02 April 2025

By Maynard Paton

Happy Wednesday! I trust your shares have performed better than mine since the start of the year.

A summary of my portfolio’s first quarter:

- Q1 return: -6.5%*

- Q1 trades: 1 Top-up (Bioventix at £30) and 1 Sell (Tristel at 352p).

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

I will do well to catch up with the FTSE 100 during 2025. The blue-chip index has powered 6% higher during this Q1, outperforming every one of my holdings. Indeed, seven of my shares declined despite the rising market.

Newsflow from my holdings has been mostly unremarkable, as demonstrated by the modest dividend improvements or unchanged payouts at Bioventix, City of London Investment, Mincon, FW Thorpe and M Winkworth. S & U has meanwhile continued to trim its dividend following adverse regulatory matters.

The subdued progress has left most of my holdings trading at prices first seen during 2017 or before, with their ratings the lowest for years. I am not short of top-up ideas.

Picking winners has certainly become harder. A quick check on ShareScope reveals only 191 of the 552 FTSE All-Share constituents — 35% — delivered share-price gains during this Q1. Over the last three years, the proportion is a woeful 33%.

You may not be surprised to learn that picking AIM winners has been even harder. During the last three years, just 20% of AIM-traded shares have moved higher.

Nonetheless, buyers remain out there for the right opportunities. I wrote about Filtronic recently, mostly to remind myself that multi-baggers do still exist!

I have summarised below what happened to my portfolio during January, February and March. (Please click here to read all of my previous quarterly round-ups). I then discuss Warren Buffett’s ‘elephant gun’ and having cash on hand to bag a bargain.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe and M Winkworth.

Q1 share trades

Bioventix

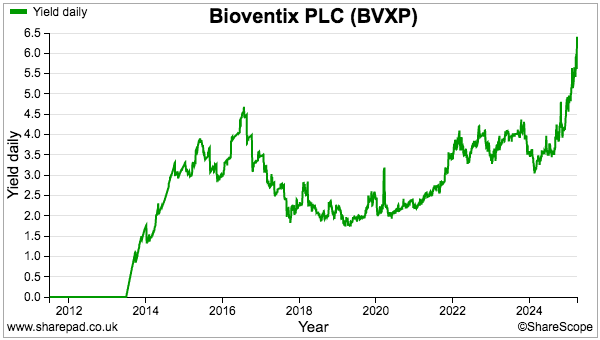

I have increased my Bioventix (BVXP) position by approximately 125% at £30 including all costs.

My top-up followed the antibody developer’s 2024 AGM and learning more about the potential for blood tests to detect the early stages of Alzheimer’s Disease (AD).

AGM attendees were told the recent emergence of AD treatments could see the “dawn of a new blockbuster era” for neurology blood tests, and that BVXP might learn within twelve months whether or not some of its AD diagnostic antibodies could become part of the industry’s “final selection“.

I am convinced BVXP stands every chance of making that final selection, and then prospering as AD blood tests eventually become mainstream.

The FY 2024 results were particularly encouraging on the AD front. They confirmed certain pipeline AD antibodies had commenced “large-scale production“ and were now generating notable R&D revenue. I concluded customers were clearly interested in the AD R&D and, with a final selection possibly due later this year, new competition would not have much time to become involved.

Indeed, I remain unsure whether BVXP has much competition for its ‘brain-derived tau’ AD antibody. AGM attendees were told the company “kind of got there first” with this particular test, and I speculate the blood-testing industry is now in too much of a hurry to consider AD latecomers. All told, I believe an established AD antibody could easily become by far BVXP’s largest source of revenue.

BVXP’s promising AD work seems to have been overshadowed entirely by the company’s commercialised antibodies going ex-growth. This week’s H1 2025 figures warned of sales up just 1% and profit down 4%, and the £24 shares are back to where they were more than seven years ago. I bought on a 5.2% yield that has since improved to 6.4%. My latest BVXP review.

Tristel

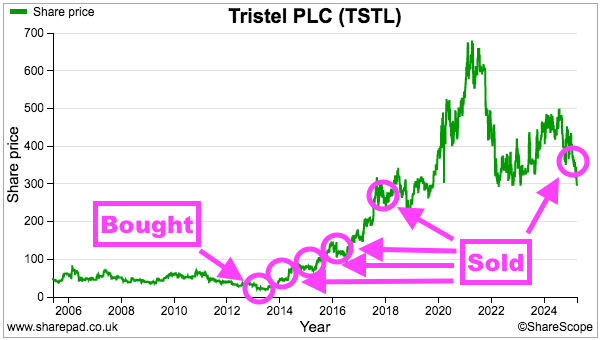

I have sold all my Tristel shares at 352p including all costs.

The disposal marks the end of an eleven-year investment that at one point rallied 14x following my 46p purchase. Although I never sold at the very top, I did manage a respectable 408% total return of which dividends represented almost 60%.

Before this Q1, I had sold at 79p during 2014, 100p during 2015, 123p during 2016 and 289p during 2017p:

My Q2 2020 portfolio review recapped in some detail how this disinfection specialist had become (at the time!) a ten-bagger. Back then I wrote:

“I have nevertheless kept the faith with Tristel — and overlooked the subsequent management mishaps — because I am confident the products are good enough to sell in greater volume no matter who is in charge.”

I have since changed my mind about who is in charge. TSTL’s executives never truly convinced me and over time the board has evolved into a depressingly standard set-up that seemingly prioritises management over shareholders.

The last straw came the other month, when the directors asked shareholders to approve an LTIP that did not publicly reveal any performance targets before the vote.

I was particularly irritated by the board devising an LTIP while the new chief executive had yet to announce the group’s financial targets (and still hasn’t). How can shareholders be sure the new LTIP correlates with those targets? I was not surprised to learn the LTIP’s minimum earnings targets were quite modest, and I now worry TSTL’s prospects may not be as bright as they once were.

Paying the former chief exec a year’s salary as a “retirement package” also seemed extremely generous given his long-time ‘over-promising and under-delivery’ of TSTL’s US expansion.

I note that at the time of my purchase, a non-exec owned 27% of the shares and soon after became chairman. He stepped down as chairman during 2018 and then started to reduce his stake. I surmise executive remuneration would be more aligned with investors if a 27% shareholder remained on the board. I was quite happy with TSTL’s previous LTIPs requiring decent share-price gains to vest. My final TSTL review.

Q1 portfolio news

As usual I have kept watch on all of my holdings. The Q1 developments are summarised below:

- Andrews Sykes: Nothing of significance.

- Bioventix: H1 2025 profit down 4% following stagnant sales, albeit accompanied by a 3% dividend lift and promising R&D commentary.

- City of London Investment: H1 2025 underlying profit up 13% despite funds under management shrinking 3% following a hefty $564m outflow.

- Mincon: FY 2024 profit collapsing 38%, although H2 profit may have remarkably increased versus H2 2023 following improved market conditions (blog coverage ceased for now).

- Mountview Estates: Nothing of significance.

- S & U: An H2 2025 update revealing the motor-finance loan book reducing by 13% plus a request for the Supreme Court to adopt a “common-sense” verdict.

- System1: A Q3 update showing platform revenue up 53% and “comfortably above” projections of a £5m FY 2024 profit.

- FW Thorpe: H1 2025 profit up 2% and intriguing talk of buybacks should the share price “significantly undervalue the company’s current position and prospects“.

- M Winkworth: An FY 2024 update predicting profit up 9% and confirming the annual dividend had increased by 5%.

Q1 portfolio returns

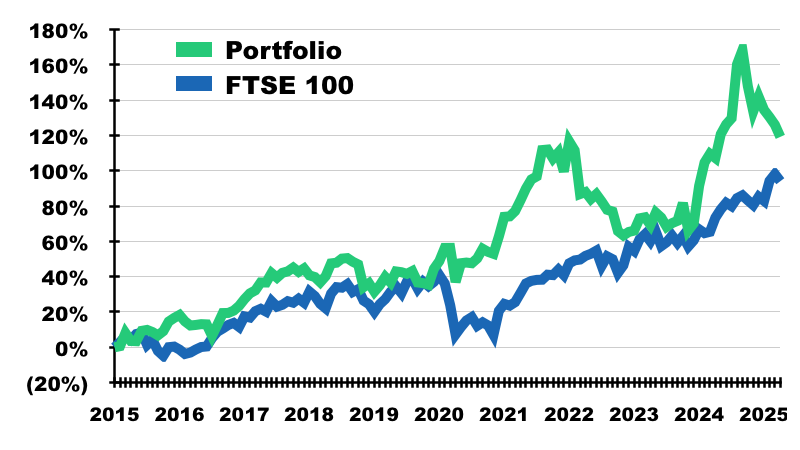

The chart below compares my portfolio’s monthly progress to that of the FTSE 100 total return index:

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me so far this year:

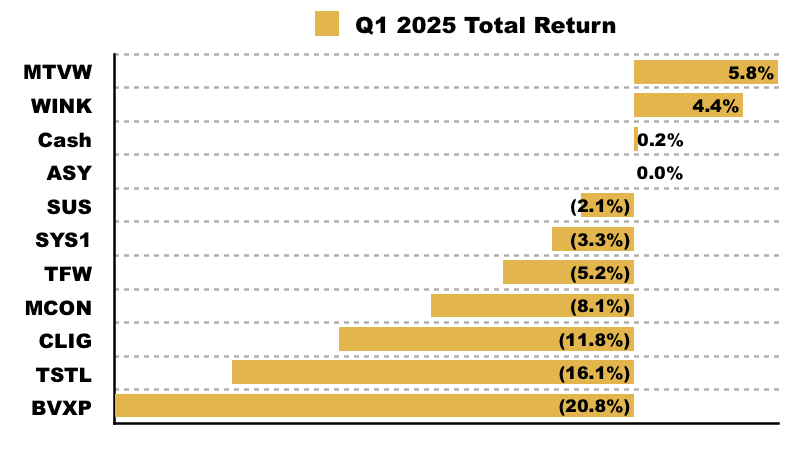

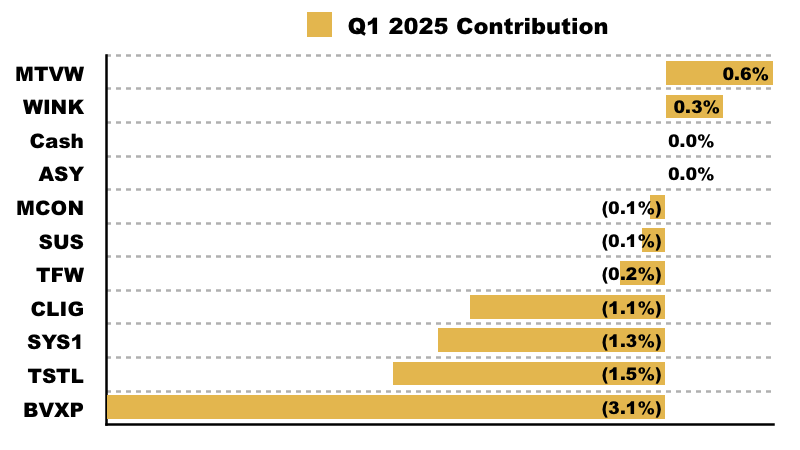

This chart shows each holding’s contribution towards my 6.5% Q1 loss:

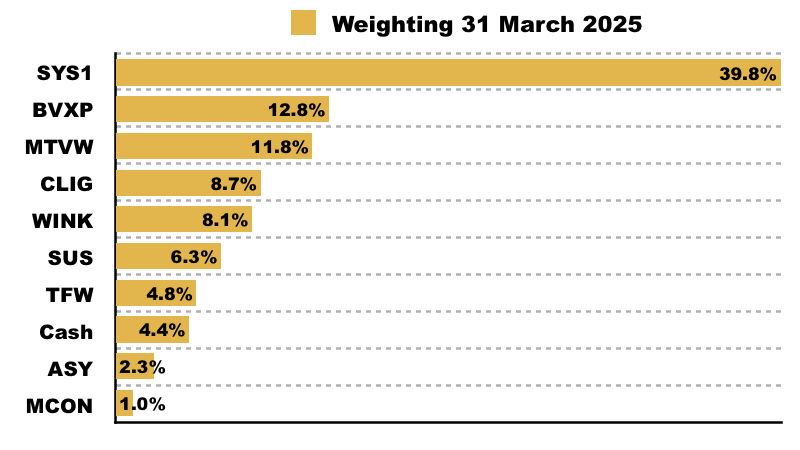

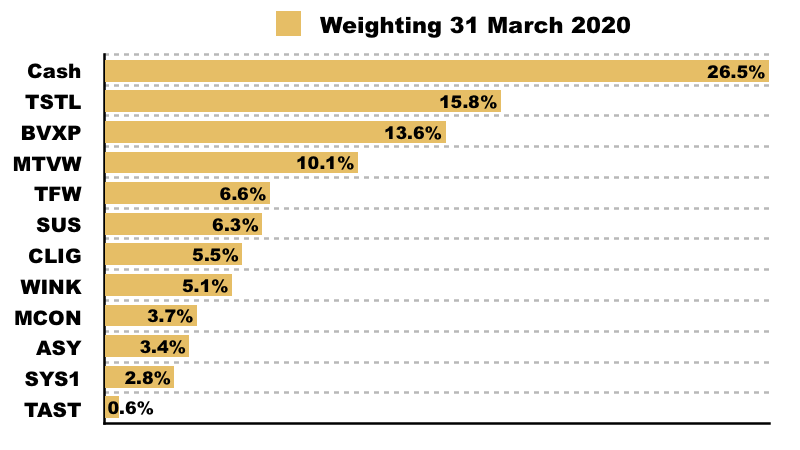

And this chart confirms my portfolio’s holdings and their weightings at the end of Q1:

Finding Ammunition For My Elephant Gun

Warren Buffett once drew a parallel between safari hunting and buying shares:

“Our basic principle is that if you want to shoot rare, fast-moving elephants, you should always carry a loaded gun.”

Mr Buffett’s “rare, fast-moving elephants” referred to the stocks he wanted to acquire — large, quality companies trading at attractive valuations — while his “loaded gun” referred to having cash on hand ready to buy.

The term ‘elephant gun‘ has since entered the market lexicon, and investors trying to emulate Mr Buffett are always told to have their ammunition ready just in case a bargain share suddenly appears.

Taking aim with 27%

My elephant gun is not quite on a par with the billions Mr Buffett invests at Berkshire Hathaway. But since commencing this blog at the start of 2015, I have always carried some cash on hand… ready to shoot when the opportunity arises.

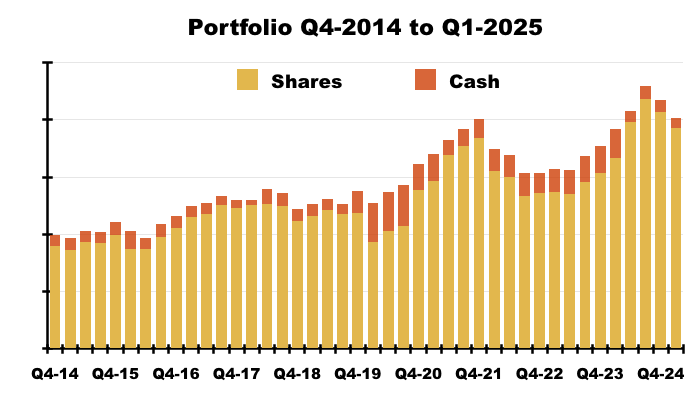

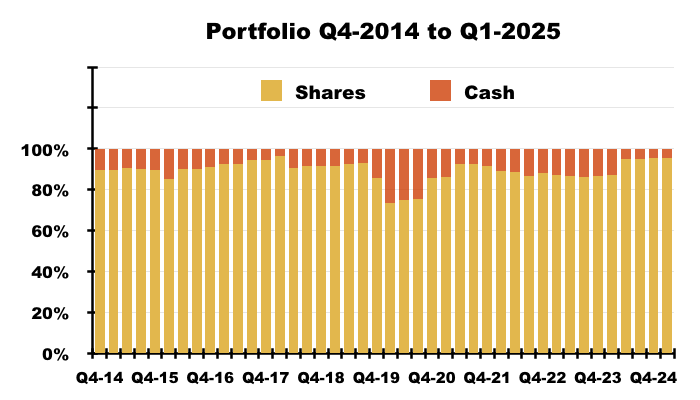

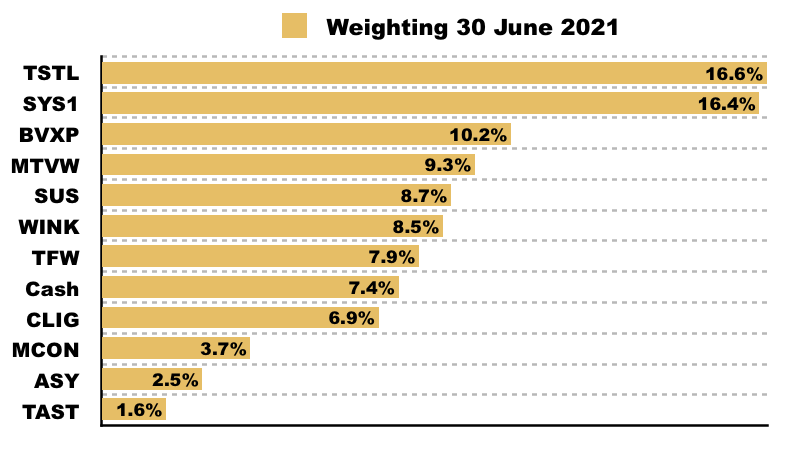

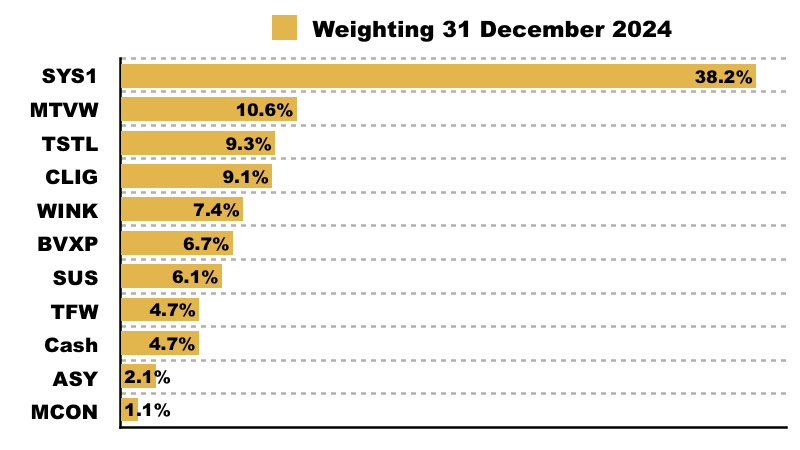

The charts below show the quarter-end splits between shares and cash within my portfolio:

My cash position has ranged between 4% and 27% and has averaged 11%.

The 27% occurred during the early stages of Covid-19 at the end of Q1 2020. Markets had just crashed and, with hindsight, that moment definitely required a large elephant gun armed and ready.

However, my 27% was not the result of some prescient pandemic preparation.

Instead, during Q4 2019, I finally gave up on long-time struggler Getech and was forced to sell illiquid disappointer Oleeo before a delisting. Those two exits took my cash weighting from 7% to 14%. Then just weeks before the lockdowns, Daejan announced it would go private and that exit increased my cash to 27%.

I eventually fired my 27% elephant gun during Q4 2020, with the main shot directed at System1.

I resumed firing during Q2 2021, with the main shot once again directed at System1.

System1 went from a 3% position…

to a 16% position:

I am not sure whether Mr Buffett would approve of my shooting, but System1 shares have subsequently performed relatively well.

Two options for reloading

Fast forward to the end of last year, and top-ups of City of London Investment, Mountview Estates and S & U had reduced my cash position to less than 5%:

My elephant gun was therefore still loaded, but my level of firepower was almost at its lowest since I started this blog. And with my portfolio no longer home to sub-standard names such as Getech and Oleeo — and with no help either from surprise bids — finding extra ammunition had become quite difficult.

Indeed, reloading the elephant gun was made even more difficult due to the relatively modest ratings applied throughout almost all of my portfolio.

I said at the start of this year that Andrews Sykes, Bioventix, City of London Investment, Mountview Estates, S & U, FW Thorpe and M Winkworth could all “exhibit top-up qualities during 2025“. I simply could not bring myself to sell down such holdings in which I really hoped to buy more!

If I wanted significant extra ammunition for my elephant gun, I was instead left with two basic options:

- Top-slice by far my largest position: System1, or;

- Sell the only other significant share I owned that was not on my top-up list: Tristel.

I chose the latter option because:

- The future prospects of System1 appeared brighter than those of Tristel, and;

- My portfolio would shift further towards the companies in which I had the greatest conviction.

During this last quarter I have used part of my Tristel proceeds to buy more Bioventix. Having bought at £30 with the price now £24, I have shot my elephant gun far too early. But at least I still have some ammunition left with my cash position at 4%.

I suspect further shots at Bioventix could be fired later this year. After all, I spent up to nine months taking aim at System1.

Dividend reinvestment pea-shooter

Selling Tristel is of course only a temporary solution for my elephant-gun dilemma. One day I will have invested my remaining 4% cash position and will once again have to find more ammunition.

The underlying ‘problem’ is that I am not adding extra cash to my portfolio. Mr Buffett may have Berkshire Hathaway’s enormous insurance ‘float’ to continually invest, but I am limited to dividends that at present add approximately 4% every year to my portfolio.

If I ever become fully invested, my elephant gun will fire more like a pea shooter as it reinvests relatively small dividends. I am not sure pea shooters are conducive to market-trouncing returns.

At some point therefore, I will have to face the inevitable: top-slicing my sizeable System1 holding to provide significant extra ammunition for my elephant gun. And yet reducing System1 will run counter to three of my past multi-bagger investments, where really I should have not top-sliced simply because they represented a large part of my portfolio!

What to do? I must confess I am not entirely sure. At least for now I have 4% to reinvest while I ponder my elephant-gun ammunition further. Beyond that, my best hope is some of my shares advance to levels where a top-slice makes obvious sense from which I can reload. But I suppose such market conditions could create the opposite elephant-gun problem…

…whereby I then have ample cash armed and ready…

…but nothing really to fire at!

Until next time, I wish you safe and healthy investing.

Maynard Paton

(*If only this were true)

Hi Maynard,

You have TFW twice in the portfolio contribution graph. I suspect one should be SYS1.

Hi Gavin, very well spotted, now corrected!

Maynard

Thanks for sharing, always instructive to read! :-)

Thanks Simon!

as always, an interesting read. thanks

Thanks m!

Maynard