26 November 2015

By Maynard Paton

Quick update on Mountview Estates (MTVW).

Event: Interim results published 26 November

Summary: Another set of bumper results from this residential-property trader. Once again gross margins held up very well while management’s outlook continues to be positive. My latest sums point to a possible NAV of £188 per share based on the firm’s previous mark-ups on sold units. I continue to hold.

Price: £113

Shares in issue: 3,899,014

Market capitalisation: £441m

Click here for my previous MTVW posts

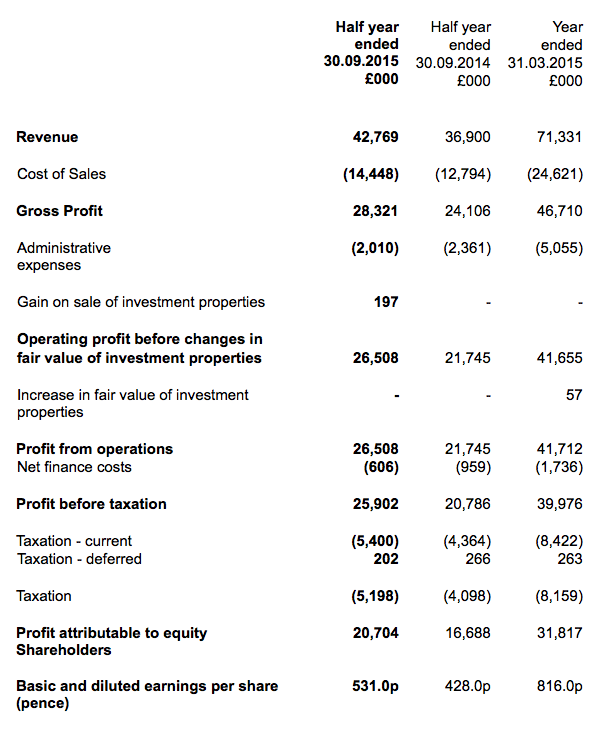

Results:

My thoughts:

* Another handsome set of results

These numbers showcased MTVW’s best-ever H1 performance and continued the trading moment witnessed within June’s record full-year results.

Revenue gained 16%, operating profit advanced 21% while net asset value (NAV) per share climbed 9%.

In addition, the first-half dividend was doubled to 200p per share, although MTVW made clear this increase was a temporary ‘front-loading’ of the annual payment due to forthcoming taxation changes.

This H1 performance also provided reassurance after the possible weak Q4 I referred to in June. (The nature of MTVW’s regulated properties means they become available for sale at any time — typically when the tenant dies — and revenue from month to month can therefore be unpredictable.)

It was significant to see MTVW’s gross margin improve further to 66% — equal to the highest level achieved back in 2008. Clearly the firm is currently able to enjoy good sales prices on the historical cost of its properties.

* Upbeat outlook

MTVW remained positive about the future:

“Acquisitions made during the first six months equate almost to those made for the last full year and there are other purchases already in the pipeline. The Company remains financially sound with gearing at a modest level and trading in line with the Board’s expectations.”

“The outlook for the Company is sound with financing in place to take advantage of any good purchasing opportunities which occur. We can never control the macro-economic situation and presently Europe is experiencing troubled times, but we remain optimistic.”

At £50m, net debt has never been lower since 2007 and compares very favourably to total assets of £363m.

* Younger member of the family appointed to the board

During June 2014 MTVW said:

“Duncan Sinclair has been with the Company for 43 years, during which he has occupied the positions of Company Secretary, Director, Executive Chairman and Chief Executive. The Company has grown and developed significantly since Duncan became Chief Executive in 1990. The search to find and establish Duncan’s successor is on-going and now intensifying. This is an important phase in the Company’s development.”

There has never been any subsequent word on finding Duncan Sinclair’s successor.

However, today’s results were accompanied by news that a younger member of the Sinclair family is to join the board. Dr Andrew Williams, a grandson of company co-founder Frank Sinclair, will replace Alistair Sinclair, a son of Frank Sinclair, as a non-exec.

Dr Williams owns 1.4% of the company and is a member of the family’s 53%-stake concert party. As such, I don’t think it likely the new director will disrupt the board too much (I know there are significant family shareholders outside of the concert party that might behave differently).

* No further revaluation developments

MTVW’s interim figures from last year revealed the group’s trading properties had a market value of £666m (with tenants in situ) versus a book value of £318m.

The group’s then chairman had suggested at the 2014 AGM that a revaluation would take place every year. However, comments at the last AGM have since scotched such plans on the basis of cost and benefits.

Valuation

These results showed trading investments of £331m which, if sold at the the average margin enjoyed during the last ten years, would be worth about £860m.

Taxing the gain at 20% and then adding on other investments of £28m and subtracting net debt of £50m, I arrive at a possible NAV of £732m or £188 a share. That compares to £180 a share I estimated in June and the £77 per share NAV reported by MTVW today on a historical-cost basis.

With the share price at £113, clearly there is still some upside possibilities here. But as before, the big unknown remains how long it will take MTVW to sell its existing properties to realise my potential £188 per share NAV.

Assuming the dividend remains at 275p per share, the yield is 2.4%

* Next update — Q3 update probably early February 2016, ex-div 18 February 2016, 200p dividend paid 29 March 2016

Maynard Paton

Disclosure: Maynard owns shares in Mountview Estates.

Mountview Estates (MTVW)

Additional comments:

http://www.stockopedia.com/content/mountview-strong-results-and-firmly-undervalued-113040/

I have posted some extra comments via the link above:

Maynard

Mountview Estates (MTVW)

Publication of 2015 interim report:

http://www.mountviewplc.co.uk/MountviewInterimReport2015.pdf

Some interesting additional figures from the full interim report:

We can now deduce the markup on the properties sold during the six months. £33,665k/ £11,535k = 192% profit. Not bad. Better than the 186% scored during the last full year, though below the record 245% recorded during 2008.

Also of note is the disclosure that the market valuation of the properties sold — based on the Allsop valuation undertaken last September — was £24,450k. The real market value was £33,665k or 37.7% greater.

The Allsop valuation indicated that MTVW’s then property estate was worth £666m with the tenants in situ. Going on this (albeit limited) data, the sites seem to be worth 37.7% more with the tenants gone.

So taking that £666m Allsop valuation figure, multiplying by 1.377 gives £917m. The difference between the then cost of the properties at Sept 2014 (£317m) and that potential real market value (£917m) is £600m, which taxed at 20% is £120m. So £917m less £120m tax less current £50m net debt plus £28m other investments gives a £776m asset value, which equals… £199/share.

These sums may not be truly accurate, because I have taken the property base as at Sept 2014, and other figures from Sept 2015, but the final result ought to be roughly right.

Maynard

Mountview Estates (MTVW):

Company cited within Crystal Amber half-year results:

There was a mention of MTVW today within Crystal Amber’s half-year statement:

http://www.investegate.co.uk/crystal-amber-fund-limited–crs-/prn/half-yearly-report/20160315070000PD94F/

“The Fund welcomes and supports Grainger’s actions to streamline the business and cut costs; however we remain concerned both with the pace and scope of cost cutting. We note that last year Grainger, with a £900 million market capitalisation, incurred administrative costs of £42 million. Mountview Estates, a company in the same sector with a market capitalisation of £450 million, incurred administrative costs of £5 million. Neither is the Fund convinced of the merits of investing £850 million into the private rental sector rather than reducing debt, particularly at the time of global financial uncertainty for asset classes.

We continue to believe that further significant value can be realised through either a spin-off of the regulated tenancies division or a sale of Grainger.”

Crystal is an activist fund and does not seem entirely happy with progress at Grainger. Interesting that Crystal wants Grainger to spin-off its regulated properties — such a transaction might provide a good value benchmark for assessing MTVW.

Maynard

Mountview Estates:

Higher stamp duty (SDLT) payments following 2016 Budget:

https://www.gov.uk/government/publications/stamp-duty-land-tax-higher-rates-for-purchases-of-additional-residential-properties

I think MTVW will have to pay the extra SDLT.

From that document’s Q&A at the end:

“Q24: Will a company be subject to the higher rates of SDLT?

A24: A company purchasing a residential property will be subject to the higher rate of SDLT, even if the property will be its only residential property. There are no special exemptions from the higher rates of SDLT for companies. However, the higher rate of SDLT will not apply in circumstances where the company is subject to the 15% rate of SDLT.”

The financial effect of the extra SDLT won’t be felt in MTVW’s profits until the properties are sold in the years ahead. In the meantime, perhaps there will be less competition buying regulated tenancies and so prices may become more favourable for buyers.

And I see at least our MTVW shareholding won’t count in deciding whether we are buying a second home:

“Q26: I have a share in a limited company which owns a property for rental to tenants. I am purchasing another property which I will own direct. I do not own any other residential property. Will I have to pay the higher rates apply?

A26: No, shareholdings in a company that owns residential property will not be counted when determining if an individual is purchasing an additional residential property, although the company may be liable to the higher rates if it purchases residential property. As this is your first purchase of a residential property the higher rates will not apply.”

All of this has prompted me to revisit the annual report and confirm the accounting treatment for MTVW’s trading properties. Here is the relevant text:

“(k) Inventories – trading properties

These comprise residential properties all of which are held for resale, and are shown in the financial statements at the lower of cost and estimated net realisable value. Cost includes legal fees and commission charges incurred during acquisition together with improvement costs. Net realisable value is the net sale proceeds which the Group expects on sale of a property in its current condition with vacant possession. Where residential properties are sold tenanted, net realised value is the current market value net of associated selling costs. There were no such sales during the financial year. The analysis of the Group revenue as at 31 March 2015 is on page 36.”

It is not 100% clear, but “cost includes legal fees and commission charges” suggests that the books carry the trading properties with SDLT included in their book-value cost (i.e SDLT is not charged to the P&L during the year of purchase).

Net realisable value of the trading properties is based on vacant possession, which should always be higher than cost.

So as I see it, the existing NAV will not be affected by the higher SDLT and the future NAV will simply have future purchased properties valued at cost with the higher SDLT included.

As such, the effect of paying higher SDLT will be felt — in cash terms — from when the higher bands are introduced…

…but in terms of MTVW’s accounting profits, will only have an effect in the P&L when the property is sold in the years ahead (the effect will be a lower gross margin to reflect the higher original SDLT cost).

Agreed, I don’t see the higher SDLT as having a more long-term effect. A lot of other events will happen between the time MTVW starts paying the higher SDLT and when it starts selling those same properties.

Maynard