30 May 2023

By Maynard Paton

H1 2022 results summary for Tasty (TAST):

- The absence of pandemic restrictions ensured H1 sales returned to pre-Covid levels, with sales per restaurant of £797k encouragingly at their best H1 level since H1 2016.

- A “steep rise in inflation in relation to wages, utilities and input supplier costs” limited underlying profit to just £0.2m and will “inevitably impact” the H2 performance.

- Pandemic-prompted rent reductions seem to have run their course, with annual lease costs appearing to return to £5m and total lease obligations staying at £52m.

- Management curtailing plans to open 5-6 new restaurants was disappointing but understandable given the “prevailing economic uncertainties“.

- Can TAST ever achieve a worthwhile margin from revenue now running at almost £45m? No evidence has emerged that TAST’s restaurant formats can easily pass on, reduce or absorb much higher costs. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TAST

- Results summary

- Revenue and profit

- Revenue per restaurant and employee

- Financials: going concern, cash and deferred payments

- Financials: landlords and leases

- New openings and rising costs

- Valuation

News links, share data and disclosure

News: Interim results for the 26 weeks to 26 June 2022 published 19 September 2022 and directorate change published 17 February 2023

Share price: 3.25p

Share count: 146,315,304

Market capitalisation: £4.8m

Disclosure: Maynard owns shares in Tasty.

Why I own TAST

- Disastrous ‘legacy’ shareholding bought initially due to experienced family management creating, building and then selling two quoted restaurant chains for £200m-plus.

- Revenue rebounding to pre-pandemic levels, greater takeaway/delivery sales, a resurgent dim-t format and the presence of net cash gives hope that all is not lost.

- Bombed-out share price might provide substantial turnaround upside… assuming the group can return to — and then maintain! — a worthwhile level of profit.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

Revenue and profit

- TAST’s outlook from the preceding FY 2021 suggested this H1 would show satisfactory trading albeit with higher costs:

“Trading prior to Christmas was strong and the start of 2022 is encouraging, but this must be tempered by the challenges which the Group expects following the end of Government support including VAT and business rates, the risk of a reduction in pent-up demand, disposable income and staycations as well as a steep rise in inflation in relation to wages, utilities and input supplier costs as the UK adjusts to Brexit, the aftermath of the pandemic and the current war in Ukraine. Accordingly, the Board views the future with cautious optimism.“

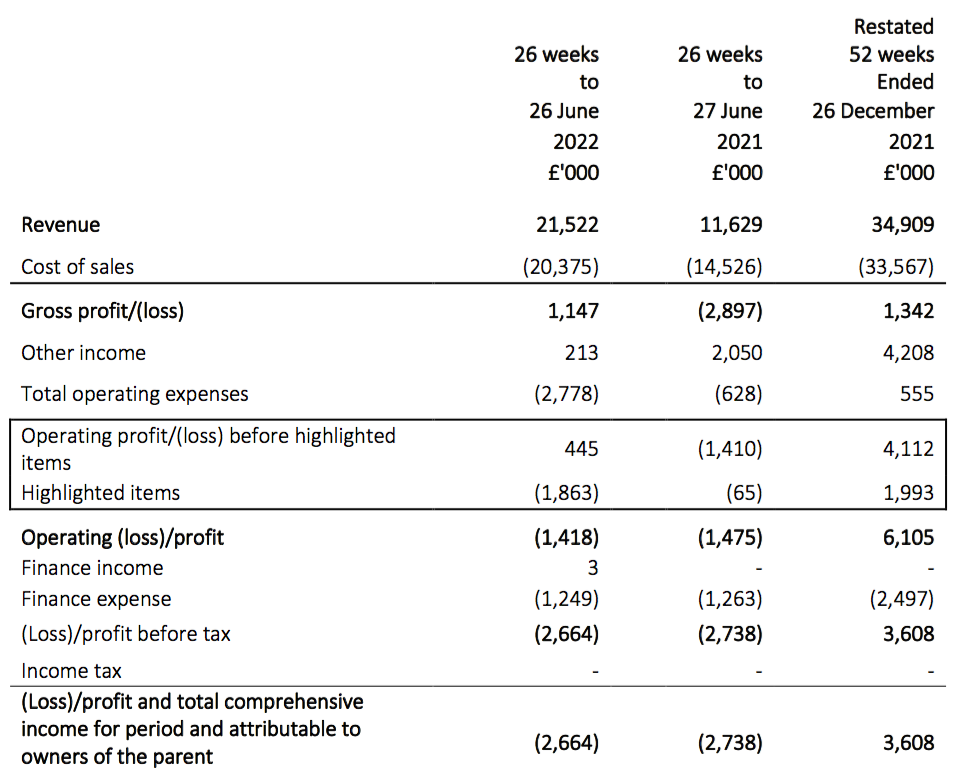

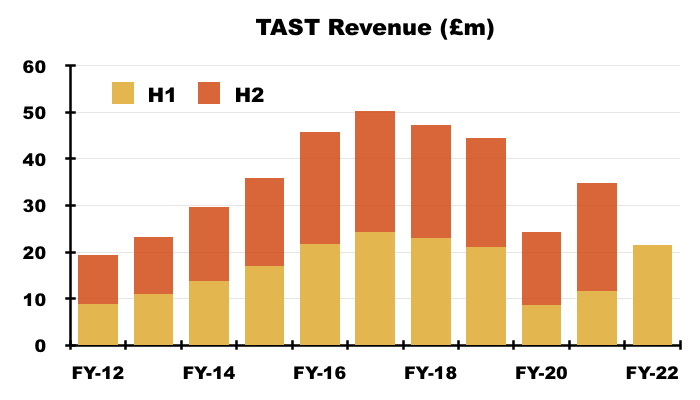

- H1 revenue in fact surged 85% to £21.5m after TAST operated without any pandemic restrictions for the first H1 since H1 2019:

- H1 revenue of £21.5m exceeded the £21.1m reported for H1 2019, and continued TAST’s recovery to trading levels witnessed before the pandemic.

- The preceding H2 2021 had reported revenue of £23.3m, which was a fraction below the £23.4m recorded for pre-pandemic H2 2019.

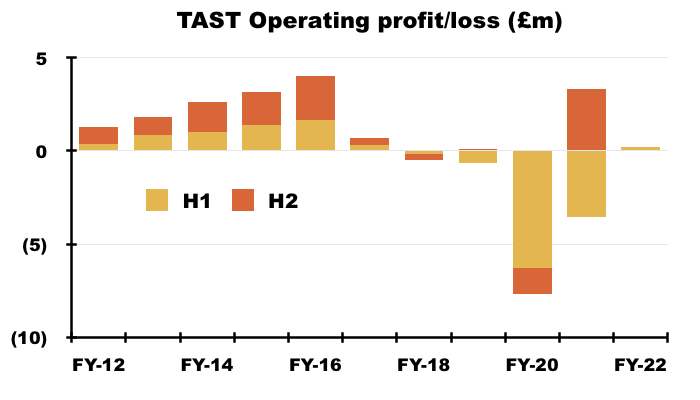

- Reflecting a “steep rise in inflation in relation to wages, utilities and input supplier costs“, operating profit was just £0.2m before a collective £1.8m charge for various ‘highlighted items’ and sub-let income of £0.2m:

- TAST did not collect any government pandemic benefits or similar during this H1.

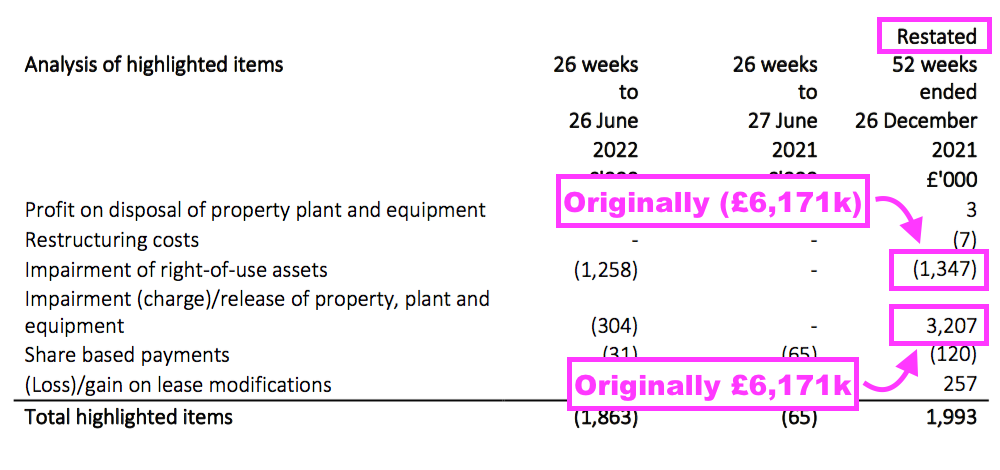

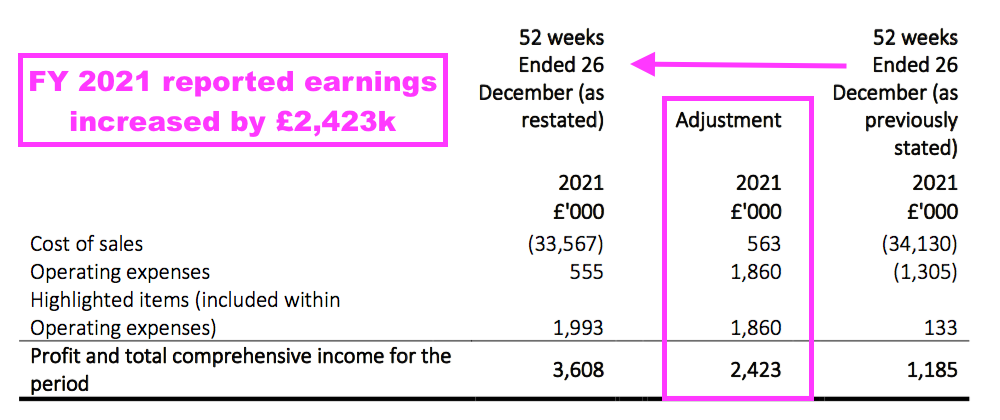

- This H1 restated various figures for the preceding FY 2021 that I said were confusing within my FY 2021 write-up:

“TAST’s highlighted items showed a confusing pair of balancing £6,171k entries for the impairment and impairment release of tangible assets“

- The restatement for the preceding FY 2021 concerned “the treatment of depreciation on impaired assets and reversal of impairment“:

- The FY 2021 restatement added a further £2.4m to that year’s total profit and was underpinned by a (revised) write-back of previously written-down assets:

- As such, the preceding H2 operating profit now seems to have been £3.3m (before highlighted items and government pandemic benefits) rather than the £2.7m I had calculated initially.

- Revising annual earnings from £1.2m to £3.6m is not a great advert for TAST’s accounting and February’s appointment of a new finance director is therefore very welcome.

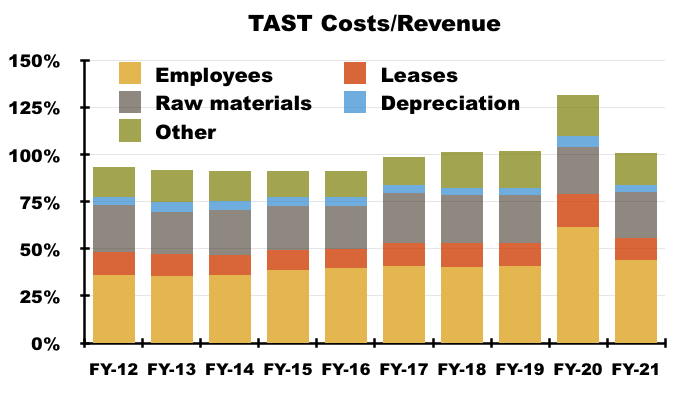

- That bumper H2 profit was generated by a very favourable 18% gross margin, while this H1’s minimal profit reflected the gross margin reducing to 5%.

- TAST acknowledged wider economic issues had limited its gross margin and would continue to do so during H2 2022:

“Like many of our competitors and the economy in general, we are facing severe headwinds. Inflationary pressures on food, labour and utility costs and the cost-of-living crisis will inevitably impact the performance of the Company for at least the remainder of the year. “

- A positive H1 snippet concerned the “resurgence” of TAST’s dim t dim sum chain:

“Our dim t brand has experienced a resurgence, and we are converting the former underperforming Wildwood in Loughton to a dim t, which is due to open in the Autumn.“

- TAST’s dim t format has for years operated as a sideshow to the group’s 48-site Wildwood pizza/pasta/burger chain, but now trades from six locations and may even have scope to enjoy further Wildwood conversions.

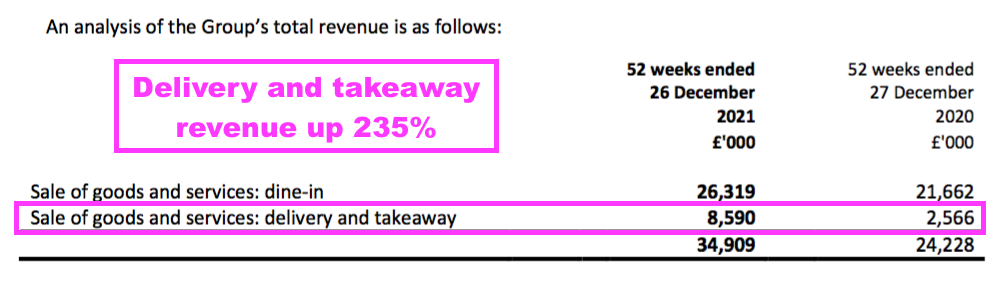

- The preceding FY 2021 results were the first to segment dine-in revenue from delivery/takeaway sales:

- But TAST sadly did not segment the dine-in/dine-out revenue for this H1, stating only that its takeaway and delivery business had “grown“.

- Delivery/takeaway sales represented 25% of total revenue during the preceding FY 2021, and such income offers shareholders the hope of improved restaurant economics versus the marginal dine-in profits experienced prior to the pandemic.

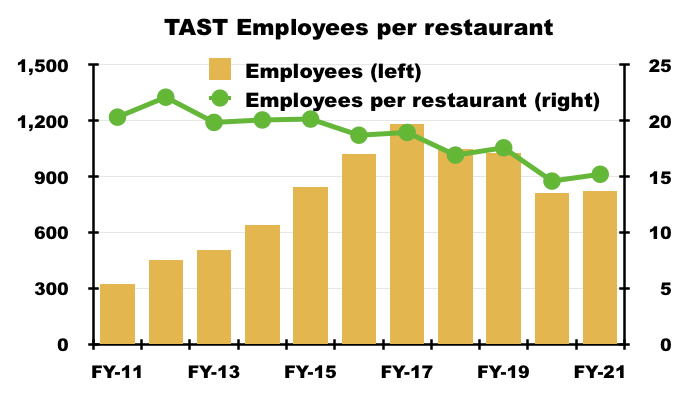

Revenue per restaurant and employee

- TAST confirmed 51 of its 54 restaurants traded throughout this H1.

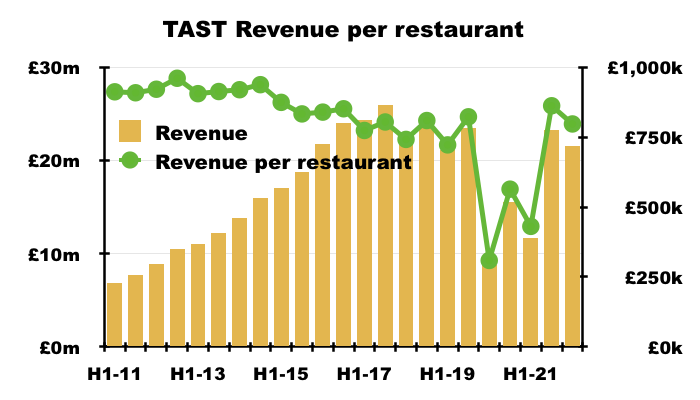

- Revenue per restaurant for H1 was £797k (£21.5m*2/54):

- £797k per restaurant compares to £722k for (pre-pandemic) H1 2019 and was the best H1 performance since H1 2016 (£839k per restaurant).

- Revenue per restaurant for this H1 and the preceding H2 was £830k and compares to £762k for (pre-pandemic) FY 2019, and was the best twelve-month performance since FY 2016 (£841k per restaurant).

- The calculation for this H1 2022 could arguably be £820k per restaurant based upon the 51 sites that traded during the six months.

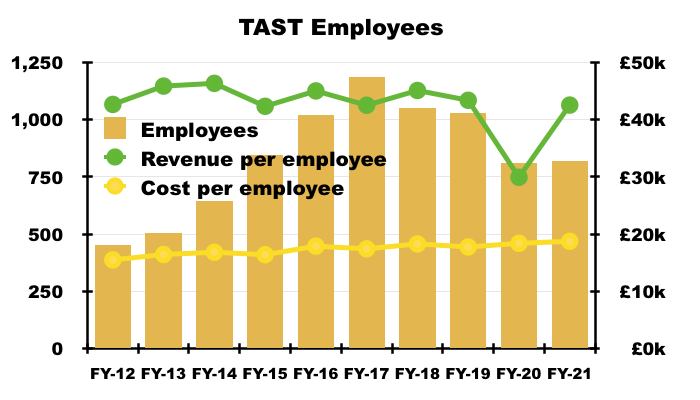

- Revenue per employee remains comparable to levels witnessed before the pandemic.

- The preceding FY 2021 had disclosed a headcount of 934, while this H1 confirmed the headcount now exceeded 1,000:

“In a tight labour market, we are pleased to say that the number of people we employ is back to over 1,000 following the requisite redundancies during the pandemic.“

- Assuming the average number of staff employed during the preceding H2 and this H1 was 1,000, revenue per employee for the twelve months was £44.8k (£44.8m/1,000).

- Years prior to FY 2020 had seen revenue per employee bob between £42k and £46k:

- This H1 included several references to staffing issues:

- “With a competitive labour market…”

- “To reduce the impact of food and labour challenges…“

- “Staff shortage challenges remain…“

- Mind you, 1,000 employees at 51 open restaurants during this H1 gives 19.6 employees per site, versus between 17 and 18 for pre-pandemic FYs 2018 and 2019:

- I suppose the employment challenge really boils down to pay, with staff shortages more likely to be remedied if wages were much higher.

- Staffing costs remain a concern, not least due to the national minimum wage advancing 10% from April 2023.

- The 2021 annual report (points 1a and 3b) included extensive text on employee engagement, including:

“We have continued to focus on selection, induction, training and retention of our employees. The Group has made significant improvements in its selection process, onboarding training programmes and career development paths. New HR and recruitment systems have been established and proposed to provide consistent and swift support to all colleagues. We have also strengthened our teams. The Group offers competitive remuneration and is reviewing its overall benefits package.

“We have been able to reintroduce manager roadshows to make our wider team feel included in our business and to have time away from their restaurants to sample new recipes, network and chat to our Board members and senior leadership team.

“A full pay and benefits review has been completed to make sure we continue to be seen as an attractive company to work for whilst remaining financially prudent.”

- Alongside TAST’s commendable focus on customer service…

“Our restaurant managers are all focusing on delivering an exceptional customer experience and train their teams on a daily basis to achieve this.”

- …the group’s employment strategy may well differentiate its restaurants in what remains a very competitive sector hampered by rather choosy diners.

- Each TAST employee cost an average £18.7k during the preceding FY 2021, while total employee costs as a proportion of revenue increased from 36% to 44% between FYs 2014 and 2021:

- That 8 percentage point increase to the proportion of revenue absorbed by staff costs helps explain why TAST’s profitability has become minimal.

Financials: going concern, cash and deferred payments

- TAST’s ‘going concern’ text continues to improve following the “existence of a material uncertainty” commentary used within the FY 2020 statement.

- This H1’s ‘going concern’ text no longer refers to the pandemic but does now mention “inflation“:

“The Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. In reaching this conclusion the Directors have considered the financial position of the Group, together with its forecasts for the next 12 months from the date of approval of these interim accounts and taking into account possible changes in trading performance. The Group monitors cash balances and impact of inflation closely to ensure there is sufficient liquidity. Accordingly, the Directors believe that it remains appropriate to prepare the financial statements on a going concern basis.”

- This H1 statement was the first since the FY 2020 results not to refer to a Company Voluntary Arrangement (CVA). The 2021 annual report confirmed a CVA had been avoided (point 1e):

“We have avoided a more formal procedure such as a CVA as a result of the support of our landlords.”

- A statement issued on 23 June 2022 — three days before this H1’s half-year-end — revealed the group’s remaining bank loan had been cleared:

“[TAST]… is pleased to announce that, due to strong cashflow and a healthy net cash balance, the Board has taken the decision to repay, in full, the Company’s £1.25 million four-year term loan (the “Facility”) from its existing bankers, Barclays Bank plc.”

- The June statement also noted cash was £8.6m:

“The Company has now repaid the amount outstanding under the Facility of £1.1 million in full and has subsequently cancelled the Facility, leaving the Group with a net cash balance of approximately £8.6 million and no debt. There will be an annualised cost saving of approximately £57,000 (calculated at today’s rates) through repayment, with no early repayment penalty.“

- Cash in fact ended this H1 at £8.0m and not the £8.6m as claimed three days prior. I presume cash balances can fluctuate significantly from day to day, possibly due to quarterly rental payments.

- Cash adjusted for deferred payments to creditors (such as HMRC and landlords) was £7m, meaning overdue bills of £1m were still to be paid.

- Deferred payments to creditors were previously £3.0m at the preceding FY 2021, indicating overdue bills of £2.0m were repaid during this H1.

- The cash position decreased by £3.0m during this H1, which excluding the loan repayment (£1.3m) and repayment of deferred creditors (£2.0m) gives (£3.0m) plus £1.3m plus £2.0m = a £0.3m ‘underlying’ inflow.

- A £0.3m underlying cash inflow reflects the minimal accounting profit of £0.2m before ‘highlighted items’ and sub-let income.

- I presume the remaining overdue bills of £1m will soon be repaid, given this H1 revealed TAST agreeing “heads of terms for a new Wildwood site in Oxfordshire.“

- Deferred creditors will not be happy remaining out-of-pocket if TAST can now afford to open a new site.

- TAST’s effective £7.0m cash position is not truly surplus to requirements.

- The cash position is inherently a by-product of owing money to suppliers and other parties, with £10m outstanding at the half-year-end suggesting approximately £9m was owed excluding deferred creditors:

Financials: landlords and leases

- This H1 statement gave a short update on the pandemic-prompted rent negotiations:

“The Group has been successful in achieving rent reductions and lease concessions across most of the estate for the period impacted by Covid-19 with the final few agreements completed during H1 2022. We are continuing to review all our leases with a view to disposing or re-gearing low performing sites. “

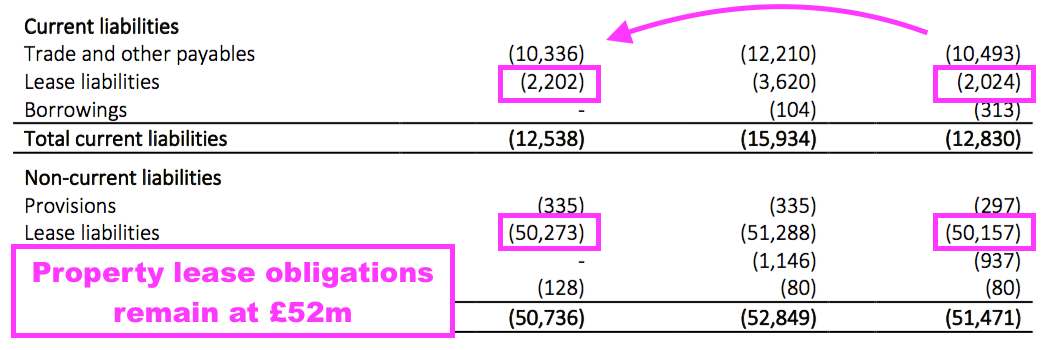

- Lease reductions unfortunately appear to be for a limited time only. TAST’s total IFRS 16 lease obligations (presented on a net present value basis) remained at £52m:

- TAST first reported its IFRS 16 lease obligations to be £56m (on a net present value basis) during H1 2020.

- I had hoped TAST would be able to reduce its total lease obligations by much more than £4m during the last two years of landlord negotiations.

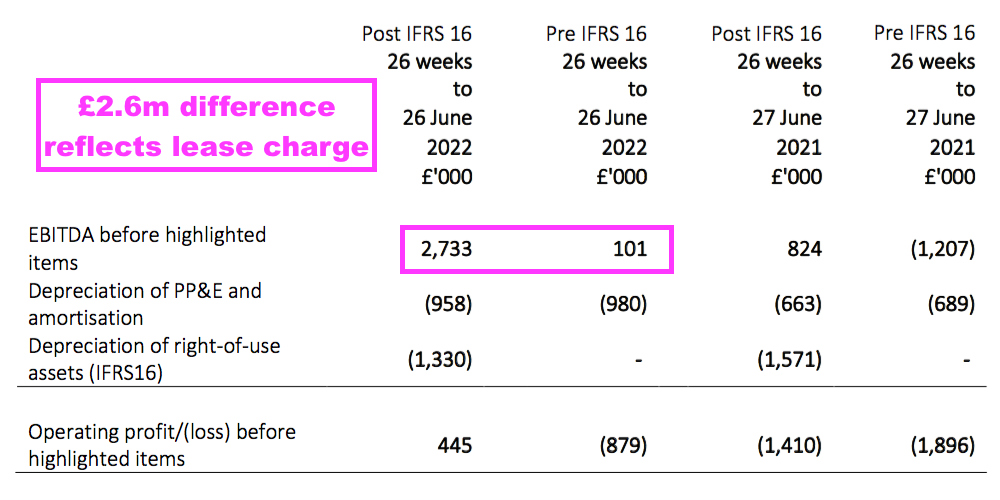

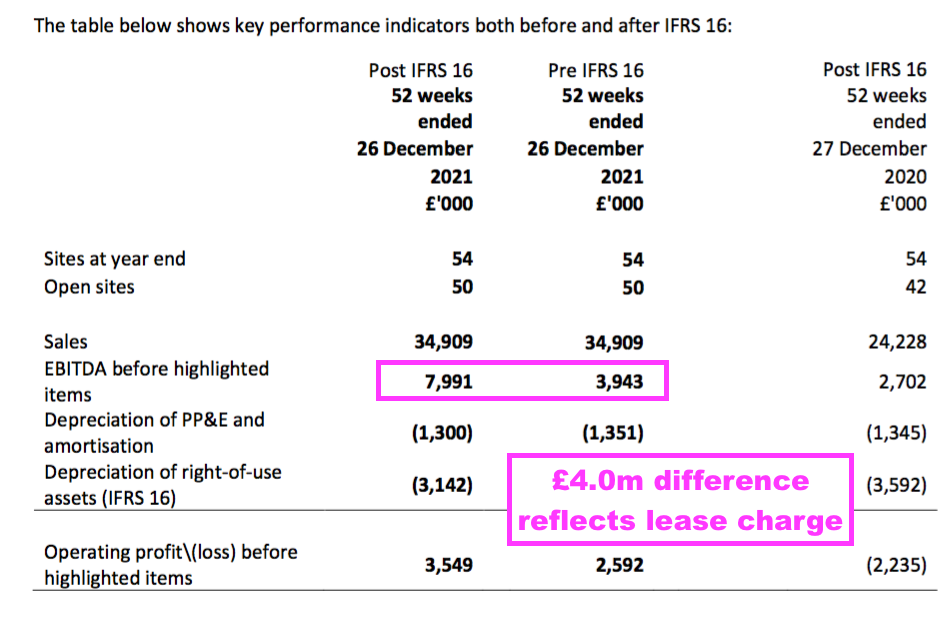

- A further unfavourable lease development was hidden within the pre- and post-IFRS 16 versions of TAST’s Ebitda, from which rent payments can be deduced:

- The £2.6m difference between the H1 2022 Ebitda numbers represents the pre-IFRS 16 lease cost that, post-IFRS 16, is now reflected within the depreciation expense and financing charge.

- £2.6m doubled gives a possible £5.2m lease charge for this FY, and implies rent reductions are indeed temporary versus the £4.0m charged during the preceding FY 2021:

- The possible £5.2m lease charge for this FY is comparable to the pre-pandemic, pre-IFRS 16 lease cost of £5.5m for FY 2019:

- I had hoped TAST would be able to reduce its annual lease obligations by much more than £0.3m per annum during the two years of landlord negotiations.

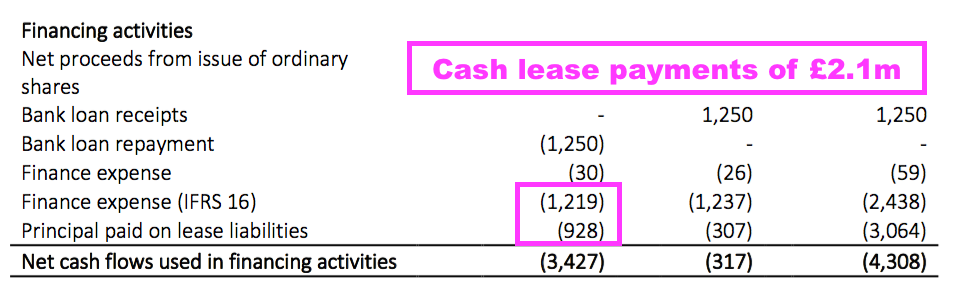

- Cash lease payments during this H1 were £2.1m, some £0.5m less than the £2.6m accounting charge, and which helped ensure ‘underlying’ cash flow was a positive £0.3m (see Financials: going concern, cash and deferred payments).

- TAST’s right-of-use lease asset ended this H1 at £35m, which arguably suggests the group would now pay £18m (£52m minus £35m) less to rent its properties were it to commence the same leases today.

New openings and rising costs

- The greatest disappointment within this H1 concerned the curtailment of TAST’s expansion plans.

- TAST admitted:

“Whilst there is a strong pipeline of sites identified, due to current uncertainties, we have slowed our previously announced expansion plans and will cautiously approach any new openings as we brace ourselves for an even more challenging economic environment, which is beginning to adversely impact our profitability in the second half of 2022. “

- Three months before this H1 statement was published, TAST talked of a pipeline of “up to five or six new units“:

“The Board believes that, with its current net cash and future cashflow, it will have sufficient funds to weather the prevailing economic uncertainties and cost pressures and also satisfy its measured expansion plans for a pipeline of up to five to six new units in 2022. The Board is progressing this strategy and has one new site under offer and is currently negotiating on three others.“

- Opening five or six new sites certainly sounded confident, given the new sites would have enlarged the estate by 10% despite TAST facing “prevailing economic uncertainties”.

- But the measured expansion plans are now limited to the aforementioned “heads of terms for a new Wildwood site in Oxfordshire“…

- …which means the “prevailing economic uncertainties” have curtailed TAST’s expansion plans even before the first new site has opened!

- TAST looks to have been caught out by higher costs during the latter stages of this H1:

“Sales performance compared to 2019 was strong but has been marred by labour shortages and inflationary pressures impacting the hospitality industry. These cost pressures became more acute towards the end of the first half of 2022.“

- TAST added:

“To reduce the impact of food and labour challenges, our menu is constantly being reviewed. We are working with existing and new suppliers to minimise disruption and continue to re-tender. The well documented utility pressures are unprecedented, and the hospitality industry is particularly badly affected. The Government unveiled an energy support plan on 8 September 2022 to support businesses for six months, but the details have yet to be announced. In the meantime, we are looking at ways of minimising our energy usage and improving efficiencies.”

- TAST’s latest menu and energy usage are assessed in my FY 2022 write-up.

- For now, the over-riding question concerns TAST’s operating economics, and whether the group can ever achieve a worthwhile margin from revenue now running at almost £45m?

- This H1 sadly provided no evidence that TAST’s restaurant formats can easily pass on, reduce or absorb much higher costs.

Valuation

- TAST’s valuation is assessed within my FY 2022 write-up.

Maynard Paton