requires no maintenance, and can be used with minimal training. Duo is an eminently affordable disinfection option. Tristel and MODT intend to combine EVA and Duo into an integrated offer to healthcare providers, with the MODT App enabling healthcare providers to ensure compliance with best disinfection practice.

The EVA System requires high-level disinfection given the area of the anatomy the device examines, and very importantly must be disinfected by a chemistry that can destroy HPV (Human papilloma virus). HPV is responsible for 5% of all cancers worldwide, 99.5% of cervical cancers, and is a leading cause of oral, throat, anal and genital cancers in both women and men.

Whilst HPV is widely believed to be sexually transmitted, numerous studies have shown that the virus also exists on gynaecological equipment. Duo has recently been proven in pioneering work by Dr Craig Meyers PhD, Distinguished Professor of Microbiology and Immunology, Penn State College of Medicine, Hershey, USA to be effective in deactivating HPV 16 and 18 strains in a two-minute contact time.

HPV 16 and 18 are the virus strains most closely associated with causing cervical cancer. The only other commercially available disinfectant to have proven efficacy against HPV 16 and 18 in the same test conditions is Trophon (www.nanosonics.com.au), a fixed location disinfection machine which would be difficult to use in lesser-resourced healthcare settings, and requiring capital investment, unaffordable in many situations.

Paul Swinney, CEO, comments: “There are 5.8 billion people worldwide who have no access to healthcare that we would consider adequate, yet a great number of this population has access to a mobile phone.

In low resource settings, whether on the African continent or in rural America, medical care is provided by nurses, trained to a general level of medical knowledge. Smartphones, combined with devices that can illuminate a part of the body and take a picture, or carry out an ultrasound scan, enable community nurses to examine the patient and transmit images for consultation provided remotely. In time, artificial intelligence will provide diagnosis. This is a new frontier in medicine that is developing rapidly.

“During our twenty-year experience in infection prevention, we have observed that disinfection is often an afterthought in medical device innovation. Our high-level disinfectants, dispensed in portable, easy-to-use formats of foam, wipes and sprays, are the only way in which these new frontier devices can be disinfected safely in a community clinic in a remote area to the same level that would be demanded in a sophisticated Western European hospital.

“MODT is at the forefront of this exciting development in healthcare, and has had the foresight to acknowledge the importance of disinfection. With its focus on women’s health, a key area for Tristel, we are making this investment to cement our relationship. MODT plans next to make its technology platform available to Ear, Nose and Throat medicine (ENT), another stronghold for our Company. Oropharyngeal cancers are one of the fastest growing types, and are linked to HPV infection.

“We believe our participation in the ownership of MODT will not only benefit Tristel strategically, but will also produce an attractive return for our own shareholders in time. We take great comfort in investing alongside the leading healthcare investor, Orbimed.”

———————————————————————————————————————————–

TSTL management has highlighted this EVA System during at least one results presentation. A picture of the device is shown in the red box:

This is probably the most important line within the RNS:

“The product was approved by the USA FDA in 2016.”

So the product is genuine and not some blue-sky prototype.

These next paragraphs are of interest:

“Duo has recently been proven in pioneering work by Dr Craig Meyers PhD, Distinguished Professor of Microbiology and Immunology, Penn State College of Medicine, Hershey, USA to be effective in deactivating HPV 16 and 18 strains in a two-minute contact time.

HPV 16 and 18 are the virus strains most closely associated with causing cervical cancer. The only other commercially available disinfectant to have proven efficacy against HPV 16 and 18 in the same test conditions is Trophon (www.nanosonics.com.au), a fixed location disinfection machine which would be difficult to use in lesser-resourced healthcare settings, and requiring capital investment, unaffordable in many situations.”

TSTL management has named Nanosonics/Trophon within its results presentations for investors to study, which is unusual in itself. It would be even more unusual to mention a rival if the rival’s product was better.

So this brings me on to Roger’s comment:

“Have you looked at the competitor and regulatory environment for this company? Nanosonics (it has a UK website) has launched a product called Trophon that uses ultrasound and hydrogen peroxide to sterilise probes. This Australian company claims that the HSE has issued Scottish and Welsh guidance that states that using just wipes is the least acceptable method for sterilisation, it is also very well established in the US, 22% of the market (8700 units sold at $5k each). (https://www.nanosonics.co.uk/clinical/high-level-disinfection-hld-why-when/). This is probably the reason for the Tristel comment that acceptance in the USA will be tortuous, basically the Trophon method is internationally accepted. Further more Tristel does not make any claims about removing HPV (human papilloma virus) from probes a key selling point for trophon.”

I looked at Nanosonics earlier in the year, but I must admit that was before the group’s interim results. The associated presentation makes for interesting reading.

Here is the Trophon product:

You put the device in the machine to clean, press a button, and wait for 7 minutes. Job done. No waste produced, no expertise necessary. I must admit I think that beats TSTL’s wipes system, which is done manually and allows for human error.

But Trophon costs more. Not only do you have to buy the machine (Rog says $5k), but there is also the accessories, consumables and service contract:

And I guess you have to buy a machine for each room in the hospital where the devices are used on patients. So the hospital bill for Trophon could be expensive.

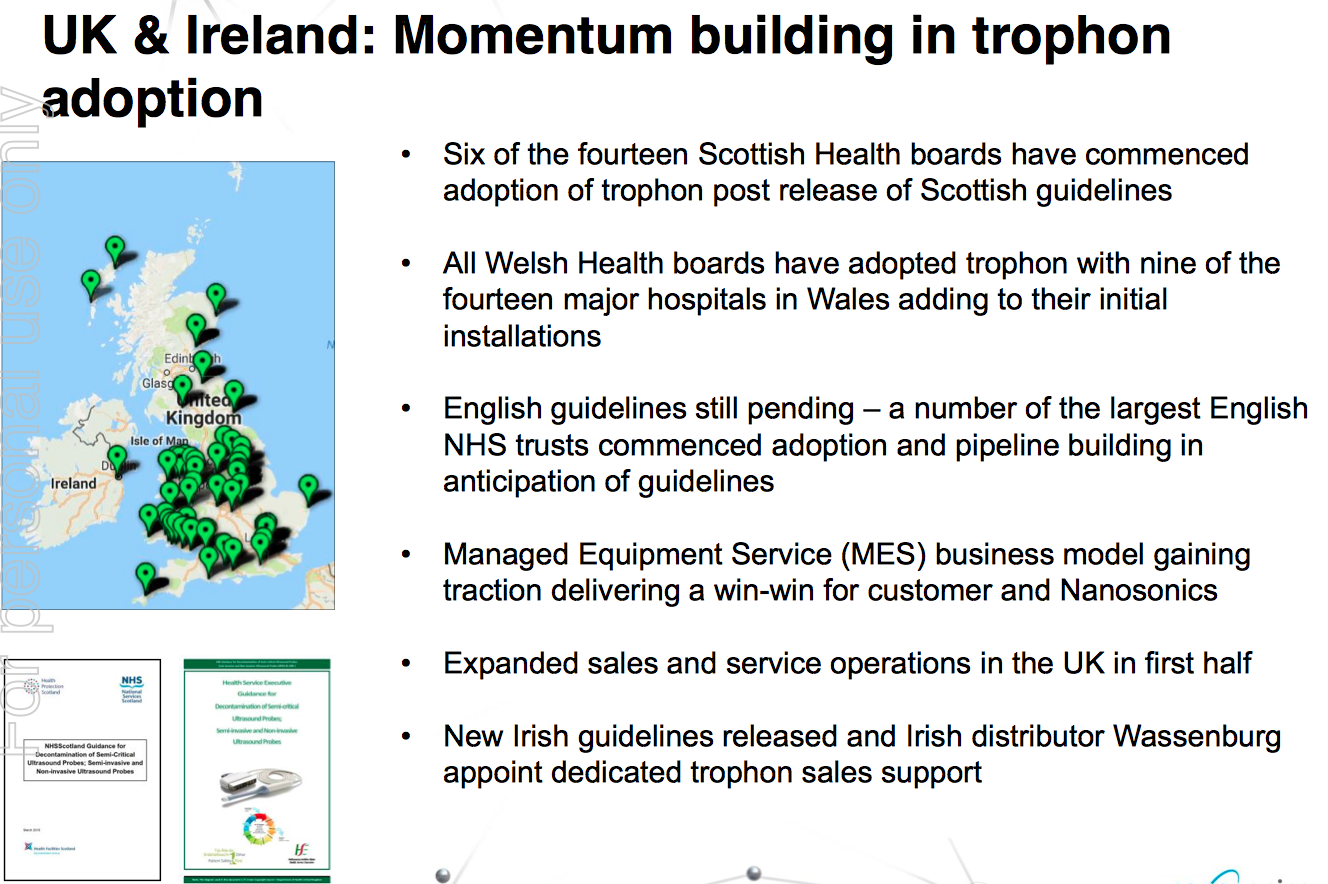

I must admit that Nanasonics’ inclusion in Scottish and Welsh NHS guidelines is a bit worrying:

NHS England is apparently on the verge of issuing guidelines that favour Nanosonics, too.

However, I have skimmed through the Scottish and Welsh NHS documents (I could not access the Irish one) on the Nanosonics UK website and they are not exactly stating hospitals must use Trophon.

The Scottish doc is non-committal on what exact product hospitals should use, but does indicate cost ought to be a factor in deciding what to buy.

The Welsh one does indicate hospitals ought to “investigate and work towards the use of automated systems“, but does mention the word ‘cost’ 40 times.

So all told, I dare say there is room for both TSTL and Nanosonics in the UK and abroad. It will boil down to cost and whether healthcare provides wish to pay large sums for automation and less chance of human error, or a lower cost and perhaps greater chance of human error. I think the biological effectiveness of both TSTL’s wipes and Trophon is the same. I reckon UK hospitals will use a mix of TSTL and Trophon, and perhaps there could be room for both in the long run. I reckon cost will always be a purchase factor, though, which will hamper Trophon.

Also, the HPV comments have been addressed by TSTL today, with recent research from ‘Dr Craig Meyers PhD, Distinguished Professor of Microbiology and Immunology, Penn State College of Medicine, Hershey, USA’. So that seems to be one less thing to worry about.

Maynard

Tristel (TSTL)

Further thoughts on Submission to EPA and Strategic Investment

I’ve pondered further on yesterday’s two RNSs. I wonder if they are connected.

I’ve looked at the mobileodt.com website.

This article indicates the smartphone colposcope costs $3.6k, while this article indicates FDA approval was received on 19 December 2016.

The latter article also says:

“The tragedy of cervical cancer – strongly addressed in major urban areas – still plagues much of America, where it is increasingly difficult for a woman to get a timely appointment with an expert gynecologist. Rural residents, specifically, disproportionately bear the burden of the 12,000 cases of cervical cancer each year. In part, this is because “approximately half (1,550, 49%) of the 3,143 U.S. counties lacked a singly ob-gyn, and 10.1 million women (8.2% of all women) lived in those predominantly rural counties.”*”

So there is a market for these devices in the States. As TSTL is to supply the disinfectant for these smartphone colposcopes, I presume the disinfectant requires some sort of approval.

As such, maybe the EPA submission for ‘intermediate’ disinfectant status for the Duo foam relates to the tie-up with MobileODT, and that EPA approval will be enough to allow the Duo foam to be used on those devices. Well, that is my guess.

Given the two RNSs were issued on the same day, I am sure there must be some connection.

Maynard

Hi Maynard,

Thanks for your very thorough analysis and updates.

On the questions that you pose for the forthcoming Open Day:

* what the likely take-up rate within the US market will be for an ‘intermediate’ disinfectant for cleaning medical devices

‘intermediate’ disinfectant is only for devices that are to be used outside the body e.g. ultrasound probes for pregnant women i.e. placed on the woman’s stomach.

The vast majority of Tristel’s cleaning will be for probes that are used internally and for those they need FDA approval.

* whether state-by-state approval is a formality or onerous

i suspect its a formality, its about environmental protection and disposal of noxious substances

* whether FDA approval then requires state-by-state approval

No it doesn’t, FDA approval is across all states. But you still need the EPA approval too which is state by state.

On the trophon product:

This product seems well established in the US, where medicine is highly litigious. I suspect that the nanosonics product is more acceptable to Doctors and the FDA because it provides a fool proof way of establishing whether a probe has been sterilised. I’ll be asking why Tristel has not developed a similar box for the US market, particularly if this is now the accepted way of doing things there (evidenced by maybe 45k units installed)?.

Hello Roger

Thanks for the informative reply. I had hoped ‘intermediate’ disinfection may have been able to clean instruments beyond ultrasound. Clearly my speculation about cleaning the smartphone device was wrong and that product will need an FDA-approved disinfectant.

Now I am pondering when exactly we will see significant US revenue. FDA approval is set for on or before 31 December 2018, so approval a year after that say? So the first revenue could be collected in 2020, with 2021 being the first opportunity perhaps for any significant revenue. That is a long time away.

Looking at the interim Nanosonics presentation, it seems Trophon has an installed base of >10,700 units in North America and the addressable market there is c40,000. So yes, Trophon seems established and I agree it is more foolproof that any manual cleaning method.

What I don’t understand is what disinfection process US hospitals currently use (aside from Trophon). I’ve asked TSTL management, and it has suggested the hospitals use antiquated techniques with bleach. Clearly not all hospitals do though, given the Trophon numbers above. And I can’t believe the hospitals dare use antiquated methods because of the litigation risk.

Also, I have asked TSTL management about the number of infections in the US that the group’s products could have prevented — to try and judge the ‘market opportunity’ there. Management said there were no published numbers. If that is the case, then how does management know the US market opportunity will provide a worthwhile return?

I mean, it should be easier to sell a new disinfectant product in the US if infection rates are high, as opposed to if infection rates are low because US hospitals are already using an effective product (e.g. Trophon).

Maynard

Tristel (TSTL)

Reader question

A reader e-mails:

——————————————————————————————————————————-

Dear Maynard

Your latest post emphasized the importance of management adaptability, given that ‘moats’ may be harder to come by.

Your detailed discussion of Tristel’s attempt to both navigate its complex regulatory environment and meet the threat of new entrants, made me wonder whether this is an example of where management may be tested to the limit. The sector seems to attract new entrants given its potential size and the relative low-cost of developing new techniques. In fact, the regulatory compliance costs seem to be the main barrier to entry.

Your effort to understand how the labyrinth of healthcare regulations globally and shifting purchasing policies in the UK might impact Tristel indicate a large degree of uncertainty. Are you relying on that skilled management team to navigate this uncertainty or do you think their core business does have certain ‘moat-like’ qualities that protect against the uncertainty and/or threats?

Given your general preference for more modestly priced shares with stable future profits baked in, Tristel seems to be highly priced in the face of such uncertainty.

Best regards as ever

——————————————————————————————————————————-

Yes, I would agree TSTL’s management is being tested right now.

My write-ups on TSTL have indicated the FDA approval process has taken much longer than expected, and the associated costs have ratcheted up, too. Plus the board has had to manage overseas efforts, in particular the Australia deal, as well as the ups and downs with the NHS. So there is a lot going on for what remains quite a small company.

It is not obvious to me the sector seems to attract new entrants, and regulatory compliance — not just the cost — is a significant hurdle for rivals to clear.

You see, you have to prove to hospitals via proper studies that your product actually works, and after that you then have to persuade hospitals that your product is easier/much cheaper/more effective to use than the existing alternatives. TSTL has, for instance, moaned for years about the laborious process of becoming accepted in the UK, and I dare say any newcomers will face the same long-winded acceptance process.

I think TSTL’s products do have some ‘moat-like’ qualities. I have sat in on a few management presentations and questions about patents, formulations, copycat competition, etc regularly crop up and the answers given seem credible to me (and I am quite cynical about these things).

Where things are somewhat less clear concern alternatives that adopt a completely different cleaning technology/approach — such as Nanosonics and its trophon machine. It would be useful to gain the perspective of a hospital on TSTL’s wipes versus trophon.

All told, I think at present I am relying more on TSTL’s products than ultra-skilled management. I would like to think that the products, once established for use in a hospital, can then sell themselves over time.

Yes, TSTL’s share price is highly priced and when I last looked, it effectively priced in the group’s own growth forecasts for the next few years. So any slip-up could lead to a de-rating. Also, sizeable US revenues appear years away, yet I dare say the current share price is factoring some success there already.

Anyway, I guess all this reflects one of the better problems to have when investing.

I brought TSTL shares a few years ago when the valuation did not require detailed knowledge of the group’s rivals, potential, competitive strengths etc to justify a purchase. But as the business has advanced, the attractions have become more apparent and the share price has climbed… and so holders/new buyers now have to do more work to assess whether the present valuation is justified.

Maynard

Hi Maynard,

I looked at my notes for the AGM meeting in 2014, when I last visited TSTL and they said that the current method used in the US was glutaraldehyde. I suspect that this is still the case, with probes being soaked in this disinfectant and then washed in a machine. Glutaraldehyde is a more harmful agent than chlorine dioxide, but it works so there is no infection risk. I doubt whether infection rates are any worse in the US than anywhere else in the world and more to do with human error than the disinfectant used. So phasing it out has big potential only from the environmental viewpoint and protection of employees from noxious agents. Trophon’s method generates even less harm and has the added advantage of “proof of cleaning” to the operator (something very important in the USA’s litigious environment). The move away from glutaraldhyde takes time because Clinicians are just so damn conservative. I’m sure that if you asked the FDA (and certainly the EPA) they would be encouraging of the move away from glutaraldehyde behind the scenes.

On FDA timings, in my experience it takes 3 months from submission to approval, as long as you have successful pre-discussions with them, so the timescales being quoted by TSTL are to do with the trials they are being asked to do by the FDA and not the submission process.

Finally have you noticed the big share sales by soler (2.5m) and swinney (689k) and Barnes (140k) on 12/4/17 (see Sharepad) . Strangely there was no RNS on this and the TSTL website still has director shareholding at the levels on 31mar17

Hello Roger

Thanks for the further comments. Ah yes, I now recall comments about glutaraldehyde. Three months from submission to approval sounds good to me. The shares sales were part of a placing, with the RNS issued on 7 April. TSTL’s website ought to have been updated to reflect the placing.

Maynard

Tristel (TSTL)

Notes from the Nanosonics AGM

Nanosonics is an Australian company that supplies a machine called trophon that disinfects medical instruments, and was been referred to by TSTL.

Here is a useful post from hotcopper.com.au from November 2016. I have lifted the complete text:

———————————————————————————————————————-

I have been a shareholder for 3 years now and Nanosonics is my one of my largest holdings. Here are my general notes and random snippets from the NAN AGM.

Firstly, I must say that I think NAN is one of the best emerging growth stories on the ASX.

Random notes in no particular order:

We have laid a solid foundation for fantastic growth. We have increased our R&D spending by 50% (currently 17% of sales) and are working on a suite of products. Steven Farrugia (co founder of some of ResMeds early patents) has already made a big impact on the company. There was a hint today that the new products will also have a consumable element building another layer of recurring revenue into the future.

The major manufacturers are coming to us and telling us what is next in their pipeline so we can build associated products to go with them (confirmed that this is other than just probes!) This is potentially huge. These new products have been requested by our customers at the point of care, address currently unmet needs and address significant markets.

We are working hard on the Japanese market which is considered the second largest market in the world for our products. First revenues from Japan expected in FY 18. We are doing research on the Chinese market with a view to seek approval in due time. We have had strong distributor demand and interest from China but we must go slow and carefully into that market. We have India on the radar but one thing at a time.

We have significantly improved our board and management with the inclusion of Steven Farrugia (Ex ResMed original), Steven Sargent (20 years with GE and involved when GE did a deal with NAN and took a stake in the company) and Marrie McDonald (CSL board and ex member of Australia’s take over panel and and a lawyer specialising in mergers and acquisitions.) We have made significant improvements in our manufacturing with Gerard Putt (ex ResMed) finding ways to make it a leaner operation.

The company is working hard to educate existing clients (this is a long term process) on the benefits of sterilising all probes not just ones used for invasive procedures. One installed trophon on average generates around $3000 a year in consumable revenue. The exact amount NAN gets directly depends on who sold the unit etc. However, if we can get our customers to just do “one” clean at the end of each day for non invasive probes this would increase consumable revenues by 30%. Think of the snowball effect here with 1000 units being installed a month and only 25% of US market currently penetrated and ROW to come. UK next major market.

Europe is picking up. Germany, France and Middle East starting to show more movement. Get this – no current guidelines in France and sometimes they don’t even clean the probes at all! We have met with the Minister of Health in France and they are starting to review this.

We have approval for Mexico and are working on that country for next year. We are working on Brazil but looks like a 4 year approval process. Working with authorities to expedite this. Our aim is to be completely global and the standard of care. There is no completion is sight. Our biggest competition is lack of awareness and education which we are working on. Being the only automated way to kill HPV virus is attracting a lot of attention.

UK guidelines due any day (hopefully latest by end of year) and will significantly increase orders as their guidelines will say they have to go to high level disinfection that only NAN provides. Hospitals waiting for this before ordering. Interesting to note that due to the British economy we have cleverly introduced a new business model called the “Managed Equipment Service” model. This allows us to place Trophons in at no cost but include the cost of the unit into increased consumables. The pay back on the unit is about 3 years with blue sky on higher consumable sales from there.

Units have a 5 to 7 year life cycle and this helps is time our generation 2 trophon. Major services are required at 5000 cycles or run throughs. So as the installed base grows replacement of old units and servicing of existing units will contribute nicely to revenue.

Our main patents are protected out to 2026 and we continue to add new IP to strengthen this. In relation to protection on consumables – we are protected in three ways – (1) Regulatory approvals – it is the system that is approved and if anyone wanted to use a generic consumable it would have to be approved by the FDA and equivalents around the world. (2) Significant IP protection giving us legal protection (3) Validated with over 1100 probes. Manufactures will not allow any generic consumables with their probes and this took years for NAN to achieve. This is a real barrier to misuse of consumables and a nice moat.

Agreements now signed with all major OEM’s of the probes in the US so they can also sell Trophon to their customers direct. This is big. We still retain the customer afterwards for installation, consumables and service agreements.

Some good quotes from the CEO, Chairman, Management and Board – as close to verbatim as possible!

CEO – “We will be the next biggest global healthcare company to come out of Australia.”

“We are not running this company for the next quarter, next year or the next few years we are running this company for the long term.”

“Once we introduce multiple products we will have a huge audience looking at us.”

“Having the best technology in itself does not guarantee success. It is all about the people.”

“We have laid the foundation and platform for solid growth.”

“We are not a technology company we are a solutions company.”

“We are very confident that the best is yet to come.”

“There is always a budget for mandatory technology.”

“We have an internal measure – we have a say it to do it ratio of 1-1.”

Chairman “The likes of Steven Sargent and Steven Farrugia did extensive due diligence before joining the company. They got an access all areas look behind the curtain and liked what they saw. They have joined us because they believe in and can see the potential we have.”

“We are on the threshold of greatness.”

“Unlike Apple we will be able to well invest our shareholders money for the future.”

Steven Sargent – “I am very optimistic about the future of Nanosonics.”

In summary – my view only – We have first mover advantage and are going to sew this thing up. I am very pleased to be a shareholder and super excited about our future potential. I cannot think of another company on the ASX that offers this sort of growth profile, quality management, competitive moat, financial position, quality recurring earnings stream, is only really getting going and is profitable. Not financial advice and DYOR.

———————————————————————————————————————-

One interesting bit:

“Interesting to note that due to the British economy we have cleverly introduced a new business model called the “Managed Equipment Service” model. This allows us to place Trophons in at no cost but include the cost of the unit into increased consumables.”

Sounds like the NHS does not pay upfront for trophons. I wonder if the expense of these machines will prove helpful for TSTL’s much cheaper wipes system.

Maynard