13 January 2022

By Maynard Paton

Results summary for M Winkworth (WINK):

- An “extraordinarily active” sales market led to an exceptional six-month performance, with the H1 £2m profit exceeding WINK’s peak annual profit from FY 2014.

- Subsequent trading updates then lifted FY 2021 expectations and announced a record quarterly dividend alongside the third special payout of the year.

- Market-share gains versus London rival Foxtons plus very encouraging progress at the company-owned Tooting office underpin the prospect of a “busy” FY 2022.

- The accounts remain in good order, with this H1 showing a super 38% margin and net cash and investments supporting close to 20% of the share price.

- Near-term earnings may well subside if housing activity cools, but WINK’s reliable dividends may limit the downside with a possible 5% income. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- Franchisee sales and lettings income

- Winkworth versus Foxtons

- Corporate-owned offices

- Financials

- November and January updates

- Valuation

Event links, share data and disclosure

Events: Interim results for the six months to 30 June 2021 published 08 September 2021, dividend declaration published 13 October 2021, trading update published 11 November 2021 and trading update published 12 January 2022

Price: 208p

Shares in issue: 12,733,238

Market capitalisation: £26.5m

Disclosure: Maynard owns shares in M Winkworth. This blog post contains SharePad affiliate links.

Why I own WINK

- Operates a London estate-agency franchising business, with progress buoyed by motivated franchisee owners capturing market share from conventional rivals.

- Franchisor set-up leads to high margins, low capital requirements and a cash-rich balance sheet able to fund attractive franchisee investments.

- Seasoned family management boasts £12m/47% shareholding and rewards investors through durable quarterly dividends and occasional special payouts.

Further reading: My WINK Buy report | All my WINK posts | WINK website

Results summary

Revenue, profit and dividend

- Upbeat outlook remarks within WINK’s FY 2020 results…

“In the first quarter we have seen a strong uptick in sales agreed and a very encouraging increase in applications for both sales and rentals.

- …followed by a very confident July RNS…

“Following an exceptionally strong performance in the sales division by the network in the first half of 2021, with preliminary figures indicating that network sales revenues exceeded those achieved for the whole of 2020, the Directors will also pay a special dividend of 2.6p per ordinary share“

- …had already signalled these H1 2021 figures would be extremely positive.

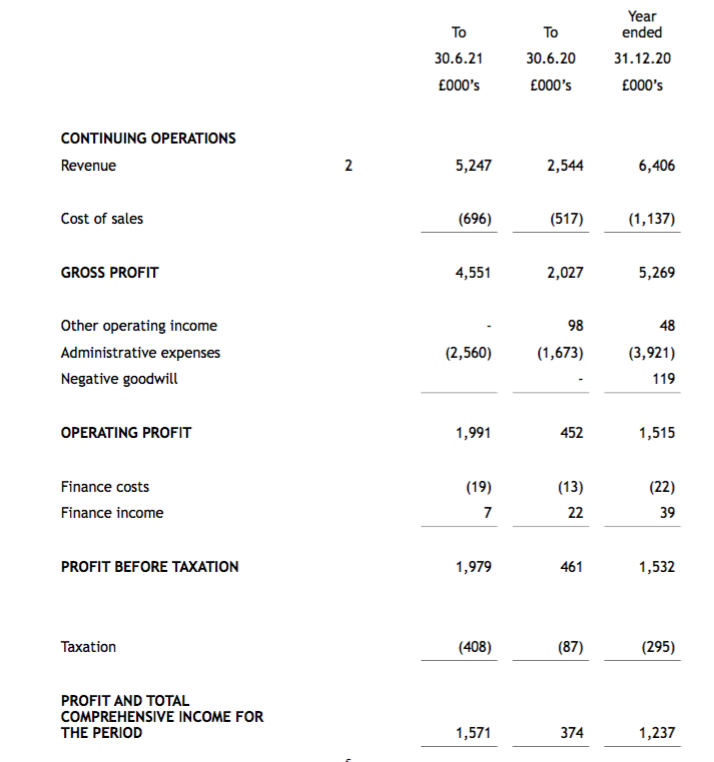

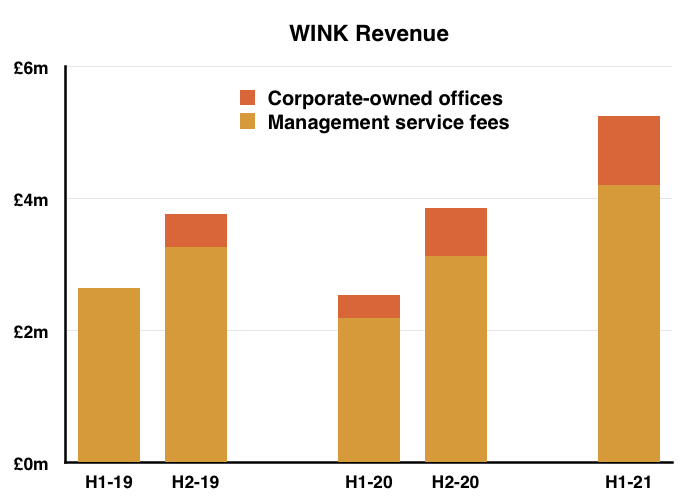

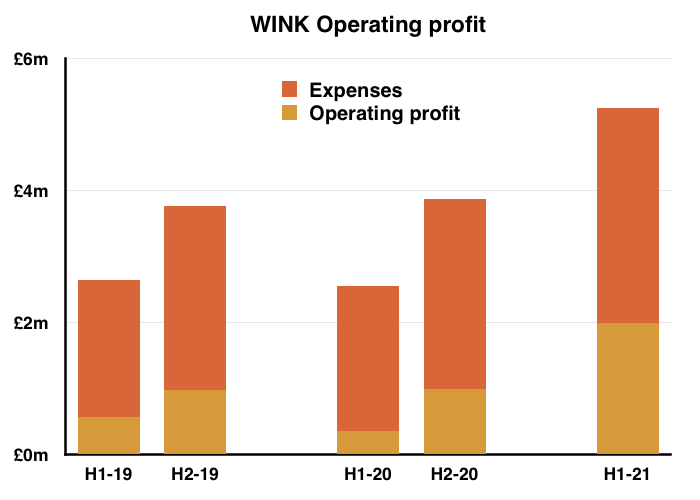

- Versus the pandemic-blighted H1 2020, revenue more than doubled to £5.2m while operating profit more than quadrupled to £2.0m:

- WINK explained the exceptional performance was due to an “extraordinarily active” sales market underpinned by:

- “pandemic-induced buyers searching for space and bringing forward moves to the country that may normally have been five years away“;

- “record low interest rates“, and;

- “the government being overtly supportive of the housing market“.

- These H1 results were by some distance WINK’s best ever for any six-month period.

- The £2.0m H1 profit in fact exceeded the group’s record £1.9m full-year profit of FY 2014.

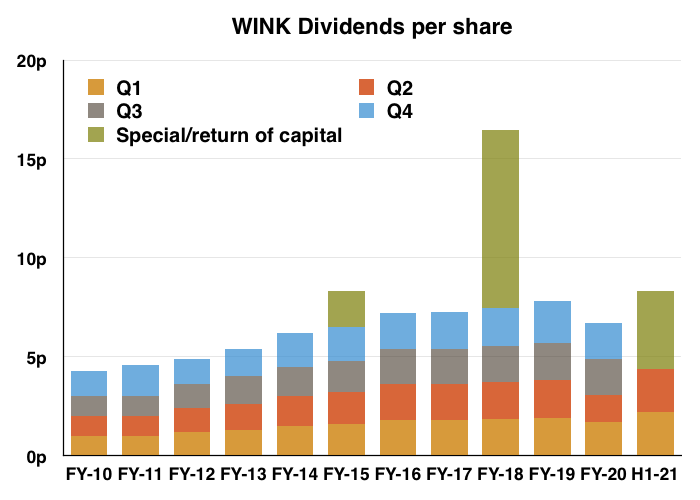

- WINK’s quarterly dividend declarations during April and July had already foretold a 4.4p per share ordinary payout for this H1 alongside 1.3p and 2.6p per share special distributions:

- WINK’s 2.2p per share Q1 and Q2 dividends were 16% higher than the equivalent (pre-pandemic) 1.9p per share payouts of FY 2019.

- Subsequent RNSs have provided further welcome dividend progress (see November and January updates). .

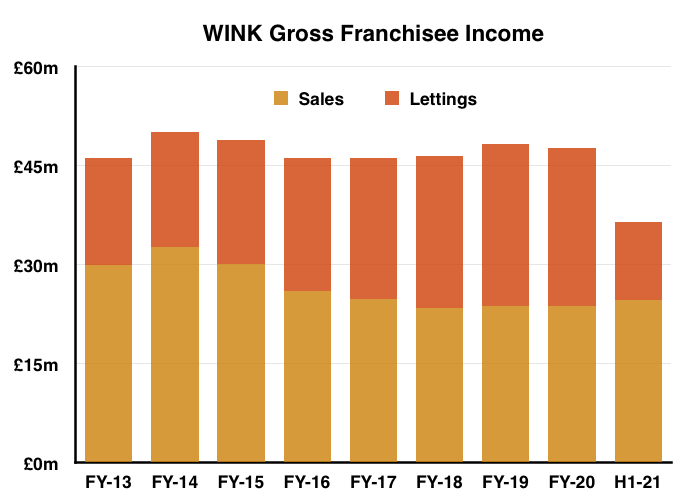

Franchisee sales and lettings income

- WINK’s franchisee network consists of approximately 100 estate-agency branches located in London and throughout south-east England.

- Franchisees pay WINK a straight 8% of all their sales and letting commissions, plus variable sums towards advertising, IT, landlord/tenant introductions and other services.

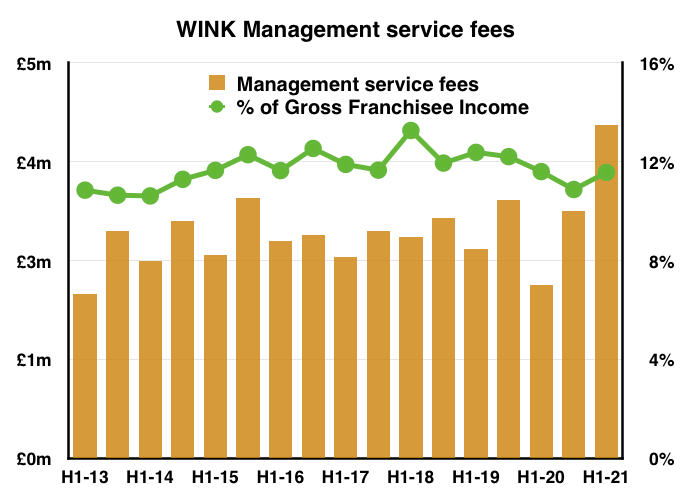

- During this H1, 11.6% of the £36m earned by the franchisees was taken by WINK as revenue:

- The 11.6% proportion improved slightly after WINK’s FY 2020 statement revealed a “conscious decision to reduce certain fees to franchisees during lockdown“.

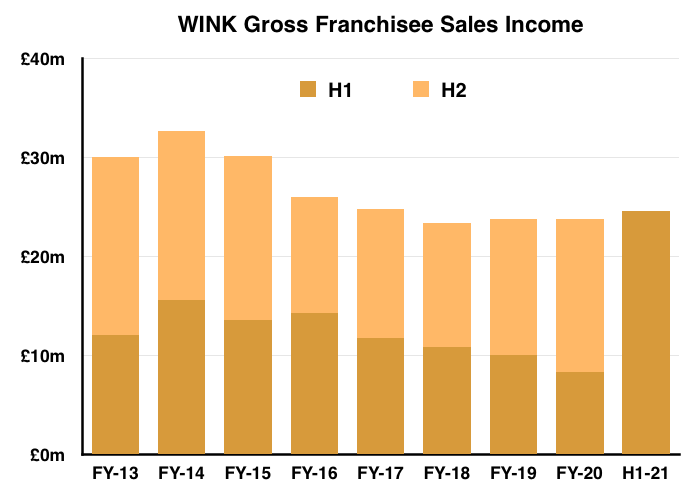

- The aforementioned “extraordinarily active” sales market allowed WINK’s franchisees to generate almost £25m from sales commissions during this H1 — matching the annual levels collected during the previous four years:

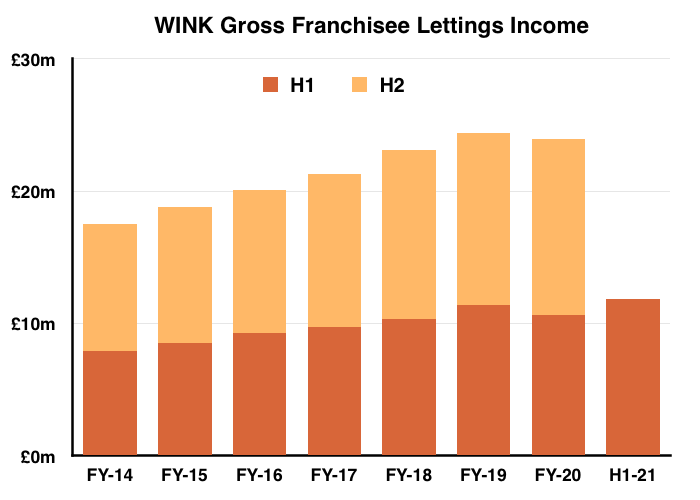

- An absence of international workers in London meanwhile meant lettings commissions collected by franchisees held steady:

- Franchisee sales commissions as a proportion of total commissions increased to 68%, the highest since WINK embarked on expanding its lettings division more than ten years ago:

Winkworth versus Foxtons

- WINK’s H1 2020 statement…

“A significant amount of management time has been spent on dealing with the unique challenges presented by Covid-19, and the prompt re-opening of all of our offices led to an increase in our market share.“

- …and its FY 2020 statement…

“We further improved our strong position in the marketplace and ranked 2nd in London with a market share of 4.53%, having increased our share of SSTC properties in 2020 by 0.35% [Source: TwentyCI]”.

- …both confirmed the group capturing greater market share.

- But this H1 2021 statement did not refer to market share.

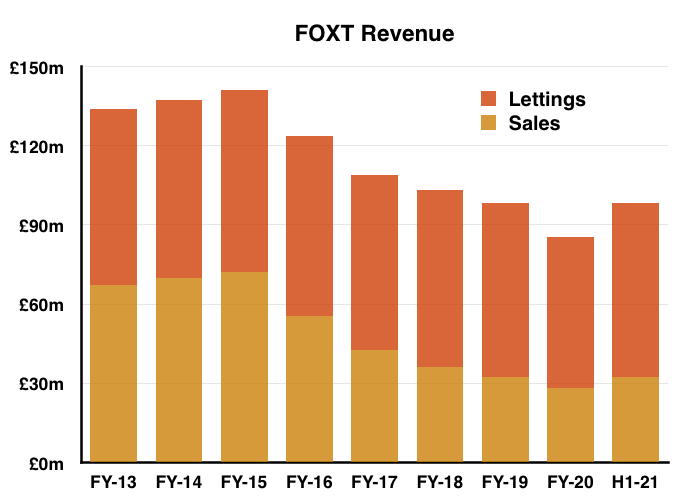

- Comparing WINK to Foxtons (FOXT) — which claims to be “London’s leading estate agent” — provides a useful guide as to the relative progress of both operators.

- FOXT in fact managed to earn more revenue during H1 2021 than during its entire FY 2020:

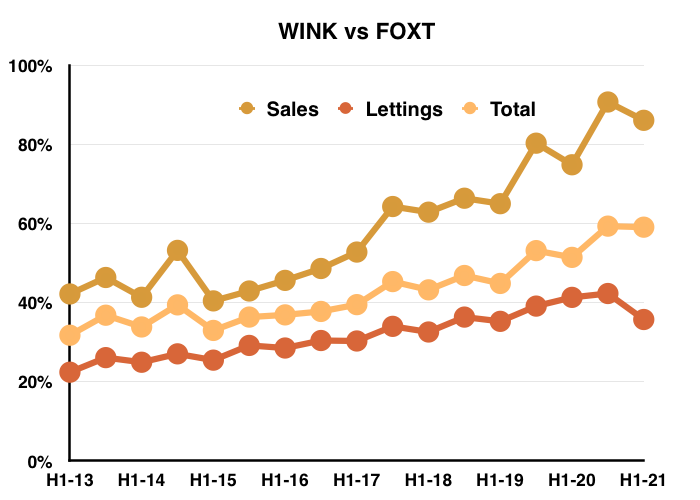

- The chart below expresses the sales, lettings and total franchisee income of WINK as percentages of the comparable FOXT revenue:

- WINK has consistently outperformed FOXT during the last few years.

- During H1 2013, total income at WINK’s franchisees represented approximately 32% of FOXT’s sales and lettings revenue (middle line above):

- That 32% proportion has subsequently increased to 59%.

- Since H1 2013:

- Total sales commissions at WINK’s franchisees have advanced from 42% to represent 86% of FOXT’s sales revenue, and;

- Total lettings commissions at WINK’s franchisees have advanced from 22% to represent 36% of FOXT’s lettings revenue.

- Note that the FOXT comparison is not strictly like-for-like. FOXT generates almost all of its revenue from branches within London while WINK has historically generated approximately 80%.

- FOXT acquiring small lettings agencies and WINK now operating its own branches (see Corporate-owned offices) also distorts the comparison.

- WINK’s self-employed franchisees do nonetheless appear to have handled London’s property market during Brexit and the pandemic far better than FOXT’s conventional employees.

- Mind you, FOXT has been subject to a shake-up and could one day recapture its lost market share.

- Recent board changes include a new chairman, a new finance director and a former FOXT boss as a new non-exec.

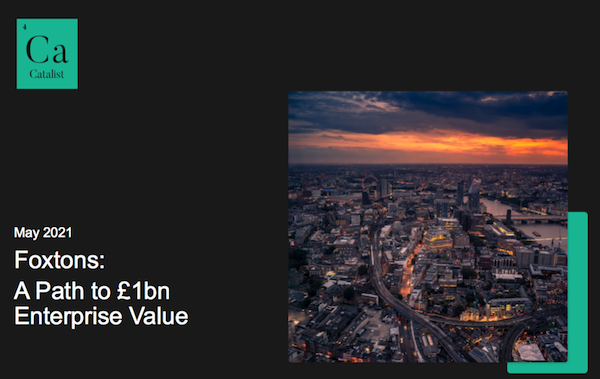

- FOXT has also attracted activist attention from Catalist Partners, which claims FOXT could one day sport an enterprise value of £1 BILLION:

- FOXT’s market cap at its recent 41p share price is £131m.

- Catalist’s plan is based upon FOXT competing against the likes of Knight Frank, Chestertons and Savills to sell more £3m-plus properties.

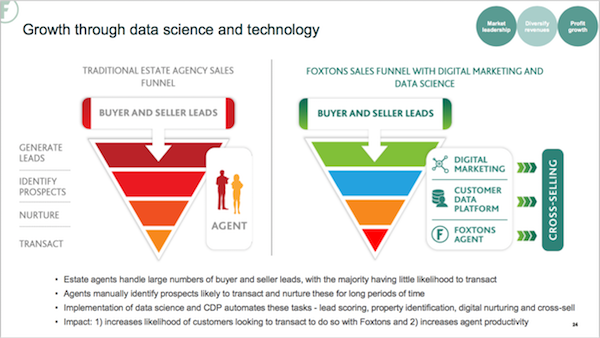

- In contrast, FOXT’s own plan remains going head-to-head with the likes of WINK on sub-£1m properties. But the plan also includes “a focus on… technology and data science… to reinforce market leadership, diversify revenue streams and grow profit“:

Corporate-owned offices

- Revenue from WINK’s two controlled branches — Tooting and Crystal Palace in London — kept up with the group’s main franchising income.

- Revenue from these corporate-owned offices represented 20% of total revenue during this H1, versus 19% for the preceding H2.

- To recap, WINK acquired:

- The 2020 annual report (point 15) said the two offices would lead to greater ‘front line’ insight:

“As with the acquisition of Tooting Estates Limited as a subsidiary, Crystal Palace Estates Limited will keep Winkworth in touch with and learning from front-end experiences and industry trends. It will also provide a live platform to test and develop future digital initiative and evolve our centralised CRM systems, which will be of benefit to all our franchisees.”

- My emailed questions to last year’s (behind-closed-doors) AGM elicited this explanation of the hybrid franchisor-owner strategy:

“Our business strategy is to attract the right people into the network and, in circumstances where we have the best-placed person but that person perhaps lacks sufficient funds, incentivise them appropriately.

We are open to taking an equity position to facilitate bringing that person on board, and to offer them with a route to equity ownership. In return, we expect to generate a return over and above the 8% that we typically achieve through an independent franchise.

Franchising, however, remains our main focus and will continue to shape the business and its profits going forward.”

- The early contribution from the Tooting office has been very encouraging.

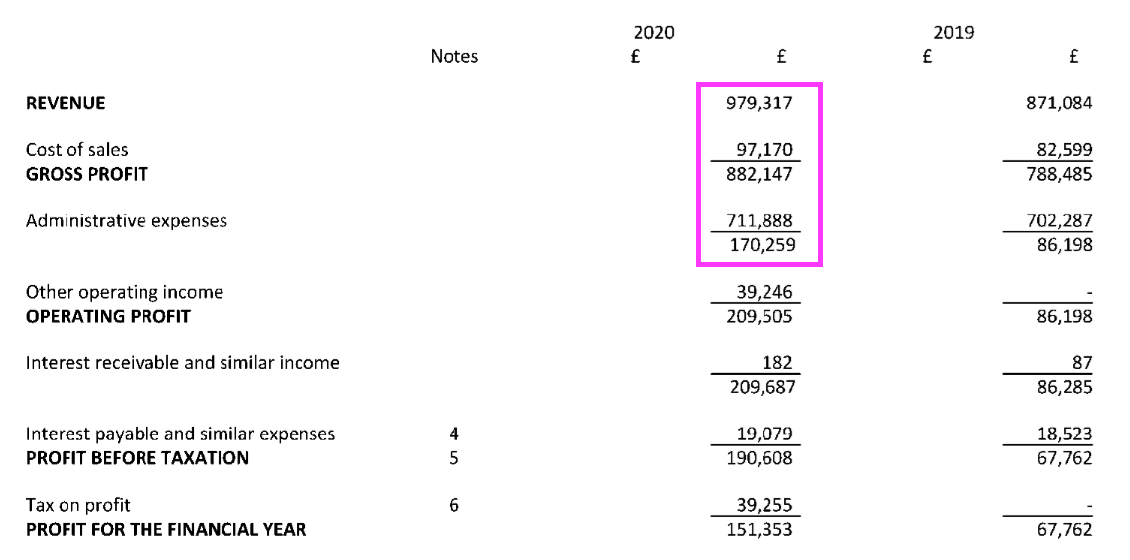

- Companies House shows Tooting Estates delivering revenue of £979k and an underlying operating profit of £170k for FY 2020:

- During this H1, WINK paid £137k to increase its ownership of Tooting Estates from 55% to 90%:

7. ACQUISITION OF FURTHER SHAREHOLDING

On 31 March 2021, Winkworth Franchising Limited acquired a further 35% of Tooting Estates Limited, which operates the Winkworth franchise in the Tooting area, for £136,963. The Heads of Terms in relation to the acquisition were signed on 23 March 2021.

- Paying £137k for 35% values the entire Tooting operation at £391k.

- Acquiring an underlying FY 2020 operating profit of £170k for £391k seems a very good deal.

- Tooting’s profit appears to have increased since FY 2020.

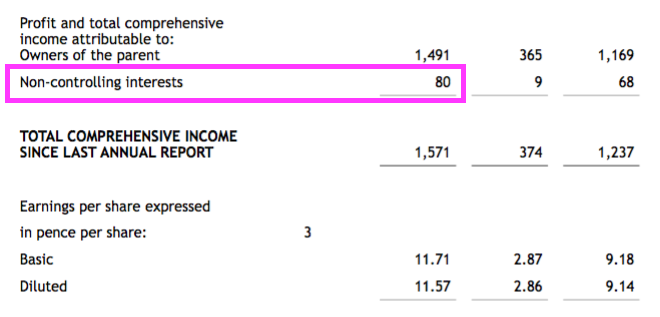

- Earnings accruing to the minority Tooting owner were £80k during this H1:

- The minority owner controlled a 27.5% average of Tooting during the six months, implying total Tooting earnings were £291k for this H1 or £582k annualised.

- The Tooting and Crystal Palace branches generated aggregate sales of £1,038k during this H1. Had the branches remained as franchisees, WINK would have earned revenue of approximately £125k — somewhat less than Tooting’s earnings of £291k.

- Tooting’s £291k earnings less the minority owner’s £80k gives £211k attributable to WINK.

- WINK’s £211k from Tooting represents 14% of the total £1,491k earnings attributable to the group during this H1.

- Owning 100% of Tooting throughout this H1 would have upped that proportion from 14% to almost 19% (£291k/£1,571k).

- A significant percentage of earnings being dependent on a single agency branch is not ideal, although that dependence is counterbalanced by the effective 30%-plus earnings return on the latest £391k Tooting valuation.

Financials

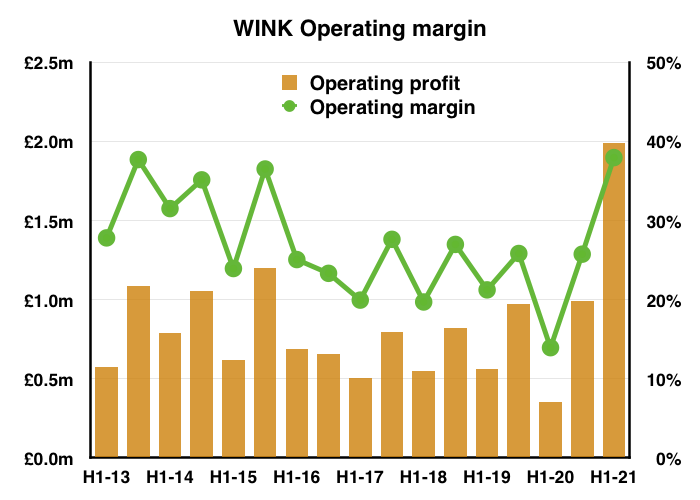

- The most remarkable ratio from these H1 results was the operating margin.

- WINK managed to convert almost 38% of revenue into profit, a level not seen since H2 2013:

- The super margin during this H1’s “extraordinarily active” sales market confirms property transactions generate a much higher profit than lettings income.

- Property sales are of course less predictable than monthly lettings payments.

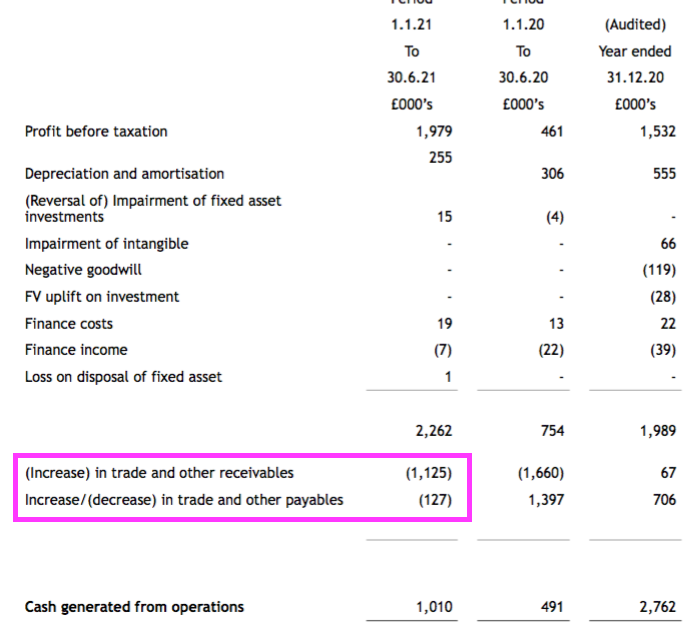

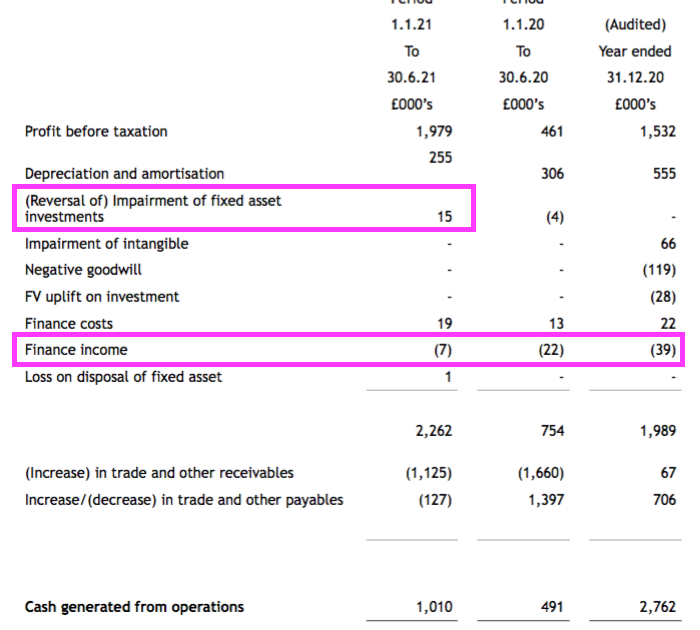

- Despite WINK’s buoyant trading, cash conversion was not the best during this H1.

- Operating profit of £2.0m translated into operating cash flow of £1.0m following a £1.2m adverse working-capital movement:

- WINK witnessed a similar build-up of receivables during H1s 2019 and 2020, which reversed during the subsequent H2s.

- An H2 receivables/cash-flow reversal seems to have occurred this time, too, after WINK’s update earlier this week announced another special dividend (see November and January updates).

- The working-capital movement, dividends of £0.8m, a tiny £28k spent on capex and the £137k Tooting investment left the half-year cash position £0.1m lighter at £4.6m.

- The 2020 annual report (note 13) revealed WINK’s assets included start-up loans to franchisees of £525k.

- Conventional bank debt and pension obligations remain at zero.

- A £15k (or 22%!) reduction to WINK’s small equity portfolio was charged to operating profit:

- The portfolio is now valued at £56k.

- Net cash and investments are therefore £5.1m or 40p per share.

- Finance income from that £5.1m reduced to a very low £7k during the half. This £7k could mean WINK has given franchisees with start-up loans (total: £525k) an interest-payment holiday.

November and January updates

- WINK’s H1 outlook expected property transactions to moderate during H2…

“The ending of the stamp duty holiday, the re-opening of foreign travel in August, and transactions due to complete in July having been brought forward to June will, inevitably, mean that some of the fervour will come out of the sales market.”

- …and rental activity to recover:

“We have seen a significant upturn in activity in the rental market as the return to work brings tenants back to London and houses in outer London recover to their pre-pandemic rents.“

- But an update during November revealed H2 trading had been “strong” in both sales and lettings:

“Trading conditions have remained strong since the upturn in the first half of the year, with London sales and rentals, which account for some 75% of our revenues, being buoyant.“

- WINK therefore upgraded its expectations:

“As a result of this buoyant level of activity during the current year, Winkworth’s full year revenues are expected to exceed management forecasts and our full year profits to be materially higher than expectations. For the year ahead, with a return to more normal conditions in sales and an improved rental market in London, we look forward to the continued underlying growth of the business.“

- The trading statement earlier this week was also positive:

“Sales activity in Q4 2022 remained brisk, with continued interest in relocation post the heightened level of transactions triggered by the stamp duty holiday, which ended in September…

Our rental business experienced some normal seasonal slowdown after several months of intense activity but remained strong in London.”

- WINK therefore upgraded its expectations again:

“Winkworth’s full year revenues have again exceeded management expectations and pre-tax profits are expected to be ahead of market forecasts at the time of the last trading update.“

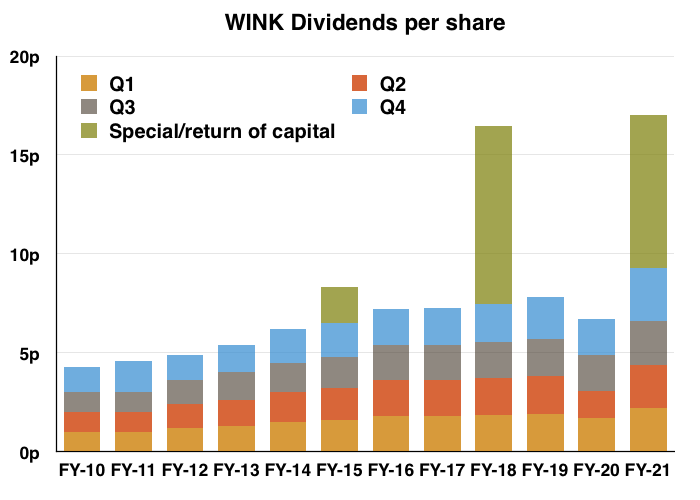

- WINK underlined the H2 performance by declaring a record 2.7p per share quarterly dividend alongside the third special payout of the year:

“The directors of Winkworth are pleased to announce that the Company will pay an ordinary dividend of 2.7p (2020: 1.8p) per share for the fourth quarter of 2021, together with a special dividend of 3.8p per share, in recognition of the continued strong performance in the second half of the year. This brings the total dividend payments declared for the year to 17.0p (2020: 6.68p).”

- Including October’s Q3 2.2p per share dividend, WINK’s payout history now looks like this:

Valuation

- Shareholders must now guess what proportion of the exceptional activity of FY 2021 will carry through into FY 2022.

- Was the bumper FY 2021 a one off? Or has the pandemic and Brexit resolution re-ignited London’s housing market for the next few years?

- WINK’s update this week appeared positive:

“Buyer demand over the end of year break has been reported at record levels and sellers finally seem to be returning to the market. While this may hold back the solid growth in prices of the last two years, it bodes well for the number transactions and we expect another busy year.”

- Recent headlines from Property Industry Eye meanwhile painted a mixed picture:

- House price growth set to ‘slow considerably’

- One in three property sales fall through as market returns to ‘familiar conditions’

- Busiest festive period on record for homemovers, [Rightmove] data shows

- Housing market returning to pre-pandemic normality

- Agents urged to prepare for ‘a very busy year’

- Room for growth: UK housing market will continue ‘its upward climb‘

- ‘Race for space’ fuels demand for property in prime regional markets

- Operating profit during this (exceptionally strong) H1 plus the preceding (buoyant) H2 was £3.0m.

- Operating profit during pre-pandemic FY 2019 was in contrast £1.3m.

- Maybe somewhere in the middle — say, £2.2m — might prove the best guess of greater post-lockdown/Brexit transactions mixed with a general cooling of activity.

- Profit of £2.2m taxed at standard 19% UK tax leaves earnings of nearly £1.8m or 13.9p per share.

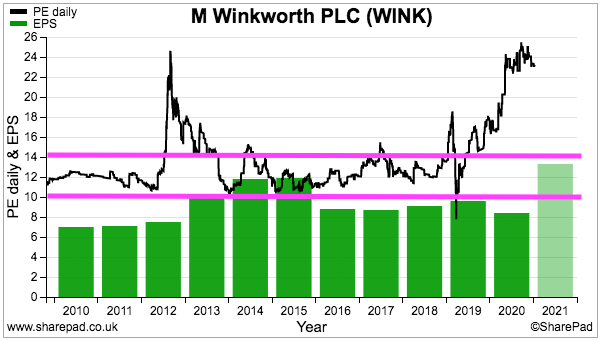

- Dividing the 208p share price by 13.9p per share gives a P/E of 15x.

- Assume the cash and investments of 40p per share are not required for the business to operate successfully, and a cash-adjusted P/E could be (168p/13.9p) = 12x.

- A multiple of 12x or 15x or somewhere in between does not feel completely outrageous for a business that has been trading very well and handing out special dividends.

- But the rating is not out of keeping with WINK’s typical trailing P/E of 10x-14x:

- WINK’s typical rating has reflected the group’s largely stagnant profit between FYs 2016 and 2020.

- But arguments for a upward re-rating include:

- A medium-term revitalisation of the London housing market following the pandemic and Brexit;

- Further market-share gains from FOXT and others;

- The possibility of higher margins as property transactions remain elevated, and;

- Additional Tooting-type deals that can deliver significant returns on investment.

- The aforementioned record Q4 dividend completes an ordinary FY 2021 payout of 9.3p per share that supports a trailing yield of 4.3%.

- Annualising the Q4 dividend gives a potential ordinary FY 2022 payout of 10.8p per share and a possible 5.0% yield.

Maynard Paton