09 September 2015

By Maynard Paton

Quick update on M Winkworth (WINK).

Event: Interim results published 8 September

Summary: A somewhat lacklustre set of results, blamed on a nervous pre-election housing market and extra costs associated with a corporate-relocation department. While the potential of additional lettings income looks promising, cash generation remains disappointing. I still like the simplicity of this franchising business, but must admit to having doubts about the size of its full potential. I continue to hold.

Price: 143p

Shares in issue: 12,676,238

Market capitalisation: £18.1m

Click here to read previous WINK posts

Results:

My thoughts:

* These results lacked financial commentary

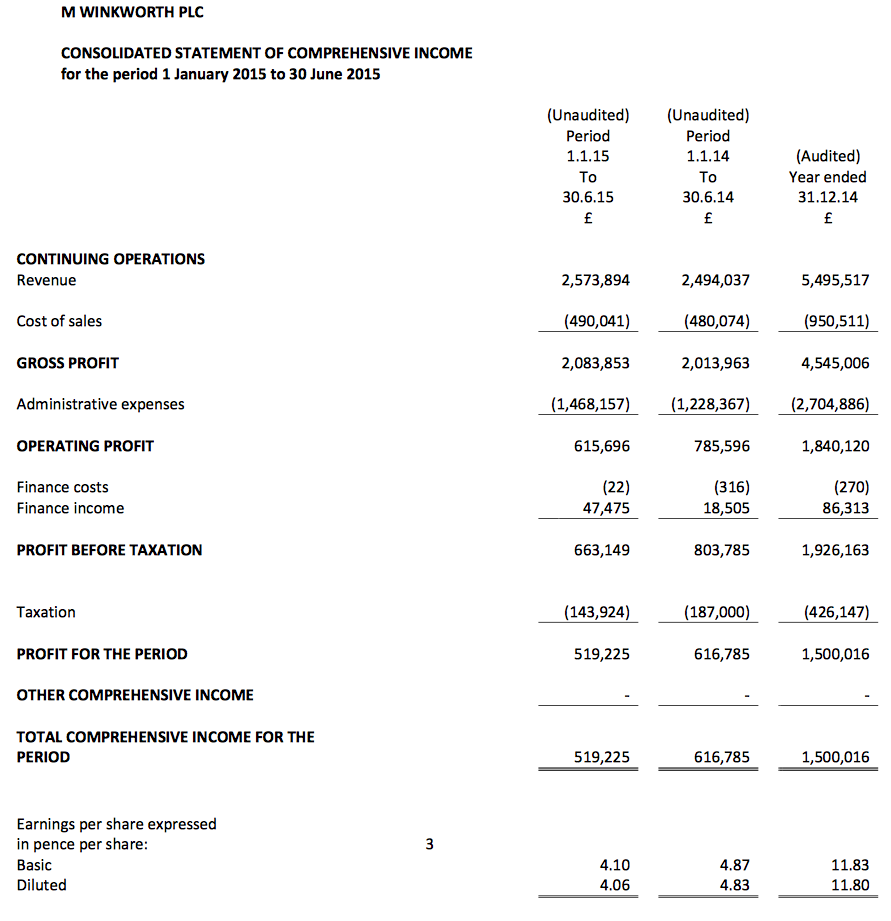

I was struck by the lack of financial commentary within this statement. In a 1,300-word report, only the following related to the accounts:

“During an uneven first half, Winkworth’s revenues rose by 3.2% to £2.57 million (2014: £2.49m), Profit before taxation was down 17% to £663,149 (2014: £803,785), cash generated was down 34% to £290,240 (2014: £436,582) and dividends of 3.3p were declared and paid (2014: 2.9p).”

The rest of the statement explained how the property market had become subdued before the election, why activity may now pick up, and (albeit briefly) why profits had fallen short of last year.

All told, it was not the most informative of updates.

* The performance was comparable to that of Foxtons

On the face of it, WINK’s results were not spectacular. Revenue edged 3% higher while operating profits dived 22%. The shortfall was blamed on costs associated with establishing a corporate-relocation department and “retreating from poor locations”.

Still, the performance was comparable to that of Foxtons (FOXT), which also suffered from pre-election jitters. In July, this London estate-agency rival reported first-half revenue sliding 2% and operating profits also diving 22%.

WINK noted its lettings-related revenue had improved by 7% to now represent 38% of its gross franchisee income. My sums indicate gross franchisee income relating to property sales fell 11% — although this was not confirmed in the results. For what it is worth, FOXT’s first half also witnessed income from property sales drop 11%.

* Letting income still ‘well set’ for 50% of revenue

I was pleased WINK re-confirmed that “rentals are well set to reach our medium-term goal to represent 50% of total revenue”.

As before, I trust this goal will be achieved by rental income growing rather than property-sale income contracting! WINK reckons the aforementioned corporate-relocation service could provide a useful boost to its rental activities, which I feel provide a more dependable source of income than traditional sales commissions.

Anyway, I believe rental income growing to 50% of gross franchisee income could mean WINK’s own revenue may increase by £1.5m — and perhaps add a further £0.5m to profits. These numbers are not insignificant when compared to current revenue of £5.6m and profits of £1.7m.

* Cash flow continues to support franchisees

My previous posts on WINK have applauded the group’s high margins and its high equity returns — both 20%-plus during this first half despite the extra costs.

But cash flow remains disappointing. You see, WINK has lent significant sums to its franchisees, with £1m outstanding at the end of 2014 and a further £150k or so lent during the latest six months.

Such loans, and the general tardiness of the franchisees to pay their fees to WINK (see point 2 in this comment), meant the vast majority of operating profit for this first half was absorbed into working capital.

In fact, the cash movements left WINK’s cash pile some £0.4m lighter at £2.1m.

Overall, the cash flow situation is not great and I’m hopeful the next year or two will see i) some of the earlier franchisee loans paid back, and; ii) fees owed to WINK paid more promptly.

At least WINK was confident enough to lift its first-half payout by 6.6% to 3.2p per share.

Valuation

* Trailing operating profits now stand at £1.7m and, taxed at a standard 20%, would produce earnings of £1.3m or 10.5p per share.

* Subtract the group’s £2.1m net cash position from the current £18.1m market cap (at 143p), and I get an enterprise value of £16.0m or 126p per share.

* Then divide that 126p by my 10.5p earnings estimate and I arrive at a P/E of 12. Not an obvious bargain given 2015 profits are likely to be down on last year, though management is optimistic of a “resumption of growth” for 2016. The trailing 6.4p per share dividend supplies a 4.5% yield.

Next events: Q3 dividend announcement early November, possible trading statement early December.

Maynard Paton

Disclosure: Maynard owns shares in M Winkworth.

WINK:

Broker note published (paid-for by WINK):

http://www.edisoninvestmentresearch.com/research/report/m-winkworth4

Contains a few extra stats on how WINK’s central London, non-central London and country offices performed during the six months.

But there was nothing on the amount spent on the new departments that depressed profits.

However, the note did include this text (my bold):

“Building corporate services: the centralised company relocation service, which directs leads to the franchises, was strong in H115. Since launch in March 2015, the corporate rentals department has generated revenue for Winkworth of £14k (run rate well ahead of the 2015 target of £30k), working for diverse clients ranging from Unilever, through Facebook and the US Embassy, in addition to international financial services companies.

– Building a brand and services with an international focus: both inbound (eg the China desk has been strong), but also outbound (eg UK buyers of properties in France, Spain, Italy and Portugal). The centralised client services department has referred 671 applicants to franchisees and generated 560 appraisals, leading to 125 instructions. The latter would generate £955k in front office fees if all completed (£76k for Winkworth).”

Crikey — these new departments are certainly small right now in terms of revenue for WINK.

Maynard

M Winkworth (WINK)

Trading Update and Market Outlook:

http://www.investegate.co.uk/m-winkworth-plc–wink-/rns/trading-statement-and-market-outlook/201511110700062260F/

Summary

Despite the unexpectedly clear-cut election outcome in May, the anticipated bounce in the housing market has not materialised in 2015, with the sales market being particularly slow in prime central London. We believe that while concerns around the General Election limited transactions, particularly at the upper end of the market, a large part of the slowdown can be attributed to the stamp duty changes introduced in the latter part of 2014, which saw a significant rise in the tax for properties above £900,000. Transactions below this threshold have been more buoyant, particularly as interest rates have remained low and mortgage lending has increased.

The Board of the Company expects full year revenues for 2015 to be in line with 2014. Costs associated to investment in new projects will be higher than anticipated as our Client Services Department in particular, set up to generate new sales opportunities for franchisees, has taken longer than estimated to reach breakeven. As a consequence, it is expected that profits for 2015 will be slightly below market expectations. Our dividend is well covered, and with no debt and solid cash-flow we expect to be able to maintain our progressive pay-out policy.

This will still be the second best ever year for Winkworth, despite transactions still being 26% off their historic peak. We are particularly pleased with the continued growth of our rentals business, with lettings in 2015 achieving double the revenues generated in 2006. We continue to focus our efforts on promoting and running a single, well-respected brand and adding maximum value to our existing franchisees while also looking to attract high quality professionals that may be looking to leave prime agencies and seek new opportunities. We are improving the mix of our business and have this year re-sold eight offices to introduce new, higher-quality franchisees who we believe will help drive growth in both income per office and market share.

Market Outlook

Market conditions moving into 2016 are likely to be similar, with stamp duty undermining demand for more expensive properties but low mortgage rates and wage inflation adding momentum at the lower end of the market. As a result of this cautious outlook for the industry we believe that there will be opportunities for us to attract new talent to the Winkworth brand. We are experiencing a pick-up in new franchising inquiries and have three offices scheduled to open in the early part of next year, with more under discussion.

The private rental sector now represents 30% of the London property market and we expect rentals to continue to grow in importance, with a shortage of supply underpinning prices. We anticipate steady growth of 3-4% in the price of Greater London rentals, slightly above wage inflation, and growth in our own business at around double this rate as our investment in lettings starts to come to fruition.

With the initiatives taken to maximise revenue-generating opportunities, further organic growth and tight control of costs we look forward to 2016 with confidence.

I perhaps should have predicted this update coming.

I’d already seen rival estate agents Foxtons and Countrywide issue lacklustre statements of late, and to be honest, I suppose the news from WINK could have been worse.

To summarise, WINK blamed i) a slower-than-expected housing market, and; ii) additional costs relating to a new department for the current-year’s “slight” profit shortfall.

Anyway, broker Edison Research had previously forecast revenue of £5,715k and an operating profit of £1,657k for 2015.

Now it seems as if revenue will match last year’s £5,496k and perhaps operating profit could now come in at, say, £100k less (or 6%) at £1,557k.

Such an outcome would broadly match WINK’s 2013 performance and, as the firm said in today’s update, “still be the second best-ever year” for the group.

Elsewhere in the statement, I was pleased WINK did not reveal any loss of momentum on the lettings side of the business.

WINK predicts rent prices in Greater London growing by 3-4%, but anticipates its own lettings income expanding at around double that rate as new investments pay off.

Growth of 6-8% would match the 7% lettings improvement reported within September’s interims -— and the 7-8% compound rate the group has enjoyed since 2006.

Lettings provide a more predicable income than traditional property sales commissions, and I dare say WINK’s goal remains to ensure rents advance from 38% to 50% of total revenue in the medium term.

Valuation

* If operating profit were to come in at £1,557k, earnings would be £1,246k or 9.8p per share after 20% standard tax.

* Subtract the group’s £2.1m net cash position from the current £19.6m market cap (at 155p), and I get an enterprise value (EV) of £17.5m or 138p per share.

* Then divide that 138p by the 9.8p earnings estimate and I arrive at a P/E of 14. Not an obvious bargain given 2015 profits are likely to be down somewhat on last year.

* Include £1m of loans lent to franchisees as part of the cash pile, the EV then drops to 130p per share and the P/E falls to 13.

* The trailing 6.5p per share dividend supplies a 4.2% yield and WINK expects to maintain its progressive dividend policy.

Maynard

M Winkworth (WINK)

I mentioned in the Blog post above:

Something I have since realised is that WINK does collect a reasonable rate of interest from these loans.

For full-year 2014, interest received came to £86k. Cash in the bank averaged about £2.6m during the year, so the effective interest rate was 3.3%. That seems very high with today’s base rate at 0.5%.

Instead, assume 1% from the bank gives bank interest of £26k and leaves about £60k to be earned from the loans to franchisees. Those loans averaged £695k during 2014, so implying they earned an 8.6% rate of interest. Not bad.

For the first half of 2015, total interest received was £47k. Average cash during the six months was £2.3m, so an effective interest rate of 4.0%. Again, looks high in light of 0.5% base rates.

Assume 1% from the bank again, and I arrive at £12k bank interest and therefore £35k interest from franchisee loans. Such loans topped £1m during the six months, so would imply they earned a 6-7% interest rate. Again, not too bad.

So I suppose these loans aren’t all bad — assuming they are paid back of course. I now feel I should always include these loans alongside cash in my valuation sums. That said, it would be much better generally if WINK did not have to lend its money to ensure its franchisees could start trading.

(EDIT: 18 Nov 2015: Just to add to this subject, Belvoir Lettings (BLV) has issued this statement:

http://www.investegate.co.uk/belvoir-lettings-plc–blv-/rns/acquisitions-in-southampton-and-brighton-and-hove/201511180700040607G/

BLV has lent out loans totalling £118,500 to two of its franchisees and expects to receive interest of £10k per annum for the three-year term. That equates to an interest rate of 8.4%. Not bad. Also, these loans should help these two franchisees receive an extra £250k of revenue, of which almost £30k will be paid as annual fees to BLV. So that extra £30k does not appear to be a bad return either.)

Maynard

M Winkworth (WINK)

Dividend Declaration:

http://www.investegate.co.uk/m-winkworth-plc–wink-/rns/dividend-declaration/201512160700071654J/

“M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce a special dividend for the year ending 31 December 2015 of 1.8p as per the timetable below.

Winkworth has paid a dividend of 1.6p for each of the first three quarters of 2015 and the special dividend payment will increase the total paid relating to the financial year to date to 6.6p.The dividend relating to the fourth quarter will be announced in February.

Winkworth continues to be cash generative and has a healthy balance sheet. This payment is consistent with the Company’s intention of maintaining a progressive dividend policy.”

A 1.8p per share special dividend. Nice.

This payment underlines how keen WINK is to pay out excess cash to shareholders.

The firm already pays its dividends quarterly while the trailing twelve-month payout of 6.5p per share is already a fair chunk of earnings, which I believe currently run at close to 10p per share.

At the last count, net cash was £2.1m or 17p per share, so this 1.8p special payment will hardly break the bank. Nonetheless, it is an encouraging signal — I’s like to think WINK would not declare a special payout if it was experiencing difficult trading conditions.

Maynard

M Winkworth (WINK)

Company publication of 2015 London housing statistics:

Following up the 11 November trading update (see above comment), WINK has published this report on the prime central London property market:

https://gallery.mailchimp.com/021021e0297f8702239bca5c7/files/2016_01_Winkworth_PCL_8pp_January_WEB.pdf

General gist is that transaction levels last year were c20% down on last year with prices down c5%. The only immediate bright spot is that April’s stamp-duty changes may prompt a rush of transactions during the first quarter of 2016.

Maynard

M Winkworth (WINK)

New Office Openings:

http://www.investegate.co.uk/m-winkworth-plc–wink-/rns/new-office-openings/201602040700069636N/

“M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is pleased to announce a positive start to 2016 and the opening of three new offices with a further four under negotiation.

As part of its policy of both building and strengthening its portfolio, new offices are being opened in Colindale, Potters Bar and Milford-on-Sea. Two new Winkworth offices were opened and eight franchises were resold to new agents in 2015. With the addition of the new openings in 2016, the Company will have over 100 offices by the end of the first quarter, predominantly in the London area and the South-East of England.

Dominic Agace, CEO of Winkworth, commented: “In the fourth quarter we saw a doubling of new franchise enquiries over the previous period and we have entered 2016 with a strong start across our whole network. Our lettings business continues to make excellent progress and, with record low interest rates and wage inflation returning, there are signs that the sales market remains well underpinned.””

Few points on this statement:

* Reaching the 100-office milestone has beens slow. When WINK floated in late 2009, the firm operated from 86 offices. The above statement refers to resold franchises and I understand WINK can resell under-perfoming branches to new franchisees. Hopefully that is the case here, rather than savvy franchisees selling up because of difficult market conditions ahead.

* I had to look on a map to discover Colindale is in North London and Milford-on-Sea is on the south coast in Hampshire.

* The chief exec’s comments seem relatively promising. Having read WINK’s stats on 2015 (see comment above), I guess the firm’s sales are also being “well underpinned” by house-purchases aiming to beat April’s stamp-duty increase for second homes.

* The chief exec’s comments appear to tally with the remarks from rival London agency Foxtons.

http://www.investegate.co.uk/foxtons-group-plc–foxt-/rns/trading-statement/201602030700078657N/

“The Group achieved a solid performance during 2015 with revenue growth across all business segments. Group turnover was up 4% to £150m, despite latest available data showing London property sales transaction levels being some 11% below prior year…”

“Although it is too early to predict residential property sales transaction trends for 2016 the Company enters 2016 with an encouraging sales pipeline, a strong lettings book and a proven strategy for further growth through organic branch expansion.”

My earlier research has shown FOXT and WINK to have reported very similar sales and lettings progress, so I’m hopeful this FOXT update will be positive for WINK. It is also interesting to see FOXT declare a special dividend within its latest statement — WINK declared a special dividend just before the end of last year.

Maynard

M Winkworth (WINK)

Dividend declaration:

http://www.investegate.co.uk/m-winkworth-plc–wink-/rns/dividend-declaration/201602100700085362O/

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.7p per share for the fourth quarter of 2015. Including this and the special dividend of 1.8p announced on 15 December 2015, the total dividend paid to shareholders for the financial year ended 31 December 2015 will be 8.3p per share. The timetable is as follows:

Ex-Dividend Date * 18/02/16

Record Date ** 19/02/16

Expected Payment Date 17/03/16

—————————————

Q4 dividend of 1.7p. Gives a full-year ordinary dividend of 6.5p, which is 0.3p or 5% higher than 2014. Trailing yield at 130p is now 5% exactly. Not bad.

Maynard

M Winkworth (WINK)

Chief exec interview:

http://www.ibtimes.co.uk/winkworth-ceo-booming-china-will-power-prime-central-london-property-demand-1543263

Naturally he’s upbeat on London property. But has he slipped in some good news? (my bold)

“While Agace said he thinks 2016 will be “patchy” for prime property, Winkworth’s start to the year has been “better than expected”.

“We expect it to outperform what we initially said, but it’s early days,” he claimed. “I think central London is coming to a point where it will have absorbed the stamp duty. I don’t think it’s quite there yet. I expect that to happen hopefully through the course of this year and the signs are it’s started better than expected. Interestingly, our South Kensington office, that I was in contact with the other day, say they have had their best January start in three years. And that’s in the £1m-£2m ($1.4m-$2.8m, €1.2m-€2.5m) flat market, so the lower end of prime central London.”

Hopefully the “better than expected” trading can continue once the new stamp-duty rates come into force in April. Promising, nevertheless.

Maynard