4 February 2015

By Maynard Paton

You may have gathered by now that I do like my companies to have hefty insider ownership.

My theory is simple: I’m convinced directors are more likely to run their businesses successfully — and are therefore more likely to deliver satisfactory returns to outside investors such as you and me — if they boast significant shareholdings themselves.

I’m certainly hoping that’s going to be the case at Andrews Sykes (ASY), where the chairman and his family own 90% — yes 90%! — of the company.

Such shareholder dominance will of course mean this £127m hire business won’t be for everyone. Indeed, the tycoon in charge has adopted a very haphazard dividend policy and does not believe in standard boardroom governance. He is also very old at 94.

Nonetheless, a closer look ASY’s accounts reveals exactly why he wants to own so much of this company. Super margins, immense cash flow and lofty returns on capital in particular mark ASY out as a top-quality operator — and drew me in during May 2013 at an average of 233p.

So far at least, the threat of being ‘done over’ by a boardroom fiefdom has not emerged.

Instead, I have enjoyed a satisfactory return, with the shares rising to 300p — plus a sizeable 29.7p dividend for 2013 representing a lovely 12.7% income on my purchase price.

At A Glance

- Leading supplier of heating and air-conditioners for commercial hire

- High margins and generous cash flow offset lack of growth

- Dominant shareholder responsible for huge buyback plan and irregular dividend history

It started with a small depot in Wolverhampton

Andrews Sykes (ASY) was established during 1964 when John Andrews began importing portable heaters from America to sell in the UK.

It wasn’t long before Andrews Industrial Equipment started renting out the heaters and, by 1969, the firm was offering air-conditioners for hire to help generate business in the summer.

Mr Andrews sold up during the late 1980s and the new owners merged the business with Sykes Pumps —a prominent pump rental business.

These days, ASY claims to be the UK’s leading specialist hire group. As well as heaters, air-conditioning units and pumps, the business now supplies boilers, chillers, ventilation fans and dehumidifiers.

ASY reckons its longevity has been due to ensuring its customers — many of which are construction groups — are given only the “safest, most reliable equipment sourced from the world’s top manufacturers”, and making it all available for hire on a “24/7/365” basis. Depots outside the UK now represent 31% of sales.

ASY’s website has all the details, including this useful blog of customer case studies.

Sales and profits have been ‘range bound’ for a decade

The onset of the early 1990s recession thumped ASY and prompted a protracted boardroom battle, which eventually saw major shareholder Jacques Murray — the aforementioned idiosyncratic tycoon — gain control in 1994.

Fresh managers had turned losses into annual profits of £13m by 1998, although the decision that year to spend £50m on Cox Plant was a disaster.

Problems soon emerged at the acquired subsidiary and it was eventually sold for just £20m a few years later. Replacement managers were also appointed.

For the last ten years, ASY’s progress can be described as ‘range bound’. Sales have bobbed between £50m and £60m, while operating profits have come in anywhere between £11m and £18m. Thankfully there have been no more acquisitions!

The banking crash caused a few worries, with ASY taking on further borrowings in 2008 to pay a gigantic dividend (I’ll come back to that later). The shares traded as low as 68p during 2009, but have since recovered to 300p following some impressive cash generation and debt reduction.

I now look forward to freezing winters and scorching summers

This table summarises ASY’s progress during the last five years:

| Year to 31 December | 2009 | 2010 | 2011 | 2012 | 2013 |

| Sales (£k) | 54,358 | 55,951 | 53,838 | 58,380 | 61,072 |

| Operating profit (£k) | 12,937 | 13,942 | 11,882 | 14,221 | 14,683 |

| Finance income (£k) | (889) | (132) | (92) | (59) | 87 |

| Other items (£k) | 1,253 | 564 | 3,113 | 592 | 194 |

| Pre-tax profit (£k) | 13,291 | 14,374 | 14,903 | 14,754 | 14,964 |

| Earnings per share (p) | 26.3 | 24.2 | 27.1 | 26.4 | 27.3 |

| Dividend per share (p) | - | 11.1 | 6.6 | 7.1 | 29.7 |

Although 2013 did see sales and profits improve, they do remain below the £67m and £18m recorded during 2008.

Indeed, it is quite amusing to see that ASY has, since 2006, introduced itself as a “thriving business in a dynamic sector” within its annual reports. ASY may be thriving, but it is not exactly growing.

ASY’s annual reports have also referred regularly to the “unhelpful” weather. In fact, it always seems as if different parts of the business do well — and don’t do well! — each year.

Here’s an extract from the 2011 annual statement to show you what I mean:

“Our main hire and sales business in the UK and Northern Europe has faced challenging trading conditions throughout 2011 mainly as a result of unhelpful weather conditions but also due to the current economic conditions.”

“Trading in the first half remained flat and profit was adversely affected by the temperate weather at the end of the 2010/11 winter which resulted in an early end to the heating season. This was followed by another mild summer that failed to stimulate demand for our all important air conditioning products. Unlike last year, the start of the 2011/12 winter was also mild which did not allow our heating division to compensate for the under-performance of the air conditioning business. The last 18 months have also been unusually dry resulting in the drought conditions recently announced for some parts of the UK.”

Now here’s an extract from the 2012 annual statement (you’ll see the first sentence is copied from 2011!):

“Our main hire and sales business in the UK and Europe has again faced challenging trading conditions throughout 2012 mainly as a result of unhelpful weather conditions but also due to the current economic conditions.”

“The weather at the start of the year was mild but that was soon replaced by the arrival of a cold spell of weather in February and March which stimulated the demand for our heating products. The summer was one of the wettest on record which did not stimulate demand for our air conditioning business. However, it did help our UK pumping business which saw turnover return to a more normal level.”

And here’s an extract from the 2013 annual statement (oh look, the first sentence is copied from 2012!)

“Our main hire and sales business in the UK and Europe has again faced challenging trading conditions throughout 2013 mainly as a result of some unhelpful weather conditions but also due to economic conditions…”

“The weather at the beginning of the year was relatively cold thereby helping the performance of our heating division. However, this was short lived and was replaced by much milder conditions which lasted until the middle of June when a spell of warmer weather finally arrived giving a boost to our all-important air conditioning hire and sales business. The autumn and winter that followed were exceptionally mild and wet which did nothing for our heating products but which did assist the performance of our UK pumping business.”

So what ASY needs for a bumper year is:

- A freezing cold winter (to prompt demand for heaters);

- A blisteringly hot summer (to prompt demand for air conditioners), and;

- Torrents of rain during the rest of the year (to prompt demand for pumps).

That combination sadly did not occur during 2014.

Half-year results issued in September revealed sales down 10% and profits down 32% — apparently, an “unseasonably mild winter” caused lower demand for portable heaters.

ASY also admitted it had experienced a “disappointing” third quarter and the shares slumped from 385p to 275p on the day.

War hero turned self-made multi-millionaire

I think it is fair to say ASY chairman Jacques Murray is not your typical company director. For a start, he served in the Second World War.

Born in Paris in 1920, Mr Murray escaped to the UK in 1940 and joined the RAF, where I gather he flew on 38 missions as a navigator. He was awarded the French Legion of Honour and later became a British national.

Having then built a fortune from fire extinguishers — he owns 99%(!) of fire-extinguisher firm London Security (LSC) — Mr Murray took on Andrews Sykes at the ripe old age of 74… and this year turns 95.

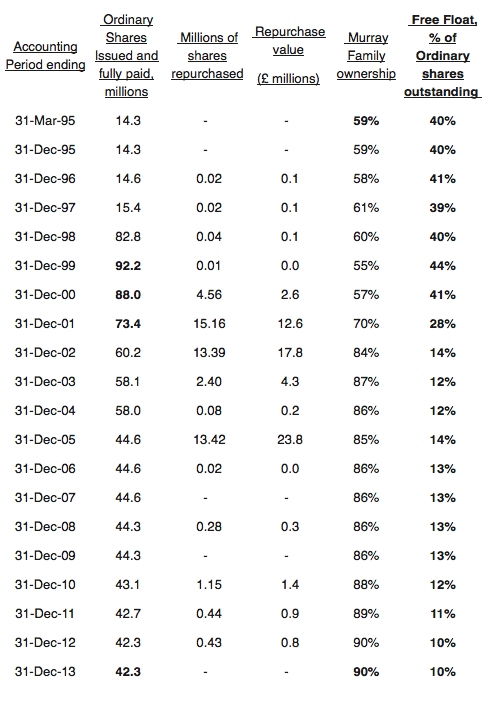

Mr Murray’s 90%/£114m family shareholding in ASY is the result of an astonishing level of share buybacks. This article at valueinvestorclub.com contains a very informative table:

Since 2000, ASY’s share count has fallen 55% to 42 million and I calculate the average price per share bought back was about 126p. That does not seem a bad investment with the shares now at 300p.

Mr Murray does not oversee day-to-day management of ASY — he leaves all that to managing director Paul Wood. Mr Wood was appointed to his current role in 2006 and is the only executive on the board.

The non-execs include Mr Murray’s two sons, both of whom are in their 40s and who look set to inherit their father’s business interests. The family holds substantial investments in various European and Miami hotels (reputedly worth £300m-plus) alongside its £286m LSC shareholding.

ASY’s other non-execs are all long-time associates or employees of the Murray family, which underlines — as if you didn’t know already — who exactly is in charge here. It’s no surprise to me that ASY’s annual reports do not include any reference to corporate governance.

Nonetheless, Mr Murray and co are not milking ASY dry with fat-cat salaries.

Mr Murray himself does not take a wage and the non-execs do not receive extravagant fees. There are no options in place either. True, Mr Wood’s take-home pay has jumped considerably during the last two years, but overall the board appears good value to me.

It is ASY’s accounts that really underpin this investment

I’m certainly impressed with ASY’s cash flow:

| Year to 31 December | 2009 | 2010 | 2011 | 2012 | 2013 |

| Operating profit (£k) | 12,937 | 13,942 | 11,882 | 14,221 | 14,683 |

| Depreciation and amortisation (£k) | 4,964 | 4,239 | 3,911 | 4,006 | 4,459 |

| Cash capital expenditure (£k) | (1,661) | (1,745) | (6,582) | (4,715) | (4,392) |

| Working-capital movement (£k) | 2,213 | 162 | 499 | (474) | (82) |

| Increase to net cash (£k) | 14,120 | 7,713 | 5,460 | 5,277 | 3,471 |

| Net cash/(debt) (£k) | (2,808) | 4,905 | 10,365 | 15,642 | 19,133 |

In particular, the depreciation charged against earnings has more than covered ASY’s actual cash expenditure on tangible assets. Such accounting is very welcome at this asset-based business, and gives the notion of conservative financial controls.

Cash movements within working capital also look favourable.

Overall, ASY’s cash generation added a huge £36m to its coffers between 2009 and 2013, and transformed a substantial net debt position into an attractive net cash situation. (September’s interims revealed net cash was a healthy £15m, or 36p per share.)

ASY’s cash flow was large enough to pay dividends of £18m during the last five years, too.

Elsewhere on the balance sheet, there is a defined-benefit pension scheme that is presently showing a funding surplus.

Past accounts reveal ASY has pumped an extra £10m into the pension scheme since 2006 to shore up what was a niggling deficit. I’d like to think the current surplus means further special contributions won’t be needed.

I’m encouraged ASY’s ‘operational’ assets have consistently produced lucrative levels of profits for investors. During 2013 for example, average net assets (excluding net cash) of almost £24m generated after-tax profits of nearly £12m — a return of 46%. The same calculation has topped 40% for the previous five years.

ASY’s operating margins suggest the firm enjoys a commanding competitive position. Profits from group sales were an attractive 24% in 2013 and have in the past reached 26%. Margins at the main UK and Europe division have in fact surpassed 27% since 2008.

A P/E of 16 or a P/E of less than 11?

ASY is not an obvious bargain if you look only at September’s interims.

Doubling up those first-half results gives an operating profit of £9m and earnings of close to £7m or 16p per share.

Subtract the £15m net cash position from the £127m market cap and we have an enterprise value of £112m or 264p per share. Divide that 264p by my 16p per share earnings guess and the underlying P/E is 16.

That rating does not look cheap, but let’s assume 2014 is a one-off bad year. After all, ASY’s performance throughout the previous ten years was ‘range bound’.

The average operating profit reported between 2004 and 2013 was almost £14m, which could convert into earnings of about 25p per share.

On my 264p per share enterprise value, this alternative earnings guess supports a P/E of less than 11.

For what it’s worth, I recall my 233p buy price equated to a P/E of 8.

I think with sales and profit growth hard to come by at ASY, I would need to buy at a similar rating again to make the most of the firm’s super cash generation and dividends…

Assuming any dividends are paid, that is…

Mr Murray seems to pay himself (and me) a dividend whenever he fancies.

Let’s look at my first table again:

| Year to 31 December | 2009 | 2010 | 2011 | 2012 | 2013 |

| Sales (£k) | 54,358 | 55,951 | 53,838 | 58,380 | 61,072 |

| Operating profit (£k) | 12,937 | 13,942 | 11,882 | 14,221 | 14,683 |

| Finance income (£k) | (889) | (132) | (92) | (59) | 87 |

| Other items (£k) | 1,253 | 564 | 3,113 | 592 | 194 |

| Pre-tax profit (£k) | 13,291 | 14,374 | 14,903 | 14,754 | 14,964 |

| Earnings per share (p) | 26.3 | 24.2 | 27.1 | 26.4 | 27.3 |

| Dividend per share (p) | - | 11.1 | 6.6 | 7.1 | 29.7 |

You will see recent dividends have been up and down, and earlier payments are no more straightforward. A token 3p was declared in 2003, 15p was paid in 2004, then there was nothing in 2005, 2006 and 2007, and then a gigantic 33.6p was distributed in 2008.

The 2008 payout was notable, not least because a similar-sized (£15m) payout was declared at exactly the same time at LSC.

I have read on bulletin boards that Mr Murray ploughed the £30m he received into his hotel investments… which gives the impression he views ASY (and perhaps LSC) as a bit of a ‘cash cow’.

The timing of the 2008 payout was unfortunate, as it did increase ASY’s net debt just as the banking crash was unfolding. So a risk to holding ASY is that Mr Murray continues to expand his hotel empire and once again orders ASY to borrow large sums to pay him (and me) enormous dividends.

Another major danger here is a de-listing

Mr Murray could easily take ASY private. I might then be stuck with a derisory take-out offer or — even worse — have to panic-sell at a distressed price to avoid holding an unquoted share.

That said, Mr Murray has played fair with his dominant shareholding for the last ten-plus years and I suppose if he was ever going to take ASY private, he would have done so at 68p during the banking crash.

I cannot know for sure, but my research into other family-dominated firms suggests a stock-market quotation offers ASY:

- Greater transparency and reassurance for customers and suppliers;

- Operational benefits and greater financial discipline from the additional reporting;

- The opportunity for smaller family shareholders to dispose of their investments, and;

- The ability to raise funds through further share issues or to motivate staff with share options (although many family firms I have come across do neither!)

I trust one of those reasons will keep ASY on the stock market for some time to come.

And let’s not forget Mr Murray is 94… and will not be around forever. What his sons do when they take charge is anyone’s guess.

I’d like to think Murray Senior has already handed down his business acumen to his boys, but you never can tell with family. They may order a de-listing or gear the business up for lavish dividends themselves.

I hope he’s still declaring dividends at 100

As I say, I’m convinced directors are more likely to deliver satisfactory returns to outside investors if they boast significant shareholdings themselves. And there is no doubt Mr Murray boasts a significant ASY shareholding!

So far I have enjoyed a satisfactory gain with ASY. The business continues to generate wonderful returns on capital and superb cash flows, the latter having funded a sizeable dividend for me with the excess piling up nicely on the balance sheet.

Thinking back, I made sure I bought ASY on a lowish P/E multiple because the track record did not indicate dramatic sales and profit growth during the years ahead.

I guess September’s disappointing interims are proof of the seasonal ups and downs this business can face. Nevertheless, I am sure the “unhelpful” weather will even out over time. (Roll on a summer heatwave and some panic hiring of air conditioners!)

In the meantime, I hope ASY’s cash position is now of a size that can allow the group’s future profits to be mostly (if not entirely) distributed through comfortable dividends…

…and that the idiosyncratic Mr Murray can keep declaring the payouts until he reaches at least 100!

Until next time, I wish you happy and profitable investing!

Maynard Paton

Disclosure: Maynard owns shares in Andrews Sykes.

Some useful links for anyone interested:

http://boards.fool.co.uk/andrew-sykes-asy-building-a-picture-10813221.aspx?sort=whole

http://www.valueinvestorsclub.com/idea/Andrews_Sykes_Group_PLC/113115

http://www.growthcompany.co.uk/features/4475/andrew-fitton.thtml

http://www.birminghampost.co.uk/business/manufacturing/rich-list-2015-no3—8479568

http://uk.advfn.com/cmn/fbb/thread.php3?id=11502813 (post 961)

https://www.miamihotelgrandbeach.com/miami-beach-hotel-development-team

Thanks for this excellent and entertaining article on Andrews Sykes in which I also own shares. As you correctly suggest, the main danger seems to be if the majority owners decide to take the company private without providing other shareholders with reasonable recompense. However, in this event I think I am correct in saying that you would have the option of remaining a shareholder in the private company. It has been my experience as a shareholder with a couple of other formerly listed companies (ANS and Industrial Control Services) that when they were taken private they did rather well so, if you can take a really long view, going private is not necessarily a disaster. Of course, Sykes is a completely different kettle of fish but I think it may well continue to prosper as a private company with lower administrative costs, although I would much prefer if it stayed public!

Hello John

Thanks for the comment. Yes, my limited experience of public companies going private is the same as yours. I used to own Dealogic shares and I agreed to the tender offer when it went private a few years ago, although I had the option of staying in. Then I heard this year it was acquired by another firm at 4x the tender price. Oh well.

Maynard