06 May 2015

By Maynard Paton

Quick update on Andrews Sykes (ASY).

Event: Final results published 06 May

Summary: Results better than I had expected. A dismal first half was followed by a less dismal second half and the outlook for 2015 appears relatively promising. Accounts still showcase solid financials and I’m pleased ASY’s 90% owner continues to share the wealth through sizeable dividends. The yield is 7.9% at 300p. I continue to hold.

Price: 300p

Shares in issue: 42,262,082

Market capitalisation: £127m

Click here for my previous ASY posts.

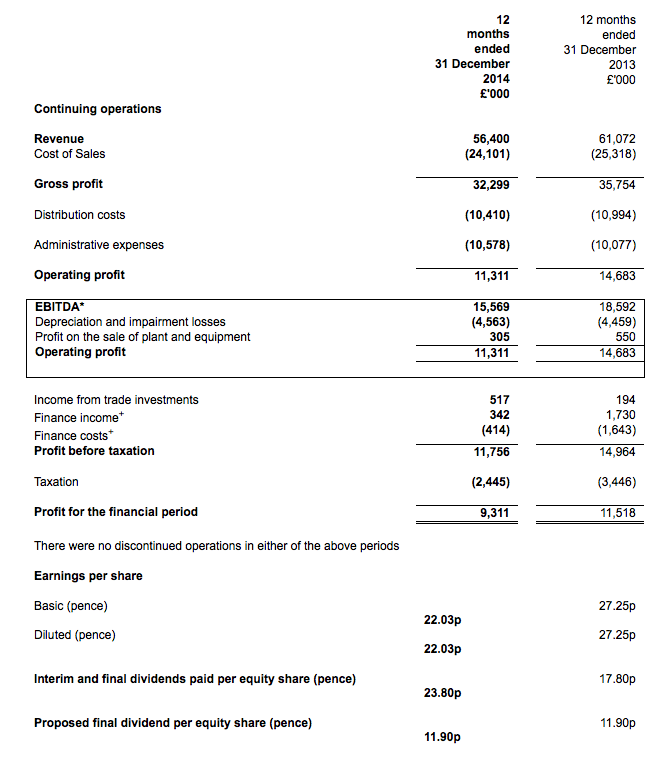

Results:

My thoughts:

* These results were better than I had expected

Issued in September, ASY’s interim figures had already revealed H1 profits down 32% — apparently, an “unseasonably mild winter” caused lower demand for the hire group’s portable heaters. The same statement also owned up to a “disappointing” third quarter.

So it was some relief to read ASY’s second half had not fared as badly as the first. Here is the split between the two halves:

| H1 2013 | H2 2013 | FY 2013 | H1 2014 | H2 2014 | FY 2014 | ||

| Revenue (£k) | 29,774 | 31,298 | 61,072 | 26,759 | 29,641 | 56,400 | |

| Operating profit (£k) | 6,427 | 8,256 | 14,683 | 4,349 | 6,962 | 11,311 |

H2 revenue slipped 5% to push H2 profits down by ‘only’ 16%. Today’s statement described the year as having witnessed “challenging trading conditions” — a term used by ASY for at least the last three years now.

Still, ASY did confirm last year’s “under-performance” had been “largely addressed” by the end of the fourth quarter — with trading having “nearly recovered” to the levels of 2013.

I was also reassured by the firm’s immediate outlook: “Consequently, we are now able to look forward to 2015 with a more optimistic outlook.”

* Accounts still showcase super financials

I was pleased a disappointing year did not translate into disappointing accounting measures.

For instance, full-year operating margins were a robust 20% while return on average equity was a decent 22%.

Cash flow appeared good, too, with capital expenditure covered by the depreciation charged against earnings. Year-end net cash looked healthy at almost £17m while the final-salary pension scheme continues to run at a £1m surplus.

The full 2014 annual report should be published by the end of next week and I will double-check ASY’s cash flow, including the firm’s working-capital movements and the level of any additional pension-scheme contributions.

I also need to look into ASY’s trade investments, which have a book value of just £164k but produced an income of £517k last year.

* Mr Murray blessed us with another dividend

The ‘idiosyncratic tycoon’ that owns 90% of ASY has rewarded his fellow shareholders with another dividend. As you may recall, ASY’s past dividends have been somewhat haphazard.

Anyway, a final 11.9p per share payout matches that declared at the half-year stage and gives 23.8p per share for the full year. The payout was not quite covered by earnings, which is why the shares at 300p yield 7.9%.

Valuation

These annual results showed operating profits (plus trade-investment income) of almost £12m, which translated into earnings of £9m or 22p per share.

Subtracting the £17m net cash position from the £127m market cap, I arrive at an enterprise value of £110m or 260p per share. Divide that 260p by the 22p per share earnings and the underlying P/E is 12.

But let’s assume ASY can recover from its woes of 2014. After all, profits last year were the lowest since 2005 and have in the past been £6m higher.

The average operating profit reported between 2004 and 2014 is almost £14m, which could convert into earnings of about 25p per share. On my 260p per share enterprise value, this alternative earnings figure supports a P/E of 10.

As I mentioned in my February ASY write-up, my initial 233p buy price equated to a P/E of 8…

And with ASY continuing to struggle to produce any longer-term sales and profit growth, I still believe I need to buy at a similar rating to make the most of the firm’s cash generation and dividends.

* Next update — probably interim results during late September.

Maynard Paton

Disclosure: Maynard owns shares in Andrews Sykes.

2014 annual report now published and available:

http://www.andrews-sykes.com/admin/imagegallery/files/pdfs/reports/Annual_Report_2014.pdf

The report includes a fair bit of text that was not contained in the original results RNS. I’ve picked out one or two little snippets of extra information. Plus I’ve scanned the accounting notes for anything of interest.

Here is what I found:

1) Quantifying the Q4 recovery

The results RNS claimed “…by the end of the fourth quarter, trading had nearly recovered to the previous year’s levels.”

In fact the Q4 performance was 0.5% shy of last year:

2) Swiss business becoming profitable

ASY’s Swiss business is probably very small, but it is pleasing to see it is no longer sapping money from the wider group:

3) Main UK/European business remains blessed with high margins

Even in a difficult year, it is good to see ASY’s main division continuing to earn robust margins. Operating margins were 23% before central costs:

4) 15 new employees

I’m surprised ASY took on 15 new employees during a year when revenue fell 8%. I am also surprised that figure included an extra 10 managers or administrators:

Anyway, at least 8 new sales and distribution people were taken on as well. Plus, the average cost of each employee dropped from £32,765 to £32,204.

5) Boss receives lower pay

I see ASY’s managing director received £23k less through his pay packet in 2014 than 2013:

I assume the difference is due to Mr Wood collecting less (if anything) in the way of a bonus during 2014 after profits fell so heavily. The numbers suggest to me that Mr Wood collects quite a high basic salary (£300k-plus?) and a relatively low bonus.

6) Trade investment looks like ‘hidden asset’

I mentioned in the above Blog post that ASY collected a £517k dividend from a trade investment that was in the books at £164k.

Here is the associated accounting note:

Looking through past annual reports, I see this trade investment has provided dividends totalling £1,703k during the last five years and £2,892k during the last ten years. Annual dividends received from this investment have ranged from zero to £980k.

Taking the average of about £300k, I guess this trade investment may really be worth £3m (7p per share) or so. But as the above accounting note states, ASY has no influence on dividend decisions with the business concerned and it might be a bit cavalier to suggest ASY could turn that investment into a (supposed) £3m anytime soon.

So I think for valuation purposes I will use the average £300k of past trade-investment income to work out the P/E etc. My sums in the Blog post above remain valid.

7) Pension contribution reduction

I welcome the news that ASY no longer needs to pay as much into its defined-benefit pension scheme. Contributions will drop from £900k-plus to £120k:

I am pleased the pension scheme continues to show a £1m surplus as the plan’s assets continue to produce a return that offsets the benefits paid and the ever-increasing actuarial liabilities.

8) Cash flow in full

I did say within the above Blog post that I would double-check ASY’s cash flow, including the firm’s working-capital movements and the level of any additional pension-scheme contributions.

Here’s what was missing from the original results RNS:

An extra £778k was pumped into the pension scheme over and above what was charged to headline earnings. However, that figure should reduce substantially during 2015 (and hopefully beyond) given the aforementioned accounting note that indicated a £120k contribution this year.

Meanwhile, working-capital movements looked acceptable, although the aggregate outflow of £1,569k was the largest since 2008. ASY has traditionally offered very strong working-capital management, so I am not unduly worried by what was still a respectable cash-generative year.

I couldn’t find anything else in the 2014 annual report that warranted any comment.

Maynard