02 November 2024

By Maynard Paton

FY 2024 results summary for Mountview Estates (MTVW):

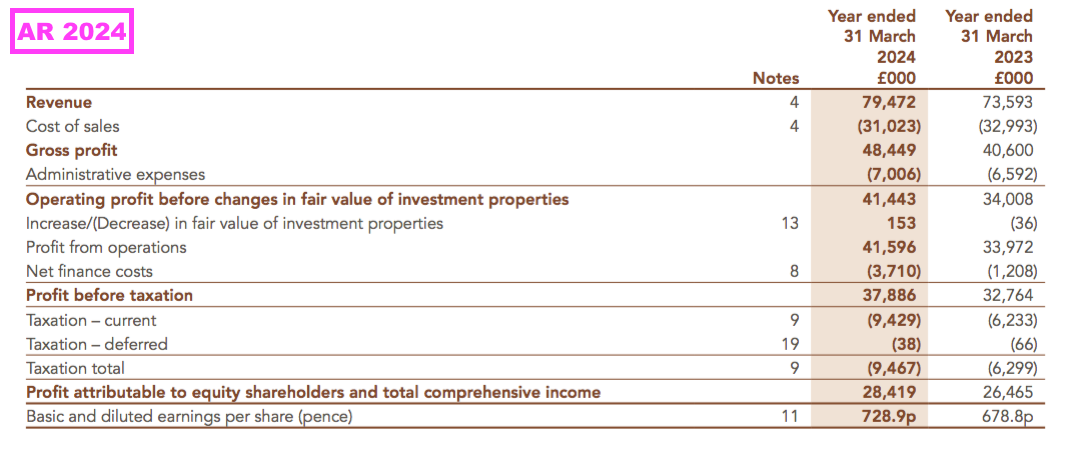

- A reasonable FY performance, which showed revenue up 8%, profit up 22% and the final dividend up 10% after buyers looking for “improvement potential” paid “good prices” for a more normal “profile” of properties.

- Sales by larger landlords allowed MTVW to spend a substantial £48m on new properties, but the advance to net asset value (NAV) was just 2% after MTVW took on greater debt, paid 6%-plus interest, incurred higher tax and sold properties for £59m.

- The absence of another formal estate valuation remains frustrating, especially given properties purchased after a 2014 valuation continue to realise subpar ‘reversionary’ gains and the overall property-sales gross margin was less than 60% for the third consecutive year.

- The board continues to be well paid, attract 30%-plus protest votes and enjoy entrenched support through a family concert party… although not every family member seems a die-hard shareholder and recent AGM remarks even hinted MTVW could one day undertake a trade sale.

- The £90 shares offer a 5.8% income, trade 12% below NAV — the steepest discount for at least ten years — and may be worth £182 if the group’s properties were all sold today at their vacant possession value. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own MTVW

- Results summary

- Revenue, profit, net asset value and dividend

- Trading properties: disposals

- Trading properties: acquisitions

- Trading properties: gross margin and rental income

- Trading properties: properties valued by Allsop

- Trading properties: properties not valued by Allsop

- Financials: balance sheet

- Financials: costs and employees

- Boardroom: protest votes

- Boardroom: new non-executive and executive pay

- Sinclair family concert party

- Valuation

News links, share data and disclosure

- Annual results for the twelve months to 31 March 2024 published 20 June 2024;

- Update on General Meeting voting outcome published 20 May 2024;

- AGM attendance on 14 August 2024;

- Result of Annual General Meeting published 14 August 2024;

- Director/PDMR Shareholding published 19 September 2024, and;

- Notice of General Meeting published 23 October 2024.

- Share price: £90

- Share count: 3,899,014

- Market capitalisation: £351m

- Disclosure: Maynard owns shares in Mountview Estates. This blog post contains SharePad affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy (and similar) properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family manager who continues to lead an aggregate 50%/£177m concert-party shareholding.

- Properties are carried at cost, and when eventually sold at their ‘reversionary’ values may generate total proceeds significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Revenue, profit, net asset value and dividend

- Despite referring to “economic difficulties”…

[H1 2024]

“Despite the economic difficulties being suffered throughout the country…”

…

“We will not abandon our financial prudence, but I am determined that we shall protect our staff from the worst economic misfortunes“

…

“We live in difficult times, but I believe that this Company will continue to prosper and can continue to care for its staff and its shareholders.”

- …the preceding H1 reported quite satisfactory progress and provided hope this FY might not be as bad as MTVW’s weak share price has suggested (see Valuation).

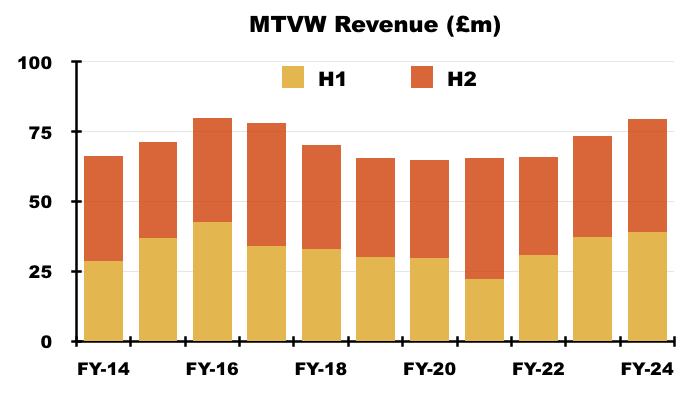

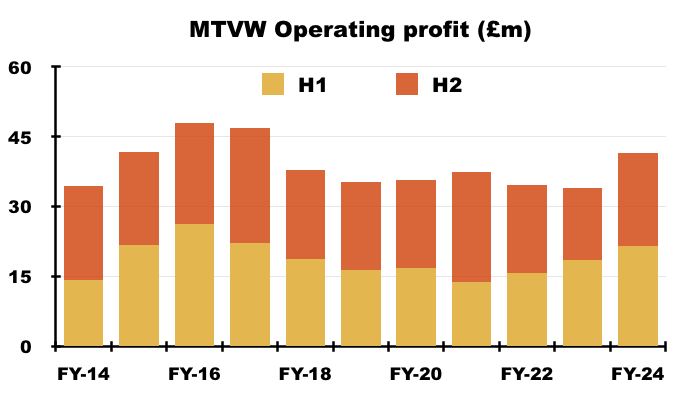

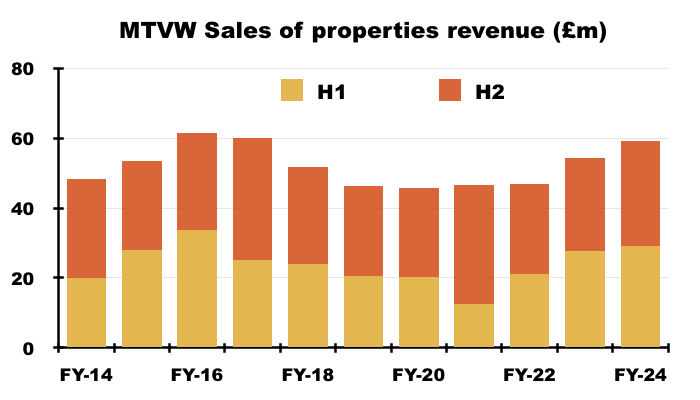

- H2 revenue gained 11% to £40.2m while H2 operating profit advanced 29% to £19.9m:

- The H2 performance meant FY revenue increased 8% to £79.5m, the highest level ever bar FY 2016 (£79.8m)…

- …and FY operating profit improved 22% to £41.4m, the highest level since FY 2017 (£46.8m).

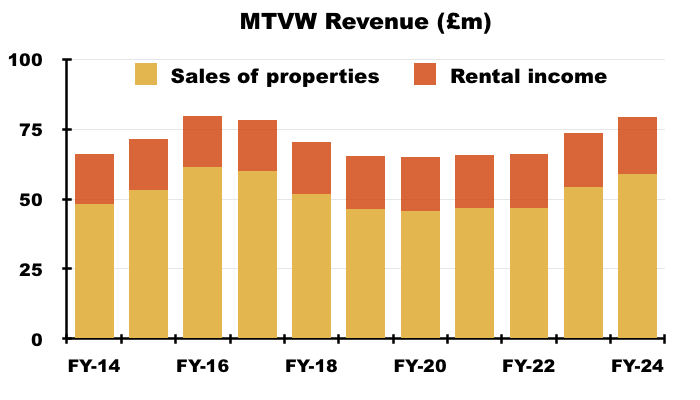

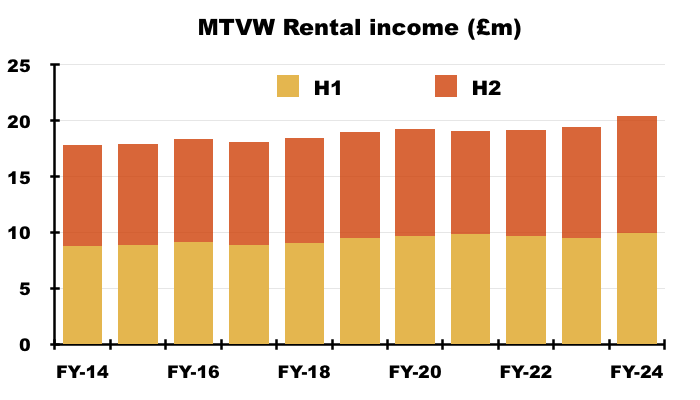

- Revenue was split 74%/26% between property sales and rental income, which broadly matched the preceding ten-year average (73%/27%):

- Note that MTVW typically sells its regulated-tenancy properties when the tenancy ends — which almost always occurs when the tenant dies:

“Regulated tenancies by their nature are not for any specific period of time and in most cases they do not become vacant until the death of the tenant. It is difficult to predict with any certainty the time at which Mountview’s inventory properties might become vacant.”

- The mix of properties becoming available for sale — and the total proceeds and profit MTVW generates — can therefore vary significantly from one set of results to the next (see Trading properties: disposals and Trading properties: gross margin and rental income).

- This FY once again reiterated a “finely balanced” outlook for the housing market…

“Looking forward economic indicators, including projected inflation levels, are looking more positive albeit projected to lead to only sluggish growth in the coming years leaving many households yet to regain pre-pandemic real disposable income levels. Thus the wider outlook is once more finely balanced as any one of a number of factors could tip the balance“

- …but also repeated the claim that MTVW’s “lower priced” property portfolio could escape the worst of any economic ructions:

“We are fortunate that the properties that Mountview brings to auction are typically in high demand as they offer a lower priced entry to the housing market or, if sold to developers, provide opportunity for ‘developer profit’. We are hopeful therefore that Mountview will continue to be well placed to weather any continued downturn in the general housing market, should it occur, through both continuing sales of attractive properties and also with the opportunity to purchase potentially discounted replacement properties both through auction and private tender.”

- MTVW reckoned this FY was supported through buyers paying “good prices” for properties with “improvement potential“:

“We have mentioned before the attractiveness of Mountview properties coming up for sale… and, despite the seeming weakness in the London housing market compared with the rest of the UK, this has continued to be the case in the current year with good prices being achieved whatever the route to market.

We do anticipate that this trend will continue into the current year, as buyers faced with higher interest rates look for properties with improvement potential.“

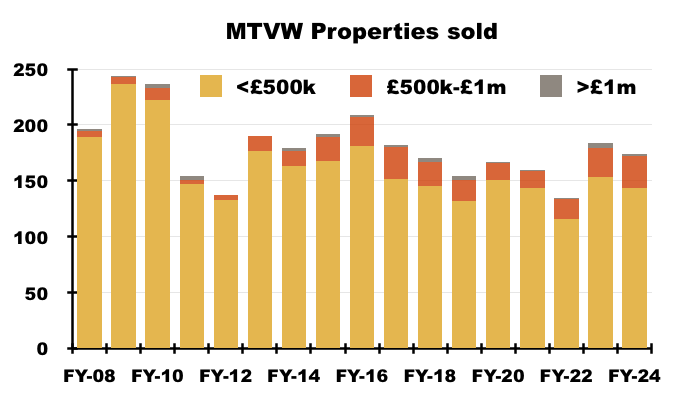

- Most of MTVW’s properties are located within London or south-east England, and 708 (86%) of the 820 properties sold during the last five FYs achieved less than £500k:

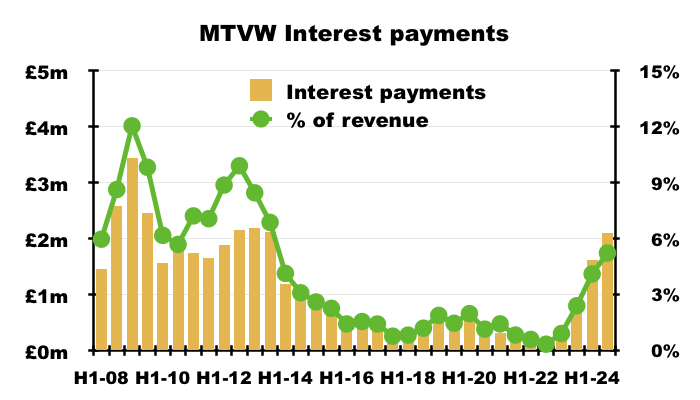

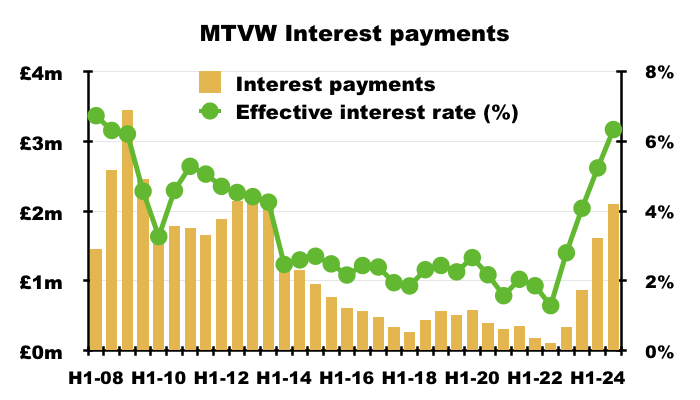

- FY interest payments more than tripled to £3.7m due to the higher rate of interest paid on a greater level of debt (see Financials: balance sheet).

- In fact, interest payments absorbed 5.2% of revenue during H2, the highest six-month proportion since H2 2013 (6.9%):

- MTVW bemoaned the higher tax rate limiting earnings growth to 7%:

“It is a matter of great disappointment that the Government had seen fit to increase Corporation Tax by over 30% (19% to 25%) thus limiting the increase in earnings per share to 7.4%.”

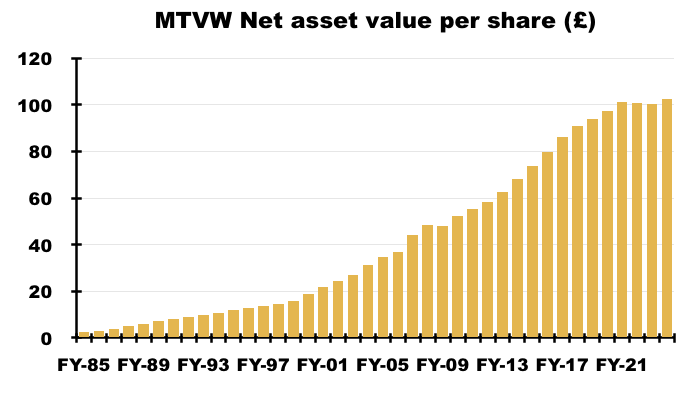

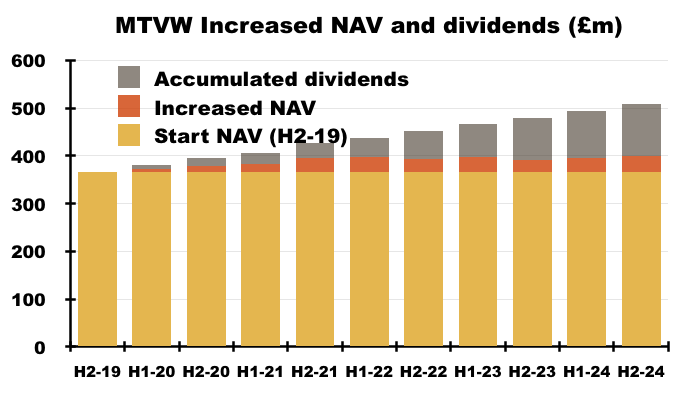

- FY earnings of £28m less the £19m dividends paid during the year meant this FY’s net asset value (NAV) increased by just £9m (+2%) to £400m or £102.50 per share:

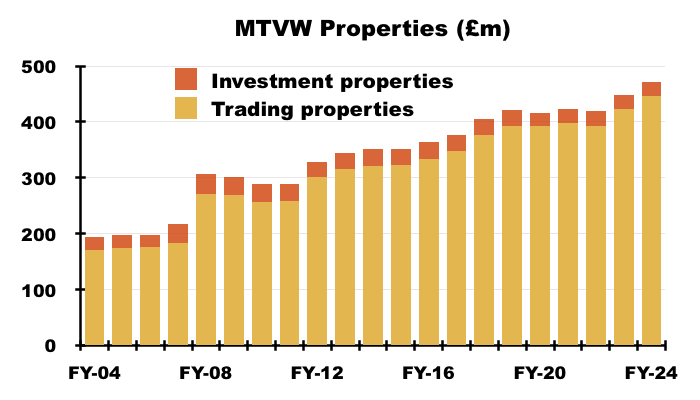

- FY NAV of £400m comprised properties of £472m, debt of £67m and net other liabilities of £6m, and exceeds the £351m market cap (see Valuation).

- This FY set a new NAV high following FYs 2022 and 2023, during which NAV dropped a fraction after MTVW paid two special dividends amounting to a combined £5.25 a share:

- NAV has increased by approximately £33m or 9% since H2 2019.

- Include dividends paid of £108m, and the combined additional NAV and dividend return comes to £141m or 38% over five years:

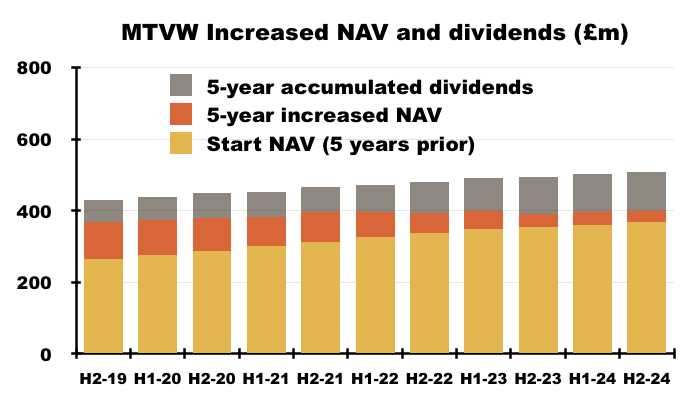

- Five-year shareholder returns through increased NAV and dividends have slowed during recent years.

- For example, increased NAV and accumulated dividends came to £153m during the five years to H2 2021 (a 49% combined NAV and dividend return) — and reached £164m during the five years to H2 2019 (a 62% combined NAV and dividend return):

- The hope is future NAV and dividend growth can now improve by MTVW continuing to sell for “good prices” while undertaking shrewd property purchases. This FY suggested such investments have been made:

“The Company has made many good purchases during the year ended 31 March 2024 and continues to be in position to take advantage of good opportunities.”

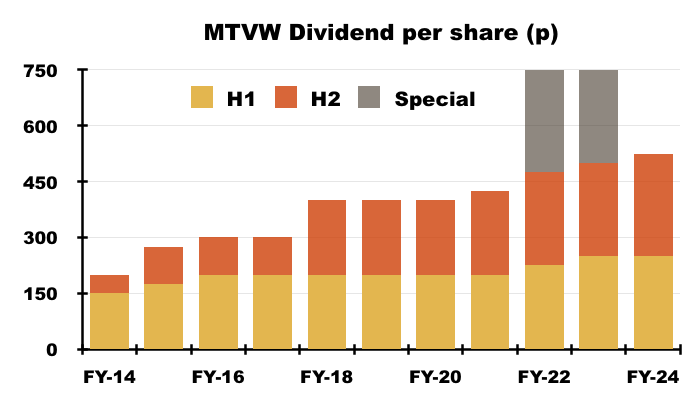

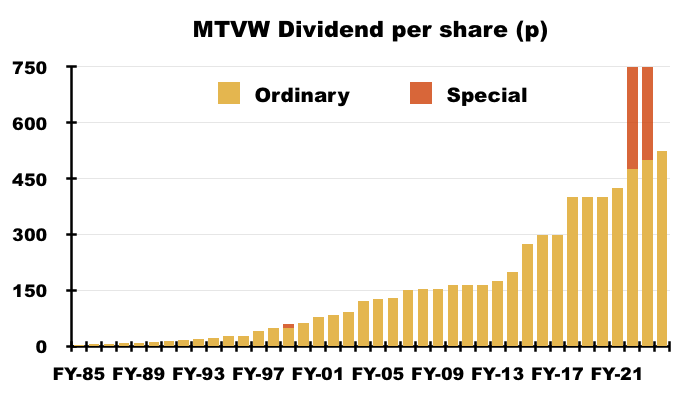

- This FY lifted the final dividend by 10% to 275p per share to take the FY payout 5% higher to 525p per share:

- Companies House shows the ordinary dividend has never been cut since at least 1985 — after which the payout has risen 117-fold.

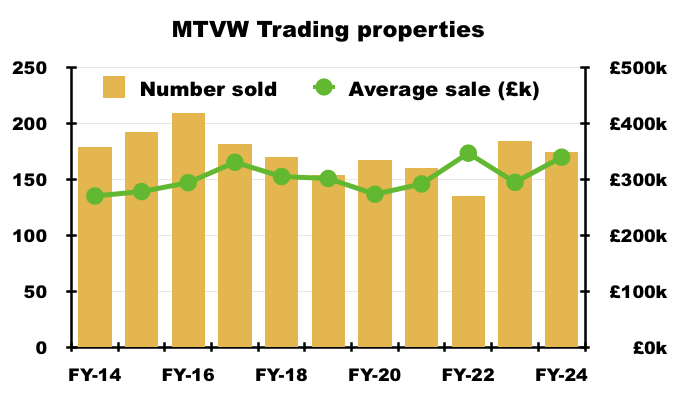

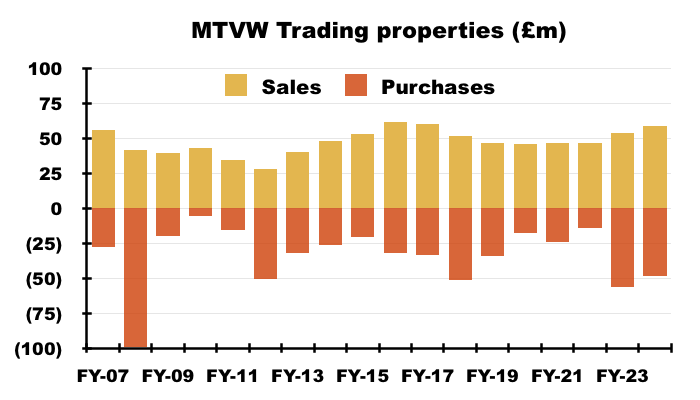

Trading properties: disposals

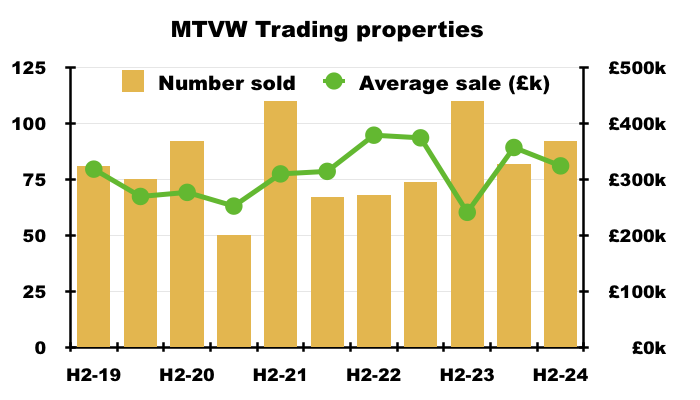

- The 174 properties sold during this FY were split 82 during H1 and 92 during H2:

- The 174 properties sold almost matched the 173 average witnessed during the preceding ten years:

- This FY’s average sale price of £340k did not appear influenced by numerous sales of ground rents, which had distorted the comparable FY’s £295k average sale price (or £395k average without ground rents).

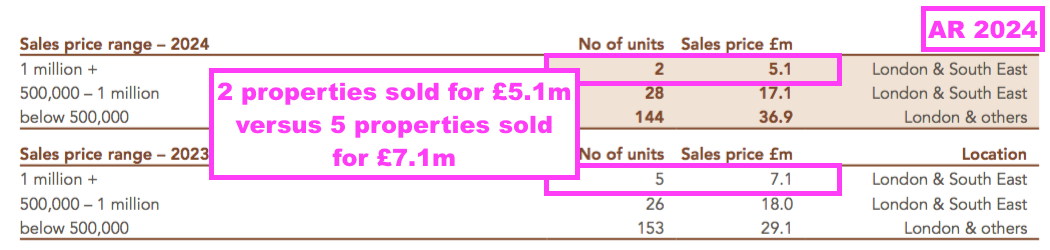

- Average sale prices can also be skewed by MTVW occasionally raising £1m-plus from a single transaction. This FY included two £1m-plus disposals, while the preceding FY included five:

- This FY’s £340k average sales price was at the upper end of the £273k-£347k range witnessed since FY 2017.

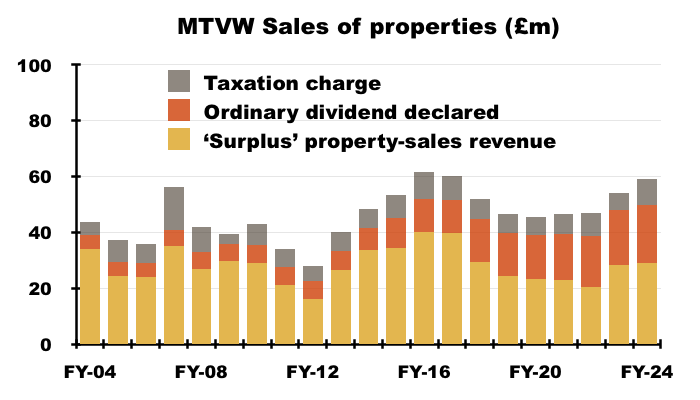

- The higher average sales price meant total FY proceeds from sold properties climbed 9% to £59m — not far short of the record £61m from FY 2016:

Trading properties: acquisitions

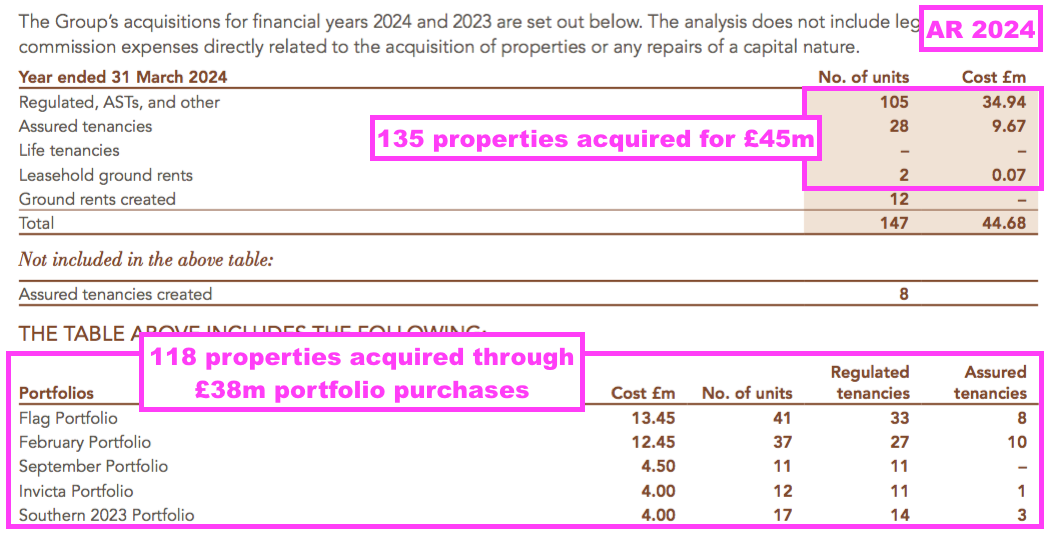

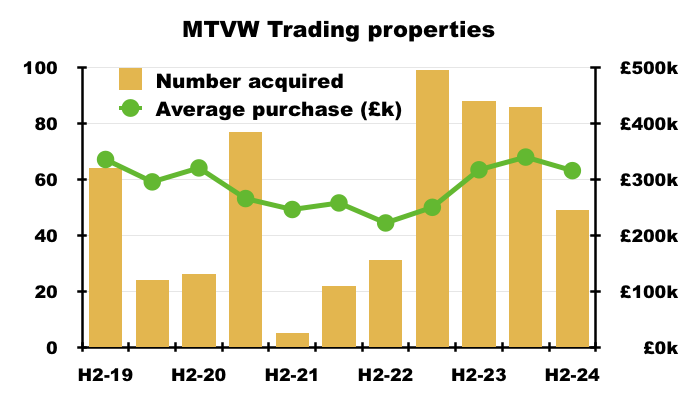

- This FY witnessed 135 properties acquired for £45m (before purchasing expenses):

- The 135 properties acquired were split 86 during H1 and 49 during H2:

- 49 properties acquired during H2 2024 versus 80-plus purchased during each of H1 2024, H2 2023 and H1 2023 may suggest shrewd buying opportunities have become slightly harder to find.

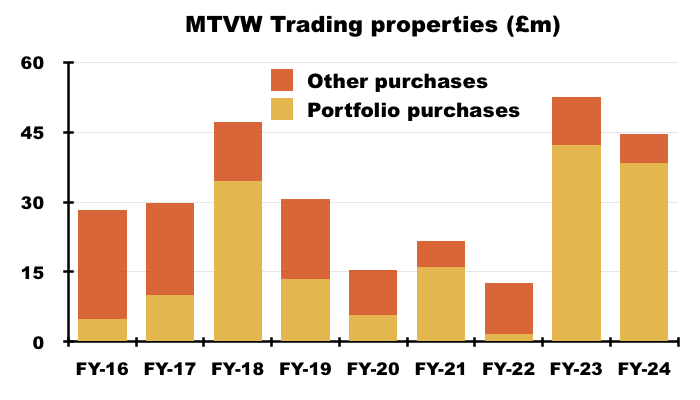

- Of the £45m (before purchasing expenses) spent acquiring properties during this FY, a chunky £38m (86%) was spent on portfolios of properties:

- Coupled with an even chunkier £42m spent acquiring property portfolios during the comparable FY, MTVW’s recent buying activity does appear to be prompted by larger landlords wishing to sell.

- The comparable FY implied market and/or regulatory concerns were causing some landlords to exit the sector:

[FY 2023] “There are hypotheses circulating that the growing opportunities for purchasing have arisen due to either general concerns about the property market or more directly, concerns among buyers about acquiring properties with sitting tenants in the face of proposed reforms to the rental market. In either case both play into Mountview’s core values around careful purchasing of primarily regulated tenancies and patience in waiting for vacant possession, with the latter highly aligned with the aims behind the proposed leasehold reform. “

- This FY did not speculate on why some landlords were selling, but did mention “changing and evolving legislation“:

“Operationally, we will monitor the requirements resulting from changing and evolving legislation. This will include environmental legislation and the Leasehold and Freehold Reform Act (2024) (the Act) hastily rushed through Parliament during the wash-up period prior to Parliament being dissolved on 30 May 2024. Early comments have noted not just the terms of this Act but also its gaps, which will need future legislation. Moreover, implementing even the current Act will require further secondary legislation.”

- Board remarks at the 2023 AGM implied forthcoming legislation had prompted the aforementioned disposals of ground rents during the comparable FY.

- However, my layman interpretation of this government guide to the Leasehold and Freehold Reform Act does not suggest MTVW’s portfolio of regulated tenancies will become an obvious casualty of the new legislation.

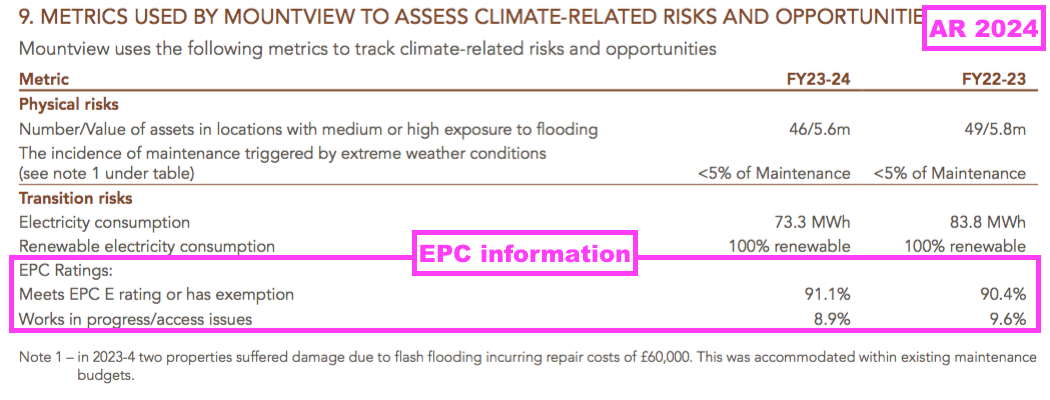

- But proposals to overhaul EPC rules for rented properties is likely to create extra costs for MTVW.

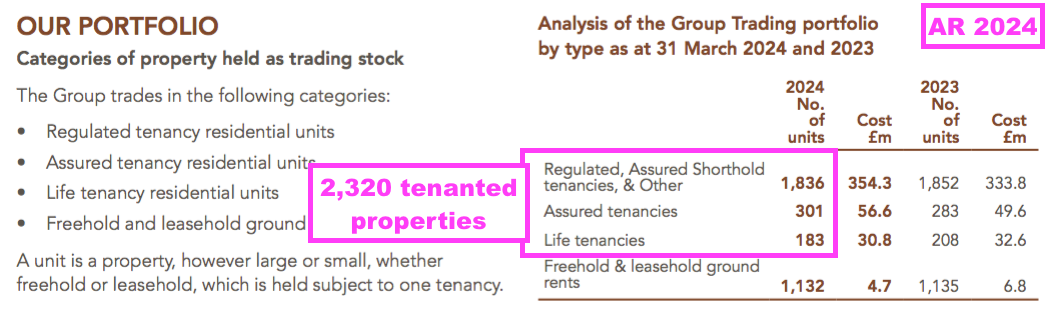

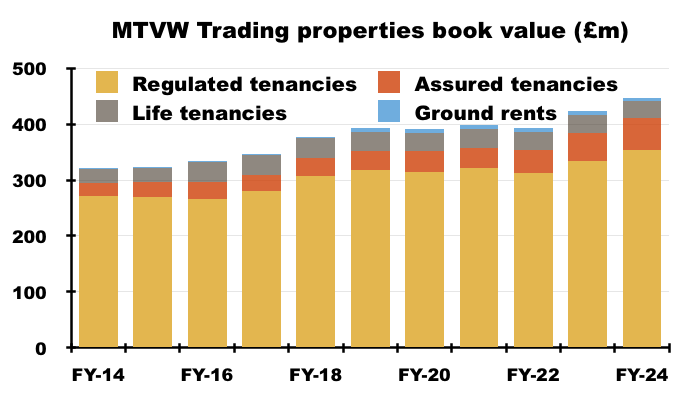

- This FY showed MTVW owning 2,320 tenanted properties, which suggests a possible EPC improvement bill of up to £19m or £4.76 per share based on Rightmove’s £8k estimate:

- 91% of MTVW’s properties have an EPC rating of E or above (or are exempt), with 9% yet to receive an assessment:

- Including purchasing expenses, this FY witnessed £48m used to buy new properties — well above the average £29m spent annually since an enormous £100m was invested during FY 2008:

- Following this FY’s acquisitions and disposals, regulated tenancies remain MTVW’s predominant trading property:

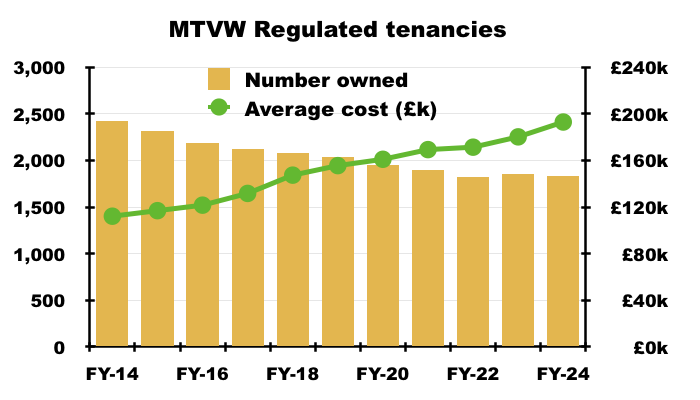

- The market for MTVW’s regulated tenancies will continue to shrink. Such tenancies have not been created since 1989 and Allsop has estimated fewer than 75,000 now exist.

- The number of regulated tenancies owned by MTVW topped 3,000 25 years ago, topped 2,400 ten years ago but today stands at less than 1,900:

Trading properties: gross margin and rental income

- MTVW’s margin and profit can fluctuate due to the unpredictable mix of properties becoming available for sale during any particular period.

- The percentage gain on each property sold — reflected by MTVW’s gross margin — is typically correlated to the duration of MTVW’s ownership, which can range from a few years to a few decades.

- This FY implied the profile of properties sold had reverted to some normality:

“In 2023/24, and in contrast with last year, the improved sales performance also translated into improvements throughout the rest of the P&L, as the cost factors related to timing and location of purchase reverted to the kind of profile we saw before 2022.“

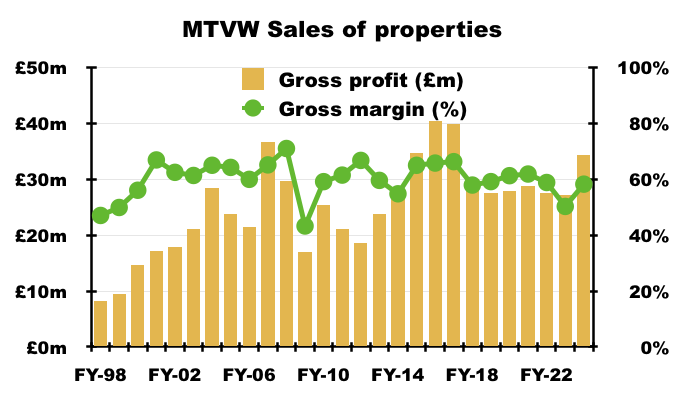

- In fact, this FY’s 58% gross margin achieved through property sales was a welcome improvement on the unusually low 50% registered during the preceding FY:

- However, this FY was the third consecutive FY with a property-sales gross margin of less than 60% — the first time such a run has occurred since the three years to FY 2000.

- A property-sales gross margin of 58% is equivalent to buying a property for £100k and selling it for £238k.

- The run of sub-60% gross margins now gives a lower five-year average versus the preceding five-year periods:

- FYs 2020 to 2024: 58% average;

- FYs 2015 to 2019: 63% average;

- FYs 2010 to 2014: 60% average;

- FYs 2005 to 2009: 61% average, and;

- FYs 2000 to 2004: 62% average.

- The lower-than-normal gross margins may suggest past property purchases were bought for too much or/and sold for too little.

- Still, gross margins can rebound significantly as the unpredictable mix of properties becoming available for sale changes. For example, the 43% property-sales gross margin for FY 2009 had rebounded to a super 67% by FY 2012.

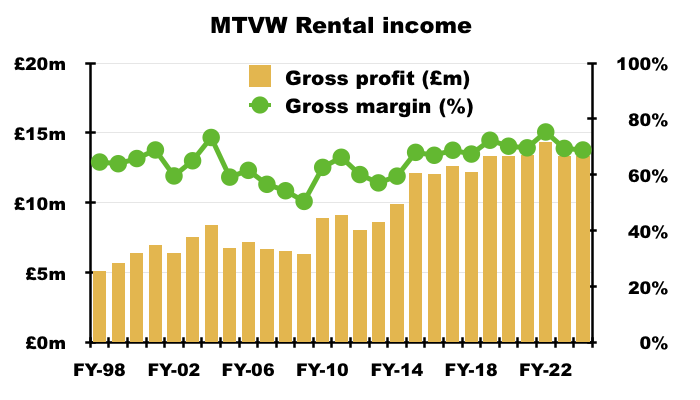

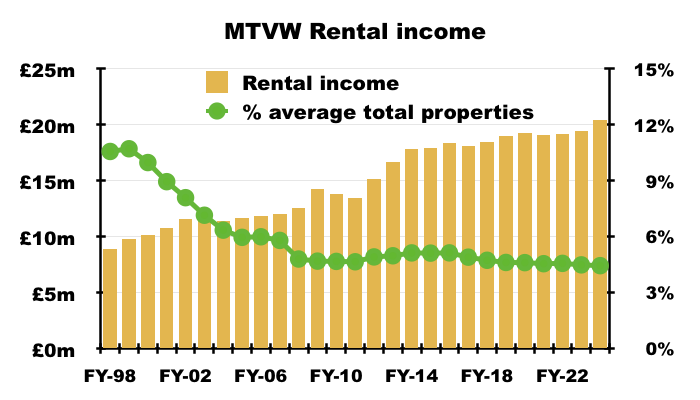

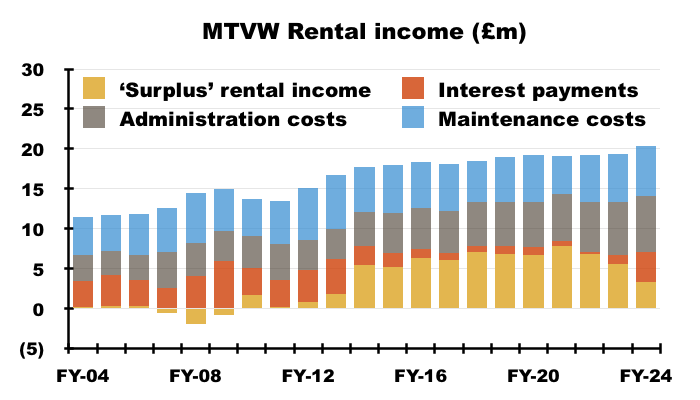

- MTVW’s FY rental income gained 5% to set a new FY record at £20.4m:

- The FY rental-income gross margin remained at a normal 69%:

- During the last ten years, FY rental income has gained 15% or £2.6m while the carrying value of all properties has advanced 35% or £121m:

- The figures suggest for every net £1m spent on new properties during the last ten years, an extra £21k (2.1%) has been added to the rent.

- On a five-year basis, rental income has advanced by £1.4m versus the carried value of properties increasing by £51m — suggesting an extra £27k (2.7%) has been added to the rent for every net £1m spent on new properties.

- Board comments at the 2024 AGM implied MTVW sought to buy regulated tenancies supplying rental incomes of between 2.5% and 3% of cost.

- FY rental income of £20m equates to an effective 4.4% rental yield from this FY’s average £460m carrying value of all properties:

- 4.4% is the lowest rental yield from MTVW’s properties since at least FY 1998.

- Board comments at the 2024 AGM revealed MTVW’s rental income was used to fund property maintenance costs, administration costs (see Financials: costs and employees) and interest costs (see Financials: balance sheet), and implied such income was viewed as a ceiling to limit expenditure and borrowings.

- This FY generated a rental income ‘surplus’ of £3m after rental income of £20m paid maintenance costs of £6m, administration costs of £7m and bank interest of £4m:

- If rental income is used to fund property maintenance costs, administration costs and interest costs, then the proceeds from property sales are left to cover tax and dividends.

- This FY generated a £29m ‘surplus’ of property-sales revenue following the £20m declared ordinary dividend and £9m taxation charge:

- A £29m ‘surplus’ of property-sales revenue should leave ample room for further payout improvements while reinvesting the rest into new purchases.

Trading properties: properties valued by Allsop

- MTVW continues to dispose of properties at a reasonable premium to a past valuation.

- To recap, MTVW commissioned property agent Allsop during September 2014 to assess the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties owned at the time.

- The Allsop assessment was based on MTVW’s properties remaining in their regulated-tenancy state and therefore excluded any ‘reversionary’ gain (i.e. the value uplift that occurs when a regulated tenancy finishes, the rent reverts to a proper market level and the property can then be sold at a fair market value).

- The Allsop assessment was never applied to the formal accounts. MTVW’s properties instead remain on the balance sheet at their cost price.

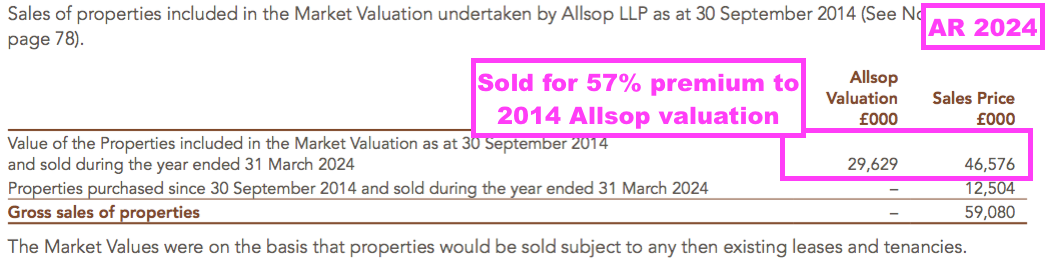

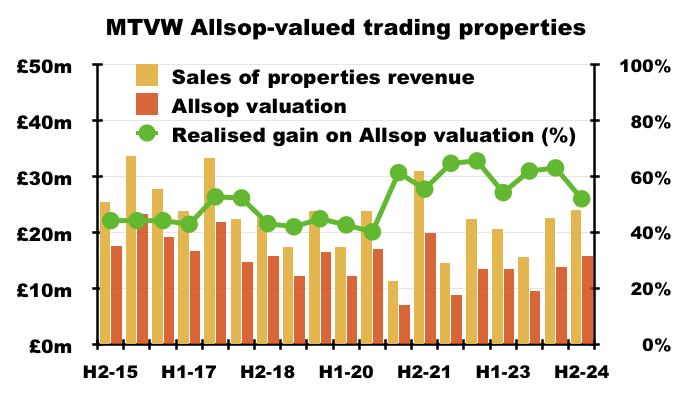

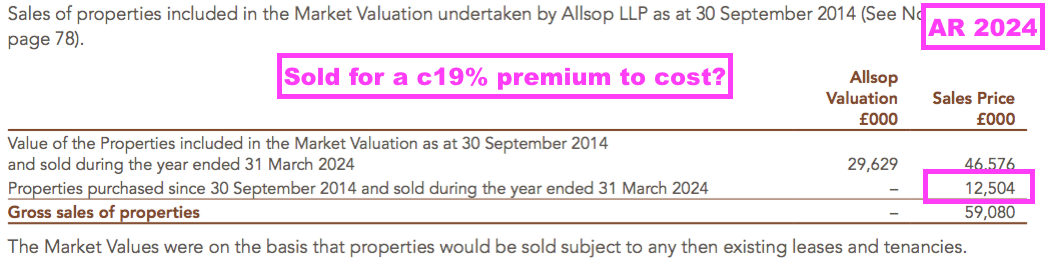

- Following the Allsop assessment, MTVW reveals the proceeds from sold properties versus their Allsop valuation:

- This FY witnessed MTVW sell properties with a combined £29.6m Allsop valuation for £46.6m — a premium of 57%.

- This FY’s 57% premium was split 63% during H1 and 52% during H2:

- The H1 63% premium was MTVW’s highest save for the 65-66% achieved during FY 2022.

- The H2 52% premium was MTVW’s lowest since H2 2020.

- The realised premium versus the Allsop valuation can fluctuate depending on the mix of properties sold during that particular period.

- The realised premium has implications for estimating MTVW’s potential share price (see Valuation).

- During the 9.5 years following the Allsop assessment, MTVW has raised £434m from selling properties the agent had valued at £289m.

- Selling properties that Allsop had valued at £289m implies the book value (i.e. the original cost) of the properties sold was £138m (i.e. £289m divided by the aforementioned 2.1x multiple).

- Selling Allsop-valued properties with a £138m book value indicates Allsop-valued properties with a £180m book value remain within MTVW’s ownership (i.e. the £318m book value at the September 2014 assessment less the £138m since sold).

- If MTVW has taken 9.5 years to sell Allsop-valued properties with an estimated original book value of £138m, the remaining Allsop-valued properties of £180m could therefore take a further 12 years to sell.

- This FY showed total trading properties possessing a £446m book value, implying properties purchased after the Allsop review have a £267m book value (i.e. £446m less the remaining Allsop-valued properties of £180m).

- As more Allsop-valued properties are sold and other properties are purchased, the less relevant the 2014 Allsop valuation becomes to MTVW’s share price.

- MTVW’s results commentary has never referred to the Allsop valuation since the assessment was undertaken, and this FY repeated the following explanation from previous years:

“The [Allsop] valuation is not a useful tool for running the business because we are always going to await vacant possession, and no perceived uplift in value can justify selling a tenanted property. The nature of our business and the rules and conventions under which we operate place no obligation upon us to value our trading stock at any given time and therefore the valuation has not been updated since.”

- Numerous shareholders have questioned the board during several AGMs about the prospect of another Allsop-type valuation. However, the board has repeatedly rejected another assessment. Reasons given have included:

- The assessment is not used by management;

- The assessment is expensive, and;

- There is no accounting requirement.

- Board comments at the 2024 AGM confirmed the directors were unanimous in their decision not to undertake another Allsop-type valuation.

- An irony perhaps of the board not undertaking another valuation is that, should the directors want to sell, they may not achieve a satisfactory price for their shares.

- The wife of MTVW non-exec Dr Andrew Williams for example raised £315k after selling MTVW shares during September at £92.50 — 10% below this FY’s NAV (see Sinclair family concert party).

- Had MTVW undertaken another Allsop-type assessment and revealed further ‘hidden value’ within its property estate, the shares may now be trading above NAV…

- …and the wife of Dr Williams may have raised somewhat more than £315k (see Valuation).

- I maintain MTVW should tone down the board’s pay (see Boardroom: new non-executive and executive pay) and use the savings to implement regular valuations to provide greater clarity about the inherent value of the group’s property estate.

- In particular, further valuations would help shareholders judge the astuteness of MTVW’s more recent purchases (see Trading properties: properties not valued by Allsop).

- The board may argue MTVW’s long-term dividend and NAV records do not suggest outside shareholders have been unfairly treated by a lack of formal valuations.

- September 2024 marked ten years since the Allsop assessment was undertaken. I doubt the board has commissioned another revaluation to publish within the upcoming interim results to celebrate the anniversary.

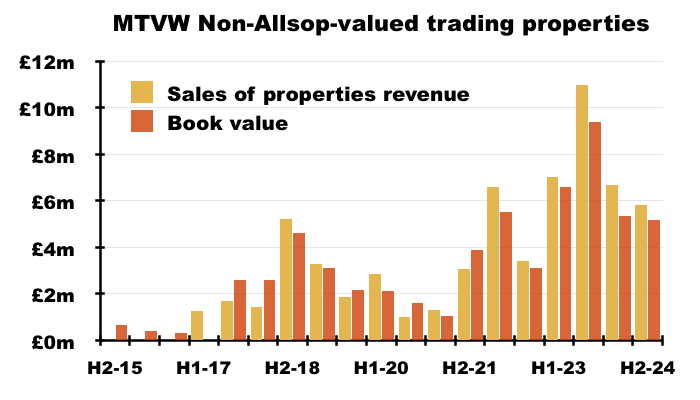

Trading properties: properties not valued by Allsop

- The Allsop assessment and associated disclosures allow shareholders to evaluate the properties not valued by Allsop.

- During this FY, properties bought after the Allsop valuation raised proceeds of £12.5m:

- But what was the original cost of those properties that raised the £12.5m?

- The Allsop-valued properties sold during this FY had an Allsop valuation of £29.6m, which suggests their book value (i.e. purchase price) was £29.6m/2.1x = £14.1m.

- The total book value of properties sold during this FY was £24.7m, which implies the book value of the properties bought after the Allsop valuation and sold during this FY was £24.7m less £14.1m = £10.5m.

- Raising £12.5m from selling properties with an estimated £10.5m purchase price indicates MTVW disposed of the properties at a 19% premium.

- Board AGM remarks (during both the 2021 and 2023 events) stressed MTVW purchased regulated tenancies at 75% of their vacant possession value.

- In theory at least, a regulated property purchased one day at 75% of vacant possession value — which then becomes vacant the next day — should enjoy an immediate 33% ‘reversionary’ value uplift.

- I estimate during the 9.5 years following the Allsop valuation, MTVW has raised a total £64m from selling properties not valued by Allsop with an estimated book value (i.e. purchase price) of £60m:

- I estimate during the last five years, MTVW has raised a total £49m from selling properties not valued by Allsop with an estimated book value of £44m.

- My estimates indicate MTVW’s purchases following the Allsop assessment of September 2014 have led to ‘reversionary’ value uplifts well below the 33% that buying at 75% of vacant possession should generate.

- My estimates could easily explain why NAV growth has slowed and property-sales gross margins have declined during recent years; properties bought and then sold since September 2014 have seemingly realised limited gains.

- My estimates may also explain why the share price has made little headway during the same time:

- Of course, not every property MTVW has purchased following the Allsop assessment has been sold.

- Those properties not valued by Allsop but still owned by MTVW could be sitting on huge paper gains, while those that have been sold were held for relatively short durations that would always limit their final profit.

- Furthermore, MTVW acquires properties other than regulated tenancies, which may require more than the 9.5 years since the Allsop assessment to maximise their upside.

- Still, buying properties for an estimated £60m/£44m and selling for £64m/£49m can’t be deemed a rousing success — especially when 33% ‘reversionary’ uplifts should be enjoyed — and probably explains the pointed questions from David Pears at the 2023 AGM.

- The 2024 AGM witnessed a further bout of pointed questions, primarily from Craig Murphy (see Boardroom: protest votes and Sinclair family concert party) with a few from myself, about the gains realised from properties bought after the 2014 Allsop valuation.

- Board responses to those question at the 2024 AGM included:

[AGM 2024]

“We’re satisfied that the purchasing process is robust“

“We are content with the returns which have been delivered.“

“Calculations from the outside are based upon summary level information and lead to a different answers to what you get from the inside, which include precise costs associated with the individual properties.“

- The board also referred to:

- Purchase costs;

- Valuations being inherently imprecise;

- The mix of properties sold each year;

- Factors influencing individual properties, and;

- Longer periods of ownership tend to lead to higher gross margins.

- Purchase costs include stamp duty, which for companies buying residential properties was lifted during 2016 and lifted again earlier this week.

- Purchase costs are included within the carrying value of the trading properties:

“INVENTORIES – TRADING PROPERTIES

These comprise residential properties, all of which are held for resale, and are shown in the financial statements at the lower of cost and estimated net realisable value. Cost includes legal fees and commission charges incurred during acquisition together with improvement costs. Net realisable value is the net sale proceeds which the Group expects on sale of a property in its current condition with vacant possession.“

- The board said during the 2024 AGM that it would consider disclosing more information to prove how recent purchases have realised satisfactory gains.

- In the meantime, the lack of any further Allsop-type assessment leaves me to assume the properties not valued by Allsop but still carried on the balance sheet are unlikely to have an eventual sale value vastly in excess of their aforementioned £267m aggregate purchase price.

Financials: balance sheet

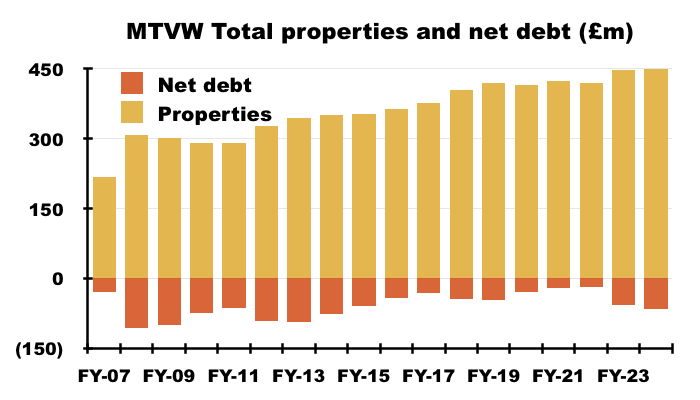

- MTVW’s accounts remain very straightforward, with properties and debt the two prime entries.

- The aforementioned £48m spent on new properties alongside a favourable working-capital movement left free cash flow at £10m, with dividends of £19m then increasing FY net debt from £56m to £66m.

- Net debt at £66m is the highest since FY 2014 (£77m) but is equivalent to only 14% of the group’s £472m total property estate:

- For perspective, MTVW operated with net debt equivalent to 25% or more of its property estate during FYs 2008, 2009, 2010, 2012 and 2013.

- MTVW’s banking facilities allow borrowings of up to £90m, equivalent to 19% of the total property estate.

- Finance costs of £3.7m for this FY were more than triple the £1.2m for the comparable FY, and implied a 6.3% interest rate on H2’s £66m average debt:

- My estimated H2 interest cost of 6.3% is the highest since H1 2008 (6.7%).

- This FY reconfirmed MTVW’s borrowings are variable rate with a margin of approximately 2% above SONIA:

1. The Group has a short-term borrowing facility of £10 million (2022: £10 million) with Barclays Bank. This is due for review in November 2023 and the rate of interest payable is:

• 1.6% over base rate on overdraft

• Headroom of this facility at 31 March 2023 amounted to £9.94 million (2022: £10 million).

2. The Group has a £60 million (2022: £60 million) long-term revolving loan facility with Barclays Bank with a termination date of March 2027. The rate of interest is 1.9% above SONIA. The loan is secured by a cross guarantee between Mountview Estates P.L.C. and its subsidiaries. The loan is not repayable by instalments. Headroom under this facility at 31 March 2023 amounted to £20 million (2022: £58 million).

3. The Group has re-negotiated a £20 million long-term revolving loan facility with HSBC Bank. The termination date for this facility is March 2028. The rate of interest payable on the loan is 2.1% above SONIA. The loan includes a Negative Pledge. The loan is not repayable by instalments. As at 31 March 2023 headroom under this facility amounted to £3.3 million (2022: £2.8 million).”

- SONIA is currently 4.95%, which means MTVW should now be paying approximately 6.95% on its debt.

- Assuming gross debt stays at £67m and SONIA stays at 6.95%, annual finance costs would advance from £3.6m to £4.7m, or 119p per share, during FY 2025.

- Paying an extra £1m or so through higher interest will dampen immediate NAV growth…

- …but should (in theory!) enhance longer-term NAV — assuming of course the properties purchased by the extra borrowings generate eventual returns well in excess of my projected 6.95% annual debt cost!

- Board remarks during the 2024 AGM reiterated an informal gearing limit of 25%.

- The aforementioned rental-income surplus of £3m after all maintenance, administration and finance costs would (in theory!) allow MTVW to borrow a further £48m at 6.95%, which would take gearing to 24%.

Financials: costs and employees

- This FY’s £9.5m tax charge was MTVW’s first that was derived under the current 25% UK standard rate, and would have been £7.2m under the previous 19% rate.

- The £2.3m extra tax eroded this FY’s NAV by approximately 58p per share.

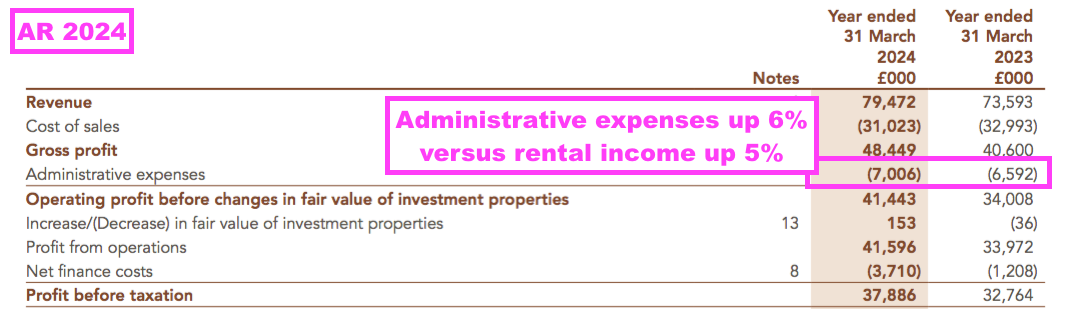

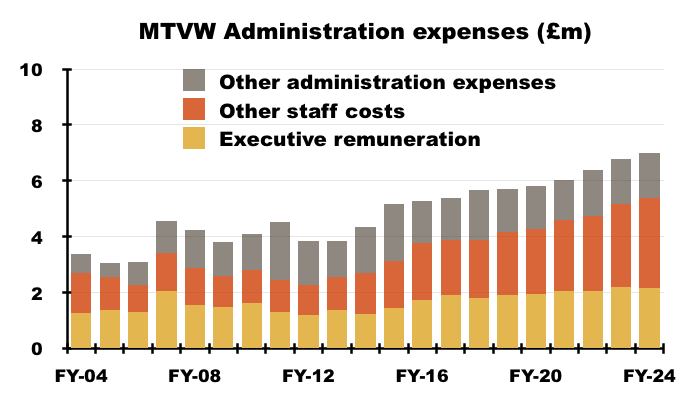

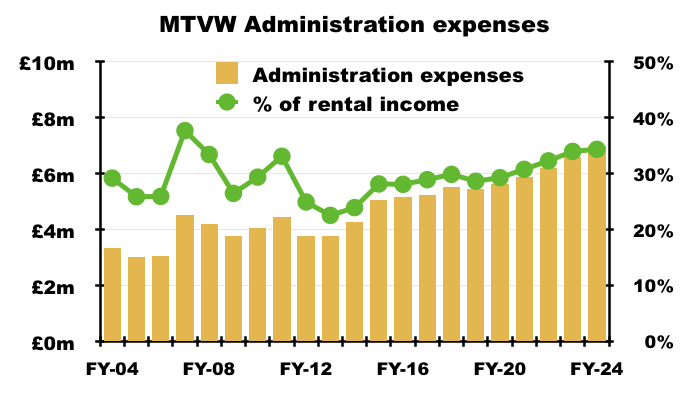

- FY administration expenses increased 6% to £7m:

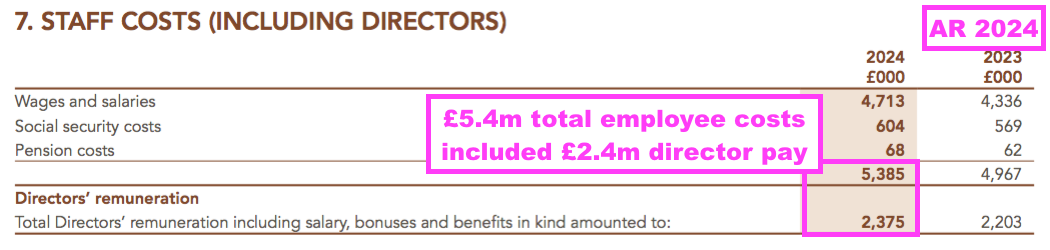

- Employee costs remain the majority of administration expenses. FY administration expenses comprised employee costs of £5.4m and other costs of £1.6m.

- A significant proportion of employee costs are payments to the directors. FY employee costs consisted of £2.4m paid to the directors and £3.0m covering the salaries of other employees plus the group’s social security expense:

- Executive pay remains substantial (see Boardroom: new non-executive and executive pay).

- Total FY employee costs advanced 8% following 30% bonuses and “over-inflation salary increases“:

“As in recent years, in the light of both their performance and our desire to help protect them from the impact of cost of living factors, which are outside their control, we have taken the opportunity to award bonuses of over 30% of salary and also, continuing the trend over a number of years, of granting over-inflation salary increases.“

- FY administration costs excluding employee costs stayed at £1.6m for the third consecutive year:

- Total administration expenses absorbed 34% of rental revenue during this FY, the highest proportion since FY 2007 (38%):

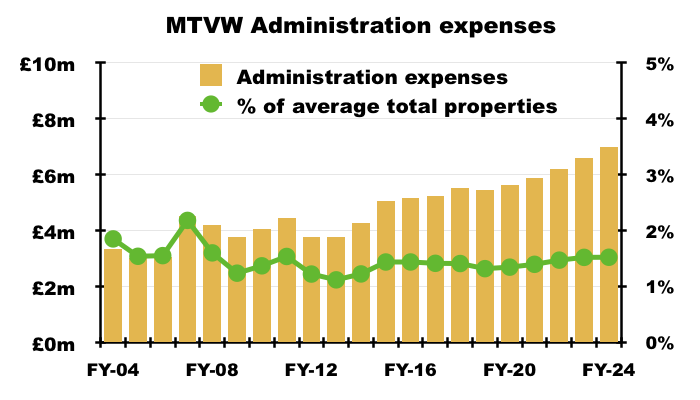

- Mind you, administration expenses versus the value of total properties have remained very consistent at approximately 1.5%:

- Higher salaries for employees — and directors! — may therefore not be entirely out of step with the group’s NAV progress.

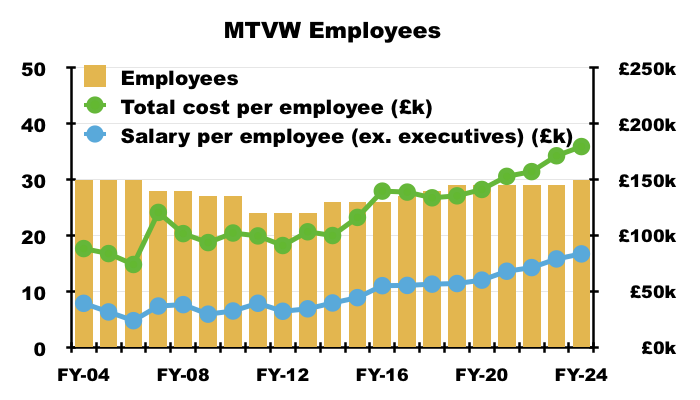

- Staff numbers have bobbed between 25 and 30 over time while the total cost per employee has advanced to £180k:

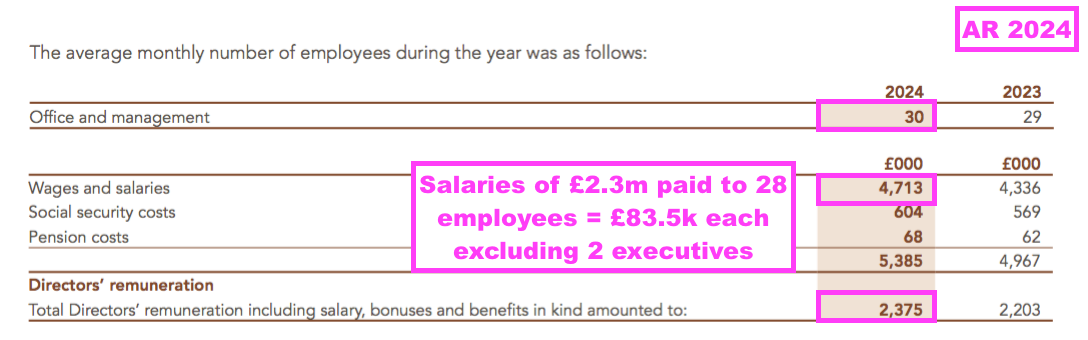

- Exclude the executives, and the average employee salary may be a useful £83.5k:

- For perspective, during the last ten years total employee costs have climbed 107% while the ordinary dividend is up 163% and NAV is up 50%.

- MTVW’s chunky salaries may be a by-product of keeping other expenditure to a bare minimum. In particular, audit fees absorbed a tiny 0.13% of this FY’s revenue.

- Nothing is certainly spent on investor communications beyond the annual report, the occasional terse RNS, hosting shareholder meetings and the website.

Boardroom: protest votes

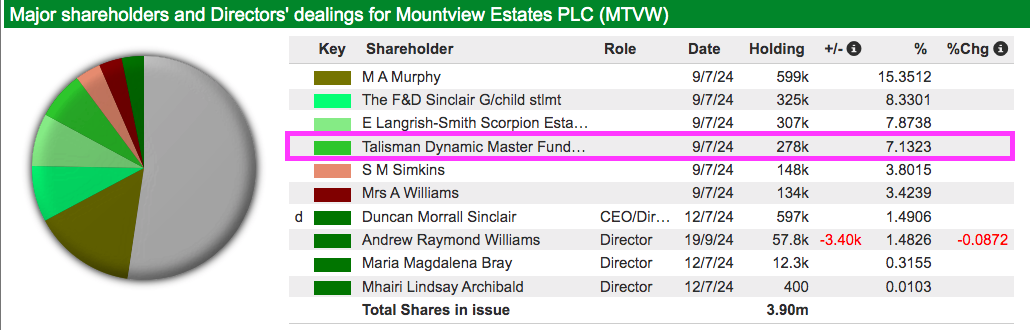

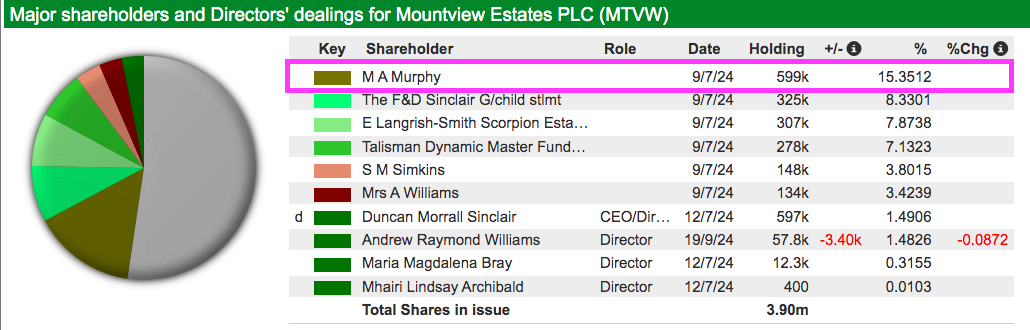

- MTVW’s shareholders fall into three camps:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and at the last published count controlled 50.4% of the shares (see Sinclair family concert party);

- The Murphy family and connected parties, who claim to own 24% of the shares and whose leading shareholder is Margaret Murphy, the chief executive’s sister, and;

- Everybody else, who own approximately 25% of the shares.

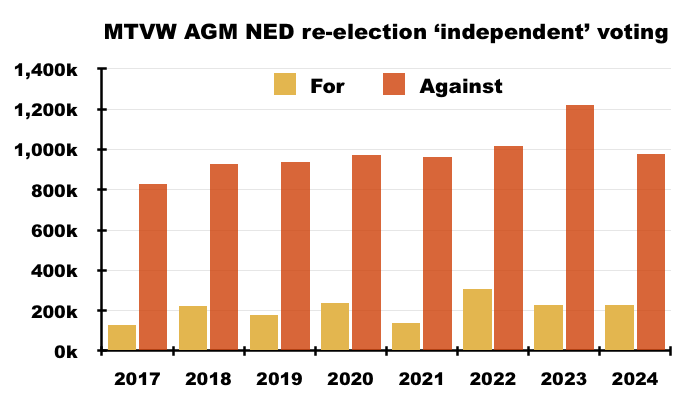

- MTVW’s last eight AGMs have witnessed c30% protest votes against:

- Re-electing certain non-execs and, recently, both the executives;

- Approving the board’s pay, and;

- Re-appointing the auditors.

- The protest votes have been led by the Murphy family and connected parties.

- From what I gather, the Murphy family:

- Is aggrieved about the board’s (generous) pay;

- Has lost the trust of the non-execs to act on the views of all shareholders;

- Is frustrated about a general lack of influence at board level, and;

- Has become increasingly concerned about the low gains realised on properties purchased following the Allsop valuation (see Trading properties: properties not valued by Allsop).

- The Murphy family stated during the 2021 AGM that it was no longer in direct communication with the board and would engage with the directors only through a “public forum“. I understand that policy remains in place.

- Among the attendees at the 2023 AGM was David Pears, who is a member of the Pears family that owns property group William Pears and controls a 7% MTVW stake through the family’s Talisman investment fund:

- Judging by the 2023 AGM’s post-meeting chit-chat, let’s just say Mr Pears was not a happy shareholder.

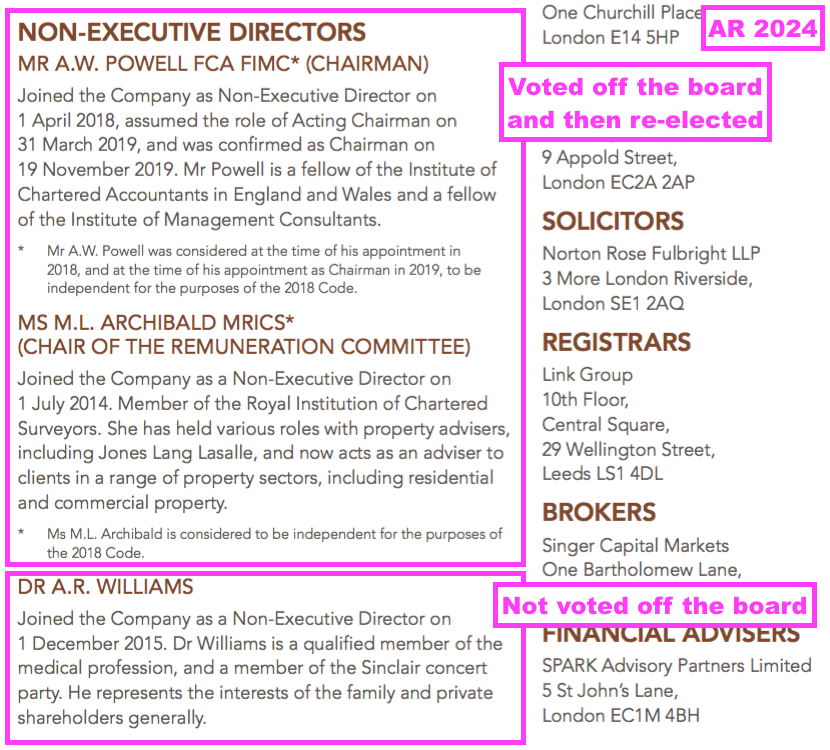

- The Murphy family, (presumably) Talisman and other unhappy shareholders prevented the re-election of certain non-execs at the 2024 AGM — and the seven prior AGMs:

- I don’t know why c243k fewer protest votes — equivalent to 6% of the share count — were lodged during 2024 versus 2023.

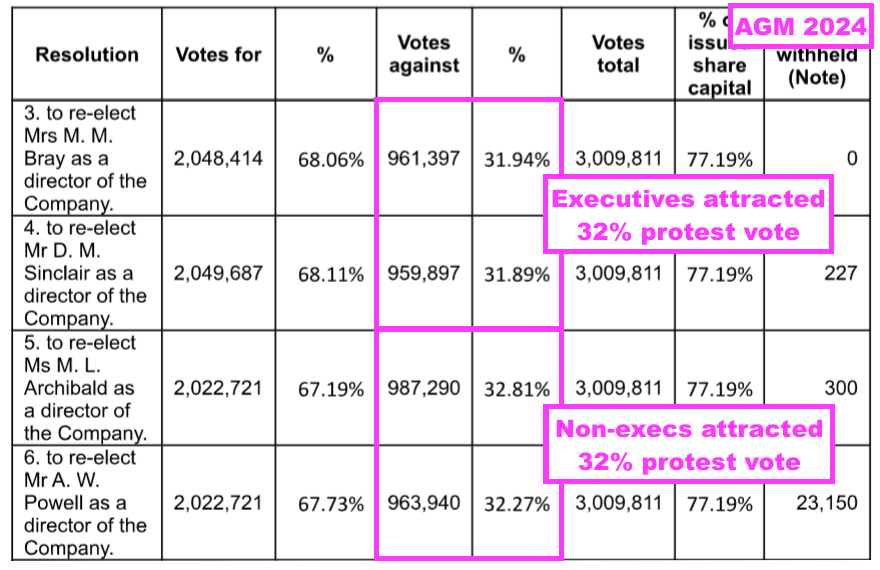

- I am quite sure the Murphy family (and connections) and Talisman participated in the 2024 AGM voting, given the polls revealed a 32% protest vote against MTVW’s two executives:

- The Murphy family (and connections) and Talisman have clearly become fed-up with the executives, given the votes against the executives have increased from immaterial numbers to 3%, then 9% and now 32% during the last three years.

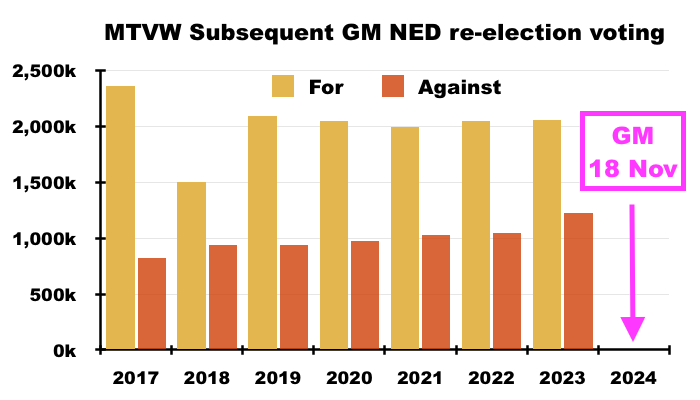

- Following each AGM, MTVW is entitled to convene a general meeting (GM) and hold a further vote to re-elect the ousted non-execs.

- The ousted non-execs have (to date) all been re-appointed at the subsequent GMs because the Sinclair family concert party can then vote on the non-exec re-elections (unlike at the AGMs, where the concert party is prohibited from voting on particular ‘independent’ resolutions):

- Stock-market rules dictate any company incurring a 20%-plus AGM or GM protest vote has to contact the unhappy investors and publish an update to all shareholders within six months.

- Six months after the 2023 GM, during May 2024, MTVW announced:

[RNS May 2024] “Following the meeting, the Company identified, as far as possible, those shareholders who did not support the resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage, other shareholders raised matters which are under consideration by the Board and its Committees. The Board is grateful to those shareholders who took part in the engagement process and value the feedback provided. The Company re-affirms its commitment to ongoing shareholder engagement and will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.””

- Board remarks at the 2024 AGM did not reveal which shareholders engaged and which matters were raised:

[AGM 2024] “The discussions were with shareholders who are not here today and we will not disclose what was said, and certainly not without their permission. They raised questions and, where we felt that it was appropriate that we could make the change, we have.“

- I speculate the shareholders who “raised matters which are under consideration by the Board and its Committees” included David Pears, who did not attend the 2024 meeting.

- Whether any of the matters raised have actually converted into action remains to be seen.

- But 15 AGM/GM protest votes since 2017 suggest the “engagement process” has no influence on board decisions.

- The ineffective protest votes have not yet persuaded the Murphy family to sell; Companies House indicates Margaret Murphy has maintained a 500k-plus shareholding since at least 1980:

- Talisman has not announced any selling since reporting its last purchase during January 2023:

Boardroom: new non-executive and executive pay

- The ongoing search to find a replacement non-executive was discussed at length during the 2024 AGM.

- The replacement non-exec will be ‘independent’ of the Sinclair family concert party, and could therefore allow the Murphy family and other unhappy shareholders to enjoy greater influence at board level.

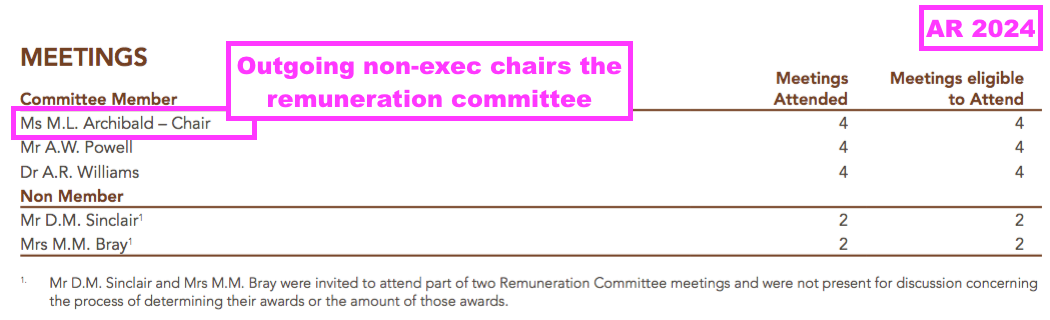

- The preceding FY claimed the replacement non-exec would be recruited within “six to nine months”:

[FY 2023] “The Nomination Committee has commenced its search for a new, suitably experienced and qualified independent Non- Executive Director and has engaged an external recruitment consultant Stephenson Executive Search Ltd, which has no other connection with the Group. The Nomination Committee is reasonably confident that it will be in a position to complete the recruitment and appointment process within the next six to nine months. It is envisaged that the new independent NED will have a short period of overlap with Ms Archibald to enable a smooth and seamless transition of Ms Archibald’s role and duties as chair of the Remuneration Committee and her other committee membership roles and responsibilities.

- The 2023 annual report was published on 28 July 2023, and therefore the new appointment ought to have been announced by the end of April 2024.

- This FY revealed:

- No replacement had been found, and;

- The outgoing non-exec would now stay on until 31 March 2025:

“In 2023 the Committee were aware that Mhairi Archibald’s service agreement covering her third tenure as a NED was due to end on 30 June 2023 and at that point would reach the nine-year limit usually applicable to NED tenures in accordance with the 2018 Code and related guidance. The Committee therefore started its search for a new, suitably experienced and qualified independent NED and engaged an external recruitment consultant Stephenson Executive Search Ltd, which has no other connection with the Group, for this purpose.

The search is on-going and, while we have yet to fill the position, the Committee remains focused on completing the search and appointment. In the meantime, the Committee has agreed to extend Ms Archibald’s contract until 31 March 2025 with the aim of completing the new appointment and enabling a short period of overlap with Ms Archibald. This will ensure a smooth and seamless transition of Ms Archibald’s role and duties as chair of the Remuneration Committee and her other committee membership roles and responsibilities.”

- Corporate-governance protocols say non-execs should serve no more than nine years on the same board. MTVW’s outgoing non-exec will have served ten years and nine months if/when she leaves the board on 31 March 2025.

- Board remarks at the 2024 AGM about the non-exec search can be summarised as:

- A number of candidates were interviewed;

- None were deemed suitable;

- They were unsuccessful for a variety of reasons (including “the chemistry was not right“), and;

- The search continues with further interviews in the coming weeks.

- MTVW published a circular last month that detailed the voting procedure for the upcoming General Meeting to reinstate the two non-execs ousted during the 2024 AGM.

- The circular included a resolution asking shareholders to approve lifting the total fees paid to the non-execs from £250k to £350k:

[Circular October 2024] “A third resolution is included in the notice of general meeting that addresses the issue of directors’ fees. The Company will seek shareholders’ approval to amend Article 96 of the Company’s Articles of Association to increase the level of total fees payable to Non-Executive Directors from £250,000 to £350,000. This will provide sufficient headroom for the appointment of an additional NED which may occur within the next few months, taking the total of NEDs to four (from three) to allow for a period of overlap between the incoming and outgoing NEDs.”

- For this FY, the non-execs were paid a total £194k and will receive a total £200k for FY 2025:

“The Board considered the fees payable to the Non-Executive Directors and approved increases of £2k for each NED thus £108k to £110k for the Chairman, an increase of 1.85%, and from £43k to £45k for other Non-Executive Directors representing a 4.65% increase year on year.”

- The existing £250k limit on total non-exec pay ought to cover any overlap between the replacement non-exec and the outgoing non-exec, given:

- Total non-exec fees for FY 2025 will be £200k;

- The outgoing non-exec will be paid £45k during FY 2025;

- Her replacement may also collect £45k, and;

- The period of overlap should not be too long.

- I suppose the new £350k limit on total non-exec pay can be viewed in two ways.

- Either MTVW could recruit a renowned non-exec ‘heavyweight’, who demands a hefty fee but who will truly represent independent shareholders at board level.

- Or MTVW could recruit another compliant non-exec, who demands a hefty fee to compensate for being subject to regular protest votes and awkward questions at shareholder meetings.

- The circular said further non-exec interviews would take place:

[Circular October 2024] “The Board is progressing its search for a new NED and has a shortlist of candidates to interview.“

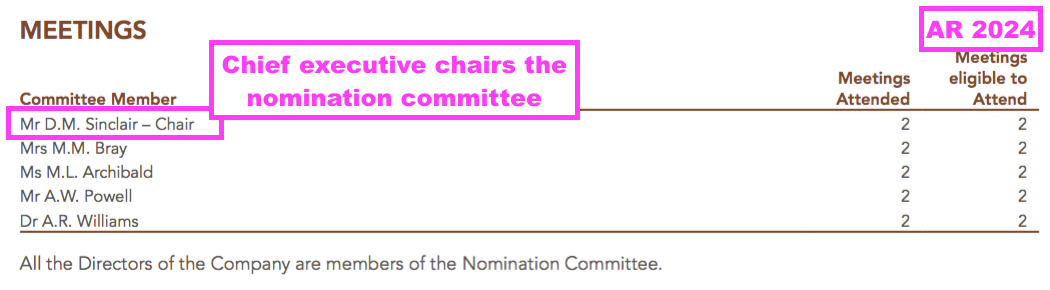

- The absence of an appointment is not encouraging for the Murphy family and other unhappy shareholders. The worry is the board’s nomination committee, which is chaired by chief executive Duncan Sinclair, is not pursuing the appointment with suitable urgency:

- Perhaps the board has struggled to find a qualified non-exec who meets the appropriate diversity criteria. This FY stated:

“The Board is aware that the target in LR 9.8.6 R(9)(a)(ii), having at least one Board member from a minority ethnic background, has not been met and its consideration will form part of its deliberations in building a diverse and inclusive culture on the Board.”

- The outgoing non-exec is chair of the remuneration committee, and I speculate the replacement non-exec will then take that role:

- Chairing the remuneration committee is of course a vital board role given the history of executive pay.

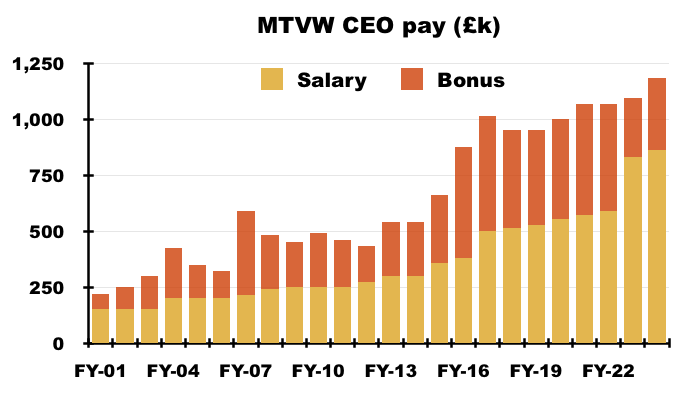

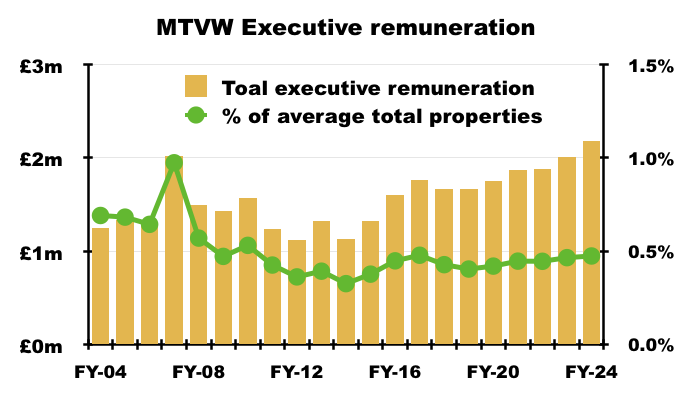

- In particular, the chief executive has collected a bonus every year since at least 2001, and such bonuses have pushed his total pay beyond £1m since FY 2020:

- The feeling among many AGM attendees over the years is the executives are paid handsomely for essentially:

- Putting vacant properties into auction;

- Collecting rent, and;

- Buying properties during recent years that may not have earned worthwhile gains on disposal.

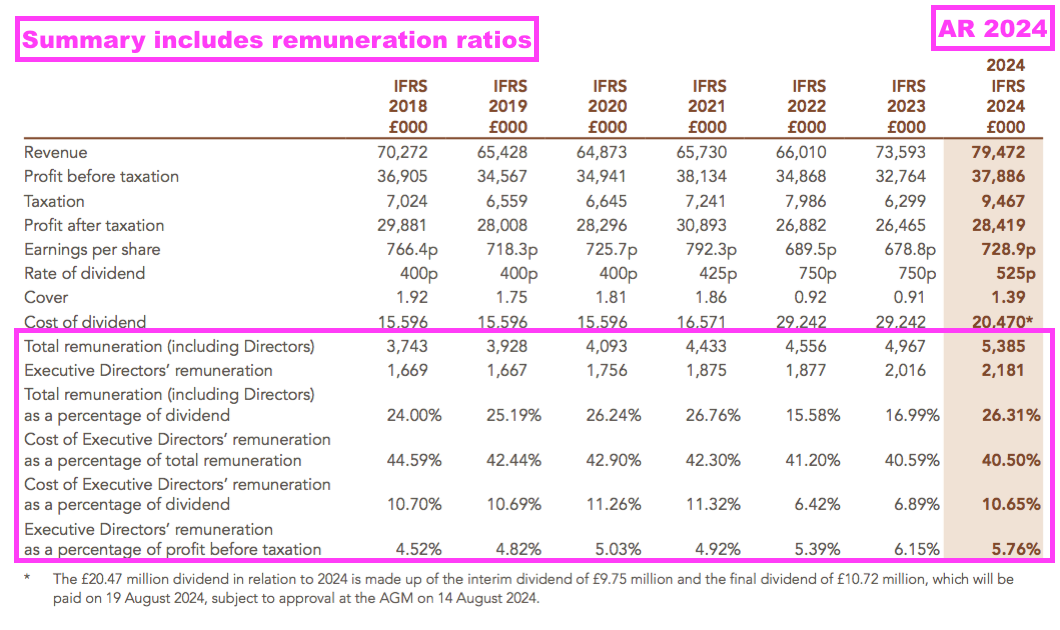

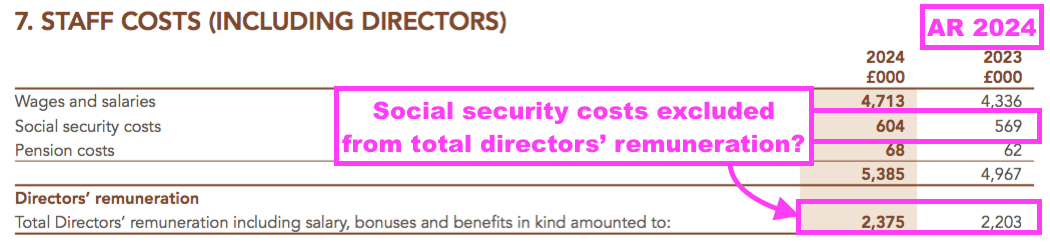

- MTVW is the only company I know that includes executive-remuneration ratios within its annual reports:

- The remuneration ratios may not be strictly accurate, as I believe the executive-remuneration figures exclude the associated social security costs:

- Total executive pay has been equivalent to a consistent 0.5% of the total property estate:

- 0.5% of the total property estate does not sound a lot, but starts to add up given the total property estate advanced by just 12% — or 2.3% per annum — between FY 2019 and this FY.

- One positive about the board’s remuneration is the absence of a share-option scheme. MTVW has in fact not issued any new shares since at least 1979.

- The sole non-exec who is not voted off the board at every AGM is Dr Andrew Williams, who is a grandson of MTVW co-founder Frank Sinclair.

- Dr Williams is a member of the Sinclair family concert party (but has not been listed as such — see Sinclair family concert party) and apparently “represents the interests of the family and private shareholders generally“:

- I attended MTVW’s 2019, 2021, 2023 and 2024 AGMs and Dr Williams did not speak during the formal Q&A sessions at all four events.

Sinclair family concert party

- The Sinclair family concert party is led by MTVW chief executive Duncan Sinclair, and eight years of the party outvoting unhappy shareholders prove the arrangement effectively controls the group.

- MTVW first formally mentioned the concert party during FY 2005, at which point the aggregate party shareholding was “approximately 53%“.

- The last update on the aggregate shareholding occurred during November 2022 and declared a 50.4% ownership.

- MTVW last confirmed the membership of the Sinclair family concert party during January 2020:

- Anray Limited (associated with Mrs Angela Williams)

- Mrs Elizabeth Langrish-Smith

- Mrs Emma Adjaye

- Mr James Langrish-Smith

- Mr Matthew Langrish-Smith

- Scorpion Estates Limited (associated with Mrs Elizabeth Langrish-Smith)

- Mrs Susan Mary Simkins

- Mr Ronnie Simkins

- Miss Louise Simkins

- Mr Thomas Simkins

- Whitehart Holdings Pty Ltd (associated with Mr Alistair Sinclair)

- Viewthorpe (Old) Limited (associated with Mr Alistair Sinclair)

- Mr Duncan Sinclair

- Sinclair Estates Limited (associated with Mr Duncan Sinclair)

- The Sinclair Charity (associated with Mr Duncan Sinclair)

- Viewthorpe (Subco2) Limited (associated with Mrs Susan Mary Simkins)

- Mrs Angela Williams

- Mr Rupert Williams

- Courtland Capital Limited (associated with Mr Rupert Williams)

- Frank & Daphne Sinclair Grandchildren Settlement

- Leading concert-party members Mr Alistair Sinclair, Mrs Elizabeth Langrish-Smith, Mrs Angela Williams and Mrs Susan Simkins are children of MTVW co-founder Frank Sinclair.

- Chief executive Duncan Sinclair is the son of MTVW co-founder Irving Sinclair.

- I believe every other concert-party member listed above is a relation of either Mrs Elizabeth Langrish-Smith, Mrs Angela Williams or Mrs Susan Simkins.

- The question for unhappy shareholders is how long can the Sinclair family concert party remain intact to retain effective control of the group?

- Companies House reveals the leading party members are between 69 and 77 years old:

- Duncan Sinclair (born October 1947);

- Mr Alistair Sinclair (born September 1949);

- Mrs Elisabeth Langrish-Smith (born April 1952);

- Mrs Angela Williams (born April 1952), and;

- Mrs Susan Simkins (born May 1955).

- At some point the collective 50.4% will be controlled entirely by younger members of the Sinclair family, who may have an alternative approach to handling a £177m aggregate investment.

- Indeed, the aforementioned disposal of shares by the wife of non-exec Dr Williams (see Trading properties: properties valued by Allsop) shows that not every member of the concert party is a die-hard MTVW shareholder.

- After the £315k disposal by the wife of Dr Williams, other concert-party members need only sell shares worth £1m or so at £90 for the concert party’s stake to fall below 50%…

- …which may then allow the concert party to be outvoted.

- No wonder board remarks at the 2024 AGM about the concert party’s holding were limited to simply “It’s over 50%“.

- From what I can tell from my AGM attendances and messages via my contact page, the concert party has not lined up a family member to one day succeed chief executive Duncan Sinclair.

- Back in 2014, MTVW’s then chairman had indicated succession planning was underway:

[FY 2014] “Duncan Sinclair has been with the Company for 43 years, during which he has occupied the positions of Company Secretary, Director, Executive Chairman and Chief Executive. The Company has grown and developed significantly since Duncan became Chief Executive in 1990. The search to find and establish Duncan’s successor is on going and now intensifying. This is an important phase in the Company’s development.“

- But a year later that chairman had left and Duncan Sinclair said he was staying put:

[FY 2015] “Our management teams continue to evolve and it may become appropriate to appoint one or more of these personnel to the Board. The continuing good results and the sound financial structure of the Company are a testimony to tried and trusted methods and tried and trusted personnel. Whilst we are aware of the need for our management structure to evolve for the future benefit of the Company, our results do not suggest that radical surgery is needed as a matter of urgency.

“The default retirement age has been abolished and shareholders will be aware that many companies are being well served by men and women who would once have been regarded as being of advanced years. I may be considered to fall into this category, but I will be happy to step aside when we have in position those of proven ability who are capable of producing results at the level for which I have been responsible for an extended period of years.“

- With Duncan Sinclair still in charge today, that 2015 text suggests MTVW has never found anybody to match his “proven ability”.

- At some point of course, a new chief executive will be needed and, without an obvious family successor, the Sinclair family concert party could be at risk of losing its grip on the boardroom.

- But the wait for a leadership change could be protracted. Chief executive Duncan Sinclair is 77 and his father, co-founder Irving Sinclair, retired from the board at 86.

- Still, MTVW has always been a company for long-haul investors. The group was established during 1937 and floated during 1960, since when the shares have climbed from (an estimated) 11p to £90 with at least another £60 per share of dividends declared along the way.

- Family shareholders (even unhappy ones) have generally kept their shares through thick and thin… attracted presumably by the genuine asset backing, reliable dividend and the prospect one day of a trade sale when family leadership is no longer available.

- Board remarks during the 2024 AGM provided encouragement that a trade sale may one day occur. When asked about what happens to MTVW when the shrinking pool of regulated tenancies finally disappears, the chief executive said:

[AGM 2024] “We will have to consider what else to do. It could be that we just gradually pay dividends and ultimately return the capital and wind up the company in that manner. On the other hand, there may be another company that has other specialisations but is very capable of taking the rump of our portfolio, who may come in and buy that rump. We’re not very near that date yet.“

- In the meantime, one could surmise while MTVW patiently waits for its regulated properties to be vacated to earn a suitable return…

- … unhappy shareholders are patiently waiting for the boardroom to be vacated to earn a suitable return.

Valuation

- MTVW’s shares might be attracting bid interest today were it not for the majority concert-party holding.

- I calculate the shares could be worth £182 were all of the group’s regulated tenancies to end immediately and the properties then sold at a fair market value.

- The following table outlines my £182 sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less sold Allsop-assessed stock (£k) | (137,904) |

| 179,747 | |

| Allsop-premium-to-book | 2.10x |

| Sold-premium-to-Allsop | 1.57x |

| 591,558 | |

| Stock purchased since Sept 2014 | 266,651 |

| Possible property stock value (£k) | 858,209 |

- I have taken the estate’s September 2014 value of £318m and subtracted the (estimated) £138m book value of Allsop-assessed properties sold since that date.

- I then multiplied the £180m remainder by the 2.1x ‘Allsop-premium-to-book’ multiple and then added the 57% ‘sold-premium-to-Allsop’ gain that was realised during this FY.

- I arrived at a £592m estimate for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has acquired additional properties with a £267m book value.

- I have assumed these additional properties will be sold for their £267m book value — based upon my analysis of properties bought and then sold since the Allsop assessment (see Trading properties: properties not valued by Allsop).

- Adding the £592m and the £267m together gives £858m.

- This next table adjusts that £858m for 25% taxation, the £26m conventional property portfolio, net debt and other liabilities to give a possible NAV of £708m or £182 per share:

| Possible property stock value (£k) | 858,209 |

| Less tax at 25% (£k) | (102,953) |

| Plus other investments (£k) | 25,568 |

| Less net debt (£k) | (65.761) |

| Less other liabilities (£k) | (6,573) |

| Possible NAV (£k) | 708,490 |

| Possible NAV per share (£) | 181.71 |

- My estimated NAV sums are not perfect, and the following questions remain unanswered:

- How long will MTVW take to sell all of its properties?

- Will future house-price inflation compensate for being unable to sell all the properties immediately?

- How relevant is the 2014 Allsop assessment today?

- Will properties bought since the 2014 Allsop assessment continue to be sold close to cost price?

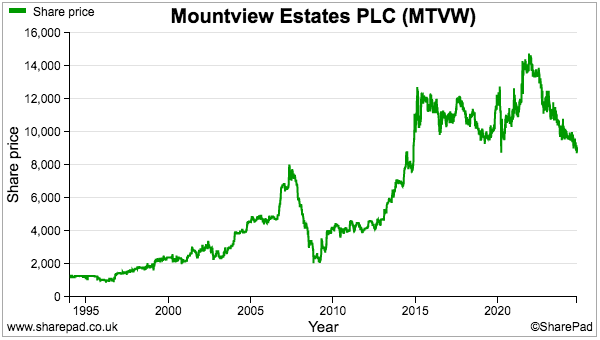

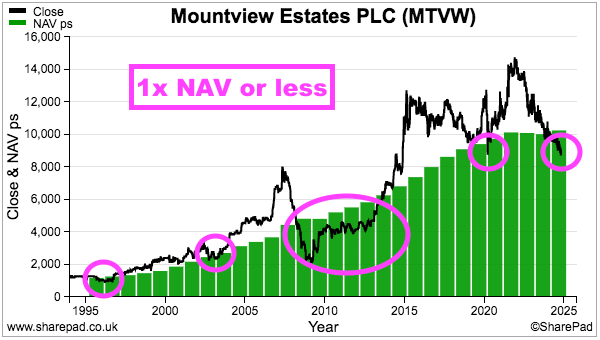

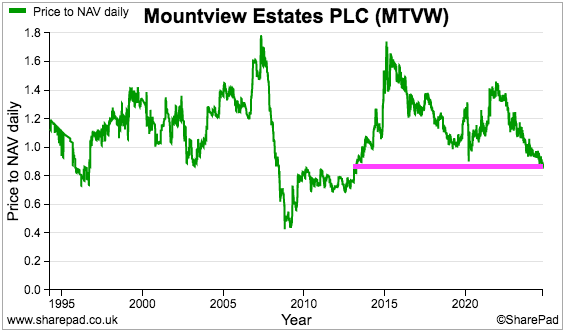

- MTVW’s shares have drifted lower to trade 12% below NAV:

- The best time to buy appears to be when the market cap trades at (or below) NAV, at which point no future gains from any property purchases are priced into the valuation.

- What future gains could lie ahead?

- As noted earlier, the combined additional NAV and dividend return over the last five years comes to £141m or 38% — equivalent to a compound average return of 6.7%:

- The next five years repeating that 6.7% annualised return may not enthuse prospective investors given:

- MTWV’s returns have been declining over time;

- Post-2014 property purchases appear to have realised very modest gains;

- Ongoing protest votes have not persuaded the board to undertake a new Allsop-type valuation, and;

- New legislation will probably increase costs and reduce future margins.

- Perhaps a discount to NAV is actually now required to generate suitable investment returns.

- The 12% discount to NAV is the steepest for more than ten years:

- For what it is worth, my original MTVW purchase occurred during 2011 when the £42 shares traded at 0.75x the then £55 per share NAV.

- For further perspective, the shares sank to £21 at the depths of the 2008 banking crash, giving buyers a 0.44x NAV multiple versus the then £48 per share NAV.

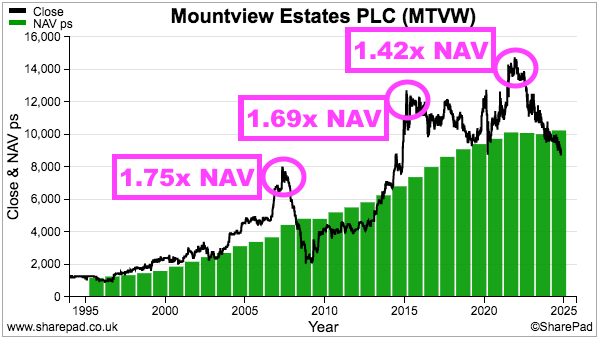

- Taking a positive view, the aforementioned 2014 Allsop assessment pushed the shares to £125 during early 2015 as buyers paid 1.69x the then £74 per share NAV:

- Another Allsop assessment divulging further ‘hidden value’ could easily prompt a favourable price-to-NAV re-rating.

- Occasional bouts of wider market optimism can also push the share price well beyond NAV. In particular:

- The £145 peak during 2021 was equivalent to 1.42x the then £102 per share NAV, and;

- The £80 peak during 2007 was equivalent to 1.75x the then £46 per share NAV.

- At least future returns from today should be front-loaded by dividends:

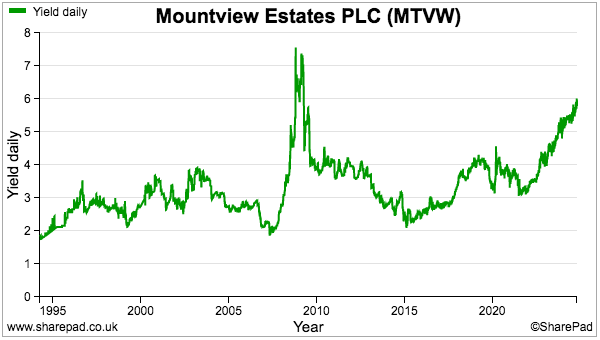

- The illustrious ordinary payout supplies a 5.8% income at a £90 share price — the highest yield for at least 30 years excluding the banking crash.

Maynard Paton

I think the upgrading of the EPC from E to C will be much more than the Rightmove estimate of 8k. All properties are old housing stock and the upgrade can be considerable and even unsightly eg insulation on internal walls or worse externally. I think that a figure of 25-30k a property would be more realistic.

As a longstanding holder of MTVW I am a bit disappointed with the slightly spivvy way it is run. There aren’t many tenancies of this type left to buy, so what is the plan?

Thanks for your detailed analysis though.

Best wishes

Bertie

Hi Bertie

Thanks for the message. On the EPC, I think Allsop has touted a £10k EPC estimate in the past and the figure as you say could be a lot more. I asked at the 2023 AGM about EPC costs, and the board would not divulge the proportion of properties in band D or below, nor was a rough cost per property disclosed. At the time, the board needed further detail of the legislation before trying to predict the upgrade cost per property.

On the long-term plan, this was asked at the 2024 AGM and the board said the company could continue to carry on or perhaps entertain an offer to sell up:

“We will have to consider what else to do. It could be that we just gradually pay dividends and ultimately return the capital and wind up the company in that manner. On the other hand, there may be another company that has other specialisations but is very capable of taking the rump of our portfolio, who may come in and buy that rump. We’re not very near that date yet.“

Maynard

Maynard

I have held Mountview for eight years and sold it this morning at a 25% loss. I just ran out of patience. No doubt there will be a bid at £200 a share tomorrow. You should be congratulated on the quality of your analysis which I had hoped would get the board to provide some more information to refute or support your comments.

Mountview should not be a public company. The information provided to shareholders is inadequate. I have no knowledge of the likely asset value, no information is provided on age structure of tenants, the CEO who is the largest shareholder is hugely overpaid for such a small and simple one product company. I have attended two AGMs during this period and no questions were properly answered. No information on succession planning, No information on long term plan. A badly run company with incompetent communications. My fault – I should never have bought the shares all those years ago.

Hi Max

Thanks for the comment. All very fair points, and sadly reflected by the market cap trading below the historical NAV cost of the properties! The saving grace is I guess the CEO will not be around for ever and, at that point, some sort of corporate action should realise the true value of the balance sheet. But all that may take another eight years at least :-(

Maynard

Thank you for the detailed analysis on Mountview Estates Maynard. We’ll add to our holding.

Thanks Vic!

Just a quick follow-up on purchase costs. I mentioned in the blog post above that MTVW spent £45m last year on new properties excluding purchase costs, but £48m with purchase costs included. Greater purchase costs may be influencing the returns MTVW enjoys when properties are eventually sold.

MTVW disclosed the £45m within this section of the annual report:

The text says: “The analysis does not include legal and commission expenses directly related to the acquisition of properties, or any repairs of a capital nature”

I derived the £48m by calculating the difference between the year-end stock figures (£446m less £423m = £23m) and then adding on the cost of properties sold (£25m).

Purchase costs (and repairs of a capital nature) therefore came to £48m less £45m = £3m — equivalent to 8% of the initial £45m spent.

Going back over the last 10 years, I reckon MTVW has spent a total £300m on new properties before expenses and a total £32m on purchase costs and repairs, which means on average MTVW added almost 11% each year to acquisition spend through legal fees or improvement expenses.

There is sadly no real pattern to the numbers. FY 2023 saw acquisition spend advance 7% due to legal fees and improvement expenses, while FY 2015 saw a 17% advance. FY 2010 in fact saw a massive 68% advance.

I get the impression the purchase-cost fluctuations must be due primarily to repair expenditure, which I suppose can vary significantly from year to year. I would expect stamp duty on purchases (and perhaps legal fees and commissions) to vary in line with the amount spent.

All told, the ultimate judge of MTVW’s past property buying is the property-sales gross margin, and that has (very unusually) been less than 60% for three years now. Maybe MTVW is not achieving sales prices that adequately compensate for the near-11% extra purchase and improvement costs experienced during an average year.

Maynard

Mountview Estates (MTVW)

AGM attendance 14 August 2024

Below are my notes from MTVW’s 2024 AGM. All five directors were present, alongside 20+ attendees. Questions were asked by Craig Murphy, myself and a number of other investors.

The meeting was once again recorded on audio — certain major shareholders do not get on and disagree about the group’s corporate governance, board membership and other matters. A recording could therefore be useful as to who said what. My notes are paraphrased/summarised.

The meeting was the usual robust affair, with almost all the questions and statements from the floor including — or at least politely implying — criticism of the board. Dissident shareholder Craig Murphy even mentioned my blog :-)

Despite being an accountant and being pressed repeatedly from different investors, the chairman did not present any facts or figures to counter claims that MTVW’s recent purchases have realised gains far below the levels the board aims to achieve (i.e. a 33% ‘reversionary’ value uplift when buying at a 75% discount to vacant possession value).

Mind you, the chairman did concede the board could consider disclosing more information to explain the matter, which is something I suppose. Non-execs Mhairi Archibald and Andrew Williams did not speak during the meeting. Dr Williams has now not spoken in the last four MTVW AGMs I have attended.

(CM: Craig Murphy; DS: Duncan Sinclair (chief executive); MB: Marie Bray (finance director); MTVW: Chairman; MP: Maynard Paton; Q: Another shareholder)

————–

CM: What management and financial information do the NEDs receive as part of their oversight of the executives?

MTVW: At each meeting get a set of financials, a profit and loss account, with notes about costs. Get notes of properties which have been bought/sold, and anything else deemed relevant. Also get bank balances.

Q: On succession planning, you were aware that Ms Archibald’s tenure was due to end on 30th June 2023. She has been voted down by the independent shareholders many times. If she is voted down today, the honourable thing for her to do is to say “I’ve done my nine years, and in accordance with the Code, I will accept the verdict of the independent shareholders“.

MTVW: Have interviewed a number of people. None worked out. Search is continuing. Have a further round of interviews In the coming weeks.

Want to keep the board balanced and retain her skills. Decided to offer extension which would take her up to the end of this financial year. Then include a period of handover with the incoming NED.

Q: In seeking a replacement for Ms Archibald, you appear to have been dilatory in the extreme. You are now taking help from headhunters. You could have done that two years ago.

MTVW: Started process last year. Before then would be potentially premature. We are where we are. Not where we hoped we were going to be last year.

Q: Is succession planning is one of your risk issues?

MTVW: Not regarded as a risk issue. But general succession is covered during nomination meetings. In particular succession for Ms Archibald and Duncan Sinclair. Satisfied arrangements will cover short-term absence. For long-term absence, process described in the nomination report will start.

CM: My calculations and those of Maynard Paton both suggest that, since the valuation in 2014, the sales proceeds of properties bought since 2014 are about £10m short of what buying at 75% of vacant possession value would suggest.

Why haven’t you commented on this? Are these figures broadly correct? Will you publish the cost of sales split between pre-valuation and post-valuation purchases?

MTVW: What drives gross margin and revenue are related and outside the company’s control. Applies both to the pre- and post-2014 purchases. IRRs generally over both periods are pretty much the same. Some are up, some down. Some disappoint. Very rare a property is sold for a loss.

CM: If you are buying at 75% of vacant possession and selling the property when it is vacant, do you agree there should be a minimum 25% gross profit margin?

MTVW: Not all properties achieve 25%. Also need to account for costs of purchase. 25% margin is based upon assessments at the time of purchase, which might then change. “We’re satisfied that the purchasing process is robust.”

CM: Post-2014 purchases have achieved 7%-8% gross margin. Are you saying the 18% difference is due to a drop in property prices or other extra costs?

MTVW: Not sure what to add about difference between purchase and sale prices. Seen examples where the 2014 valuation was a long way out from the ultimate value. Only things that matter are purchase and sales prices, not the assessed value at some mid-point. “We are content with the returns which have been delivered.”

DS: Rental income is at least 2x the interest charge. Your calculations may be attributing quarterly interest charges to the small number of properties that are sold each year. If you attribute it proportionately, I think your figures should be very different.

[I am not sure the second comment is correct. Craig Murphy was referring to gross margin, and interest costs are not accounted within cost of sales. Although maybe there are financing-admin costs include within cost of sales.]

CM: Will you commit to publishing the split that I asked for within three weeks?

MTVW: Request is noted. We’ll consider it.

Q: Investment properties purchased in 1999 have been less successful than anticipated because of their rental returns. Why did you get it wrong?

MTVW: Looked at the potential at the time, which includes rental income and also capital-gain potential. Good number have been sold.

Q: Two adverse online comments from tenants. One of whom said they had no heating. Do you use Google?

MB: Yes we use Google. There is a dispute and can’t give details. “You have to know both sides and the argument behind this“. We look after our tenants very well. “We fulfil all the regulations which are required to make the lives of the tenants, most of whom are very elderly, as comfortable as possible.” Have lots of tenants and these are just two “very unfortunate incidents“.

[Note: Google reviews here]

MP: Going back to Craig’s question, he mentioned my blog about the purchases since 2014. Are you saying my blog calculations are wrong? What am I missing?

MTVW: “Calculations from the outside are based upon summary level information and lead to a different answers to what you get from the inside, which include precise costs associated with the individual properties.”

Understand your calculations. Can see how they stack up. But they don’t represent individual properties.

MP: Outside shareholders are getting the wrong impression then from your accounts. Craig has drawn his conclusion and I am drawing the same conclusion. David Pears last year was drawing the same conclusion as well, that perhaps the properties you have been purchasing since the valuation in 2014 have not realised the gains that a 25% discount to vacant possession would suggest.

If you look at the share price now, which is £96 and trading below net asset value, it looks like the wider market is not convinced about your purchases in the last 5 or 10 years. Do you have any comments on that?

MTVW: Drivers for sales and cost of sales all based on factors completely outside of the company’s control. But with longer holding periods, you get the larger gross margins. But you get lower gross margins where the average holding period is lower. Accept what you’re saying about more information. Can consider what else disclose.

MP: You should disclose more information on the margins of the properties being sold. That way we get the right calculations. Otherwise, we all draw the wrong conclusions. We’re all thinking, and the market is thinking, that the properties you’ve bought recently are just not making the gains that you suggest they can. You should disclose more information so we can get the right information and we can then draw the right conclusion.

MTVW: Noted.

Q: Discussion shows a desire for more information. Company is listed on the stock exchange and has an obligation to inform shareholders. Company should undertake a new valuation so we would not have to look back at 2014.

If purchasing team can value properties for purchase [at 75% of vacant possession value], they can also value the owned properties and then tell us what all these properties are worth to a third party.

MTVW: Valuation team calculates a value and sets upper buy limit. Company’s key strength is patience to get possession. Only at possession is the property sold and the value then is what matters.

DS: “Every sale goes across my desk. I look at the purchase price which is one of the certainties we have and I look at the sale price which is the other certainty we have.”

Had a property purchased in 2003 for £78k. In 2014 valuer gave a price of £175k. Auctioneers guided the price at £155k this year. Reserved at £170k. Sold at £171k. More than doubled our money in 20 years. But look at the different figures.

Q: Vital the purchase team has competence to judge a property’s market value when buying. And therefore they have same the competence to do that analysis to the existing estate.

[Lots of subsequent discussion then followed about the intricacies of property valuations, all of which I did not minute]

CM: If purchases after 2014 have been at 75% of vacant possession, publishing additional information will show that. Now had 10 years of accounts and “if you don’t publish the additional information in the near future, I think you’re going to have an EGM on your hands to ask more detailed questions“. Market is getting a completely wrong impression of the purchases over the last 10 years.

MTVW: Will look at the information that we publish. Understand the desire to segment

[Lots of subsequent discussion followed between CM and the chairman about IRRs and vacant possession discounts, and the chairman apparently mixing the two up, all of which I did not minute]

CM: Instead of paying 75% of vacant possession, maybe you’re paying 90% or 95% of vacant possession. And is that a concern? Issue is you are paying more than you should.

MTVW: Subjectivities are involved and will be times when they outperform. Will be times when they don’t. Kind of where we are. Have heard the comment and understand it.

MP: You have spent £100 million on new properties over the last two years. How much extra rental income should that £100 million generate?

MTVW: Haven’t got the details. Typically look for 2.5%-3%.

DS: A regulated rent is set according to the accommodation. “The idea of a regulated rent is that it’s the same in Chelsea, Charlton or Chesterfield.” Obviously the values of the property are different. You can buy a regulated tenancy at 75% is because that rental return is so much less than the full market return.

[The line “The idea of a regulated rent is that it’s the same in Chelsea, Charlton or Chesterfield” caused much discussion among attendees in the post-meeting chat. At least two attendees who are/were professionally involved in the sector independently said to me that DS was very mistaken. One attendee even claimed DS had “deteriorated“).

MP: With the pool of regulated tenancies shrinking every year, what’s the eventual end game for the company? Is it going to continue operating until the very last regulated tenancy is bought and sold, which could be several decades away. Or is there an alternative outcome for the company?

DS: Go back to the 1988 Rent Act, and some then thought in 30 years the sector would not exist. They thought the average regulated tenant was middle-aged. But some were in their 20s, so now in their 50s.

“That 30 years starts now, rather than in 1989“. People who once bought regulated tenancies have gone different ways. Less properties to buy, but less people now trying to buy them.

“We will have to consider what else to do. It could be that we just gradually pay dividends and ultimately return the capital and wind up the company in that manner. On the other hand, there may be another company that has other specialisations but is very capable of taking the rump of our portfolio, who may come in and buy that rump. We’re not very near that date yet.”

Q: You say another company might take the rump of the business. Have you ever had any approaches, either for the whole company or for the investment properties?

[After some whispering between the chairman and chief executive…]

MTVW: No.

[Now followed a mini-Q&A about two specific ground rents in Kensington (interrupted by the questioner’s phone ringing!), all of which I did not minute]

MP: The annual report says that the board engaged with some shareholders to seek their views after last year’s AGM, and some shareholders raised matters which are under consideration by the board. So what were those matters which were under consideration by the board?

MTVW: “The discussions were with shareholders who are not here today and we will not disclose what was said, and certainly not without their permission.” “They raised questions and, where we felt that it was appropriate that we could make the change, we have.”

[Seems like the discussions were held with major shareholder David Pears, who attended the 2023 AGM and was not present at this 2024 meeting]

MP: Have those matters been raised today in this meeting?

MTVW: No.

MP: At last year’s AGM there were significant votes against the executives as well as the non-executives. So has there been a board response to that? Is there any sort of different way of operating after that voting?

MTVW: Always try to engage with the shareholders who vote against. We took on their comments and made changes if something that was relevant. But difficult to say what the concerns are of the shareholders who do not engage with us.

[Now came a question/statement about regulated rent calculations in Chelsea, and whether such rents are indeed the same as in other parts of London as DS claimed earlier. The shareholder, a property investor, explained how different areas have different regulatory rents, just like market rents can differ from area to area. I did not minute the subsequent back-and-forth, but DS did conclude by pointing to the annual report and stating…]

DS: “This thing is already getting to where it’s fit for a weightlifting contest. Fifty years ago, eight pages told you everything you needed to know… Does this company make a profit? Yes. Does this company pay a dividend? Yes. When does it pay the dividend? All that information, the vital information is in there.”

CM: Company articles allow gearing of up to 300% but requests by independent shareholders to reduce that limit have been overruled by the chief executive. Does the chief executive think the 300% limit is too high?

MTVW: Articles were passed in 2010. Not going to take it to 300%. Never going anywhere near it. Borrowing limits are set “in accordance with currently accepted criteria” and that figure gives 300%. If our advisors said to use different criteria, we would.

[Now followed a mini-Q&A between Craig Murphy and the chairman about Mhairi Archibald’s status as an ‘independent’ non-executive and the finer points of corporate-governance disclosures, all of which I did not minute]

CM: The chief executive is now an ex-member of the ICAEW. Was there a complaint or did he simply resign?

DS: “I think that is a question about my private life. I refuse to answer it, and you should not have the impertinence to ask it.”

CM: What is the number of shares — not a percentage — held by the concert party?

MTVW: “It’s over 50%, and that’s all I’m saying.”

MP: Gearing is now at 14%. Said last year you’d be comfortable going up to 25%. Is that still the case?

MTVW: Yes, but doesn’t mean we will. Consider the point when rental income become in danger of being exceeded by interest costs. 25% gives comfort that there is headroom. Getting to that point would cause us to review.

MP:Do you look at rental income and making sure rental income covers admin costs and all your interest costs as well, so you have a positive balance after all those?

MTVW: Yes.

MP: If rental income is less than those costs, that would be some cause for concern? You would study the debt level a bit more closely?

MTVW: When looking at a purchase, we know the interest cost and the rental return. That drives how much we would pay. The overall portfolio covers all the admin costs, the cost of sales for the rental side and the interest costs.

MP: I assume there is no forthcoming valuation. Is that still the case?

MTVW: Yes.