***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

18 September 2025

By Maynard Paton

I am once again looking for ‘value bargains’ and revisiting a screen that identifies companies trading at less than book value.

Importantly, this screen attempts to avoid ‘value traps’ by demanding the shares offer net cash, dividend payments and a history of trading above book value.

The exact filter criteria I redeployed were:

- A price to net tangible assets of no more than 1;

- A dividend being paid during the most recent year;

- A 10-year average price to net tangible assets of at least 1;

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

- A share price denominated in pounds sterling.

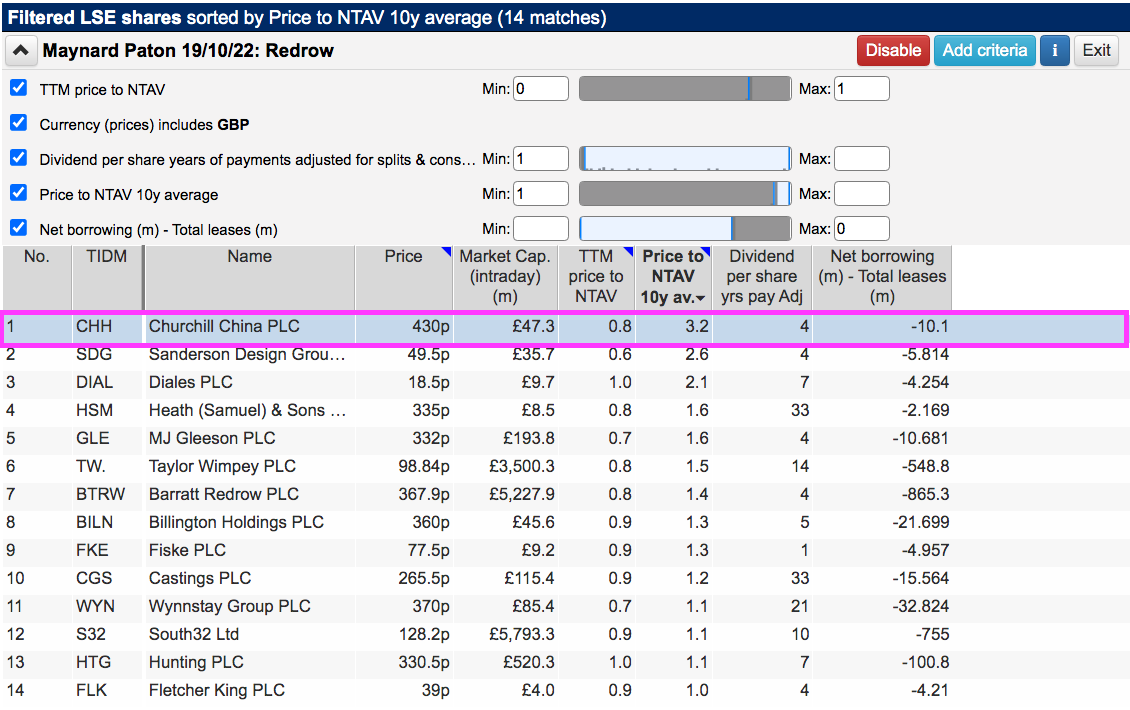

This time ShareScope returned 14 companies:

I selected Churchill China because, among the 14 shortlisted companies, its shares had previously traded at the highest average multiple of net tangible assets.

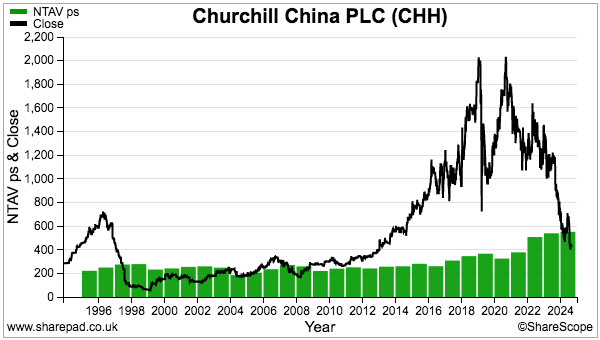

Sure enough, Churchill’s 430p shares are priced at 21% less than the 545p per share net tangible asset value:

And yet the shares have in the past traded at beyond 5x net tangible value.

Let’s take a closer look.

Read my full CHURCHILL CHINA article for ShareScope >>Maynard Paton

Excellent analysis, as per usual!

I’m slightly more positive on this (as a cyclical play).

1. Increasing inventory isn’t good to see, as clearly they aren’t selling enough product! However, plates / mugs don’t suffer from obsolescence, so I doubt we’ll see any major stock write downs. The issues, which their hospitality end markets are suffering from, aren’t going to be fixed by a slight reduction in plate prices?

2. Longer term they have been successfully in implementing automation. With increased costs to employers now I hope they redouble their efforts on this.

3. I think the hospitality market is in a cyclical, rather than structural, decline. Good quality plates (available quickly) will always be needed by restaurants. Churchill may have a tough few years ahead, but there’s very little solvency risk, given the net cash and asset backing.

I need to do more work, but I see it as a cheap option (over the next 5 years or so), with limited downside (given the 10* current PE).

Usually with option like investment – junior minors, oilers etc there is a risk of it expiring worthless (the company going bankrupt). It’s rare to find a “decent” business with such options like investment characteristics!

Hi Peter

Thanks for the message. I must admit I was disappointed I could not be more positive on CHH. Very commendable the business has been operating for so long in what has been a very difficult industry for UK operators. One issue that was raised during that ‘Troubleshooter’ episode was having to keep the ‘sausage machine’ rolling — i.e. the business could not just stop and then restart manufacturing. So I think if the stock keeps building and customer orders remain slow, the risk of stock provisions will grow. CHH claims the lack of plate sales is due to customers opening fewer sites, which does suggest some cyclical element and a possible recovery once the industry rebounds and operators open new sites. I have found to my cost through TAST that the hospitality sector now has poor economics and I just can’t become convinced the wider sector will soon become lucrative for CHH — unless diners become willing to pay much more for meals.

Maynard