30 November 2024

By Maynard Paton

FY 2024 results summary for System1 (SYS1):

- The positive transition to data services continues, with a new “performance culture” delivering FY platform revenue up 43%, the highest reported FY profit for seven years and a reinstated annual dividend.

- SYS1’s “unique selling proposition of predictiveness” keeps winning ad-testing clients, plaudits and attention, but remains frustratingly under-exploited for innovation testing that offers a 5x addressable market.

- The bumper 87% gross margin, record £208k revenue per employee and near-£10m cash position were counterbalanced by one-off profit gains, mediocre bank interest and hefty bonuses obscuring margin progress.

- The board’s true growth ambitions will be revealed through a revised LTIP, and I would trust the award-winning directors to retain the scheme’s £45m-£88m revenue range and reinstate a profit ‘underpin’.

- A tantalising illustrative projection of revenue doubling to £60m should be very achievable given SYS1’s “3 Reasons to Believe“, and would support an adjusted Ebitda of £18m — and possible £16 share price — if the group’s margin target is met.

Contents

- News links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue, profit and dividend

- Strategic-review initiatives

- Platform versus non-platform

- Ad testing versus Innovation testing and Brand tracking

- United States

- Fame generation

- John Kearon

- Platform clients

- Employees and bonuses

- LTIP

- Financials

- Q1 and Q2 2025 trading statements

- Valuation

News links, share data and disclosure

- Annual results, presentation and webinar published/hosted 03 July 2024;

- Management Q&A session hosted 12 July 2024;

- Q1 2025 trading statement published 12 July 2024;

- Canaccord Growth Conference presentation hosted 13 August 2024;

- AGM attendance 25 September 2024, and;

- Q2 2025 trading statement published 22 October 2024.

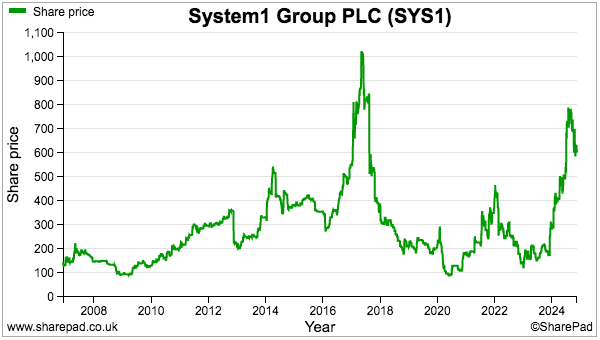

- Share price: 600p

- Share count: 12,689,073

- Market capitalisation: £76m

- Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Research specialist that forecasts the success of television adverts, with progress resting upon “unmatchable predictiveness” backed by “unique IP” delivered at “market-beating speed and value” through a “world-class product suite“.

- Transition from bespoke consultancy towards automated ‘platform’ services continues apace and is increasingly underpinned by solid revenue growth, improving financials and healthy net cash.

- Growth opportunities through ‘innovation testing’, the United States and multinational customers support the company’s £18m illustrative Ebitda projection and a potential £16 share price.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Revenue, profit and dividend

- Upbeat comments within January’s Q3 statement…

[Q3 2024] “The Group enters the final quarter of the year with good trading momentum following a consistently strong December quarter. As a consequence, the Board believes that the Group is now well placed to deliver results ahead of previous expectations. Revenue for the current financial year is expected to be at least £29 million (FY23: £23.4 m) and statutory profit before tax to be comfortably above £2 million and materially ahead of current consensus (FY23: £0.7m).”

- …followed by further upbeat comments within April’s Q4 statement…

[Q4 2024] “Q4 Revenue of £8.7m was 30% higher than the equivalent quarter last year, lifting FY24 Revenue to £30.0m, up 28% year on year. Platform Revenue growth remained strong (+37% in Q4; +42% for the year) buoyed by the successful H2 launch of TYA Pro+ and more than 50% Platform Revenue growth in Q4 in the US where Revenue grew quarter on prior quarter throughout FY24.

Following an exceptional H1, gross profit margins returned to expected levels in H2, achieving 87.0% for the year as a whole (FY23: 84.2%), ahead of our 85% benchmark. Net cash increased by £3.3m in H2 FY24 and £3.9m across the year, resulting in year-end net cash of £9.6m (FY23: £5.7m).

Based on the unaudited management accounts, Profit before Taxation for the year ended 31 March 2024 is expected to amount to £2.8m, up £2.1m on FY23 and ahead of market expectations (revenue: £29.1m, profit before tax : £2.4m). This Profit before Taxation figure includes the release of £0.4m of provisions related to a now-closed sabbatical scheme.”

- …had already confirmed this FY would be very positive.

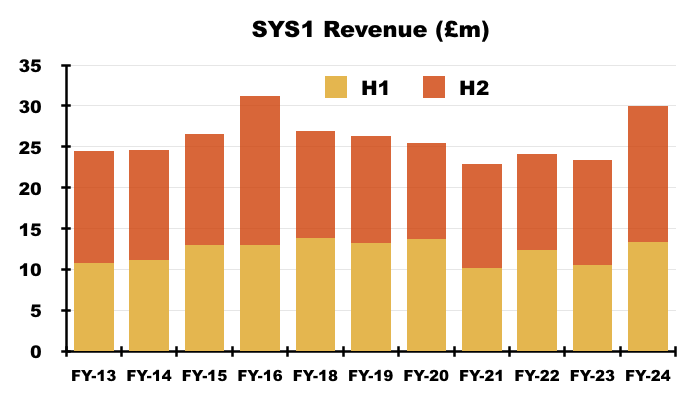

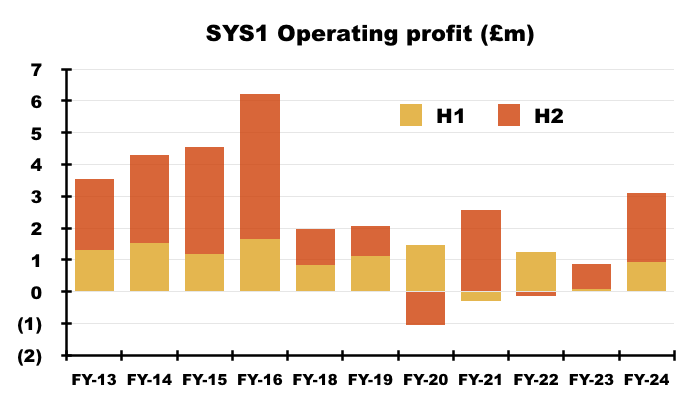

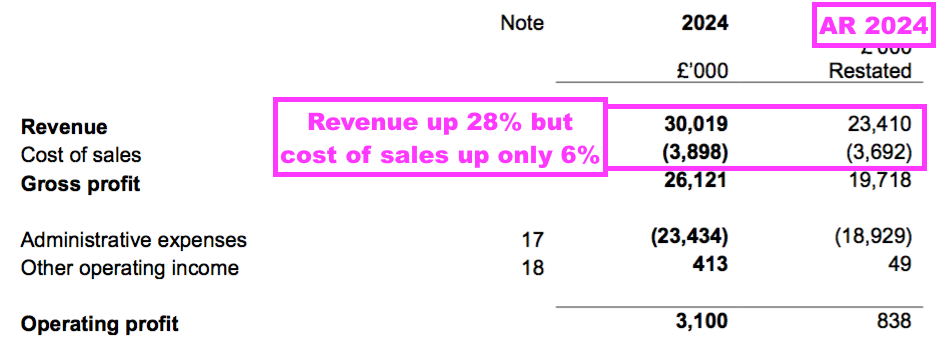

- FY revenue did indeed increase 28% to £30.0m, while FY platform revenue was a fraction better than predicted, up 43% to £24.8m.

- This FY’s gross margin was indeed 87.0% and this FY’s net cash did indeed finish at £9.6m.

- The FY pre-tax profit was in fact £3.1m — well ahead of the £2.8m anticipated within the Q4 statement — and did indeed include a £0.4m provision release (see Financials).

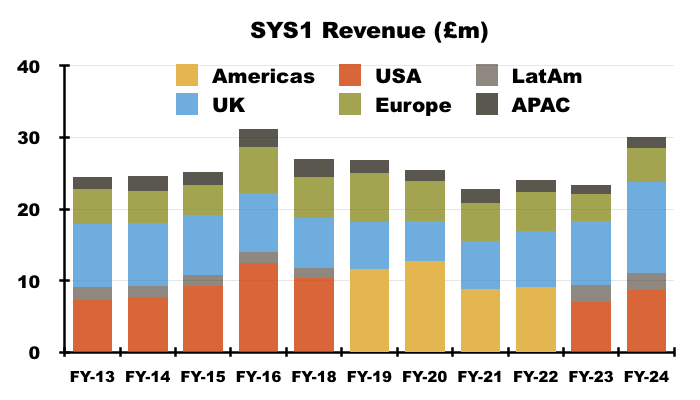

- FY revenue of £30.0m was the highest since FY 2016 (£31.2m):

- H2 revenue increased 29% to £16.7m, the best six-month effort since H2 2016 (£18.2m).

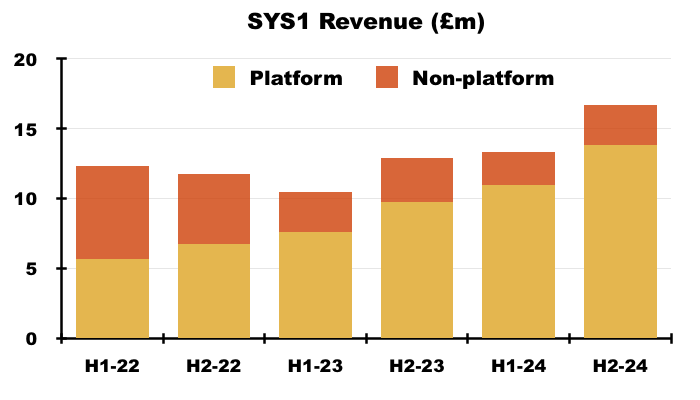

- 83% of FY revenue was supported by platform revenue, due in part to FY non-platform revenue (i.e. bespoke consultancy income) declining 13% to £5.2m (see Platform versus non-platform):

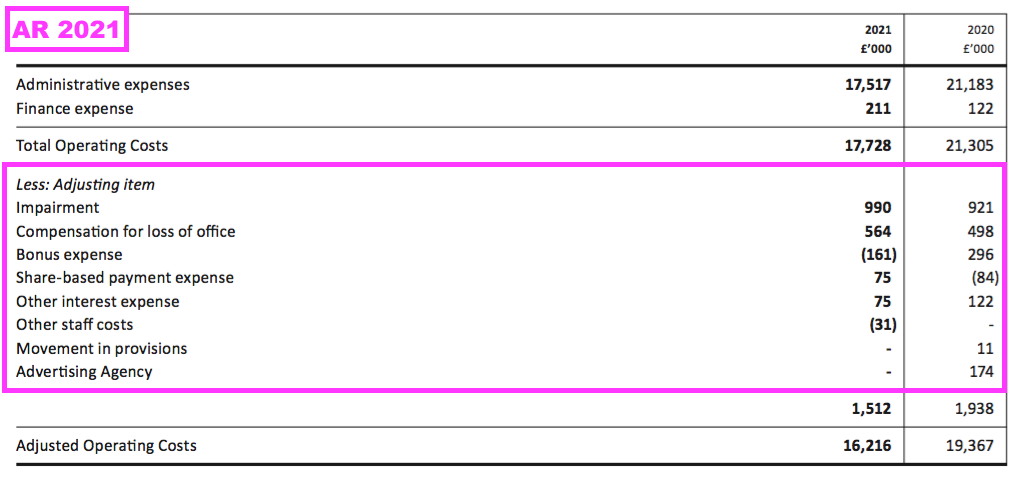

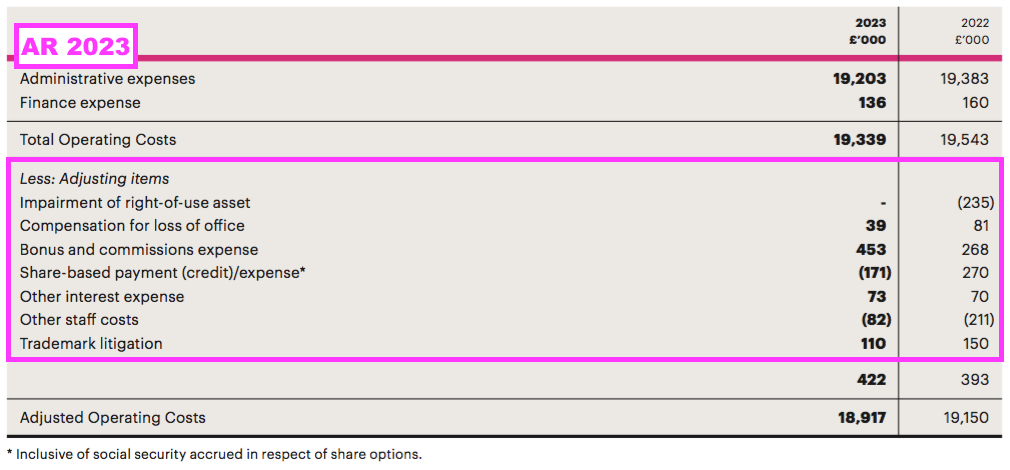

- FYs 2020, 2021, 2022 and 2023 had each featured an array of adjusting items:

- But this FY pleasingly limited adjusted profit measures to just adjusted Ebitda, which is calculated by adding back share-based payments to Ebitda. All the other adjusting items and adjusted profit measures were thankfully dispensed with.

- As well as the aforementioned £0.4m provision reversal, this FY’s operating profit included other income of £0.4m that seemed entirely related to a trademark-infringement settlement.

- In addition, SYS1 continues to capitalise certain software development expenditure. This FY witnessed a net £0.3m spent on new IT systems that bypassed the income statement. Total software development costs yet to be amortised against earnings now stand at £1.4m (see Financials).

- Note that SYS1 restated the comparable FY after reclassifying an office sublease under IFRS 16…

“During the year ended 31 March 2024 the Group determined that the sublease of its former New York office, previously accounted for as a right-of-use asset, should have been presented as a finance lease receivable. The following table summarises the impact of the prior period reclassification on the financial statements of the Group. There is no impact on basic or diluted earnings per share. “

- …although the impact on the comparable FY’s operating profit was minimal.

- This FY’s reported £3.1m operating profit was £2.2m greater than the comparable FY and was the highest since FY 2016 (£6.2m):

- H2 operating profit was £2.2m, up £1.4m on the comparable H2.

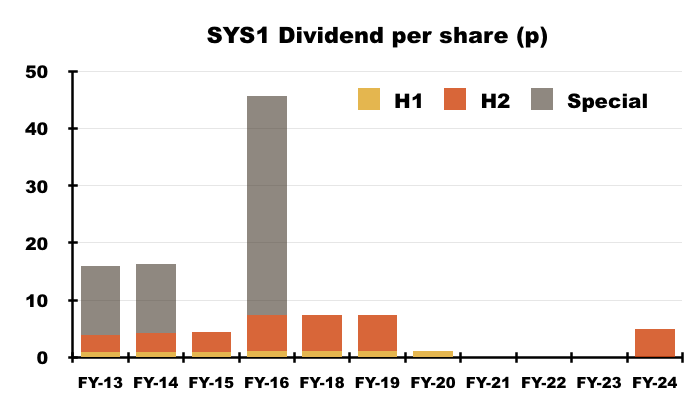

- April’s Q4 statement had already signalled this FY would declare a dividend, and this FY revealed a 5p per share payout:

“No dividend was paid during FY24. In April 2024 the Board announced its intention to resume paying dividends, in line with the existing policy to distribute 30-40% of after-tax earnings through the cycle. At this stage the Board expect this to be through the declaration of a single ordinary dividend each year alongside the Company’s full year results. The Board is proposing a dividend of 5.0 pence per share for FY24…“

- The 5p per share dividend is the first payout for more than four years…

- …and suggests SYS1 has now reached a ‘base’ level of earnings from which the business can recover/grow further.

- Management’s FY webinar explained why a single dividend — rather than the more conventional interim/final payout split — would be declared each year:

“It’s just simpler for a small company. The admin cost and the regulatory processes around declaring a dividend seem to us to be not entirely worth it. And it’s not as if people will be buying us only for the dividend. The yield isn’t going to be that high because we’re still investing in the business, so we’re primarily a growth stock.

And also, where you have an interim dividend and a final dividend, the amount where the interim dividend is pitched can create a lot of noise and speculation about what the board is signalling and what it means. Quite often, that is just noise and it just creates a distraction from what’s really going on in the business.”

Strategic-review initiatives

- H1 2023 announced a strategic review that concluded SYS1 should devote greater attention to:

- The group’s “unique selling proposition [of] ‘predictiveness’“;

- Digital ads;

- The world’s largest advertisers;

- Partnerships with media groups, such as the existing tie-ups with ITV and LinkedIn;

- Partnerships with industry agencies, such as Omnicom/BBDO, and;

- The United States.

- The strategic review was triggered by shareholders frustrated by how SYS1 had struggled to fully exploit its “world class” market-research products and deliver worthwhile, dependable earnings.

- The unhappy shareholders were unconvinced by the strategic review and, during April 2023, requisitioned a General Meeting (GM) that proposed a number of board changes, including:

- The appointment of former SYS1 chief executive Stefan Barden as executive chairman, and;

- The demotion of SYS1 founder/executive John Kearon to a non-exec role (see John Kearon).

- Shareholders rejected the proposed board changes by 58% to 42%, which left the strategic review in place.

- (Although without Mr Kearon’s 22% shareholding, the proposed board changes would have passed 57% to 43%!).

- This FY touched upon the initiatives presented by the strategic review.

- SYS1 reiterated its ‘unique selling proposition of predictiveness’, with this FY stating:

“Our clients are clear that our ability to capture, measure and interpret emotional responses to creative content is the number one reason they buy from us, and many say that we do what no-one else in the market can do.”

- This FY also cited marketing expert Mark Ritson saying SYS1 had “come to dominate the field of pre-testing“:

“Influential Marketing Professor Mark Ritson published an article in Marketing Week, showcasing how SKY use System1 pre-testing capability early in the process to predict business results in the short and long term and enable quick decision making. In the article he describes System1 as having “come to dominate the field of pre-testing in a remarkable short period of time”. Marketing Professor Peter Field followed this with evidence from the IPA database showing that those campaigns that pre-tested did better than those that didn’t and credits System1 as one of the reasons for that difference.”

- Mr Ritson’s Marketing Week article provided this useful insight into SYS1’s predictive accuracy:

[Marketing Week April 2024] “So Sky did something every marketer should do: it tested the testers. The brand already had advanced econometric data on previous campaigns stretching back more than four years, which reviewed the performance of all of its ads and what they had or hadn’t done for its business. It asked System1 to go back into its archive and rate all the Sky ads’ long- and short-term impact. It then compared what each ad actually achieved, according to Sky’s assessment, versus what System1 predicted it would have done.

And the results were stunning. On both short-term sales impact and longer-term brand building, System1’s predictions were incredibly accurate. Multiplying out the System1 prediction with the amount of media money Sky invested in each ad produced a near-perfect correlation with Sky’s own econometric results.

Sky now pre-tests around 400 commercials a year. “

- No wonder the FY webinar declared:

“Our customers are crying out for help and we’re the only ones who can truly help.“

…

“We believe we’re the world’s best at what we do and we’re delivering this to our customers.“

…

“Underpinning this is our USP, and that USP is taking emotion and translating it into business results creating predictive outcomes for our marketing audience.“

- Helping the USP is the group’s “truly unique” database of 100,000-plus advert tests, which was referenced during the 2024 AGM:

[AGM 2024]

“The database is truly unique“

“It’s the quality of the database that makes the difference…There are plenty of suppliers who can give you every grocery ad that’s been done in the last five years. But there’s nobody else at the moment who can tell you how well those ads have done. And we can. We’ve got enough volume to make [our analysis] meaningful, but clearly our challenge is to grow [the database] constantly. Because the bigger that database, the more efficient it is. [The database] fundamentally underpins everything we do.“

- The board also claimed during the AGM that only SYS1 measured “how people feel when they’re watching an ad”:

[AGM 2024] “In terms of the defensibility, we are the only people in the business who measure how people feel when they’re watching an ad.And we’re able to not only understand how they feel, but translate that into predictive outcomes. That is the special sauce of SYS1. And that’s what we’ve got to keep special and continue to build upon.“

- This FY provided a short update about partnerships…

“Partnerships – Partnerships help drive Fame, generate co-branded thought leadership to be shared with the industry, and enable introductions to partners’ clients. New partnerships solidified in FY24 include Pinterest, resulting in research on digital ads; Radiocentre, resulting in the publication of the Listen Up!; and Aardman. New partnerships with TikTok and Effie will be highlighted with research coming in FY25.“

- …and an even shorter update on Digital ads:

“Test Your Ad has expanded to cover all media types from early-stage scripts to finished films, to ensure we have the fastest, most predictive, actionable products that meet our customers’ needs. Alongside the TV testing, we now offer [Test Your Ad] for Digital, Audio, Out of Home and Print testing, allowing our customers to test full campaigns across media types.”

- I get the impression the Partnerships and Digital initiatives now assist what this FY defined as “3 Reasons to Believe“:

- In fact, the strategic review appears to have morphed into those “3 Reasons to Believe” and the following growth opportunities:

- Innovation (see Ad testing versus Innovation testing and Brand tracking);

- United States (see United States), and;

- The world’s largest advertisers.

- The strategic review originally announced Mr Kearon had been given the “priority task of securing new business and partnership opportunities in the US“.

- However, the FY webinar confirmed Mr Kearon was back in the UK and currently working on “strategic opportunities” with AI and “setting out the future strategy for the next three-plus years” (see John Kearon).

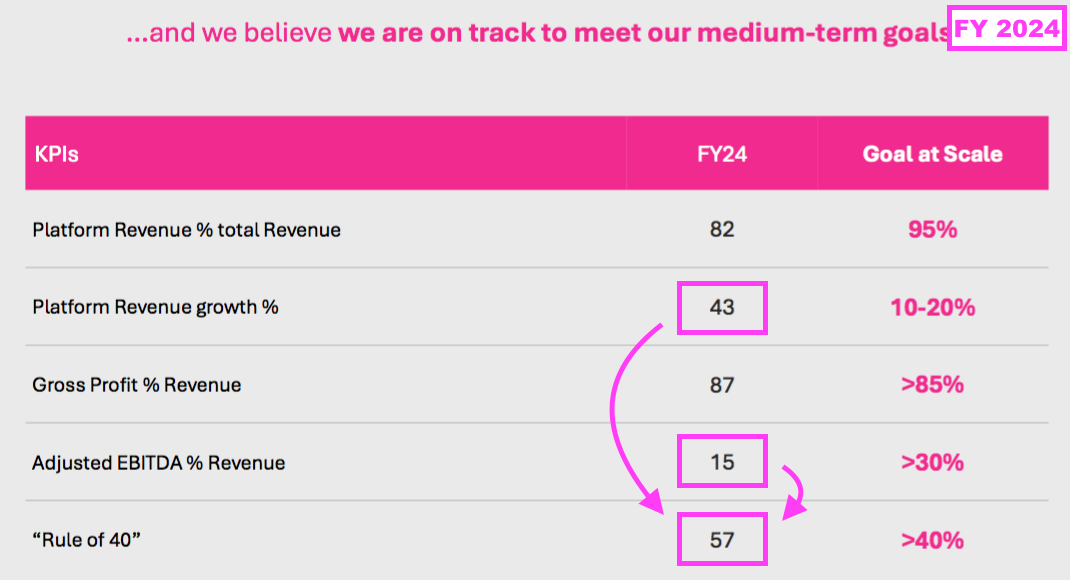

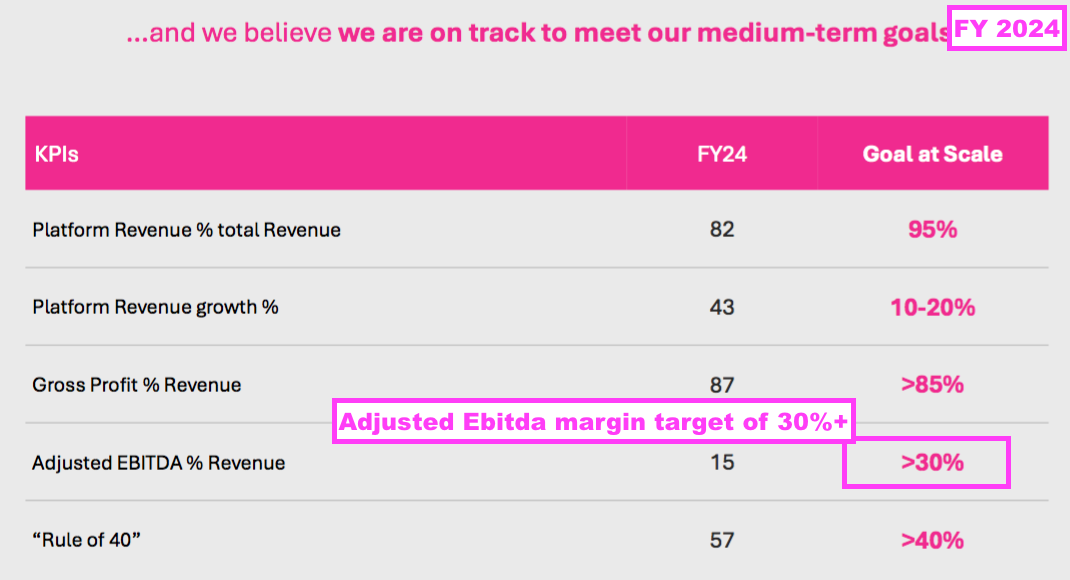

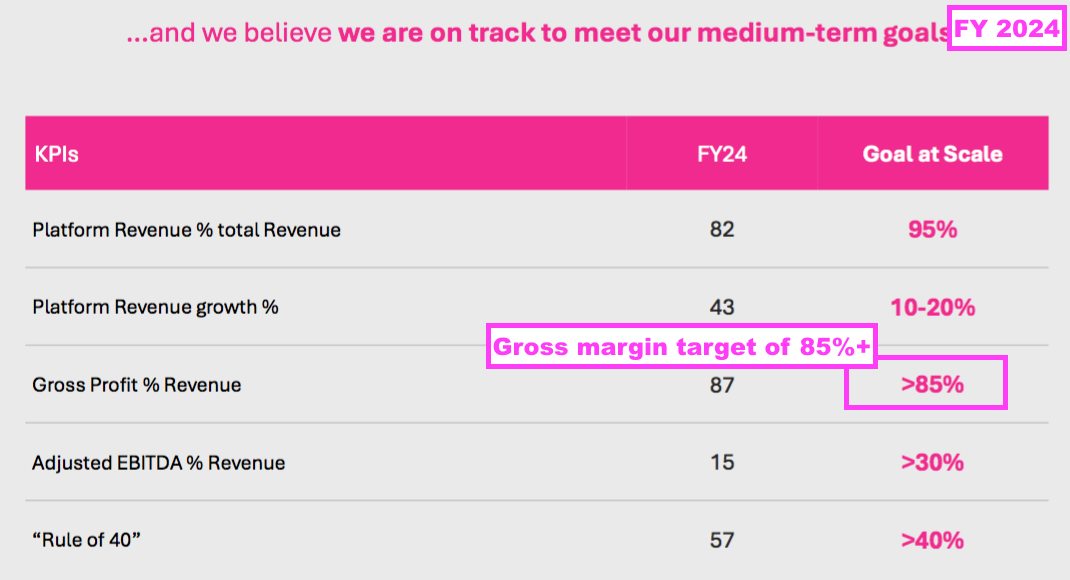

- The ‘Rule of 40’ target introduced by the strategic review was maintained for this FY:

- The Rule of 40 measure is derived by adding platform revenue growth (FY 2024: 43%) to the total adjusted Ebitda margin (FY 2024: 15%) and aims to reach at least 40%.

- The Rule of 40 measure came to 57%, and would still have been met if SYS1 added total revenue growth (FY 2024: 28%) instead to the total adjusted Ebitda margin.

- All told, SYS1 looks to have adhered to its strategic-review initiatives and this much improved FY performance — followed by upbeat statements during July and October (see Q1 and Q2 2025 trading statements) — might on the surface imply shareholders were right to reject the proposed GM board changes.

- But the GM protest votes do seem to have had an impact on SYS1.

- In particular, Mr Kearon’s work on “strategic opportunities” — in which he admitted during the 2024 AGM had left him as a “mad inventor” — suggest his role is very much behind-the-scenes and not at the forefront of the primary platform strategy (see John Kearon).

- Furthermore, the FY presentation revised a tantalising projection first published during February’s Capital Markets Day that illustrates FY revenue doubling and a possible Ebitda outcome (see Valuation):

- The illustrative Ebitda projection seemed a direct answer to a question Mr Barden raised at the April 2023 GM:

[Stefan Barden April 2023] “6) Valuation: As a result, and you might want to pass this to Chris, if successful, how much could System1 be worth in say 2 to 3 years time?

a) If you can’t give a valuation what would the shape of the P&L be? For example, your 25% CAGR sales growth aspiration is a doubling in sales every 3 years. What is the associated cost structure?“

- I continue to speculate SYS1’s board has found a middle ground between Mr Kearon and Mr Barden to move the group’s platform strategy forward after the GM.

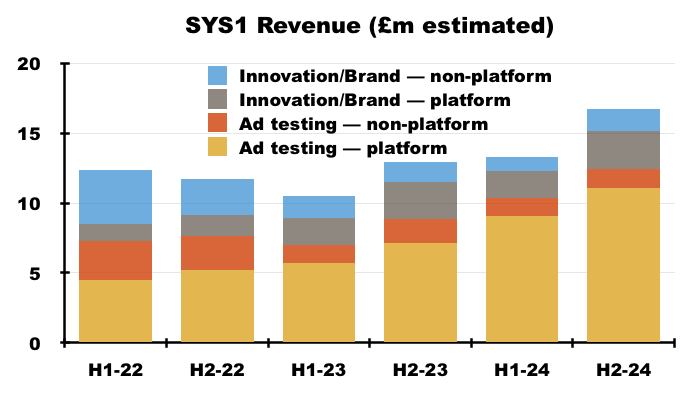

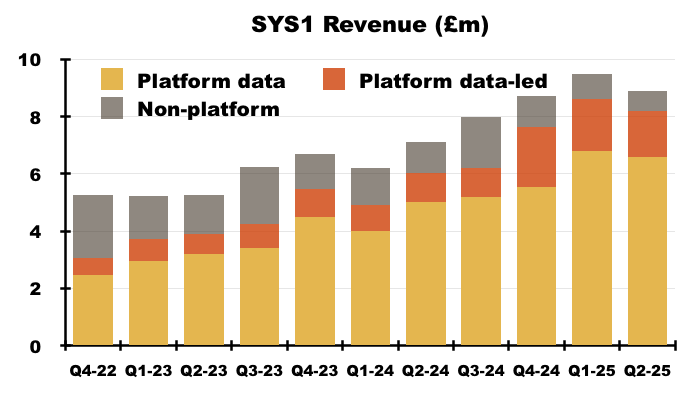

Platform versus non-platform

- SYS1’s strategic review validated the group’s shift from supplying bespoke consultancy work to providing automated data services via a “marketing decision-making platform“.

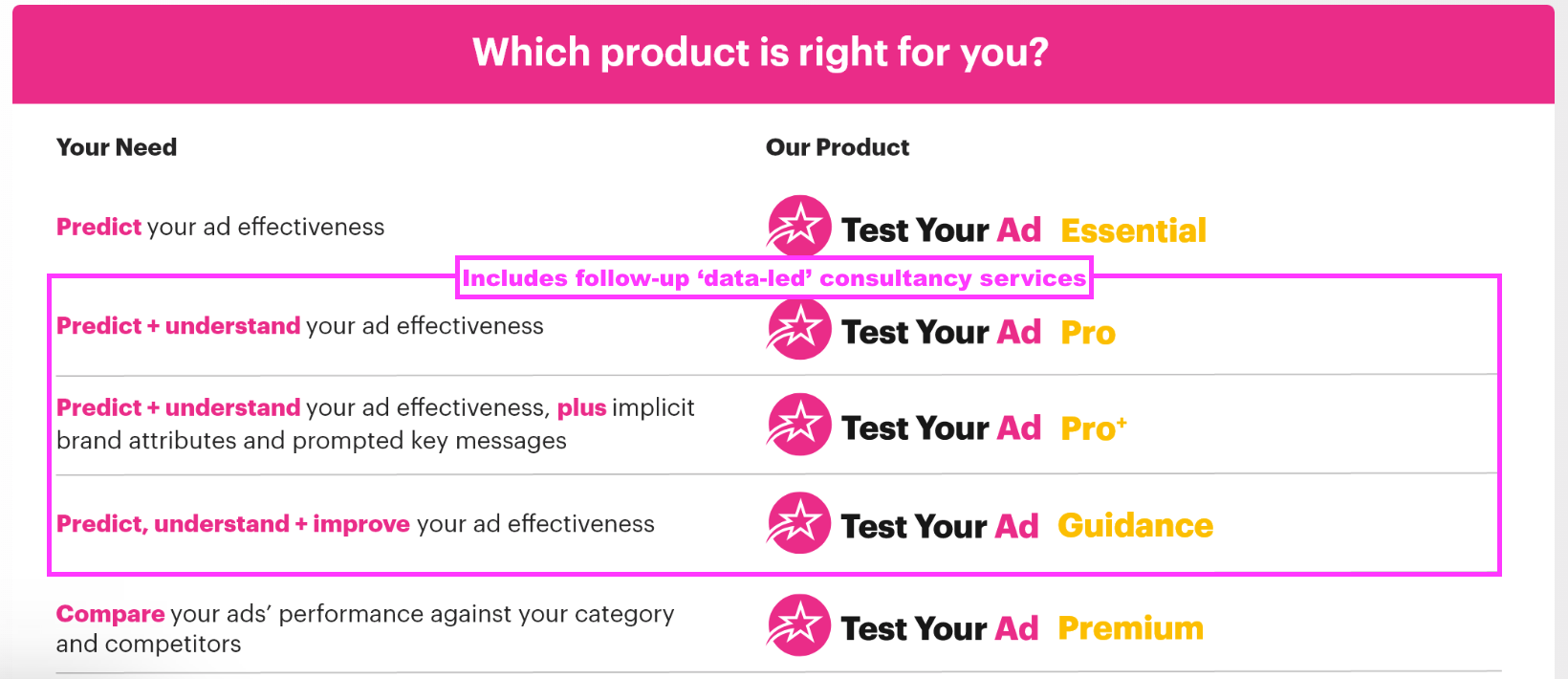

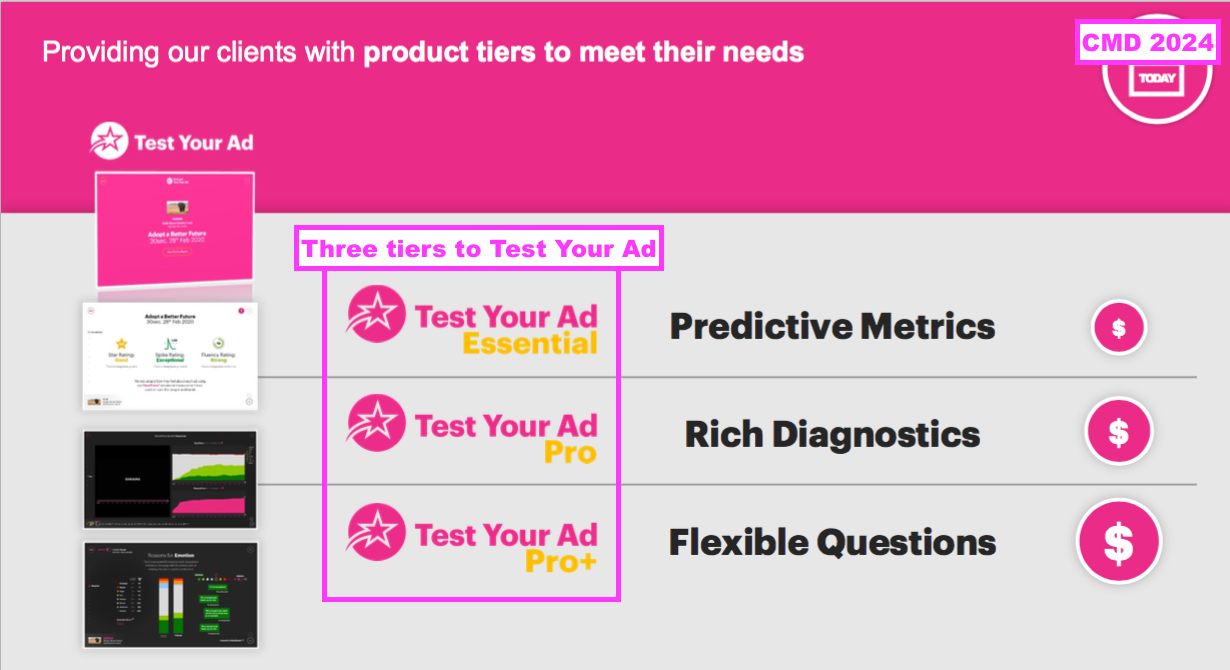

- Platform products are led by Test Your Ad (TYA)…

- …which was launched during April 2020 and allows customers to upload proposed adverts to SYS1 and receive a report within 24 hours based upon the verdict of an online panel:

- Platform revenue is supported by Test Your Innovation (TYI) and Test Your Brand (TYB), which perform the same online-panel function for product ideas and company brands:

- TYB and TYI were launched during November 2021 and May 2022 respectively.

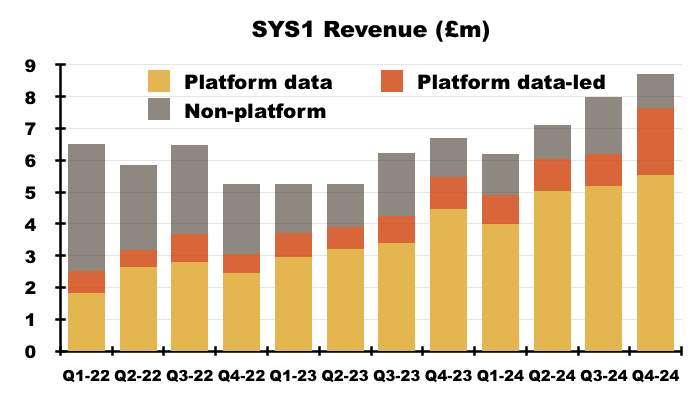

- Platform ‘data’ revenue is bolstered by ‘data-led’ consultancy revenue, which consists of follow-up improvements and guidance from SYS1’s marketing experts:

- This FY revealed:

- FY platform ‘data’ revenue up 41% to £19.8m;

- FY platform ‘data-led’ revenue up 51% to £5.0m;

- H2 platform ‘data’ revenue up 36% to £10.7m, and;

- H2 platform ‘data-led’ revenue up 66% to £3.1m.

- Note that the split of platform revenue can vary from quarter to quarter:

- For instance, Q4 2024 witnessed platform ‘data-led’ revenue surge to 28% of total Q4 platform revenue, versus 16%-18% for the preceding Q1, Q2 and Q3.

- This FY reported TYA Pro+ — the top-tier TYA service that supplies extra data insights — had spearheaded the group’s progress (see Ad testing versus Innovation testing and Brand tracking):

“Test Your Ad Pro+ has been a game-changer as we’ve built the ability to deliver customer and project-specific customisation in a scalable manner, through the automated platform.“

- The FY webinar noted TYA Pro+’s “project-specific customisation” helped convert customers from old bespoke contracts to automated platform services:

“TYA Pro+…allowed us to effectively automate some features that could previously only be delivered with a complex bespoke workaround.“

- FY non-platform revenue fell 13% to £5.2m, which SYS1 had previously said would have been a “good outcome“. H2 non-platform revenue dropped 9% to £2.9m.

- This FY indicated the non-platform work would continue to dwindle:

“Bespoke consultancy will likely fall as we reach the end of some long-term contracts that will not renew, however this should not significantly affect overall group revenue or profit growth.“

- But February’s Capital Markets Day did emphasise how bespoke consultancy was still required to assist some large clients to join SYS1:

[CMD 2024] “We have also learnt we need the ability to retain bespoke consultancy, which allows customers to transition from what they are doing to day to what they could and should be doing in the future. We know this is only a very small part of our offering, likely around 5% at scale, and something that we offer to new or very large customers with his revenue potential to help them come on board.“

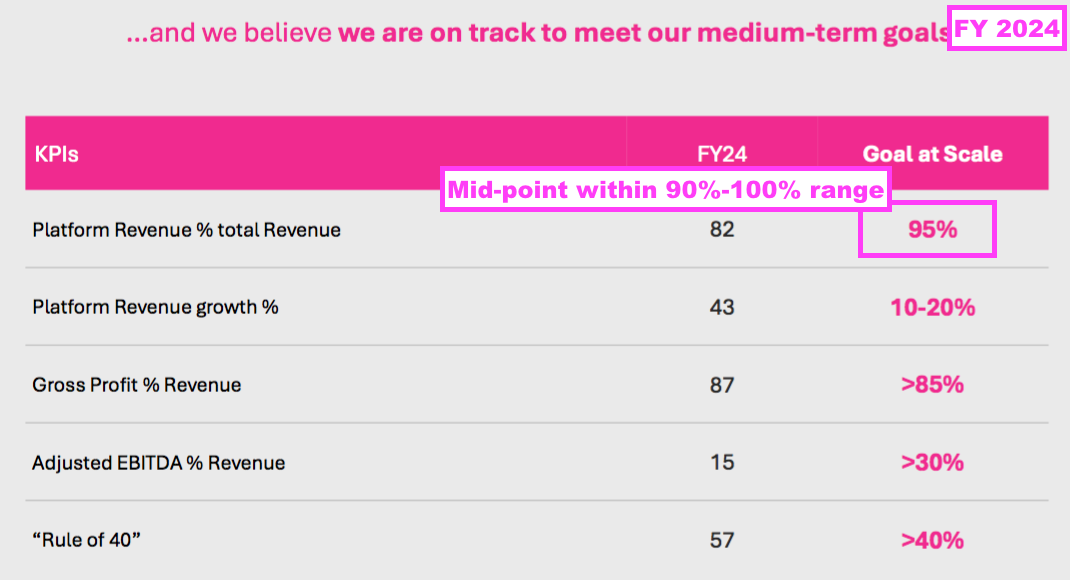

- The FY presentation confirmed platform revenue could reach 95% of total revenue “at scale“:

- However, the FY webinar did admit the 95% was the middle of a 90%-100% range:

“In terms of our strategic medium-term goals, we’re saying that platform revenue should be between 90% and 100% most years from here on in compared to 82% last year. So the middle of that range is 95% platform revenue growth at scale“

- If non-platform revenue remains at approximately £5m, then platform revenue at 95% would suggest total revenue “at scale” would be £100m…

- …but platform revenue at 90% would suggest total revenue “at scale” would be £50m.

- Although the preceding H1 presentation suggested approximately £1.3m of non-platform revenue involved advert testing…

- …this FY’s presentation did not hint at how non-platform income was spread throughout TYA, TYI and TYB.

- Assuming non-platform revenue of £1.3m involved advert testing during H2 as well as H1, then this FY witnessed:

- Platform TYA revenue of approximately £20.1m;

- Non-platform TYA revenue of approximately £2.7m;

- Platform TYI/TYB revenue of approximately £4.7m, and;

- Non-platform TYI/TYB revenue of approximately £2.6m:

- The FY presentation reiterated a “medium-term goal” of a 30%-plus adjusted Ebitda margin:

- SYS1’s non-platform heyday witnessed Ebitda margins of 20%:

- In theory at least, the ‘scalable’ platform services ought to enjoy a much higher margin than the non-platform consultancy work… but obviously superior economics have yet to emerge at group level.

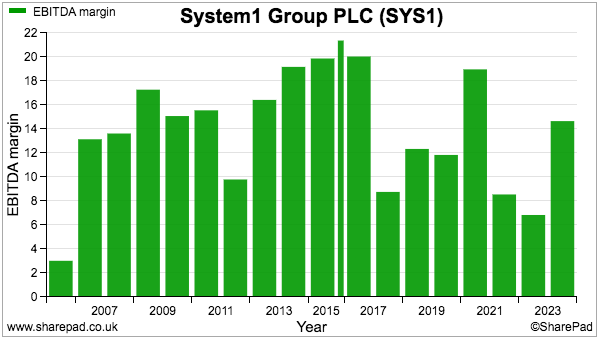

- Still, the adjusted Ebitda margin KPI is improving. The comparable FY registered an 8% adjusted Ebitda margin, which improved to 13% during this FY’s H1 and to 16% during H2.

- The forthcoming H1 2025 will reveal how further the adjusted Ebitda margin has improved.

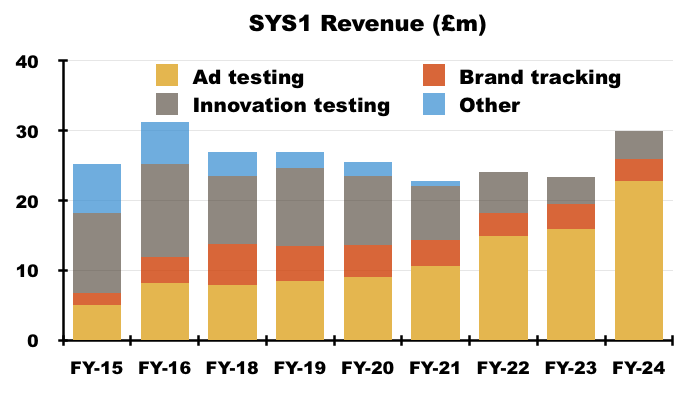

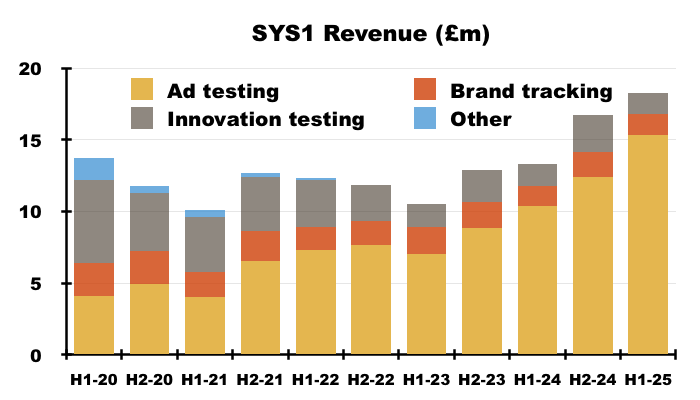

Ad testing versus Innovation testing and Brand tracking

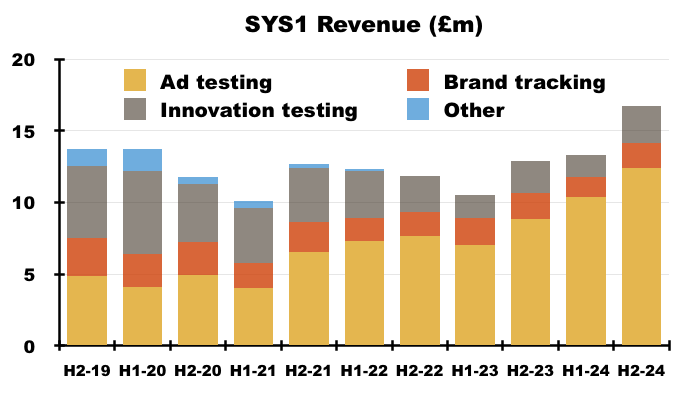

- Ad testing — via the TYA platform service and certain non-platform consultancy work — continues to dominate SYS1’s revenue:

- Ad-testing revenue supported 76% of FY revenue versus 68% during the comparable FY and just 20% during FY 2015.

- While FY ad-testing revenue gained 43% to £22.8m…

- …FY innovation-testing revenue advanced 5% to £4.1m and FY brand-tracking revenue slid 13% to £3.2m.

- However, both innovation testing and brand tracking performed better during H2 than H1; H2 innovation-testing revenue gained 14% (H1: down 6%) while H2 brand-tracking revenue fell 3% (H1: down 24%).

- This earlier chart (if accurate!)…

- …shows FY platform revenue from innovation testing and brand tracking (c£4.7m) lagging far behind the platform revenue from ad testing (c£20.1m).

- At least platform revenue from innovation testing should soon improve after this FY highlighted the (post-FY) relaunch of TYI:

“With our customer-centric focus, in April 2024 we have launched a new Test Your Innovation product suite to replace Test Your Idea. This repositions the previous version in a way that better suits our clients, ensuring our products neatly follow a standard product development cycle. This exciting development will help accelerate our growth in the Innovation space in the upcoming year.”

- Whereas the initial TYI platform service had involved bespoke consultancy work and assessed a limited range of product characteristics, the relaunched TYI offers five distinct automated steps…

- .. and can assess a variety of different product characteristics:

- I also believe prospective customers can now begin using TYI at any of the five steps.

- The FY webinar noted innovation testing was once SYS1’s main earner:

“If you think back to our BrainJuicer days, Innovation used to be the core product that we offered and what we were very famous for.”

- Innovation testing generated 45% of total revenue during FY 2015, versus 14% for this FY:

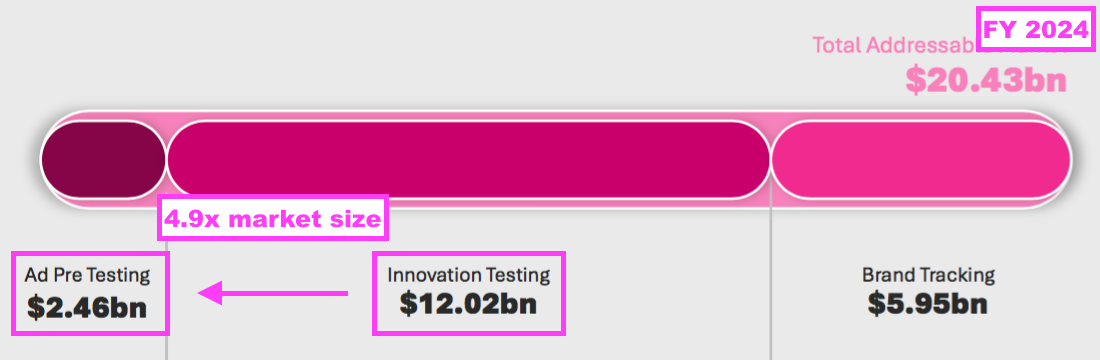

- The FY presentation reminded shareholders TYI’s addressable market is almost 5x the size of TYA’s addressable market:

- TYI could therefore become a much greater money-spinner than TYA, which this FY encouragingly implied:

“The relaunch of our Test Your Innovation product suite will allow us to create a revenue stream for Innovation that could eventually become bigger than our Comms [advert-testing] revenue stream. We say this because according to ESOMAR research, the target addressable market for innovation is 4.8X that of communications at $12.02bn.“

- But the FY webinar confessed substantial promotional work would be required to get the revamped TYI off the ground (see Fame generation):

“We need to make sure that the Innovation product is as good [as Advertising], which we believe it is. And we need to make sure the marketing, fame and credibility is as high as it is in Advertising, which it isn’t yet but will be.Then once we’ve got all that, we’ll expect Innovation to be a sitting alongside Advertising as an equal partner if not a bigger partner in the future.“

- Management acknowledged during my Q&A that existing TYI clients would not necessarily spend more on the relaunched TYI, as the initial service was “already answering their questions“.

- But cross-selling between TYA and TYI (and TYB) could improve. SYS1 used this FY to divulge for the first time the proportion of multi-service customers:

“We are starting to focus on cross-selling our comms [advert testing], innovation and brand tracking product lines. In FY24, 2% of our clients bought all 3 product lines, but this contributed to 13% of total revenue. 13% of our clients bought more than one product line, contributing to 45% of total revenues for the year.”

- The FY webinar additionally revealed 8% of clients bought advertising and innovation products, contributing to 24% of total revenue.

- A somewhat unsatisfactory 92% of customers therefore purchased TYA without TYI (or vice versa), which does suggest significant scope to cross-sell TYI (or even TYA).

- Mind you, these statistics are undoubtedly skewed by SYS1’s multitude of smaller customers. What will ultimately count for shareholders is the proportion of SYS1’s largest customers paying for both TYA and TYI (see Platform clients).

- The FY webinar suggested material TYI growth would commence from FY 2026:

“Going forwards we think there’ll be marginal growth this year but really we’ll start to see high percentage growth from next year onwards and the challenge then will be for us in terms of how fast we can make it grow… We think that it can definitely have legs to be growing fast from next year onwards.”

- TYA’s platform revenue went from zero to approximately £20m within four years, but management during my Q&A was hesitant TYI could match that performance:

“We think even if you do three years [at 50%], you still haven’t quite got £20m. So, starting from [Innovation’s] £4m, you go £4m, £6m, £9m etc“

- Similar to the preceding H1 and February’s Capital Markets Day, this FY did not really mention TYB.

- Following this FY and previous updates, I have concluded TYB is likely to:

- Generate greater non-platform revenue than platform revenue;

- Be purchased without both TYA and TYI;

- Be purchased by a larger customer;

- Enjoy less of a competitive advantage than TYA and TYI, and;

- Not feature significantly within SYS1’s growth plan.

Fame generation

- This FY recapped the group’s “step-changed” promotional work:

“We have step-changed the volume and quality of System1 fame creation in FY24. We have worked in partnership with global industry-leading companies, which we promote through a wide range of channels, focussed primarily on the US and UK and secondarily into our other key markets in Brazil, Germany, France, Asia and Australia. The result of this fame-building activity is an increase by over 40% of leads generated in the US and UK vs FY23.”

- “Fame-building” activities consist of:

- PR;

- Events;

- Partnerships;

- “Uncensored CMO” podcasts;

- Ad of the Week articles, and;

- “Thought Leadership“.

- The Uncensored CMO podcast hosted by Jon Evans “step-changed” its output from fortnightly to weekly at the start of this FY.

- Podcast guests during this FY included marketing executives from Octopus Energy, Google, Diageo, L’Oreal, Tesco, LEGO, Salesforce, NBCUniversal, Airbnb, Just Eat, Confused.com, Amazon, Mailchimp and Cadbury…

- …presumably all of whom had some professional interest in SYS1’s services.

- FY platform revenue advancing 43% suggests the PR, events, podcasts and “thought leadership” have proven effective within the industry.

- Mind you, the “fame building” has not yet reached parts of the mainstream media.

[BBC November 2024] “The decision to use familiar ideas and characters is a smart one, said Lynne Deason, head of creative excellence at analysts Kantar.

“Consistency pays in advertising,” she said. “Sticking with the same creative approach often makes it easier for people to know which brand is being advertised.

“It can build a sense of nostalgia too, adding to the entertainment factor.“

- SYS1 has been ranking festive adverts for years and, awkwardly, the BBC’s chief customer officer was actually a SYS1 podcast guest during October.

- This FY signalled greater promotional spend during FY 2025:

“In the coming year we will step up investment in attracting, winning and retaining customers to continue our growth trajectory.“

- A top priority for SYS1 must be to promote TYI with the same vigour as TYA. After all, TYI enjoys a much greater addressable market than TYA, and SYS1 did enjoy significant revenue from innovation testing in years gone by.

- SYS1’s website currently lacks meaningful TYI promotion.

- SYS1’s research for example — including Break Through, Compound Creativity and The Extraordinary Cost of Dull — all focuses on improving the effectiveness of adverts.

- And among the website’s nine case studies, eight relate to advertising and only one covers product innovation that was published during 2022.

- Management said during my Q&A that “thought leadership” for TYI was “definitely” required and should involve a podcast, a weekly blog and a book…

- Lemon and Look Out are books written by SYS1’s chief innovation officer, Orlando Wood:

- Both books help the reader understand advertising effectiveness, albeit using very ‘System2’ lessons drawn from very highbrow sources:

- Mr Wood now works four days a week at SYS1, with his fifth day devoted to his own advertising-effectiveness course:

- My impression following the 2023 and 2024 AGMs alongside my management Q&As is Mr Wood will not undertake that much TYI promotional work.

- Exactly who will lead TYI’s “thought leadership” therefore remains unclear.

- Nonetheless, effective “fame building” for TYI ought to be much easier now that TYA has been established, especially if that aforementioned quote from Mark Ritson is actually true and SYS1 has indeed “come to dominate the field of pre-testing“.

- Mr Wood devising his own course prompted a new ‘Conflicts of Interest’ section within this FY’s ‘Principal Risks and Uncertainties’:

“Conflicts of Interest

Directors’ and employees’ personal, financial or business affairs may result in situations where the company’s interests are not fully aligned with their own.

The Board formally records directors’ interests at each meeting, and directors’ new external appointments are notified as soon as is practical. Below board level the company reviews senior employees’ outside interests on a case-by-case basis to ensure no detriment to the company arises.“

- Board remarks at the 2024 AGM suggested SYS1 was very happy with Mr Wood fulfilling his “outside interests”:

[AGM 2024] “Orlando is running educational courses, which is one of our best new business tools, because he’s indoctrinating a whole new generation of young marketing people into his thinking and therefore the ways of System1.

Part of the deal we have with Orlando is that we have numerous places on every course that we can introduce specific clients to. It’s actually a win-win situation.“

John Kearon

- This FY gave the impression SYS1 founder and executive director John Kearon was no longer working full time:

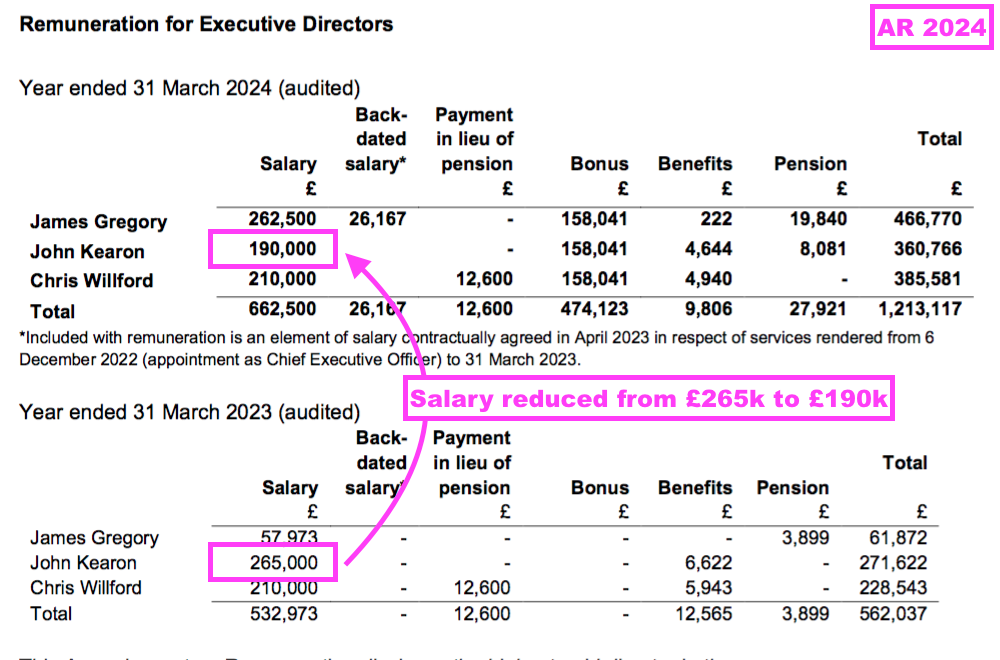

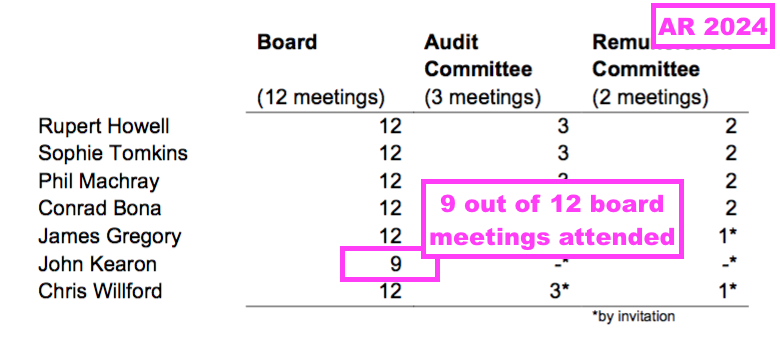

- Mr Kearon’s pay was reduced by 28%…

- …and he attended only nine of the twelve board meetings:

- Board remarks during the 2024 AGM highlighted Mr Kearon’s new role and his work in America had led to the lower pay and meeting absences:

[AGM 2024] “John took a pay cut because he was stepping down as chief executive and doing a different job. And we thought that was beyond noble of him.

And the only time anybody’s missed a board meeting is because if they’ve been in North America and the timings have all been wrong. There was one John missed when he was with Rolex.“

- The FY webinar revealed Mr Kearon’s new role involves AI:

“A great example is where John [Kearon] has been working with natural-language processing and understanding how it can help improve our quality of our products. Our products collect from our market research respondents ‘verbatims’… and we’re able to now use AI off the back of John’s exploration and innovation to ensure that we have high-quality respondents on our platform and keep that level of quality super high.”

- Mr Kearon said during the 2024 AGM he was a “mad inventor” and was not working part time:

[AGM 2024] “James [Gregory, CEO] and Chris [Willford CFO] just do [the webinars] brilliantly. We split up the roles rather than everyone doing everything, and left me being a mad inventor.“

“Frankly, I’m in my happy place inventing… When I’m enthused and excited, I don’t think part time would be an accurate description.“

- I did not vote for Mr Kearon at the April 2023 GM, and I do not know whether shareholders who did vote for Mr Kearon had expected him to subsequently:

- Not attend investor webinars;

- Not attend every board meeting;

- Not really participate in AGMs, and;

- Work in the background on AI.

- Maybe Mr Kearon is in fact more suited to a behind-the-scenes “mad inventor” role than the position of chief executive.

- Earlier this year, Mr Kearon commendably admitted to LBB Online that he had handed SYS1’s leadership to “someone more capable of scaling the business” while resisting becoming a “backseat driver” in the boardroom:

[LBB Online May 2024]

“LBB> What experience or moment gave you your biggest lesson in leadership?

It was when I had my first employees, rather than partners, and felt a work-related responsibility beyond myself.

If you’ll indulge me with a second more recent one, it was handing over the CEO reins to my number two, James Gregory, at the end of 2022, and adapting to being his number two.

I had to ensure staff knew he was now the boss and worked hard to resist any backseat driving while still making supportive, meaningful contributions. There’s inevitably a moment for the ‘funny founder’ of a business to park their ego, let go and hand the leadership to someone more capable of scaling the business.

But that rarely happens voluntarily and often, the decision is made for them by their Board/Partners/Investors, who find a way to force them out.

I guess what I am saying is – it was an act of leadership, to give up the leadership, and 18 months later, my reward has been the company’s stellar growth and being back in my happy place leading our innovation.”

Platform clients

- SYS1’s transition from bespoke consultancy work to automated platform services had led to frustratingly inconsistent references to both ‘clients’ and ‘customers’.

- A multinational ‘client’ can provide the group with multiple regional ‘customers’, and the inconsistency meant accurately tracking SYS1’s progress through a revenue per client or customer measure was impossible.

- Revenue per client/customer measures are important because they allow shareholders to judge whether the new platform services are becoming more popular — and therefore becoming more valuable.

- The preceding H1 and comparable FY had created some reporting consistency after both presented information about ‘platform clients’.

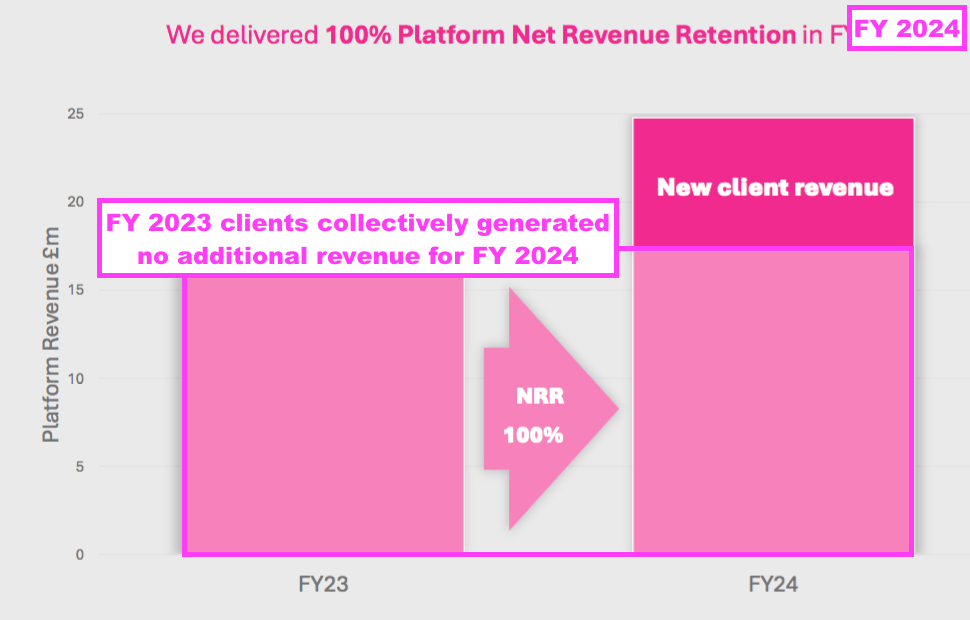

- However, this FY introduced a new measure of tracking SYS1’s client/customer revenue progress — net revenue retention:

“We saw excellent levels of revenue growth, with total revenues up 28% and platform revenues up by 43%. We have started to make good progress in maximising revenue opportunities within our existing client base but have opportunity to make further inroads in this space. We had a Net Revenue Retention Rate on total platform revenue of 100%.“

- This FY said net revenue retention was 100% and therefore the extra platform revenue was generated entirely from new clients:

- The FY webinar welcomed this FY’s 100% net revenue retention:

“A question we’ve had a few times has been around our net revenue retention. So how much of our revenue are we keeping year on year from our existing client base? What’s lovely to say is from the people buying our platform revenue products, 100% of that stayed year on year.”

“That’s not to say every single customer spent the same amount. But if you take the customer base and what they spent in FY 2023, we took the same amount of revenue from that customer base in [FY 2024].“

- I would have expected net revenue retention to surpass 100% — i.e. platform customers during the comparable FY to have collectively spent more during this FY — given SYS1’s platform services are still relatively new.

- At least the FY webinar suggested 100% ought to be the minimum retention rate for the platform:

“In reality our benchmark will always be to beat 100%. It’s the first time we have set out this metric and it’s one we’ll be able to track and report going forwards.”

- Management said during my Q&A:

- The 100% retention rate was greater than it had been and ought to be a “baseline and not a ceiling“;

- Approximately 80% of clients stay the same year on year;

- Clients could “spend significantly more than they do with us today”, and;

- A retention rate should be published every year, but not every half-year because the calculation may then become “incredibly confusing”.

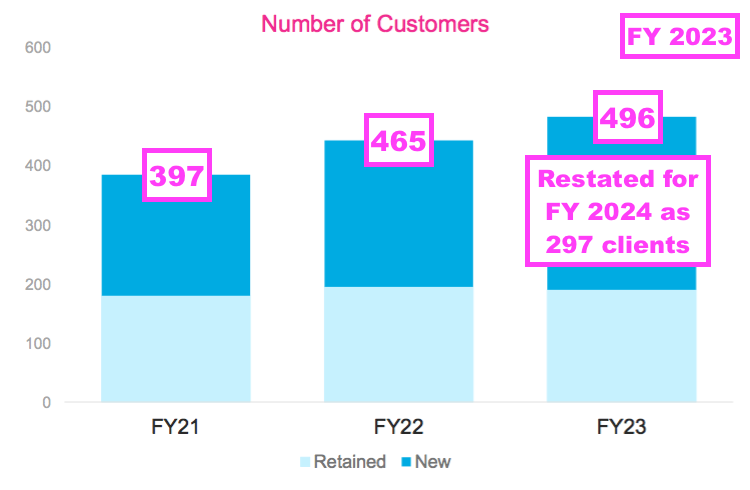

- This FY revealed the number of clients increased from 297 to 428 and the number of new clients were 260. As such, 129 clients must have disappeared during this FY.

- Note that a client is deemed ‘new’ for this FY if they:

- Employed SYS1 for the very first time, or;

- Returned as a client following an absence during the comparable FY.

- The 260 new clients brought in collective revenue of £8.3m, split £7.5m on platform services and £0.8m on non-platform services.

- Revenue per client dropped from £79k (£23.4m/297) to £70k (£30.0m/428), although the comparable FY did refer to 496 ‘customers’ and not 297 ‘clients’:

- The 260 new clients seemed to have brought annualised average revenue of £64k (£8.3m/260*2).

- The FY webinar implied how revenue per client can be distorted by large numbers of small clients.

“£79k… that’s basically the revenue in FY 2023 divided by the number of clients and the equivalent figure for FY 2024 is £70k.

So on that basis [revenue per client] did decline. Would we read anything into that? Not particularly. It’s not a metric we particularly look at in the business, because the more successful we are, [the more we] recruit low-cost-to-service clients — people who might just test one ad a year or one every two years. They’re cheap to serve and they are profitable”.

- Management added to its revenue-per-client opinion during my Q&A:

“The problem with the tail [of small customers] is, by getting more famous, we win more people who spend £5k a year. That is not a downside because it doesn’t cost us more to acquire them because they come for free.

We aren’t targeting them. We aren’t reaching out to them. They’re people who come to us and want to give us some money. But what that does is it really skews the average client.“

- This FY suggested a better guide to revenue per client was revenue per larger client:

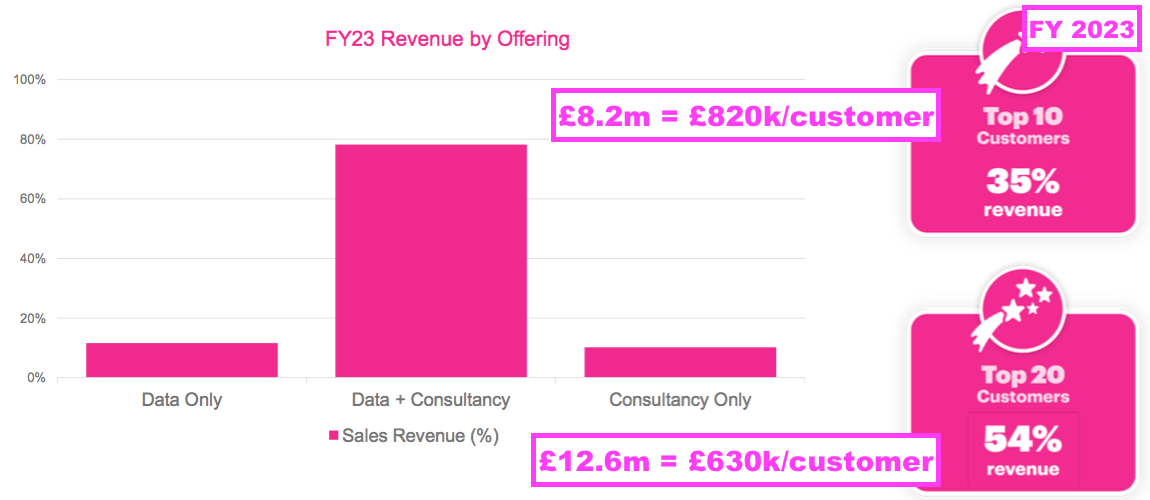

“Concentration in our top 10 and top 20 clients was consistent year on year. Our top 10 clients made up 30% of revenue and our top 20 clients 45% of revenue. All of our top 20 clients in FY24 bought platform products with 78% of spend from the top 20 clients being on data and data-led consultancy. No one client in FY24 was larger than 5% of total company revenue.“

- That text indicated the following:

- Average revenue per clients 1-10 was £900k;

- Average revenue per clients 1-20 was £675k;

- Average revenue per clients 11-20 was £450k;

- Average revenue per clients 21-428 was £40k, and;

- Client 1 spent no more than £1.5m.

- Note that the comparable FY used revenue from the top 10 ‘customers’, which I assume was not calculated the same way as this FY’s revenue from the top 10 ‘clients’:

- Management during my Q&A acknowledged the confusion caused by inconsistently using ‘customers’ and ‘clients’:

“We do a poor job on this. We need to work out how we use just one going forward.“

- I can only trust future FYs will consistently disclose net revenue retention and revenue from the top 10 and 20 clients. That way SYS1 can highlight the growing attraction of the platform services to help validate the wider growth strategy to shareholders.

- February’s Capital Markets Day suggested the very largest customers (not clients!) could in time spend £3m a year versus this FY’s top-10 (client!) average of £900k:

[CMD 2024] “Fairly consistently, our top ten customers represent about a third of the company’s revenue. We have had a situation in the past when a single customers was more than 10%, and I think we could have two or three customers that could become close to 10%… in the next couple of years. It is very plausible we can have multiple customers over £1m and have some customers over £2m and maybe some over £3m. That is not at all out of the question.“

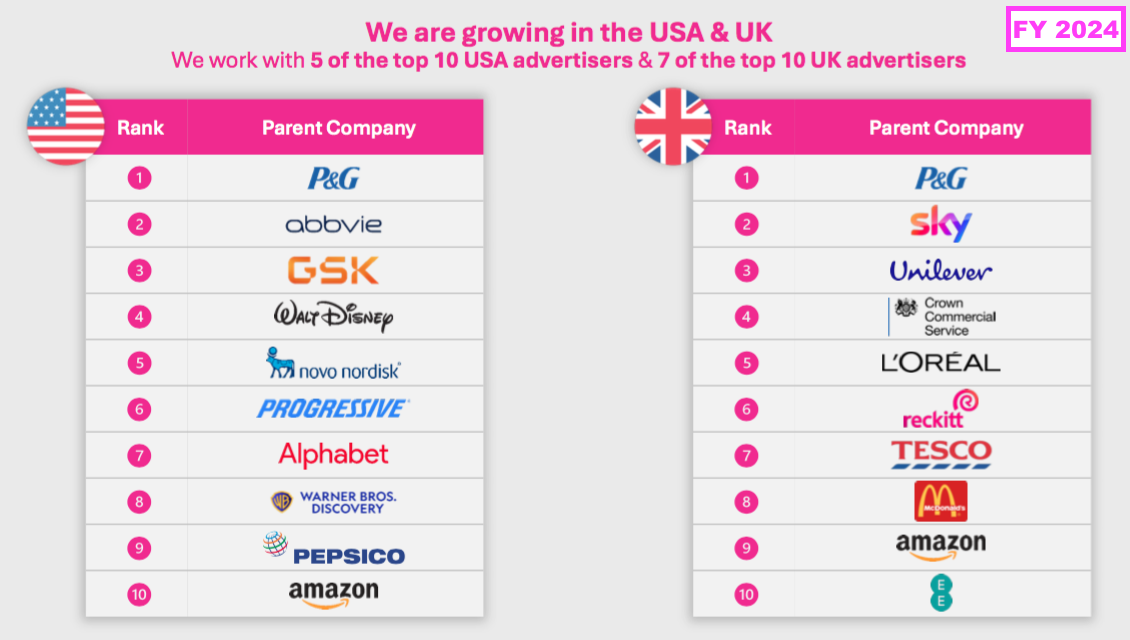

- I presume all the familiar names below spend a total of more than £3m every year on testing adverts and innovations through different suppliers…

- …although I am not sure whether SYS1 knows how, say, Unilever, exactly splits its ad-testing activities between SYS1 and rival ad testers.

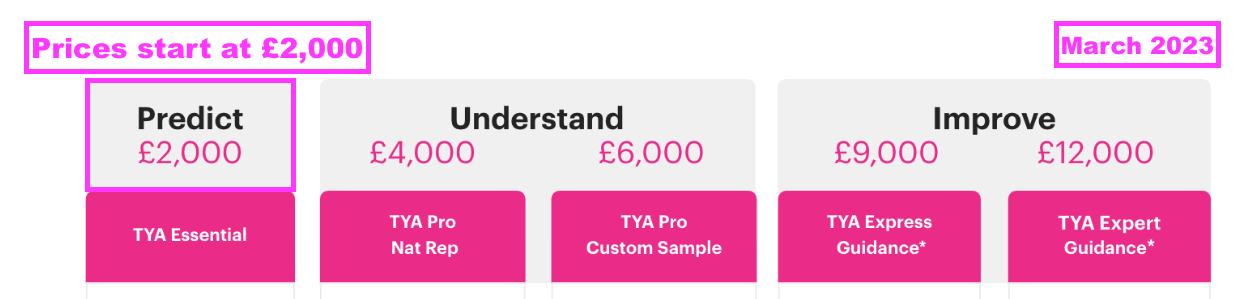

- TYA price rises may have favourably influenced this FY’s revenue retention and revenue per client ratios.

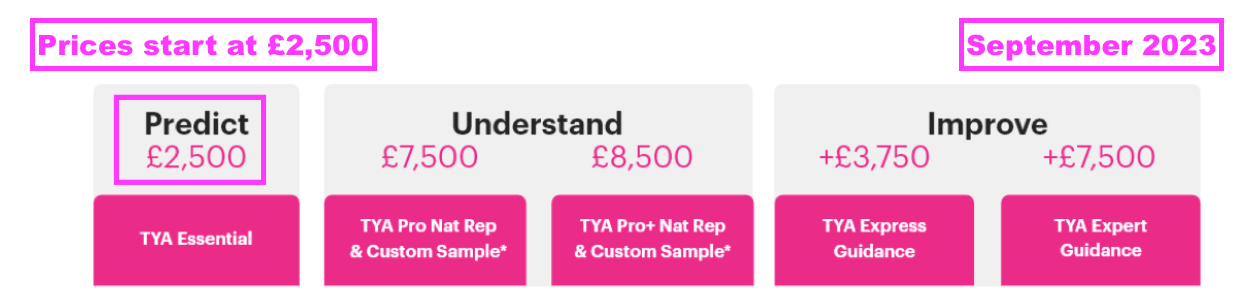

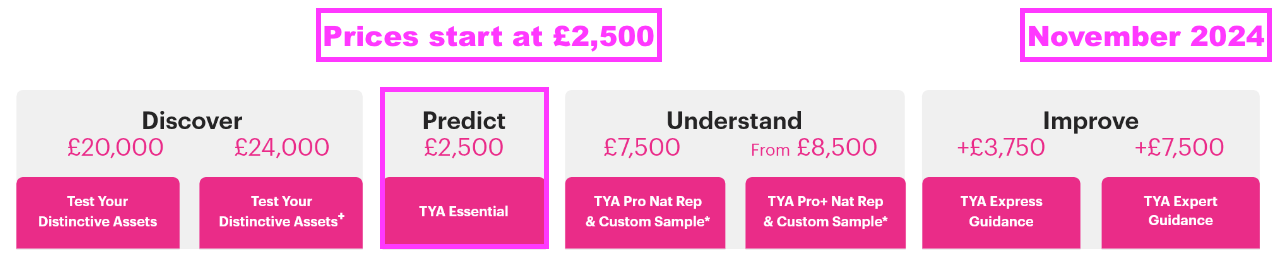

- My H1 2023 review — published during March 2023 and therefore before this FY commenced — showed TYA prices starting at £2,000…

- …while my FY 2023 review — published during September 2023 and therefore during this FY — showed TYA prices starting at £2,500:

- TYA prices have not changed since 2023:

United States

- This FY recounted the “massive opportunity to win” in the United States:

“We believe we have significant headroom to grow the base of the business we have today… as well as the massive opportunity to win in the US, where we have the chance to create an Innovation offering that is as great as our Advertising offering and to continue to win with the world’s largest advertisers.”

- New appointments have been made to capture greater US revenue:

“We are making headway into the US market. Our go-to-market investment in FY24 has grown our fame, and we plan to increase this investment for the year ahead. We have strengthened the commercial teams across sales and marketing, with Michael Perlman joining as global Chief Commercial Officer, and Alex Banks as SVP Commercial Americas, leading the US and LatAm sales teams – both executives are based in the US and have significant commercial leadership experience in our industry sector. “

- Michael Perlman and Alex Banks are SYS1’s latest pair of senior US salesmen.

- The 2023 Capital Markets Day revealed the appointments of Jason Chebib and Steve Olenski as senior US executives…

- …while the comparable FY confirmed the appointments of Jon Bond and Noah Brier as US advisors:

- According to social media, Messrs Chebib and Olenski no longer work for SYS1, while SYS1 has never since mentioned Messrs Bond and Brier.

- Mr Perlman participated in SYS1’s Canaccord Annual Growth Conference presentation during August, which suggests he may be a longer-term appointment:

- Management during my Q&A said Mr Perlman:

- Is “very well trained and seasoned“;

- Is a “super fit” for the business;

- Had “hit the ground running“;

- Will do a “very good job” by employing the “right system, the right process and the right people”;

- Has been “renegotiating some of our contracts with some of our big clients”, and;

- Can “motivate to push for bigger numbers year on year”.

- Management also cautioned during my Q&A that salaries of US salespeople are “double” what they are in the UK, but “you do get a lot of impact“.

- The push into the US was reflected by this FY disclosing US revenue for the first time since FY 2018:

- SYS1 amalgamated its US revenue into ‘Americas’ revenue during FY 2019, which in hindsight may have signalled all was not well within the US operation back then.

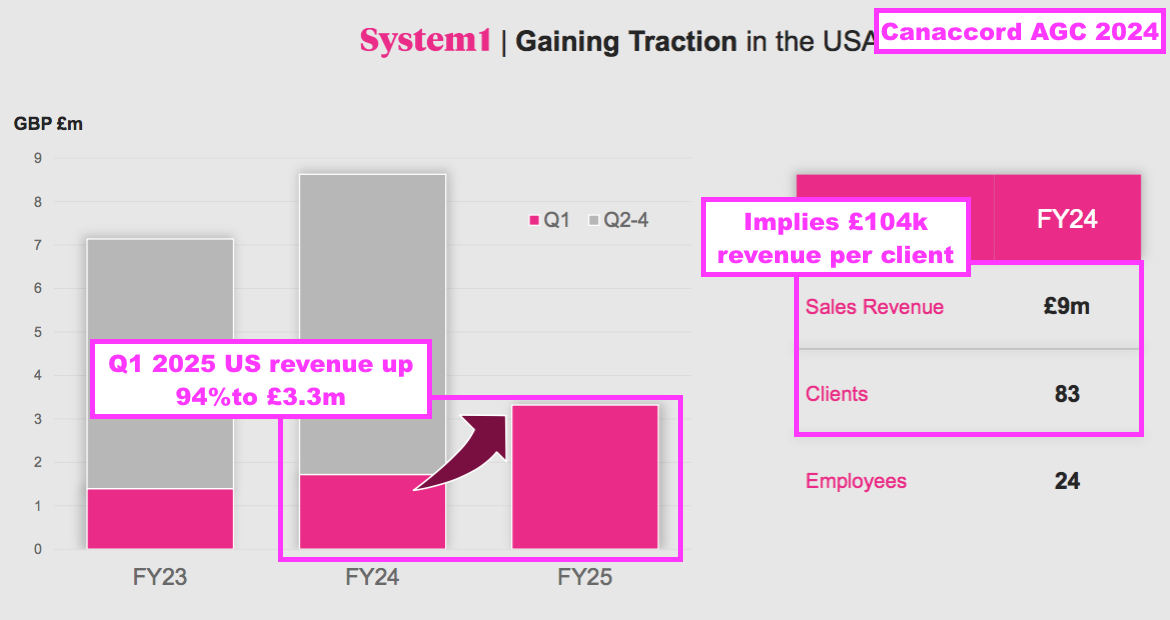

- This FY witnessed US revenue gain 22% to £8.6m to represent 29% of total revenue.

- The US had been SYS1’s fastest growing and largest market. Between FYs 2006 and 2016, US revenue surged from £0.4m to £12.5m to support 40% of total revenue.

- Note also that innovation testing supported 42% of revenue during SYS1’s FY 2016 US heyday:

- SYS1 therefore has a strong US-TYI heritage, which I trust Mr Perlman can exploit to the full alongside TYA.

- Management acknowledged the importance of US-TYI during my Q&A:

“We can’t hang around…we need to get our flag in that US innovation space. That’s why we said this is a year of investment“.

- Mr Perlman’s Canaccord presentation revealed this FY served 83 US clients:

- Revenue per US client was therefore £104k (£8.6m/83), which means revenue per non-US client was £62k (£21.4m/345) and underlines why SYS1 is focused on “winning in America“.

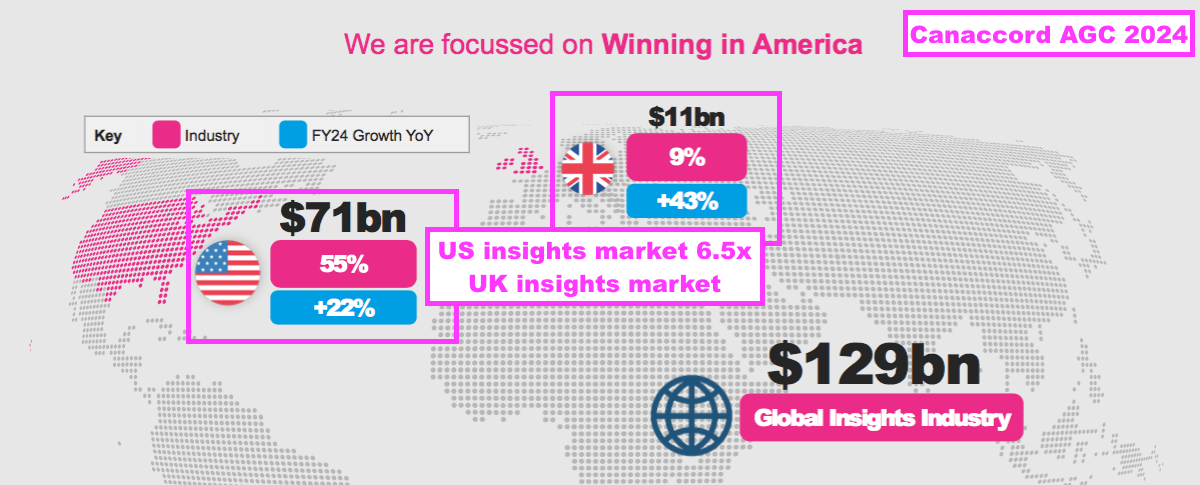

- Indeed, Mr Perlman’s Canaccord presentation suggested the US ‘insights’ market was at least six times larger than the equivalent UK market…

- …which may imply US revenue could in time reach six times this FY’s UK revenue of £12.7m (i.e. £76m).

- Mr Perlman’s Canaccord presentation also confirmed US revenue jumped 94% to £3.3m during Q1 2025 to support 35% of total Q1 revenue. The subsequent Q2 2025 update revealed US revenue advanced 60% (see Q1 and Q2 2025 trading statements).

Employees and bonuses

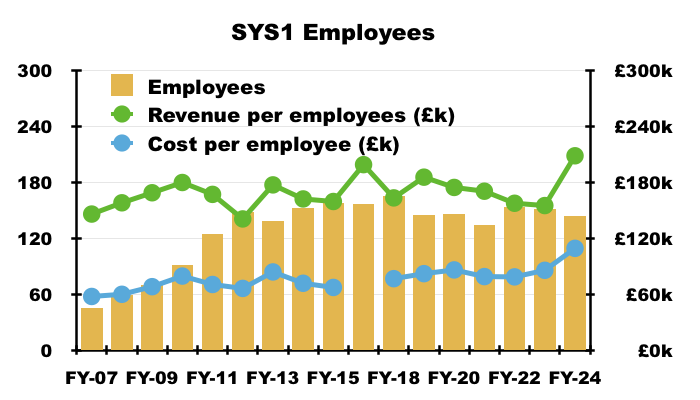

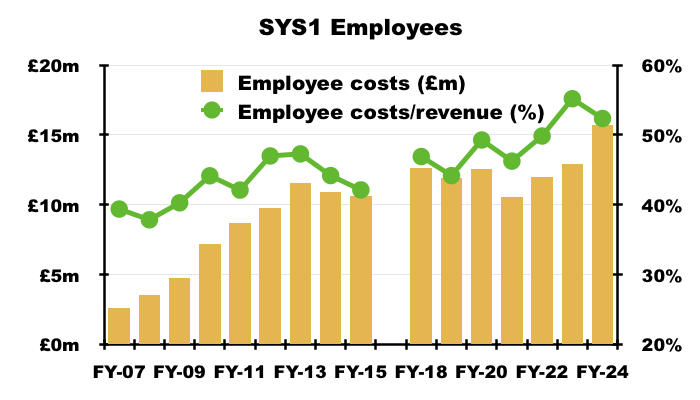

- Probably the most encouraging development during this FY was lifting revenue by 28% with seven fewer employees:

- FY revenue of £30.0m and the 144 headcount equated to a new record revenue per employee of £208k:

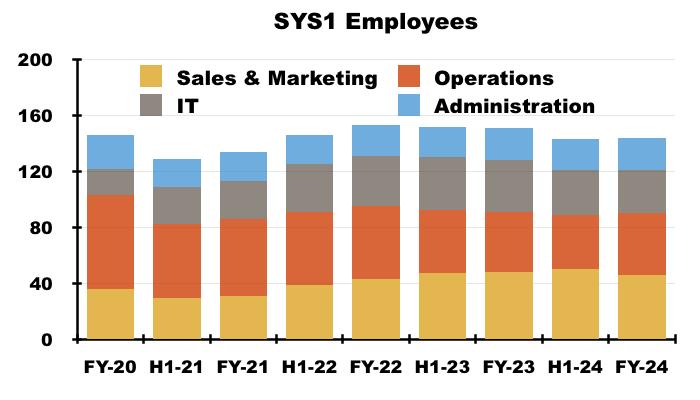

- My chart below shows how the roles within SYS1’s workforce have changed between FY 2020 and this FY:

- The workforce proportions have changed as follows:

- Sales and marketing: from 25% to 32%;

- Operations: from 46% to 31%;

- IT: from 13% to 22%, and;

- Administration: maintained at 16%.

- The shift away from ‘consultancy’ operations staff towards sales and IT employees clearly reflects the group’s platform strategy and — encouragingly — SYS1”s “scalable growth model” beginning to emerge on a per-employee basis.

- This FY said another 20 employees would be recruited during FY 2025:

“We recognise that we will need to invest in FY25 to deliver our growth ambitions and we have created, and are already filling or recruiting 20 new roles in FY25. As the business grew faster than expected in FY24, some of these roles are in operational and support positions to ensure we continue to deliver high-quality outcomes for our clients. The other roles are investments in future growth across our commercial and marketing teams, with significant focus in the US.”

- Although 20 extra employees versus a 144 average during this FY suggests the average headcount could advance 14%…

- …the Q1 and Q2 2025 trading statements indicate the additional staff are performing well with H1 2025 revenue up 38% (see Q1 and Q2 2025 trading statements).

- Management made the following points about recruitment during my Q&A:

- Some of the 20 new employees are “catch-up” recruitment;

- About two-thirds of the 20 new employees are sales and marketing, with the rest being ‘back office’;

- New sales and marketing staff tend to take one to two years to reach their expected “annual quota“;

- “We’re growing the business fast and we need to keep growing fast. These 20 do not mean we’re done.“;

- “We’re comfortable” the new recruits can help SYS1 “achieve the numbers that Canaccord have set out for the year“, and;

- The average headcount for FY 2025 may be approximately 160, which could in time support revenue “the other side of £40m“.

- This FY claimed the group’s “performance culture” underpinned the positive progress:

“FY24 has been a strong year in building out our performance culture and we have highly motivated teams with strong retention and employee engagement. We create an environment where all colleagues can do their jobs with ease to ensure they are focussed on adding value to our clients. We monitor staff satisfaction quarterly with focus teams owning actions on the feedback provided. By removing the blockers from our teams’ day-to-day lives, we have seen staff happiness reach record levels in FY24, and this was further enhanced with System1 recognised as a “Sunday Times Great Place To Work” in the UK for the first time.”

- The “performance culture” appeared driven by a revamped bonus scheme that paid an extra £2.8m during this FY:

“In the second half of FY23 we changed the way that most people in the business are rewarded by placing greater emphasis on variable pay linked to growth in the Group’s gross profit. FY24 was therefore the first full year of this approach which we believe is working well. Whereas only a few colleagues received a cost-of-living increase to their salary, variable pay across the Group rose by £2.8m year-on-year as a result of significantly higher sales volumes and improved profit margins.”

- Bonus and commission expenses were £453k during the comparable FY, suggesting this FY’s total variable pay was approximately £3.25m (£2.8m+£453k).

- Board remarks at the 2024 AGM said the bonus-inspired culture “worked brilliantly“:

[AGM 2024] “One of the things we felt was really missing in the company was short-term incentives to drive the sales process. And it also gives us flexibility on our cost base if we don’t hit targets because obviously it’s very much variable and was based on huge stretch targets. And we’re delighted to say it worked brilliantly. There is no other word for it“

- The preceding H1 reported staff bonus and commission payments of £1.1m, which implies H2 paid out £2.15m.

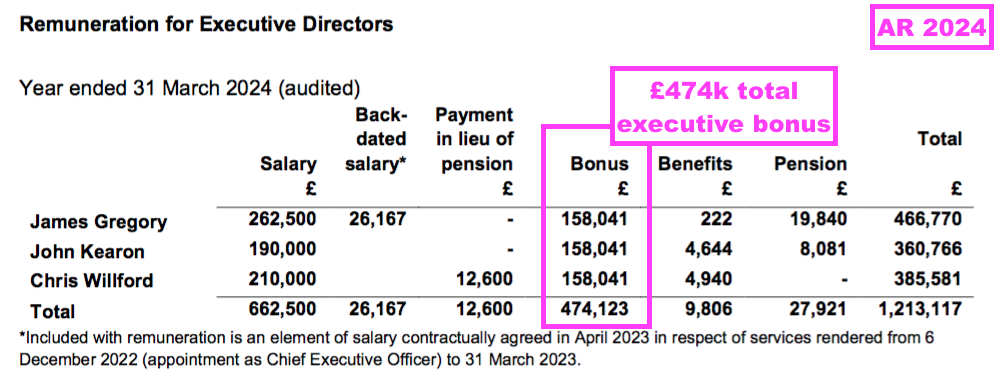

- SYS1’s three executive directors collected a combined £474k of the total £3.25m — the first boardroom bonuses paid since FY 2013:

- The long absence of boardroom bonuses is due to SYS1’s LTIP scheme, which dictated participants would forgo annual bonuses in exchange for the LTIP’s options:

[AR 2014] “Under this proposed [LTIP] scheme the executive directors will forgo all annual bonuses, but receive equity options based on a substantial increase in earnings per share over the three years, backed by a share price underpin. The members of the senior management team will have an increased bonus potential of up to 50% of base salary, but without any future equity participation.”

- Despite the LTIP dictating the executives would not receive bonuses, last year the board introduced an executive bonus scheme for this FY:

[AR 2023] “In the period to March 2023 the Committee judged that delivery of the Group’s long-term growth strategy was the primary objective and no short-term awards were granted. For the period to March 2024, the Committee considered that, in light of the recent strategic review, short-term incentives (bonuses) matched to the near-term goals of the strategic review would be applicable to retain and reward Executives.”

- This FY’s positive performance confirms the annual bonuses worked very well, although whether the senior management still require an LTIP — which last vested during FY 2017 — remains up for debate (see LTIP).

- Employee bonuses are based mostly on gross profit, which during this FY advanced by £6.4m, or 32%, to £26.1m.

- Extra variable pay of £2.8m therefore absorbed 44% of that extra £6.4m gross profit, which is a significant proportion and perhaps indicative of SYS1’s “scalable growth model” accruing more benefits to staff than shareholders.

- Indeed, this FY’s total staff costs increased 22% to £15.7m and absorbed 52% of revenue:

- However, board remarks at the 2024 AGM did not indicate every £6.4m of additional future gross profit would have £2.8m absorbed by extra variable pay:

[AGM 2024] “It isn’t a strictly linear relationship between gross profit [and variable pay].

For example, for people with sales incentives, their incentives will be very much aligned to their on target earnings, their salaries. So they may have a potential of earning 30% or 50% or 80% of salary. And that, whilst it’s linked to financial performance, is not a distribution of a share of gross profit.”

“And I think it’s also worth saying that the targets are stretching because we want to carry on having a good performance”.

“If the level of performance improvement is similar this year versus last year, you can expect a similar level of payout, not double the payout.”

- I interpret those AGM remarks as meaning SYS1 could repeat this FY’s estimated £3.25m variable pay if gross profit during FY 2025 repeats this FY’s 32% growth.

- This FY mentioned the executive bonuses only for this FY and the comparable FY:

“FY23: Participants in the 2021 LTIP did not participate in the Company’s annual bonus or profit share scheme and had no other short-term incentive plans. Therefore, over the period to March 2023, the only remuneration received was base salary and benefits.

FY24: Executives earned cash bonuses for exceeding annual targets. Targets were set such that no bonus accrued until Adjusted Profit before Taxation (= Profit before Taxation and Share-Based Payments) exceeded the budgeted performance for that measure. In view of the exceptional performance during FY24, with profit before taxation up by over 4x on FY23, and progress made towards delivering the long-term strategy, the Committee decided to remove the originally proposed 50% of salary cap on the FY24 bonus for Executive Directors.“

- Board remarks at the 2024 AGM confirmed the existence of an executive bonus scheme for FY 2025, although the measures used were not disclosed:

[AGM 2024] “Into FY 2025, there is a similar mix of fixed remuneration, variable short-term remuneration. It’s…a very similar structure in terms of it being aligned with the financial performance of the business.“

LTIP

- This FY mentioned the group’s LTIP was unlikely to vest:

“During the year we reintroduced a short-term incentive plan (STIP) for members of the executive committee and our three executive directors. We did this because in spite of the impressive turnaround in financial performance, the Long-Term Incentive Plan will likely not meet its lowest threshold even if revenue growth in the new financial year matches an exceptional FY24.”

- To recap, SYS1’s current LTIP was introduced during FY 2017, was extended during FY 2019 and then modified during FY 2021 with some vesting conditions reduced and the plan limit increased to 10% of the share count.

- The LTIP’s current vesting conditions are:

- A share price of 400p or more;

- Revenue of at least £45m, with full vesting at £88m;

- Adjusted earnings greater than zero, and;

- The remuneration committee “being satisfied with the level of profitability for the financial year immediately preceding the year of vesting and the overall corporate and share-price performance since 31 March 2021.”

- The LTIP expires after FY 2025, and this FY did not expect revenue to increase a further 50% to £45m by FY 2025 for the LTIP to vest:

“This means that 50% revenue growth is required in FY25 for any vesting to occur under the 2021 LTIP and accordingly no charge has been recognised in FY24 as the probability of this being achieved has been assessed as low.”

- This FY indicated the senior managers plan to enjoy both annual bonuses and an LTIP during FY 2025 and beyond:

“The retention and reward of our key people is a mission critical priority. Going forward we favour a blend of short- and longer-term incentives for the most senior executives and will provide further detail on this in 2025.”

- As mentioned earlier, SYS1’s LTIP was approved by shareholders on the understanding that the LTIP participants forwent annual bonuses.

- The aforementioned “brilliant” impact of short-term bonuses on this FY’s performance might suggest SYS1 does not need an LTIP to prosper.

- Board remarks at the 2024 AGM said the LTIP was needed to help staff retention and engender employee-shareholder alignment should the company grow “three, four, five times“:

[AGM 2024] “In principle, we think we do [need an LTIP]. A lot of it’s to do with the nature of the senior employees in the company, who are quite entrepreneurial and very ambitious. Some of them could, in different circumstances, go off and then [start] their own businesses.

A long-term scheme has much more capability to retain people for the long term rather than saying ‘we had a great year this year, can’t say we’re having a great year next year, so I’m out of here’.

“We want the employees to be aligned with shareholders’ long-term vision for the business, and not focus very much on the short term”.

“The LTIP [allows employees to] benefit alongside shareholders. If we grow the company three, four, five times, where is the employee’s longer term reward for being a big part of that? And the answer is the LTIP.“

- A revised LTIP covering FYs 2026 to (probably) 2029 is expected to be presented to shareholders for approval at the 2025 AGM.

- The current LTIP’s minimum revenue target of £45m and maximum revenue target of £88m are very attractive to shareholders given this FY’s revenue of £30m.

- However, board remarks at the 2024 AGM did not commit to retaining the LTIP’s £45m-£88m revenue range:

[AGM 2024] “There aren’t many of the characteristics [of the current LTIP] you won’t see in the new scheme. Importantly, the targets, both market conditions and non-market conditions, they will flow somewhat from… what the business should be achieving over three years, five years.”

“We need the targets to be both stretching and challenging, but also achievable so that the LTIP remains an incentive to them. And there’s a delicate balance to get right. Therefore, we think you’ll see a range as we did before, but probably not such an extreme range between thresholds and the kind of stretch performance.”

—

“There’s a difference between ‘finger in the air ambitions’ and actually stuff based on a practical analysis of the reality of the situations we face and the markets we face.“

- I interpret those board remarks as meaning the revised LTIP will almost certainly lower the £88m maximum revenue target and quite likely lower the £45m minimum target as well.

- I believe the revised LTIP’s minimum revenue target should remain at £45m.

- After all, with a minimum £45m revenue target, this FY’s £30m revenue needs to advance by 50% by FY 2026 for the revised LTIP to vest…

- …which does not seem an outlandish target for a business that has just recorded H1 2025 revenue growth of 38% (see Q1 and Q2 2025 trading statements).

- I believe the revised LTIP’s maximum revenue target should remain at £88m.

- After all, if the revised LTIP runs to FY 2029, then increasing FY revenue from £30m to £88m by FY 2029 requires a 24% CAGR — a growth rate that does not seem outlandish given those board AGM remarks of employee-shareholder alignment should the company grow “three, four, five times”.

- If the LTIP targets are reduced, then the number of LTIP options should be commensurately reduced as well.

- This FY confirmed the number of LTIP options:

“At 31 March 2024, the number of options granted under the 2021 LTIP reached 1,185,139 (or 9.0% of issued ordinary share capital of maximum capacity at 10%).”

- I calculate the current LTIP (and 58k various other options) could increase the share count by up to 1,244k, or 10%, to 13,933k.

- Unlike the addressable-market stats and “illustrative at scale” projections (see Valuation), the revised LTIP’s revenue-target range will reveal the board’s true growth ambitions and what really could be achievable during the next few years.

- I would also like the revised LTIP to reinstate a “profit underpin“. When the current LTIP was introduced during FY 2017, earnings had to reach £7m before any vesting occurred.

- The revised LTIP really ought to include an adjusted Ebitda underpin before any vesting occurs, which should help cement the all-important employee-shareholder alignment.

- After all, SYS1 now tracks an adjusted Ebitda KPI and has tantalised investors with an illustrative “at scale” adjusted Ebitda projection (see Valuation).

- …which suggests outside shareholders can safely trust the board to implement a first-class revised LTIP…

- …assuming the board is serious about employee-shareholder alignment and growing the company “three, four, five times”.

Financials

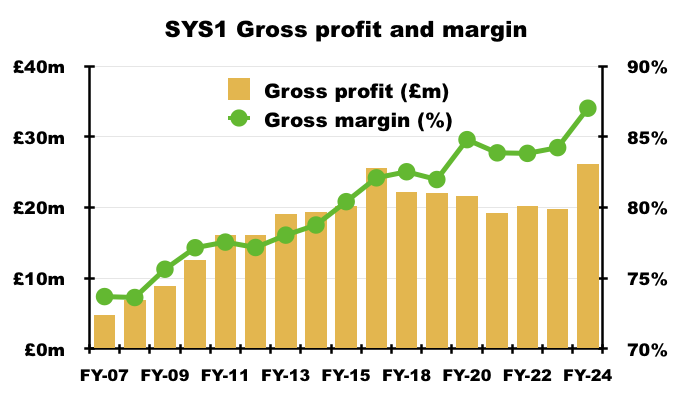

- The most promising financial measure of this FY was gross margin, which set a new FY record of 87%:

- An 87% gross margin implies SYS1 can buy online-panel responses for £13 and repackage that data for sale at £100.

- The H2 gross margin of 86% could not match the bumper H1 gross margin of 88%.

- The FY 87% gross margin exceeded SYS1’s minimum “at scale” 85% gross margin:

- The gross-margin improvement followed “efficiencies in the supply chain“:

“Direct costs increased by 6% year on year on revenue growth of 28%, reflecting a higher proportion of platform revenue and efficiencies in the supply chain, including further automation and new outsourcing partners. As a consequence of these improvements the gross profit margin rose by 3 points to 87%“

- This FY webinar said the gross-margin improvement was due in part to a new “API solution” and price increases:

“Gross-profit margin bounced up three points to 87% on the back of some supply chain efficiencies, including an API solution that allows us to onboard new respondent panel suppliers and increase competition between our suppliers.

We also managed to put some price increases through last year and the year before which also helped margin.

We’re not guaranteeing to keep gross-profit margin rising above last year’s level and we’re not even guaranteeing to keep it at last year’s level because it is exceptionally high in our sector at 87%.

Our benchmark for gross profit margin is 85% and we’ve been at or around that for a few years now. If we start to fall below that 85% then that probably means we need to increase our prices.”

- Management said during my preceding H1 Q&A that more than 80% of direct costs relate to outsourced panels.

- This FY’s operating profit was bolstered by two one-off items.

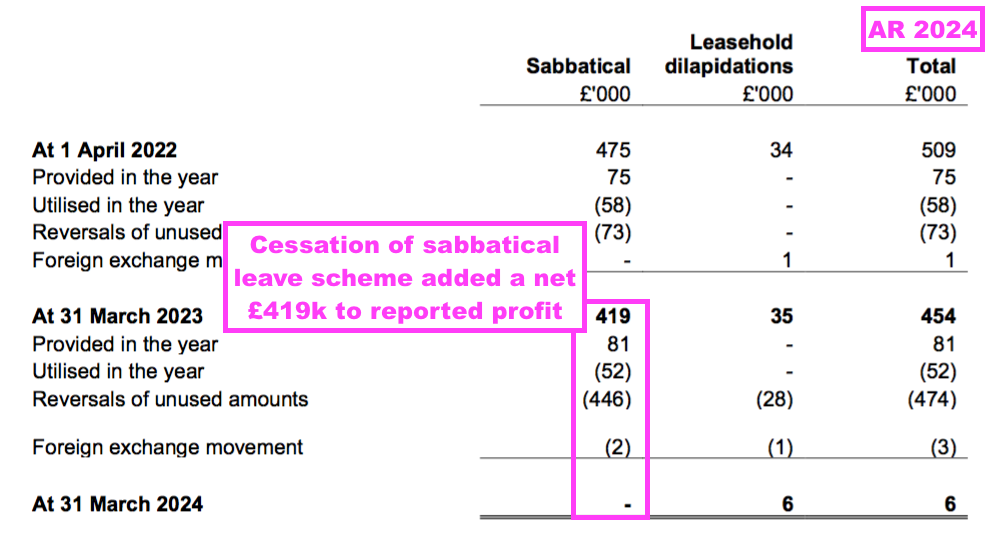

- First, a net £419k provision reversal relating to the cessation of the group’s sabbatical leave scheme:

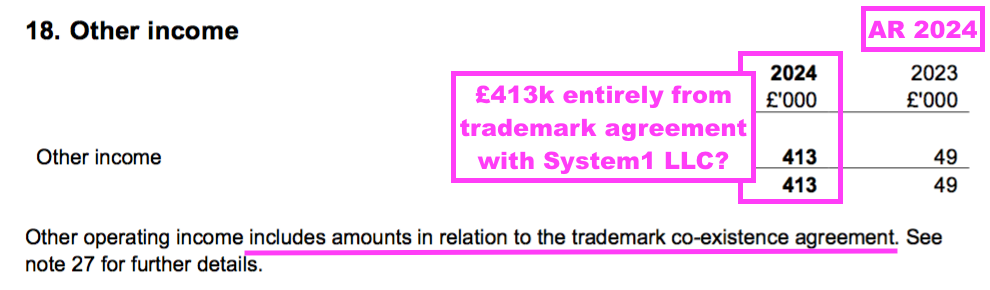

- Second, ‘other income’ of £413k that seemed related entirely to a trademark-settlement agreement:

- Reported operating profit of £3.1m was therefore £2.3m excluding these two items.

- Reported adjusted Ebitda of £4.4m was therefore £3.5m — and the adjusted Ebitda margin was therefore 12% — excluding these two items.

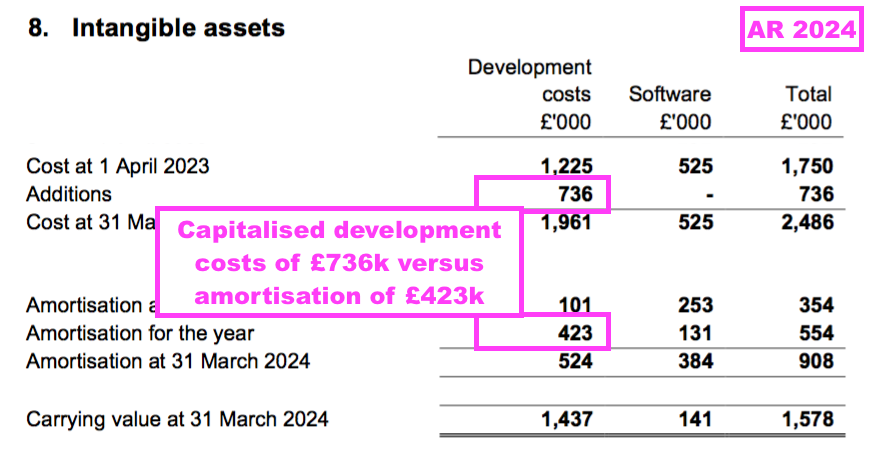

- Note also that development costs of £736k were capitalised onto the balance sheet, with only a £423k amortisation charge expensed against this FY’s profit:

- Capitalised development costs of £1.4m remain to be expensed against future profit, although this FY hinted such capitalised costs ought now to reduce.

“Development costs relate to costs capitalised for the development of the “Test Your” platform (carrying value £464k; 2023: £865k), which completed during the year ended 31 March 2023, and the Supply Chain Automation platform (carrying value £930k; 2023: £259k), which enables System1 to interface (via API) with multiple suppliers of panel respondents, was substantially completed at the end of the year ended 31 March 2024.”

- Indeed, H2 capitalised costs amounted to only £236k and were satisfactorily reflected by the associated H2 amortisation charge against earnings of £229k.

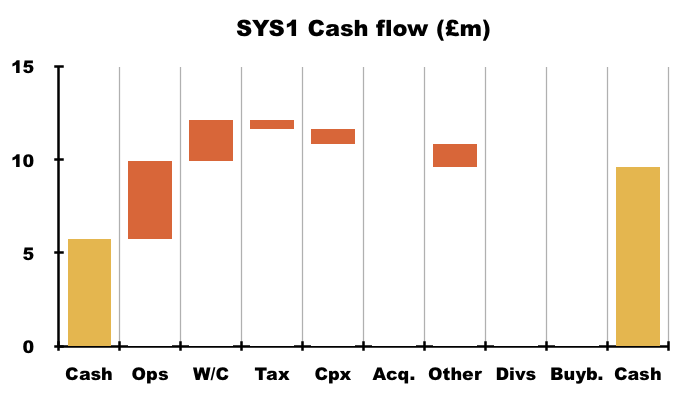

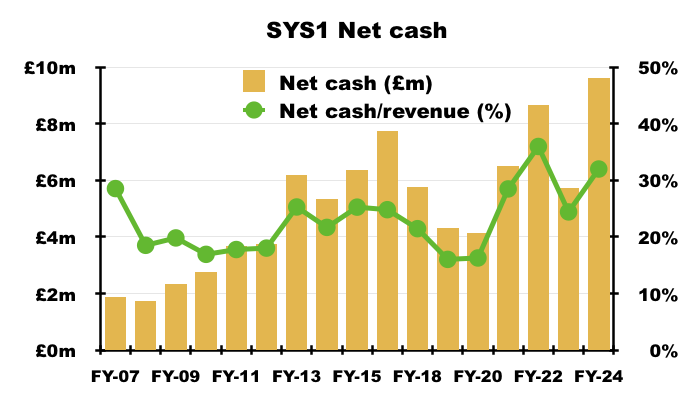

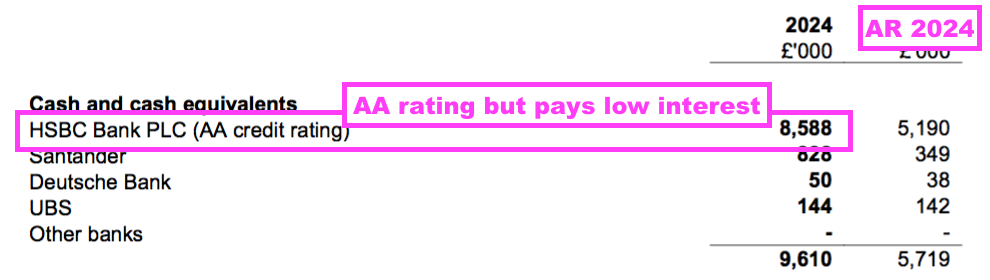

- Cash generation appeared adequate after net cash ended the FY £3.9m higher at £9.6m:

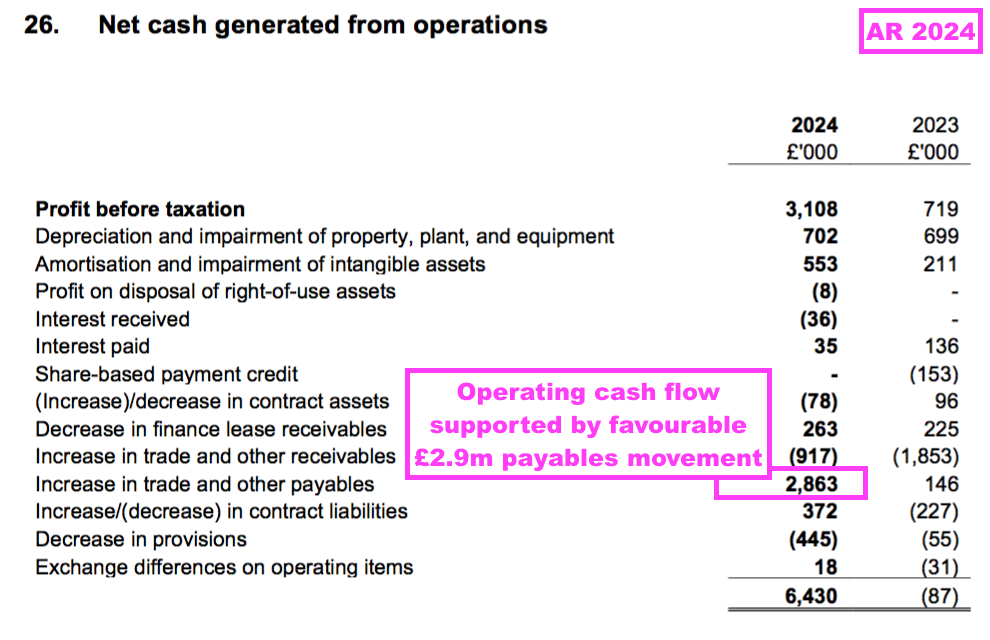

- Mind you, a favourable £2.9m payables movement mostly supported the free cash performance…

- …which reflected staff bonuses of £2.6m owed at the year-end (see Q1 and Q2 2025 trading statements).

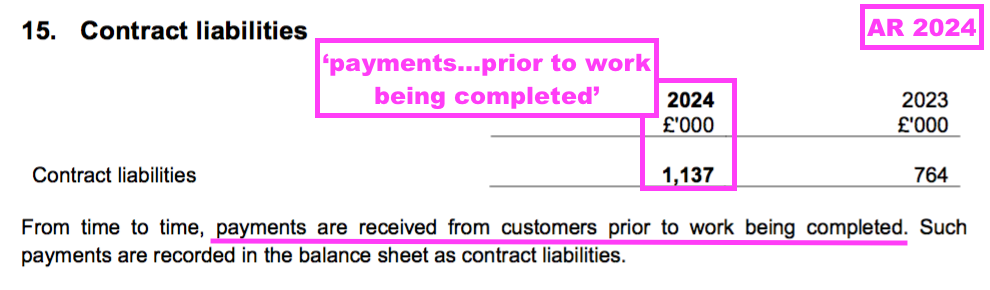

- Helping cash flow as well are ‘contract liabilities’, which reflect up-front customer payments and ended this FY at a useful £1.1m:

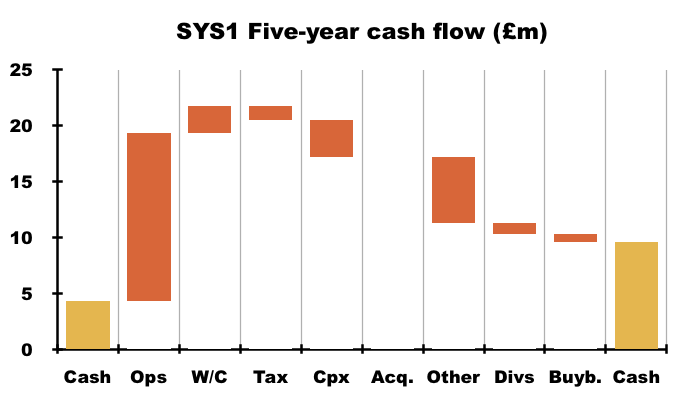

- Despite including some very difficult years, SYS1’s five-year cash flow seems quite credible after being assisted by favourable working-capital movements and modest tax payments:

- ‘Other’ in my cash-flow chart above is dominated by office lease costs, which run at approximately £1m a year and should not be ignored when evaluating SYS1’s cash flow.

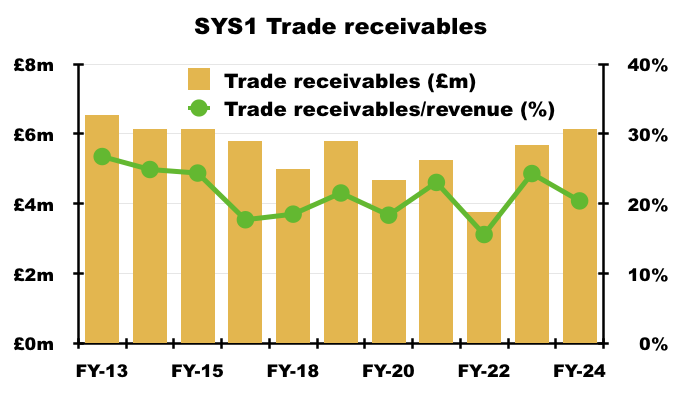

- FY trade receivables at £6.1m were equivalent to 20% of revenue, a proportion that did not suggest SYS1 had extended credit terms to win extra custom:

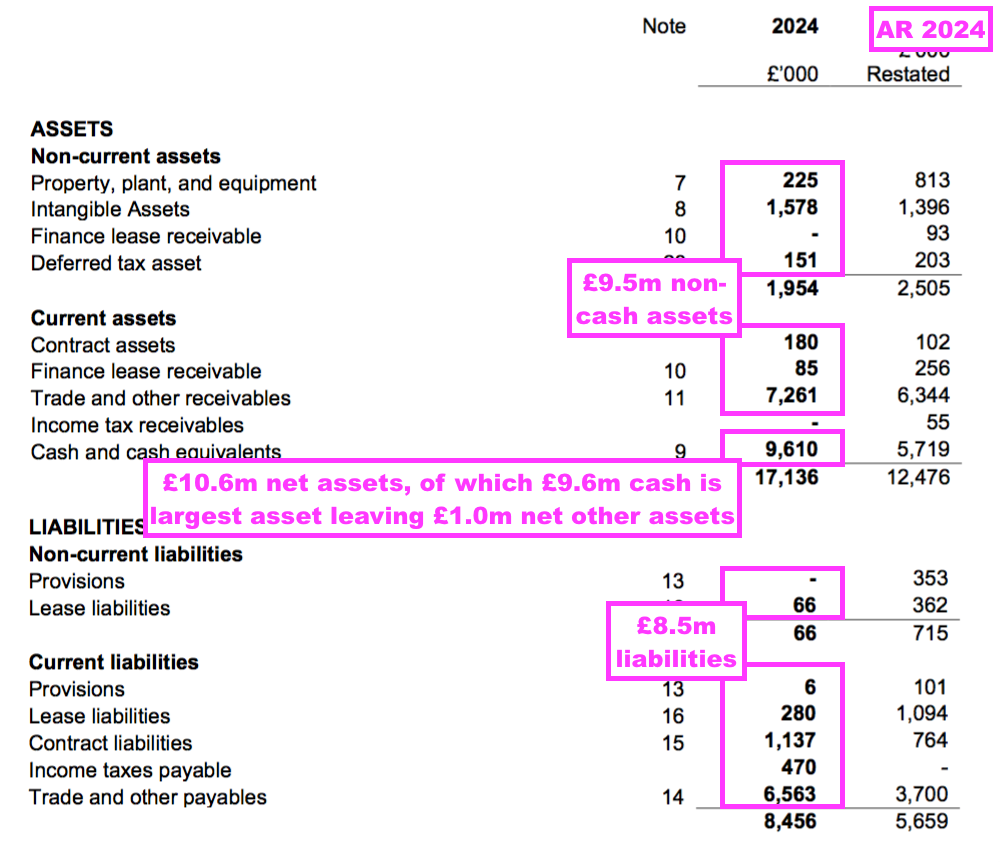

- SYS1’s balance sheet implies the business is an inherently capital-light operation.

- FY net assets of £10.6m less the net cash of £9.6m leaves just £1m covering net working capital, intangibles and tax entries:

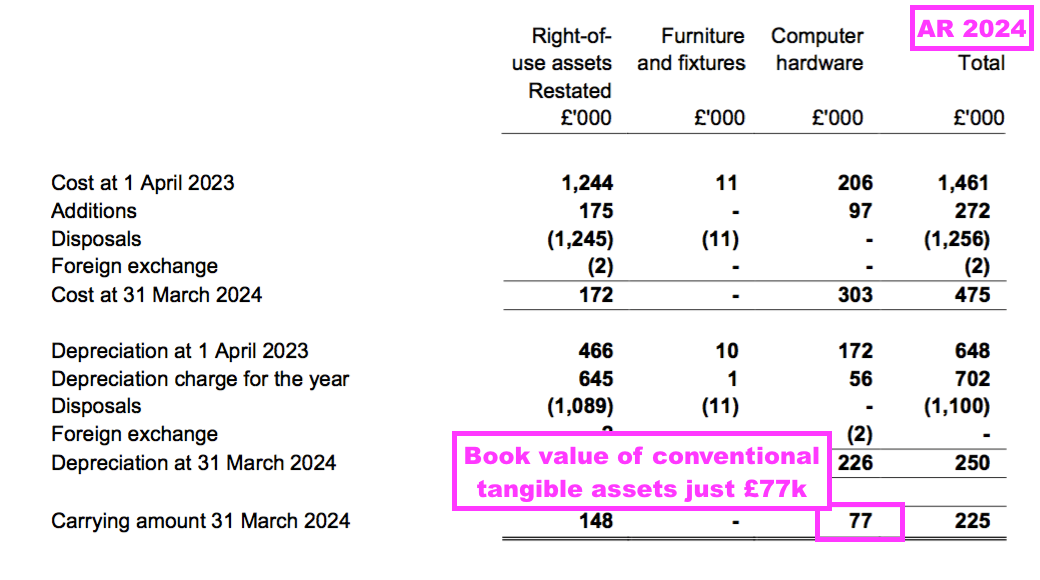

- In fact, FY conventional tangible assets are limited to just office computers with a £77k book value:

- This FY’s £9.6m net cash position was equivalent to a sizeable 31% of revenue:

- Management disclosed the following points about the cash during my Q&A:

- The board, “most shareholders” and “many customers” wanted to “see cash in the business“;

- Potential large customers can take “great comfort” from the group’s cash and knowing a new supplier “will be around” for the next few years;

- The group’s cash flow has “real seasonality“, with stronger H2 cash flow as bonuses and tax are paid in H1 (see Q1 and Q2 2025 trading statements), and;

- Surplus cash will be distributed through dividends because buybacks and tender offers “don’t work” with SYS1’s concentrated share register.

- Despite the significant cash position, this FY disclosed just £36k interest — all of which was recorded during H2 and equates to an annualised H2 interest rate of less than 1%.

- For perspective, fellow portfolio members Bioventix earned 3.3% and Tristel earned 2.5% on their respective cash.

- SYS1’s main bank is HSBC:

- Ditching HSBC and collecting, say, 2% on the £9.6m would earn SYS1 an extra £192k a year to help mitigate higher staff costs.

- SYS1’s “real seasonality” with cash flow was demonstrated through the subsequent H1 2025, during which cash declined by £0.7m (see Q1 and Q2 2025 trading statements).

- SYS1 continues to carry no bank debt and no pension complications.

Q1 and Q2 2025 trading statements

- SYS1’s Q1 and Q2 2025 trading statements were positive.

- The Q1 statement published during July revealed:

- Q1 platform revenue up 74% to £8.6m;

- Q1 US platform revenue up 164% to £2.9m (implying Q1 non-US platform revenue up 50% to £5.7m);

- Q1 non-platform revenue down 30% to £0.9m;

- Q1 total revenue up 53% to £9.5m;

- A Q1 gross margin of 87%, and;

- A Q1 cash outflow of £1.5m leaving net cash at £8.1m.

- The Q1 performance was better than SYS1 had expected:

[Q1 2025] “Customer demand was exceptionally strong in the first quarter, somewhat ahead of our own expectation. It’s early in the year but this strong first quarter performance puts us firmly on track for sustainable growth and to achieve our full-year expectations.“

- Those “full-year expectations” were the “market consensus” FY 2025 estimates of revenue at £36.5m and profit before tax at £4.4m (see Valuation).

- The Q2 statement published during October revealed:

- Q2 platform revenue up 35% to £8.2m;

- Q2 non-platform revenue down 32% to £0.7m;

- Q2 total revenue up 25% to £8.9m;

- An H1 gross margin of 87%, and;

- A Q2 cash inflow of £1.2m plus adverse FX movements of £0.4m leaving cash of £8.9m.

- The Q2 performance was not as exceptional as Q1, with platform revenue £0.4m lower during Q2 than Q1:

- The last time SYS1 reported a sequential quarterly reduction to platform revenue occurred during Q1 2024, following which SYS1 then reported four consecutive record platform-revenue quarters.

- The Q2 statement indicated a £2.4m H1 2025 pre-tax profit before a £0.1m credit:

[Q2 2025] “Based on the unaudited management accounts, the Group expects to report a Statutory Pre-Tax Profit of c£2.5 million for the half-year including a £0.1m credit to share-based payments (H1 FY24: £0.9m).”

- Doubling up the H1 2025 performance would give total revenue of £36.6m and a pre-tax profit of c£4.8m…

- …which at least match the aforementioned FY 2025 consensus estimates of revenue of £36.5m and profit before tax of £4.4m.

- The Q1 and Q2 statements both referred to buoyant US progress, with US revenue over the six months “more than double” that of the comparable H1 2024.

- However, H1 2025 growth was driven entirely by ad testing after innovation testing and brand tracking finished “broadly in line” with H1 2024:

- Fame-building activities for TYI have therefore still to emerge (or at least take effect).

- The Q2 update said:

[Q2 2025] “We are continuing to win and retain business with the world’s largest advertisers and will be accelerating and significantly increasing investment in the coming months to build our position in America and revitalise System1’s Innovation proposition.”

- I am not sure whether “revitalise System1’s Innovation proposition” means revitalising the TYI fame-building activities…

- …or actually revitalising the underlying TYI service.

- I do hope TYI does not require a second relaunch, although the aforementioned lack of TYI promotion on the group’s website is not encouraging.

- The Q2 statement also noted:

[Q2 2025] “Gross Profit in H1 FY25 reached £16.0m at a margin of 87.3% (H1 FY24: £11.7m at 87.8% margin). Operating expenditure increased by £2.6m (+23% on H1 FY24), due to increased investment in people, product and marketing to fuel the next phase of growth.”

- In other words, H1 2025 witnessed extra gross profit of £4.3m fund additional operating costs of £2.6m to leave an incremental profit of £1.7m — equivalent to 40% of the extra gross profit.

- For comparison, this FY witnessed extra gross profit of £6.4m fund additional operating costs of £4.5m to leave an incremental profit of £1.9m — equivalent to 30% of extra gross profit.

- Those rough sums suggest H1 2025 enjoyed an improved operating margin, but only the full results for H1 2025 (and beyond!) will confirm whether the platform economics are really strengthening and SYS1 is truly scaling its business for the benefit of shareholders.

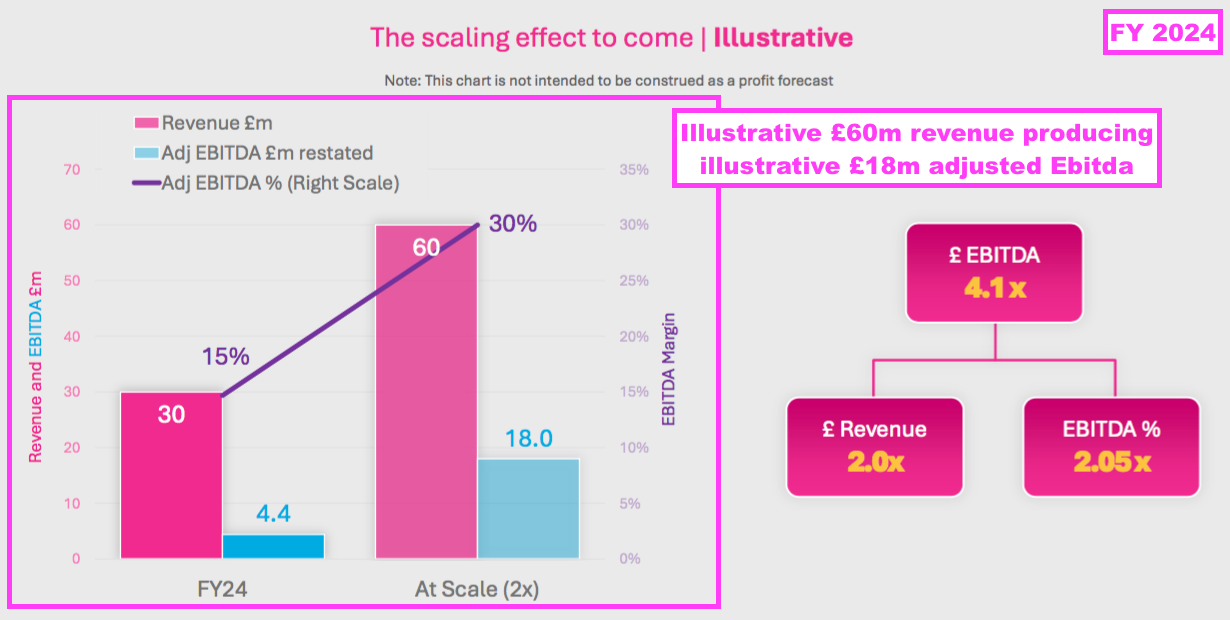

Valuation

- To demonstrate how SYS1 could scale its platform services for the benefit of shareholders, the FY presentation updated an illustrative projection of revenue doubling (to £60m) and the resultant projection of adjusted Ebitda (£18m):

- The £18m illustrative Ebitda projection seems a direct answer to a question Mr Barden raised at the April 2023 GM:

[Stefan Barden April 2023] “6) Valuation: As a result, and you might want to pass this to Chris, if successful, how much could System1 be worth in say 2 to 3 years time?

a) If you can’t give a valuation what would the shape of the P&L be? For example, your 25% CAGR sales growth aspiration is a doubling in sales every 3 years. What is the associated cost structure?“

- Mr Barden’s reference to “25% CAGR sales growth” reflected SYS1’s commentary ahead of the April 2023 GM:

[RNS 2023] “We have stated our ambition to become a Rule of 40 company. To do this, we will need to deliver revenue growth of the ‘Predict Your’ and ‘Improve Your’ products, plus EBITDA margin, to total 40. While we are in growth mode, we expect the majority of this to come from revenue, so the Company will need to be growing revenue at a minimum of 25% over the coming years.“

- If SYS1 expands its total revenue at a 25% annual compound rate, then the illustrative £60m revenue projection would be achieved after three years (i.e. during FY 2027).

- If both SYS1’s illustrative revenue and adjusted Ebitda projections are achieved during FY 2027, I would argue a small-cap growing revenue at a 25% CAGR and enjoying a 30% adjusted Ebitda margin would trade on a premium multiple….

- …and today’s £76m market cap would in turn offer compelling upside.

- Assuming:

- Depreciation and amortisation continue to absorb 5% of revenue, and;

- Tax is charged at the standard 25% UK rate…

- …the £18m illustrative Ebitda projection would translate into earnings of approximately £11m, which at, say, a 20x P/E would support a £220m market cap or a £16 share price on a fully diluted basis.

- SYS1’s illustrative projections do appear plausible.

- After all, very few quoted small-caps are confident enough to provide tantalising illustrative projections of revenue and Ebitda… and no sensible board would publish such illustrative projections unless they were reasonably achievable.

- I would venture £60m ought to be SYS1’s minimum revenue ambition given the aforementioned “3 Reasons to Believe” and:

- The platform services enjoy a ‘unique selling proposition of predictiveness’;

- The group has a negligible market share within a huge addressable market, and;

- The board has now established a “performance culture” for growth.

- Indeed, this FY’s revenue of £30m would be able to advance to £60m if, say:

- TYI platform revenue reaches c£15m (versus this FY’s TYA platform revenue of c£20m);

- TYA US platform revenue adds £10m to this FY’s estimated c£6m;

- TYA non-US platform revenue adds £10m to this FY’s estimated c£14m;

- TYB platform revenue remains unchanged, and;

- Non-platform revenue of £5m goes to zero.

- SYS1 has never put a timescale on its illustrative “at scale” projections, and I presume the longer revenue takes to double, the less likely the £18m illustrative adjusted Ebitda will be achieved due to cost inflation.

- Management said during my Q&A that achieving the illustrative projection by FY 2027 would be “pretty good going”.

- Management also said during my Q&A that a “lot” of shareholders would be “ecstatic” if revenue doubled to £60m and the adjusted Ebitda margin reached “north of 20%” rather than the illustrative 30%.

- I don’t understand why any shareholders should be “ecstatic” if the adjusted Ebitda margin reached “north of 20%” when SYS1’s “at scale” ambitions clearly show an Ebitda margin of 30% or more:

- The management Q&A left the impression the illustrative projection would not be achieved within three years, a feeling that is supported by the following broker estimates on SharePad:

- Revenue expected to advance from £30m to £42m by FY 2026 does indeed suggest attaining revenue of £60m — and the illustrative adjusted Ebitda of £18m — by FY 2027 will be a very a tall order.

- The FY 2025 estimates signal a 16% Ebitda margin, which in turn implies platform revenue must grow by 24% (to c£31m) for SYS1 to meet its Rule of 40 target.

- The FY 2026 estimates signal an 18% Ebitda margin, which in turn implies platform revenue must grow by 22% (to c£38m) for SYS1 to meet its Rule of 40 target.

- 24% and 22% platform-revenue growth is less than the 25% revenue CAGR cited by SYS1 ahead of the April 2023 GM:

[RNS 2023] “We have stated our ambition to become a Rule of 40 company. To do this, we will need to deliver revenue growth of the ‘Predict Your’ and ‘Improve Your’ products, plus EBITDA margin, to total 40. While we are in growth mode, we expect the majority of this to come from revenue, so the Company will need to be growing revenue at a minimum of 25% over the coming years.“

- All told, my £220m market-cap/£16 share-price calculations do seem too optimistic for FY 2027… but should still be viable for FYs 2028 or 2029.

- The broker forecasts within SharePad support a 25x P/E for FY 2025 and suggest the 600p shares are anticipating significant growth for FY 2026 and beyond:

- My optimistic projections must be countered by various possible drawbacks, including:

- Larger customers in the States take much longer to attract than expected;

- TYI struggles to re-establish itself due to insufficient ‘fame generation’ and/or having lost too much ground to dynamic rivals;

- Ebitda margins never reach the targeted 30% due to greater-than-projected staff bonuses, promotional spend and/or development costs;

- Employee productivity deteriorates as senior managers receive lower LTIP targets and diverge from the platform strategy to fulfil their own “outside interests“, and;

- The incoming batch of shareholders engages less with the board than the outgoing batch of shareholders, who originally pressed for the April 2023 GM and seemingly injected much-needed urgency into SYS1’s platform-strategy recovery.

- As shareholders await SYS1’s progress towards the illustrative £60m revenue and £18m adjusted Ebitda, the 5p per share dividend supports a tiny 0.8% income.

Maynard Paton

Hi Maynard