04 March 2015

By Maynard Paton

Today I’m continuing my hunt for Watch List shares with a look at Goodwin (GDWN).

Here are the initial attractions that prompted this research:

Illustrious financial history: Profits have surged 16-fold since 2000

Owner-orientated bosses: Family management boasts 53%/£107m shareholding

Interesting valuation: The shares are 32% off their high, leaving the trailing P/E at 11

As usual, I’m applying a question-and-answer template to help me pinpoint companies that match the criteria set out in How I Invest. I’m looking for as many Yes answers as possible.

Activity: Specialist engineer of industrial valves and alloy castings

Website: www.goodwin.co.uk

Share price: £28

Shares in issue: 7,200,000

Market capitalisation: £202m

Does the business boast a respectable track record?

Yes.

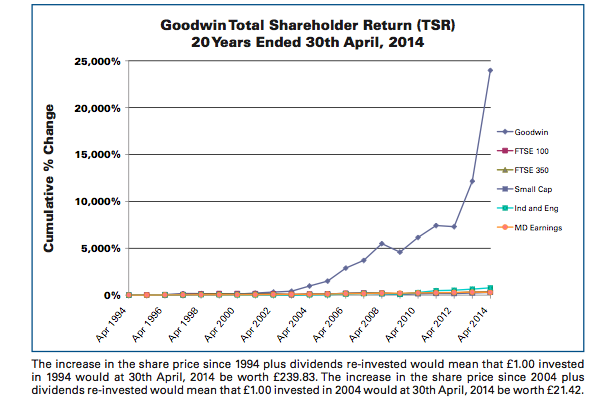

GDWN was established way back in 1883 and joined the stock market during the late 1950s. The chart below was extracted from GDWN’s 2014 annual report and shows an astonishing total-return performance for the last 20 years:

The 239-fold profit has been due to GDWN’s very impressive financial growth rates:

| 2010 to 2014 | 2005 to 2014 | 2000 to 2014 | |

| Sales CAGR | 5.4% | 14.4% | 11.6% |

| Pre-tax profit CAGR | 12.9% | 24.0% | 20.3% |

| Dividend per share CAGR | 8.8% | 13.6% | 19.5% |

Setbacks during the last 15 years have occurred only in 2011 (operating profits down 37%) and 2000 (operating profits down 80%, dividend down 50%). Progress otherwise has been up and up.

Recent years have witnessed a buoyant performance, in part due to greater sales to the energy industry and a substantial margin uplift. The special dividend was a nice touch, too:

| Year to 30 April | 2010 | 2011 | 2012 | 2013 | 2014 |

| Sales (£k) | 92,996 | 92,908 | 107,911 | 126,964 | 130,828 |

| Operating profit (£k) | 14,044 | 8,860 | 13,085 | 21,156 | 24,541 |

| Share of associate profit (£k) | 226 | 342 | 393 | 273 | 314 |

| Finance income (£k) | (959) | (1,054) | (1,205) | (1,133) | (760) |

| Pre-tax profit (£k) | 13,311 | 8,148 | 12,273 | 20,296 | 24,095 |

| Earnings per share (p) | 118.15 | 50.89 | 124.83 | 211.76 | 264.38 |

| Dividend per share (p) | 27.78 | 29.17 | 32.08 | 35.29 | 42.35 |

| Special dividend per share (p) | - | - | - | 17.65 | - |

Something to note: Not a single exceptional item has been declared during the last 15 years!

Has the business grown mostly without acquisition?

Yes.

The last 15 years have seen total acquisition spend of just £7m.

Has the business mostly self-funded its growth?

Yes.

The latest balance sheet displays share capital of £0.7m versus earnings retained by the business of £77m.

Does the business possess an asset-strong balance sheet?

Sort of.

GDWN generally operates with modest net debt — at the last count cash was £7m while borrowings were £22m. The loans do not seem problematic to me with 2014 profits at £25m.

The books also show land and buildings at £21m, which are carried at cost. Given the age of this business, I suspect the current market value of these sites could be substantially more than their accounting value.

Another major plus-point for this venerable operator is the absence of any defined-benefit pension obligations.

Does the business convert profits into free cash?

Not exactly.

| Year to 30 April | 2010 | 2011 | 2012 | 2013 | 2014 |

| Operating profit (£k) | 14,044 | 8,860 | 13,085 | 21,156 | 24,541 |

| Depreciation and amortisation (£k) | 3,288 | 3,352 | 3,809 | 3,530 | 4,118 |

| Cash capital expenditure (£k) | (4,235) | (7,398) | (4,569) | (9,409) | (15,082) |

| Working-capital movement (£k) | (4,798) | (7,656) | (5,156) | (6,384) | 5,988 |

| Net debt (£k) | (674) | (9,338) | (11,667) | (13,595) | (3,643) |

The last five years have witnessed some £41m of cash capital expenditure versus an aggregate £18m depreciation and amortisation charge. Furthermore, aggregate cash of £18m has been diverted into working-capital requirements. These are material sums when total operating profits for the period were £82m.

All told, it looks as if GDWN has converted about half of its operating profit into free cash since 2010. Generally that’s a poor conversion… unless it’s clear the reinvested money has been put to good use. Thankfully that’s the case at GDWN — profits have nearly doubled in the same time.

The 2014 annual report admits further significant cash investment will be required to support future growth. So I dare say GDWN’s payout ratio — the proportion of profits distributed as a dividend — will remain low at less than 25%.

Does the business enjoy a competitive advantage?

Possibly.

Margins at the larger Mechanical Engineering division reached an attractive 19% during 2013 and 2014. For what it is worth, GDWN claims this division is “world renowned for and the market leader in the design, manufacture and supply of Dual Plate Check Valves for use in the world`s hydrocarbon, energy and process industries”.

This text also caught my eye in the 2011 annual report: “R&D in Goodwin Steel Castings has resulted in a patent being granted to the company for its unique way of producing very large super nickel castings capable of operating at higher temperatures in advanced ultra super critical fossil fuelled power stations.”

And the 2014 annual report mentioned: “Our position as the leading global supplier of super nickel cast alloys…”

I also like the long-term view of the group’s R&D expenditure (from the 2012 annual report): “As a key performance indicator, R&D continues within all group companies whether it is to reduce manufacturing cost or develop new products that we consider there is a significant need for in the market over the next ten or more years.”

Does the business produce a respectable return on equity?

Yes.

Return on average equity for 2014 was £19m/£66m = 29% excluding non-controlling interests. Incredibly, the same calculation has topped 20% every year bar 2011 since 2005.

Does the business employ capable executives?

Yes.

John Goodwin and Richard Goodwin have served as executive chairman and managing director respectively since 1992, and have therefore overseen the outstanding track record above.

Succession plans seem to be in place, too, with three younger members of the Goodwin family also present as board executives.

Does the business employ good-value-for money executives?

Yes.

GDWN’s remuneration policy is worth reading (my bold):

“As will be seen below, the long term ongoing Total Shareholder Return on investment (TSR ) is more than acceptable, whether it be over five years, ten years or twenty years, but this has been achieved by the Directors and the Company taking long term policy decisions that at the time did not necessarily produce what a short term trader would have wanted in terms of annual profit and dividend. It is for this reason that Goodwin PLC has no desire to put excessive annual bonuses as a prime motivator to its Directors as this so often leads to undiscerning decisions being made that detrimentally affect the long term wealth of a company. Directors’ remuneration is designed to promote the long-term success of the Company.

In any company there are specific individual circumstances that on occasions will merit special treatment in a given year for a director either to keep or look after the person, indeed no different than we may do for an employee. In the matrix of remuneration for Directors you will note the Company has given itself flexibility to deal with specific circumstances which may not even be able to be made public for confidentiality reasons of which there are many. However, bearing in mind the performance of the Company over the past 20 years and more and that the Director salaries are anything but excessive versus the norm of other PLCs, this is the Board’s policy.

The Company has found over the years that this method of managing remuneration, which is principally monitored by the Managing Director and audited by the Chairman, has produced a team of cohesive Directors who have achieved results that surpass the average PLC performance, be it of the FTSE 100 or the FTSE 350, by a large margin. The unacceptable results over the past six years of many supposedly Blue Chip companies run with independent boards with very much incentivised executive directors is something that the Board of Goodwin PLC has no intention of emulating…”

Lovely stuff.

Both John and Richard Goodwin have seen their basic pay rise by an average of 8% a year since 2000 to £308k — which seems very fair to me given how pre-tax profits have surged to £25m. There have been no bonuses to speak of and minimal pension contributions as well.

Does the business employ owner-orientated executives?

Yes.

The Goodwin family still control at least 53% of the business — a shareholding presently worth at least £107m. The size of the stake has reduced only slightly I believe during the last decade or so.

I also like the lack of any option scheme and how the share count has remained static since at least 2000.

Does the business enjoy reasonable growth prospects?

Not in the short term.

Interim results issued during December showed sales up 3% and profits up 9%, but the group supplies the embattled oil and gas industry… and the chairman’s statement suggested the next 18 months could see lower profits:

“We have in the first half of this new year seen a continued fall off of activity in the oil and gas industry associated with lower oil barrel prices and the reduced investment by the major oil and gas companies. We started this new financial year with a record work load of £101 million, but this has steadily been decreasing as the order input fell behind our sales output. This decreasing workload will make it likely that the performance in the second half of this financial year and next year will not be as good as the first half of this financial year…”

“2015/16 Outlook

Whilst currently it is declining, we still have a good order book backlog in most of our companies. Time will tell whether we can find satisfactory levels of work to fill the gap temporarily caused by the slow down in the oil and gas industry which we think will be quieter for a couple of years.”

Looking further out, however, the board is more confident. Here’s an extract from the 2014 annual report:

“Whilst the energy mix is changing over the long term, it is considered that fossil fuels will likely remain the dominant energy resource in the future and hold 80% of the energy mix by 2035. Crude oil, natural gas (including shale gas) and coal we think will be evenly split in the energy market and it is unlikely by then that there will be any dominant energy form.

These sectors by definition have a long term future as the world population continues to grow and attain higher living standards, especially in the Pacific Basin. Over the past 50 years the world population has more than doubled from 3.2 billion to 7.3 billion people and in that same time the average energy consumption per person has also gone up by 50%. As the developing world continues to evolve, this average increase in energy consumption per person on the planet is unlikely to subside, so long term there will remain a significant demand for industrial products for the fossil fuel industries.”

Does the share price stand a good chance of becoming a bargain?

Possibly.

GDWN’s enterprise value at £28 a share is its £202m market cap less its cash of £7m plus its debt of £22m… that is, £217m or £30 a share.

Reported earnings for the year to October 2014 were 275p per share, which when interest costs are excluded come to about 282p.

The trailing P/E on my EV and EPS calculations is therefore £30/282p = 10.6.

That multiple does not look expensive to me.

However, profits are set to drop and the experienced management does not foresee any rebound for at least 18 months.

So I have three immediate worries:

- GDWN’s customers in the oil and gas industry stop spending for a protracted period of time (after all, the oil price has nearly halved);

- GDWN’s profits fall heavily, as the group’s recent (and significant) investments in plant, working capital and staff are under-utilised;

- GDWN’s bumper profits from 2013 and 2014 turn out to be ‘freak’ results, making the trailing P/E somewhat academic.

Looking at GDWN’s valuation another way, if I want to double my money during the next five years, I need the share price to reach £56 assuming the dividend is held at 42p per share.

A so-so P/E of 12.5 on that £56 indicates annual earnings would have to advance to 434p per share — up 10% a year on average from the last reported 275p. Such a recovery is possible of course, but positive progress will be back-end loaded during my five-year horizon.

Is it worth watching Goodwin?

Yes.

GDWN’s offers lots of positives for me — the track record is superb, the managers are top-notch and the reported returns on equity are wonderful.

All that matters now I reckon is determining a great entry price. £28 feels reasonable, but I don’t get the feeling it is an obvious bargain. For now, I think it might pay to await a lower price and/or see just far profits do drop. In the meantime, I’ll do more sums.

Maynard Paton

Disclosure: Maynard does not own shares in Goodwin.

Hi Maynard, Glad to see GDWN has joined your watch list!. I bought fractional ownership in GDWN with the intention of holding for decades providing the fundamentals remain sound. If the company can continue to compound ROIC like it has for the past 20 years the current price seems more than fair value.

I think this quote by Charlie Munger sums it up well.

‘Over the long term, it’s hard for a stock to earn a much better return that the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you’re not going to make much different than a six percent return – even if you originally buy it at a huge discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay an expensive looking price, you’ll end up with one hell of a result.’ – Charlie Munger

I’ve got a number of interesting compounding machines on my watch list and I’ll be in touch shortly with a few more ideas.

Regards,

David

Mayn

Thanks for the Goodwin analysis, interesting company, one I know in the Oil and Gas industry, reliable from what I recall.

David

Q3 update out today:

http://www.investegate.co.uk/goodwin-plc–gdwn-/rns/interim-management-statement/201503130930023808H/

“Goodwin PLC today announces its third quarter Interim Management Statement for the period 1st November 2014 to 31st January 2015.

The consolidated, abbreviated and unaudited income statement below for the nine months’ trading ending 31st January 2015 shows revenue of £108.5 million (2014: £103.1 million) and profit before taxation of £17.3 million (2014: £18.0 million).

There have been no significant adverse events and the trading situation as advised at last year end and at the end of the first half of this year is starting to ease down associated with reduced capital expenditure by the oil and gas companies and tighter market pricing.”

No surprise about the “trading situation“.

My sums indicate the Q3 operating profit was £4,101k — the lowest quarterly profit since the 3 months to July 2012 (£3,930k). Since then, every quarter has delivered profits between £5m and £7.3m. Clearly the O&G sector downturn has started to bite and annualising the latest quarter gives yearly operating profits of £16m — versus £24.5m seen during FY2014.

I still need to do more work on GDWN’s valuation, but for now I remain on the sidelines. Hopefully profits will fall further, pulling down the share price and creating a super opportunity to buy for a long-term recovery.

Maynard

Hi Maynard, thanks for that detailed review.

Goodwin’s pretty high on my watchlist at the moment. I’ve almost bought it a couple of times in the past but the price has been just that bit too high. For what it’s worth, on a purely quantitative basis because I haven’t looked at the company in nearly as much detail as you, Goodwin does look like pretty good value at the moment. According to my spreadsheet it has:

10-year growth rate of 14%

10-year growth “quality” of 83% (how often revenues/earnings/dividends went up)

10-year “net” ROCE (net of interest and tax) of 18%

Borrowings at less than 1-times 5-year average post tax profits

10-year free cash flow/dividend ratio of 1.8

10-year capex/earnings ratio of 0.7 (below 1 is quite low)

PE10 (price to 10-year earnings) of 20 (higher than average but it’s an above average company)

The only real downside for me is that lack of dividend yield, but if those retained earnings can be deployed at around 20% then that’s fine by me.

Will be interesting to see if you end up buying it.

John

Hi John,

Thanks for the feedback. Yes, GDWN does look good value on a trailing profit basis, but I am convinced the next year or so will see lower profits and a share price lower than the £28 I cited in the article. My earlier comment noted GDWN’s Q3 figures and profit reduction, and I do get the impression the sizeable drop-off in the O&G sector could reverberate for some time. I am on the sidelines at present. Oh, I see the price is now £23, so it has paid to wait so far. I genuinely do not have a price in mind right now.

Maynard

Goodwin’s 2015 annual results were published this morning:

http://online.morningstarir.com/servlet/HsPublic?context=ir.access&ir_option=RNS_NEWS&item=2140987509964800&ir_client_id=319

“I am pleased to report that the pre-tax profit for the Group for the twelve month period ending 30th April 2015 was £20.1 million (2014: £24.1 million), a decrease of 16.6% on revenue of £127.0 million, 2.9% lower than last year. The Directors propose an unchanged ordinary dividend of 42.348p.”

Q4 did not appear great. My sums indicate the fourth quarter produced revenues of £18,568k (down 33% from £27,719k last year) and operating profit of £2,768k (down 54% from £6,014k last year). On a half-yearly basis, it looks as if Goodwin is back to where it was during the six months to April 2012, when revenues were £54m and operating profits were close to £7m.

The downturn within the oil and gas sector hurt GDWN’s 2015 performance:

“This deterioration in gross profit and pre-tax profit earned stems from the oil and gas engineering market sector, with order placing activity having substantially contracted in the first quarter of the financial year…”

But there might be some clouds lifting:

“The Group order workload as at 30th April 2015 was 22% lower than twelve months earlier and stood at £79 million. This level of workload increased in the first two months of the new financial year such that as at the time of writing this report there is a possibility that the performance in this new financial year will not be as bad as feared.”

Within the accounts, I note capex was substantial at £18m and caused net debt to move from less than £4m to close to £10m (however, the year-end figure was less than the £15m seen at the half-year stage). The original Blog post above referred to GDWN’s admission that “further significant cash investment will be required to support future growth“. From a preliminary skim, I could not see any worrying movements elsewhere in the numbers.

The share price does not seem like an obvious bargain at £26. Enterprise value (EV) is about £27/share and divided by 2015 EPS of 208p gives a P/E of 13. Dilemma is of course is whether the bumper first half (EPS of 141p) or the challenging second half (EPS of 67p) is more likely to occur during the next few years, what with the oil price remaining at recent lows and subdued industry activity likely for the foreseeable future. I am still on the sidelines.

The accompanying presentation to these results — http://www.goodwin.co.uk/2015/ — contained some updated and impressive charts, such as this:

Perhaps it could just pay to simply remember the LTBH credentials of this business and not worry too much about waiting for the perfect price. (Although the cheapskate in me finds that hard to do!)

Maynard

PS Interesting too that GDWN has now appointed a non-exec director: http://www.investegate.co.uk/goodwin-plc–gdwn-/rns/directorate-change/201504160700493599K/

The 2014 annual report had said: “In view of the Group’s present size and proven track record, non-executive directors are not thought to be appropriate, due to the time and cost likely to be involved and the lack of opportunity for adding significant value to the business.”

Looks like GDWN has finally found someone that could add “significant value“.