***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 July 2025

By Maynard Paton

“I stress the long-term advisedly, because our entire emphasis is towards the development of a worldwide group of businesses which by their very nature require their managements to take a long view.

Many companies in the group are in excess of 100 years old. These enterprises have acquired particular skills, traditions and ethos, and we see ourselves more in the nature of custodians or trustees than as owners.

That is, we do not see these assets as objects or commodities or bits of paper that can be traded, but rather as living entities from which, if properly managed, we might earn an attractive return on our investment.”

You could be forgiven for thinking that statement was written by Warren Buffett to his Berkshire Hathaway shareholders. But the author was in fact Gordon Fox, then the chairman of Camellia, back in 1990.

By employing a very long-term investment approach, Mr Fox enjoyed great success building Camellia into a mini Berkshire-type conglomerate. But rather than textiles, insurance and banks, Mr Fox instead focused primarily on agriculture…

…and between 1969 and 1999 compounded Camellia’s net asset value (NAV) from less than £500k to £170 million — equivalent to a 21% average annual growth rate.

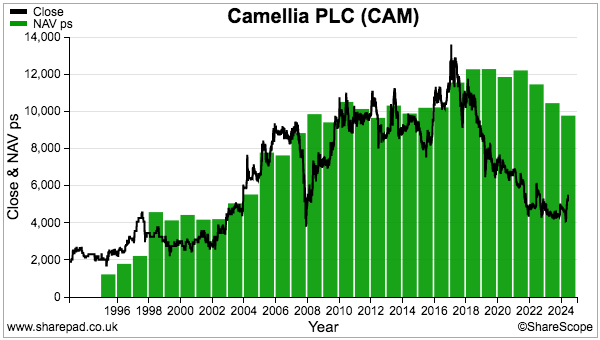

Camellia’s NAV has since advanced to approximately £300 million and is chock-full of cash and investments…

…yet the share price has declined 60% since its 2018 peak:

Investors can today buy at a 50%-plus discount to the value of the balance sheet.

So what exactly has happened at this NAV ‘compounder’? Is the NAV really worth £300 million? And have the £54 shares become a bargain?

Let’s take a closer look.

Read my full CAMELLIA article for ShareScope >>