30 May 2023

By Maynard Paton

FY 2022 results summary for Tasty (TAST):

- A woeful H2 performance delivered a full-year £2m loss following a trio of Christmas-trading “impediments” combined with “unprecedented inflationary costs“.

- Rising staff wages, stagnant revenue per employee, a return to pre-pandemic rents and a debatable depreciation policy do not suggest TAST’s cost structure will improve any time soon.

- Comparisons with Restaurant Group and Fulham Shore suggest TAST’s menus are in fact inherently flawed and confirm a radical business overhaul was needed during the pandemic.

- The departure of an experienced industry manager after only a year as a TAST executive may well indicate the main Wildwood restaurant format is broken.

- TAST now looks a lost cause with a de-listing a possibility. I continue to hold with vague hopes of a recovery, although formal blog coverage has ceased.

Contents

- News link, share data and disclosure

- Why I own TAST

- Results summary

- Revenue and loss

- Restatements of FY 2021

- Revenue per restaurant and employee

- Financials: going concern, cash and deferred payments

- Financials: landlords and leases

- Financials: cost analysis

- Comparison with Restaurant Group and Fulham Shore

- Revised menu, expansion plans and board change

- Valuation and cessation of blog coverage

News link, share data and disclosure

News: Annual results for the 52 weeks to 25 December 2022 published 30 March 2023

Share price: 3.25p

Share count: 146,315,304

Market capitalisation: £4.8m

Disclosure: Maynard owns shares in Tasty. This blog post contains SharePad affiliate links.

Why I own TAST

- Disastrous ‘legacy’ shareholding bought initially due to experienced family management creating, building and then selling two quoted restaurant chains for £200m-plus.

- Bombed-out share price might provide substantial turnaround upside… assuming the group can return to — and then maintain! — a worthwhile level of profit.

- But difficult economic conditions have exposed inherent flaws within TAST’s cost structure and the main Wildwood restaurant format may now have become broken.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

Revenue and loss

- The preceding H1 2022 had already admitted a difficult H2 would hamper this FY 2022 performance:

“Like many of our competitors and the economy in general, we are facing severe headwinds. Inflationary pressures on food, labour and utility costs and the cost-of-living crisis will inevitably impact the performance of the Company for at least the remainder of the year.“

“...we brace ourselves for an even more challenging economic environment, which is beginning to adversely impact our profitability in the second half of 2022.“

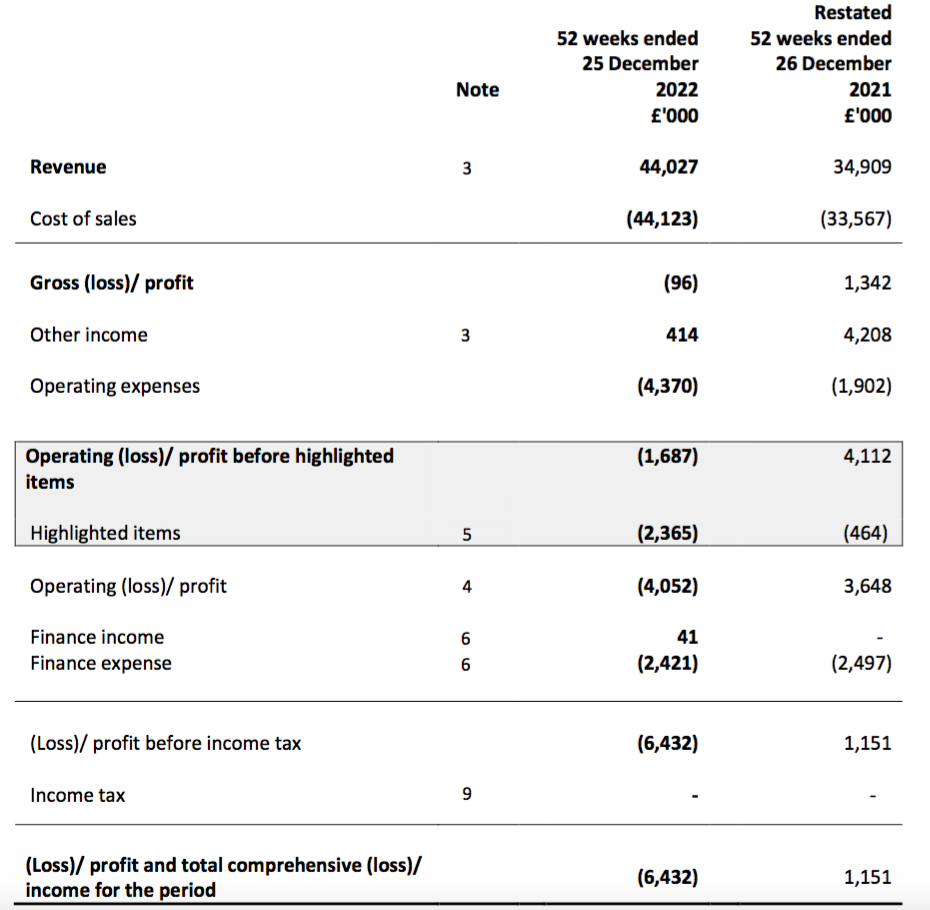

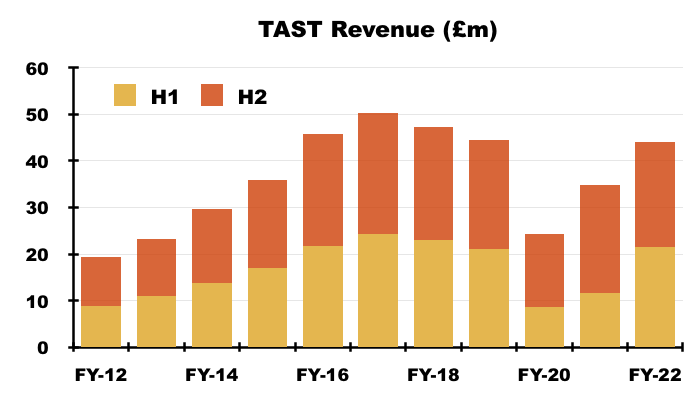

- FY revenue advanced 26% to £44.0m, but that improvement occurred entirely during H1:

- H2 revenue declined 3% to £25.5m and, pandemic-blighted H2 2020 aside, was the lowest H2 revenue since H2 2015 (£18.7m).

- TAST cited a trio of Christmas-trading “impediments“:

“The Group delivered strong sales growth, despite the severe impediments of transportation strikes, the World Cup, and bad weather all coinciding with the most important trading period of the year. We have estimated the adverse sales impact of all these factors to be in excess of £0.65m.”

- Even including TAST’s £0.65m estimate of lost festive trade, H2 revenue would still have been 1% lower than the comparable H2 2021.

- The preceding H1 commentary about the “more challenging economic environment” that was “beginning to adversely impact our profitability in the second half” was reflected very clearly within this FY statement.

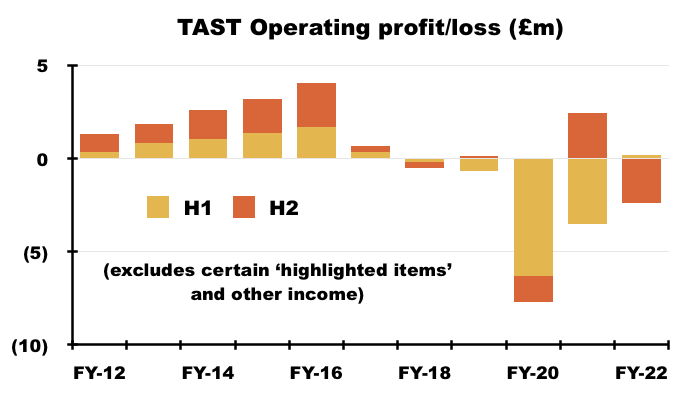

- TAST reported an FY operating loss of £2.2m before sub-let income of £0.4m and certain ‘highlighted items’ that totalled £2.3m:

- The preceding H1’s £0.2m profit before sub-let income and certain ‘highlighted items’ meant H2 delivered a woeful £2.4m loss. TAST explained:

“The energy crisis and unprecedented inflationary costs suppressed the results further, significantly increasing our running costs.“

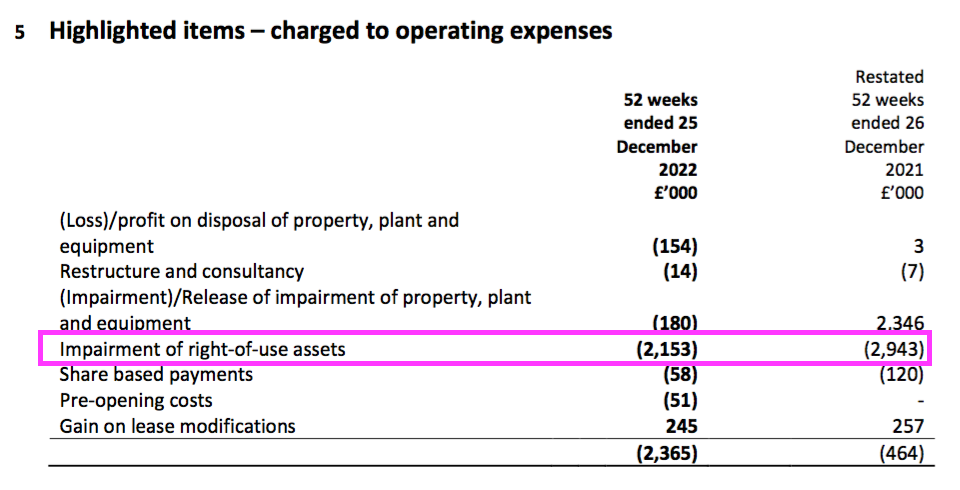

- TAST’s highlighted items were dominated by a further £2.2m write-off against the ‘right-of-use’ value of the group’s property leases:

- Write-offs against the value of the group’s ‘right-of-use’ property leases now total £15m since FY 2020 (see Financials: landlords and leases).

- This FY revealed a further restatement of the comparable FY 2021 results (see Restatements of FY 2021).

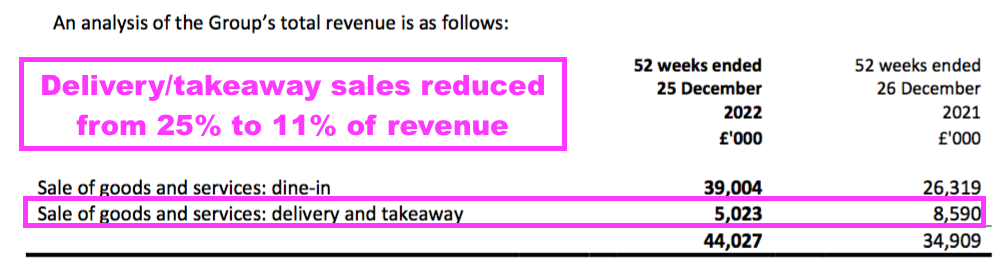

- TAST said this FY had witnessed a “marginal” return to dine-in sales:

“Delivery and takeaway have remained strong throughout the year but there has been a marginal shift towards dine-in.“

- Dine-in sales in fact increased from 75% to 89% of total revenue, with delivery/takeaway sales declining by £3.6m:

- I had hoped delivery/takeaway sales representing 25% of total revenue during the comparable FY 2021 would offer some hope of improved restaurant economics versus the minimal dine-in profits experienced prior to the pandemic.

- I am left to ponder:

- Whether the return to dine-in sales has led to this FY’s operating loss, and;

- What implications the lower delivery/takeaway sales will have on TAST’s future.

Restatements of FY 2021

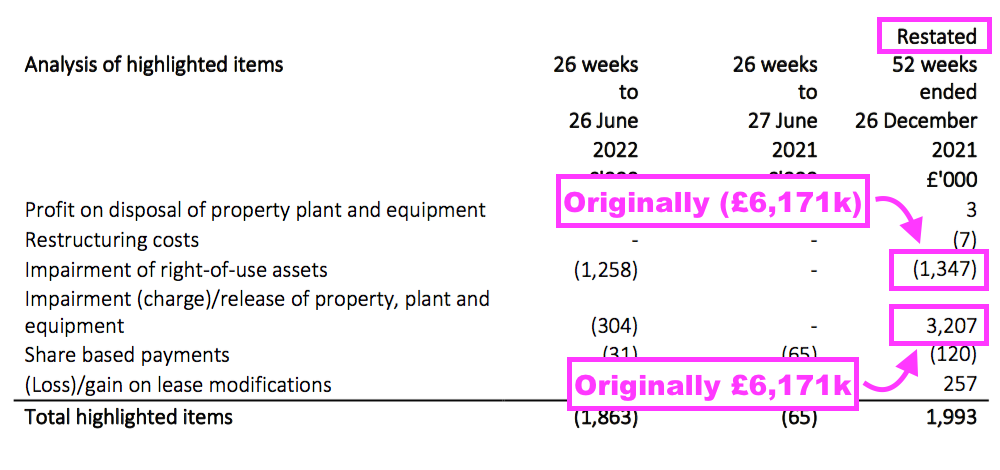

- TAST’s highlighted items showed a confusing pair of balancing £6,171k entries for the impairment and impairment release of tangible assets

- The preceding H1 2022 had restated those confusing FY 2021 figures:

- The H1 restatement added a further £2.4m to FY 2021’s total profit and was underpinned by a (revised) write-back of previously written-down assets:

- Revising annual earnings from £1.2m to £3.6m was not a great advert for TAST’s accounting, and February’s appointment of a new finance director was therefore very welcome.

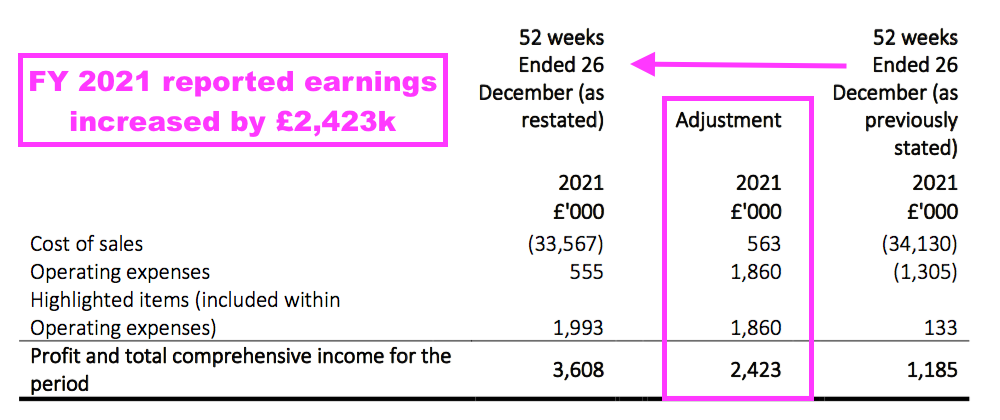

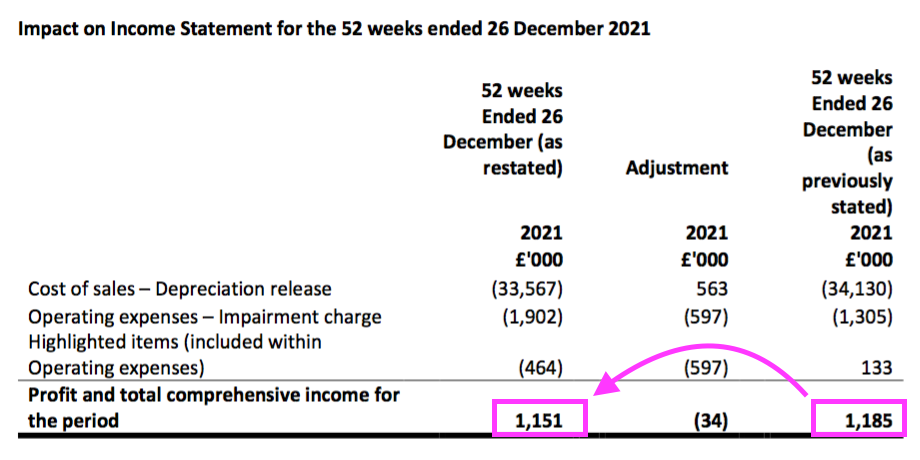

- The new finance director looks to have unearthed further errors. This FY admitted:

“During the preparation of the interim accounts, management identified a calculation error within the impairment workings for the prior year, whereby the depreciation that would have been charged had there been no impairment was not being correctly considered as per IAS 36. At this stage £1.9m was adjusted against 2021 reserves. However, on further review of the complex adjustment it was identified that the adjustment needed to be recognised in both 2020 and 2021. This resulted in an impairment release of £2.46m in 2020 and an impairment charge of £0.6m in 2021. The cumulative impact of this was £1.9m in line with the adjustment identified in the interim.

In addition, a related prior-year adjustment arising from the same issue has been recognised in 2021, whereby the depreciation charge on ROU assets should have been reduced for the impairment to allow depreciation to run to the end of the life of the lease.”

- Oh dear. After the original FY 2021 statement said earnings that year were £1,185k…

- … and the subsequent H1 2022 then claimed FY 2021 earnings were actually £3,608k…

- …. this FY statement now declared FY 2021 earnings were in fact £1,151k:

- The former finance director was paid a handy £150k last year to twice publish incorrect FY 2021 figures:

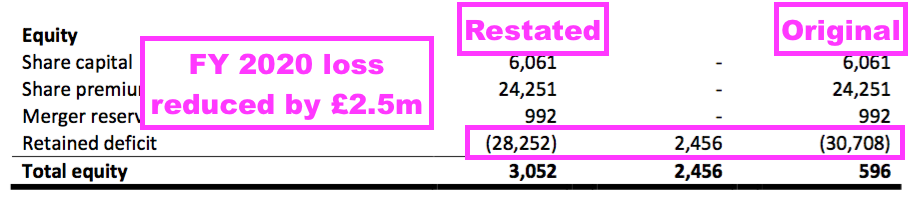

- Retained losses for FY 2020 were restated from £30.7m to £28.3m:

- Reducing FY 2020 retained losses by £2.5m means the reported loss for FY 2020 has been revised from the original £12.7m to £10.2m.

- A silver lining of TAST suffering ‘basket-case’ accounts for many years is such restatements (and re-restatements) are rather academic to the progress of the business.

- I am thankful the restatements reflect accounting adjustments to depreciation and write-offs, and not the discovery of missing cash.

Revenue per restaurant and employee

- This FY disclosed encouraging news about TAST’s pizza/pasta/burger Wildwood chain (48 sites).

- Another Wildwood previously blighted by the pandemic re-opened during H2, while the two Wildwoods yet to recover from Covid restrictions are to be sold:

“We reopened two Wildwood restaurants which were closed during the pandemic, and we are now trading from 52 restaurants out of a total estate of 54.

We have started a process to sell the two restaurants that remain closed, and we will also consider the sale or surrender of other underperforming sites.“

- A positive snippet concerned TAST’s dim t dim-sum chain (6 sites). A restaurant conversion has “exceeded expectations” and further rebrandings are being considered:

“We also converted Wildwood Loughton into a dim t in November 2022 with results which have exceeded expectations. Dim t has proved to be a robust brand over the last few years due to both a rise in popularity for Asian food and also an increased demand for takeaway and delivery of this cuisine. Given the initial solid performance of this converted unit we are currently considering other opportunities to rebrand within our estate.”

- TAST’s dim t format has for years operated as a sideshow to Wildwood, but the smaller chain could be TAST’s path to recovery if this now “robust brand” can be rolled out further.

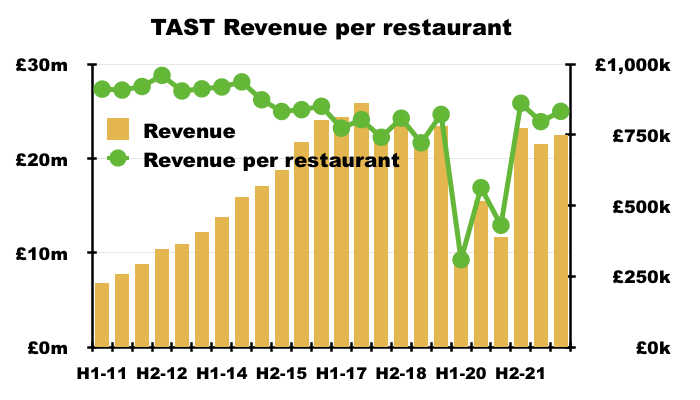

- Based on all 54 locations, revenue per restaurant for this FY was £815k and was the best FY achievement since FY 2016 (£841k):

- Based on all 54 locations, H2 revenue per restaurant was £834k and perhaps would have matched the £862k enjoyed during the comparable H2 2021 were it not for that aforementioned trio of Christmas-trade impediments.

- Revenue per restaurant for this FY was arguably £839k based upon the 51 sites that on average traded throughout the twelve months.

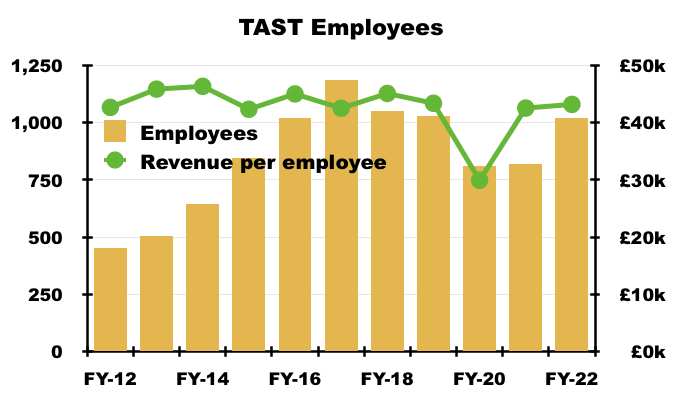

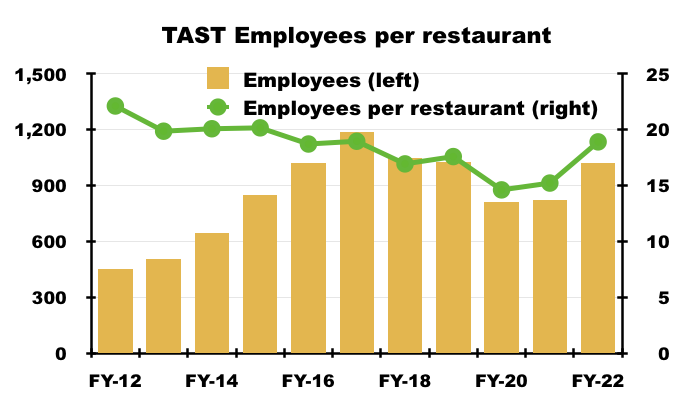

- The average number of employees during the year surpassed 1,000 after dropping towards 800 during pandemic-blighted FYs 2020 and FY 2021:

- Revenue per employee was £43k for this FY and remains within the £42k-£46k range witnessed before the pandemic.

- The preceding H1 included several references to recruitment problems, but this FY indicated such issues may have eased:

“We are pleased to report that as at 25 December 2022, we employed just under 1,100 people across the business, an increase of 100 from the previous year and a sign that the labour shortage seems to have stabilised. However, competition is still considerable for good-quality candidates, and we remain committed to ensuring the Group is a competitive, attractive and supportive environment in which to work. “

- The easing of recruitment issues seems reflected by the number of employees per restaurant, which at approximately 19 for this FY is the highest since FY 2017 (19):

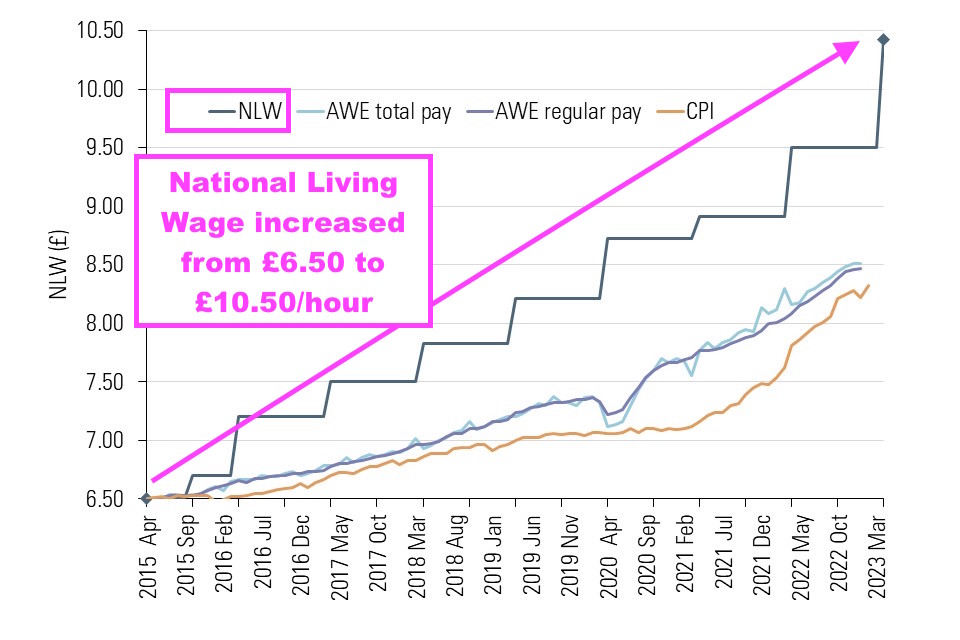

- TAST warned of higher staff costs for the year ahead after the National Living Wage was increased during April:

“Whilst we welcome the removal of the temporary increase of National Insurance of 1.25% introduced in November 2022, the increases in April 2023 of the National Living Wage and general inflationary wage pressures will inevitably result in higher labour costs, which will be impossible to absorb completely. We continue to be committed to improving labour efficiency through a focus on the trading day-parts, forecasting and scheduling.“

- The National Living Wage has advanced 62% from £6.50 to £10.50 an hour following its introduction during April 2015:

- Rising wages without commensurate advances to staff productivity (i.e. TAST’s standstill revenue per employee) will further squeeze TAST’s margin.

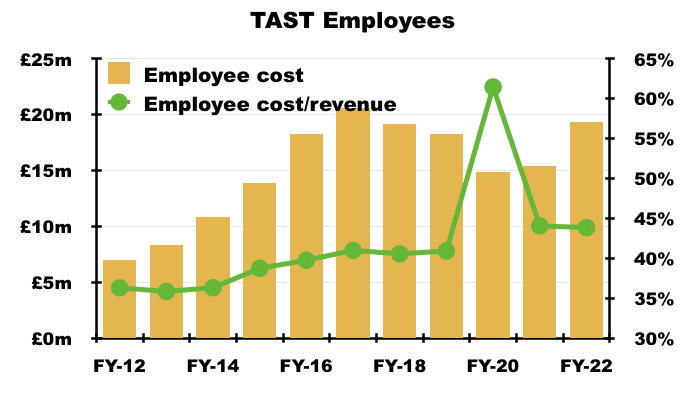

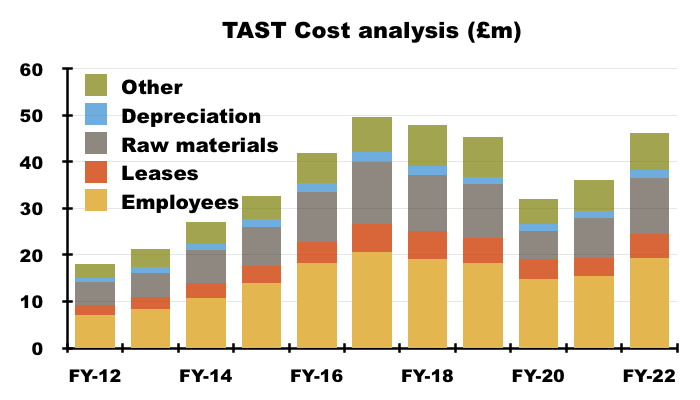

- Indeed, each TAST employee cost an average £18.9k during this FY, while total employee costs as a proportion of revenue has increased from 36% to 44% between FYs 2014 and 2022:

- That 8 percentage-point increase to the proportion of revenue absorbed by employee costs helps explain why TAST’s profitability has become minimal (see Financials: cost analysis).

Financials: going concern, cash and deferred payments

- TAST’s ‘going concern’ text continues to improve following the “existence of a material uncertainty” warning used within the FY 2020 statement.

- This FY’s ‘going concern’ text now focuses on the “cost-of-living crisis” rather than the pandemic:

“The pandemic led to high uncertainty and disruption in the economy and hospitality industry; the energy and cost-of-living crisis followed this. Throughout this period costs were controlled carefully, and cash outflows reduced. Over the last 12 months we have seen inflationary increases directly due to utility increases and shortages caused by the war in Ukraine. These increases appear to have stabilised.

The Group monitors cash balances and prepares regular forecasts, which are reviewed by the Board. These forecasts include our best estimates and judgements based on currently available information and current environment. Judgement is particularly required as to the impact on trade of cost-of-living crisis and inflation.

Given the ability of the Group to manage costs, cash position and the availability of the unutilised overdraft the Directors believe that it remains appropriate to prepare the financial statements on a going concern basis.“

- The preceding H1 2022 had confirmed

- Cash was £8.0m;

- Deferred payments to creditors (e.g. HMRC and landlords) were £1.0m, and;

- Debt was zero after a £1.3m loan was cleared during the period.

- Cash ended this FY at £7.0m, implying H2 witnessed a cash outflow of £1m.

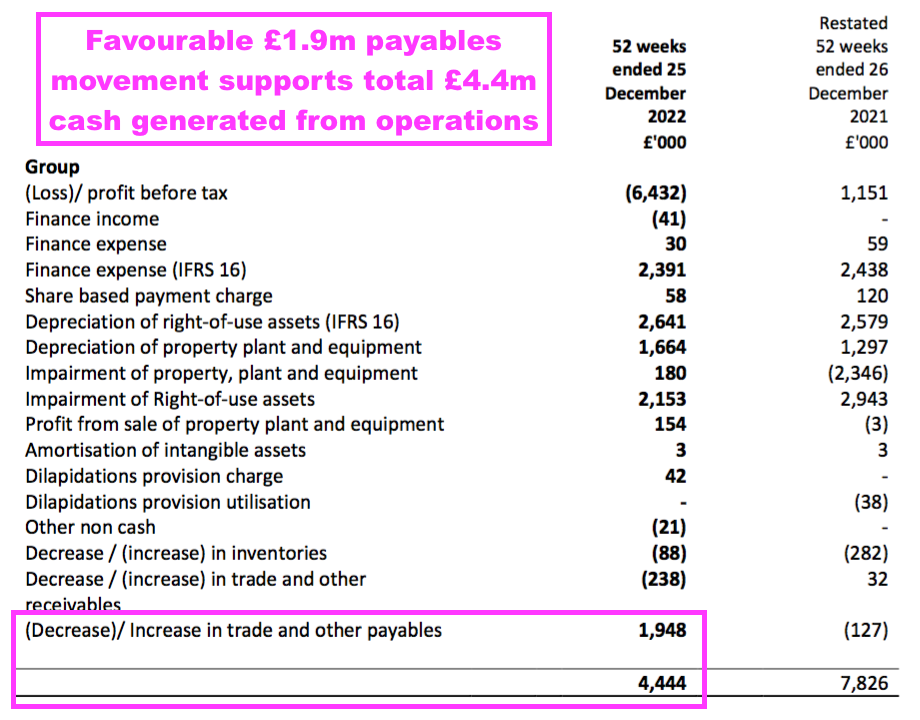

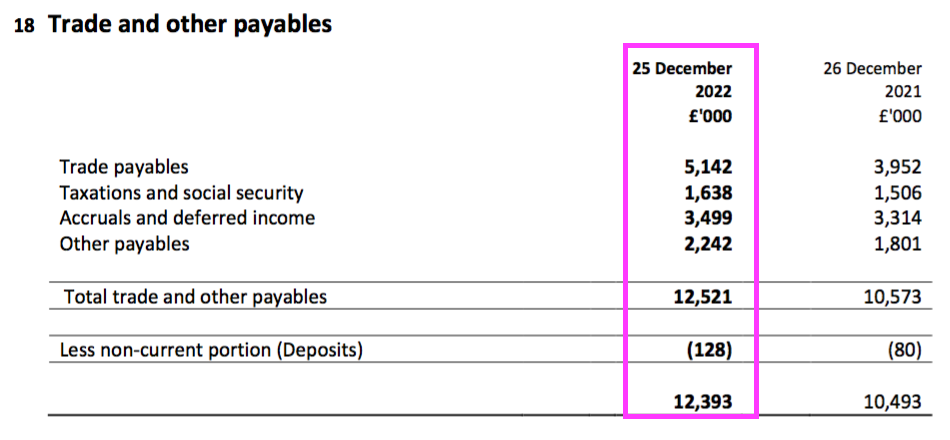

- A favourable increase to trade and other payables…

- …ensured cash flow for this FY and H2 in particular was a lot better than the reported loss.

- The increase to trade and other payables underlines how TAST’s £7m net cash is not truly ‘surplus’ cash.

- The cash position is in fact entirely a by-product of owing money to suppliers and other parties, with £12.4m outstanding at the year end:

- TAST had mentioned ‘deferred payments to creditors’ within its previous results, but no such mention was made within this FY (such deferred payments relate to tax and rent that were postponed during the pandemic).

- I therefore assume TAST has now made good the £1m of deferred payments outstanding at the preceding H1.

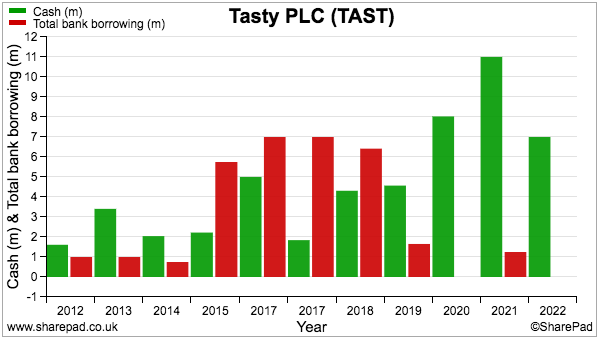

- Net cash at the end of FY 2019 was £2.9m and, amazingly enough, three years of sub-standard results have since witnessed TAST’s net cash improve to £7.0m:

- I should add the bulk of that three-year cash improvement occurred at the start of FY 2020 through a lucrative property sale.

- Still, TAST appears to have navigated the pandemic (and its aftermath) with the help and patience of its suppliers and creditors…

- …but I doubt those suppliers and creditors will always be so accommodating given the ongoing tricky economy.

- The over-riding worry is TAST continues to incur losses, and suppliers and creditors then worry about payment and demand tighter terms…

- …and the cash position is then depleted towards zero.

Financials: landlords and leases

- The preceding H1 indicated rent reductions negotiated during the pandemic were for a temporary period only….

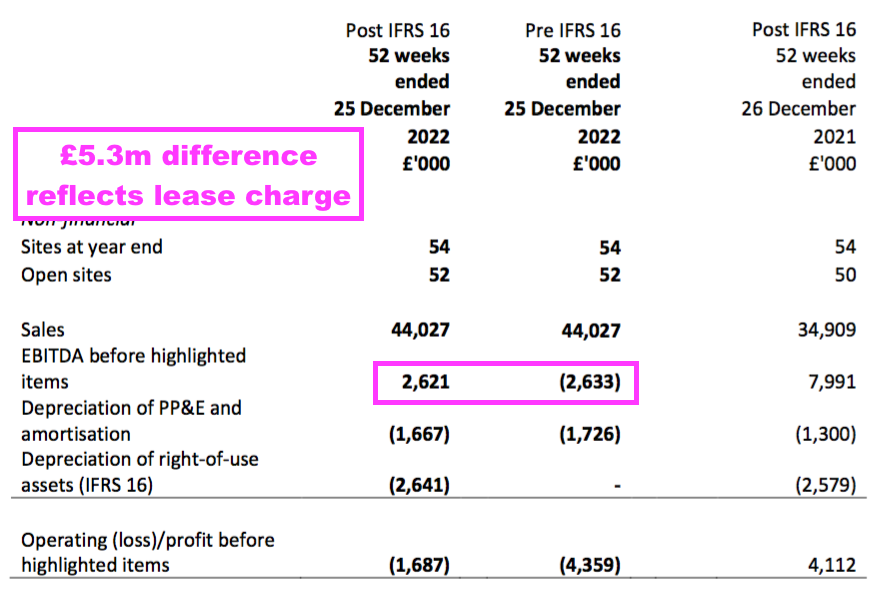

- …and sadly this FY confirmed annual lease costs had returned to pre-pandemic levels:

- The £5.2m difference between the FY 2022 Ebitda numbers represents the pre-IFRS 16 lease cost that, post-IFRS 16, is now reflected within the depreciation expense and financing charge.

- The £5.2m lease charge for this FY is comparable to the pre-pandemic, pre-IFRS 16 lease cost of £5.5m for FY 2019:

- I am disappointed TAST could only reduce its annual lease payment by £0.3m per annum following two years of landlord negotiations.

- Paying £5.2m for 54 restaurants equates to £97k per outlet, which matches the rent cost per outlet for FYs 2014 to 2019.

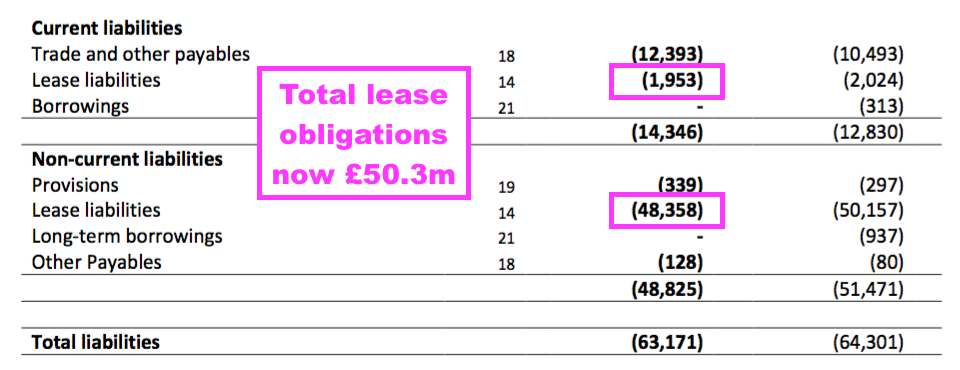

- At least TAST’s total lease obligation has reduced slightly.

- TAST first reported its IFRS 16 total lease obligation to be £56m (on a net present value basis) during H1 2020.

- This FY showed the IFRS 16 total lease obligation (on a net present value basis) declining by £2m from the preceding H1 2022 to £50m:

- The £2m reduction to the total lease obligation may reflect a rent negotiation:

“The Group has successfully re-geared one lease and will continue to review current lease terms and also consider disposing of poorer performing sites. There are a few leases with termination provisions effective this year, which will allow us to either renegotiate terms or surrender the lease.“

- I am hopeful further lease renegotiations (or lease surrenders) can reduce TAST’s total lease obligations further.

- TAST’s right-of-use lease asset ended this FY at £33m, which arguably suggests the group would now pay £18m (i.e. total lease obligations of £50m minus £33m) less to rent its properties were it to commence the same leases today.

Financials: cost analysis

- Evaluating TAST’s costs might help determine whether the business can ever enjoy worthwhile levels of profit following the pandemic…

- …or whether the loss incurred during this FY (and particularly H2) actually means the business has become broken.

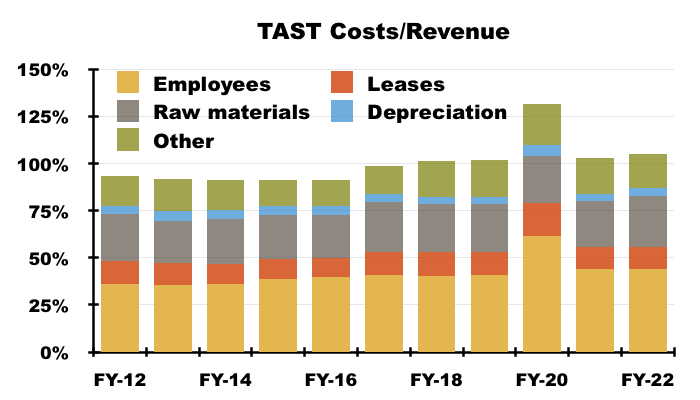

- Let’s not forget that what TAST described as “challenging” trading conditions before the pandemic had already led to minimal profits during FYs 2017, 2018 and 2019 as total costs reached 100% (or more) of revenue:

- TAST kept lease costs under control before the pandemic at between 10% and 12% of revenue. Lease costs were an estimated 12% of revenue during this FY.

- Raw materials (e.g. ingredients) were also kept reasonably steady at between 23% and 27% of revenue before the pandemic. They were 25% of revenue during FY 2021 and increased to 27% of revenue during this FY.

- As noted earlier, employee costs increased from 36% to 44% of revenue between FY 2012 to FY 2022 (see Revenue per restaurant and employee).

- Other costs rising from 16% to 19% of revenue between FY 2012 and FY 2019 was another contributor to the pre-pandemic margin collapse. Other costs absorbed 18% of revenue during this FY:

- Other costs include utility expenses, for which this FY admitted would remain “at least double that of historical costs” and had prompted “selective Monday closures“:

“In 2022, our energy costs rose substantially in line with many in the hospitality industry and often resulted in four times more cost than the 2019 equivalent. When the current energy cap reduces at the end of March 2023 with advice from our newly appointed energy brokers, we are adopting a revised hedging strategy to reduce our energy costs. While we hope that pressures on energy costs have peaked, we expect prices toremain higher than pre-pandemic levels and estimate this to be at least double that of historical costs. We are working on unit level energy efficiency improvements and selective Monday closures to reduce costs.”

- TAST consumed 6% more energy during this FY:

“The Group’s total energy consumption for the 52-week period ended 25 December 2022 was 13,638,208 kWh (2021:12,872,041 kWh) the increase reflecting a greater number of our sites trading in 2022, with no Covid-19 related restrictions.“

- Using 6% more energy when revenue gained 26% shows TAST’s energy-saving efforts to be working.

- TAST’s own energy-intensity ratio — emissions per m2 of floor area — declined by 6%:

“An energy intensity ratio of 0.134 (2021: 0.142) has been measured using the metric of tonnes CO2e per m2 floor area (“tCO2e”).”

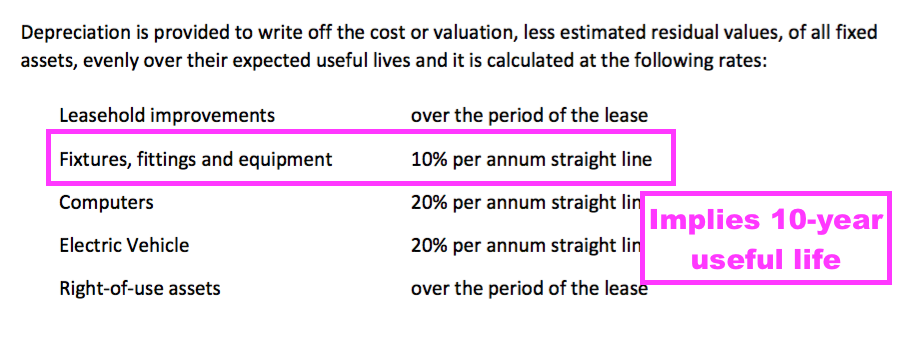

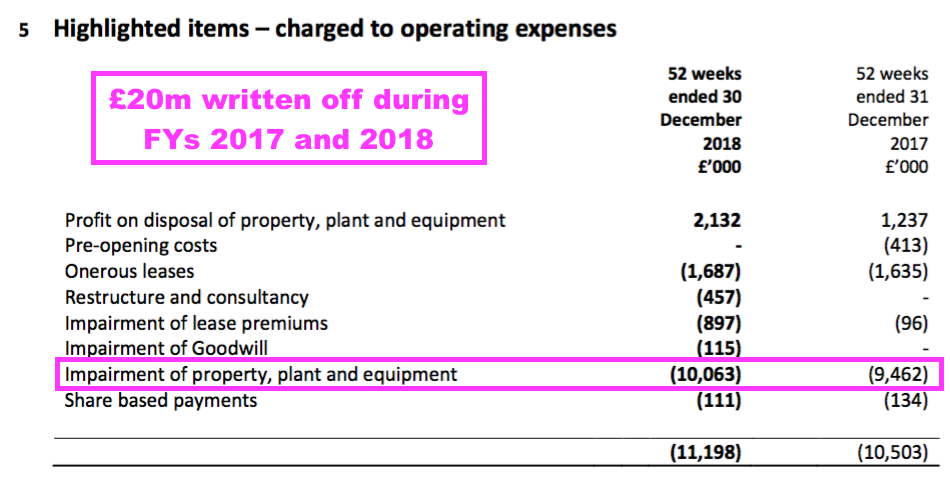

- TAST’s depreciation has bobbed around the 4-5% level of revenue for years and was 4% during FY 2022.

- But TAST’s depreciation policy does seem relatively generous with an effective ten-year useful life for fixtures, fittings and equipment:

- True, TAST’s depreciation policy has not been too relevant of late as the group curtailed capex and instead raised money by selling leases.

- But do remember TAST’s operating troubles during FYs 2017 and 2018 led to write-offs of £20m before the pandemic:

- Those write-offs may not have been so hefty had a more conservative depreciation policy been applied. The hefty write-offs also suggest earnings prior to FY 2017 were flattered somewhat.

- All told, these FY figures sadly do not suggest a radical (and favourable) change to TAST’s cost structure will emerge any time soon.

Comparison with Restaurant Group and Fulham Shore

- Further analysis of TAST’s costs can be garnered through comparisons with quoted sector operators Restaurant Group (RTN), owner of Frankie & Benny’s and Wagamama, and Fulham Shore (FUL), owner of Franco Manca and The Real Greek.

- The table below confirms TAST spends far more on employees and raw materials relative to RTN and FUL:

| TAST | RTN | FUL | |

| Year to | 25 Dec 2022 | 01 Jan 2023 | 27 Mar 2022 |

| Revenue (£k) | 44,027 | 883,000 | 82,702 |

| Employee costs (£k) | 19,240 | 334,400 | 29,625 |

| Inventory costs (£k) | 12,000 | 184,500 | 14,690 |

| Employee costs/Revenue | 44% | 38% | 36% |

| Inventory costs/Revenue | 27% | 21% | 18% |

- A kind interpretation of that table is TAST underprices its menu…

- …and TAST did claim within this FY:

“We have avoided aggressive discounting and promotions, maintaining a competitive advantage through pricing and a value proposition.”

- Mind you, I can’t help but feel TAST simply pays too much for staff and ingredients.

- TAST seems very energy inefficient versus RTN and FUL, too.

- The latest annual accounts for RTN and FUL show both generating revenue of more than £5 for every kWh consumed, while TAST produces only revenue of £3.24 (£44m/13.6 gWh):

| TAST | RTN | FUL | |

| Year to | 25 Dec 2022 | 01 Jan 2023 | 27 Mar 2022 |

| Revenue (£k) | 44,027 | 883,000 | 82,702 |

| Energy consumed (gWh) | 13.638 | 174.095 | 14.770 |

| Revenue/kWh (£) | 3.23 | 5.07 | 5.60 |

- I had thought TAST’s unprofitability was due mostly to high employment costs, which unlike rents and ingredient expenses, are dictated by government regulation (i.e. the National Living Wage) and not market forces.

- But following the comparisons with RTN and FUL, TAST’s unprofitability appears due to an inherently flawed menu that requires costly ingredients, too many employees and too many other expenses to implement.

- Without TAST somehow improving revenue and/or reducing costs, through:

- Re-focusing the menu towards more profitable dishes;

- Improving employee/restaurant efficiency, and/or;

- Employing a completely different model to traditional dine-in (e.g. delivery/takeaway)…

- …I fear the economics of TAST’s business will remain very poor.

Revised menu, expansion plans and board change

- The pandemic could have been the opportunity for a radical menu overhaul to perhaps revitalise TAST’s progress.

- Returning TAST to profit post-Covid-19 requires some radical management thinking.

- The business lost money during the two years before the pandemic, so going back to the same menu with the same discounts with the same way of working at the same locations does not seem viable.

- The pandemic has instead brought an opportunity to reshape the group entirely.

- Possible ways to lower costs and/or increase staff productivity include:

- Go takeaway/delivery only;

- Adopt a very simple menu and self-service dining (see Toby Carvery);

- Implement a CVA to jettison all the problem sites, or;

- Become a franchisor and let others run the restaurants.

- A radical menu overhaul has sadly not occurred.

- TAST’s primary Wildwood format unfortunately remains based on a broad mix of pizzas, pastas and burgers…

- … that did not attract hordes of diners during the “challenging” (pre-pandemic) FYs of 2017, 2018 and 2019…

- …and still appears to be struggling given this FY’s £2m trading loss.

- Hope now rests on a new Head of Food devising a winning (and profitable) menu:

“We are constantly reviewing our menu and increasing the choice of options, including lunch and light options. With our newly appointed Head of Food and our central kitchen production we have significantly improved our food quality and consistency which is borne out by customer survey reports. With approximately three menu changes a year, we can adapt products to suit availability and changing tastes and we always review ways to offer vegan and gluten-free options.”

- TAST added:

“To ensure we are accessible to a broader consumer group, we have maintained a very low entry price point for both pizza and pasta for Wildwood and noodles for dim t – dishes which continue to be very popular with our customers.“

- The following 15 dishes featured on the Wildwood menu during August 2022 and remain on the latest version:

- Starters

- Mixed olives: still £3.95

- Garlic tiger prawns: were £8.35, now £8.95

- Mushroom aracini: was £6.75, now £7.15

- Grill

- Classic cheeseburger: was £12.95, now £14.50

- Philly cheesesteak sandwich: was £14.95, now £15.95

- Full rack of ribs: was £18.95, now £19.45

- Pizza

- Margherita: still £7.95

- Vegetable primavera: was £13.95, now £15.25

- Grilled courgette & goat’s cheese: was £12.25, now £13.25

- Pasta

- Classic spaghetti pomodoro: still £7.95

- Traditional Bolognese: was £11.75, now £13.95

- Oven-baked chicken and mushroom penne: was £12.95, now £14.50

- Other

- Chicken & asparagus risotto: was £12.95, now £13.95

- Caesar salad: was £11.45, now £11.85

- Fries: still £4.35

- TAST has indeed kept a “very low entry price point for both pizza and pasta” (£7.95), but has lifted prices throughout the rest of the menu. The average price change of those 15 dishes is 6.4%, with the Traditional Bolognese costing 19% more.

- I calculate revenue would need to rise 4.4% just to cover a possible 10% increase to total staff costs following the new £10.50 per hour National Living Wage.

- Let’s just hope diners remain happy to pay the higher menu prices.

- Let’s also hope TAST’s new Head of Food considers ingredient costs and production efficiency as well as culinary matters when devising future menus.

- This menu from 2016 shows a classic cheeseburger priced at £11.65, which the latest menu carries at £14.50 — up 24%.

- Rising menu prices versus stagnant revenue per employee imply employees have been serving fewer diners over time, which in turn suggests…

- …the greater sales per restaurant during FY 2022 were supported mostly by rising menu prices and not extra diners.

- This FY confirmed earlier plans to open 5-6 new sites had been scrapped:

“The Group’s expansion plan of opening additional sites will be reviewed once inflation and the economy have stabilised.”

- TAST did hint that expansion may one day be considered:

“Unfortunately, we expect some businesses will struggle to survive with their current estate, and there will be many opportunities to acquire good sites.”

- I would argue TAST has struggled with its own estate following this FY’s £2m trading loss, and really ought to be solving its own problems before talking of “opportunities to acquire good sites“.

- A very disappointing development from this FY concerned executive director Harald Samúelsson.

- Mr Samúelsson’s appointment as an executive last year was particularly welcome due to his long and seemingly successful industry career:

“Harald Samúelsson has over 20 years of experience in the UK restaurant industry. From 2000 to 2008, Harald helped grow Strada Restaurants from 4 to 54 restaurants in the UK in a senior operations position. In 2008, Harald joined Côte Restaurants as joint Managing Director, growing the group from 2 to 72 restaurants. In 2013, Harald co-led a management buy-out of Côte with CBPE Private Equity for £100m and in 2015 co-led a sale of Côte to BC Partners for £245m. During his Côte tenure, Harald was also joint Managing Director at Bill’s restaurants from 2010 to 2012. In 2016, Harald joined Honest Burgers as a Senior Advisor and set up a property development company in Spain with projects in the Valencia, Madrid and Barcelona areas.”

- This FY admitted Mr Samúelsson has now reverted to his earlier non-exec position:

“In addition, Harald Samúelsson, who joined the Board in May 2021, is permanently relocating to Spain from 1 April 2023 and will revert to his previous position as an independent non-executive Director. Harald Samúelsson has over 20 years of experience in the UK restaurant industry.”

- The obvious worry is Mr Samúelsson has not liked what he has seen during his year as a TAST executive, and has decided life would be much easier working on his property interests in Spain.

Valuation and cessation of blog coverage

- TAST gave encouraging remarks about early FY 2023 trading:

“The sales performance for the start of 2023 has been better than initially expected, but it is still challenging.”

“We are conscious that demand may be favourable due to the savings built up over the pandemic and the real impact of the cost-of-living crisis may still materialise, however year-to-date performance in 2023 has been slightly better than expected. “

- A return to pre-pandemic work patterns may have helped:

“We previously reported that the pandemic negatively impacted our city centre sites due to fewer commuters, tourists and theatregoers. The London sites are now performing better with the return of tourists and the theatre shows, and there has also been an uplift in lunch trade as people slowly increase the frequency that they attend the office.“

- TAST suggested both sales and costs will be higher during FY 2023 than this FY:

“Performance to date is ahead of management expectations, although at this stage, it is difficult to predict the full extent of the cost of living crisis and input cost inflation and shortages given the level of uncertainty that still exists in the industry and economy in general…”

“We are living in very unpredictable times, both politically and economically, and these no doubt will continue to be factors in the performance of the Group for the coming year.”

- Revenue of £44m during this FY does not require a huge operating margin to leave a profit that would make the £5m market cap a remarkable bargain.

- A margin of 4% on £44m for example leads to a £1.8m operating profit and a possible P/E of less than 4.

- But can TAST return to a sustainable level of profit?

- A mix of:

- Higher staff/ingredient/energy expenses;

- Lease costs returning to almost pre-pandemic levels, and;

- A decision to maintain “a competitive advantage through pricing and a value proposition”…

- …does not suggest the economics of TAST’s business will improve in the near future…

- …and I dare say the Wildwood format in particular looks broken.

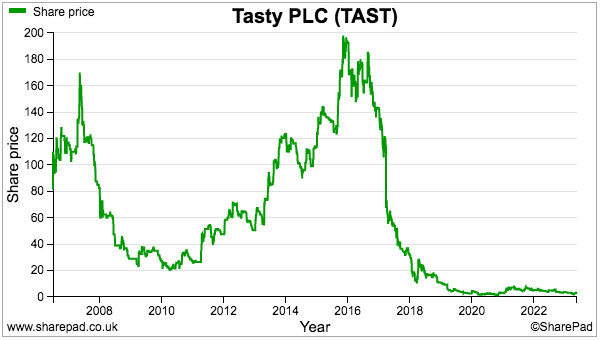

- I have held TAST shares throughout the group’s last five years of difficulties with the hope the price could one day multi-bag should sales advance and margins recover.

- However, I believe this FY statement — and particularly the poor H2 — has underlined why a radical overhaul was needed during the pandemic…

- …and I should not be too surprised by this FY loss.

- After all, I did write within my FY 2021 review:

“The obvious worry is the H2 2021 performance was exceptional and a host of macro-economic problems will soon dampen sales and lift costs to then restrict TAST to minimal profits at best. “

- Although I have toyed with exiting TAST, I continue to hold because the shares:

- Are very illiquid and difficult to sell in bulk;

- Represent less than 1% of my portfolio, and;

- May actually multi-bag if I my doubts prove unfounded.

- But I have decided to cease formal blog coverage of TAST as I no longer want to spend time evaluating what now looks to be a lost business cause.

- My original TAST buy report cited the family management’s then 48%/£30m shareholding as one of the three reasons I invested in TAST…

- …but that same management shareholding could in fact prompt the end of my TAST investment.

- The directors, former directors and various close associates currently form a 40% concert party and today’s rough sector conditions for TAST (and rough market conditions for AIM nanocaps in general) could mean a de-listing is forced upon outside shareholders.

- Many of the same individuals involved with TAST voted for Richoux to cancel its AIM quote during 2019…

- …and that small restaurant chain eventually went bust during 2021.

Maynard Paton

Hi Maynard,

Appreciate the level headed analysis as always, pity this one didn’t work out. We all have our duds in investing, but the way you face them head on, not slinking away from them, is incredibly admirable. Btw, have you looked at MacFarlane plc? They’re a UK packaging distributor, with a long history of profitable growth. Might be worth a look as it fits your slow and steady approach? One of their larger holders (an investment trust) is reducing its position, putting a lid on the share price in the meantime.

Thanks Peter. Yes, TAST has not worked out, but I have learnt a lot about cost analysis from the experience that I hope will help me avoid future losers. Never looked at MACF, but will remember the name if the share ever crops up on a SharePad filter for a SharePad article.

Maynard

Tasty (TAST)

Portfolio trade

Just to confirm I have sold my entire TAST position for about 2p per share in recent weeks. Reasons should be clear from the blog post above. An opportunity to exit arose when liquidity suddenly improved and I had already accepted the consequences of the ‘what if it now multi-bags’ dilemma. Including the proceeds from earlier sold shares, my total TAST investment finished with an 85% loss.

Maynard