Apologies! This BVXP H1 2025 review has taken somewhat longer than expected to produce. BVXP’s FY 2025 results are due tomorrow (27 October) and to avoid any reader confusion in the morning, an email alert has not been sent.

26 October 2025

By Maynard Paton

H1 2025 results summary for Bioventix (BVXP):

- A very unspectacular six months, showing revenue up only 1% to reflect what the company maintains are “mature” markets for diagnostic antibodies. Profit meanwhile fell 4% following greater external spend on R&D.

- With neither the secondary application for troponin nor the biomonitoring projects attracting much commercial interest, future growth now seems dependent entirely on the Alzheimer’s R&D — revenue from which “increased” during this H1.

- “Large-scale” antibody manufacturing, further promising scientific papers, a royalty arrangement with a prominent researcher alongside a possible supply agreement with Beckman Coulter suggests the Alzheimer’s work has increasing potential to one day become a substantial commercial success.

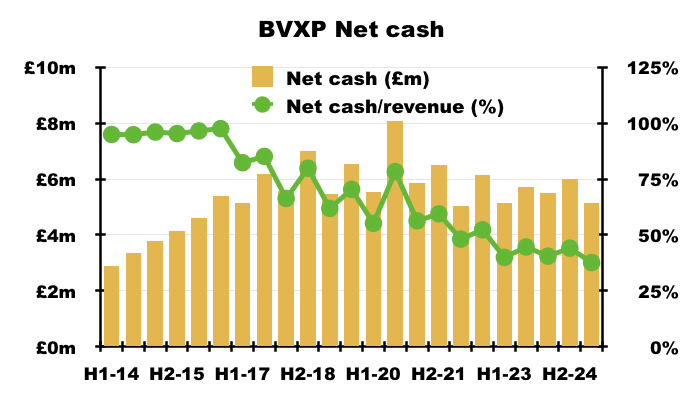

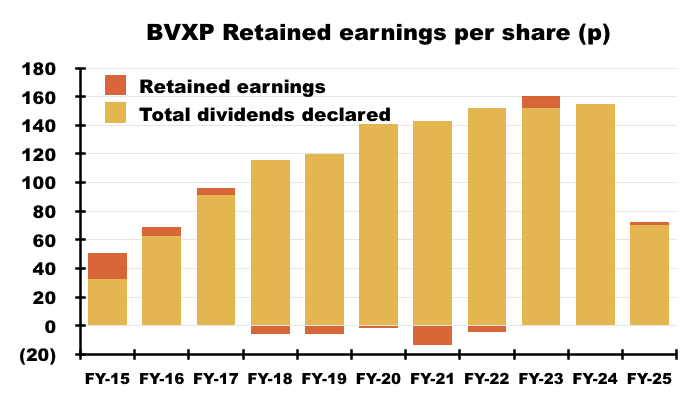

- Although the H1 dividend was (surprisingly) lifted 2p per share, FY 2025 earnings are forecast to decline slightly and leave dividend cover below 1x. The £5m cash position therefore looks primed to fund the greater R&D.

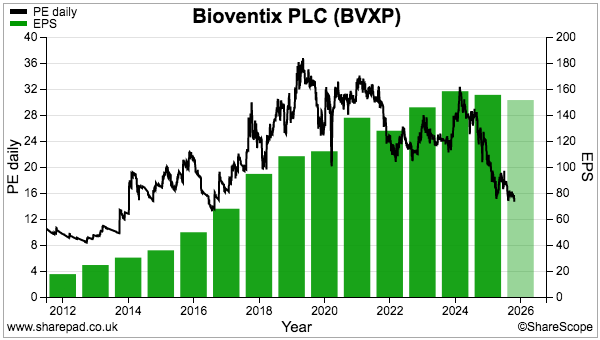

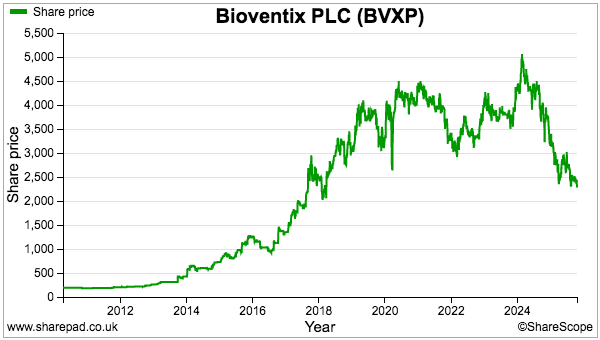

- The lack of near-term profit growth has left the £24 shares trading at a level first achieved during 2017 and offering their highest-ever yield at 6%-plus. They may also value the Alzheimer’s R&D at a very pessimistic zero. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Royalty income and physical sales

- Vitamin D

- Troponin and other antibodies

- Alzheimer’s R&D: revenue

- Alzheimer’s R&D: Alzheimer’s treatments

- Alzheimer’s R&D: neurodegeneration and brain-derived tau

- Alzheimer’s R&D: royalties paid to researchers

- Alzheimer’s R&D: amyloid plaques and p-tau

- Alzheimer’s R&D: tau tangles

- Other R&D

- Financials: margin and employees

- Financials: balance sheet and cash flow

- Boardroom

- Valuation

News links, share data and disclosure

- Interim results and presentation for the six months to 31 December 2024 published 31 March 2025.

- Share price: £24

- Share count: 5,224,860

- Market capitalisation: £125m

- Disclosure: Maynard owns shares in Bioventix. This blog post contains ShareScope affiliate links.

Why I own BVXP

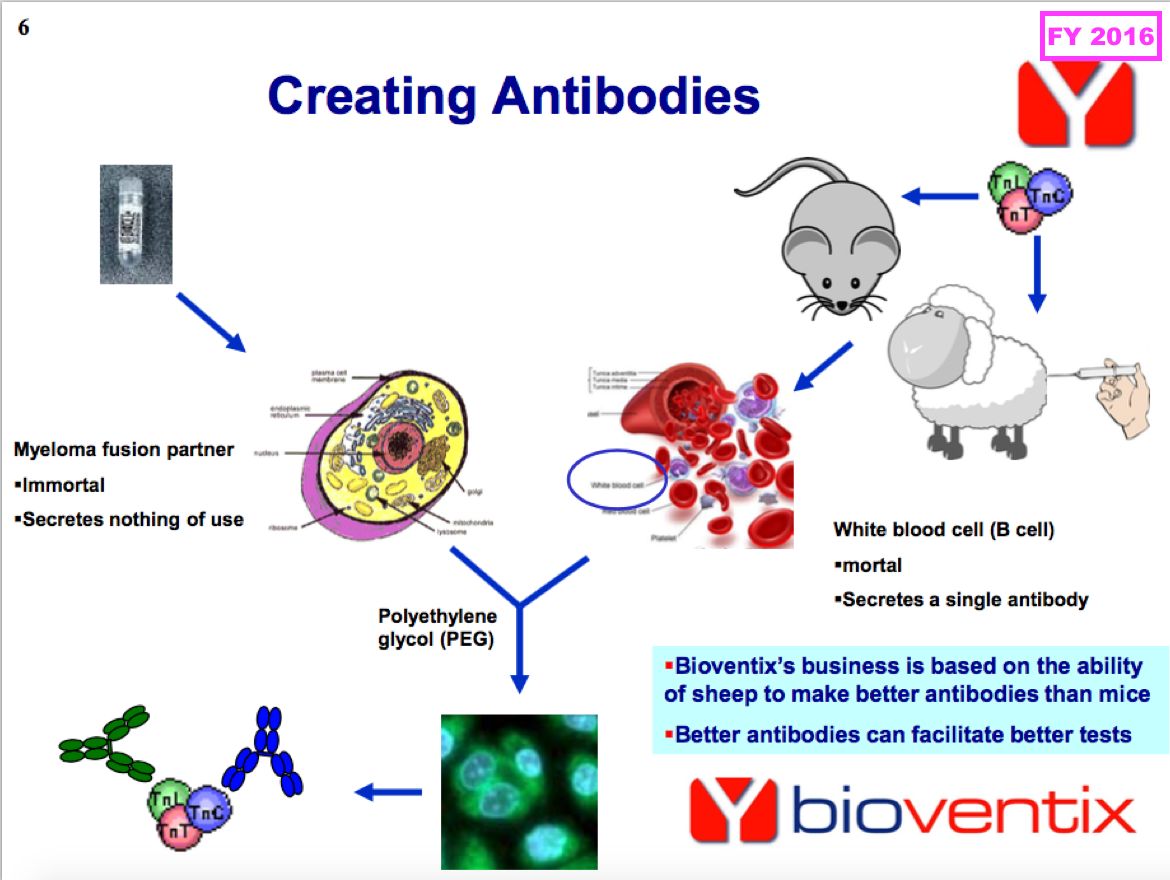

- Develops diagnostic blood-test antibodies, substitution for which can be limited due to protracted regulatory testing that in turn can lead to revenue continuity for a decade or two.

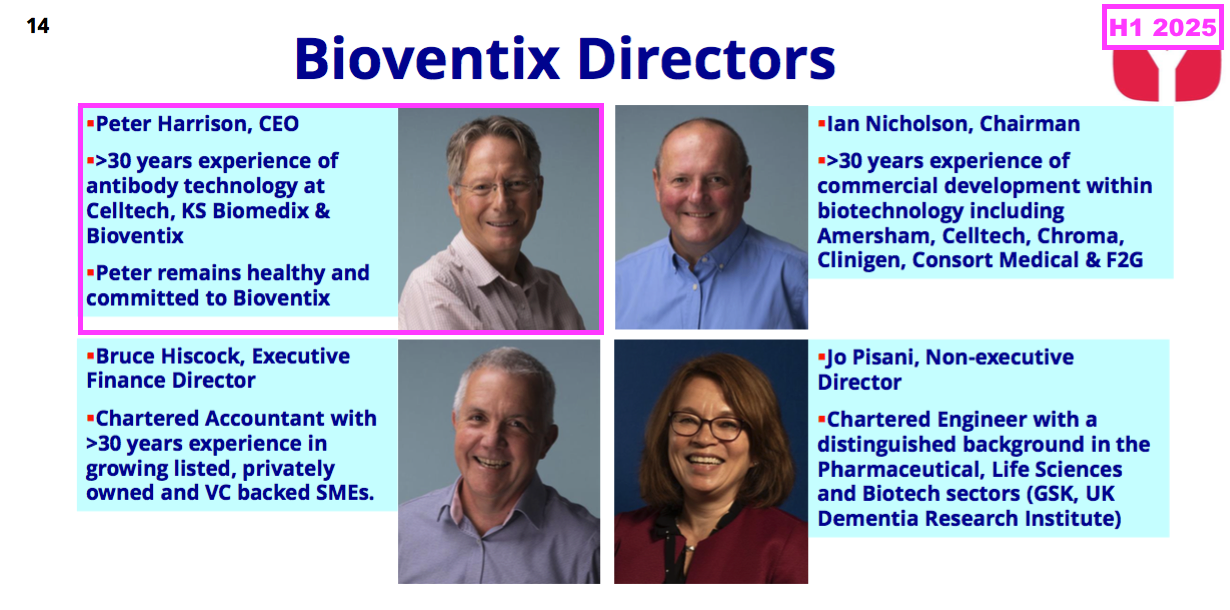

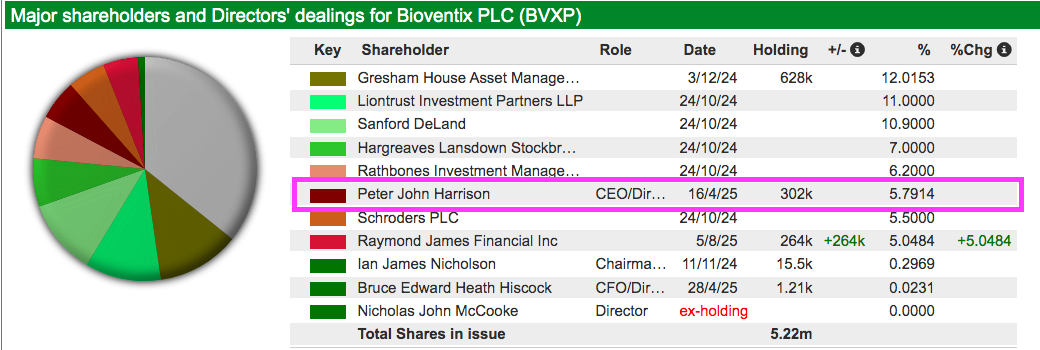

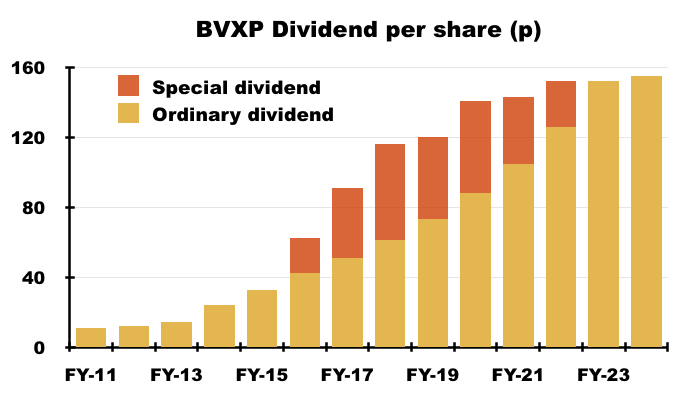

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, prefers a cash-rich balance sheet, retains a 6%/£7m shareholding and has declared seven special dividends.

- Employs ‘scalable’ royalty model that requires few employees and leads to terrific margins, generous cash flow and immense returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit and dividend

- The preceding FY was below BVXP’s expectations, and the accompanying outlook commentary mentioning “steady growth” and “mature diagnostic markets”…

[FY 2024] “We are pleased with our financial results for the year, which we believe reflect steady growth in the use of our established products in more mature diagnostic markets. We remain very encouraged by the very early signs of success for our Tau/Alzheimer’s antibodies and we look forward to more progress into the future.”

- …did not suggest this H1 would suddenly deliver a spectacular performance.

- The preceding FY falling below expectations was due partly to a “customer error in the incorrect application of a historic royalty percentage“, which led BVXP to admit royalties from its troponin antibody had been “overreported and overpaid” since FY 2022 (see Troponin and other antibodies).

- To correct the accounts for the error, the £327k of “overreported and overpaid” troponin sales previously recognised during FYs 2022 and 2023 was subtracted from the preceding FY’s revenue.

- This H1 did not make clear whether the comparable H1’s revenue was flattered by including some of the “overreported and overpaid” troponin sales.

- The preceding FY’s troponin royalty error emphasised BVXP’s:

- Dependency on accurate customer calculations in order to publish reliable financial information, and;

- Lack of ‘visibility’ over the ‘downstream’ usage of its antibodies (see Royalty income and physical sales).

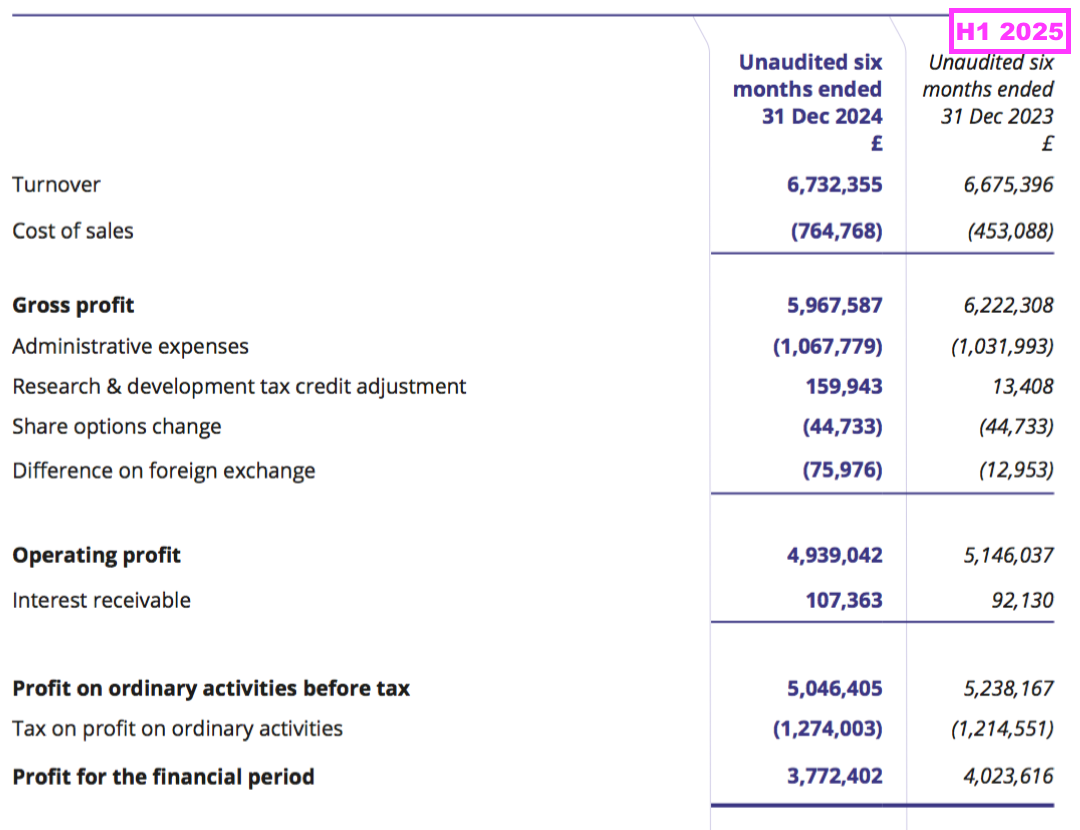

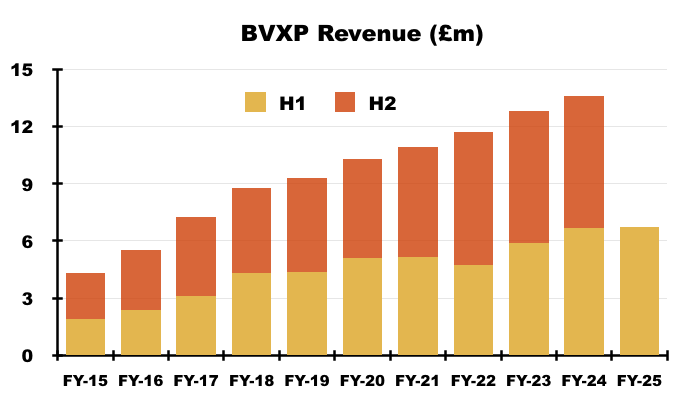

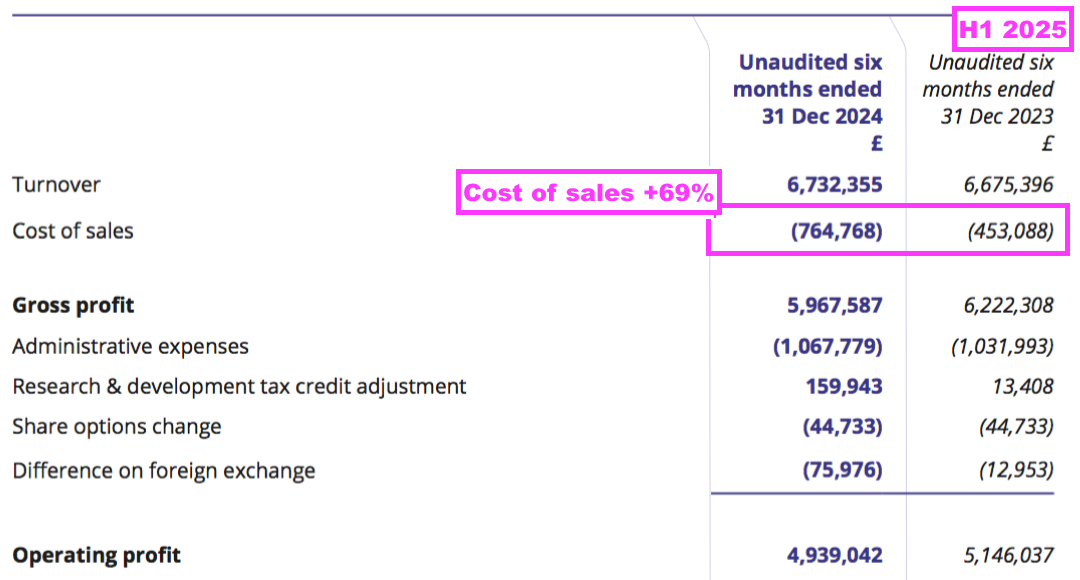

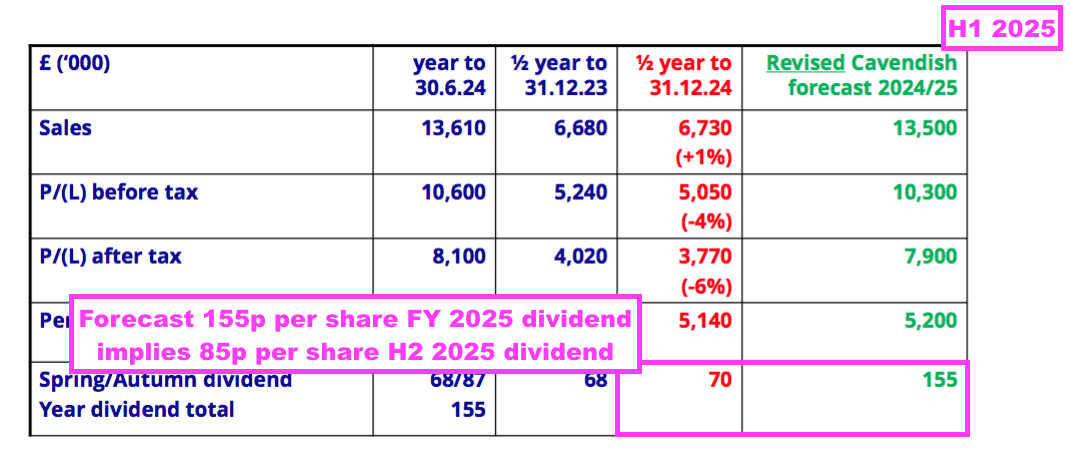

- Reported revenue for this H1 gained just 1% to £6.7m to set a new H1 record:

- This H1 repeated the preceding FY by describing the company’s markets as “mature“:

“Sales of our vitamin D antibody and other core antibodies were all more or less in line with last year’s sales reflecting the mature nature of the diagnostic products that our antibodies support.”

- BVXP has described its markets as “mature” since FY 2023:

[FY 2023] “Sales of vitD3.5H10 increased by 7% to £5.8 million which reflects analysts’ expectation for a relatively mature global IVD market.”

- Currency movements did not seem to distort this H1’s revenue performance.

- The preceding FY reiterated at least 50% of revenue is earned in USD…

[FY 2024] “We estimate that 50-60% of our total sales are directly linked to US Dollars via physical product pricing in US Dollars or indirectly linked to US Dollars via royalties based on downstream US Dollar sales. The remainder of the currency split is dominated by Euros and important Asian currencies.”

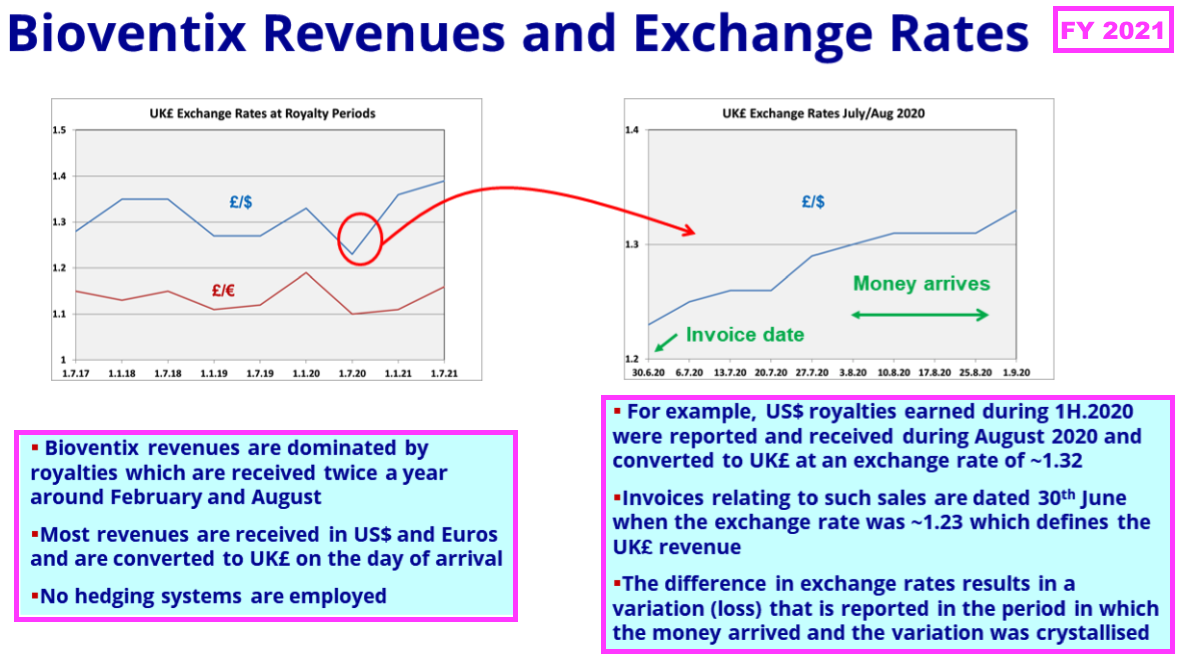

- …while FY 2021 explained how royalty revenue in particular is influenced by exchange rates prevailing at the date of each balance sheet:

- Royalty invoices for this H1 were dated 31 December 2024, at which point GBP:USD was 1.252.

- Royalty invoices for the comparable H1 were dated 31 December 2023, at which point GBP:USD was 1.275.

- As such, USD-invoiced royalty revenue appeared to be translated into GBP at a 2% higher rate during this H1 versus the comparable H1.

- Note that the subsequent H2 2025 may experience a notable adverse translation from USD to GBP.

- USD-invoiced H2 2025 royalty revenue will be dated 30 June 2025, at which point GBP:USD was 1.373 — some 8% weaker than the 1.265 recorded on 30 June 2024.

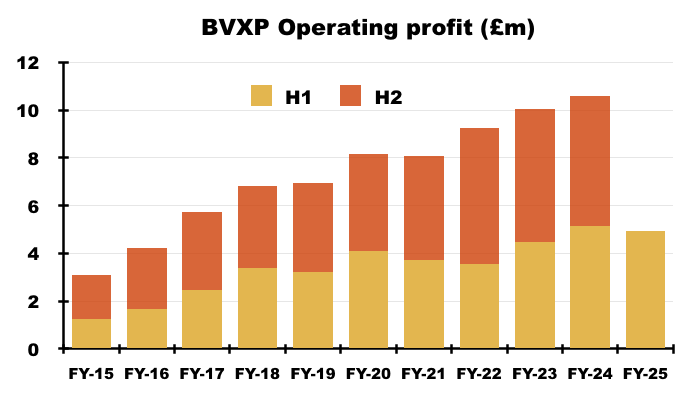

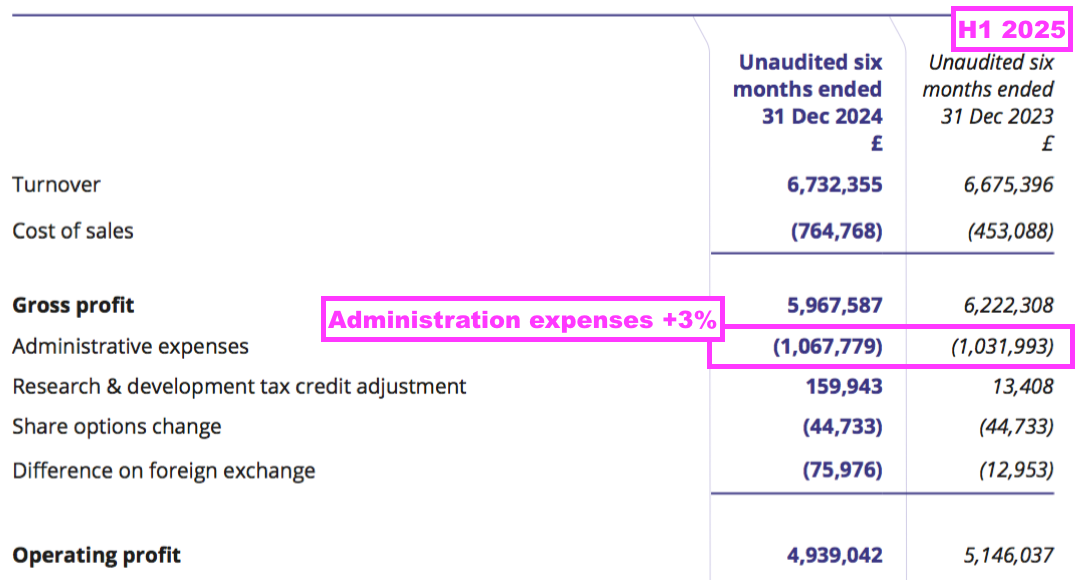

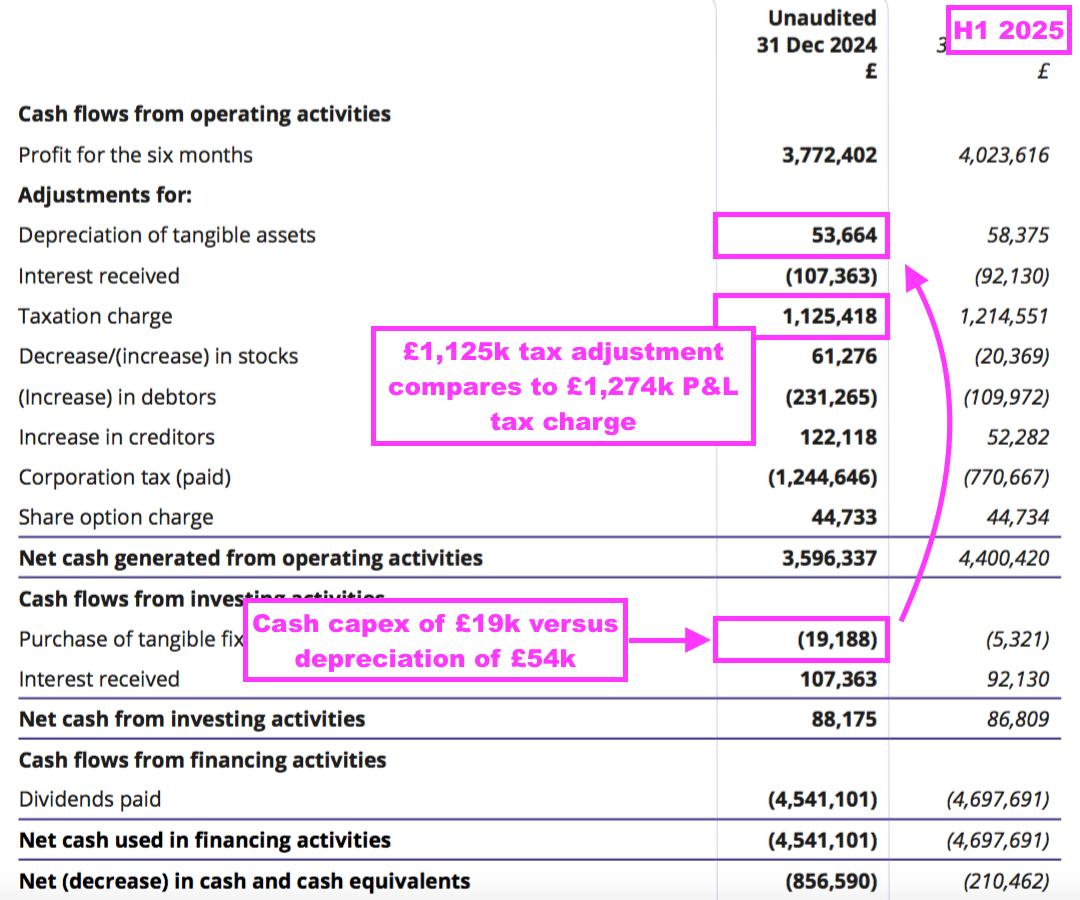

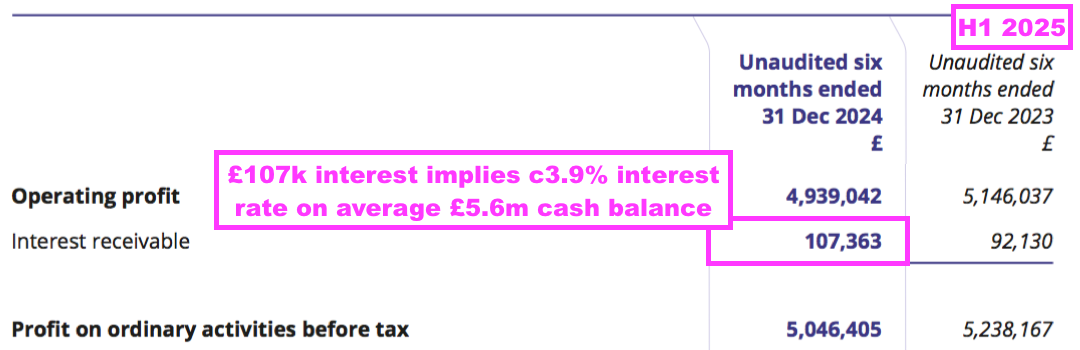

- Reported H1 operating profit slid 4% to £4.9m:

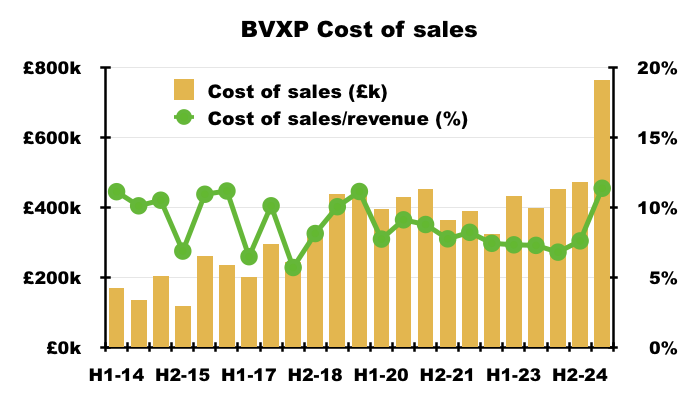

- H1 cost of sales soaring 69% suppressed both gross profit and operating profit:

- Cost of sales in fact absorbed 11.4% of revenue, the highest proportion since H2 2011 (20.3%):

- This H1 confirmed the higher cost of sales was due to greater external R&D (see Alzheimer’s R&D: royalties paid to researchers and Other R&D):

“Increased external research and development spending on the industrial pollution and water quality projects, as well as for our Alzheimer’s disease projects, was incurred in the period and thus, as such cost is treated as a direct cost, there is corresponding reduction in the reported profit“.

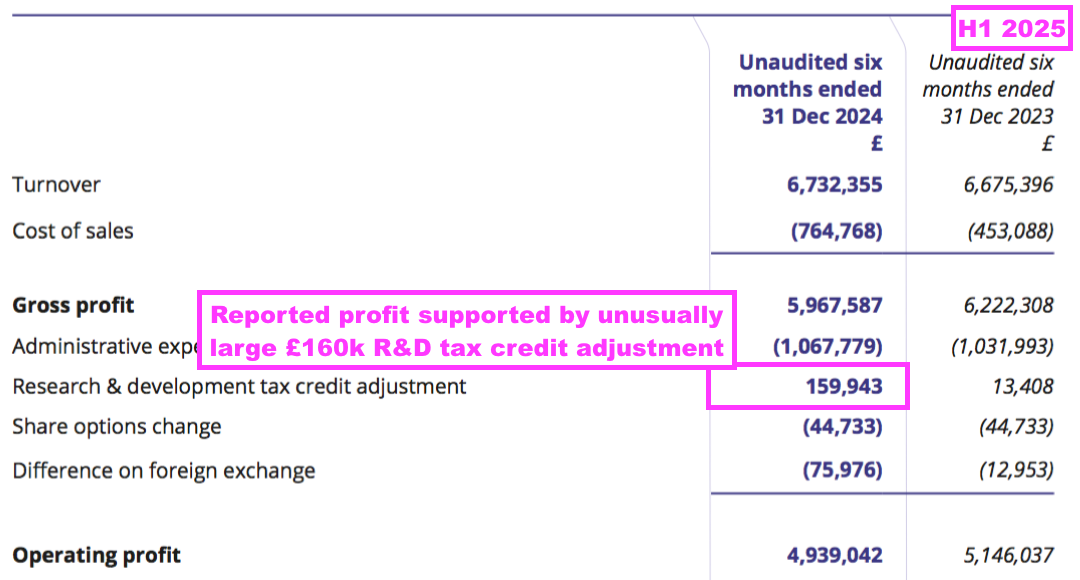

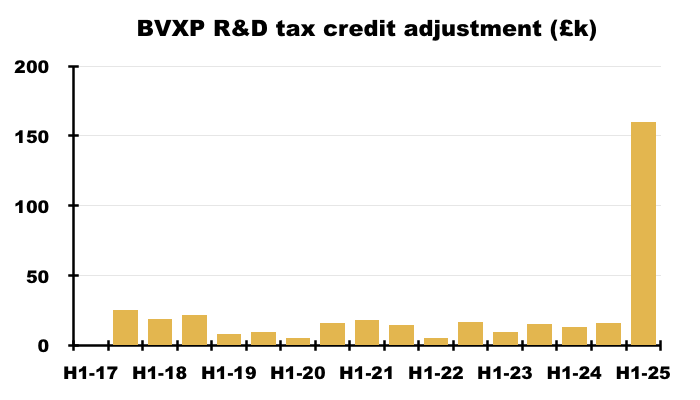

- Reported profit was boosted by an unusually large and unexplained £160k R&D tax credit adjustment:

- Perhaps the most surprising news of this H1 concerned the dividend.

- After the preceding H2 dividend was reduced by 3p to 87p per share, this H1 seemed likely to me to declare an unchanged H1 payout.

- But this H1’s payout was actually lifted 2p to 70p per share:

“We continue to follow our established dividend policy of distributing post-tax profits to shareholders. For the period under review, the Board is pleased to announce an interim dividend of 70 pence per share which represents a 3% increase on the interim dividend paid last year (68 pence per share).“

- I interpret this H1’s reference to “established dividend policy of distributing post-tax profits to shareholders” to mean earnings will now be distributed entirely to shareholders through dividends.

- This H1’s 72p per share earnings were indeed (almost) entirely distributed through the 70p per share H1 dividend.

- In contrast, the comparable H1 said the “established dividend policy” would increase future payouts in tandem with earnings:

[H1 2024] “Recent changes to the headline rate of Corporation Tax has had an impact on our reported earnings and cash flows. Nevertheless, we will endeavour to follow our established dividend policy of increasing our distributions to shareholders in line with increases in our post tax profit.“

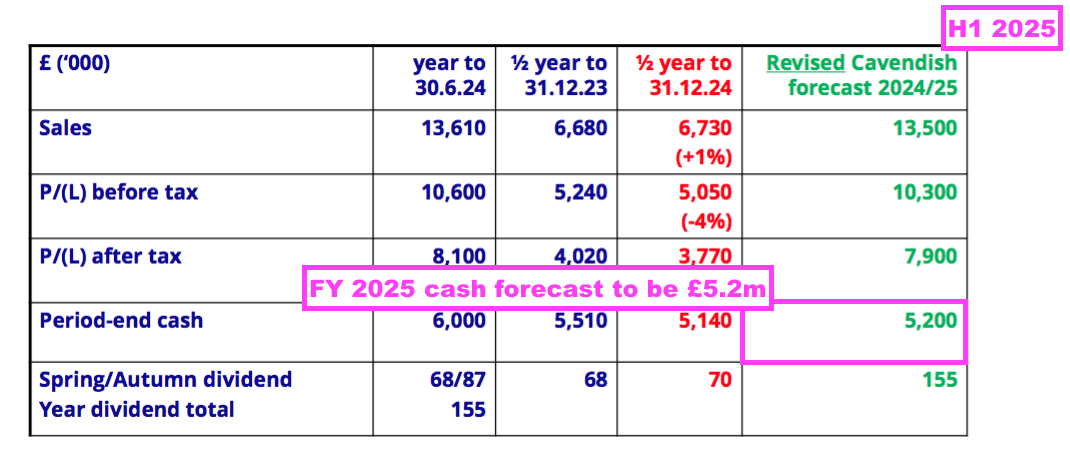

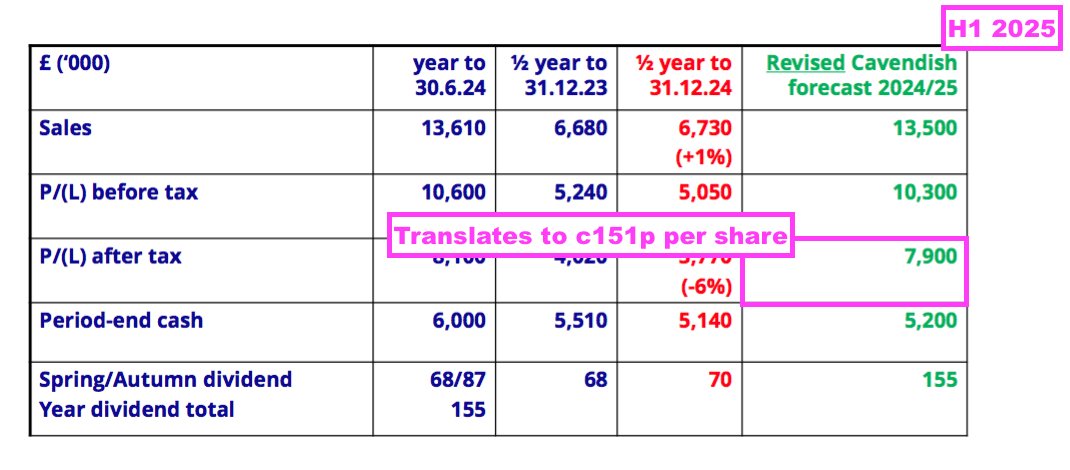

- This H1 showed BVXP’s broker projecting a maintained 155p per share dividend for FY 2025:

- A maintained 155p per share payout for FY 2025 implies an 85p per share dividend for H2 — a reduction of 2p per share versus the preceding H2’s 87p per share dividend.

- BVXP’s broker is anticipating FY 2025 earnings of £7.9m, which translates into approximately 151p per share — 4p per share lower than the broker’s projected 155p per share FY 2025 dividend.

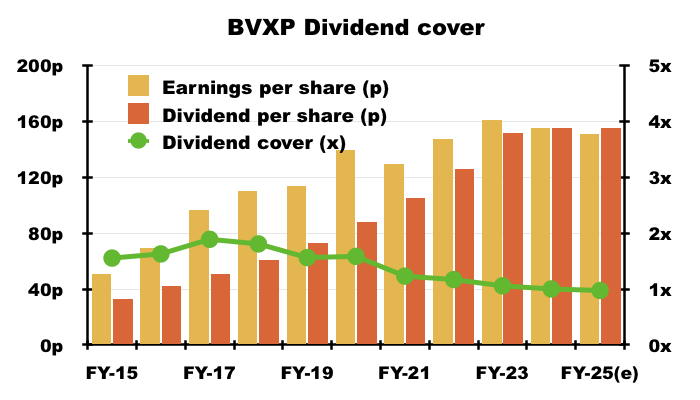

- Dividend cover for FY 2025 is therefore set to decline below 1x:

- Dividend cover falling below 1x arguably means BVXP is funding its greater cost of sales (i.e. greater external R&D) by dipping into its cash position (see Financials: balance sheet and cash flow). This H1 confirmed:

“Costs: increased investment in external R&D (Tau, industrial pollution, water quality) drawing on some cash reserves are included in cost of sales reducing headline margin.“

Royalty income and physical sales

- BVXP’s customers are predominantly major in vitro diagnostic (IVD) companies, such as Roche, Siemens and Abbott, which manufacture blood-testing machines and incorporate BVXP’s antibodies into blood-test reagent packs to help diagnose a variety of health conditions:

- BVXP’s revenue is earned mostly through IVD customers:

- Purchasing BVXP’s antibodies and incorporating them into reagent packs, and;

- Paying a small royalty for every reagent pack subsequently sold ‘downstream’ to the owners of the blood-test machines (typically hospitals).

- The amounts collected through physical sales and royalties is determined mostly by the volume of antibodies required for a particular blood test. Some tests require 100s or 1,000s more antibodies than others:

- Antibodies used in large volumes tend to earn larger physical sales and collect smaller royalties, whereas antibodies used in smaller volumes tend to earn smaller physical sales but collect larger royalties.

- The preceding FY reiterated the tiny mass of physical antibodies sold:

[FY 2024] “We currently sell a total of 15–20 grams of purified physical antibody per year, which accounts for 25–30% of our annual revenue.”

- The antibodies are sold in liquid form, and 20 grams equates to five or six litres of shipped product:

- BVXP discloses the split between royalty income and physical sales within only its FY results, and sure enough this H1 did not disclose a royalty-physical split.

- BVXP’s revenue has historically been divided approximately two-thirds royalties and one-third physical sales:

- The two revenue types have expanded at similar rates. Between FYs 2019 and 2024 for example, royalty income advanced by 46% while physical sales advanced by 48%.

- BVXP’s royalties typically capture approximately 2% of the ‘downstream’ sales of the blood-test reagent packs that incorporate the company’s antibodies.

- While BVXP’s royalty percentage is fixed, the associated reagent-pack sales to which the royalty percentage is applied may vary… meaning BVXP is not entirely in control of its eventual royalty income.

- Board remarks at the 2022 AGM confirmed BVXP suffered “limited visibility” over its royalty income. Attendees were told:

- BXVP does not know what its customers charge for blood-test reagent packs, and if/when those charges increase or decrease;

- Similarly, BVXP does not know the volume of reagent packs sold by its customers that include royalty-earning antibodies;

- BVXP therefore has “limited visibility” to analyse its royalty income, and;

- “The royalty is based on net sales after deductions and that is all [the customers] are required to declare.”

- FY 2023 revealed China accounted for approximately half of all physical sales:

[FY 2023]“Sales to China remain strong accounting for ~50% of total physical sales. Chinese downstream assay price pressure has increased through aggressive central health authority procurement mechanisms”

- The preceding FY suggested China continued to account for half of all physical sales, and confirmed “more significant” Chinese royalties should soon be collected:

[FY 2024] “Our shipments of physical antibody to China continued to increase. Some sales are made directly and some are made through five appointed distributors. More regulatory approvals for domestic Chinese customers using our antibodies have been registered, leading to more significant flows of royalty payments owing from these customers.“

- Sales to China have grown significantly over time. FY 2013 reported China represented approximately 10% of all shipments:

[FY 2013] “We are also cautiously optimistic about growth prospects in China. There are rapidly emerging Chinese customers and this represents a growth opportunity. It is noteworthy that in the financial year, around 10% of Bioventix shipments (including samples) were destined for China. The actual revenues are less than 10% of the total but the volume of shipments is encouraging for future growth.”

- This H1 briefly confirmed Chinese physical sales remained “healthy“:

“China: physical product sales remained healthy.”

- This H1’s accounts included “estimates” for Chinese royalties:

“Estimates for Chinese royalties are included whereas declared revenues for CY 2024 will be confirmed for inclusion in the final 2024/25 results.”

- The preceding FY acknowledged how Chinese customers may pay their royalties up to a year after utilising BVXP’s antibodies:

[FY 2024] “Chinese customers declare and pay royalties in arrears on a calendar year basis and we therefore have to accrue for such revenue, in both full year and interim results, basing our revenue expectation on previous experience.”

- The preceding FY also admitted a Chinese customer had paid its royalties only “as a result of internal and external audit processes”:

[FY 2024] “As a result of internal and external audit processes, it was only in May 2024 that we received payment from a Chinese customer for the royalties earned in 2023 and therefore our revenue for 2023/24 has benefited by £239k from our prudent assessment of accrued royalty revenue in respect of previous periods.”

- I trust Chinese customers do not always require an audit process to persuade them to pay.

- In contrast to Chinese customers, BVXP’s established EU/US customers typically pay their royalties:

- During August for BVXP antibodies utilised between January and June, and;

- During February for BVXP antibodies utilised between July and December.

- Board remarks at the 2024 AGM provided further details of Chinese IVD companies. Attendees were told:

- The likes of Mindray, Snibe and Autobio are “modelling themselves very aggressively” on EU/US IVD equivalents;

- BVXP’s Chinese agreements are now focused on a handful of local operators that the company knows “very, very well“;

- Sales are no longer made to Chinese academics/distributors;

- Chinese competition is “very serious” and “we’re stuck with that“;

- Chinese IVD companies appear to be focusing more on new tests rather than revamping established tests, and;

- Switching from a BVXP antibody to a Chinese antibody would be as “non-trivial” for a Chinese IVD company as it would be for a EU/US IVD company.

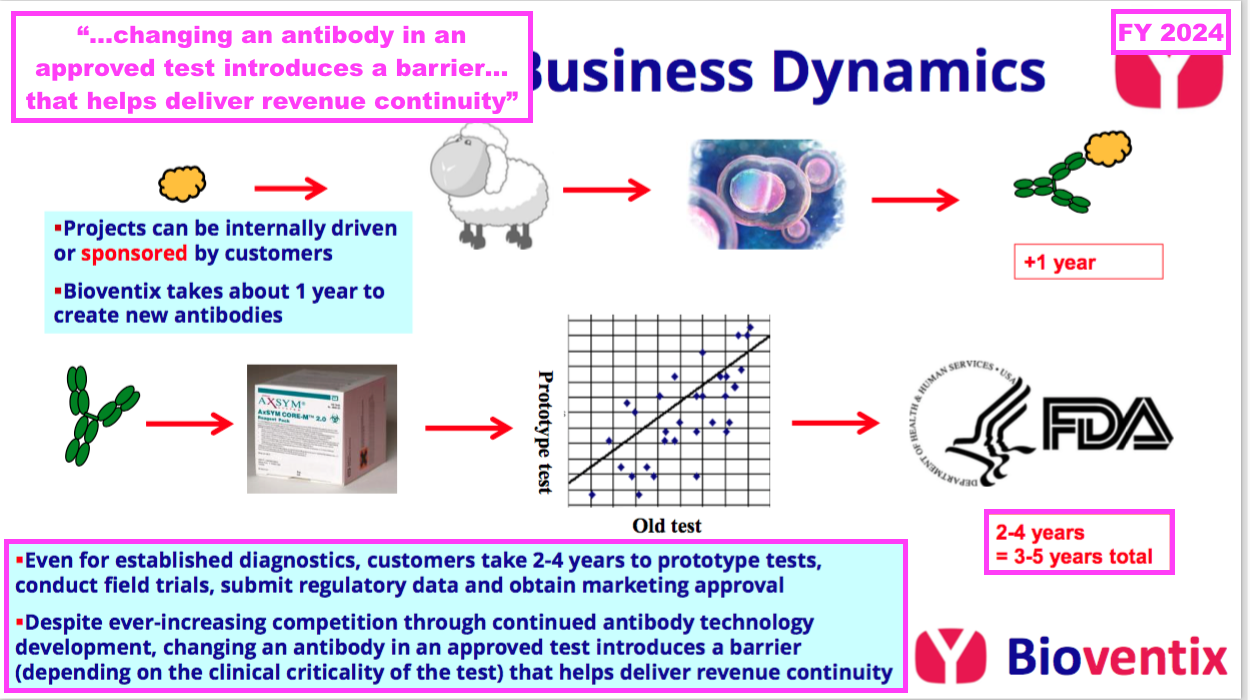

- The preceding FY reiterated why substituting proven diagnostic antibodies is “non trivial“: the replacement version must undertake clinical tests and obtain regulatory approval before a commercial launch:

[FY 2024] “The process of subsequent development thereafter by our customers can take many years before registration or approval from the relevant authority… is obtained and products can be sold to the benefit of the customers, and of course Bioventix, through the agreed sales royalty.

However, because of the resource required to gain such approvals, after having achieved approval for an accurate diagnostic test using a Bioventix antibody, there is a natural incentive for continued antibody use. This results in a barrier to entry for potential replacement antibodies which would require at least partial repetition of the approval process arising on a change from one antibody to another.

This barrier to antibody replacement arises from a combination of factors driven by the clinical criticality of the test and the potential consequences of making such a change, which include the time and cost to register any changes required to validate the performance of the replacement antibody.“

- As such, the healthcare/IVD industry can be very reluctant to replace a proven blood test, which means established diagnostic antibodies can remain commercial for extended periods.

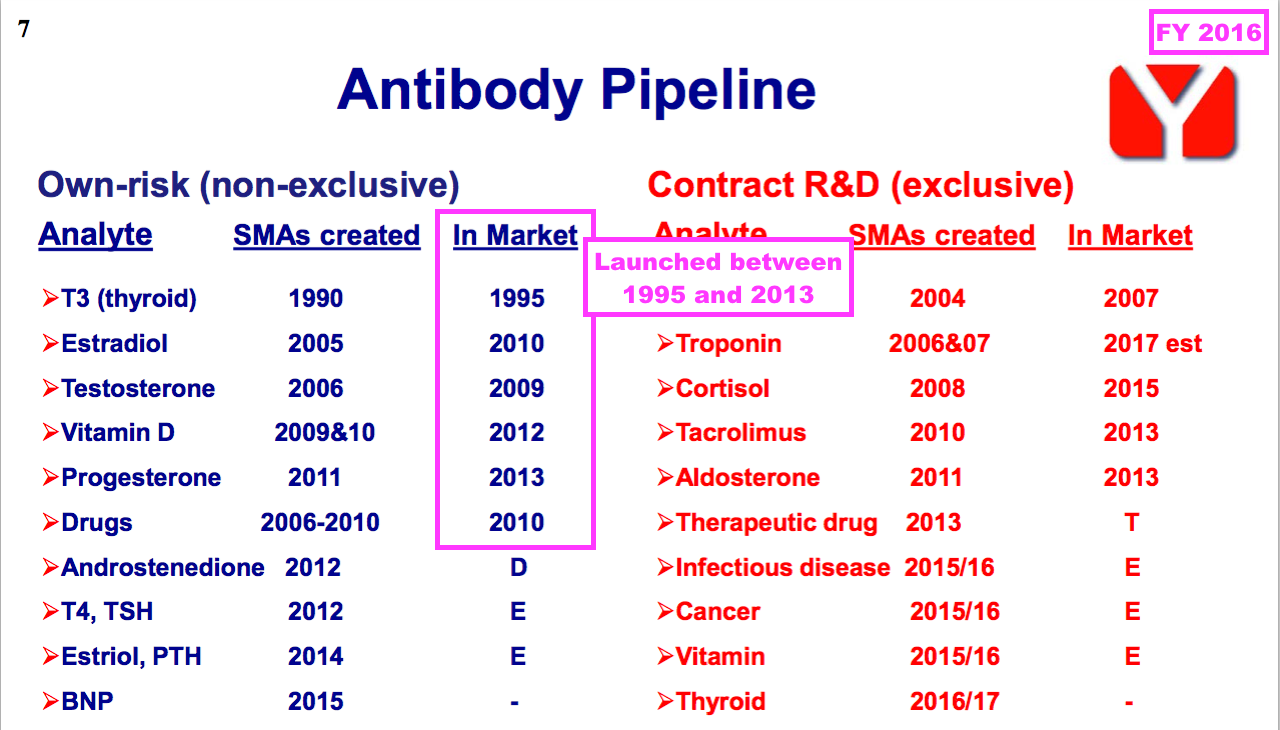

- FY 2016 revealed how a number of BVXP’s current antibodies were first launched more than ten years ago, with Tri-iodothyroxine (T3) seemingly celebrating an astounding 30 years on the market (see Troponin and other antibodies):

Vitamin D

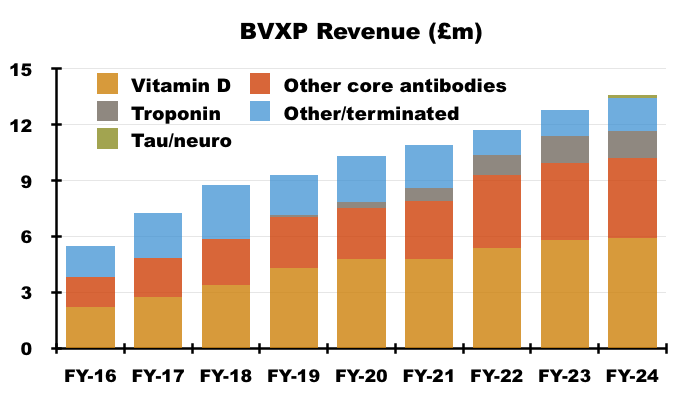

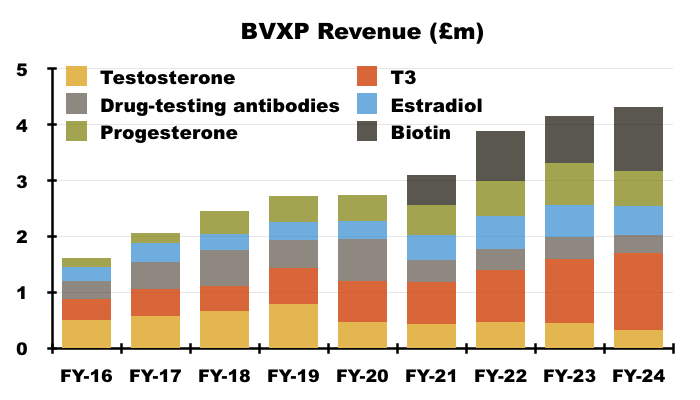

- By far BVXP’s best seller is its vitamin D antibody, which has represented between 38% and 47% of revenue since FY 2016:

- Similar to the disclosure of royalty income and physical sales, BVXP only divulges the revenue from its leading antibodies within its FY results.

- H1 presentations therefore (oddly) repeat the slide showing the individual antibody contributions from the preceding FY:

- I speculate BVXP’s reluctance to disclose individual H1 antibody revenue is due to the company’s apparent limited visibility towards physical sales and royalty income, which could leave six-month fluctuations open to misinterpretation by impressionable shareholders.

- This H1 provided only the shortest of updates on the vitamin D best-seller:

“Sales of our vitamin D antibody and other core antibodies were all more or less in line with last year’s sales reflecting the mature nature of the diagnostic products that our antibodies support. “

- The preceding FY revealed vitamin D revenue gained only 1% in what had become a “relatively mature global IVD market”:

[FY 2024] “Our most significant revenue stream continues to come from the vitamin D antibody called vitD3.5H10. This antibody is used by a significant number of diagnostic companies around the world for use in vitamin D deficiency testing. Sales of vitD3.5H10 increased by 1% to £5.9 million which reflects analysts’ expectation for a relatively mature global IVD market.”

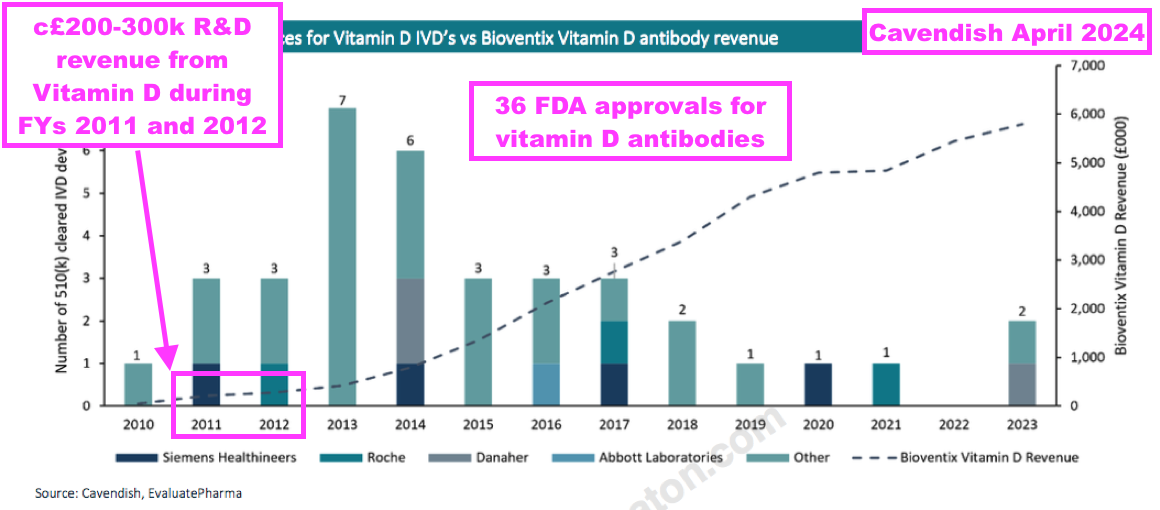

- An informative broker note issued last year highlighted 36 vitamin D tests being approved for use within the United States between 2010 and 2023:

- BVXP started development on vitamin D during 2008 and revenue was first achieved during 2011.

- Note that vitamin D “moved into large-scale manufacturing” and generated R&D-revenue (from customers testing the antibody for research purposes) during FYs 2011 and 2012 — i.e. before a wider clinical test was launched:

[FY 2011] “One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008. A leading antibody called vitD3.5H10 has moved into large-scale manufacturing at the company in order to supply increased quantities of antibody required for our customers’ own R&D use. Revenue from the supply of this product has been generated for the first time during the period. No major licensing deals have yet been concluded, however, the Directors are optimistic about the future value of this particular antibody and anticipate that significant licensing deals will be forthcoming in the future.“

[FY 2012] “During the year Bioventix’s leading vitamin D antibody, vitD3.5H10, moved into large-scale manufacture in response to customer demand and revenue from the supply of this product has continued to grow during the period. Whilst no significant commercial vitamin D assays based on vitD3.5H10 are currently in the market, the Directors remain optimistic that this antibody will generate revenues for the Company in future periods. The Company has also entered into additional licensing deals with major diagnostics companies in respect of vitD3.5H10.”

- From that broker note above, vitamin D appeared to generate R&D revenue of approximately £200k during FY 2011 and approximately £300k during FY 2012.

- Vitamin D generating R&D revenue may have positive omens for BVXP’s Alzheimer’s antibodies, three of which have recently moved into “large-scale production for commercial supply” and started to earn R&D revenue from customer testing (see Alzheimer’s R&D: revenue).

- Vitamin D revenue going from zero to almost £6m within 13 years may give some idea as to the potential of BVXP’s Alzheimer’s antibodies (see Valuation).

Troponin and other antibodies

- The comparable H1 acknowledged revenue from troponin antibodies — used within blood tests to help diagnose suspected heart attacks — had been “a little below expectation“:

[H1 2024] “Whilst our total sales continue to grow, our sales relating to troponin antibodies were a little below expectation.“

- At the time BVXP cited “temporary operational issues” at its customers:

[H1 2024] “We continue to believe that temporary operational issues experienced by our partner customers have slowed the rollout of their improved troponin assays. Whilst this has inhibited growth short term, there is no obvious reason to doubt the previous forecasts for future growth of troponin related revenues in the longer term.”

- The preceding FY then admitted troponin revenue had been “overreported and overpaid” during FYs 2022 and 2023 by a total £327k:

[FY 2024] “During the year the Company became aware that, due to a customer error in the incorrect application of a historic royalty percentage, they had overreported and overpaid troponin royalty revenues since July 2021.”

- This troponin error emphasised BVXP’s aforementioned “limited visibility” towards customer royalty payments.

- The preceding FY also revealed (correctly calculated) troponin revenue was “below… expectations”:

[FY 2024] “After correctly allocating the revenue to each of the years 2023/24 and 2022/23, our total troponin antibody royalty revenue from Siemens Healthineers and another separate technology sub-license increased by 3% during the year from £1.41 million to £1.45 million. The level of these royalties and their growth are below our previous expectations based on downstream assumptions.”

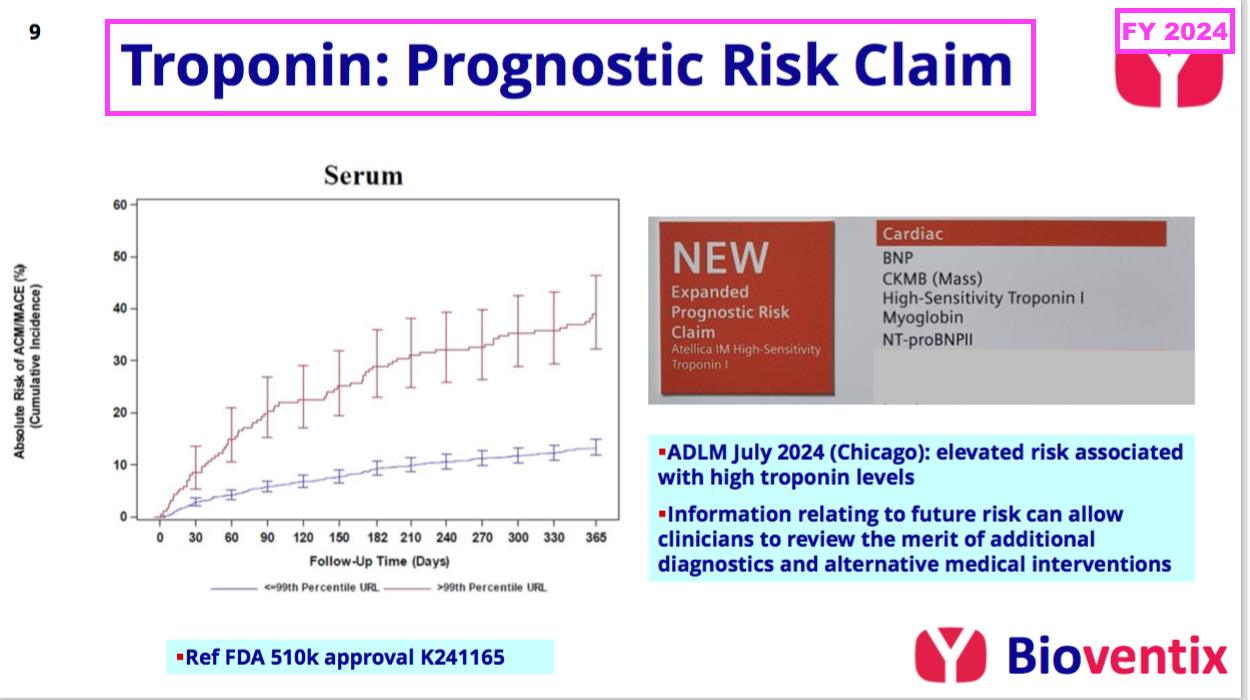

- The preceding FY revealed BVXP’s troponin revenue could be enhanced by the same blood test being used to “assess the impending risk of a future adverse cardiac event“:

[FY 2024] “In contrast to the disappointment of troponin sales in the current application of acute chest pain (i.e. suspected heart attack in A&E centres), we are pleased to note that Siemens have received FDA approval for a revised label claim for their troponin assay that covers a new prognostic application. This enables troponin levels to be measured in “at risk” patients and/or patients who have already been diagnosed with a cardiac condition, whose troponin levels may now be measured to assess their impending risk of a future adverse cardiac event. This risk information can then be used to help clinicians consider additional diagnostic procedures or to review therapeutic alternatives. We expect that this new application will stimulate additional troponin assay use and our associated royalties, thus increasing the market opportunity.”

- Board remarks at the 2024 AGM provided further details of this secondary troponin application. Attendees were told:

- Siemens was “optimistic” this “whole new market for troponin” would “boost sales“;

- Some cardiologists would now “just measure everybody” who visits their clinics with this secondary test, and;

- The first indication of progress should have emerged by March 2025.

- This H1 admitted troponin sales had remained below expectations:

“Our sales relating to troponin antibodies were steady and a little below our expectation.”

- This H1 also confessed the secondary troponin application had yet to prove popular with Siemens’ customers:

“In November 2024, we reported that Siemens had received FDA approval for a revised label claim for their troponin assay covering a new prognostic application. This was an encouraging development, but it remains too early to see the significant adoption of this application and therefore the use and sales of the assay and an uplift in our associated royalties.“

- This H1 disclosed extremely little about the company’s other core antibodies:

“Other core historic antibodies: sales were similarly steady.“

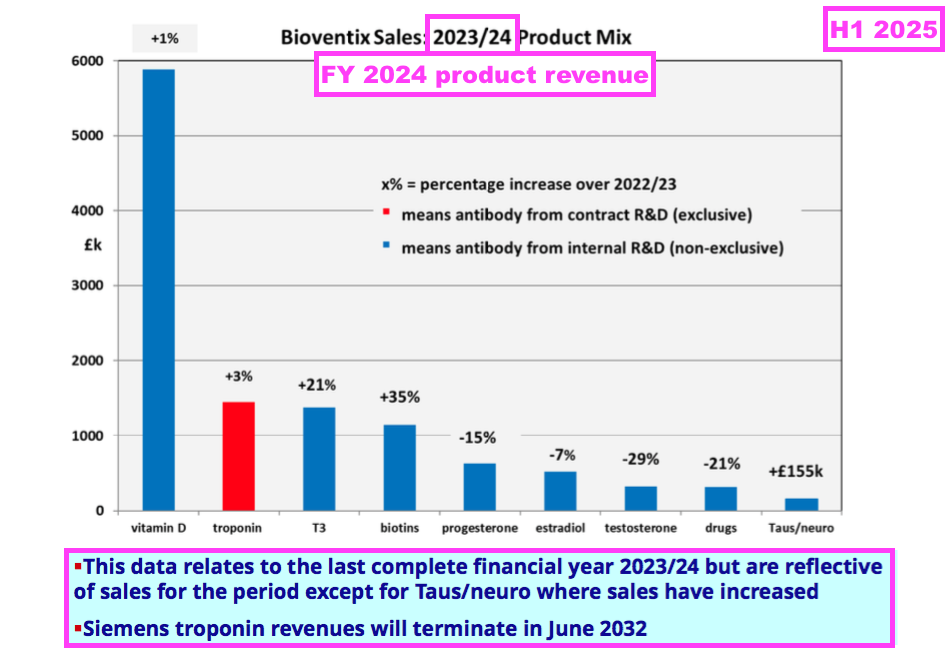

- The preceding FY showed the other core antibodies improving their collective revenue by 4%, although individual product revenue experienced wide fluctuations:

[FY 2024]

• T3 (tri-iodothyronine): £1.38 million (+21%)

• biotins and biotin blockers: £1.14 million (+35%)

• progesterone: £0.63 million (-15%)

• estradiol: £0.52 million (-7%)

• testosterone: £0.33 million (-29%)

• drug-testing antibodies: £0.32 million (-21%).

- Underlining the longevity of successful diagnostic antibodies, many of BVXP’s other core antibodies have been on the market since at least 2013:

- Not shown on that FY 2016 slide is biotin, which I understand from the 2022 AGM has been on the market since 1999.

Alzheimer’s R&D: revenue

- By far the most promising development at BVXP concerns the company’s work creating antibodies to potentially identify and monitor Alzheimer’s disease (AD) through blood tests.

- AD is currently identified and tracked through brain scans and/or lumbar punctures, both of which — unlike simple/fast/cheap blood tests — are impractical for widespread screening and monitoring for potential AD.

- The preceding FY announced the AD research had achieved initial revenue of £155k:

[FY 2024] “Our research into Tau antibodies and Alzheimer’s diagnostics continues to progress and we are delighted that our early work has now translated into a modest revenue stream from antibodies now entering commercial manufacture.

…

Total Tau revenues for the year were above our expectation at £155k.”

- That AD revenue was earned mostly through IVD customers ordering repeat samples for their own R&D:

[FY 2024] “Our commercial policy is to supply initial evaluation samples of antibodies free of charge. If antibodies perform well on prototype assay systems at our IVD customers and additional supplies are ordered, these are charged at regular prices and such repeat sales have generated revenues during the year. These revenues are not only additive but also indicate that our antibodies could feature in future commercial assays.”

- The preceding FY said the repeat AD orders offered “some encouragement” that BVXP’s AD antibodies will one day feature within mainstream commercial AD blood tests:

[FY 2024] “We have supplied a number of major IVD companies with antibodies from our growing Tau antibody portfolio. It is encouraging that a small number of these companies have requested additional quantities of the antibodies supplied. Not only does this add modestly to our overall revenues but it also offers some encouragement that our antibodies will play some part in the future neurological panel offerings of our customers.“

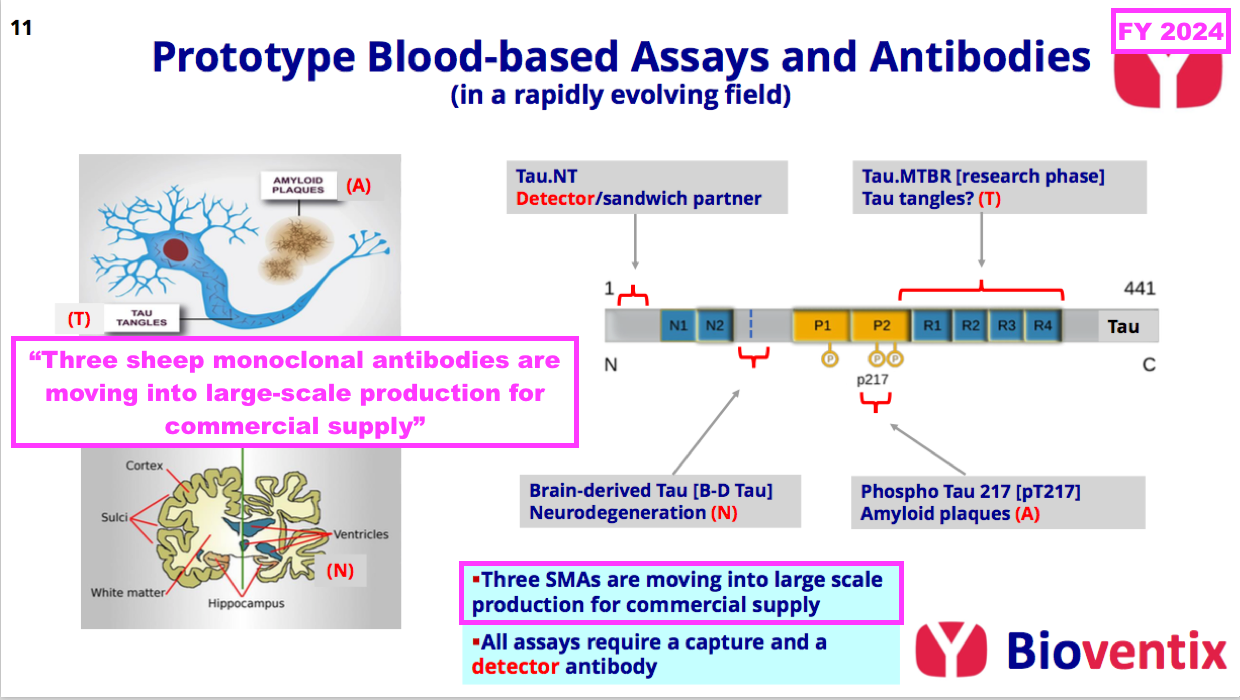

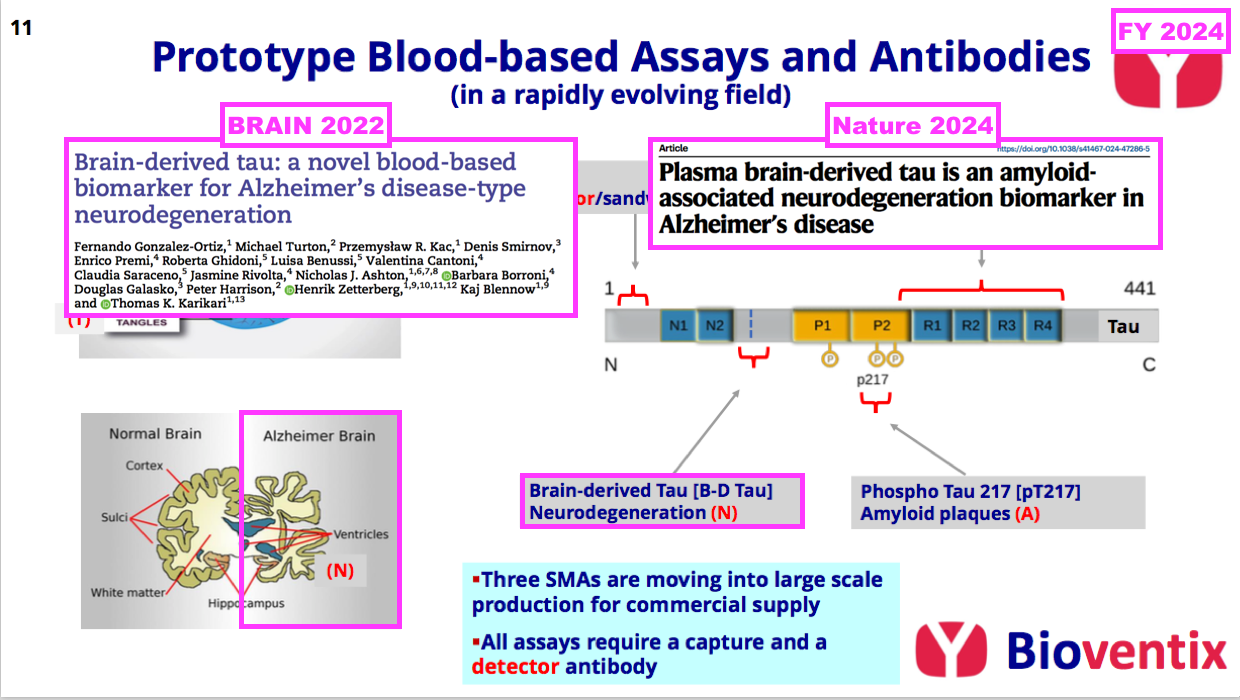

- The preceding FY underlined the promising AD work by announcing the “large-scale production” of three AD antibodies:

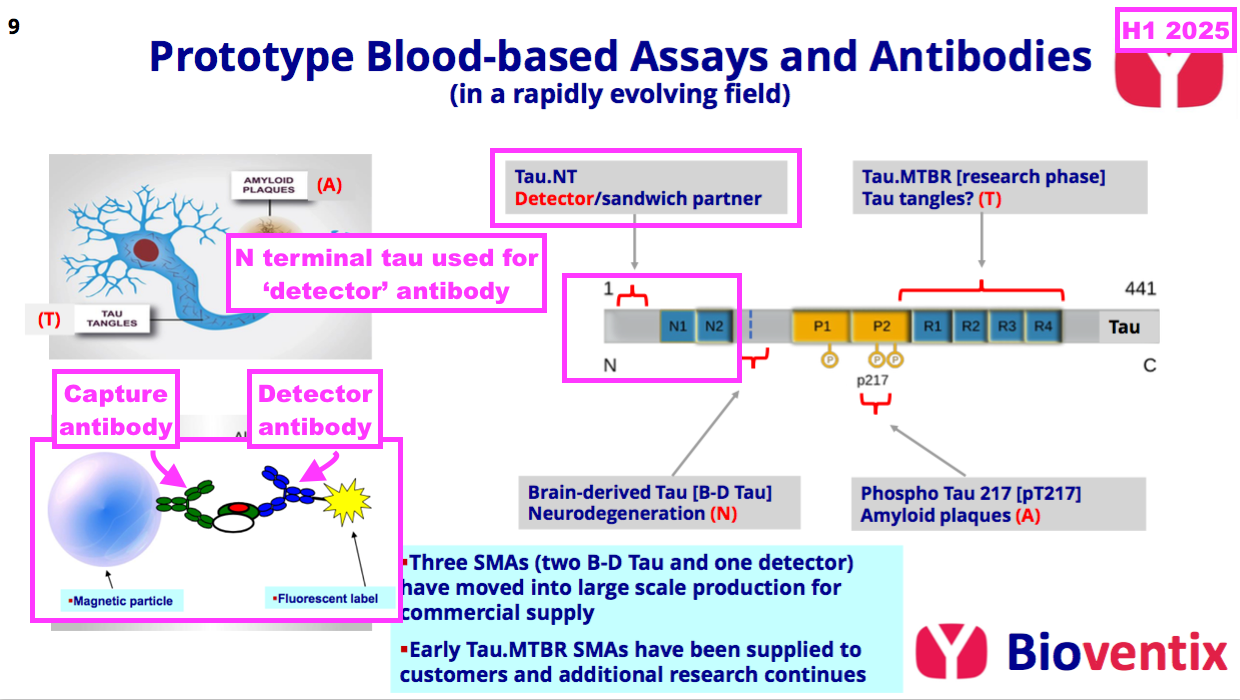

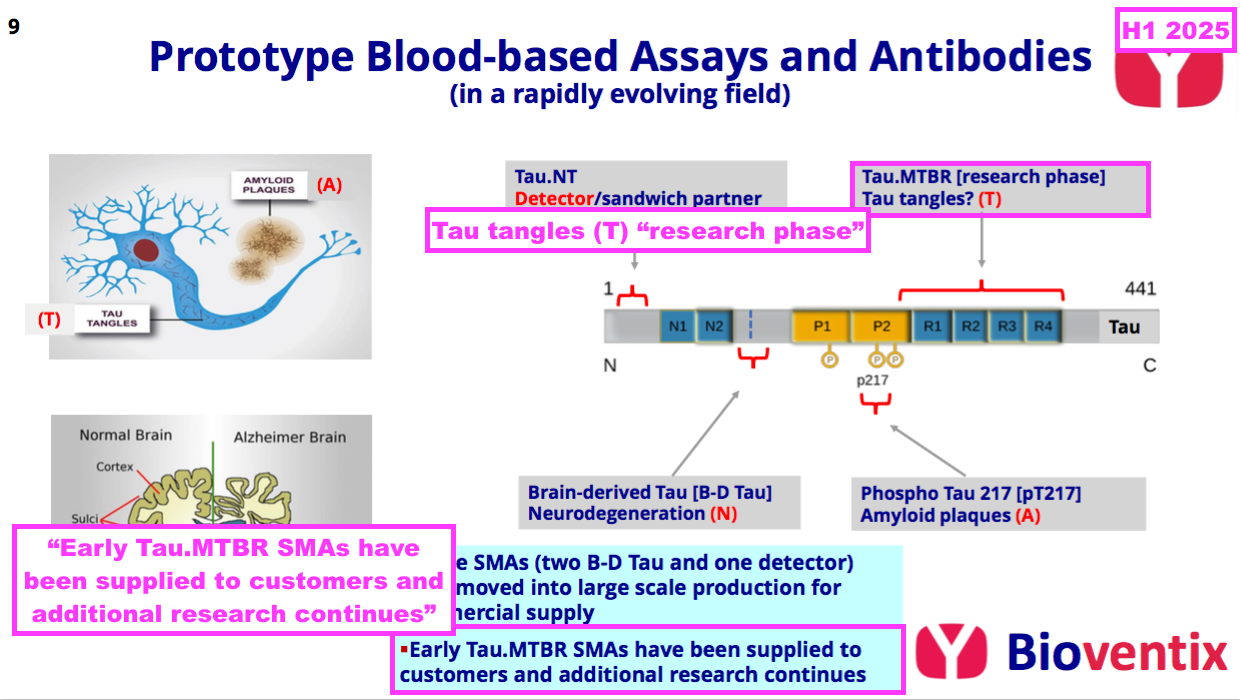

- The preceding FY did not reveal exactly which three AD antibodies were moving into “large-scale production“, but this H1 confirmed the three were two brain-derived tau antibodies (see Alzheimer’s R&D: neurodegeneration and brain-derived tau) and a ‘detector’ antibody (see Alzheimer’s R&D: amyloid plaques and p-tau):

“The level of research interest at our in vitro diagnostic customers in the field of neurology, initially focusing on Alzheimer’s disease testing continues to increase. Three of the Tau antibodies that Bioventix has created have already moved into full-scale manufacture. Two of these are aimed at brain-derived Tau for neurodegeneration testing and the other is a detector antibody that can pair with Bioventix or other specific antibodies (i.e. p-tau217) as part of customer test designs.”

- Implementing “large-scale production” of AD antibodies for customer R&D purposes is very reminiscent of the aforementioned “large-scale manufacturing” of vitamin D antibodies for customer R&D purposes during FY 2011:

[FY 2011] “One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008. A leading antibody called vitD3.5H10 has moved into large scale manufacturing at the company in order to supply increased quantities of antibody required for our customers’ own R&D use. Revenue from the supply of this product has been generated for the first time during the period. No major licensing deals have yet been concluded, however, the Directors are optimistic about the future value of this particular antibody and anticipate that significant licensing deals will be forthcoming in the future.“

- Vitamin D soon became BVXP’s best seller, which does imply antibodies generating notable income during early R&D testing have proven themselves to be very popular very quickly…

- …and should therefore be more likely to become rather lucrative following a full commercial launch.

- The preceding FY’s AD revenue was earned during H2 and board remarks at the 2024 AGM indicated the AD revenue actually commenced during Q4 2024 (April-June 2024).

- Multiplying the £155k AD revenue by four gives a theoretical £620k annualised AD revenue…

- …which is double the aforementioned £300k or so vitamin D seemingly earned through customer R&D testing during FY 2012.

- This H1 did not disclose the exact AD R&D revenue but said such revenue had “increased“:

“Sales of these Tau antibodies for research use only assays have increased during the period and we remain optimistic about the future prospects for these and other additional antibodies that could feature in neurological blood testing assays into the future.”

- I trust the AD R&D revenue earned during the six months of this H1 was at least twice the £155k revenue earned during the three months of Q4 2024.

- This H1 gave a positive outlook for the AD R&D:

“Increased sales of Tau antibodies for Alzheimer’s disease have been a highlight and we continue to remain excited about the future for these antibodies as the scientific output of our collaboration with University of Gothenburg increasingly translates into commercial success.“

- The positive outlook for the AD R&D is supported by the emergence of new AD treatments.

Alzheimer’s R&D: Alzheimer’s treatments

- The preceding FY reiterated how the approval of lecanemab and donanemab had created greater interest among IVD companies to launch blood tests that identify and monitor AD:

[FY 2024] “Recently, the approval of first generation AD therapeutics (lecanemab jointly developed by EISAI and Biogen, and donanemab from Eli Lilly) have changed the perception of AD therapy, and it is likely that second generation therapeutics, or combination therapies will further help to slow the disease process. Patients presenting early in the ATN [amyloid/tau/neurodegeneration] pathway appear to benefit most from therapy. Therefore, ATN assessments can be used not only to screen for patients suitable for therapy but also for monitoring patients whilst on therapy.”

- Within the United States, lecanemab was approved for clinical use during 2023 while donanemab was approved for clinical use during 2024.

- Within Europe, lecanemab was approved for clinical use during 2025 while donanemab still awaits full approval.

- Despite the pioneering medical results from lecanemab and donanemab, their uptake among AD patients has not been significant.

- According to “Disparities in Early Lecanemab Uptake Among US Medicare Beneficiaries“, just 1,582 of 550,945 patients diagnosed with AD within the United States were treated with lecanemab during the nine months to March 2024. This research from lecanemab co-developer Eisai meanwhile states only 4,903 US patients undertook at least six months of lecanemab treatment up to December 2024.

- The seemingly slow uptake in the States is presumably due to the low cost-effectiveness of the treatments (“Cost-Effectiveness of Lecanemab for Individuals With Early-Stage Alzheimer Disease“).

- Within the UK for instance, lecanemab and donanemab have not been approved for NHS usage because they were both deemed as being “not good value for money“:

[NICE August 2024] “The [lecanemab and donanemab] treatments have been shown to delay progression from mild to moderate Alzheimer’s by 4-6 months but the overall costs of purchasing and administering the drug remain high and the benefits too small.”

- Meanwhile in Europe, lecanemab was approved for clinical use this year and was launched first in Austria and Germany during August and September respectively.

- The tardy approval process in Europe — with donanemab yet to receive full authorisation — has led to criticism from leading AD researchers:

[The Lancet May 2025] “By delaying the adoption of donanemab, the EMA has effectively signalled to Europe’s patients with Alzheimer’s disease that they are second-class citizens. Although the rest of the world cautiously but optimistically adopts disease-modifying treatments, Europe is lagging behind. This conservative stance not only delays patient access to innovation, but also sends a discouraging message to researchers and drug developers. Without greater clarity and coherence, Europe risks becoming an increasingly unattractive environment for pharmaceutical innovation in areas of urgent medical need.”

- For now at least, the high cost and seemingly modest medical benefits of lecanemab and donanemab will limit the number of AD patients undertaking such treatments… and therefore perhaps limit the demand for blood tests to identify patients for such treatments.

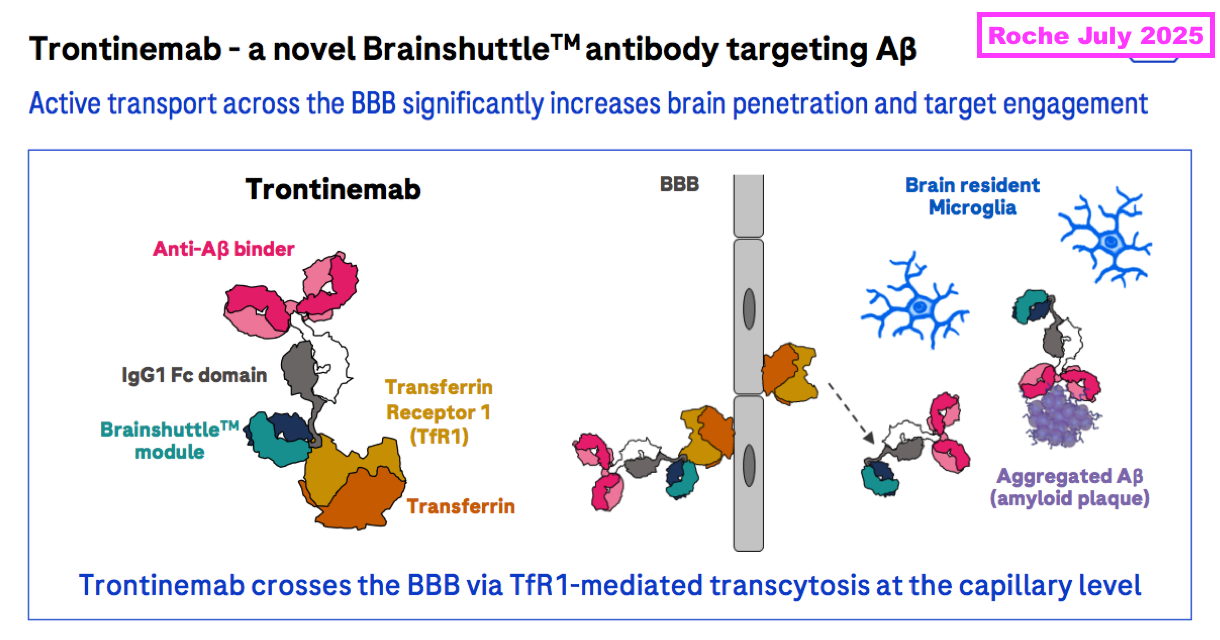

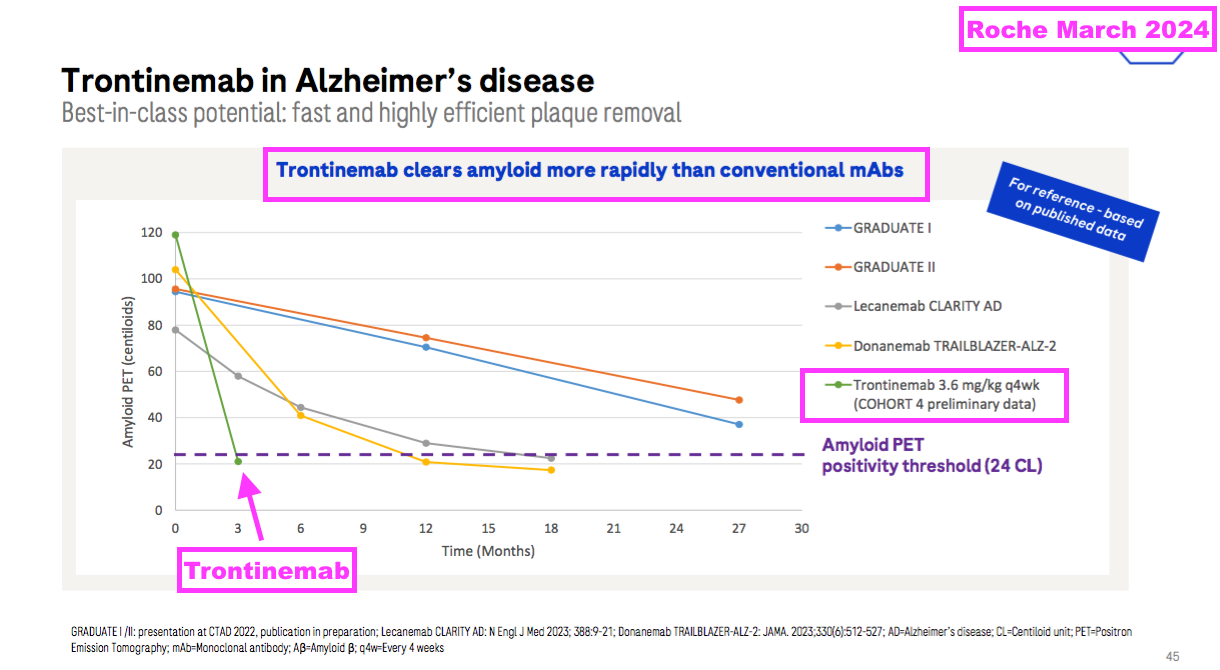

- But the next generation of AD treatments are undergoing trials, with trontinemab seemingly among the front runners.

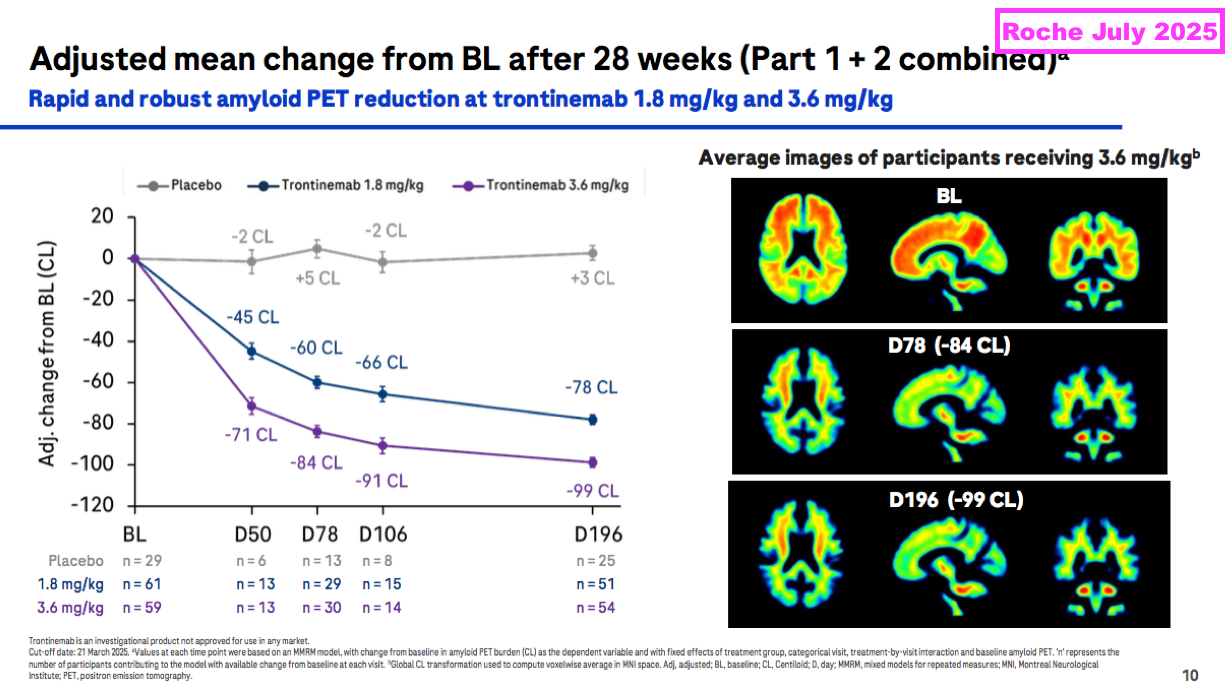

- Trontinemab is under development by Roche and utilises something called a “transferrin receptor” alongside transcytosis to penetrate much more of the brain with corrective antibodies than lecanemab and donanemab:

- During what appeared to be a landmark presentation, Roche claimed earlier this year that 91% of test participants exhibiting early signs of AD no longer exhibited early signs of AD after 28 weeks of trontinemab doses:

- Roche claims trontinemab is more effective than lecanemab and donanemab and incurs fewer side effects:

- AD experts at the UK Dementia Research Institute have become very excited by trontinemab’s progress:

[UK Dementia Research Institute July 2025]

“These results show it could be faster and safer than previous drugs, which would mean less monitoring. That could bring down the costs significantly as it would mean fewer MRI scans, so that would hopefully mean it would get NICE approval.”

…

“Evidence presented at the Alzheimer’s Association conference in Toronto on trontinemab is very promising, showing that the drug can effectively and rapidly clear amyloid from the brain, seemingly with very few side effects.”

…

“The biggest news, however, came from Roche, which is moving full speed ahead with trontinemab into phase III trials. Trontinemab is a monoclonal antibody targeting amyloid plaques, engineered with a transferrin receptor–mediated shuttle to enhance blood–brain barrier penetration. Phase II data were remarkable: the drug produced rapid amyloid plaque clearance, improved multiple biomarkers, and showed a much lower incidence of ARIA, even in APOE4 homozygotes.”

- Note the trontinemab findings were conducted through a Phase 2 trial and a much larger Phase 3 trial still needs to be undertaken — and generate favourable clinical results! — before regulatory approval can be sought.

- Recruiting volunteers for trontinemab’s Phase 3 trial is already underway.

- Results from trontinemab’s Phase 3 trial are not expected until 2028.

- According to “Alzheimer’s disease drug development pipeline: 2025“, trontinemab is one of 138 potential AD treatments being assessed by 182 clinical trials.

- I am hopeful trontinemab — or one of the other 137 potential AD treatments presently undergoing trials — will one day enjoy widespread clinical use that spurs significant demand for blood tests that can identify the early onset of AD.

- Board remarks at the 2024 AGM told attendees the emergence of AD treatments could lead to the “dawn of a new blockbuster era” for wider neurology diagnostics, albeit “during the 2030s“.

- I think the slow uptake of lecanemab and donanemab — alongside another few years awaiting favourable progress from trontinemab — underline how AD blood tests will not find widespread clinical use until “during the 2030s“.

- After all, there seems little point mass-screening the general public for early signs of AD if a suitable, cost-effective treatment has yet to be approved.

- In the meantime, ongoing revenue from the AD R&D should mean BVXP stands a chance of participating in the “dawn of a new blockbuster era” for AD blood tests as and when a suitable, cost-effective treatment emerges.

Alzheimer’s R&D: neurodegeneration and brain-derived tau

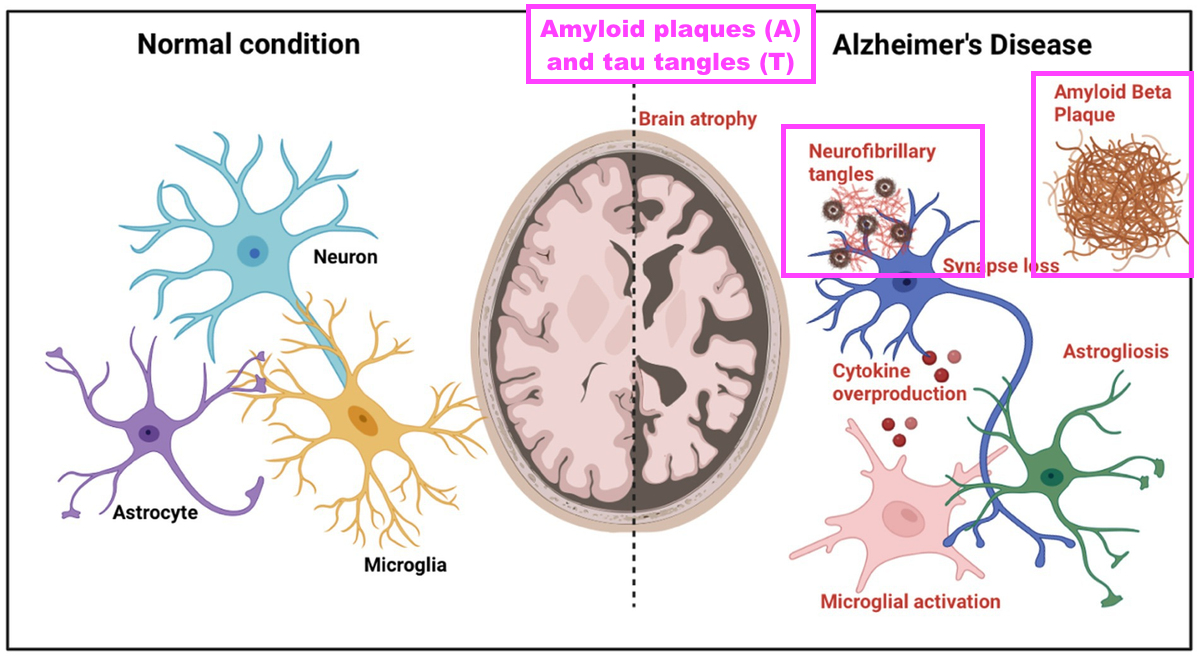

- FY 2023 first explained to BVXP shareholders how the onset of AD is defined through three parts of an “ATN framework“:

[FY 2023] “Over the last few years, a considerable amount of lab resource has been allocated to the tau project and Alzheimer’s disease (AD) diagnostics. AD is a complex disease that manifests itself differently across the patient population. At a cellular level, nerve cells (neurons) become associated with amyloid (A) plaques that build up outside the neurons. This is followed by the build-up of tau (T) tangles inside the neurons. These pathological processes then result in neuronal cell death and the symptoms of neurodegeneration (N) that accompany this. This “ATN” framework is used by neurologists to define the disease pathway that progresses many years before patient symptoms become more obvious. “

- BVXP appears to enjoy a favourable R&D position within the neurodegeneration (N) part of the ATN framework:

- Neurodegeneration is the process of the brain shrinking as neurons are lost through the long-term build-up of amyloid plaques (A) and tau tangles (T):

- BVXP started collaborating with the University of Gothenburg (UGOT) during early 2020 to create new antibodies for identifying and monitoring AD…

- ..and H1 2023 then announced UGOT’s first published results of BVXP’s brain-derived tau antibody:

[H1 2023] “We continue to create new antibodies which will be subjected to assay development and validation using clinical samples at the world-renowned laboratory of Kaj Blennow and Henrik Zetterberg at the University of Gothenburg. Using a novel Bioventix antibody, our academic collaborators in Gothenburg have recently published data on a novel assay that detects “brain-derived” Tau in blood (Brain 2022: 00; 1-14).”

- H1 2023 also noted brain-derived tau could be a “useful” indicator of neurodegeneration (N):

[H1 2023] “Brain-derived Tau levels in blood appear to mimic Tau levels in cerebral spinal fluid and could be a useful blood biomarker for neurodegeneration that occurs later in the Alzheimer’s disease pathway.”

- My layman interpretation of the associated UGOT/BVXP scientific paper — “Brain-derived tau: a novel blood-based biomarker for Alzheimer’s disease-type neurodegeneration” (published December 2022) — derived the following conclusions:

- Brain-derived tau in blood seems able to replicate the established AD-identification qualities of spinal-fluid tau, and;

- Unlike alternative indicators of neurodegeneration (such as neurofilament light), brain-derived tau in blood can differentiate between AD and other neurological disorders.

- The associated scientific paper even claimed brain-derived tau could “complete” the ATN framework for AD blood tests:

[BRAIN December 2022] “Brain-derived tau is a new blood-based biomarker that outperforms plasma total-tau and, unlike neurofilament light, shows specificity to Alzheimer’s disease-type neurodegeneration. Thus, brain-derived tau demonstrates potential to complete the AT(N) scheme in blood, and will be useful to evaluate Alzheimer’s disease-dependent neurodegenerative processes for clinical and research purposes.”

- BVXP’s website lists five other scientific papers involving brain-derived tau:

- “Preanalytical stability of plasma/serum brain-derived tau“;

- “Association of Serum Brain-Derived Tau With Clinical Outcome and Longitudinal Change in Patients With Severe Traumatic Brain Injury“;

- “Levels of plasma brain-derived tau and p-tau181 in Alzheimer’s disease and rapidly progressive dementias“;

- “Plasma brain-derived tau is an amyloid associated neurodegeneration biomarker in Alzheimer’s disease“, and;

- “Association of Plasma Brain-Derived Tau With Functional Outcome After Ischemic Stroke“.

- My searching through the PubMed database identified a batch of further scientific papers mentioning ‘brain derived tau’:

- “Safety and immunogenicity of two Tau-targeting active immunotherapies, ACI-35.030 and JACI-35.054, in participants with early Alzheimer’s disease: a phase 1b/2a, multicentre, double-blind, randomised, placebo-controlled study“;

- “The plasma p-tau217/BD-tau ratio improves biomarker short-term variability in memory clinic patients“;

- “Plasma brain-derived tau: analytical and clinical validation of the first commercial immunoassay“;

- “Brain-derived tau to measure treatment effect in Alzheimer’s disease and frontotemporal dementia“;

- “Blood biomarkers for brain injury in chronic subdural hematomas: postoperative dynamics and relation to long-term outcome“;

- “Brain-Derived Tau as an Outcome Marker in Guillain-Barré Syndrome: A Retrospective Cohort Study“;

- “Umbilical cord blood p-tau217 and BD-tau are associated with markers of neonatal hypoxia: a prospective cohort study“;

- “Plasma levels of the neuron damage markers brain-derived tau and glial fibrillary acidic protein in Lyme neuroborreliosis: A longitudinal study“;

- “Plasma N-terminal tau fragment is an amyloid-dependent biomarker in Alzheimer’s disease“;

- “Plasma p-tau217 and neurofilament/p-tau217 ratio in differentiating Alzheimer’s disease from syndromes associated with frontotemporal lobar degeneration“;

- “Clinical value of novel blood-based tau biomarkers in Creutzfeldt-Jakob disease“;

- “Plasma brain-derived tau correlates with cerebral infarct volume“;

- “Neuronal plasma biomarkers in acute ischemic stroke“, and;

- “Plasma Brain-Derived Tau in Prognosis of Large Vessel Occlusion Ischemic Stroke“.

- From what I can tell, all the papers within this further batch either had UGOT involvement or referenced the UGOT/BVXP paper “Brain-derived tau: a novel blood-based biomarker for Alzheimer’s disease-type neurodegeneration“, which I presume means the studies all employed the BVXP brain-derived tau antibody.

- My layman interpretation of this further batch of papers concluded brain-derived tau:

- Has some clinical value assessing the safety of two potential AD treatments;

- Has some clinical value assessing traumatic brain injury, strokes, Creutzfeldt-Jakob disease and Guillain-Barré syndrome, and;

- Does not have obvious clinical value assessing neuroborreliosis and frontotemporal degeneration.

- Probably the most significant paper within this further batch is “The plasma p-tau217/BD-tau ratio improves biomarker short-term variability in memory clinic patients“, which suggests brain-derived tau can improve the accuracy of tests for p-tau217 — a leading biomarker to identify the early stages of AD (see Alzheimer’s R&D: amyloid plaques and p-tau).

- That paper’s conclusion correlates with two papers listed on BVXP’s website:

- …which suggest brain-derived tau can successfully identify patients with a greater risk of neurodegeneration through AD beyond a pure p-tau181/p-tau217 test (see Alzheimer’s R&D: amyloid plaques and p-tau).

- The most concerning paper within this further batch is “Plasma N-terminal tau fragment is an amyloid-dependent biomarker in Alzheimer’s disease“…

- …which was published during January 2025 by a group of Chinese scientists and identified plasma N‐terminal tau as outperforming brain-derived tau when identifying AD-related neurodegeneration:

[Alzheimer’s & Dementia January 2025] “In conclusion, our findings suggest that plasma NT1‐tau is an AD‐specific biomarker that can predict subsequent disease progression as measured with greater tau aggregation and faster Aβ accumulation, brain atrophy, and cognitive decline. Moreover, plasma NT1‐tau appears to outperform plasma brain-derived tau and NfL in detecting Aβ‐associated neurodegeneration, highlighting the probability of plasma NT1‐tau as an AD‐specific neurodegeneration biomarker for disease stage classification and patient screening and monitoring in clinical trials. This study provides novel insights into the role of plasma NT1‐tau in AD pathophysiology.”

- Similar to brain-derived tau, N-terminal tau mixed with p-tau217 can seemingly produce a better test to identify potential early AD. “Plasma p-tau217 and N‐terminal tau (NTA) enhance sensitivity to identify tau PET positivity in amyloid‐β positive individuals” cites:

[Alzheimer’s & Dementia November 2023] “Combining p-tau217 and NTA‐tau resulted in the strongest agreement with the tau PET‐based classification.”

- I am therefore concerned by N-terminal tau appearing to be a genuine challenger to BVXP’s brain-derived tau to identify AD-related neurodegeneration…

- …not least because this H1 confirmed BVXP’s immediate AD progress rested mostly upon two brain-derived tau antibodies:

“The level of research interest at our in vitro diagnostic customers in the field of neurology, initially focusing on Alzheimer’s disease testing continues to increase. Three of the Tau antibodies that Bioventix has created have already moved into full-scale manufacture. Two of these are aimed at brain-derived Tau for neurodegeneration testing and the other is a detector antibody that can pair with Bioventix or other specific antibodies (i.e. p-tau217) as part of customer test designs.”

[gsbmba99 ADVFN October 2025] “I asked Peter [Harrison, BVXP chief executive] about the paper on N-terminal tau earlier this year. Peter said that he had antibodies for N-terminal tau ready to use but that he believed UGOT’s preference remained for BD-Tau. Note that Kaj Blennow from UGOT was a co-author on the Chinese paper so UGOT would certainly be aware of the competing capabilities of the biomarkers. It could be the case that BD-Tau has more interesting additional applications like stroke or traumatic brain injury or staging.”

- True, BVXP does have “antibodies for N-terminal tau ready to use”, but this H1 reiterated BVXP having only a ‘detector’ antibody using N-terminal tau:

- I am therefore not sure whether BVXP has its own version of the N-terminal tau antibody that could be employed as an alternative to brain-derived tau.

- At least the N-terminal tau ‘detector’ antibody implies BVXP is already quite familiar with the AD-indication qualities of N-terminal tau.

- Interestingly enough, N-terminal tau features reasonably prominently on the website of Quanterix (QTRX):

- QTRX is a $275m Nasdaq-quoted manufacturer of “ultrasensitive” immunoassay analysers, which are apparently “up to 1000x” more powerful than conventional analysers:

- QTRX used to promote BVXP’s brain-derived tau at the top of its website:

- But now QTRX simply lists BVXP’s brain-derived tau with all its other assays:

- Board remarks at the 2024 AGM confirmed only “modest” QTRX royalties contributed to the preceding FY’s £155k AD revenue.

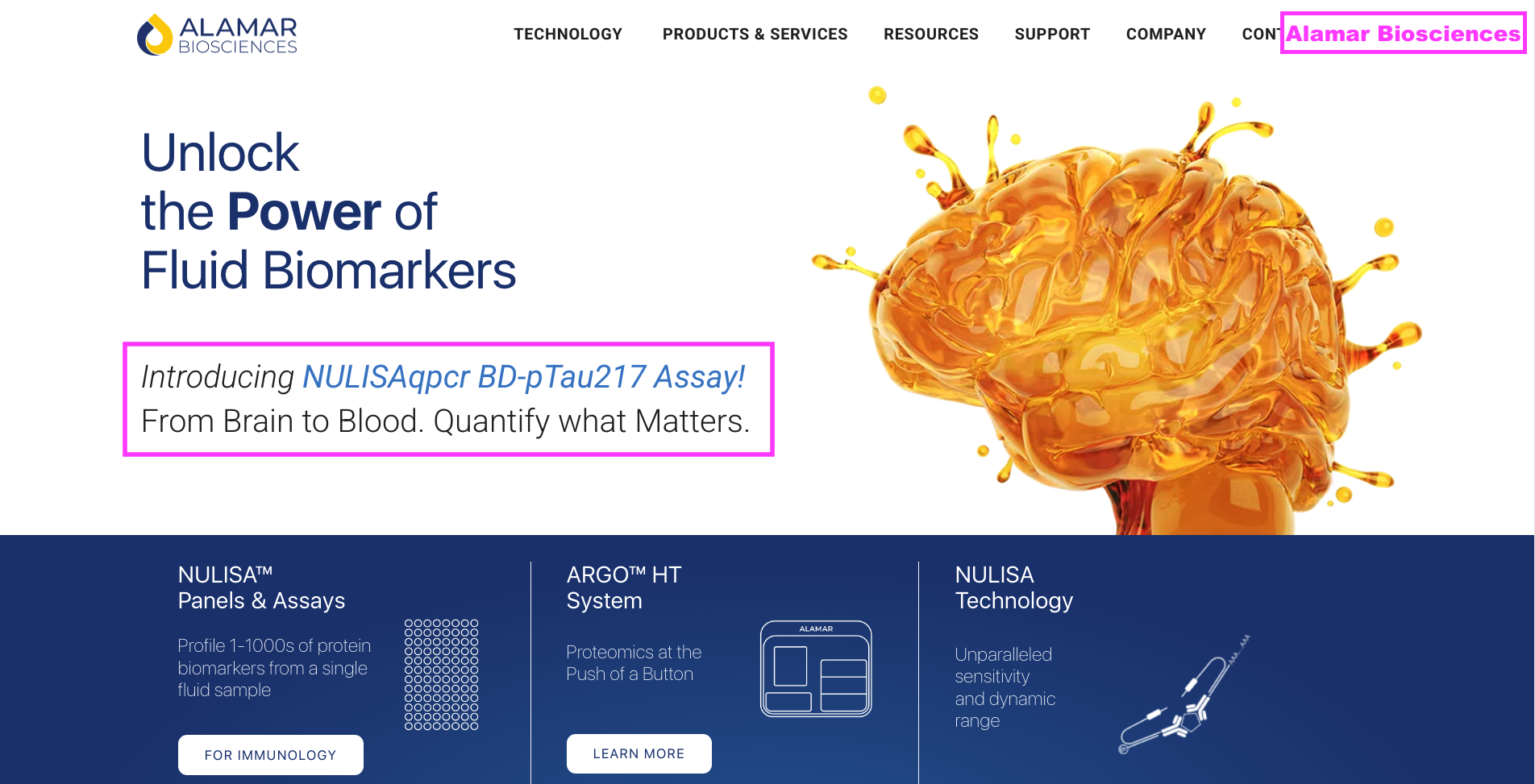

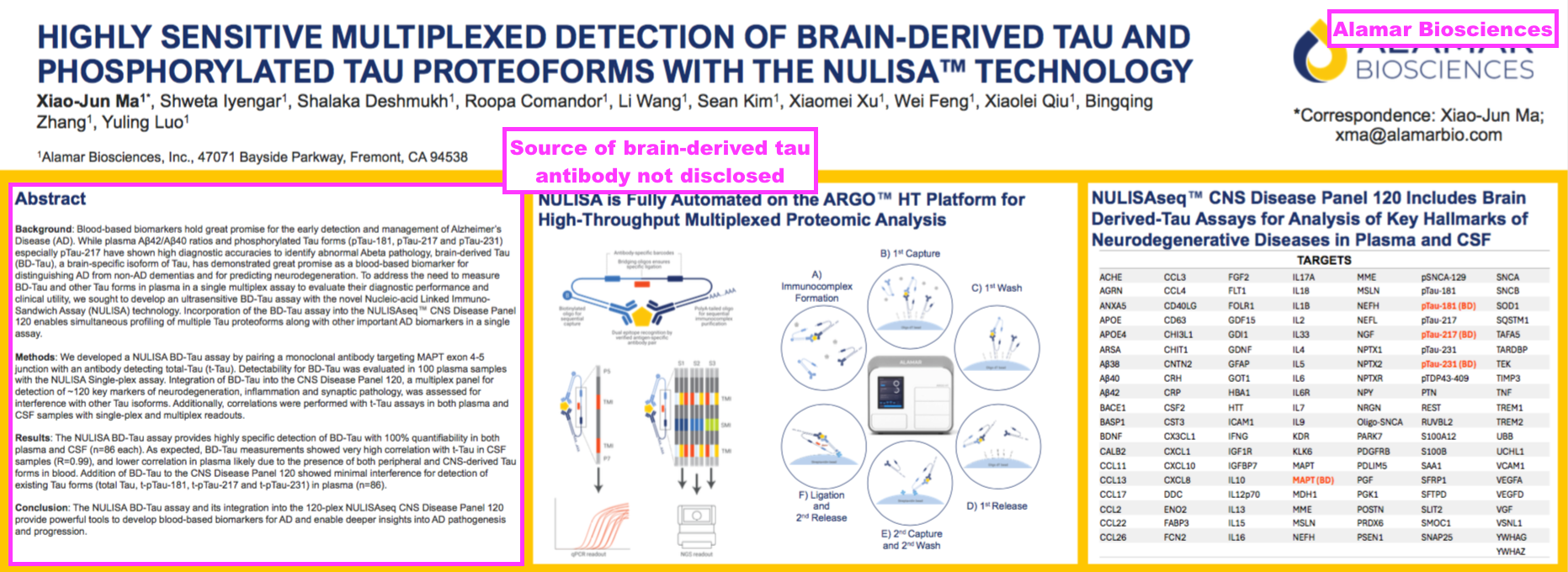

- I speculate whether Alamar Biosciences is now working with BVXP through a brain-derived tau assay.

- Alamar manufacturers a “proteomics platform“, which apparently can assess thousands of proteins simultaneously in just one thousandth of a millilitre of blood:

- Alamar presently appears more excited about brain-derived tau than QTRX. Alamar’s homepage is dominated by the introduction of the NULISAqpcr BD-p-tau217 assay:

- Alamar describes BD-p-tau217 thus:

[Alamar Biosciences October 2025] “BD-p-tau217 is a brain-derived phosphorylated tau protein isoform that serves as a highly specific biomarker for neurodegenerative disease. Tau proteins are distributed throughout the body, but only a fraction found in blood originates from the brain, with the majority secreted by peripheral organs. Elevated levels of BD-p-tau217 in cerebrospinal fluid (CSF) are a hallmark of Alzheimer’s Disease (AD), while increased blood p-tau217—primarily from peripheral sources is associated with other neurodegenerative diseases.”

- This Alzforum article conveys encouraging comments from a trio of AD experts about Alamar’s brain-derived tau assays:

[Alzforum August 2025]

“At this year’s Alzheimer’s Association International Conference, held July 27-31 in Toronto, scientists introduced a plethora of new assays for biomarkers that could improve diagnosis and tracking of AD pathology. Topping the list were immunoassays for brain-derived (BD) phospho-tau isoforms that turn up in plasma.

Data hot off the bench of the lab of Jonathan Schott, University College London, indicated that these tests outperformed those for systemic p-tau fragments in identifying people who have amyloid and tau pathology. “The BD versions are just much better” Schott told a small audience during a product presentation hosted by Alamar Biosciences, Fremont, California. Alamar now include BD p-tau isoforms in its human CNS panel.

…

The data drew praise from people in the field. “Plasma BD-tau isoforms are really important,” Henrik Zetterberg, University of Gothenburg, Mölndal, Sweden, told Alzforum. “We can finally account for peripheral nerve damage that we might see in diabetes or ALS that can drive up plasma p-tau,” he said.

Gil Rabinovici, University of California, San Francisco, expressed similar sentiments. “It is very exciting to have more precise ways to measure protein from the brain rather than picking up proteins in the peripheral pool as well,” he told Alzforum. “This is such a fast-moving field. The blood-based markers are rapidly getting better.”

- …but I speculate the chances of Alamar using BVXP’s brain-derived tau are reasonably good.

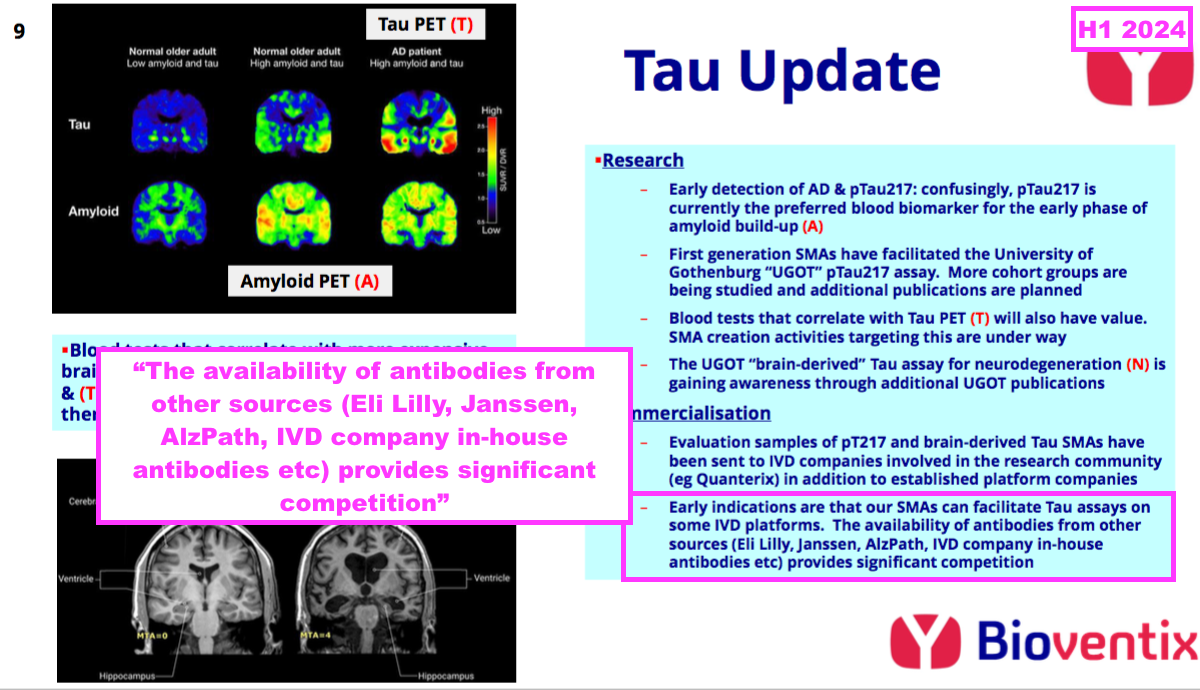

[Beckman Coulter September 2025] “Beckman Coulter Diagnostic… today launched the industry’s first fully automated Brain-derived Tau (BD-Tau) research use only (RUO) immunoassay test.

…

BD-Tau, an isoform of brain-derived tau, is emerging as a highly promising blood-based biomarker for neurodegenerative research… Unlike total tau (t-tau) and phosphorylated tau (p-tau), BD-Tau offers enhanced specificity; by detecting the short form of brain-derived tau directly in the blood, it accurately reflects central nervous system pathology while minimising confounding factors from peripheral tau sources. This makes BD-Tau a more precise and accessible indicator for neurodegeneration than prior tau markers.”

- Beckman is a major manufacturer of IVD machines and its brain-derived tau assays are presently used for research purposes on its “groundbreaking” DxI 9000 immunoassay analyser:

- I speculate Beckman is using BVXP’s brain-derived tau antibodies. Within Beckman’s brain-derived tau documentation, I note a reference to “sheep monoclonal anti-BD-Tau antibody” — and BVXP develops only sheep monoclonal antibodies.

- Note that Beckman’s “groundbreaking” DxI 9000 offers “industry-leading high throughput” of up to 450 tests per hour, which according to ADVFN contributor gsbmba99 may provide an advantage over QTRX and Alamar:

[gsbmba99 ADVFN October 2025] “The Beckman DxI 9000 has a capability of 450 units/hour according to this analysis commissioned by Quanterix. The Beckman machine will do more tests in 2 hours than a Quanterix machine will in a day. I suspect that if testing volumes increase, volumes will eventually shift to the high-throughput platforms that can provide similar sensitivity but vastly higher throughput and away from ultra high precision platforms with limited throughput like Quanterix or Alamar.”

Alzheimer’s R&D: royalties paid to researchers

- Searching the PubMed database reveals ten scientific papers mentioning ‘Bioventix’ beyond those published on BVXP’s website or identified using the aforementioned ‘brain derived tau’ search:

- “Amyloid beta and tau are associated with the dual effect of neuroinflammation on neurodegeneration“;

- “CSF total tau as a proxy of synaptic degeneration“;

- “Plasma biomarkers identify brain ATN abnormalities in a dementia-free population-based cohort“;

- “Plasma biomarkers, brain amyloid pathology, and cortical thickness in a diverse middle-aged community cohort: the HCP-CoBRA study“;

- “Alzheimer’s Association Clinical Practice Guideline on the use of blood-based biomarkers in the diagnostic workup of suspected Alzheimer’s disease within specialised care settings“;

- “Equivalence of Plasma and Serum for Clinical Measurement of p-tau217: Comparative Analyses of Four Blood-Based Assays“;

- “Associations Between Changes in Levels of Phosphorylated Tau and Severity of Cognitive Impairment in Early Alzheimer Disease“;

- “The potential dual role of tau phosphorylation: plasma phosphorylated-tau217 in newborns and Alzheimer’s disease“;

- “Repeated plasma p-tau217 measurements to monitor clinical progression heterogeneity“, and;

- “Plasma p-tau212 as a biomarker of sporadic and Down syndrome Alzheimer’s disease“.

- “Equivalence of Plasma and Serum for Clinical Measurement of p-tau217: Comparative Analyses of Four Blood-Based Assays“ caught the attention of blog reader Gregory.

- Gregory noted the ‘conflicts of interest’ section of that paper contained this intriguing disclosure:

[Journal of Neurochemistry July 2025] “[Thomas K. Karikari] has received royalties from Bioventix for the transfer of specific antibodies and assays to third-party organisations.”

- I did not know BVXP paid royalties to AD researchers. Maybe that partly explains why this H1’s cost of sales surged by the aforementioned 69%.

- Dr Karikari runs his own research lab at the University of Pittsburgh and has employed brain-derived tau within his research:

[The Karikari Lab October 2025] “Notable achievements include the development of the first commercially available plasma p-tau181 assay, which is now widely used, along with immunoassay methods for plasma p-tau212, p-tau217, and p-tau231. Recently, the Karikari Laboratory introduced an innovative plasma brain-derived tau marker, specifically targeting tau protein originating from the central nervous system.“

- Dr Karikari’s website lists all his scientific papers, and the following seven declared the receipt of BVXP royalties:

- “Amyloid beta and tau are associated with the dual effect of neuroinflammation on neurodegeneration“;

- “Associations of 18 F-RO-948 Tau PET with Fluid AD Biomarkers, Centiloid, and Cognition in the Early AD Continuum“;

- “Plasma biomarkers, brain amyloid pathology, and cortical thickness in a diverse middle-aged community cohort: the HCP-CoBRA study“;

- “Plasma brain-derived tau: analytical and clinical validation of the first commercial immunoassay“;

- “Alzheimer’s Association Clinical Practice Guideline on the use of blood-based biomarkers in the diagnostic workup of suspected Alzheimer’s disease within specialised care settings“;

- “Plasma biomarkers identify brain ATN abnormalities in a dementia-free population-based cohort“, and;

- “Equivalence of Plasma and Serum for Clinical Measurement of p-tau217: Comparative Analyses of Four Blood-Based Assays“.

- I am not quite sure whether Dr Karikari’s disclosure of BVXP royalties is entirely accurate for each of those seven papers.

- For example, “Amyloid beta and tau are associated with the dual effect of neuroinflammation on neurodegeneration” refers only to PET and MRI scans and does not incorporate any blood tests — and presumably therefore has no BVXP involvement.

- Five of the other seven papers refer to QTRX, to which BVXP supplies AD antibodies and perhaps indicates a three-way commercial relationship between Dr Karikari, BVXP and QTRX.

- The remaining paper — “Equivalence of Plasma and Serum for Clinical Measurement of p-tau217: Comparative Analyses of Four Blood-Based Assays” — refers to Alamar, and perhaps indicates a three-way commercial relationship between Dr Karikari, BVXP and Alamar.

- My contact form is open for anyone with insight into BVXP paying royalties to AD researchers.

Alzheimer’s R&D: amyloid plaques and p-tau

- I am not convinced BVXP enjoys a favourable R&D position within the amyloid plaques (A) part of the ATN framework.

- To recap, FY 2023 stated:

[FY 2023] “A leading blood biomarker for “A” is a phosphorylated form of tau called p-tau217. A prototype assay from Gothenburg using an SMA has now been established which has performed well with frozen patient samples from a number of different cohorts. The “effect size” (AD patients relative to controls) has been x2-4 which is similar to other leading groups and likely to be clinically useful. The percentage of false positives and false negatives is also relatively modest confirming potential clinical utility.”

- FY 2023 also directed shareholders to this UGOT/BVXP scientific paper about p-tau217: “A novel ultrasensitive assay for plasma p-tau217: performance in individuals with subjective cognitive decline and early Alzheimer’s disease“.

- Detecting the early onset of AD through the build-up of amyloid plaques in the brain can be performed by identifying the presence of phosphorylated tau through epitopes such as p-tau217, p-tau181, p-tau205, p-tau212 and p-tau231.

- According to “Blood phosphorylated tau for the diagnosis of Alzheimer’s disease: a systematic review and meta-analysis“, which was published during September 2025 and analysed 113 different p-tau studies, p-tau217 remains “the highest-performing biomarker for identifying biologically defined Alzheimer’s disease“

- However, BVXP is one of many antibody developers that has worked on a p-tau217 test. The comparable H1 even name-checked a few competitors:

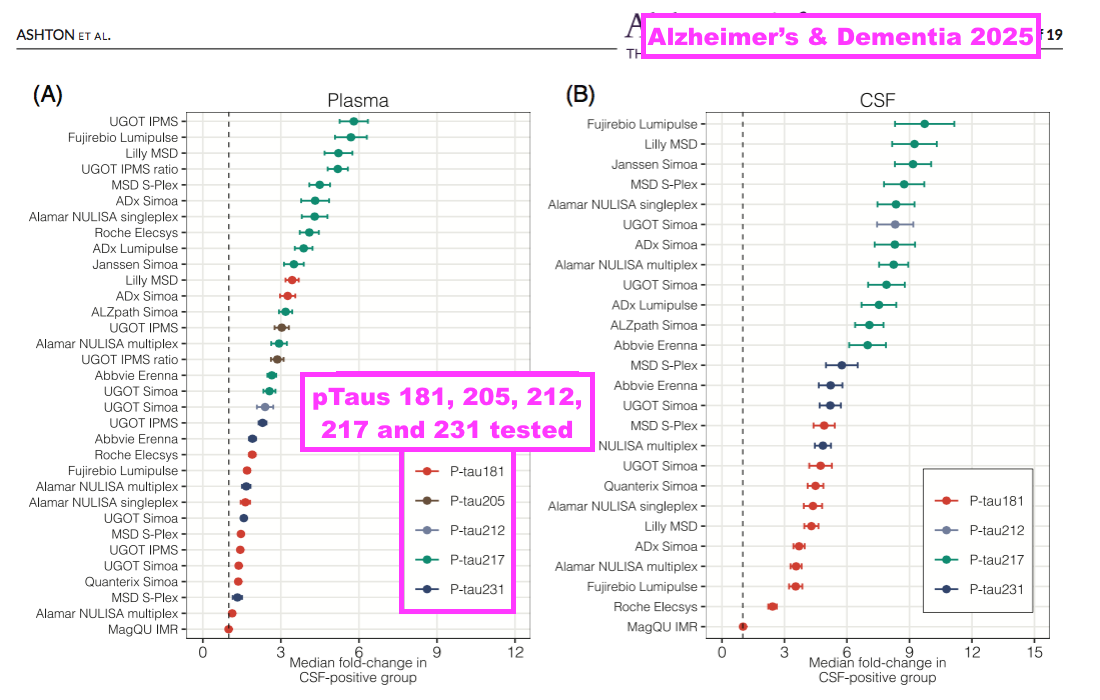

- The scale of the p-tau217 competition is reflected by “Alzheimer’s Association Global Biomarker Standardization Consortium (GBSC) plasma phospho-tau Round Robin study”, which was published during February 2025 and reported the outcome of 31 different p-tau antibody tests.

- Of the 31 different tests, 13 involved p-tau217 and suppliers included Abbvie, ADx, Alamar, ALZpath, Eli Lilly, Fujirebio, Janssen, Meso Scale, Roche and UGOT/BVXP:

- BVXP’s p-tau217 test — now named UGOT p-tau217 — was the first p-tau217 test to be developed for “pure academic interests” and wider research purposes:

[Alzheimer’s & Dementia November 2023] “Even though plasma p-tau217 assays on different platforms from some biotechnology/pharmaceutical companies are expected to become commercially available in the next few months, having an assay developed completely from an academic source removes restrictions such as the need to have the results cleared by the company in question before data can be published. Moreover, the companies tend to select cohorts with clinical and biomarker characterisation that align with their commercial interests, thereby limiting access to these assays. Getting rid of these limitations by providing access to a plasma p-tau217 assay with pure academic interests opens the possibility for assay testing and optimisation in real-life scenarios.”

- “Pure academic interests” implies revenue from UGOT p-tau217 will not be significant for BVXP.

- Board remarks at the 2024 AGM provided additional p-tau217 insight. Attendees were told:

- “We are well behind a company called ALZpath“;

- Any p-tau217 revenue is likely to be “modest“, and;

- “One or two” customers have concluded p-tau217 testing, and BVXP has not been included in their final selection (“Some ships have already sailed… We were too late to get in“).

- Management comments during a ShareSoc seminar last year confirmed ALZpath leads the p-tau217 field:

[BVXP seminar November 2024]“There’s competition from people that have been in the field longer than we have. There’s a company called ALZPath, who have got a really good p-tau217 antibody that’s really difficult to compete with.”

- The aforementioned study of 31 p-tau tests provided some encouragement about BVXP’s brain-derived tau:

[Alzheimer’s & Dementia February 2025]

“Caution must be taken not to over interpret the meaning of absolute values of plasma p-tau. Peripheral factors may also come into play in increased plasma p-tau levels, and unexpectedly high plasma p-tau values can also be observed in a single timepoint in healthy individuals followed over several weeks and in N-terminal assay designs. Other more brain-specific tau biomarkers such as brain-derived tau (BD-tau) or assays that are more reflective of tau pathology may provide further information in this context.”

- The text suggested combining tests for p-tau217 and brain-derived tau provided a more accurate assessment of the patient’s AD status.

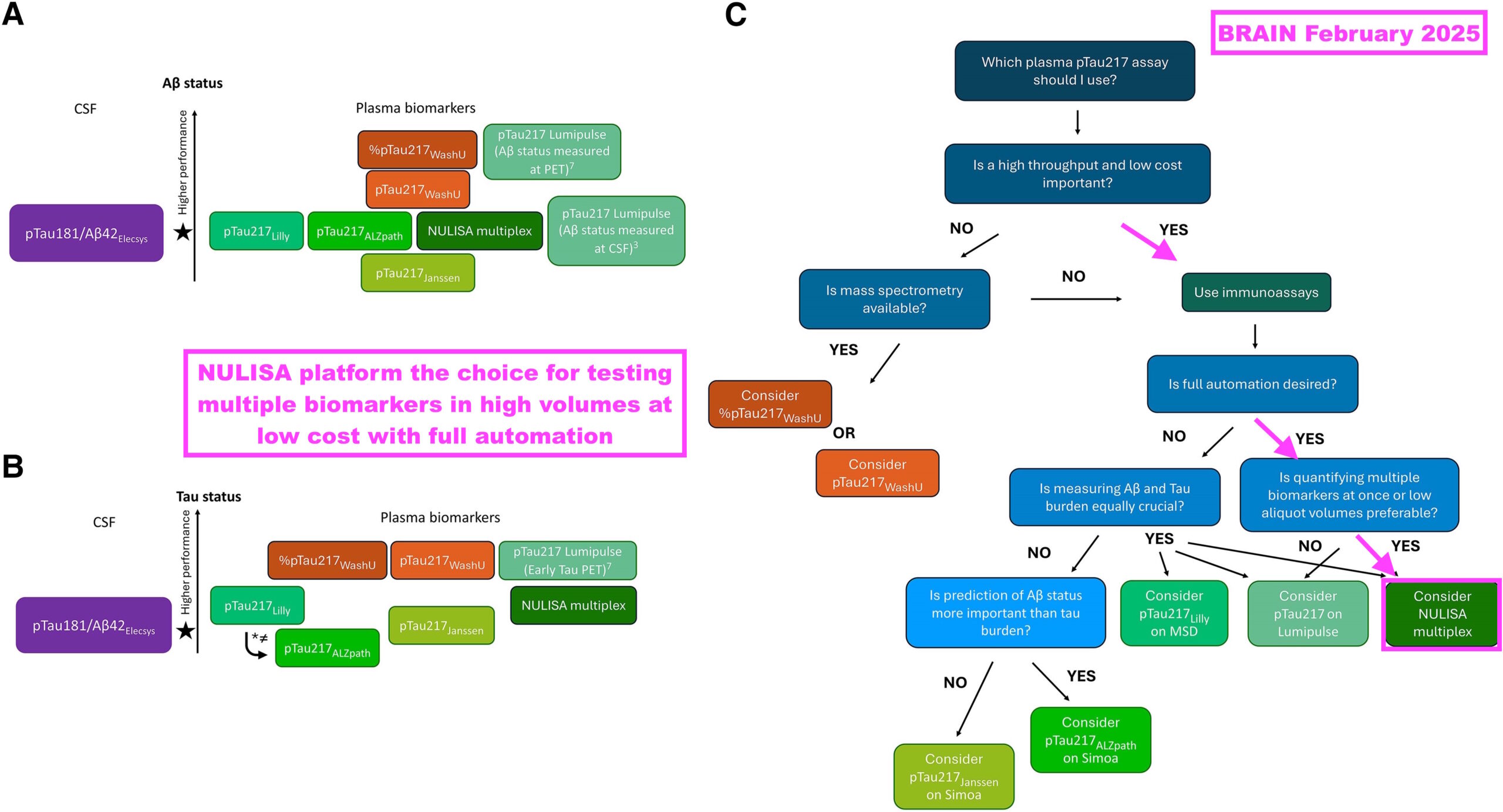

- “Which plasma p-tau217 assay should I use in clinical practice? Pandora’s box demystified” was published during February 2025 and summarised not just the efficacy of several p-tau217 assays, but also the practicalities of each assay within an actual clinical setting:

[BRAIN February 2025] “If blood-based biomarkers are to live up to their promise of being a more equitable form of screening for Alzheimer’s disease, then prioritising mass spectrometry-based assays might not necessarily be the right call. The reality is that such assays require expensive instruments and highly trained personnel and can achieve only a relatively low throughput. These assays might not therefore be the weapon of change this biomarker revolution requires.

Immunoassays offer a cheaper and more scalable alternative to mass spectrometry. The MSD and SIMOA platforms have been used extensively in Alzheimer’s disease research due to their lower costs and high sample processing capacity. While not (yet) as widespread, one of the newest kids on the block—the NULISA platform—has shown great promise with its fully automated pipeline, ability to analyse multiple biomarkers at the same time, high sensitivity (attomolar) and low aliquot volume needed for analysis.“

- The research included a simple decision tree that highlighted Alamar’s NULISA platform and its p-tau217 assay as the most suitable for high-volume, lower-cost testing:

- Not many p-tau217 tests have actually been approved for clinical diagnostic usage.

- C2N Diagnostics received permission during February 2025 to market its p-tau217 test for clinical purposes within the UK, while Fujirebio received permission during May 2025 to market a p-tau217 test for clinical purposes within the United States.

- I speculate BVXP’s only commercial involvement with p-tau217 could be through the aforementioned N-terminal tau ‘detector’ antibody, which could be paired with a third-party p-tau217 antibody:

- This H1 said the N-terminal tau ‘detector’ antibody had moved into “full-scale manufacturer“:

“Three of the Tau antibodies that Bioventix has created have already moved into full-scale manufacture. Two of these are aimed at brain-derived Tau for neurodegeneration testing and the other is a detector antibody that can pair with Bioventix or other specific antibodies (i.e. p-tau217) as part of customer test designs.“

- “Full-scale manufacture” implies BVXP’s ‘detector’ antibody will be produced in significant volumes…

- ..and I speculate significant volumes are likely to mean a tie-up with a popular p-tau217 test.

- I maintain BVXP has gained a scientific edge with p-tau212 and Down Syndrome, a condition that eventually develops AD.

- Searching for p-tau212 on the PubMed database still reveals only two scientific papers — both of which were co-authored by BVXP and employed BVXP-developed antibodies:

Alzheimer’s R&D: tau tangles

- BVXP’s present R&D position within the tau-tangle (T) part of the ATN framework is hard to determine.

- This H1 said a “growing panel” of antibodies had been created to mimic the tau-tangle results of Tau PET scans:

“In addition to those Tau antibodies already created and in manufacture described above, we have a growing panel of new Tau antibodies aimed at assays that could correlate with the results of Tau PET brain scans. Such assays are recognised by our customers as having value in the future as the scope of neurological blood testing expands. As with previous antibodies, the validation of our new antibodies will be carried out at the University of Gothenburg.“

- This H1 also revealed “early” tau-tangle antibodies had now been supplied to customers:

- This H1 appeared to show progress versus earlier tau-tangle commentary. Management remarks during a ShareSoc seminar last year for example were quite vague on the company’s tau-tangle R&D:

[BVXP seminar November 2024] “We haven’t quite worked out with our esteemed friends in Gothenburg exactly if any of the targets that we’re going for in this MTBR [microtubule-binding region] are of use. And that’s going to be ongoing. I can see us working on Tau well into next year, probably towards the end of next year.”

- Board remarks at the 2024 AGM were similarly vague. Attendees were told “no one’s quite sure what will work out” and the first news would come from UGOT, possibly during 2025.

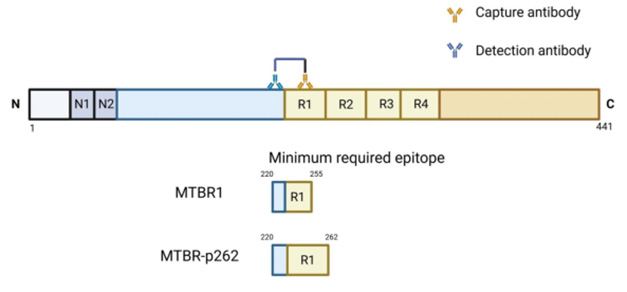

- News of sorts from UGOT has emerged this year about tau-tangles and MTBR epitopes. Alzforum reports:

[Alzforum August 2025] “Clinics may soon be able to detect these MTBR fragments on commercial immunoassay platforms. At AAIC in Toronto last month, scientists led by Kaj Blennowat the University of Gothenburg, Mölndal, Sweden, introduced two new immunoassays for MTBR, dubbed MTBR1 and MTBR-p262. The latter only binds to fragments containing a phospho group on amino acid 262.

Both assays detect fragments containing an epitope in the first microtubule-binding repeat. Both seem to track with tau pathology. For now, the assays work well for cerebrospinal fluid. Blennow told Alzforum he hopes to get them working in plasma, adding that several companies are interested in developing them commercially.”

- The Alzforum article also referred to BVXP:

[Alzforum August 2025] “To this end, Fernando Gonzalez-Ortiz in Blennow’s lab collaborated with scientists at Bioventix. This biotech company in Farnham, England, specialises in generating sheep antibodies for diagnostics. Companies then license its antibodies to create assays on their respective diagnostic platforms. Besides having generated an antibody that recognises isoforms of tau only made in the brain, Bioventix generated antibodies that cover many regions of tau, including those that span the MTBR.“

- For now at least, UGOT/BVXP’s MTBR tau-tangle prototypes work using only spinal fluid rather than blood. The MTBR1 assay also detects Creutzfeldt-Jacob disease, which may indicate that test is best suited for identifying neurodegeneration rather than tau tangles. The MTBR-p262 assay meanwhile requires further studies to determine its tau-tangle qualities.

- The Alzforum article compares UGOT/BVXP’s tau-tangle work to that of eMTBR-tau243 developed by Washington University in St Louis.

[Alzforum August 2025] “Previous work from Kanta Horie and colleagues at Washington University, St. Louis, indicated that MTBR-243 in the CSF, and eMTBR-tau243, a fragment of the MTBR region that can be detected in plasma, are better markers for tangles than any of the various phospho-tau fragments, which begin to climb in blood before tau PET scans turn positive. In Toronto, these scientists reported that eMTBR-243 specifically recognises tangles containing a mixture of three-repeat and four-repeat tau isoforms, such as those found in AD and chronic traumatic encephalopathy.”

- The eMTBR-tau243 work was spotlighted by “Plasma MTBR-tau243 biomarker identifies tau tangle pathology in Alzheimer’s disease“, which was published during March 2025 and claims eMTBR-243 is “more strongly associated” with tau tangles than other epitopes:

[Nature March 2025] “We developed a new blood biomarker, plasma eMTBR-tau243, that is more strongly associated with, and more specific to, the tau tangle pathology of AD than other established AD plasma biomarkers including %p-tau217. Furthermore, plasma eMTBR-tau243 had a significantly stronger correlation with brain atrophy and cognitive measures than %p-tau217 and %p-tau205, which indicates its potential utility for stage of clinical diagnosis and clinical trials. For example, plasma eMTBR-tau243 could potentially serve as an alternative to tau-PET for monitoring tau pathology in clinical trials and could improve diagnostic and prognostic accuracy in clinical practice.”

- Further work on eMTBR-tau243 is still required. Downsides to the MTBR-tau243 assay include the requirement for a “relatively large volume of plasma (1.5 ml)” and its development using mass spectrometry that could limit high-volume testing.

- Searching for MTBR-tau on the PubMed database reveals no major tau-tangle progress with MTBR-tau other than eMTBR-tau243.

Other R&D

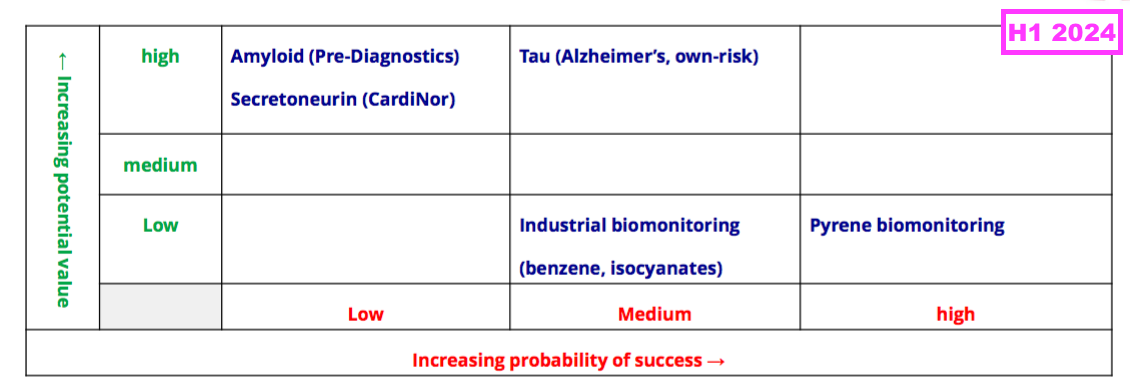

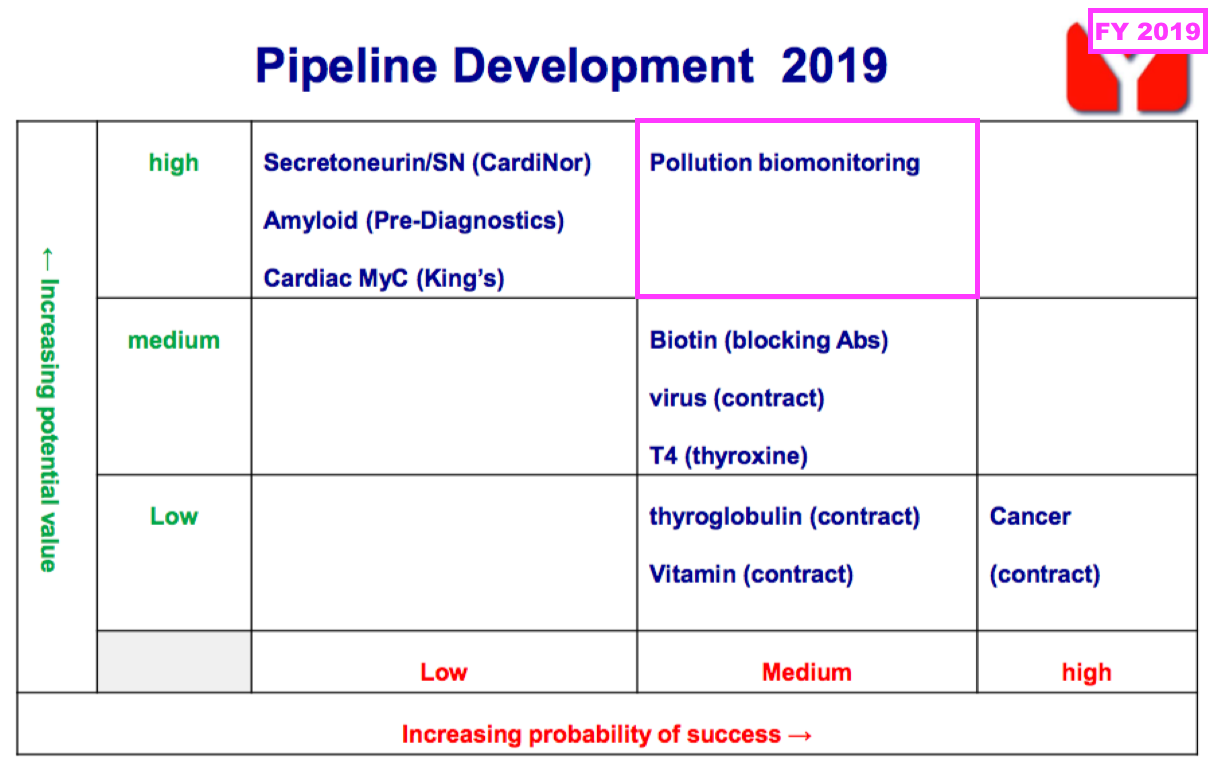

- The commercial potential of BVXP’s other R&D efforts appear increasingly immaterial versus the AD work.

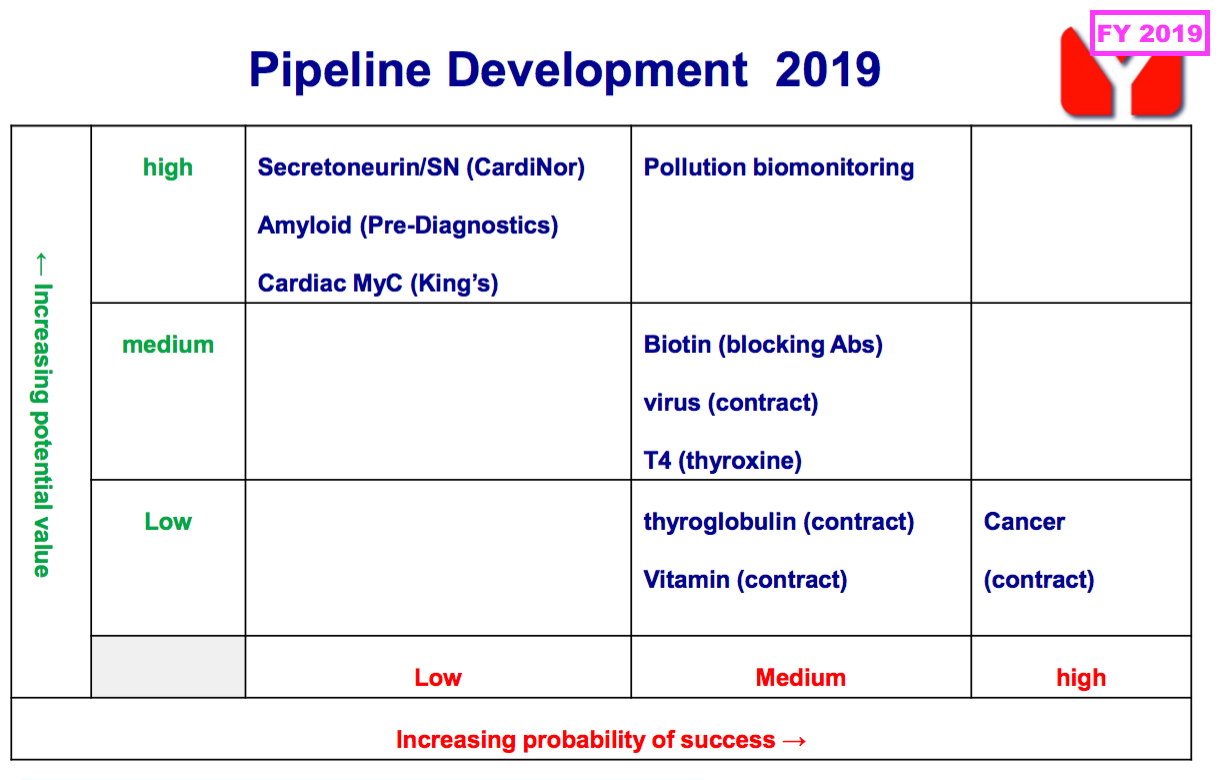

- Note the comparable H1’s pipeline grid that outlined the company’s research projects and their chances of success…

- …was absent for the preceding FY and did not return for this H1.

- BVXP’s other R&D efforts consist of:

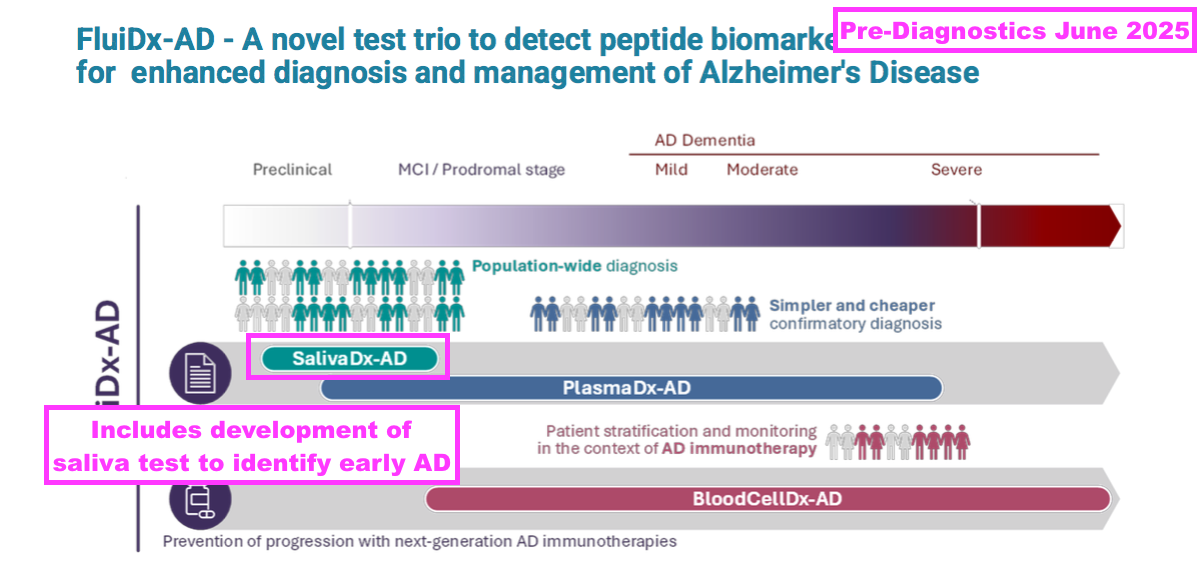

- An investment in Norwegian blood-test research firm Pre-Diagnostics;

- Three industrial-biomonitoring projects, and;

- A water-quality project:

- Pre-Diagnostics is studying the side effects of AD treatments and encouragingly updated investors during June with the following “important milestones going forward“:

[Pre-Diagnostics June 2025]

• ARIA data to be presented for industrial partners (2025)

• Proof-of-concept for saliva as screening test AD (2026)

• Optimisation AD-tests (EU-project tech part) (2025/26)

• Parkinson test proof-of-concept (2025)

• Commercial service lab (fluid samples, dementia) (2025)

• Clinical validation in EU project (FluiDx-AD) (2026/27)

• Partnering/license agreement, ARIA test (2026/27)“

- Pre-Diagnostics targeting a “partnering/licensing agreement” by 2026/2027 appears promising, but the same management team was expecting a licensing agreement by 2025 two years ago:

[Pre-Diagnostics August 2023] “In 2022 Pre Diagnostics was selected as a client by a top-tier global financial services firm, highly specialised in Diagnostics and Device. The management team is aiming at a licensing agreement by 2025, which also could create a basis for stock-listing or trade sale of shares.”

- Pre-Diagnostics won an €8m EU grant last year to work on FluiDx-AD — a trio of research projects that includes testing for early AD through saliva:

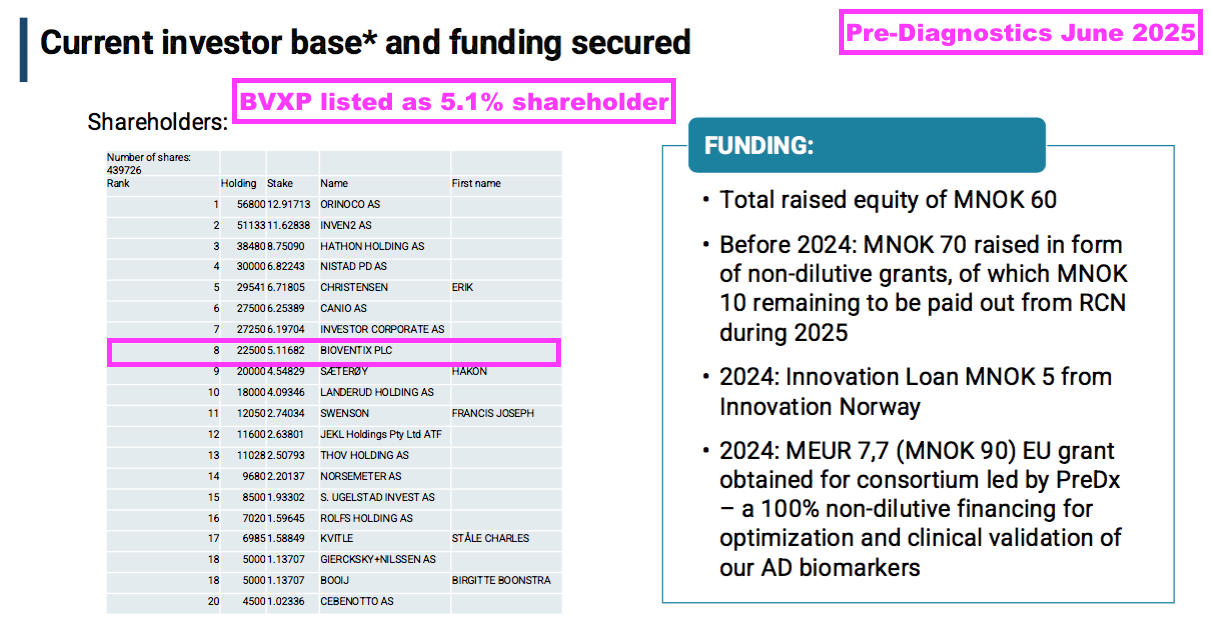

- The same presentation confirmed BVXP is a 5.1% Pre-Diagnostics shareholder:

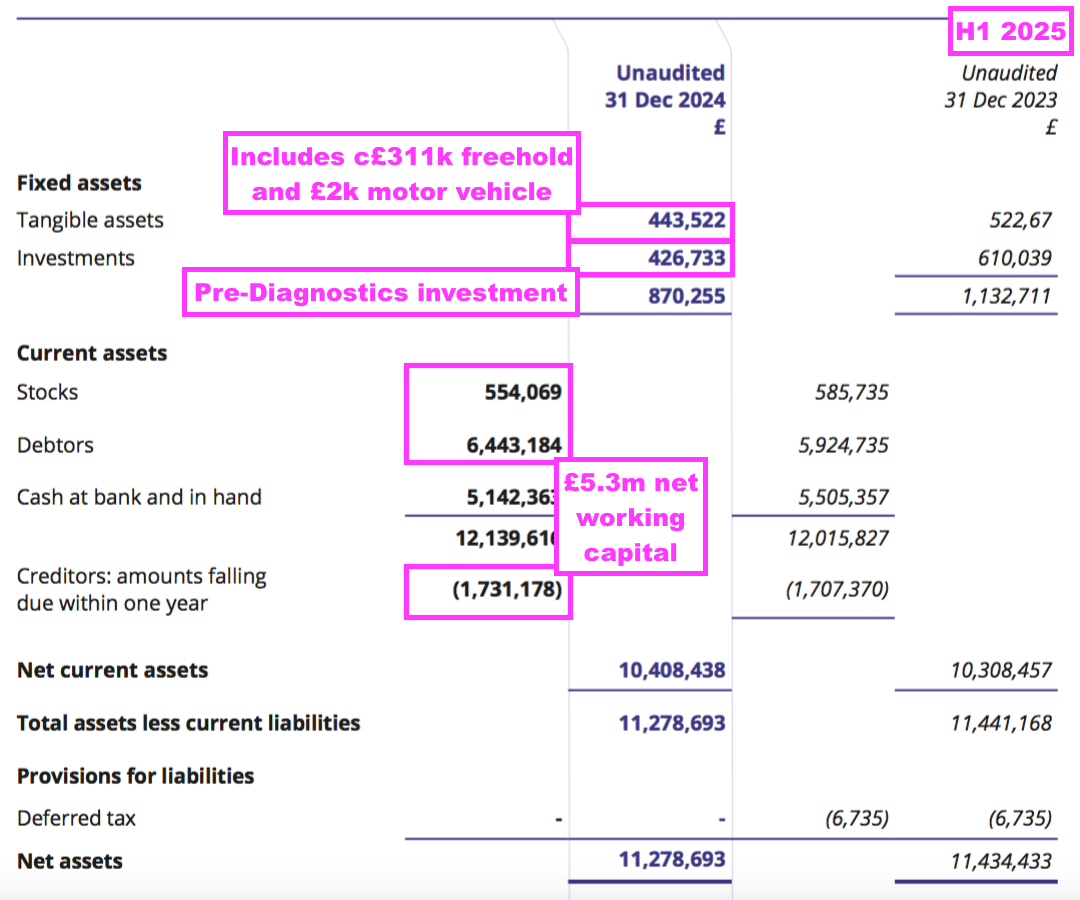

- This H1 showed BVXP’s Pre-Diagnostics investment still valued at its £427k cost. I don’t know whether Pre-Diagnostics has raised further equity following BVXP’s investment.

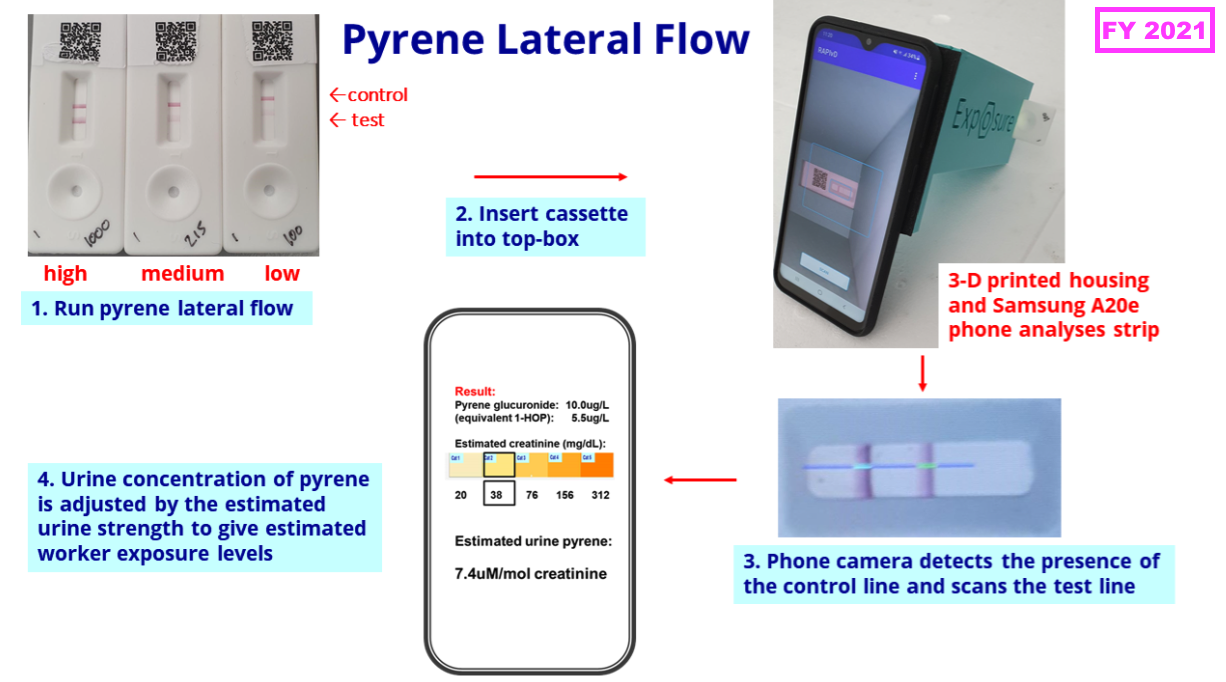

- FY 2019 first disclosed the company’s industrial-biomonitoring R&D:

- FY 2021 then outlined the kit required for an industrial-biomonitoring test:

- This H1 confirmed the first biomonitoring project was still to conduct a firefighter trial after seemingly attracting no commercial interest from industrial employers:

“We are pleased with the continued development of our industrial pollution exposure assays. We are planning a field trial with firefighters using our prototype lateral flow test for pyrene, previously trialled in industrial workers’ urine.“

- The second and third biomonitoring projects remain in a development phase:

“Antibody developments are in progress for two additional industrial pollutants, benzene (associated with the petrochemical industry) and isocyanates (used in the plastics and paints industry). We plan to continue our internal and external investment in these areas. “

- Whether any of the three biomonitoring tests — for pyrene, benzene and isocyanates — ever become commercial remains to be seen.

- For perspective, BVXP’s AD work commenced after the start of the biomonitoring work, yet earned revenue of £155k during the preceding FY.

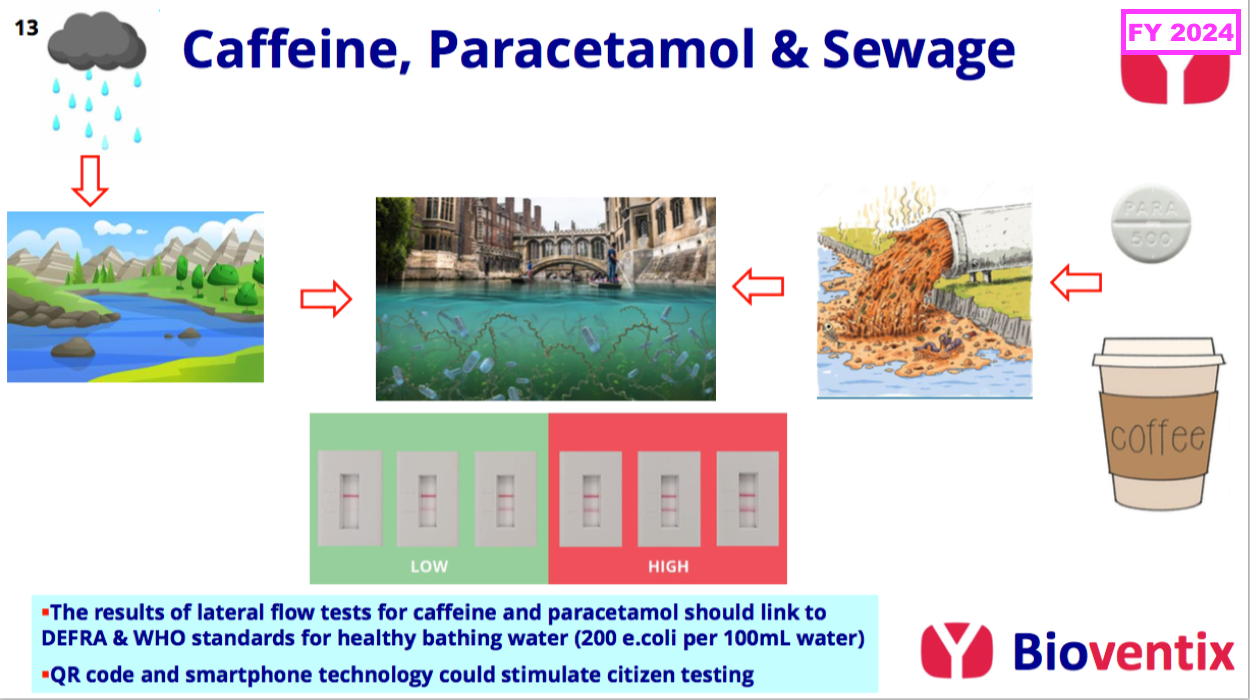

- The preceding FY announced a new water-quality project that will “harness [BVXP’s] experience with ‘sandwich’ antibodies, lateral-flow systems, together with phone-app technology, to facilitate rapid riverside tests”:

- This H1 revealed water-quality field trials could occur during the second half of 2025:

“The water quality project mentioned in […] November 2024 continues to progress. This project is based on the riverbank measurement of both caffeine and paracetamol, either individually or in combination, as markers of human-derived by-products in “fresh water”. Laboratory based tests and lateral ow devices are in development and we anticipate that field trials will be possible during the second half of 2025.”

- Note the preceding FY admitted the biomonitoring and water-quality projects incurred external expenditure of approximately £200k:

[FY 2024] “The industrial biomonitoring and water pollution projects have required significant external expenditure during the year of approximately £200k. As we develop the projects, we expect this expenditure to continue and grow modestly into the future. Using our cash resources to support the steady internal organic growth of our business has been a consistent feature of our strategy.”

- For perspective, approximately £200k was equivalent to more than 20% of the preceding FY’s cost of sales of £927k.

- An unfavourable theme of BVXP’s biomonitoring and water-quality projects is that no in-house blood-test work is involved.

- Such in-house blood-test R&D led to vitamin D transforming the company’s progress ten years ago…

- …and perhaps will lead to the aforementioned AD antibodies transforming the company’s progress during the next ten years.

- Management comments during a ShareSoc seminar last year included some rather alarming references to the relative competitiveness of BVXP’s research technology:

[BVXP seminar March 2024] “Reverse engineering is increasingly easy. But also, while we have been around for 20 years, antibody technology has raced ahead.

Twenty years ago, I think our technology was quite special, but I think that’s less so now.

There is a lot more antibody technology competition full stop. I think the ability of people not just to copy our antibodies, but to make ones better than our older antibodies, is much more the reality of being in 2024.

What protects our historic business is that it’s still a bit of an annoyance, or more than that, for someone to change an antibody, even if it’s a bit better… Because this [industry] is regulated, switching antibodies is something that people would reluctantly do.

So I think our historic business is quite well protected through this immense inertia of continual use.

For the future and new projects like Tau and Alzheimer’s, that’s a bit more of a blank sheet of paper. And we’re going into bat making antibodies for Tau against people with 2024 technology. And we’re still a little bit 1980s.

But we do things to improve and compete as best we can. Competition is an issue, particularly for new projects.”

- I speculate the absence of in-house blood-test R&D beyond AD may be due to the company utilising antiquated antibody technology.

- Certainly BVXP’s capex — just £19k during this H1 — does not suggest the company is continually revamping its equipment to stay competitive (see Financials: balance sheet and cash flow).

- That earlier pipeline grid from FY 2019 still provides a sobering view on BVXP’s R&D:

- Six years on, and nothing on that grid (including the biotin ‘blockers’) has since become an obvious money-spinner.

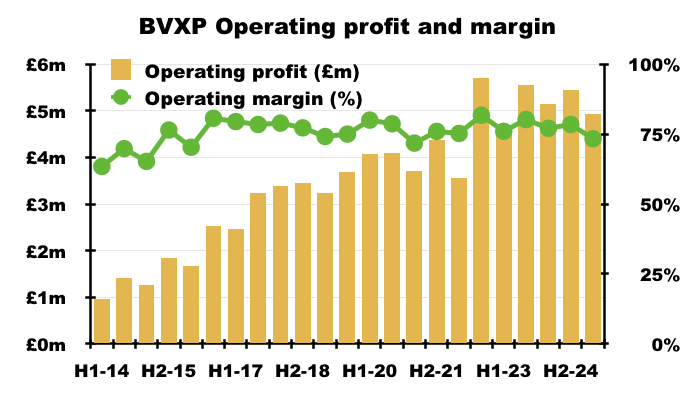

Financials: margin and employees

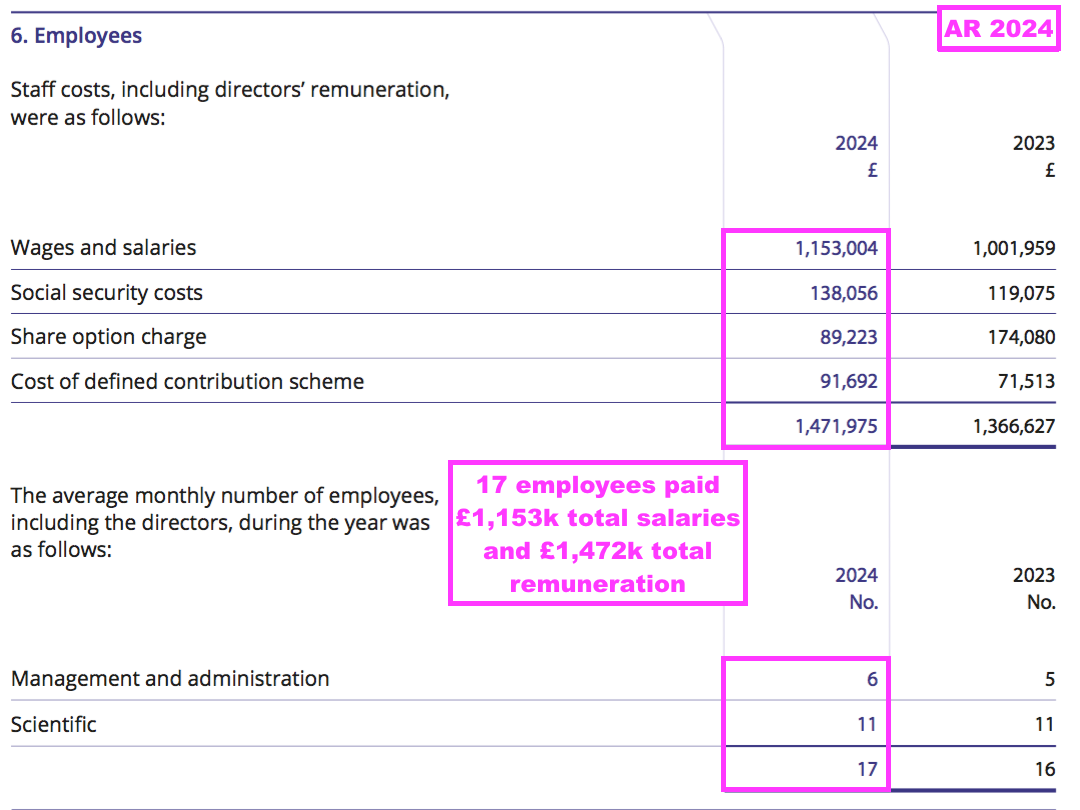

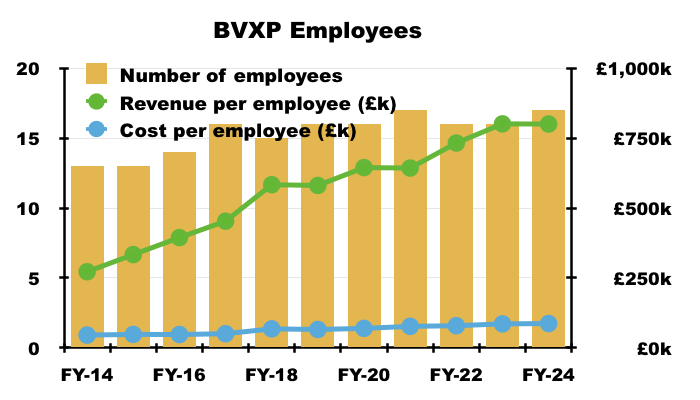

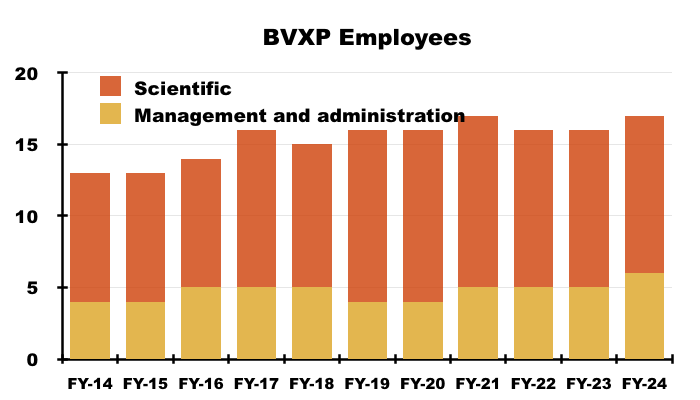

- Revenue earned from regular worldwide blood tests using antibodies developed by only 17 employees continues to translate into some wonderful accounts.

- Despite the aforementioned greater cost of sales, this H1 still enjoyed a terrific 73% operating margin:

- Administrative expenses advanced at a slightly faster pace than revenue (3% versus 1%):

- BVXP’s largest cost continues to be its workforce, which typically represents approximately 50% of total expenses. H1 administration expenses up 3% therefore reflects the muted FY 2025 salary increases reported by the preceding FY:

[FY 2024] “In June 2024 the Remuneration Committee recommended in inflationary increases of up to 5% for the Company’s employees, including the directors; these increases were implemented on 1 July 2024.“

- Note that the preceding FY witnessed employee salaries advance a hefty 15% versus revenue gaining only 6%: