02 April 2015

By Maynard Paton

Today I’m continuing my hunt for Watch List shares with a look at Zytronic (ZYT).

Here are the initial attractions that prompted this research:

Appealing financials: Accounts showcase 15%-plus margins and an asset-rich balance sheet

Rising dividend: Payout has advanced 5-fold between 2005 and 2014

Interesting valuation: The shares could offer a possible P/E of 11

As usual, I’m applying a question-and-answer template to help me pinpoint companies that match the criteria set out in How I Invest. I’m looking for as many Yes answers as possible.

Activity: Designer and manufacturer of industrial ‘touch screens’

Website: www.zytronicplc.com

Share price: 270p

Shares in issue: 15,263,468

Market capitalisation: £41.2m

Does the business boast a respectable track record?

Yes.

ZYT has been designing and manufacturing specialised composite glasses and plastics for electronic display units since the mid-1980s. Recent years have seen the group develop heavy-duty touch screens for cash machines, gaming units and industrial equipment.

ZYT floated during 2000, when revenues were £4.5m, operating profits were £0.5m and the dividend was 1p per share. By 2014, revenues had reached almost £19m, operating profits had topped £3m while the dividend had advanced to 10p per share.

The growth rate, however, has moderated over time:

| 5 years to 2014 | 10 years to 2014 | 15 years to 2014 | |

| Sales CAGR | 3.5% | 8.0% | 11.1% |

| Operating profit CAGR | 6.6% | 24.3% | 13.0% |

| Dividend per share CAGR | 14.9% | 19.6%* | 17.9%** |

(*9 years to 2014; **14 years to 2014)

ZYT has suffered three setbacks as a quoted company.

The dotcom crash triggered losses during 2002 and 2003 and a two-year disappearance of the dividend. Profits then fell during 2007 as two significant customers held back orders, while profits dropped again during 2013 following a “general absence” of large one-off projects.

At least the dividend has made steady progress during the last five years:

| Year to 30 September | 2010 | 2011 | 2012 | 2013 | 2014 |

| Sales (£k) | 18,483 | 20,488 | 20,424 | 17,282 | 18,886 |

| Operating profit (£k) | 2,925 | 3,481 | 4,084 | 2,253 | 3,263 |

| Other operating income (£k) | 112 | 187 | 187 | 94 | - |

| Exceptional items (£k) | - | - | - | (413) | - |

| Finance income (£k) | (113) | (111) | (76) | 5 | (2) |

| Pre-tax profit (£k) | 2,924 | 3,557 | 4,195 | 1,939 | 3,261 |

| Earnings per share (p) | 14.9 | 18.3 | 22.2 | 11.1 | 19.6 |

| Dividend per share (p) | 7.0 | 7.7 | 8.5 | 9.1 | 10 |

In fact, the payout is up five-fold from the reinstated 2p declared during 2005 — and was never cut during the banking crash. The £413k write-off reported for 2013 is the only exceptional item recorded during the last ten years.

Has the business grown mostly without acquisition?

Yes.

ZYT purchased the assets of a business back in 2000 and has not acquired anything since.

Has the business mostly self-funded its growth?

Yes.

The latest balance sheet displays share capital of £7m versus earnings retained by the business of £11m. In addition, the share count has expanded by just 6% since 2001.

Does the business possess an asset-strong balance sheet?

Yes.

At the last count, cash was £7.8m while debt was £1.5m and other financial liabilities were £0.2m.

A bonus is land and freehold assets of £2.9m. There are no defined-benefit pension obligations.

Does the business convert profits into free cash?

Yes.

| Year to 30 September | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (£k) | 2,925 | 3,481 | 4,084 | 2,253 | 3,263 |

| Depreciation and amortisation (£k) | 987 | 1,157 | 1,039 | 1,075 | 1,034 |

| Net capital expenditure (£k) | (868) | (822) | (968) | (712) | (585) |

| Working-capital movement (£k) | (162) | (116) | (537) | 919 | 115 |

The last five years have seen cash capital expenditure covered entirely by the depreciation and amortisation charged against reported profits. Aggregate working-capital movements have witnessed a favourable inflow of cash over the same period, too.

Does the business enjoy a competitive advantage?

Possibly.

ZYT refers to “patented technology” within its 2014 annual report (my bold):

“The Group’s competitive advantages are based upon both the patented technology relating to the operation of the touch sensors and the lamination techniques and processes… which are a feature of all the Group’s products.

These advantages allow the Group to produce products that have optical clarity and ruggedness and can be customised to include individual features for customers, including privacy filters and anti-reflective and anti-glare properties. In the case of touch sensors, these advantages also result in the significant ability for them to be used by bare fingers and gloved hands and result in their not experiencing positional drift and therefore not requiring periodic re-calibration.

The growth of the Group and its future prospects come from the exploitation of this relatively new touch sensor technology. Our focus on the development of this patented technology has resulted in both the continual improvement to the operation and functionality of the touch sensors and the expansion of the range of different glass-based products available.”

Furthermore, the 2014 annual report outlines why ZYT’s products are different to those of its rivals:

“Unlike the majority of other touch technologies, the active component of Zytronic’s technology is embedded behind the glass front for protection, providing a true safety laminated, pure-glass fronted construction.”

The group has also developed multi-touch screens, which are capable of detecting up to 40 independent ‘touch points’. The associated patents are in the pipeline:

“We still continue to await the outcome of the initial MPCT development UK patent applications made in May 2012, but have progressed to the next stages of international patent application, having moved forward with the international national phase applications for three of the key patents for Europe, USA and China.”

All that said, the 2014 annual report does contain this small-print that suggests some of ZYT’s patents are actually owned by a third-party (my bold):

“(v) Royalty payments

Under the terms of its patent licence, Zytronic Displays Limited pays royalties to the patent owner on the value of the touch sensors that it sells. An agreed annual payment is made by monthly instalment under the licence…

Management reviews its forecasts of future sales to determine whether any impairment has occurred which might affect the carrying value of the prepayment.

From 1 January 2008, and for each subsequent calendar year, the annual payment will increase either by the greater of RPI or to the level of the previous year’s actual royalties.”

Such third-party ownership is quite disappointing — it suggests ZYT’s fortunes are not entirely in its own hands.

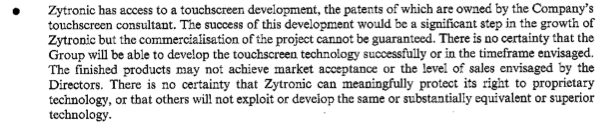

So I’ve done a big of digging and discovered this extract from ZYT’s flotation document, which refers to a “touchscreen consultant” owning some patents:

And here is an extract from ZYT’s 2004 results:

“Intellectual property

In June of this year, an agreement was completed which extends until 2014 Zytronic’s rights to the Intellectual Property relating to its touchscreen technology. This agreement has also given Zytronic the rights to manufacture the electronic controlling device for the touchscreen, which will further improve margins as the Group moves forward.”

I do not know how operationally significant this agreement was, or whether it remains that important today (or indeed remains in force). But these third-party patents are something prospective investors ought to bear in mind and do require further investigation.

Anyway, even with the royalty payments, ZYT has still managed to enjoy respectable margins — operating margins averaged 16.7% between 2010 and 2014 and hit 20% in 2012. Such levels of profitability are quite impressive as I understand ZYTs customers include a few large and powerful (and possibly hard-pressed) banks.

I should add that ZYT’s top three customers have represented at least 40% of annual revenues since 2009 and provided 43% of the top-line during 2014. So any cutbacks at those clients could hurt profits — as was witnessed during 2007 and 2013.

Does the business produce a respectable return on equity?

Sometimes.

Return on average equity for 2014 was £3m/£17m =17%, although stripping out the net cash from the equity base gives a 2014 calculation of 24%.

However, the only other years the cash-adjusted figure has topped 20% are 2011 and 2012 — most other years have seen the number at a so-so sub-15%.

Does the business employ capable executives?

I think so.

Chief executive Mark Cambridge has served in senior management roles since 2000 and took the top job in 2008. ZYT’s financial history since his appointment has been steady but not spectacular. Mr Cambridge is 51, so succession plans are not an obvious requirement at present.

Does the business employ good-value-for money executives?

Yes.

Mr Cambridge received a £116k basic salary and £58k bonus during 2014 — which do not look excessive for a business making profits of £3m-plus. Mr Cambridge’s pay has risen at a modest 3% per annum since 2009.

Does the business employ owner-orientated executives?

No.

ZYT is certainly not blessed with substantial insider ownership. Mr Cambridge owns ordinary shares worth only £137k, while the entire board has £542k (a 1.3% stake) riding on the share price.

I also see Mr Cambridge boasts three times as many options as ordinary shares and that total staff options represent a sizeable 6% of the current share count.

Interestingly, the bulk of Mr Cambridge’s options will come good if, among other things, ZYT’s pre-tax profits surpass £4.5m during 2016. For comparison, pre-tax profits for 2014 were £3.3m.

Is Mr Cambridge’s £4.5m option target a reliable indicator of future profits? Possibly not — I note Mr Cambridge failed to enjoy any benefits from a previous option scheme, because ZYT’s earnings fell short of scheme’s minimum target every year between 2009 and 2013.

Does the business enjoy reasonable growth prospects?

Possibly.

The 2014 annual results issued in December sounded positive for 2015:

“Whilst we are only a couple of months into the new financial year the sales and order book are ahead of last year and our focus is on continuing to increase value for shareholders now and into the future.”

An AGM update in February then reiterated the optimism:

“The Board is pleased to announce that further to the outlook statement given in December, trading for the first four months of the current financial year continues to be ahead of the comparable period last year and in line with management’s expectations.”

I’d like to think longer-term demand for touch screens will be positive, as various devices and machines gravitate towards the technology.

Does the share price stand a good chance of becoming a bargain?

Possibly.

I’ve calculated ZYT’s enterprise value (EV) to be its £41m market cap (at 270p) less its net cash of £6m (40p per share) giving £35m (230p per share).

Assuming the current first half of 2015 can match the second half of 2014, then I reckon pre-tax profits could be running at £3.7m.

Applying tax at 16% — my best guess for ZYT’s tax rate following the group’s successful claim for R&D tax credits — I arrive at earnings of £3.1m or 20.4p per share.

The potential P/E on my EV and EPS calculations is therefore 230p/20.4p = 11.3. The 10p dividend supports a useful 3.7% income as well.

Those ratings do not look expensive to me.

Is it worth watching Zytronic?

I’m not sure.

Among the positives, ZYT offers a decent dividend record, appealing accounts, a loyal boss and an inexpensive valuation.

However, I just do not get the feeling ZYT can rank alongside my other Watch List shares — notably Goodwin and Latchways — in terms of financial track record, returns on shareholders’ equity and proven executive ability. The impressive features within ZYT’s accounts have occurred only since 2010, while Goodwin and Latchways have impressed for far longer.

One issue to investigate further is just how dependent ZYT is on third-party patents. I might be worried about nothing here, but I can’t recall ever finding a ‘quality’ company having to pay up for similar royalty agreements.

All told then, ZYT seems a good company — but unlike the ones already on my Watch List, I just don’t think I’d be salivating to load up on the shares if the price fell heavily. I confess this could be a mistake, but I simply feel more comfortable passing on ZYT for now.

In the meantime, I’ll see if I can dig a bit deeper into the group’s patent arrangements.

Maynard Paton

Disclosure: Maynard does not own shares in Zytronic.

Thank you for your interesting and informative appraisal of Zytronic. As a holder I do hope you will follow up with a note of your further digging into the group’s patent arrangements.

Thanks Alan — I shall endeavour to do just that

From ADVFN board

That Patent Office decision looks like a simple error correction to me: three of Zytronic’s employees were co-inventors, only one of their names went through as an inventor by mistake, and the decision fixes that mistake. A bit unusual, but all perfectly amicably settled.

To see what happened in more detail, see https://www.ipo.gov.uk/p-ipsum/Case/PublicationNumber/GB2502600 and in particular the two documents dated 28 November 2014 (click on the “Documents” case view link to the right to see them).

Gengulphus

I have done some further digging.

First, some further information from ZYT’s Admission document:

“7.5% of the net sales value of all products sold which are manufactured under the licence” does not seem insignificant to me.

I am sure it is this agreement that was referred to within ZYT’s 2004 results (extract in the post above), and renewed for 10 years to 2014.

I have searched for ‘Zytronic patents’ and came across this document: http://www.walkermobile.com/Touch_Technologies_Tutorial_Latest_Version.pdf

Page 4 of that PDF refers to “Zytronic (first license from Ronald Binstead, an inventor in the UK)“.

A search for ‘Ronald Binstead’ gives this:

http://binsteaddesigns.com

http://binsteaddesigns.com/history1.html

http://binsteaddesigns.com/history2.html

…which refers to ZYT. The website also suggests Mr Binstead continues to patent touchscreen technology.

All told, it looks to me as if ZYT has paid a not insignificant sum to Mr Binstead during the last 15 years for use of his touchscreen patents. It does not appear that Mr Binstead is or has ever been an employee of Zytronic.

Searches for ‘Binstead Zytronic patents’ give pages such as these:

http://www.google.co.uk/patents/US5844506

http://www.google.com/patents/EP1298803A3?cl=en

So as I see things, the upshot is ZYT has depended somewhat on Mr Binstead’s patents for the last 15 years. How much dependence is difficult to say, but a 7.5% royalty on the full product, plus an RNS announcement in 2004 confirming the agreement had been renewed, suggests the dependence was significant.

Anyway, the question now is whether ZYT remains dependent on somebody else’s patent to succeed? I cannot find any reference to the royalty agreement being extended past 2014, and I wonder if the patent in question has actually expired. Whatever, I just don’t get a good feeling about a small business that has paid to use somebody else’s idea for 15 years in a sector (touchscreens) where development and change can be very rapid.

Maynard

This was buried in the 2012 FY if i remember correctly:

“Subsequent royalties will be fully expensed on a monthly basis, until the end of life of the relevant patents and therefore the agreement in 2015.”

It would appear the first generation (single) was his but the second (multi) is Zytronics?

Might help with the Zytronic Patents:

http://worldwide.espacenet.com/searchResults?submitted=true&locale=en_EP&DB=EPODOC&ST=advanced&TI=&AB=&PN=&AP=&PR=&PD=&PA=zytronic&IN=&CPC=&IC=

Gengulphus did a rather lengthy and good explanation of patents.

Appreciate the time and effort you put in to your reports Maynard. Just a quick point, I know you were cautious on Zytronic, would be interested in your opinion after the recent bullish results.

Thanks Jay.

ZYT’s results looked fine to me. The numbers looked good and I see the commentary said “and focus on products with our proprietary technology”. That seemed to suggest there had been less focus in the past. If future results continue like these, then I will have been wrong to have been so cautious. Oh well.

Maynard

Early pioneer of touchscreen technology, Binstead Designs Limited (“BDL”), is pursuing a High Court claim for patent infringement, breach of confidence and breach of contract, against North-East England headquartered Zytronic Displays Ltd (a wholly owned subsidiary of Zytronic plc).

Formerly a licensee of BDL, the current dispute concerns allegations that Zytronic Displays Ltd is using BDL’s proprietary know how in the course of its manufacturing activities. In doing so, BDL asserts that Zytronic Displays Ltd is infringing UK Patent 2541336, which teaches an innovative method for forming a touch sensor.

The trial of the proceedings, which were issued on 27 November 2017, is listed to take place in October 2019.

BDL’s director, Mr Ronald Binstead, said of the dispute:

“It is with considerable reluctance that I have taken this action against a company that I worked alongside for many years. However, BDL is an innovation led business that cannot afford to allow infringements to go unchecked, not only on its own part, but also in fairness to other licensees”.