08 November 2016

By Maynard Paton

Quick update on Getech (GTC).

Event: Final results for the year to 31 July 2016 published 08 November 2016

Summary: A lot happened at GTC before these results and I am no longer as keen on the group as I once was. That said, the figures from this specialist data supplier to the oil and gas industry were not truly awful — a profitable second half gives hope that one day the business will recover. The asset-rich balance sheet also lends support. But a new boss and various acquisitions just don’t make me entirely comfortable. I continue to hold.

Price: 28p

Shares in issue: 37,562,415

Market capitalisation: £10.5m

Click here for all my previous GTC posts

Results:

My thoughts:

* A lot happened during the run-up to these results

There have been three significant developments at GTC since I reviewed the firm’s first-half numbers during April:

1) Profit warning

A profit warning was issued in June that blamed a “very depressed” oil and gas market. The alert was not too surprising given GTC supplies geological data to the sector, but at least the group did say it expected to generate a profit before tax for the full year.

That profit expectation was reassuring given the first-half loss, but closer inspection of these 2016 figures showed the reported profit was achieved only through a one-off gain (see later).

2) Acquisition of Exprodat

GTC agreed to buy this geographical information systems consultancy for £1,760k during July.

I concluded at the time that:

“It seems this deal will diversify GTC’s services to the oil sector, as well as diversify its services to outside the oil sector. As such, GTC’s dependence on its proprietary geodata libraries will diminish, which may help in the shorter term, but long term — assuming an oil-sector recovery — may not make the group’s margins and cash flow as attractive as they once were.

The deal also makes GTC’s progress even more complicated to evaluate.”

3) Appointment of new chief executive

GTC announced the appointment of Dr Jonathan Copus as chief executive during August.

Dr Copus has worked as an exploration geologist at Royal Dutch Shell, as an equity analyst at Deutsche Bank and as chief financial officer at Salamader Energy. He is only 44, too.

The appointment did not look too bad in the circumstances.

* GTC diverging from my portfolio

When I bought my GTC shares during 2013 and 2014, the firm had been run by a long-time employee, had not bought other businesses and appeared to boast an array of lucrative, proprietary data.

All that was enough to keep me holding the shares as the business suffered from the oil-price crash.

However, now there is a new chief exec, while the aforementioned Exprodat deal and the larger ERCL purchase have signalled (perhaps) that the proprietary data may not be all that lucrative anymore.

As such, I am starting to feel there may be better long-term homes for my GTC money.

You see, what has become (belatedly) obvious to me is that GTC does not compare too well to, say, BrainJuicer and Bioventix — two new shares I bought earlier this year — both of which are run by long-time, owner-founder executives who don’t rely too much on acquisitions for growth.

* What the small-print revealed about the predicted profit

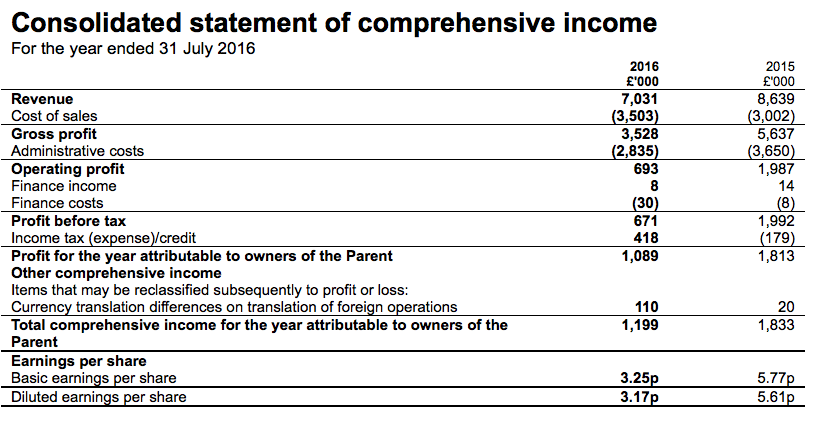

These annual results were the worst for some years:

| Year to 31 July | 2012 | 2013 | 2014 | 2015 | 2016 |

| Revenue (£k) | 6,441 | 8,011 | 6,593 | 8,638 | 7,031 |

| Operating profit (£k) | 1,254 | 2,221 | 969 | 1,987 | 693 |

| Finance costs (£k) | (7) | 25 | 32 | 5 | (22) |

| Other items (£k) | - | - | - | - | - |

| Pre-tax profit (£k) | 1.247 | 2,246 | 1,001 | 1,992 | 671 |

| Earnings per share (p) | 3.18 | 5.57 | 5.21 | 5.77 | 3.25 |

| Dividend per share (p) | 1.00 | 2.00 | 2.20 | 2.20 | - |

Reported revenue dropped 19%, though don’t forget the 2016 performance was supported by a full-year contribution from ERCL.

Had ERCL been owned throughout 2015, the revenue drop for 2016 would have been 40%.

An operating profit of £693k was declared, although the small-print revealed the results were boosted by a one-off £845k gain (my bold):

“Getech’s second half profit before tax amounted to £1,375,000. This included an £845,000 write-down adjustment made to the fair value of the ERCL acquisition earn-out provision (the amount by which the total cash consideration for the ERCL acquisition has reduced from our original expectation). Full year profit before tax was £671,000 (2015: £1,992,000).”

I think it was somewhat cavalier of the group to suggest in June that these results would show a pre-tax profit — and not explain that such a profit would be underpinned only by this one-off gain.

(At least the new chief exec had yet to be appointed when June’s statement was issued.)

* A much better second half

I’m thankful GTC enjoyed a better second half:

| H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | ||

| Revenue (£k) | 3,619 | 5,020 | 8,639 | 3,288 | 3,743 | 7,031 | |

| Operating profit (£k) | 703 | 1,284 | 1,987 | (697) | 1,390 | 693 |

A few extra contracts talked about at the half-year stage combined with an underlying 17% reduction to the cost base gave rise to a second-half profit.

Adjust for the aforementioned £845k gain and the H2 operating profit would have been £545k.

Still, that level of H2 profit does not feel too bad in light of the first-half loss and June’s profit warning.

* Capital expenditure and cash flow

Although GTC’s cash flow shows nothing obviously untoward, there are a few niggles.

| Year to 31 July | 2012 | 2013 | 2014 | 2015 | 2016 |

| Operating profit (£k) | 1,254 | 2,221 | 969 | 1,987 | 693 |

| Depreciation and amortisation (£k) | 203 | 214 | 240 | 366 | 671 |

| Net capital expenditure (£k) | (51) | (190) | (190) | (1,364) | (856) |

| Working-capital movement (£k) | 766 | 942 | (1,574) | 573 | (448) |

| Net cash (£k) | 2,606 | 4,249 | 3,423 | 3,694 | 1,888 |

Capitalised development costs is now one area I’m unsure of.

In the past I had concluded the firm’s hefty intangible expenditure — which is not charged against profit but instead travels directly to the balance sheet — related to a certain multi-satellite project.

I had expected this capitalised expenditure to reduce substantially from this year on, but I read the following extract and wondered whether further capitalised expenditure will now continue:

“Getech has continued to invest in its Globe platform, with expenditure of £824,000 (2015: £977,000). The Globe platform is amortised over a 3 to 7 year period, and the first full year of amortisation has resulted in an increase in the Group amortisation costs from £186,000 in the 2015 financial year to £479,000 in the 2016 financial year. The Globe platform continues to be a key asset to Getech, forming the basis for many of the Company’s cutting-edge products.”

Expenditure of £824k and associated amortisation of £479k leaves a £345k difference — which is a notable sum for this small business.

I do not mind capitalised expenditure, just as long as the associated amortisation is adequate and reported profit is not boosted artificially.

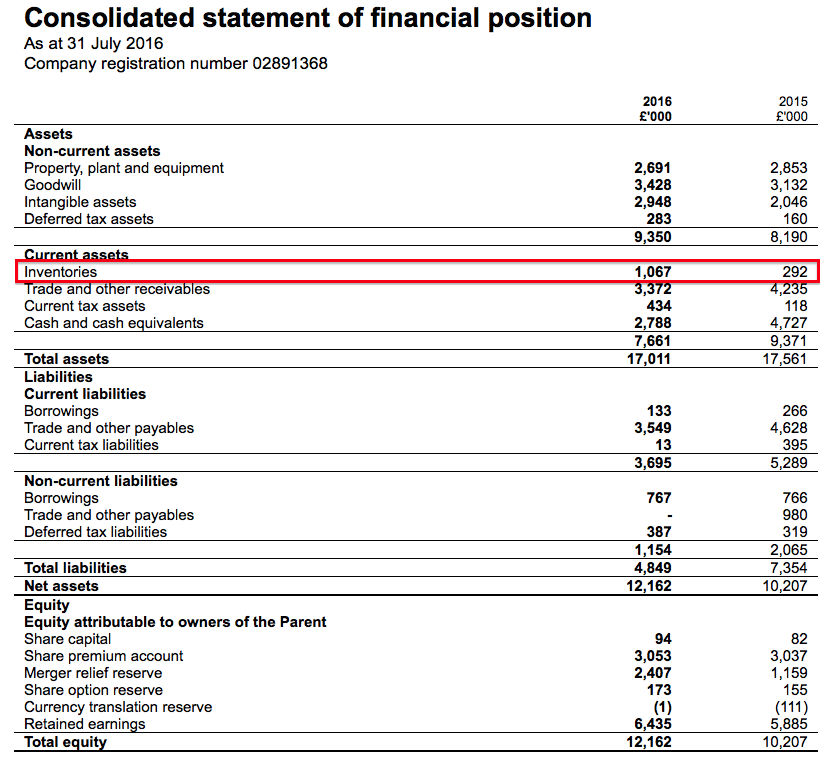

Elsewhere in the numbers, GTC’s total working capital-movement for 2016 did not look too worrying. But I did notice stock levels surge by a significant £775k to £1,067k:

At least GTC suggested the movement was more of a timing issue than a backlog of unsold products:

“Inventories have increased by £775,000 over the year (2015: £112,000) due to the timing of the multiclient Regional Reports product cycle, with several new reports nearing completion at the end of the financial year, creating new products to be sold in 2017.”

* Balance sheet and ERCL earn-out

GTC’s balance sheet remains relatively strong.

Alongside net cash of £1.9m, there is freehold property that should continue to carry a £2.5m book value (the upcoming annual report should confirm this).

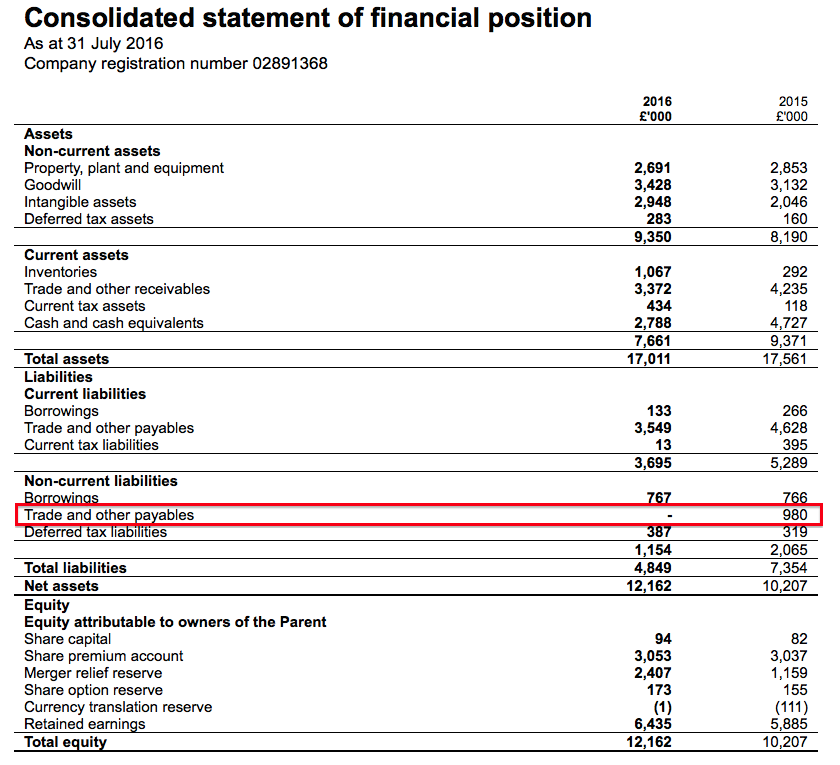

One notable balance sheet movement is the disappearance of a long-term £980k liability:

This liability reflected GTC’s potential payment to cover an earn-out relating to the ERCL purchase last year.

I had sensed this earn-out was somewhat high given how the wider group had performed following the acquisition.

Anyway, the £980k cancellation relates to the aforementioned £845k one-off gain (my bold):

“Getech’s second half profit before tax amounted to £1,375,000. This included an £845,000 write-down adjustment made to the fair value of the ERCL acquisition earn-out provision (the amount by which the total cash consideration for the ERCL acquisition has reduced from our original expectation).”

To cut a long story short, I reckon the earn-out provision is now £135k and has to be paid during the current financial year (to July 2017).

* A handful of positives to support a recovery

The management narrative contained a few paragraphs of hope for shareholders (my bold):

“While the market is at best uncertain, our dialogue with our customers remains vigorous and the Group has a pipeline of significant sales proposals awaiting approval. As we approach the end of our customers’ budget year, for the first time in several years, feedback from clients leaves us encouraged by the market mood; the recent increase in the oil price gives our customers more confidence that their budgets will become available in 2017.”

“Having built an unparalleled suite of global geological and geophysical knowledge bases, Getech is now moving towards a model where the Group is focussed on enhancing this offering through providing better access to its data sets and refocussing its products and services so that they more specifically address the commercial challenges faced by our customers.”

“As a key part of its activities, Exprodat has developed, and licenses commercially, several GIS software packages that support petroleum exploration. During the current downturn, the client retention of these subscription-based software products has been approximately 95%; this brings a substantial client base to Getech, with a significant proportion of recurring income.”

At what point any of this eventually translates into a proper recovery unfortunately remains anyone’s guess.

But if a recovery does arrive, GTC may once again sport some attractive financial ratios. The operating margin and return on average equity in particular could rebound to past highs:

| Year to 31 July | 2012 | 2013 | 2014 | 2015 | 2016 |

| Operating margin (%) | 19.5 | 27.7 | 14.7 | 23.0 | 9.9 |

| Return on average equity* (%) | 27.1 | 59.1 | 44.7 | 33.3 | 13.0 |

(*adjusted for net cash)

Summary

I am not really tempted to buy more GTC shares because of my earlier comments about the company diverging from the bulk of my portfolio.

However, for now at least, the business has net cash, enjoyed a profitable H2 and still provides a range of specialist data and services — although revenue from the wider group is now increasingly earned from other products.

I suppose one day I could look back at GTC and declare the current 28p share price as having been a superb buying opportunity — assuming the oil and gas sector recovers and GTC capitalises on the revival.

In the meantime, though, I guess other businesses with greater tenured management and less dependence on acquisitions could also generate robust returns.

Maynard Paton

Disclosure: Maynard owns shares in Getech.

Getech (GTC)

Publication of 2016 annual report:

http://www.getech.com/wp-content/uploads/2016/11/Getech-Group-plc-Annual-Report-and-Accounts-2016.pdf

Here’s what I noted in the latest annual report.

1) Business positives

A few more snippets from GTC that suggest the main business (pre-acquisuitions) enjoys a good competitive advantage.

2) Substantial shareholders

I thought disclosing shareholders with 3% or more of the company was the standard for annual reports.

GTC has gone for 10%, which is a bit annoying as quite a few GTC employees now own 3%-plus as they received GTC shares in exchange for their ERCL or Exprodat shares:

3) Board meetings

I always look at these board-meeting numbers, just to see if any directors are not pulling their weight:

At least Dr Carey leaves at the end of 2016, so I guess his absences are understandable.

Mr Edwards was the lead executive of ERCL, so his absences are a bit of a shame. I am pleased there were two audit meetings against one remuneration meeting — I do prefer my boards to talk more about audits and risk than their own pay.

4) Director pay

Director wages appear under control:

Nice to see non-execs Fielding and Stephens taking fee reductions this year and doing their bit to reduce costs.

Non-exec chairman Dr Paton enjoyed a greater fee, presumably due to his increased workload following the chief exec change. It is unusual that a non-exec chairman receives a pension contribution — I get the impression he is more part-time non-exec/part-time exec.

5) Employee numbers

I was surprised to see the staff number rise from 100 to 114, especially as GTC had referred to reducing its cost base by an annualised 22% during the second half:

Exprodat brought 20 new employees to the group in June 2016, and ERCL brought 26 new employees in April 2015.

So 46 new ‘acquired’ staff were employed during the last two years when average staff numbers went from 75 to 114 — an increase of 39.

It therefore seems to me the headcount at the main business has been reduced by 7 (39 less 46) — which does not seem a lot of redundancies.

Revenue per staff member at £61k for 2016 was the lowest since 2010, and the second-lowest since the 2005 flotation. (It was £114k in 2013)

6) Largest customer and geographical revenue split

This is probably the most encouraging table within the whole annual report:

Firstly, GTC’s 2016 performance was not dominated by a particularly large client. Between 2011 and 2015, every year saw at least one client produce 12% or more of total revenue.

Secondly, we have confirmation that UK revenue represented only 12% of total revenue. I trust the weaker GBP could help GTC’s top line during 2017.

This note suggests profit would have been higher during the year had GBP traded at its current level:

7) R&D cutback

I see the general cost-cutting has impacted the amount spent on R&D:

Not great, but perhaps understandable given the group’s position.

The R&D figure reported for 2015 was £1,341k in the 2015 annual report — so an unexplained adjustment has occurred to show it now as £1,434k.

8) Acquisition of Exprodat

The small-print suggests Exprodat did not have a great year:

I therefore reckon Exprodat recorded revenue of £2,408k and a pre-tax loss of £264k for the year to 31 July 2016.

That compares with revenue of £3,419k and a pre-tax loss of £109k reported for calendar 2015 as disclosed at the time of acquisition.

The £109k loss was explained at the time as being due to “one-off restructuring expenses“, and I trust the £32k profit Exprodat recorded during its 7 weeks or so as part of GTC is more representative of its future performance.

That said, Exprodat suddenly losing revenue of £1m is quite scary — unless some of that revenue was actually from GTC itself.

9) Goodwill value

This is an unusual accounting note for a small company:

It appears to suggest GTC’s acquired goodwill — which is in the books at £3m — could actually be worth almost £12m.

For context, GTC’s current market cap is £10.5m at 38p.

10) Trade payables

An interesting note here:

First, other payables now total £635k.

It has never been 100% clear, but I have deduced other payables have mostly represented the future earn-out payments of acquisitions.

The £845k write-off mentioned in the Blog post above has essentially cleared that £980k other payable liability, and the remaining £135k must now be part of that £635k figure.

Also, GTC remains on the hook for £250k to pay for Exprodat, which is I guess also included in that £635k.

Second, deferred income and accruals remain sizeable, albeit lower than 2015. This entry generally represents upfront payments from clients for services yet to be delivered, and it is useful to have such income on the balance sheet ready to be ‘earned’ for 2017.

11) Trade receivables

This is something to watch:

While year-end trade receivables of £2,371k represents a not-unusual 34% of revenue, the size of receivables past-due-but-not-impaired has increased during a year when revenue actually decreased.

These past-due-but-not-impaired receivables represent 15% of 2016 revenue — for perspective, the figure bobbed between 3% and 9% during the previous five years.

Maybe this is purely a timing issue. Or maybe GTC’s hard-pressed oil-sector clients are struggling to settle invoices.

12) Intangible amortisation

So here is the full intangible assets note:

It seems to me GTC spent £823k on internal intangible developments and the associated amortisation was £266k — a sizeable £557k difference that is greater than the figure I had mooted in the Blog post above.

Within the annual report, GTC confirms the multi-satellite project -=- which I believe these development costs relate to — has now been completed.

As such, I do not expect major intangible expenditure next year. But that may prove to be wishful thinking. Either way, the amortisation charge should be somewhat higher during 2017.

(The £451k software development intangible shown in the note above relates to the purchase of Exprodat.)

13) Miscellaneous

GTC’s freehold is now valued at £2,475k and 2,250k options represent 6.0% of the total share count.

Maynard

Getech (GTC)

AGM statement:

http://www.investegate.co.uk/getech-group-plc/rns/agm-statement/201612130700076302R/

I was quite surprised by this statement, not least because it was GTC’s first AGM statement since 2009. The statement also contained some welcome news about contracts.

Here is the full text:

———————————————————————————————————————————–

At today’s Annual General Meeting, Jonathan Copus, the Chief Executive Officer of Getech (AIM; GTC), a provider of data, studies and services to the natural resources and energy sectors, will give the following update:

“In 2016 Getech focused its operations on targeted investment in our core business, counter-cyclical M&A, and the active management of costs. These actions combined to deliver a significant rebound in profitability in the second half of our 2016 financial year. Since reporting 2016 results, we have secured several strategically important new contracts and our day-to-day activities continue to be focused around the customer, profitability and diversified growth.

Business update

In 2016 Globe entered its sixth year of continuous customer support, the MultiSat programme was delivered, a wide range of new Regional Reports were released and we completed an extensive, multi-disciplinary basin review for Sonangol. We continued to support the Mozambique Government’s petroleum activities, captured new World Bank funded consultancy opportunities in Sierra Leone and in June 2016 we strengthened our offering through the acquisition of Exprodat, a provider of cutting-edge Geographic Information Systems (GIS) services and software products.

Since the completion of this transaction, Getech has focused its geoscience, GIS, software and consulting skills on growing the Group’s operations both within and beyond our core oil & gas exploration customer base. It is pleasing therefore to announce that we are ending the calendar year having secured a new sale of Globe phase-two to a super-major, and we have been contracted by the UK Oil and Gas Authority (the “OGA”) to develop and implement a GIS information management strategy. This work for the OGA extends our operations beyond our core exploration market, being focused on spatial data that spans the full E&P asset life-cycle. In addition, having won our first contract within the nuclear industry in the previous financial year, Getech is currently at an advanced stage of discussions to expand on this work.

Financials

As previously announced, financially, 2016 was a year of two distinct halves. In the first half, slow trading and higher costs lead to a loss before tax of £704,000. In response, Getech took a range of hard decisions and implemented a significant programme of cost control measures. From a lower cost base, and with a 14% rebound in revenues, our underlying performance significantly improved in H2-16; the Group reporting a full year profit before tax of £671,000.

We believe these operational and financial highlights illustrate that despite the challenges faced by the wider natural resources market, our clients continue to see value in our integrated, multi-disciplinary approach, which in turn is underpinned by excellent data, high quality staff, and a strong GIS platform.

The Board however also continues to act with prudence. The Group remains focused on cost control throughout the business and the Board decided to not propose a 2016 dividend.

Outlook

Looking to 2017, although the outlook for our core exploration market remains uncertain, feedback from customers leaves us cautiously encouraged by the market mood. We have no intention however to sit back and wait for a rebound.

With an expanded operational skill set, Getech is entering a period where we are focused on profitability and opportunities to enhance and diversify our commercial offering. We will do this through an improved value proposition around our activities, the provision of better access to our data/analysis and refocusing of our products and services so that they more practically address the day-to-day commercial challenges faced by our customers; our goal being to deliver products and services with practical applications and demonstrable value”.

Stuart Paton, Chairman of Getech Group plc, said: “I am extremely pleased with the progress that the Company has made in the last four months under the leadership of our new CEO Dr Jonathan Copus. The market remains challenging and we continue to have to make difficult decisions to ensure the robustness of the business. However, with new leadership, diversification into new areas, and a stronger oil price, I am confident in the future growth of Getech. Central to achieving this is cultural change, and at the heart of this lies the continued integration of activities across our project teams and offices. I would like to take this opportunity to thank all of Getech’s staff for their continued hard work and dedication.”

———————————————————————————————————————————–

Key lines on contracts are:

“Since reporting 2016 results, we have secured several strategically important new contracts”

“It is pleasing therefore to announce that we are ending the calendar year having secured a new sale of Globe phase-two to a super-major, and we have been contracted by the UK Oil and Gas Authority (the “OGA”) to develop and implement a GIS information management strategy.”

“In addition, having won our first contract within the nuclear industry in the previous financial year, Getech is currently at an advanced stage of discussions to expand on this work.”

The tone of the statement is quite encouraging, at least in light of the last few years and GTC’s struggles to win business during the oil-price downturn.

Another interesting piece of text was this:

“Central to achieving this [future growth] is cultural change”

I wonder if the new chief exec is now implementing a more profit-focused approach to the business. You see, GTC was formed by professors from Leeds University and I suspect the business may have had more of an academic bias in the past.

I still maintain that GTC has diverged away from the bulk of my portfolio, what with its unproven chief exec and various acquisitions. But at least there are now signs of a recovery appearing at the business.

Maynard