28 September 2025

By Maynard Paton

H1 2025 results summary for FW Thorpe (TFW):

- As predicted, a “marginally ahead” H1 performance that reported revenue up 1%, profit up 2% and the dividend up 3.5% following mixed progress within the group’s divisions.

- After a few subdued years, Zemper was this H1’s welcome highlight — the Spanish subsidiary reported revenue up 13% and profit up 65% to reflect the initial promise expected from the significant c£35m purchase cost.

- Elsewhere, Thorlux was held back by SchahlLED, the Dutch businesses could not repeat their bumper efforts from last year while Ratio suffered increased losses that prompted the joint venture to undertake a debt-for-equity swap.

- The accounts remain in very good shape, showing an acceptable 15% group margin, healthy £52m net cash, commendable stock control, a favourable tax charge and yet another small gain from selling surplus assets above book value.

- Management remarks of undertaking buybacks if the shares “significantly undervalue” the group’s prospects are intriguing, given the 300p price was first achieved during 2016 and might be overlooking TFW’s distinguished operating history. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux and SchahlLED

- Netherlands

- Zemper

- Ratio Electric

- Other companies

- Financials

- Boardroom

- Valuation

News link, share data and disclosure

- Share price: 300p

- Share count: 118,935,590

- Market capitalisation: £357m

- Disclosure: Maynard owns shares in FW Thorpe. This blog post contains ShareScope affiliate links.

Why I own TFW

- Develops professional lighting systems with a long-established reputation for high product quality, leading technical innovation, first-class service and sustainable manufacturing processes.

- Management overseen by family non-execs who boast decades of board experience, steward a 43%/£153m shareholding and occasionally favour special payouts.

- Conservative accounts display healthy operating margins, substantial cash reserves, impressive working-capital management and illustrious rising dividend.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary

Revenue, profit and dividend

- This H1 was never going to overwhelm after the preceding FY supplied a “modest growth” outlook…

[FY 2024] “Consolidated as a whole, the outlook is positive with modest growth expectations.”

- …and the 2024 AGM said this H1 would be “marginally ahead” of the comparable H1:

[AGM 2024] “Since the beginning of the new financial year, orders and revenue are modestly ahead of the same period last year, with the usual ‘ebb and flow’ across the Group. The Board expects half‐year results to be marginally ahead of last year.“

- This H1 was indeed “marginally ahead” of the comparable H1.

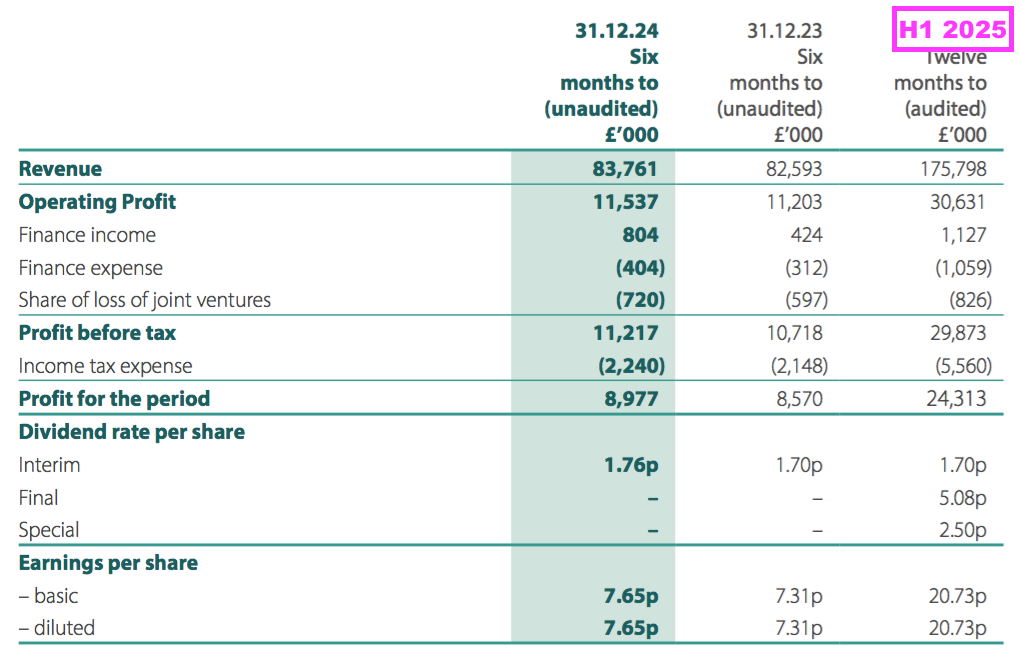

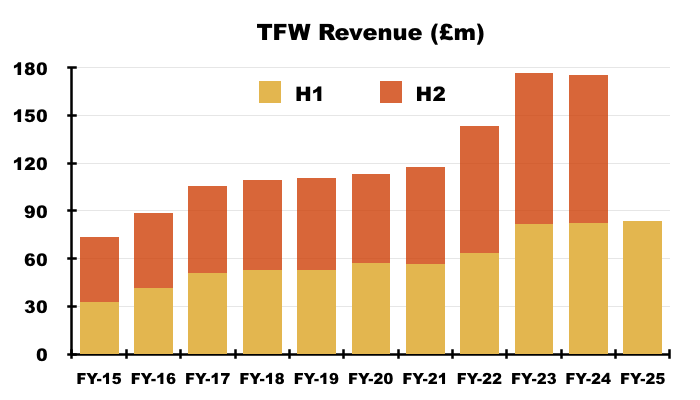

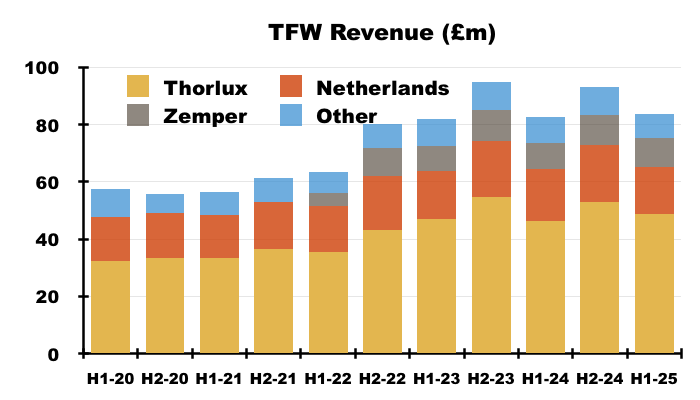

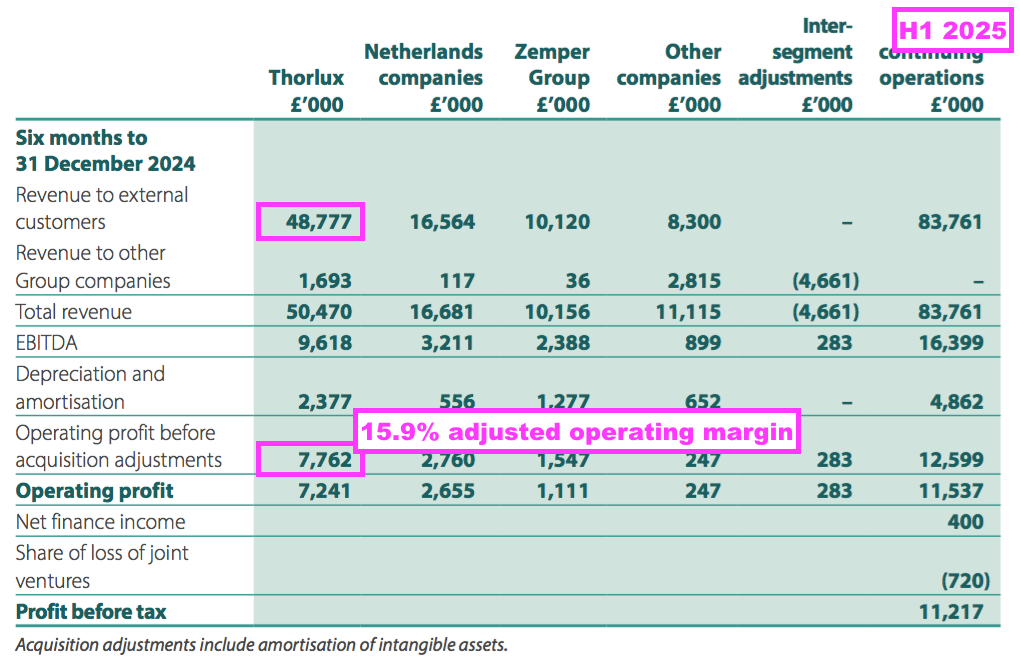

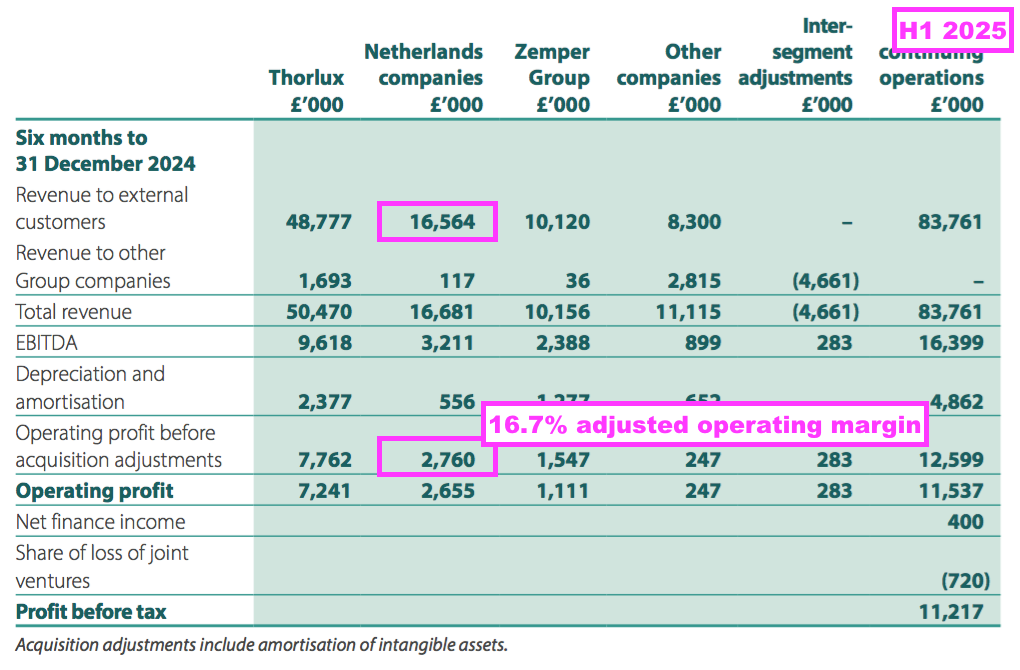

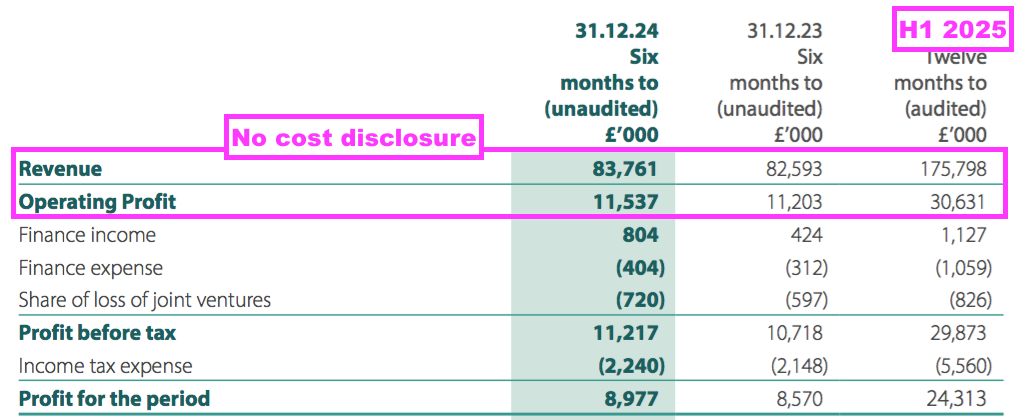

- H1 revenue inched 1% higher to £84m and set a new H1 record:

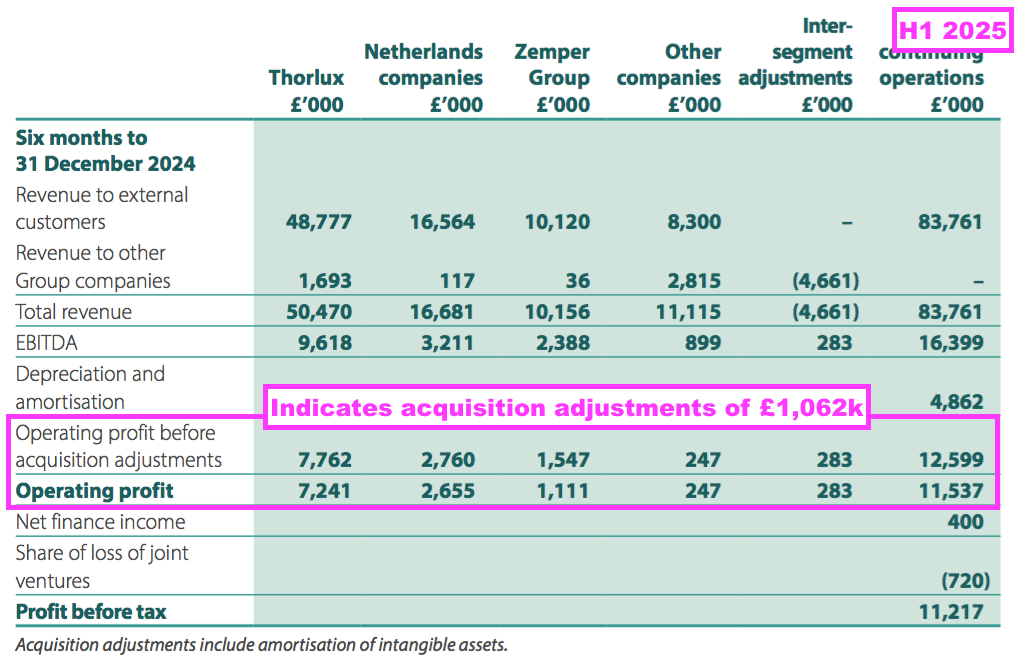

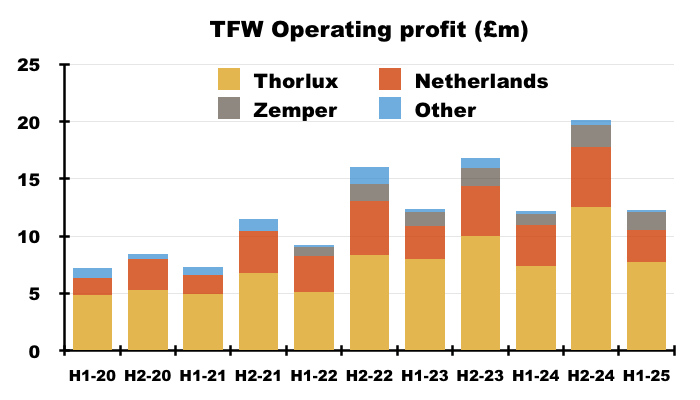

- TFW’s statutory operating profit includes the amortisation of acquired intangibles as well as changes to acquisition earn-out provisions:

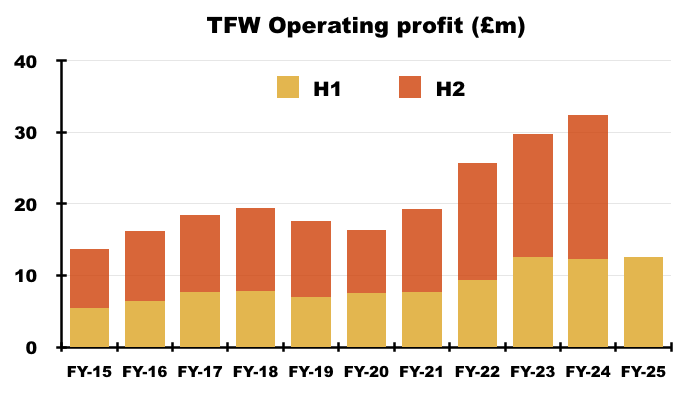

- Adjusting for these acquisition-related items, H1 operating profit gained 2% to set a new £12.6m H1 record (by just £39k):

- Note that this H1’s operating profit appeared suppressed by a sizeable £1.8m foreign-exchange loss revealed within the cash flow statement (see Financials).

- Divisional performances were mixed.

- Thorlux and Zemper were said to have traded “positively“, Lightronics was “unable to match the record figures” of the comparable H1, SchahlLED suffered from the “ongoing recession in Germany” while the group’s collection of Other subsidiaries remain a sideshow:

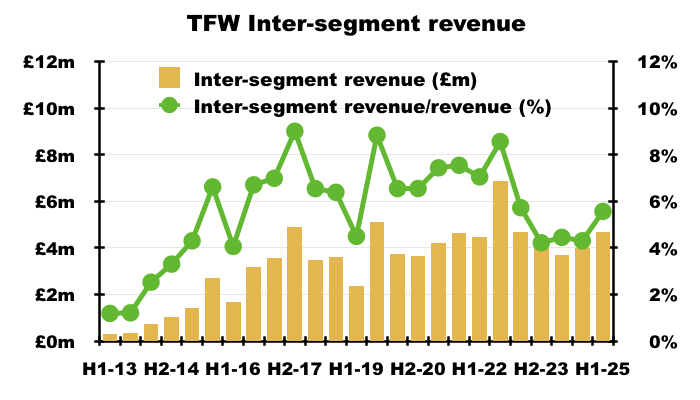

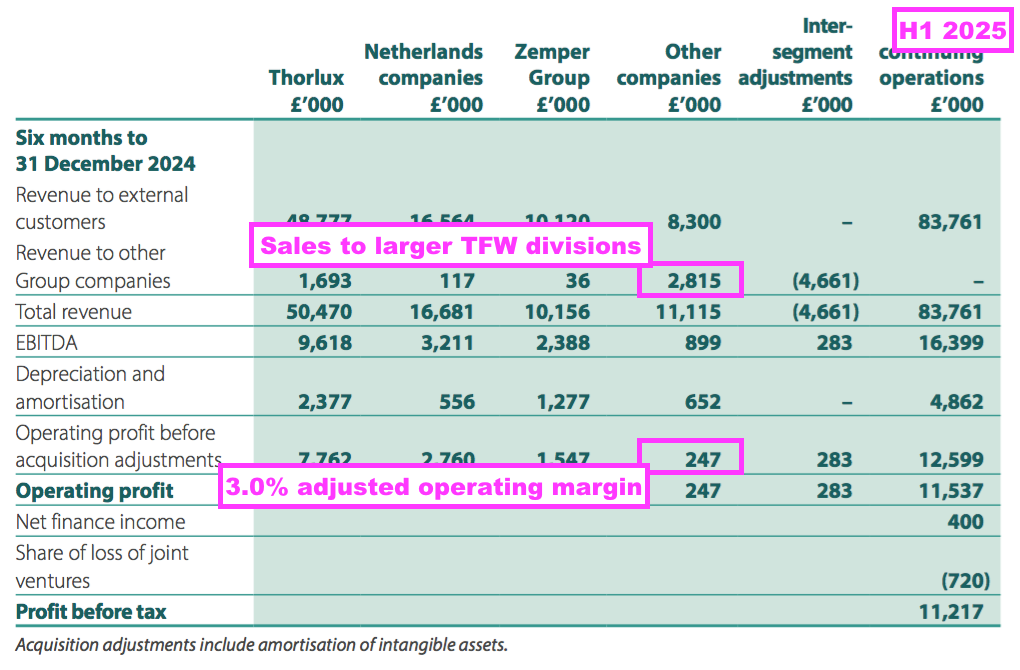

- This H1 appeared to witness improved co-operation between TFW’s various divisions. H1 inter-segmental revenue — representing revenue from products sold by one division to another — was £4.7m, the highest amount since H1 2023 (see Other companies):

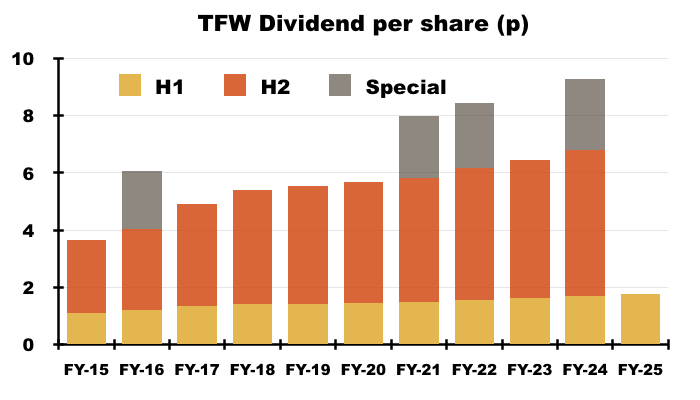

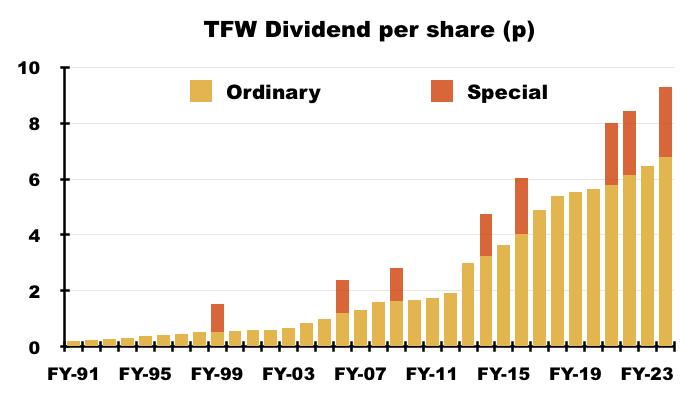

- The H1 dividend was lifted 3.5%:

- The ordinary dividend looks on course for its 23rd consecutive annual increase and has not been cut since at least 1991:

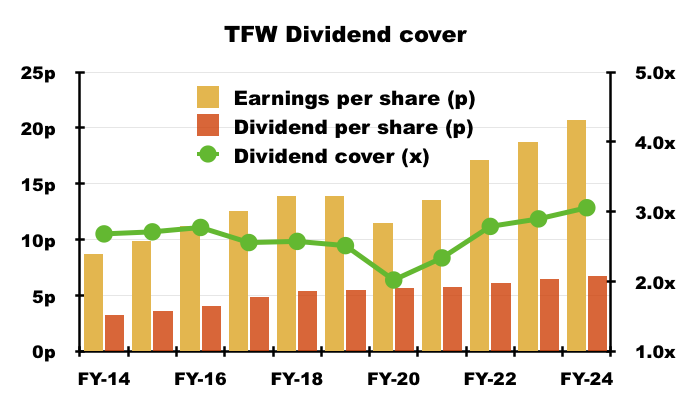

- The illustrious payout record has in part been supported by TFW’s high dividend cover:

- Keeping dividend cover at 2.5x before the pandemic allowed TFW to lift the FY 2020 payout by 2% despite earnings that year declining 18%.

- Dividend cover during the preceding FY surpassed 3x, which allows even greater scope to raise the payout should future earnings falter.

- The ordinary dividend has expanded at a 7.6% CAGR between FYs 2014 and 2024, and has been complemented by three specials during the last four FYs.

Thorlux and SchahlLED

- Thorlux manufactures a wide range of professional lighting equipment — most notably the SmartScan system — and represents approximately 60% of the group:

- The division has operated since 1936 and attracts customers through innovative products, manufacturing excellence, bespoke designs and high-quality service (point 4) that combine to provide buyers with “peace of mind” (point 7).

- Thorlux’s lighting offers a “low total cost of ownership“, with modest maintenance requirements, extended working lifetimes and, increasingly, significant energy savings (point 7):

- Thorlux first manufactured energy-saving lighting during 1994 (point 3), has undertaken a carbon-offsetting scheme since 2009 and aims to reach ‘net zero’ by 2040 (point 18a).

- The preceding FY’s case studies included work for West Midlands Trains that has lasted for “nearly a decade“…

[FY 2024] “Thorlux has worked closely with West Midlands Trains and Network Rail for nearly a decade to modernise the lighting systems at 150 sites, including 145 stations. Additionally, Thorlux has supplied luminaires and control systems for the brand-new £56 million University Station in Birmingham.”

- …which suggests customers can supply repeat orders for extended periods:

- West Midlands Trains expects to save more than £1m a year on lighting costs through Thorlux:

[FY 2024] “Even with lighting levels increasing by 500% at certain stations to achieve industry standards compliance, WMT has reduced carbon emissions by 65%. With increased efficiency cutting lighting energy costs, plus reduced upkeep (planned, reactive and callout) and other factors, WMT calculates it will save over £1 million per year on its combined total energy and maintenance spend.”

- Many of Thorlux’s projects involve educational, healthcare and other public facilities. Establishments recently employing Thorlux include:

- Emphasising Thorlux’s ‘green’ credentials, the preceding FY’s annual report devoted a mammoth 28 pages to TFW’s ‘sustainability’ activities and climate-related disclosures (point 18):

- This H1 reiterated Thorlux not only designs lights to save energy usage…

“The Board continues to invest into new product development across the Group, with emphasis on technical innovations that provide environmentally friendly solutions to our customers.”

- …but also rejigs its operations to save energy usage:

“While major production investments were limited during the period, the Board has recently approved an investment into new machinery for the Thorlux factory. These upgrades will speed up operations whilst saving significant amounts of energy, reducing costs and environmental impact. Thorlux has also placed orders to refresh its transport fleet with newer, more efficient vehicles, including its first fully electric delivery vans.”

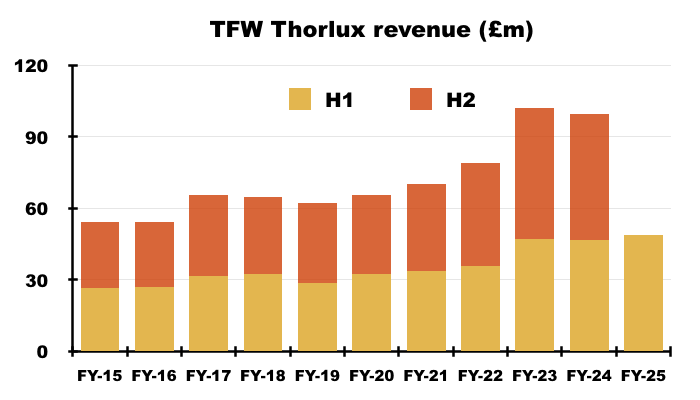

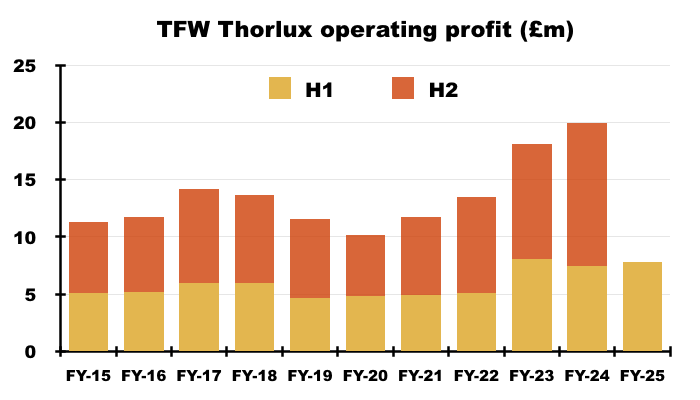

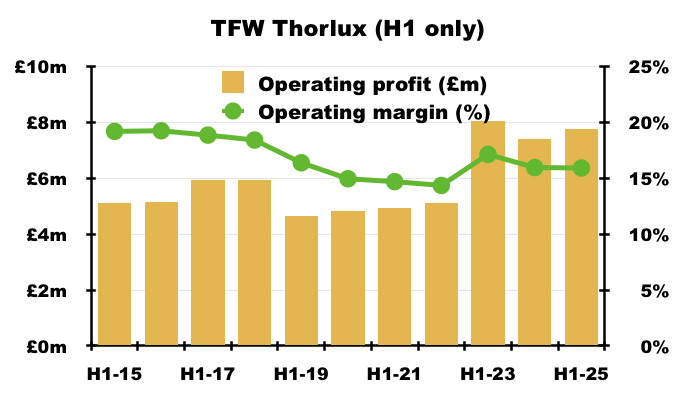

- H1 Thorlux revenue gained 5% to £48.8m to set a new H1 divisional record:

- H1 adjusted operating profit likewise gained 5% to £7.8m and set a new H1 divisional record:

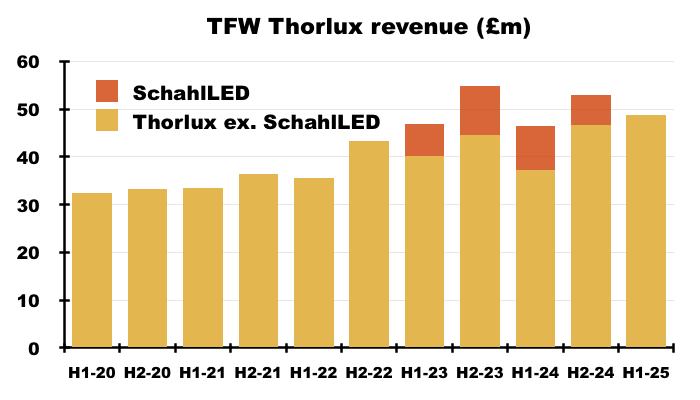

- Thorlux’s performance has been distorted by SchahlLED, which was acquired during FY 2023 and amalgamated into the division.

- Thorlux started working with SchahlLED during 2019, after which the German lighting installer quickly became Thorlux’s largest customer:

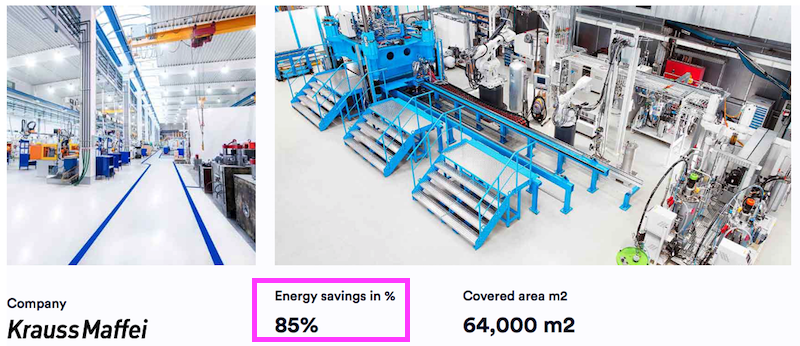

- SchahlLED’s customers tend to be large industrial companies. For example, a SchahlLED case study involving KraussMaffei reported an 85% reduction to energy costs through installing Thorlux lighting. The customer apparently enjoyed a “high return on investment with a payback period of less than 3 years“:

- TFW has previously disclosed SchahlLED’s revenue contribution to Thorlux, but did not do so for this H1:

- This H1 admitted SchahlLED’s performance was “impacted by the ongoing recession in Germany.”

- I presume SchahlLED’s revenue and profit declined during this H1, and therefore Thorlux’s revenue and profit excluding SchahlLED both increased by more than the division’s overall 5%.

- At the time of TFW’s purchase, SchahlLED had reported annual revenue of €15.9m.

- The preceding FY reported SchahlLED revenue of £15.4m, which translated into approximately €18.6m.

- SchahlLED lifting revenue from €15.9m to €18.6m within three years does not seem too awful.

- Thorlux’s H1 adjusted operating margin was a useful 15.9%:

- The 15.9% H1 divisional margin was within the 14-17% H1 range witnessed since H1 2019…

- …but was a few percentage points below the 18%-plus scored regularly up to H1 2018.

- I am hopeful Thorlux can soon revive its H1 margin towards 18% now that the division is selling direct into Germany through SchahlLED.

- TFW purchased 80% of SchahlLED for €14.6m during FY 2023 plus an additional €1.2m paid during the preceding FY.

- This H1 did not disclose anything about acquiring the remaining 20% of SchahlLED.

- The preceding FY said the outstanding 20% SchahlLED earn-out was:

- Estimated using a “forecast EBITDA assumption“;

- Expected to be €6.33m, and;

- Set to be paid from September 2025.

- TFW has confirmed to me this H1 included a £5.1m SchahlLED earn-out that was accounted for within non-current liabilities (i.e. is expected to be paid more than one year after the balance sheet date).

- £5.1m translated into €6.15m at the end of this H1 — a little below the €6.33m reported by the preceding FY.

- The initial €14.6m plus the additional €1.2m to acquire 80% of SchahlLED, alongside the remaining €6.15m 20% earn-out, gives a total €22.0m (£19.0m) purchase cost.

- SchahlLED was therefore acquired at 10x the £1.9m adjusted operating profit delivered during the preceding FY.

- This H1 did not disclose SchahlLED’s profitability.

Netherlands

- TFW’s Dutch businesses — Lightronics and Famostar — represented approximately 21% of the group during this H1.

- Lightronics manufactures mostly street lighting and was acquired during FY 2015 for an initial £8.3m that included a £1.9m debt repayment.

- Famostar manufactures mostly emergency lighting and was acquired during FY 2018 for an initial £6.3m:

- A £15m earn-out payment during FY 2022 took the total Dutch acquisition cost to £30m.

- Example project wins in the Netherlands include:

- The preceding FY hinted this H1 may not be so buoyant for Lightronics:

[FY 2024] “Lightronics was the stand out performer for 2023/24 by a distance… This year’s figures will be tough to beat; however, the [Lightronic] business starts the new financial year with a reasonable order book and good pipeline.”

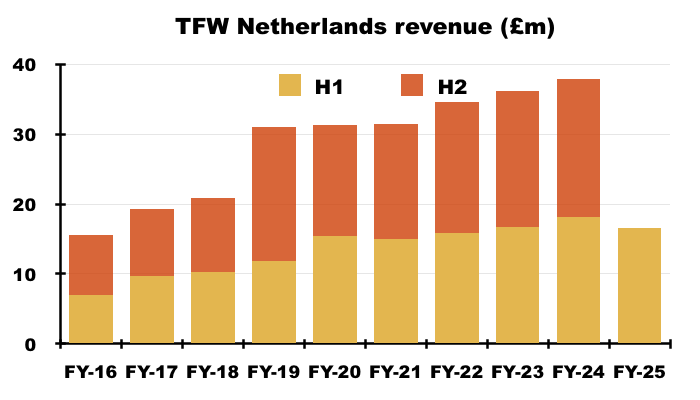

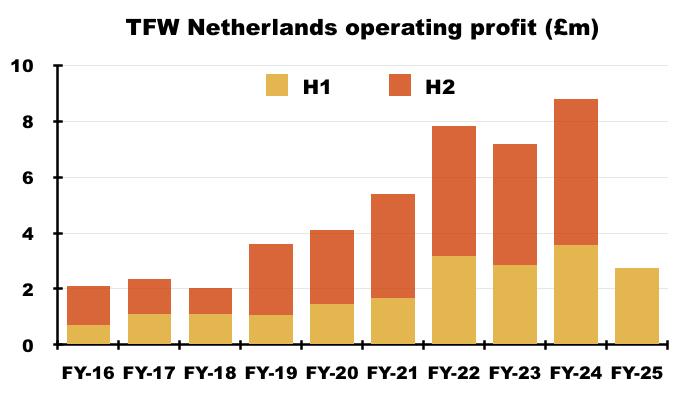

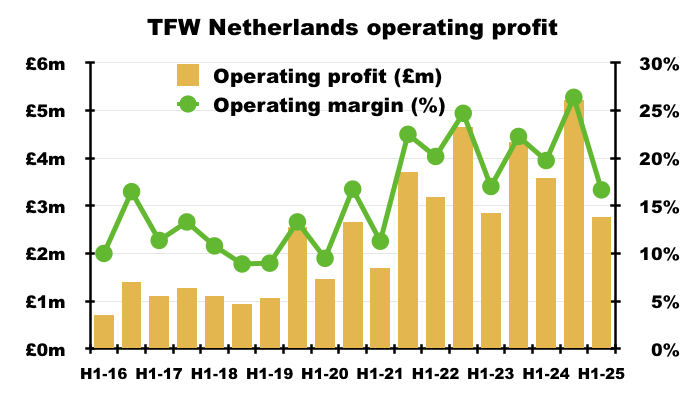

- Sure enough, H1 Dutch revenue slid 9% to £16.6m and caused H1 adjusted Dutch operating profit to dive 23% to £2.8m:

- The lower H1 Dutch revenue and adjusted profit translated into an H1 adjusted Dutch operating margin of 16.7%:

- While not as healthy as the comparable H1’s 19.7%, this H1’s 16.7% margin was still very acceptable and surpassed the adjusted margin at Thorlux:

- Despite this H1’s Dutch performance not matching the comparable H1’s performance, both Lightronics and Famostar appear to have performed well within TFW.

- Aggregate Lightronics/Famostar revenue for this H1 and the preceding H2 was £36m versus less than a combined £18m at the time of their purchases.

- Aggregate Lightronics/Famostar adjusted operating profit for this H1 and the preceding H2 was £8.0m versus a combined £2.3m at the time of their purchases.

- Twelve-month Dutch adjusted profit of £8.0m from a total £30m Dutch investment equates to a very satisfactory 27% pre-tax return.

- The 27% pre-tax return is all the more remarkable considering Lightronics suffered a major fire at its primary manufacturing facility during FY 2021:

- TFW commendably widened its boardroom composition during October 2022 after appointing Frans Haafkens as the group’s “first recognised independent” non-executive (see Boardoom):

- Mr Haafkens has worked with TFW since TFW bought Lightronics from his private-equity group during FY 2015.

- Mr Haafkens’ investment firm co-purchased Famostar with TFW during FY 2018, and bought a majority stake in Ratio Electric a year before TFW bought a 50% stake during FY 2022 (see Ratio Electric).

- During the 2024 AGM, Mr Haafkens admitted he sold the Dutch businesses to TFW “too cheap“ (which was “not very Dutch“), and the businesses had been a “really good investment” for TFW.

- I expect Mr Haafkens’ “hands-on” private-equity approach can assist TFW with further acquisitions.

- The past few years have witnessed TFW’s main board slimmed down to six directors, which I speculate allows Mr Haafkens and his private-equity background to exert greater influence over the group’s strategy (see Boardroom).

Zemper

- Encouraged by the success of the Lightronics and Famostar acquisitions, TFW purchased Spanish emergency-lighting specialist Zemper during FY 2022:

- Prominent buildings employing Zemper’s lighting include:

- A further 13.5% was purchased for €6.1m during FY 2023, and another 13.5% was then purchased for €5.0m during the preceding FY.

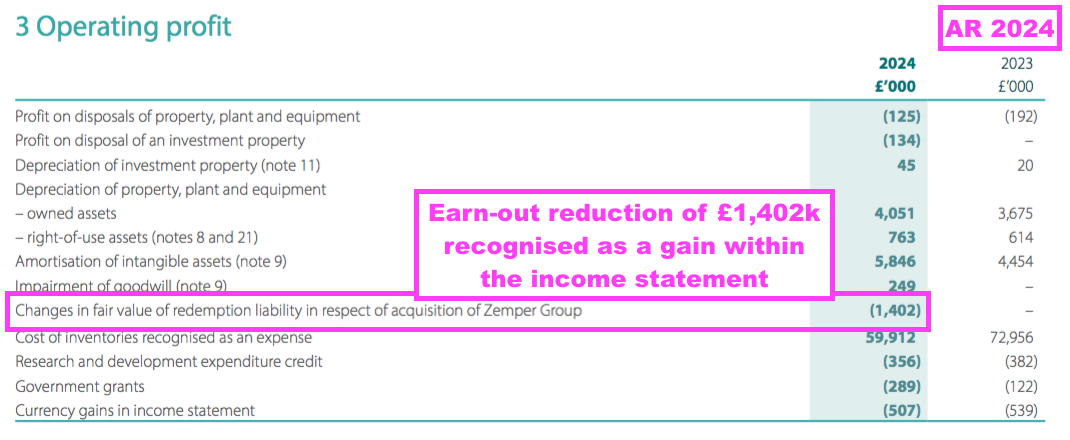

- Paying €1.1m less for 13.5% during FY 2024 versus FY 2023 did not suggest Zemper’s performance had lived up to expectations.

- Indeed, the preceding FY admitted the estimated cost to acquire the remaining 10% of Zemper had been reduced by £1.4m:

- But perhaps Zemper is now starting to perform following a few subdued years.

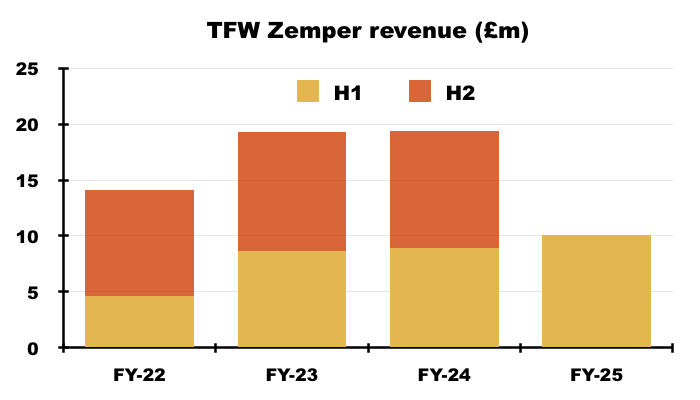

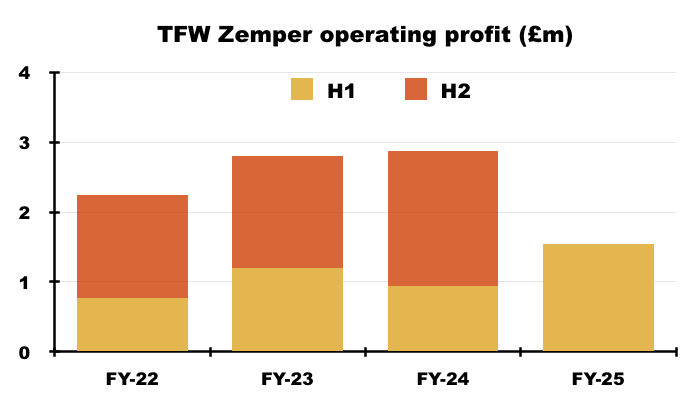

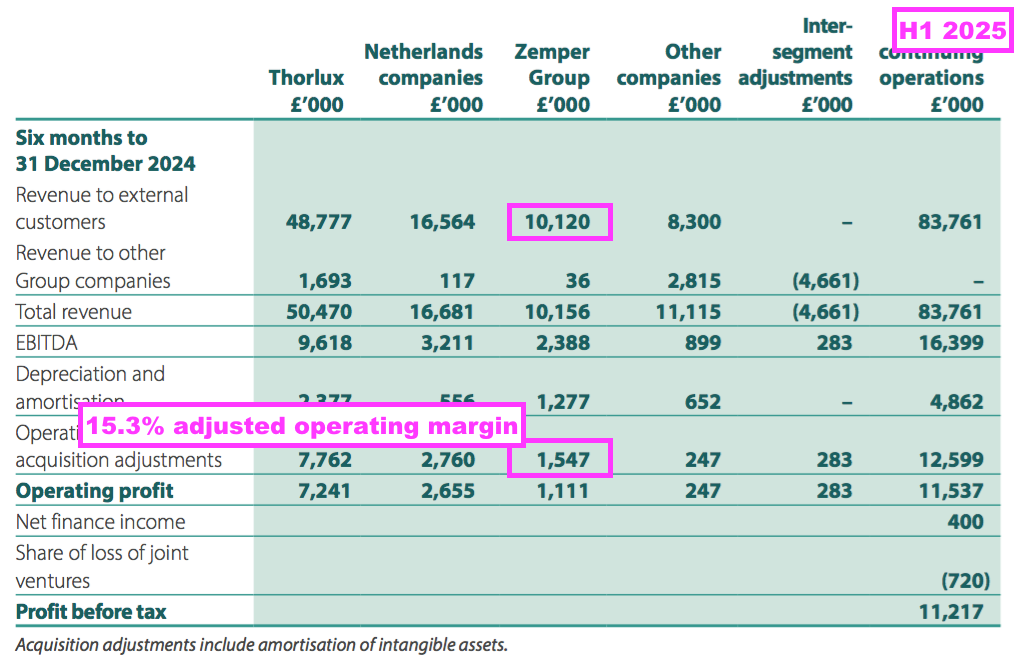

- Zemper’s H1 revenue in fact gained 13% to £10.1m:

- Zemper’s H1 adjusted operating profit meanwhile rallied a super 65% to £1.5m:

- Zemper’s H1 efforts led to a useful 15.3% adjusted margin and a notable improvement on the comparable H1’s 10.4%:

- The preceding FY said the outstanding 10% Zemper earn-out was:

- Estimated using a “forecast EBITDA assumption“;

- Expected to be €6.00m, and;

- Set to be paid from September 2025.

- TFW has confirmed to me this H1 included a €6.00m (£4.97m) Zemper earn-out that was accounted for within current liabilities (i.e. is expected to be paid within one year from the balance sheet date).

- After €5m was paid to acquire an additional 13.5% during the preceding FY, this H1’s improved Zemper progress may now justify paying €6m to acquire the final 10%.

- This H1’s improved Zemper progress may also lift the subsidiary’s ‘goodwill headroom’, which had been reduced from £25m to just £5m during the preceding FY (point 34).

- Zemper’s improved performance may reflect the sophisticated facilities at the division’s Spanish factory:

- Board remarks during the 2024 AGM noted “everybody who’s been to the factory is blown away by the technology.“. Zemper’s factory is in fact “far more automated and advanced” than Thorlux’s factory.

- The preceding FY noted a “proprietary charging system“ that emphasised the subsidiary’s scope for technical innovation:

[FY 2024] “The use of durable components, tested with thermal cameras to identify critical points, has extended the lifespan of all products in the EVO-10 range. This includes the design and manufacture of LEDs guaranteed for 100,000 hours.

…

For batteries, Zemper conducted the largest study to date on LiFeP04 batteries for emergency lighting applications, in collaboration with experts from the IMDEA Institute.

…

Additionally, Zemper has created a proprietary charging system for LiFeP04 batteries that maximises energy efficiency and extends battery lifespan.”

- The preceding FY also spotlighted Zemper’s leading role with other group subsidiaries through the ‘Firefly‘ project:

[FY 2024] “The Firefly project was a collaboration, led by Zemper in Spain, with engineers from all emergency lighting businesses in the Group.”

- Firefly is a “pivotal” emergency lighting system that includes “enhanced” lithium-battery technology and “more optical distribution variations to help eliminate or reduce risk to escapees“:

- Zemper’s aggregate revenue for this H1 and the preceding H2 was £20.5m versus approximately £17.4m at the time of purchase.

- Zemper’s aggregate adjusted operating profit for this H1 and the preceding H2 was £3.5m versus approximately £3.3m at the time of purchase.

- Certainly the size of TFW’s outlay to purchase Zemper suggests a fair amount of successful projects and/or synergies are expected from the Spanish subsidiary.

- To date TFW has paid €32.5m (€20.3m + €1.1m + €6.1m + €5.0m) for 90% of Zemper, and paying TFW’s estimated €6.0m for the remaining 10% would take the total Zemper purchase to €38.5m or approximately £35.5m.

- A £35.5m total purchase is 10x the trailing twelve-month £3.5m Zemper adjusted operating profit.

- For perspective, the £30m paid for the Dutch subsidiaries is 3.75x their trailing twelve-month £8.0m adjusted operating profit.

Ratio Electric

- Ratio Electric is headquartered within the Netherlands and develops electric-vehicle (EV) charging systems:

- EV charging is a departure from TFW’s lighting expertise. At the time of the Ratio investment, TFW said:

[RNS December 2021] “This is an exciting opportunity for the Group. FW Thorpe’s know-how in electrical engineering, manufacturing and lighting, combined with Ratio’s experience in electrical vehicle charging will allow the introduction of new products into the UK market as well as supporting growth in Ratio’s existing markets.

We see similarities in technology and engineering skills, giving the Group the opportunity to diversify into new areas of engineering with high growth potential.”

- Ratio’s “high growth potential” seems only to have brought high costs.

- TFW acquired 50% of Ratio during FY 2022 for £5.8m, with a loan note issued for £0.9m “to help fund the development of the business”.

- Although TFW’s share of Ratio’s profit was £228k during FY 2022, the group’s share of the joint-venture losses were £520k during FY 2023 and £826k during the preceding FY.

- The preceding FY admitted Ratio had “struggled” during the last few years and had taken longer to establish than expected:

[FY 2024] “The Group’s joint venture with Ratio Electric has struggled to make good contributions, but it has achieved significant growth in its Smart charger products, and it has established the Ratio UK company design and production facilities and product range… New projects and companies always seem to take longer to start and be harder to establish than one first believes.“

- The preceding FY also confirmed the additional losses had prompted the loan notes to increase to £3.4m.

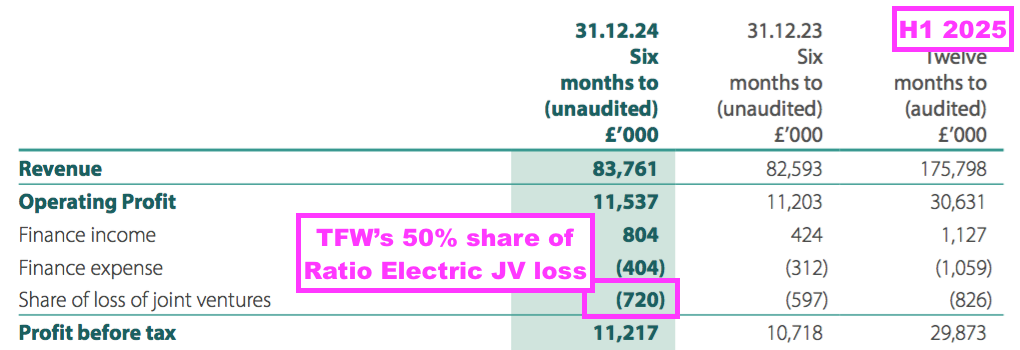

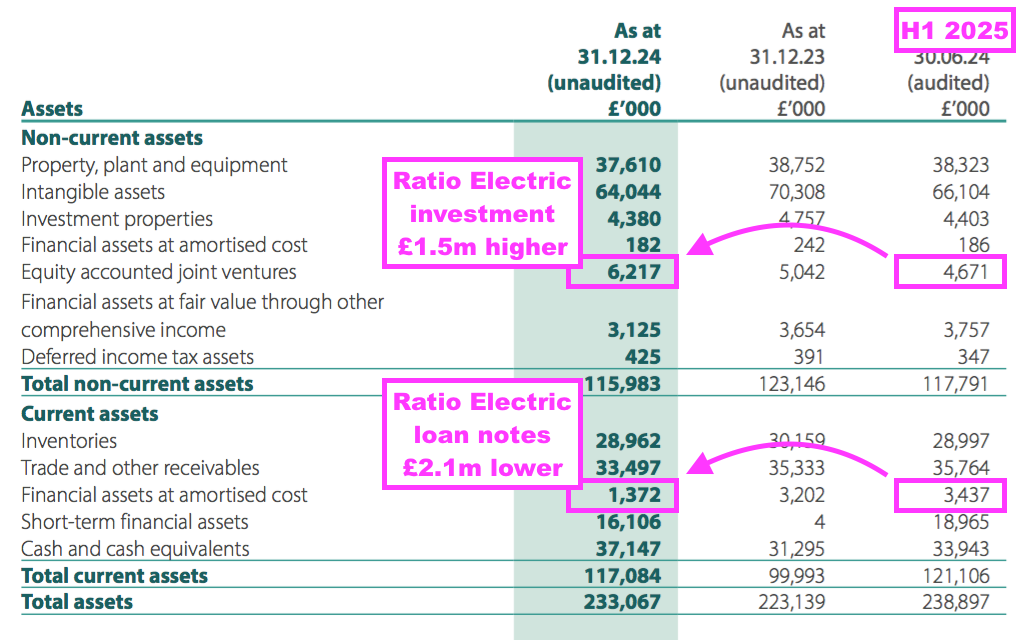

- This H1 revealed TFW’s share of Ratio losses amounting to a further £720k:

- This H1 also revealed TFW’s 50% share of Ratio’s equity increasing from £4.7m to £6.2m, and the group’s loan notes issued to Ratio decreasing from £3.4m to £1.4m:

- TFW confirmed to me “the increase in the investment value and the decrease in loans was a result of the capitalisation of the €2,850k (£2,362k) loan to Ratio Holdings“.

- Ratio has therefore undertaken a debt-for-equity swap, which does not feel very promising and reiterates how the joint venture has taken much longer than expected to establish.

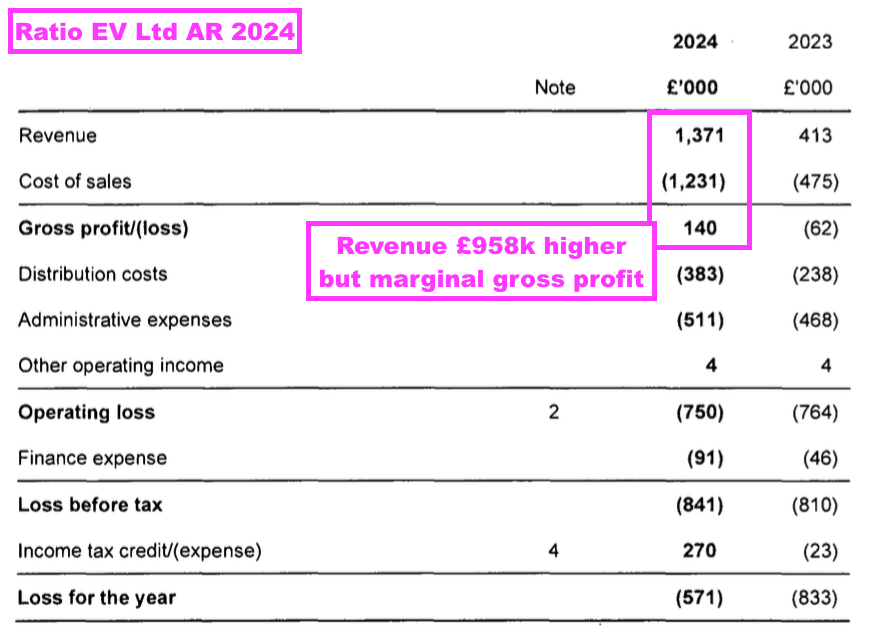

- Companies House shows Ratio’s UK subsidiary more than tripling revenue during calendar 2024 but making only a marginal gross profit:

- Accumulated losses at Ratio’s UK subsidiary now total £1.9m after three years of operation.

- Mind you, Ratio’s UK subsidiary generating £1m-plus revenue confirms the EV chargers are finding a few customers.

- Ratio’s UK website lists sites used by Kilwaughter, Bell’s Healthcare, Staycold Export and ThermoFisher Scientific as case studies.

- Board remarks at the 2024 AGM referred to Ratio receiving a “breakthrough” order, which might signal the operation can emerge from its present sub-scale position.

- Ratio’s losses have not stopped the joint venture starting an operation in Denmark.

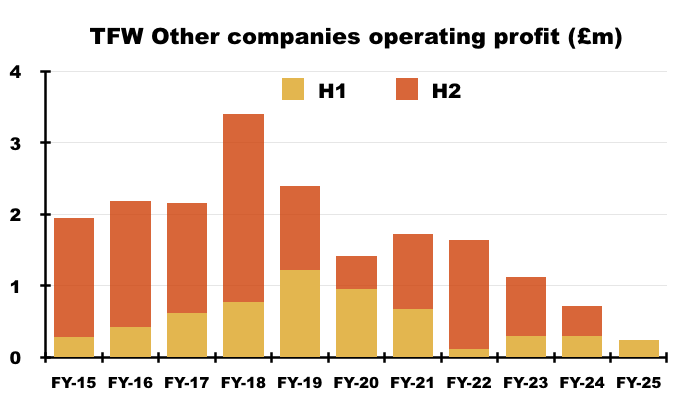

Other companies

- TFW’s Other companies consist of:

- TRT Lighting, which supplies lighting for roads and tunnels, and earns revenue of approximately £9m;

- Philip Payne, Solite and Portland, which between them supply emergency lighting, cleanroom lighting and shop lighting to earn combined revenue of approximately £11m, and;

- A handful of overseas Thorlux offices.

- The preceding FY made clear the combined efforts of the Other companies were not satisfactory:

[FY 2024] “The Board would like to see better contributions from all its smaller UK companies – especially, but not only, TRT Lighting. All these smaller companies have undergone changes to their subsidiary board structures in recent times, and improvements to, or diversification of, their product ranges where required. The Board looks forward to these changes enabling bigger contributions to Group profits from these businesses in the future.“

- That board instruction to the Other companies may have enjoyed a positive effect. This H1 implied these smaller UK operations had shown a “pleasing upturn“:

“Thorlux Lighting and Zemper started the year very positively, while all other UK companies showed a pleasing upturn.“

- But the figures seemingly told a different story.

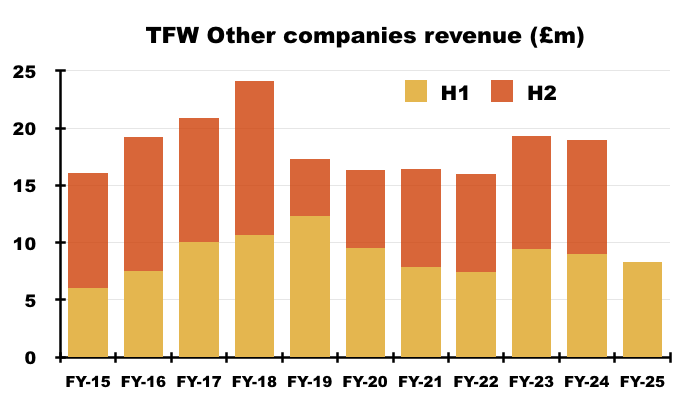

- H1 Other revenue fell 8% to £8.3m while H1 Other adjusted operating profit dived 18% to just £247k:

- The limited H1 Other profit might be due simply to TRT Lighting, which registered a loss during the preceding FY and continues to lose money:

“TRT Lighting’s efforts to boost order income are yielding positive results, although the company remains loss-making at the half year point.“

- Companies House for Philip Payne, Solite and Portland shows the trio all making money during the preceding FY with an aggregate £1m-plus profit.

- That said, the level of Other profit — with or without TRT Lighting — does leave these subsidiaries as a sideshow to Thorlux, the Dutch businesses and Zemper.

- I speculate Philip Payne, Solite, Portland and possibly TRT Lighting are kept on by TFW primarily because they supply products and services to the group’s larger operations:

- Attendees were told during the 2024 AGM that Philip Payne, Solite and Portland each have a minimum £5m revenue target (versus their actual revenue of £4m or less for the preceding FY).

- TFW has in the past (eventually) taken decisive action with struggling smaller subsidiaries. Sugg Lighting (revenue sub-£2m) was sold during FY 2015 while Compact Lighting (revenue £4m) was absorbed by Thorlux during FY 2018.

Financials

- TFW’s H1 figures have always been light on details, with accounting items such as gross profit and operating costs not disclosed:

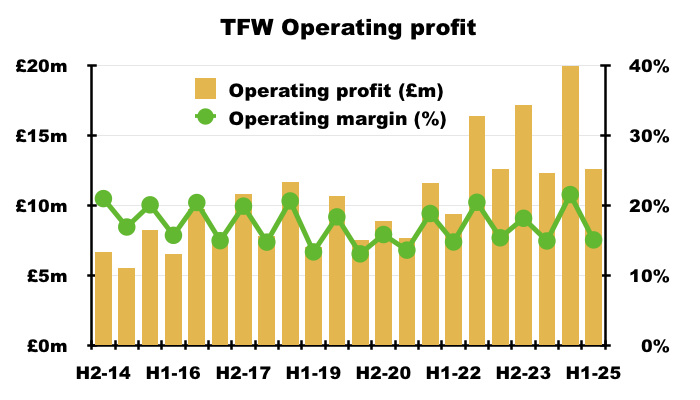

- The aforementioned margins for Thorlux, the Dutch businesses, Zemper and the Other companies left the group’s adjusted operating margin at an acceptable 15.0%:

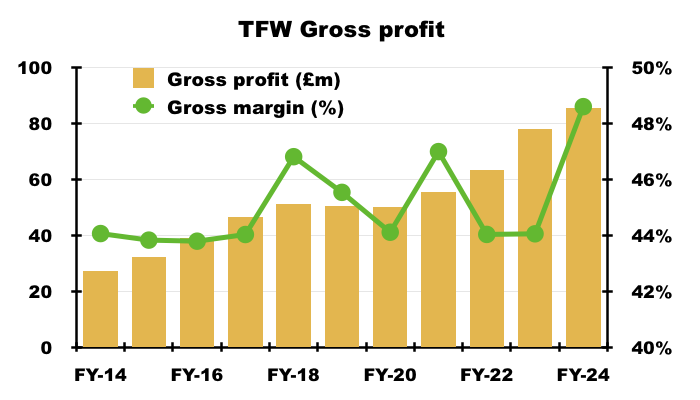

- The preceding FY registered a 49% gross margin — the highest since at least FY 1996:

- The preceding FY’s improved gross margin was in part supported by TFW’s ‘green thinking’, which led to some exceptional stock management and procurement (point 18d):

[FY 2024] “All Group companies are required to meet ambitious targets to reduce waste to landfill through the economical use of resources and recycling of materials. Through better planning, the Group has successfully managed inventory, minimised excess stock, streamlined deliveries and eliminated unnecessary purchases.”

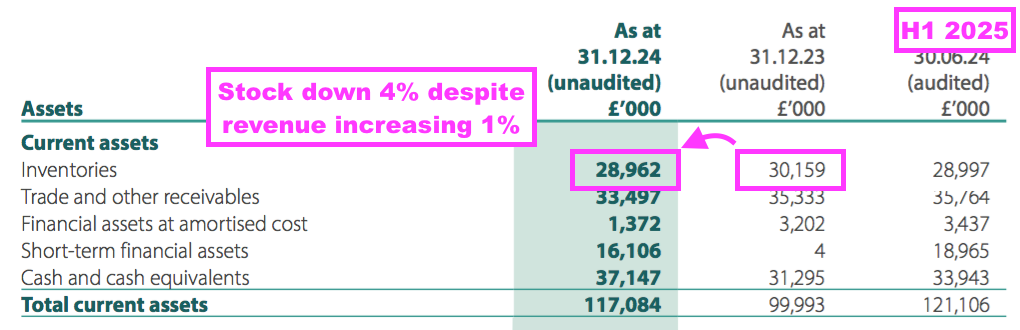

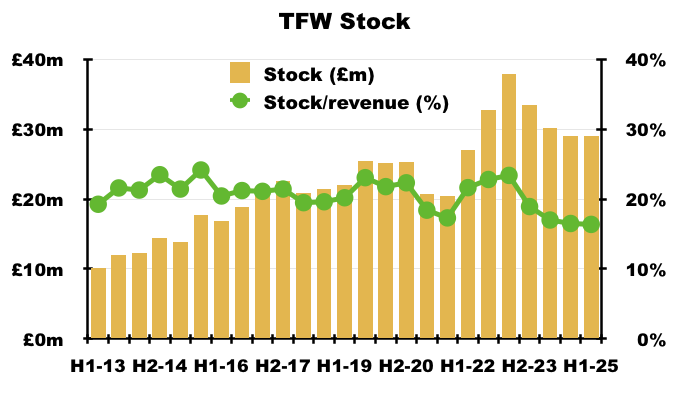

- Stock ended this H1 4% lower at £29m versus the comparable H1…

- … and was equivalent to 16.4% of trailing twelve-month revenue:

- Stock equivalent to 16.4% of twelve-month revenue is the lowest (i.e. most favourable) level since at least H1 2013.

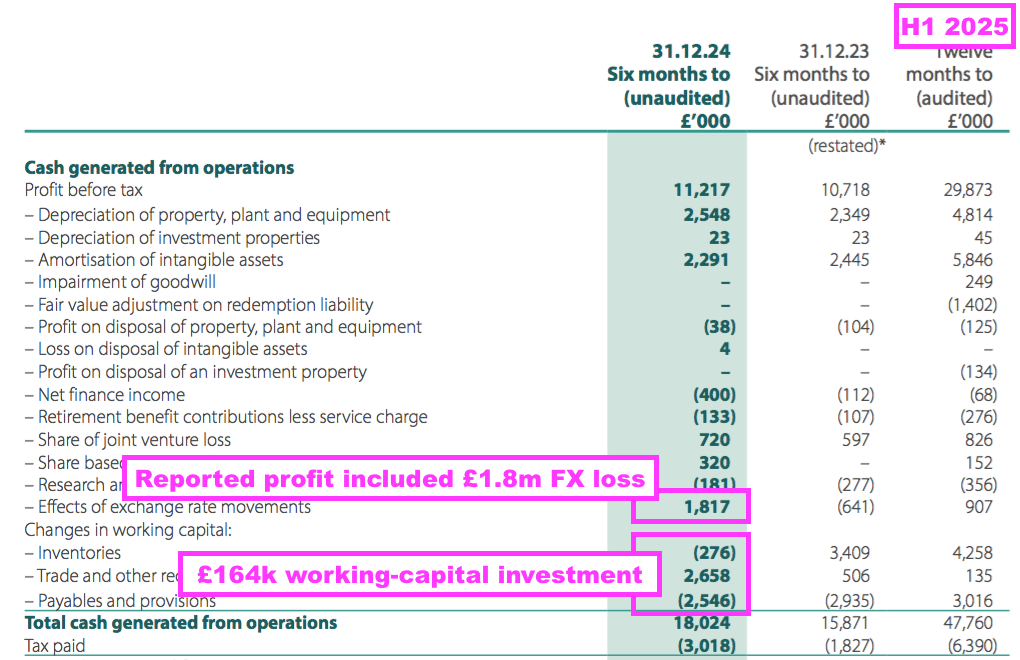

- TFW’s commendable stock management helped bolster this H1’s cash conversion — just £164k was invested into extra working capital during this H1:

- A sizeable £1.8m foreign-exchange cash flow credit — which suggests this H1’s profit was suppressed by adverse currency movements — ensured this H1’s cash conversion was very satisfactory.

- H1 operating cash flow of £18.0m less tax of £3.0m less capex of £3.4m less lease costs of £0.6m less Ratio loan funding of £0.4m plus net finance income of £0.8m meant estimated adjusted earnings of approximately £10.0m translated into free cash of £11.4m.

- Free cash of £11.4m less dividends paid of £8.9m less a handful of other minor items — including £469k paid to the minority owners of SchahlLED and Zemper — increased the cash position by only £345k during the six months.

- Still, H1 cash at £53m remains substantial and reflects TFW’s policy to “maintain a strong capital basis”:

[FY 2024] “The Group’s policy has been to maintain a strong capital basis in order to maintain investor, customer, creditor and market confidence. This sustains future development of the business, safeguarding the Group’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders.“

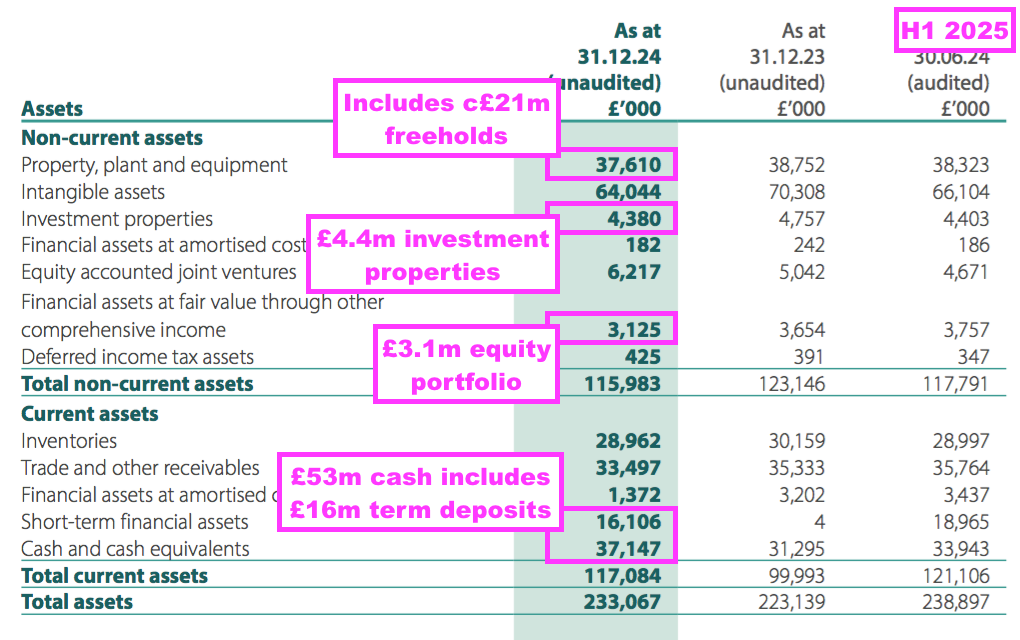

- Financial liabilities — relating entirely to loans acquired through Zemper or SchahlLED — meanwhile have been reduced to less than £2m.

- The £53m cash included £16m sat within term accounts of at least three months:

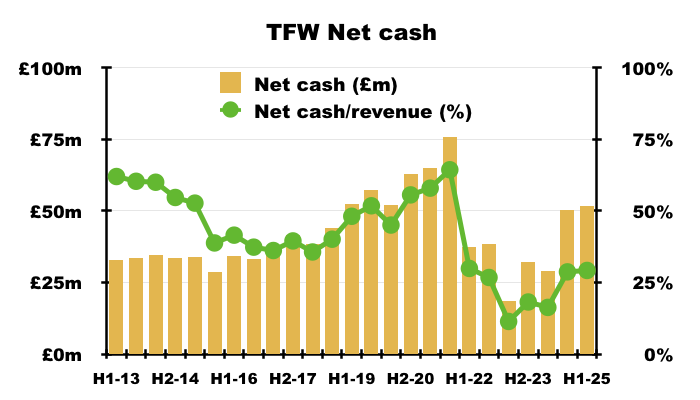

- Net cash of £52m is equivalent to 29% of trailing twelve-month revenue, which is reassuringly high compared to most quoted companies but relatively low for TFW:

- Net cash of £52m is more than enough to cover the £10m or so TFW estimates will cover the final earn-outs for Zemper and SchahlLED… and leave enough for another significant acquisition and even for some share buybacks (see Boardroom).

- The cash and Ratio investments are complemented by:

- Freeholds, which the preceding FY carried at £21m;

- Investment properties, which are mostly woodland for tree planting and carried at £4m, and;

- A UK equity portfolio worth £3m.

- Finance income during this H1 was £804k, and includes dividend income, rental income and loan-note income as well as bank interest income. I estimate the preceding FY witnessed a rather low 1.3% interest rate on the cash.

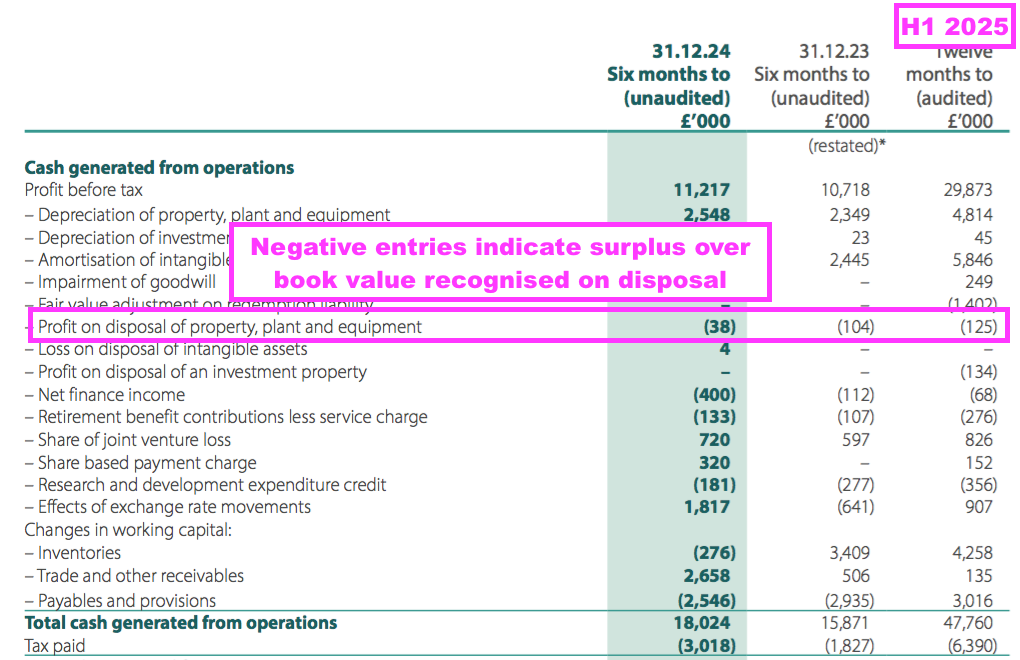

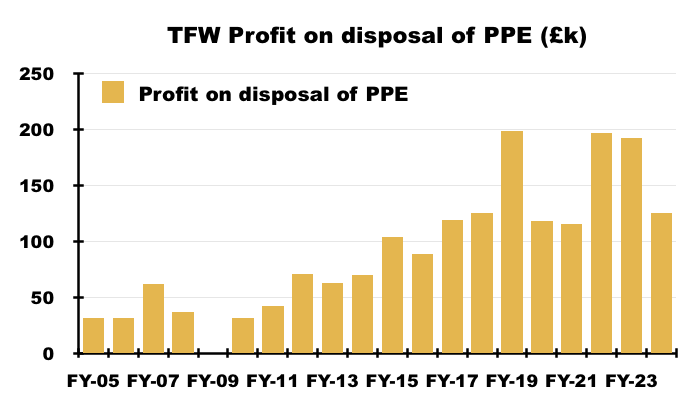

- Underlining TFW’s conservative accounting, this H1 declared a further ‘profit on disposal of property, plant and equipment’:

- Registering a profit from the disposal of property, plant and equipment means the items sold had been written down on the balance sheet to valuations below their eventual disposal proceeds.

- The past two decades have witnessed profits from the disposal of property, plant and equipment during all but one year:

Boardroom

- TFW’s boardroom has experienced a number of changes during the last few years.

- The aforementioned Frans Haafkens was appointed as the group’s “first recognised independent” non-executive during October 2022.

- Three directors then retired during 2023 and 2024, which slimmed the main board down from nine directors to six:

- TFW raised eyebrows last year when the roles of chief executive and group financial director were combined:

[RNS May 2024] “FW Thorpe Plc announces the following changes to the board structure, to become effective from 1 July 2024:

Mike Allcock will step down as Executive Chairman and Joint Chief Executive and take up the role of Non-Executive Chairman.

The position of Chief Executive will be assumed by Craig Muncaster whilst retaining the role of Group Financial Director. Craig has been Joint Chief Executive since 2017 and Group Financial Director since 2010.”

- I still can’t recall a quoted business the size of TFW — market cap of £357m, revenue of £177m and adjusted operating profit of £33m — deciding to amalgamate its two top executive positions.

- The preceding FY said the slimmed-down main board was counterbalanced by “strengthening the subsidiary boards“:

[FY 2024] “The Board’s head count has naturally decreased in recent years in favour of strengthening the subsidiary boards at the operating companies and promoting a focused group of managers from within that can support Group activities when called on.”

- The appointment of Mr Muncaster as chief executive/group finance director ultimately has the blessing of the two Thorpe non-executives, both of whom:

- Have spent their careers at TFW;

- Are now in their 70s, and;

- Have (presumably) accrued plenty of knowledge about management recruitment during the last few decades.

- I doubt the Thorpe non-executives would risk their combined 43%/£153m shareholding on a mis-judged chief executive appointment.

- I continue to speculate the board re-jig signals a different approach to group strategy and ‘capital allocation‘.

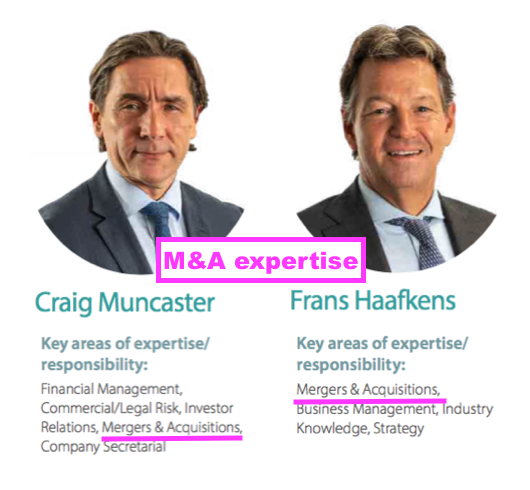

- After all, Mr Muncaster and Mr Haafkens were deemed by the preceding FY to have “Mergers & Acquisitions” expertise…

- …and major boardroom decisions of the last ten years have included purchasing Lightronics, Famostar, Zemper and SchahlLED for what looks to be an aggregate £80m-plus.

- This H1 provided a refreshing line on the board’s ‘capital allocation’ thinking:

“The Board continues to assess the opportunities to maximise returns from the Company’s strong balance sheet, which may include share buybacks where it considers that the share price significantly undervalues the Company’s current position and future prospects.”

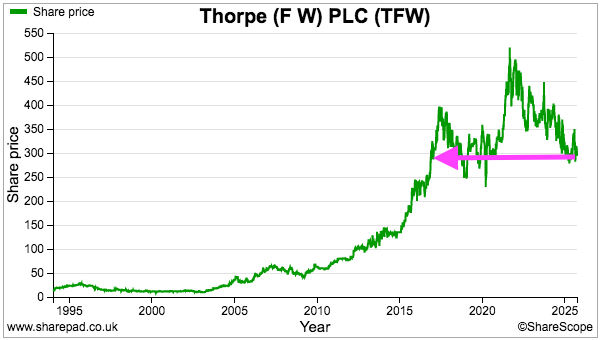

- With the 300p shares back to a level first achieved during late 2016…

- …buybacks may well provide a better return than conducting another acquisition.

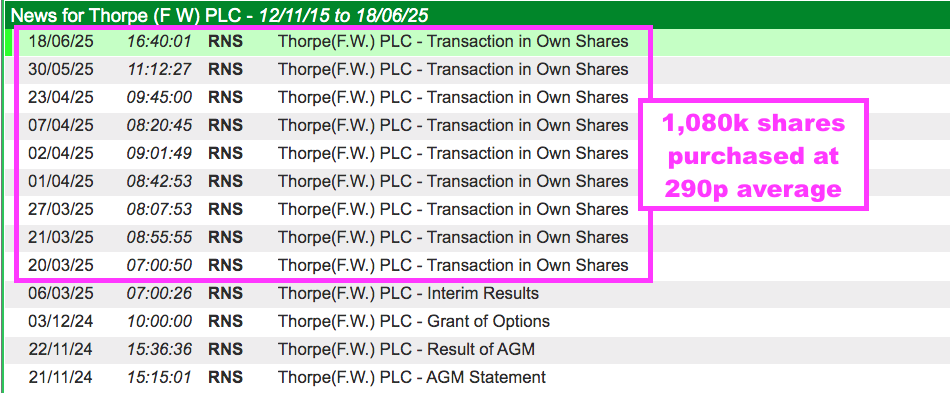

- Following this H1, TFW has purchased 1,080k shares at an average 290p for a total £3.1m outlay:

- All 1,080k purchased shares are held in treasury, which typically means they will be reissued to satisfy option exercises.

- At the last count, shares held in treasury numbered 2,674k while granted options numbered 2,725k (c2% dilution).

- I am hopeful TFW will at some point undertake buybacks for cancellation. Such buybacks should be more indicative of when the board considers the share price “significantly undervalues the Company’s current position and future prospects”.

- TFW’s buyback activity has been favourable but very infrequent.

- From what I can tell, TFW’s most significant buyback occurred during FY 2000, when 8% of the share count was purchased and cancelled at (a split-adjusted) 11.5p per share.

- Other notable buybacks occurred during:

- FY 2009, when £900k was spent purchasing shares for treasury at (a split-adjusted) 41p, and;

- FY 2014, when £1,628k was spent purchasing shares for treasury at 125p.

- Perhaps the real signal for when the share price “significantly undervalues the Company’s current position and future prospects” will be when ‘capital allocators’ Mr Muncaster and Mr Haafkens undertake a personal purchase.

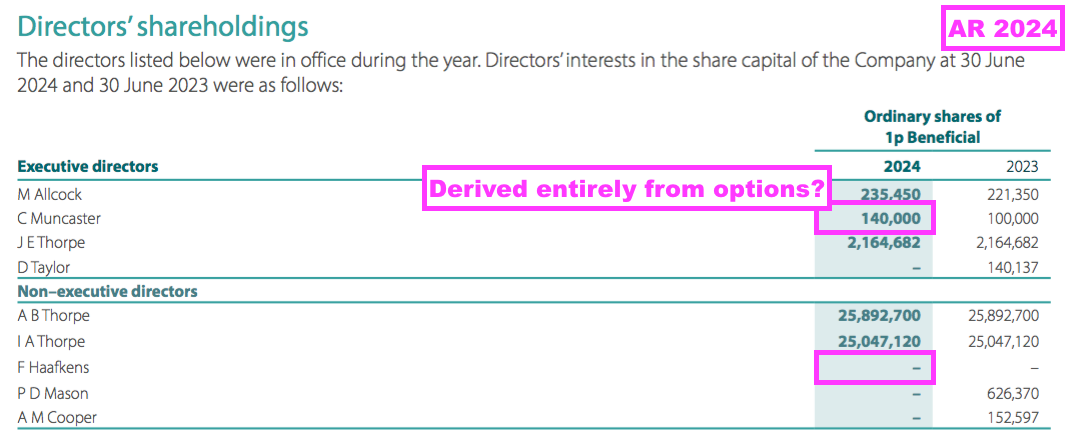

- ShareScope data suggests Mr Muncaster’s holding has been derived entirely from options while Mr Haafkens owns no shares:

Valuation

- Matching the modest progress delivered by this H1, this H1 in turn predicted FY 2025 would show only a “marginal improvement“:

“At the time of writing, the Group’s order book remains strong, and revenue is marginally ahead of last year. Forecast rising costs, mainly due to wage and National Insurance increases, will be offset by certain material cost reductions and efficiency improvements. As a result, the Board anticipates a marginal improvement in profit for the financial year ending June 2025.“

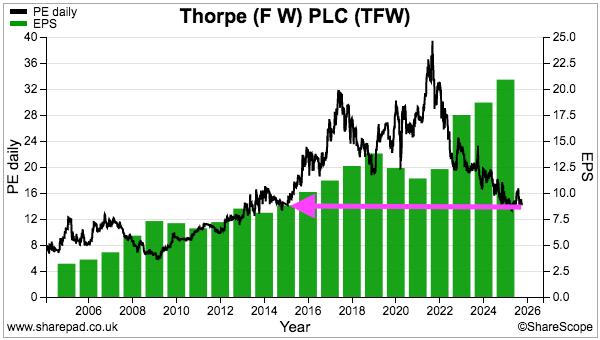

- Applying the 25% standard UK tax rate to the trailing twelve-month £32.7m adjusted operating profit gives earnings of £24.5m or approximately 20.6p per share.

- The 300p shares therefore trade at 14-15x my earnings estimate, which is the lowest multiple for ten years:

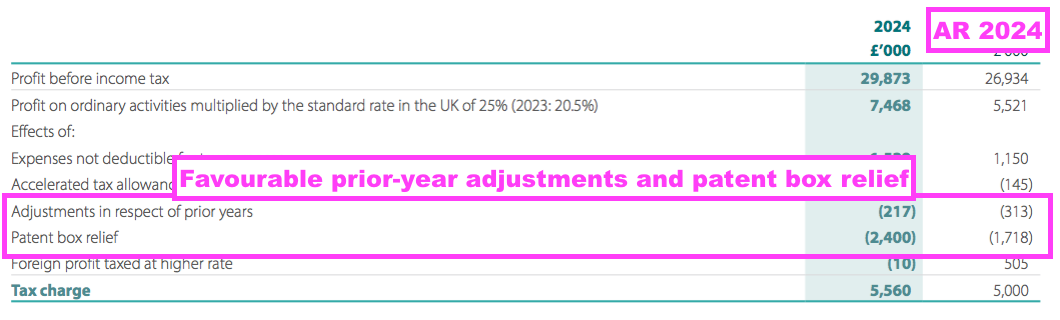

- Note that patent box relief and “refunds received for prudent assumptions” have reduced TFW’s tax charge by almost £12m since FY 2015 (point 32):

- Due in part to patent box relief and refunds, aggregate tax charged during this H1 and the preceding H2 amounted to £5.7m, or only 17.6% of the aggregate £32.1m pre-tax profit.

- A 17.6% tax rate would convert the trailing twelve-month £32.7m adjusted operating profit into earnings of £26.9m, or 22.6p per share, to support a 13-14x multiple.

- My calculations could be fine-tuned further for the £52m net cash and £10m aggregate forecast earn-out for Zemper and SchahlLED.

- Further tweaks could be applied to cater for Ratio, all the investments and that sizeable £1.8m foreign-exchange loss.

- But such adjustments would probably just confirm TFW’s recent valuation has become somewhat reasonable for the first time in many years.

- During my time as a shareholder, TFW has:

- Evolved through acquisitions from a UK-centric business into a pan-European operator;

- Lifted operating profit from £11m to an adjusted £33m;

- Extended its run of consecutive dividend increases to 22 years and declared five special payouts, and;

- Increased its market cap from approximately £94m to £357m.

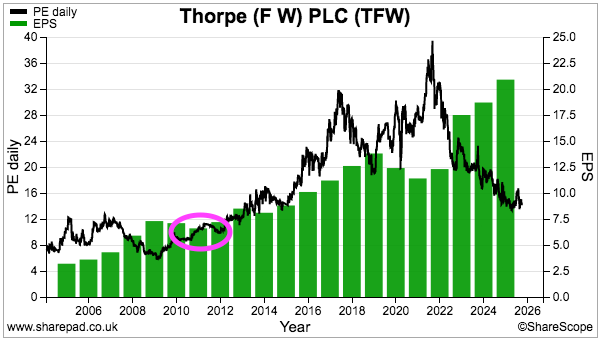

- Maybe those 13-plus years of positive progress could mean the chances of buying at a 10x-or-less multiple have become much less likely.

- I would venture today’s multiple may not entirely reflect TFW’s:

- Long-time operational resilience, as demonstrated by those 22 years of consecutive dividend increases;

- Appealing returns from acquisitions purchased on low multiples (e.g. Lightronics and Famostar);

- Possible growth opportunities through Zemper synergies and cross-selling further into Europe, and;

- Future orders supported by new product launches and ongoing concerns about elevated energy costs.

- The bear case beyond general economic challenges includes:

- Zemper, SchahlLED and Ratio not performing quite as expected following significant purchase expenditure;

- Mr Muncaster and Mr Haafkens undertaking ambitious acquisitions without adhering to a suitable KPI;

- A slowing transition to energy-saving lighting;

- Reduced public spending on schools, hospitals and other prominent TFW sectors;

- The board’s desire to “promote from within“, which may preclude innovative thinking from outside of the group, and;

- Management’s CPI+2% EPS LTIP target implying moderate growth prospects.

- As the board ponders how to employ the £52m net cash position, the 300p shares trade at a level first achieved during late 2016…

- …while the trailing 6.84p per share ordinary dividend supplies a modest 2.3% income.

Maynard Paton