14 September 2016

By Maynard Paton

Quick update on M Winkworth (WINK).

Event: Interim results for the six months to 30 June 2016 published 13 September 2016

Summary: A quite satisfactory statement that suggested this London-dependent estate agency should be able to cope with the capital’s slower property market. Indeed, the business appears keen to expand and the pace of its new franchisee openings may in fact accelerate. Margins remain high, the balance sheet remains strong and a P/E of 7 seems to price in a lot of bad news. I bought more shares in August and continue to hold.

Price: 115p

Shares in issue: 12,733,238

Market capitalisation: £14.6m

Click here for all my previous WINK posts.

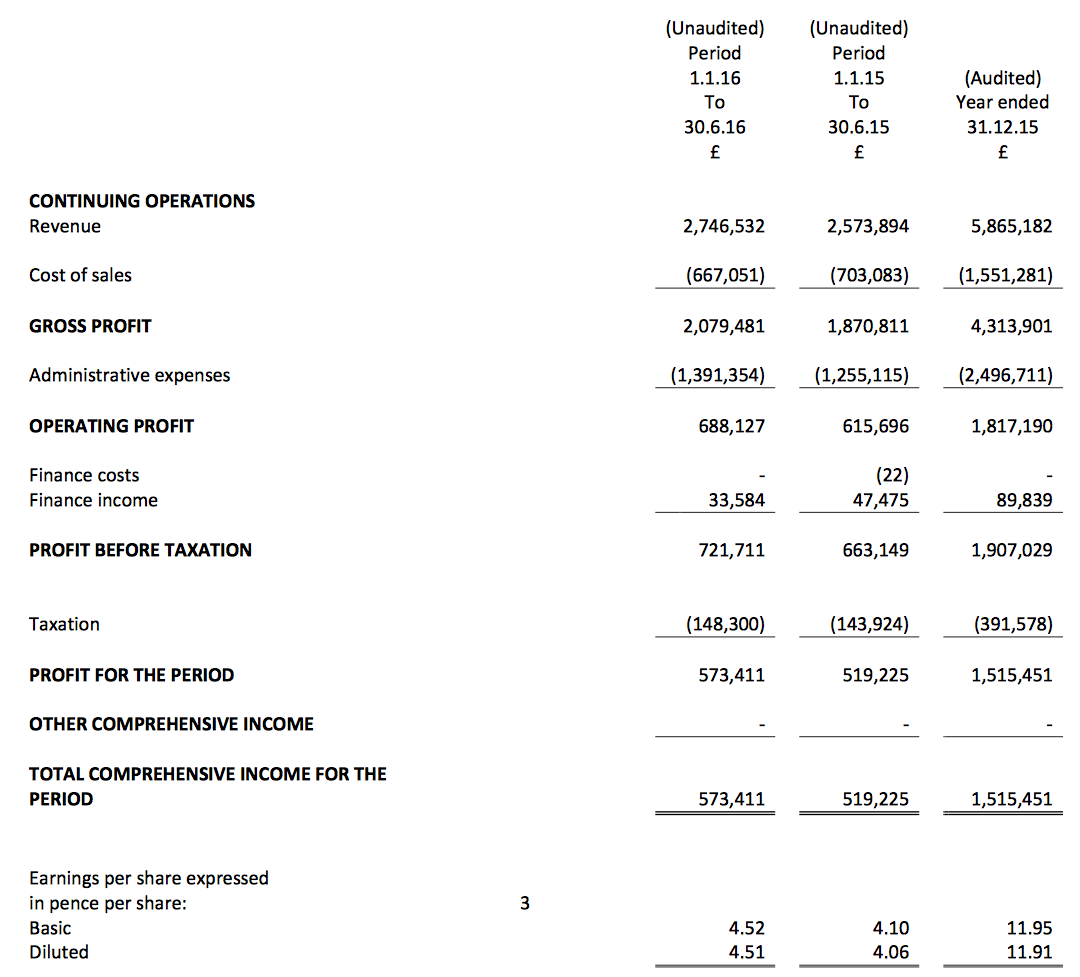

Results:

My thoughts:

* These results were quite satisfactory

I suppose WINK’s statement could have been a lot worse. Rival London estate agent Foxtons (FOXT) issued a profit warning a few days after the EU referendum and worries about a slowing housing market in the capital have dogged WINK’s shares ever since.

In the event, WINK’s figures were not too bad.

Bolstered by a bumper first quarter, during which buyers completed transactions ahead of new stamp-duty rates, WINK’s revenue gained 7% to £2.75m.

Commissions from property sales gained 5% while lettings-related income climbed 11%. I note lettings-related income now represents 40% of total revenue, up from 33% two years ago, and is closing in on the group’s 50% target.

WINK admitted it experienced a “slowing sales market” during the second quarter, although the firm expects trading to “pick up from the lows of June and July” and therefore is confident that it can “perform satisfactorily during the current financial year”.

Past years have seen some 80% of revenue emanate from the group’s London-located franchisees, although WINK is not too dependent on scarce buyers of prime Zone 1 properties. Earlier this year, the group confirmed the average property sale price throughout its offices was £645k.

Interestingly, WINK added that rental applications were up 40% year-on-year in July, so giving the firm a “strong start” to the second half (at least in the lettings division).

I also see visits to WINK’s website have recovered strongly since the Brexit vote:

* Bravado from the new franchising manager

I am pleased WINK continues to keep almost 12% of all the income produced by its franchisees as its own revenue. I’m also pleased the business is positive about future franchisee opportunities (my bold):

“A further two new offices were opened in Colindale and Marlborough, while three existing offices were resold to new management. One office in the UK and two in Portugal were closed.

Over the coming six months we anticipate a further 6-8 new openings and a further 1-2 resales, while longer term we expect to see an increase in opportunities both to convert existing businesses to the Winkworth brand and to grow new franchises.

A weaker sales market tends to encourage employees whose income is declining to boost their earnings by owning equity in an estate agency, while existing agents look to grow their market share, reduce costs and explore new options, of which we are one. “

I see on WINK’s website that the group’s new franchising manager has shown some bravado by predicting up to 50 new franchises could be opened during the next five years:

“As the housing market bounces back into life after the summer break and the Brexit vote, we believe it is the right moment to put our foot on the accelerator,” says Mountford. “If all goes according to plan, we intend to open between eight to ten new franchises a year over the next five-year period.”

Hopefully the new man will indeed kick-start an enlarged franchise network. Following WINK’s flotation during 2009, the firm’s network has grown slowly, from 86 to only about 100 branches today.

WINK’s relatively upbeat view on expansion contrasts with FOXT, which said within its July results that it was “reviewing the pace of our branch openings over the short term and may slow the pace of expansion in response to market conditions”.

* No major faults within WINK’s accounts

Despite WINK spending an unspecified amount on an office move, the first-half operating margin still increased a fraction to a robust 25%.

WINK’s cash position dropped by £0.3m to £2.8m during the six months as the business appears to have loaned up to £0.7m to new franchisees. The rest of the cash generated was effectively paid out as dividends.

I noted in March that WINK does earn respectable sums from these loans to franchisees.

This half produced interest of £34k, which seems light compared to last year’s £47k, but nonetheless represented 5% of the overall pre-tax profit.

These accounts did not divulge the exact amount loaned to franchisees (it was £1.2m at the end of 2015), and management remarks suggest further loans will be made:

“We believe that there is a significant opportunity for us to grow the franchise base by adding quality businesses and people at reasonable valuations. With net cash available in excess of £2.8m, we will invest in new franchising capacity in order to ensure that we capture the best available opportunities without endangering our dividend policy.”

Valuation

WINK’s operating profit for the year to June 2016 was close to £1.9m, which after 20% standard tax gives earnings of £1.5m or 11.9p per share.

Adjusting the £14.6m (at 115p) market cap for my £4.0m estimate of cash and franchisee loans, I arrive at an enterprise value of £10.6m or 83p per share.

Then dividing that 83p by my 11.9p per share earnings guess gives a P/E of just 7.

Meanwhile, the trailing dividend is 6.9p per share and supports a 6% income.

Even with a fragile housing market in London — plus the risk perhaps of online competition — those ratings appear very good value to me.

So much so, I must confess to buying more WINK shares last month. I increased my holding by 43% and paid 110p including all costs.

Maynard Paton

Disclosure: Maynard owns shares in M Winkworth.

M Winkworth (WINK)

Trading Update:

http://www.investegate.co.uk/m-winkworth-plc/wink/trading-update/201611101516319084O/

Oh dear — a “moderate” profit warning. Here is the full text:

—————————————————————————————————————–

In our interim statement we referred to ongoing economic uncertainty, but noted that trading was expected to pick up from the lows of June and July and that transactions in the country and suburban London markets were expected to return to growth in the latter part of the year. At that point, stock levels across the industry were low as sellers waited for greater visibility before marketing their property.

Since that time we have seen purchasers returning, albeit at a lower level than this time last year, and a moderate upturn in sales. Uncertainty continues to weigh on transactions, however, as some sellers withdraw from the market with the intention of reviewing their situation in 2017.

Meanwhile, we have seen rental prices softening in line with an increase in supply of properties following the surge in buy-to-let purchases prior to the rise in stamp duty in the spring. We do not expect to see this dynamic changing in the immediate future.

As a result of the slower than anticipated level of activity over the autumn, both sales and full year profits are likely to be moderately below market expectations. We are today, nonetheless, declaring an increased dividend for the third quarter of 1.8p and the full year ordinary dividend payment will once again be ahead of the previous year.

Going into 2017, we continue to anticipate a further 6-8 new openings and a further 1-2 resales, while longer term we expect to see an increase in opportunities both to convert existing businesses to the Winkworth brand and to grow new franchises.

Dominic Agace, Chief Executive Officer of Winkworth, commented:

“The referendum on Europe and results of the US presidential elections have provided much cause for reflection over the course of this year and it is perhaps no surprise that some homeowners have put moves on hold as a result. The fundamentals of the housing market in London and its surrounding areas remain strong, however, and with a business model which adapts well to changes in market activity we remain very confident in the long term outlook for the Company.”

—————————————————————————————————————–

WINK appointed a new house broker earlier this year, and here are the broker’s forecasts from September:

So perhaps 2016 earnings could be about 9p per share.

I should add that WINK provided a subdued update this time last year, and it transpired the group enjoyed a buoyant December and the 2015 figures were actually better than expected.

That said, WINK’s references to the “long-term outlook for the Company” does suggest the short- to medium-term outlook could be somewhat cloudy.

Anyway, assuming earnings are 9p per share, my quick sums based on the Valuation numbers fem the Blog post above give a cash-adjusted P/E of 8.7x at a 110p share price.

The announcement of a Q3 1.8p per share dividend means the 12-month payout is running at 7.1p per share and supports a 6.4% income.

Maynard

M Winkworth (WINK)

Diary of an estate agent:

http://www.homesandproperty.co.uk/property-news/diary-of-an-estate-agent-streatham-a106086.html

Could be the usual estate-agent guff of course, but WINK’s new office in Streatham, south London appears to be busier than it has been:

Wednesday

There is without a doubt more activity now than there has been since Brexit.

Maynard

M Winkworth (WINK)

Issue of share options:

http://www.investegate.co.uk/m-winkworth-plc–wink-/rns/issue-of-share-options/201609260814437886K/

This option grant was announced back in September, but I forgot to remark on it at the time. The interesting point is the exercise price — 200p:

On 13 September 2016, options over 0.5p ordinary shares in M Winkworth plc (the “Company”) were granted to Dominic Agace, Chief Executive Officer of the Company. The options are exercisable at a price of 200 pence per share with effect from 13 September 2019.

Clearly WINK will have to go some for the chief executive to enjoy these options when the current share price is 110p and the business appears to be committed to at least sustaining a hefty 7.2p per share dividend.

That said, I do like these types of options, which are defined by an exercise price much higher than the present share price. Clearly the board felt 200p ought to be achievable at some point.

Maynard

M Winkworth (WINK)

Website traffic data

I occasionally visit Alexa.com to check on website traffic to winkworth.co.uk. It is a crude tool, as it reveals website data only in terms of global ranked popularity (1st, 2nd, 3rd etc), rather than disclose absolute page views etc. However, the accompanying charts can give a useful indicator of waxing or waning traffic.

Here is the latest Alexa chart for winkworth.co.uk:

Not great.

But if anything the chart of rival London agent Foxtons looks worse:

In fact, a whole host of property websites — including Rightmove — appear to have lost their popularity during the last few months:

Maynard

Too much attention to Presidential election maybe Maynard!

M Winkworth (WINK)

Q4 Dividend Declaration:

http://www.investegate.co.uk/m-winkworth-plc/wink/dividend-declaration/201702080700092633W/

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.8p per ordinary share for the fourth quarter of 2016. The total dividend paid to shareholders for the financial year ended 31 December 2016 will be 7.2p per ordinary share. The timetable is as follows:

Ex-Dividend Date * 16/02/17

Record Date ** 17/02/17

Expected Payment Date 16/03/17

No surprises here. A 1.8p per share matches the payments for Q1, Q2 and Q3. The next (Q1) dividend announcement in May ought to be interesting. That payment will be the first for the current 2017 financial year and may provide some indication of whether trading is as subdued as the share price suggests.

Maynard

M Winkworth (WINK)

Preliminary Results from Foxtons (FOXT)

http://www.foxtonsgroup.co.uk/investors/results/files/foxtons_preliminary_annual_results_2016.pdf

http://www.foxtonsgroup.co.uk/investors/results/files/foxtons_annual_results_2016_presentation.pdf

Today’s results from FOXT contained various snippets about the London housing market. I like to monitor FOXT as the agency is London’s largest and WINK’s business performance has generally tracked that of FOXT up and down.

According to FOXT, higher stamp-duty rates and the EU referendum prompted property transactions to slump in the capital during the second half of 2016.

FOXT estimates transaction numbers from Q2, Q3 and Q4 were 44% below the corresponding quarters of 2015, and are now running at levels seen during 2009 and the depths of the banking crash.

Here are two charts from FOXT’s presentation:

The downturn saw FOXT’s H2 revenue from property sales drop a substantial 38%, from £38.7m to £24.0m. That performance does not bode too well for WINK’s upcoming figures.

The table below compares WINK’s gross franchisee revenues (for property sales and lettings) against those of FOXT. Generally WINK’s gross sales revenue is about 45% of FOXT’s, while its lettings revenue is 28% of FOXT’s.

During the last three halves, the WINK-to-FOXT sales revenue ratio has improved from 40% to 43% to 45%, so I can only hope that mini-trend continues for H2 2016… and that WINK’s H2 property-sales revenue does not drop 38%.

WINK’s ambition is to derive 50% of its revenue from lettings, and I get the impression that target may be reached if WINK has indeed suffered a dismal H2 for property sales transactions.

Maynard

M Winkworth (WINK)

Chestertons Blog

http://www.chestertons.com/research-and-insight/insights/a-strong-start-to-2017/

Courtesy of topazfrenzy on the ADVFN boards — a straw to clutch about London property sales (my bold).

The second and third quarters of last year were some of the toughest faced by the London property market for a few years, with less people buying and selling as they adjusted to the referendum result and took time to digest what it meant for them and the country. However, this pause in market activity seems to have been only very temporary as Chestertons’ 32 branches all saw a considerable uplift in activity in the last six weeks of the year, with more buyers registering and more sellers looking to sell.

That activity has pushed through in 2017 giving us a very strong start to the year with the number of sales up 15% from this time last year, which is even more impressive when you remember that there was a gold rush by investors looking to complete on purchases before the 3% Stamp Duty surcharge was introduced in April last year.

M Winkworth (WINK)

Article on Property Eye:

http://www.propertyindustryeye.com/is-life-returning-to-prime-central-london/

“Agents are reporting the prime central London (PCL) market is returning to life, with a suggestion that gazumping is back.

Buying agent Camilla Dell, managing partner of Black Brick, said properties in the prime central London area are now selling fast and often at over asking price.”

A straw to clutch perhaps.

Maynard