01 July 2025

By Maynard Paton

Happy Tuesday! I hope the first six months of 2025 have been positive for your shares.

A summary of my portfolio’s first half and Q2 trading:

- H1 return: -11.1%*

- Q2 trades: 2 Top-ups (Bioventix at £24.08 and S & U at £14.64).

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

What a difference a year makes. Twelve months ago I was trumpeting “my best-ever H1 [+20%] since I commenced this blog at the beginning of 2015“.

Today I am staring at my weakest relative six-month performance since I commenced this blog at the beginning of 2015! Year to date my portfolio is down 11.1% while the FTSE 100 has powered 9.5% higher. I will now have to re-read whether I am a good investor :-(

This year’s underperformance follows the rollercoaster share price at System1, in which I have an oversized position because of its multi-bagger potential. That potential took a knock during April following an ominous Q4 update that implied a slowing of key revenue streams and talked of a “downside risk” to client budgets.

Let’s just say System1‘s FY results and Q1 update next week are likely to prove pivotal to my portfolio’s 2025 performance.

Newsflow from my other holdings has been mixed, with a 10% dividend lift from M Winkworth somewhat counterbalancing flat payouts at Andrews Sykes and Mountview Estates. And despite a dividend cut at S & U, the specialist moneylender has been my best performer this year!

Possibly the most intriguing announcement during the last three months was the sudden and unexplained departure of the chief executive of City of London Investment.

Abrupt exits do not occur if all is going well and I am braced for unfavourable short-term news. But I welcome the board’s decision to seek fresh leadership to help find new clients, as this fund manager’s investing style is commendable and its cash/bond returns have been impressive.

I have summarised below what happened to my portfolio during April, May and June. (Please click here to read all of my previous quarterly round-ups). I then discuss my investing approach and how I hope to become a better investor.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe and M Winkworth.

Q2 share trades

Bioventix

I have increased my Bioventix (BVXP) position by approximately 8% at £24.08 including all costs.

Nothing has really changed since my Q1 2025 BVXP top-up, apart from the shares declined and offered a 6.4% dividend yield at my purchase price. My latest BVXP review.

S & U

I have increased my S & U (SUS) position by approximately 40% at £14.64 including all costs.

I spent 13.5 hours during the Easter weekend watching the recordings of the Supreme Court hearing about ‘secret commissions’ within the motor-finance industry.

The possibility of the Supreme Court upholding an earlier legal verdict — and therefore opening the floodgates to substantial compensation claims — has overshadowed SUS’s shares since October.

My layman view of the recordings did not suggest the Supreme Court would simply rubber-stamp the earlier legal verdict. Among the five Lord Justices hearing the case, the tone of questioning from the two most vocal Lords (Briggs and Hodge) did appear more supportive towards the lenders (Close Brothers and MotoNovo) than the borrowers (Miss Hopcraft, Mr Johnson and Mr Wrench).

Assuming the deliberations of the Lord Justices follow a path similar to the hearing, I suspect the lenders could emerge as winners with at least a 3-2 decision.

Submissions on both sides covered the legal definitions of “bribery” and “fiduciary duty“, and I would summarise the hearing as the lenders taking a wider, practical view of both terms with the borrowers spotlighting the finer details of particular case laws.

A very positive outcome for the lenders was forecast by the legal experts at Quadrant Chambers, who commendably hosted this post-hearing seminar. They concluded only the most “egregious” of ‘secret commissions’ may be subject to repayment and dismissed the notion of widescale compensation payments:

[Quadrant Chambers] “On the invite, we asked whether the Supreme Court would apply the brakes to these cases [against the motor-finance lenders]. We don’t say the Supreme Court has put the handbrake on, but the brakes are certainly on the car, there are nails in the tyres and it’s not driving very well. It has not been towed yet, but it is not looking good.“

I wrote in my H1 2025 review:

“Given the £14 shares trade at 0.73x NAV — a rating last seen at the banking-crash lows — investors have seemingly decided SUS could be liable to repay ‘secret’ commissions of up to £63m… although the “appropriate compensation” could arguably be minimal.“

After watching all 13.5 hours of the hearing, I would be amazed if the Lord Justices unanimously found in favour of the borrowers. At £14.64, I believed the risk-reward ratio strongly favoured a top-up… but let’s see what the Supreme Court actually decides. A decision is expected this summer. My latest SUS review.

Q2 portfolio news

As usual I have kept watch on all of my holdings. The Q2 developments are summarised below:

- Andrews Sykes: FY 2024 operating profit up 2% to a record £23.2m despite revenue slipping 4% following French depot closures and “poor summer temperatures“.

- Bioventix: Nothing of significance

- City of London Investment: Q3 2025 funds under management suffering a further $212m outflow plus the sudden — but probably welcome — departure of the chief executive.

- Mincon: Q1 2025 talking remarkably of “strong” order books followed by the retirement of founder Patrick Purcell from the board (blog coverage ceased for now).

- Mountview Estates: FY 2025 net asset value inching less than 1% higher to a record £103.27 per share after the “law of averages” led to fewer sold properties.

- S & U: Adverse regulatory developments reducing FY 2025 pre-tax profit by 29% offset subsequently by “above budget” Q1 2026 motor-finance trading.

- System1: An ominous Q4 2025 implying slower ad-testing/US revenue growth plus an LTIP requiring a 635p share price to vest.

- FW Thorpe: Nothing of significance.

- M Winkworth: FY 2024 revenue up 17% and underlying operating profit up 24%, then supported by the Q1 2025 dividend up 10% plus an informative AGM (notes coming soon).

Q2 portfolio returns

The chart below compares my portfolio’s monthly progress to that of the FTSE 100 total return index:

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me so far this year:

This chart shows each holding’s contribution towards my 11.1% H1 loss:

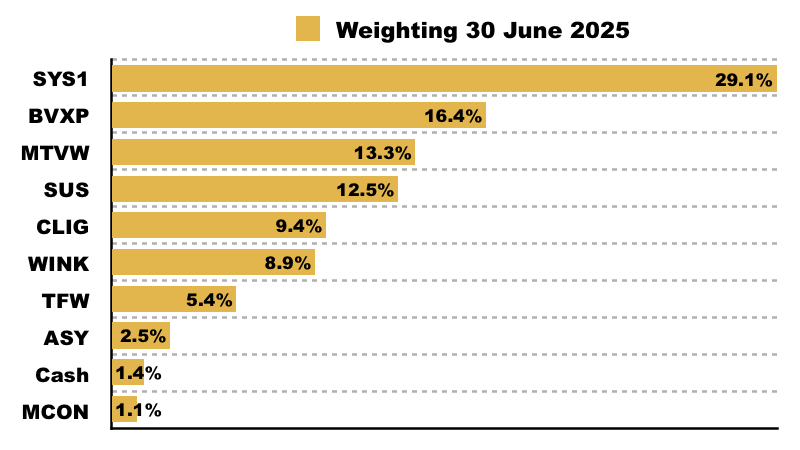

And this chart confirms my portfolio’s holdings and their weightings at the end of Q2:

How I (Now) Invest

I have been buying shares for approximately 30 years and writing this portfolio blog for more than ten.

During all that time I have often tweaked my investing philosophy as I learn more about what works for me in the markets. The same reflective process also leads me to increase my commitment to certain aspects of my approach.

I thought it useful to clarify a number of points that I have mulled over of late. I am hoping what follows can eventually help me become a better investor.

1. Deeper company understanding

I last introduced a new share to my portfolio during 2017. Eight years without buying a completely fresh idea makes me extremely unusual among private investors.

I never suddenly decided to buy only existing holdings. The approach instead simply evolved over time as I delved deeper into my positions to understand them just that little bit more than most of the market.

I now realise I continue to learn significant information about each holding years after my initial purchase, and I now doubt I would ever have the same insight and purchase conviction with a completely new investment.

This ‘deeper understanding’ strategy — at least in theory! — ought to increase my chances of identifying a bargain within my portfolio while decreasing the chances of panic selling during a crash. The approach also helps me run a concentrated portfolio, which I still believe creates a greater chance of long-term outperformance.

I continue to analyse a different company every month through my ShareScope articles, which every so often provide me with a possible portfolio idea.

I do have a handful of names on my watchlist to maybe buy one day… but future portfolio movements are more likely be top-slicing an existing position to top-up another.

2. Embracing smaller positions

I used to believe a new share would never be worth buying unless I was prepared to invest 10% of my portfolio on Day 1. My thinking has since moved on and I am now prepared to purchase much lower amounts at first.

This change of heart is due in part to practical considerations. As my portfolio has become larger — and because the shares I like are generally illiquid — that 10% ambition has become increasingly unworkable.

Take Andrews Sykes (ASY) for example. I first bought these shares during 2013 and ended up with a modest 3% portfolio position because the price rallied quickly and I stopped buying.

ASY has since typically represented 2-3% of my portfolio and I have often wondered how this position could ever influence my overall return. But I now take the view this 2-3% position prompts me to monitor the company closely — and gives me the chance to take it towards a 10%-plus position if/when I identify an appealing top-up opportunity.

Any new share I now buy will almost certainly be a sub-3% position. I am sure I will then develop more conviction about the new holding… and that even better buying opportunities will arise thereafter!

3. Employees versus owners

I do sometimes question whether all UK small-caps are now run for the benefit of their employees rather than their owners. In fact, some companies always seem keen to lift the remuneration of their ‘most important assets’ even though their shareholders might be facing a stagnant dividend income.

The employee-vs-shareholder conflict almost certainly stems from most executives being long-time employees. They have established an entrenched mindset of following instructions for a salary and a possible bonus, with priorities such as career development and flexible working eclipsing the abstract task of delivering shareholder value. Boards may well mention ‘shareholder alignment’, but often the amount spent on their shares tells a different story.

I have always been convinced directors with substantial shareholding are far more likely to possess an ‘owner mindset’ — one that believes their workforce is inherently employed to reward shareholders through greater earnings and higher dividends.

But these days I am even more convinced about the need for ‘owner mindsets\, especially as institutions just seem to waive through generous executive pay and soft LTIPs that then flow down to the lower ranks.

I now always seek to invest alongside somebody with the shareholding clout who ensures the board behaves like owners.

4. Thinking for myself

I follow various investor newsletters through Substack and several have been dabbling with AI to research new ideas. Although their results to date have been less than impressive, the temptation to save time and effort is great. One Substacker has even declared an ‘AI policy’, so readers can presumably distinguish between him and his bot.

I have never used ChatGPT or similar, and never will for investing. I am an old-school stock-picker, and my ABC of investing remains: Assume nothing, Believe nobody and Check everything.

I truly believe investors should be studying companies for themselves rather than outsourcing the work to a persuasive bot. Reading annual reports requires effort of course, but at least you will gain much greater knowledge — that should lead to better decisions — versus the AI-adoption crowd.

Such are my old-school ways, I still input accounts manually into a spreadsheet. That way restatements, exceptional items, pension deficits and other bookkeeping nasties come to light and help form a judgment.

I know ChatGPT and similar scrape my website for source material. There is an old computer-science concept called ‘garbage in, garbage out’ and I can only hope AI is scraping the right websites.

5. 40-year horizon

Warren Buffett will retire as Berkshire Hathaway chief executive at the end of 2025 at 95 years of age. If I can last as long as Mr Buffett has as Berkshire’s CEO, then I have another 40 years of investing ahead of me.

Four decades years is a long time to compound my wealth, assuming of course: i) I make it to my 90s, and; ii) I don’t spend my portfolio in the meantime!

Anticipating I have decades left to invest helps insulate me from market ructions (‘this too will pass‘) and leads me towards businesses run with similar long-haul attitudes. Family-controlled companies in particular can be ideal candidates for such extended horizons.

I used to view investments on a five-year horizon, hoping they could double during that time. These days I occasionally imagine my portfolio simply becoming a mini-Berkshire… stocked with reliable, owner-managed ‘permanent’ holdings that could compound without fanfare over a decade or two.

Mr Buffett tends to prefer buying entire companies outright over buying minority stakes through the stock market, and a good discipline for me is to consider whether I too would want to own my holdings outright.

Summary

We all evolve as investors. Since 2004 for example, my investments have ranged from FTSE buy and holds such as London Stock Exchange to microcap value traps such as 3 Legs Resources.

I have chalked up a few successes, sworn off certain types of shares and gradually learnt to focus on a small group of familiar companies in which I might enjoy an edge over most of the market.

Within my company reviews, I have increasingly placed a greater emphasis on ‘workforce productivity‘ to help avoid shares where the board and employees are paid too much for doing too little.

What is somewhat scary is that, if I do have another 40 years of investing ahead of me, I am not yet half-way through my stock-picking career. I trust I will continue to evolve as an investor and no doubt I will publish many more ‘How I (Now) Invest’ updates before 2065.

Until next time, I wish you safe and healthy investing.

Maynard Paton

Thanks for the update ! I love to read these (as all your posts, by the way, even and especially when the company discussed doesn’t fit into my limited investment horizon).

Thanks Simon!

I suspect you read the excellent Dc Smith books by Peter Grainger.

You have a very idiosyncratic portfolio but I do wonder about Mountview. Yes it owns properties with protected rents that will rebar when the current occupiers die but is there not a significant opportunity cost in holding the shares, meaning the money could be better deployed elsewhere?

As always your pieces are interesting, informative and searingly honest.

Thanks Stephen. I suppose the MTVW money could always be better deployed elsewhere, but right now the price is back to where it was 10 years ago and I would like to think better returns will occur during the next 10 years. It will never multibag, but its assets are simple, safe and presently relatively cheap versus the market cap. There is also an outside chance of a ‘corporate event’ one day given the CEO leads the family concert party, has no obvious successor and is 77 years old.

Maynard

Several sources claim that Warren Buffet made 98% of his gains after the age of 65, Maynard. Having reached that age milestone myself, it’s a comforting thought.

On a separate note, my sincere thanks for your time and effort in making your research available. It’s always a pleasure reading them.

Thanks Chris! Hope your compounding goes well.

Maynard

> Several sources claim that Warren Buffet made 98% of his gains after the age of 65, Maynard. Having reached that age milestone myself, it’s a comforting thought.

I presume this is just taking absolute values due to how compounding math works.

I find it hard to believe his IRR% was better when he got more capital, I think he’s said this multiple times as well it’s easier to make money with less capital.

Hi Maynard,

I have some feedback on your investment style as I’ve followed over the past few years.

My own returns have tracked the SP500 index since 2019 FWIW.

This is just my opinion:

1. You focus too much on ‘forever’ buy and hold without doing risk management. The benefit of public markets is that you have immediate liquidity, when a stock becomes closer to your perceived intrinsic value you should really be cutting it down imo. Example is SYS1, it had a massive run up of >200%. Did it’s intrinsic value really increase >200% or did the market just get overhyped and ignore downside potential?

Your investment of just buying and holding means you are paying a public liquidity premium without ever taking advantage of it, you might as well go invest in the private market.

At a huge portfolio % allocation it is absolutely a mistake to not sell off after this type of short term rise, there are still downside risks and you aren’t a C-level executive with insider knowledge.

2. You focus on dividends too much, as evidenced in this post, just like most UK investors do too much. Dividends are usually the least efficient way to return gains to shareholders given the tax %. Investing in the company (Capex, employees with careers & bonuses), buybacks (if the companies shares are undervalued) should all be preferred.

Only if a company has uninvested excess cash just sitting on the books would a dividend be prudent which most of your companies do not I believe so most shouldn’t even be paying dividends.

3. You focus too much on line-item data. Yes you find some inconsistencies sometimes in RNS’s like cakebox, but the time spent doing this vs the reward is not worth it imo. Most companies are not outright committing fraud.

Also, not using LLM’s is a huge mistake. You can throw entire annual reports & TU’s into Gemini’s 2.5 pro version and have it find accurate red flags and reference everything correctly. You can also use deep research to quickly find stocks rather than screeners.

4. I see a lot of relative ratios but never DCF’s or macro-based thinking (i.e stocks that would be hit by tarrifs when trump got elected which affects intrinsic value).

5. UK companies are much more poorly run overall than US companies in terms of ROIC. The management is not as good, the market is not as big etc.

Being focused on UK small caps right now makes sense because AIM is in the gutter, but it made no sense to not look at US stocks pre-2020 before the bubbles imo.

I think you would benefit from learning more overall on different ways to invest such as macroeconomics, corporate finance courses etc

Thanks

Hi Martin

Many thanks for the feedback. All good points.

“1. You focus too much on ‘forever’ buy and hold without doing risk management. The benefit of public markets is that you have immediate liquidity, when a stock becomes closer to your perceived intrinsic value you should really be cutting it down imo.”

I have sort of addressed the ‘trim your winners’ dilemma here: https://maynardpaton.com/2024/10/03/q3-2024-running-multi-baggers-to-40-or-more-of-your-portfolio/#running-multi-baggers-to-40-or-more-of-your-portfolio

Essentially I have lost out in the past by not keeping the faith with large positions that went on to multi-bag. When its price peaked, SYS1 was reporting accelerated revenue growth and publishing upbeat ‘growth scenarios’ that I felt made the shares worth holding even after the 200% rise.

“2. You focus on dividends too much, as evidenced in this post, just like most UK investors do too much.”

Probably have not made this clear, but I use some of the dividends to cover my living expenses. So no dividends = no blog. I would say most of my companies have surplus cash on the books that justify some dividends. The payouts are questionable at MCON (debt/profit issues) and possibly SUS (legal worries).

“3. You focus too much on line-item data.”

I was a financial writer for 15 years and during that time was a share tipster. There is nothing more embarrassing in that line of work than conveying a bullish view — only then for something bad to happen that was already spotlighted in the small-print. Can damage your credibility, as a few commentators discovered with CBOX. I am pretty sure 99% of PIs don’t delve into the accounts. Tim Steer’s book ‘The Signs Were There’ offers good examples of what the market often misses.

“4. I see a lot of relative ratios but never DCF’s or macro-based thinking”

I looked at DCFs 25 years ago and was never convinced about the terminal value often forming the bulk of the result. I thought a simpler way would be to slap on a multiple to today’s cash flow rather than something derived well into future. I try to be ‘vaguely right’ rather than ‘precisely wrong’ as somebody once said. Not sure I can add anything on the macro side and I don’t think even Mr Trump knows how his tariffs will play out.

“5. UK companies are much more poorly run overall than US companies in terms of ROIC. The management is not as good, the market is not as big etc.”

Agreed. I have always invested in the UK, I am familiar with the nuances of the market, and would just find it hard to migrate to the US — especially after that market has done so well.

Maynard

> I have sort of addressed the ‘trim your winners’ dilemma here

Yes it’s not easy. Personally, if I see a large value rise in one of my stocks where I feel the intrinsic value hasn’t risen the same amount (i.e it’s getting closer to roughly where I think the intrinsic value is) then I will start selling some as the risk in theory should be going up.

Andrew Brenton of Turtle Creek is a good example of doing this and achieving 20% CAGR (In the Canadian market, not even the US). He gave an example in one of his videos of the returns he’s got by doing this vs if he would have bought and hold and it’s a substantial difference.

Also, 35% is just a massive allocation for a small cap like SYS1. I got up to 15% once with WJG and suffered an overnight drop of 50%.

The issue I’ve found with purely buy & hold is that if/when the stock does drop & the market overreacts you can’t easily buy more because you allocation is extremely high. You are exposed to massive company specific risk.

> Probably have not made this clear, but I use some of the dividends to cover my living expenses

You should be able to ‘create’ your own dividends though. A companies stock price should always drop by the amount of dividends it pays because the company has less cash on it’s book so it’s worth less (obviously in small caps where the market is less efficient this isn’t always a 1:1 ratio).

Warren Buffet has spoken about this, just sell from capital appreciation (which also ties in to point 1) and create your own dividends, it’s the same thing but you are more likely to own companies with better management.

> I try to be ‘vaguely right’ rather than ‘precisely wrong’ as somebody once said.

There’s no right or wrong answer as we both know and I too use relative ratios however they still suffer from having implicit future projections baked into them, just like a DCF does but it’s not as obvious. Aswath Damodaran has mentioned this a few times.

But yeah, thanks for posting all your updates, it’s not easy to post about stocks when things happen and I hope future updates are more positive than this unfortunate SYS1 update!

2 of my biggest holdings right now are Greggs & Wise (both at 10%), I think Greggs might be worth another look right now for you as you’ve done a post on it before and it’s the easiest company in the world to understand.

Thanks again

Hi Martin

Thanks for the extra comments.

“You are exposed to massive company specific risk.”

Very true. I suppose if the rest of my portfolio had doubled in the last five years as SYS1 has, then the issue would not be as pressing — even though the company-specific risk to SYS1 would be exactly the same. All will boil down to how the company performs from here. There are lots of examples of great stocks enduring major drawdowns on the way to mega-bagger status. People trimmed at what they thought was the top, but (with hindsight!) really should have held on through the declines. I will investigate Turtle Creek to see what they bought!

“Warren Buffet has spoken about this, just sell from capital appreciation

I have tried to ‘sell from capital appreciation’ in lieu of of dividends, and found it difficult to undertake in practice. All the time I was thinking about ‘should I sell now?’ as I was worried about being forced to sell at a low when the income was needed. Dividends should not fluctuate as much as share prices. The boards that supply most of my dividends seem quite capable, as their dividends have risen over time and they collect large sums from such payments as well.

“2 of my biggest holdings right now are Greggs & Wise (both at 10%),”

I actually prefer Wise :-) Have heard some convincing commentary about the business and, if it really does disrupt international money transfers, it sounds like a business you could buy and hold without needing to trim at intrinsic value!

Maynard

On point 2: I believe Maynard says his investments are in ISAs and a SIPP. ISAs are capital and dividend tax free. And dividends in this case allow tax free income without having to sell down one’s position.

Hi Maynard,

Hope all is well?

Many thanks for your blog, and as always, your honesty when you it comes to analysing your investing approach.

One thing I’ve wondered is whether the amount of research you undertake can leave you partial to sitting on positions for too long (eg. Tasty / Mincon). By the end of some of your posts I find myself thinking “this is an absolute basket case.” But yet, you always seem to still have it as a position. Have you ever thought about taking a “cut your losers early approach?”

I also find it incredible that despite analysing many shares (for sharescope) over the past few years, you still haven’t taken a new position in any of them (despite UK markets becoming more attractive from a valuation standpoint).

I feel like there are better marginal returns from undertaking less detailed research, but being more active in portfolio management. 20% of the work will get you 80% of the way there etc…

In my opinion, there around 800ish shares in the UK market. There are many obvious reasons to not buy 98% of them. Investing is a game where you’re looking for a reason to say “no”.

However, I have only been investing for a couple of years, so you are certainly more experienced than me! And I’d be interested to hear your thoughts.

Best wishes!

Hi Peter,

Thanks for the comment. Yes, I should have cut TAST far earlier than I did. I had assumed the family owners, after previous successes, could have turned it around. But over time I gradually realised the economics of the sector had permanently deteriorated from the family’s heyday. When a share falls to becomes 1% of my portfolio, I have tended to leave it as the downside is just 1% of my portfolio, but a recovery could be a multi-bagger. MCON is 1% of my portfolio, I am no longer writing about it, but I keep it because things may turn around :-) The last statement read somewhat positive versus the languishing share price. But let’s see.

I have thought about less research and more portfolio management, and whether that can lead to greater returns, but that style is not in my nature. You don’t know as much about the business and tend to become more swayed by what the market thinks, and there is a trader-y element to the portfolio. That works for some people, but it’s not me.

I need to evaluate my long-term portfolio performance and identify what each holding has contributed to my return. My gut feel is that, rather than not selling major losers, my portfolio just tracking the FTSE over time is more to do with shares such as MTVW, SUS, CLIG, BVXP and TFW flat-lining over the last 5-10 years.

Maynard

Some good news! The Supreme Court has upheld appeals from two motor-finance lenders that should now eliminate substantial compensation claims against SUS.

The appeal announcement, press summary and full 110-page judgment are available here: https://supremecourt.uk/cases/uksc-2024-0157

The Court debated whether car dealers had a “fiduciary duty” — in other words, a ‘single-minded loyalty’ — towards the customer/borrower when arranging a finance deal…

…and decided car dealers do NOT have a fiduciary duty… which means the ‘secret commissions’ paid by the lenders to the dealers cannot be deemed to be ‘bribes’. As such, lenders such as SUS do not have to pay back commissions that were never fully disclosed to the borrower at the time of the car purchase.

A few lines from the press summary:

“Neither the parties themselves nor any onlooker could reasonably think that any participant was doing anything other than considering their own interest”

“Furthermore, the dealer was not providing credit brokerage as a distinct and separate service from the sale transaction”

“At no point did the dealer give any kind of express undertaking or assurance to the customer that in finding a suitable credit deal it was putting aside its own commercial interest as seller”

“The dealer was not an agent for the customer in the negotiation of the finance package with the lender. The dealer was undertaking an intermediary activity and did not have the authority to enter into legal relations on the customer’s behalf”

“The Court holds that these typical features of the transactions under review do not give rise to a fiduciary duty sufficient to create liability for bribery either under the common law tort or pursuant to the principles of equity. They are incompatible with the recognition of any obligation of single-minded or selfless loyalty by the dealer to the customer when sourcing and recommending a suitable credit package”

“An offer to find the best deal is not the same as an offer to act altruistically”

“A finance package on acceptable terms was always going to be an integral part of what had to be negotiated to bring the transaction to fruition, and no reasonable onlooker would think that, by offering to find a suitable finance package, the dealer was thereby giving up, rather than continuing to pursue, its own commercial objective of securing a profitable sale”

“Nor is the role of the dealer in selecting and negotiating a suitable finance package for the customer one in relation to which a fiduciary obligation of loyalty can be implied in law or in fact”

“Any element of trust and confidence that the dealer will secure the best available finance package is not of the type where the customer trusts the dealer to act with single-minded loyalty towards the customer, to the exclusion of its own interests”

Could the Court’s verdict been predicted? From my blog post above:

“A very positive outcome for the lenders was forecast by the legal experts at Quadrant Chambers, who commendably hosted this post-hearing seminar. They concluded only the most “egregious” of ‘secret commissions’ may be subject to repayment and dismissed the notion of widescale compensation payments”

Quadrant was spot on!

I am pleased to say I made the right interpretation of the case hearing:

“My layman view of the recordings did not suggest the Supreme Court would simply rubber-stamp the earlier legal verdict. Among the five Lord Justices hearing the case, the tone of questioning from the two most vocal Lords (Briggs and Hodge) did appear more supportive towards the lenders (Close Brothers and MotoNovo) than the borrowers (Miss Hopcraft, Mr Johnson and Mr Wrench)…

After watching all 13.5 hours of the hearing, I would be amazed if the Lord Justices unanimously found in favour of the borrowers.”

I note the full judgment refers to a line of questioning from the hearing to Mr Weir, the legal representative for the borrowers, which by the tone of the judges at the time did seem to doubt the validity of his answer:

“When the court put an example of this to Mr Weir, he submitted that in a case where the proffered finance package proved to be unacceptable (or unaffordable) to the customer, the dealer would be released from its stage two fiduciary obligation of loyalty to the customer, to enable it to resume an arm’s length commercial negotiating position. We regard that analysis as commercially and legally unrealistic.”

The Court’s judgment ought to leave SUS in a relatively favourable industry decision.

In particular, the group never participated in discretionary commission arrangements (DCAs), which remain subject to redress claims that may hamper sector rivals for some time to come.

In fact, Secure Trust Bank (STB) announced last month it was exiting vehicle financing:

“The Group announces it will stop new lending within its Vehicle Finance business and put the existing book into run-off. This decision reflects the historical financial performance and medium-term outlook of the Vehicle Finance business, both on an absolute basis and relative to other parts of the Group, and its sub-scale nature.”

STB’s vehicle-finance loan book was £558m, which is more than double SUS’s latest £273m motor-finance loan book. I speculate opportunities for market-share growth may arise for SUS as STB and others leave the field.

Plus the s166 investigation mandated by the FCA has now completed, leading to a recovery in collection levels and motor-finance loans being “above budget“.

I am therefore hopeful SUS’s fortunes have suddenly turned positive, and earnings and dividends can now swiftly recover after what has been a difficult year or two!

Maynard

Your legal analysis here has been spot on Maynard. Let’s see where SUS opens tomorrow, hopefully around book value!

Thanks Peter. I was not as confident as the experts at Quadrant, who seemed absolutely convinced only the Johnson case would succeed (and it was the only case of the three that did). But I thought the risk-reward at c£14 was in my favour given the tone of the questioning during the hearing. Book value I think is closing in on £20 a share, so that is the first step to a recovery. Could even in time trade at a premium!

Latest FCA news here:

https://www.fca.org.uk/news/statements/fca-consult-compensation-scheme-motor-finance-customers

Assuming SUS has not charged ‘unfair’ commissions (as per Johnson), then the group should be in the clear and not liable to pay any redress. FCA estimates total industry redress cost of DCAs to be between £9n and £18b. Will cover agreements going back to 2007.

Maynard