04 November 2022

By Maynard Paton

Results summary for M Winkworth (WINK):

- An acceptable H1 performance that would always struggle against the comparable (and exceptional) H1 but encouragingly matched the preceding H2.

- The subsequent Q3 update provided reassuring ‘mini-budget’ commentary, reiterated an earlier £2.1m profit forecast and announced a further 23% quarterly dividend lift.

- Claims of a leading SSTC market share may contradict statistics from Foxtons, with fresh leadership at the London rival set to create stiffer competition.

- A robust 25% margin plus £4m net cash left the accounts in good order, although cash conversion was impacted by rising intangible expenditure and more franchisee loans.

- The gloomy outlook for the economy and housing market looks responsible for the possible 10-13x P/E and yield that approaches 7%. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- Franchisee sales and lettings income

- Winkworth versus Foxtons

- Corporate-owned offices

- Financials

- Valuation

News links, share data and disclosure

News: Interim results, presentation and webinar for the six months to 30 June 2022 published/hosted 07-08 September 2022 and dividend declaration published 12 October 2022

Share price: 160p

Share count: 12,733,238

Market capitalisation: £20.4m

Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, with progress buoyed by motivated franchisee owners building their own local agencies and capturing greater market share.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments.

- Seasoned family management boasts £10m/47% shareholding and rewards investors through durable quarterly dividends and occasional special payouts.

Further reading: My WINK Buy report | All my WINK posts | WINK website

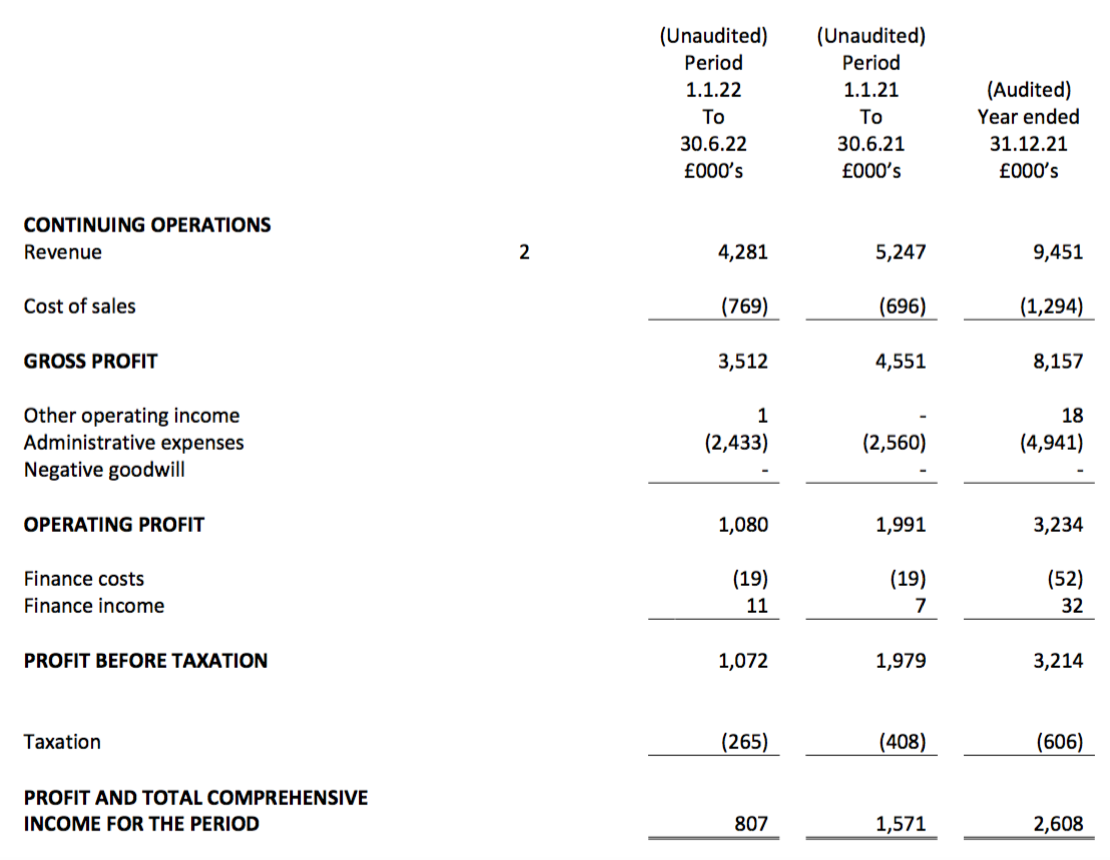

Results summary

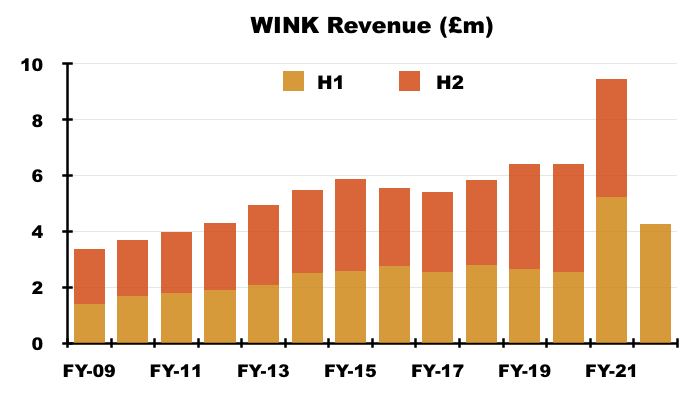

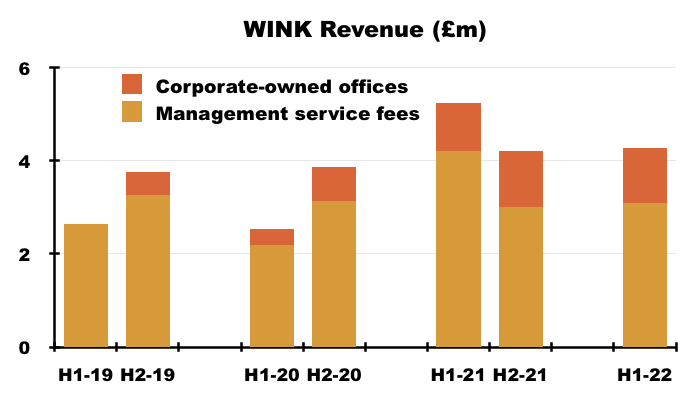

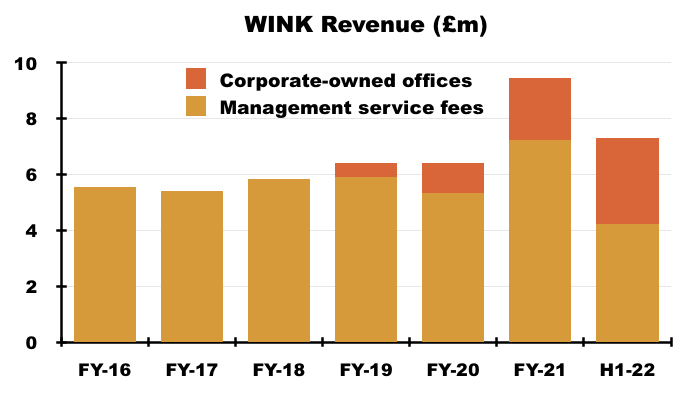

Revenue, profit and dividend

- These H1 2022 results were always going to struggle against the comparable H1 2021 that enjoyed an “extraordinarily active” sales market.

- The absence of “pandemic-induced buyers” and stamp-duty holidays prompted WINK to reveal during July that franchisee sales income had dropped 40%.

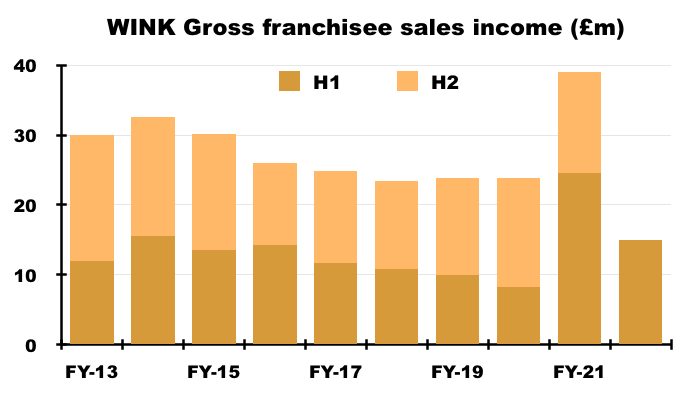

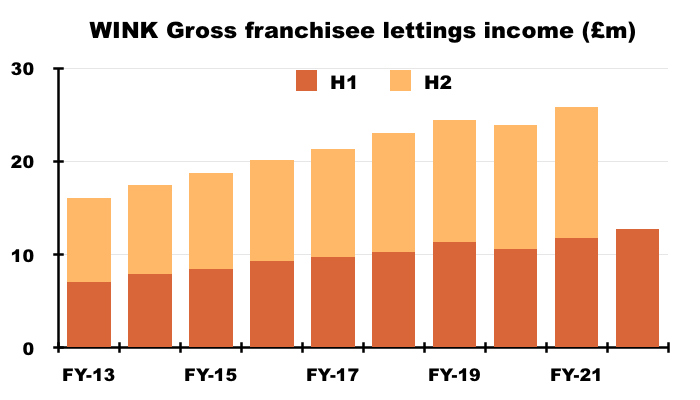

- This statement confirmed franchisee sales income fell 39% to £15.0m while franchisee lettings income, said by WINK during July to have advanced 6%, in fact gained 8% to £12.7m:

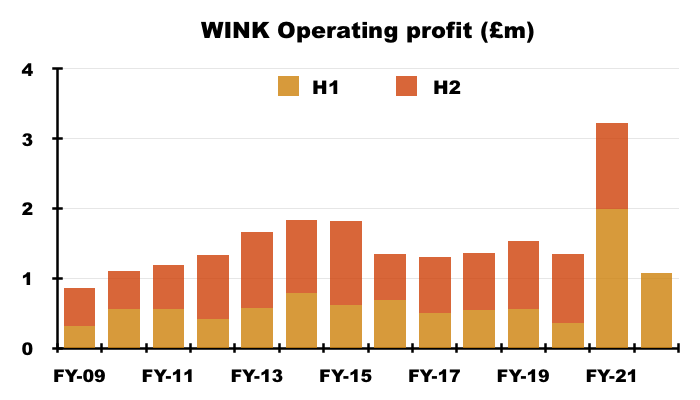

- The franchisees’ efforts translated into H1 revenue declining 18% and H1 reported operating profit diving 46%:

- Despite the hefty shortfalls versus H1 2021, this H1 delivered a similar performance to the preceding H2 2021 and a significant improvement versus the pre-pandemic H1 2019.

- Progress was not complicated by exceptional items, with non-trading charges limited only to a £20k investment write-down.

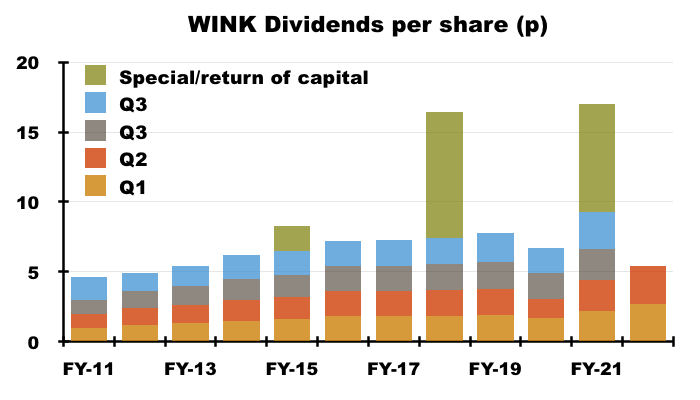

- WINK’s FY 2021 results and July’s trading update had already heralded quarterly dividends that totalled 5.4p per share for this H1:

- Rather impressively, total ordinary dividends of 5.4p per share are 23% higher than the 4.4p per share ordinary payout for the comparable bumper H1 2021.

- Mind you, the comparable bumper H1 2021 included two special dividends (1.3p and 2.6p per share), with a third special (3.8p per share) announced during the subsequent H2.

- No specials have been declared to date for FY 2022.

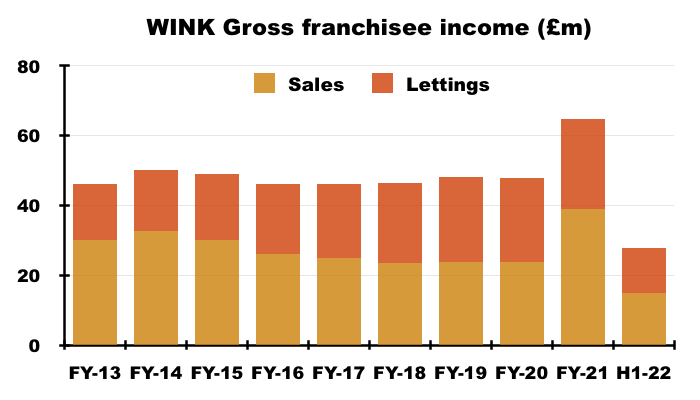

Franchisee sales and lettings income

- WINK’s franchisee network consists of 103 estate-agency branches located throughout London and south-east England.

- Franchisees pay WINK a straight 8% of all of their sales and letting income, plus variable sums towards IT, training, landlord/tenant referrals and other services.

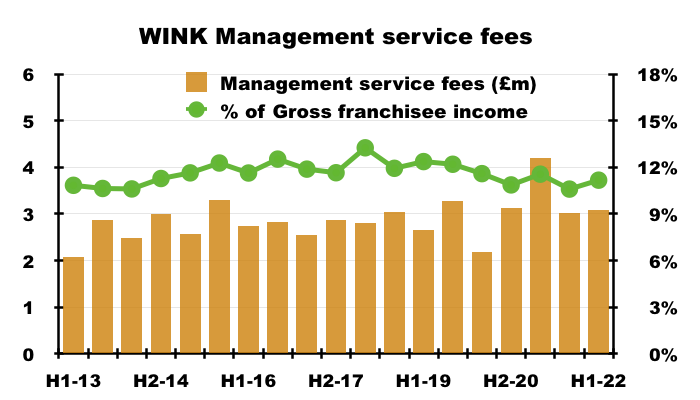

- During this H1, 11.2% of the £27.7m earned by the franchisees was taken by WINK as revenue:

- The 11.2% proportion was the lowest for an H1 since H1 2014 (10.6%).

- The slightly declining proportion may well be due to franchisee income becoming larger and franchisees no longer requiring commensurate expenditure on WINK’s extra services.

- The preceding FY 2021 statement talked of franchisee sales income continuing to exceed franchisee lettings income during this H1:

“Winkworth benefits from a broadly even mix between sales and rentals, but for the immediate future we expect our sales commissions to account for more than half of total revenues, as was the case in 2021.”

- Sure enough, WINK said H1 sales activity was “strong” as “buyers returned to city centres post-pandemic“:

- WINK also said H1 letting activity remained “extremely busy“, with such activity assisted by rent increases. Total franchisee lettings income set a new H1 record:

- Franchisee lettings income as a proportion of total franchisee income was 46% for this H1, and recovered towards what management described during the webinar as the “normalised” 50:50 split:

- WINK suggested franchisee sales income might continue to exceed franchisee lettings income for H2:

“Despite a backdrop of increasing interest rates leading to higher funding costs, our sales applicants remain high. Sales applicants in July 2022 were 4% ahead of July 2021 and 26% ahead of July 2019. Lettings demand continues to be strong, with applicants up 7% versus July 2021 and 44% ahead of 2019. “

- October’s Q3 trading update did not contradict an ongoing bias towards sales:

“Trading in the third quarter of the financial year was good, with a sharp increase in sales year-on-year due in part to an overhang of uncompleted transactions from the second quarter, but also as levels of interest remained strong. Lettings showed good growth, held back only by a shortage of available properties, particularly in London.“

- Assuming franchisee lettings income holds steady at almost £27m, perhaps total franchisee income is running at an annualised £54m with franchisee sales income just beyond £27m.

- Aside from the bumper FY 2021, total franchisee income has in the past topped £50m only once (FY 2014: £50.1m).

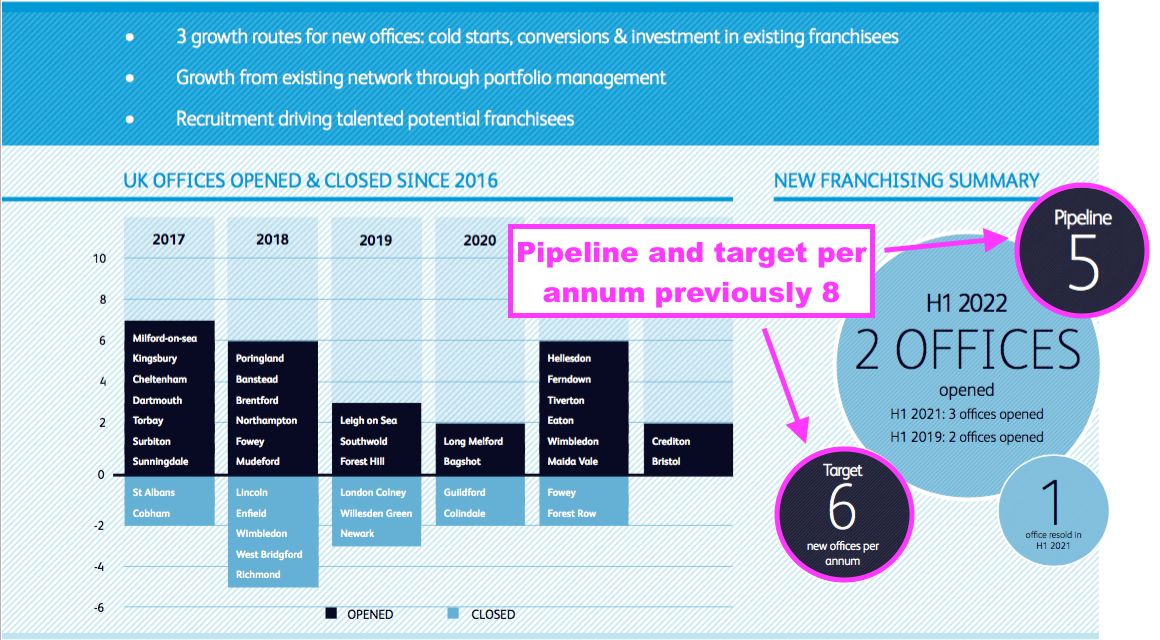

- WINK updated a useful slide that highlighted new and closed franchisee offices:

- Two minor changes from the FY 2021 presentation suggest the rate of new office openings has slowed:

- The target of six new offices per annum was reduced from eight, and;

- The pipeline of five offices was reduced from eight.

- Some 28 offices have been opened and 17 have been closed since FY 2016.

- Some new offices have not worked out; Fowey for example was opened and then closed a few years later.

- But closed offices can re-open; Wimbledon for example was shut and then re-opened a few years later.

- Expanding the franchisee network has been slow going. The 103 franchised branches operating during this H1 compare to 86 quoted within the 2009 flotation document.

- But revenue growth may not be entirely correlated to opening new offices. My notes from the 2016 AGM explain management’s thinking on branch numbers:

“WINK’s franchise network has expanded from 86 to c100 branches in the last 6 years. I said that seems like slow progress. The chairman suggested his experience was that in some years it was good to open offices, and some times it was good to consolidate. He made the point that in the early 90s, the business made a greater profit with 35 offices than it did earlier with more than 40.

- Management reiterated during the webinar how growth can be achieved despite the total office count remaining unchanged: less productive franchisees are replaced by more productive owners:

“We spend a lot of time [on] portfolio management… it’s valuable to us that [when we] get a franchisee that may have reached the end of its proactive lifespan, we introduce new vigour to it through new, hungry franchisees who will acquire the business and use their energy to take it forward.

And where we have done that we have seen fantastic results. So recent sales have been Ealing, Shepherds Bush, Fulham, and they have all increased revenue and I think they will all beat 2021 revenue this year.

The revenue increases on these key offices… the opportunities are equivalent to opening four or five new offices, so it is a way for us to grow our revenue as well as reinforcing and reinvigorating our existing network and making the most out of key locations.“

- The 2021 annual report (point 4j) divulged the resold Fulham office was partly acquired by the chief exec’s wife.

- One office was resold during this H1 and two were resold during FY 2021.

Winkworth versus Foxtons

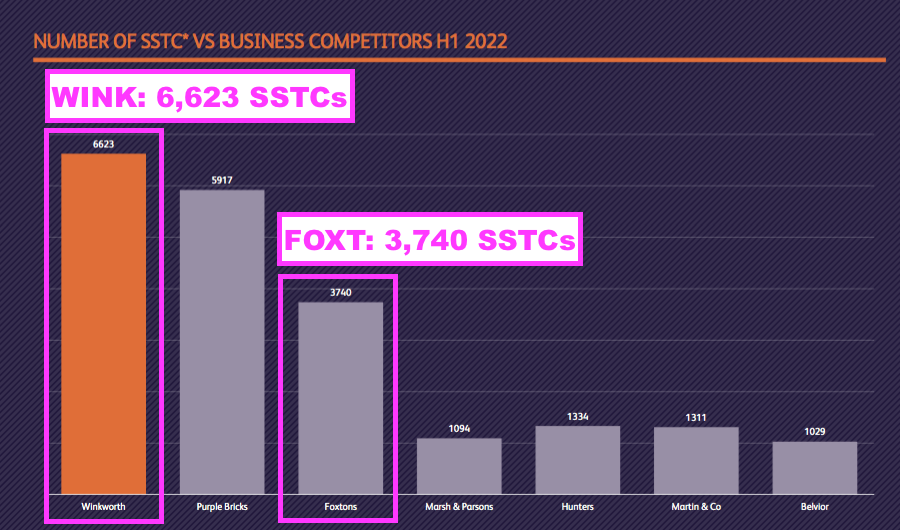

- The H1 2022 presentation included encouraging statistics about market share:

- The preceding FY 2021 presentation omitted the same chart, although did state WINK was “number 2 in London by SSTC market share“.

- Note that WINK’s new slide is based on “Winkworth office geography“, which is possibly not the same as “in London“.

- Market shares based on sold-subject-to-contracts (SSTCs) are obviously subject to those contracts completing, and therefore may not be true reflections of competitor outperformance.

- The slide’s comparison to Foxtons (FOXT) — which claims to be the “largest estate agent in London” and is a prominent WINK rival — is informative.

- The slide claims WINK enjoyed 77% greater SSTCs than FOXT during H1.

- However, WINK reported gross franchisee sales income of £15.0m during H1 while FOXT reported sales revenue of £20.8m.

- Explanations as to how WINK can report 77% more SSTCs than FOXT — but also report sales income 28% lower than FOXT — include:

- WINK’s SSTCs not converting into actual sales;

- FOXT doing particularly well in areas not covered by WINK’s “office geography“, and/or;

- FOXT charging much greater fees per sales transaction than WINK.

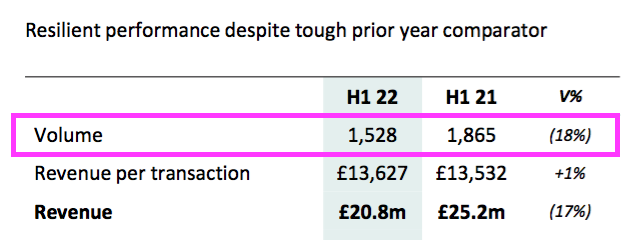

- FOXT’s H1 2022 presentation revealed sales completions of 1,528:

- I am not sure how 1,528 completions should correlate to the 3,740 SSTCs attributed to FOXT within that WINK slide.

- Perhaps the 3,740 SSTCs mean FOXT will enjoy a healthy H2.

- To help resolve any market-share confusion, WINK should follow the lead of FOXT and fellow estate-agency franchisor Belvoir (BLV) and simply publish the number of properties sold through its network:

- FOXT’s standard 2.5% (before VAT) selling fee implies the company’s average sale price achieved during H1 2022 was approximately £545k, which I understand puts FOXT in a similar market bracket as WINK.

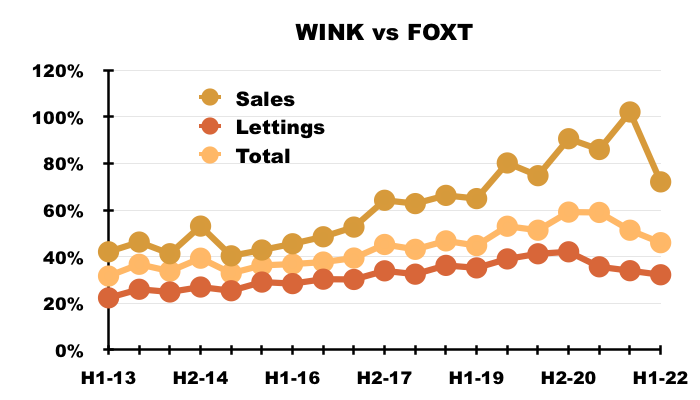

- The chart below expresses the sales, lettings and total franchisee income of WINK as percentages of the comparable FOXT revenue:

- The rising trend lines indicate WINK’s self-employed franchisees handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees…

- …although this H1 did witness FOXT improve its sales performance markedly versus WINK.

- Note that comparing WINK with FOXT is not strictly like-for-like. FOXT generates almost all of its revenue from branches within London while WINK has historically generated approximately 80%.

- Further comparison distortion is caused by FOXT acquiring and selling businesses.

- FOXT has been subject to a management shake-up this year. The stand-in chief exec suggested the other month that FOXT had not been paying the required “attention to detail“:

“Do not over complicate your business, which is what was happening at Foxtons. Essentially, estate agency is a simple business and is about doing the right things brilliantly. Call people back, charge a proper fee, show your worth, send the best people out to valuations, ensure your marketing is smart and stands out from the crowd, and try to do things differently from competitor agents. The key when doing the tasks is a relentless attention to detail“

- And FOXT’s recently appointed permanent chief exec is confident of a turnaround:

“I’m delighted to be back at Foxtons and to have met with so many of the talented team since my arrival in September. The business has significant unfulfilled potential and there is a shared understanding and vision of how we can deliver this. I am excited about leading this reset and determined we can get Foxtons back on the front foot.“

- FOXT’s revitalised board could leave WINK facing stiffer competition from its rival in what could be a difficult time for the housing market generally (see Valuation).

- WINK’s management was asked about FOXT during the H1 webinar:

Q: What are you doing right that Foxtons is not that has resulted in your superior performance?

A: Ha ha, everything. No, I would say it is people led, we are a long-term business and we have been growing steadily in a considered manner with the right people. If we look at those outer London areas and then go outwards, we have some long-term, incredibly experienced, successful operators who are delivering. I feel the general environment is moving towards local business, who want to connect with a proprietor and want to do business with them and someone with experience. Our platform puts us in a good place hopefully versus all competitors going forward.”

Corporate-owned offices

- WINK’s two controlled branches — Tooting and Crystal Palace in London — continue to hold their own versus the group’s wider franchisee network.

- Revenue from these corporate-owned offices represented 28% of total revenue during this H1, matching the 28% witnessed during the preceding H2 2021 and surpassing the 20% seen during the comparable H1 2021:

- To recap, WINK acquired:

- An initial 55% of Tooting Estates for £23k and a £92k loan during FY 2019, and;

- 100% of Crystal Palace Estates for zero during FY 2020.

- The 2020 annual report (point 15) said the two offices would lead to greater “front-end” insight:

“As with the acquisition of Tooting Estates Limited as a subsidiary, Crystal Palace Estates Limited will keep Winkworth in touch with and learning from front-end experiences and industry trends, It will also provide a live platform to test and develop future digital initiative and evolve our centralised CRM systems, which be of benefit to all our franchisees.”

- Complementing the two majority-owned branches is WINK’s start-up Developments and Commercial agency, which provides advice about converting business premises into residential accommodation.

- WINK said Developments and Commercial was “expected to be profitable in 2022 and to grow significantly in 2023.“

- WINK was also bullish on Tooting and Crystal Palace:

“Winkworth Tooting is now well-established and has retained its leading position by market share for sales agreed in the area. Winkworth Crystal Palace has continued to grow, both its market share and revenues and is expected to make an increasingly significant contribution going into next year.“

- Management said during the webinar that Crystal Palace revenue might grow by between 20% and 30% this year. The presentation slides stated the branch was number six for its area based on SSTCs.

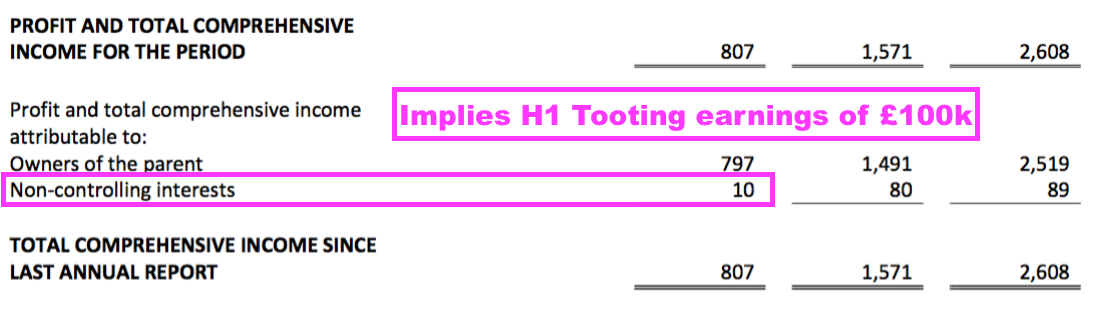

- WINK paid £137k during FY 2021 to increase its ownership of Tooting Estates from 55% to 90%.

- Paying £137k for 35% priced the entire Tooting operation at £391k.

- The 10% of Tooting not owned by WINK enjoyed earnings of £10k during this H1:

- The £10k/10% implies the Tooting office generated H1 earnings of £100k, versus £90k for the preceding H2 2021.

- WINK’s £90k share from Tooting during this H1 represented 11% of the total £797k earnings attributable to the group. The proportion for the preceding H2 2021 was 8% (£81k/£1,028k).

- Relying on the Tooting office for approximately 10% of group earnings is not ideal, although that dependence is offset by collecting a remarkable twelve-month post-tax profit of £190k from the implied £391k investment.

- The £1,185k revenue WINK earned from Tooting, Crystal Palace and the Developments and Commercial division may have converted into revenue of £133k had the trio of subsidiaries operated as franchisees and paid the aforementioned 11.2% average commission to WINK.

- Assume that estimated £133k would then incur no costs other than standard 19% UK tax, the resultant £108k contribution would have surpassed Tooting’s actual earnings of £100k.

- As such, WINK could have been slightly better off during this H1 had Tooting, Crystal Palace and Developments and Commercial been standard franchisees.

- But I would like to think Tooting, Crystal Palace and Developments and Commercial would not have performed as well if they were standard franchisees.

- In addition, WINK’s optimistic commentary on Tooting, Crystal Palace and Developments and Commercial does not signal the subsidiaries are set to underperform the typical franchisee.

- This H1 statement did not specifically mention plans to acquire new corporate-controlled offices. The tone in fact highlighted a desire to retain cash and lend money to proven operators only:

“Our strategy remains to maintain a positive cash balance through the cycle, and to make loans selectively to franchisees looking to expand…”.

Financials

- WINK’s accounts remain in good shape.

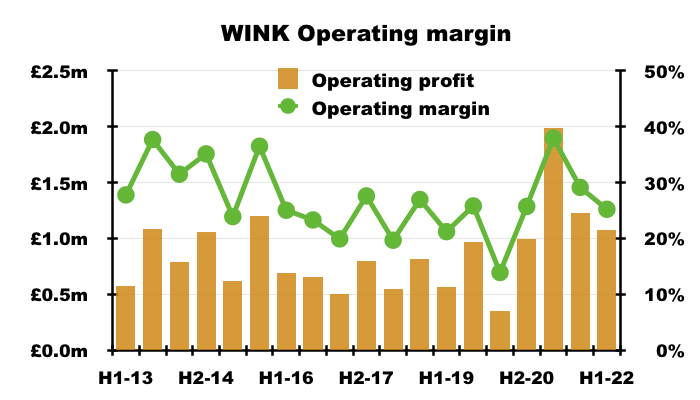

- Although not as high as the remarkable 38% witnessed during the comparable H1 2021, the 25% operating margin during this H1 was the best H1 conversion of revenue into profit since H1 2014:

- The lower margin versus the comparable H1 2021 and preceding H2 2021 (29%) coincides with lower sales transactions, and implies sales commissions attract much higher profit than lettings income.

- Property sales are of course less predictable than monthly lettings payments.

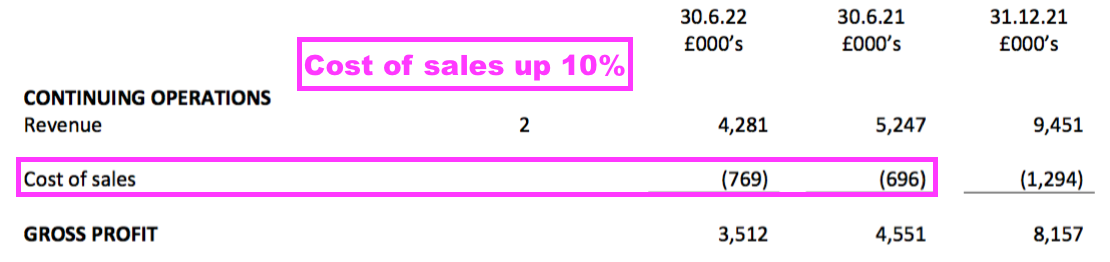

- One oddity among these H1 numbers was how cost of sales could advance 10% while revenue dropped 18%:

- Cash conversion was adequate after earnings of £0.8m funded dividends of £1.2m, extra working capital of £0.4m and franchisee “prepaid acquisition support” payments of £0.2m, which all left cash £0.9m lighter at £4.1m.

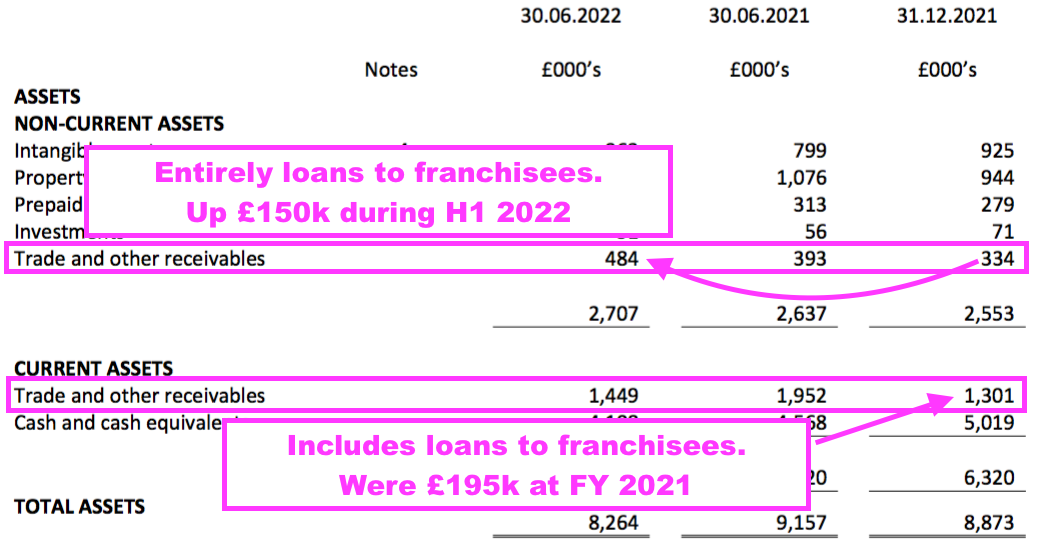

- Note that WINK’s working capital includes loans to franchisees, which during this H1 increased by at least £150k:

- Loans to franchisees peaked at £1.2m during FY 2016, and the subsequent reduction to £0.5m by FY 2021 had suggested greater (and welcome) sufficiency among new franchisees.

- Loans to franchisees could now surpass £0.6m following the extra £150k lending.

- Franchisee “prepaid assisted support” payments increased by a notable £165k during this H1, which puts such expenditure on course for its highest annual level since FY 2014 (£199k).

- Prepaid assisted support reflects cash paid to franchisees to convert their existing agencies into WINK offices, with the expense amortised against earnings over the term of the franchise agreement (point 4f):

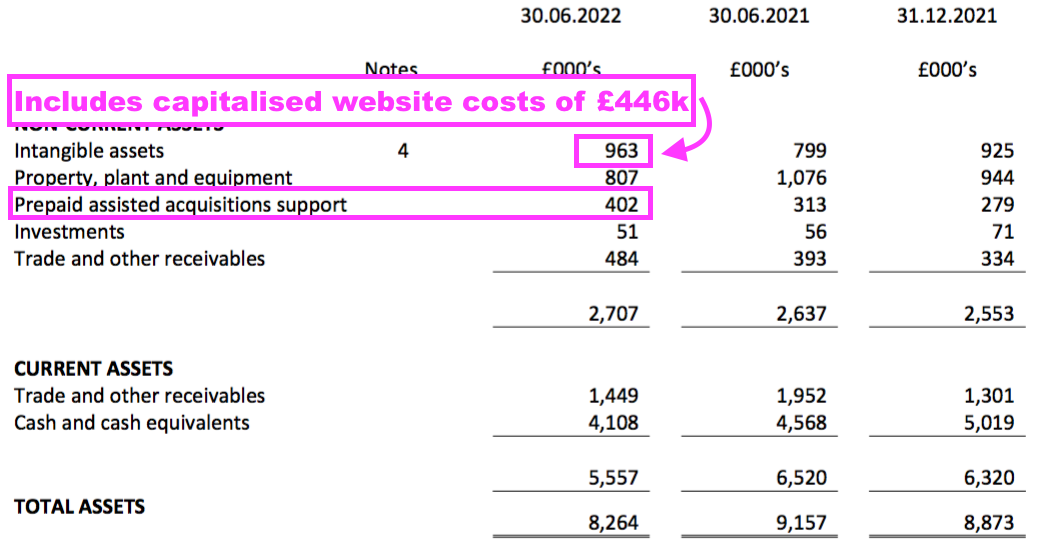

- Also piling higher during this H1 were capitalised website costs, which came to £108k and lifted their associated book value to £446k.

- My calculations concerning the useful life of WINK’s website costs within the 2021 annual report did not look right (points 4a and 4d).

- Combining the carrying values of prepaid assisted support and capitalised website costs gives almost £0.9m, all of which has yet to be expensed through the income statement.

- Bank debt and defined-benefit pension obligations remain at zero.

- An investment portfolio that ended FY 2021 at £71k declined by £20k (28%) during H1.

- Net cash, (estimated) loans to franchisees plus investments finished the half at £4.8m or 38p per share.

- Finance income from that £4.8m was a very low £11k during this H1 and some earlier 2021 annual-report guesswork (point 4l) indicated the franchisees were paying 3.8% on their loans.

- WINK remains a very capital-light business. Net asset value excluding cash/loans/investments (£4.8m) and intangibles (£1.4m) for FY 2021 was only £469k.

Valuation

- WINK’s July update kindly included a profit forecast for FY 2022:

“While the UK economic outlook and confidence in the housing market remain in question, the Directors are pleased with the Company’s performance in H1 2022 and expect that full year pre-tax profits will be in line with the market forecast of £2.1m, marking a substantial increase on the outcome for 2019.“

- Unlike the preceding FY 2021 statement, these H1 results referred to cyclicality and economic matters that suggested some management caution:

“Estate agency is a cyclical business, tied to the UK economy and a fluctuating market, and one where the ability to retain cash brings both stability and opportunities…

…much will depend on the trajectory of interest rates and macro-economic factors.“

- But a Q3 update during October provided reassuring ‘mini-budget’ commentary and reiterated the earlier profit forecast:

“We have not as yet witnessed a negative impact from the mini-budget on applications and sales and, although higher mortgage rates are likely to put a cap on further price appreciation, we anticipate that an increased supply of properties and persistent strong demand will support transactions for the rest of the current year.

The Directors expect that full year pre-tax profits will be at least in line with the market forecast of £2.1m.“

- A pre-tax profit of at least £2.1m indicates H2 will repeat this H1 performance.

- A pre-tax profit of at least £2.1m is below the £2.4m I had calculated by doubling the preceding H2 2021 within my FY 2021 write-up.

- Pre-tax profit of £2.1m taxed at the upcoming 25% UK standard rate leaves earnings of £1.6m or 12.4p per share.

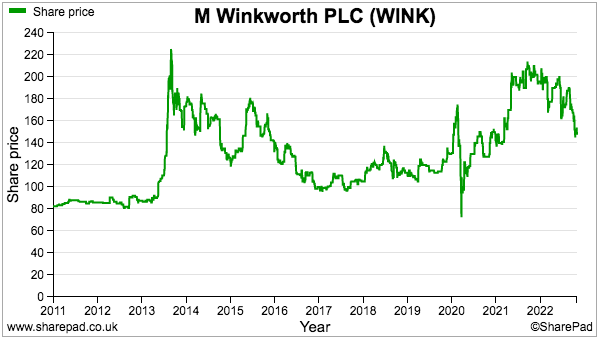

- Dividing the 160p offer price by 12.4p per share gives a P/E of 13x.

- Assume the cash and investments of 38p per share are not required for the business to operate successfully, and a cash-adjusted P/E could be (122p/12.4p) = 10x.

- But the aforementioned WINK commentary of “our strategy remains to maintain a positive cash balance through the cycle” does hint of the cash position being fundamental to the group’s progress.

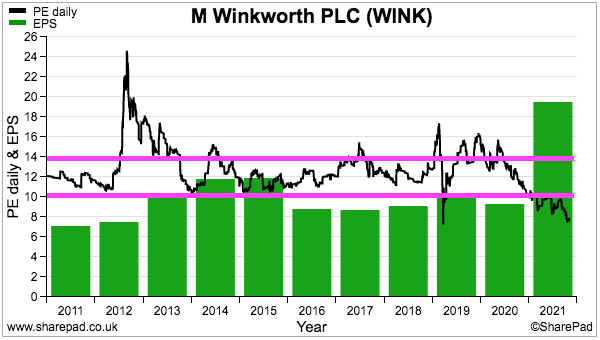

- A multiple of 10x or 13x or somewhere in between appears modest, but is not out of keeping with WINK’s typical trailing P/E of 10x-14x:

- WINK’s past rating has reflected the group’s largely stagnant profit between FYs 2016 and 2020.

- WINK’s current rating may reflect economic problems upsetting the housing market.

- The headlines from Property Industry Eye are gloomy:

- UK house prices to fall sharply, new five-year house price forecast shows

- Sharp rise in property sales falling through amid rising mortgage rates

- Homeowners’ monthly mortgage repayments soar as rates rise

- UK housing market headed for a ‘correction’, five-year forecast shows

- House price growth slows sharply, new data shows

- UK house prices to fall as mortgage rate hike hits ‘buying power’

- House prices to fall by 8% next year, Lloyds warns

- Conveyancers urged to prepare for ‘significant fall in work volumes’

- WINK re-emphasised its “progressive dividend” ambition during this H1:

“With a limited fixed cost base, a healthy cash balance and no debt, we remain confident. Our considered growth strategy is to support talented and proven franchisees in acquiring businesses and to expand our equity ownership of businesses in partnership with established operators. In this way, we believe we can outperform market trends and continue to pay a progressive dividend.“

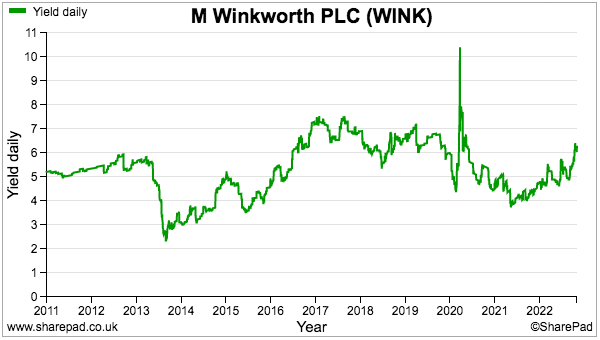

- October’s Q3 update announced a 2.7p per share quarterly dividend that was 23% ahead of the prior-year Q3 payout and matched the distributions for the preceding Q1 and Q2.

- A 2.7p per share dividend for Q4 would then give 10.8p per share for the full year to support a 6.8% income at 160p. The trailing yield is shown below:

- A 10.8p per share dividend would be covered just 1.15 times by my 12.4p per share earnings guess.

- I asked management about dividend cover during the H1 webinar:

“Q: Dividend cover was less than 1.2 times in this half, and may decrease in future if a progressive dividend policy is pursued and earnings stagnate due to reduced sales activity. What is the board’s policy of dividend cover, and would the board be comfortable with dividend cover of less than one?

A: Interesting question. I think we are committed to an ordinary dividend where trading permits. It would have to be some fairly dramatic changes to our circumstances to impact on that. Short term? Interesting question, it would be something that the board would have to consider if cover dropped to less than one.

A bit of a commitment was shown by the pandemic, where we paid the quarterly dividend amid the lockdown with a 20% reduction, so we are committed to that dividend and we were able to do that because of the defensive nature of our business and comfort in the lettings business underpinning it all. So I suppose that is our view on it, we are keen to maintain it.“

- The board therefore has good reason to ensure the dividend is sustained during any difficult times.

Maynard Paton

M Winkworth (WINK)

Trading update published 22 November 2022

A positive update, although the outlook for FY 2023 may not be so straightforward. Here is the full text interspersed with my comments:

——————————————————————————————————————

M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce the following trading update for the ten months ending 31 October 2022.

Market conditions remained strong in Q3, with network sales 38% higher than in Q3 2021, reflecting both an overhang of uncompleted transactions from Q2 and still strong levels of demand.

Lettings were ahead by 13% over the same period, with London rentals continuing to be driven by higher prices rather than a significant increase in new mandates.

——————————————————————————————————————

Q3 “network sales” I think relates to property sales transactions, rather than total revenue. Up 38% sounds great and, if repeated for Q4, would give gross H2 franchisee sales income of £19.9m — versus £15.0m for H1.

Q3 lettings up 13% if repeated for Q4 would give gross H2 franchisee lettings income of £15.8m.

If my interpretation of these increases is correct, then total franchisee income for FY 2022 could be c£63m — just £2m short of the exceptional FY 2021.

——————————————————————————————————————

After the announcement of the mini budget at the end of September 2022, which led to a sharp rise in the cost of borrowing, new buying registrations fell significantly. Sales already underway, however, continued to progress, with a limited number of fall throughs and our results for October were good.

With the steps taken to reverse most of the measures introduced in the mini budget we expect to see mortgage rates continuing to moderate and sales demand rebounding in November 2022, before we enter the traditionally quiet Christmas period. Rentals demand remains strong and the shortage of available properties continues to underpin the sales market.

——————————————————————————————————————

The concerning phrase here is “new buying registrations fell significantly“.

Mortgage rates have a clear effect on property-market interest and I think the days of sub-1% base rates have now gone for good. The question therefore is how transaction numbers will fare with higher rates — will asking prices drop, and in turn (eventually) increase transaction volumes?

A personal anecdotal experience of a recent rent increase underpins WINK’s assertion of rentals demand remaining strong.

——————————————————————————————————————

The Company has a healthy pipeline of three new offices due to come on board over the coming twelve months.

As a result of this buoyant level of activity in the second half of 2022, Winkworth’s full year revenues are expected to exceed management forecasts and our full year pre-tax profits to be ahead of the current market forecast of £2.1m.

Dominic Agace, Chief Executive Officer of Winkworth, commented:

“Winkworth has performed well in 2022, a year that has been marked by both political and economic uncertainty but, ultimately, benefited from strong levels of UK employment. While higher mortgage rates are leading the consensus to point to a weaker property market in 2023, we believe that our performance next year will be underpinned by the unfulfilled needs of homeowners to move, renewed interest in London property from international buyers and rising prices in the rentals market.”

——————————————————————————————————————

Yes, “a weaker property market in 2023” sounds about right.

Mind you, WINK performed relatively well in the weaker Brexit-stifled London market pre-pandemic, and I trust the group’s self-motivated franchisees can maintain their edge in what may prove a difficult economy for the next couple of years.

Three new offices is below the annual target of six stated in the H1 presentation.

At least pre-tax profit is expected to be higher than the market’s earlier £2.1m prediction, and the prospect of a small special dividend to complement the Q4 payout may not be totally unrealistic.

Maynard

M Winkworth (WINK)

Trading Update and Dividend Declaration published 11 January 2023

Just catching up with this statement from January. Here is the full text:

——————————————————————————————————————

“M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce the following trading update for the financial year ending 31 December 2022.

Despite the hiatus in the property market provoked by the mini budget in Q4 2022, the year as a whole saw a buoyant level of activity in both sales and rentals. As buyers continued to return to London, interest in property sales remained dynamic and Winkworth ranked second by properties exchanged in the city for the year as a whole(1).

Transaction levels in the country markets were firm, with some signs of sellers downsizing in part due to the higher costs of holding larger properties as a result of higher energy costs and a drive towards greater energy efficiency. This trend may result in larger country houses coming to the market, as a result of which lower transaction volumes may in part be offset by higher value transactions.

Both London and country rentals have continued to be strong, albeit with price growth slowing as affordability ceilings are reached and, in the short term at least, accidental landlords increase available stock. Prime London lettings, where the directors believe that there is still headroom for higher prices, remains the most active part of the rental market for Winkworth.

We opened two offices in 2022, in Bishopston in Bristol, creating a new area for growth, and in Crediton, adding to our localised Devon network. We are in negotiations to open up to a further six offices over the coming 12 months.

Winkworth’s full year pre-tax profits, subject to the audit, are expected to be modestly ahead of the current market forecast of £2.3m and net cash at year end stood at c.£5m (2021: £5m). The Company expects to announce its final results for the year ended 31 December 2022 on or around 19 April 2023.

The directors of Winkworth are pleased to announce that the Company will pay an ordinary dividend of 2.9p (2021: 2.7p) per share for the fourth quarter of 2022, bringing the total ordinary dividend payments declared for the year to 11.0p (2021: 9.3p).

The timetable for the payment of the ordinary dividend is as follows:

Ex-Dividend Date: 19/01/23

Record Date: 20/01/23

Expected Payment Date: 16/02/23

(1) based on postcodes where Winkworth has listed a property – Source: TwentyEA

Dominic Agace, Chief Executive Officer of Winkworth, commented:

“While the challenges facing the sales market in 2023 have been widely voiced and it will be hard to match the strength of the conditions witnessed in 2022, we are very pleased with our sales results for last year and are less downbeat than the consensus on the outlook for prices in the current one. Lettings market activity abated towards the end of 2022, but we expect it to be strong again in 2023.”

——————————————————————————————————————

Pleasing to read FY 2023 profit will be “modestly ahead” of the expected £2.3m, which followed the upgrade during November that signalled FY profit would be ahead of the then £2.1m projection.

A lifted 2.9p per share Q4 dividend is also promising. Sadly there was no accompanying special payout as I had speculated after the November update.

Cash at £5m gives a £0.9m improvement on the £4.1m at the half year, and reverses the £0.9m outflow witnessed during H1. I get the impression cash flow/earnings approximate to the dividends paid during the twelve months, which are four quarterlies of 2.7p and a special of 3.8p = 14.6p per share.

Looking ahead, I guess a lot will depend how stern the “challenges facing the sales market in 2023” will become.

Opening “up to” a further six offices during 2023 suggests the group’s target of opening six a year may not be attained, which perhaps reflects the tougher market conditions.

Maynard

M Winkworth (WINK)

Dividend Declaration published 12 April 2023

Just catching up with this statement from April. The Q1 dividend of 2.9p per share matches the preceding Q4 payout and, if recent history is anything to go by, ought to set the level for Qs 2 and 3. The twelve-month trailing payout is therefore 11.6p per share.

Here is the full text:

——————————————————————————————————————

“The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 2.9p per ordinary share for the first quarter of 2023 to shareholders.

The timetable is as follows:

Ex-Dividend Date: 20/04/2023

Record Date: 20/04/2023

Expected Payment Date: 18/05/2023

The Company will announce its audited financial results for the year ended 31 December 2022 on 19th April 2023.

During the end of year audit process, the Board became aware of an issue concerning technical compliance with the Companies Act 2006 in relation to a historic dividend payments. Although there were sufficient distributable reserves and cash held in the Group which could have been distributed, dividends were declared at times when the Company did not hold adequate distributable reserves by reference to its relevant historic annual accounts. The Company’s historic reported trading results and financial condition are entirely unaffected.

The Board proposes to put a resolution to Shareholders at its 2023 annual general meeting to address this past issue.”

——————————————————————————————————————

The technical dividend infringement is not ideal, but the same administrative oversight has caught out a number of companies of late including City of London Investment and IntegraFin. WINK failed to file its interim results with Companies House (CH) and sufficient distributable reserves were not therefore confirmed with CH at the time of certain dividend payments.

Maynard