20 May 2025

By Maynard Paton

H1 2025 results summary for Mountview Estates (MTVW):

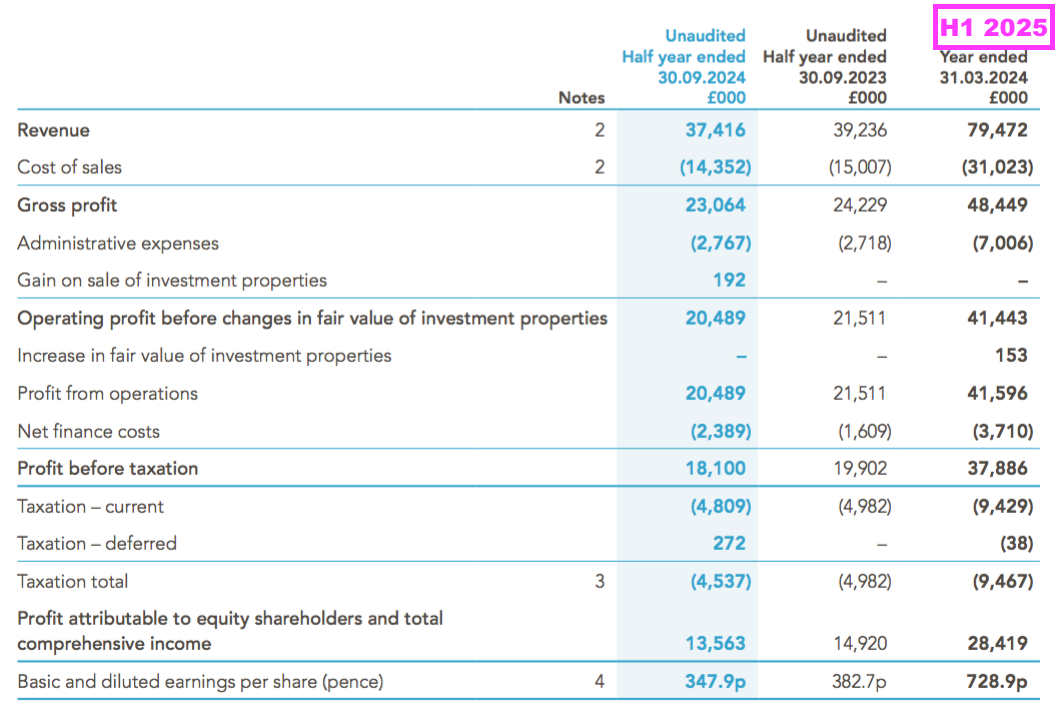

- Not the greatest of H1s, as “economic difficulties” and fewer property disposals combined to cut both revenue and profit by 5%, although the interim dividend was maintained and net asset value (NAV) crept to a record £103 per share.

- Property sales delivered a sub-60% gross margin for the fourth consecutive H1, which increasingly suggests ‘reversionary’ gains from regulated tenancies have inherently reduced and/or MTVW has simply overpaid for many past purchases.

- Properties bought and sold following the 2014 valuation continue to realise modest gains, with no obvious adverse trends concerning transaction costs and tenancy mix. The absence of another valuation has now left two non-execs ‘short-changed’ by selling shares below NAV.

- A new non-exec with a “keen focus on governance, risk and compliance” provides hope the board may adopt some fresh thinking on shareholder engagement, estate valuations and director pay, especially as protest votes have reached a record 33% of the share count.

- Recent share purchases by the chief executive may have signalled a tantalising buying opportunity, while the £97 price now offers a 5.4% income, trades 6% below NAV and may be worth £169 if the group’s properties were all sold today at their ‘vacant possession’ value. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own MTVW

- Results summary

- Revenue, profit, net asset value and dividend

- Trading properties: disposals

- Trading properties: acquisitions

- Trading properties: gross margin

- Trading properties: rental income

- Trading properties: properties valued by Allsop

- Trading properties: properties not valued by Allsop

- Financials: balance sheet

- Financials: administration expenses and employees

- Boardroom: protest votes

- Boardroom: new non-executive and director pay

- Valuation

News links, share data and disclosure

- Interim results for the six months to 30 September 2024 published 20 November 2024;

- Update on Annual General Meeting voting outcome published 14 February 2025;

- Director/PDMR Shareholding published 26 March 2025;

- Directorate change — Contract Extension published 31 March 2025, and;

- Update on General Meeting voting outcome published 16 May 2025.

- Share price: £97

- Share count: 3,899,014

- Market capitalisation: £378m

- Disclosure: Maynard owns shares in Mountview Estates. This blog post contains ShareScope affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy (and similar) properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family manager who continues to head an aggregate 50%/£191m concert-party shareholding.

- Properties are carried at cost, and when eventually sold at their ‘reversionary’ values may generate total proceeds significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Revenue, profit, net asset value and dividend

- Having reported reasonable progress and mentioned “more positive” economic indicators…

[FY 2024] “Looking forward economic indicators, including projected inflation levels, are looking more positive albeit projected to lead to only sluggish growth in the coming years leaving many households yet to regain pre-pandemic real disposable income levels. Thus the wider outlook is once more finely balanced as any one of a number of factors could tip the balance“

- …the preceding FY suggested this H1 might have delivered a small improvement on the comparable H1.

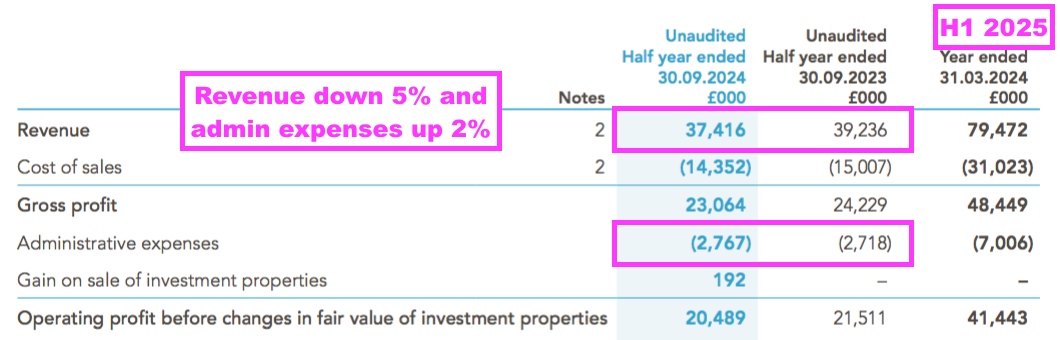

- This H1 in fact cited “economic difficulties” for a lower profit…

“The economic difficulties being suffered throughout the country have contributed to the Company’s gross profit for the six months ended 30 September 2024 decreasing by 4.5% and profit before tax by 9.0%”

- …and, somewhat ominously, disclosed a sub-60% gross margin from the sale of properties for the fourth consecutive H1 (see Trading properties: gross margin).

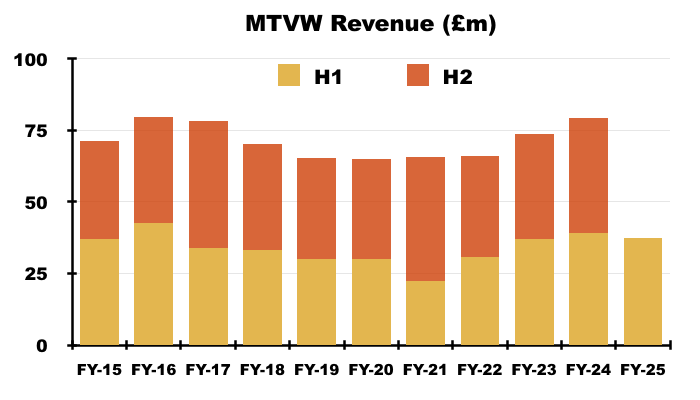

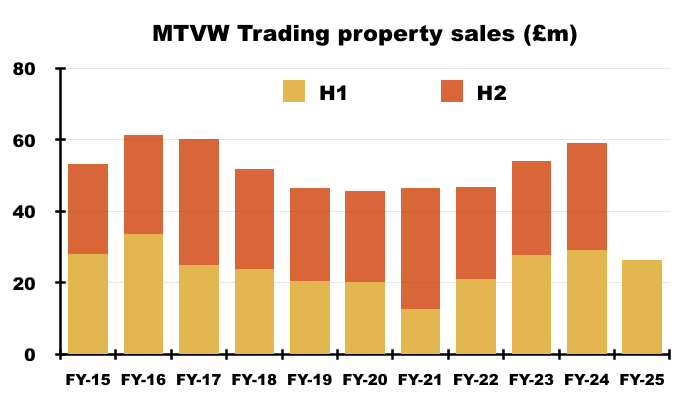

- The sale of fewer properties caused H1 revenue to decline 5% to £37.4m:

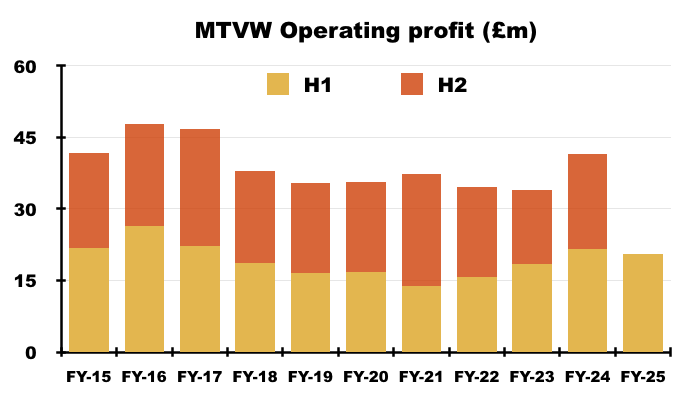

- H1 operating profit in turn slipped 5% to £20.5m:

- For context, H1 revenue was 13% lower and H1 operating profit was 22% lower than H1 2016, during which revenue reached a record £42.8m and operating profit reached a record £26.3m.

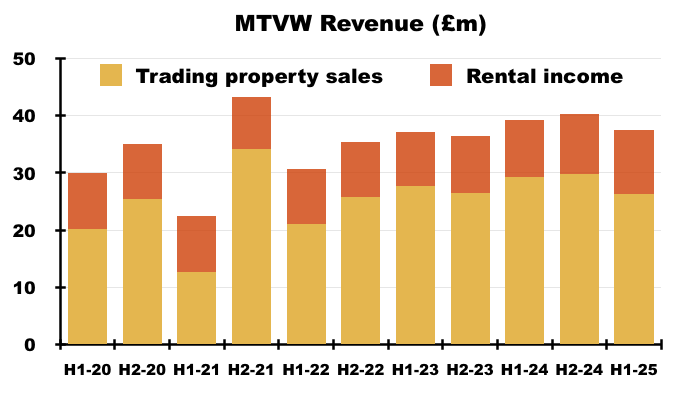

- This H1’s revenue was split 70%/30% between property sales and rental income, which matched the average of the ten preceding H1s (71%/29%):

- Note that MTVW typically sells its regulated-tenancy properties after obtaining ‘vacant possession’ — which in most cases does not occur until the tenant has died:

[FY 2024] “Regulated tenancies by their nature are not for any specific period of time and in most cases they do not become vacant until the death of the tenant. It is difficult to predict with any certainty the time at which Mountview’s inventory properties might become vacant.”

- The mix of properties becoming available for sale — and the total proceeds and profit MTVW generates — can therefore vary significantly from one set of results to the next (see Trading properties: disposals and Trading properties: gross margin).

- This H1 did not suggest the economy had suddenly improved…

“We live in difficult times, but I believe that this Company will continue to prosper and can continue to care for its staff and its shareholders.“

- …but the commentary did imply employee costs may (once again) increase significantly (see Financials: administration expenses and employees).

- At least the preceding FY had reiterated MTVW’s “lower priced” portfolio could escape the worst of any economic downturn:

[FY 2024] “We are fortunate that the properties that Mountview brings to auction are typically in high demand as they offer a lower priced entry to the housing market or, if sold to developers, provide opportunity for ‘developer profit’. We are hopeful therefore that Mountview will continue to be well placed to weather any continued downturn in the general housing market, should it occur, through both continuing sales of attractive properties and also with the opportunity to purchase potentially discounted replacement properties both through auction and private tender.”

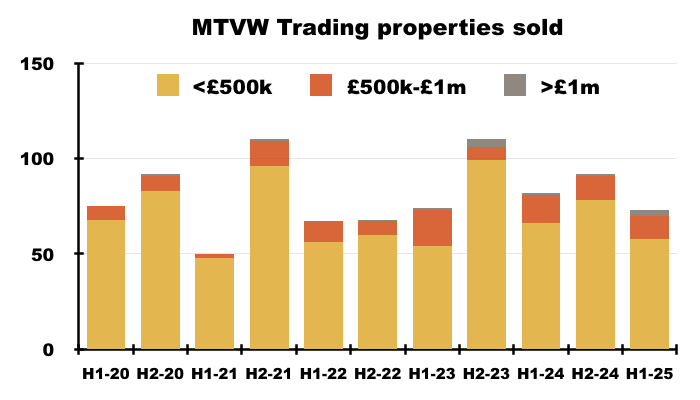

- MTVW’s properties are located mostly within London and south-east England, and 658 (86%) of the 818 properties MTVW sold during the five years to this H1 achieved less than £500k:

- This H1 bemoaned the higher cost of borrowing:

“Although interest rates have been reduced slightly in recent months, they are still at levels last experienced over ten years ago and are a significant factor in our increased costs”

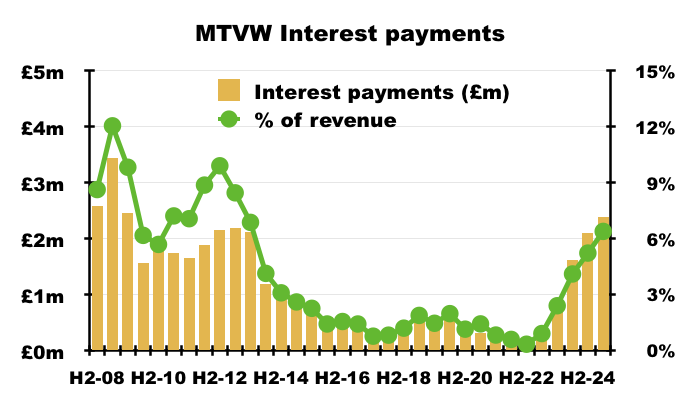

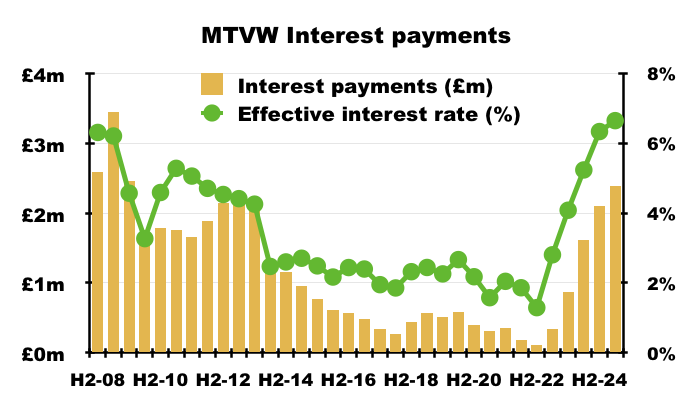

- H1 interest payments in fact surged 48% to £2.4m due to a higher rate of interest paid on a greater level of debt (see Financials: balance sheet).

- H1 interest payments absorbed 6.4% of H1 revenue, the highest six-month proportion since H2 2013 (6.9%):

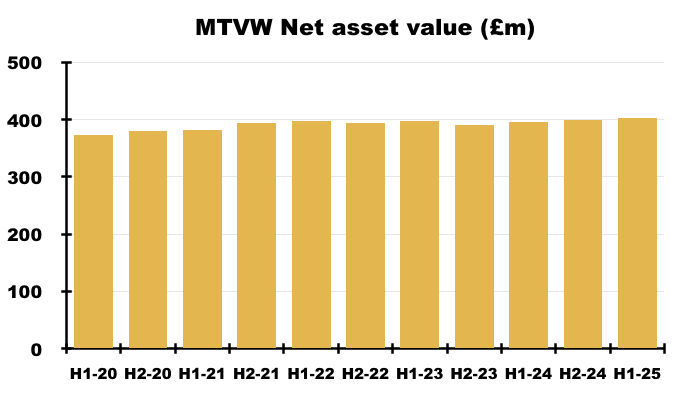

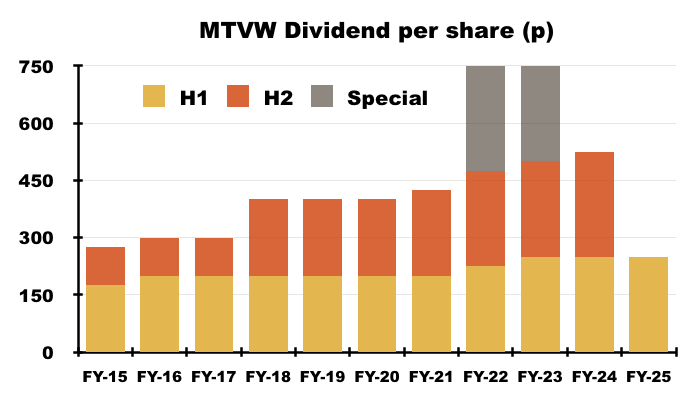

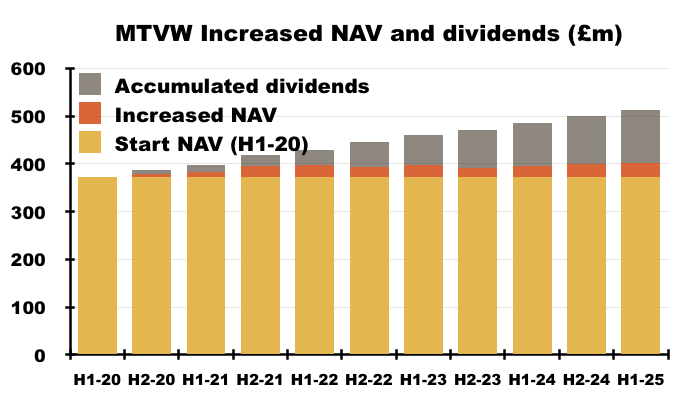

- H1 earnings of £14m less the £11m final dividend from the preceding FY meant net asset value (NAV) increased by just £3m to £402m or £103.22 per share:

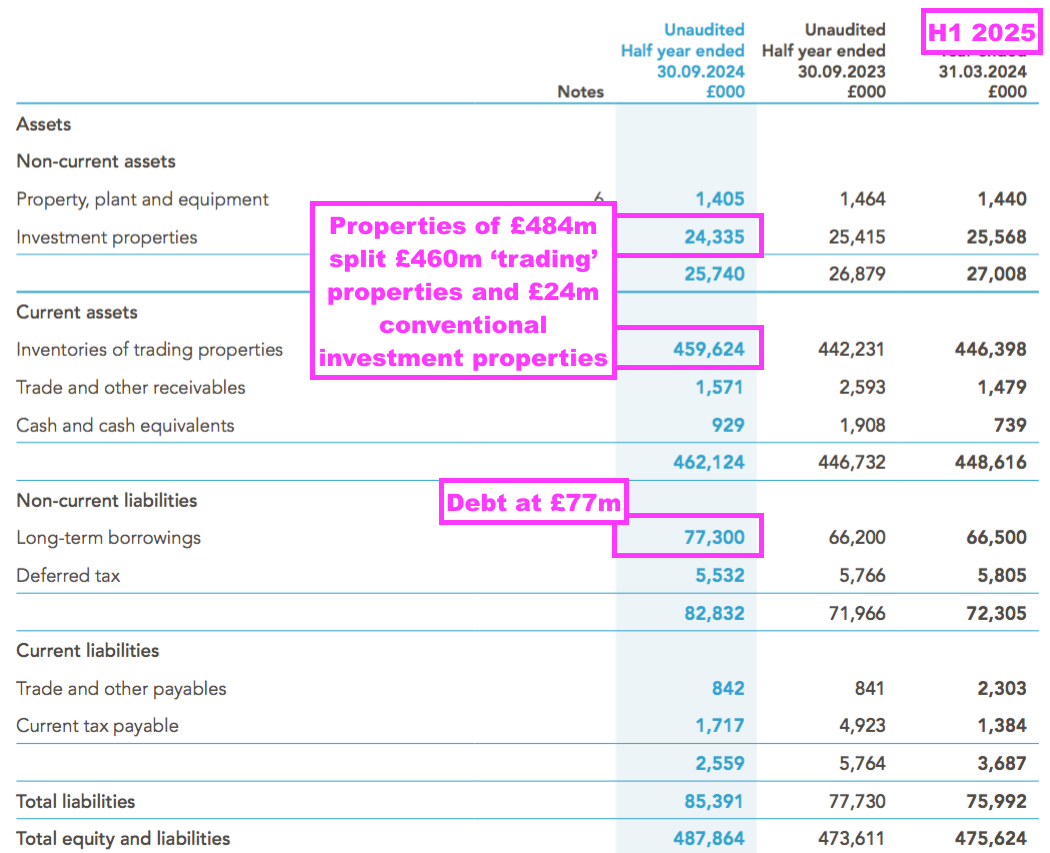

- H1 NAV of £402m:

- Comprised properties of £484m, debt of £77m and net other liabilities of £4m;

- Set a new record high, and;

- Exceeds the £378m market cap (see Valuation).

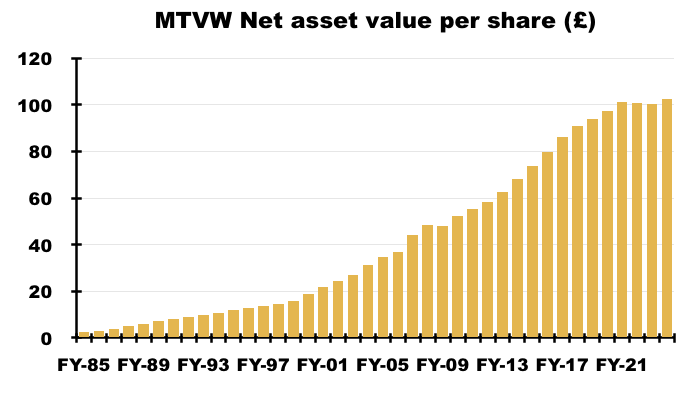

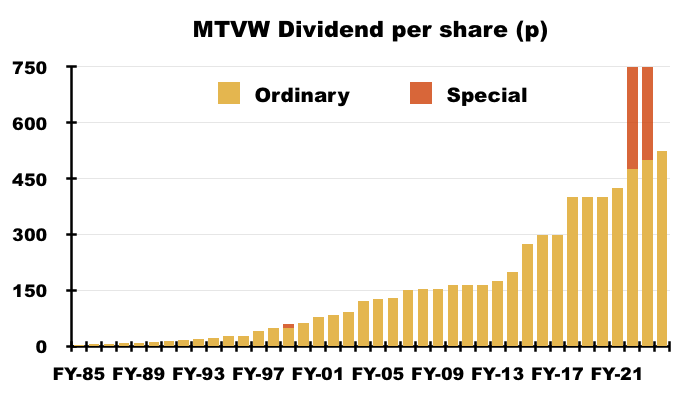

- Companies House reveals MTVW boasting an illustrious long-term NAV:

- NAV has settled around £100 per share during recent years, in part due to special payouts totalling 525p per share declared during FYs 2022 and 2023:

- The 525p per share paid as special dividends could have otherwise been retained to bolster NAV.

- This H1’s dividend was kept at 250p per share.

- The annual ordinary dividend has never been cut since at least 1985:

- The combination of NAV growth and the rising dividend has in the past handsomely rewarded long-term shareholders. But such returns have moderated over time.

- For example, during the five years to this H1, NAV has increased by £29m and paid dividends have totalled £111m to give a combined £140m:

- Versus NAV of £373m five years ago, the combined £140m equates to a 38% return.

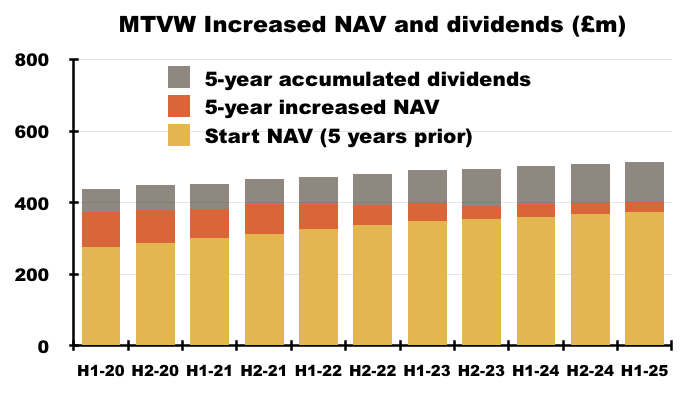

- In comparison, increased NAV and accumulated dividends came to £153m during the five years to H1 2021 (a 50% combined NAV and dividend return) — and reached £164m during the five years to H1 2018 (a 70% combined NAV and dividend return):

- The hope is future NAV and dividend growth can soon improve by MTVW undertaking shrewd property purchases. This H1 suggested such investments have been made:

“Our purchasing activity, which is the future of the Company, has remained strong during these six months and we continue to be offered further opportunities. Our financial strength should enable us to take advantage of the best of these, but we will not compromise our financial prudence.”

Trading properties: disposals

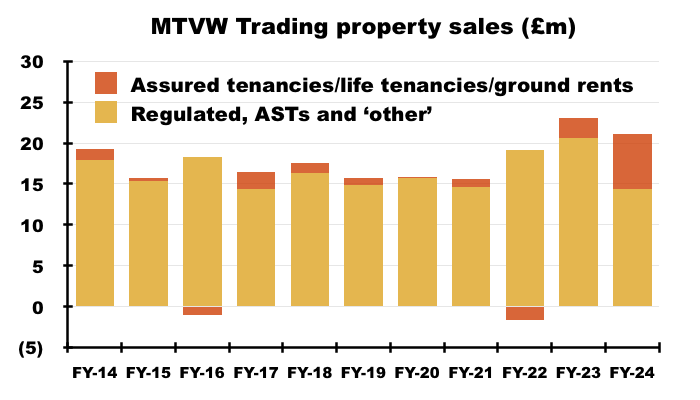

- H1 revenue from property sales fell 10% to £26m:

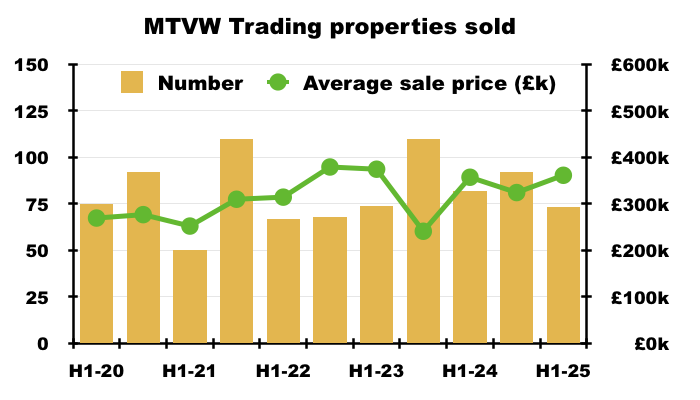

- The property-sales shortfall was due to MTVW disposing of 73 units during this H1 versus 82 during the comparable H1:

- The average H1 sale price (before transaction expenses) of £361k was commensurate with the £356k achieved during the comparable H1 and the £374k achieved during H1 2023.

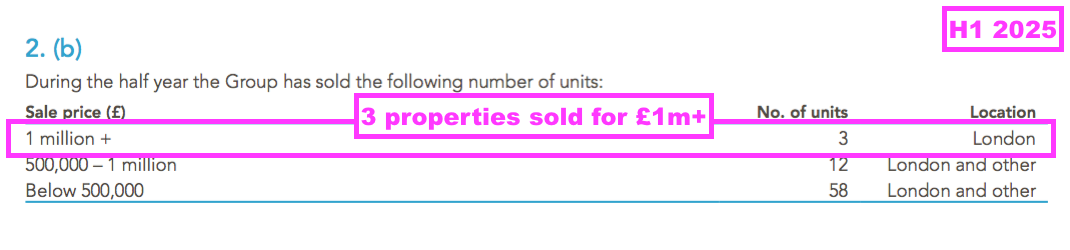

- Average sale prices can be skewed by MTVW occasionally raising £1m-plus from a single transaction. This H1 included three £1m-plus disposals, the most for an H1 since at least H1 2016:

- The information MTVW publishes for its H1s does not allow shareholders to deduce the mix of tenancy types sold during the period.

- But for each FY, the mix of tenancy types sold can be deduced by comparing the amount invested in each type of tenancy and adjusting for property purchases undertaken during that FY.

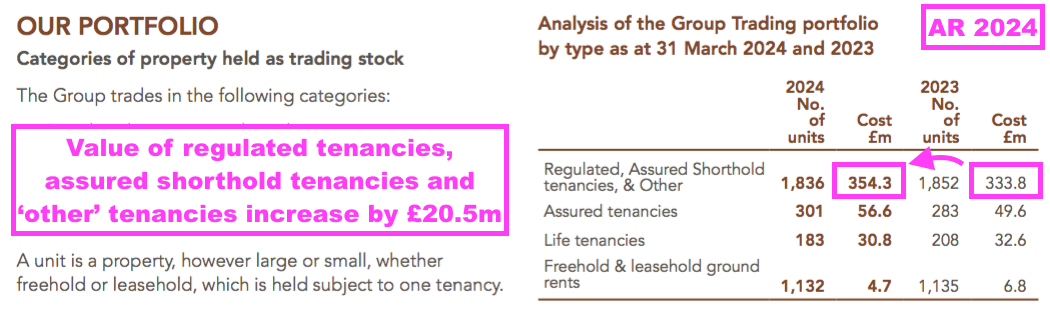

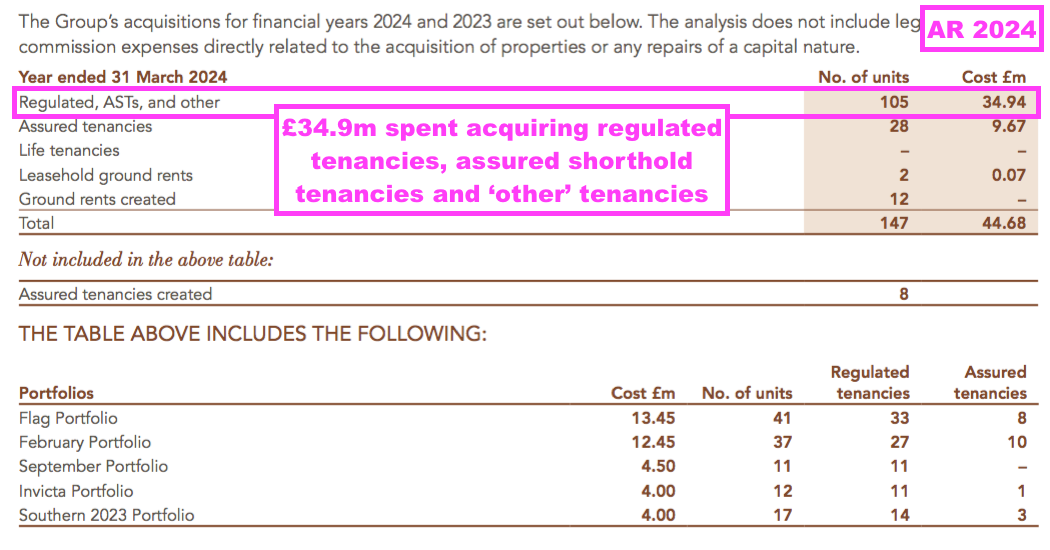

- For example, the preceding FY reported the year-end book value of regulated tenancies, assured shorthold tenancies and ‘other’ properties had increased by £20.5m:

- The preceding FY also reported £34.9m spent acquiring new regulated tenancies, assured shorthold tenancies and ‘other’ properties:

- The book value of the regulated tenancies, assured shorthold tenancies and ‘other’ properties that were sold during the preceding FY was therefore £34.9m less £20.5m = £14.4m:

- Note that my calculations (or MTVW’s information) may not be strictly accurate, because FYs 2016 and 2022 give a negative value for the assured tenancies, life tenancies and ground rents sold.

- Analysing the mix of tenancy types sold could in time help explain why:

- The gross margin from property sales has declined to less than 60% (see Trading properties: gross margin), and;

- Gains achieved from properties purchased since the Allsop valuation appear quite modest (see Trading properties: properties valued by Allsop).

- My calculations do not indicate an obvious change to the mix of tenancy types sold, although the preceding FY did witness a significant £7m sale of assured tenancies, life tenancies and ground rents.

- Board remarks during the 2023 AGM revealed MTVW had sold ground rents due to legislative changes (e.g. the Ground Rent Act 2022 and the Leasehold and Freehold Reform Act 2024):

[AGM 2023]

“Q: Sale of 50 ground rents, seems a significant number.

MTVW: Due to the Leasehold Reform Act. Analysed our ground rents and decided to put them up for auction. Sold them because they were not going to gain further value. Going to be a future trend of analysing and selling the freehold ground rents.“

- The preceding FY disclosed ground rents representing approximately 1% of the group’s trading-property estate:

- My layman interpretation of the Leasehold and Freehold Reform Act does not suggest MTVW’s core portfolio of regulated tenancies will become an obvious casualty of the new legislation.

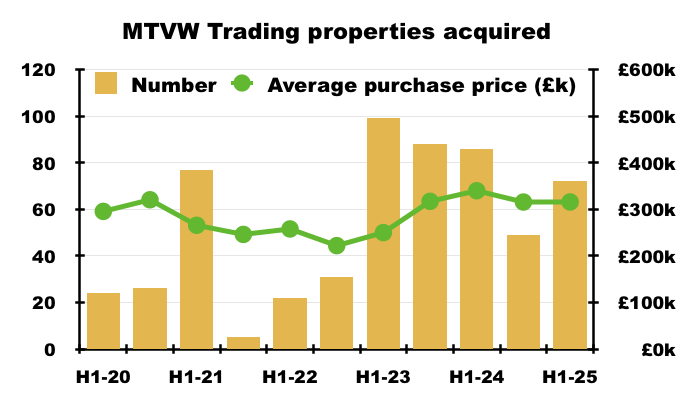

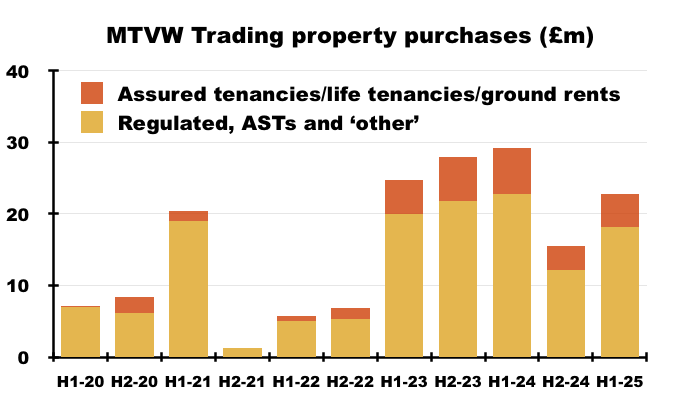

Trading properties: acquisitions

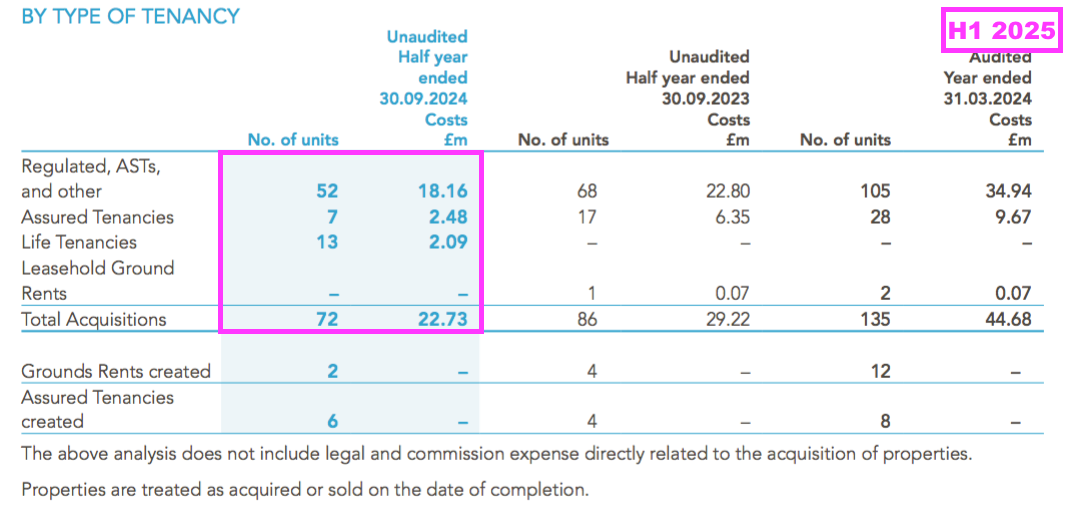

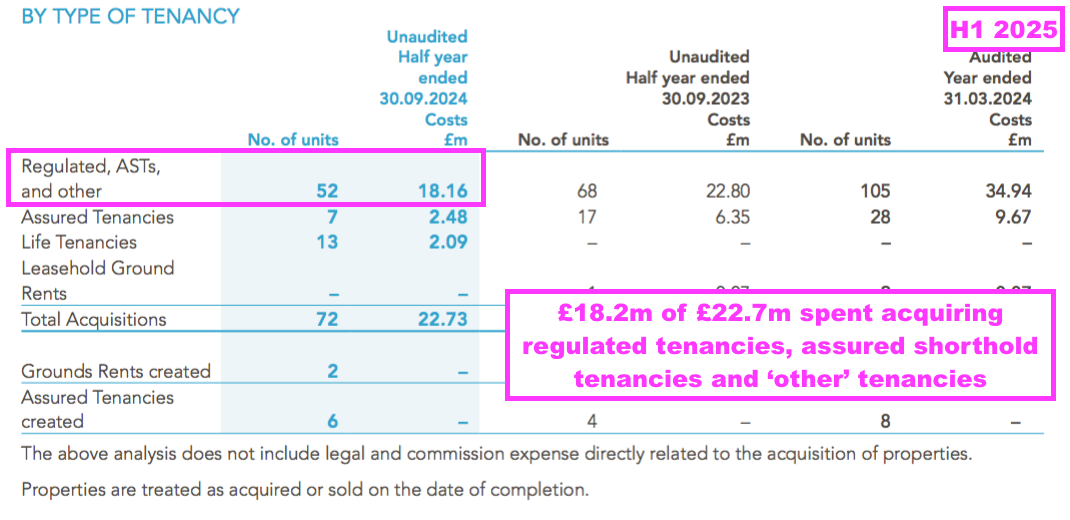

- Some £23m (before transaction expenses) was used to acquire 72 properties during this H1:

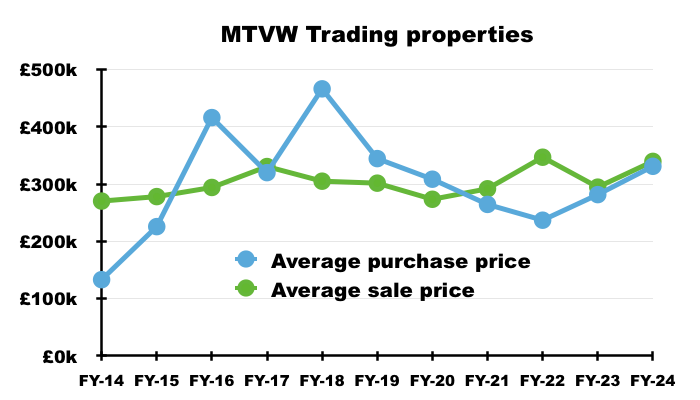

- The average purchase price (before transaction expenses) was £316k and very similar to the average witnessed during the preceding 18 months:

- The average £316k purchase price (before transaction expenses) was £45k less than the average £361k sale price (before transaction expenses).

- The difference between the average selling price and the average buying price may not have any practical relevance to MTVW’s future progress. But MTVW selling at higher prices and buying at lower prices does feel more reassuring than the other way around.

- For what it is worth, the preceding four FYs witnessed MTVW achieve an average selling price greater than its average buying price:

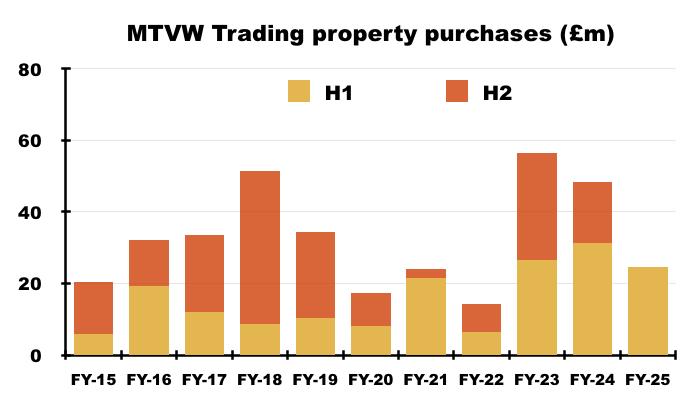

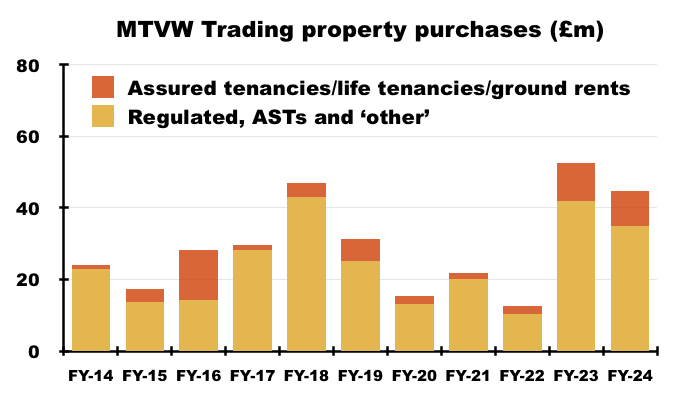

- MTVW’s property expenditure remains relatively elevated, which I trust means shrewd buying opportunities have not yet dried up.

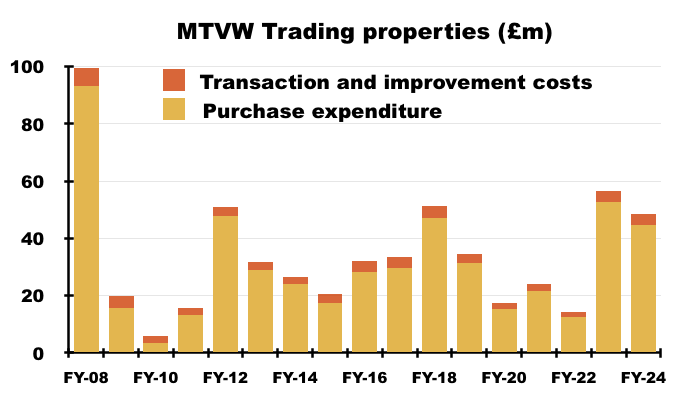

- Including transaction expenses and improvement costs, this H1’s £25m expenditure on property purchases compares to an H1/H2 average of £17m throughout the preceding ten FYs:

- The preceding two FYs revealed a substantial £80m spent acquiring portfolios of properties…

- …which implies the elevated buying activity has been prompted by larger landlords selling in bulk.

- This H1 did not speculate why landlords were selling, but the preceding FY did mention “changing and evolving legislation“:

[FY 2024] “Operationally, we will monitor the requirements resulting from changing and evolving legislation. This will include environmental legislation and the Leasehold and Freehold Reform Act (2024) (the Act) hastily rushed through Parliament during the wash-up period prior to Parliament being dissolved on 30 May 2024. Early comments have noted not just the terms of this Act but also its gaps, which will need future legislation. Moreover, implementing even the current Act will require further secondary legislation.”

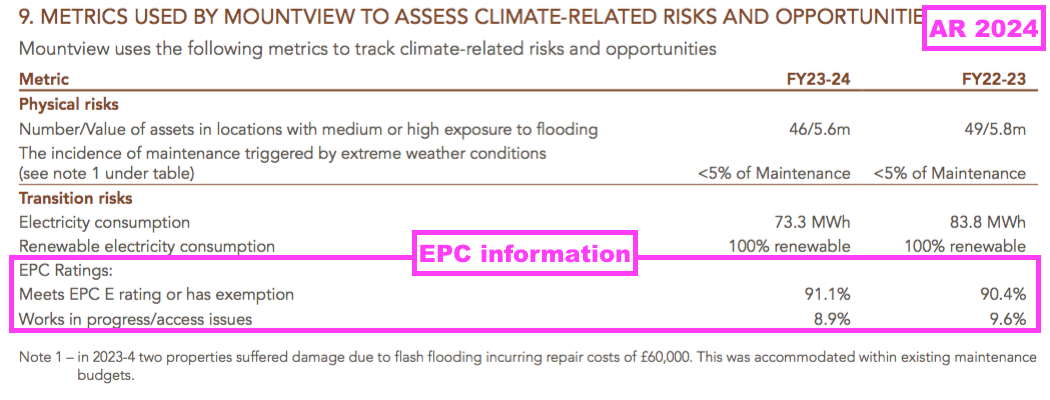

- “Changing and evolving legislation“ includes government proposals to raise the energy efficiency-standards of rented properties, which seems likely to create extra costs for MTVW.

- The government is proposing rented properties must possess an Energy Performance Certificate (EPC) rating of C or above from 2028 for new tenancies and from 2030 for all tenancies.

- MTVW’s EPC information only discloses 91% of the group’s properties have an EPC rating of E or above (or are exempt), with 9% yet to receive an assessment:

- A question about the proportion of properties that would require an EPC upgrade yielded the following unsatisfactory response during the 2023 AGM:

[AGM 2023]

“Q: Rough estimate of the number of properties affected by EPC?

MTVW: We know the current EPC ratings of our properties. Choose your own expenditure cap and multiply that by a proportion of our property portfolio. Won’t say what that proportion is. We do know the proportion, but don’t have it to hand. Would be very unfair and unreasonable to start making a guess on that question. All we have is the figure which is presented in the annual report of the number of properties that meet EPC or have an exemption.”

- I therefore speculate the proportion of properties that will require upgrading from EPC ratings D or E to C to be significant.

- The government’s energy-efficiency consultation sought views on whether “landlords should be required to invest up to a maximum of £15,000 per property on improvements to meet the standard (the ‘cost cap’), after which they could register a 10-year exemption to continue to let the property if it does not reach the standard.”

- The same proposals referred to “government modelling” and “on average, properties will require between £6,100 and £6,800 worth of investment to meet the standard under the preferred metric approach.”

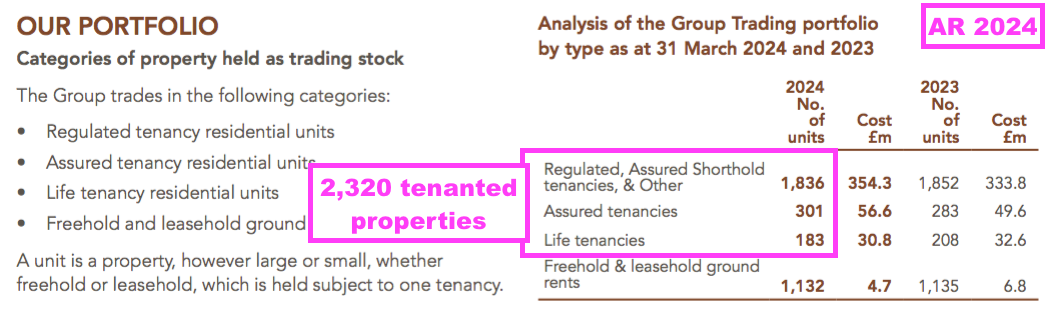

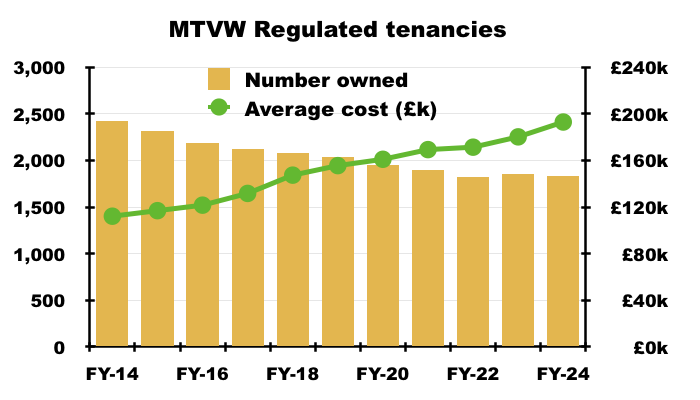

- The preceding FY showed MTVW owning 2,320 tenanted properties:

- 2,320 tenanted properties imply a possible energy-efficiency improvement bill of up to:

- £15m (almost £4 a share) based on the £6.45k “government modelling” mid-point estimate, or;

- £35m (almost £9 per share) based on the proposed £15k maximum.

- MTVW seems unlikely to pass on much (if any) of the extra EPC costs to tenants, given rents for the group’s core regulated-tenancy portfolio are set by local Valuation Offices.

- The book value of the trading properties includes “improvement costs“:

[FY 2024]

“INVENTORIES – TRADING PROPERTIES

These comprise residential properties, all of which are held for resale, and are shown in the financial statements at the lower of cost and estimated net realisable value. Cost includes legal fees and commission charges incurred during acquisition together with improvement costs. Net realisable value is the net sale proceeds which the Group expects on sale of a property in its current condition with vacant possession.“

- Expenditure to upgrade properties to EPC rating C therefore seems likely to be capitalised as stock and pass through the income statement only at the point of disposal.

- The government’s latest energy-efficiency consultation follows an initial 2020 consultation, and the general tardy progress of EPC reform to date could mean the aforementioned 2028 and 2030 timescales will be deferred. Buy-to-let lender Paragon for example has urged the government to delay the full 2030 implementation to 2035.

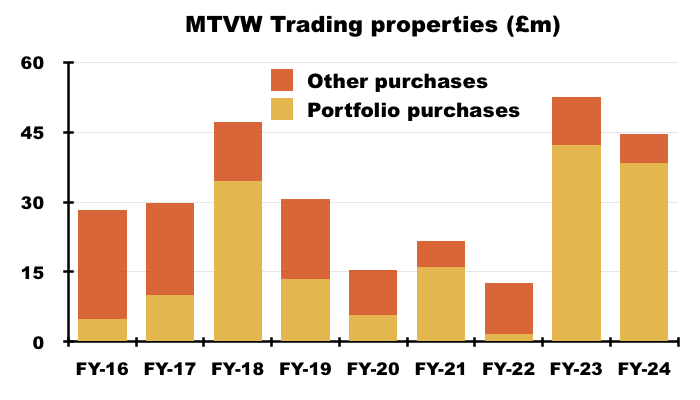

- Up to 80% of this H1’s £23m property expenditure (before transaction and improvement costs) was spent acquiring MTVW’s core regulated-tenancy properties:

- Up to 80% correlates with the up to 81% average seen during the preceding ten FYs:

- MTVW has spent up to £131m acquiring regulated tenancies during the last five years…

- …which suggests the market for regulated tenancies has not disappeared just yet.

- Regulated tenancies have not been created since 1989, and the very youngest tenants of such properties will now be in their mid-50s.

- The market for trading regulated tenancies could therefore last another two or three decades, although transaction activity will inevitably dwindle over time.

- The number of regulated tenancies owned by MTVW surpassed 3,000 25 years ago, surpassed 2,400 ten years ago but the preceding FY showed less than 1,900:

Trading properties: gross margin

- MTVW’s margin and profit can fluctuate due to the unpredictable mix of properties becoming available for sale during any particular period.

- The percentage gain on each property sold — reflected by MTVW’s gross margin — should be correlated to the duration of MTVW’s ownership, which can range from a few years to a few decades.

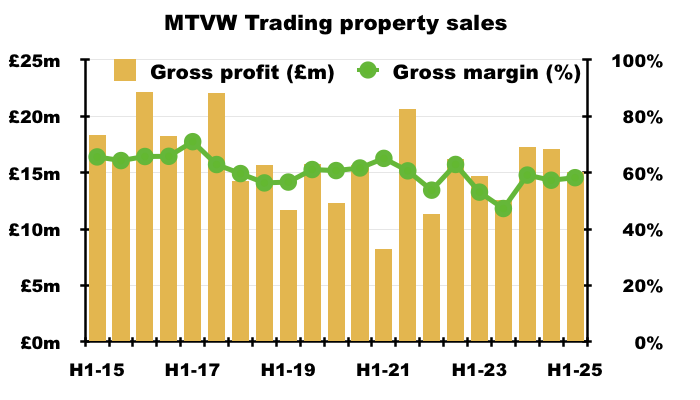

- This H1 registered a 57% property-sales gross margin:

- A property-sales gross margin of 57% is equivalent to buying a property for £100k and selling it for £233k.

- The preceding FY was the third consecutive FY with a property-sales gross margin of less than 60%…

- …and this H1’s 57% looks set to make it four consecutive FYs.

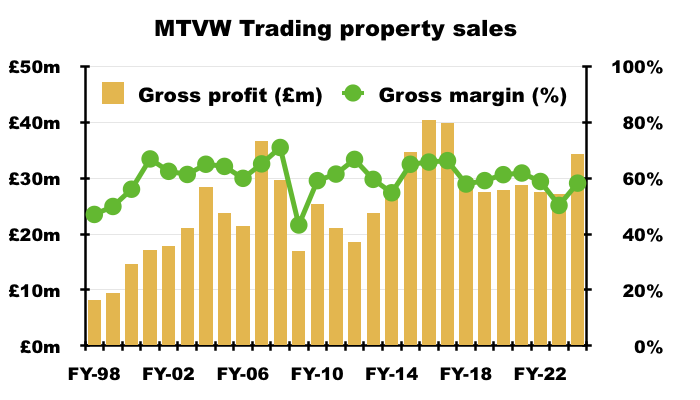

- A four-year run of sub-60% FY property-sales gross margins is very unusual. The last time such a run occurred was the four years to FY 2000.

- The run of sub-60% gross margins now gives a lower five-year average versus the preceding five-year periods:

- Five years to this H1: 58% average;

- Five years to H1 2020: 62% average, and;

- Five years to H1 2015: 61% average.

- The lower-than-normal gross margin suggests properties have been increasingly acquired for too much and/or sold for too little.

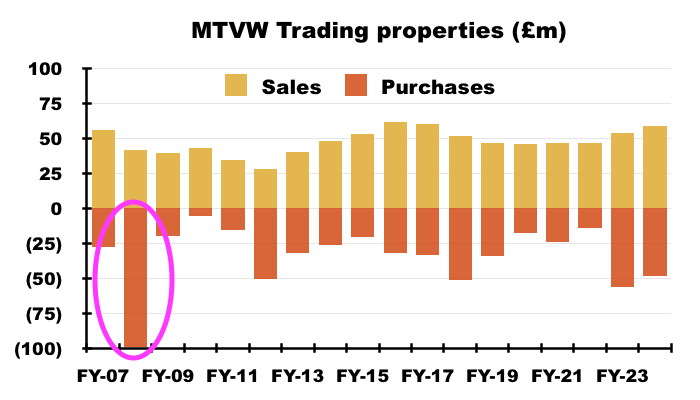

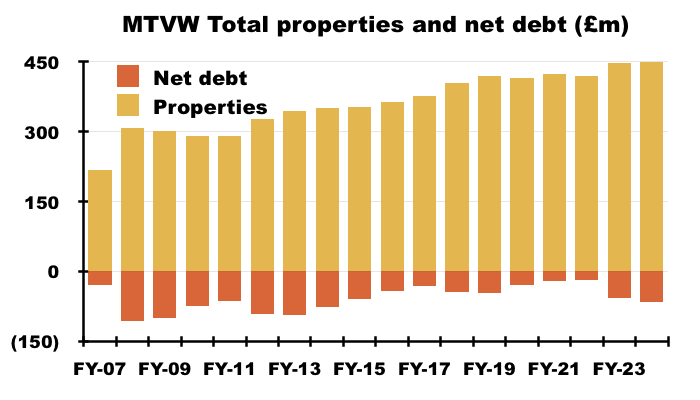

- In particular, the £100m spent acquiring properties during FY 2008 may not have delivered the subsequent gains MTVW expected at the time:

- The £100m spent during FY 2008 was by far MTVW’s largest annual payment for additional properties… and the purchases occurred when house prices had started to falter ahead of the banking crash.

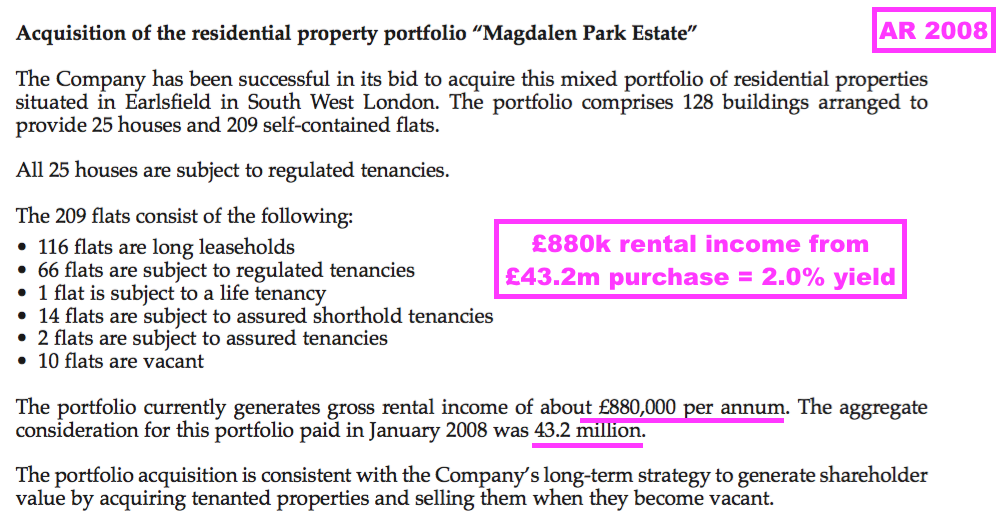

- Some £43m of that £100m was used to purchase Magdalen Park Estate in south-west London:

- The initial 2.0% rental yield from the Magdalen estate may not have offered tremendous value when, the year before, MTVW’s other properties were yielding a collective 5.5% on their purchase cost (£12m/£218m).

- Certainly the estimated gains on the purchases following the Allsop valuation imply MTVW may have paid too much to acquire properties since 2014 (see Trading properties: properties valued by Allsop).

- The aforementioned tenancy profiles of the properties bought and sold do not indicate a significant change to the mix of tenancy types traded, which in turn suggests the sub-60% gross margin may indeed be due simply to ‘high’ purchase prices.

- Bear in mind the ‘reversionary’ gains available from regulated tenancies — i.e. the value uplift that occurs when a regulated tenancy finishes, the rent reverts to a proper market level and the property can then be sold at a fair market value — will inherently reduce over time, as tenants become older and the duration to ‘vacant possession’ becomes shorter.

- The days of 60%-plus property-sales gross margins may have therefore gone for good, as the ‘reversionary gain’ potential continues to narrow for today’s regulated-tenancy buyers.

- Still, gross margins can rebound significantly as the unpredictable mix of properties becoming available for sale changes. For example, the 49% property-sales gross margin for H1 2014 had rebounded to a super 66% by H1 2015.

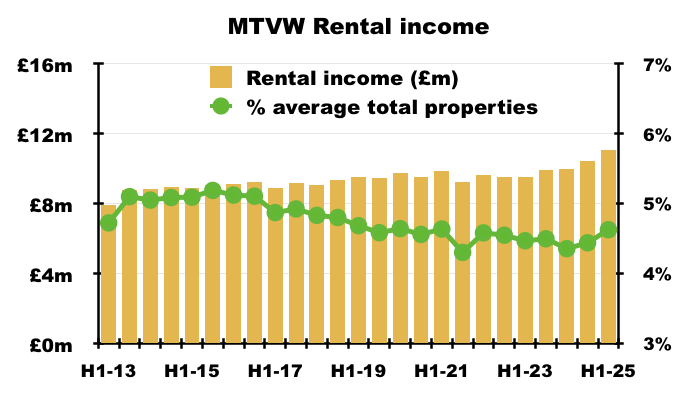

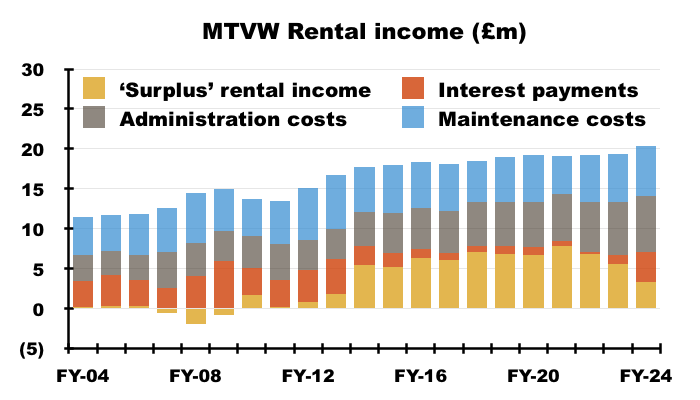

Trading properties: rental income

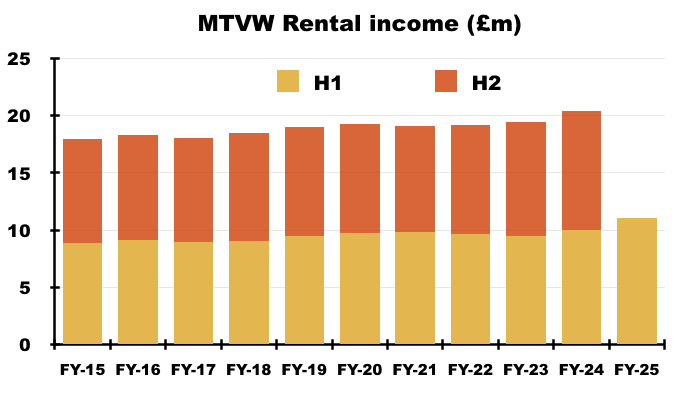

- MTVW’s H1 rental income gained a useful 11% to set a new six-month record of £11.1m:

- The greater rental income reflects the elevated rate of recent acquisitions — and perhaps a higher rental yield on purchase.

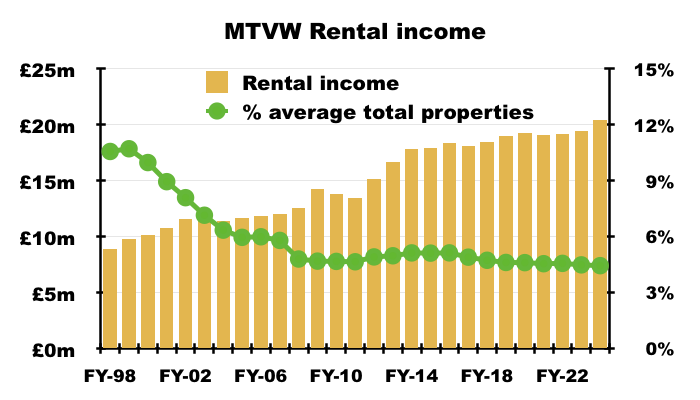

- MTVW appears to have enjoyed a step-change to rental income, whereby twelve-month rental income now exceeds £21m after settling within the £18m-£19m range since FY 2016.

- During the five years to this H1, twelve-month rental income has gained 12% or £2.3m while the book value of all properties has advanced 16% or £66m:

- The figures suggest for every net £1m spent on new properties during the last five years, an extra £34k (3.4%) has been added to the rent.

- Board remarks at the 2024 AGM implied MTVW sought to buy regulated tenancies supplying rental incomes of between 2.5% and 3% of cost.

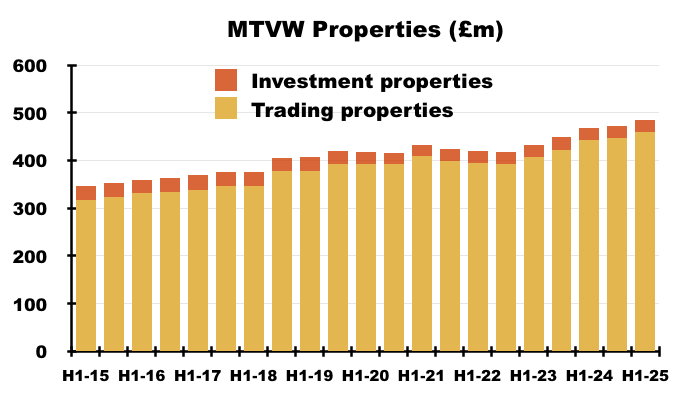

- H1 rental income of £11m equates to an effective 4.6% rental yield from this H1’s average £478m book value of all properties:

- 4.6% is a small but welcome improvement on the 4.4% witnessed during the preceding FY, which was the lowest rental yield since at least FY 1998:

- 4.6% is also ahead of the present 4.25% base rate.

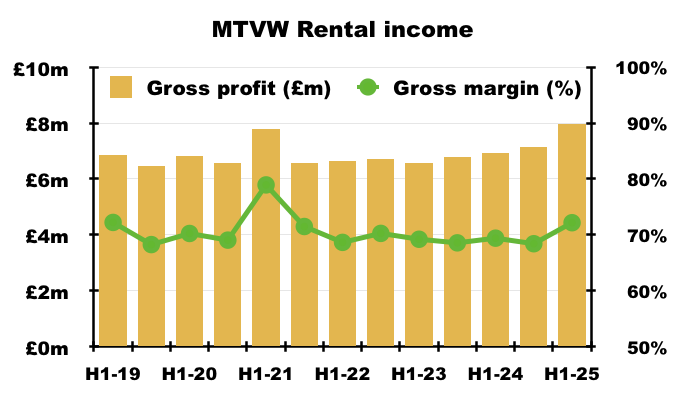

- Barring the 79% spike registered during the pandemic when certain maintenance work was deferred or cancelled, this H1’s 72% rental-income gross margin was the highest since H1 2019 (72%):

- I trust this H1’s improved rental-income gross margin supports the notion of MTVW now acquiring properties with a higher initial yield and generally undertaking shrewd purchases.

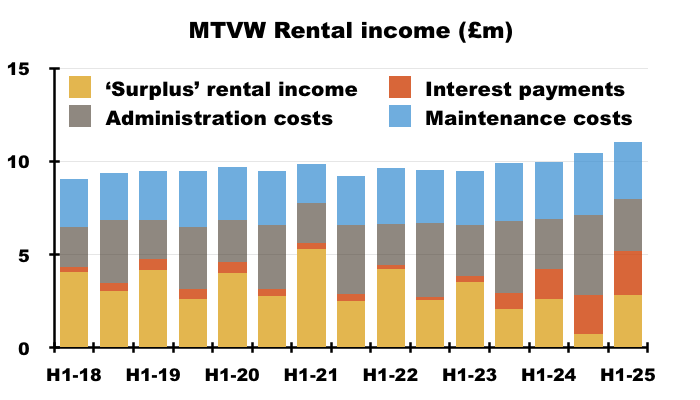

- Board remarks during the 2024 AGM revealed MTVW’s rental income was used to fund property maintenance costs, administration expenses (see Financials: administration expenses and employees) and interest payments (see Financials: balance sheet), and implied such income was viewed as a ceiling to limit expenditure and borrowings.

- This H1 generated a rental income ‘surplus’ of £2.8m after rental income of £11.1m paid maintenance costs of £3.1m, administration costs of £2.8m and bank interest of £2.4m:

- Twelve-month ‘surplus’ rental income now runs at approximately £3.5m, which provides useful headroom for higher operating costs and interest rates (see Financials: balance sheet). However, annual ‘surplus’ rental income did exceed £5m between FYs 2014 and 2023:

Trading properties: properties valued by Allsop

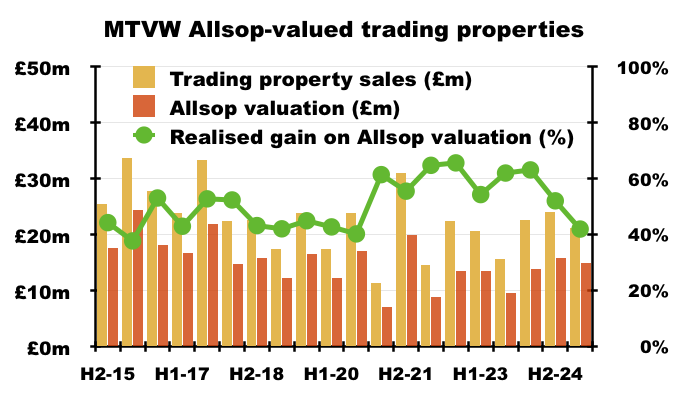

- MTVW continues to dispose of properties at a premium to a past valuation.

- To recap, MTVW commissioned property agent Allsop during September 2014 to assess the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties owned at the time.

- The Allsop assessment was based on MTVW’s properties remaining in their regulated-tenancy state and therefore excluded any ‘reversionary’ gains.

- The Allsop assessment was never applied to the formal accounts. MTVW’s properties instead remain on the balance sheet at their cost price.

- Following the Allsop assessment, MTVW reveals the proceeds from sold properties versus their Allsop valuation:

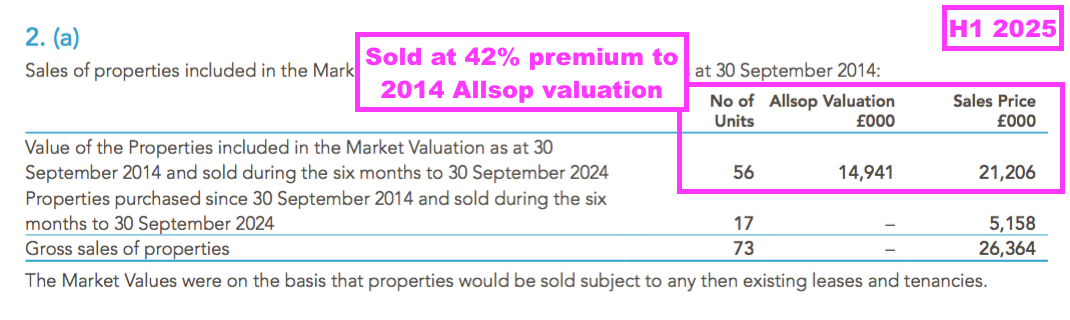

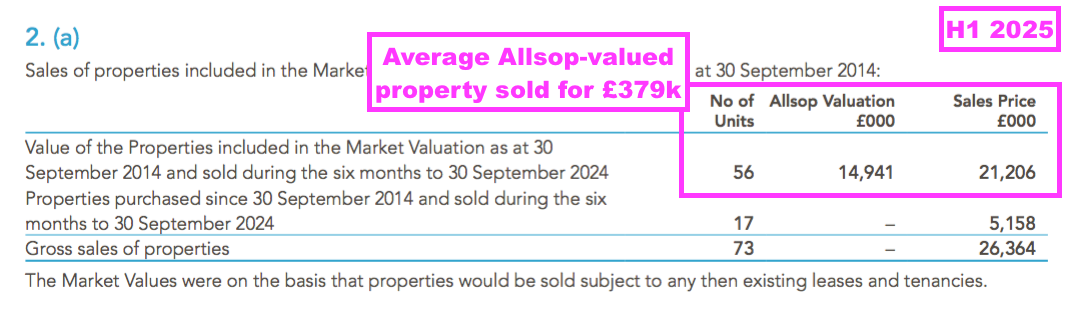

- This H1 witnessed MTVW sell properties with a combined £14.9m Allsop valuation for £21.2m — a premium of 42%:

- Rather oddly, this H1’s 42% premium was well below the 60%-plus premiums enjoyed during FYs 2022 and 2023, and was the lowest since H1 2016 (38%).

- I would venture the low, 42% premium was due primarily to an unfortunate mix of sold properties that did not quite live up to their expected disposal value.

- After all, every Allsop-valued property was acquired before or during 2014, and previous sales of Allsop-valued properties have yielded worthwhile premiums of up to 66%.

- Note that MTVW did not appear to incur weaker selling prices for its Allsop-valued properties. The 56 sold during this H1 achieved an average £379k…

- …compared to £314k during the comparable H1 and £363k during H1 2023.

- The realised premium to the Allsop valuation has implications for estimating MTVW’s potential share price (see Valuation).

- During the ten years following the Allsop assessment, MTVW has raised £455m from selling properties the agent had valued at £304m.

- Selling properties that Allsop had valued at £304m implies the book value (i.e. the original cost) of the properties sold was £145m (i.e. £304m divided by the aforementioned 2.1x multiple).

- Selling Allsop-valued properties with a £145m book value indicates Allsop-valued properties with a £173m book value remain within MTVW’s ownership (i.e. the £318m book value at the September 2014 assessment less the £145m since sold).

- If MTVW has taken ten years to sell Allsop-valued properties with an estimated £145m book value, the remaining Allsop-valued properties of £173m could therefore take a further 12 years to sell.

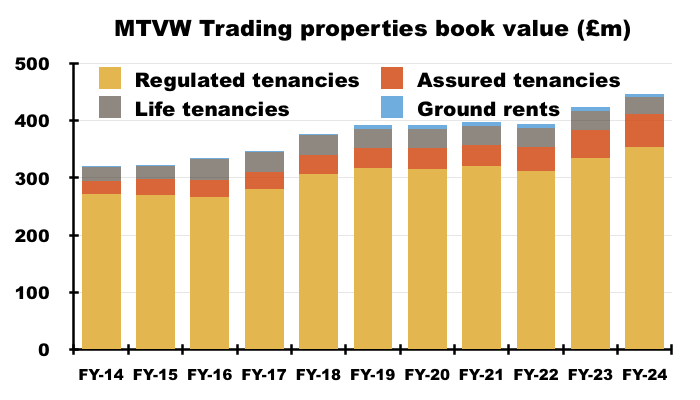

- This H1 showed total trading properties possessing a £460m book value, implying properties purchased after the Allsop review have a £287m book value (i.e. £460m less the remaining Allsop-valued properties of £173m).

- As more Allsop-valued properties are sold and other properties are purchased, the less relevant the 2014 Allsop valuation becomes to MTVW’s share price.

- MTVW’s results commentary has never referred to the Allsop valuation since the assessment was undertaken, and the preceding FY repeated the explanation why:

[FY 2024] “The [Allsop] valuation is not a useful tool for running the business because we are always going to await vacant possession, and no perceived uplift in value can justify selling a tenanted property. The nature of our business and the rules and conventions under which we operate place no obligation upon us to value our trading stock at any given time and therefore the valuation has not been updated since.”

- Numerous shareholders have questioned the board during several AGMs about the prospect of another Allsop-type valuation. However, the board has repeatedly rejected another assessment. Reasons given have included:

- The assessment is not used by management;

- The assessment is expensive, and;

- There is no accounting requirement.

- Board remarks during the 2024 AGM confirmed the directors were unanimous in their decision not to undertake another Allsop-type valuation.

- An irony perhaps of the board not undertaking another valuation is that, should the directors wish to sell, they may not achieve a satisfactory price for their shares.

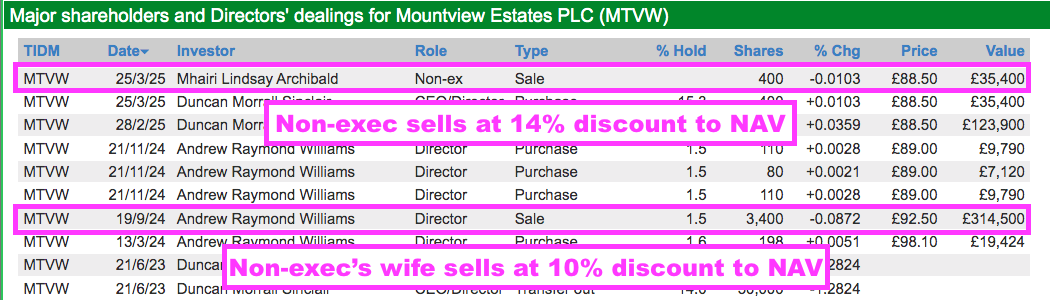

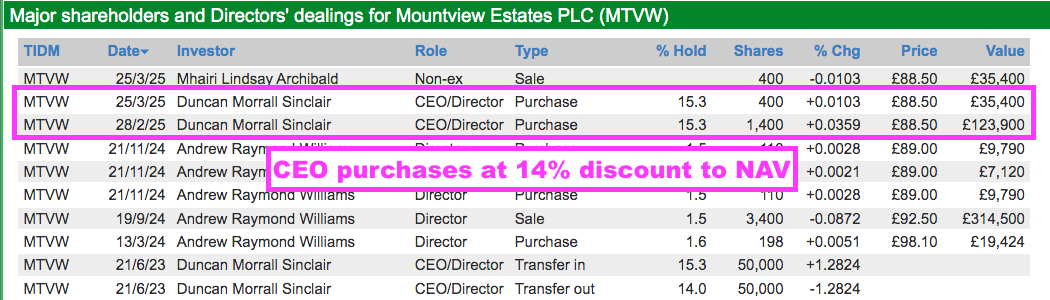

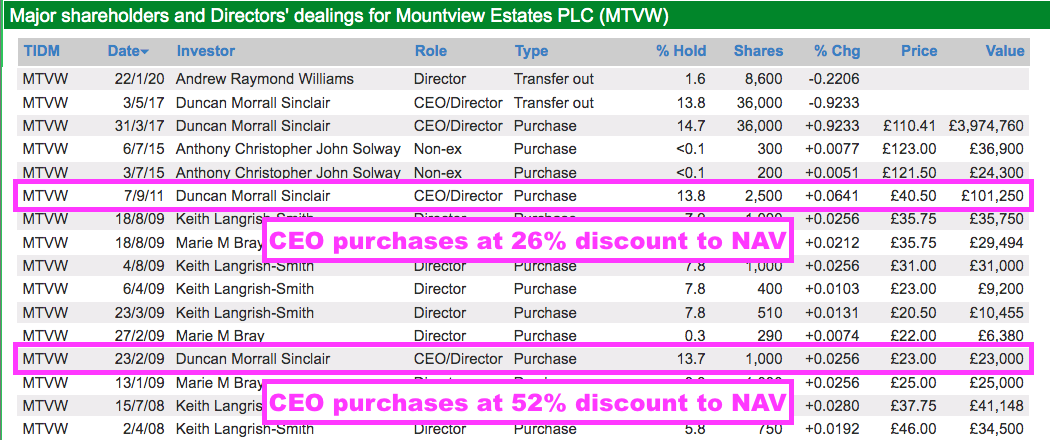

- The wife of MTVW non-exec Dr Andrew Williams for example raised £315k after selling MTVW shares during September at £92.50 — 10% below this H1’s NAV per share.

- MTVW non-exec Mhairi Archibald meanwhile raised £35k after selling MTVW shares during March at £88.50 — 14% below this H1’s NAV per share:

- Had MTVW undertaken another Allsop-type assessment and revealed further ‘hidden value’ within its property estate, the shares may now be trading above NAV…

- …and both the wife of Dr Williams and Ms Archibald may have raised somewhat more than they did (see Valuation).

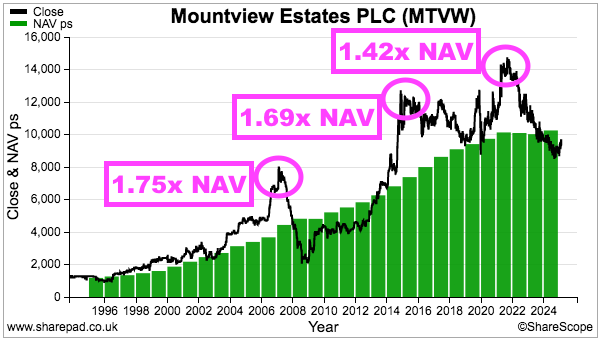

- Note that the 2014 Allsop valuation — and the revelation that the property estate could be worth 2.1x its then book value — prompted the share price to rally to £125:

- Another valuation that reveals further ‘hidden value’ could once again re-rate the shares (see Valuation) and prevent directors (and other shareholders) from being ‘short-changed’ by the market should they ever wish to sell.

- I maintain MTVW should implement regular Allsop-type valuations to provide greater clarity about the inherent value of the group’s property estate.

- In particular, further valuations would help shareholders judge the astuteness of MTVW’s recent purchases and perhaps allay worries of:

- Prolonged sub-60% property-sales gross margins, and:

- Modest premiums realised on properties bought and sold following the 2014 Allsop valuation (see Trading properties: properties not valued by Allsop).

- Board remarks at the 2021 AGM revealed the Allsop valuation cost £600k and “would be more now“.

- Even if another Allsop assessment cost £1m, the shareholder value created through an increased market-cap could make the process extremely worthwhile. The shares moving from £97 to, say, £117, following a favourable valuation would create additional market value of £78m.

- The cost of regular valuations could be offset partly by savings generated from:

- Toning down executive pay (see Boardroom: new non-executive and director pay), and;

- Appointing non-execs that are supported by independent shareholders and the subsequent cessation of general meetings that cost £50k a pop (see Boardroom: protest votes).

- The board may argue MTVW’s illustrious NAV and dividend records have served outside shareholders very well despite the lack of formal valuations.

Trading properties: properties not valued by Allsop

- The Allsop assessment and associated disclosures allow shareholders to evaluate the properties not valued by Allsop.

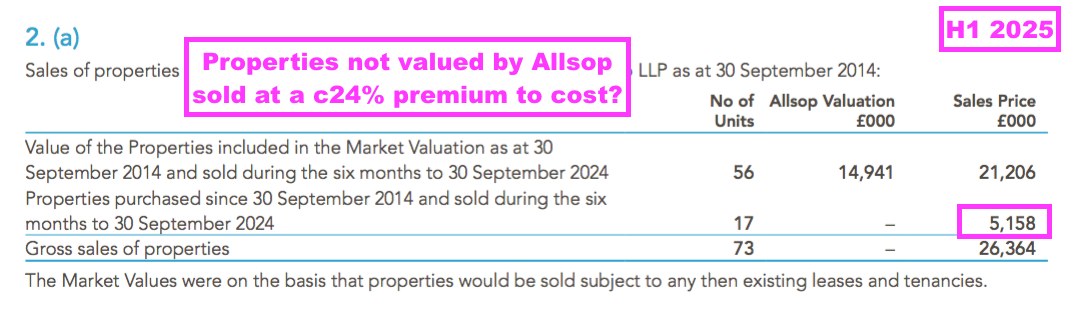

- During this H1, properties bought after the Allsop valuation raised proceeds of £5.2m:

- But what was the original cost of those properties that raised the £5.2m?

- The Allsop-valued properties sold during this H1 had an Allsop valuation of £14.9m, which suggests their book value (i.e. purchase price) was £14.9m/2.1x = £7.1m.

- The total book value of properties sold during this H1 was £11.3m, which implies the book value of the properties bought after the Allsop valuation and sold during this H1 was £11.3m less £7.1m = £4.2m.

- Raising £5.2m from selling properties with an estimated £4.2m purchase price indicates MTVW disposed of the properties at a 24% premium.

- Board remarks during both the 2019 AGM and the 2023 AGM stressed MTVW purchased regulated tenancies at 75% of their ‘vacant possession’ value.

- In theory at least, a regulated property purchased one day at 75% of ‘vacant possession’ value — which then becomes vacant the next day — should enjoy an immediate 33% ‘reversionary’ gain.

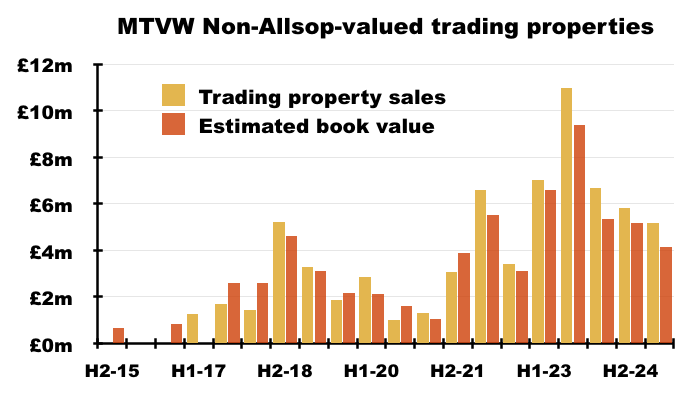

- I calculate during the ten years following the Allsop valuation, MTVW has raised a total £69m from selling properties not valued by Allsop with an estimated book value (i.e. purchase price) of £64m:

- I calculate during the five years to this H1, MTVW has raised a total £51m from selling properties not valued by Allsop with an estimated book value of £46m.

- My estimates indicate MTVW’s purchases following the Allsop assessment of September 2014 have led to ‘reversionary’ gains somewhat below the 33% that buying at 75% of ‘vacant possession’ should generate.

- My estimates could easily explain why the property-sales gross margin has been less than 60% during recent years; properties bought and then sold since September 2014 have seemingly realised only modest gains.

- My estimates may also explain why the share price has made little headway during the same time:

- Of course, not every property MTVW has purchased following the Allsop assessment has been sold.

- Those properties not valued by Allsop but still owned by MTVW could be sitting on huge paper gains, while those that have been sold were held for relatively short durations that would always limit their final profit.

- Furthermore, MTVW acquires properties other than regulated tenancies, which may require more than the ten years since the Allsop assessment to maximise their upside.

- Still, buying properties for an estimated £64m/£46m and then selling for £69m/£51m can’t be deemed a rousing success — especially when 33% ‘reversionary’ uplifts should be enjoyed.

- My Allsop calculations and those undertaken by other shareholders probably explain the pointed questions about MTVW’s purchases during the 2023 AGM and the 2024 AGM.

- Board remarks to those questions during the 2024 AGM included:

- “We’re satisfied that the purchasing process is robust“;

- “We are content with the returns which have been delivered“, and;

- “Calculations from the outside are based upon summary level information and lead to a different answers to what you get from the inside, which include precise costs associated with the individual properties.“

- Note that transaction costs (as well as improvement costs) are included within the book value of the trading properties:

[FY 2024]

“INVENTORIES – TRADING PROPERTIES

These comprise residential properties, all of which are held for resale, and are shown in the financial statements at the lower of cost and estimated net realisable value. Cost includes legal fees and commission charges incurred during acquisition together with improvement costs. Net realisable value is the net sale proceeds which the Group expects on sale of a property in its current condition with vacant possession.“

- I am not convinced greater transaction and improvement costs have moderated MTVW’s property gains over time. My estimates do not show an obvious uplift to such expenses:

- The absence of a follow-up Allsop-type assessment leaves me to assume the properties not valued by Allsop but still carried on the balance sheet are unlikely to enjoy an eventual sale value vastly in excess of their aforementioned £287m aggregate purchase price.

Financials: balance sheet

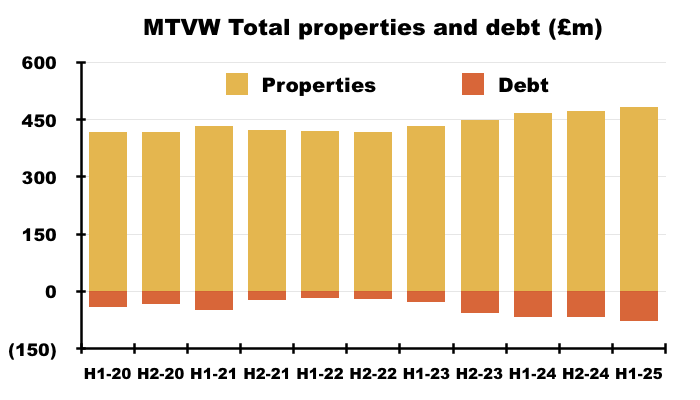

- MTVW’s accounts remain very straightforward, with properties and debt the two prime entries:

- The aforementioned £25m spent on new properties (including transaction and improvement costs) led to a free cash outflow of £1m, with dividends of £10m then increasing H1 debt from £67m to £77m.

- Debt at £77m is the highest since H2 2014 (£78m), but is equivalent to only 16% of the group’s £484m total property estate:

- For perspective, MTVW operated with net debt equivalent to 25% or more of its property estate during FYs 2008, 2009, 2010, 2012 and 2013:

- MTVW’s banking facilities allow borrowings of up to £90m, equivalent to 19% of the total property estate.

- A repeat of this H1’s £11m debt increase during H2 would take debt to £88m and require MTVW to extend its £90m borrowing facilities in order to undertake significant further purchases.

- Finance costs of £2.4m for this H1 were 48% greater than the £1.6m for the comparable H1, and implied a 6.65% interest rate on this H1’s £72m average debt:

- My estimated H1 interest cost of 6.65% is the highest since H1 2008 (6.73%).

- The preceding FY reconfirmed MTVW’s borrowings incur an approximate 2% margin above SONIA.

- SONIA is currently 4.21%, which means MTVW should now be paying approximately 6.21% on its debt.

- Trailing twelve-month interest costs are £4.5m, and assuming debt stays at £77m and SONIA stays at 4.21%, annual finance costs would advance to £4.8m.

- Paying an extra £0.3m or so through higher interest will trim immediate NAV growth…

- …but should (in theory!) enhance longer-term NAV — assuming of course the properties purchased by the extra borrowings generate eventual returns well in excess of my projected 6.21% annual debt cost!

- The aforementioned £3.5m rental-income surplus after all maintenance, administration and finance costs should (in theory!) allow MTVW to borrow a further £56m at 6.21%, which would take gearing to 28%.

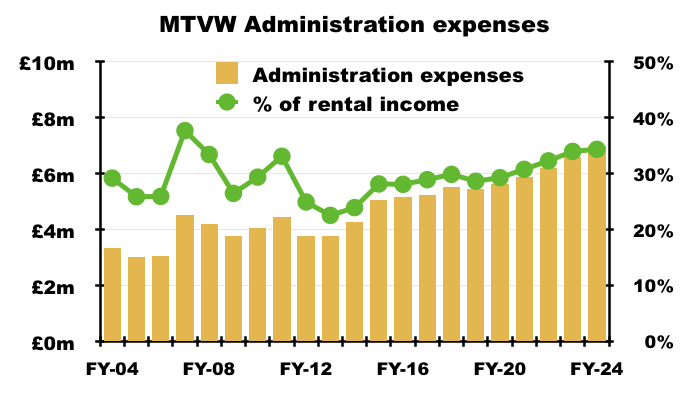

Financials: administration expenses and employees

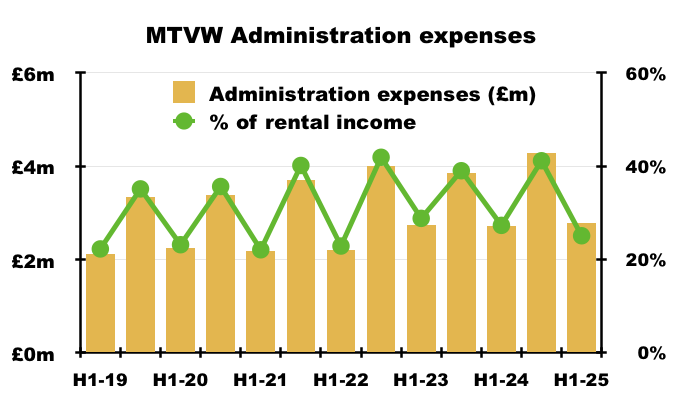

- H1 administration expenses gained 2% despite the lower revenue:

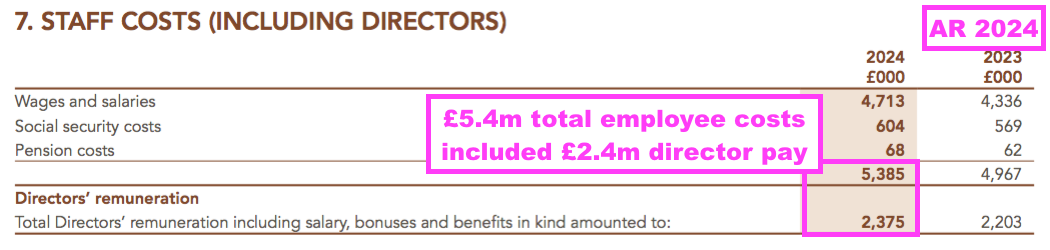

- Employee costs represent the majority of administration expenses. During the preceding FY, administration expenses comprised employee costs of £5.4m and other costs of £1.6m.

- A significant proportion of employee costs are payments to the directors. During the preceding FY, employee costs consisted of £2.4m paid to the directors (see Boardroom: new non-executive and director pay) and £3.0m covering the salaries of other employees plus the group’s social security expense:

- Administration expenses absorbed 25% of rental income during this H1, a welcome reduction from the 27% recorded during the comparable H1 and 29% recorded for H1 2023:

- Note that administration expenses are weighted towards H2 — presumably due to year-end employee bonuses! — and the annual proportion absorbed from rental income has increased steadily since FY 2013:

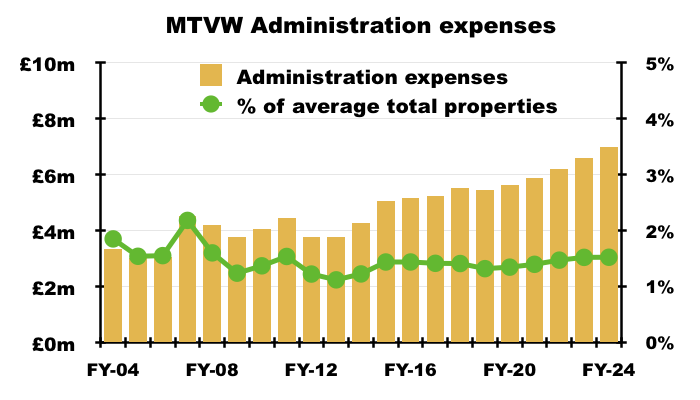

- Mind you, annual administration expenses versus the value of total properties have remained very consistent at approximately 1.5%:

- Higher salaries for employees — and directors! — may therefore not be entirely out of step with the group’s progress.

- MTVW’s chunky director pay may be a by-product of not operating an option scheme, not contributing to executive pensions and keeping other expenditure to a bare minimum.

- Nothing is certainly spent on investor communications beyond the annual report, the website, the occasional terse RNS and hosting shareholder meetings.

- I understand the general meeting that follows the protest votes at each AGM costs £50k to host…

Boardroom: protest votes

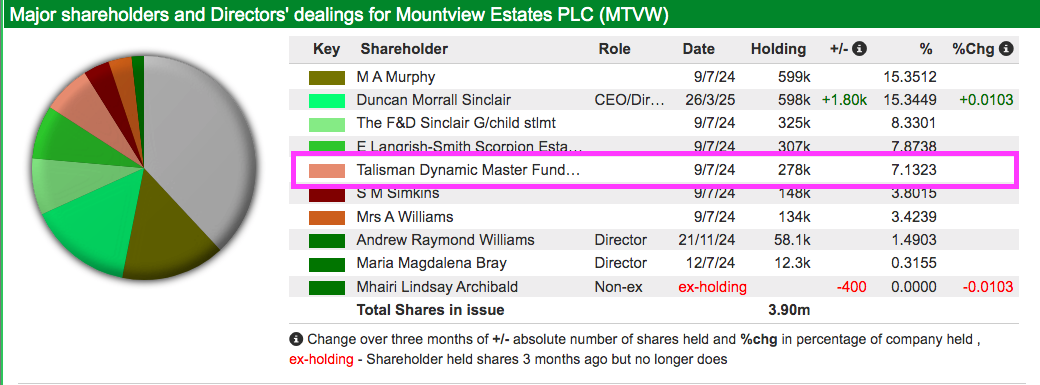

- MTVW’s shareholders fall into three camps:

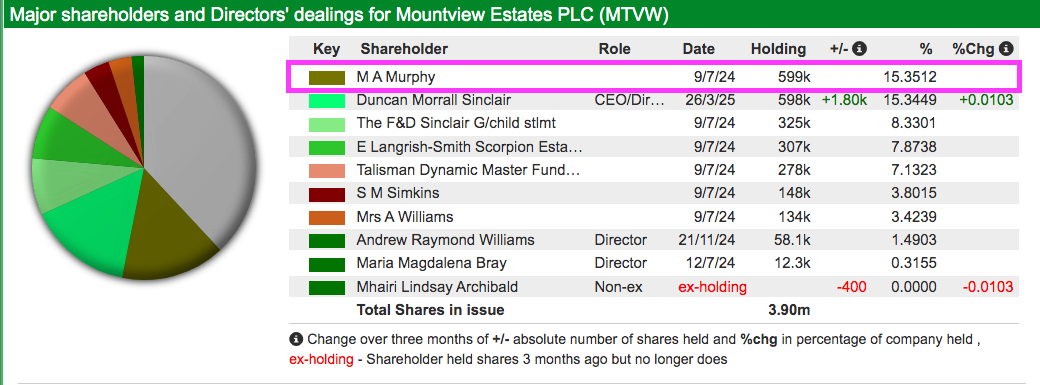

- The Sinclair family concert party, which is led by MTVW chief executive Duncan Sinclair and at the last published count controlled 50.4% of the shares;

- The Murphy family and connected parties, who claim to own 24% of the shares and whose leading shareholder is Margaret Murphy, the chief executive’s sister, and;

- Everybody else, who own approximately 25% of the shares.

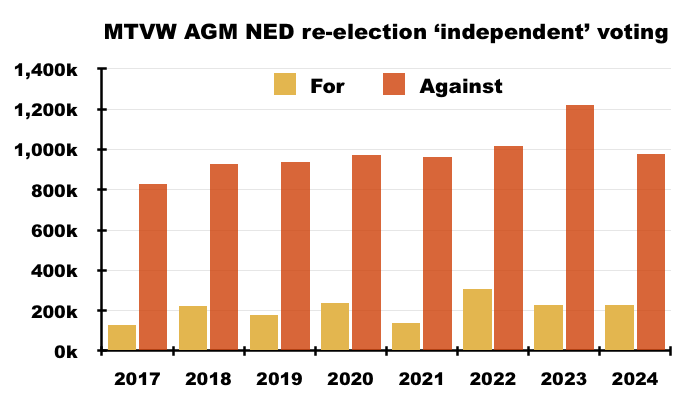

- MTVW’s last eight AGMs have witnessed c30% protest votes against:

- Re-electing certain non-execs and, recently, both the executives;

- Approving the board’s pay, and;

- Re-appointing the auditors.

- The protest votes have been led by the Murphy family and connected parties.

- I understand the Murphy family:

- Has lost the trust of the non-execs to act on the views of all shareholders, and;

- Is frustrated about a general lack of influence at board level.

- Particular grievances held by the Murphy family concern MTVW’s:

- Interpretation of the corporate-governance code concerning ‘independent’ non-execs;

- Executive and employee pay;

- Lack of transparency over the size of the concert party’s combined holding;

- Borrowing limits as set by the group’s articles of association (a disagreement seemingly dating back to 1991), and;

- Low gains realised on properties purchased following the Allsop valuation.

- The Murphy family stated during the 2021 AGM that it was no longer in direct communication with the board and would engage with the directors only through a “public forum“. I understand that policy remains in place.

- Among the attendees at the 2023 AGM was David Pears, who is a member of the Pears family that owns property group William Pears and controls a 7% MTVW stake through the family’s Talisman investment fund:

- Mr Pears is not a happy shareholder, at least judging by his 2023 AGM questions.

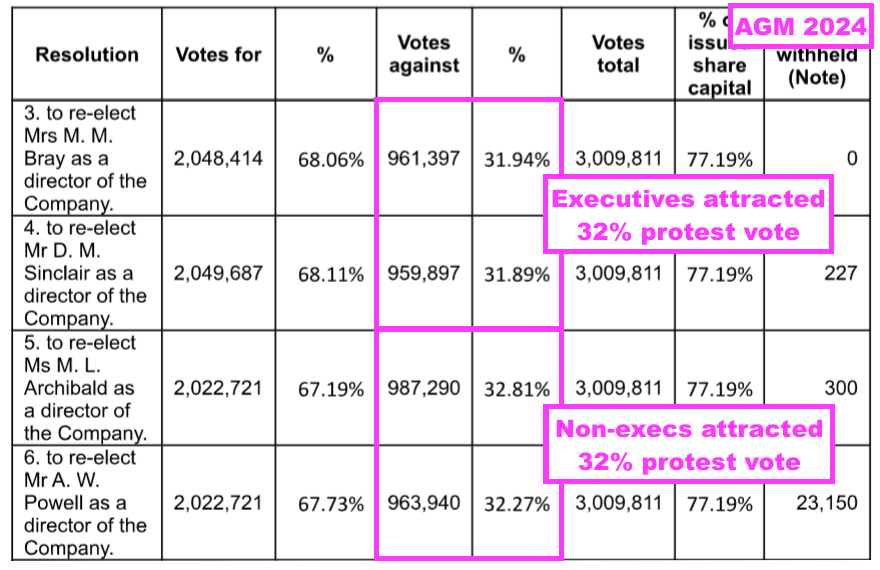

- The Murphy family, Talisman and other unhappy shareholders prevented the re-election of the independent non-execs at the 2024 AGM — and the seven prior AGMs:

- The Murphy family (and connections) and Talisman have clearly become fed-up with the executives, too, given the votes against the executives have increased from immaterial numbers to 3%, then 9% and now 32% at the last three AGMs:

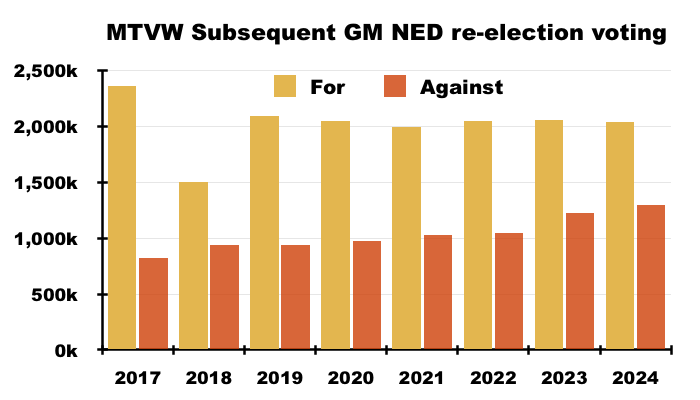

- Following each AGM, MTVW is entitled to convene a general meeting (GM) and hold a further vote to re-elect the ousted non-execs.

- The ousted non-execs have (to date) all been re-appointed at the subsequent GMs because the Sinclair family concert party can then vote on the non-exec re-elections (unlike at the AGMs, where the concert party is prohibited from voting on ‘independent’ resolutions):

- I did not attend the 2024 GM, but I understand the event was a lively affair characterised by differences of opinion between the board and the Murphy family.

- Held during November, the 2024 GM attracted almost 1.3 million protest votes — equivalent to 33% of the share count and the highest proportion since the protest votes commenced during 2017.

- Stock-market rules dictate any company incurring a 20%-plus AGM or GM protest vote has to contact the unhappy investors and publish an update to all shareholders within six months.

- Six months after the 2024 AGM, during February, MTVW announced:

[RNS February 2025] “Following the 2024 AGM, and as it has done previously, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage. The Company remains committed to shareholder engagement and we will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.”

- Six months after the 2024 GM — just last week! — MTVW announced:

[RNS May 2025] “Following the General Meeting, and as it has done previously, the Company identified, as far as possible, those shareholders who did not support the resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage, other shareholders raised matters which are under consideration by the Board and its Committees. The Board is grateful to those shareholders who took part in the engagement process and value the feedback provided. The Company re-affirms its commitment to ongoing shareholder engagement and will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.”

- The different wording about shareholder engagement within those two announcements does not appear to have any great relevance.

- After all, 16 AGM/GM protest votes since 2017 suggest engaging with the board has become a futile undertaking.

- However, the ineffective protest votes have not yet persuaded the Murphy family to sell; Companies House indicates Margaret Murphy has maintained a 500k-plus MTVW shareholding since at least 1980:

- Talisman has not announced any selling since reporting its last purchase during January 2023:

- The voting at the 2025 AGM will be intriguing following the appointment of a new non-exec…

Boardroom: new non-executive and director pay

[RNS November 2024]

“Mountview Estates P.L.C. announces that Tracey Hartley MSc MBA MRICS FTPI has been appointed as an independent Non-Executive Director of the Company, with effect from 1 January 2025. Tracey will join the Audit and Risk Committee, Remuneration Committee and Nomination Committee on appointment.

Tracey has over 25 years of expertise in residential property investment, property, and asset management across Estate, Block, and Build to Rent (BTR) sectors. She has also established a strong track record in senior leadership, strategy, and operations.

Her career includes a decade in Operations and Fund Management roles at Grainger, and she has served as the Head of Residential at The Howard de Walden Estate, JLL – The Crown Estate, and Chief Operating Officer at Cortland Europe before joining CompassRock International as Senior Director – Operations in June 2024.

Tracey has a keen focus on governance, risk, and compliance, ensuring best practices are followed across all levels of operations. Her industry-shaping roles include participating in the Government’s Private Rented Sector (PRS) Taskforce, serving as the current Chair of the British Property Federation (BPF) Residential Management Committee, being a member of the BPF Living Sectors Board and the RICS UK & Ireland World Regional Board.

Duncan Sinclair, Chief Executive Officer, commented:

“Tracey brings a wealth of relevant experience to the board. We welcome her to Mountview and look forward to working with her.”

- Ms Hartley’s “keen focus on governance, risk, and compliance, ensuring best practices are followed across all levels of operations” could make her a welcome appointment for unhappy shareholders…

- …assuming her adherence to corporate-governance “best practices” rubs off on MTVW’s board!

- Ms Hartley’s bio published by MTVW is the same as that published by her employer, but this insightful interview reveals an unconventional CV involving a weekend job at an estate agent and obtaining a degree through the Open University.

- I therefore trust Ms Hartley brings some fresh thinking and differing opinions to the board (on regular estate valuations in particular!):

- Ms Hartley is deemed ‘independent’ of the Sinclair family concert party, and she could therefore act as a conduit between the board and the Murphy family, Talisman and other unhappy shareholders.

- Recruiting Ms Hartley to succeed the aforementioned Ms Archibald has certainly taken MTVW some time. Ms Hartley was appointed on 1 January 2025, some 18 months after Ms Archibald’s standard nine-year non-exec term ended on 30 June 2023!

- No doubt Ms Hartley will be asked many questions at the 2025 AGM — not least about:

- How she intends to act as a true ‘independent’ non-exec and therefore not attract regular protest votes, and;

- MTVW’s corporate governance and whether it meets with her “best practices“.

- MTVW may put Ms Hartley’s “best practices” for governance and compliance to the test; the preceding FY listed six non-compliances against the corporate-governance code (point 19).

- Ms Hartley succeeding Ms Archibald raises the question of who will chair MTVW’s remuneration committee. The role will become vacant when Ms Archibald finally departs the board after the 2025 AGM.

- Rem-comm chair is of course a vital board position given the history of executive pay.

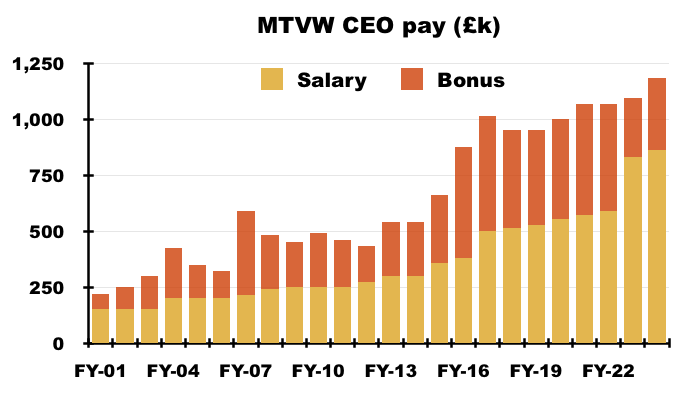

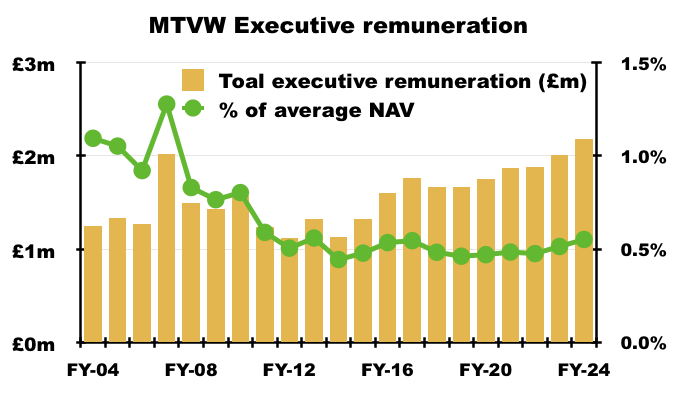

- In particular, the chief executive has collected a bonus every year since at least FY 2001, and such bonuses have pushed his total pay beyond £1m since FY 2020:

- The feeling among many AGM attendees over the years is the executives are paid generously for essentially:

- Putting vacant properties into auction;

- Collecting rent, and;

- Buying properties during recent years that may not have earned worthwhile gains on disposal.

- The executives may argue their pay has been justified over the longer term.

- Between FYs 2005 and 2024 for example, total executive pay came to £32m…

- …while NAV has advanced from £122m to £400m.

- Executive pay during the preceding FY absorbed approximately 0.5% of NAV, which does not sound a lot…

- … but starts to add up when NAV has advanced by just 8% — or 1.5% per annum — during the five years to this H1.

- Another rem-comm issue could concern non-exec fees, after the latest GM asked shareholders to approve raising the overall limit for such fees from £250k to £350k.

- The proposed £350k limit was somewhat higher than the total £194k the non-execs were paid during the preceding FY.

- Board remarks during the 2024 GM suggested the new £350k limit was not because Ms Hartley had demanded a significant fee to become a non-exec:

[GM November 2024] “A limit is a limit, it doesn’t mean [the £350k] is something… that we have to aspire to get to. It is a matter of giving enough room for the business to be run efficiently without resorting to EGMs every five minutes to change this limit…. when hopefully the £350k will prove very adequate for a number of years.”.

Valuation

- I calculate the shares could now be worth £169 were all of the group’s regulated tenancies to end immediately and the properties then sold at a fair market value.

- The following table outlines my sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less sold Allsop-assessed stock (£k) | (145,032) |

| Remaining Allsop-assessed stock (£k) | 172,619 |

| Allsop-premium-to-book | 2.10x |

| Sold-premium-to-Allsop | 1.42x |

| 513,576 | |

| Stock purchased since Sept 2014 (£k) | 287,005 |

| Possible property stock value (£k) | 800,581 |

- I have taken the estate’s September 2014 value of £318m and subtracted the (estimated) £145m book value of Allsop-assessed properties sold since that date.

- I then multiplied the £173m remainder by:

- The 2.1x ‘Allsop-premium-to-book’ multiple, and;

- The 1.42x ‘sold-premium-to-Allsop’ multiple that was realised during this H1.

- I arrived at a £514m ‘vacant possession’ value for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has acquired additional properties with a £287m book value.

- I have assumed these additional properties will be sold for their £287m book value — based upon my analysis of properties bought and then sold since the Allsop assessment.

- Adding the £514m and the £287m together gives £801m.

- This next table adjusts that £801m for 25% taxation, the £24m conventional property portfolio, the £77m debt and the residual other liabilities of £4m to give a possible NAV of £658m or £169 per share:

| Possible property stock value (£k) | 800,581 |

| Less tax at 25% (£k) | (85,239) |

| Plus other investments (£k) | 24,335 |

| Less debt (£k) | (77,300) |

| Less net other liabilities (£k) | (4,186) |

| Possible NAV (£k) | 658,191 |

| Possible NAV per share (£) | 168.81 |

- My estimated NAV sums are not perfect, and the following questions remain unanswered:

- How long will MTVW take to sell all of its properties?

- Will future house-price inflation compensate for being unable to sell all the properties immediately?

- How relevant is the 2014 Allsop assessment today?

- Will properties bought since the 2014 Allsop assessment continue to be sold close to cost price?

- Note my sums conservatively apply this H1’s 42% premium that was realised on the Allsop-valued properties. Applying the average 55% premium realised during the preceding five FYs, I arrive at a possible NAV of £694m or £178 per share.

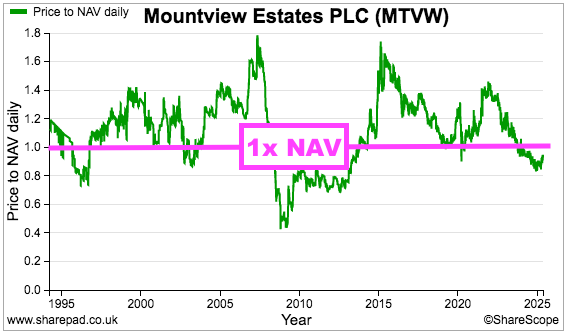

- MTVW’s shares continue to trade below NAV:

- The best time to buy should be when the market cap trades at or below NAV, at which point no future gains from any property purchases are priced into the valuation.

- What future gains could lie ahead?

- As noted earlier, the combined additional NAV and dividend return over the five years to this H1 was £140m or 38% — equivalent to a 6.6% CAGR:

- The next five years repeating that 6.6% CAGR may not enthuse prospective investors given:

- MTWV’s returns have been declining over time;

- Post-2014 property purchases appear to have realised modest gains;

- Ongoing protest votes have not persuaded the board to conduct a new Allsop-type valuation, and;

- New EPC (and other?) legislation will probably increase costs and reduce future margins.

- Perhaps a discount to NAV is actually now required for investors to generate a suitable total return.

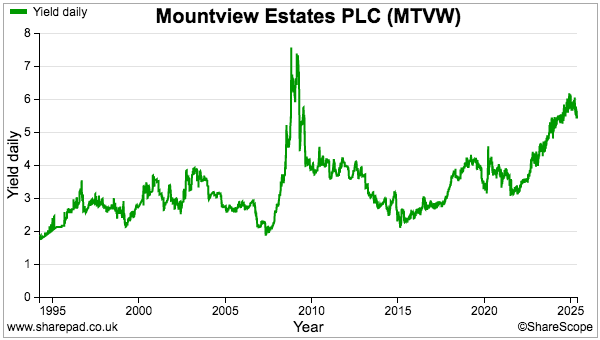

- The £97 shares offer a 6% discount to this H1’s £103 per share NAV:

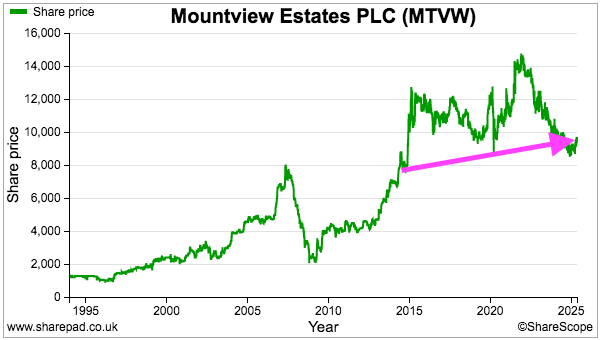

- A 6% discount appears good value, but is not quite the 13% discount that was available during Q4 2024 when I purchased more at £90.

- For further perspective, my original MTVW purchase occurred during 2011 when the £42 shares traded at a 24% discount to the then £55 per share NAV.

- For even further perspective, the shares sank to £21 at the depths of the 2008 banking crash, giving buyers a 56% discount versus the then £48 per share NAV.

- Something to consider perhaps is the chief executive’s recent share buying.

- He purchased shares at £88.50 earlier this year, including those sold by non-exec Ms Archibald:

- According to ShareScope, the chief executive previously purchased shares during 2011 at £40.50 and before that during 2009 at £23:

- The chief exec enjoys a 15%/£58m personal shareholding and does not really need to buy more shares. I therefore trust his infrequent purchases are signals for when he finds the discount to NAV irresistible.

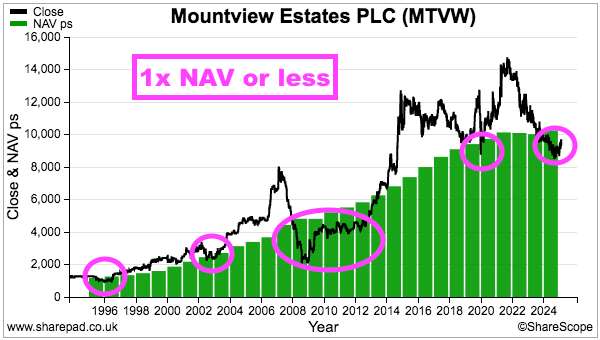

- MTVW’s shares have not always traded at a discount.

- In particular, the 2014 Allsop assessment pushed the shares to £125 during early 2015 as buyers paid a 69% premium to the then £74 per share NAV:

- Another Allsop assessment divulging further ‘hidden value’ could easily prompt a favourable price-to-NAV re-rating.

- Occasional bouts of wider market optimism can also push the share price well beyond NAV. In particular:

- Buyers at the £80 peak during 2007 paid a 75% premium to the then £46 per share NAV, and;

- Buyers at the £145 peak during 2021 paid a 42% premium to the then £102 per share NAV.

- You never know, the shares may one day trade above NAV due to a trade-sale occurring.

- When asked during the 2024 AGM about whether MTVW will continue to operate until the shrinking pool of regulated tenancies finally disappears, the chief executive hinted the group’s estate could be sold beforehand:

[AGM 2024] “We will have to consider what else to do. It could be that we just gradually pay dividends and ultimately return the capital and wind up the company in that manner. On the other hand, there may be another company that has other specialisations but is very capable of taking the rump of our portfolio, who may come in and buy that rump. We’re not very near that date yet.“

- At least future returns from today should be front-loaded by dividends:

- The illustrious ordinary payout runs currently at 525p per share and supplies a useful 5.4% income at £97.

Maynard Paton

Don’t we need to apply an appropriate discount rate to the vacant possession NAV to calculate the true NAV? A £100,000 vacant possession property is worth considerably less today if you are forced to hold it for ten years at below market rents to realise that £100,000. Perhaps their own assessment of currently buying regulated properties at 75% of vacant possession NAV is a fair discount to apply to your own calculation of £169 NAV ?

Hi Javed,

Thanks for the message.

You could apply a discount. But my calculations are based on today’s values or at least values based on recent sales within the portfolio.

So, if a property became vacant and sold today, I work out it would raise £100k. But if I am forced to hold it for ten years before sale, then I would like to think future house-price inflation will counter the time-value discount and I will end up in 10 years with a sum equivalent to £100k in today’s money. Well, that is the theory!

I recognise my sums are not perfect and would welcome any alternative calculations, especially as these shares have always been ‘cheap’ and I may have missed something.

Maynard

I had the same thought than Javed. According to your calculations, a property could be valued higher immediately after purchase. That’s certainly not the case. Let’s say, normally it would be worth 100k, but because it is subject to rent control, it is being sold for 75k. You shouldn’t value it at 100k one day later.

Rather, this is the source for future profits – or put in other words: Mountviews profits rely on your “market value NAV” being higher than the stated NAV (of historical costs).

Nevertheless, since some properties are close to being vacant (old tenant) or are already vacant and are therefore worth more than their historical acquisition costs, the market value is likely to be higher than the stated NAV.

Hi Winter

Thanks for the message.

“According to your calculations, a property could be valued higher immediately after purchase. That’s certainly not the case. Let’s say, normally it would be worth 100k, but because it is subject to rent control, it is being sold for 75k. You shouldn’t value it at 100k one day later.”

Funnily enough that is how MTVW’s board (during at least one AGM in recent years) has described how the group buys properties. It finds a regulated tenancy that could be worth £100k tomorrow without the regulated rent, and aims to pay £75k today (i.e. a 25% discount) with the regulated rent.

Of course, the property does not become available for sale the next day. But over time house-price inflation and perhaps modest rent increases should lift that £100k higher. My theory is that, once the property is sold in, say, 10 years time, the valuation achieved would be equivalent to £100k in today’s money.

The value of the properties should increase over time. In particular, the Allsop valuation conducted in Sept 2014 plus MTVW’s subsequent disclosures indicate MTVW is currently selling properties purchased before Sept 2014 at c3x their original value. Perhaps if that c3x gain is discounted back to the time of purchase, we may arrive at the equivalent of £100k versus a £75k purchase price.

Note that about a third of my £169/share valuation is based simply upon the purchase price of the properties (those acquired since Sept 2014). So I am not expecting any gains from those assets, which may prove very conservative and perhaps offsets any optimism with the other part of the calculation.

Maynard

That’s how it works. But the discount also compensates for the low rents due to the rent control. Without it, it would obviously be a bad deal – to pay the normal price for a property that yields a lower rent than a comparable one, maybe for decades. I can’t assess if the discount is maybe higher than it ought to be, due to the uncertainty of the remaining duration of the tenancy. Maybe normal private buyers shy away from that risk, while Mountview can diversify that away, like an insurance company. Maybe that’s the explanation why they were able to show such a good performance in the past with unlevered real estate, which seems very unusual.

Due the low rental income as a percentage of book value (or NAV), only a small percentage of the earnings and the dividend is covered by the rents. They rely on sales above book value to maintain earnings and the dividend. That’s no problem, it’s just their business model! But one should not double count that. Well, at least to a certain degree.

As far as I have understood, they could get a nice premium to book value if they sold all of their properties immediately – given that there was a instant buyer for all of them. That would indeed be an extra upside.

You deduct tax in your NAV calculation. That’s not wrong for the liquidation value.

But if a buyer takes over the entire plc, then there is no tax, right? That’s why there is another version of NAV which takes that into account. So for a buyer who wants to hold the real estate portfolio and not liquidate it, the NAV is even higher.

Hi Winter,

Yes, this tax angle seems correct. I have only really considered a liquidation valuation as the likelihood of a buyer has always appeared very remote.

Maynard