17 August 2025

By Maynard Paton

FY 2024 results summary for Andrews Sykes (ASY):

- A rather mixed FY, as “unseasonally cool summer weather“, French depot closures and currency movements reduced revenue by 4% and kept the dividend at 25.9p per share for the third consecutive year.

- UK progress was once again supported by water pumps, income from which gained 2% to set a seventh consecutive FY record. A new water-treatment service meanwhile offers promise.

- The heatwave absence cut sales throughout Europe by as much as 28%, although fresh local management lifted Middle Eastern income by a welcome 37% and established a new Saudi venture.

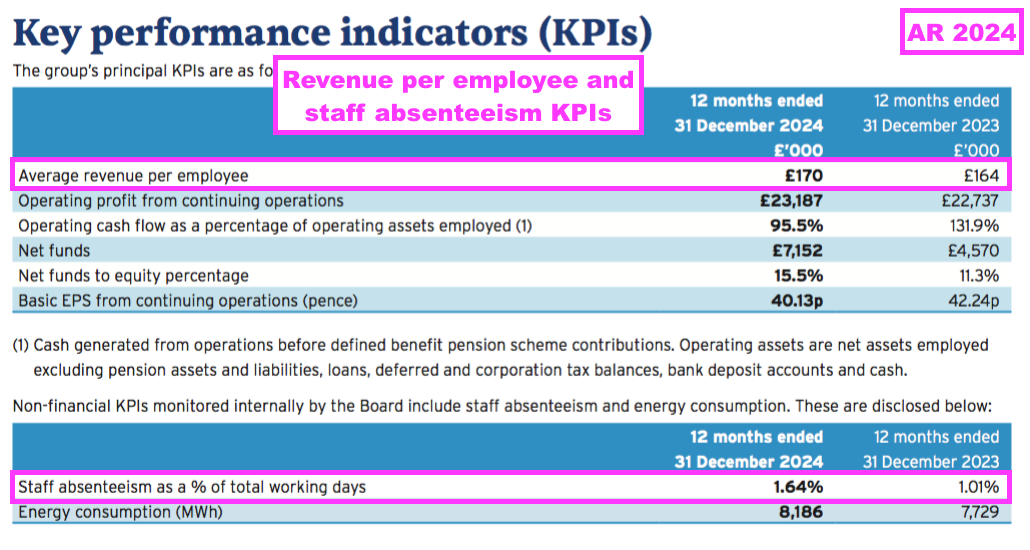

- Revenue per employee reached a new £170k high after the workforce was reduced to its lowest level since at least 2004. The improved staff productivity helped deliver a record 30.5% FY margin.

- The 5% yield could be complemented by further special dividends should net cash once again top £30m, but the group’s limited free float and distinctive corporate governance have rarely led to a premium rating. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own ASY

- Results summary

- Revenue, profit and dividend

- UK

- Europe

- Middle East

- Financials: hire revenue and hire equipment

- Financials: margin and employees

- Financials: cash flow and working capital

- Financials: balance sheet and return on equity

- Boardroom

- Valuation

News link, share data and disclosure

- Annual results for the twelve months to 31 December 2024 published 07 May 2025.

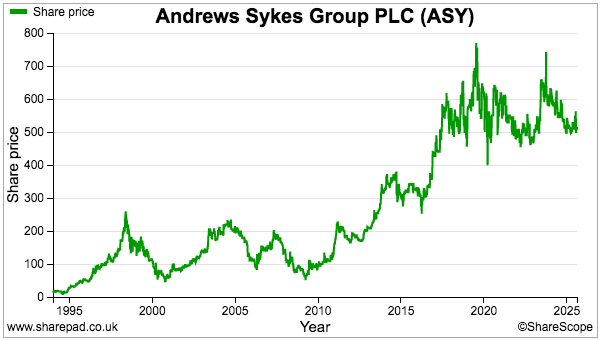

- Share price: 515p

- Share count: 41,858,744

- Market capitalisation: £216m

- Disclosure: Maynard owns shares in Andrews Sykes. This blog post contains ShareScope affiliate links.

Why I own ASY

- Supplies industrial pumps, air conditioners and portable heaters for hire, with success based on a prompt 24/7/365 service, high-quality rental fleet and trade-only customer base.

- Straightforward accounts regularly showcase super margins, generous cash flow, net cash and very satisfactory returns on equity.

- Chairman and family are 90%/£194m shareholders, appreciate special dividends and say their “presence and requirements… have resulted in a strategy with the key aim of creating long–term shareholder value“.

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Revenue, profit and dividend

- A standstill H1 that included a mixed H2 outlook…

“Trading in the second half of the year to date has been more subdued than in the comparable period of last year. A slow start to the summer season with cooler than average July temperatures recorded in the UK and Northern Europe has limited the overall revenue opportunities for the Group in these jurisdictions. Southern Europe and the Middle East continue to trade positively compared to the prior period.”

- …had already suggested this FY might struggle to surpass the performance set during the comparable FY.

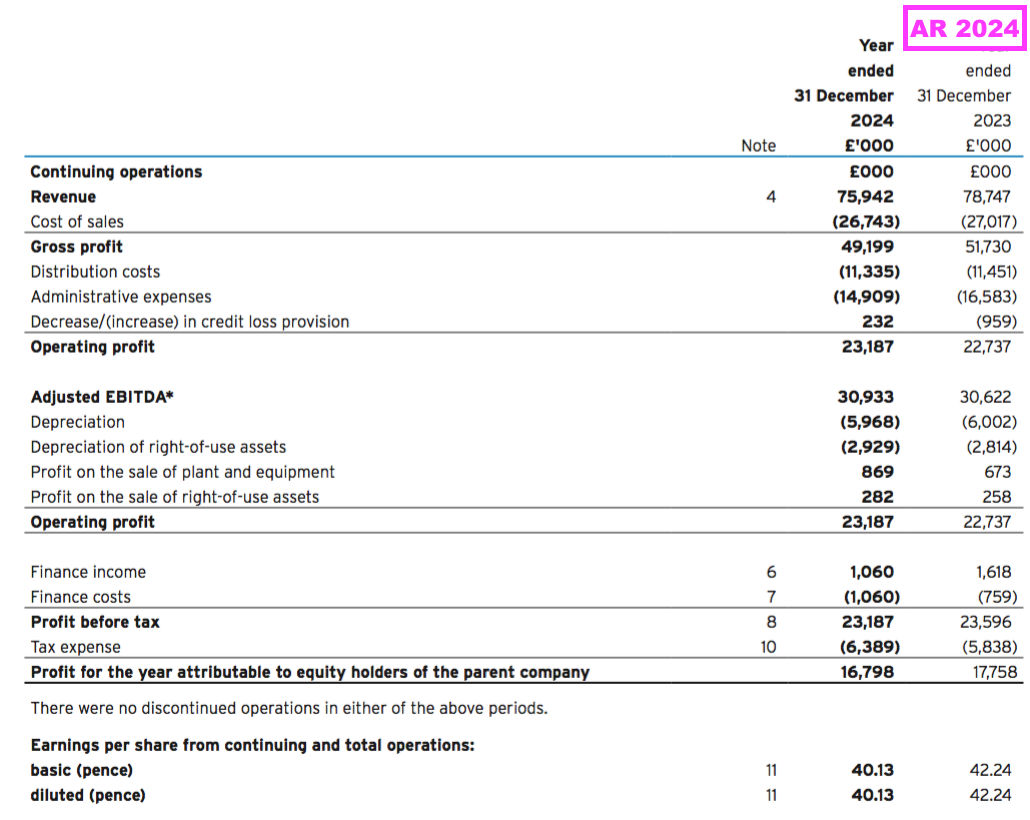

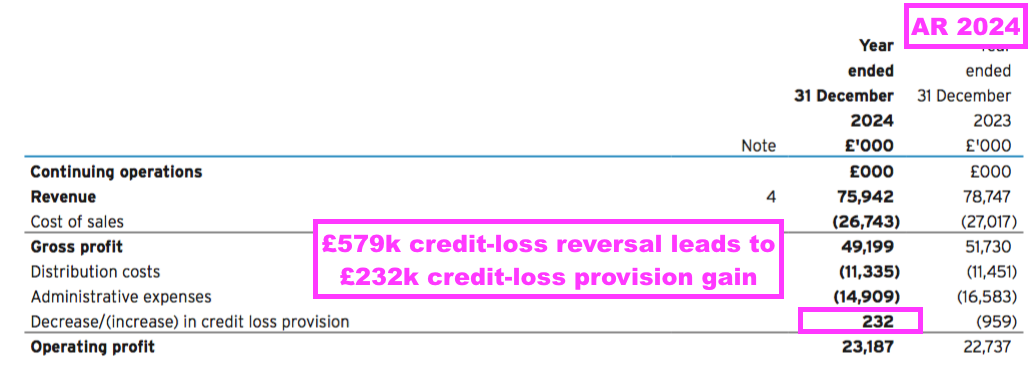

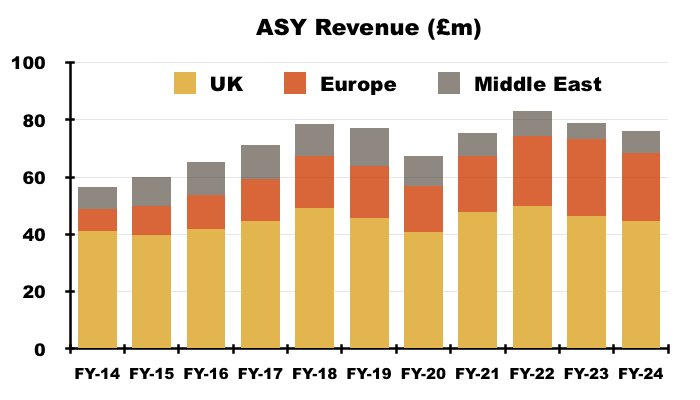

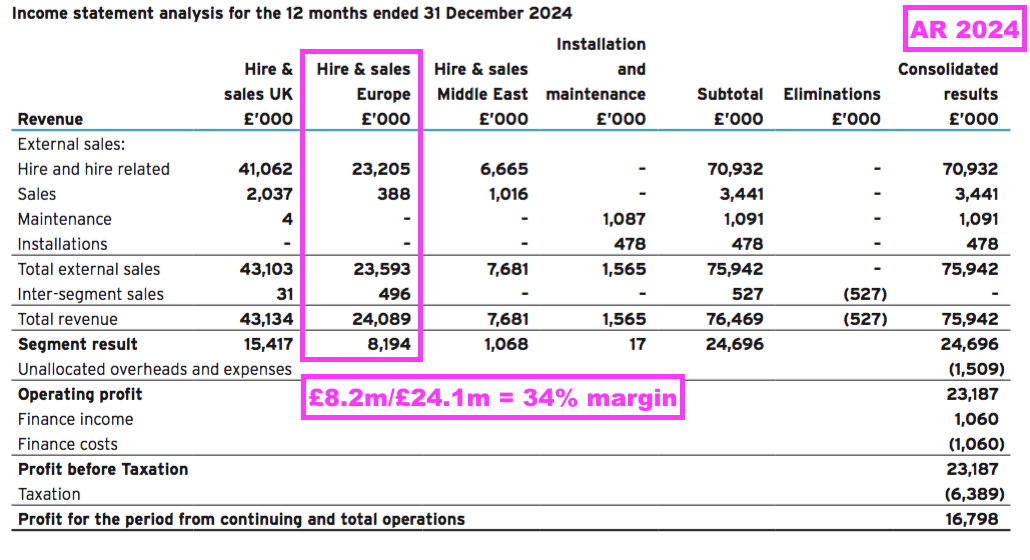

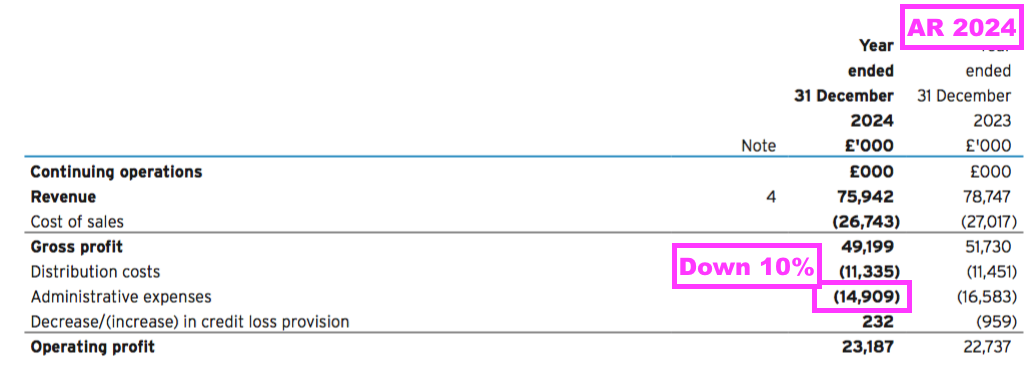

- FY revenue in fact declined 4% to £75.9m:

- This FY claimed “underlying” FY revenue slipped only 0.5% excluding the effects of:

- Closing the group’s French depots (see Europe), and;

- Currency movements:

“Of this £2.8 million decrease, £1.5 million was a result of the previously taken decision to cease operating within the French market. A further £0.9 million decrease was as a result of stronger Sterling exchange rates versus the Euro and the Dirham. Excluding these two factors, underlying turnover was down year on year just £0.4 million or 0.5%.”

- This FY described trading as “strong” despite “unseasonally cool summer weather”:

“Andrews Sykes’ trading remained strong during 2024 and we are pleased to report that the Group as a whole has again delivered a record level of operating profitability.

…

2024 was not without its challenges, with revenue opportunities being constrained by the unseasonally cool summer weather experienced in the UK and across much of Europe.”

- Extreme weather — particularly extensive rain, heatwaves and cold snaps — typically prompt sudden demand for the group’s hire equipment (primarily water pumps, air conditioners and temporary boilers).

- Progress from year to year can therefore fluctuate due to different climatic conditions.

- Mind you, this FY’s “unseasonally cool summer weather” did not appear to have a disastrous impact on “underlying” revenue.

- Indeed, heatwaves may not necessarily create significant additional revenue through greater demand for air conditioners, at least within ASY’s main UK division. FY 2022 for instance reported UK revenue up only 4% despite a 40-degree summer leading to UK air-con hire activity soaring 36% (see UK).

- Water pumps appear to be ASY’s largest earners in the UK and are the only equipment supplied to customers in the Middle East. This FY in fact highlighted greater investment within the water side of the business:

“During the year, the Board approved a significant capital expenditure for a new product range within the UK pump sector. A decision was made to invest £0.5 million within water treatment plant. In reaching this decision, the Board considered the group’s overall cash levels, the return on each asset along with its expected utilisation and the potential for expansion of the water treatment division.“

- Water pumps are now complemented by equipment for water treatment, which ASY started to offer during this FY (see Financials: hire revenue and hire equipment).

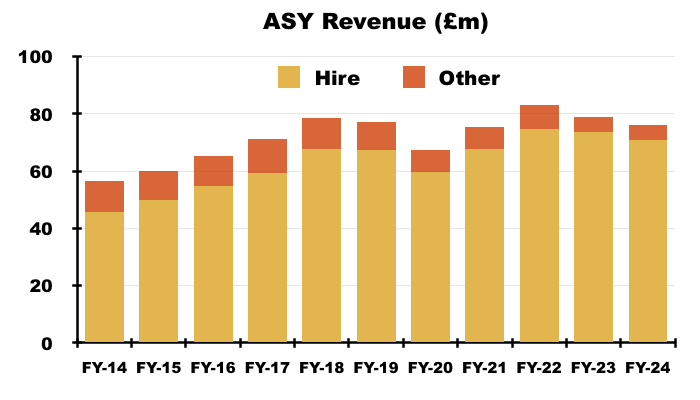

- The temperature fluctuations, French closures and currency movements left FY revenue from ASY’s core hire activities down 4% at £70.9m:

- ASY’s ‘Other’ sources of FY revenue — essentially equipment sales and installing/maintaining fixed air-con systems — meanwhile stayed at £5.0m and contributed 7% to this FY’s top line (see Other).

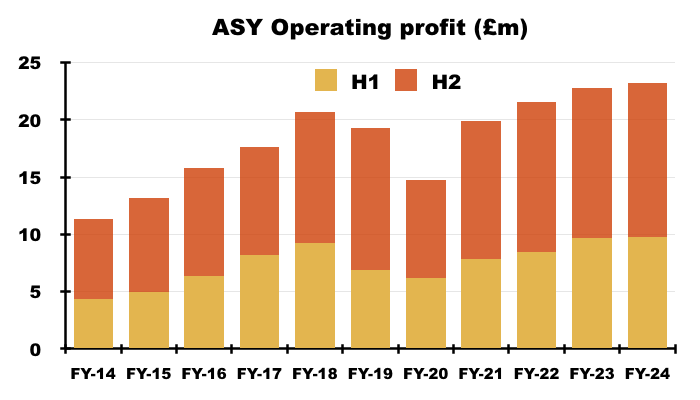

- Despite this FY’s lower revenue, FY operating profit improved 2% to a record £23.2m:

- This FY explained the profit advance was due to “tight cost control” and a “focus on… key accounts“:

“However, our long-standing commitment to tight cost control and leveraging our strong relationships with customers have allowed us to not only maintain but increase our operating profitability over the previous year.”

…

“…the focus on our key accounts means the Group has still produced operating profit growth despite reporting a lower revenue.”

- “Key accounts” are presumably the large, high-spending customers that this FY said supported approximately 50% of the business:

“We regard customer relationships as being of the utmost importance and our key account customers, which account for, approximately, 50% of our business, are visited by a customer relationship manager on a quarterly basis to ensure we are meeting their expectations.”

- ASY’s website refers to the following (presumably “key“) customers:

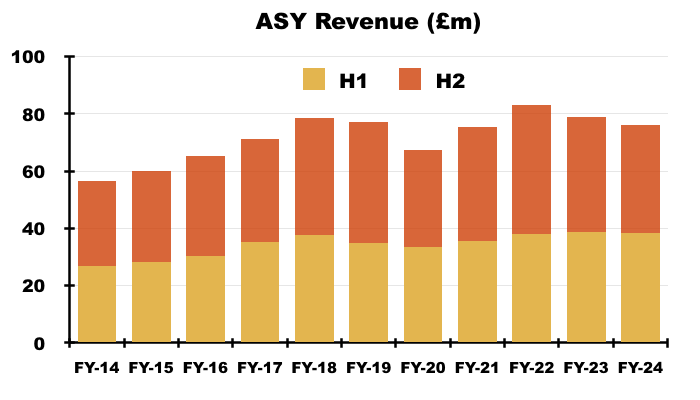

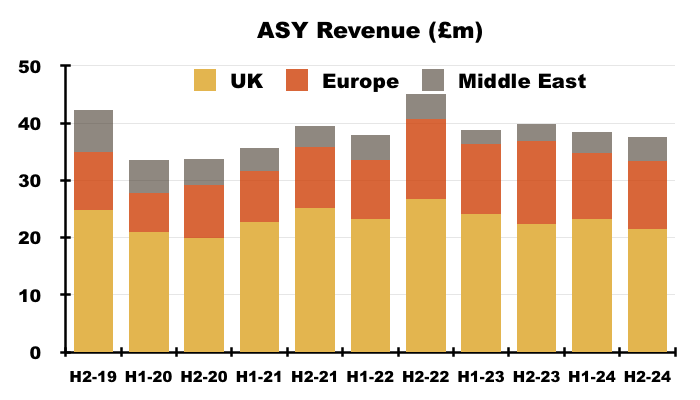

- Note that H2 witnessed revenue slide 6% to £37.6m, and yet H2 operating profit gained 3% to £13.5m to set a new record for any H1 or H2.

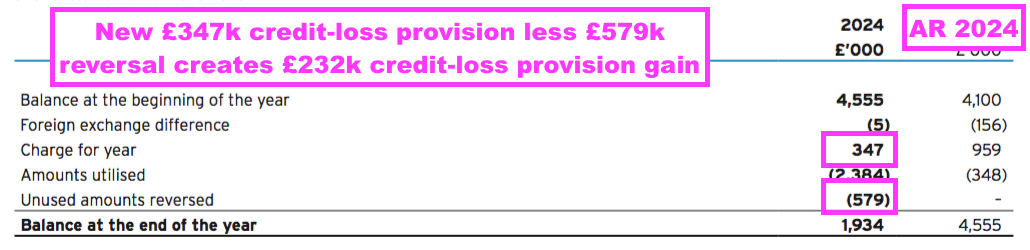

- This FY’s profit advance was supported entirely by provision movements.

- This FY’s income statement showed a £232k gain from changes to the group’s credit-loss provision:

- The credit-loss provision reflects the expected bad debts from late-paying customers, and ASY collecting payments of £579k that had been previously written off led to this FY’s £232k extra profit:

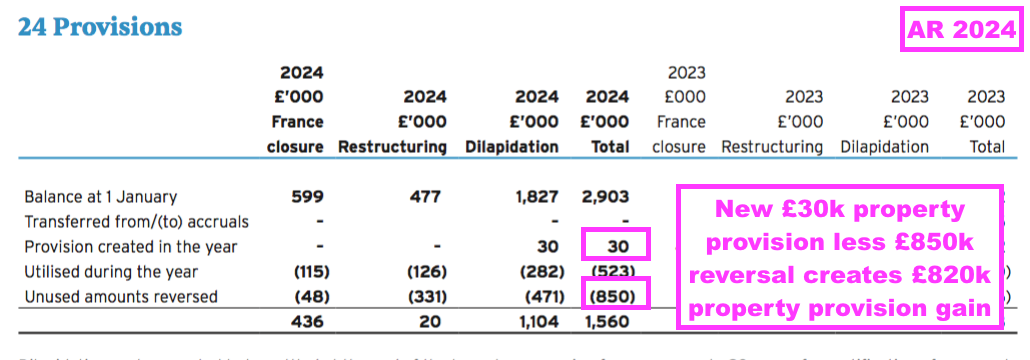

- Not shown in the main income statement was a net £820k reversal of expected property-closure costs:

- The property-closure provision reflects the anticipated expenses from shutting depots, and this FY’s “commercial negotiations” with landlords…

“Despite this decrease in revenue, through careful cost management and commercial negotiations for the early exit of previously vacated lease properties, operating profit has increased by 2.0%, or £0.5 million…“

- …led to lower-than-expected exit costs, and a net £820k gain within reported profit.

- Excluding changes to credit-loss provisions and property-closure provisions, FY operating profit would have declined 10% to £22.1m.

- ASY has never presented an ‘adjusted’ profit to exclude movements to the credit-loss provision and the property-closure provision.

- This FY’s provision reversals strongly suggest ASY was simply very prudent with its original expense estimates.

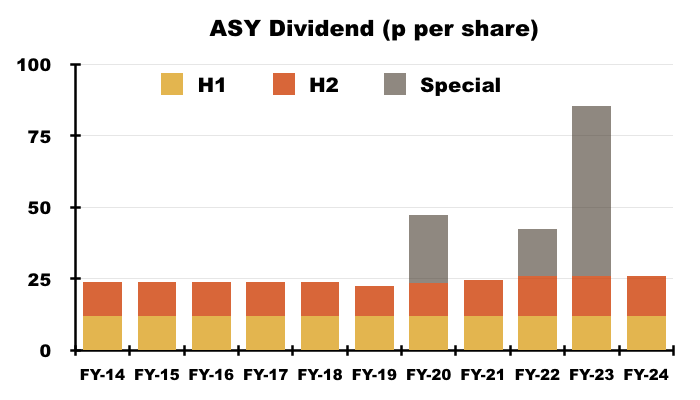

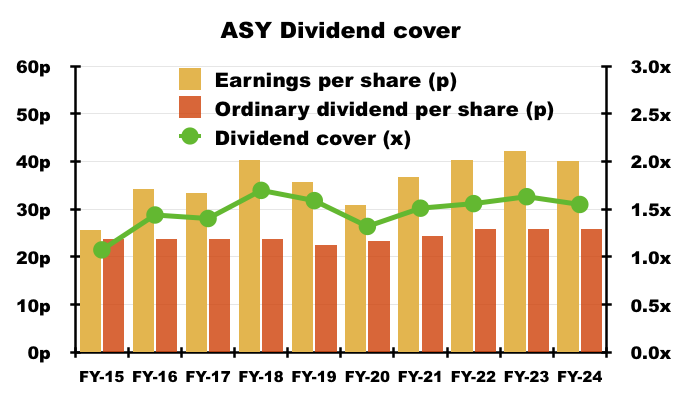

- This FY’s profit performance prompted the final dividend to be set at 14p per share that left the FY payout at 25.9p per share for the third consecutive year:

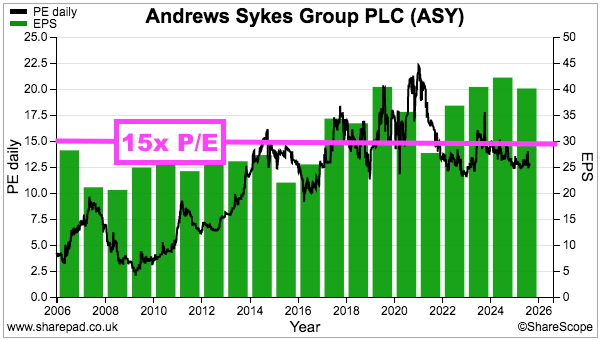

- FY earnings at 40.1p per share covered the FY dividend 1.55x versus a ten-year average of 1.48x:

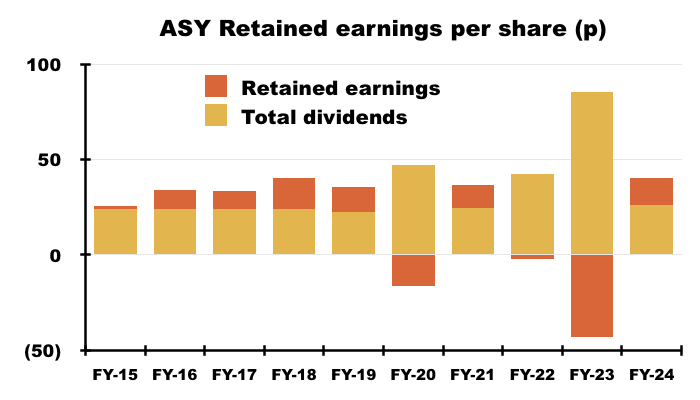

- During the last ten years, ASY has earned an aggregate 360p per share of which 343p per share has been distributed via ordinary/special payouts. The low level of retained earnings has in turn led to some very appealing returns on equity (see Financials: balance sheet and return on equity):

UK

- ASY can trace its UK Sykes history back to the 1850s and its UK Andrews history back to the 1960s:

- The combined group today offers a trade-only nationwide rental service supplying pumping equipment, air conditioners, air purifiers, chillers, heaters, boilers, dehumidifiers and ventilation units:

- ASY’s competitive edge is based upon depots providing first-class 24/7/365 customer service…

“By providing a premium level of service 24 hours per day, 365 days per year, we have become the preferred suppliers to many major businesses and operations spanning a huge range of industries and geographic locations. Our reputation for providing high levels of training to our staff whilst maintaining a strict health and safety workplace, within an environmentally conscious culture, makes us an employer of choice for our industry.”

- …stocking the best and most relevant equipment for different clients…

“Continual investment in new technology ensures that we provide our customers with new solutions to overcome their operational challenges. We constantly review and refresh our fleet of rental equipment to ensure that we set the standards within the rental industry throughout the UK, Europe and the Middle East.”

- …and offering “bespoke solutions” that perhaps not every competitor can supply:

“[ASY] is one of the market leaders in the rental of specialist hire equipment, offering bespoke solutions to our customers for their temporary or emergency needs“.

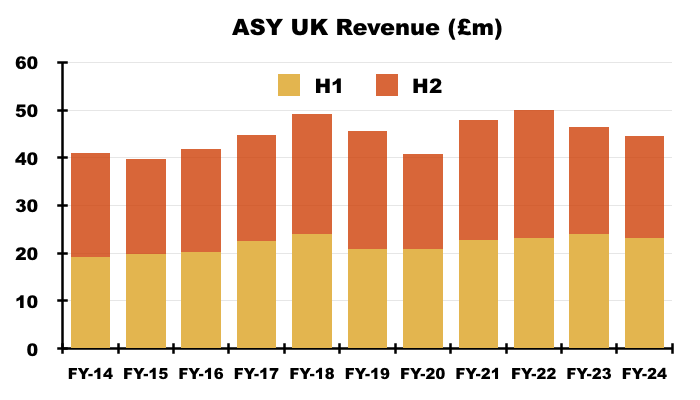

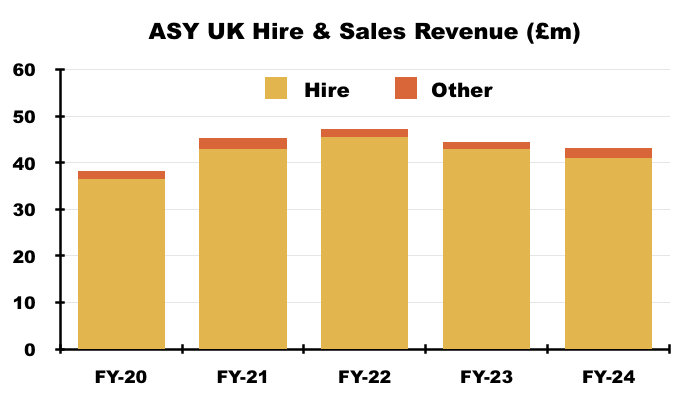

- Total FY UK revenue declined 4% to £44.7m with the shortfall spread evenly across H1 and H2:

- The revenue decline was due primarily to the chilliest UK summer since 2015:

“This [UK] result was reflective of the poor summer weather experienced with the UK having the lowest average summer temperature since 2015, mitigated by commercial successes in the early lease exit from previously vacated properties.”

- ASY’s UK revenue is dominated by the group’s UK Hire and Sales division.

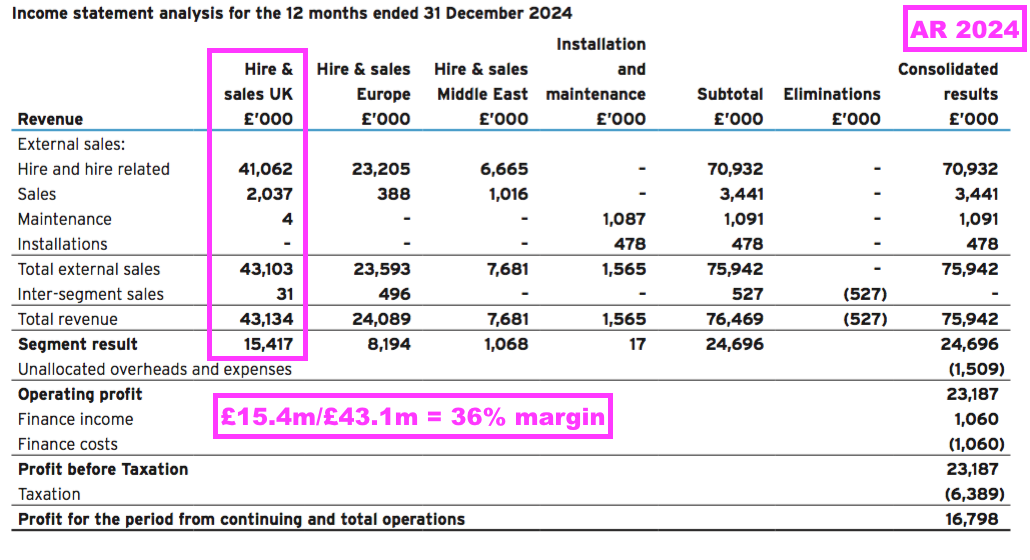

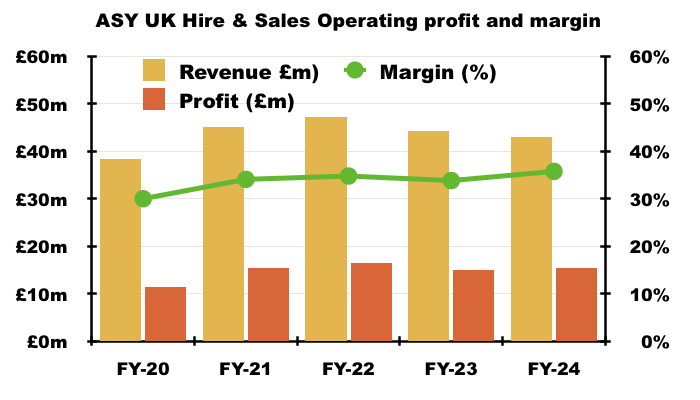

- During this FY, UK Hire and Sales represented 57% of group revenue and 62% of group profit, which led to a super divisional margin of 36%:

- The UK Hire and Sales FY margin has surpassed 30% ever since ASY separated its UK and European divisional reporting during FY 2020:

- The main UK division’s 36% margin was supported by the aforementioned reversals to expected property-closure costs:

“This [UK] result was reflective of the poor summer weather experienced with the UK having the lowest average summer temperature since 2015, mitigated by commercial successes in the early lease exit from previously vacated properties.”

- The property-closure reversals helped lift FY profit for the main UK division by 3%.

- Revenue from the main UK division is generated almost entirely from hire activities:

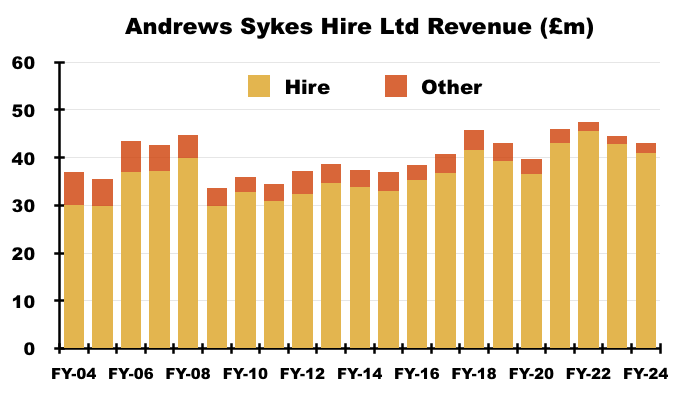

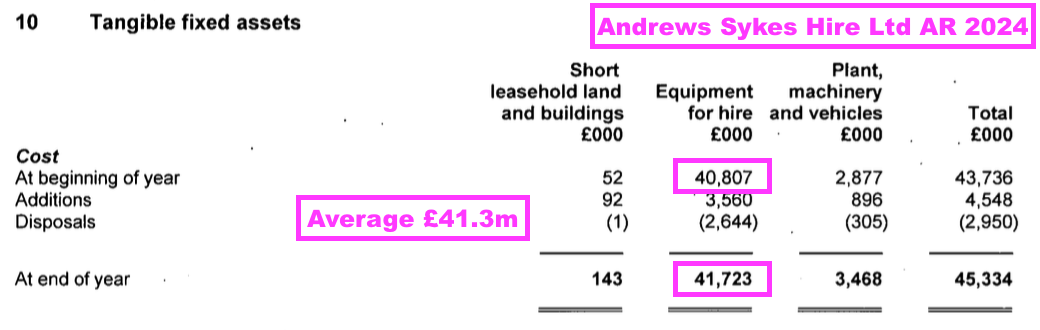

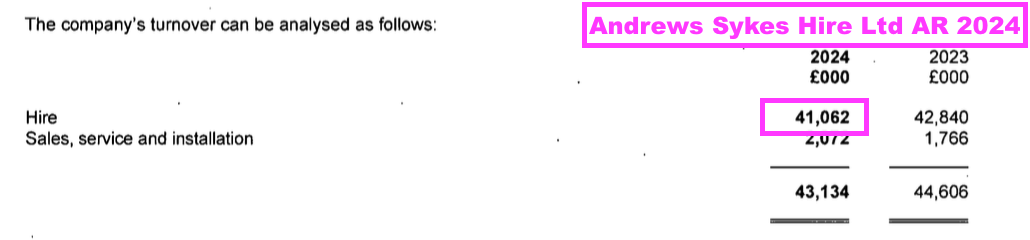

- The main UK division effectively reflects the progress of ASY’s main UK subsidiary, Andrews Sykes Hire Ltd, for which Companies House shows the following revenue:

- UK hire revenue has advanced from £34m to £41m during the ten years to this FY — equivalent to a very modest 1.9% CAGR.

- This FY disclosed the following UK growth rates for two categories of hire equipment:

“Air conditioning hire was down £2.8m or 33.9% on the prior year. Pump hire continues to grow with revenues at record levels for the seventh year in a row and 2.0% higher than 2023.”

- UK air-conditioning hire revenue down £2.8m or 34% suggests such income declined from c£8.2m to c£5.4m during this FY.

- The comparable FY had reported UK air-con hire revenue down £1.3m or 14%:

[FY 2023] “The UK hire business experienced a 6% turnover decrease when compared to last year, driven by negative comparisons for our air conditioning division against an exceptional prior year which was aided by the record temperatures experienced in the UK during 2022… Current year air conditioning hire was down £1.3m or 14.0% on prior year.”

- I therefore calculate this FY and the comparable FY witnessed UK air-con hire revenue decline an aggregate £4.1m or 43% from c£9.5m to c£5.4m.

- UK air-con revenue peaked during FY 2022, when a 40-degree summer lifted such income by 36% from c£7.0m to c£9.5m. This FY’s UK air-con revenue was therefore c23% below the c£7.0m level recorded for FY 2021.

- This FY’s air-con revenue of £5.4m supported c13% of this FY’s UK hire revenue.

- UK progress seems dominated by pump hire, with such revenue up 2% during this FY to limit the main UK division’s FY revenue shortfall to 3%.

- This FY’s 2% UK pump-hire improvement follows a 2% pump-hire advance during the comparable FY, a 4% advance during FY 2022, a 16% advance during FY 2021 and a 3% advance during FY 2020.

- UK pump-hire revenue has therefore gained c29% since FY 2019. UK pump-hire revenue has in fact achieved “record levels” for the last seven FYs.

- This FY did not mention chiller and boiler revenue, but Companies House reveals a 4% chiller and boiler FY revenue shortfall within ASY’s main UK subsidiary:

[Andrews Sykes Hire Ltd AR 2024] “Chiller and boiler revenues have stabilised but remain under pressure and are 4% down on 2023.“

- The 4% UK chiller and boiler shortfall follows a 12% reduction during the comparable FY, a 14% reduction during FY 2022 and a 7% reduction during FY 2021.

- ASY’s website says the UK operation trades from 35 depots versus 32 cited within my comparable FY review…

- …although this FY oddly repeated the comparable FY (and the FY before that) and said the main UK subsidiary operates from 22 locations:

“Our main UK trading subsidiary, Andrews Sykes Hire, has 22 locations covering the UK and employing around 280 members of staff.“

- This FY recapped how seven UK depots were amalgamated into two larger sites:

“Restructuring provision relates to the continuing property relocation within the UK. During 2022, four properties were vacated and merged into one large consolidated site. The associated costs involved included expected move costs and redundancy. The majority of these costs were incurred during 2023. During the previous year, three further property locations were vacated and merged into one larger facility. The associated costs involved included expected move costs and other associated landlord costs. The majority of these costs were incurred during 2024.“

- Exiting those seven UK sites led to the aforementioned “commercial negotiations for the early exit of previously vacated lease properties“ that created the aforementioned £820k credit to this FY’s profit.

- ASY’s UK property relocations have not yet improved the utilisation of the UK hire fleet. UK hire revenue compared to the original cost of the UK hire equipment remains at 1x (see Financials: hire revenue and hire equipment).

- Nor have the UK depot relocations really assisted the main UK subsidiary’s employee productivity (see Financials: margin and employees).

- ASY’s UK operations include installing and maintaining permanent air-conditioning systems, revenue from which has rarely generated a material profit (see Other).

- Total FY UK revenue represented 58.8% of group revenue — the lowest-ever FY proportion for ASY’s domestic market:

- Total H2 UK revenue represented 57.1% of group H2 revenue:

Europe

- ASY’s European operations consist of the following six countries and 15 depots:

- Netherlands:

- Established 1971

- 4 depots (Amsterdam, Bleiswijk, Hoogeveen, Oirschot)

- Belgium:

- Established 2007

- 3 depots (Antwerp, Brussels, Kortrijk)

- Italy:

- Established 2011

- 4 depots (Bologna, Milan, Toscana, Verona)

- Switzerland:

- Established 2013

- 2 depots (Geneva, Zurich)

- Luxembourg:

- Established 2014

- 1 depot (Luxembourg)

- Germany:

- Established 2023

- 1 depot (Frechen)

- Netherlands:

- The European operations have expanded faster than the UK operations.

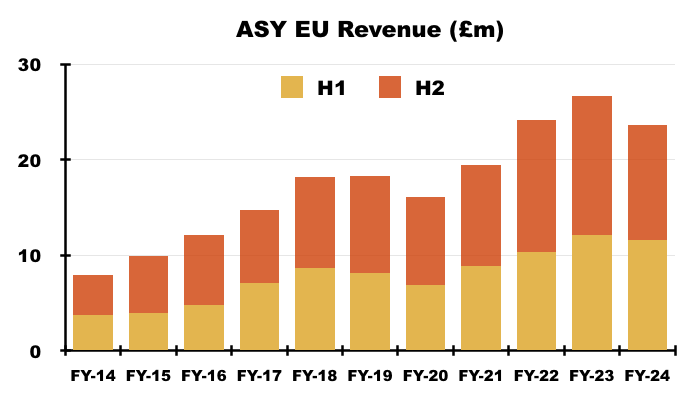

- Between FY 2013 and the comparable FY for example, European revenue advanced from £10.4m to £26.7m to increase the European proportion of group turnover from 17% to 34%.

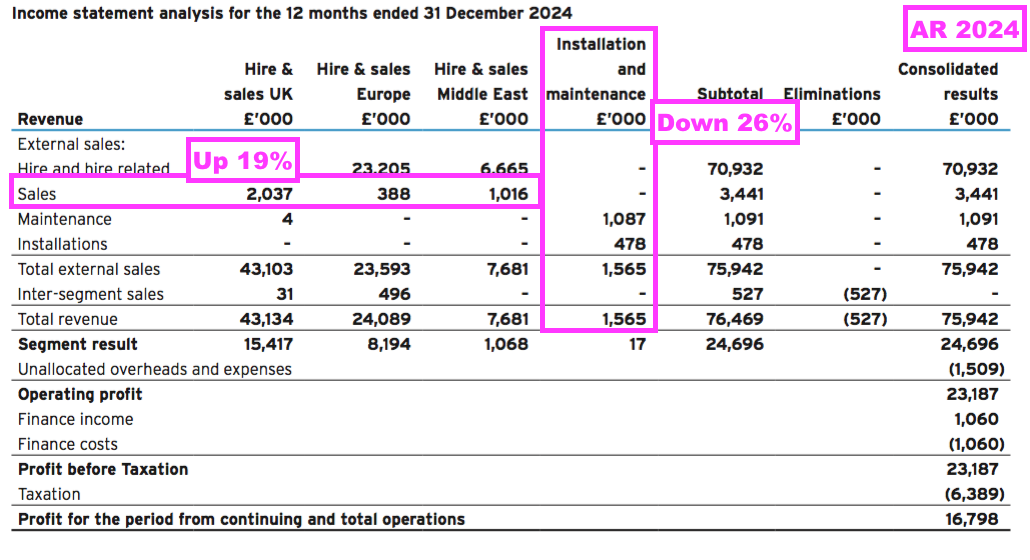

- But this FY witnessed European revenue drop 12% to £23.6m to support 31% of group turnover:

- £2.2m of the £3.1m reduction to FY European revenue related to the aforementioned French depot closures and currency movements:

“£1.5 million of the [European] revenue reduction was a result of ceasing our loss making French operations… Stronger Sterling exchange rates also negatively impacting our European subsidiaries reported revenues by £0.7 million as compared to 2023.“

- The preceding H1 revealed the closed French depots had accounted for £1m of lost H1 revenue:

[H1 2024] “This decrease was predominantly due to the loss of approximately £1.0 million of turnover from our loss making French operation which, as previously reported, was closed with effect from November 2023.”

- The closed French depots must therefore have accounted for £0.5m of lost H2 revenue…

- …which does not entirely explain why H2 European revenue dropped 17.5%, or £2.5m, to £12.0m.

- Alongside adverse currency movements, the European depots appeared to suffer from this FY’s heatwave absence. This FY confirmed Europe, similar to the UK, experienced “cooler summer temperatures”:

“Northern Europe in particular was impacted by the same cooler summer temperatures as seen in the UK and has been reflected in decreased chiller and air conditioning hire revenues.”

- In fact, every European market reported lower (or “limited“) FY revenue:

- Netherlands: revenue down 3%;

- Belgium: revenue down 21%;

- Luxembourg: revenue down 28%;

- Italy: revenue down 7%;

- Switzerland: revenue down 28%, and;

- Germany: “limited” revenue.

- Similar to the main UK division, European revenue is dominated by hire activities:

- Unlike the UK division, the European operations do not have an illustrious heritage of supplying water pumps. ASY’s (Middle East!) website reveals the group’s Italian subsidiary became the “first European location outside the UK to offer pump-hire services” during FY 2021.

- FY European revenue excluding France declined 6%, and I surmise the Netherlands — with its FY revenue down only 3% versus 20%-plus declines in Belgium, Luxembourg and Switzerland — is by some distance ASY’s largest European market.

- This FY was very difficult for Belgium, Luxembourg and Switzerland, but the trio had lifted revenue by 91%, 101% and 69% respectively throughout the preceding three FYs.

- Italy endured a rough H2, as the country’s FY sales fell 7% despite H1 sales gaining 11%. Note the preceding three FYs had witnessed Italian revenue gain 20%, 73% and 25%.

- The comparable FY announced the opening of ASY’s first German depot:

[FY 2023] “At the same time we are pleased to announce the incorporation of our new subsidiary, Klimamieten AS GmbH, in Germany and look forward to the development of this exciting market.”

- The German market has not been as “exciting” as expected. This FY owned up to the new German depot’s “limited revenue generated so far, undoubtedly impacted by the wider stagnant German economic situation.”

- Future German expansion may therefore be slow going, which has been the case at all of ASY’s European operations.

- ASY opened its first European depot during 1971 and by 2011 operated from only six European locations. Following the French exit, European depots have increased from those six to 15.

- The exit from France — which between 2011 and 2021 expanded from zero to six depots — emphasises European success is not guaranteed.

- As well as unfavourable weather conditions, ASY’s European subsidiaries are each dependent on only a handful of depots:

- Significant progress or difficulties at an individual depot can therefore have a notable impact on the performance of the associated European subsidiary.

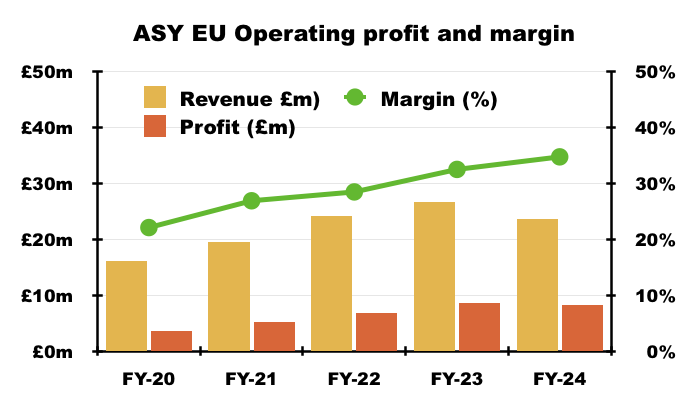

- Despite the small number of European depots, profitability across the continent is superb. Closing the loss-making French depots helped the combined European operations enjoy a lovely 34% margin during this FY:

- That 34% margin could improve further should European revenue rebound during FY 2025.

- The European FY margin has increased every year since it was first disclosed during FY 2020:

Middle East

- ASY’s Middle Eastern operations were established during 1976 and presently consist of the following six countries and nine depots:

- United Arab Emirates (Sharjah, Abu Dhabi, Dubai and Ruwais);

- Qatar (Doha);

- Oman (Muscat);

- Bahrain (Sitra);

- Kuwait (Kuwait City), and;

- Saudi Arabia (Abqaiq).

- The Middle Eastern depots supply only water pumps and equipment for ‘dewatering’, a process that lowers the groundwater table for excavation:

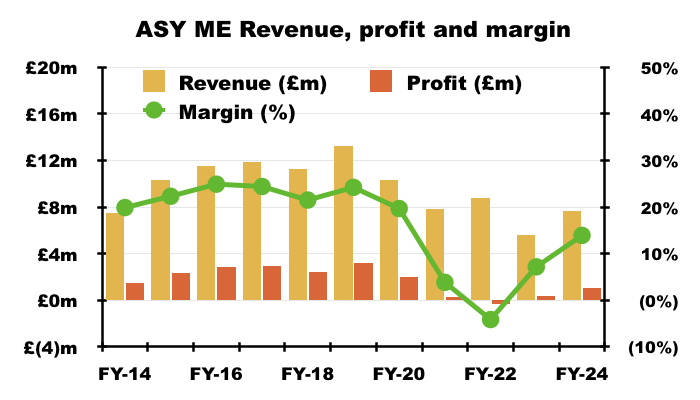

- Middle Eastern progress has recovered following a difficult few years.

- To recap, between FY 2019 and the comparable FY, Middle Eastern revenue collapsed from more than £13m to less than £6m while profit of more than £3m plunged to just £0.4m:

- Amid the division’s lack of new projects alongside customers not settling their bills, the comparable FY reported new local management was undertaking a turnaround:

[FY 2023] “New local management has been installed during the current year and a turnaround of this business is underway. It is pleasing that core hire revenues in the second half of the year are 38.1% up on the first half of the year and in line with that generated in the previous year. Management is confident of a return to increasing profitability in the Middle East.”

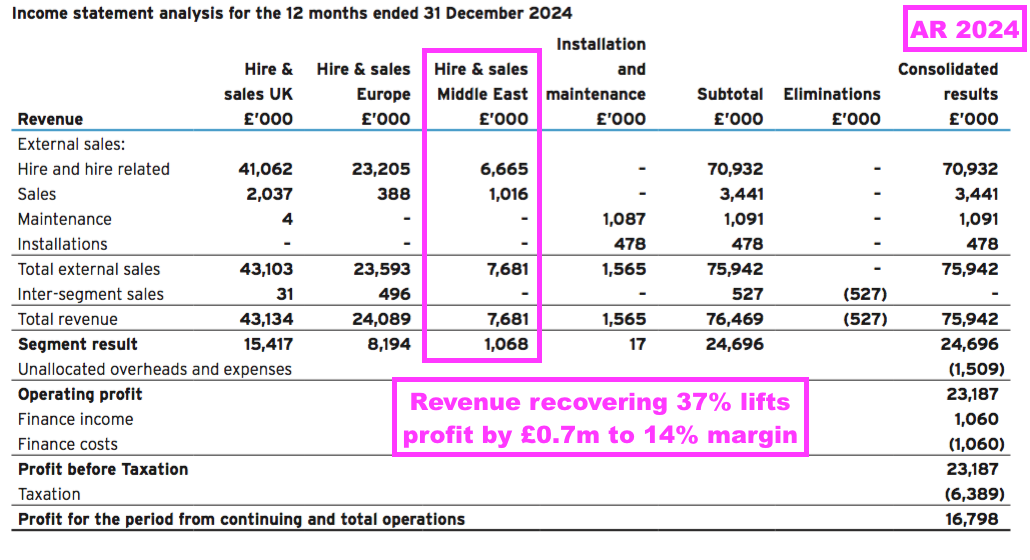

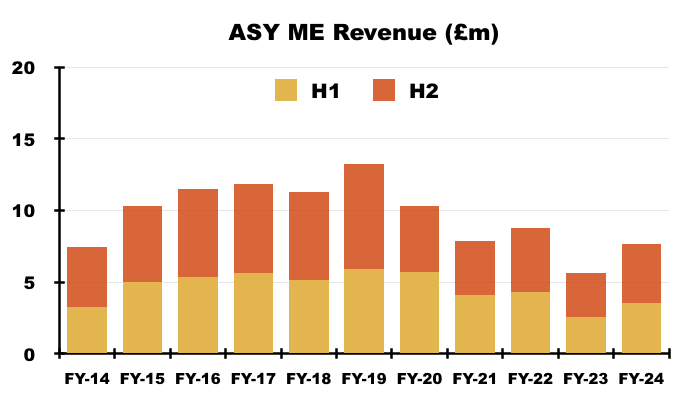

- This FY reported FY Middle Eastern revenue up 37% to £7.7m to support 10% of group FY revenue:

- FY Middle Eastern profit meanwhile improved by £0.7m to £1.1m, in part due to lower bad debts:

“This [Middle Eastern] result marks a strong turnaround driven by the new local management who were installed during the summer of last year. The increased operating profit is reflective of the increased revenue allied with expected credit losses remaining under control, with a charge of £0.1 million in 2024 compared to £0.2 million in 2023.“

- This FY extended the recovery of Middle Eastern revenue since the H1 2023 low:

- H1 2023 revenue: £2.6m;

- H2 2023 revenue: £3.0m;

- H1 2024 revenue: £3.6m, and;

- H2 2024 revenue: £4.1m:

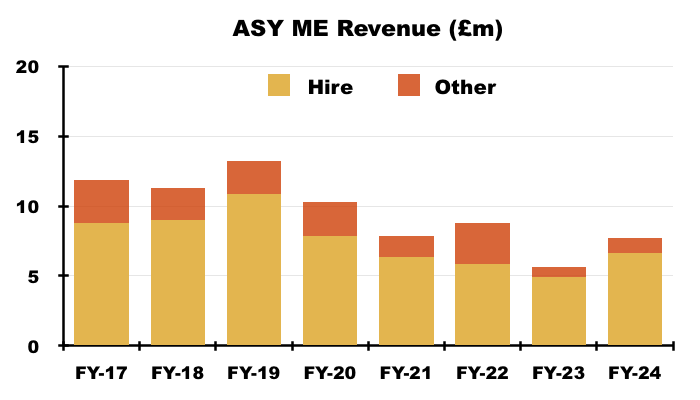

- FY Middle Eastern revenue from hire activities at £6.7m was the highest since FY 2020 (£7.9m):

- This FY confirmed ASY’s (re-)entry into Saudi Arabia and described the country as a “significant growth opportunity“:

“During the year we have been working on plans to enter the Saudi Arabian market which is currently experiencing a well publicised construction boom in an effort to diversify the Saudi Arabian economy. We are delighted to announce that a new subsidiary incorporated in Saudi Arabia opened in early 2025 and will be managed by our UAE management team who have done such a good job in turning around our existing business in the Middle East.

This market represents a significant growth opportunity in 2025 and beyond.”

- The new Saudi Arabian subsidiary does not represent ASY’s first venture into the country. ASY’s website reveals Oasis Sykes opened in Saudi Arabia during 1976, while an associated £164k investment was written off during FY 2017:

[FY 2017] “The above investment represented a 40% interest in the ordinary share capital of Oasis Sykes Limited, a company incorporated in Saudi Arabia and having an issued share capital of £410,000. The investment was not accounted for as an associate as the group does not and is unable to exercise significant influence, including decisions concerning the declaration and payments of dividends. Dividends were accounted for on a receipts basis, no amounts were received in the current or preceding period. During the current year, the directors performed a review of the operation and have formed the opinion that the carrying value in the books is not supported by underlying assets and there are no realistic prospects of a recovery in the future. Accordingly, the investment has been written off as its fair value is considered to be negligible.”

- At its FY 2019 peak, the Middle Eastern division supported 17% of group revenue and enjoyed a 20% profit margin, which perhaps explains why ASY has persisted with what was once a lucrative region.

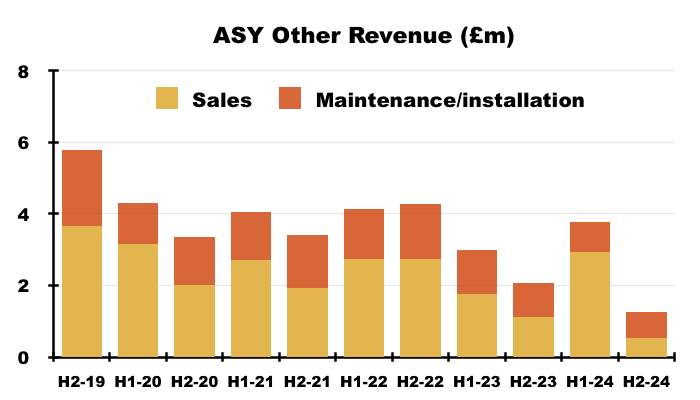

Other

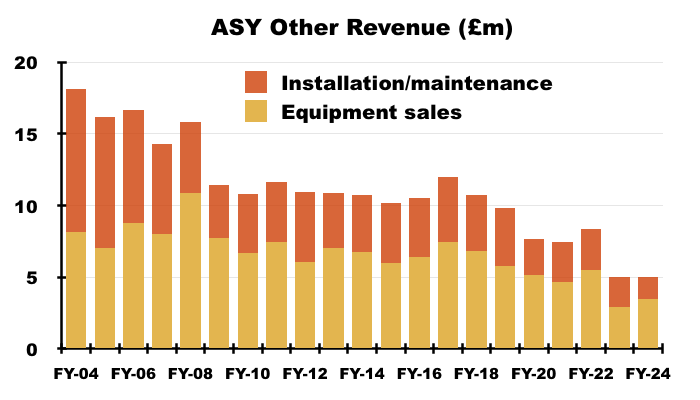

- ASY’s Other activities — involving equipment sales and the installation/maintenance of permanent air-conditioning systems — still appear in terminal decline:

- Although FY revenue from equipment sales gained £0.5m to £3.4m, FY revenue from installation/maintenance lost £0.6m to £1.6m:

- Other revenue proved very unpredictable during this FY, with the H2 contribution of £1.2m the weakest six-month effort since at least FY 2018:

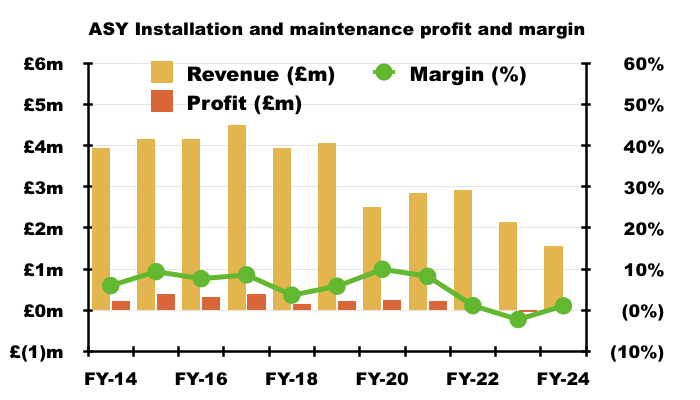

- Profit from installation and maintenance services has been negligible for years:

- Profit from equipment sales has also been questionable.

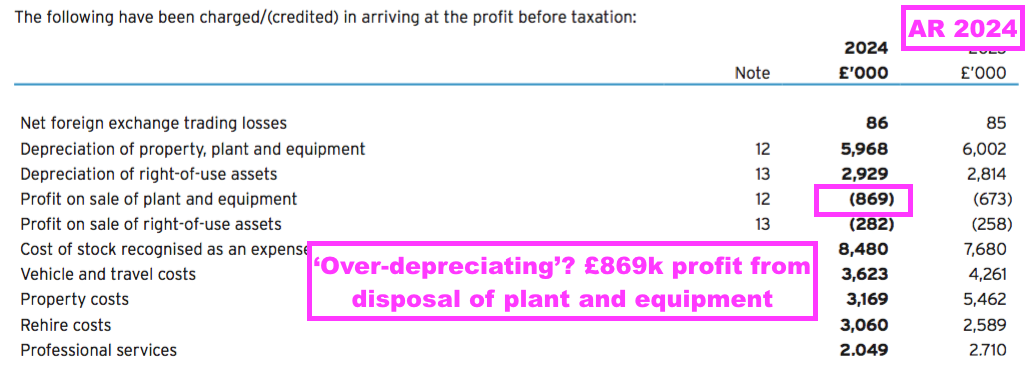

- For example, this FY confirmed stock sold was £8.5m:

“The cost of stock recognised as an expense in the period was £8,480,000 (2023: £7,680,000)“

- Equipment sales of £3.4m versus stock sold of £8.5m suggests the equipment was sold at a £5.1m loss.

- But this FY included new text about revenue recognition:

“Hire-related activities including delivery, collection and labour charges and the provision of fuel-management services are considered to be unbundled from the underlying rental lease and are recognised on a point-in-time basis in accordance with IFRS 15.”

- ASY’s fuel-management services involve the supply of oil and gas to customers to power their hired boilers, heaters and pumps.

- Fuel expenditure can be significant for customers. ASY’s fuel-management case studies indicate oil for industrial boilers costs up to £4k a week.

- I therefore believe the £8.5m cost of stock includes fuel sold to customers. So contrary to my past conclusions, equipment sales may well be profitable!

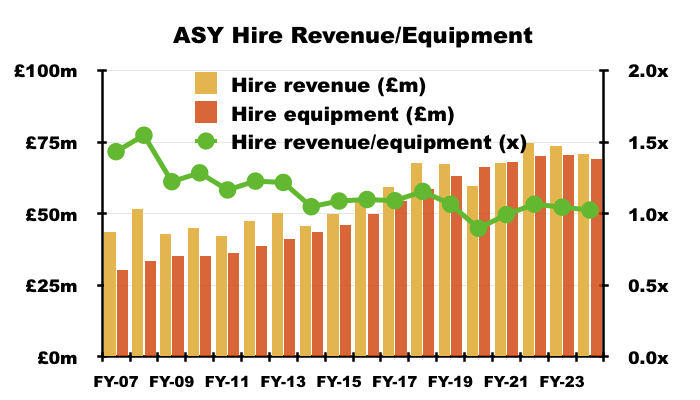

Financials: hire revenue and hire equipment

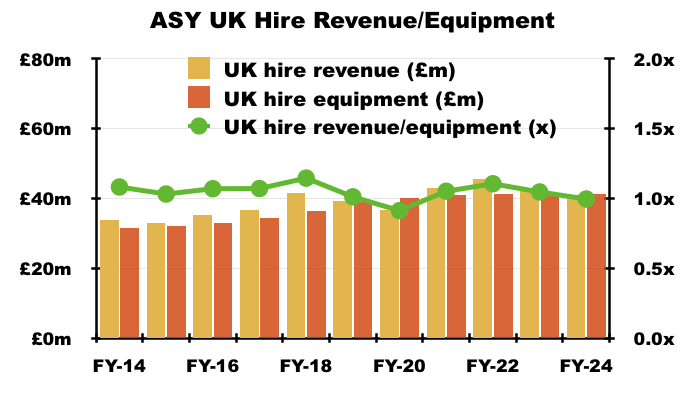

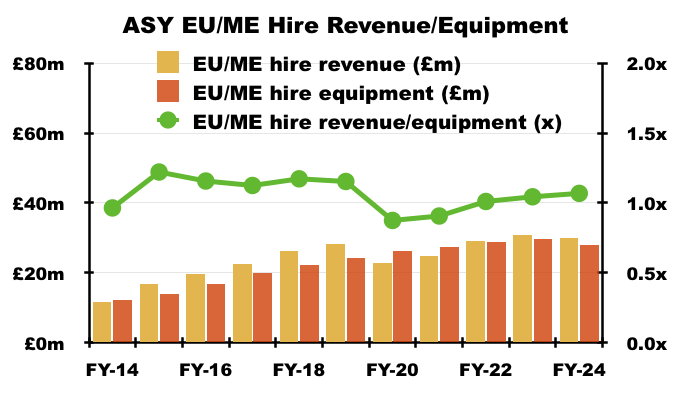

- The productivity of ASY’s hire equipment deteriorated slightly versus the comparable FY but remains within the range witnessed since FY 2014.

- I measure hire-equipment productivity by dividing hire revenue by the historical cost of the hire equipment. Using historical cost rather than book value avoids distortions caused by depreciation rates.

- FY hire revenue was £70.9m, while the historical cost of hire equipment averaged £69.2m:

- Hire revenue of £70.9m divided by an average hire-equipment cost of £69.2m gives 1.02x:

- Hire-equipment productivity greater than 1x means ASY recoups the cost of new hire equipment through hire (and hire-related) fees within a year.

- Hire-equipment productivity has bobbed between 0.90x and 1.16x since FY 2014, which suggests ASY has been unable to:

- Dramatically improve utilisation of its equipment, and/or;

- Raise hire fees faster than the cost of new equipment.

- Between FYs 2006 and 2013, hire-equipment productivity ranged between 1.17x and a remarkable 1.57x.

- The much higher rates from c15 years ago reflect some very impressive hire-equipment productivity from outside the group’s main UK subsidiary.

- However, the impressive hire-equipment productivity within Europe and the Middle East has since ‘normalised’ towards the UK rate.

- For perspective, ASY’s main UK subsidiary employed hire equipment that averaged a £41.3m historical cost during this FY…

- …while the subsidiary’s hire revenue was £41.1m:

- UK hire revenue of £41.1m divided by an average UK hire-equipment cost of £41.3m gives 1.00x:

- Within Europe and the Middle East, average hire-equipment employed was £27.9m (£69.2m less £41.3m) versus hire revenue of £29.9m (£70.9m less £41.1m) to give 1.07x for this FY:

- ASY being unable to really improve its group hire-equipment productivity is not ideal, but at least the measure is reasonably consistent.

- Note that the aforementioned new FY text about revenue recognition confirms hire revenue includes extra charges for delivery, collection, labour and fuel:

“Hire-related activities including delivery, collection and labour charges and the provision of fuel-management services are considered to be unbundled from the underlying rental lease and are recognised on a point-in-time basis in accordance with IFRS 15.”

- Hire-equipment productivity does therefore not entirely correlate to equipment rental rates, but could instead be influenced significantly by delivery, collection, labour and fuel charges.

- The aforementioned investment into additional water-treatment plant could improve ASY’s hire-equipment productivity:

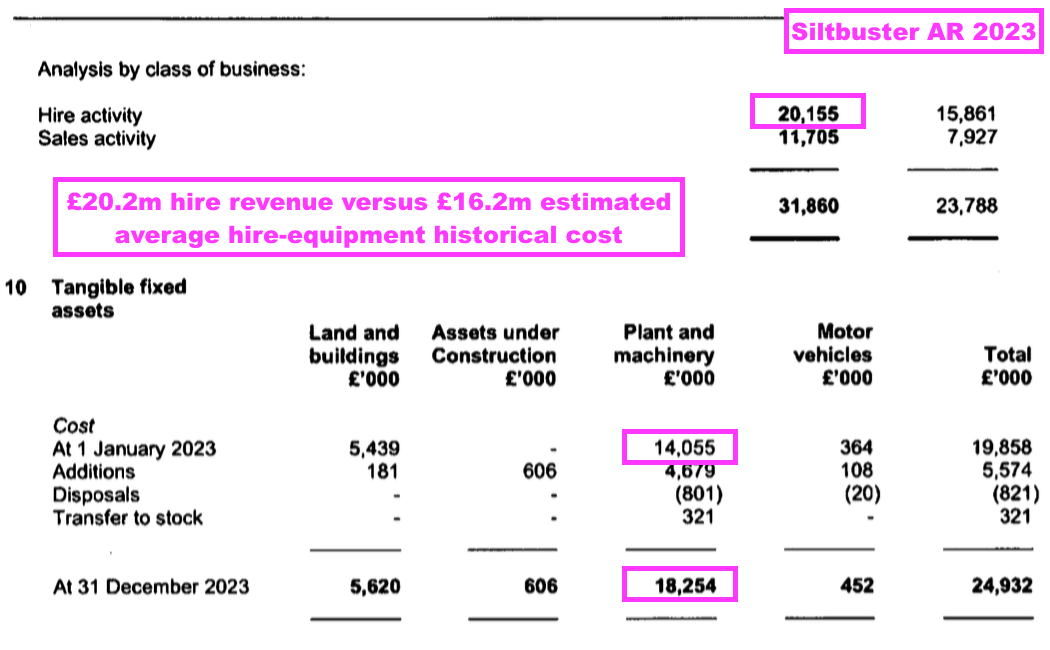

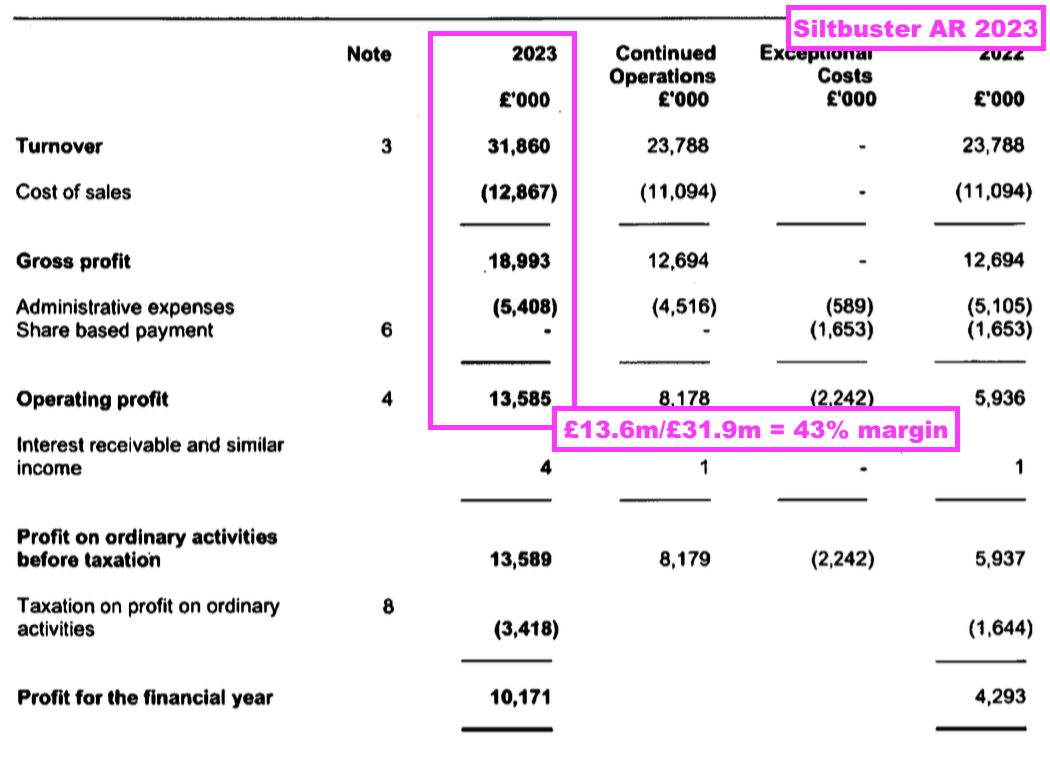

- An online search reveals Siltbuster claiming to be the “UK market leader in environmental solutions for responsive water and wastewater treatment” and operating “the UK’s largest rental fleet” within the sector:

- Companies House shows Siltbuster recording hire revenue of £20.2m and employing hire equipment with at most a £16.2m average historical cost during FY 2023:

- True, Siltbuster offers a far larger and more comprehensive water-treatment service than ASY does at present, but hire-equipment utilisation of at least 1.25x (£20.3m/£16.2m) shows the potential of this hire sub-sector.

- Indeed, Siltbuster’s 43% operating margin for FY 2023 strongly implies water treatment generally could be extremely lucrative for ASY:

Financials: margin and employees

- Charging customers extra for delivery, collection, labour and fuel might help explain ASY’s elevated margin.

- Or perhaps the group’s healthy profitability stems simply from customers paying a premium for the group’s “emergency” or “business critical” service:

“[ASY] is one of the market leaders in the rental of specialist hire equipment, offering bespoke solutions to our customers for their temporary or emergency needs“

…

“We aim to provide dependable high-quality services to our business partners in the UK, Northern Europe and the Middle East. We often provide business critical solutions to key businesses and are instrumental in helping our customers achieve their goals.”

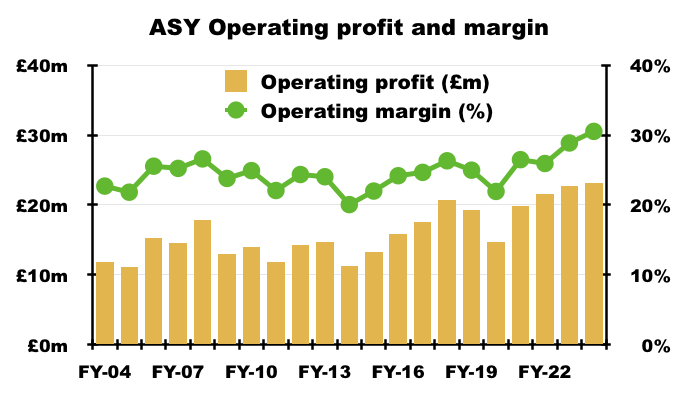

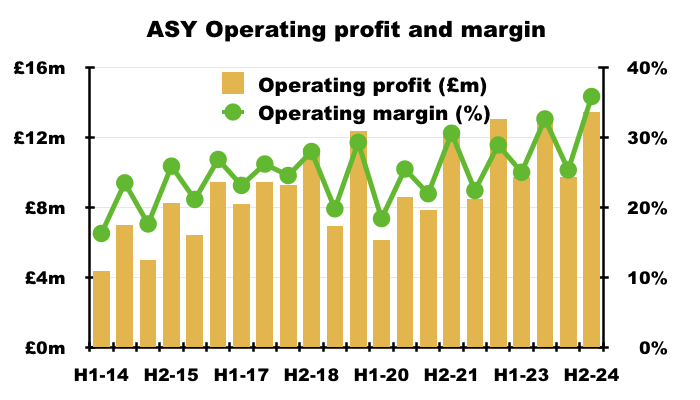

- The aforementioned profitability within the UK and European divisions ensured the group converted a record 30.5% of FY revenue into profit:

- A 25.3% H1 margin was followed by a terrific 35.8% H2 margin — the highest for any H1 or H2 since at least H1 2008:

- Supporting margins during this FY was a 10% reduction to administration expenses, which probably reflects the aforementioned £820k property-closure provision gain:

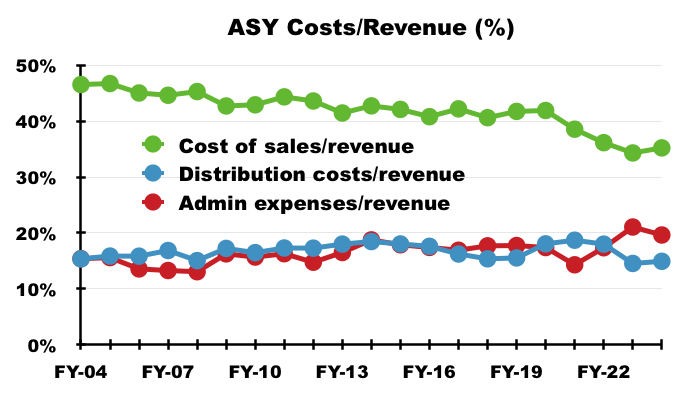

- ASY’s margin improvement over time has been underpinned by cost of sales reducing from more than 40% prior to FY 2021 to 35% for this FY:

- Although this FY’s margin was flattered by the aforementioned provision gains, ASY arguably suppresses its profit by ‘over depreciating’ its hire equipment (see Financials: cash flow and working capital).

- Employees remain ASY’s largest expense, and commendable workforce management continues to assist ASY’s profitability.

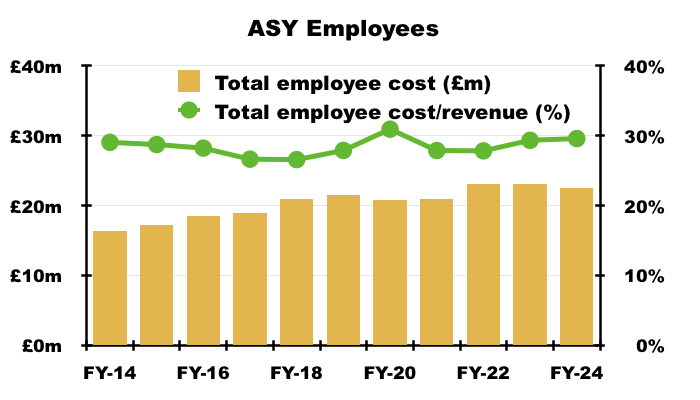

- FY salaries and other staff costs were trimmed 3% to £22.5m and absorbed 30% of FY revenue:

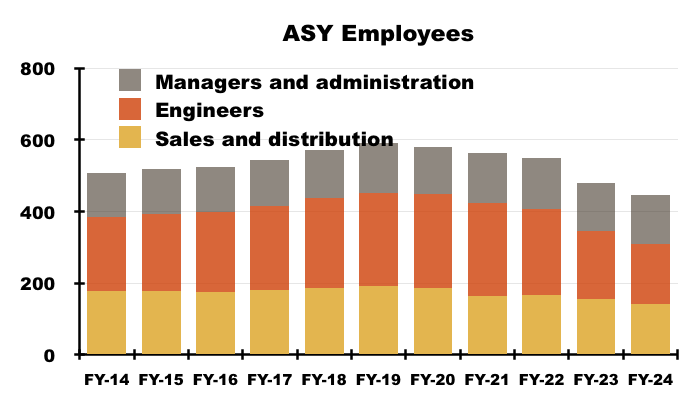

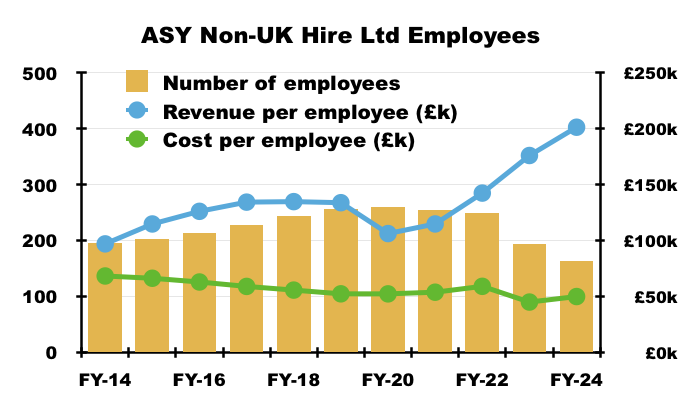

- Aided by the French depot closures, the FY headcount was reduced by 33, or 7%, to 446:

- 446 is the lowest headcount since at least FY 2004.

- This FY said the reduced headcount was “driven by operational efficiencies“.

- I speculate ASY’s hire equipment no longer requires as much maintenance as it once did.

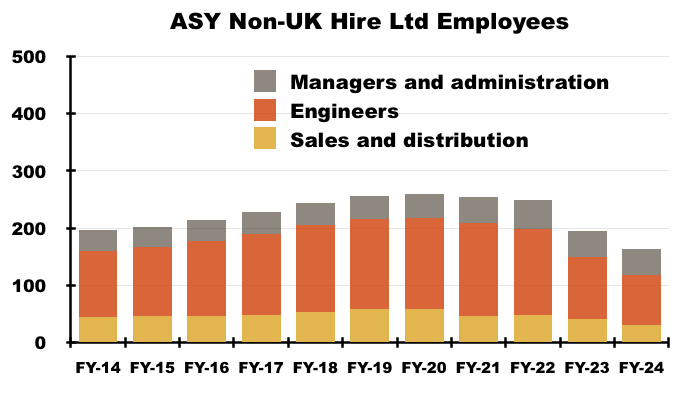

- The number of employed engineers has reduced by 93 to 167 between FY 2021 and this FY. Of those 93 fewer engineers, 75 were from outside the main UK subsidiary:

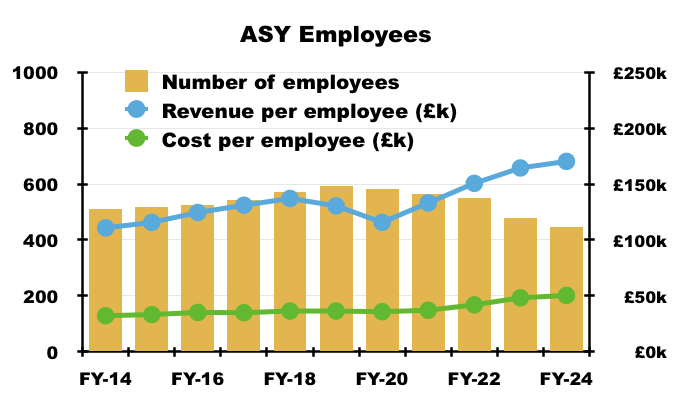

- Although ASY now employs some 21% fewer people versus FY 2021, FY revenue during the same time has improved by 1%.

- This FY witnessed the cost per employee reach a record £50k and revenue per employee reach a record £170k:

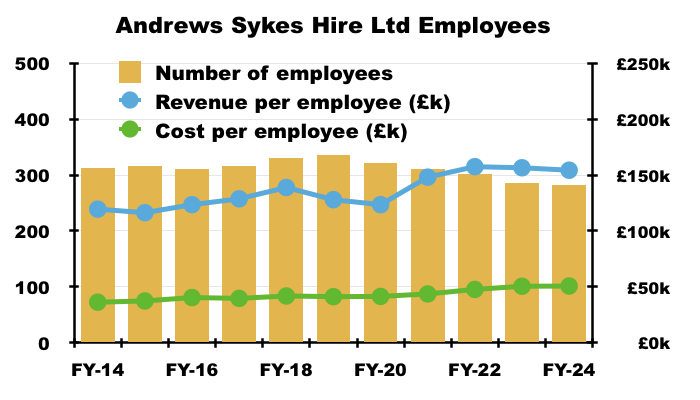

- Within ASY’s main UK subsidiary, this FY’s employee productivity and average salary remained at levels similar to the previous three FYs:

- This FY’s employee productivity therefore improved mostly outside the UK.

- Presumably through the French closures and the Middle Eastern recovery, revenue per employee outside the main UK subsidiary reached £201k during this FY:

- I am convinced ASY’s reduced headcount and its employee KPIs are not a coincidence:

- The absenteeism KPI is calculated by something called the Bradford Factor:

“The group uses Bradford Factor scoring across all entities, a common means of measuring worker absenteeism. In using this measure to manage absenteeism, the group has managed to keep overall staff absenteeism low. The increased staff absenteeism metric during the year was due to several employees going on long-term sick. The Board are pleased with the overall level as, excluding the long-term sick, the staff absenteeism % was comparable to the prior year. The group would seek a reduction in 2025.“

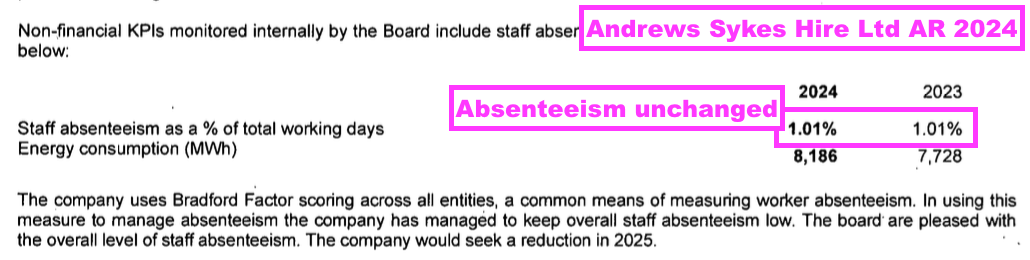

- This FY showed the absenteeism KPI increasing from 1.01% to 1.64% due to “several employees going on long-term sick“.

- ASY’s main UK subsidiary showed absenteeism unchanged for this FY…

- …implying the long-term sickness occurred overseas.

- Between FY 2020 and the comparable FY, group absenteeism had reduced from 1.67% to 1.54% to 1.42% to 1.01%.

- Every quoted company should publish an absenteeism KPI. Investors may then find fewer companies run primarily for the benefit of employees.

- My above analysis leads me to believe the pandemic and/or the fresh leadership appointed during FY 2021 has helped ASY find more efficient ways of working (see Boardroom).

Financials: cash flow and working capital

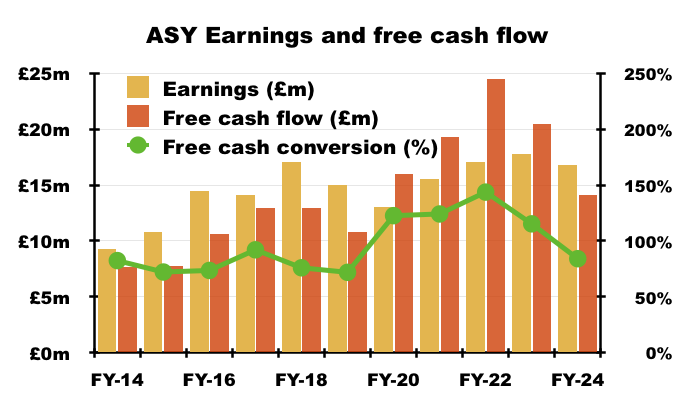

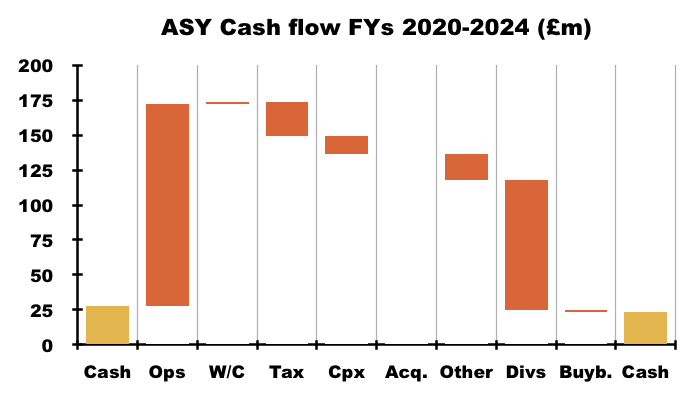

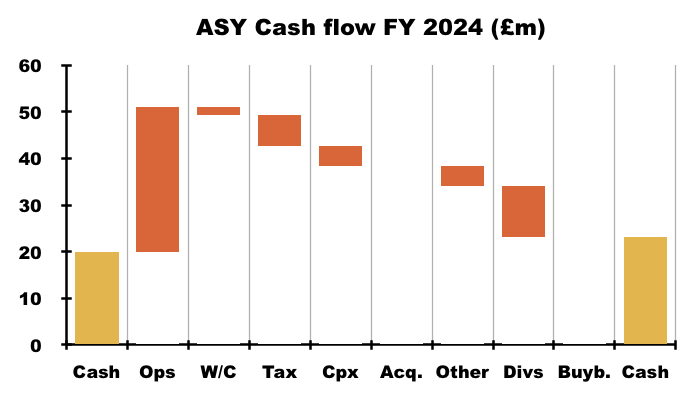

- ASY has developed an impressive record of converting earnings into free cash.

- During the four years between FY 2020 and FY 2023 for example, aggregate free cash flow exceeded aggregate reported earnings by a healthy £17m:

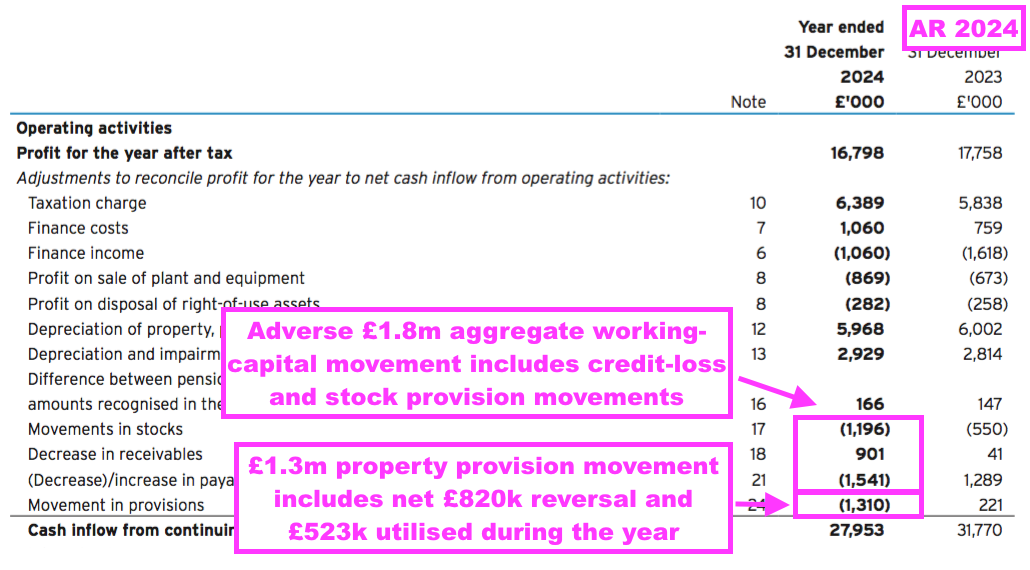

- For this FY, reported earnings of £16.8m translated into free cash of £14.1m. The relatively modest FY cash conversion was due primarily to:

- An adverse £1.8m working-capital movement, and;

- A net £1.3m reduction to property-closure provisions:

- For the prior four FYs, ASY’s cash conversion was bolstered by:

- A positive £3.0m aggregate working-capital movement, and;

- A net £2.0m aggregate reduction to property-closure provisions:

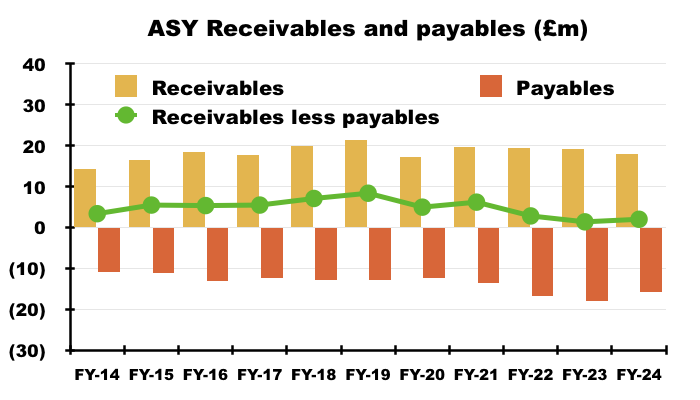

- ASY’s working-capital management has been particularly impressive during recent years, with receivables edging lower (i.e. payments collected more quickly) and payables edging higher (i.e. expenses paid more slowly):

- Between FY 2019 and this FY, the difference between receivables and payables has reduced from £8.4m to £2.0m, thereby releasing £6.4m for investment into extra stock.

- In fact, during the last five FYs, aggregate cash of £145m was generated through operations alongside an additional net £1m released from working capital:

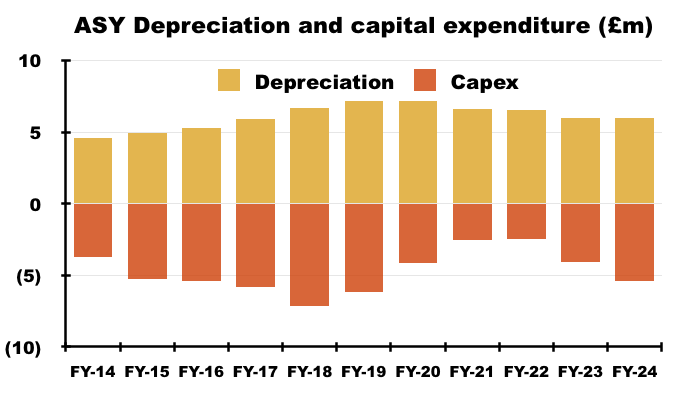

- Assisting cash conversion further is ASY’s prudent deprecation policy.

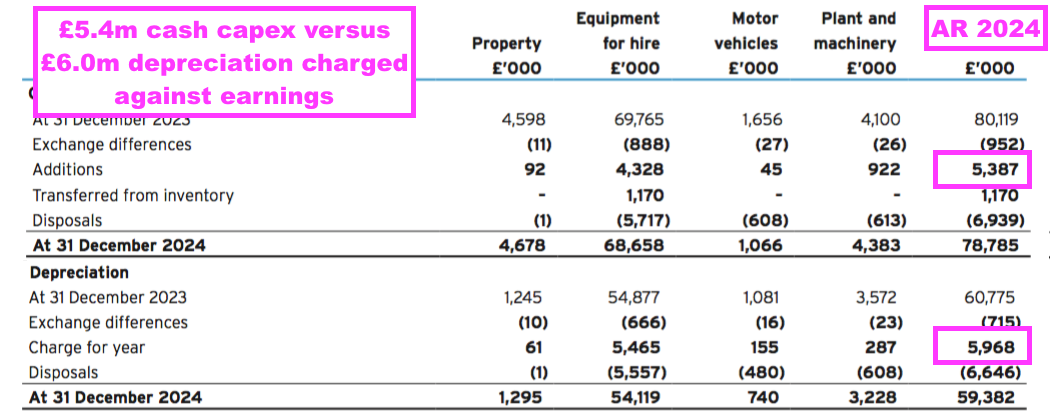

- This FY’s depreciation of property, plant and equipment was £6.0m versus FY cash capital expenditure of £5.4m:

- Depreciation has now exceeded cash capital expenditure every year since FY 2019:

- During the last five FYs, aggregate depreciation charged against profit was £32m versus an aggregate £19m capex.

- ASY’s cash flow movements are complicated by the group acquiring equipment as stock for resale but then capitalising a proportion of that stock into the hire fleet.

- This FY reported stock of £1.2m was transferred into the fleet…

“In addition, a further £1,170,000 of items held in stock at 31 December 2023 (2023: £2,522,000 items held in stock at 31 December 2022) have been capitalised in the hire fleet this year.”

- …and, in total, the five years to this FY have witnessed a £10m transfer.

- This £10m is arguably capital expenditure rather than stock investment, but the £10m plus the aforementioned £19m five-year capex is still less than the aforementioned £32m five-year depreciation charge.

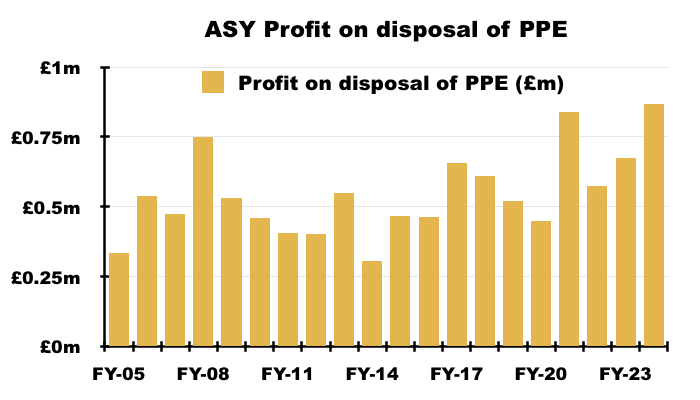

- ASY’s ‘over-depreciating’ its assets has resulted in asset disposals registering consistent gains over book value.

- This FY recorded an £869k profit from the disposal of plant and equipment:

- ASY has recorded a profit from the disposal of property, plant and equipment every year since at last FY 2005:

- This FY reiterated why fully depreciated equipment is retained:

“To provide sufficient asset availability for periods of extreme weather, the group routinely keeps Nil net book value items rather than scrap them.”

- This FY repeated why the disposal gains should not be extrapolated throughout ASY’s entire hire fleet:

“The profits on the disposal of hire assets represent occasional requests to sell hire assets, often to an existing customer, and are not considered by management to indicate that there is positive residual value in the entire hire assets portfolio. The group also considers market-based evidence from other comparable industry competitors when assessing the useful economic life of its assets.“

- ASY’s new auditor has become interested in ASY’s nil-valued assets. This FY’s single key audit matter concerned the depreciation policy:

“Property, plant and equipment is depreciated over the economic lives of the assets. Useful economic lives (UELs) are based on management’s estimates of the period that the assets will generate revenue, which are reviewed annually for continued appropriateness. This estimation impacts the depreciation expense recorded in the financial statements and the carrying value of these assets.

There are several points of judgement that management apply when setting the UELs and notably, due to various factors, there are a significant amount of hire assets held on the balance sheet at nil net book value but which are still generating revenue when required.”

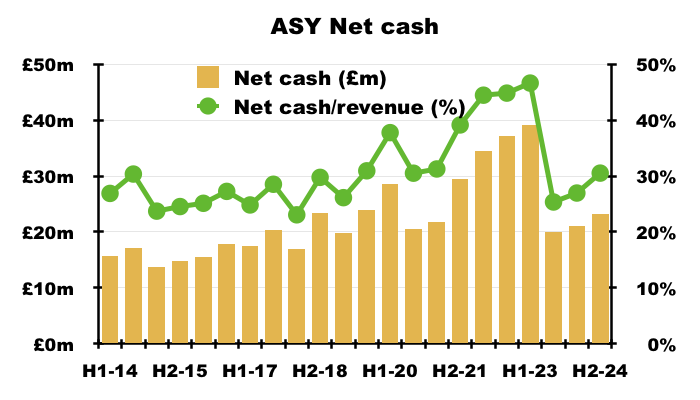

- This FY’s £14m free cash funded a £10.8m dividend payment and bolstered cash in the bank by £3.1m to £23.2m (55p per share):

- During the last five FYs, aggregate operating cash of £145m plus a £1m working-capital release less £19m capex plus £6m asset disposals left £133m to i) pay tax of £24m, ii) pay leases and debt reductions of £19m, and; iii) return a mighty £93m to shareholders through dividends:

Financials: balance sheet and return on equity

- ASY’s balance sheet remains free of bank debt and therefore this FY’s £23.2m cash position means net cash was equivalent to 31% of FY revenue:

- ASY has declared three special dividends during the past few years, but net cash at £23m may not be enough to fund a further extra payout just yet.

- The special-dividend benchmark appears to be £30m or more:

- When net cash reached £30m during FY 2020, a 23.7p per share/£10m special dividend was declared;

- When H1 2022 reported net cash at £31m, a 16.6p per share/£7m special dividend was declared, and;

- When H1 2023 reported net cash at £39m, a 59.4p per share/£25m special dividend was declared.

- Net cash reaching close to £30m may not take too long.

- Repeating this FY’s £14m free cash flow during both FY 2025 and FY 2026 would take the cash position to £29m assuming ordinary dividends remain at £11m per annum.

- An alternative to another special dividend could be occasional buybacks (see Boardroom).

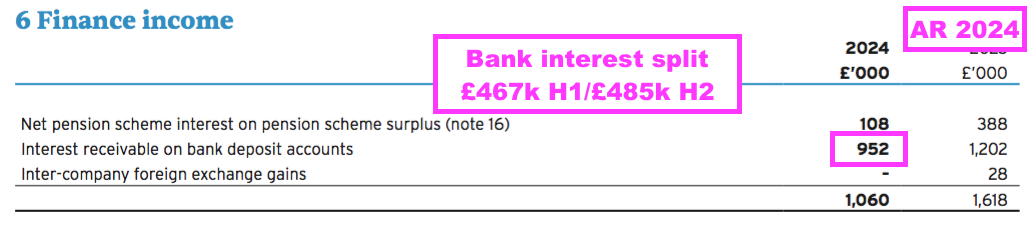

- This FY said the cash earned interest at a welcome 4.4%:

“Deposit accounts comprise instant access interest-bearing accounts and other short-term bank deposits with a maturity of three months or less on inception. Interest was received at an average floating rate of, approximately, 4.4% (2023: 4.3%).“

- Sure enough, FY bank interest of £952k implied a 4.4% return from the £21.6m average FY cash position:

- ASY’s bank interest improved from H1 to H2 — £467k versus £485k — which implied interest on the average H2 £22.1m cash was again 4.4%.

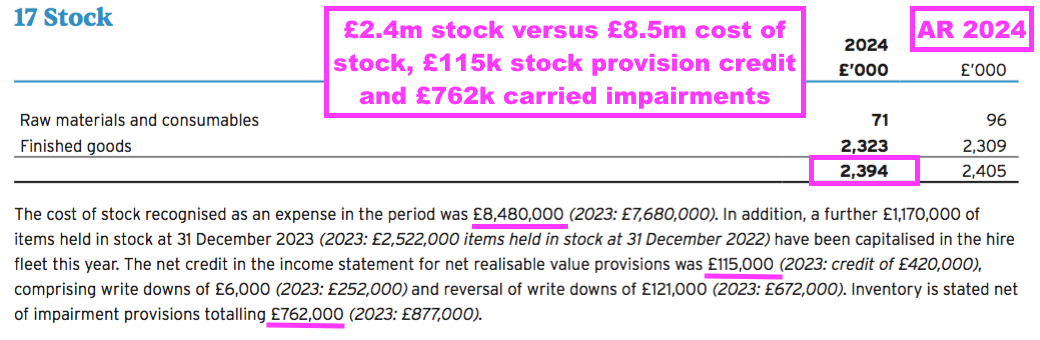

- This FY showed stock of £2.4m:

- The stock footnotes highlight further prudent accounting through another example of provision reversals.

- For both this FY and the comparable FY, profit gains were created after previous stock write-downs were reversed:

“The net credit in the income statement for net realisable value provisions was £115,000 (2023: credit of £420,000), comprising write downs of £6,000 (2023: £252,000) and reversal of write downs of £121,000 (2023: £672,000).”

- The stock provisioning seems significant to the carrying value of the stock. This FY said the £2.4m carrying value was calculated after an £0.8m write-down:

“Inventory is stated net of impairment provisions totalling £762,000 (2023: £877,000).“

- A £0.8m write-down equates to a very significant 32% of this FY’s stock value and may indicate ASY suffers from material levels of stock obsolesce or damage. The figures imply £8 of every £32 invested in stock is written off (before reversals!).

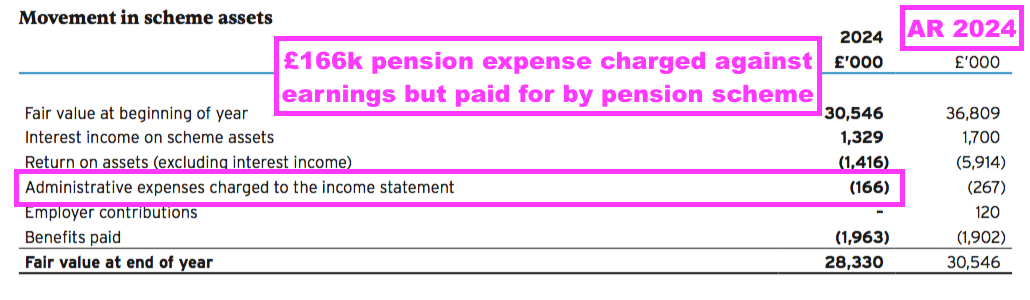

- ASY’s pension scheme remains interesting.

- H1 2023 announced the pension-scheme’s obligations had been “fully de-risked” though a buy-in with Canada Life, while the comparable FY then confirmed no cash contributions would be paid to the scheme during this FY:

[FY 2023] “This transaction, whilst significantly reducing the defined benefit pension scheme surplus recorded on the balance sheet, means that future liabilities are fully de-risked and the company will not be required to contribute significant cash payments into the pension scheme to fund adverse liability movements…

No cash contributions are to be made during 2024.”

- This FY indeed revealed no contributions were made…

“Consequently, the group has made total contributions to the pension scheme of £Nil during 2024 (2023: £120,000) and expects to make contributions of £Nil during 2025.”

- …and said no contributions should be made during FY 2025.

- Note this FY suggests ASY continues to accrue a pension-scheme expense against earnings that is actually funded by the pension scheme (and not shareholders!):

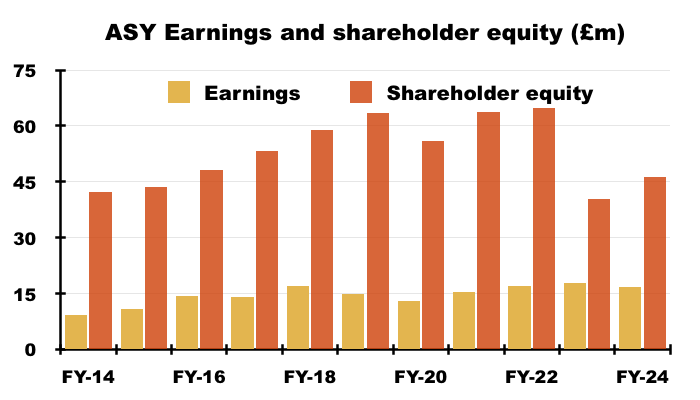

- ASY’s aforementioned record of distributing almost all its earnings through ordinary and special dividends leads to an incredible incremental return on equity.

- Between FY 2014 and this FY, reported earnings have gained £7.5m while net asset value has advanced only £4.1m:

- I would be delighted if ASY retained an extra £4.1m to deliver extra earnings of £7.5m during the next ten years.

- The underlying return on investment within ASY’s hire operations therefore appears superb.

- For example, during this FY, shareholder equity excluding the cash position averaged approximately £22m while earnings excluding bank interest were £16m — leading to a remarkable cash-adjusted conventional ROE in excess of 70%.

Boardroom

- ASY has been controlled by the Murray family since 1994, at which time Jacques-Gaston Murray employed his near-30% shareholding to force a boardroom reshuffle and appoint himself as non-executive chairman.

- By 2005, a mix of further share purchases and significant buybacks had increased Mr Murray’s holding to approximately 85%.

- Mr Murray maintained his controlling interest until 2008, at which point he transferred the holding to his sons Jean-Jacques Murray and Jean-Pierre Murray:

[RNS November 2008] “The Company has been notified today that on 26 October 2008, the Chairman, Mr Jacques-Gaston Murray, transferred his controlling interest in the Tristar Corporation in equal proportion to two trusts; the Jean-Jacques Murray Trust and the Jean-Pierre Murray Trust. Accordingly these two trusts are now the ultimate controlling parties of the Tristar Corporation and subsequently the ultimate controlling parties of the Company.

“The Tristar Corporation continues to control EOI Sykes Sarl which in turn has a beneficial interest in 36,377,213 ordinary shares of one pence each in the Company (‘Ordinary Shares’) representing approximately 82.17% of the Company’s issued share capital. As a result of this transaction, the beneficial interest of Mr Jacques-Gaston Murray has decreased from 37,687,369 to 1,310,156 Ordinary Shares representing approximately 2.96% of the issued share capital of the Company.”

- Mr Murray passed away during 2023 and the board is now led by Jean-Jacques Murray, who immediately succeeded his father as chairman and then took on executive duties during early 2024:

[RNS February 2024] “The Company announces the following changes to the Board of Andrews Sykes (the “Board”) with effect from 12 February 2024:

· Jean-Jacques Murray, will become Executive Chairman. Jean-Jacques Murray has been Non-Executive Chairman since June 2023 and prior to that was Non-Executive Vice-Chairman since February 2007.

· Jean-Pierre Murray will assume the role of Non-Executive Vice-Chairman. Jean-Pierre Murray has been a Non-Executive Director since August 2008.”

- Both Jean-Jacques Murray and Jean-Pierre Murray are long-time ASY board members; the former became a non-exec during 1994 while the latter became a non-exec during 2008.

- At the last count, the Murray family boasted a 90%/£194m shareholding.

- Jean-Jacques Murray becoming executive chairman remains very intriguing.

- After all:

- ASY had coped well employing just one board executive (ASY’s managing director) since 2011, and;

- The Murray family had previously never undertaken an executive ASY role since taking the controlling interest during 1994.

- I have previously speculated Jean-Jacques Murray might now be contemplating a corporate sale.

- But if a bid does not materialise, outside shareholders ought still to be treated well. This FY reiterated the benefits of the “presence and requirements of a long-standing majority shareholder”:

“The presence and requirements of a long-standing majority shareholder has resulted in a strategy with the key aim of creating long–term shareholder value.”

…

“Shareholder value in the medium term to long term is intended to be delivered by driving operational excellence across the group and growing within selected markets and geographies. The Board believes that the presence and requirements of a long-standing controlling shareholder helps focus the company’s strategy on long-term shareholder value creation.”

- Those benefits include the aforementioned three special dividends:

- The special payouts have been complemented by the very occasional buyback. The comparable FY witnessed the board authorise £1.9m for share repurchases at an average 644p per share — 25% greater than the recent 515p.

- This FY said the £1.9m purchase “enhanced earnings per share and were for the benefit of all shareholders“.

- The £1.9m buyback has yet to prove as positive an omen as ASY’s previous significant buyback. The shares have more than tripled since FYs 2010, 2011 and 2012, when an aggregate £3.1m was spent cancelling shares at a 155p average.

- Given the Murray family already owns 90% of the shares, I suspect most outside shareholders would prefer surplus cash to be distributed by additional special dividends rather than see the 10% free float squeezed even further.

- ASY has authorisation to acquire 12.5% of the share count (i.e. the Murray family could in theory buy out everybody else using ASY’s own cash!) and this FY reiterated further buybacks “may be made in the right circumstances if the necessary funds are available“.

- The special payments, the occasional buybacks — and the underlying cash-generative business that funds them! — go a long way to counterbalance the Murray family’s distinctive approach to corporate governance.

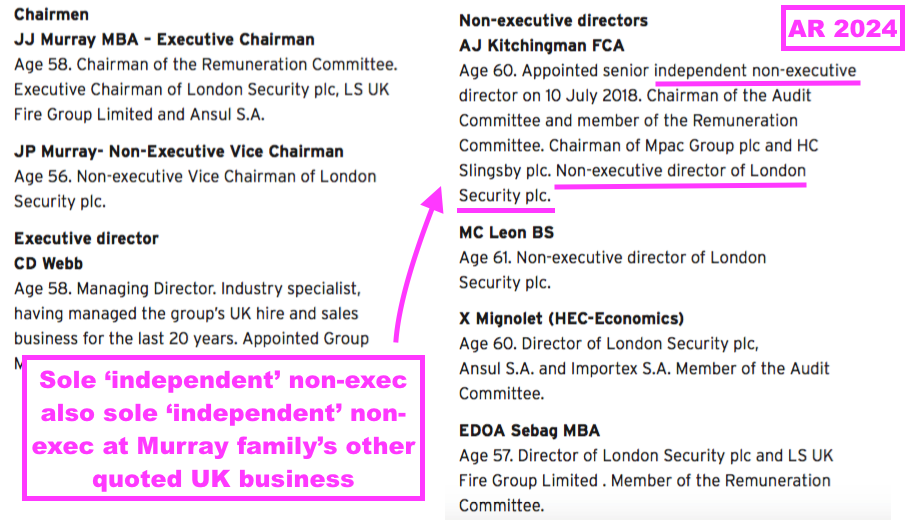

- Accompanying the two Murray directors on the board are:

- ASY’s managing director;

- Three non-independent non-executives, and;

- One independent non-executive:

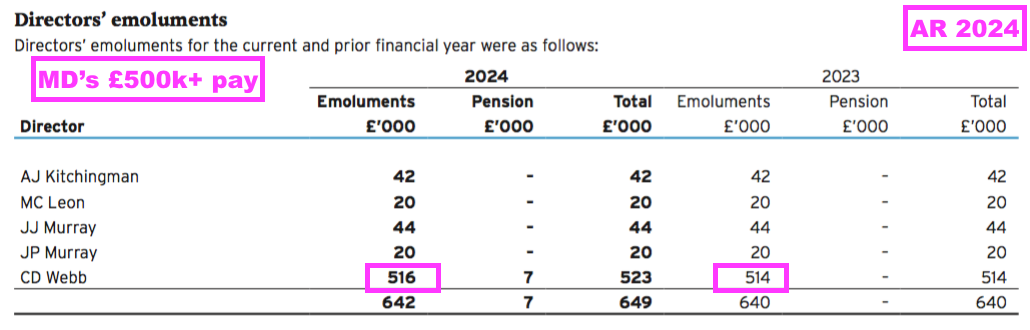

- The group MD seems a safe and loyal pair of hands. He took up his current position during Q1 2021 after leading ASY’s main UK subsidiary for 15 years.

- The group MD is assisted by the group finance director, who was also appointed during Q1 2021 but is not a board member.

- I speculate the Q1 2021 appointments of the group MD and FD alongside the aforementioned post-pandemic improvements to cash generation, operating margins and employee productivity are not a coincidence.

- Note that the MD owns no shares and does not seem underpaid:

- The most appealing feature of ASY’s board remuneration is the lack of an LTIP.

- The three non-independent non-executives are all long-time associates of the Murray family, and each has served as a non-exec far longer than the ‘best practice’ nine years (one non-exec was appointed during 1997 while the other two were appointed during 2007).

- ASY’s website implies not all of the non-independent non-execs are truly active board members:

[ASY website] “In order to reduce the administrative burden at Board meetings and to optimise the decision making process, I [Jean-Jacques Murray] often act as a conduit for the aggregated views and opinions of many of these non-independent directors.“

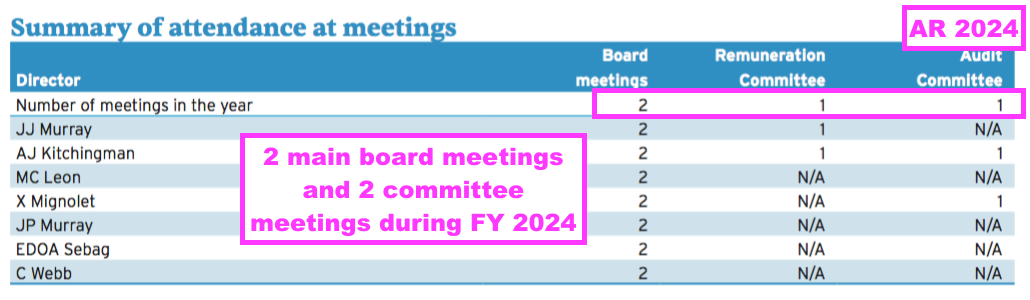

- The “administrative burden” of main board meetings may not be huge, given only two such meetings were held during this FY, the comparable FY and the FY before that:

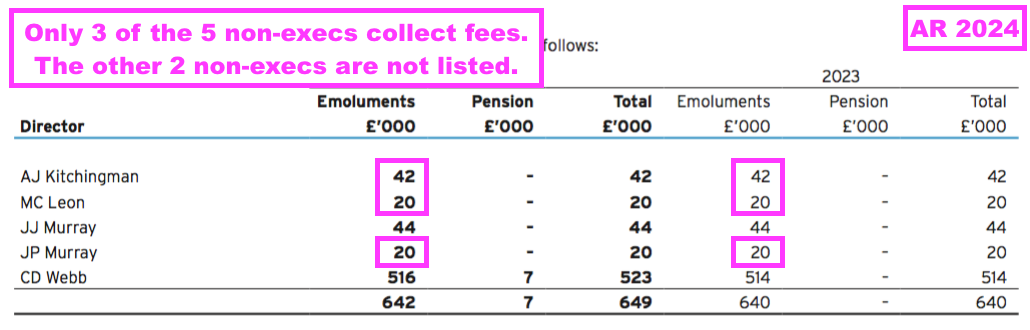

- I note two of the non-independent non-execs do not collect fees:

- The sole independent non-executive has served on the board since 2018. He previously worked as ASY’s broker and now sits as an independent non-exec at the Murray family’s other UK quoted business.

- This FY reported why the board is not seeking another independent non-exec:

“The company has only one independent non-executive director whereas the code recommends that boards have at least two independent non-executive directors. The Board considers that there is sufficient independence on the Board taking into account the shareholder base of the company. For this reason the Board has no current plans to appoint an additional independent non-executive director but will keep the matter under review.“

- My notes from ASY’s 2016 AGM recounted the Murray family were ‘hands off’ shareholders who welcomed ASY’s reporting obligations as a quoted company:

[Maynard Paton 2016] “The controlling family, who are not involved in the operation of the business, like the higher levels of management governance a stock-market listing can provide“

- I must attend another ASY AGM to double-check:

- How ‘hands off’ the Murray family is now given Jean-Jacques Murray has become executive chairman, and;

- Whether the Murray family continue to appreciate the reporting standards of a stock-market listing.

- Preferring the higher reporting standards of a public company has possibly reduced the chance of a de-listing that a 90% shareholding can suddenly enforce on minority investors.

- Indeed, I am hopeful the Murray family keeping ASY quoted for 31 years means the de-listing risk is not as great as perhaps it once was.

- Despite the de-listing risk, I purchased ASY shares during 2013 at an average 233p and the subsequent dividends (ordinary and special) have taken my total ASY income to 396p per share. Add on my 282p per share capital gain and this investment has returned a 12% CAGR.

- I am not sure whether the board’s lack of outside shareholder engagement — no presentations or webinars are conducted — correlates to that positive CAGR.

Valuation

- This FY gave only terse comments about the prospects for FY 2025:

“Positive trading momentum has continued into the current year, with overall performance in the year to date in line with the Board’s expectations. The Group is confident in its core markets, its revenues and its profits.”

“[ASY] remains strong: the experience of our senior management team, coupled with our development plans, provide optimism for further progress in 2025 as we navigate through the current macroeconomic climate in which we operate. The group continues to develop new sales channels and propositions, which will enable the business to take advantage of favourable market conditions and opportunities as they arise. At the same time, the company continues to carefully control its cost base and ensure that satisfactory levels of profit can be achieved even during difficult market conditions.“

- The 515p shares are valued at almost 13x this FY’s 40p per share earnings, which does not appear expensive for a high-margin, cash-rich and cash-generative business that may offer further expansion opportunities within Europe and the Middle East:

- The valuation sums could be fine-tuned for a long list of items, including the £23m net cash position, standard tax rates, those provision reversals, that pension-scheme charge, the regular disposal gains and IFRS 16 leases.

- For perspective, I recall my purchase at 233p during 2013 was conducted on a P/E of 8.

- Bear in mind ASY’s P/E has bobbed around the 15x mark during the last ten years and has rarely climbed to a premium rating:

- Reasons for a consistently modest P/E include:

- The Murray family’s 90% ownership and limited free float;

- A lack of significant reinvestment opportunities for growth, underlined by those three special dividends, and/or;

- The profit ups and downs due to the weather.

- Plus ASY’s economies of scale may not be fantastic. In particular, a persistent 1.0x limit has seemingly emerged between revenue generated from the group’s hire equipment and the original cost of that hire equipment:

- A sustained P/E re-rating may therefore require ASY to earn greater revenue from its existing hire equipment, rather than through consolidating its UK locations and/or opening more depots within Europe and the Middle East.

- During the next few years, earnings could be enhanced by:

- A greater frequency of beneficial weather conditions;

- Further improvements to workforce management;

- New depots opened in Europe (Germany?);

- A continued recovery within the Middle East, and;

- The new water-treatment service becoming popular.

- But dividends — with occasional specials perhaps declared when the cash pile surpasses £30m — seem likely to remain the primary source for returns at present.

- The 25.9p per share payout for this FY supplies a useful 5.0% income at 515p.

Maynard Paton