***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

09 August 2025

By Maynard Paton

This month I have gone ‘back to basics’ by employing an old screen that identifies companies with strong balance sheets, robust margins and rising dividends.

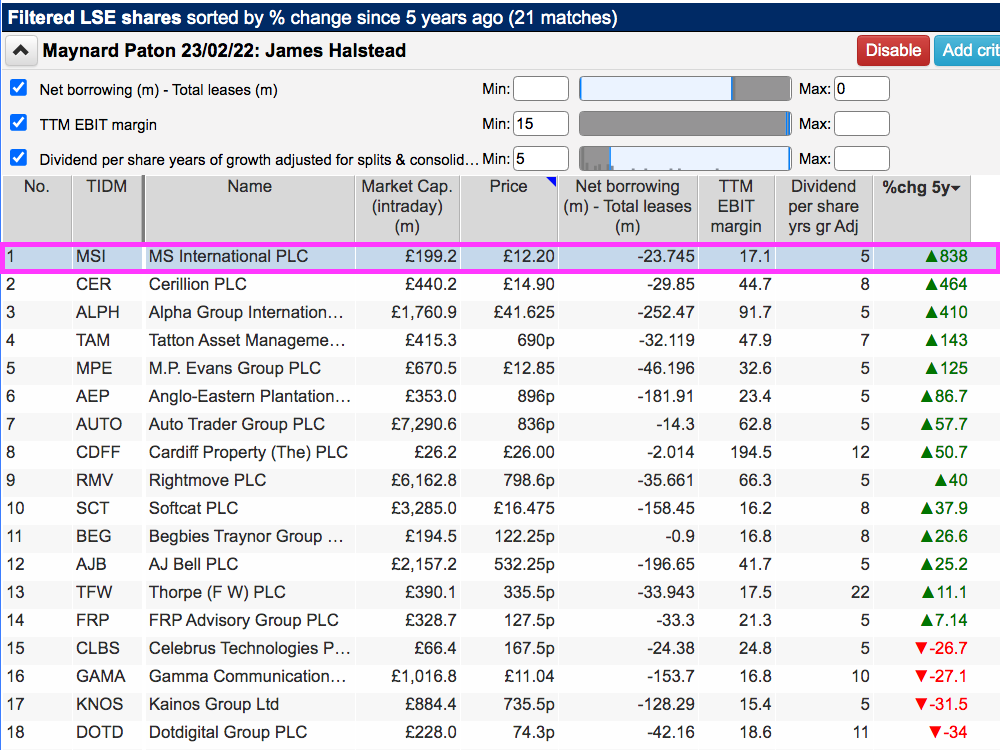

I must admit I was disappointed my three ‘quality’ criteria returned only 21 names:

The exact filters I applied for this search were:

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations);

- A trailing 12-month operating margin of 15% or more, and;

- A minimum five-year record of annual dividend improvements.

I added an extra column to the screening results to sort the 21 names on five-year share-price performance.

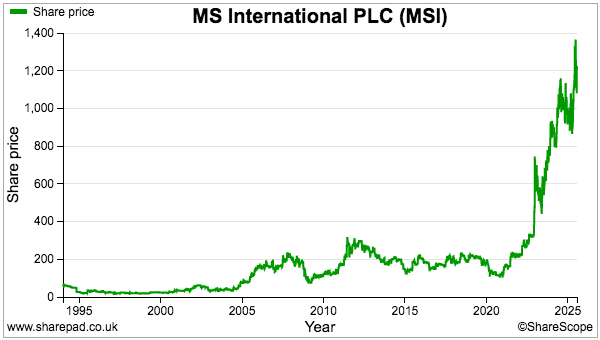

I selected MS International because its shares had surged an amazing 838% since July 2020:

Let’s take a closer look.

Read my full MS INTERNATIONAL article for ShareScope >>Maynard Paton

High quality article on MSI as always Maynard.

I’ve had a long hate/love relationship with the company. I initially bought a small position in 2007 and sold in 2017 vowing never to return due to the lack of corporate governance, high executive salaries and lacklustre performance due to the woeful support from the UK Mod which continues to today.

I was quite sceptical when alerted by an investor friend in 2021 highlighting the potential of the US Naval contract with the potential to displace BAE as supplier of Mk38 small calibre weapons. After some new research I took a position and attended the 2021 Agm. I maintain it is the most important company Agm to attend as the information in the public space is so limited. I was reassured that despite the highlighted flaws in the company the opportunity was credible and potentially transformational and built a decent position. This contract was unrelated to the Ukrainian conflict. I’ve now clocked up 5 visits to a Holiday Inn just off the A1 to meet the board.

One thing I hadn’t appreciated when taking a position was the potential of the new land based system. MSI are world leaders in 30mm cannon mounts and 30mm is the smallest calibre manufactured with programmable ‘airburst’ ammunition which has been particularly effective in downing drones.

A couple of observations from your article

The £54m middle eastern contract was to a single country and according to my calcs has already surpassed the headline number.

I think the contract liabilities relate primarily to US Naval contracts as the US DoD contracts on pretty favourable working capital terms (also starting to become more evident at Goodwin with their US Naval exposure) to support the military supply chain.

Lord Lee has built up his current holding in more recent times rather than retaining it from his time on the board.

My personal view is that Nicholas Bell will not in time take the reigns of the business and that the likely corporate outcome is a short term streamlining of the business to a pure defence play followed by a trade sale of the defence business once the potential of the counter drone land based product is fully realised.

Hi Patrick

Thanks for the message. When writing the article I did double-check the ADVFN board and noticed you had written about the 30mm guns, so I knew then I had to avoid any great mistakes! Well done on the investment, especially going back in after 10 years of earlier disappointment. Not easy to do. Yes, AGMs for this type of company can be extremely valuable and, although MSI’s corp-gov suggests a good Q&A might not occur at the meetings, I am glad the board provided useful info to those making the effort to attend. I think the latest statement suggests a streamlining will become more likely given the higher (but rejected) bid for the non-core operations, and an eventual trade sale seems very plausible as you say.

Maynard

Hi Maynard, thanks for another great article. I’m not sure if you’re aware that the links within the article to the Substack writer you referenced are actually pointing to your own Sharescope article about Cerillion. I assume this is a mistake.

Thanks John,

Yes this is a mistake, the links I sent to ShareScope were:

https://substack.com/home/post/p-161945890 and https://substack.com/home/post/p-161963662

Maynard