11 December 2015

By Maynard Paton

Quick update on Electronic Data Processing (EDP).

Event: Preliminary results published 11 December

Summary: As expected, this dull software microcap reported no miracles. Cost savings should underpin the firm’s near-term progress, but revenue growth remains as elusive as ever. At least EDP still enjoys plenty of recurring income and has committed again to a hefty 5p per share dividend. I’m trusting the trio of North American funds that hold 28% of this stock will one day stir-up some corporate action so we can all exit at an advantageous price. I continue to hold.

Price: 63p

Shares in issue: 12,610,976

Market capitalisation: £7.9m

Click here for my previous EDP posts

Results:

My thoughts:

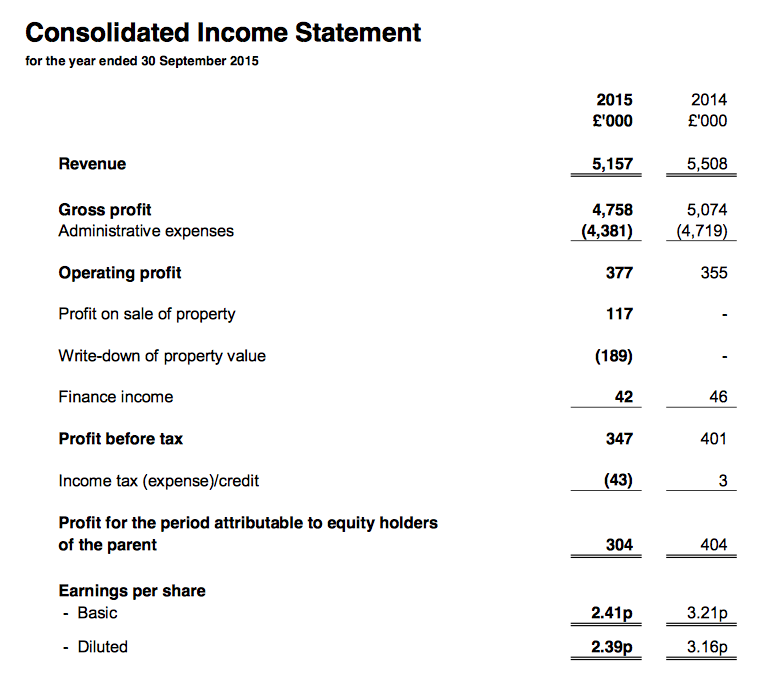

* Revenue at its lowest since 1985!

Following EDP’s underwhelming interim figures, I was not expecting miracles with these annual results.

In the event, the loss of a £300k contract at the start of the financial year ensured revenue fell 6%. The group’s top line is now 25% below that recorded in 2008 — and is at its lowest level since 1985.

However, various cost-saving measures did help reported operating profit gain £22k on 2014:

| H1 2014 | H2 2014 | FY 2014 | H1 2015 | H2 2015 | FY 2015 | ||

| Revenue (£k) | 2,662 | 2,846 | 5,508 | 2,519 | 2,638 | 5,157 | |

| Operating profit (£k) | 136 | 219 | 355 | 159 | 218 | 377 |

It’s worth noting EDP’s costs included a ‘one-off’ £76k restructuring charge during 2015, of which £56k was expensed during H1 and £20k during H2. Adjust for that expenditure and the H1/H2 profit split was £215k/£238k.

The strong point of EDP’s business remains its recurring income. Annual software licences and hosting fees stayed high at 79% of revenue (or £4,074k), although such income decreased by 7% on 2014. The firm continues to claim its turnover is moving towards “stronger ongoing subscription revenues”.

* Further small cost savings to be made

EDP had previously flagged the prospect of annual cost savings of £200k, and these results suggested such savings had now been achieved.

Looking ahead, the group reckons the long-awaited sale of a surplus property in Milton Keynes ought to save another £35k annually. In addition, a recent office move ought to yield a further £25k a year.

That prospective £60k total saving is material when the reported operating profit in these results was £377k.

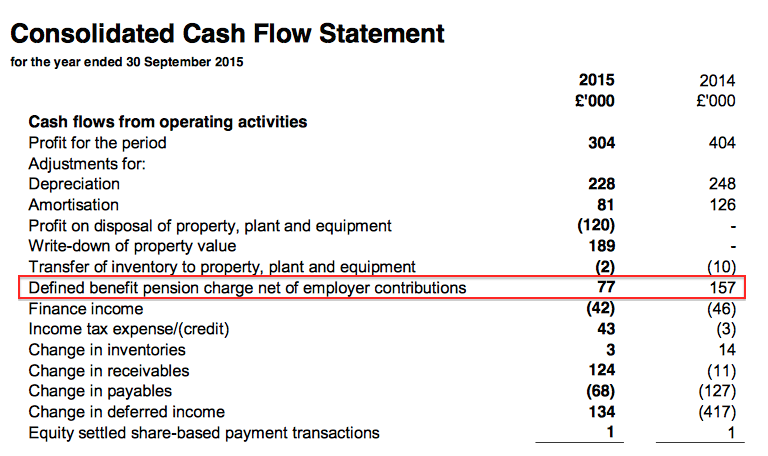

* Profit understated due to pension accounting?

I wonder if EDP’s reported profit is understated due to the nuances of pension-scheme accounting.

Here is today’s narrative on the pension scheme (my bold):

“In sharp contrast with the IAS19 valuation, the most recent triennial actuarial valuation of the scheme, which was performed at 31 July 2013, showed a small surplus on an ongoing funding basis.”

“Importantly, as a result of the scheme being fully funded on this basis, the Group is not currently required to make cash contributions into the scheme.”

“The defined benefit pension scheme comprises a grouped funding arrangement whose sole asset is a with-profits insurance policy backed by corporate bonds. The main difference between the IAS19 valuation and the ongoing funding valuation is that IAS19 requires the scheme asset to be valued at the insurance policy’s discontinuance surrender value at the period end. This valuation does not take into account the guaranteed annuity rates which have been secured by the policy and which are included in the ongoing scheme funding valuation.”

To cut a long bookkeeping story short, EDP’s pension is in reality fully funded. However, the accounting rules dictate the scheme has to show a £2,265k deficit due to the exclusion of the fund’s annuity investment.

Anyway, EDP has no need to make cash contributions to the scheme (and naturally does not make any), yet reported profit is lowered by the pension accounting.

The accounts show £77k — a significant sum — was charged against profit in relation to the scheme for 2015, although there was no associated cash cost:

* Balance sheet remains flush with cash and property

I’m pleased EDP has made some (slow) progress with its surplus properties.

For a start, today’s results showed a £425k sale and £117k profit following the disposal of a building in Sheffield.

Meanwhile, the aforementioned site in Milton Keynes looks likely to be sold for £1,181k — albeit £189k lower than its previous book value.

Cash flow during the year once again looked useful, with my calculation of surplus net cash coming in at £3,482k.

Throw in the Milton Keynes site as well and I arrive at surplus net cash and property of £4,663k or 37p per share.

* Slight upgrade to the outlook?

Given EDP’s declining revenue, I might be clutching at straws with the following.

But the group’s chief exec does sound a little more optimistic than this time last year.

Back in 2014, the boss said (my bold):

“We have a strong product and services offering, a robust business model and considerable financial strength which will enable us to meet the challenges we will face in the forthcoming year. Having strengthened our sales team we expect to be well positioned to take advantage of those new business opportunities which do arise.”

Twelve months on, he now seems a fraction more confident of EDP enjoying “opportunities” (my bold):

“We have positioned the business to address the challenges we expect to face by strengthening our product R&D and sales teams over the last two years. Our new product offerings have already been well received by customers and should provide us with good opportunities over the coming year.“

This may be another straw-clutch perhaps, but I also see EDP’s deferred income increased slightly on last year.

The gain was only £134k to £2,065k, but it was the first advance to deferred income since 2008. Deferred income broadly represents up-front customer payments, and uplifts here could signal uplifts to future revenue.

Given EDP’s awful long-term sales record, I will take any glimmer of a turnaround!

* One reason I still hold this share is because it looks cheap

The obvious valuation measure remains the dividend.

EDP reconfirmed its ambition of paying 5p per share for 2016, which supports a 7.9% income at 63p.

Sadly these results have prompted me to downgrade my future operating profit guess. I was previously looking at £592k, but in hindsight I may have over-egged the £200k-plus of savings the business had been anticipating.

Now I am going for today’s reported £377k operating profit plus the £76k restructure cost plus the £60k of future property savings. All that gives me a total of £513k.

Applying a standard 20% tax rate would in turn produce earnings of 3.25p per share — not enough to cover the promised 5p dividend.

Nevertheless, strip out the 37p per share of surplus cash and property from the 63p share price, and EDP’s enterprise value (EV) comes to 26p per share. The P/E on my EV and earnings calculations is therefore 26p/3.25p = 8.

I must add that EDP’s tax charge for 2015 was 12% due to R&D tax credits. As such, ongoing earnings could be higher and the underlying P/E might be closer to 7.

* The other reason I still hold this share is because of this trio of investors

I mentioned in my February write-up that EDP’s shareholder register contains three North American value funds.

At the last count, the trio controlled 28% of EDP and I am convinced the end-game these funds have in mind is some sort of corporate deal.

The largest of the three funds bought in at 55p during 2013 and I’d like to think its managers expect further upside from today’s 63p.

* Next events — ex-div 3 March 2016, 3p dividend paid 6 April 2016, interim results late May 2016.

Maynard Paton

Disclosure: Maynard owns shares in Electronic Data Processing.

Hey Maynard,

I’ve been watching these guys for a while. Interesting company, and the yield makes it investable IMO – without it it’d just be another strange listed cash-pile with a small business attached!

I always find it a little depressing that they say they are expensing £1m of R&D annually. This investment indicates either that their R&D is being woefully misallocated or, more likely, there is quite a lot of running you need to do to stand still with their software products. It’s just not at that sweet scale yet.

This thing has to be worth meaningfully more private than public. They’re even LSE listed. I would’ve thought the assorted public company/audit/regulatory/corporate governance costs aren’t too far off their entire reported net profit figures. I think the only really compelling IRRs you’ll see occur if they manage to significantly turn the operating business around and get it growing, though.

A curious one.

Lewis

Hello Lewis

Thanks for the comment.

Yes, these and past results talk a lot on R&D, product investment, awards etc, the impact of which on revenue has been zilch really. I do wonder if the firm is living off inert customers — a friend of mine works for a firm that has paid for EDP software for 20 years. I guess the aggro/cost factor involved in changing suppliers has kept that firm loyal. It is harder for EDP to find new customers.

Good point on the listing costs and long term, I agree, revenue needs to advance to drive any sort of re-rating.

Maynard

Hi gents. I’ve been writing EDP up for Monday. I’m confused by the R&D, its 20% of revenue (which seems huge in comparison to other companies I follow). There’s only one other thing that’s huge about EDP and that’s the dividend. What makes me uneasy are the two are completely at odds. If it carries on paying out more than it earns it will slowly liquidate itself. So why the heavy investment?!

Hi Richard

In the 2014 annual report, R&D expenditure is described as “principally the continued enhancement of Quantum VS and Vecta” — which to me is bog-standard normal product development for a software firm. So it does seem as if EDP is being a tad cavalier by referring to such expense as R&D — it is hardly the cutting-edge R&D you’d associated at a biotech firm for example. That said, EDP has received R&D tax credits, so clearly some of the spending has met the HMRC guidelines.

I do not think it was a great coincidence that the arrival of Boyles on the shareholder register in 2013 was followed a few weeks later by the announcement of special 5p dividend. I am convinced Boyles has engaged with management behind the scenes to sustain this enhanced payment, and EDP’s cash and sole remaining surplus property can continue to fund the higher dividend for a few more years yet.

Maynard

Electronic Data Processing (EDP)

Publication of 2015 annual report:

http://www.edp.co.uk/investor/EDP_Annual_Report_&_Accounts_2015.pdf

I’ve had a look through and discovered the following points of interest:

1) Confirmation of hosting revenue:

EDP has regularly cited its proportion of hosting revenue within its preliminary results RNS. However, that figure was missing for 2015. But the proportion was published in the annual report — 51%:

We now know hosting revenue fell 8% from £2,864k to £2,630k.

2) Viability statement:

This is something new for 2015:

It confirms EDP enjoys contracts that last for between three and five years.

3) Director pay

I’m pleased to see there’s been very little in way of board pay rises:

However, the directors did walk away with a collective £26k bonus. Bonus levels are judged on adjusted operating profit, which after bonuses fell from £553k to £459k.

So… a bit galling for us shareholders to fund a bonus when profits fell (reported profits gained mostly because of lower pension-scheme costs), but that is what can happen when the bonus pool is based upon a basic percentage of profit. At least the board did not pay itself the full 10% of adjusted profit it can do.

4) Small change to amortisation costs:

This may be something or nothing, but EDP’s capitalised expenditure on R&D is now being amortised over three to seven years:

Previously the amortisation was over five to seven years. The shorter duration indicates the lifespan of the firm’s development spend is no longer as long as it was, which may be due to rising competitive pressures.

5) Employee information:

Despite the 6% overall revenue drop, the staff count reduced by just two:

So revenue per head has dropped for the fourth consecutive year and now stands at £78k.

Also, sales and admin staff remain at 17. The chief exec’s statement refers to “strengthening our new business sales team“, so I wonder if the new additions were replacements for less-effective salespeople.

6) Tax rate:

The chief exec’s statement refers to the 12% effective tax rate for 2015 being due to “relief on qualifying Research and Development expenditure and the fact that no tax was payable on the freehold property sale“.

But the value of the the R&D tax credits and the property tax relief are not clear from the tax note below:

It would be useful for shareholders to have an R&D tax-credit figure to gauge just what underlying post-tax profits could be.

7) ‘Past due’ trade receivables:

It appears EDP serves a lot of late-paying customers:

Some 48% of gross trade receivables were ‘past due’ or impaired last year.

That 48% proportion seems high for a software business that enjoys recurring income from licence fees etc. At least the 48% is lower than the 50%-plus seen during the previous two years and is not way out of line with the years prior to that.

I have not seen anything too untoward within EDP’s working-capital movements over time, so I guess these ‘late payers’ do pay eventually. One positive I have seen is the annual impairment charge from non-payers has dwindled from £181k in 2008 to £54k for 2015, so some progress has been made there.

Maynard

Electronic Data Processing (EDP)

Notification of shareholding:

http://www.investegate.co.uk/elec-data-process—edp-/rns/holding-s–in-company/201602221230067463P/

Not what I was expecting. Boyles Asset Management, which is one of a trio of North American ‘value’ funds that own notifiable holdings in EDP, has admitted to trimming its position.

Boyles’ investment has been reduced from 2,291,000 to 2,253,000 shares, which now represents 17.87% of the wider share count.

Interestingly, the previous holding notification from Boyles occurred in May last year:

http://www.investegate.co.uk/elec-data-process-/edp/holding-s–in-company/201505201037217586N/

Back then, the fund reported it had increased its holding from 2,266,000 to 2,276,000 shares. So following that May notification, Boyles had bought a further 15,000 shares before today’s announcement.

All told, the selling here does not look significant — and presumably there has been a keen buyer as I have been surprised the share price has held up so well throughout this year’s market ructions.

To be fair, I can’t blame Boyles for selling a few EDP to fund purchases in other shares. This fund first declared a notifiable stake in May 2013 and EDP’s underlying business has not really set the world on fire since then. I, too, have wondered about trimming my own holding just in case better opportunities arise elsewhere. I’ve been in the share since Sept 2012 and still hope the ‘value’ will be outed one day!

Maynard

Electronic Data Processing (EDP)

Statement regarding Strategic Review:

http://www.investegate.co.uk/elec-data-process—edp-/rns/statement-re-strategic-review/201604181400025325V/

This is promising news. EDP has put itself up for sale:

“EDP announces today that it has decided to conduct a review of various strategic options open to the Company to maximise value for shareholders, which could include a sale of the Company.

Whilst the Board believes that the Company has a secure future as an independent business, the Board has taken this decision in order to seek to unlock value for shareholders whilst safeguarding the interests of all stakeholders.

The Board has appointed BDO LLP as financial adviser for the purposes of the strategic review.”

It seems to me the three North American value funds on EDP’s shareholder register have had enough and have stirred up some long-awaited corporate action.

At the last count, the trio controlled 28% of EDP and as I wrote in the Blog post above, “I am convinced the end-game these funds have in mind is some sort of corporate deal”.

This Strategic Review puts EDP under City Takeover Rules and all 1%-plus shareholders will have to declare Opening Position Disclosures in the next fortnight. Their subsequent share dealings will have to be disclosed, too. As such, the positions of the trio of North American funds will become quite clear.

I suspect all three funds have a cash-exit takeover in mind. I certainly do.

Maynard

Electronic Data Processing (EDP)

Opening Position Disclosures.

Some OPDs starting to come though now.

Let’s start with the trio of active investors:

1) Olesen Value: 694,696 shares (5.51%)

http://uk.advfn.com/stock-market/london/electronic-data-processing-EDP/share-news/Olesen-Value-Fund-L-P-Form-8-3-Electronic-Data/71255883

I had previously recorded Olesen as owning 661,600 shares (5.25%) from August 2015: http://www.investegate.co.uk/elec-data-process—edp-/rns/holding-s–in-company/201508261044381343X/

2) Ewing Morris: 649,855 shares (5.15%)

http://uk.advfn.com/stock-market/london/electronic-data-processing-EDP/share-news/Ewing-Morris-Co-Investment-Partners-Ltd-Form-8-3/71243899

Ewing Morris has not changed its position since its last holdings RNS of December 2014: http://www.investegate.co.uk/elec-data-process—edp-/rns/holding-s–in-company/201412191509443574A/

3) Boyles Asset Management: 2,253,000 shares (17.87%)

http://uk.advfn.com/stock-market/london/electronic-data-processing-EDP/share-news/Elec-Data-Process-Form-8-3-Electronic-Data-Proc/71269164

Boyles Asset Management has not changed its position since its last holdings RNS in February 2016:

http://www.investegate.co.uk/elec-data-process-/edp/holding-s–in-company/201602221230067463P/

Now to the other OPDs:

First off, Sanderson PLC: 292,500 shares (2.32%)

http://uk.advfn.com/stock-market/london/electronic-data-processing-EDP/share-news/Sanderson-Group-PLC-Form-8-3-Electronic-Data-Pro/71354323

Sanderson’s accounts show the stake was bought during the year to September 2012 for £131k, or 45p per share, and has always been accounted for as a short-term financial asset. So I guess Sanderson does not see the investment as anything strategic. Sanderson is a small-cap software business focusing on SMEs, so there is a little similarity with EDP.

Interestingly, Sanderson’s directors have owned up to holding a further 67,587 shares (0.54%).

Next, some (presumably) individual investors:

Spencer Crooks: 262,500 shares (2.97%)

John Rockliff: 175,000 shares (1.98%)

Julia Micklethwaite: 158,000 shares (1.25%)

Finally, some institutions:

Royal Bank of Scotland: 196,875 shares (2.23%)

Mercantile Investment: 175,000 shares (1.39%)

Maynard (no OPD needed :-( )