30 August 2024

By Maynard Paton

H1 2024 results summary for FW Thorpe (TFW):

- A 5% dividend advance was the highlight of this rather subdued H1, as revenue gained 1% and profit fell 2% after customers apparently finished (very) early for Christmas.

- Divisional performances were extremely mixed, with Dutch profit up a super 25%, Thorlux’s profit sinking a disappointing 8%, Zemper’s profit still to show its full potential and Ratio’s losses becoming even larger.

- The accounts remain in good shape, showing an acceptable 15% group margin, healthy net cash of £29m and a very welcome stock reduction, although Ratio has (probably) required extra funding and the pension scheme may one day follow suit.

- The roles of chief executive and finance director have been combined, which alongside a slimmed-down board raises concerns about executive technical expertise, a concentration of leadership power and future M&A that may not be adequately challenged.

- A possible 20x P/E seemingly reflects TFW’s distinguished operating history, future “synergy initiatives” and continual demand for energy-saving lighting rather than the group’s modest near-term prospects, doubts about the re-jigged board and the risk of an aggressive acquisition strategy. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux and SchahlLED

- Netherlands

- Zemper

- Ratio Electric

- Other companies

- Financials: Thorlux versus non-Thorlux

- Financials: balance sheet and cash flow

- Financials: pension scheme

- Boardroom

- Valuation

News links, share data and disclosure

- Interim results for the six months to 31 December 2023 published 14 March 2024;

- Circular published 22 March 2024, and;

- Directorate changes published 23 May 2024.

- Share price: 375p

- Share count: 118,935,590

- Market capitalisation: £446m

- Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Develops professional lighting systems with a long-established reputation for high product quality, leading technical innovation, first-class service and sustainable manufacturing processes.

- Management overseen by family non-execs who boast decades of board experience, steward a 43%/£191m shareholding and occasionally favour special payouts.

- Conservative accounts display useful operating margins, substantial cash reserves, consistent working-capital management and illustrious rising dividend.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary

Revenue, profit and dividend

- Remarks within the preceding FY that acknowledged this H1 had commenced with “slightly lower” orders…

[FY 2023] “As a whole, the outlook from the sales teams is positive. At the start of this new financial year, orders are slightly lower than in the same time period last year, and there is some evidence of projects slowing. Costs are under control and some margin improvements have been made, which will provide an improved return on sales. Revenues, however, are expected to see slower growth than in the recent few years.”

- …followed by an AGM statement that reiterated subdued progress…

[AGM 2023] “Since the beginning of the new financial year, orders and revenue are marginally ahead of the same period last year ‐ there being some ups and downs across the Group. We expect half‐year results to be similar to last year.

The sales teams remain positive, the pipeline is good but projects seem a little slower to materialise than in past years.“

- …had already forewarned these results would not be spectacular.

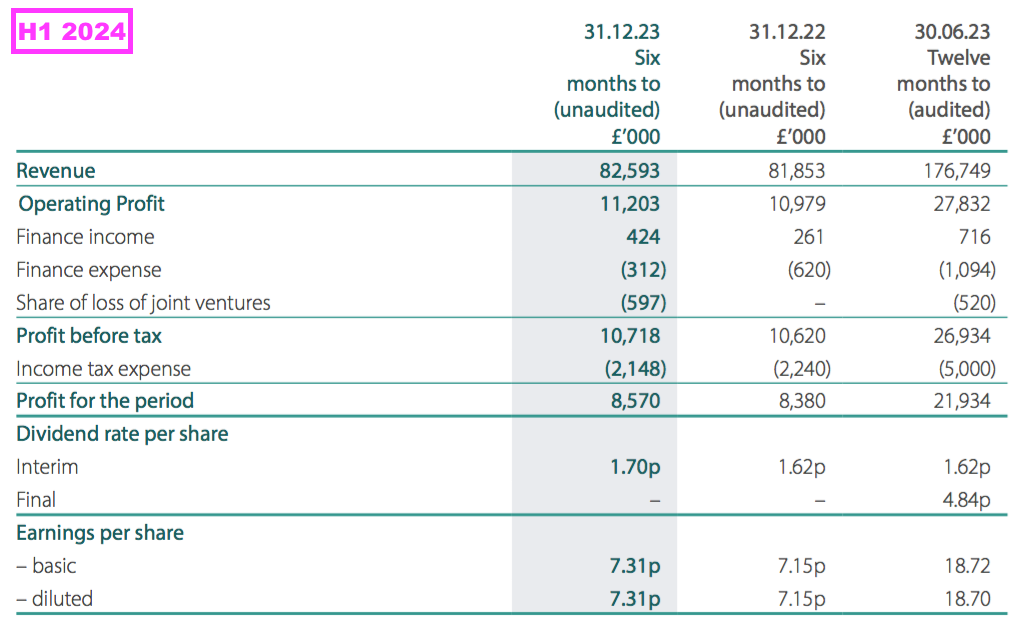

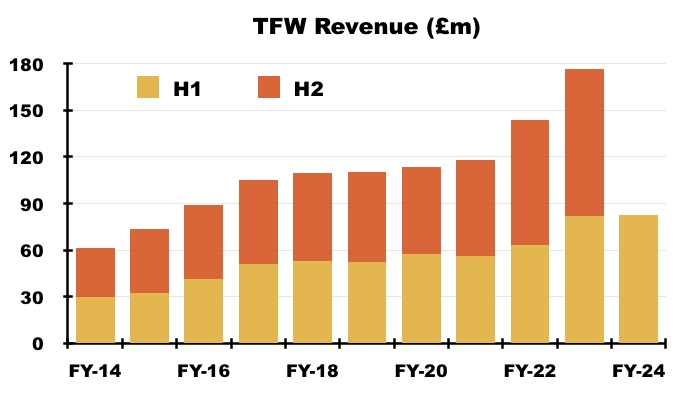

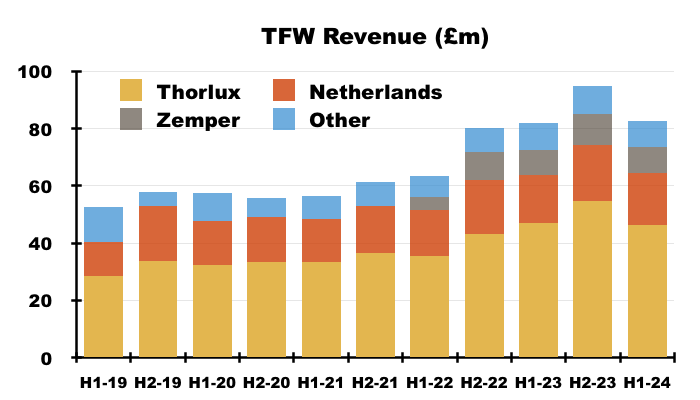

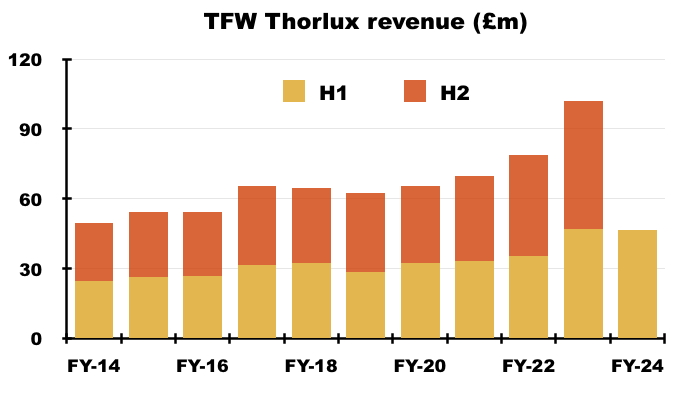

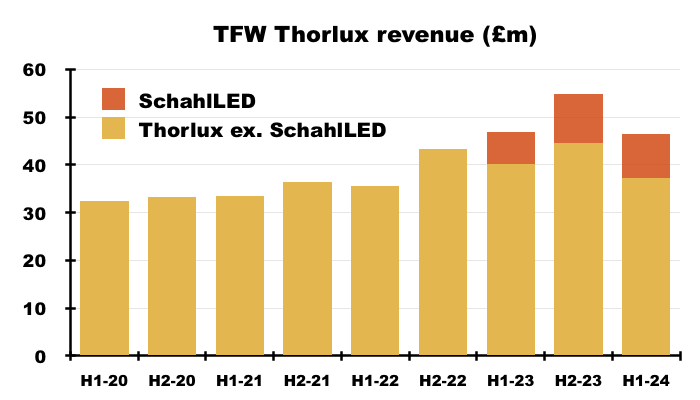

- A new H1 record was nonetheless set for revenue, which inched 1% higher to £83m:

- The top line was supported by SchahlLED, which was purchased during September 2022 and contributed for three months during the comparable H1 but six months during this H1.

- Excluding SchahLED, H1 revenue declined 2% to £73m (see Thorlux and SchahlLED).

- TFW appeared to blame the lacklustre revenue performance on “very early” festive celebrations…

“It seems that customers finished for Christmas very early: December was particularly slow across all parts of the Group, thus suppressing results at the half year point when compared with the prior year.

- …which judging by the preceding FY’s remarks seemed to commence during October.

- At least the subsequent H2 started well:

“I am pleased to say that trading bounced back with a vengeance in January, giving the Group a good start for its run-in to the full year.”

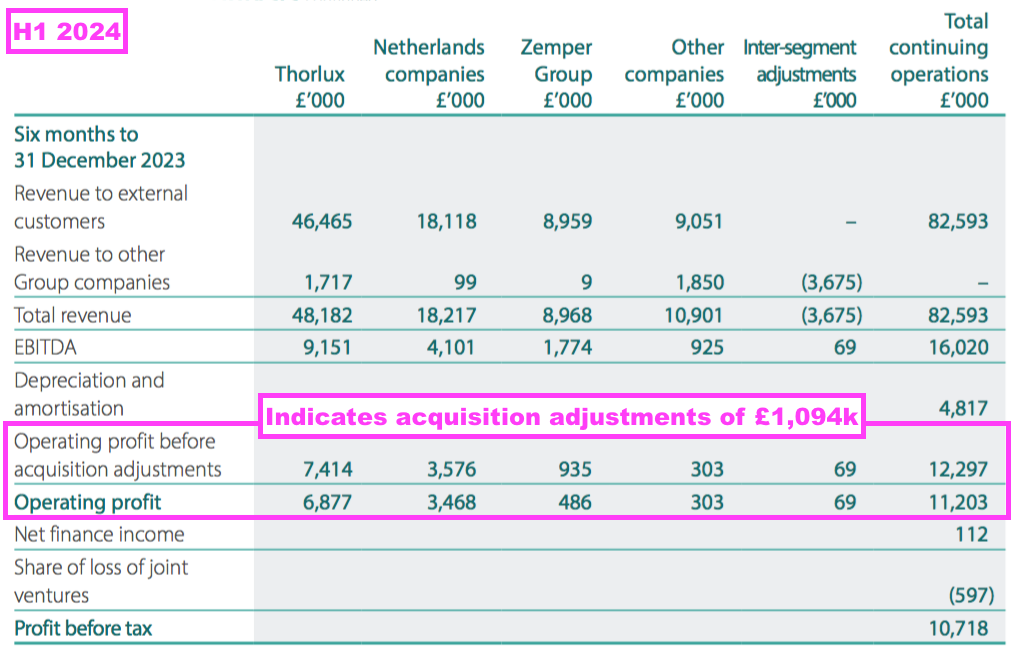

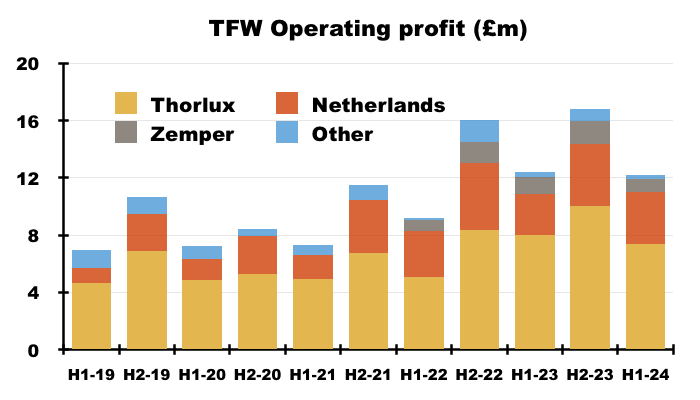

- TFW’s statutory operating profit includes the amortisation of acquired intangibles as well as (I believe) changes to acquisition earn-out provisions:

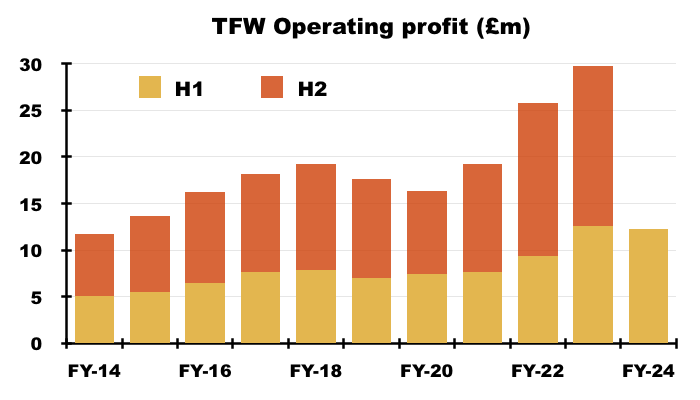

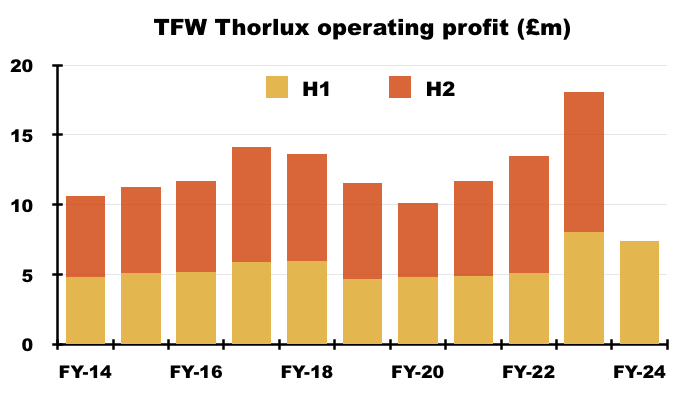

- Exclude these acquisition adjustments, and H1 operating profit declined 2%:

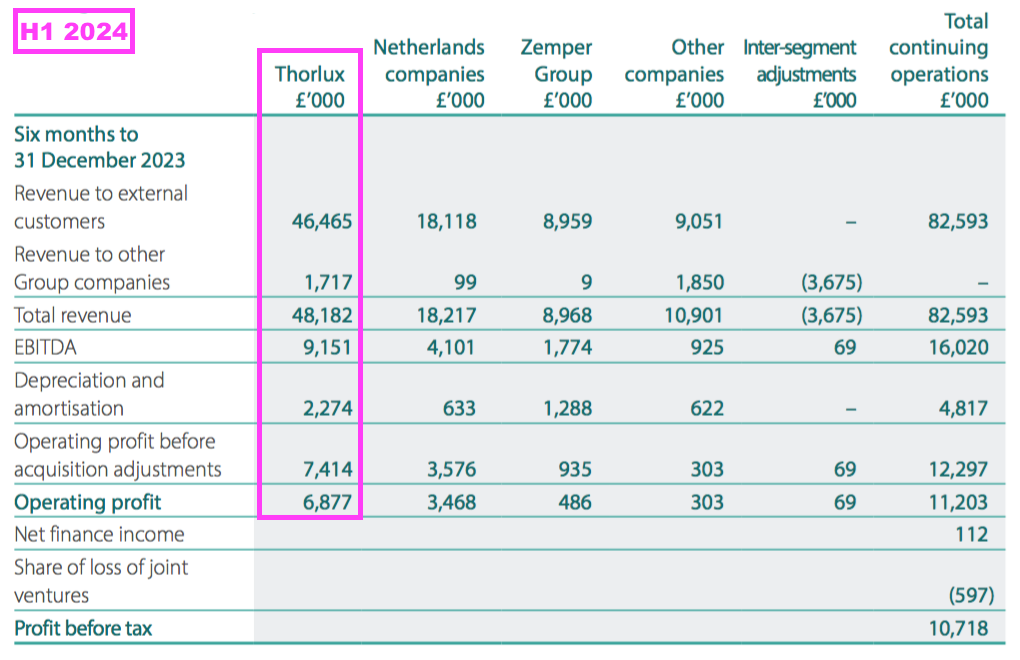

- Divisional performances were extremely mixed.

- Thorlux without SchahlLED suffered a reversal in fortunes, the Dutch operations enjoyed a strong six months, Zemper has still to show its full potential while the various Other subsidiaries remain a sideshow:

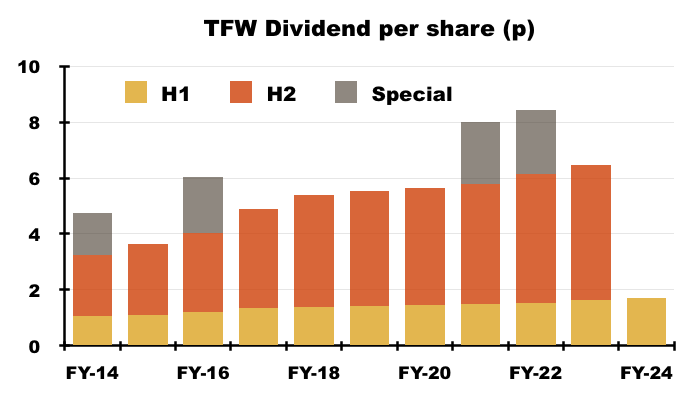

- The only headline measure definitely moving in the right direction was the dividend, which was lifted 5%:

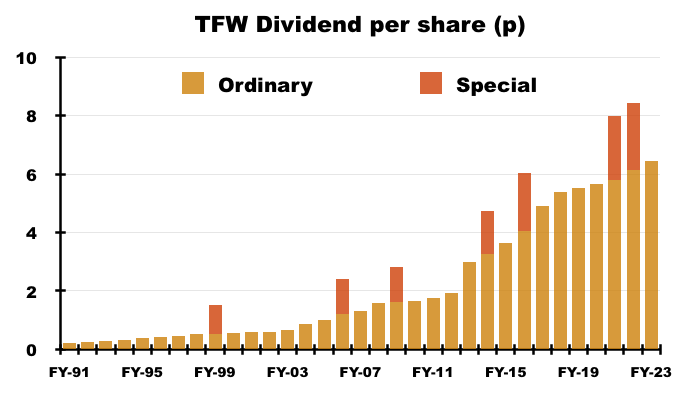

- The ordinary dividend looks on course for its 22nd consecutive annual increase and has not been cut since at least 1991:

- The ordinary dividend has expanded at an 8% CAGR during the last 10 years.

- Special payouts were declared during FYs 2021 and 2022, but understandably ceased following significant expenditure on SchahlLED, Zemper and joint-venture Ratio Electric.

Thorlux and SchahlLED

- Thorlux manufactures a wide range of professional lighting equipment — most notably the SmartScan system — and represents approximately 60% of the group:

- The division has operated since 1936 and attracts customers through first-class products, manufacturing excellence and high-quality service (point 4) that provide buyers with “peace of mind” (point 7).

- Buildings recently employing Thorlux include:

- Thorlux’s lighting offers a “low total cost of ownership“, with modest maintenance requirements, extended working lifetimes and, increasingly, significant energy efficiency (point 7):

- Thorlux first manufactured energy-saving lighting during 1994 (point 3), has undertaken a carbon-offsetting scheme since 2009 and harbours an ambition to reach ‘net zero’ by 2040 (point 15e).

- Some 31% of this H1’s word-count was devoted to the “road to net zero” and efforts to offset emissions and reduce gas usage.

- Emphasising Thorlux’s ‘green’ credentials, this H1 claimed a “unique approach to sustainability“:

“In Spring 2024, some interesting patent-applied-for products are being launched. These new products have a unique approach to sustainability, being 3D machined from oak which is harvested from sustainable European forests. (Hopefully, one day, the Group will be able to use its own wood from its sustainable forests.)“

- Thorlux launched the “patent-applied-for products” — branded Acorn — after this H1. These new lights are housed in wood and have “achieved an industry-leading [‘circular economy’] TM66 score of 3.1, which has been verified as the highest published score of any luminaire under the LIA/CIBSE certification scheme TSD-012 to date.”:

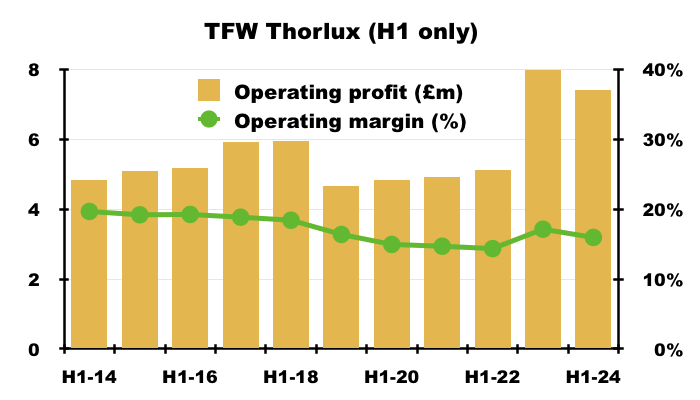

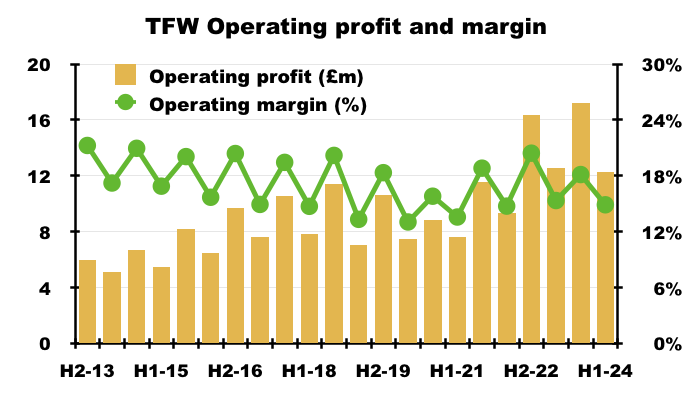

- Despite the sustainability push, this H1 witnessed Thorlux’s revenue decline 1% to £46m and operating profit (before acquisition adjustments) fall 8% to £7.2m:

- Thorlux’s performance was disappointing given SchahlLED was acquired during the comparable H1 and amalgamated into the division.

- TFW disclosed SchahlLED revenue was £9.1m during this H1…

“Included in the Thorlux segment are additional revenues from SchahlLED of £9.1m and operating profit of £0.5m.”

- …versus £6.7m during the three months of ownership within the comparable H1:

“Included in the Thorlux segment are additional revenues from SchahlLED of £6.7m and operating profit of £0.4m.“

- Excluding SchahLED, Thorlux revenue therefore dropped 7% to £37m:

- Thorlux started working with SchahlLED during 2019, after which the German lighting installer quickly became TFW’s largest customer before being acquired by TFW:

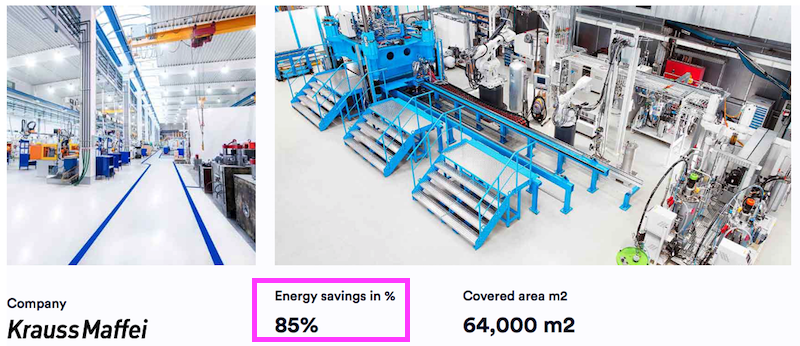

- A SchahlLED case study involving KraussMaffei reported an 85% reduction to energy costs through installing Thorlux lighting. The customer apparently enjoyed a “high return on investment with a payback period of less than 3 years“:

- This H1 claimed Thorlux’s margins had improved:

“The Group has, overall, managed these inflationary pressures well, with Group operating margins maintained; Thorlux and Lightronics, in particular, show margin improvements.“

- Thorlux’s margins ought to have improved given the division now benefits from selling direct into Germany through SchahlLED.

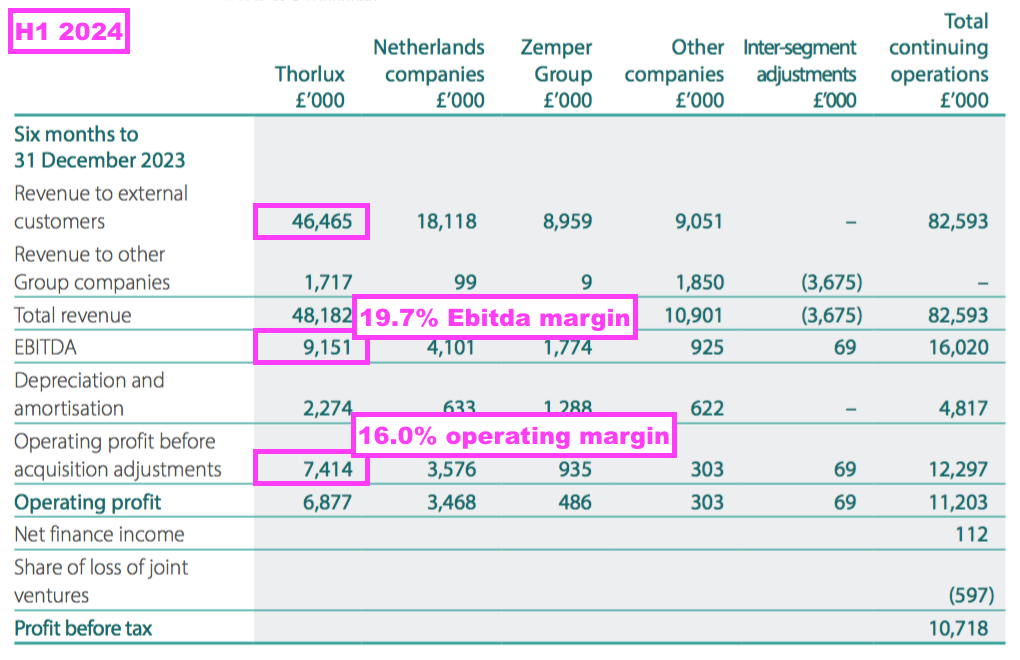

- Mind you, the divisional figures did not entirely show Thorlux’s margins improving:

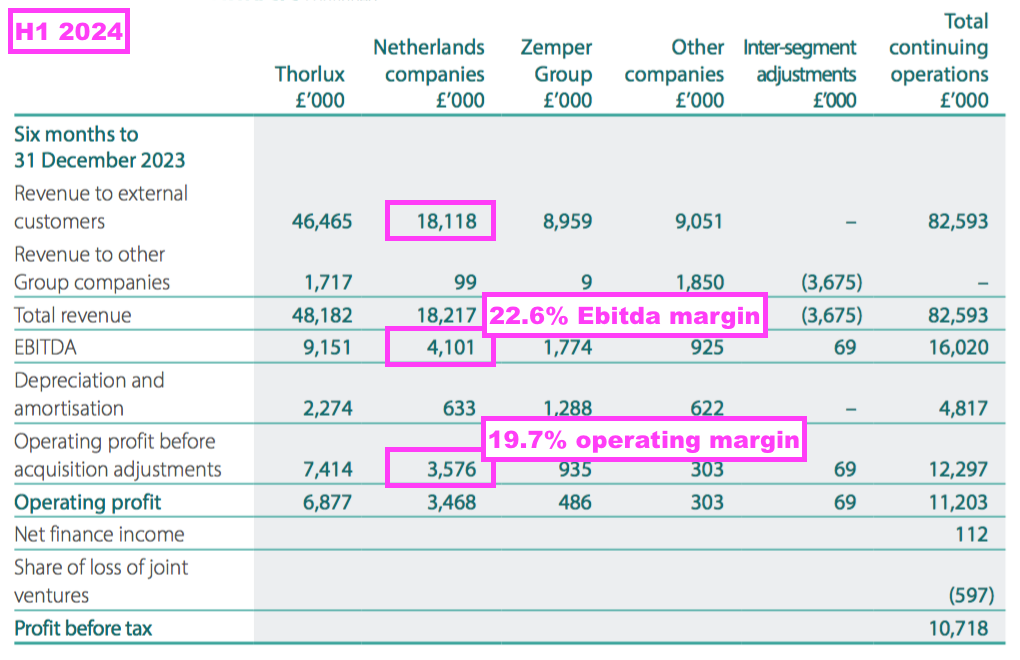

- True, this H1’s Thorlux Ebitda margin was 19.7% versus 18.6% for the comparable H1.

- But this H1’s Thorlux operating margin was 16.0% (before acquisition adjustments) versus 17.1% (before acquisition adjustments) for the comparable H1.

- Note that Thorlux’s margins could be calculated by:

- Including or excluding revenue to other group companies;

- Including or excluding SchahlLED, and;

- Including or excluding acquisition adjustments…

- …to give a wide permutation of margin outcomes.

- This H1’s 16.0% divisional margin was within the 14-17% H1 range witnessed since H1 2019…

- …but was a few percentage points below the 18%-plus scored regularly up to H1 2018.

- This H1 did not disclose anything about acquiring the remaining 20% of SchahlLED.

- The preceding FY stated TFW was set to pay €7.5m/£6.6m for the remaining 20% to take the total payment to €22.1m/£19.5m:

[FY 2023] “On 23 September 2022, the Group acquired 80% of the share capital and hence control of Lumen Intelligence Holding GmbH, a company that holds 100% equity interest in SchahlLED Lighting GmbH, a turnkey provider of intelligent energy saving lighting products for the industrial and logistics sectors. The company was acquired for an initial consideration of €14.6m (£12.9m). There is a fixed commitment to acquire the remaining shares, based on current best estimates, a further €7.5m (£6.6m) could be payable, which is subject to future performance conditions.”

- The original acquisition announcement said the SchahlLED earn-out would be based upon Ebitda generated during the preceding FY:

[RNS 2022] “FW Thorpe has paid an initial consideration of €14.6m (circa £12.8m) and could pay an additional amount to be determined by SchahlLED’s EBITDA performance in the year ending 30 June 2023.“

- My interpretation of the following text from the preceding FY…

[FY 2023] “Included within other payables are commitment to purchase the remaining outstanding shares (redemption liability and contingent consideration) in Electrozemper S.A. of €12,623,000 (£10,853,000) and Lumen Intelligence Holding GmbH of €7,508,000 (£6,455,000). Of these amounts €6,248,000 (£5,372,000) is included in current liabilities and €13,883,000 (£11,936,000) in non-current liabilities.”

- ...is that most or all of the final 20% consideration will be paid during FY 2025.

- My calculations from the preceding FY implied the £19.5m mooted consideration for SchahlLED equated to possible Ebitda multiple of less than 5.

Netherlands

- TFW’s Dutch businesses — Lightronics and Famostar — represent approximately 30% of group profit.

- Lightronics manufactures mostly street lighting and was acquired during FY 2015 for an initial £8.3m that included a £1.9m debt repayment.

- Famostar manufactures mostly emergency lighting and was acquired during FY 2018 for an initial £6.3m:

- A £15m earn-out payment during FY 2022 took the total Dutch acquisition cost to £30m.

- Both Lightronics and Famostar appear to have performed well within TFW.

- Aggregate Lightronics/Famostar revenue for the preceding FY was £36m versus less than a combined £18m at the time of their purchases.

- Aggregate Lightronics/Famostar operating profit (before acquisition adjustments) for the preceding FY was £7.2m versus a combined £2.3m at the time of their purchases.

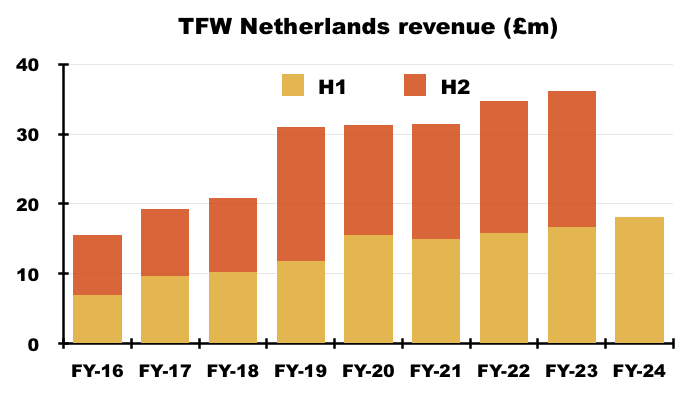

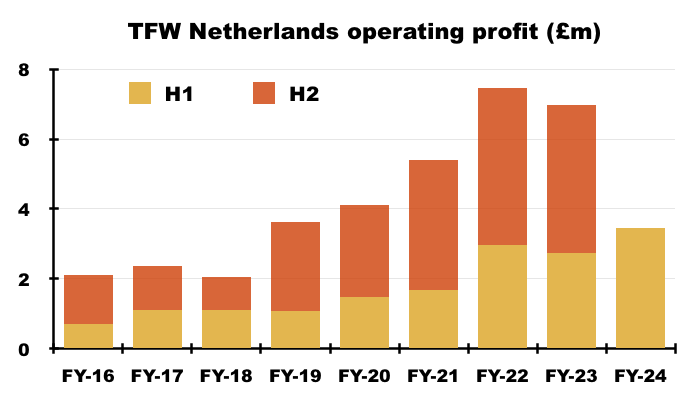

- Following a weaker performance during the preceding FY, the Dutch businesses reported much better H1 progress to set H1 Dutch records for both revenue and operating profit.

- H1 Dutch revenue increased 8% to £18m and lifted H1 Dutch operating profit (before acquisition adjustments) by 25% to £3.5m:

(Famostar acquired during H1 2018 but reported within Netherlands from H2 2019)

- TFW hinted that progress at Lightronics was responsible for the super H1 profit advance:

“The Group has, overall, managed these inflationary pressures well, with Group operating margins maintained; Thorlux and Lightronics, in particular, show margin improvements.“

- The Dutch H1 operating margin (before acquisition adjustments) was a healthy 19.7% and, unlike Thorlux, did improve versus the comparable H1 (17.0%):

- The Dutch H1 Ebitda margin improved from 19.1% to 22.6%, too.

- Recent project wins in the Netherlands include:

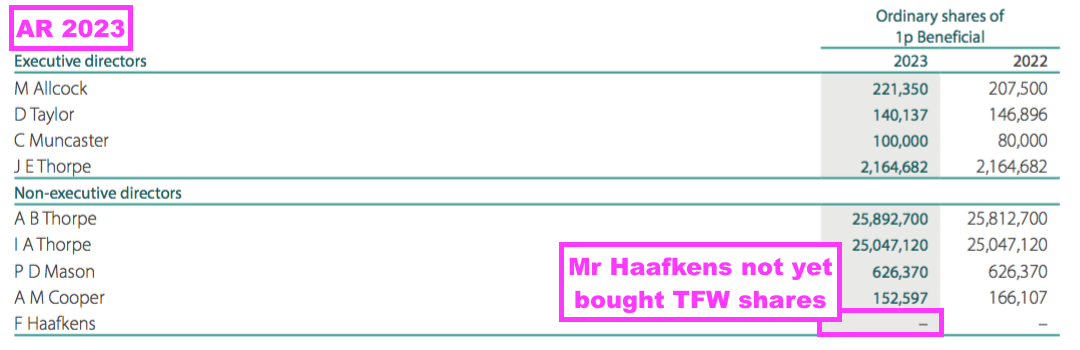

- TFW commendably widened its boardroom talent during October 2022 after appointing Frans Haafkens as the group’s “first recognised independent” non-executive:

- Mr Haafkens has worked with TFW since TFW bought Lightronics from his private-equity group during FY 2015.

- Mr Haafkens’ investment firm co-purchased Famostar with TFW during FY 2018, and bought a majority stake in Ratio Electric a year before TFW bought a 50% stake during December 2021 (see Ratio Electric).

- I expect Mr Haafkens’ “hands-on” private-equity approach can assist TFW with further acquisitions… although he has yet to identify the investment potential of TFW’s shares:

- The past year or so has seen TFW’s main board slimmed down from nine to six directors, which may allow Mr Haafkens to exert greater influence over the group’s direction.

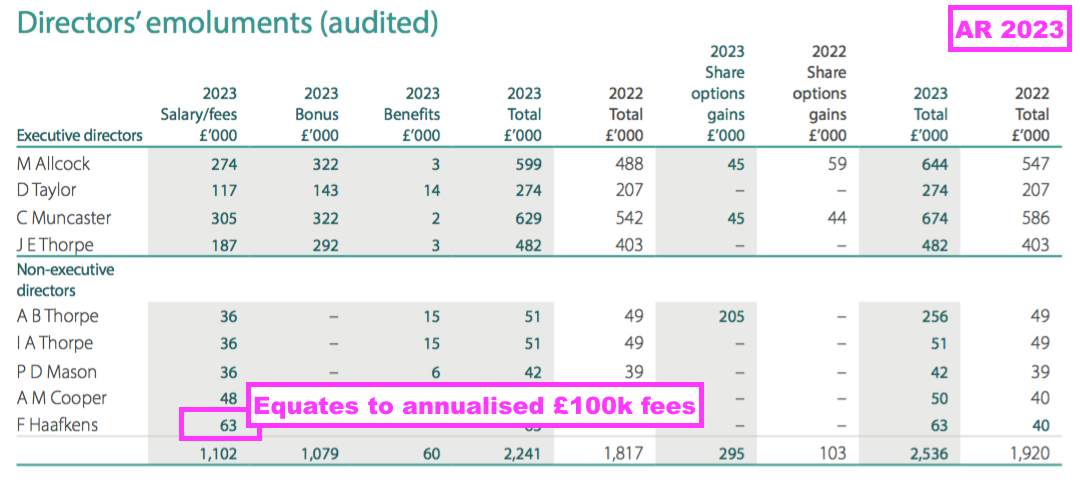

- Mr Haafkens’ £63k non-exec fees for FY 2023 equate to an annualised £100k…

- …which is at least twice as much as the fees for the other non-execs, and suggests TFW was keen to recruit Mr Haafkens to the board (see Boardroom).

Zemper

- Encouraged perhaps by the success of the Lightronics and Famostar acquisitions, TFW purchased Spanish emergency-lighting specialist Zemper during October 2021:

- Prominent buildings employing Zemper’s lighting include:

- A further 13.5% was purchased for £5.3m during the comparable H1:

[H1 2023] “On 12 September 2022, the Group purchased a further 13.5% of the share capital of Electrozemper S.A. with a cash payment of £5.3m (€6.1m), as part of its commitment to acquire the remaining shares.“

- Another 13.5% was then purchased for £4.3m during this H1:

“On 3 October 2023, the Group purchased a further 13.5% of the share capital of Electrozemper S.A. with a cash payment of £4.3m (€5.0m), as part of its commitment to acquire the remaining shares.“

- Paying £1m less for 13.5% during this H1 versus the comparable H1 suggests Zemper’s performance has not been encouraging.

- The preceding FY implied below-par trading within Zemper’s domestic Spanish market (point 11a), and this H1 suggested better sales were still registered elsewhere:

“Zemper improved export revenues to France and Belgium.“

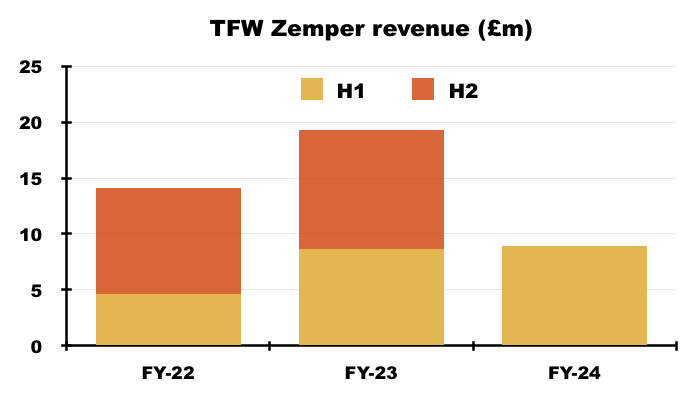

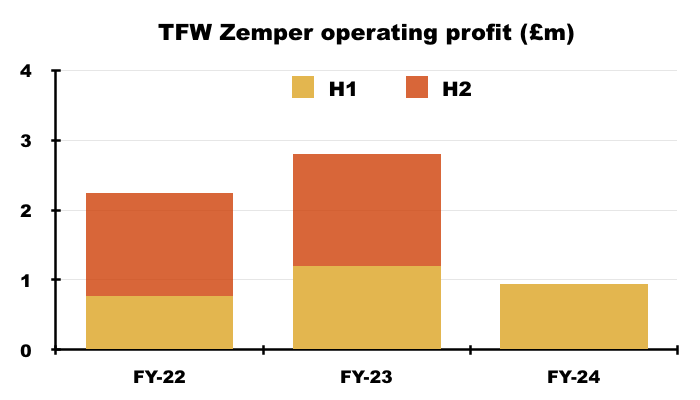

- Although Zemper’s H1 revenue increased 3% to £9m, H1 operating profit (before acquisition adjustments) dived 22% to £0.9m:

- The preceding FY suggested Zemper’s “synergy projects” might bear fruit during FY 2024:

[FY 2023] “Synergy projects continue, and the Zemper team has added some significant emergency lighting knowledge and technical expertise to the Group. Projects include in-sourcing of troublesome plastic components, standardisation of product offerings across multiple territories, and continual development of shared product ideas. These synergies take time to implement, but the Group expects to see some benefit later in the new financial year.”

- Albeit more than two years after the Zemper purchase, this H1 confirmed the first “synergy initiative” had become commercial:

“Group product synergy initiatives have advanced, and the Group’s first shared technology emergency range, designed and manufactured by Zemper, is due for launch this summer.”

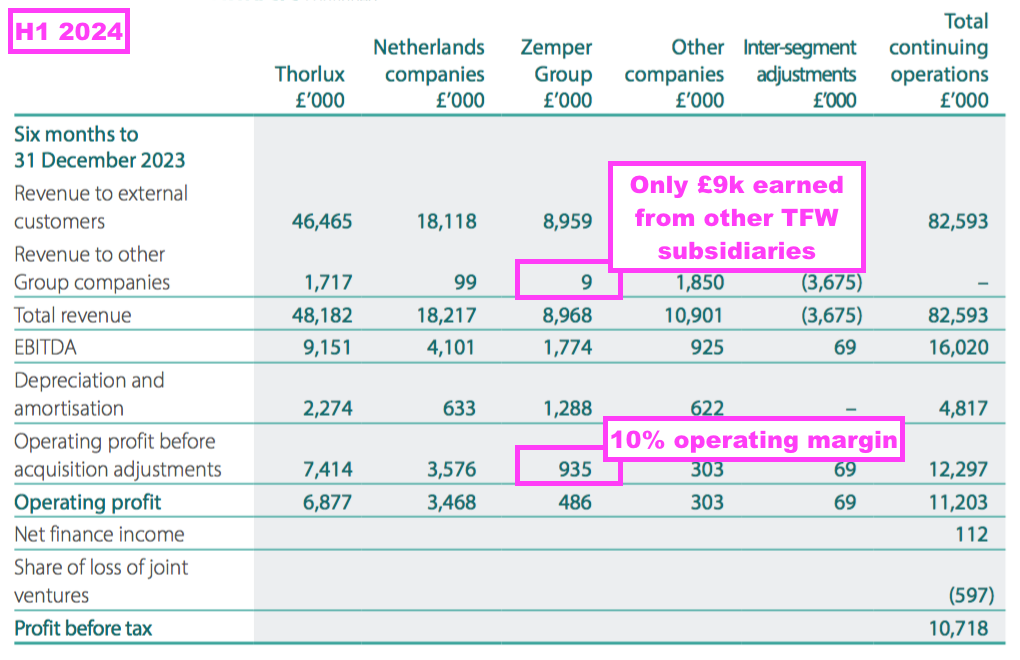

- Synergies to date appear very limited. This H1 indicated Zemper earned six-month revenue of only £9k from other TFW operations:

- Zemper’s H1 margin of 10% (before acquisition adjustments) — versus 14% during the comparable H1 and 17% during H1 2022 — did not indicate obvious synergies either.

- I would like to think Zemper’s 10% operating margin (before acquisition adjustments) will soon improve and the subsidiary can represent much more than the present c10% of the wider TFW group.

- Indeed, the preceding FY included intriguing commentary about Zemper possibly developing the SmartScan equivalent for emergency lighting:

[FY 2023] “Some significant technological projects are underway to harness Zemper’s design, technical and manufacturing know-how. These projects will support the Group’s electronic operations and its aspirations for premium connected technology in the emergency-lighting sector.”

- Certainly TFW’s outlay to purchase Zemper suggests a fair amount of successful product development is expected from the Spanish subsidiary.

- To date TFW has paid £30.5m (£19.9m + £1.0m + £5.3m + £4.3m) for 90% of Zemper, and the latest 13.5% stake acquired for £4.3m implies the remaining 10% may be acquired for £3.2m to take the total Zemper purchase to £33.7m.

- A £33.7m total purchase versus TFW’s trailing twelve-month group operating profit (before acquisition adjustments) of nearly £30m makes Zemper a very significant acquisition.

- Zemper produced an aggregate £4.2m Ebitda during the preceding H2 and this H1, which values Zemper at 8 times Ebitda based upon a £33.7m total purchase price.

- 8 times Ebitda does not seem outrageous, but is higher than my estimated sub-5 times multiple paid for SchahlLED and what is now sub-4 times paid for Lightronics/Famostar.

- Zemper’s higher valuation may reflect the subsidiary’s “self-sufficient” factory…

[FY 2023] “Zemper’s facility in Spain is a credit to its founding family’s professionalism. The company is very self-sufficient, with ownership of all its intellectual property, and with its own laboratory test facilities and state-of-the-art manufacturing equipment.”

- …and/or the 15-year longevity of acquired ‘customer relationships’ (point 31), which suggests loyal clientele and reliable orders.

- I am hopeful the forthcoming FY 2024 results will outline Zemper’s progress and potential in greater detail:

Ratio Electric

- Ratio Electric is headquartered within the Netherlands and develops electric-vehicle charging systems:

- Electric-vehicle charging is a departure from TFW’s lighting speciality. At the time of the Ratio investment, TFW said:

[RNS 2021] “This is an exciting opportunity for the Group. FW Thorpe’s know-how in electrical engineering, manufacturing and lighting, combined with Ratio’s experience in electrical vehicle charging will allow the introduction of new products into the UK market as well as supporting growth in Ratio’s existing markets.

We see similarities in technology and engineering skills, giving the Group the opportunity to diversify into new areas of engineering with high growth potential.”

- Ratio’s “high growth potential” seems only to have brought high costs.

- TFW acquired 50% of Ratio during December 2021 for £5.8m, with a loan note issued for £0.9m “to help fund the development of [the] business”.

- The preceding FY then revealed the loan note had increased to £1.3m, with a further £1.3m loan note issued to Ratio’s UK operation.

- Issuing extra loan notes was not encouraging, and sure enough Ratio recorded a £1m loss for the preceding FY:

[FY 2023] “In the year to 30 June 2023, the joint venture, Ratio Holdings B.V. generated a loss after tax of €1,199,000 (£1,041,000) (2022: profit after tax of €683,000 (£588,000)).

The Group has recognised its 50% share of loss of €599,000 (£520,000) (2022: profit of €342,000 (£290,000)) in the Income Statement, less costs in the parent company of £nil (2022: £62,000).”

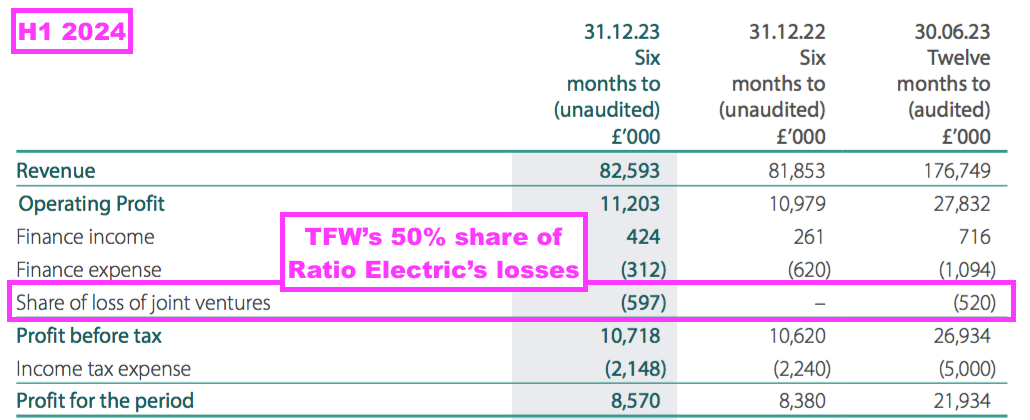

- Somewhat ominously, TFW registered a £597k loss from Ratio for this H1…

- …which means the annualised run-rate of Ratio losses now exceeds £2m.

- This H1’s Ratio commentary noted improved UK sales but also acknowledged ongoing losses:

“In recent weeks, Ratio sales in the UK have started to gather some momentum, especially for the IO7 illuminated post; however, the UK and the Netherlands are loss making in these early days whilst investment is made in improved technology to satisfy market requirements.”

- I interpret “to satisfy market requirements” to mean Ratio’s products are not yet resonating with customers.

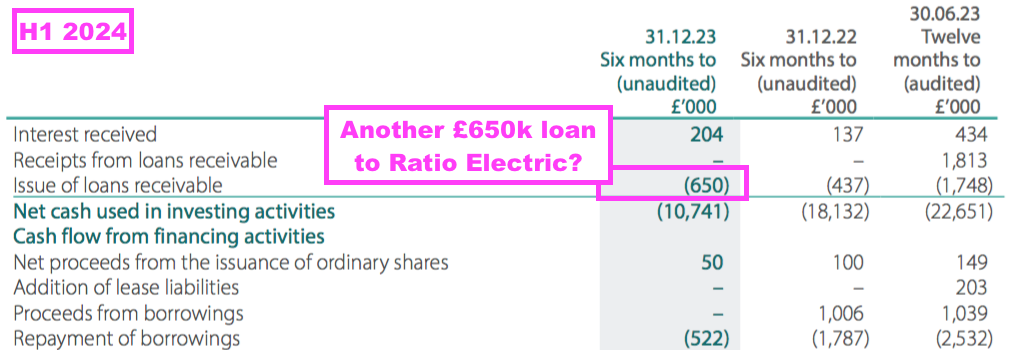

- This H1’s cash flow revealed the issue of an extra £650k loan note:

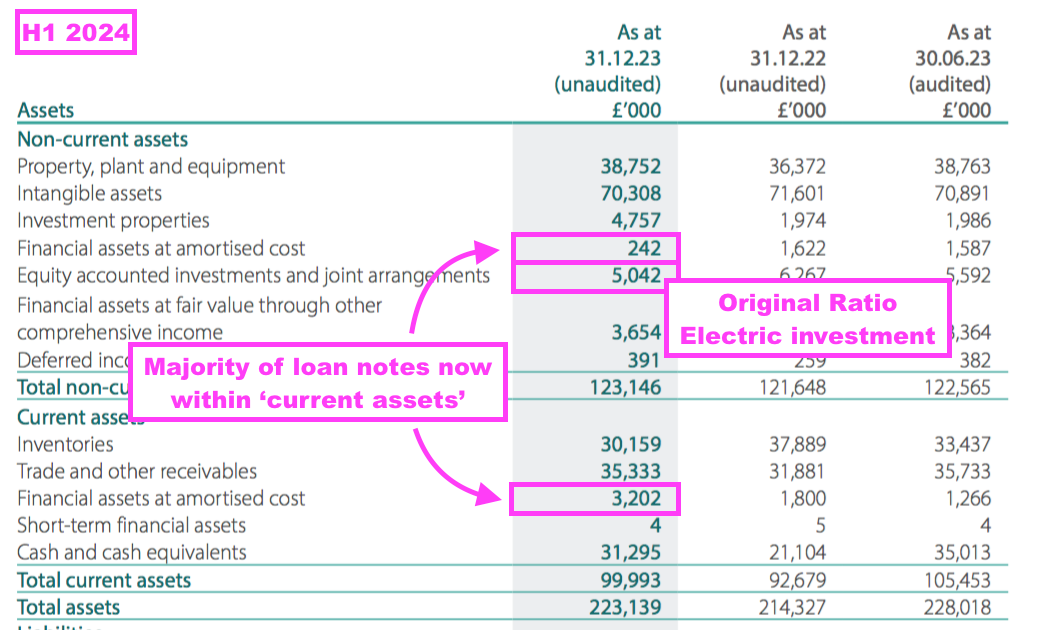

- I speculate that £650k loan note is a further advance to Ratio, with total loan notes to Ratio perhaps now standing at c£3.3m.

- This H1 saw the vast majority of the loan notes become current assets…

- …which suggests almost all of Ratio’s notes are due to be repaid (or refinanced?) during H2 2024 and/or H1 2025.

- After registering the aforementioned H1 £597k loss, TFW’s Ratio equity investment is carried presently at £5.0m.

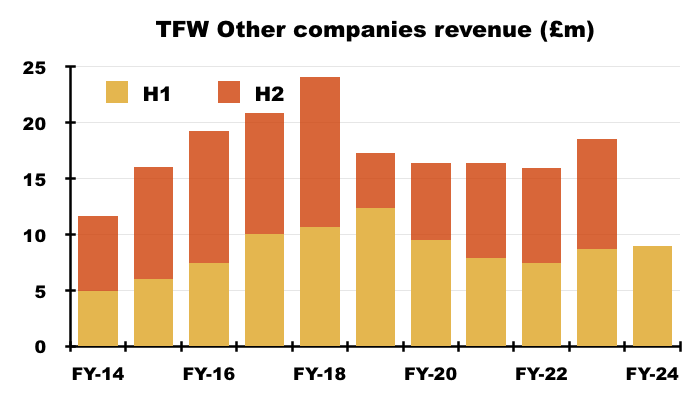

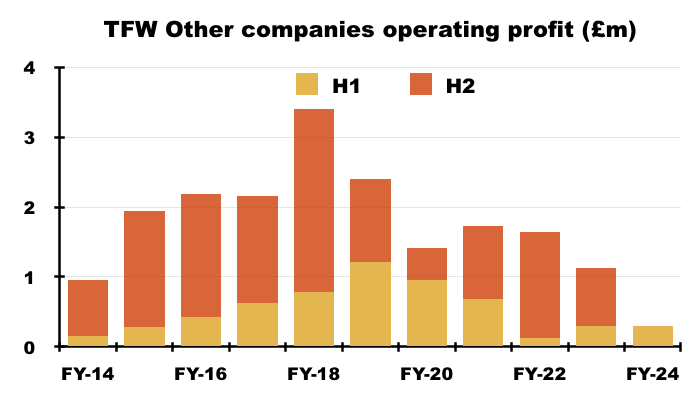

Other companies

- TFW’s Other companies consist of:

- TRT Lighting, which supplies lighting for roads and tunnels, and earns revenue of approximately £10m;

- Philip Payne, Solite and Portland, which between them supply emergency lighting, cleanroom lighting and shop lighting to earn combined revenue of approximately £11m, and;

- A handful of overseas Thorlux offices.

- None of these Other subsidiaries warranted a mention within this H1.

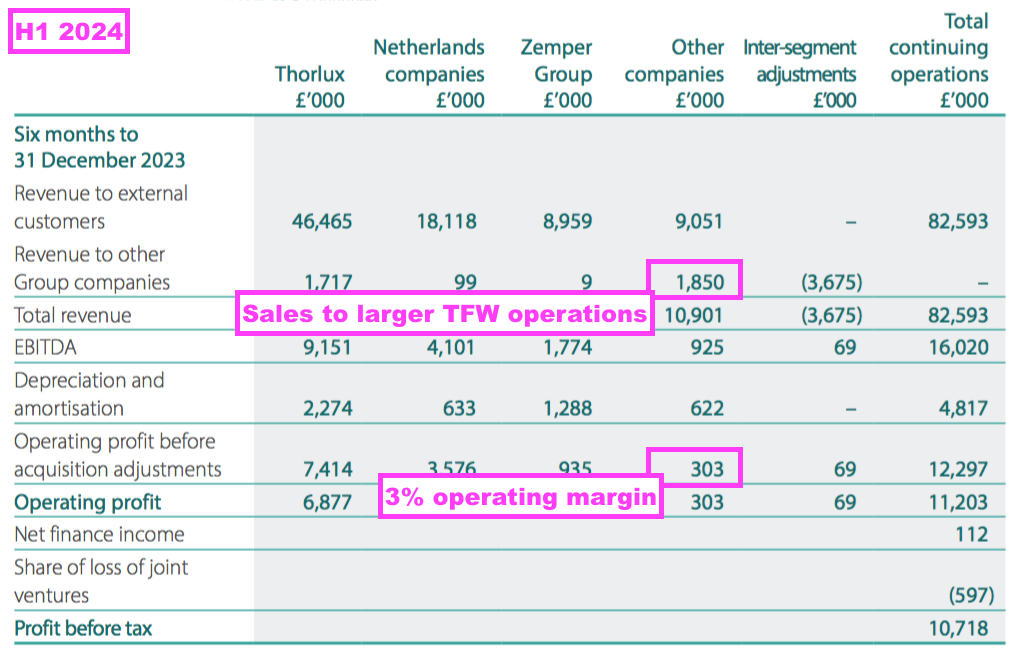

- H1 Other revenue declined 4% to £9m while H1 Other operating profit (before acquisition adjustments) advanced 2% to £0.3m:

(Includes Famostar for FY 2018 and H1 2019)

- With an annualised operating profit (before acquisition adjustments) of c£1m and this H1 showing a 3% operating margin, the Other subsidiaries have effectively become a sideshow to Thorlux, the Dutch businesses and Zemper.

- I speculate Philip Payne, Solite, Portland and possibly TRT are kept on by TFW primarily because they supply products and services to the group’s larger operations:

Financials: Thorlux versus non-Thorlux

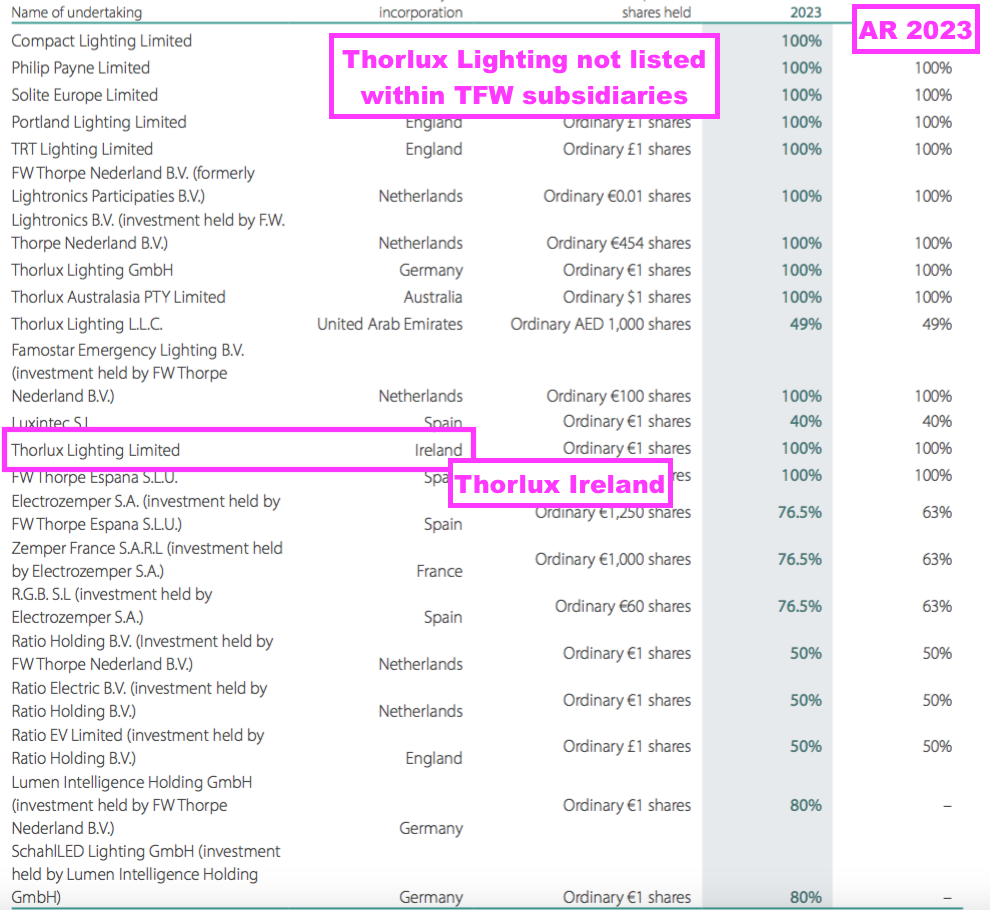

- TFW’s annual reports provide extra details about Thorlux that may well have gone unnoticed by most shareholders.

- The extra details certainly went unnoticed by me; I have held TFW shares since 2010 and only clocked this information a few weeks ago (point 38).

- Within the TFW group, the top-level holding company is actually Thorlux and all the other operations — Lightronics, Famostar, Zemper, TRT Lighting, etc — are really subsidiaries of Thorlux.

- The auditors’ report gives a clue, by noting Thorlux as “the Company“:

[FY 2023] “In establishing the overall approach to the Group audit, we identified two reporting units, which, in our view, required an audit of their complete financial information both due to their size and risk characteristics. These are Thorlux Lighting (the Company, located in the UK), and Lightronics (located in the Netherlands).”

- Other clues were the absence of Thorlux within the list of group subsidiaries…

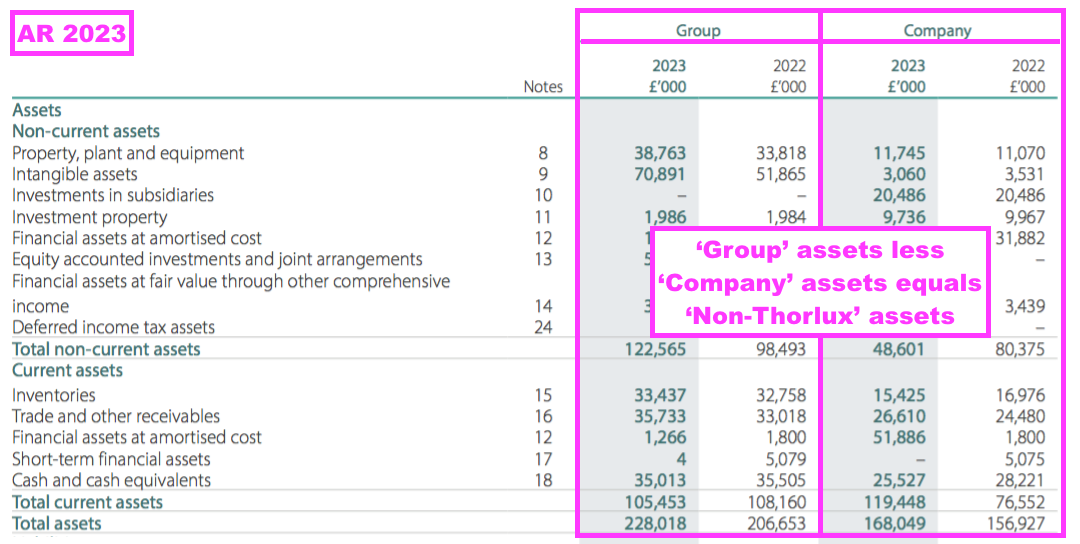

- Stock-market rules dictate quoted businesses must declare the balance sheets of their top-level holding company within their annual reports.

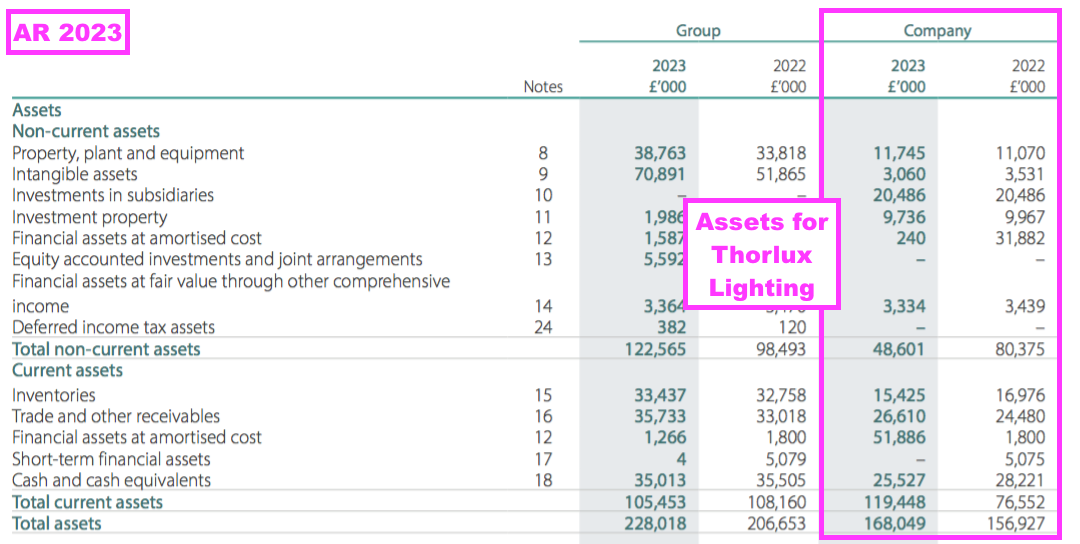

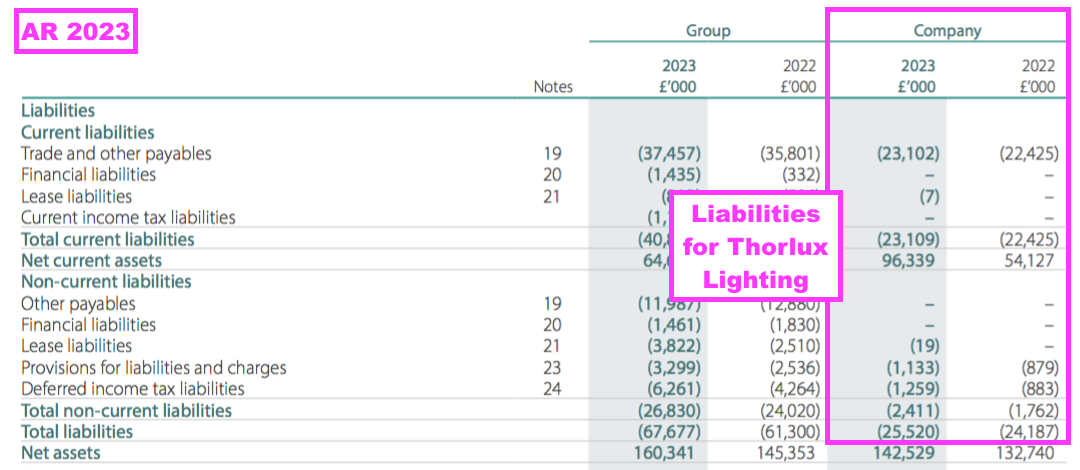

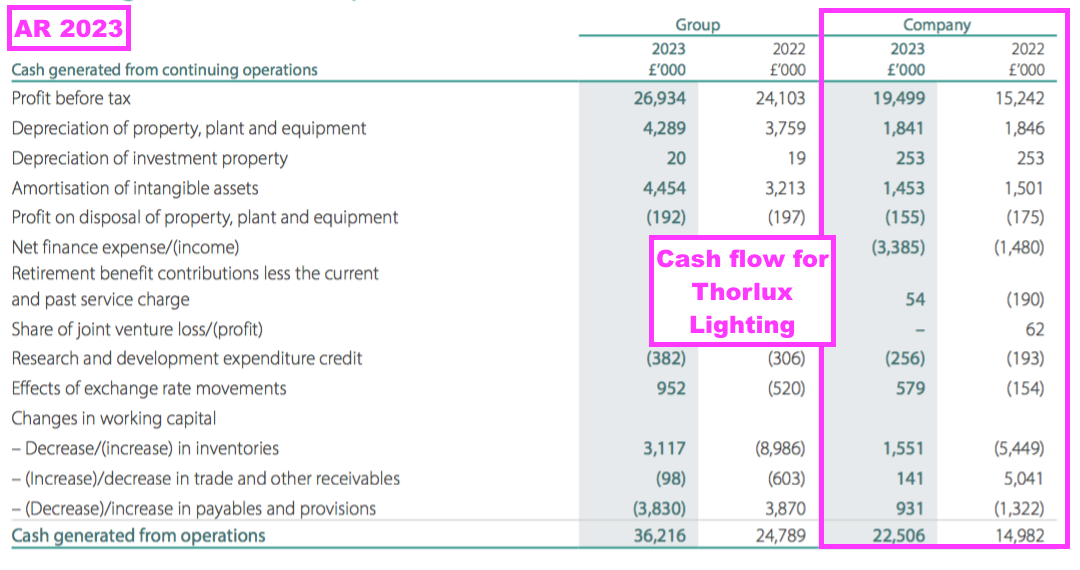

- For TFW, this means Thorlux’s assets and liabilities are disclosed for all to see:

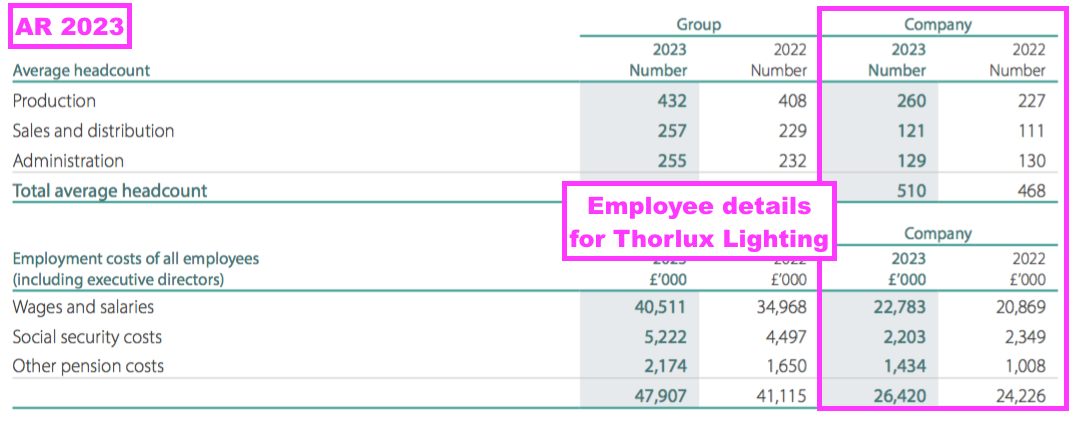

- Other information disclosed by TFW for Thorlux include the cash flow statement…

- …and employee information:

- Stock-market rules sadly do not require quoted businesses to disclose the income statements of their top-level companies.

- Thorlux’s income statement therefore remains a mystery beyond the segmental information supplied within TFW’s results:

- Subtracting the Thorlux numbers from the group numbers gives the ‘non-Thorlux’ numbers covering Lightronics, Famostar, Zemper, TRT Lighting, etc:

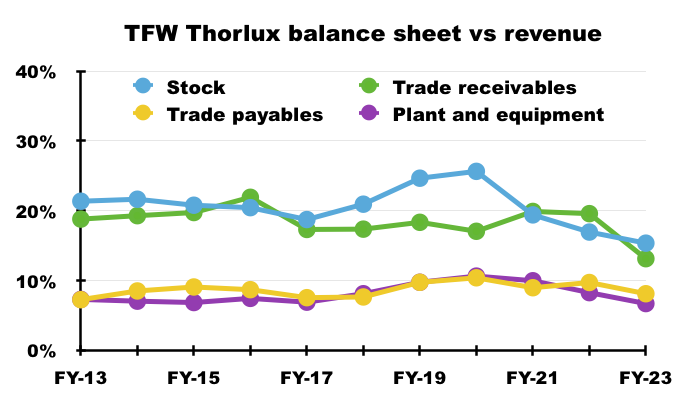

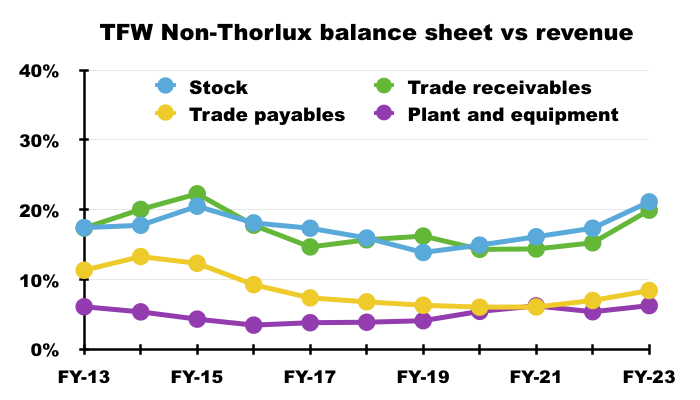

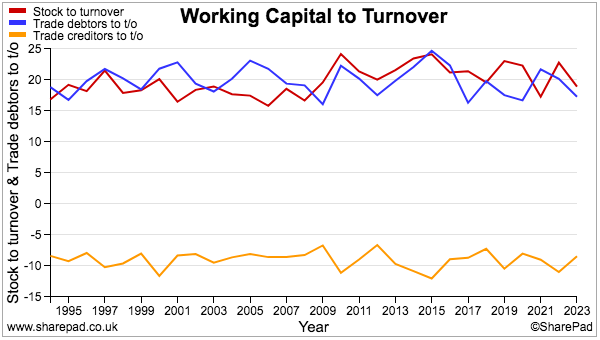

- Thorlux looks to have better working-capital management than non-Thorlux:

- Thorlux’s stock and trade debtors are equivalent to 13-15% of revenue, versus 20-21% for non-Thorlux.

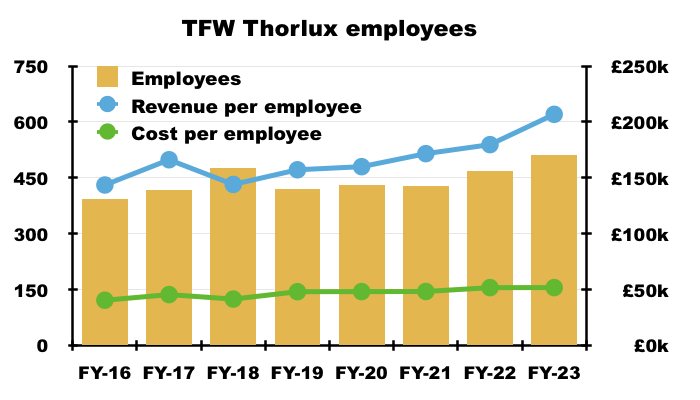

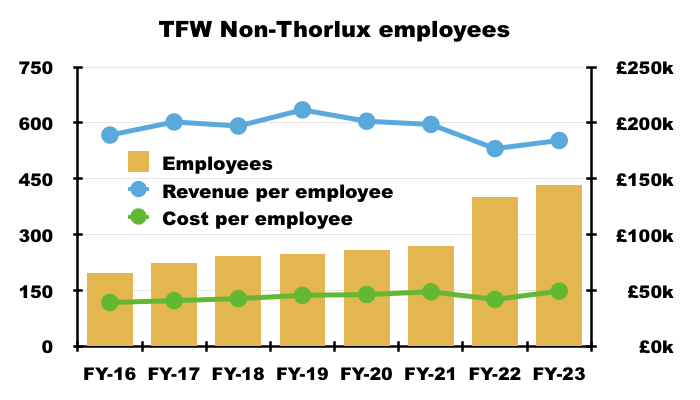

- Thorlux’s employee productivity has recently shaded that of non-Thorlux, too:

- Revenue per employee at Thorlux has now topped £200k while revenue per employee at non-Thorlux has slipped below £200k.

- However, employee costs at Thorlux and non-Thorlux are very similar at an approximate £51k average.

- All told, I am encouraged non-Thorlux’s ratios are generally close to those of Thorlux — the success of which since 1936 has funded all the acquisitions to establish non-Thorlux.

- I hope to derive more Thorlux/non-Thorlux ratios within my FY 2024 write-up.

Financials: balance sheet and cash flow

- The preceding FY answered a regular question from “some shareholders” about the group’s substantial cash position:

[FY 2023] “For many years some shareholders have questioned the rationale behind the Group holding large cash reserves.The Board chooses to maintain a large reserve as one never knows what is around the corner, as proven recently by the COVID lockdown. The Board remains prudent, with no plans to move away from this philosophy, and will not fund further growth unless it can do so from cash reserves.”

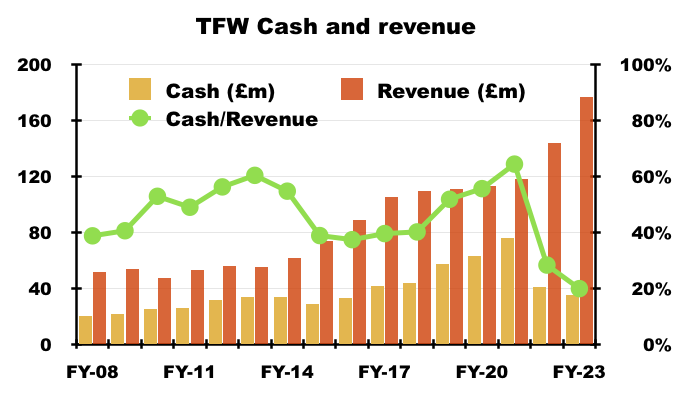

- The “large reserve” showed by this H1 amounted to £31m, while ‘financial liabilities’ (bank debt, factoring liabilities and government loans associated mostly with Zemper) were £2m.

- The “large reserve” is not as large as it once was. Cash reached almost £80m — the equivalent of more than 60% of revenue — by FY 2021 before the significant expenditure on the final Dutch earn outs and the purchases Zemper, Ratio and SchahlLED:

- Still, cash of £31m is more than enough to cover my estimated £3.2m to complete the Zemper purchase and the estimated £6.6m to complete the SchahlLED purchase.

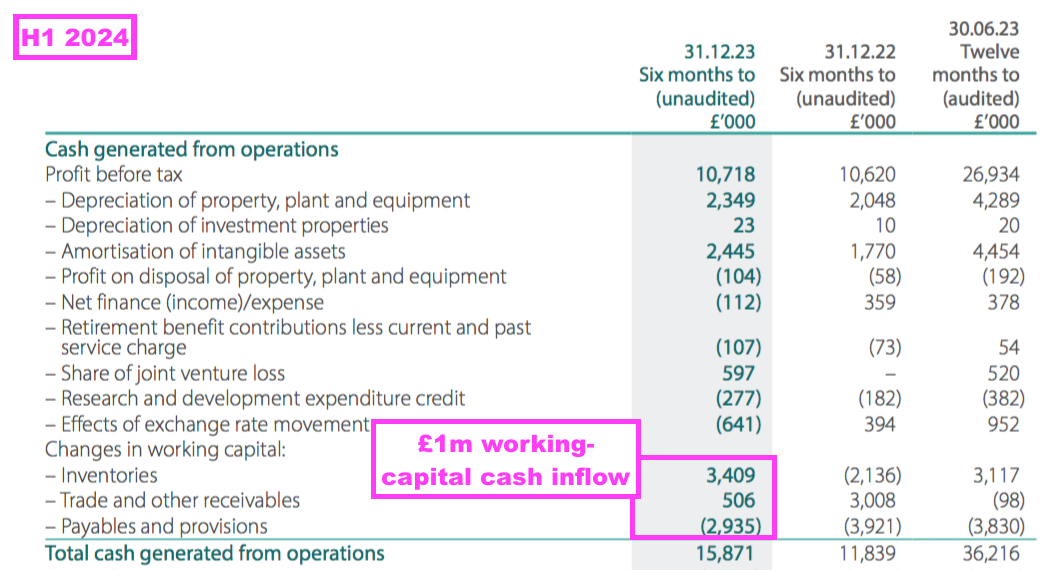

- H1 cash conversion was very satisfactory. H1 operating cash flow of £15.9m less tax of £1.8m less capex of £4.0m less lease costs of £0.6m plus net finance income of £0.3m meant reported earnings of £8.6m translated into free cash of £9.8m.

- The bulk of the £1.2m difference between earnings and free cash flow was caused by a favourable £1m reduction to working capital:

- This H1 noted stock levels had reduced:

“Stock has continued to be reduced in a carefully controlled way whilst good stock levels are maintained for strategically important items.”

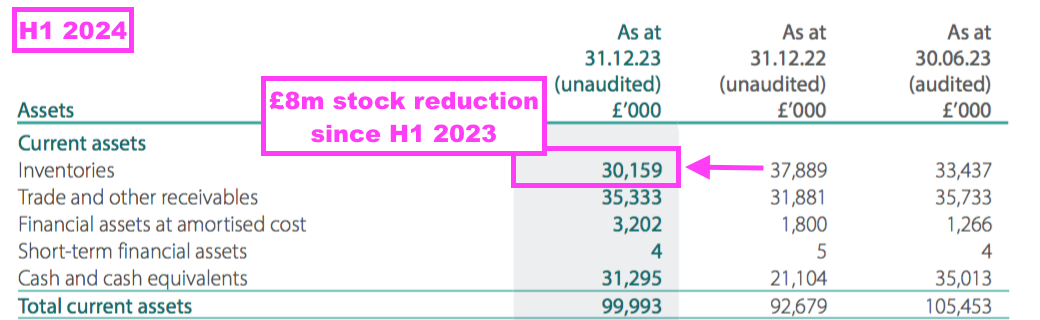

- Stock ended this H1 at £30m, some £3m lower than the preceding FY and £8m lower than the record £38m level registered by the comparable H1:

- Stock at £30m is equivalent to 17% of trailing twelve-month revenue of £177m.

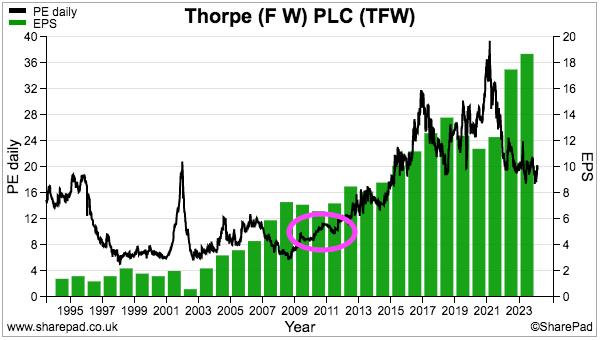

- 17% is at the lower end of the 16-24% range witnessed during the last few decades (red line below), and suggests stock levels are indeed being “carefully controlled“:

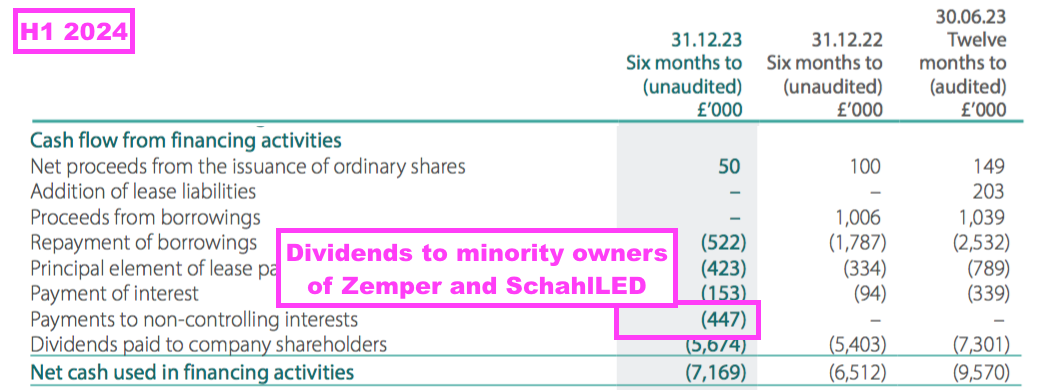

- H1 free cash of £9.8m then funded the aforementioned £4.3m spent purchasing 13.5% of Zemper, the aforementioned £0.7m loaned to Ratio Electric, £2.0m spent on additional tree-planting land, £5.7m paid as dividends and £0.4m paid to the minority owners of Zemper/SchahlLED:

- The £447k paid to the minority owners of Zemper/SchahlLED appears to be the very first accounting entry of its kind, and implies the £755k profit the two minority owners earned during the preceding FY (point 25) was enough to pay them a dividend during this H1.

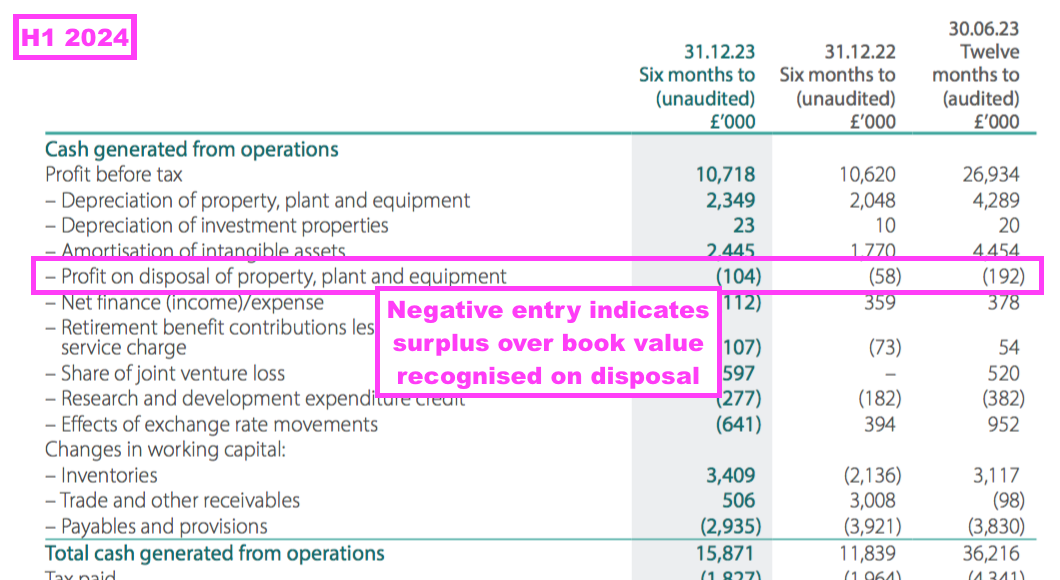

- TFW’s cash flow statement includes consistent ‘profit on disposal of property, plant and equipment’ entries:

- These profits suggest a conservative depreciation policy, whereby equipment is written down on the balance sheet to valuations below the eventual disposal proceeds.

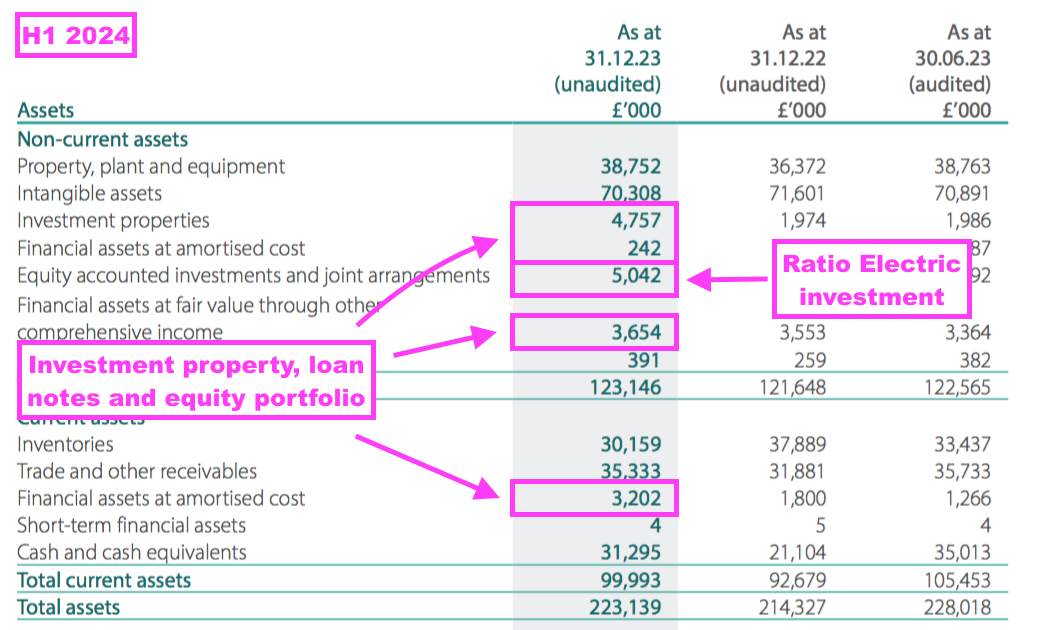

- Alongside cash of £31m, the balance sheet carries investment properties of £5m, the aforementioned £5m Ratio Electric investment, loan notes (mostly to Ratio Electric) of £3m and an equity portfolio of £4m:

- TFW’s range of investment assets generated a useful £424k income during this H1, although only the FY numbers divulge the different sources of income to indicate whether TFW is earning suitable returns on its cash.

- The mix of divisional performances led to an acceptable 14.9% group operating margin (before acquisition adjustments), versus 15.3% for the comparable H1 and 16.8% for the preceding FY:

Financials: pension scheme

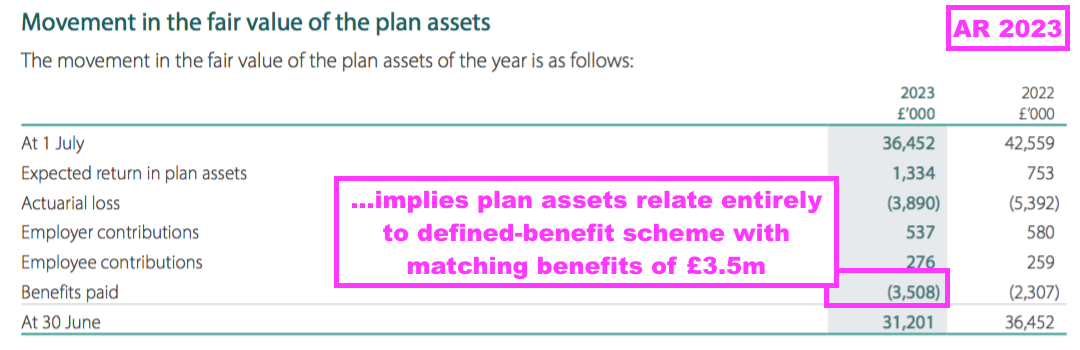

- TFW operates a “hybrid” defined-benefit/defined-contribution pension scheme. The preceding FY explained:

[FY 2023] “The Group operates a funded hybrid pension scheme for employees in the UK….

…

The contributions of the pure defined contribution, the defined benefit underpin and pure defined benefit elements are paid into one pension scheme, where the contributions and assets are segregated and ring-fenced from each other.”

- I have considered the scheme further and have become more concerned (point 36).

- I had previously wondered whether the defined-contribution element of the scheme was mixed in with the following tables from the preceding FY:

- But on further reflection, I now believe those tables relate only to the defined-benefit element of the scheme.

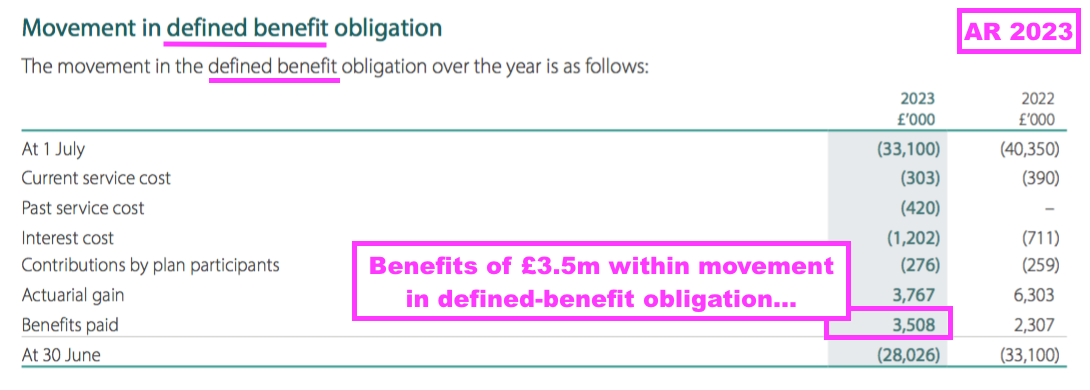

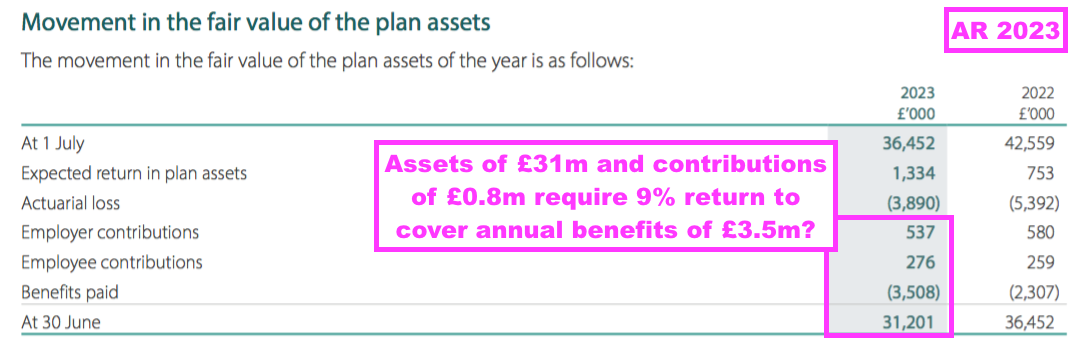

- The preceding FY showed annual benefits of £3.5m being paid from scheme assets that had been reduced to £31m:

- With contributions of only £0.8m, I would argue the scheme requires annual 9% returns or its assets may risk permanent erosion.

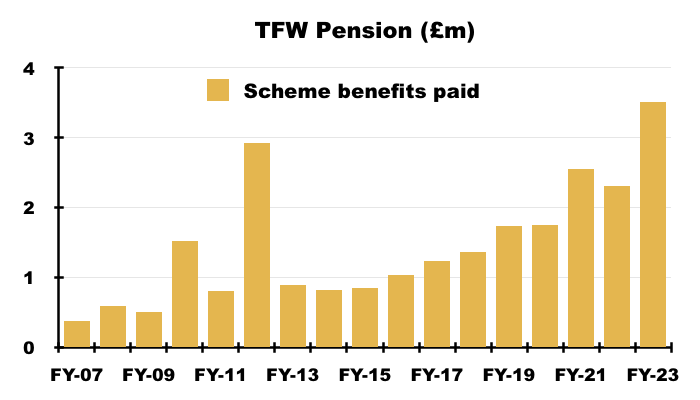

- Although the scheme’s benefit payments can fluctuate from year to year, the general trend is up:

- The preceding FY suggested the group’s FY 2024 scheme contribution would be just £364k:

“The Group expects to pay £364,000 contributions (2022: £361,000) into the pension scheme during the forthcoming year.“

- While I doubt TFW’s pension scheme will evolve into a ‘black hole’ that will disrupt the wider group, employer contributions ought to be a lot higher than the projected £364k to ensure the plan’s assets of £31m are not eroded further by yearly benefit payments of £3.5m.

- The scheme’s next triennial funding review will be calculated as at 30 June 2024. The resultant contribution recommendation will provide shareholders the best insight into the scheme’s financial requirements.

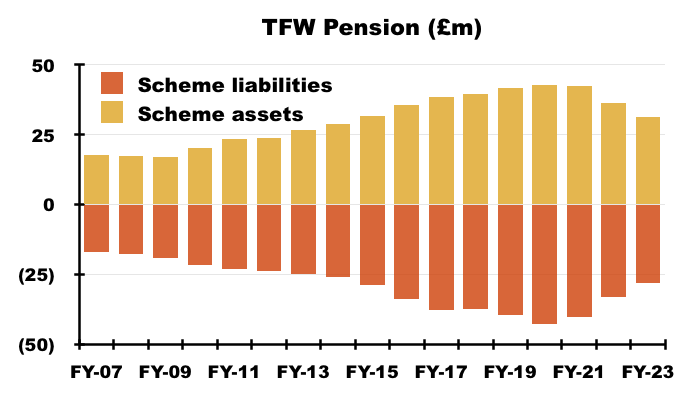

- For some perspective, TFW and its employees have contributed an aggregate £21m into the defined-benefit scheme between FYs 2007 and 2023… yet the scheme’s assets have advanced by only £17m during the same time while the liabilities just seem to mirror the ups and downs of the assets:

Boardroom

- TFW’s boardroom has experienced a number of changes during the last two years.

- The aforementioned Frans Haafkens was appointed as the group’s “first recognised independent” non-executive during October 2022.

- Two directors then retired during July 2023:

- Executive David Taylor, a long-time MD of Philip Payne, and;

- Non-exec Tony Cooper, a former Thorlux director.

- And another director — non-exec Peter Mason, a former group FD — retired during January 2024:

- Those departures slimmed the main board down from nine directors to six:

- TFW then raised eyebrows during May with another board change The roles of chief executive and group financial director were combined from July:

[RNS 2024] “FW Thorpe Plc announces the following changes to the board structure, to become effective from 1 July 2024:

Mike Allcock will step down as Executive Chairman and Joint Chief Executive and take up the role of Non-Executive Chairman.

The position of Chief Executive will be assumed by Craig Muncaster whilst retaining the role of Group Financial Director. Craig has been Joint Chief Executive since 2017 and Group Financial Director since 2010.

Mike Allcock, Chairman of FW Thorpe Plc said:

Having spent 40 years working at FW Thorpe Plc it’s time to take things a little easier. Straight from school I’ve only ever had one employer, so all that I am I owe to them.

We have spent the last few years building stronger management teams around the Group subsidiary companies to support the transition to the current Group board structure. I will continue to keep a watching brief on the technical and engineering aspects of the business whilst supporting the next generation of “youngsters” to develop and flourish.

I would like to personally congratulate Craig Muncaster on his promotion to the new role, wish him continued success and thank him for his tremendous hard work and support since joining the company in 2010.”

- I can’t recall another quoted business the size of TFW — market cap of £446m, revenue of £177m and operating profit (before acquisition adjustments) of £30m — deciding to merge the positions of chief executive and finance director.

- TFW has always employed a somewhat unconventional board.

- For example, few quoted businesses employ joint chief executives — yet TFW has employed the following joint chief executives since FY 2001:

- Andrew Thorpe and Peter Mason to FY 2010, then;

- Andrew Thorpe and Mike Allcock to FY 2017, and then;

- Mike Allcock and Craig Muncaster to FY 2024.

- Mr Thorpe and Mr Allcock have also served as executive chairmen — a corporate governance no-no — for many years.

- The board has no nomination committee nor an audit committee (point 18) while the remuneration committee does not exactly produce a verbose report (point 19).

- And directors stand for AGM re-election every three years, whereby best practice today is standing for re-election every year.

- Appointing Mr Muncaster to the combined role of chief executive and group finance director creates three worries.

- First, Mr Muncaster may become stretched with his extra executive responsibilities and certain tasks could be overlooked.

- Second, Mr Muncaster obtains significant management power, which reduces the scope for different executive opinions at board level.

- And third, Mr Muncaster has limited technical knowledge of TFW’s products.

- The 2023 annual report lists Mr Muncaster’s areas of expertise and responsibility as:

[AR 2023] “Financial Management, Commercial/Legal Risk, Investor Relations, Mergers & Acquisitions, Company Secretarial”

- In contrast, the 2023 annual report lists Mr Allcock’s areas of expertise and responsibility as:

[AR 2023] “Lighting & Controls Technology, Product Design/Management, Industry Knowledge, Marketing, Strategy“

- True, Mr Allcock remains as non-executive chairman and, as the announcement said, will “continue to keep a watching brief on the technical and engineering aspects of the business”.

- But Mr Allcock’s board duties will be part time, and the danger is competitors improve their innovation…

- …and TFW loses ground due to a lack of board executives with technical engineering knowledge.

- James Thorpe, now the only other executive alongside Mr Muncaster, may not be able to help on technical matters. The 2023 annual report lists his areas of expertise and responsibility as:

[AR 2023] “Sales & Marketing, Business Development, Digital Marketing“

- Still, the appointment of Mr Muncaster as chief executive/group finance director has the implicit blessing of the two Thorpe non-executives, both of whom:

- Have spent their careers at TFW;

- Are now in their 70s, and;

- Have (presumably) accrued plenty of knowledge about management recruitment during the last few decades.

- I doubt the Thorpe non-execs would risk their combined 43%/£191m shareholding on a mis-judged chief executive appointment.

- This line from the announcement may be significant:

[RNS 2024] “We have spent the last few years building stronger management teams around the Group subsidiary companies to support the transition to the current Group board structure.”

- Perhaps Mr Muncaster has always been earmarked for this unusual combined role since he took up the joint chief executive position seven years ago.

- I speculate the board re-jig signals a different approach to group strategy and capital allocation.

- After all, Mr Muncaster and Mr Haafkens are both deemed by the 2023 annual report to have “Mergers & Acquisitions” expertise…

- …and major boardroom decisions of the last ten years or so have included purchasing Lightronics, Famostar, Zemper and SchahlLED for what could be an aggregate £80m-plus.

- I get the impression the private-equity deal-making between Mr Muncaster and Mr Haafkens will now set the tone for TFW’s future expansion.

- Maybe Mr Allcock decided such expansion would not be appropriate for him. Perhaps he did not fancy creating further “synergy initiatives” with Zemper that would help justify its purchase.

- Mr Allcock turns 57 later this year, so ‘old age’ was not an obvious reason for his retirement.

- Mr Muncaster is 50 years old, so time should be on his side to develop TFW for the long run.

- Mr Muncaster has overseen some very appealing accounts since joining TFW during FY 2010. Perhaps he imposed greater financial discipline on R&D, so only those products likely to deliver decent returns saw the light of day that therefore kept the group’s financials in good health.

- Could Mr Muncaster in his new combined role evaluate TFW’s Other subsidiaries? I speculate the Other subsidiaries have been kept on by the board’s ‘lighting’ directors, but may well be re-organised by a ‘numbers’ boss.

Valuation

- This H1 provided an acceptable outlook:

“At the time of writing, the general order book and revenue for the Group as a whole are good. Within the Group, therefore, we look forward to an improved situation at the year end, providing there are no sudden changes to the economic outlook “

- Applying the 25% UK tax rate to the trailing £30m operating profit (before acquisition adjustments) gives earnings of £22m or approximately 19p per share.

- My calculations could be fine-tuned for the:

- Net cash (£29m);

- Forecast earn-outs (c£10m);

- The Ratio Electric investment, loan notes, investment property and equity portfolio (£17m), and;

- Potential operating improvements at Zemper and the Other subsidiaries…

- …but such adjustments would not make a huge difference to the £446m market cap that my guesswork says is supported by a 20x multiple.

- My decision to purchase TFW between 2010 and 2012 was made much easier because the shares were then valued at a more modest c10x P/E multiple:

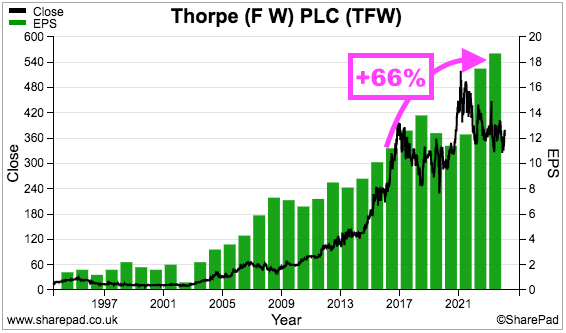

- Despite reported earnings advancing 66% between FY 2016 and the preceding FY, the shares at 375p have traded sideways throughout the same period:

- The introduction of a new five-year option scheme that targets annualised EPS growth of just CPI +2% does not suggest an imminent profit surge.

- Perhaps today’s buyers are (still) willing to pay a healthy 20x multiple because of TFW’s:

- Long-time operational resilience, as demonstrated by 21 years of consecutive dividend increases;

- Appealing returns from acquisitions purchased on low multiples (e.g. Lightronics and Famostar);

- Possible growth opportunities through Zemper’s “synergy initiatives” and cross-selling into new territories (e.g. Europe through overseas subsidiaries), and;

- Future orders supported by product launches such as Acorn and ongoing concerns about elevated energy costs.

- The bear case beyond general economic challenges include:

- Zemper, SchahlLED and Ratio Electric not performing as expected following significant purchase expenditure;

- Mr Muncaster and Mr Haafkens embarking on an aggressive acquisition spree;

- A lower priority given to lighting innovation and technical matters at board level, and;

- The introduction of CPI +2% EPS targets underlining the group’s modest organic-growth prospects.

- As shareholders await the first strategic decisions from the revamped board, the trailing 6.54p per share ordinary dividend supplies a modest 1.7% income at 375p.

Maynard Paton

Thanks for your usual excellent analysis Maynard.

At the time of Thorpe’s Ratio BV acquisition on 2nd December 2021 the company said

“The acquisition is expected to enhance earnings per share in the financial

year ending 30 June 2023.” Your write-up shows that this does not appear to have been achieved yet in its most recent results announced on 3rd October 2024 the company says

“Recent acquisitions continue to perform in line with expectations”. Surely this is not true in the case of Ratio which has been a disappointing acquisition? Perhaps the company would say that it is referring to more recent expectations rather than its expectations for Ratio in 2021, but I think that attempted “get-out” would also reflect badly on the company. I think investors will need to keep a close eye on Zemper and Ratio and I would argue that investors need more evidence that these are good acquisitions before further cash is used to buy any additional companies.

Thanks John. Good spot — I had not recalled the ‘enhanced 2023 earnings’ projection made at the time of the Ratio acquisition. Yesterday’s figures showed an £826k loss accorded to Ratio, with TFW lamenting “New projects and companies always seem to take longer to start and be harder to establish than one first believes.“. I would agree with your verdict, and I would like to see positive progress from Zemper in particular — it was TFW’s largest purchase undertaken on a higher multiple than previous deals — before further M&A.

Maynard