16 June 2015

By Maynard Paton

Quick update on Record (REC).

Event: Final results published 16 June

Summary: Satisfactory results, with a positive outlook and a 10% dividend lift supporting my belief that REC’s recovery is gathering pace. However, news of a 10% company-wide salary hike for staff was not so pleasing, and my earnings guess for 2016 has been trimmed accordingly. Nevertheless, the accounts remain impressive and the valuation looks lowly, and I have bought more shares today.

Price: 37p

Shares in issue: 221,380,800

Market capitalisation: £81.9m

Click here for my previous REC posts.

Results:

My thoughts:

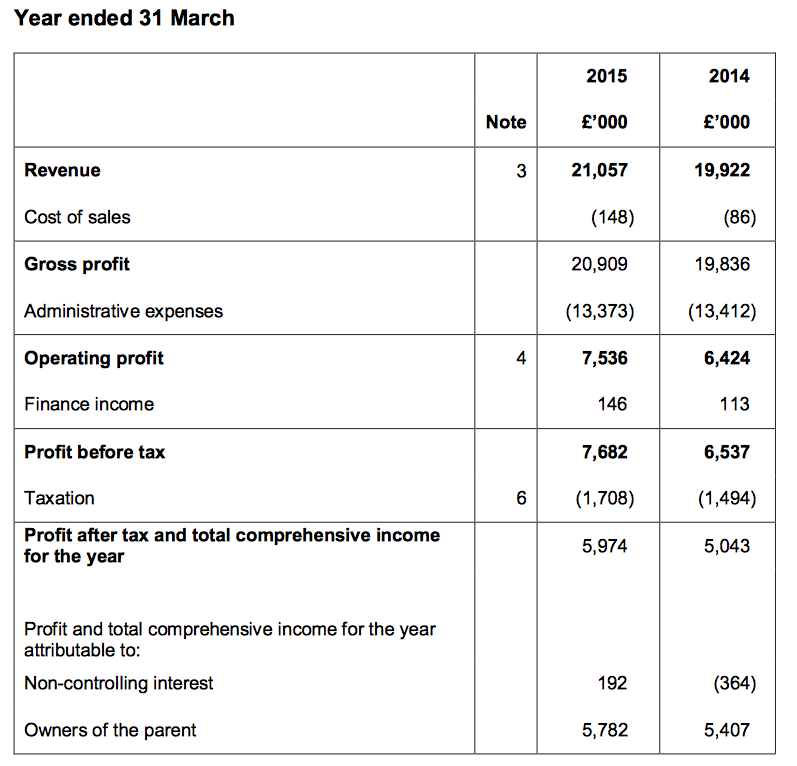

* These results were quite satisfactory

REC’s revenue and profit advances had already been indirectly flagged through the group’s quarterly updates — a statement in April revealed effective client assets under management (AUMe) had grown 7% to $55.4bn during the year.

REC described these results as the “second successive year of growth” and certainly the splits between the two halves now show consistent progress following the group’s difficulties post-banking crash:

| H1 2014 | H2 2014 | FY 2014 | H1 2015 | H2 2015 | FY 2015 | ||

| Revenue (£k) | 9.872 | 10,050 | 19,922 | 10,058 | 10,999 | 21,057 | |

| Operating profit (£k) | 3,003 | 3,421 | 6,424 | 3,497 | 4,039 | 7,536 |

* Comprehensive management commentary and full accounting notes

Top marks for REC for publishing what is almost a complete annual report as its final-results announcement.

Few companies provide such comprehensive detail in their RNS statements — especially among companies valued at about £80m — and the lengthy disclosure does give a positive impression of REC’s management, transparency and financial controls.

* ‘High level of engagement with potential clients’

I was pleased REC could issue a positive view on its near-term prospects (my bold):

“With divergence in monetary policies and geopolitical and economic uncertainty seemingly set to continue for the foreseeable future, contributing to renewed and sometimes heightened volatility in currency markets, we would expect the increased focus on currency-related issues to be maintained.

“This view is reinforced by the current high level of engagement with potential clients and investment consultants across a broad range of currency issues. The pace and extent to which this engagement translates into new business opportunities is necessarily uncertain.”

“However, the Group is well placed to take advantage of such opportunities as they arise by servicing clients’ needs to the highest possible standards and in doing so generating long-term sustainable growth for shareholders.”

* A pleasant surprise to see the dividend up

The best news for me was a lift to the dividend. The final payout has been raised 20% to 0.9p to take the annual dividend up 10% to 1.65p per share.

REC’s payout had previously been stuck at 1.5p per share for the last three years and I’d like to think the uplift underpins REC’s upbeat outlook.

* I did not expect all the staff to receive a 10% pay increase

Something I did not expect was REC to give all of its staff a 10% pay increase. The group said (my bold):

“The trend towards higher fixed remuneration in financial services in general and banking in particular is something that the Group has had to recognise. We have chosen to do so in a way that reflects the contribution of every part of the firm to our clients’ outcomes, by a one-off firm-wide salary increase of 10%, with effect from 1 May 2015, outside the normal salary review round.”

There was no word on whether REC’s employee bonus scheme — where staff share 30% of pre-bonus profits — would be reduced to offset the extra cost. I suspect it won’t.

* Accounts still showcase super financials

In particular, these results showed full-year operating margins at a robust 36% and return on average equity (prior to any net cash adjustments) at a healthy 20%.

Cash flow was wonderful yet again, with a minimal amount absorbed into working capital and little spent on fixed assets. It all meant year-end net cash and investments could advance £3m to almost £29m.

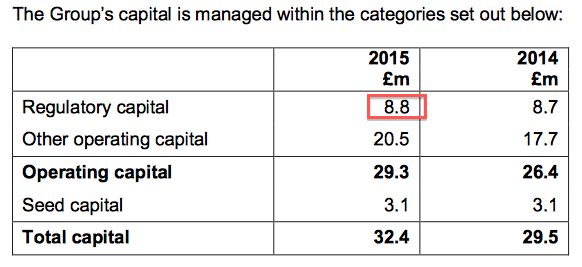

* Regulatory capital disclosed at almost £9m

I believe these results were the first to disclose exactly the cash REC needs on hand to satisfy its regulatory requirements:

In effect, this £8.8m sum is part and parcel of the underlying business and should not be deemed as ‘surplus’ cash.

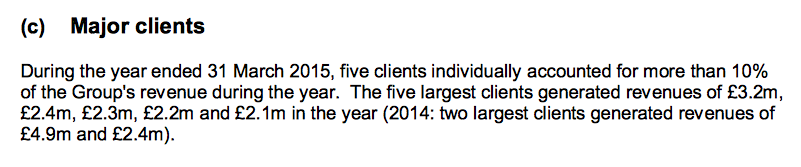

* Still dependent on a handful of large clients

I see REC’s spread of large clients has become a little more even:

These results revealed the group’s largest client represented 15% of revenue — the lowest proportion since the figure was disclosed in 2010.

REC’s results presentation revealed the top ten clients represented 76% of revenue (£16.1m), the lowest proportion since 2011.

* ‘Tactical bespoke mandate’ still invested

Probably the most significant development to emerge from REC this year was news of a “tactical bespoke mandate” that brought in an extra $1.75b of client money during March.

The mandate was significant because it involved REC’s Currency for Return product, which has generally floundered since the banking crash and but may now be seeing greater client interest. What’s more, this product earns lucrative management fees.

Anyway, these results confirmed the tactical mandate in question “remains substantially unchanged” and that “part of [it] may… only be temporary”.

In the past I have wondered whether to allow for the temporary nature of this mandate. But I have since concluded there is no real point, since all of REC’s clients can withdraw their money at very little notice — and quite a few have done so in the past!

So from now on, my valuation sums will include this tactical mandate in its entirety.

Valuation

Here are my calculations.

First, I’ve derived potential USD management fees from the AUMe figures and fee rates within these results. I’ve then converted the USD fees into GBP at £1:$1.56.

| Year to 31 March 2016 (est) | AUMe ($bn) | Fee Rate | Management fee (£k) |

| Dynamic Hedging | 9.2 | 0.15% | 8,846 |

| Passive Hedging | 41.2 | 0.03% | 7,923 |

| Currency for Return | 4.8 | 0.16% | 4,923 |

| TOTAL | 21,692 |

Next, I’ve added 10% to the staff cost and subtracted that, other operating costs, and the 30% bonus pool, to arrive at an operating profit:

| Year to 31 March 2016 (est) | |

| Management fees (£k) | 21,692 |

| Less staff costs (£k) | (6,600) |

| Less other costs (£k) | (4,200) |

| Less 30% profit share (£k) | (3,268) |

| Operating and pre-tax profit (£k) | 7,625 |

After standard 20% tax, my sums suggest earnings could be 2.76p per share.

REC’s market cap at 37p is £82m. Adjusting that for net cash and investments of £29m and the regulatory capital requirements of £8.8m, I make REC’s enterprise value (EV) to be £62m or 28p per share.

Then dividing my EV by my 2.76p per share earnings guess, the P/E for the underlying business comes to 10.

Meanwhile, the trailing 1.65p per share dividend supports a 4.5% income.

* I have decided to buy more

There are few shares around in this market that offer super margins, generous cash flow, veteran management, hefty insider ownership, an asset-rich balance sheet, recovering profits and growing signs of further operational advances — all for a possible P/E of 10. At least that is what I feel you get with REC.

True, there are risks. Major clients and mandates may disappear, and all the talk of greater engagement with new customers may come to nothing. Nonetheless, I have taken the plunge and increased my REC holding by 14% today, buying at 37.1p including all costs. My average entry price is now 25.5p per share, including all costs.

* Next update — a Q1 statement on 17 July.

Maynard Paton

Disclosure: Maynard owns shares in Record.

Record’s 2015 Annual Report now published and available:

http://ir.recordcm.com/files/13/report/webPDF_Record_AR15%20-4.pdf

The report did not include that much extra information, as the original RNS results statement contained a comprehensive management narrative as well as the full accounting notes. The extra details reserved for the annual report concerned corporate governance etc.

Here is what I found that was worth noting:

1) Founder Neil Record has become a non-executive

I am quite sure there has never been an RNS to announce Neil Record stepping down from his executive duties to become a non-exec.

But the 2015 annual report confirms he is now a non-exec:

Last year’s annual report had simply referred to Mr Record as chairman, and seemed careful in not defining him as either a non-executive or an executive. The 2013 annual report (and those before) had him down as an executive.

But I see the City presentation accompanying these 2015 results still shows Mr Record as an executive:

2) Board pay up by 3%…and a further 10% for next year

The execs received a 3% pay rise during 2015, which I suppose is acceptable given us shareholders will see our (dividend) income rise 10%:

(I also see Mr Record received a cheeky £9k in lieu of a pension payment, even though he is now a non-exec).

As noted in the original Blog post above, REC has given all of its staff a 10% pay rise for 2016… and the executives (and non-execs) will enjoy the same pay hike as well:

I have to add that while director wages have indeed been “little altered” over the last seven years, the same cannot be said for profits. Pre-tax profits were £40m in 2008 — now they are less than £8m.

Anyway, here are the new salaries and fees:

3) Meeting numbers and attendees

I always like to double-check the stats on board meetings:

With REC, I see 2015 was the 6th consecutive year the board held more remuneration meetings than ordinary and audit meetings. To be fair, I guess a lot of the discussion covers the pay of the workforce (and the group bonus pool structure) rather than the wages of the execs. Nonetheless, clearly the managers love to talk about pay and they are not badly remunerated as well.

Also, non-exec David Morrison missed two meetings last year. Now that in itself is not a major warning sign, but for the last five years now Mr Morrison has missed at least two meetings a year. The independent non-execs number 3 out of 8 board members, and a ‘part-time’ non-exec isn’t going to help the board’s balance.

Maynard

Q1 update published today:

http://ir.recordcm.com/regulatory-news-item.asp?newsid=2068689

A very steady update, with effective client money under management (AUMe) up 2% to $56.6bn during the 3 months to June 2015:

There was nothing else of major significance contained within the statement, although REC did mention “a new mandate with six underlying clients” was signed in the quarter and is expect to be funded in the current quarter.

Although new client mandates generally remain elusive, the wider outlook still appears positive (my bold):

I’m also hopeful that talk this morning of the Bank of England perhaps lifting rates next year could encourage further product interest.

Feeding today’s Q1 AUMe numbers into my valuation sums, I arrive at potential annual management fees of £21,924k. Less the same costs referred to in the original Blog post above, and less the 30% bonus pool, my figures point to a possible operating profit of £7,786k. Less 20% tax gives me earnings of 2.81p per share.

Using the same EV and surplus cash numbers as applied in the Blog post above, the P/E for the underlying business remains at 10 with share price at 37p. The trailing dividend yield remains 4.5%.

As I wrote in the Blog post above, I continue to feel there are few shares around that, similar to REC, offer super margins, generous cash flow, veteran management, hefty insider ownership, an asset-rich balance sheet, recovering profits and growing signs of further operational advances — all on a possible P/E of 10.

***STOP PRESS*** 11:33am

I have decided to take the plunge once again and further increase my REC holding. Including all costs, I have bought at 36.9p and increased my holding by 18% today. My average entry price is now 27.2p per share, including all costs.

Maynard