***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 May 2025

By Maynard Paton

I remarked the other month how most flotations had suffered badly during the last few years.

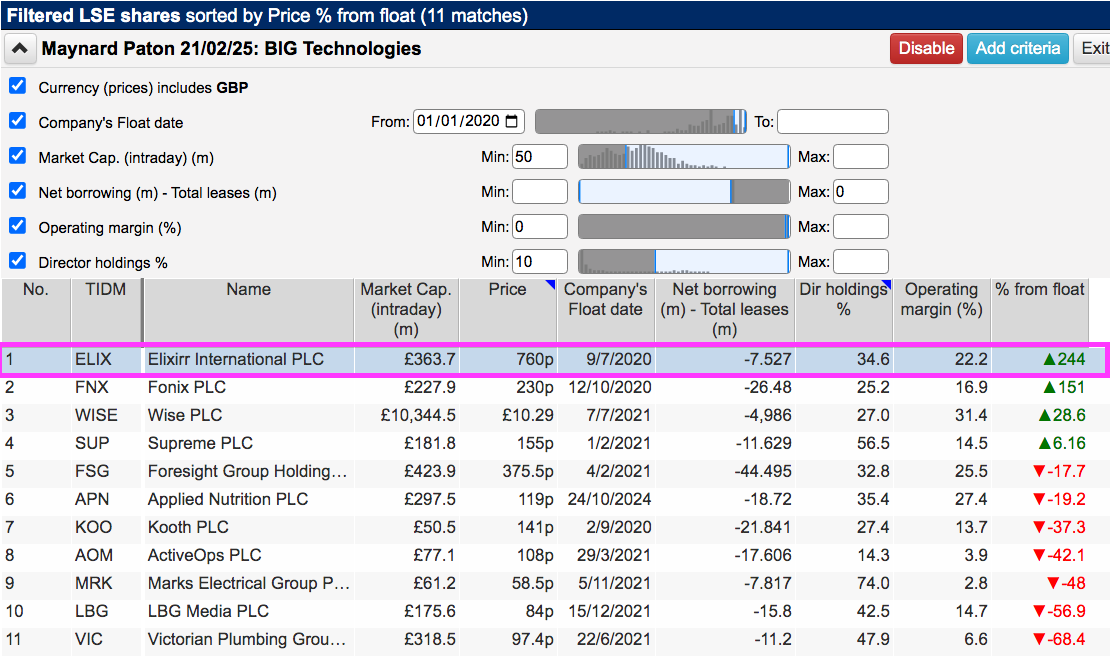

ShareScope lists 233 shares that joined the stock market since the start of 2020, of which 178 (76%) currently trade below their listing price — including 72 that have lost 80% or more of their value.

I consequently devised a ShareScope screen to rummage through the IPO carnage to find potential buying opportunities.

I sought companies that had:

- Floated since the start of 2020;

- A market cap of more than £50 million;

- Net cash;

- A positive operating margin;

- Director holdings of 10% or more, and;

- A GBP-denominated share price.

When I first employed this screen I selected BIG Technologies, in part because of its then 49% post-IPO share-price slump. BIG’s shares then took a further tumble after firing its chief executive for misleading the board!

I therefore decided this time to study a flotation winner!

I selected Elixirr International entirely because of its impressive 244% post-IPO share-price gain.

Let’s take a closer look.

Read my full ELIXIRR INTERNATIONAL article for ShareScope >>Maynard Paton

Hi Maynard,

With regard to Elixirr’s £18m EBT expense – rather than deducting it as an expense to get to true free cash flow, do you not adjust the share issue to the fully diluted amount to account for this?

Kind Regards,

Joe

Hi Joe

Yes, perfectly valid to adjust the share count for the options instead of treating the EBT purchases as an expense. Mind you, ELIX has historically used cash flow to purchase shares for the EBT, so such a ‘dilution’ model may diverge significantly from reality over time. Indeed, ELIX arranged a £45m revolving credit facility to fund future growth…

“The Group also agreed a £45.0 million revolving credit facility (“RCF”) with NatWest to support delivery of our organic and inorganic growth strategy, whilst limiting equity dilution.”

…and says the RCF will help limit equity dilution. I think I would work on actual cash flows here, which would double check on the amounts available for future acquisitions, what leeway there is with the dividend and whether future expansion will necessitate borrowings.

Maynard

Understood, I think it’s one I would need to spend more time figuring out whether the company is run for the benefit of employees vs making the best use of cash to create value for shareholders!

Many thanks for the explanation.

Kind regards,

Joe

Well, this is a consultancy and shareholders are arguably left with whatever the partner consultants have not demanded for themselves and the other employees. There may be good reason why rivals such as McKinsey etc are run as private companies!

Maynard