15 March 2016

By Maynard Paton

Quick update on French Connection (FCCN).

Event: Preliminary results for the year to January 2016 published 15 March

Summary: An improved set of figures following last year’s awful interims. However, the numbers do suggest FCCN experienced a weaker Christmas while the cash pile really can’t afford another £9m outflow. Online sales were miserable, too. Still, Retail gross margins during H2 were the highest since 2011 and new board members may well help the moribund management. This value investment still requires inordinate patience… and I continue to hold.

Price: 43p

Shares in issue: 96,253,134

Market capitalisation: £41m

Click here for my previous FCCN posts

Results:

My thoughts:

* Improved second half, but did the Retail division suffer a weak Christmas?

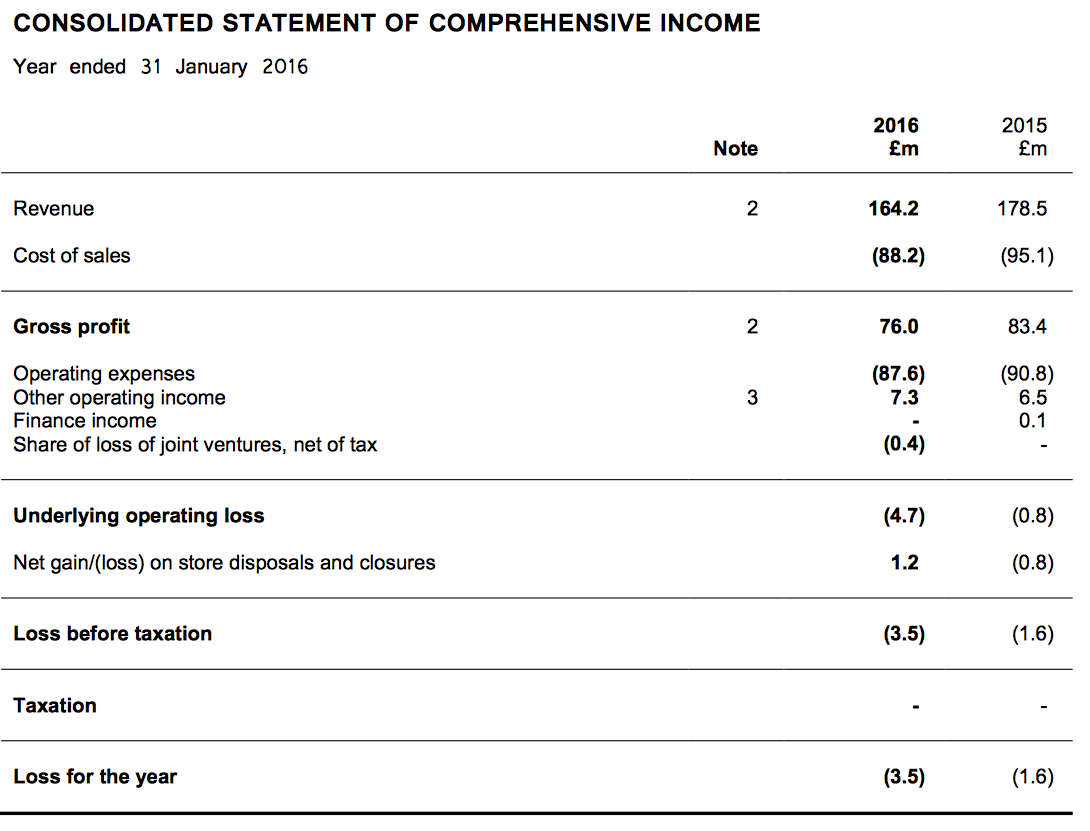

September’s basket-case set of interim figures meant that these full-year numbers were never going to be great.

In the event, FCCN reported its seventh pre-tax loss in the last eight years and the fourth consecutive absence of any annual dividend.

A trading statement in November had already hinted of improved trading and the second half did indeed score a slightly larger profit than the second half of the previous year (£3.2m vs £3.1m):

| H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | ||

| Revenue (£m) | 84.0 | 94.5 | 178.5 | 75.8 | 88.4 | 164.2 | |

| Operating profit (£m) | (3.9) | 3.1 | (0.8) | (7.9) | 3.2 | (4.7) |

However, the H2 progress was due to greater licensing income and lower central costs. Sadly the troubled Retail division witnessed its H2 loss widen on last year (-£4.5m vs -£3.8m):

| H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | ||

| Retail profit (£m) | (7.5) | (3.8) | (11.3) | (11.1) | (4.5) | (15.6) | |

| Wholesale profit (£m) | 6.2 | 8.4 | 14.6 | 5.5 | 7.8 | 13.3 | |

| Licensing profit (£m) | 2.9 | 3.6 | 6.5 | 3.0 | 4.3 | 7.3 | |

| Common overheads (£m) | (5.6) | (5.1) | (10.7) | (5.2) | (4.1) | (9.3) | |

| Finance income (£m) | 0.1 | 0.0 | 0.1 | 0.0 | 0.0 | 0.0 | |

| Joint venture (£m) | 0.0 | 0.0 | 0.0 | (0.1) | (0.3) | (0.4) | |

| Operating profit (£m) | (3.9) | 3.1 | (0.8) | (7.9) | 3.2 | (4.7) |

I also note that like-for-like (LFL) sales within the Retail division look to have slipped over the Christmas period.

November’s update had said LFL sales had gained 0.2% between August and November, but today’s statement admitted LFL sales had dropped 2.4% between August and January.

* The cash position really can’t afford another £9m outflow

Further evidence perhaps of a not-so-great Christmas comes from FCCN’s cash position.

Going on November’s update and today’s results, it seems as if the group’s cash pile advanced from £6.1m to £14.0m during December and January — up £7.9m.

However, in comparison, the year before saw cash in those two months move from £7.6m to £23.2m — up £15.6m.

Sure, there could be timing issues or one-off factors at play here. But the contrast does not look great.

Plus, with FCCN’s cash pile eroding by £9.2m during the year, a repeat performance for 2016/7 might now push the business into the red during the low season.

I trust the possibility of soon going overdrawn is galvanising management to ensure otherwise.

* A 58% H2 Retail gross margin!

There was some good H2 news within the Retail division.

Though Retail revenue fell by £3.6m and gross profit dropped by £1.4m, the division’s H2 gross margin came in at 58.2% — the first time FCCN’s high-street stores have scored a 58%-plus gross margin since the six months ending July 2011!

| H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | ||

| Retail revenue (£m) | 49.9 | 53.4 | 103.3 | 42.6 | 49.8 | 92.4 | |

| Retail gross profit (£m) | 28.7 | 30.4 | 59.1 | 24.0 | 29.0 | 52.9 | |

| Retail operating expenses (£m) | (36.2) | (34.2) | (70.4) | (35.1) | (33.5) | (68.5) | |

| Retail profit (£m) | (7.5) | (3.8) | (11.3) | (11.1) | (4.5) | (15.6) | |

| Retail gross margin (%) | 57.5 | 56.9 | 57.2 | 56.3 | 58.2 | 57.3 |

FCCN claimed the H2 gross-margin performance was due to “increased full-price trading, shorter discount periods and an increase in the input margin for the Winter season”.

Whatever the reason, higher gross margins do indicate a better product and I just hope this 58% level can be sustained to help stem the Retail division’s losses.

For some perspective, FCCN’s high-street gross margin was 64% during the firm’s mid-2000s heyday.

* Small advance to store/concession sales per square foot

Another little glimmer of hope comes in the form of sales per square foot of selling space.

Including concessions as well as company-owned shops (but excluding franchisee-run outlets), I reckon H2 witnessed sales of £305 per square foot — up £10 on H2 of the previous year.

* Miserable online revenue

I was disappointed to see FCCN’s e-commerce sales down by 7% or so during H2:

| H1 2015 | H2 2015 | FY 2015 | H1 2016 | H2 2016 | FY 2016 | ||

| Retail revenue (£m) | 49.9 | 53.4 | 103.3 | 42.6 | 49.8 | 92.4 | |

| Online sales (%) | 22 | 24 | 23 | 22 | 24 | 23 | |

| Online sales (£m) | 11.2 | 12.6 | 23.8 | 9.5 | 11.8 | 21.3 |

I doubt the group’s online revenue is influenced that much by store closures, so I see these sales as a decent benchmark of the group’s underlying progress.

For the record, online sales were £22m and £23m during 2013 and 2014 respectively, so the £21m sold during 2016 really is quite poor.

At least FCCN has implemented a new computer system to help revitalise its Internet efforts.

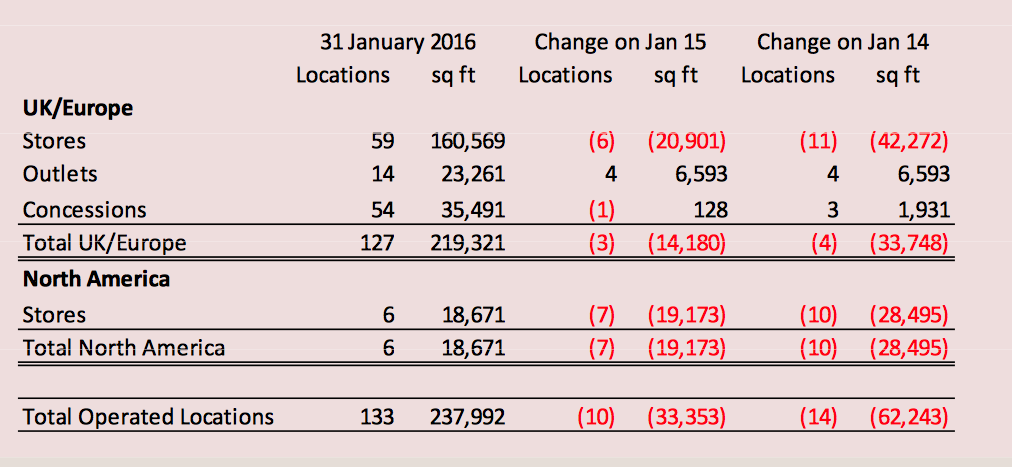

* Further store closures

I’m pleased FCCN continues to close its loss-making stores.

Some 13 shops were shut last year and a further 3 or 4 are set to go during the current year. The presentation accompanying these results summarised the shrinking high-street estate:

A quick check on FCCN’s website shows 41 stores remain open in the UK, of which nine are located in London.

I suspect the vast majority of the group’s loss-making shops are within that 41, and possibly the majority of the losses stem from the nine (presumably high-rent) stores in London.

FCCN’s Regent Street store will shut this month and I hope its closure can save a material amount of money.

(I’ve always assumed FCCN’s outlets and concessions all pay rent (or equivalent) based on a percentage of turnover, and so they should not be losing money through onerous leases.)

* Encouraging new board members

Probably the most encouraging announcement of the day concerned two new boardroom appointments.

The news is welcome because FCCN’s top management really does need some fresh blood.

Indeed, founder/boss Stephen Marks and operations director Neil Williams — as well as FCCN’s two non-execs — have all been on watch throughout the group’s awful results during the last eight years.

Certainly FCCN’s new finance director might be a useful recruit. He has worked at online fashion giant ASOS:

“Lee Williams will take up the role of Group Finance Director with effect from 4 April 2016, filling the vacant position. Lee is currently Director of Finance for ASOS Plc, the global online fashion destination, where he has been for the last 15 months.”

Furthermore, the new non-exec has a background in clothing rather than accounting/finance (although he was fired last year from Abercrombie & Fitch!):

“Christos Angelides has been appointed as an Independent Non-Executive Director of the Group with immediate effect. Christos brings significant expertise in fashion retailing, having spent the majority of his career at Next Plc in a number of senior management roles, with the last 14 years on the main board as Group Product Director.”

You never know, one day founder Stephen Marks may decide to step down and appoint a dynamic new chief exec (I wish he would). Mr Marks turns 70 in May.

* Valuation

My ‘value’ investment theory remains simple — if the £15m-plus losses at the Retail division can eventually disappear by closing a load of shops, the present valuation should look like a bargain.

Today’s figures show non-Retail profit less common costs at £10.9m, which compares to a current market cap of £41m.

For what it is worth, the immediate outlook is not a total disaster. Mr Marks claims: “The reaction to this year’s collections has been strong”.

I must admit, I have been impressed by FCCN’s recent light show — while the new Spring/Summer 2016 range has attracted some attention.

But as I have written before, FCCN shareholders have experienced no end of false dawns during the last decade — and there’s still no evidence to suggest the business has been turned around for good just yet.

Maynard Paton

Disclosure: Maynard owns shares in French Connection.

French Connection (FCCN):

Notification of Major Interest in Shares:

Forgot to mention this in the Blog post above — Will Adderley of Dunelm fame acquired a 5% FCCN stake not so long ago:

http://maynardpaton.com/2015/11/30/french-connection-wow-2-4m-compensation-for-closing-a-loss-making-store/#comment-8791

Useful that a very rich and proven retail entrepreneur has joined the shareholder register.

Maynard

French Connection (FCCN):

Notification of Major Interest in Shares:

http://www.investegate.co.uk/french-connection/fccn/tr-1–notification-of-major-interest-in-shares/201603161216383080S

Encouraging to see that Will Adderley has increased his stake. He’s added 890,161 shares to take his holding to 5,853,586 or 6.1%.

Other main outside shareholders are Liad Meidar/Gatemore (http://gatemore.com/institutions/team-member/liad-meidar), with 8.0%, and Schroders with 9.7%. Boss Stephen Marks has 41.7%.

Maynard

French Connection (FCCN)

Appointment of new directors at WA Capital:

https://beta.companieshouse.gov.uk/company/07306402/filing-history

Companies House reports Marion Sears and Darren Wright have been appointed directors at WA Capital, the investment vehicle of Will Adderley.

The appointment of Marion Sears is interesting. She is a non-exec at Dunelm and Dumelm’s website cites she has “extensive City, investor and banking experience including mergers and acquisitions.”

WA Capital essentially holds 30% of Dunelm on behalf of Will Adderley and family, a few property investments and now the FCCN stake.

Idle speculation — it is difficult to see why Mr Adderley would need the help of Marion Sears with WA Capital, unless he requires her “extensive City, investor and banking experience” to assist with acquiring further FCCN shares :-)

Maynard

French Connection (FCCN):

Notification of Major Interest in Shares:

http://www.investegate.co.uk/french-connection/fccn/holding-s–in-company/201603181218495921S/

Will Adderley of Dunelm adds a further 1,001,000 shares to 6,854,586 or 7.1% of FCCN.

Maynard

French Connection (FCCN):

WA Capital sells 7.7m Dunelm shares:

http://www.investegate.co.uk/dunelm-group-plc–dnlm-/rns/update-on-secondary-placing/201604130700080005V/

Will Adderley’s investment vehicle raises £70m. Firepower to buy more FCCN? Let’s hope so.

Maynard

French Connection (FCCN):

Notification of Major Interest in Shares:

http://www.investegate.co.uk/french-connection–fccn-/rns/holding-s–in-company/201606281128524924C/

Will Adderley of Dunelm adds a further 997,325 shares to 7,851,911 or 8.2% of FCCN.

Maynard

French Connection (FCCN)

Appointment of new non-executive:

I mentioned in the Blog post above that FCCN had appointed a new non-executive director with fashion experience — Christos Angelides.

In retrospect, I overlooked his appointment as an non-exec. Some digging shows he was Group Product Director for Next for at least 10 years until 2014, when he left for Abercrombie & Fitch.

The Guardian described Mr Angelides as the “power behind the throne” at Next when he left for A&F:

http://www.theguardian.com/business/nils-pratley-on-finance/2014/jun/10/next-christos-angelides-abercrombie-replace

Anyway, Bloomberg says he was fired from A&F in late December last year:

http://www.bloomberg.com/news/articles/2015-12-22/abercrombie-executive-angelides-is-fired-removing-ceo-contender

Mr Adderley then declares a notifiable FCCN holding in early January, and Mr Angelides then turns up as a non-exec this week. Coincidence?

I now wonder whether founder Stephen Marks is lining up Mr Angelides as the “dynamic new chief exec” I mentioned in the Blog post. That must be the case (I hope!)…

Maynard

French Connection (FCCN)

Publication of 2016 annual report:

http://www.frenchconnection.com/stormsites/fcuk/media/pdf/IR/year%20ended%2031%20January%202016.pdf

There are a few points of interest.

1) Director pay

Executive pay increased by 2% last year:

And will increase by 2% during the current year:

At least the increase is in line with that received by FCCN’s wider staff. The execs do seem to enjoy chunky wages for a business that has lost money during seven of the last eight years. I suppose their salaries are a throwback to FCCN’s heyday of 2005, when annual profit topped £30m.

2) Staff numbers

I like to keep track of FCCN’s staff productivity:

I am pleased staff numbers have dropped for at least the eighth year running, and the total payroll cost has dropped for the seventh year running.

However, payroll as a percentage of revenue has inched higher again, to 21.8% (£164.2m/£35.8m) — versus 21.2%, 20.5%, 20.8% and 19.8% for 2015, 2014, 2013 and 2012 respectively.

Also, payroll per staff member has inched higher again, to £18,090 (£35.8m/1,979) — versus £17,797, £17,228, £16,817 and £16,654 for 2015, 2014, 2013 and 2012 respectively.

Revenue per staff member has dropped to £82,791 (£164.2m/1,979) — versus £84,040 for 2015. But this ratio has fluctuated before, with £83,880, £80,728 and £84,441 being recorded for 2014, 2013 and 2012 respectively.

All in all, I guess these staff stats are not all that bad given FCCN’s poor year.

3) Lease costs

The most important part of this annual report is the disclosure on property leases. Culling stores and reducing lease costs is central to FCCN returning to profit.

Given that the store count and the associated selling space both reduced during the year, I was surprised the lease cost increased by £0.2 to £24.1m for 2016. However, rents receivable (from sub-let stores) increased by £0.7m, so I suppose the net effect was a £0.5m decrease:

The net £21.8m (£24.1m less £2.3m) lease cost compares to £22.3m, £25.1m and £27.0m for 2015, 2014 and 2013 respectively, so the downward trend remains intact.

What is notable, though, is the higher lease cost per square foot of selling space.

I calculate FCCN operated from an average of 219,242 square feet during 2016, and paying a net £21.8m lease cost gives a £99.43 cost per square foot. That compares to £87-£92 for 2012-2015.

So it appears only very low rent stores were closed during 2016, and/or some other stores have suffered notable rent increases.

Or perhaps the figures have been skewed by the rent on FCCN’s HQ increasing: http://maynardpaton.com/2015/04/24/french-connection-profit-warning-means-radical-action-is-now-required/#comment-4872

Whatever, I feel those lease stats are overshadowed by this particular accounting note:

This is a very welcome development, as it shows FCCN’s total future lease obligations dropping a significant £33.8m to £111.2m. This is the seventh year running that FCCN’s total lease obligations have reduced (they were £306.1m in 2009).

I suspect the recently closed Regent Street, London store was influential when arriving at the £111.2m figure. The store was closed two months after the 31 January balance sheet date, so the store’s future lease obligations in the 2016 accounts should amount to just two months’ payments.

Anyway, with an annual lease cost of £24.1m before rent receivables, and £111.2m of total future lease cost obligations, you could argue FCCN’s average store currently has 4.6 years (£111.2m/£24.1m) of lease payments to run.

In contrast, the same calculation for 2015, 2014, 2013 and 2012 showed 6.1, 6.0, 6.8 and 7.7 years of lease payments to run. So the store closures made during 2016, while not really impacting the P&L cost, have shortened the overall lease duration.

Indeed, the total lease obligation note above shows that FCCN has to pay at least £20.1m + £59.7m = £79.8m of lease costs during the next five years — or £16m a year. That compares to at least £19.9m and £20.3m a year based on the same calculation using the 2015 and 2014 accounts.

As such, can we look forward to an annual £4m lease payment reduction throughout the next five years? I hope so.

I reckon the bulk of the potential £4m saving saving relates to the cost of the Regent Street store. For context, the lease on the group’s Oxford Street store is reported to cost £3.2m-plus a year.

Anyway, an annual £4m lease cost reduction would have reduced FCCN’s underlying operating loss to just £0.7m for 2016 — in what was a bad year for the firm. That is something worth thinking about.

Something else worth thinking about is that the closed stores were ‘non-contributing’ and the Regent Street store was reporting ‘trading losses’, so the total saving from their closures may be greater than just the associated lease costs.

As such, perhaps FCCN is not actually that far away from break-even, assuming a half reasonable trading performance.

Finally…I wonder wether the distinct lease savings — and a potential return to break-even — helped to prompt the new (ex-ASOS) FD, the new (ex-Next) non-exec and the new major shareholder (Will Adderley) to come aboard.

There is the risk I am adding 2 and 2 and getting 5 here, but I am starting to see the Regent Street closure as a turning point for FCCN.

Maynard

Thank you for the analysis, it’s thorough and really captures bifurcated nature of this company. One thing I do suspect however is the divergence between retail and wholesaling/licencing is likely to become even more pronounced. I noted in the last AGM that you attended two years ago, Marks stated that only 15% of the retail operations were profitable with most borderline. With the chill wind that has blown over retailers in the last six months, it seems likely that new unprofitable stores have taken the place of money losing stores that have already been shutdown. I reckon that FCCN are trying to hit a moving target on the retail side, and can’t help but wonder should they be more aggressive in ramping down the retailing business. To me, it makes no sense of spending any more time devoting time, money or energy to a lousy business especially when there is so much potential in their other two businesses (i.e. licensing and wholesaling). Do you feel that this is the way the company is going, or will they try to fight what looks like a losing fight by remaining in the retail business?

Like yourself, I would have fears that the loss of a high street presence could damage the brand. However, I would argue that the business would be far better increasing brand exposure and awareness to existing third party retail channels. Perhaps deals could be done with the likes of Debenhams to feature more prominent advertising or better placement of FCUK goods? The same goes for online – why not approach a major e-tailer like Amazon – get a deal done to have the FCUK products greater prominence. A direct retail presence seems an expensive way of maintaining the brand.

Hello Tabhair,

Thanks for the comment.

With the chill wind that has blown over retailers in the last six months, it seems likely that new unprofitable stores have taken the place of money losing stores that have already been shutdown. I reckon that FCCN are trying to hit a moving target on the retail side, and can’t help but wonder should they be more aggressive in ramping down the retailing business.

Good point about the ‘moving target’. I too suspect some of the profitable stores from some years ago have become loss-makers now. The current word from the execs remains generally the same — most of the stores are close to break-even but lose a bit of money, a few lose a lot (e.g. Regent St, which was losing £0.5m), and a handful make money (mostly in smaller towns).

You then have to consider all of the associated non-store costs (presumably logistics etc) that are not charged at store level but are included in the Retail division.

The trouble here is that these associated Retail costs may not decline as quick as the overall store count, because you will still need warehouses etc even for a much smaller store base. So the theory of reducing the Retail losses to zero may not be that achievable. The Retail division made a £12m profit in 2005 when the FCUK brand peaked. Since then it has broke-even or lost money.

To me, it makes no sense of spending any more time devoting time, money or energy to a lousy business especially when there is so much potential in their other two businesses (i.e. licensing and wholesaling). Do you feel that this is the way the company is going, or will they try to fight what looks like a losing fight by remaining in the retail business?

I agree that Retail should be shut down completely and the business should re-focus on the two profitable divisions. I have made this point very clear to Mr Marks in writing. I get the feeling the board wants to keep some stores for ‘brand presence’, although they have to, given some sites are locked into long leases. Sadly none of the executives have said at the AGMs I have attended” “look, we’re going to close every store we can”.

Perhaps deals could be done with the likes of Debenhams to feature more prominent advertising or better placement of FCUK goods? The same goes for online – why not approach a major e-tailer like Amazon – get a deal done to have the FCUK products greater prominence. A direct retail presence seems an expensive way of maintaining the brand.

FCCN does have concessions in House of Fraser and I believe such space arrangements are generally agreed as a percentage of revenue. I understand that the group’s outlet stores ahem similar rent arrangements. If you look at Ted Baker, its stores are mostly small concessions, and it has been able to make such space work very well economically with the gross margins it enjoys on its particular ranges. If FCCN wishes to retain a high-street presence, then concessions and outlets, where the rent is based on a proportion of revenue, is the only the way to go.

The economics of FCCN’s retail division is just one factor here, though. The group’s underlying product has been mostly poor over the last few year (judging by LFL revenue) and ultimately you do have to look at the executive team for the blame.

Marks really ought to be hunting for a fresh and dynamic chief exec to lead a turnaround — though sadly I think Christos Angelides (the new non-exec) may be out of the group’s price bracket. Mr Angelides earned about £18m in total (salary, LTIPs, bonuses etc) at his last five full years at Next.

Maynard

(PS Good luck with your blog!)

French Connection (FCCN)

AGM attendance

I attended this morning’s FCCN AGM at the company’s offices in central London.

This was my second FCCN AGM — I attended the gig two years ago — and this meeting followed the same awkward format as before.

That is, chairman Stephen Marks goes through the motions with the ordinary resolutions, then wraps up the meeting without any questions from the floor. Although attendees can chat with the directors afterwards, it is difficult to then remember on the train home what they all said. Mr Marks did his usual disappearing trick soon after the formal meeting ended.

Anyway, this is my best recollection of what was said. I must admit I did not go fully armed with many questions to this meeting as this business has under-performed for years — and there really ought to be fresh executive blood injected to kick-start a proper recovery. On that note, I was glad the new FD and new non-exec both turned up and could answer a few questions.

From what I can gather, ordinary shareholders numbered two — just me and A N Other. Other attendees appeared to be staff, to ensure the resolutions were voted through on a show of hands, and advisors. All board members were present.

My AGM report of two years ago referred to the sartorial choice of Mr Marks, and today Mr Marks was again casually dressed. But new non-exec Christos Angelides went one better than jeans and a T-shirt — he attended the meeting in ‘double denim’. Witnessing such an AGM dress-code was a first for me — either worn by directors or investors! But I did think Mr Angelides carried his style well.

Mr Angelides was the main draw for me at this AGM, and he confirmed he is actively helping out the group. He’s spending a few afternoons every so often giving advice and suggestions on product design and other aspects of the business. He said Mr Marks had given him full rein to look at all parts of the group. I thought this ‘active’ non-exec role sounded quite promising, rather than him joining the other two non-execs on the board as a token appointment.

I commented to Mr Angelides about how his 15 years as Next’s product director would make him very useful to the board, but Mr Angelides modestly claimed his spell at Next was all in the past and made the comparison to football managers — there are always ups and downs and you can be great at one moment and not-so-great the next. So he was taking nothing for granted. I get the impression any impact he may have at FCCN won’t be felt immediately as the ranges he will be looking at now won’t be in the stores for some time. He didn’t seem too sure whether he could make a material difference to the group’s progress as a non-exec anyway — though to be fair he has been a FCCN non-exec for only two months.

In terms of his other work, Mr Angelides is also in a similar consulting role with the Lewis family, which owns River Island.

So…any chance of him becoming an exec at FCCN? He is not actively considering any full-time work at present, and is taking stock to consider what he wants to do (he left Next in 2014 to join Abercrombie & Fitch, but that appointment lasted only a year or so). Sadly I did not get the impression he was mega-desperate to join FCCN as an executive.

One welcome comment from Mr Angelides was about the value of the FCCN brand. He joined the board as he thought the brand was well-known and had a lot of value, but a lot of that value was not reflected by the level of revenue. He wanted to ‘get under the bonnet’ to see how things worked at FCCN and see if he could help close that gap.

Other snippets of info from the other directors:

* The Regent Street site was losing £0.5m a year, and was one of FCCN’s 3 big losing stores. The Oxford Street store loses money but not as much. The estate has lots of stores that lose a little money, and there are some stores that do make a profit (generally in smaller towns).

* Closing Regent Street was broadly positive given the compensation, but it was an ‘iconic’ site and a downside to closing stores is that it does reduce ‘brand presence’ and loss-making outlets can still have some ‘value’ in that regard. Doubtful whether the retail division as a whole could break-even in the near term. I did not get the impression FCCN wanted to close every store.

* FCUK revival on T-shirts was due to a general fashion trend of going back to the 90s, rather than being desperate for fashion ideas. So FCCN revived FCUK, and now the range has moved onto something else.

* New FD — joined due to greater role at FCCN. Role at ASOS was mostly corporate. Sadly I did not get the impression his experience at ASOS would transform FCCN into some online-retailer wonder business.

* All directors I spoke to were very positive about Mr Angelides.

* New ‘head of creative womenswear’ appointed last summer. Her ranges are dribbling though now and will be available fully for the upcoming Winter season. Early signs are apparently promising. Nothing given on current trading, but “last week was good”.

* The A N Other shareholder told me after the meeting that a director said that the directors generally (though I suspect the director actually meant Mr Marks) had suffered ‘psychological damage’ after the disastrous Spring 15 collection that thumped the H1 figures. I just wonder if it was that damage that finally prompted the hunt for a decent, hands-on retailer non-exec.

That’s all I can remember. I forgot to ask about Will Adderley (see Comments above). Over-riding thought after the AGM was that Mr Angelides is at least somewhat active at FCCN and that can only be a good omen.

Maynard

French Connection (FCCN)

Activist investor writes to FCCN board

Gatemore Capital Management has apparently written to the FCCN board demanding some changes. Here is an article from the Times dated 31 July 2016:

http://www.thetimes.co.uk/article/revolt-at-french-connection-39vhdckgl?shareToken=58a2fc2b2e6825e1aa86e34cde67fd03

———————————————————————————————————————————-

Revolt at French Connection

An activist investor is attempting to shake up French Connection, calling on the struggling fashion retailer to ditch its famous FCUK logo, writes Oliver Shah.

Gatemore Capital Management, an American fund, has built an 8% stake in the listed company. It wrote to the board last week criticising French Connection’s “disappointing” performance since the 2008 crisis — a period in which its share price has dropped from more than 100p to 40p. The fund urged founder Stephen Marks, 70, to split his roles as chairman and chief executive, and called for the replacement of non-executive directors Dean Murray and Claire Kent, who it said would “soon be losing their status as independent” after nearly nine years on the board.

Gatemore said that French Connection had fallen behind rivals such as Ted Baker and SuperGroup. It called on the company to boost profit margins, reduce the size of product ranges, speed up the closure of loss-making stores — and ditch the FCUK logo because it is no longer “aspirational”. French Connection agreed that performance needed to improve but said it disputed many of Gatemore’s “assertions”.

———————————————————————————————————————————-

I am surprised it has taken Gatemore this long to write to the board. Gatemore is run by Liad Meidar, who first disclosed a 3%-plus holding back in November 2013.

I wrote to FCCN chairman Stephen Marks during April 2015 and made many of the same points as Gatemore. I suggested to Mr Marks that he: i) step down to become a non-executive, and; ii) appoint a new and incentivised chief executive to transform the business into a pure licensing and wholesale business.

Gatemore’s reference to the non-execs does not go far enough really. Dean Murray and Claire Kent have both sat as non-execs since 2008 and overseen FCCN’s embarrassing performance. Neither non-exec has any hands-on fashion background and I can only assume their appointments are token gestures to appease the corporate governance box-tickers.

Anyway, it is useful that Gatemore has gone public as a dissident shareholder. Let’s hope Will Adderley via WA Capital also demands a board shake-up.

In other FCCN news, I see non-exec Christos Angelides picked up 100,000 shares last week at an 36.25p average:

http://www.investegate.co.uk/french-connection–fccn-/rns/director-pdmr-shareholding/201607251300581387F/

http://www.investegate.co.uk/french-connection–fccn-/rns/director-pdmr-shareholding/201607271131013945F/

http://www.investegate.co.uk/french-connection–fccn-/rns/director-pdmr-shareholding/201607281056205207F/

Sure, Mr Angelides collected £18.5m in pay, bonuses, LTIPs, pension contributions etc during his last five full years as a director of Next. As such, £36k spent on FCCN shares is peanuts to him. But Mr Angelides does have vast hands-on fashion experience, the purchase came just before FCCN’s year-end, and he is the first FCCN non-exec in decades (maybe even ever) to hold any shares. So there are some straws to clutch there.

Maynard

French Connection (FCCN)

Activist investor requests FCCN meeting

Further developments with FCCN and Gatemore via The Guardian:

https://www.theguardian.com/fashion/2016/sep/18/french-connection-stephen-marks-refuses-discuss-turnaround-plan-fashion-retail?

—————————————————————————————————————

Stephen Marks is refusing to sit down with an activist investor that wants him to surrender his dual role as chairman and chief executive of the struggling fashion chain French Connection.

The retailer will update the City on first-half trading on Tuesday and Gatemore Capital Management, the US hedge fund that has built an 8% stake, is seeking a meeting with the full board to discuss ideas to improve its financial performance that were set out in a letter to the company in July.

Liad Meidar, a Gatemore managing partner, said it wanted the audience to discuss a turnaround plan under which the long-serving non-executive directors Dean Murray and Claire Kent would be replaced.

The pair have been on the board since 2008 so will soon lose their status as “independent” under the UK corporate governance code. Gatemore also wants the retailer to accelerate plans to shut unprofitable stores and to “move on” from using its well-known FCUK label.

“He [Marks] is not really willing to have an open conversation about why French Connection is underperforming,” said Meidar, who added that a wider shareholder base was unifying around its ideas. “You have a 41% shareholder who is running this business at his leisure, not for for the benefit of all shareholders.”

French Connection confirmed that Marks, who founded the business in 1972, would not be meeting any shareholders as part of the interim results roadshow, with briefings to be handled by other members of its executive team, which includes the new finance director, Lee Williams, who joined from its online rival Asos.

French Connection, which also owns the brands Toast and Great Plains, made a £3.5m loss in 2015. The shares are changing hands for 40.75p, giving the retailer a market capitalisation of £40m.

Marks has mapped out a plan for a return to the brand’s previous glories that involves shutting unprofitable stores and improving its ranges. The company has also enlisted the highly regarded fashion executive Christos Angelides, who has worked with Next and Abercrombie & Fitch, as an independent non-executive director. At its full-year results in March, Marks insisted the business was moving in the right direction.

Its recent collections have been well received by the fashion press, but any progress is against a backdrop of tough trading, with Next and John Lewis both reporting a fall in first-half profits last week.

—————————————————————————————————————

Encouraging to see further noises emanating from Gatemore. Clearly nobody from the activist group has ever attended the AGM, as if they had they would know Mr Marks does not engage with shareholders direct — he leaves all that to his fellow execs.

I think this line from Gatemore sums up the situation well:

“You have a 41% shareholder who is running this business at his leisure, not for for the benefit of all shareholders.”

Interim results tomorrow — they are usually awful. Let’s hope Christos has spent a few afternoons with the design group and his impact is starting to be felt.

Maynard