10 November 2015

By Maynard Paton

Quick update on Mincon (MCON).

Event: Q3 trading update published 10 November

Summary: A very pleasant statement from this drill manufacturer, which confirmed earlier trading improvements had been sustained. Indeed, revenue, profit and — very importantly — cash flow, all advanced to seemingly defy the mining-sector downturn. I just wonder if the recent appointment of Joe Purcell, son of the group’s founder, as chief exec has had an immediate impact. Profit extrapolations are now showing an interesting valuation and I continue to hold.

Price: 55p

Shares in issue: 210,541,102

Market capitalisation: £116m

Click here for all my previous MCON posts

Statement:

My thoughts:

* Improved trading has continued through the year

August’s interim results had already shown Q2 improving on Q1, and I was pleased to see Q3 recording further progress.

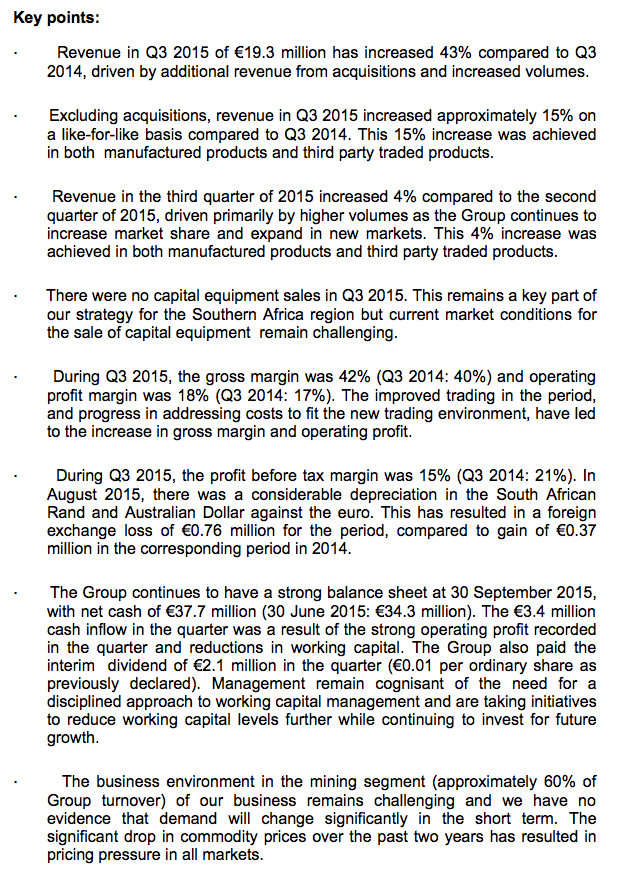

Underlying revenue gained 15% on last year to €19.3m, with operating margins rising from 17% to 18%. I therefore calculate Q3 operating profit — aided possibly by recent acquisitions — gained 51% on 2014 to €3.5m.

MCON confirmed its greater revenue had been driven “primarily by higher volumes as the Group continues to increase market share and expand in new markets”. Meanwhile, the profit improvement was achieved in part by “addressing costs to fit the new trading environment”.

All told, it was a very encouraging performance — especially as 60% of group revenue was earned from manufacturing drills and bits for the battered mining sector.

* Q1 versus Q2 versus Q3, and 2014 versus 2015

Today’s statement and earlier updates have allowed me to construct the following tables (some figures are estimated):

| Q1 2015 | Q2 2015 | Q3 2015 | |

| Revenue (€k) | 14,112 | 18,628 | 19,300 |

| Gross margin | 38% | 43% | 42% |

| Gross profit (€k) | 5,363 | 8,010 | 8,106 |

| Operating margin (%) | - | - | 18% |

| Operating profit (€k) | - | - | 3,474 |

| Pre-tax margin (%) | 12% | 15% | 15% |

| Pre-tax profit (€k) | 1,693 | 2,794 | 2.895 |

| Q1 2014 | Q2 2014 | Q3 2014 | Q4 2014 | |

| Revenue (€k) | 10,080 | 13,332 | 13,497 | 17,635 |

| Gross margin | 50% | 45% | 40% | 40% |

| Gross profit (€k) | 5,040 | 6,001 | 5,399 | 7,112 |

| Operating margin (%) | - | - | 17% | - |

| Operating profit (€k) | - | - | 2,294 | - |

| Pre-tax margin (%) | 22% | 14% | 21% | 17% |

| Pre-tax profit (€k) | 2,218 | 3,240 | 2,834 | 2,957 |

Today’s update saw MCON disclose its quarterly operating margin for the first time — the reason being because the firm had suffered a notable foreign-exchange loss during August:

“During Q3 2015, the profit before tax margin was 15% (Q3 2014: 21%). In August 2015, there was a considerable depreciation in the South African Rand and Australian Dollar against the euro. This has resulted in a foreign exchange loss of €0.76 million for the period, compared to gain of €0.37 million in the corresponding period in 2014.”

The cost of such foreign-exchange movements are accounted for within the financing section of MCON’s income statement, which explains why the Q3 pre-tax margin fell from 21% to 15% on the year.

Anyway, I have to say operating margins at 18% look superb for a business where a substantial part of trading “remains challenging” and has resulted in “pricing pressure in all markets”.

* Better cash flow and working capital

A clear positive from today’s statement was the commentary on cash flow:

“The Group continues to have a strong balance sheet at 30 September 2015, with net cash of €37.7 million (30 June 2015: €34.3 million). The €3.4 million cash inflow in the quarter was a result of the strong operating profit recorded in the quarter and reductions in working capital. The Group also paid the interim dividend of €2.1 million in the quarter (€0.01 per ordinary share as previously declared). “

I had previously cited MCON’s wayward cash generation as one of the drawbacks to its business. However, it appears the managers have now started to reverse what had been a poor trend.

Adjusting for the dividend, some €5.5m of cash was produced during Q3 — versus my earnings guess of €2.7m. Most of the difference ought to be a favourable working-capital movement, which will help offset the quite unfavourable movement witnessed during the first half.

* Is the acquisition strategy starting to bear fruit?

The cash production meant MCON’s bank balance now stands at €37.7m, or roughly 13p per share.

As far as I can tell, this cash pile all remains earmarked for acquisitions and MCON says it is “continuing discussions with a number of potential acquisition partners with a view to extending the Group’s product range and adding new customers and new geographic markets”.

During the 18 months to June 2015, the group spent €10m on purchasing smaller subsidiaries and I wrote back in August that there were “still no obvious signs that the corporate activity has enhanced returns for shareholders”.

However, after this encouraging statement, I now wonder whether the financial benefits of the acquisition strategy are beginning to peep through.

Valuation

Assuming Q4 can replicate Q3, I calculate underlying operating profit for 2015 could come in at €11.8m, which converts to £8.3m at £1:€1.41.

Taxed at the 21% applied during the first half, current-year earnings could then be £6.6m or roughly 3.1p per share.

Subtracting the €37.7m (£26.7m) net cash position from the £116m market cap, my estimate of MCON’s enterprise value is £89m or 42p per share.

Then dividing that 42p per share by my 3.1p per share EPS guess gives a multiple of around 13-14 at the present 55p offer price.

Alternatively, assuming the Q3 performance can be sustained for the next twelve months, then my earnings guess comes to 3.7p per share and the underlying P/E would be around 11-12.

Were further profit improvements to actually occur, that latter rating would not look too excessive.

* Next update — final results in March 2016.

Maynard Paton

Disclosure: Maynard owns shares in Mincon.