***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 July 2026

By Maynard Paton

I am not a great fan of the fund-management industry.

I cannot think of another sector where the employees typically collect enormous salaries while the customers can pay hefty charges yet sometimes get very little in return.

Quite often us amateur investors are much better off with simple index trackers rather than falling for the industry’s persuasive advisers and glossy brochures.

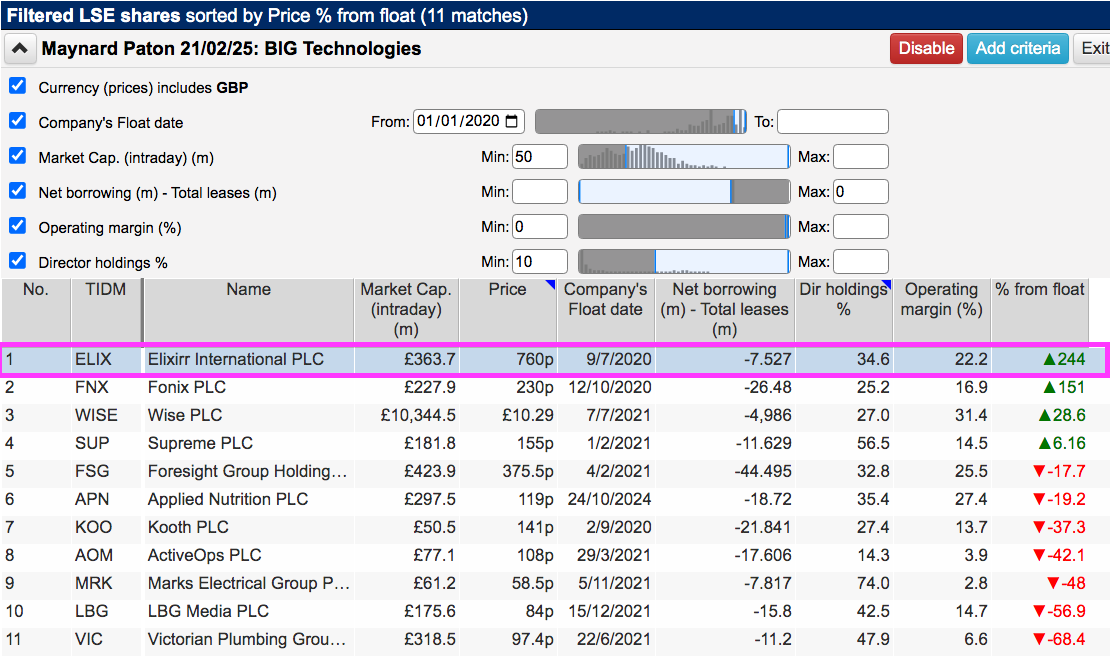

Yet here I am about to study Foresight Group — a fund manager that seems to be defying the wider sector trends of client-money outflows and squeezed management fees.

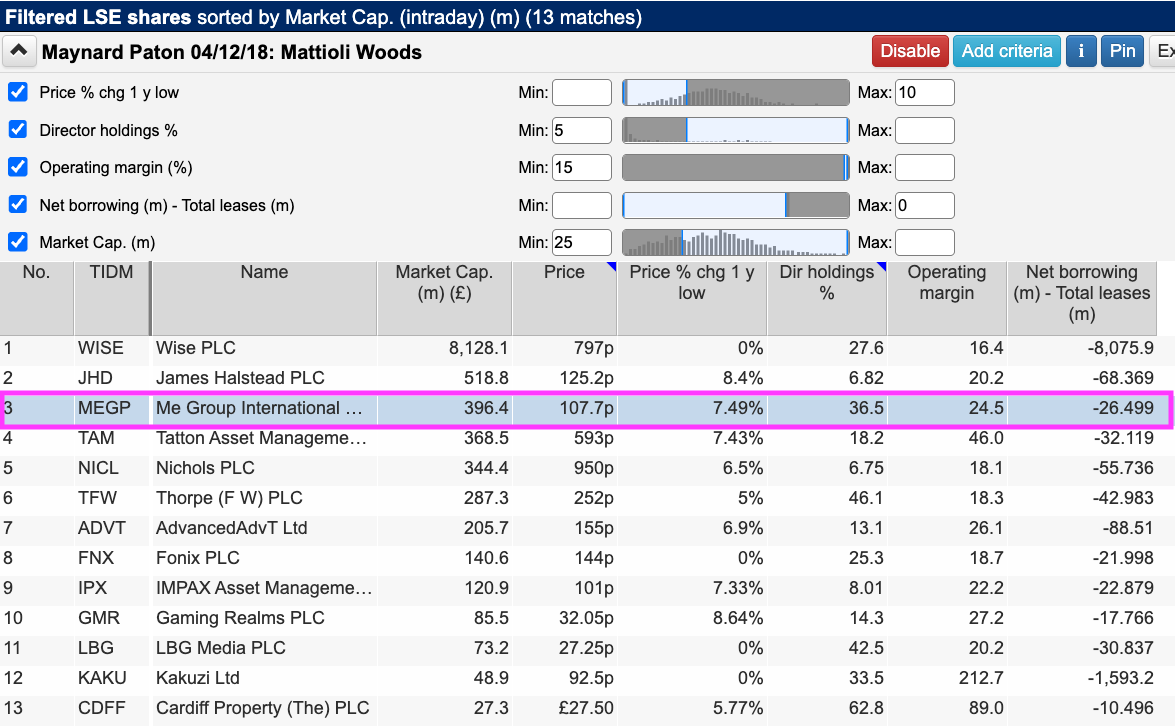

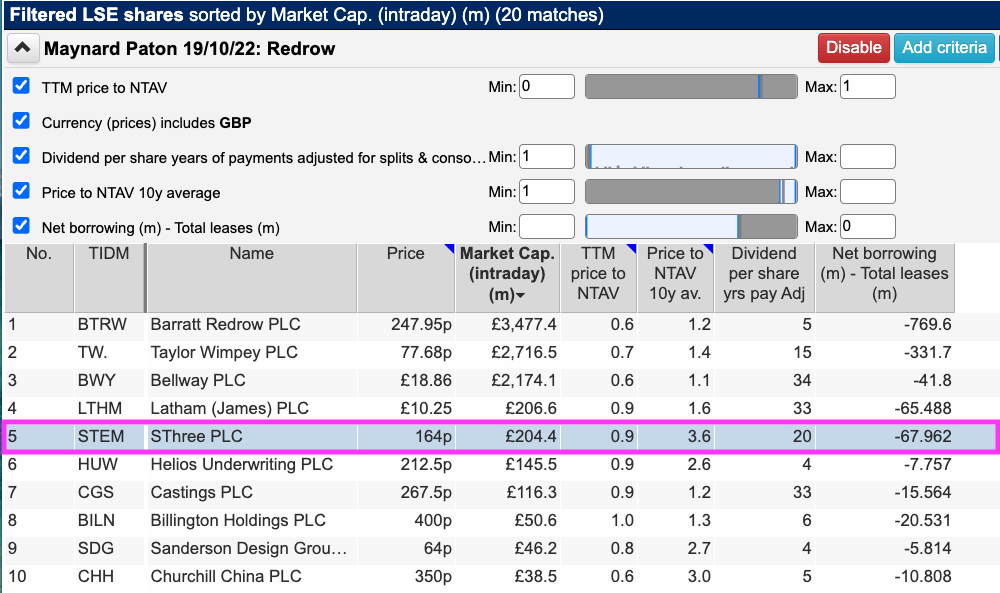

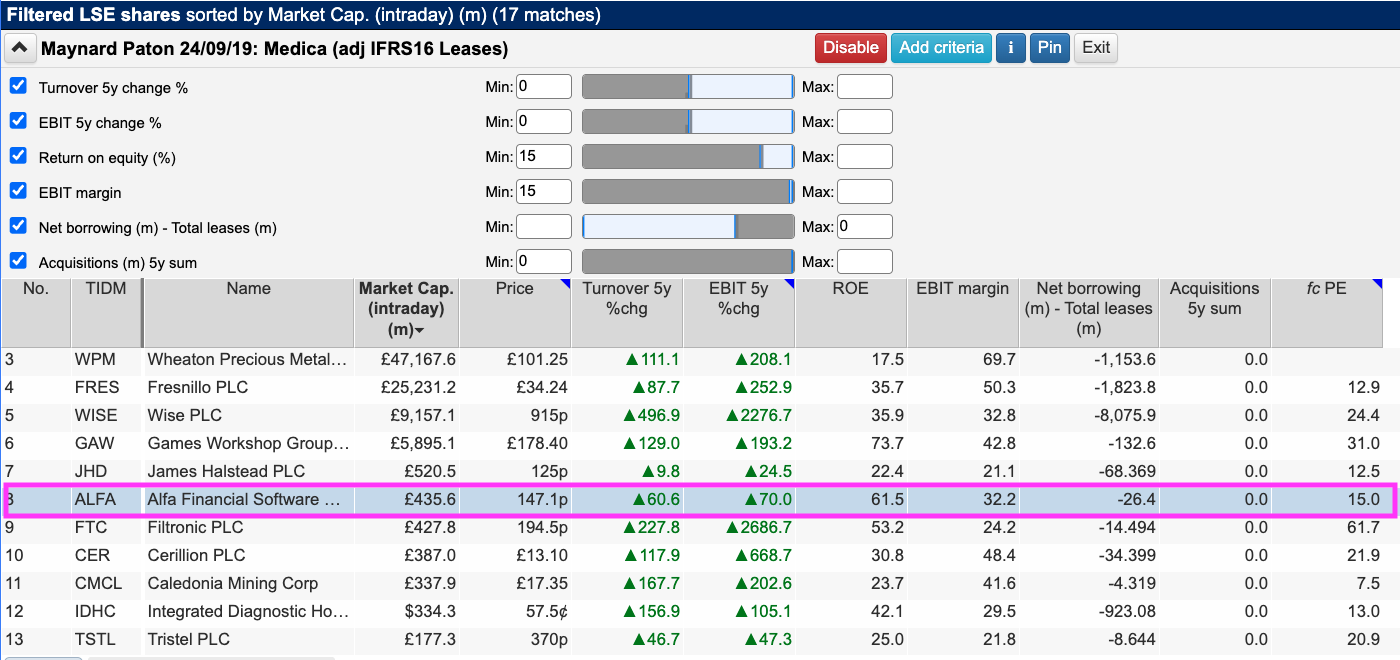

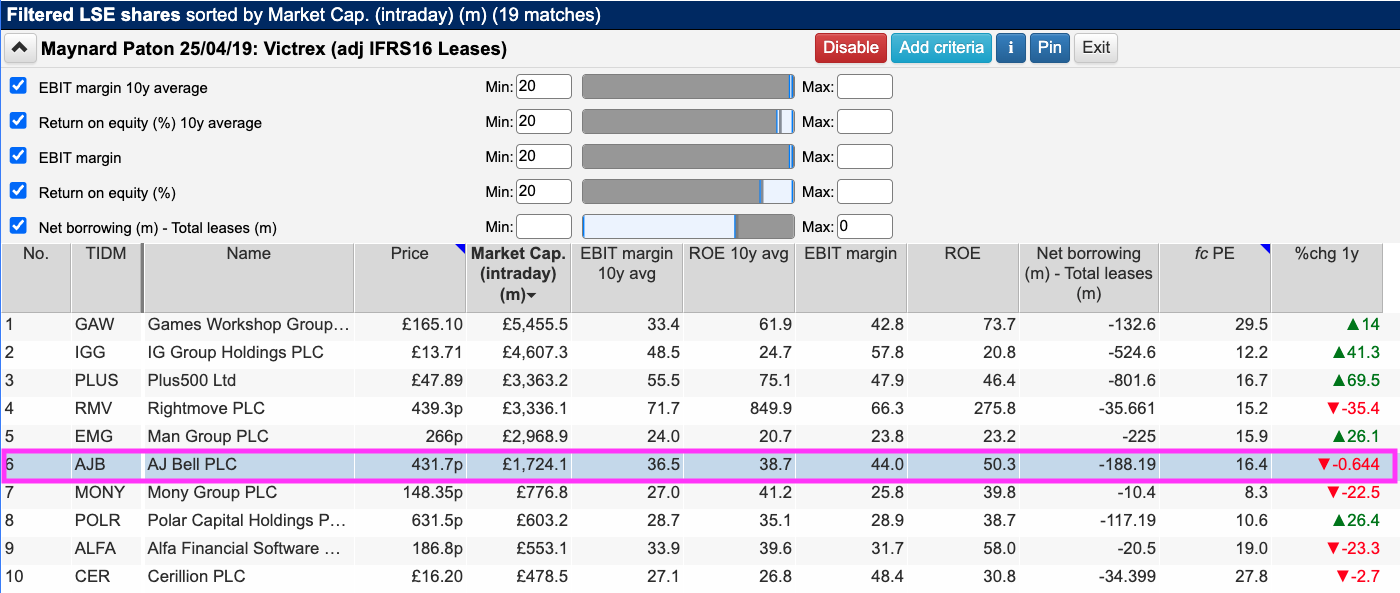

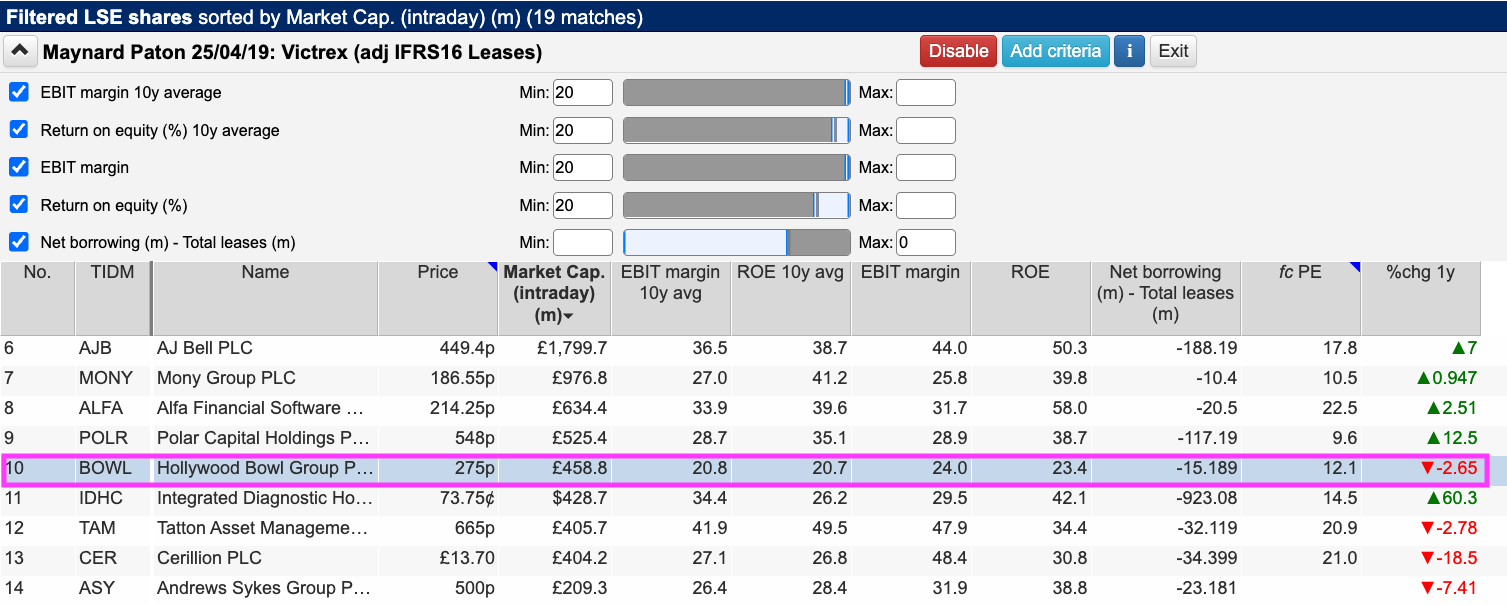

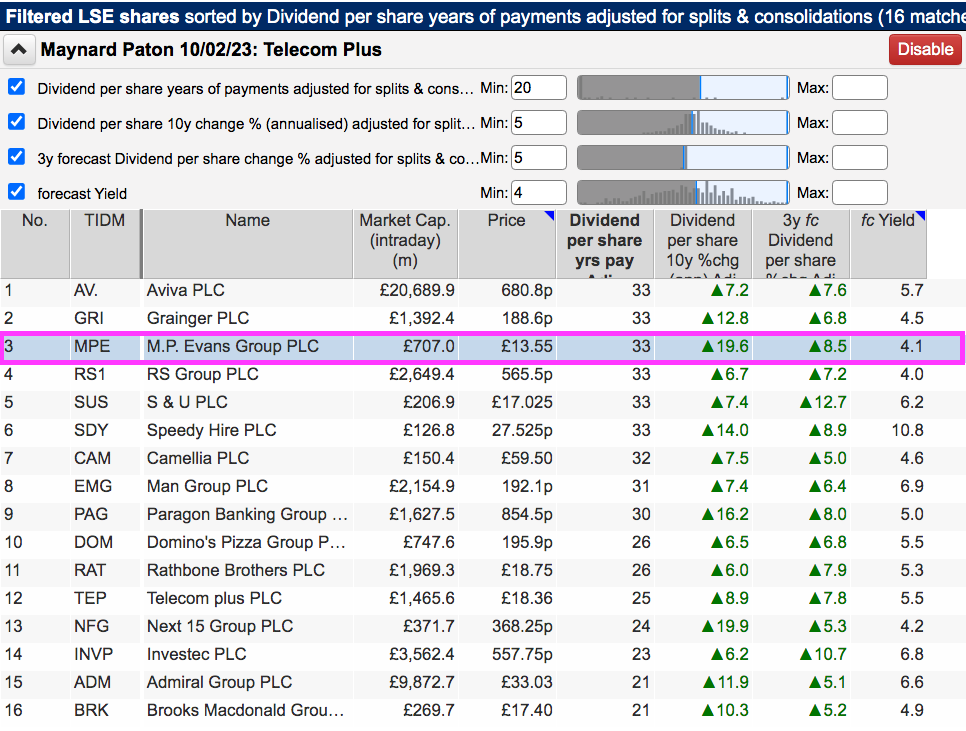

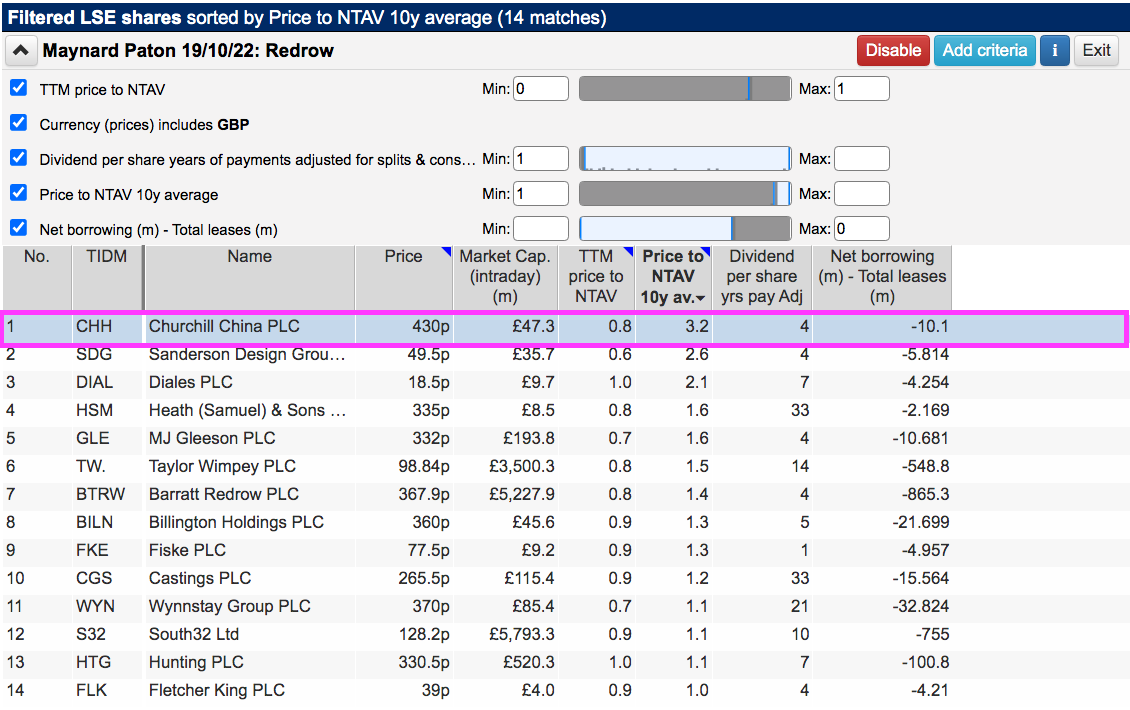

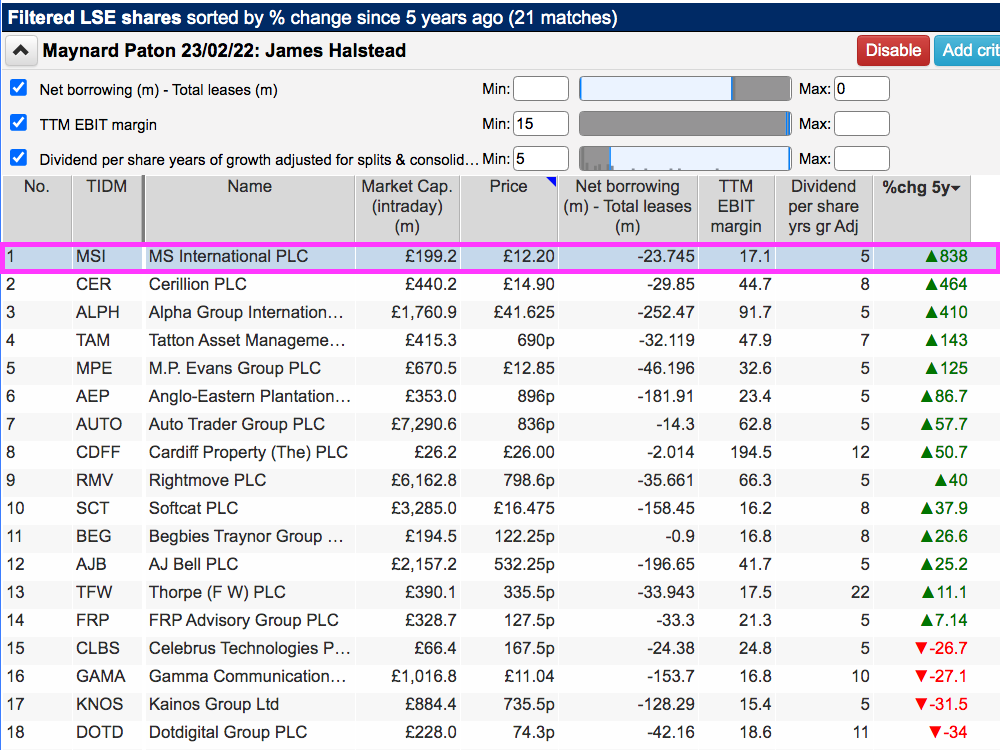

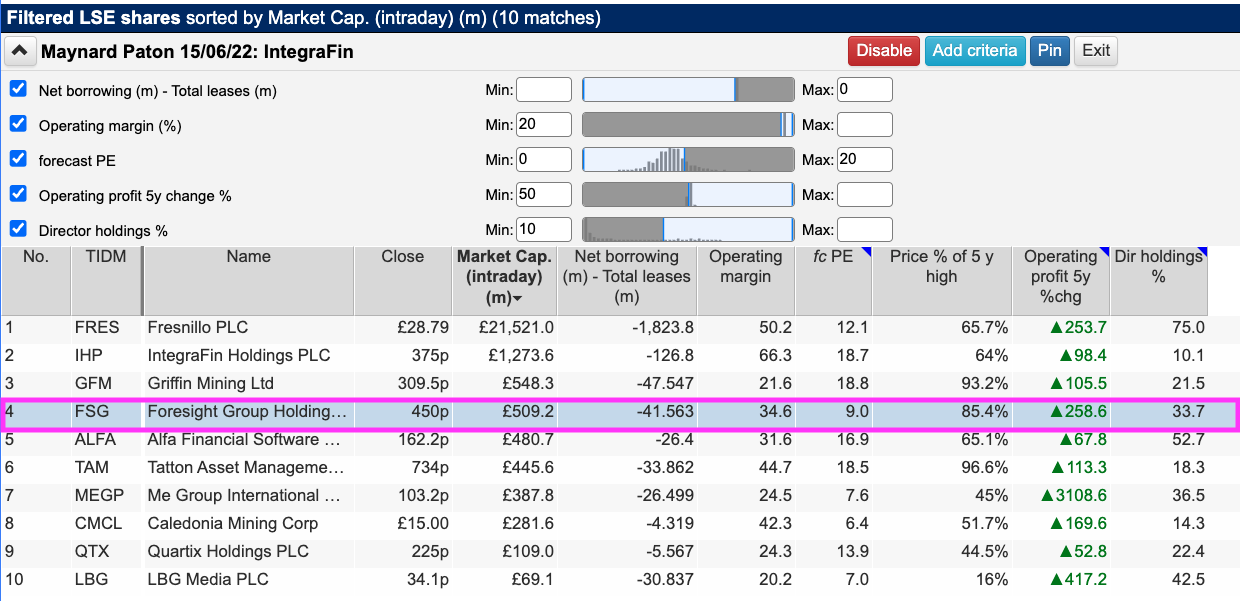

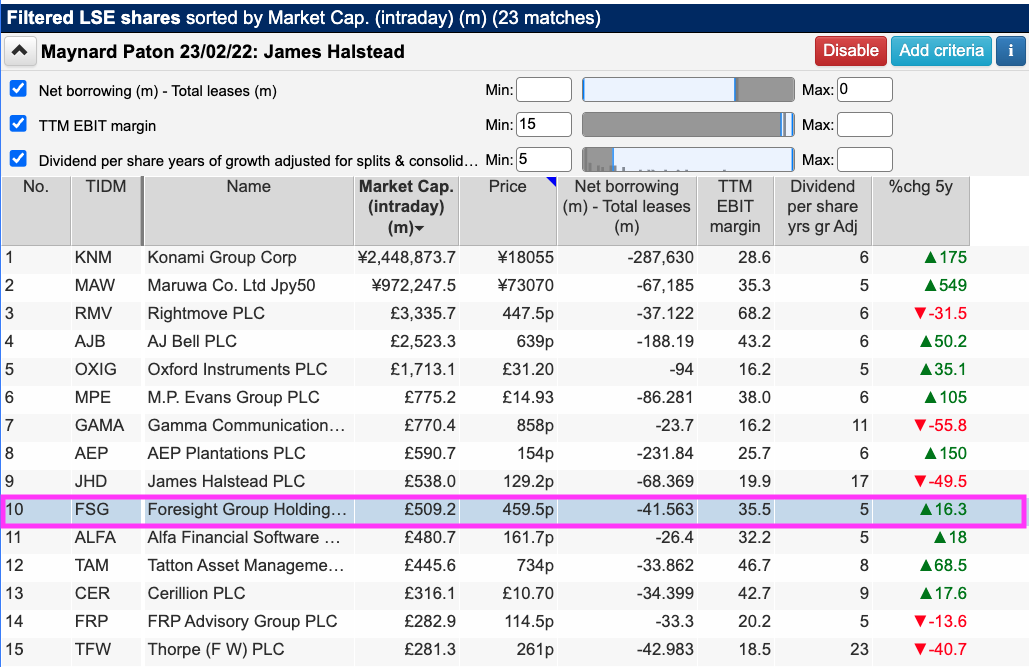

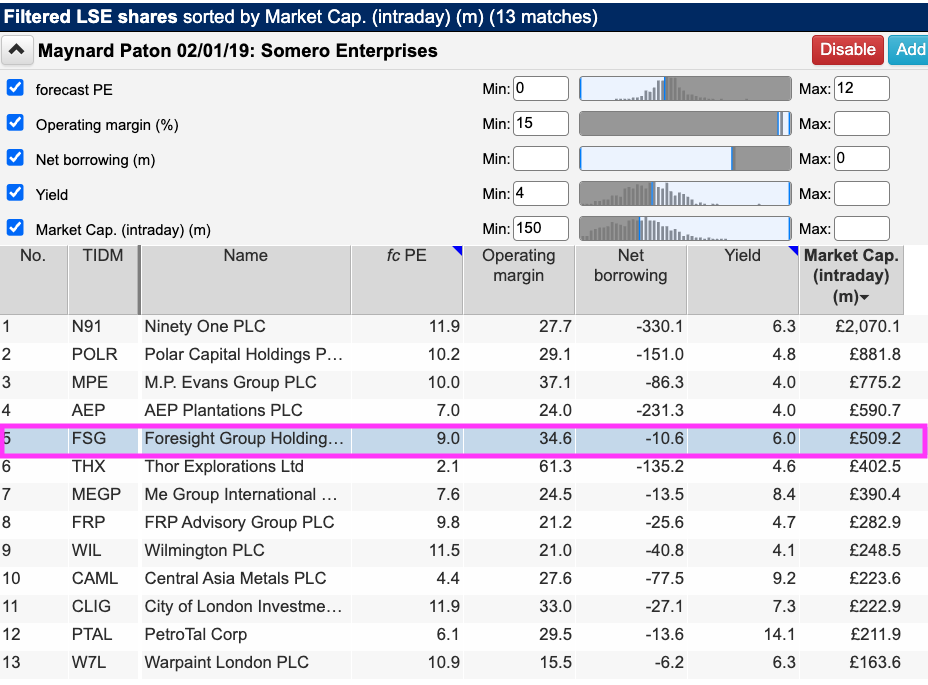

Foresight has recently appeared on the ShareScope screens I employed to identify Integrafin, James Halstead and Somero Enterprises:

Foresight’s high margin, net cash position, rising profits, modest valuation and significant director shareholdings may be enough to put my industry prejudices aside.

Let’s take a closer look.

Read my full FORESIGHT GROUP article for ShareScope >>Maynard Paton