29 July 2024

By Maynard Paton

FY 2023 results summary for M Winkworth (WINK):

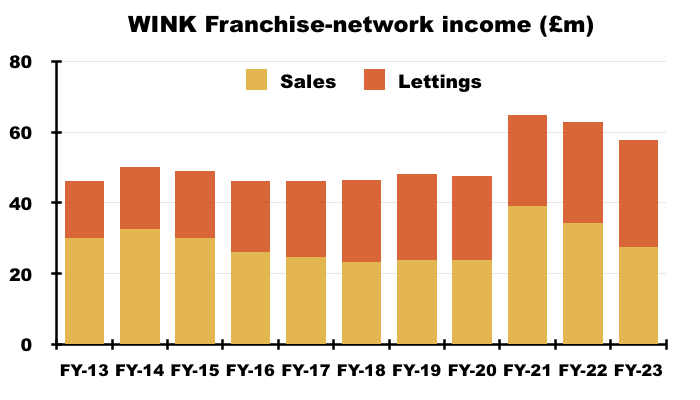

- Only the dividend advanced higher (+6%) as a suppressed property market alongside greater costs left franchise-network income 8% lower, revenue unchanged and profit down 25%.

- Requiring every franchisee to be a “top three contender” prompted nine branch closures but underpinned industry-leading sales, lettings and conversion statistics versus (now anonymous) rival agents.

- Company-owned offices now include Pimlico and collectively reported a £0.48m profit, although divisional progress remains dominated by Tooting — the exit strategy for which is unclear.

- After reporting a lower margin, adverse cash conversion and weaker employee productivity, a post-FY update heralded a stronger FY 2024 that supports a possible 12-14x P/E and near-6% yield.

- Celebrations marking the chairman’s 50-year tenure invite bid speculation, especially following the appointment of two non-execs with M&A backgrounds and sector merger activity involving Property Franchise and Belvoir. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- Franchisees: network and competitive advantage

- Franchisees: branch openings and closures

- Franchisees: sales and lettings

- Winkworth versus Foxtons

- Company-owned offices: strategy and progress

- Company-owned offices: Tooting

- Financials

- Valuation

- Potential bid target?

News links, share data and disclosure

- Annual results, presentation and webinar for the twelve months to 31 December 2023 published/hosted 17-18 April 2024;

- Q1 dividend declaration published 10 April 2024;

- Q2 dividend announcement and trading update published 10 July 2024, and;

- Directorate changes published 05 June 2024.

- Share price: 200p

- Share count: 12,908,792

- Market capitalisation: £25.8m

- Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, with progress buoyed by motivated franchisees capturing market share through expert knowledge, tip-top service, realistic valuations and competitive fees.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments.

- Seasoned family management boasts £12m/47% shareholding, rewards investors through durable quarterly dividends and seems likely one day to consider an M&A exit.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Revenue, profit and dividend

- This FY was never going to be spectacular after the preceding H1 confessed to a 26% lower profit and January’s Q4 update then admitted higher interest rates had continued to suppress the property market:

[Q4 2023] “The rise in interest rates, which began after the mini budget in Q4 2022 and was sustained through 2023 by the fight against inflation, took its toll on the UK property market…

Hesitancy on behalf of buyers, however, along with legal delays in conveyancing, led to a downturn in transactions. Winkworth’s network completed sales for the year fell by some 19%.

The shortage of rental property in 2023 and consequent rise in prices translated into an increase in our network [letting] revenues of around 5%, offsetting the slower sales completions.

Winkworth’s full year pre-tax profits, subject to audit, are expected to be in line with the current market forecast of £2.1m (31 December 2022: £2.47m) and net cash at year end, following increased investment in new offices in 2023, to be at least £4.4m (31 December 2022: £5.25m).“

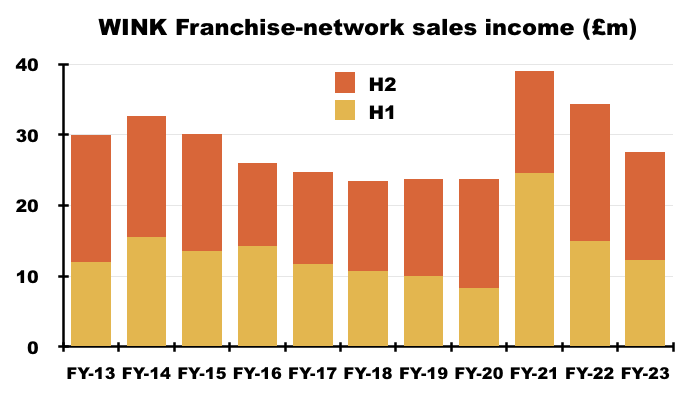

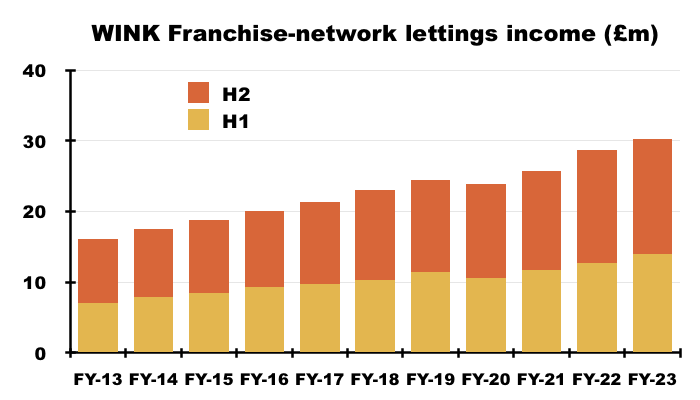

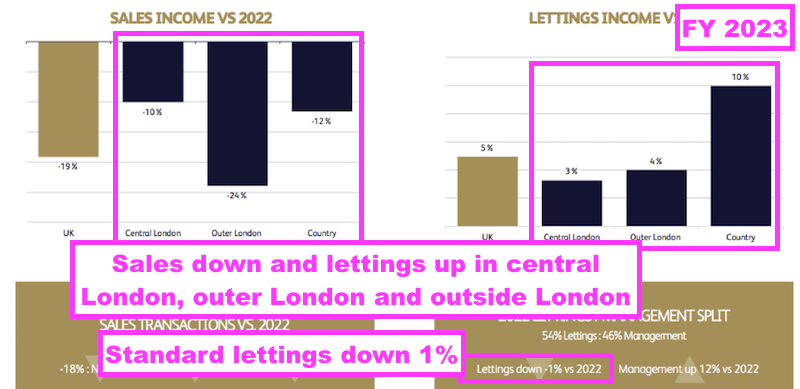

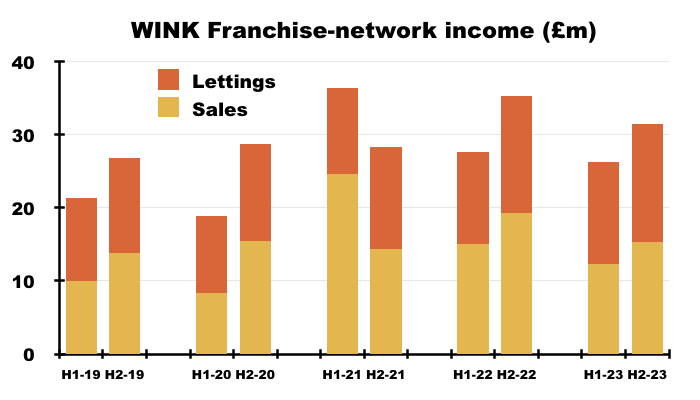

- FY franchise-network sales income in fact dropped 20% to £27.6m while FY franchise-network lettings income did indeed climb 5%, to £30.2m:

- Total FY franchise-network income was therefore left 8% lighter at £57.8m.

- H2 progress appeared worse than H1, with H2 franchise-network sales income falling 20% (versus H1 down 18%)…

- …and H2 franchise-network lettings income improving only 1% (versus H1 up 10%):

- WINK’s FY pre-tax profit was indeed £2.1m as predicted by January’s Q4 update.

- However, FY pre-tax profit was boosted by the inclusion of ‘negative goodwill’ of £252k after WINK took control of its Pimlico franchise (see Company-owned offices: strategy and progress).

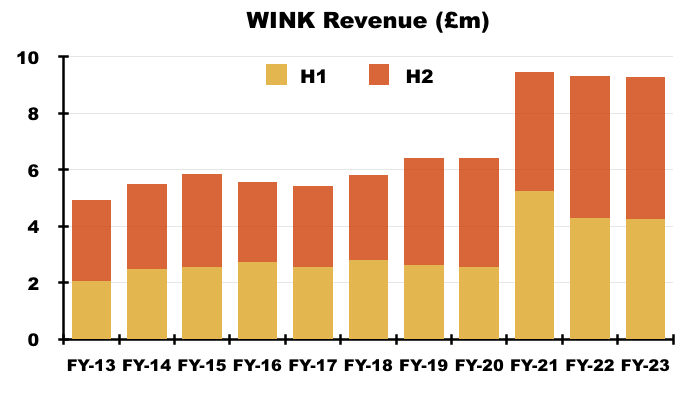

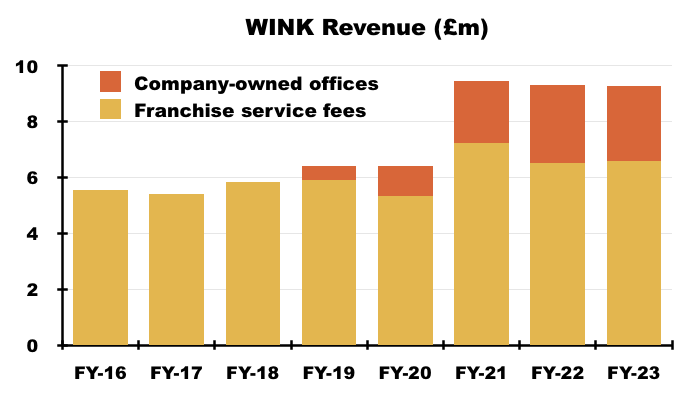

- FY revenue remained at £9.3m, with H2 revenue flat at £5.0m:

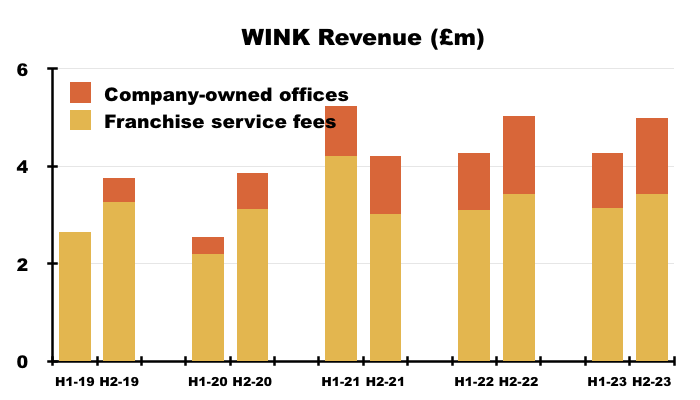

- FY revenue from franchise service fees and company-owned offices remained unchanged at approximately £6.6m and £2.7m respectively:

- FY revenue from franchise fees was able to remain unchanged at £6.6m despite total franchise-network income declining 8% because WINK captured a greater proportion of franchise-network income for itself (see Franchisees: network and competitive advantage).

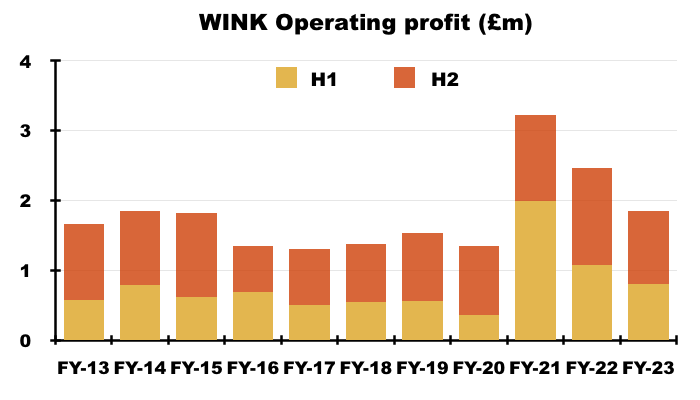

- Extra administrative costs of £0.6m meant FY operating profit before negative goodwill declined 25% to £1.8m (see Financials):

- After H1 operating profit dropped 26% to £0.8m, H2 operating profit excluding negative goodwill declined 24% to £1.0m.

- This FY was the first to disclose the collective profitability of the group’s company-owned offices (see Company-owned offices: strategy and progress):

“The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited, the newly acquired Lumley 1 Limited [Pimlico] and Winkworth Development and Commercial Investment Limited, contributed revenue of £2.69 million (2022: £2.78 million) and £0.48 million (2022: £0.57 million) of profit before tax.“

- Pre-tax profit from the main franchising operation was therefore approximately £1.67m (£2.15m less £0.48m) from revenue of £6.6m.

- WINK’s reported profit was not complicated by major adjustments, with non-trading charges beyond the aforementioned negative goodwill limited to a favourable £31k fixed-asset movement.

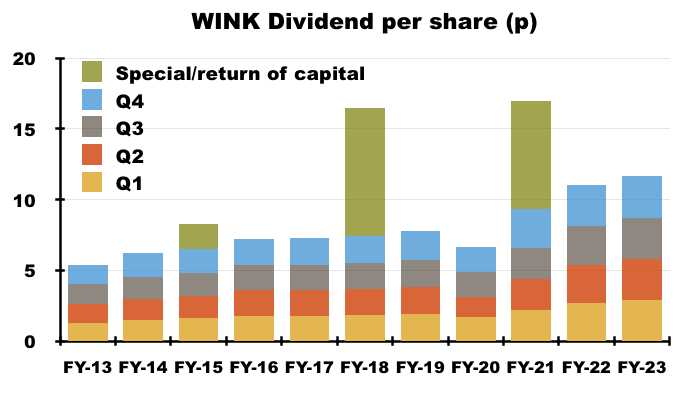

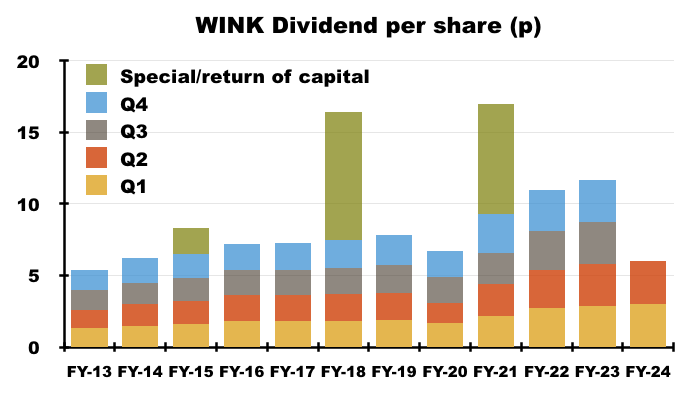

- October’s Q3 update and January’s Q4 update had already revealed quarterly payouts of 2.9p and 3.0p per share respectively, which took the total FY payout to 11.7p per share:

- This FY’s 11.7p per share total payout was the only headline measure moving in the right direction — up 6% versus the 11p per share for the comparable FY.

- Following this FY, announcements during April and July declared 3p per share Q1 and Q2 dividends, which took the prospective total FY 2024 payout to 12p per share (see Valuation).

Franchisees: network and competitive advantage

- WINK’s franchise network consists of 98 estate-agency branches located throughout London and affluent areas of southern England.

- Franchisees pay WINK a straight 8% of all of their sales and lettings income, plus variable sums towards IT, training, marketing, legal, compliance, landlord/tenant referrals and other services (point 7a).

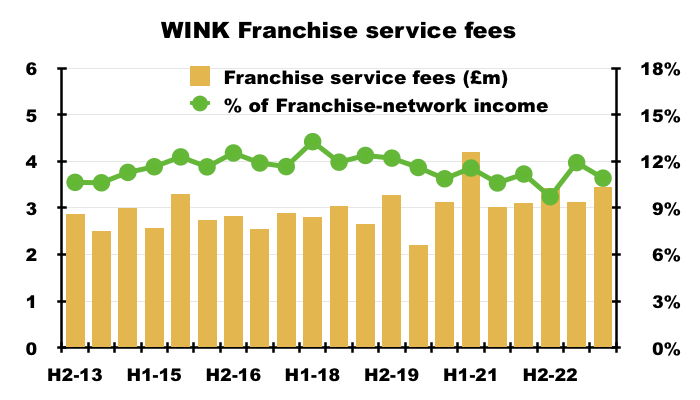

- During this FY, £6.6m, or 11.4%, of the £57.8m earned by the franchisees was taken by WINK as services fees:

- The 11.4% proportion was the highest since FY 2019 (12.3%) and was a welcome improvement on the preceding FY’s proportion of 10.3%.

- Management’s H1 webinar explained the 11.4% proportion was in part supported by:

- Greater set-up fees from new and resold branches, and;

- An extra £120k earned by the group’s Asia-Pacific desk.

- The 2023 annual report indicates WINK’s competitive edge is based upon ensuring the franchisees provide a tip-top service to support a highly reputable brand:

“The essence of Winkworth’s franchise proposition lies in its brand and reputation.

…

Winkworth places significant value on the integrity of its brand, upholding it through exemplary standards of ethics and business conduct in all interactions.

…

Winkworth strives to maintain a reputation for the highest standards of business conduct. The directors always endeavour to operate to the highest ethical standards in order to maintain and promote the reputation of the Company.

…

We have strong local market knowledge and expertise, both in London and in the country markets, and we commit to maintaining competitive fees while delivering unparalleled service to meet our customers’ needs.

…

We aim to expand our portfolio of rental properties by providing landlords with top-tier service“

- As such, not everyone that applies to become a franchisee is successful:

“Winkworth has a rigorous vetting procedure for new franchisees and only a small number of applicants are successful in joining the group. Once accepted, franchisees are closely monitored to make sure that they achieve the best practice service levels expected of them and remain compliant with the law. Winkworth provides regular training through it’s centralised in-house training academy, alongside which it runs regular compliance audits of franchisee offices, both remote and in-person.”

- Appointing higher-quality franchisees helps ensure each branch can generate healthy commissions and — as this FY described — remain “fit for purpose throughout the property cycle” (see Franchisees: sales and lettings).

- Franchise-network income per branch during this FY was approximately £590k (£57.8m/98).

- That £590k compares to almost £200k per branch during FY 2009, nearly £500k per branch during FY 2016 but £635k during FY 2021.

- Management’s FY webinar stated a branch’s market share was more important than comparing its income to the network average:

“[A branch’s income] varies hugely as to what is acceptable and what is not. A franchise in, say, Dartmouth has low costs but commensurately lower revenues. In central London costs are higher but revenue potential is high. To average it out is always difficult as it does not reflect either. But we can see what we can do with the transparency on that.

One size unfortunately doesn’t fit all, there isn’t one metric we could apply to all offices fairly. That’s why we look at market share per area because it’s fairer. If you’re within the top three in your area, with some exceptions, that is a sustainable place to be, but revenues will be very different for, say, Dartmouth compared to Chelsea.”

- This FY reiterated branches have to become a “top three contender” or risk closure (see Franchisees: branch openings and closures):

“In line with our ambition to be a top three contender in local markets, in 2023 we decided not to renew certain franchises where our standards were not being met and results were below expectations.”

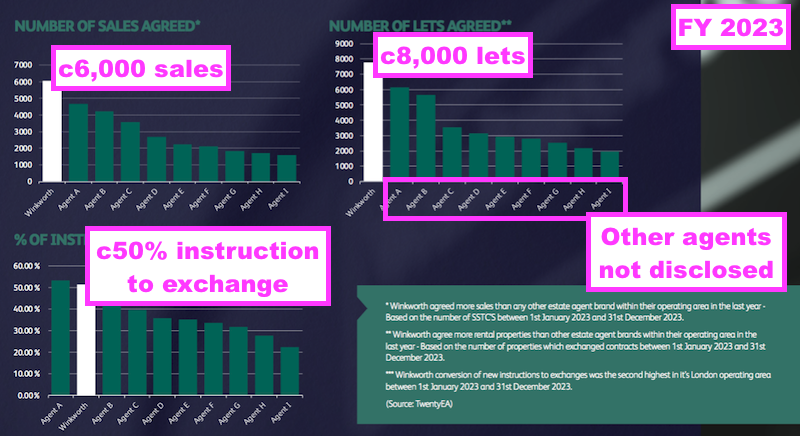

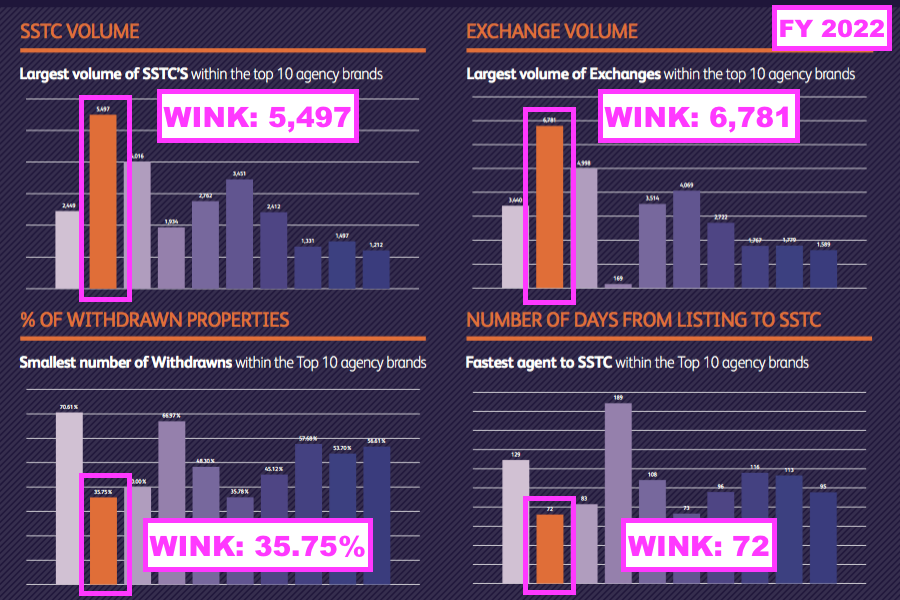

- Statistics from this FY underlined the greater effectiveness of the typical WINK franchisee versus nine other sizeable agents:

- Unlike previous presentations, this FY presentation sadly did not disclose the identities of the other agents.

- Only the number of sales agreed (or solds-subject-to-contract) was divulged during both this FY (c6,000) and the comparable FY (5,497):

- This FY suggested the ‘% of instructions to exchange’ was a vital group KPI:

“We have always been primarily a sales-oriented estate agency and we judge our success by our instructions to sales ratio, where we rank one of the leaders in the industry.”

- The higher the proportion of instructions converted into exchanges, presumably the more likely the franchisee agent:

- Values properties realistically, and;

- Generates a greater income per hour for his/herself and WINK.

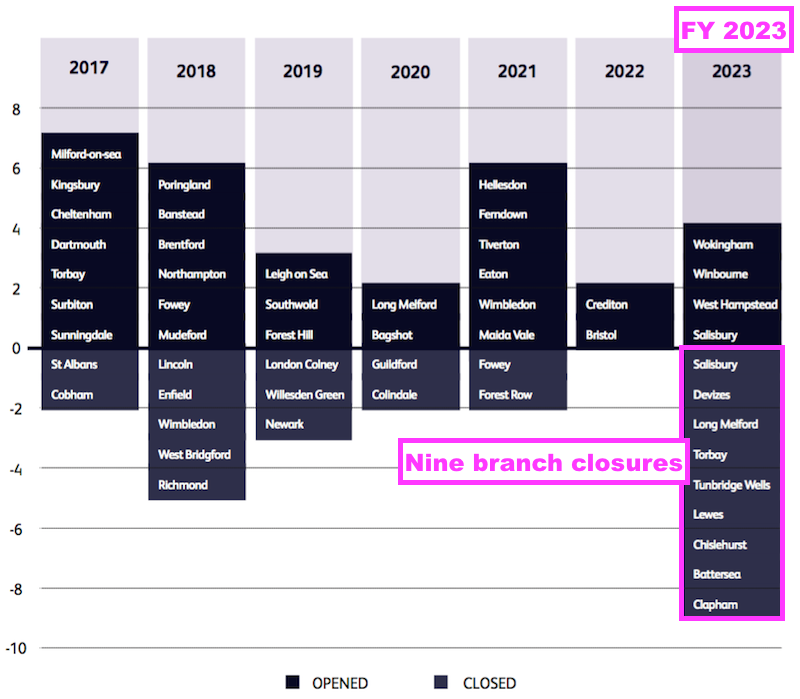

Franchisees: branch openings and closures

- Following some vague commentary during the preceding H1, this FY confirmed the Battersea and Clapham branches had been closed:

“This led to the closure of Battersea and Clapham offices, and the sale of the Kennington Lettings business to our Kennington sales franchisee, who is now also empowered to open a further office in his territory.“

- Seven other franchised branches were also closed during this FY…

- …although Salisbury was quickly re-opened. Long Melford was open only for three years.

- Management’s FY webinar stated WINK:

- Had employed a “much more proactive focus” on franchisee-branch management, and;

- Was “happy to walk away from certain markets”…

- …which probably explains why nine locations were shut during this FY.

- Management’s FY webinar also explained how struggling franchisees affected nearby offices and the wider network:

“What we want is a healthy and strong network. If we have offices that are perhaps underperforming or struggling, that does have a knock-on effect on our network. It also has a knock-on effect on our future growth. Because if we open an office near to one that is not trading as well as perhaps it could be clearly why would we open a new Winkworth if the neighbour is not operating. “

- Some 30 branches have been opened and 23 have been closed since FY 2017.

- Opening a net seven new branches over seven years underlines the slow expansion of the franchise network. The 101 WINK locations operating during this FY compare to 86 quoted within the 2009 flotation document and 94 quoted within the 2016 annual report.

- The target number of new branches remains six per annum, which seems a reasonable ambition but will no doubt be offset by additional closures.

- This FY confirmed three new branches had already opened during FY 2024 with perhaps another eight to open in London alone:

“We have already opened three new offices this year in St Leonard’s, adding to our existing Exeter network through a supported acquisition, Leamington Spa and Stoke Newington. With up to eight new franchisees set to join our London network in 2024, and our portfolio management initiatives revitalising ambition and growth right across the business, we are excited by the outlook for the current year. “

- The preceding H1 included bold commentary about reinvigorating London branches, whereby “new blood” could triple or quadruple a location’s revenue:

[H1 2023] “In London, we have identified further opportunities to both introduce new blood to existing businesses and to significantly improve the sales performance of offices with strong underlying lettings businesses. We believe that in certain situations we may be able to increase the available franchise revenue three or four-fold, the equivalent of opening multiple cold start offices.“

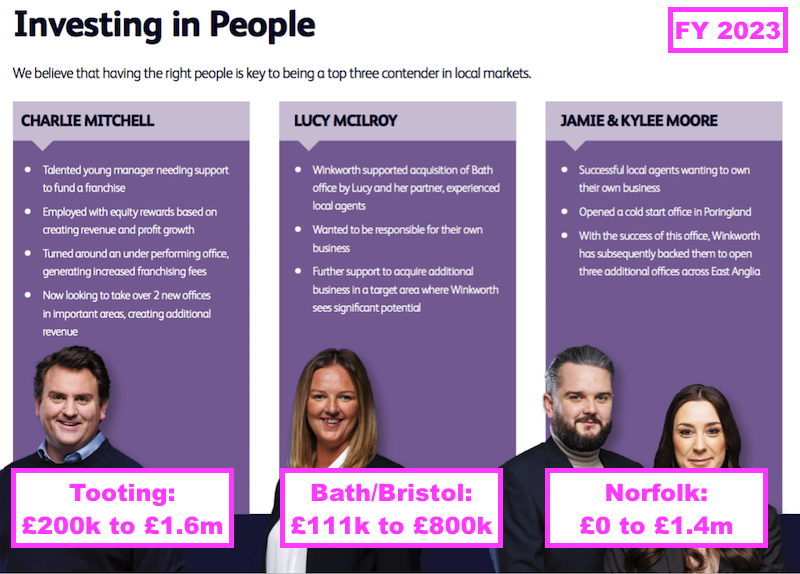

- Management’s FY webinar disclosed three examples of “new blood” excelling at their respective branches:

- Management’s FY webinar presented a new slide that summarised the extra revenue earned since FY 2018 from seven resold franchise branches, six new franchise branches and two WINK-acquired offices:

- Management’s FY webinar explained:

- The six new branches were all opened by the franchisees that had earlier purchased a nearby resold franchise, and;

- By FY 2023 the 15 resold/opened/acquired locations had combined to generate extra revenue of £3.3m (up 46%).

- Note that of that additional revenue of £3.3m, £1.4m was apparently delivered by the acquired Tooting office alone (see Company-owned offices: Tooting).

Franchisees: sales and lettings

- The lower sales income and greater lettings income generated by franchisees during this FY were spread throughout the branch network:

- Sales transactions down 18% versus franchise-network sales income declining by the aforementioned 20% suggests the franchisees collected slightly lower commissions per transaction during this FY.

- Unlike previous presentations, this FY presentation did not divulge the number of exchanges to allow shareholders to calculate the average agent commission per sales transaction:

- Statistics disclosed within the comparable FY (and preceding H1) had suggested agents earned average sales commission of £5.1k (H1 2023: £5.4k) per exchange.

- Note that the 2023 annual report admitted “pressure on commissions may escalate“:

“Risk: In a market with reduced trading activity, pressure on commissions may escalate, potentially resulting in lower earnings from fewer transactions. Specifically, Winkworth is vulnerable to shifts in the London market, as the majority of its revenue stems from franchisees concentrated in this region.

Management action:We have strong local market knowledge and expertise, both in London and in the country markets, and we commit to maintaining competitive fees while delivering unparalleled service to meet our customers’ needs.“

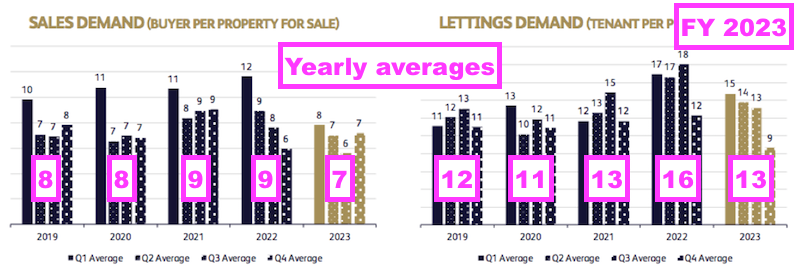

- The FY presentation admitted the number of potential buyers per property for sale had dropped to seven — the lowest number since at least FY 2019:

- The FY presentation also noted the number of potential tenants per property to let had reduced to 13, with just nine reported for Q4 — the lowest quarterly figure since at least Q1 2019.

- This FY acknowledged lettings activity moderated during H2 due to “affordability” reasons:

“Our lettings business grew by a further 5% compared to financial year 2022, despite a tempering of activity in H2 as affordability levels were reached.”

- The tone of WINK’s lettings commentary contrasted with that of the preceding H1, which noted “extreme” competition among tenants:

[H1 2023] “With an ongoing reduction of supply in the private rental sector due to landlords exiting the market following increasing costs and proposed new changes in legislation, the competition for properties to rent continued to be extreme.”

- FY franchise-network lettings income gained 5% due entirely to more landlords employing WINK’s full property-management service, income from which gained 12%:

“Within this [5% lettings income advance] we were particularly pleased so see the ongoing growth of the property management segment of our business, with revenues growing by 12% compared to financial year 2022 and now accounting for 26% of our total network revenues.”

- In contrast, FY franchise-network income generated through the standard lettings service for ‘hands-on’ landlords declined 1%.

- Lettings income has grown at a relatively consistent pace, increasing 88% between FYs 2013 and 2023:

- The sales-rental network split during this FY was 48%:52%.

- 52% is the highest-ever proportion of FY franchise-network income represented by lettings.

- This FY suggested the sales-rental split may reverse to favour sales during FY 2024:

“2024 has started more briskly than expected, with our sales agreed to the end of March 23% ahead of 2023…

We have witnessed some price weakening in the rental market with supply increasing (23% ahead of 2023 to end of March 2024) and demand declining (5% behind 2023 to end of March 2024).“

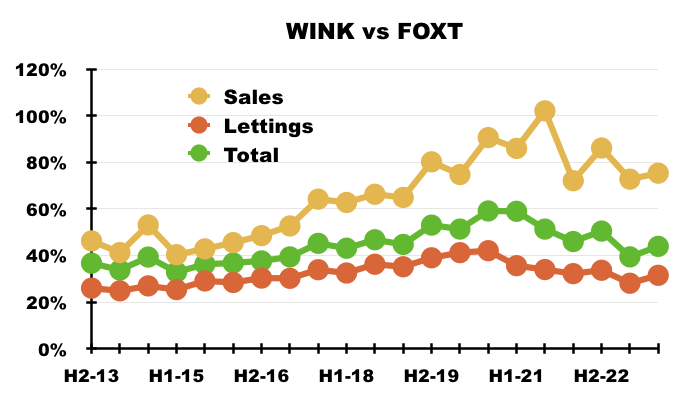

Winkworth versus Foxtons

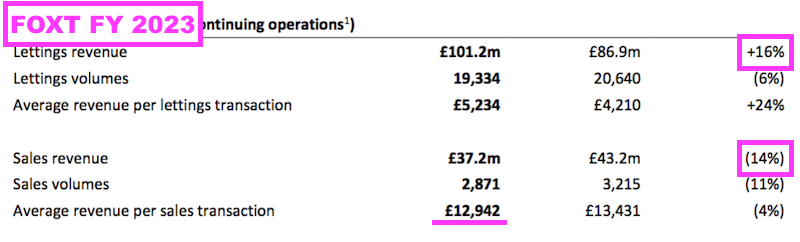

- Foxtons (FOXT) claims to be “London’s leading estate agency” and remains as good a benchmark as any to assess WINK’s relative progress.

- FOXT experienced similar FY 2023 trends to WINK, with sales revenue down and lettings revenue up:

- Note FOXT’s £13k average revenue per sales transaction.

- FOXT charges a standard 2.5% + VAT for sole agency status for selling a London property.

- Charging 2.5% + VAT as sales commission seems high, but all credit to FOXT for actually achieving 2.25% + VAT during FY 2023 given “pressure on commissions may escalate” in a low-volume property market.

- The chart below expresses the sales, lettings and total franchisee income of WINK as percentages of the comparable FOXT revenue:

- The rising trends until FY 2021 indicate WINK’s self-employed franchisees handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees…

- …although FOXT has improved its performance markedly versus WINK since FY 2022.

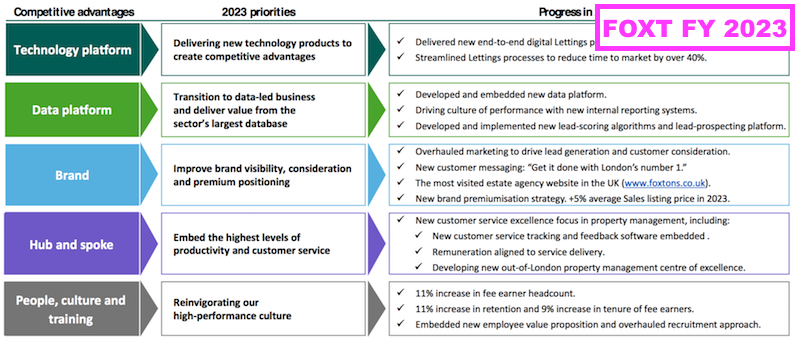

- FOXT’s improvement is linked to the 2022 appointment of a fresh chief executive, who has instigated a number of initiatives to revitalise the group:

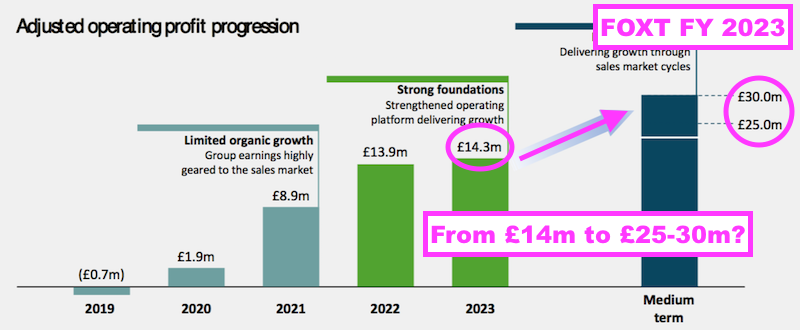

- FOXT’s adjusted operating profit for this FY was £14m, and the new boss has said the “medium-term target“ is £25m-£30m:

- Meeting that £25m-£30m ambition in a sluggish property market could mean FOXT becomes very focused on taking market share from WINK and other agents.

- Note that comparing WINK with FOXT is not strictly like-for-like. FOXT generates almost all of its revenue from locations within London while WINK’s franchisees have historically generated approximately 80% from the capital and for this FY generated 75%.

- Further distortion is caused by FOXT and WINK acquiring and/or selling businesses.

- FOXT also collects interest on client monies held as deposits for lettings (an extra £4.1m during FY 2023).

- FOXT’s revitalised leadership could nevertheless leave WINK facing stiffer competition, and may even have prompted WINK to close some of those nine branches during this FY (see Franchisees: branch openings and closures).

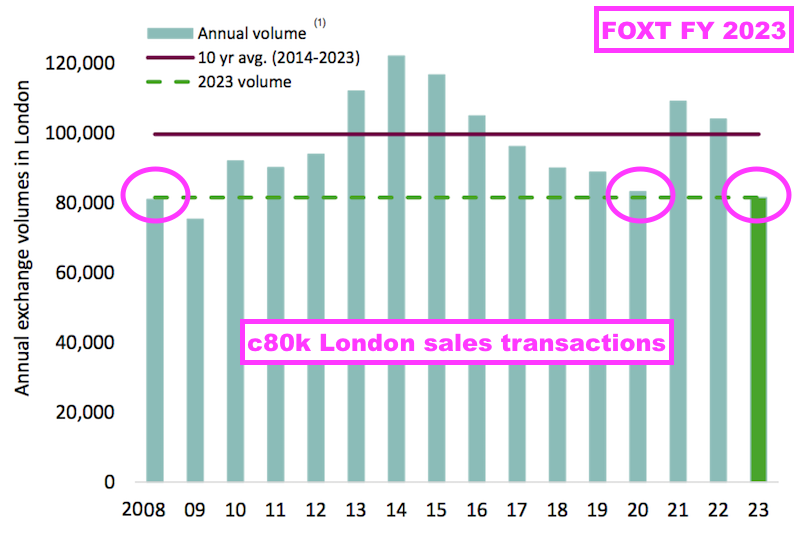

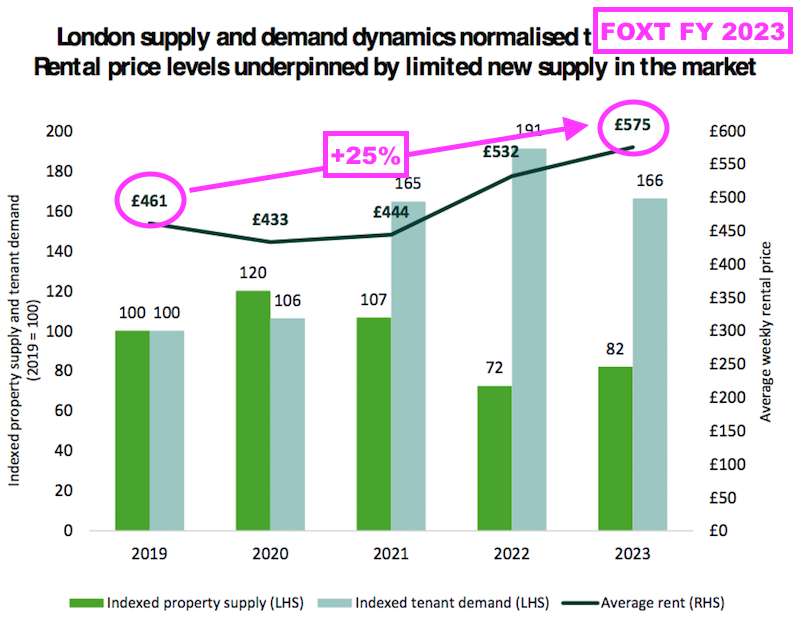

- FOXT’s FY 2023 provided two useful charts on the London property market.

- Transaction volumes at c80,000 during 2023 broadly matched the levels witnessed during both the 2008/9 banking crash and 2020 pandemic lockdowns:

- Weekly rents within the capital meanwhile have advanced by 25% between 2019 and 2023:

- FOXT’s charts could argue that any growth exhibited by WINK, FOXT and other London agents over time may have been supported solely by higher property prices and rents rather than increased market shares.

- For example, I note WINK’s franchisee lettings income between FYs 2019 and 2023 advanced 24% (from £24.4m to £30.2m) to match the 25% average rent increase in the FOXT chart.

- Management’s FY webinar suggested greater FOXT (and other) competition could be “positive” for WINK as it may persuade more independent agents to become a WINK franchisee:

“In some ways competition is positive for us because the more challenges there are for independent businesses, the more talent is available. When Purplebricks launched, they were a feeder of franchisees because people wanted to future-proof their business and have the support of us to be competitive. So we look at all these things as opportunities and we back ourselves as mature and established agents in London to meet them.“

Company-owned offices: strategy and progress

- This FY witnessed WINK take control of its Pimlico office after the franchisee did not renew his/her agreement:

“While our Pimlico office was taken back, we used our assisted acquisition support strategy to relaunch it alongside an entrepreneurial partner who has the opportunity to receive equity in this franchise as its potential is realised.”

- Pimlico joins fellow London offices Tooting and Crystal Palace as WINK-owned offices that will give the group greater “front-end” insight:

“As with the acquisitions of Tooting Estates Limited and Crystal Palace Estates Limited, Lumley 1 Limited [Pimlico] will keep Winkworth in touch with and learning from front-end experiences and industry trends. It will also provide a live platform to test and develop future digital initiatives and evolve our centralised CRM systems, which will be of benefit to all our franchisees.”

- But management’s webinar comments have regularly suggested the purchases are driven more by improving lacklustre branches through talented agents. For example, this FY’s webinar said:

“The agenda we started with these offices was to bring people in who are really good at what they do, but don’t have the money [to launch their own franchise]. We are a franchise business and the better the people we have, the better our 8%, and we want to maintain our model as a franchise business.”

- Management’s FY webinar also clarified these company-owned offices ought to:

- Take three years to turn around, and;

- Not be long-term investments:

“We are very wary that there is a development cycle for each office and it probably is three years. What we are doing is taking a business that is not in the top three, perhaps lower down the level, and we are investing in it with the right people and resources to put it in the top three. And that takes time to feed through. So we do not want too many in a development-cycle phase or exposed to the ups and downs of the market, so when we feel they are established in the top three we feel they are a through-the-cycle business.

The game is not to be long-term owners of these businesses. It is to bring the talent in, boost revenue opportunities from key markets where there are high revenue opportunities and once you have that 8% going for 20 years we can move our resources to the next place.”

- The trio of WINK-owned offices is complemented by the group’s in-house Development and Commercial Investment (DCI) agency, which handles sales of new builds and commercial properties.

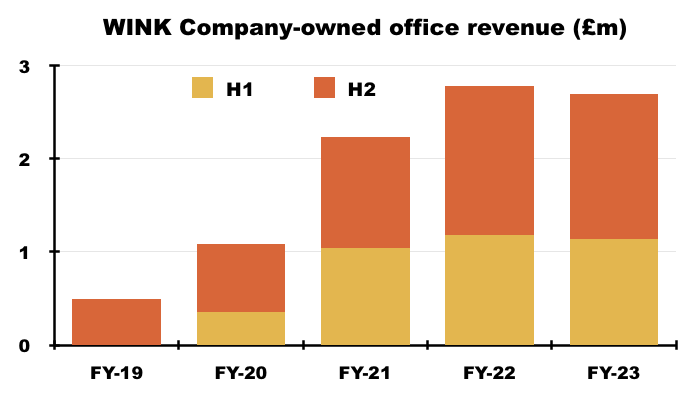

- This FY revealed revenue from company-owned offices dropped 3% to £2.7m:

- Management’s FY webinar divulged:

- Tooting revenue fell £125k;

- Crystal Palace revenue gained £135k;

- Pimlico revenue contributed £75k, and;

- DCI revenue fell £170k.

- Revenue from company-owned offices represented 29% of total revenue during this FY, versus 30% for the comparable FY and 24% for FY 2021:

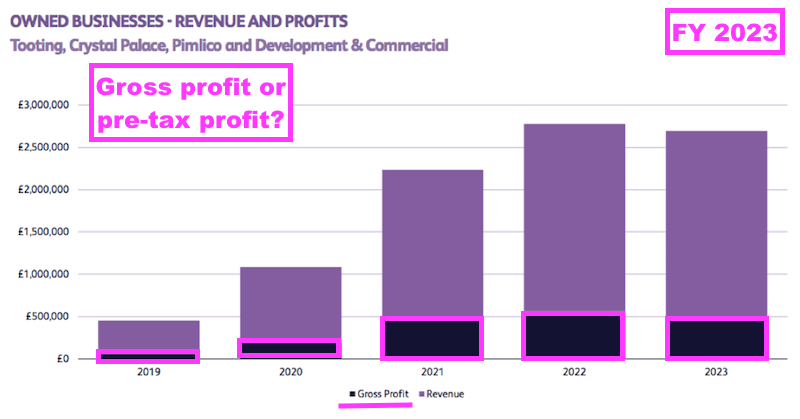

- The FY presentation showed “gross profit” from company-owned offices remaining at approximately £500k:

- But the 2023 annual report implied the presentation was in fact showing pre-tax profit of approximately £500k:

“The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited, the newly acquired Lumley 1 Limited [Pimlico] and Winkworth Development and Commercial Investment Limited, contributed revenue of £2.69 million (2022: £2.78 million) and £0.48 million (2022: £0.57 million) of profit before tax.“

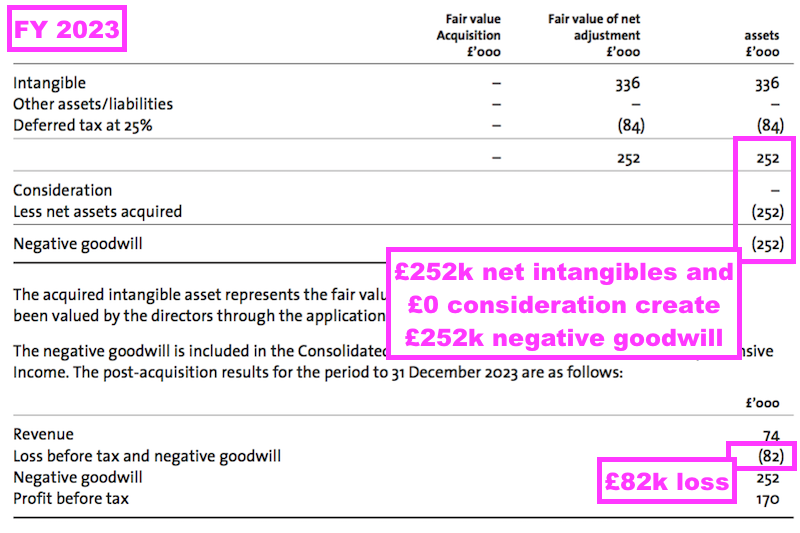

- The Pimlico transaction created ‘negative goodwill’ — an unusual but legitimate accounting concept that arises when the purchase price of an acquisition is less than its net asset value.

- This FY revealed Pimlico:

- Was acquired for zero on 20 October 2023;

- Incurred losses of £82k up to 31 December 2023;

- Carried net intangibles of £252k, and;

- With the benefit of negative goodwill, added £170k to pre-tax profit.

- Excluding the £170k Pimlico contribution, FY pre-tax profit from Tooting, Crystal Palace and DCI seemingly declined from £570k to £310k.

- Management’s FY webinar revealed the company-owned offices incurred extra costs of £0.35m, which was in part due to:

- Crystal Palace “gearing up” for growth, and;

- The launch of a new-homes venture within the DCI agency.

- Still, an FY £310k pre-tax profit from Tooting, Crystal Palace and DCI does not seem too awful given:

- Tooting was acquired for approximately £300k between FYs 2019 and this FY;

- Crystal Palace was acquired for zero during FY 2020, and;

- DCI was established internally during FY 2020.

- I get the impression the £310k profit was dominated by Tooting, helped in part by Crystal Palace and possibly counterbalanced by losses at DCI.

- Upcoming documents on Companies House (to be published here, here, here and here) may clarify where exactly the division’s profit was generated.

- Management’s FY webinar encouragingly suggested a fourth company-owned office would only emerge once Crystal Palace and Pimlico had established themselves:

“We don’t have an ambition at this point [to have a certain number of company-owned offices]. We would look at another one once we were sure Crystal Palace is delivering and Pimlico was up and running and then we would also probably look to exit one.”

- While the welcome returns from Tooting (see Company-owned offices: Tooting) imply positive outcomes for Crystal Palace and Pimlico, I remain convinced long-term shareholder success within a sector dependent on individual talent is most likely to be earned through the franchisor approach.

Company-owned offices: Tooting

- WINK’s Tooting office has been a major success. Management’s FY webinar claimed a new manager lifted Tooting revenue from £200k to £1.6m during his tenure in charge between FYs 2018 and 2023:

- The FY webinar confirmed the successful Tooting manager had moved on but was looking at opening two new WINK offices:

“In terms of the entrepreneurial partnership, we’re actually looking forward to certain franchisees owning shares. Our Tooting office has done fantastically well for us and the franchisee has received funds for selling his shares back to us and is now looking to own two new Winkworth franchises.“

- Following this FY, the successful Tooting manager acquired the WINK franchises of Streatham and Herne Hill.

- How long WINK will retain control of its Tooting office remains unknown.

- The FY webinar disclosed Tooting’s lettings manager and replacement sales manager now have the opportunity to earn “10%-plus” of the shares in their office:

“The lettings manager is an important part of the business having trebled her lettings business. She’ll be receiving some equity this year and, for the new person in sales, that is also their goal. We have a view that the management in these businesses can grow a stake of up to 10%-plus so there is plenty for people who deliver the revenue to go for.”

- As WINK’s “game” for company-owned offices is “not to be long-term owners“, how the group will eventually exit Tooting is unclear.

- WINK acquired the final 10% of Tooting from the office’s former successful manager for £137k during this FY — implying the full value of Tooting is almost £1.4m.

- I suspect few franchisees are likely to pay WINK £1.4m for Tooting given a “cold start” branch can be launched for £120k-200k.

- Tooting’s £1.4m valuation may also explain why:

- Tooting’s former successful manager chose not to become the Tooting franchisee, and;

- The office’s current ’employee’ managers look set to own only “10%-plus” if they become successful.

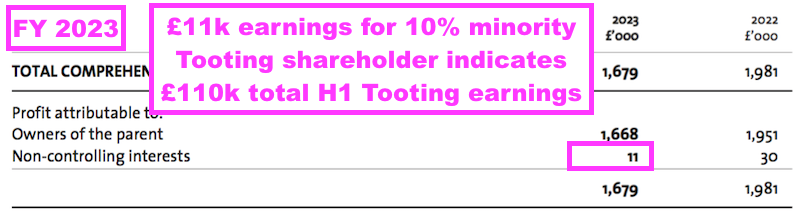

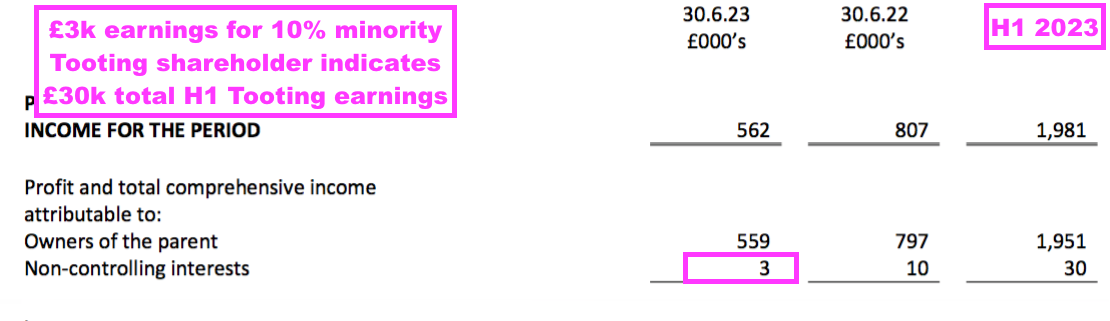

- The finer details of Tooting’s profitability appear inconsistent.

- WINK purchased the final 10% of Tooting at the start of H2 2023, and this FY suggested H1 Tooting earnings were £111k:

- But the preceding H1 suggested H1 Tooting earnings were £30k:

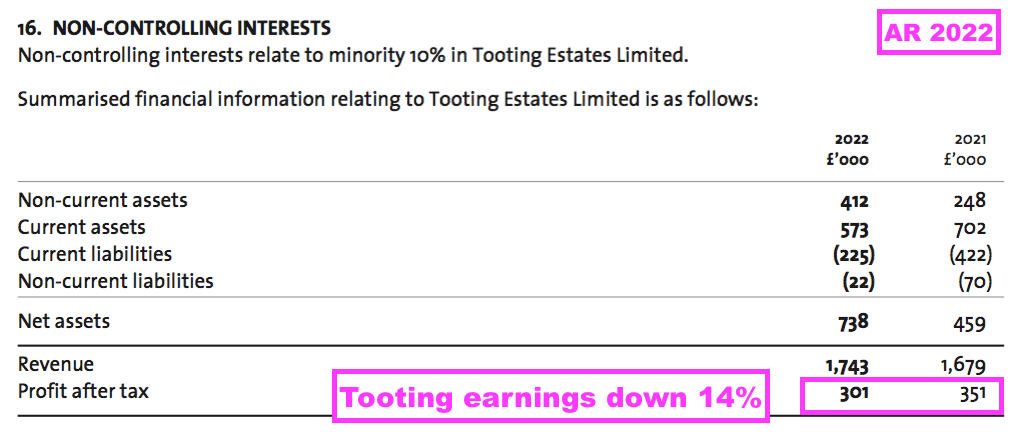

- For perspective, Tooting earnings during FY 2022 were £301k and during FY 2021 were £351k:

- I note management’s FY webinar admitted the Tooting office had — following the departure of its previously successful manager — slipped from number one to number two within its area

Financials

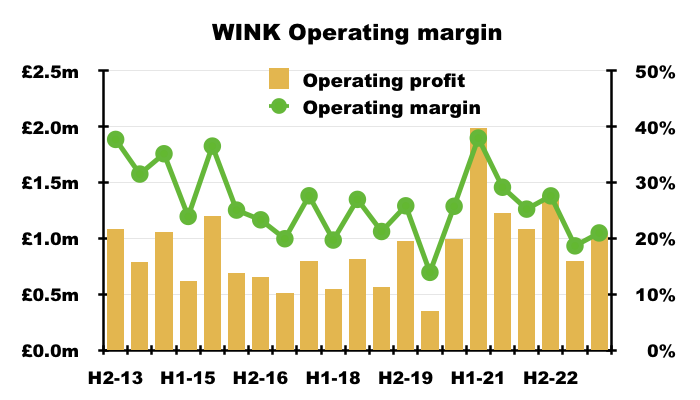

- This FY showed the margin impact from the slower property market and the start-up expenses for Crystal Palace, Pimlico and DCI.

- WINK converted 20% of revenue into profit, the lowest for any FY following the group’s FY 2009 flotation:

- For perspective, the average FY margin between FYs 2009 and 2018 — during which WINK operated as a pure franchisor — was a very appealing 29%.

- Applying that 29% margin to this FY’s franchise service fees of £6.6m gives an approximate £1.9m profit, which is £0.2m greater than my aforementioned £1.67m assumption (see Revenue, profit and dividend).

- Management’s FY webinar implied the main franchising division may not be as profitable as it once was. The division incurred extra FY costs of £0.25m due to:

- A general pay increase and catch-up payments for “underpaid, under-rewarded staff“, and;

- A £50k “cost-inflation impact“.

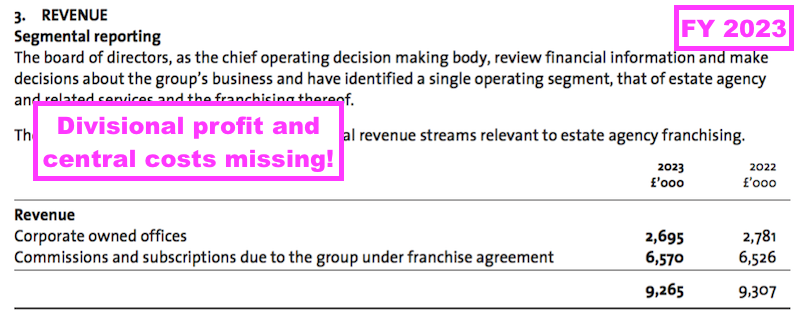

- Rather than disclose divisional profitability only within the small-print…

“The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited, the newly acquired Lumley 1 Limited [Pimlico] and Winkworth Development and Commercial Investment Limited, contributed revenue of £2.69 million (2022: £2.78 million) and £0.48 million (2022: £0.57 million) of profit before tax“

- …WINK should really confirm divisional profitability within the accounting notes to help shareholders determine the progress made within the main franchising operation:

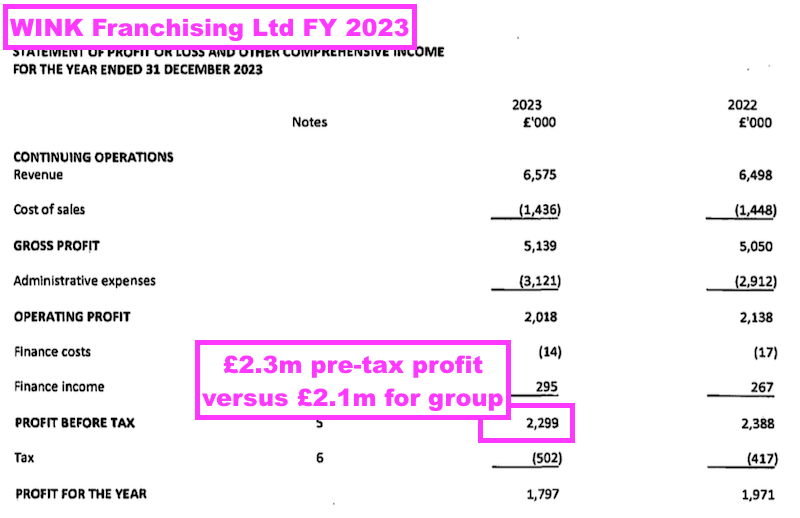

- Companies House shows WINK’s main Winkworth Franchising subsidiary earning a £2.3m pre-tax profit for this FY:

- I cannot reconcile WINK reporting a group £2.1m pre-tax profit when the main franchising subsidiary reported a £2.3m pre-tax profit and the company-owned offices were said to have delivered a £0.48m pre-tax profit.

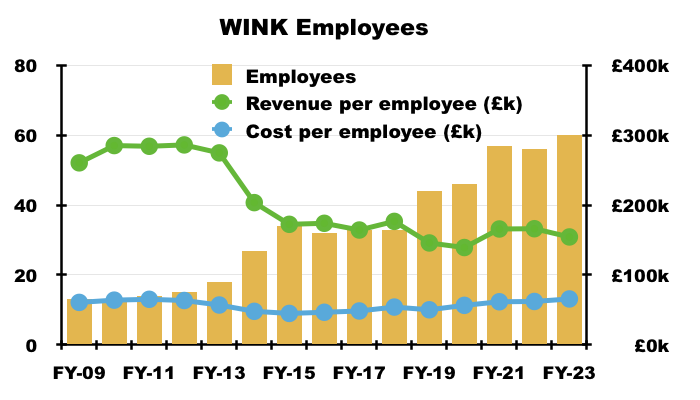

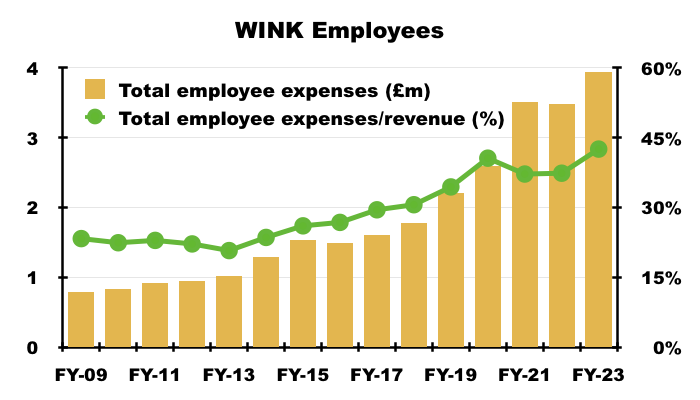

- Something I am clear on, though, is the weakening of employee productivity:

- Revenue per employee was more than £280k for FYs 2010, 2011 and 2012, but was £173k for FY 2015 and £154k during this FY.

- Two key years for employee productivity are:

- FY 2015, which saw WINK recruit extra personnel to handle i) client referrals within the network, and; ii) businesses looking to relocate executives, and;

- FY 2019, when WINK started its company-owned office strategy with the purchase of Tooting.

- The extra personnel recruited during the last decade have absorbed a much greater share of revenue:

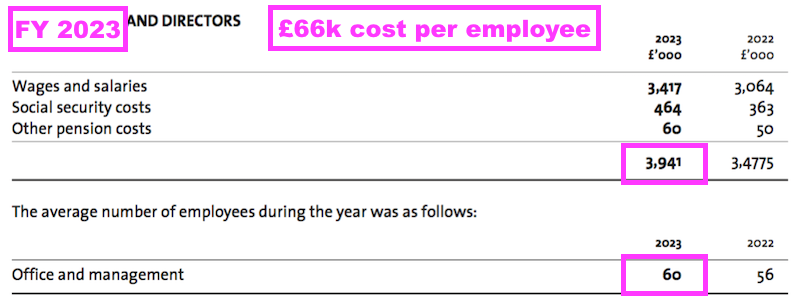

- At least salaries have been kept under control, with a £65k average employee cost during FY 2011 versus a £66k average during this FY:

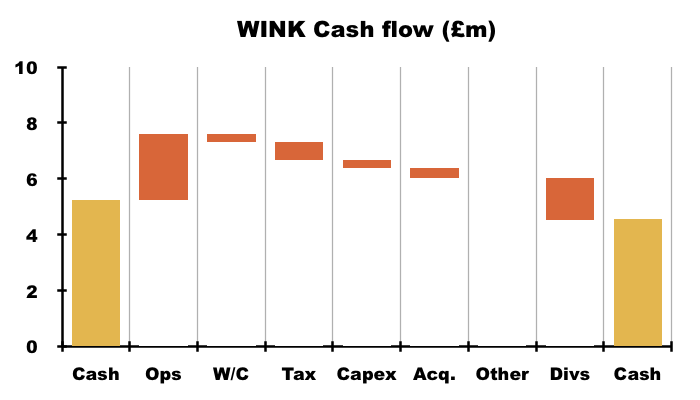

- Cash generation was slightly better than January’s Q4 update had implied. The Q4 update said this FY would show net cash of “at least £4.4m“, but net cash was in fact £4.5m.

- Mind you, reported FY earnings of £1.7m translated into FY free cash flow of only £1.0m.

- The modest FY cash conversion was due to:

- An adverse £0.3m working-capital movement, and;

- Cash payments for capex and tax exceeding the associated accounting charges by almost £0.4m:

- A £1.5m dividend, payments for ‘assisted acquisitions support’ and acquiring the final 10% of Tooting then left FY cash £0.7m lighter at £4.5m (35p per share).

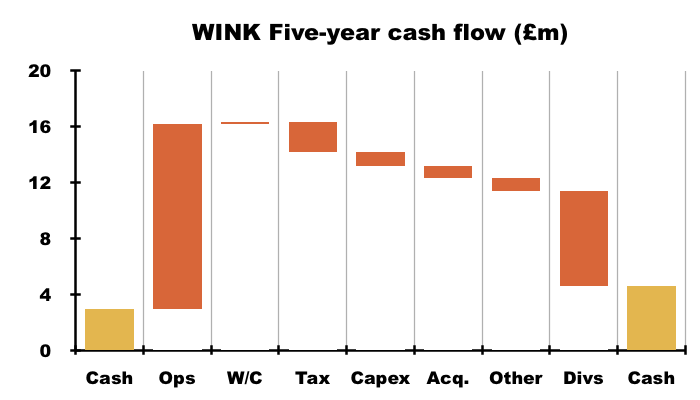

- Over five years, WINK’s cash generation has been very satisfactory. A total £13.2m operating cash flow funded additional working-capital, tax, capex and lease costs of £3.9m to allow bumper dividend payments of £6.8m, acquisitions of £0.9m and net cash to advance by £1.6m:

- WINK’s balance sheet remains free of bank debt and defined-benefit pension obligations.

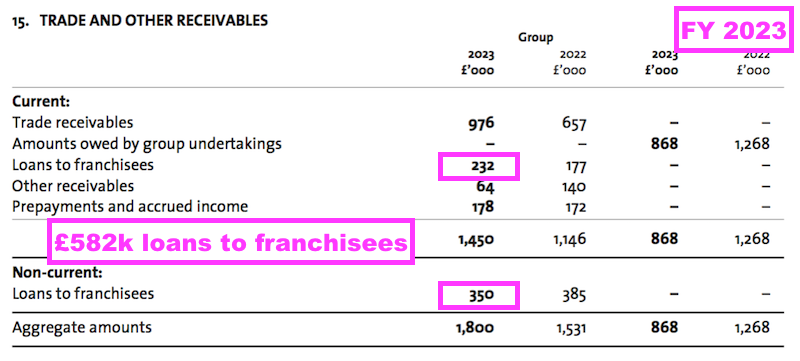

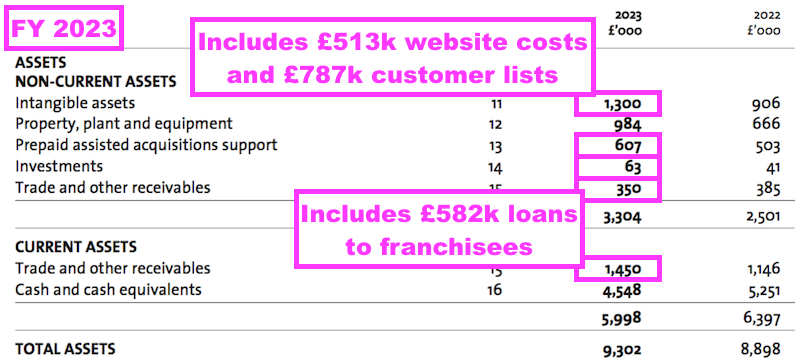

- The balance sheet includes loans to franchisees of £582k:

- Other balance sheet items include capitalised website costs of £513k, mystery investments of £63k and ‘assisted acquisitions support’ of £607k:

- ‘Assisted acquisitions support’ are sums paid by WINK to help franchisees:

- Convert their existing agencies into WINK franchises;

- Launch new WINK franchises in neighbouring locations, and/or;

- Acquire additional businesses (typically lettings portfolios).

- The carrying values of ‘assisted acquisitions support’ (£607k), ‘customer lists’ acquired with Tooting, Crystal Palace and Pimlico (£787k) and capitalised website costs (£513k) amount to £1.9m, all of which has yet to be expensed through the income statement.

- Finance income of £88k was equivalent to a 1.6% return from the £4.9m average FY cash position and the £572k average FY loans to franchisees.

- WINK’s finance income improved from H1 to H2 — £34k versus £54k — which could mean interest on the cash and loans is running at approximately 2%.

- But 2% still seems low, especially as management’s FY webinar confirmed loans to franchisees were paying interest to WINK at a “certain amount over base“.

- The FY webinar also implied monies placed on longer-term deposits might improve the rate of interest during FY 2024:

“The cash balance does fluctuate during the year and typically cash builds up towards the back end — that’s the nature of our business. A lot of the activity comes in Q3, which determines how the year pans out. We’ve put funds on longer term deposits at the back end of the year and that’s something we’re monitoring. We’re balancing our ability to lock up cash for longer periods with our ability to be able to deploy those funds into building the businesses… which may impact our ability to earn interest in the short term but will significantly improve the performance of the business in the longer term.“

- For perspective, NatWest for example offers a 35-day notice business account paying 3.25% AER (variable).

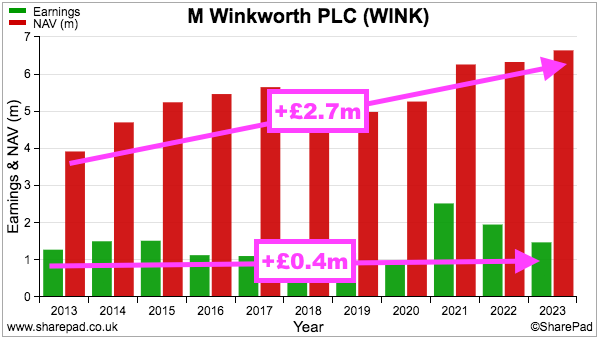

- Despite WINK’s low returns on its hefty cash position, retained earnings over time have delivered a useful incremental profit.

- During the last ten years for instance, net asset value has advanced by £2.7m to deliver additional earnings of £0.4m — an incremental return of 15%:

- Earnings growth seems driven by WINK’s intangible expenditure because net tangible assets remain negligible. This FY showed office and computer equipment with a £73k book value while receivables (excluding franchisee loans) of £1.2m are offset completely by payables (excluding lease liabilities) of £1.4m.

- Emphasising the absence of hefty reinvestment requirements, between FYs 2014 and 2023 WINK reported aggregate earnings of 118p per share of which 100p per share (85%) were declared as ordinary or special dividends.

Valuation

- This FY said FY 2024 had started well for sales but less so for lettings:

“2024 has started more briskly than expected, with our sales agreed to the end of March 23% ahead of 2023, bolstered by mortgage providers reducing rates in anticipation of a rate cutting programme by the Bank of England.”

…

“We have witnessed some price weakening in the rental market with supply increasing (23% ahead of 2023 to end of March 2024) and demand declining (5% behind 2023 to end of March 2024).”

- July’s Q2 update reiterated the positive H1 for sales — which ought to lead to a stronger H2 — while suggesting lettings had also made progress:

“Following expectations that interest rates had hit their peak in January, the sales market picked up significantly in Q1 2024 and, despite rates remaining unchanged, improved sentiment on the UK economy maintained this momentum. Winkworth’s sales agreed in H1 2024 were 19% higher than the comparable period in 2023. With transaction times still extended, however, we would expect many of the sales agreed in H1 2024 to complete in H2 2024.

Lettings activity remained positive in H1 2024, albeit increased sales activity and affordability ceilings having been reached led to a greater supply of rental properties and a fall in applicants.

Preliminary results show H1 2024 network sales up by approximately 8% on H1 2023 and H1 2024 network lettings by approximately 4% compared with the prior year.“

- The Q2 update confirmed further changes to the branch network…

“As planned, in the first half of the year the Company opened three new offices and resold four franchises.”

- ..and indicated FY 2024 pre-tax profit would advance £0.5m to £2.4m excluding negative goodwill:

“The Directors expect pre-tax profits for the year to 31 December 2024 to be in line with market expectations of £2.4 million.“

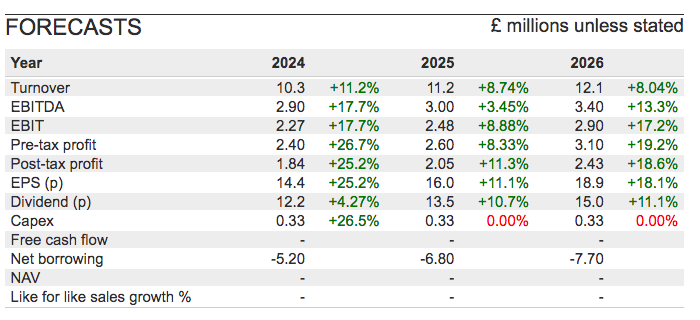

- FY 2024 pre-tax profit of £2.4m compares to £2.5m for (pandemic-boosted) FY 2022, £3.2m for (pandemic-boosted) FY 2021, £1.5m for (pandemic-blighted) FY 2020 and £1.6m for (pre-pandemic) FY 2019.

- £2.4m after standard 25% UK tax gives earnings of £1.8m or 13.9p per share.

- Earnings of 13.9p per share ought to support further quarterly dividends of 3p per share and supply an FY 2024 payout of 12p per share:

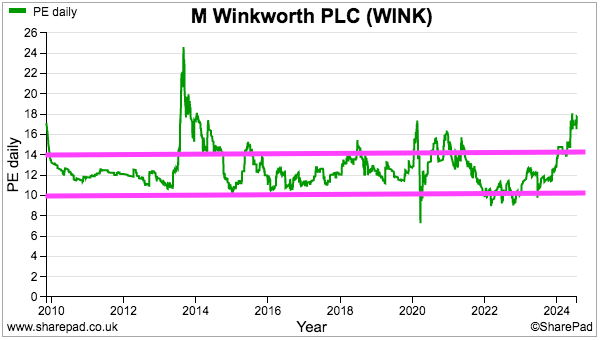

- Dividing the 200p share price by my 13.9p per share earnings guess gives a P/E of 14x.

- Assume the £4.5m/35p per share cash position is not required for the business to operate successfully, the cash-adjusted P/E could be (165p/13.9p) = 12x.

- A multiple of 12x or 14x or somewhere in between is not outrageous, but nor is it beyond WINK’s typical trailing P/E of 10x-14x:

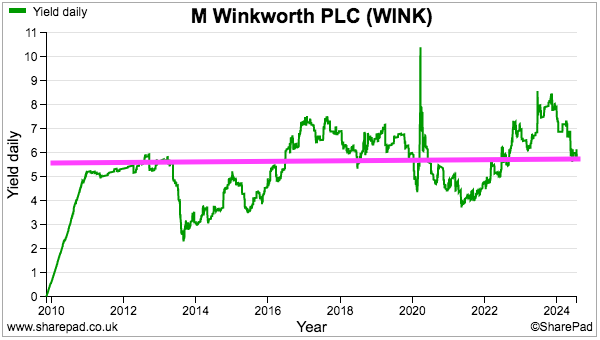

- The likely 12p per share FY 2024 dividend meanwhile supports a useful — but not entirely unusual — 5.7% income:

- WINK’s current rating may not entirely reflect the prospect of double-digit earnings growth during the next few years:

- While revitalised franchisee branches and the occasional Tooting-type investment could underpin near-term progress, longer-term earnings growth might require a fundamental improvement within the wider property market.

- Supporting that earlier FOXT chart, HMRC statistics indicate property transactions nationally have yet to recover from their 2007 heyday — and industry ‘growth’ therefore has since been supported only by higher prices:

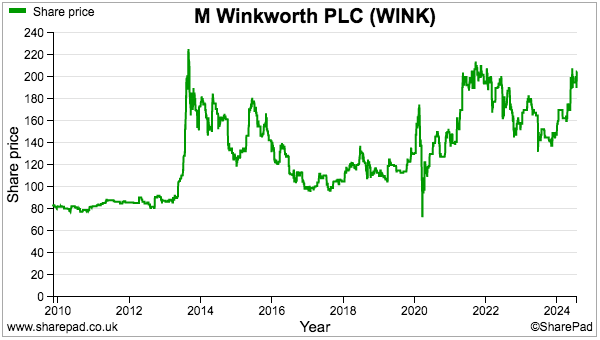

- I first bought WINK during 2011 at 90p and the shares have since delivered a very generous income. Total payouts (ordinary and special) throughout the last 13 years have totalled 120p per share to recoup my entire initial investment.

- Add on the 110p per share capital gain during the same 13 years to those dividends, and my initial 90p purchase has retuned approximately 10% a year:

- 10% a year is an acceptable but not incredible return, and the risks for long-term shareholders hoping for more include:

- Transaction volumes within London and nationally continuing to stagnate;

- Industry ‘growth’ faltering as higher mortgage rates diminish property valuations;

- Openings and closures within WINK’s franchise network combining to yield minimal extra earnings, and;

- Group margins weakening further due to lower workforce productivity and/or greater fixed costs within the company-owned offices.

Potential bid target?

- WINK’s chairman concluded this FY by referring to his 50-year tenure:

“At our AGM in May 2024, I look forward to celebrating my half century at the helm of Winkworth and next year’s 190th anniversary of the Company’s foundation – milestones which I believe are a testament to our enduring legacy.”

- The half-century AGM celebrations took place at The Lansdowne Club in Mayfair, which seemed a lavish alternative versus the usual head-office event.

- Celebrating 50 years of leading WINK invites speculation about succession planning and bid potential.

- After all, the chairman is 81 years old and, after having bought WINK outright during 1974, still retains a 41%/£10.6m shareholding.

- Will his 41% stake one day be handed to other family members? Possibly — WINK’s chief exec (a 6%/£1.5m shareholder) is the chairman’s son and presumably would still run the group on behalf of the family.

- But could WINK be sold?

- WINK announced two intriguing new non-execs during June:

“M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce the appointments of Tom Fyson and Jonathan Adams as Non-Executive Directors of the Company, and as members of the Audit Committee and Remuneration Committee respectively, with effect from 4 June 2024.”

- Both new non-execs currently work as business consultants with M&A knowledge:

“Tom Fyson is a Managing Director of Blackdown Partners, an independent advisory firm providing public and private businesses with advice on corporate finance, M&A, capital markets, investor relations and strategy. He brings over 20 years of financial experience, having begun his career at KPMG, where he qualified as a chartered accountant, before moving into corporate finance in 2006.

Jonathan Adams spent 14 years in M&A and as an equity analyst at JPMorgan before working as a global fund manager, initially at Citigroup and, subsequently, for 16 years at Investec. In 2022, he founded Butterwalk Advisory LLP, providing advice to, and investing directly in, small cap companies. He is a Senior Advisory Board Member to King’s College Cambridge’s Entrepreneurship Lab, a privately funded body with the goal of increasing awareness of entrepreneurship amongst its student membership. “

- Hiring two non-execs with M&A knowledge may well be a response to the recent merger between Property Franchise (TPFG) and Belvoir — two major lettings-agency franchisors each with long acquisition histories.

- Among TPFG’s earlier acquisitions was Hunters Property, a property franchisor purchased for a £29m enterprise value during 2021.

- Hunters enjoyed network income of £43m, revenue of £12.5m and an adjusted profit before tax of £2.8m before becoming part of TPFG.

- Shortly after the Belvoir merger completed, last month TPFG announced the £20m purchase of property-marketing specialists The Guild of Property Professionals and Fine & Country. TPFG stated at the time:

“The Acquisition fits within the Group’s strategy to acquire accretive businesses with complementary and recurring revenue streams which deliver network expansion and geographic growth“

- WINK could certainly deliver network expansion and geographic growth for TPFG.

- TPFG’s network presently includes more than 900 franchises, of which approximately 100 are located within London.

- WINK’s 53 or so franchisee branches (alongside its three company-owned offices) within London would certainly strengthen TPFG’s exposure to the capital.

- Whether TPFG would actually want to own WINK remains to be seen.

- And even if TPFG was amenable to a deal, could TPFG then offer a suitable premium to WINK’s current £25.8m market cap?

- TPFG may not be the only potential bidder for WINK. Recent years have witnessed consistent sector M&A.

- The likes of Leaders Roman (120-plus acquisitions since 2010) and Lomond (40-plus acquisitions since 2021) for example have consolidated smaller agencies through the support of private equity, with Leaders Roman sold for £188m during 2022 and Lomond reputedly looking for a buyer paying “well in excess of £100m“.

- London agent Chestertons meanwhile was sold for a reported £100m last year to a French property-services group, while fellow London agent Dexters was subject to a mooted £130m investment by private-equity firm Oakley Capital during 2021.

- Of course, any deal for WINK is dependent on whether the chairman would actually want to sell.

- I nonetheless speculate at least one trade buyer should be attracted to this profitable, cash-rich franchisor operating within London and southern England…

- …where a premium take-out valuation could be justified by removing listing costs, unprofitable ventures and less-productive employees.

Maynard Paton

M Winkworth (WINK)

Publication of 2023 annual report

Here are the points of interest beyond those noted in the blog post above:

1) CHAIRMAN’S STATEMENT

A few snippets here.

A comment about how customers may still employ WINK some 30-plus years after their first property purchase/rental:

“With my 60 years’ experience in the business, I believe the creation of long-term goodwill generated by quality franchisees builds the strength of the brand and enables us to benefit from that goodwill as our network expands. Over the years, we have nurtured the relationship with our customers and people who began by purchasing their first property through us in the 1970’s or renting through us as of the 1990’s, are now still dealing with Winkworth as they approach retirement.”

I must admit I am not entirely convinced about such long-term loyalty to estate agents. Perhaps there is some loyalty to the actual agent, but not to the brand. For the typical owner-occupier, property transactions are conducted very infrequently and a ‘beauty parade’ of agents is normally undertaken.

A mention of AI:

“Our franchisor organisation and accounting systems have grown substantially since we started franchising in 1981 and we now consider it is time to integrate AI into the group accounting process to eliminate some of our semi-manual processes. This will free up more time for financial compliance and speed up cash flow.”

Not sure AI should be used for accounting processes. “Semi-manual” processes ought really to be eliminated by standard IT procedures.

And a mention of WINK’s new executive director:

“Finally, as alluded to at the time of our interim results, we have taken the first step towards reviewing the composition of our board and broadening its expertise. This initiative is aimed at ensuring the future leadership structure supports the continued success of the Company and its stakeholders.

This process began in February 2024 with the appointment of Tara Tan as an executive director. Tara provides strategic and transactional guidance to the business development team and to the day-to-day commercial operations team, as well as overseeing brand protection, network compliance and training. As our efforts progress, we anticipate making further announcements in due course.”

I can’t recall mentioning the new director on my blog. So here is the announcement:

————————————————————–

“M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce the appointment of Tara Tan to its Board as an Executive Director with effect from 12 February 2024.

Tara, a qualified solicitor with over 20 years’ experience, joined the Winkworth team in 2001 and became a director of Winkworth Franchising Limited (“WFL”) in 2004 as Director of Legal and Business Affairs. Tara stepped down from WFL and left the Company in 2006 to focus on other interests. She re-joined in 2012 as a consultant, and in 2014 was appointed to work full time as General Counsel before re-joining the Board of WFL in 2020.

Tara will provide strategic and transactional guidance to the business development team and to the day-today commercial operations team, as well as continuing her work on brand protection, network compliance and training.

Commenting on Tara’s appointment, Simon Agace, Non-executive Chair of Winkworth, said: “Tara represents a fresh approach to helping franchisees manage compliance by combining training with a more aligned compliance team consisting of industry, legal and financial professionals. The aim is to offer better protection to Winkworth and its franchisees in a competitive industry facing increasing regulation.”

Commenting on her appointment, Tara said: “Winkworth is a heritage brand to whose success I and many at Winkworth, both as franchisees and franchisor, have devoted our careers. For me it has been almost 20 years of close involvement with the Company, so I am delighted with the opportunity to further develop and grow the business.”

————————————————————–

I note 20 years of “close involvement” with WINK have resulted in Ms Tan owning 3,522 shares.

2) GROUP STRATEGIC REPORT

a) Cost of sales

A reminder that cost of sales includes legal expenses for renewing — and in this case, terminating — agreements with franchises:

“Cost of sales were in line with 2022 with the increased legal costs associated with the settlement agreement with the former franchisee in Battersea, Clapham, Pimlico and Kennington Lettings offset by various cost reductions.”

b) Administrative expenses

The advantage of a pure franchise operation for shareholders is the franchisee takes on responsibility for their employees and their pay. With company-owned branches, WINK now suffers greater exposure to salary inflation with perhaps no reciprocal benefit to revenue:

“The cost of living crisis impacted the business and the increase has been largely driven by the increased salary and on costs in both the franchising business and in the Corporate owned offices that supported their development, and the general inflationary impact on costs.”

c) Working capital

This text is confusing:

“The reduced profitability and deferred payment terms for certain debtors meant that our working capital levels decreased from 2022, and we had cash balances of £4.55m at the year end (2022: £5.25m). We continue to have no external debt.”

I calculate working-capital levels increased on 2022 by £427k (current receivables were £1,450k versus £1,146k while current payables were £1,556k versus £1,575k). Mind you, WINK still operates with £106k greater current payables than receivables, so the general working-capital profile remains appealing.

The text “deferred payment terms for certain debtors” is new for 2023 and implies some franchisees have cash-flow issues. Note 15 shows trade receivables up 49% from £657k to £976k despite revenue remaining broadly flat. The £0.3m adverse working-capital movement referred to within the blog post above appears to have been caused by these “deferred payment terms“… i.e. franchisees being given extra time to pay.

3) PRINCIPAL RISKS AND UNCERTAINTIES

Some changes here for 2023.

a) Geopolitical developments

A reworded risk that essentially warns of interest rates remaining higher for longer and a “cost of living crisis“:

“Geopolitical tensions and conflict may reignite inflationary pressures, potentially keeping interest rates elevated compared to past decades. In the UK, increased finance costs for both new homebuyers and existing homeowners seeking to refinance their mortgages amid a cost of living crisis could adversely affect housing prices and transaction volumes.”

Alongside WINK’s “long history” and “conservative management“, a “balanced model” is now also cited as mitigation against adverse economic events:

“Winkworth’s balanced model between sales and lettings revenues provides protection against downturns in either market.”

b) Competition

Another reworded risk that now suggests online agents are no longer the threat they were once perceived to be:

“While the growth in market share of online estate agents appears to have stabilised, the emergence of innovative or discounted service models may exert pressure on commissions, potentially leading to reduced revenues for the company.”

c) Sales market

A reworded mitigation against the possibility of fewer property transactions, particular in WINK’s main London market:

“We have strong local market knowledge and expertise, both in London and in the country markets, and we commit to maintaining competitive fees while delivering unparalleled service to meet our customers’ needs. We strive to cultivate trust and confidence, fostering enduring relationships and earning recurring business.”

d) Lettings market

A reworded mitigation against the possibility of adverse rental regulations:

“We aim to expand our portfolio of rental properties by providing landlords with top-tier service and striving to equitably meet the needs of both landlords and tenants.”

e) Recruitment of franchisees and the building of franchises

No text changes, but a reminder of a “robust…selection process” for new franchisees:

“Winkworth has a new franchising department which runs a robust marketing and selection process. The department verifies the suitability of its prospective franchisees and provides ongoing training and monitoring once new franchisees are accepted into the Group. The Board monitors the performance of the new franchising team and is focused on identifying innovative ways of attracting successful new franchise owners.”

f) Reputational risk

This text from 2022 has been removed for 2023:

“Whilst Winkworth conducts extensive checks on the suitability of its prospective franchisees, it cannot be entirely certain that a franchisee does not have some potentially embarrassing adverse history which may come to light and which risks damaging the reputation of the brand.”

The removal reads as if WINK no longer “conducts extensive checks“. Or maybe WINK is now “entirely certain” it can unearth any “potentially embarrassing adverse history“.

Other parts of the text have been reworded, but still emphasise “brand and reputation“:

“The essence of Winkworth’s franchise proposition lies in its brand and reputation. The manner in which both Winkworth and its franchisees engage in business and deliver services can significantly influence financial outcomes. Any shortfall in meeting the needs and expectations of sellers, buyers, landlords, and tenants by franchisees could significantly affect Winkworth’s overall business, operations, and financial health. Moreover, non-compliance with regulations, legislation or best practice also poses a risk to Winkworth’s brand and reputation.”

As before, not every franchisee applicant is successful:

“Winkworth has a rigorous vetting procedure for new franchisees and only a small number of applicants are successful in joining the group. Once accepted, franchisees are closely monitored to make sure that they achieve the best practice service levels expected of them and remain compliant with the law. Winkworth provides regular training through it’s centralised in-house training academy, alongside which it runs regular compliance audits of franchisee offices, both remote and in-person.”

g) Legal & regulatory environment

Another reworded risk, emphasising the importance of “brand and reputation” again:

“The legal and regulatory environment in which Winkworth operates is changing and evolving. Winkworth must stay abreast of these changes, ensuring compliance while also proactively navigating situations or behaviours that could potentially harm its financial stability, brand integrity, and reputation.”

h) Digital infrastructure and IT risk

Another reworded risk, which reiterates IT giving a “crucial competitive edge“:

“Winkworth’s IT and digital infrastructure serves as the backbone connecting our network, providing a crucial competitive edge. Nevertheless, it also entails reliance on IT systems, technology, and external suppliers, thereby exposing us to potential risks. These risks encompass technical malfunctions and the escalating menace of cyber-attacks.”

i) Public health

Text about the risk of Covid-19 has been removed.

4) SECTION 172

a) Shareholders

Always good to see shareholders listed as the first stakeholder in a 172. The 2023 text was enhanced:

”We value the significance of our partnership with shareholders and are committed to fostering long-term investor loyalty. To achieve this, we prioritise consistent communication by providing regular updates on market insights, our strategic positioning, and our financial returns.”

Pleased to see the board still values the AGM…

“Acknowledging the significance of the AGM, the board views it as an occasion to engage with private shareholders. Directors make themselves available for informal discussions with shareholders immediately after the AGM to hear their perspectives.”

…although the text does read as if the directors are averse to formal questions during the meeting. I last attended a WINK AGM during 2016, and I really ought to attend another.

b) Franchisees

A slightly awkward text change for 2023.

The 2022 text said the purchase of company branches was not a “departure from our traditional franchising approach“:

“Meetings are held with representative groups of franchisees to share their input on key strategic and operational issues. The ownership of Tooting Estates Limited and Crystal Palace Estates Limited, whilst not representing a departure from our traditional franchising approach, will improve our own awareness of day-to-day market issues and their impact on customers, suppliers and other stakeholders.”

But for 2023 the company-owned branches are now “aligned with our established franchising model“:

“We convene meetings with select groups of franchisees to gather their perspectives on important strategic and operational matters. The acquisition of Tooting Estates Limited and Crystal Palace Estates Limited, although aligned with our established franchising model, has enhanced our understanding of ongoing market dynamics and how they affect our customers, suppliers, and other stakeholders.”

I must admit I am still not clear whether the company-owned branches are primarily to give WINK insight into front-line estate agency, or primarily used for proving grounds for would-be franchisees, or are simply investments. Probably a mix of all three.

c) Customers

Reworded text that once again emphasises the importance of WINK’s “brand“:

“In a highly competitive environment, securing and retaining customers is paramount. Winkworth places significant value on the integrity of its brand, upholding it through exemplary standards of ethics and business conduct in all interactions. Through bolstering its digital footprint, the company is actively adapting to exceed the changing demands of both franchisees and their clientele, ensuring continued satisfaction and relevance.

d) Community and environment

WINK’s environmental commentary was limited to the following:

“Winkworth is a carbon neutral company. Our Corporate Carbon Footprint (CCF) has been independently calculated and we are continuously reducing our carbon emissions while offsetting unavoidable ones through carbon offset projects.

– Encourage involvement in local communities across our network.

– Rotate the charities that we support to match the footprint of our business and the communities that we operate in.

– Promote the Eden Greenspace system to offices, allowing them to allocate a percentage of their fees to a number of different environmental projects in the UK and across the globe.

Community and environment

The Company priorities the awareness of how its operations affect both the community and the environment. It sets high standards for both its employees and suppliers, expecting them to adhere to stringent guidelines in their daily business practices.”

The minimal text contrasts with the pages of ESG commentary and emissions statistics published by other quoted companies. The difference I suspect is due to WINK being quoted on AIM and not the main market. Details of the CCF noted in the text were not published in the 2023 report.

5) REPORT OF THE DIRECTORS

Once again a very short director report, which on the one hand is saving time and money, but on the other gives very little away to outside shareholders. As long as the business performs satisfactorily, I hope the directors continue to save time and money.

a) Compliance with the QCA Code

I never like companies referring to their websites for QCA matters. They should put the QCA commentary in their annual reports, which allows shareholders to look back for any changes made from year to year:

“As mentioned in the Chairman’s Statement on Corporate Governance, Winkworth adheres to the QCA Code on Corporate Governance. Full details of how the ten principles have been applied are shown on our website http://www.winkworthplc.com. The website was reviewed for compliance with the QCA Code on 26 March 2024 and was updated accordingly.”

Here is the QCA link.

A few snippets:

Re-emphasising the board’s cautious approach:

“Winkworth looks to grow its franchise network and add like-minded entrepreneurial franchisees and offices to the network. Not, however, through growth at any cost, as new franchisees need to adhere to the Winkworth brand values. We also have a conservative approach to financing expansion.”

A line about the group’s competitive positioning:

“Winkworth plans to remain competitive in the current market by operating a model that emphasises our premium, pro-active service through :-

* Good, experienced agents with strong local area knowledge; and

* A visible high street presence.”

WINK does not employ a formal nominations committee, although the text below reads as if the Agace family (chairman Simon and CEO Dominic) is effectively that committee:

“The Board is supported by the Audit and Remuneration Committees. Given the relatively small size of the Board, this as a whole fulfils the responsibilities of a Nominations Committee with the Chair and CEO leading on the board nomination and appointment process.”

Best practice these days is the directors seek re-election every year:

“All continuing Directors stand for re-election every three years.”

Another line about the group’s competitive positioning:

“With our people-based ethos and as a premium, customer-focussed business dependent on its reputation, we understand that our success depends on everyone working under the Winkworth brand doing so with respect, loyalty and pride. All our offices need to ensure we exceed our customers’ expectations by delivering the highest quality service at all times so that our customers not only return, but also share their experience with other potential customers.”

b) Composition, experience and training

Text confirming the 3%-plus shareholding of non-exec Lawrence Alkin:

“Whilst Lawrence Alkin owns more than 3% of the Ordinary Shares of M Winkworth PLC, he is considered to be independent…”

A sad RNS during February announced the death of Mr Alkin. WINK’s website shows a 3.1% holding. Will be interesting in time to see where this 3.1% ends up, if the beneficiaries do decide to sell. WINK is a very illiquid share and the 3.1% can’t just be dumped into the market. Could a trade buyer be willing to take on the 3.1%?

c) Time commitments, meeting attendance and board-committee reports

Non-execs are still expected to put in 15 days a year. Eleven board meetings were held in 2023, with only Mr Alkin missing one meeting. He missed two of ten in 2022. Nice to see three audit meetings versus one remuneration meeting, as per 2022.

The board’s committee reports were the same short efforts from the previous year.

Remuneration: “The Committee, chaired by Lawrence Alkin and with John Nicol in attendance met in December to discuss and approve certain bonuses in respect of 2023 and the 2024 remuneration of the Executive Directors and key senior managers in the group.”

Audit: “The Committee, chaired by John Nicol, and with Lawrence Alkin in attendance met three times in 2023. In March the Committee met with Crowe to discuss and approve the 2022 Accounts and to review the Audit. In September, the Committee met to discuss and approve the 2023 Interim results and Announcement. In December, the Committee met to discuss Risk and approve the Accounting Policies.”

6) REPORT OF THE INDEPENDENT AUDITORS

No major changes here for 2023.

a) Materiality and scope

Materiality still at 5% of three-year average pre-tax profit:

“Based on our professional judgement, we determined overall materiality for the Group financial statements as a whole to be £128,000 (2022: £120,000) based on 5% of the average profit before tax over the 3 financial years to the reporting date, a benchmark chosen to normalise the effects of the Covid-19 pandemic on the Group.”

A full-scope audit is undertaken by group auditor Crowe on the main franchising subsidiary, while Tooting is audited by separate auditor Duncan & Toplis:

“The parent company and Winkworth Franchising were subject to full scope audit by ourselves, Tooting Estates was audited by a component auditor.”

b) Key audit matter

The single key audit matter remains revenue recognition and “completeness“, the latter referring to the possibility some franchisees may not declare all of their commissions to WINK:

“There is a risk that revenue is receivable and not recorded, especially due to the under reporting of revenue on the part of franchisees. Therefore there is a potential risk in terms of the completeness of revenue being recognised…”

I understand payments by customers to franchisees for property sales are handled by WINK’s IT system, so any under-reporting of commissions will either involve i) payments for property sales accepted through different methods, or more likely ii) rental payments.

7) ACCOUNTING POLICIES

a) Revenue

A reminder that WINK earns a flat 8% of franchisee sales and lettings commissions:

“The group earns a straight 8% by value on all sales and lettings income generated by the franchisees.”

b) Intangible assets

Ah, website costs that were amortised over 3-6 years but were changed for 2022 to 6 years… are now back to 3-6 years:

“The website development costs are amortised over their useful life which is deemed to be 3 to 6 years. Customer lists are amortised over 15 years on a straight line basis.”

I generally view website costs as just another ongoing cost that should be expensed as incurred.

That said, WINK’s website-development accounting is not really material to the group. During the last five years for example, total operating profit has amounted to £10.4m while website costs of only £442k have effectively bypassed the P&L onto the balance sheet.

Customer lists — essentially an intangible to reflect the acquired value of existing clients at Tooting, Crystal Palace and Pimlico — are still amortised over 15 years. I presume this lengthy timescale reflects the longevity of landlords serviced by WINK’s branches generally. The customer-list accounting can give some indication as to the revenue of the acquired branch (point 20).

c) Prepaid assisted acquisitions support

A reminder that prepaid assisted acquisitions support is essentially ‘goodwill’ paid to franchisees to start/acquire/expand their business:

“Prepaid assisted acquisitions support represents amounts paid to franchisees on the incorporation of their business into the Winkworth brand. The amounts paid to franchisees are contributions towards their growth plans, which in turn will grow the Winkworth brand.

Amounts paid to franchisees are amortised over the initial 10 year franchise agreement on a straight-line basis as a reduction in revenue.”

One notable change to this text for 2023 is the absence of this line:

“They are tested for impairment at each reporting date by reference to the financial performance of the relevant franchise.”

This absence implies the support expenditure is no longer assessed for write-offs. I trust this missing line is an oversight, rather than WINK not being straight with shareholders. Such capitalised expenditure should be assessed every year and impaired if necessary.

d) Property, plant and equipment

Ah, another change back to a 2021 accounting policy, this time for the depreciation rate of fixtures and fittings:

“Fixtures and fittings – 25% straight line”

The rate was previously between 15% and 33%. Fixtures and fittings have a minuscule £64k book value.

e) Financial instruments

All new text for 2023:

“Basic financial assets, including trade and other debtors and cash and bank balances are initially recognised at transaction price, unless the arrangement constitute a financing transaction, where the transaction is measured at the present value of the future receipts discounted at a market rate of interest.

Debt instruments are subsequently carried at amortised cost, using the effective interest rate method.

Trade creditors are obligations to pay for goods or services that have been acquired in the ordinary course of business from suppliers. Accounts payable are classified as current liabilities if payment is due within one year or less. If not, they are presented as non-current liabilities. Trade creditors are recognised initially at transaction price and subsequently measured at amortised cost using the effective interest method.”

Seems quite standard.

f) Critical accounting estimates and judgements

Unchanged from 2022, various percentages that explain the valuation sums for intangible customer lists (point 20):

“The valuation of customer lists was based on industry multiples of 150% of the historic lettings revenue and 100% of the sales revenue, discounted by 30% for lettings and 70% for sales revenues, to reflect the future prospects and inherent goodwill relating to the staff of the business. An assumption has been made that cash flows from the lettings business will fall by7% per annum.”

Assuming lettings cash flow will fall by 7% a year seems quite pessimistic.

8) EMPLOYEES AND DIRECTORS

Director pay has started to appear awkward:

The chief exec’s combined salary/bonus advanced 6% from £249k to £264k… despite this FY’s operating profit (excluding negative goodwill) sliding 25% to £1.8m.

That said, between 2018 and 2023, the chief exec’s combined salary/bonus has advanced 66%, while the ordinary dividend has gained 57% from 7.45p to 11.7p plus there has been special payouts totalling 7.7p.

Arguably shareholders have therefore seen their total income appreciate in line with the chief exec’s income, so the issue of rising boardroom pay has not become critical just yet. But I think the matter will continue to simmer, especially if group profit remains stagnant.

Note that total board pay was £601k, up 12%, and was significant versus the overall £1.8m operating profitability of the business. For perspective, during 2015 when operating profit was also £1.8m, the board was paid a total £330k.

The two execs finished 2023 owning 387k options, which represent all of WINK’s outstanding options.

Once again WINK has not calculated an options charge against profit. Options at year-end represented 3.0% of the share count and their IFRS 2 cost I am sure would have been greater than zero. Indeed, the chief exec exercised 102k options during 2023 at 102p, and with the shares on that day at 142p, he earned a useful £43k. That £43k is now worth more than £100k with the shares at 200p-plus.

9) PROFIT BEFORE TAX

Audit fees remain at £69k or 0.7% of revenue, which is not a low percentage going by this ad-hoc audit comparison from the other year.

A slight presentation revision this year clarifies the non-audit fees, which remain relatively high compared at £31k to the £69k audit cost. Non-audit fees are typically tax related, and good practice is to keep non-audit fees low to ensure there is no undue ‘influence’ on the auditor.

10) TAXATION

Taxation is not my strong point, but I am pleased this FY’s adjustments are not significant:

Pretty sure the £59k adjustment relates to the £252k negative goodwill.

11) INTANGIBLE ASSETS

Details of the acquired customer lists and capitalised website costs:

For the customer lists, amortisation of £51k = 6% of the average original £815k cost ((£643k+£986k)/2) and underlines the c15-year amortisation timescale.

But for the website costs, amortisation of £120k = 12% of the average original £980k cost ((£869k+£1,091k)/2) and suggest perhaps an 8-year amortisation timescale… albeit the stated useful life is 3-6 years. Still, the sums involved have been relatively small versus the group’s overall profit (point 7b).

12) PROPERTY, PLANT AND EQUIPMENT

Details of the (very low-value) tangible assets (point 7d):

A book value of £77k for computers and office equipment compares to a £1.8m operating profit — WINK is not a business that requires hefty capex to grow!

13) PREPAID ASSISTED ACQUISITIONS SUPPORT

Details of the prepaid assisted acquisitions support (point 7c):

Amortisation of £113k was exceeded by actual cash expenditure of £217k.

Perhaps reflecting optimistic industry conditions, total prepaid support for 2022 and 2023 was £533k versus a total £457k for the seven years to 2021. So a step-change to prepaid support expenditure, which may or may not be bullish for shareholders. The £607k net book value of prepaid support compares to £1m for 2014, so WINK has spent large prepaid support sums before.

Prepaid-support investments therefore may not always be successful. There was a £66k prepaid-support impairment for 2020 and a somewhat sneaky £106k net disposal in 2016, whereby capitalised prepaid-support of £106k was seemingly sold for zero. A similar £17k disposal occurred during 2018.

14) INVESTMENTS

Quoted investments gained 54% during 2023:

The 54% gain followed a 44% loss in 2022. I guess this small portfolio is employed for reasons beyond purely financial.

Always worth keeping an eye on the operational subsidiaries listed in the report.

WINK’s development and commercial (DCI) subsidiary reported sales of £349k and a thumping £245k operating loss for 2023 (Companies House).

Crystal Palace showed retained losses increasing from £198k to £277k for 2023, so perhaps an operating loss of c£100k given the tax charge was £20k (Companies House).

Lumley 1 (Pimlico) reported maiden retained earnings of £187k for 2023, which was due entirely to the £252k negative goodwill (Companies House). Pimlico scored a £82k pre-tax loss before the negative goodwill (point 20).

Tooting reported a profit before tax of £296k for 2023, versus £378k for 2022 (Companies House).

I wrote in the blog post above: “I cannot reconcile WINK reporting a group £2.1m pre-tax profit when the main franchising subsidiary reported a £2.3m pre-tax profit and the company-owned offices were said to have delivered a £0.48m pre-tax profit.”

I suspect I did not account for the £252k negative goodwill within that £0.48m. My rough sums suggest DCI, Crystal Palace, Pimlico and Tooting contributed an aggregate c£131k loss for 2023, which with the negative goodwill included gives a £121k profit.

That said… I can’t reconcile WINKs stated £480k profit for the company-owned offices:

“The Winkworth-owned offices, Tooting Estates Limited, Crystal Place Estates Limited, the newly acquired Lumley 1 Limited [Pimlico] and Winkworth Development and Commercial Investment Limited, contributed revenue of £2.69 million (2022: £2.78 million) and £0.48 million (2022: £0.57 million) of profit before tax.“

If Tooting reported £296k and Pimlico reported £170k (point 20) and DCI reported (£245k), I get £221k. There is no way Crystal Palace then achieved £259k profit to arrive at £480k, when its 2023 accounts suggest to me a £100k operating loss.

Clearly I am missing something, and I perhaps understand why WINK has been reluctant to publish proper divisional profits within the accounts:

15) TRADE AND OTHER RECEIVABLES

This note highlighted the impact of the aforementioned “deferred payment terms for certain debtors” (point 2c):

Year-end trade receivables at £976k are equivalent to 10.5% of revenue — the highest percentage since 2016 (11.5%) and before that 2012 (11.6%). For the prior three years, the percentage was a remarkably consistent 7.1%. Would be useful to understand if certain franchisees are struggling with cash flow.

This line still suggests WINK does not give up on late payers until the very end:

“Impaired receivables are only written off following the conclusion of administration proceedings.”

The provision for doubtful unpaid invoices increased by £39k to £118k, which is not ideal but the provision was c£300k for both 2018 and 2019.