18 May 2018

By Maynard Paton

Update on Andrews Sykes (ASY).

Event: Preliminary results for the twelve months to 31 December 2017 published 18 May 2018

Summary: These results were quite satisfactory, although sadly the record figures I had hoped for did not entirely come through. Indeed, after a bumper first half, I note the second half could only match last year’s H2. Nevertheless, I was pleased the specialist hire group did not have to rely on “significant extremes in climatic conditions” to stimulate extra demand for its air conditioners, heaters and pumps. Meanwhile, margins remain high at 24%, net cash has grown to a hefty £20m and a 14x cash-adjusted P/E does not seem that excessive. I continue to hold.

Price: 520p

Shares in issue: 42,262,082

Market capitalisation: £220m

Click here to read all my ASY posts

Results:

My thoughts:

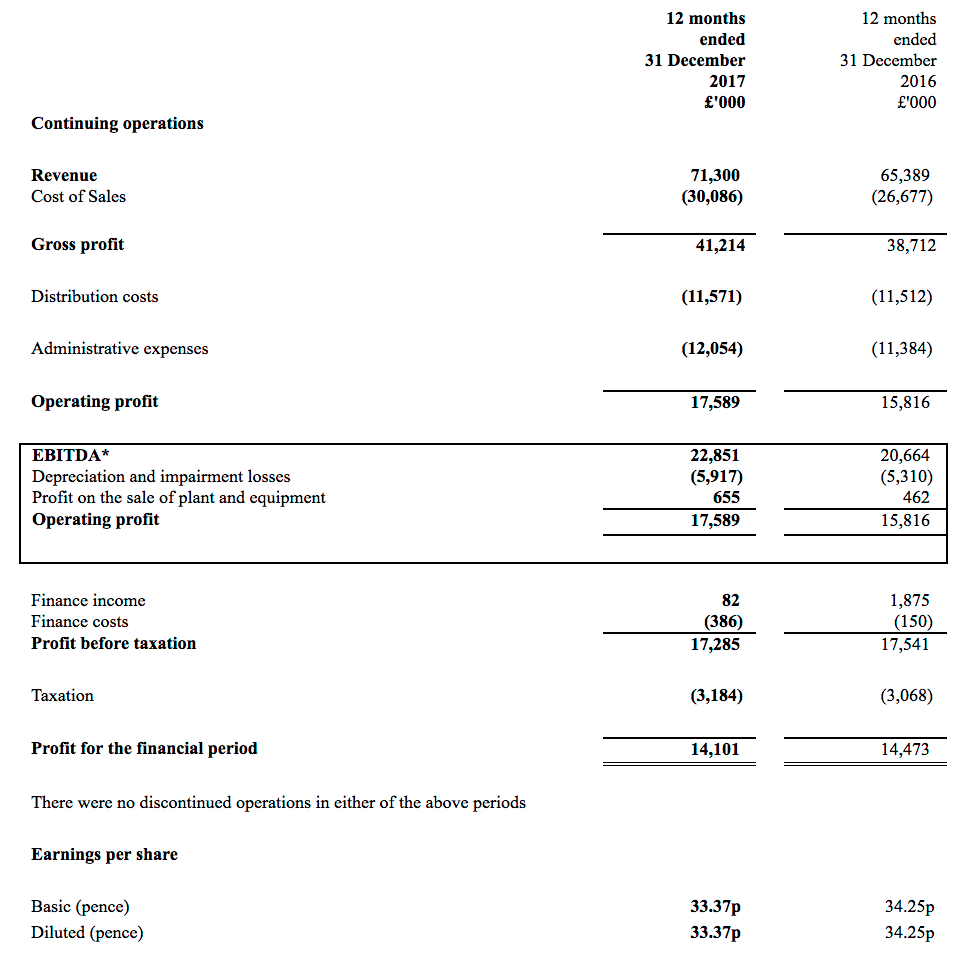

* Another year of “robust operational management” delivers fresh revenue high

Following September’s bumper interims, I had hoped ASY was on course to deliver record results for 2017.

Sadly this announcement revealed only one all-time accounting high — revenue gained 9% to set a fresh £71.3m peak. Operating profit advanced 11% to £17.6m — just £0.3m shy of the level set during 2008.

I was pleased that, once again, ASY cited “robust operational management” as the basis for the underlying financial improvement.

Demand for ASY’s equipment increases during prolonged periods of hot, cold and wet weather, and 2017 apparently was another year that lacked “significant extremes in climatic conditions”.

“Strong and improved” progress was reported within ASY’s main UK division as well as its various European operations. A “strong and stable” effort was delivered by the Middle Eastern subsidiary.

This table summarises ASY’s progress during the last five years:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Revenue (£k) | 61,072 | 56,400 | 60,058 | 65,389 | 71,300 |

| Operating profit (£k) | 14,683 | 11,311 | 13,208 | 15,816 | 17,589 |

| Finance income (£k) | 87 | (72) | 159 | 1,725 | (304) |

| Other items (£k) | 194 | 517 | - | - | - |

| Pre-tax profit (£k) | 14,964 | 11,756 | 13,367 | 17,541 | 17,285 |

| Earnings per share (p) | 27.3 | 22.0 | 25.6 | 34.3 | 33.4 |

| Dividend per share (p) | 29.7 | 23.8 | 23.8 | 23.8 | 23.8 |

The first-half/second-half split confirmed the 2017 advances were confined to H1:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 30,287 | 35,102 | 65,389 | 35,334 | 35,966 | 71,300 | |

| Operating profit (£k) | 6,395 | 9,421 | 15,816 | 8,171 | 9,418 | 17,589 |

ASY admitted that the significant improvements witnessed during the first half — H1 revenue gained 17% while H1 profit gained 28% — could not be “maintained indefinitely”.

I should add that H2 2016 was a record second-half for profit, and H2 2017 very nearly matched it.

For what it is worth, the board signed off the annual statement by stating it was “cautiously optimistic for further success” — a phrase used within the previous five full-year results.

* High margin, net funds… and a pension surplus that continues to absorb cash

These preliminary results did not reveal anything too worrying within the accounts.

In particular, my operating margin and return on average equity calculations continue to show attractive figures:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating margin (%) | 24.0 | 20.1 | 22.0 | 24.2 | 24.7 |

| Return on average equity (%) | 27.2 | 21.7 | 25.2 | 31.5 | 27.8 |

Furthermore, cash generation appeared sound, with capital expenditure once again covered by the depreciation charged against earnings:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit (£k) | 14,683 | 11,311 | 13,208 | 15,816 | 17,589 |

| Depreciation and amortisation (£k) | 4,459 | 4,563 | 4,959 | 5,310 | 5,917 |

| Net capital expenditure (£k) | (3,686) | (3,216) | (4,523) | (4,719) | (4,929) |

| Working-capital movement (£k) | (82) | (1,569) | (3,090) | (2,157) | (801)* |

| Net cash (£k) | 19,133 | 16,846 | 14,558 | 17,673 | 20,293 |

(*estimated)

These preliminary accounts were not complete though, and I have had to estimate the working-capital movement for 2017 from the figures made available.

I note ASY said it paid nearly £1m into the group’s defined-benefit pension scheme during the year. This sum is deemed to be a ‘deficit recovery’ payment and, due to complicated accounting quirks, is not charged to headline earnings.

(Bear in mind that, during the last five years, ASY’s balance sheet has consistently shown a pension-fund surplus — and yet the firm has still had to inject £3m into the scheme during the same time.

It just goes to show how final-salary pension schemes can just keep on absorbing extra cash — even when these schemes show more assets than liabilities!)

Anyway, I will have to study ASY’s full annual report later this month to double-check the group’s exact working-capital movements and pension-scheme situation.

Free cash flow for the year came to a useful £13m, of which £10m was spent on dividends and £3m was added to the bank. Net cash now stands at £20.3m or 48p per share.

The cash generation supported the declaration of the now usual 11.9p per share/£5m final dividend, which gave a 23.8p per share payout for the fourth consecutive year.

Valuation

ASY’s operating profit presently runs at £17.6m and translates into earnings of £14.4m, or 34.1p per share, using the 18% tax charge applied in these results.

Subtract the £20.3m net cash position from the £220m market cap (at 520p) and the enterprise value comes to £200m or 472p per share. Then divide that 472p by my 34.1p per share earnings guess and I arrive at an underlying P/E of approximately 14.

I must admit, a 14x multiple does not look too racy in today’s market for what is a high-margin, cash-rich business that has just lifted its annual operating profit by 11%.

If you adjust ASY’s reported profit to include the aforementioned £1m ‘deficit recovery’ pension contribution, then the multiple approaches 15.

Meanwhile, the trailing yield is a useful 4.6%, and my 34.1p per share earnings calculation covers the 23.8p per share payout 1.4 times.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in Andrews Sykes.

Thanks for the ever-helpful note. I was somewhat surprised by the market reaction given the underlying profit growth and the nice cash balance. oh well – given the wide spread I would still want a small bit more movement to add more but its a happy hold for me as is.

Thanks James. It does not take many trades to move this share price around. I am happy to hold, too.

Maynard

Andrews Sykes (ASY)

Publication of 2017 annual report

ASY’s annual reports do include a fair bit of management narrative that is not produced in the original results RNS. However, for 2017 the additional text did not contain any great revelations from what I could see. But there were a few snippets of interest.

1) Extra narrative

The extra management narrative did outline a little bit more as to what happened during the year:

I believe the Swiss operation is the only division losing money at present.

2) Strategic risks

Brexit now makes its first appearance among ASY’s ‘strategic risks’:

3) Future development

‘Significant new developments’ are on the horizon:

4) Revenue split

This note confirms European revenue gained 21% and now represents 21% (19%) of total revenue:

5) Business segments

It was pleasing once again to see ASY’s main division continuing to earn robust margins:

A profit of £15,237k from revenue of £54,918k gives a 27.7% margin before central costs. The Middle Eastern division enjoyed a 24.4% margin.

6) Cash flow

ASY does have the niggling habit of producing only part of the cash flow statement within its results RNS. Here is the missing section:

I did not clock the £164k trade-investment write-off within the original results RNS (the balance sheet showed it had disappeared). The cash flow statement shows a £770k excess pension contribution and an aggregate £1,155k working-capital movement (versus my original £801k guess). Still, the £1,155k is the lowest amount of cash absorbed by working capital since 2013.

7) Key audit matters

Having read a few 2017 annual reports now, I am now sure the rules for Audit reporting and disclosure have been expanded. ASY’s report includes this neat audit-risk chart:

8) Director pay

Crikey — ASY’s managing director took home an extra £134k of emoluments during the year:

A 36% pay rise for an 11% operating-profit improvement — and a standstill dividend — does seem extravagant to me. The bonus element (if there is one) is not separated from the overall emolument figure, so perhaps there was a one-off performance payment involved. That said, Mr Wood’s total emoluments have doubled since 2010, which is not great when operating profit at the wider business bobbed between £12m and £15m for most of that time.

At least the c90%-owner/chairman continues to waive his fee, and there are still no director options.

Once again I thought I would include the chairman’s annual-report bio here. He must be the oldest director serving at a quoted company:

9) Employees

Some promising numbers here:

The average cost per employee fell by £234 to £34,934 and meant total staff costs represented 26.7% of revenue — the lowest percentage since 2013. Revenue per employee increased by £6k to £131k — ASY’s highest level ever bar 2008 (£136k).

10) Pension scheme

The annual-report small print revealed ASY will reduce its pension contributions to £120k for 2018 versus £920k for 2017:

I am pleased about that reduction. During five of the previous six year, ASY has pumped extra contributions of £700k-plus into the scheme.

This note summaries the scheme’s asset movements:

The scheme’s assets of £45,657k are required to pay annual member benefits of £1,687k, which is equivalent of a 3.7% required return. For 2018, the aforementioned £120k contribution will probably be offset by the scheme’s admin expenses.

I evaluated various schemes within this Comment, and 3.7% is a little on the high side. I get the impression ASY may have to increase its scheme contributions for 2019.

11) Trade receivables

Good news here.

Last year, overdue trade debtors had surpassed current trade debtors for the first time since ASY started disclosing the relevant figures in 2006. However, 2017 has seen a marked improvement:

For 2017, overdue trade debtors represented 47.9% of all trade debtors, in line with the percentages for 2013, 2014 and 2015.

Furthermore, total trade debtors as a percentage of revenue, at 21.5% (£15,331k / £70,300k) for 2017, has been bettered only once during the last decade (2008, 21.5%).

Clearly then some work has been done improving the collection of outstanding monies. I hear customers in the Middle East tend to be tardy payers.

12) Trade investment

On the face of it, this £164k write-off does not look like a big deal:

However, between 2007 and 2014, this investment delivered total income to ASY of £2.9m. Some time ago I had thought this £164k trade investment could be worth a lot more than £164k, but clearly that is not the case.

No income has been received from the investment for three years now and, after I attended the AGM two years ago, I gathered this investment had become quite problematic.

Maynard